Abstract

Although overconfidence is acknowledged as one of the most common managerial decision-making biases, much uncertainty remains about its implications for firm performance. To resolve this uncertainty, we investigate how and why CEO overconfidence is related to firm performance using meta-analytic techniques on a sample of 199 studies. In particular, relying on behavioral decision theory, we develop alternative hypotheses regarding the impact of CEO overconfidence on firm performance. Contrary to the conventional belief that CEO overconfidence is detrimental, this study reveals that CEO overconfidence is, on average, beneficial for firm performance. Drawing on recent refinements of upper echelons theory and theoretical insights from the psychology literature, we then dive deeper into this positive relationship and hypothesize that overconfident CEOs engage in strategic risk taking through cognitive, motivational, and social mechanisms. This risk taking is positively related to firm performance. Our results confirm that the positive relationship between CEO overconfidence and firm performance is partially mediated through strategic risk taking. Thus, although CEO overconfidence is a cognitive bias, it does not automatically lead to inferior performance but can create value for firms by impelling CEOs to take actions that involve risk. We also test whether this relationship is stronger under conditions of high managerial discretion. Our results generally validate these predictions. Finally, on the basis of our findings, we discuss implications and directions for future CEO overconfidence research, including determining the limits of CEO overconfidence, exploring new moderators and mediators, and investigating the implications of different operationalizations of CEO overconfidence as well as the implications for practice.

Over the past decades, there has been a surge of cross-disciplinary research into how CEO attributes influence firm performance. For management scholars, upper echelons theory (UET) has been central in explaining the importance of CEO attributes for firm outcomes. UET proposes that CEO attributes influence CEOs’ strategic decisions, which in turn affect firm performance (Hambrick & Mason, 1984). The key argument has been that top executives perceive and interpret their environments through lenses formed by their backgrounds and reflected in their attributes (Hambrick, 2007). Substantial research has shown that CEO attributes affect firm strategy and performance (e.g., Cragun, Olsen, & Wright, 2020; Harrison, Thurgood, Boivie, & Pfarrer, 2020; Ou, Waldman, & Peterson, 2018; Wowak, Mannor, Arrfelt, & McNamara, 2016).

CEO overconfidence is one attribute that has received substantial scholarly attention (Heavey, Simsek, Fox, & Hersel, 2022). CEO overconfidence is the tendency of a CEO to have an inaccurate, overly positive perception of his or her abilities or knowledge (Anderson, Brion, Moore, & Kennedy, 2012). The dominant view from the traditional behavioral decision perspective (Kahneman & Lovallo, 1993; Slovic, Fischhoff, & Lichtenstein, 1977; Tversky & Kahneman, 1974) is that overconfidence leads to detrimental firm outcomes. For example, CEO overconfidence is associated with suboptimal investment behavior (Malmendier & Tate, 2005), value-decreasing acquisitions (Malmendier & Tate, 2008), reduced corporate social responsibility activities (Tang, Mack, & Chen, 2018), and negative firm performance (Park, Kim, Chang, Lee, & Sung, 2018). However, researchers advocating newer developments in behavioral decision theory (BDT) view CEO overconfidence more positively. For example, studies have pointed to the potential benefits of CEO overconfidence (Chen, Crossland, & Luo, 2015; Picone, Dagnino, & Minà, 2014), including enhanced innovation (Galasso & Simcoe, 2011) and firm performance (Reyes, Vassolo, Kausel, Torres, & Zhang, 2020). Such competing empirical evidence indicates that despite the numerous studies on CEO overconfidence, fundamental questions remain unanswered: how and why does CEO overconfidence influence firm performance?

The present meta-analysis addresses these critical and timely questions by focusing on two shortcomings in the existing literature. First, research on CEO overconfidence is fragmented across different literature streams (e.g., strategic management and finance 1 ), which have primarily evolved independently. While these research streams have generated numerous unique insights, they have also led to independent knowledge pools on CEO overconfidence, making it difficult to gain a big picture understanding. Thus, integrating studies across different literature streams offers an opportunity for a more comprehensive understanding of the relationship between CEO overconfidence and firm performance.

Second, although prior research has demonstrated how CEO overconfidence manifests in different firm outcomes, these studies have focused on outcomes in isolation: either proximal (e.g., strategic decisions) or distal (e.g., firm performance). The underlying assumption is that the proximal outcomes of overconfidence influence the distal outcomes (e.g., Li & Tang, 2010). However, research has neglected to consider the full pathway through which CEO overconfidence influences firm outcomes (Heavey et al., 2022), which has likely limited our ability to understand how and why CEO overconfidence is related to firm performance. Indeed, upper echelons research has paid insufficient attention to the process perspective that links CEO attributes to firm performance (Liu, Fisher, & Chen, 2018; Neely, Lovelace, Cowen, & Hiller, 2020). Investigating a proximal outcome as a mediator linking CEO overconfidence to firm performance will likely provide a more nuanced understanding of this important strategic relationship.

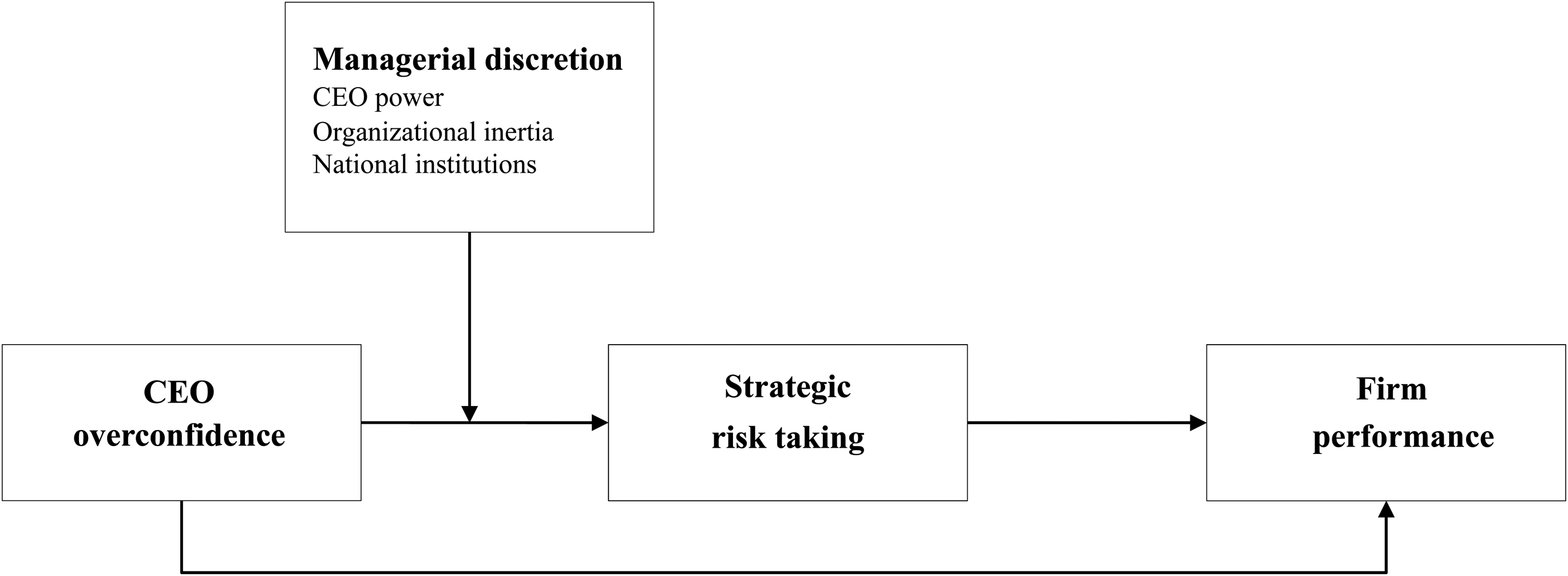

Drawing on recent conceptual refinements of UET and BDT, this study's primary objective is to develop a mediation model to explain the relationship between CEO overconfidence and firm performance. We focus on strategic risk taking as the mediator because it is an essential consideration for CEOs when making strategic decisions, over which they typically have significant discretion (Bromiley, 1991; Campbell, Jeong, & Graffin, 2019; Connelly, Li, Shi, & Lee, 2020; Shi, Connelly, Mackey, & Gupta, 2019; Wiseman & Gomez-Mejia, 1998). Strategic risk taking is the degree to which strategic decisions are associated with major capital investments that are uncertain and difficult to reverse and that have critical implications for the form and fate of firms (Kolev & McNamara, 2020). To set the scene for the mediation model, we first develop alternative hypotheses for the main effect relationship between CEO overconfidence and firm performance. We find a positive main effect relationship. We then dive deeper into this positive relationship in the subsequent mediation hypothesis. Specifically, integrating psychology research, we propose that overconfident CEOs engage in strategic risk taking through cognitive, motivational, and social mechanisms and that strategic risk taking is positively related to firm performance.

To substantiate our prediction regarding CEO overconfidence and strategic risk taking, we test the role of managerial discretion in this relationship—that is, CEOs’ latitude of action (Hambrick, 2007). CEOs can pursue varied courses of action in high-discretion settings because corporate governance mechanisms, organizational characteristics, and national institutions do not constrain CEOs’ decisions and actions. In contrast, in low-discretion settings, organizational factors and environmental conditions impose constraints that limit CEOs’ courses of action (e.g., Chatterjee & Hambrick, 2007; Simsek, Heavey, & Veiga, 2010). Thus, we argue that if our hypothesis regarding CEO overconfidence and strategic risk taking is supported, the relationship should be stronger under conditions of high managerial discretion. We conduct these tests using meta-analytic techniques on a sample of 199 primary studies.

Overall, we seek to offer two contributions. First, we contribute to the CEO overconfidence literature by clarifying the empirical relationship between CEO overconfidence and firm performance. Specifically, we show that CEO overconfidence, in general, is positively related to firm performance. This empirical evidence represents an important advance in the CEO overconfidence literature because it helps resolve the conflicting empirical findings of research on the relationship between CEO overconfidence and firm outcomes. Contrary to the predominant negative notion of overconfidence, our finding implies that CEO overconfidence is not always bad but can be valuable for firms. This contribution is a counterweight to the preponderance of prior research highlighting the negative implications of CEO overconfidence (Malmendier & Tate, 2005; Park et al., 2018; Pavićević & Keil, 2021) and serves as a foundation for future research reflecting that CEO overconfidence is not always dysfunctional.

Second, we contribute to UET by empirically demonstrating that the positive relationship between CEO overconfidence and firm performance is partially mediated through strategic risk taking. Thus, overconfident CEOs create value for firms because overconfidence impels CEOs to take actions that involve risk. We also demonstrate that the relationship between CEO overconfidence and risk taking, in general, is stronger when CEOs have more managerial discretion. These findings are important as they provide strong empirical evidence supporting the well-established theoretical predictions of UET—namely, that CEO effects take place through strategic actions and are stronger in high-discretion environments. This study additionally offers a timely response to the call for more research on the explanatory mechanisms through which CEO overconfidence is linked to firm outcomes (Heavey et al., 2022). The road map that we provide will guide future research, refining and extending the field's understanding of how this ubiquitous and vital construct is linked to performance.

Theoretical Background

Conceptualizing CEO Overconfidence

Research from psychology has suggested that overconfidence is a multifaceted construct (Moore & Healy, 2008; Moore & Schatz, 2017). Specifically, Moore and Healy (2008) highlighted three facets of overconfidence: (1) overestimation, which refers to individuals’ inflated appraisals of their actual abilities, performance, level of control over external events, and/or chances of success; (2) overplacement, which occurs when individuals believe that they are better than the average; and (3) overprecision, which refers to individuals’ excessive certainty that they know the truth. These three facets emphasize different sources of overconfidence, yet they all capture individuals’ exaggerated perceptions of themselves. While recent discussions in psychology suggest that these facets should be treated separately (Moore & Schatz, 2017), research in management and finance reflects a preference for conceptualizing overconfidence as a broad construct that encompasses these different facets (e.g., Chen et al., 2015; Chung & Hribar, 2021; Lee, Hwang, & Chen, 2017; Pavićević & Keil, 2021). In this study, we adopt Anderson and colleagues’ (2012: 719) definition of overconfidence to define CEO overconfidence as CEOs’ “inaccurate, overly positive perceptions of their abilities or knowledge.” 2

UET and the UET Process Perspective

The central premise of UET is that top managers’ attributes affect strategic decisions and firm outcomes (Hambrick & Mason, 1984). From this perspective, strategic decisions have a behavioral component such that top managers’ cognitive bases, values, and perceptions are reflected in their strategic decisions, which in turn have an impact on firm performance. Specifically, top managers’ values and cognitive bases substantially affect their perceptions of situations through their fields of vision (i.e., how they direct their attention), selective perceptions (i.e., what they notice), and interpretative frames (i.e., how they attach meaning; Hambrick & Mason, 1984). These perceptions inform their strategic decisions (Hambrick, 2007). Top managers’ values and cognitive bases arise from their individual attributes, such as their personalities and prior experiences. Due to the difficulty in obtaining data on top managers’ psychological dimensions, UET proposes that these managers’ observable attributes (e.g., background characteristics) can be used as proxies of their cognitive bases, values, and perceptions to explain strategic decisions and firm outcomes. 3 Indeed, a large body of research has demonstrated that individual CEO attributes—such as demographic characteristics (e.g., Kish-Gephart & Campbell, 2015), the Big Five personality traits (e.g., Harrison et al., 2020), core self-evaluation (e.g., Simsek et al., 2010), narcissism (e.g., Cragun et al., 2020), charisma (e.g., Wowak et al., 2016), and humility (e.g., Ou et al., 2018)—influence strategic decisions and firm outcomes.

While UET has been the foundation for many studies, there have been recent refinements to the theory, including a process perspective and the introduction of contextual factors moderating the influence of top managers’ attributes on firm outcomes. Specifically, the process perspective of UET accounts for mediation mechanisms that connect CEO attributes to firm performance through strategic decisions (Liu et al., 2018; Neely et al., 2020). For example, in their sequential process model, Liu and colleagues (2018) theorized that CEO attributes lead to strategic decisions that lead to firm performance through a series of underlying mechanisms. Studies have started to empirically test these mediation mechanisms (e.g., Jeong & Harrison, 2017; Ou et al., 2018), so the empirical evidence is limited.

Moreover, the UET process perspective emphasizes contextual factors that moderate these connections. Indeed, the “most notable” refinement to UET has been the introduction of managerial discretion moderating the influence of top managers on firm performance (Hambrick, 2007; see Hambrick & Finkelstein, 1987). Managerial discretion helps explain when top managers have more or less influence on firm strategy and performance (Hambrick, 2007; Hambrick & Finkelstein, 1987). Managerial discretion has received a great deal of attention to understand the impact of CEOs on firm outcomes and has been documented extensively in empirical studies (see Wangrow, Schepker, & Barker, 2015, for a review). Managerial discretion arises from (1) individual factors, such as the degree to which a CEO is personally able to envision or create multiple courses of action; (2) organizational factors, such as the degree to which an organization itself is amenable to an array of possible actions and empowers its CEO to formulate and execute those actions (e.g., CEO power, organizational inertia); and (3) environmental factors, such as the degree to which the environment allows a variety of options and change (e.g., national institutions; Hambrick & Finkelstein, 1987). We investigate managerial discretion at the organizational and country levels as a contextual condition.

In our study, we draw on the recent conceptual refinements of UET (Liu et al., 2018; Neely et al., 2020) and develop an upper echelons mediation model of CEO overconfidence. To set the scene for our subsequent theorizing, we theorize alternative hypotheses for the main effect relationship between CEO overconfidence and firm performance. We find a positive main effect relationship. We then dive deeper to hypothesize that the positive relationship between CEO overconfidence and firm performance happens through strategic risk taking (mediator) and that managerial discretion moderates the relationship between CEO overconfidence and strategic risk taking (Figure 1). Consistent with most management studies of overconfidence, we focus on the CEO and not the top management team.

An Upper Echelons Model of CEO Overconfidence

Hypotheses

CEO Overconfidence and Firm Performance

The extant literature offers two competing views of CEO overconfidence and its direct effects on firm performance.

On the one hand, CEO overconfidence is considered a cognitive error that negatively affects firm performance. According to the predominant view of BDT, humans systematically deviate from rational norms and statistical principles when making decisions because they have internal cognitive limitations (Kahneman, Slovic, Slovic, & Tversky, 1982; Tversky & Kahneman, 1974). These violations are interpreted as fallacies or flaws that, per definition, lead to inferior decisions because optimal decisions are determined by rational choice. Thus, cognitive biases can be dysfunctional for strategic decisions with detrimental consequences for firm performance.

Overconfidence can be dysfunctional for CEOs because their overly positive perceptions of their abilities and knowledge make them believe that they have accurate and adequate information to make decisions (Ben-David, Graham, & Harvey, 2013; Moore & Healy, 2008). Thus, they do not feel the need to search for and analyze additional information or ask for decision input from others (Tang, Li, & Yang, 2015; Zacharakis & Shepherd, 2001). Therefore, overconfident CEOs risk ignoring potential problems and overlooking new and relevant information. Additionally, overconfident CEOs tend to resist negative feedback (Chen et al., 2015), which is likely to inhibit the improvement of their decisions. Accordingly, overconfidence is harmful (Moore & Healy, 2008; Moore & Schatz, 2017) and can lead to ill-considered and erroneous strategic decisions (e.g., Malmendier & Tate, 2008; Park et al., 2018; Pavićević & Keil, 2021). For example, Park et al. (2018) demonstrated a negative relationship between CEO overconfidence and firm performance.

On the other hand, recent studies advocating newer developments in BDT have drawn attention to the potential positive side of CEO overconfidence (Chen et al., 2015; Picone et al., 2014; Reyes et al., 2020), arguing that it may have a positive impact on firm performance. According to the traditional behavioral decision perspective, assessments of what counts as an error and a dysfunctional decision are shaped by standards of rationality (Tetlock, 1992, 2000). However, in uncertain contexts, comprehensive decision making is often not possible, and no single best or right strategy for achieving strong performance exists (Hambrick, Finkelstein, & Mooney, 2005). In such contexts, “biases and heuristics can be an effective and efficient guide to decision-making” (Busenitz & Barney, 1997: 9). Thus, biases and heuristics can help CEOs cope with uncertain and complex situations (Chen, Kim, Nofsinger, & Rui, 2007; Das & Teng, 1999; Simon, Houghton, & Aquino, 2000), yielding “acceptable solutions to problems . . . in an effective and efficient manner” (Busenitz & Barney, 1997: 12). Such mechanisms are particularly relevant for strategic decisions, which are typically complex, highly uncertain, and urgent—conditions that make rational decision making infeasible (Artinger, Petersen, Gigerenzer, & Weibler, 2015; Das & Teng, 1999; Gigerenzer & Gaissmaier, 2011; Schwenk, 1984).

CEO overconfidence can be functional because it sharpens CEOs’ focus on the planned course of action, disregarding the variety of more distracting alternatives available (Navis & Ozbek, 2016). Thus, overconfidence facilitates a perceived sense of a general, or big picture, understanding of uncertain and complex situations, enabling CEOs to make pragmatic decisions when they do not have all information at hand. This tendency propels CEOs to take actions that less overconfident CEOs would not take (Bénabou & Tirole, 2002; Busenitz & Barney, 1997; Foster, Reidy, Misra, & Goff, 2011). The logic that overconfidence may impel action is consistent with prior literature linking overconfidence with proactiveness (Engelen, Neumann, & Schwens, 2015; Pallier et al., 2002) and a can-do attitude (Tetlock, 2000). The tendency of overconfident CEOs to engage in action rather than inaction may be particularly useful for taking advantage of windows of opportunity (Volk, Köhler, & Pudelko, 2014).

Based on this reasoning, we expect that CEO overconfidence may serve as an enabler in effectively and efficiently navigating the complexity and uncertainty surrounding strategic decisions and, in turn, positively influence firm performance. Recent empirical evidence supports this positive view of CEO overconfidence (Reyes et al., 2020). Importantly, although CEO overconfidence can enhance firm performance, there appear to be limits to more overconfidence. Recent research has shown that whereas moderate degrees of CEO overconfidence are beneficial, excessively high degrees of CEO overconfidence are harmful to firm outcomes (e.g., Campbell, Gallmeyer, Johnson, Rutherford, & Stanley, 2011; Goel & Thakor, 2008). 4

In sum, the traditional view in BDT emphasizes the harmful effects of CEO overconfidence on strategic decisions and thus its negative influence on firm performance. Alternatively, recent developments in BDT point out that CEO overconfidence can be beneficial for strategic decisions, thereby enhancing firm performance. Given that both views are reasonable, we offer the following alternative hypotheses:

Hypothesis 1: CEO overconfidence is negatively associated with firm performance.

Hypothesis 1Alternative: CEO overconfidence is positively associated with firm performance.

The Mediating Role of Strategic Risk Taking

While there are competing views on the nature of the direct relationship between CEO overconfidence and firm performance, researchers generally agree that overconfidence increases CEOs’ strategic risk taking. Strategic risk taking is a core strategic decision of CEOs (Campbell et al., 2019) that can be highly consequential for firm performance (Bromiley, Miller, & Rau, 2001; Bromiley & Rau, 2010). Strategic risk taking refers to the degree to which strategic decisions are associated with “major capital investments that are uncertain, difficult to reverse” and have “critical implications for the form and fate of firms” (Kolev & McNamara, 2020: 4). CEO attributes are particularly explanatory of strategic risk taking because “executive risk taking is not so much an economic calculus as an interpretive act . . . that [is] in the eyes of the beholder” (Chatterjee & Hambrick, 2011: 203).

Overconfident CEOs engage in strategic risk taking through three underlying mechanisms—cognitive, motivational, and social. First, overconfident CEOs may positively influence strategic risk taking via the cognitive mechanisms of decision making. CEO overconfidence involves cognitive mechanisms of assigning probabilities to possible outcomes and assessing their relative attractiveness (Chatterjee & Hambrick, 2007; Mannor, Wowak, Bartkus, & Gomez-Mejia, 2016). CEO overconfidence can lead to inaccurate perceptions of probabilities because CEOs tend to overestimate their control and chances of success. For example, overconfident CEOs believe that they have more information than they do and regard their information as more valuable than others’ information (Daniel, Hirshleifer, & Subrahmanyam, 1998; Moore & Healy, 2008). These inaccurate perceptions lead CEOs to have an inflated sense of control over their current situations (Li & Tang, 2010) and underestimate the influence of external factors on their chances of success (Chen et al., 2015; Langer, 1975). Indeed, the psychology literature indicates that overconfident individuals tend to believe that they can control their outcomes (Moore & Schatz, 2017; Presson & Benassi, 1996) and thus make riskier decisions.

Moreover, overconfident CEOs inaccurately assess the capabilities necessary to achieve outcomes because their overly positive perceptions of themselves and their situations lead them to believe that certain outcomes are more feasible than they are. For example, overconfident CEOs believe that they have superior decision-making abilities and are more capable than their peers (Hayward & Hambrick, 1997; Moore & Healy, 2008). These misperceptions may lead CEOs to overestimate the potential benefits of taking strategic risks and their abilities to implement these strategic decisions (Li & Tang, 2010), causing them to underestimate the likelihood and magnitude of the potential downsides of strategic risk taking (e.g., overconfident founders; Hayward, Shepherd, & Griffin, 2006). Furthermore, because overconfident CEOs are excessively certain that they know the truth and that their predictions are accurate (Moore & Healy, 2008), they do not believe that it is necessary to consider alternatives, thereby limiting their information scanning (Finkelstein, Cannella, Hambrick, & Cannella, 2009).

Second, CEO overconfidence can positively influence strategic risk taking through motivational mechanisms. Overconfidence may affect how CEOs set goals and determine the effort that they put into achieving them, which influences their risk-taking behavior. According to social cognitive theory, individuals’ self-efficacy beliefs are key motivators for setting challenging goals and raising and sustaining the effort needed to achieve these goals (Bandura, 1989). Individuals motivated by challenging goals adopt riskier strategies than individuals with less challenging goals (Ordóñez, Schweitzer, Galinsky, & Bazerman, 2009) because goals serve as reference points and shift decision makers from the domain of gains to the domain of losses, thereby changing their risk preferences (i.e., from risk aversion to risk seeking; Larrick, Heath, & Wu, 2009). Because overconfidence partly derives from overly optimistic self-efficacy beliefs (Fuchs, Sting, Schlickel, & Alexy, 2019; Picone et al., 2014), overconfident CEOs are likely to set higher goals and invest more effort to achieve them (Bénabou & Tirole, 2002; Pillai, 2010), which encourages strategic risk taking.

Furthermore, overconfidence leads to greater persistence in solving problems (Bi, Dang, Li, Guo, & Zhang, 2016) and maintaining one's initial course of action, especially when reputational concerns are salient (Ronay, Oostrom, Lehmann-Willenbrock, & Van Vugt, 2017). Such persistent behavior can encourage risk taking because individuals are likely to allocate additional resources to their initial courses of action even if they have not developed as initially expected (Brockner, 1992). Indeed, CEO overconfidence is associated with escalation of commitment (Hayward, Rindova, & Pollock, 2004; Sleesman, Conlon, McNamara, & Miles, 2012), which is characterized as a risk-taking behavior (Brockner, 1992; Wong & Kwong, 2007).

Finally, CEO overconfidence can positively influence strategic risk taking through social mechanisms. Role theories suggest that CEO attributes shape strategic decisions through interactions between CEOs and top management teams (Georgakakis, Heyden, Oehmichen, & Ekanayake, 2022). Accordingly, internal stakeholders are likely to affirm strategic risk taking by overconfident CEOs because they perceive these CEOs as competent and persuasive (Anderson et al., 2012; Von Hippel & Trivers, 2011) and capable of evaluating and pursuing risky strategies. Furthermore, overconfident CEOs attain higher social status (Kennedy, Anderson, & Moore, 2013), which they can use to dominate and control decision making. As such, overconfident CEOs are likely to gain approval from internal stakeholders to undertake strategic actions that involve risk. Moreover, the illusion of being in control of external events and the belief that their ideas will ultimately be effective and result in positive outcomes enable overconfident CEOs to envision and portray positive futures for their firms (Picone et al., 2014; Shipman & Mumford, 2011). Such overly positive visions encourage top management teams to embrace and carry forward these CEOs’ plans for their firms.

This increased strategic risk taking could explain improved firm performance. Prior research has suggested that strategic decisions that involve risk can lead to higher performance (Hoskisson, Chirico, Zyung, & Gambeta, 2017). Strategic risk taking, such as research and development (R&D) investments, is often associated with ideas and technologies that focus on new market opportunities (Koza & Lewin, 1998; Uotila, Maula, Keil, & Zahra, 2009). Such investments may generate higher returns (than less risky investments) because they generate competitive advantage and agility for threat responses (Levinthal, 1997; March, 1991). Similarly, higher capital expenditures generate more growth opportunities (Lee, 2006; Titman, Wei, & Xie, 2004), enable firms to exploit market demands (Kotha & Nair, 1995), and enhance competitive advantage (Manikas, Patel, & Oghazi, 2019) and thus firm performance.

While greater strategic risk taking can increase performance variance, such variance is likely to enhance overall firm performance (i.e., increased variance can move mean performance to the right; McGrath, 1999). Wiklund and Shepherd (2011) argued and found that firms with higher entrepreneurial orientation (of which risk taking is one dimension) exhibit greater performance variance and higher mean performance than firms with lower entrepreneurial orientation. Indeed, prior research has demonstrated that R&D investments (e.g., Arrfelt, Mannor, Nahrgang, & Christensen, 2018; Chan, Lakonishok, & Sougiannis, 2001; Eberhart, Maxwell, & Siddique, 2004) and capital expenditures (e.g., Anderson & Garcia-Feijoo, 2006; Chung, Wright, & Charoenwong, 1998; Fahlenbrach, 2009) are beneficial for firm performance. Consequently, we expect that greater strategic risk taking helps link CEO overconfidence to positive firm performance. Based on this, we offer the following:

Hypothesis 2: Strategic risk taking mediates the relationship between CEO overconfidence and firm performance. Specifically, CEO overconfidence is positively associated with strategic risk taking, and strategic risk taking is positively associated with firm performance.

Moderating Effects of Managerial Discretion

Based on UET and the managerial discretion perspective, the positive relationship between CEO overconfidence and strategic risk taking is likely stronger in contexts in which CEOs have more managerial discretion arising from CEO power, organizational inertia, and national institutions.

First, CEO power reflects the degree to which CEOs can exert their will on their firms’ strategic decisions and thus influences the impact of CEO overconfidence on firms (Finkelstein, 1992; Pfeffer, 1981). CEO power can differ across firms due to the varying structural power associated with the formal CEO position (e.g., CEO duality) and ownership structure (e.g., CEO ownership; Finkelstein, 1992; Van Essen, Otten, & Carberry, 2015). When overconfident CEOs are more powerful, they can leverage their central position in the board and significant ownership to pursue their own goals and advance personal interests and preferences relatively unchecked (Dunn, 2004; Finkelstein & D’Aveni, 1994; Zhu & Chen, 2015).

Second, organizational inertia reflects firms’ inability to enact internal change, limiting CEOs’ impact on firm strategy and outcomes (Gilbert, 2005; Hannan & Freeman, 1984). Organizational inertia is intensified in larger and older firms due to their standardized routines, established patterns of thinking and activities, and institutionalized mechanisms (Finkelstein & Hambrick, 1990; Haveman, 1993; Lavie & Rosenkopf, 2006). By engaging in such routines, patterns, and mechanisms, older and larger firms likely provide overconfident CEOs with fewer strategic options and less flexibility to adapt to change.

Third, CEOs in countries with weaker institutional constraints—formal (i.e., codified and explicit rules and standards) and informal (i.e., systems of shared meaning and the collective understanding of that meaning)—have more discretion and thus a greater impact on firms (Crossland & Hambrick, 2007, 2011). In such institutional environments, legal systems and control mechanisms, as well as social conventions, norms, and values, are enforced less and thus more tolerant of overconfident CEOs’ strategic risk taking (Crossland & Hambrick, 2011; Wang, DeGhetto, Ellen, & Lamont, 2019). 5 On the basis of this reasoning, we offer the following:

Hypothesis 3: Managerial discretion moderates the relationship between CEO overconfidence and strategic risk taking. Specifically, (a) CEO power magnifies, (b) organizational inertia dampens, and (c) weaker national institutions magnify the positive relationship between CEO overconfidence and strategic risk taking.

Research Method

Literature Search

We used complementary search strategies to identify relevant published and unpublished empirical studies before August 2021. An initial search on Google Scholar revealed different operationalizations of CEO overconfidence and different labels (e.g., hubris, optimism) despite measuring overconfidence (e.g., option-based measure), which are thus eligible for our meta-analysis. For these reasons, we opted for a broad keyword search that included the term “overconfidence” and related terms—“hubris,” “self-enhancement,” “overoptimism,” “optimism,” and “confidence.” Because the focus of our study is on CEOs, we combined these keywords with terms indicating upper echelons positions, such as “CEO/chief executive” and “manager.” With these keywords, we searched for studies in (1) the Google Scholar database as this is one of the most comprehensive academic search engines including published and unpublished studies across multiple disciplines, (2) EBSCO Business Source Complete to complement our search for published articles as this covers all business disciplines, (3) ProQuest Dissertations to search for dissertations, and 4) all journals ranked in the Financial Times 50 list. We also searched in the reference lists of previous review articles related to our topic (e.g., Grežo, 2020). Finally, we manually cross-referenced (using the snowballing technique) and backward traced all references reported in the studies of our final sample to ensure that we captured key publications. We identified more than 23,000 search results.

Inclusion and Exclusion Criteria

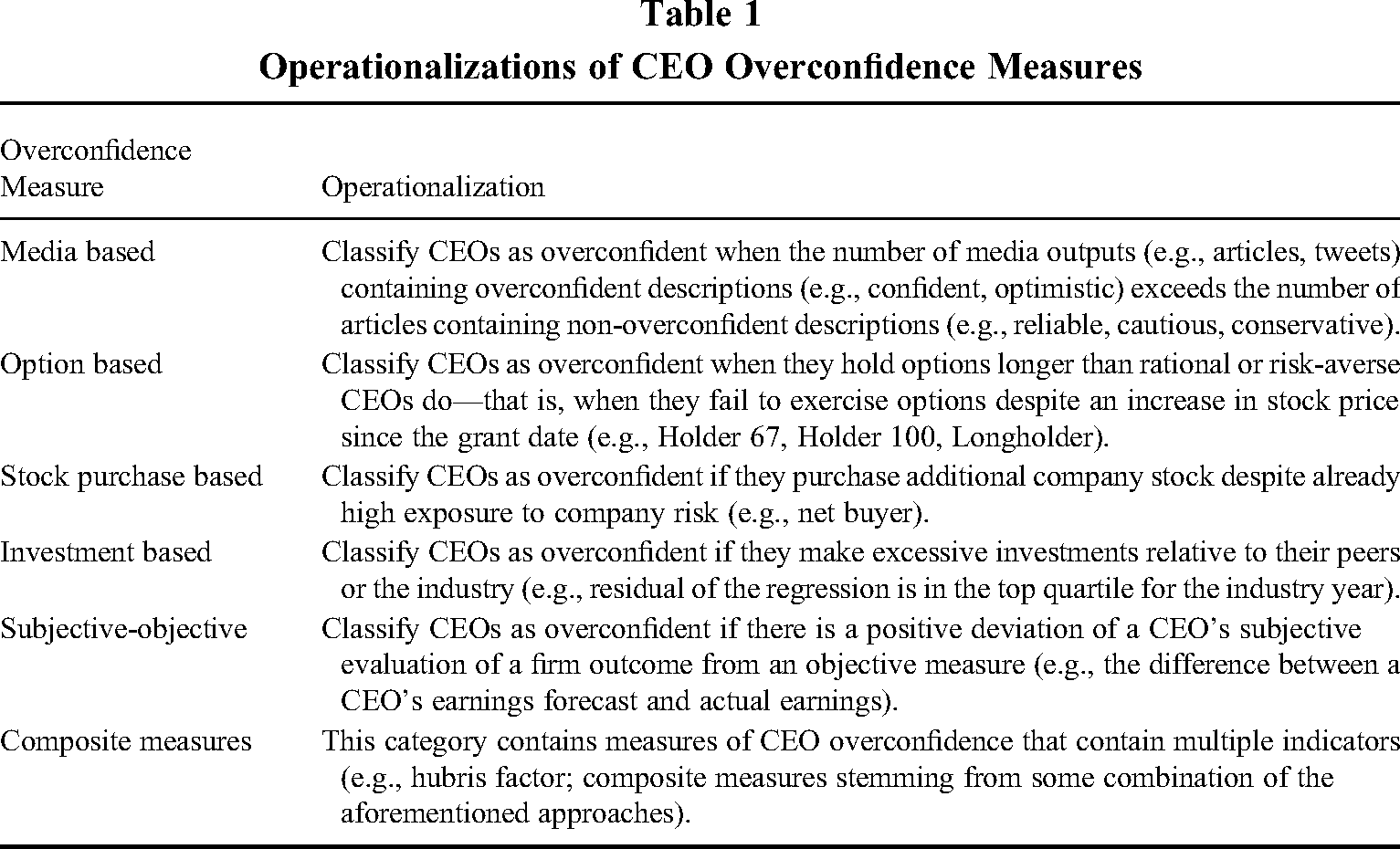

The primary studies had to meet several criteria to be included in our study. First, each study had to operationalize CEO overconfidence to reflect a CEO's misperception of his or her abilities or knowledge. These studies used six measures that reflect such a misperception: option based, stock purchase based, investment based, media based, subjective-objective, and composite. To avoid the construct identity fallacy (Steel, Beugelsdijk, & Aguinis, 2021), we did not include anything beyond these widely used and established CEO overconfidence measures. We excluded studies that reportedly measured overconfidence with variables that did not reflect a CEO's misperception, such as dispositional optimism, self-efficacy, narcissism, firm size, CEO age, and CEO compensation. We also excluded measures that have been used to capture another construct. For example, while some studies have used the prominence of CEOs’ photographs in company reports to operationalize CEO overconfidence, this measure is a widely used indicator of CEO narcissism (e.g., Zhu & Chen, 2015). To address the construct identity fallacy further, we included studies with a focal variable that was not labeled overconfidence but represented one of the six CEO overconfidence measures. The supplementary material in Appendix A details the labels/measures used in the sample's studies. Second, we included only those studies that reported at least one bivariate relationship (Pearson correlation coefficient) relevant to our meta-analysis or included statistical information such that we could calculate the necessary correlations. We excluded studies that did not focus on the variables of interest (e.g., leverage 6 ). Third, we included studies that focused on overconfidence at the CEO level and excluded studies that focused on employees or other managers, such as chief financial officers or middle managers (e.g., Iskandar-Datta & Shekhar, 2020). Fourth, to account for autocorrelation, we followed prior meta-analyses (Berrone et al., 2020) and included only studies that used lagged or same-year measures to investigate the relationship between CEO overconfidence and strategic decisions or firm performance. Fifth, following best practice recommendations (Steel et al., 2021), we included unpublished studies, such as working papers and dissertations, to mitigate the possibility of the “file drawer” problem (Rosenthal, 1979)—that is, the tendency of journals to publish studies with statistically significant results rather than nonsignificant results. Sixth, to avoid selection bias (Steel et al., 2021), we included all primary studies independent of journal quality, citation rate, or discipline. However, we excluded studies when there was an obvious error in the tables (e.g., inconsistencies in correlation tables, conflicting information about whether Pearson or Spearman correlations were reported). Seventh, following prior meta-analyses (Mackey, McAllister, Ellen, & Carson, 2021), we excluded studies not available in English to ensure that all the current authors could read the primary studies. Eight, to eliminate duplicate studies, we excluded unpublished papers later published in journals. However, we included working papers instead of their published versions when the article did not provide sufficient information (see Hribar & Yang, 2010, 2016). Finally, we excluded experiment-based studies because they often relied on subjects who were not CEOs.

We coded a final sample of 199 primary studies (146 published, 53 unpublished) from 16 countries. 7 The studies contain primary data collected between 1980 and 2018.

Coding Procedure

We read all the studies and developed a coding protocol for calculating effect sizes; classifying the variables; and assessing contextual, measurement, and study effects (Lipsey & Wilson, 2001). For a list of all the measures of the key variables, see the supplementary material in Appendix B. Two raters—one coauthor and one independent rater familiar with meta-analyses but blind to the study hypotheses—coded all the effect sizes. The initial interrater agreement (kappa; Cohen, 1960) was .95. The two raters discussed discrepancies until they reached consensus.

Effect sizes

To calculate the effect sizes, we coded all the possible bivariate correlations (i.e., Pearson product-moment) from each study for the focal relationships (e.g., between CEO overconfidence and performance, between CEO overconfidence and strategic risk taking, between strategic risk taking and performance) and the sample size (i.e., number of firms) of the underlying study. When the studies did not provide correlations, we coded other statistical information, such as means and standard deviations (reported in tests of mean differences across two groups; e.g., overconfident vs. nonoverconfident CEOs) to calculate bivariate correlations using the formulas detailed by Lipsey and Wilson (2001). When a study reported multiple measurements of the focal effect, we followed best practice recommendations (Steel et al., 2021) and prior meta-analyses (e.g., Vishwanathan, van Oosterhout, Heugens, Duran, & van Essen, 2020) and kept multiple correlations for the same relationship from the same sample statistically separate. We used a multilevel approach as a robustness check for this nested research design.

Dependent variable: Firm performance

Prior research in strategic management has strongly recommended using multiple measures to capture firm performance (Combs, Crook, & Shook, 2005; Hamann, Schiemann, Bellora, & Guenther, 2013). On the basis of theoretical relevance and prior meta-analyses (e.g., Carney, Gedajlovic, Heugens, van Essen, & van Oosterhout, 2011; Jeong & Harrison, 2017; Post & Byron, 2015), we coded two different but widely employed indicators of firm performance. First, market-based measures reflect shareholder expectations and indicate firms’ future performance potential (e.g., Keats & Hitt, 1988). In line with prior meta-analyses (e.g., Post & Byron, 2015), we included market-based measures of firm performance, such as Tobin's Q, market-to-book ratio, stock performance, and abnormal returns. Second, accounting-based measures reflect past and present firm performance and indicate firms’ internal efficiency (Daily, Certo, & Dalton, 2000). We followed prior meta-analyses (e.g., Jeong & Harrison, 2017) and included accounting-based measures of firm performance, such as return on assets (ROA), return on equity, return on total assets, profit margin, and sales growth. We used the correlations of each indicator as inputs in the analysis (e.g., the correlation between CEO overconfidence and ROA). Following prior meta-analyses (e.g., Carney et al., 2011), we tested our main models with the aggregated performance measure and provide robustness tests based on these two performance dimensions in the Supplemental Analyses section.

Independent variable: CEO overconfidence

We classified the studies’ operationalizations of overconfidence into six categories (Table 1). First, media-based measures classify CEOs as overconfident when CEOs’ language in media portrayals is rated as overconfident. For example, one measure focuses on CEOs’ coverage in the business press by comparing the number of articles using terms that imply overconfidence with the number of articles using terms that imply caution; thus, it classifies a CEO as overconfident if the number of articles containing overconfident descriptions exceeds the number of articles containing non-overconfident descriptions (Malmendier & Tate, 2008). Scholars have applied similar logic to, for example, CEOs’ tweets (e.g., Lee et al., 2017) as indicators of overconfidence.

Operationalizations of CEO Overconfidence Measures

Second, measures in the option-based category classify CEOs as overconfident when they fail to exercise options despite an increase in stock price since the grant date. Such behavior is deemed irrational because a rational and risk-averse executive should seek to exercise stock options once they are vested, as options cannot be legally traded or short-sold and holding exercisable options increases risk (Malmendier & Tate, 2005, 2008, 2015). The primary studies used different moneyness cutoff points, such as 67%, 40%, and 100% (moneyness describes the value of an option in its current state), and different periods (e.g., in the fifth year before expiration, in the year of expiration, at any or multiple points during the sample period). We included all forms of cutoff points and periods in this category as long as they captured CEOs’ stock option-exercise behavior and their systematic tendency to hold options longer.

Third, stock purchase-based measures categorize a CEO as overconfident if the CEO was a net buyer of his or her firm's stock (a net buyer of stock in more years than he or she was a net seller of stock; e.g., Malmendier & Tate, 2005) or if the CEO bought his or her firm's stock when it had a negative return (e.g., Kolasinski & Li, 2013). We included a measure in this category when it captured CEOs’ tendency to acquire more company stock despite their already high exposure to company risk.

Fourth, investment-based measures classify CEOs as overconfident if they make excessive investments relative to, for example, their peers. These measures classify a CEO as overconfident if the CEO's investment exceeds the mean investment by firms in the same industry (e.g., Ahmed & Duellman, 2011) or when the residuals of a regression of total asset growth on sales growth are in the top quartile for the industry year (e.g., Duellman, Hurwitz, & Sun, 2015). Whenever a measure captured a CEO's excessive investment behavior, we included it in this category.

Fifth, measures in the subjective-objective category classify a CEO as overconfident if there is a positive deviation of the CEO's subjective evaluation of a firm outcome from an objective measure. The studies in this category used different variables to capture firm outcomes. For example, Li and Tang (2010) calculated the deviation of CEOs’ subjectively evaluated firm performance from an objective performance measure (return on sales) during the same period. Similarly, other scholars calculated the difference between CEOs’ earnings forecasts and actual earnings (e.g., Lee et al., 2017). We included studies in this category when they captured the accuracy of CEOs’ subjective evaluations vis-à-vis objective outcomes.

Finally, if a CEO overconfidence measure contained multiple indicators as a composite measure (e.g., Hayward & Hambrick, 1997; Ouyang, Tang, Wang, & Zhou, 2022), we included it in the composite measures category because it was impossible to assign it to one of the mutually exclusive categories.

Mediator: Strategic risk taking

Following prior meta-analyses (Jeong & Harrison, 2017; Wang, Holmes, Oh, & Zhu, 2016) and other empirical studies (e.g., Bromiley, Rau, & Zhang, 2017; Campbell et al., 2019) in strategic management, we coded three indicators typically associated with strategic risk taking. First, R&D investment indicates how firms invest in creating new knowledge and technologies. These investments are associated with unpredictability because CEOs cannot foresee their outcomes (Miller & Bromiley, 1990). Prior studies have widely used R&D investment to capture strategic risk taking (e.g., Benischke, Martin, & Glaser, 2019; Campbell et al., 2019), which is typically expressed as the ratio of a firm's total annual R&D expenditures to total sales (e.g., Tang et al., 2015). Second, capital investment indicates firms’ expenditures on long-term assets and is characterized as “risky and uncertain” investment behavior (Sanders & Hambrick, 2007: 1064). Capital investment is frequently used to capture strategic risk taking (e.g., Benischke et al., 2019; Campbell et al., 2019) and is most often measured as a firm's capital spending (e.g., Malmendier & Tate, 2005). Finally, firm risk is an indirect output-based indicator that captures the riskiness of investment decision outcomes (Bromiley & Rau, 2010; Jeong & Harrison, 2017; Zolotoy, O’Sullivan, Martin, & Wiseman, 2021). Following prior studies (e.g., Jeong & Harrison, 2017), we included measures of firm risk. Prior research has shown that CEOs can indirectly affect firm risk by informing investors’ expectations of their firms’ ability to manage risk (Harrison et al., 2020) effectively. Following Wright, Kroll, Krug, and Pettus (2007) and Arrfelt et al. (2018), we captured firm risk with risk measures based on accounting (e.g., the standard deviation of a firm's ROA) and market (standard deviation of monthly total returns to shareholders).

Moderator: Managerial discretion

We followed prior studies in strategic management (e.g., Van Essen et al., 2015) and coded several indicators of structural power (CEO duality, board size, board independence) and ownership power (CEO ownership, CEO concentration) to measure CEO power. We used the mean values for these indicators from the primary studies. We reverse coded the board independence and ownership concentration scores to point in the same direction as the other CEO power variables. Following Zhu and Chen (2015), we created a composite index of CEO power by first standardizing the scores and then taking the mean of the scores. A higher index score indicates that the average CEO in a study has more power and thus more managerial discretion.

We measured organizational inertia using a composite index including two indicators that have been widely used in the literature: firm size (e.g., assets, sales, market value of equity, number of employees) and firm age (e.g., Hambrick & Finkelstein, 1987; Shimizu & Hitt, 2005; Wangrow et al., 2015). We followed the recommendations of Shimizu and Hitt (2005) and Quigley, Wowak, and Crossland (2020) to use a composite index of organizational inertia. We created the composite index of firm size and age by standardizing the scores and then taking their mean. A higher value indicates that the average firm in a study is more inertial and thus has lower managerial discretion.

We measured national institutions as countries’ formal and informal institutions based on the method developed and validated by Crossland and Hambrick (2007, 2011) and used in prior studies (e.g., Georgakakis & Ruigrok, 2017; Wang et al., 2019). We first coded the country where a particular study was conducted and then matched the external data accordingly. We used the following external data sources: for informal national institutions, data from Hofstede (2001, 2021) and Gelfand et al. (2011); for formal national institutions, data from La Porta, Lopez-de-Silanes, Shleifer, and Vishny (1999), Estevez-Abe, Iversen, and Soskice (2001), and Botero, Djankov, Porta, Lopez-de-Silanes, and Shleifer (2004). Finally, we created a composite index of the strength of country-level institutions by first standardizing the scores of formal and informal institutions for each country and then taking their mean. A higher value indicates that CEOs are less constrained by their environments and thus have higher managerial discretion.

In Appendix C, we provide a detailed description of how we coded managerial direction.

Control variables for the meta-analytic structural equation modeling

We controlled for CEO tenure, age, and gender in the meta-analytic structural equation modeling (MASEM; Hypothesis 2) because research has suggested that they can affect risk taking and performance (Benischke et al., 2019; Connelly et al., 2020; Jeong & Harrison, 2017). Because MASEM requires correlation coefficients as inputs for analysis, we coded the correlation coefficients for the relevant relationships.

Control variables for the meta-analytic regression analysis

We included several control variables in our meta-regressions (Hypothesis 3; as a robustness test for Hypotheses 1 and 1Alternative) to account for the primary studies’ characteristics. First, we included a dummy variable denoting whether a study was published or not (reference group). Second, we included each publication's impact factor provided by Clarivate Analytics to account for differences in journal quality (Carney et al., 2011). Third, we created a dummy variable indicating whether a study used panel or cross-sectional data (reference group; Joshi, Son, & Roh, 2015). Fourth, we controlled for the median year of the sample window to allow for potential changes in overconfidence over time (Carney et al., 2011). Fifth, we included a dummy variable indicating whether the effect size was based on a US sample or not (reference group) to account for the high proportion of US samples in the overall sample (Jeong & Harrison, 2017). Sixth, because CEO overconfidence has been investigated across research streams, we included a binary indicator of whether the study belongs to the management field or not (reference group). Seventh, because we included CEO overconfidence independent of whether the studies treated CEO overconfidence as a primary variable or a control variable, we created a dummy variable to indicate whether CEO overconfidence was the primary focus of the study or not (reference group). Finally, we included a dummy variable to indicate whether a study used lagged variables or not (reference group). 8

Meta-Analytic Procedure

To test our main effect (Hypotheses 1 and 1Alternative), we calculated the cumulative mean effect size estimate for the relationship between CEO overconfidence and firm performance using Hunter and Schmidt (1990) meta-analysis (HSMA). We also used HSMA to generate the cumulative mean effect size estimates as inputs for our MASEM. The central purpose of HSMA is to estimate the mean effect of one association at a time by aggregating effect sizes across many studies while correcting for sampling errors and statistical artifacts. While this approach is limited to testing multivariate theory (examining a single relationship in isolation), it offers the advantage of high statistical power from pooling a large number of observations (Combs, Crook, & Rauch, 2019).

To obtain an appropriate estimate of the meta-analytic mean effect size, we first considered differences in precision across effect sizes and variability in the population of effects by weighting the effects by the size of the sample of the underlying study (number of firms; Hunter & Schmidt, 1990; see Appendix D for the formula). Second, we corrected the individual correlations for measurement errors to account for imperfect construct validity (Hunter & Schmidt, 2004; see Appendix D for the formula). Because most studies did not report reliability coefficients, we followed best practice and applied a correction formula based on the assumption that both variables comprising individual correlations had validities of .80 (Bergh et al., 2016; Connelly, Crook, Combs, Ketchen, & Aguinis, 2018). We then calculated the cumulative effect size of the association between CEO overconfidence and firm performance, its standard error, the corresponding confidence interval, and two heterogeneity indices. As in most other meta-analyses on CEO attributes (e.g., Wang et al., 2016), there is heterogeneity in the effect sizes. For this reason, we used random effects (rather than fixed effects) models because they assume that the population effect size varies across studies (Geyskens, Krishnan, Steenkamp, & Cunha, 2009).

We used MASEM (Bergh et al., 2016) to test the mediating role of strategic risk taking in the relationship between CEO overconfidence and firm performance (Hypothesis 2). MASEM tests intermediate mechanisms in a chain of relationships. As compared with HSMA and meta-analytic regression analysis (MARA), it has the advantage of enabling powerful simultaneous tests of multiple theoretical relationships and does not require all relationships to be included in each primary study (Combs et al., 2019). In this two-stage method, we first calculated the meta-analytic effect size estimates for all relevant bivariate relationships (including controls) with HSMA. We arranged these estimates into a correlation matrix and used our meta-analytic estimates to fill in all missing cells. In the second stage, we carried out path analysis, inputting the correlation matrix into the software LISREL. We used the harmonic mean sample size because the sample sizes varied across the intercorrelations. The harmonic mean is a more conservative parameter estimate than the arithmetic mean (Viswesvaran & Ones, 1995).

We employed MARA (Gonzalez-Mulé & Aguinis, 2018)—a type of weighted least squares regression analysis—to test the moderating role of managerial discretion in the relationship between CEO overconfidence and strategic risk taking (Hypotheses 3a, 3b, and 3c). We also used MARA as a robustness test to examine how the main relationship (Hypotheses 1 and 1Alternative) changed when we included control variables. The central purpose of MARA is to test boundary conditions regarding what factors moderate the focal relationships. As compared with its alternative (i.e., comparing cumulative mean effect size estimates of subgroups with HSMA), MARA allows for simultaneous tests of multiple variables and the use of all information available in continuous moderator variables.

We used the effect sizes of CEO overconfidence and strategic risk taking as the dependent variables and modeled managerial discretion and a battery of control variables as independent variables. As with HSMA, we used sample size-weighted and measurement-corrected effect sizes. Following the recommendations by Gonzalez-Mulé and Aguinis (2018), we conducted MARA using a mixed effects model because the assumptions of a fixed effects model are not satisfied (i.e., a mature field in which the model includes all boundary conditions and the sample domain in the meta-analytic database closely matches the population). For HSMA and MARA, we used macros provided by Lipsey and Wilson (2001).

Results

Overall Effect of CEO Overconfidence on Firm Performance

While Hypothesis 1 predicted a negative relationship between CEO overconfidence and firm performance, Hypothesis 1Alternative predicted a positive relationship between CEO overconfidence and firm performance. The cumulative mean effect size estimate indicates that overall, CEO overconfidence has a statistically significant positive effect on firm performance (M = .07, p = .000, k = 441, n = 380,154, SE = .01, 95% CI [.06, .09]), supporting Hypothesis 1Alternative. 9

The mean effect (M = .07) is relatively small but is in line with prior meta-analyses on CEO attributes and firm performance in strategic management. For example, the mean effect size between CEO narcissism and firm performance is .06 (Cragun et al., 2020); that between female representation in the CEO position and long term-performance is .01 (Jeong & Harrison, 2017); and that between positive self-concept and firm performance is .07 (Wang et al., 2016). Because the outcome is firm performance, even small effect sizes can represent gains or losses of millions or billions of dollars (Dalton, Daily, Certo, & Roengpitya, 2003; Jeong & Harrison, 2017; Wang et al., 2016). To demonstrate the practical importance of Hypothesis 1Alternative, we followed the procedure by Wang and colleagues (2016) and applied our results to the sample of Agle and colleagues (2006). Our results suggest that an increase in CEO overconfidence of 1 SD is related to an increase in firm performance of 0.15 SD. Agle, Nagarajan, Sonnenfeld, and Srinivasan (2006) reported a mean future ROA (i.e., industry-adjusted ROA after 1992) of 5.94% with a standard deviation of 12.00%. In this case, an increase of 1 SD in CEO overconfidence translates to a 1.8% (12.00% × .15) increase in ROA. Given that the mean total assets of the firms in Agle et al. (2006) is US $6.5 billion (i.e., industry-adjusted ROA after 1992), an increase of 1 SD in CEO overconfidence translates into an increase of US $117 million (1.8% × 6.5 billion US dollars).

Furthermore, the effect size distribution variance is relatively high (Q = 8,934.06, I2 = .99, T2

Finally, we tested how the main relationship changed when we included control variables. The results indicate that the relationship between CEO overconfidence and firm performance is stronger when a study was published (β = .09, SE = .02, p = .000) and weaker when a journal's impact factor is higher (β = −.01, SE = .00, p = .001). The significant positive effect for median sample year suggests that the effect of CEO overconfidence becomes more positive over time (β = .00, SE = .02, p = .026); however, the beta coefficient is close to 0. The focal relationship is also stronger with a US sample (β = .13, SE = .02, p = .000). The results additionally show that panel design (β = −.02, SE = .06, p = .776), field of management (β = .02, SE = .02, p = .349), CEO overconfidence as the focus of the study (β = .00, SE = .02, p = .857), and whether the variables were lagged or at the same year (β = −.04, SE = .03, p = .271) did not have a substantive impact on the focal relationship.

The Mediating Role of Strategic Risk Taking

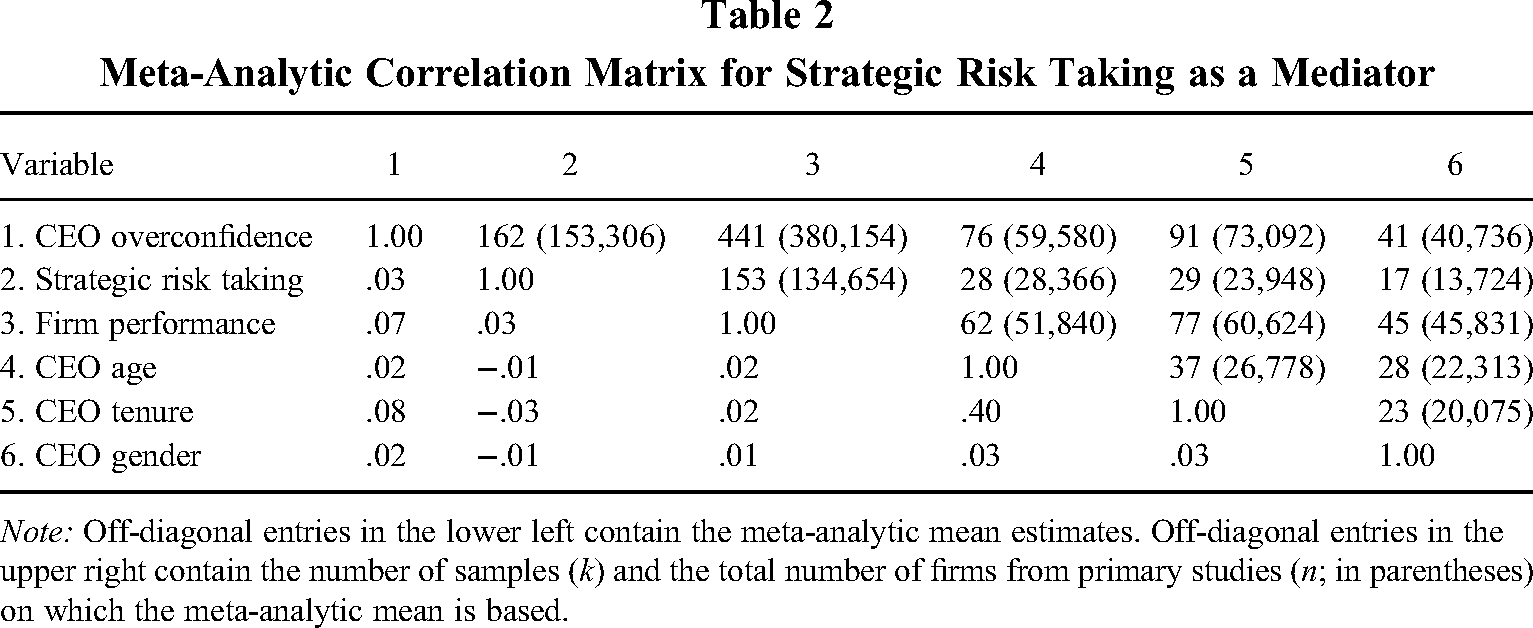

We first created a correlation matrix from the meta-analytic mean estimates of the relevant bivariate relationships to test our mediation model, which served as the input into our meta-analytic path analysis (Table 2). Each cell below the diagonal reports the results for separate HSMAs for each bivariate relationship. The cells above the diagonal show the total number of effect sizes (k) and the total sample sizes (n; i.e., number of firms) from which we derived the mean estimates. Figure 2 illustrates the model and results when controlling for CEO tenure, age, and gender. The model fits the data well (χ2 = 184.68, goodness-of-fit index [GFI] = .99, standardized root mean squared residual [SRMR] = .02, root mean squared error of approximation [RMSEA] = .07).

Structural Path Analysis of Strategic Risk Taking as a Mediator

Meta-Analytic Correlation Matrix for Strategic Risk Taking as a Mediator

Note: Off-diagonal entries in the lower left contain the meta-analytic mean estimates. Off-diagonal entries in the upper right contain the number of samples (k) and the total number of firms from primary studies (n; in parentheses) on which the meta-analytic mean is based.

Hypothesis 2 predicted that strategic risk taking mediates the relationship between CEO overconfidence and firm performance—specifically, CEO overconfidence is positively associated with strategic risk taking, and strategic risk taking is positively associated with firm performance. As reported in Figure 2, the results show that CEO overconfidence is positively related to strategic risk taking (β = .04, SE = .01, t = 7.019, p = .000) and that strategic risk taking is positively related to firm performance (β = .03, SE = .01, t = 5.265, p = .000). 10 As the direct path from CEO overconfidence to firm performance remains significant when added to the model, we conclude that strategic risk taking partially mediates the relationship between CEO overconfidence and firm performance (Aguinis, Edwards, & Bradley, 2017). The Sobel (1982) test confirms that the relationship between CEO overconfidence and firm performance is channeled through the hypothesized pathway (z = 4.47, p = .000). These results support Hypothesis 2.

Moderating Role of Managerial Discretion

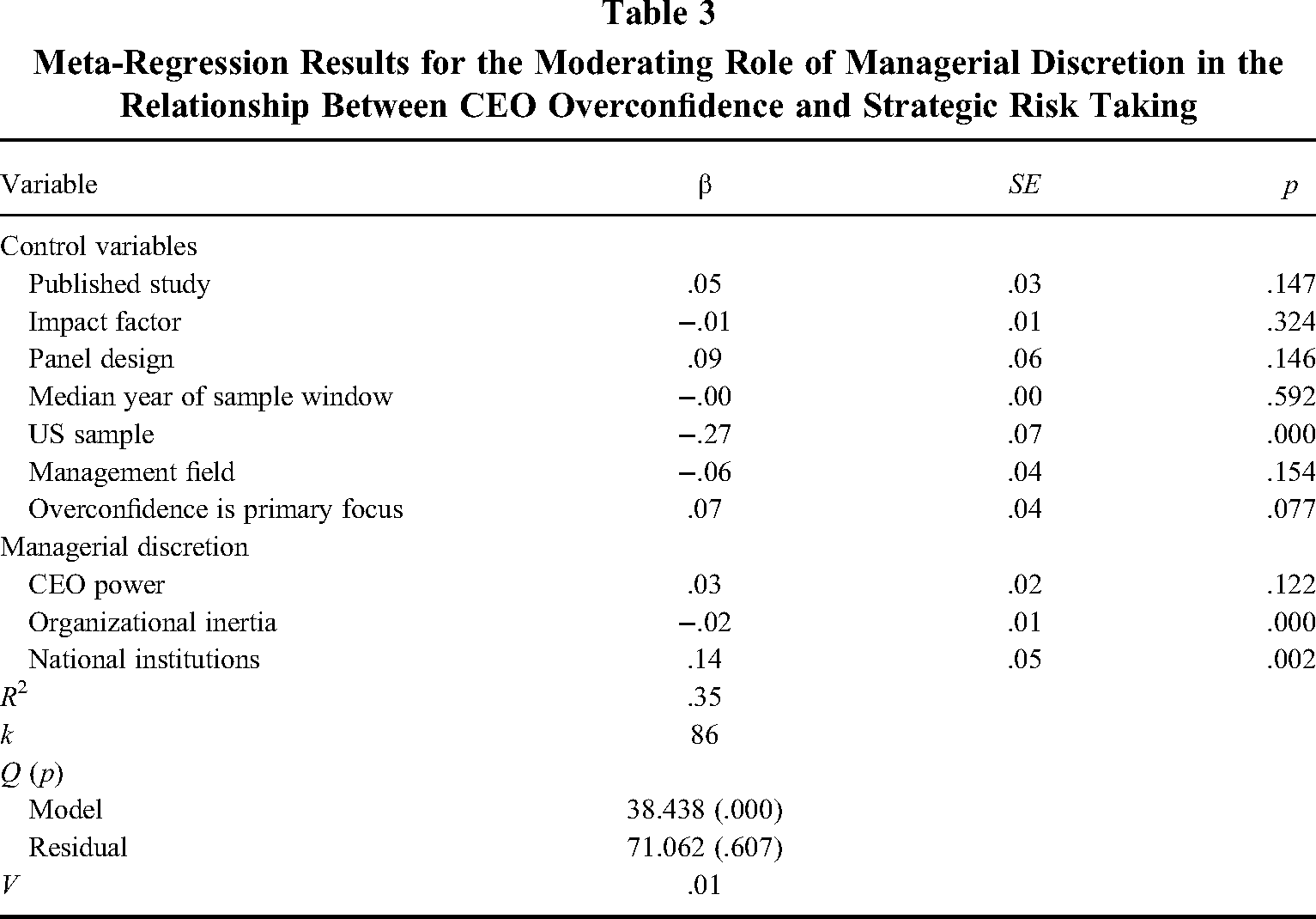

Table 3 provides the meta-analytic regression results. The dependent variable is the relationship between CEO overconfidence and strategic risk taking, and the independent variables are managerial discretion and the control variables. The model fits the data well with an R2 value of .35. The Q test of the model's residual component is nonsignificant (Qresidual = 71.06, p = .607), implying that the moderators sufficiently model the variance (see Lipsey & Wilson, 2001).

Meta-Regression Results for the Moderating Role of Managerial Discretion in the Relationship Between CEO Overconfidence and Strategic Risk Taking

Hypothesis 3 predicted that managerial discretion moderates the relationship between CEO overconfidence and risk taking such that (a) CEO power magnifies, (b) organizational inertia dampens, and (c) weaker national institutions magnify the positive relationship between CEO overconfidence and strategic risk taking. As shown in Table 3, the moderating effect of national institutions is significant and positive (β = .14, SE = .05, p = .002), and the effect of inertia is significant and negative (β = −.02, SE = .01, p = .000). The effect for CEO power is nonsignificant (β = .03, SE = .02, p = .122). Thus, these results support Hypotheses 3b and 3c but do not support Hypothesis 3a.

The results in Table 3 indicate that the relationship between CEO overconfidence and strategic risk taking is weaker for a US sample (β = −.27, SE = .07, p = .000). The results also show that while CEO overconfidence as the focus of the article (β = .07, SE = .04, p = .077) has a marginal significant impact on the relationship between CEO overconfidence and strategic risk taking, the following are nonsignificant: published studies (β = .05, SE = .03, p = .147), impact factor (β = −.01, SE = .01, p = .324), panel design (β = .09, SE = .06, p = .146), median year of sample window (β = −.00, SE = .00, p = .592), and field of management (β = −.06, SE = .04, p = .154).

Supplemental Analyses

Nonmonotonic pattern of CEO overconfidence

Recent research has argued that CEO overconfidence is nonmonotonic such that moderate levels of overconfidence are beneficial but very high levels of overconfidence are detrimental (e.g., Campbell et al., 2011; Goel & Thakor, 2008). To explore a curvilinear pattern for the relationship between CEO overconfidence and firm performance (Ng & Feldman, 2012; Rosenbusch, Brinckmann, & Müller, 2013), we coded the study-level averages of CEO overconfidence (k = 369). We then classified the study-level averages into different percentile groups: very low (10th percentile), moderate (40th–60th percentile), and very high (90th percentile) levels of overconfidence. We calculated the cumulative mean effect size estimate for each group using HSMA. The results show that for samples with very low overconfidence, the relationship between CEO overconfidence and performance is positive and marginally significant (M = .04, p = .086, k = 39, n = 28,250, SE = .03, 95% CI [–.01, .10]); for moderate overconfidence, the relationship is positive and significant (M = .08, p = .000, k = 87, n = 76,266, SE = .02, 95% CI [.04, .12]); and for very high overconfidence, the relationship is nonsignificant (M = .03, p = .161, k = 36, n = 17,208, SE = .02, 95% CI [−.01, .08]). We used the Q test based on analysis of variance to test whether the effect sizes differ as a function of group membership (Borenstein, Hedges, Higgins, & Rothstein, 2009). The results show significant between-group heterogeneity for the comparison between moderate and very high overconfidence (Q = 15.52, p = .000) and that between moderate and low overconfidence (Q = 29.00, p = .000), indicating that the magnitude of the effects varied as a function of the level of CEO overconfidence. This exploratory analysis provides some initial (but not conclusive) evidence of a possible curvilinear pattern because the overconfidence-performance relationship is significant and has a higher effect size for moderate levels of overconfidence as compared with the low and very high levels of overconfidence, which show marginally or nonsignificant relationships that are lower in effect size.

Unpacking the firm performance measures

To better understand whether performance indicators drive our findings, we disaggregated firm performance into accounting- and market-based performance measures. We used HSMA to calculate the cumulative mean effect size for each type of performance measure. For the relationship between CEO overconfidence and firm performance, the mean effect size estimates indicate that the relationships between CEO overconfidence and accounting (M = .06, p = .000, k = 212, n = 169,723, SE = .01, 95% CI [.04, .08]) and market performance (M = .08, p = .000, k = 229, n = 210,431, SE = .01, 95% CI [.06, .10]) are significant and positive.

We ran the mediation model with accounting and market performance measures. We first created the correlation matrices from the meta-analytic mean estimates among all variables of interest (the correlation tables are reported in Appendix E). The MASEM models fit the data well (χ2market = 195.910, GFI = .998, SRMR = .017, RMSEA = .078; χ2accounting = 103.625, GFI = .999, SRMR = .013, RMSEA = .058). For the market-based model, the results indicate that CEO overconfidence is positively related to strategic risk taking (β = .03, SE = .01, t = 5.851, p = .000) and that strategic risk taking is positively associated with market performance (β = .05, SE = .01, t = 8.986, p = .000). For the accounting-based model, the results indicate that CEO overconfidence is positively related to strategic risk taking (β = .03, SE = .01, t = 5.728, p = .000) and that strategic risk taking is positively but marginally significantly associated with accounting performance (β = .01, SE = .01, t = 1.905, p = .057). We used a z test (Raju & Brand, 2003) to evaluate whether the path coefficients differ across the two types of performance outcomes. The results reveal that risk taking is more strongly linked to market performance as compared with accounting performance (z = −2.823 p = .005). We discuss the implications of these findings in the Discussion section.

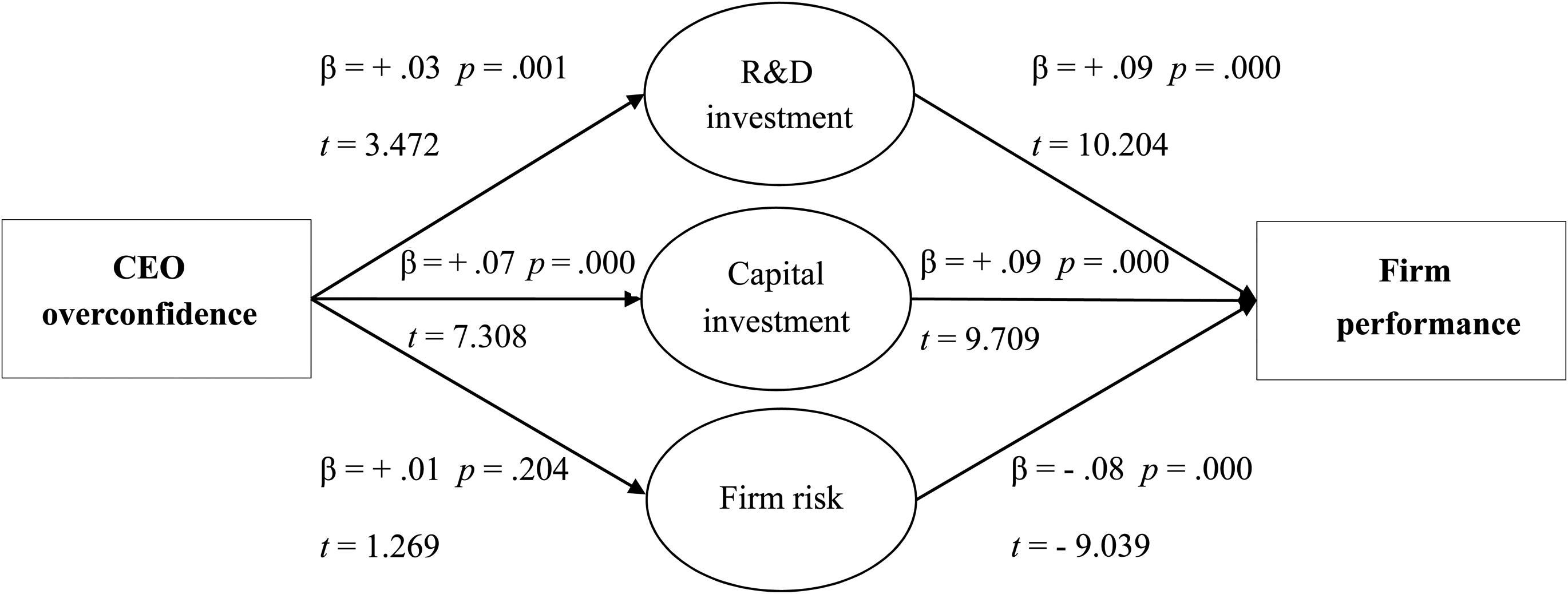

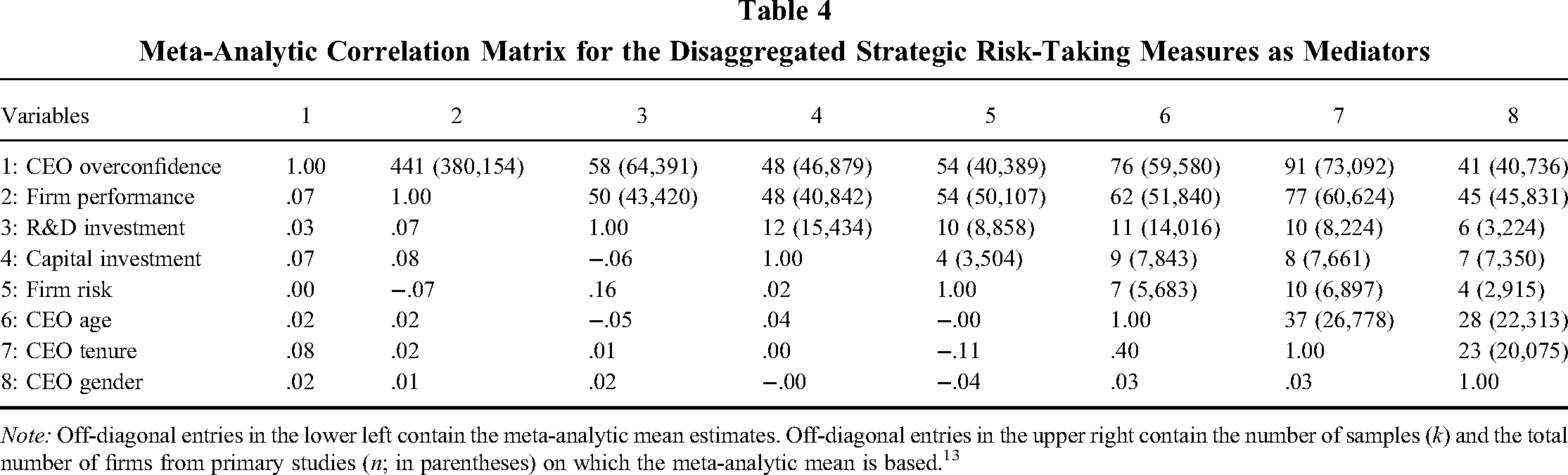

Unpacking the different strategic risk-taking measures

To better understand the nature of the mediating effects of strategic risk taking, we ran the mediation analyses with disaggregated strategic risk-taking variables. We created a correlation matrix from the meta-analytic mean estimates among all variables of interest (Table 4). The fit statistics are χ2 = 437.16, GFI = .99, SRMR = .03, and RMSEA = .096. The results in Figure 3 indicate that CEO overconfidence is positively related to R&D investment (β = .03, SE = .01, t = 3.472, p = .001) and capital investment (β = .07, SE = .01, t = 7.308, p = .000). They also indicate that R&D investment (β = .09, SE = .01, t = 10.204, p = .000) and capital investment (β = .09, SE = .01, t = 9.709, p = .000) are positively related to firm performance. Interestingly, CEO overconfidence has a nonsignificant relationship with firm risk (β = .01, SE = .01, t = 1.269, p = .204), and firm risk has a negative relationship with firm performance (β = −.08, SE = .01, t = −9.039, p = .000). These findings imply that in general, with the exception of firm risk, overconfident CEOs’ risky strategies are beneficial for firm performance.

Structural Path Analysis of Different Strategic Risk-Taking Measures as Mediators

Meta-Analytic Correlation Matrix for the Disaggregated Strategic Risk-Taking Measures as Mediators

Note: Off-diagonal entries in the lower left contain the meta-analytic mean estimates. Off-diagonal entries in the upper right contain the number of samples (k) and the total number of firms from primary studies (n; in parentheses) on which the meta-analytic mean is based. 13

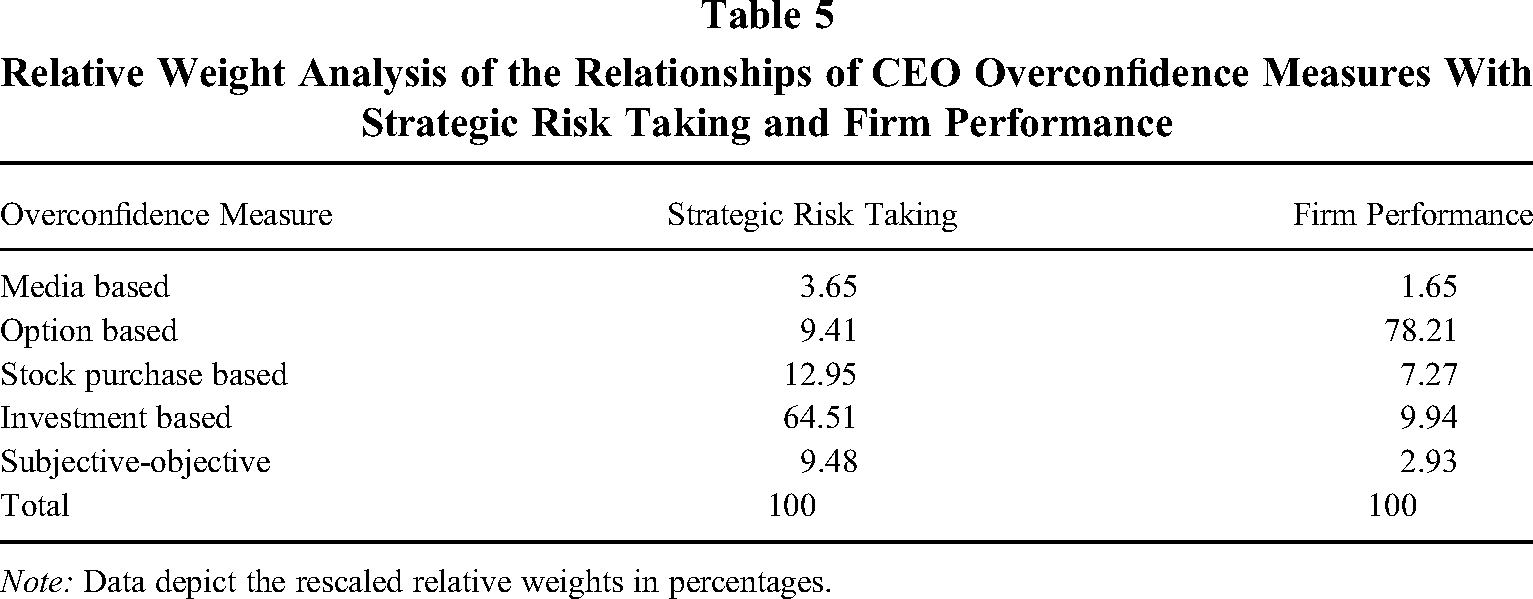

Relative weight analysis of different CEO overconfidence measures

We used meta-analytic relative importance analysis to estimate how much the different CEO overconfidence measures matter relative to the relationships of CEO overconfidence with strategic risk taking and firm performance (Oh, 2020). This approach was recently introduced for meta-analyses (e.g., Gonzalez-Mulé, Cockburn, McCormick, & Zhao, 2020). We followed Gonzalez-Mulé et al. (2020) and used Johnson and LeBreton’s (2004) relative weight analysis, which provides an index of relative importance derived as the proportionate contribution of a predictor to overall model variance that considers the correlations between predictors. The results in Table 5 show, for instance, that the option-based measures are the most important predictors of firm performance, accounting for more than 70% of the variance in firm performance (rescaled relative weights = 78.21%). 11 All other measures account for less than 10% each. Our analysis also indicates that the investment-based measures are most important for predicting strategic risk taking (rescaled relative weights = 64.51%). All other measures accounted for less than 13% each.

Relative Weight Analysis of the Relationships of CEO Overconfidence Measures With Strategic Risk Taking and Firm Performance

Note: Data depict the rescaled relative weights in percentages.

Robustness Checks

We conducted several robustness tests. First, research has suggested that CEO overconfidence can lead to CEOs’ self-attributions of prior successes (e.g., Billett & Qian, 2008). We tested this possibility using primary studies reporting lagged effect sizes for the relationship between prior firm performance and CEO overconfidence. The results show that this relationship is not statistically significant (M = −.01, p = .862, k = 30, n = 35,653), mitigating potential concerns about reverse causality.

Second, we employed two outlier detection assessments to determine if outliers influenced the results. We used one-sample-removed analysis (Borenstein et al., 2009) and multivariate multidimensional influence diagnostics (Viechtbauer & Cheung, 2010). We ran the CEO overconfidence–firm performance relationship after removing the sample's four outliers. There was no substantive change to the results presented for Hypothesis 1Alternative (M = .07, p = .000). Thus, following the best practice recommendations from Steel et al. (2021), we retained the outliers in our analyses because we did not have information on whether they were legitimate observations or errors.

Third, following the recommendations by Steel and colleagues (2021), we performed several analyses on publication bias. In addition to the comparison of study sources (published vs. unpublished) reported in the main results, we conducted the following tests: (1) Duval and Tweedie’s (2000) trim and fill, (2) selection models (Hedges & Vevea, 2005), and (3) precision effect estimate with standard errors (Stanley & Doucouliagos, 2014). The results show that the random effects trim-and-fill adjusted mean estimate is .13, and the precision effect estimate with standard errors (two-tailed weighted least squares approach) is .10. These findings might be unexpected if publication bias was present—they indicate that publication bias has led to underestimating the main effect. However, the moderate selection model adjusted estimate is .03, indicating that our main effect is moderately underestimated. These results indicate that publication bias is present, but the main effect remains relatively stable across these tests. We used the Comprehensive Sensitivity Analysis Tool (Field, Bosco, Kepes, McDaniel, & List, 2018) for all tests regarding outliers and publication bias.

Finally, to rule out the possibility that stochastic dependencies among multiple effect sizes obtained from a single primary study distorted our results, we conducted a hierarchical linear modeling meta-analysis (Raudenbush & Bryk, 2002). The results indicate that this potential distortion does not substantively influence our results (M = .09, p = .000).

Discussion

By consolidating a large body of CEO overconfidence research across disciplinary boundaries with meta-analytic methods, we offer important insights that help answer how and why CEO overconfidence influences firm performance.

First, we clarify the empirical relationship between CEO overconfidence and firm performance. Conflicting findings from past research on CEO overconfidence have hindered us from clearly inferring the link between CEO overconfidence and firm performance. This study demonstrates that CEO overconfidence is, on average, positively related to firm performance. Second, we demonstrate that the relationship between CEO overconfidence and firm performance is partially mediated through strategic risk taking. The results regarding managerial discretion essentially validate the robustness of this finding. They show that managerial discretion, except CEO power, magnifies the relationship between CEO overconfidence and strategic risk taking. These findings offer strong empirical evidence for the well-established but rarely empirically tested process perspective of UET (Liu et al., 2018; Neely et al., 2020). Our identification of strategic risk taking as a mediator is also a response to recent calls to identify explanatory mechanisms through which CEO overconfidence is linked to firm outcomes—a topic that has been largely neglected in past research (Heavey et al., 2022).

Implications and Directions for CEO Overconfidence Research

Our finding regarding the relationship between CEO overconfidence and firm performance is consistent with recent developments in CEO overconfidence research that view overconfidence in a more positive light (e.g., Galasso & Simcoe, 2011; Reyes et al., 2020). Importantly, this finding does not imply that CEO overconfidence is always beneficial or that more CEO overconfidence leads to better performance without limit. Our finding does imply, however, that while the negative side of CEO overconfidence has received more theoretical attention and is held as a common popular belief, performance benefits from CEO overconfidence do exist and should not be ignored. Thus, future research needs to pay more systematic attention to the positive side of CEO overconfidence and the conditions under which CEO overconfidence can lead to positive or negative outcomes. For example, it seems possible that the relationship between CEO overconfidence and firm performance is curvilinear and that an optimal degree of CEO overconfidence exists. Indeed, recent literature suggests that moderate degrees of CEO overconfidence are beneficial, while high degrees of CEO overconfidence are harmful to firm outcomes (e.g., Campbell et al., 2011; Goel & Thakor, 2008). Our supplementary analysis shows initial evidence of a nonmonotonic relationship. Thus, including CEO overconfidence as a linear variable in models of firm performance may be overly simplistic. Empirical evidence of nonmonotonic relationships is still rare in the overconfidence literature, and future research should seek to better understand optimal degrees of CEO overconfidence for firm performance.

Future research could explore factors that help reap the desirable outcomes of overconfidence and temper the negative effects of excessive overconfidence on firm performance. At the individual level, a promising direction for future research would be to investigate the interaction of CEO overconfidence with other CEO attributes that temper the harmful effects and magnify the positive effects of overconfidence—topics that have been largely neglected in research. For example, similar to narcissism (Owens, Wallace, & Waldman, 2015), CEO overconfidence may be beneficial for firm performance when counterbalanced by humility but may be harmful with other CEO attributes. At the firm level, compensation contracts (Chng, Rodgers, Shih, & Song, 2012) that help regulate the functional and dysfunctional effects of CEO overconfidence warrant attention in future research.