Abstract

We build on neo-institutional theory to examine the manner in which nation-level institutions systematically affect domestic acquisitions—that is, acquisitions involving acquirers and targets from the same country. Specifically, we study in what way premiums are influenced through a set of cognitive, normative, and regulatory forces. In terms of cognitive pressures, we theorize that prior premium decisions of industry peers in the same country influence focal acquisition premiums, since prior premium decisions serve as reference frames for firms. In addition, we posit that normative forces in the form of the national cultural values of uncertainty avoidance, future orientation, and in-group collectivism affect bid premiums, as these factors influence the manner in which firms deal with the uncertainty, payoff time, and merger of groups inherent to acquisitions. Furthermore, we propose that a country’s regulatory pressures through its disclosure requirements influence premiums, since they reduce information asymmetries and affect a firm’s confidence in assessing its potential gains from acquisitions. Using a sample of domestic acquisitions, we find support for several of the hypotheses. Our work offers a cross-country comparative study of how nation-level institutions affect domestic bid premiums and makes theoretical contributions to acquisition premium research and institutional theory.

Keywords

Although corporate acquisitions have been growing in numbers around the world (Institute for Mergers and Acquisitions, 2019), many fail to create value for the acquiring firms. One important element that can predict the success/failure of acquisitions is the acquisition premium (Haunschild, 1994), which refers to the difference between the price offered to acquire a target firm and the preacquisition market value of the target (Beckman & Haunschild, 2002; Laamanen, 2007). As a result, scholars and practitioners alike have attempted to understand the determinants of acquisition premiums.

While prior research has often studied deal, firm, and industry characteristics, it has largely overlooked acquisitions as embedded in institutional environments, which differ across countries. This is surprising, because external institutions exert significant pressures that shape the behaviors of firms (Marquis & Huang, 2010; Scott, 2008), which have been showcased across a wide range of managerial phenomena (e.g., Dacin, Goodstein, & Scott, 2002; Kostova, Roth, & Dacin, 2008). For example, previous management research has demonstrated the impact of nation-level institutions on acquisition prevalence (Maas, Heugens, & Reus, 2019) and performance (Morosini, Shane, & Singh, 1998). Since bid premiums are subjected to great uncertainty (Laamanen, 2007; Welch, Pavićević, Keil, & Laamanen, 2020), and because the institutional environment significantly shapes organizational decisions in the face of uncertainty (DiMaggio & Powell, 1983; Scott, 2008), work conducted in this area has the potential to shed light on the manner in which institutional forces impact acquisition premium decisions across different countries.

Interestingly, SDC Platinum data on domestic acquisitions—that is, acquisitions involving acquirers and targets from the same country—between 1991 and 2017 show that significant variation exists on country-level average acquisition premiums. For instance, the average acquisition premium offered is only 7.3% in South Korea and 11.8% in Japan, while it is 35.3% in the United Kingdom and 32.1% in the United States. Thus, it seems appropriate to conduct a cross-country comparative study of premiums to explain why differences in premiums exist across countries. Due to its analytical focus on institutional fields, we draw on neo-institutional theory that allows for the study of environmental effects (Aguilera & Grøgaard, 2019), as we examine the systematic influence of nation-level institutions on domestic acquisition premiums in a cross-country comparative analysis.

We build on research that has investigated the impact of the institutional environment on organizational decisions to derive a set of hypotheses. These hypotheses link the bid premium to (a) the cognitive pillar, which draws on behavioral orthodoxy (Xu & Shenkar, 2002); (b) the normative pillar, which is grounded in societal beliefs and norms (Kostova, 1997); and (c) the regulatory pillar, which is anchored in formal rules and sanctions as its basis of legitimacy (DiMaggio & Powell, 1983). First, we argue that prior premiums exert cognitive pressures on focal premium decisions, because previous decisions adopted by other organizations become taken-for-granted over time and part of the repertoire of legitimate solutions that focal decision-makers draw upon (Meyer & Rowan, 1977; Scott, 2008). Second, we suggest that normative forces in the form of the cultural values uncertainty avoidance, future orientation, and in-group collectivism affect bid premiums. Third, we argue a country’s disclosure requirements—the extent to which information is revealed by firms—influence premiums through regulatory pressures, due to their implications on information asymmetries inherent in acquisition premium decisions. We test these hypotheses on a sample of 21,304 acquisition premiums offered in 34 countries from 1991 to 2017 and find support for our hypotheses.

Our study links institutional theory with work on acquisitions, as we shed light on the manner in which specific nation-level cognitive, normative, and regulatory institutions affect bid premiums. As a result, we advance understanding of the antecedents of premium decisions from a cross-country comparison perspective in which we show acquisition premiums are fundamentally shaped by national institutional contexts, which demonstrates that premium decisions are both subjective and contextual (Beckman & Haunschild, 2002). Responding to calls to advance research on institutions beyond its use as a catch-all concept (e.g., Aguilera & Grøgaard, 2019), this study also helps untangle and critically assess institutions across contexts by systematically drawing on the underlying elements of neo-institutionalism and developing a nuanced understanding of how specific institutions influence firms.

Theory and Hypotheses

Acquisition premium refers to the price the acquirer/bidder offers to acquire a target firm in excess of the target firm’s prevailing market value (Cho, Arthurs, Townsend, Miller, & Barden, 2016; Hayward & Hambrick, 1997). Firms offer a price premium, because they expect to benefit from synergies that exceed the sum of the current market value of the target firm and the premium offered (Laamanen, 2007). While this rationale is widely accepted as the sensible underlying motivation for these “overpayments,” previous evidence documents that the price premium offered often has little to do with anticipated synergies, as the premium decision is complex and subject to several key challenges (Beckman & Haunschild, 2002; Welch et al., 2020).

Extant work has established that premiums are a negotiated outcome, involving multiple parties that include the firms’ CEOs and, oftentimes, their executive boards or special committees formed by the boards (e.g., Beckman & Haunschild, 2002; Hayward & Hambrick, 1997; Heitzman, 2011; Laamanen, 2007). As such, the acquirer needs to offer a price premium considered legitimate by the parties involved. Finding the appropriate premium is challenging for several reasons inherent to acquisitions, however. First, information asymmetry often hampers acquirer ability to predict the present values of future cash flows under alternative ownership/management scenarios (Baker, Pan, & Wurgler, 2012; Beckman & Haunschild, 2002). Second, even if the acquirer has complete information about the target firm at the time of the acquisition, the long payoff time creates additional challenges (Capron, 1999; Zollo & Singh, 2004). For example, future changes with respect to new technological developments, industry competitors, and governmental regulations can alter the outcome of the acquisition (Appelbaum, Gandell, Shapiro, Belisle, & Hoeven, 2000). Third, synergy is crucial in the valuation of firms, but it critically depends on how skillfully firms conduct postacquisition integration (Buono & Bowditch, 2003). Moreover, lack of information can create additional uncertainty in the negotiation and valuation of the target, as firms may misinform during negotiations (Baker et al., 2012). Hence, premium decisions are mired in great uncertainty.

Neo-institutional theory, the most prominent subdomain of institutional research, postulates that organizational decisions are driven by the intention of organizations to maintain or increase legitimacy in the face of uncertainty rather than purely by economic efficiency considerations (Scott, 2008). More specifically, external institutions exert a significant influence on the behaviors and decisions of organizations when uncertainty is pronounced (Meyer & Rowan, 1977). These external forces determine the strategies of firms and suggest that the institutional context, in which firms are embedded, constrains their operations (Oliver, 1991). Institutional scholars propose that institutions consist of three distinct pillars (Scott, 2008): the cognitive, normative, and regulatory pillar. Since premium decisions are subjected to great uncertainty, we expect firms to seek legitimacy and conform to taken-for-granted norms due to institutional pressures. Thus, we explore the manner in which these institutional pillars affect bid premiums, which should help generate insights into bid premium decisions beyond extant work.

The Cognitive Pillar and Acquisition Premium

The cognitive pillar of institutions stresses institutional elements that constitute the nature of reality and the frames through which meaning is created (DiMaggio & Powell, 1983). A cognitive view, thus, emphasizes legitimacy rooted in the adoption of a common frame of reference (Scott, 2008). As such, this cognitive view focuses on the link between the external world of stimuli and the response of individuals to these stimuli, which is essentially a collection of internalized symbolic representations of the individuals’ world (Scott, 2008). Since individuals, such as managers, interpret and make sense of the world based on their own perceptions of reality, they create cognitive maps that become taken-for-granted and reflect the repertoire of issues and solutions taken into consideration in complex and uncertain situations (Ocasio, 1997). Consequently, organizational decision makers tend to limit their search for solutions in complex and uncertain situations to alternatives that have a high level of legitimacy, particularly to those that have been adopted by other organizations (Meyer & Rowan, 1977). Institutional influences are exerted in many cases because other types of behavior are inconceivable (Scott, 2008). Solutions are then adopted simply because they are taken-for-granted as the way things are being done (DiMaggio & Powell, 1983). Hence, the prevalence of a solution is a suitable indicator of its “taken for grantedness” (Scott, 2008).

One of the key challenges of premium decisions is to determine a legitimate price premium considered appropriate and justifiable by the parties involved in the acquisition process. Based on the cognitive pillar logic, we expect the premiums offered by other firms in the same country and industry prior to a focal premium decision to constitute a reference frame perceived as legitimate for the acquirer and target firms. Prior work shows decisions made by other firms serve as taken-for-granted references for focal firms across a wide range of organizational phenomena (Scott, 2008). For instance, Salomon and Wu (2012) build on the institutional theory’s cognitive pillar to show foreign firms imitate the decisions of their domestic counterparts to gain legitimacy. In addition, Li, Yang, and Yue (2007) used the cognitive lens to reveal that firms adopt peer entry mode decisions, as these decisions are viewed as taken-for-granted and help the focal firms build legitimacy. Finally, Haveman (1993) found firms base their diversification strategies on their peers’ prior diversification activities and imitate these activities. Extant work frequently has used industry to identify a focal firm’s social reference group, whose decisions are used by the firm as a reference, because firms in the same country and industry tend to share similar challenges, constraints, and strategies (Xia, Tan, & Tan, 2008).

Building on this rationale, we argue acquirers consider the level of premiums typically offered by industry peers in the same country as a legitimate reference. That is, acquirers limit their search for potential premiums to those alternatives adopted by their peers as a means to generate legitimacy (Meyer & Rowan, 1977). As a result, a focal acquirer will offer a premium similar to what is commonly paid in the same country and industry context (Scott, 2008). While acquirers prefer to pay as little as possible, they will not consider offering a premium too low compared to prior offers or else risk losing legitimacy. Targets follow a similar rationale: While they attempt to obtain the highest possible price, they are constrained in their choice of potential premiums by their cognitive reference frame and will not consider demanding a price much greater than what is commonly considered legitimate. Therefore, the average previously offered premium in a country’s industry will be positively related to the focal firm premium. 1 Accordingly, we expect:

Hypothesis 1a: The average premiums previously offered by industry peers in the country positively relates to the premium offered in a focal acquisition.

While the cognitive view stresses the legitimacy of taken-for-granted decisions rooted in a common frame of reference (Scott, 2008), we argue the degree of taken-for-grantedness varies. Previous work on institutional theory argues institutions are “historical accretions of past practices and understandings that set conditions on action” by way of which they “gradually acquire the moral and ontological status of taken-for-granted facts which, in turn, shape future interactions” (Barley & Tolbert, 1997: 99). Thus, institutionalization comprises a lengthy process during which a behavior experiences continuous adoption across actors (Phillips, Lawrence, & Hardy, 2004). If a growing number of organizations adopt a particular behavior/solution, the more institutionalized the behavior/solution will become over time and the more costly deviation from it will be (Lawrence, Winn, & Jennings, 2001). These costs can be financial (due to increased risks involved), cognitive (due to greater thought required), and social (due to reduced access to resources) (Phillips et al., 2004).

However, there are likely ways in which perceived taken-for-grantedness is reduced. For example, in the context of acquisition premium decisions, we expect increased variability of prior premiums will reduce the degree of taken-for-grantedness and the extent to which the acquirer and target use the average premium offered in the past as a reference frame. If the acquisition premiums previously offered in the country’s industry deviate greatly from each other, acquiring and target firms likely will not perceive the average premium as the only legitimate alternative. Instead, the firms will consider a wider range of premiums as legitimate options. However, if acquisition premiums within the country’s industry context do not deviate greatly from each other, acquirers and targets will take the average premium as taken-for-granted and heavily rely on it as a stable reference for their own premium decision (Weber & Glynn, 2006). Hence, the relationship between the average acquisition premium in the past and the focal premium offer will be weaker the greater the variation of prior premiums is. We propose:

Hypothesis 1b: The variation of the premiums previously offered by industry peers in the country negatively moderates the relation between previous average premiums and the premium of a focal acquisition.

The Normative Pillar and Acquisition Premiums

The normative pillar emphasizes the rules that provide prescriptive, evaluative, and obligatory dimensions in everyday life (DiMaggio & Powell, 1983). It consists of societal values—conceptions of the preferred/desirable—and norms, which are legitimate means that specify how things should be done to pursue valued ends (Scott, 2008). Thus, normative systems specify the goals and objectives in a society and the means to pursue these goals/objectives. Expectations on how goals should be pursued are held by actors in society and are experienced as external pressures by a focal actor (Scott, 2008). Over time, and to varying degrees, the actor can externalize theses expectations to help structure its choices. Actors choose decisions not (only) because it serves their individual interests but (also) because they are expected to do so by others (DiMaggio & Powell, 1983). As a result, normative institutions impose constraints on social behavior and, at the same time, empower and enable social action (Scott, 2008). These shared values and norms are manifested in national culture (Hofstede, 2001). As such, management scholars have frequently used cultural values, which refer to shared beliefs about what is desirable and how individuals should behave in a society (House, Hanges, Javidan, Dorfman, & Gupta, 2004), to examine the normative element of institutions (e.g., House et al., 2004; Martin, Cullen, Johnson, & Parboteeah, 2007; Parboteeah, Hoegl, & Cullen, 2008).

Extant management research has predominantly used a dimensions approach to conceptualize cultural values (Tung & Verbeke, 2010). The main premise of the dimensions approach to culture is that societies confront similar basic challenges when they come to regulate human activity (Hofstede, 2001). The way societies respond to these basic challenges comprise their fundamental normative institutions while the analysis of these challenges/responses points to dimensions on which cultures can be compared (Huang, Zhu, & Brass, 2017; Siegel, Licht, & Schwartz, 2013). Given the large number of cultural dimensions and their considerable correlation with each other, we adopt prior recommendations and develop hypotheses for cultural values dimensions that should affect the premium decisions consistent with our theory (Cullen, Parboteeah, & Hoegl, 2004; Kostova, 1997). Specifically, we examine those dimensions directly related to the key challenges of acquisitions that critically affect acquisition premiums: uncertainty, payoff time, and merger of groups (Parboteeah et al., 2008; Scott, 2008).

We first examine uncertainty avoidance, which refers to “the extent to which members of an organization or society strive to avoid uncertainty by relying on established social norms, rituals, and bureaucratic practices” (House et al., 2004: 11). Institutional theorists have frequently studied the impact of uncertainty avoidance on a wide range of diverse managerial issues that relate to the tolerance of a society’s individuals and organizations toward ambiguity. Extant studies, for example, find that uncertainty avoidance stifles innovation activities of domestic firms, as it reduces the willingness of firms to take risks and explore novel solutions through experimentation (Nam, Parboteeah, Cullen, & Johnson, 2014). We study uncertainty avoidance, because uncertainty is a key challenge of acquisitions and premium decisions are characterized by considerable uncertainty (Beckman & Haunschild, 2002), particularly for the acquirer. The acquirer typically does not possess all information on the target firm, and even if the acquirer has all (or sufficient) information about the target, it cannot know for certain if the acquisition will unfold as expected (Coff, 1999; Lubatkin, 1983; Officer, 2004). The greater the premium payment, the greater the likelihood (and uncertainty) the acquirer will not be able to recoup the payment. Since the degree of a country’s uncertainty avoidance determines acquirer comfort in dealing with the increased uncertainty associated with greater premiums, acquirers from countries that score high on uncertainty avoidance likely offer a lower premium. From the target’s perspective, it can avoid facing an uncertain future by selling its firm for a certain immediate payment. Thus, the target should be more willing to accept lower acquisition premiums in higher uncertainty avoiding countries.

Hypothesis 2a: The level of uncertainty avoidance in the country negatively relates to the premium offered in a focal acquisition.

We next examine the cultural dimension future orientation, which is “the degree to which individuals in organizations or societies engage in future-oriented behaviors such as planning, investing in the future, and delaying individual or collective gratification” (House et al., 2004: 12). Previous work on institutions has used the future orientation dimension—or related time orientation dimensions such as long-term orientation—to study various managerial phenomena that are in-/directly linked to the tradeoff between immediate and future gains. For example, Buck, Liu, and Ott (2010) draw on institutional theory to demonstrate that the dimension predicts the strategic commitment of joint venture partners. Future orientation should fundamentally influence premium negotiations, because a main challenge of acquisitions is the significant time needed to generate benefits for the combined firm (Capron, 1999; Zollo & Singh, 2004). Thus, the firms involved are faced with a tradeoff between immediate payoff and delayed gratification. The acquirer needs to decide what it is willing to pay at the moment of the transaction to obtain potential future payoffs. If a country scores low on future orientation, acquirers in that country should not be willing to pay a high premium, as they are less willing to make greater immediate concessions for future gains. However, if a country scores high on future orientation, then its acquirers will be more willing to offer greater acquisition premiums in order to obtain potential benefits/gains in the future. Similarly, the target needs to assess whether it prefers immediate payment over future gains. If future orientation is high, the target will be less willing to accept a low price/premium as immediate payment for the firm in exchange for future payoffs. If, however, future orientation is low, the target will be more willing to agree on a low sales price in order to capture immediate rewards rather than potential long-term gains. Hence:

Hypothesis 2b: The level of future orientation in the country positively relates to the premium offered in acquisitions.

We further study the dimension in-group collectivism, which refers to “the degree to which individuals express pride, loyalty, and cohesiveness in their organizations or families” (House et al., 2004: 30). Extant work has frequently used the dimension to explain a wide range of phenomena that are rooted in the concern for the well-being and outcome of groups (Triandis, 1995). For instance, Bullough, Renko, and Abdelzaher (2017) build on institutional theory to show that in-group collectivism positively relates to social entrepreneurship, because the value of the enterprise is group-oriented. By contrast, Nam et al. (2014) show that in-group collectivism negatively affects firm innovation, as collectivists are more concerned with traditional normative restrictions, which hamper individual efforts in searching for nontraditional solutions. Since acquisitions essentially comprise the merger of two groups, and the ability to skillfully merge them constitutes a key challenge in acquisitions, we expect in-group collectivism to impact acquisition premiums for two main reasons. First, in-group collectivism positively relates to the pride individuals express in their own group—that is, family, colleagues, and friends, among others (House et al., 2004). Thus, target management may view its organization more favorably in collectivistic countries and expect to be paid a greater premium. At the same time, the acquirer is more confident that it can extract synergy from the target and is, thus, willing to offer a greater price. Second, target firm employees that undergo postacquisition integration tend to experience great psychological strain, including uncertainty over their employment (Buono & Bowditch, 2003). Thus, target management will be less willing to subject their firm and its members to such strain, unless the price is sufficiently high, while the acquirer will be aware of this inclination. Given the greater concern for group members in societies that greatly value in-group collectivism, greater collectivism should result in greater bid premiums. Therefore, we propose:

Hypothesis 2c: The level of in-group collectivism in the country positively relates to the premium offered in acquisitions.

The Regulatory Pillar and Acquisition Premiums

The regulatory pillar stresses the rule-setting, monitoring, and sanctioning activities of institutions (Scott, 2008). Regulative processes thus involve the establishment of rules and laws, inspection or reviewing of conformity to them by societal members, and if necessary, the sanctioning/rewarding of societal members to influence their behavior in the future (DiMaggio & Powell, 1983). Economists, in particular, have paid great attention to the explicit rules and referees of regulative institutions that constrain and regularize behaviors in markets and other competitive situations involving individuals and organizations that pursue their self-interests and behave in instrumental and expedient ways (Scott, 2008). Regulative institutions help to preserve a stable order in such settings. Force, fear, and expedience are critical ingredients of the regulative pillar of institutional theory, which predicts actors in a society behave in expedient ways. Specifically, they calculate rewards and risks—from other individuals, organizations, or the state—before making decisions (Scott, 2008). Thus, the regulative perspective views rules and laws by governments and regulatory bodies as legitimate means to exert institutional pressures through coercive mechanisms (Scott, 2008; Shi & Connelly, 2018).

Consistent with the notion of rule setting of the regulatory institutional pillar, we investigate country disclosure requirements, which refer to the legal obligation of firms to release information that can influence investor decisions (Fernandes, Lel, & Miller, 2010). Such disclosure requirements may include information on a firm’s transactions, contracts, management, and ownership (La Porta, Lopez-de-Silanes, & Shleifer, 2006). Disclosure rules are directly linked to information asymmetries, which are one of the key challenges inherent to acquisitions in general and the premium decision in particular (Baker et al., 2012). Previous research has often examined the impact of country disclosure requirements on different outcomes. For instance, prior work finds that investors value disclosure requirements, as mandatory disclosure encourages managers to focus more narrowly on maximizing shareholder value (Greenstone, Oyer, & Vissing-Jorgensen, 2006). Extant research also shows that greater disclosure is associated with better acquisition decisions and outcomes, due to the disciplinary role of these rules, particularly when monitoring by outside capital providers is more difficult and costly (Chen, 2019; Shalev, 2009). Furthermore, Buch and DeLong (2004) argue that banks in countries with a higher degree of disclosure requirements make more attractive acquisition targets, since acquirers can better assess the soundness of these banks.

Country disclosure requirements reduce information asymmetry and help mitigate the firms’ lack of information. As such, firms have access to a greater amount of more reliable information on other organizations (Greenstone et al., 2006). In the context of acquisitions, investors have high demand for balance sheet information, since acquisitions significantly influence the future operating activities and earnings of the firms involved (Chen, DeFond, & Park, 2002). Balance sheet disclosure in this setting helps investors assess the impact of the merger and acquisition on future earnings. Thus, greater disclosure requirements imply that acquirers have greater confidence in their assessment of the gains from an acquisition, because they have more information about the target firm and are able to reliably assess target capabilities, processes, and synergy potential (Officer, 2003). As a result, acquirers in countries with stronger disclosure requirements should be more willing to pay a greater premium compared to acquirers in countries with weaker disclosure requirements. Similarly, targets are aware of the willingness of acquirers to pay more and they will demand a greater premium. Hence, we hypothesize:

Hypothesis 3: The level of disclosure requirements in the country positively relates to the premium offered in acquisitions.

Method

Data

We collected a sample of domestic acquisitions—that is, acquisitions involving acquirers and targets from the same country—from the SDC Platinum database provided by Refinitiv. In total, we obtained 21,304 acquisition premium observations from 34 countries between 1991 and 2017 with deal values greater than US$1 million for whom we were able to match the dependent, independent, and control variables (Bertrand, Betschinger, & Settles, 2016; Malhotra, Zhu, & Reus, 2015). The mean deal value is US$693 million. We excluded cross-border acquisitions involving target and acquirer firms from different home countries, as the firms involved in these negotiations are embedded in two different national institutional environments, whose influences can override and distort one another. Thus, our sample captures domestic acquisitions in which both acquirer and target are from the same country, in a cross-country study. Table 1 reports the distribution of the observations by country and year.

Descriptive Statistics by Country and Year, 1991 to 2017

Dependent Variables

Acquisition premium

We calculate the dependent variable acquisition premium as the ratio of the initial offer price to the target closing stock price 4 weeks prior to the original announcement date (Kim, Haleblian, & Finkelstein, 2011; Zhu, 2013). Specifically, acquisition premium is the differential between acquirer’s bid and the target’s preannouncement market value divided by the target’s preannouncement market value. We employ a 4-week window, as information on the acquisition may have leaked prior to the official announcement and distorted the target firm’s stock price, in line with prior work (Beckman & Haunschild, 2002; Hayward & Hambrick, 1997). We also used alternative time windows that we discuss in the sensitivity tests. Moreover, we follow extant studies to remove outliers and eliminate the largest and smallest 2% of bids (Dinc & Erel, 2013). We obtain very similar results through winsorizing. The 4-week acquisition premium has a mean value of 22.4 (percent) and a standard deviation of 33.7.

Independent Variables

Prior premium decisions

To measure prior premium decisions that constitute the basis for mimetic behavior of focal firms, we calculate the mean value of the past domestic premiums offered for targets in the same industry and same country (based on two-digit SIC codes). This variable captures the average premium offered in an industry prior to a focal acquisition offer and, thus, should reflect the level of premium that is expected by industry participants and considered taken-for-granted and acceptable (DiMaggio & Powell, 1983). In line with the calculation of premiums, we removed the highest and lowest 2% of premium offers (Dinc & Erel, 2013). We included all prior premiums offered since January 1, 1990 up to a focal premium, as SDC Platinum has begun to more comprehensively collect M&A data then and because behaviors take a long time to become institutionalized (Phillips et al., 2004; Scott, 2008). However, we also employed alternative rolling time windows of 5 and 10 years to examine the robustness of our results, and we employed one- and three-digit SIC codes to account for alternative specifications of industries. The results are robust.

Variation of prior premiums

We calculate the variation of prior premiums through the standard deviation of the premiums that were offered prior to a focal premium within the same industry and same country. We again used two-digit SIC codes to classify industries. Using one-digit and three-digit SIC codes yields very similar results. While we used all premiums offered in an industry and country prior to a focal bid, as prior behaviors typically become taken-for-granted over a lengthy period of time (Lawrence et al., 2001), we also used alternative rolling time windows of 5 and 10 years, and we obtained robust results.

Uncertainty avoidance

We obtain cultural values scores for uncertainty avoidance from the Global Leadership and Organizational Behavior research (GLOBE) project (House et al., 2004). GLOBE identifies nine cultural dimensions (House et al., 2004). The uncertainty avoidance dimension has been widely used in previous research (Venaik & Brewer, 2010). Countries that score high on the uncertainty avoidance dimension tend to keep meticulous records and rely on formalized policies and procedures; by contrast, countries that score low on the uncertainty avoidance dimension keep fewer records and tend to rely on informal norms rather than formal rules (House et al., 2004). The mean uncertainty avoidance values score in our sample is 4.25, and the standard deviation is 0.39. We do not use cultural values scores from other sources, such as Hofstede (2001), as GLOBE collected data during a timespan that overlaps with our study period. Furthermore, GLOBE’s uncertainty avoidance dimension refers to rule orientation and the establishment of behaviors that reduce ambiguity, which closely aligns with our arguments, while Hofstede’s dimension captures stress and employment instability in work settings (Venaik & Brewer, 2010). In addition, we used the GLOBE project’s “should be” scores that capture cultural values, instead of its “as is” scores that measure cultural practices, because the aspirations of the firms likely determine their willingness to offer or accept a given deal premium.

Future orientation

For the cultural dimension future orientation, we again collected cultural values data from the GLOBE study (House et al., 2004). The data were collected by the GLOBE team through the same methodology that we previously described for the uncertainty avoidance dimension (House & Hanges, 2004) and have also been widely used in extant research (Venaik, Zhu, & Brewer, 2013). Countries that value future orientation show the propensity to save and invest for the future and perceive material success and spiritual fulfillment as an integrated whole; by contrast, countries that score low on the future orientation dimension tend to spend now, rather than save/invest for the future and tend to view material success and spiritual fulfillment as separate elements, whose achievements require a tradeoff (House et al., 2004). We matched the data with the countries in our sample. The mean future orientation value for our sample is 5.43. The standard deviation is 0.22. We again chose GLOBE’s cultural values scores over other cultural sources, due to the former’s theoretical underpinning and data collection methodology. Moreover, while, for example, Hofstede’s long-term orientation captures the tradition aspect of societies, GLOBE’s future orientation dimension captures preferences for planning that closely aligns with our arguments.

In-group collectivism

We also obtained cultural values data from the GLOBE study for the cultural dimension in-group collectivism (House et al., 2004). People in countries that value in-group collectivism make a strong distinction between in-groups and out-groups and emphasize relatedness with their own groups; by contrast, people in countries that score low on in-group collectivism are more inclined to make little distinction between in-groups and out-groups and emphasize rationality in behavior (House et al., 2004). The mean future orientation value for our sample is 5.67. The standard deviation is 0.205. We used GLOBE’s in-group collectivism dimension, because Hofstede’s individualism-collectivism dimension measures self-orientation versus work-orientation (Brewer & Venaik, 2011) while GLOBE’s institutional collectivism dimension captures economic systems that underscore collective interests (Bullough et al., 2017) and are thus less aligned with our theoretical arguments.

Disclosure requirements

A country’s disclosure requirements refer to the legal obligation of a firm to release, in a timely manner, all information about the firm that may influence an investor’s decision (Fernandes et al., 2010; Huddart, Hughes, & Brunnermeier, 1999). We obtained data for a country’s disclosure requirements from La Porta et al. (2006). La Porta et al. (2006) approached one attorney from each of the 49 countries in their sample and asked them to respond to a questionnaire that describes the securities laws that are applicable to an offering of shares listed in the respective country’s largest stock exchange (La Porta et al., 2006). La Porta et al. (2006) collected data on six disclosure requirements—that is, (1) prospectus, (2) compensation, (3) shareholders, (4) inside ownership, (5) contracts irregular, and (6) transactions—and calculated their arithmetic mean to obtain the total score for the country’s disclosure requirements. Of the 49 countries included in their sample, the countries with the highest disclosure requirements are Singapore and the United States, while the countries with the lowest disclosure requirements are Ecuador and Uruguay.

Control Variables

Based on a comprehensive review of extant work on acquisition premiums, we included several control variables to rule out potentially confounding factors that can affect acquisition premiums. We first include the country’s political constraint that assesses the political risk of a country, since prior work shows that political risks can dampen the expected gains from a focal acquisition (Lee, 2018). As a result, political risks can lower the bargaining power of the target vis-à-vis the acquirer and result in smaller premiums (Lee, 2018). We measured political constraint through a veto point index offered by Henisz (2000). Henisz (2000) identified the number of independent branches of government in a given country that have veto power over policy change and then, building on the assumption that the policy preferences of these branches are independently and identically distributed across a uniform policy space, calculated the feasibility of policy change. That is, where only one branch of government holds all power, political constraint is very low, whereas where power is distributed widely, political constraint is very high. We also include the country’s market capitalization over GDP and GDP growth rate, which are proxies for the country’s financial market and economic development, respectively (Li, Arikan, Shenkar, & Arikan, 2020). We collected data on both measures from World Bank’s World Development Indicators (WDI).

We include the acquirer’s prior experience, as previous work suggests that prior acquisition experience may help prevent bidders from overpaying (Kim et al., 2011). We use the number of bids the acquirer has made during the 5 years prior to the focal bid as a measure of the acquirer’s prior experience (Barkema & Schijven, 2008; Haleblian & Finkelstein, 1999; Sears & Hoetker, 2014). Data on prior acquisitions are collected from SDC Platinum. We also include dummies that indicate whether the acquirer is a public company and whether it is a financial acquirer, since these bids may have different underlying motivations and lead to different bargaining rationales (Hope, Thomas, & Vyas, 2011; Malhotra et al., 2015). For example, while targets have greater access to information on public acquirers and may use it in their negotiation, bids made by financial acquirers are more likely motivated solely by investment purposes. We also add two variables that count the number of the acquirer and target financial advisors, respectively, as advisors can prevent the acquirer (or the target) from overpaying (or underselling) (Cho et al., 2016; Zhu, 2013). We obtained data from SDC Platinum. We include the target revenue and its return on assets (ROA), which are measures of its financial size and performance and thus can be used as a bargaining chip in price negotiations (Kim et al., 2011). Data were from Datastream.

We also add the last premium offered by a bidder in the same country and industry. Prior research has shown that firms use the preceding premium as anchoring heuristics in their decision-making, so that the higher the last premium is the greater a focal premium becomes (Malhotra et al., 2015). We further include the variable equity stake that measures the percentage of ownership the bidder offers in the target firm (Chari & Chang, 2009; Connelly et al., 2010). This variable ranges from 0.1% to 100% (Malhotra & Gaur, 2014). Prior research has found that the equity stake sought positively relates with acquisition premium, because target managers may accept lower premiums, if they can retain their positions in the combined organization (Reuer, Tong, & Wu, 2012). We include a dummy for cash offer that takes the value 1, if the payment was offered exclusively in cash, and 0, if the offer included some form of contingent consideration such as stock, securities, or earnouts. Cash payments increase the uncertainty for the acquirer and thus could render them unwilling to offer higher premiums (Coff, 1999; Datta, Iskandar-Datta, & Raman, 2001). We add industry relatedness by comparing the four-digit Standard Industry Classification (SIC) codes of both firms (Malhotra et al., 2015), assigning the variable a value of 1 if the firms share the same four-digit SIC code and 0 otherwise.

We also enter dummies that indicate whether the bid was a tender offer, since tender offers that publicly address all shareholders likely need to include a higher premium to increase their attractiveness (Datta et al., 2001). We further enter the foothold held prior to the offer, which is an indicator of the knowledge the bidder has of the target and thus can be utilized by either negotiation party to improve their leverage (Weitzel & Berns, 2006). We add the deal value and dummy variables that indicate whether the deal was completed and whether the offer was hostile (Malhotra et al., 2015; Zhu, 2013). Larger deals may increase the risks for the bidder and its willingness to offer a greater premium, while completed vis-à-vis incomplete deals may differ in the way the negotiations progressed. Hostile deals likely require a greater premium, since the bidder needs to use the price to overcome the resistance of the incumbent target management. We also include a dummy that indicates whether the deal is a merger of equals and a variable that counts the number of competing bids (Laamanen, 2007). Merger of equals tend to lower premiums, because no real bidding process occurs, whereas competing bids raise the bid premium, as it improves the target firm’s negotiation position, allowing it to accept the highest auction price (Laamanen, 2007). In addition, we enter a dummy that indicates whether the deal was made in the high-tech industry as defined by Loughran and Ritter (2004), as high-tech acquisitions often involve access to valuable proprietary knowledge that demand greater price premiums (Reuer et al., 2012). We collected all these data from SDC Platinum. Finally, we include time and industry dummies to control for year- and industry-specific effects (Gamache, McNamara, Graffin, Kiley, Haleblian, & Devers, 2019; Li, Brodbeck, Shenkar, Ponzi, & Fisch, 2017).

Empirical Model

In order to examine the impact of the explanatory variables on acquisition premium, we employ least squares regression, in line with previous research (e.g., Bertrand et al., 2016; Haunschild, 1994). We use least squares regression, because the distribution of premiums resembles a normal distribution, with a slight skew, that includes negative premiums and very large premiums. Furthermore, we include year and industry dummies, and we use robust standard errors clustered at the country-level (Hope et al., 2011; Li et al., 2017). We do not employ multilevel models due to small intracluster coefficients (ICCs).

Results

Table 2 reports the summary statistics and correlation matrix. Variance inflation factors (VIFs) are less than 5 for all variables in all models. The VIFs suggest multicollinearity is not an issue with this sample (Kennedy, 2008).

Summary Statistics and Correlation Matrix, 1991 to 2017

Note: 21,304 observations. Correlations ≥0.014 or ≤−0.014 are significant at the 0.05 level.

Summary Statistics and Correlation Matrix, 1991 to 2017

Note: 21,304 observations. Correlations ≥0.014 or ≤−0.014 are significant at the 0.05 level.

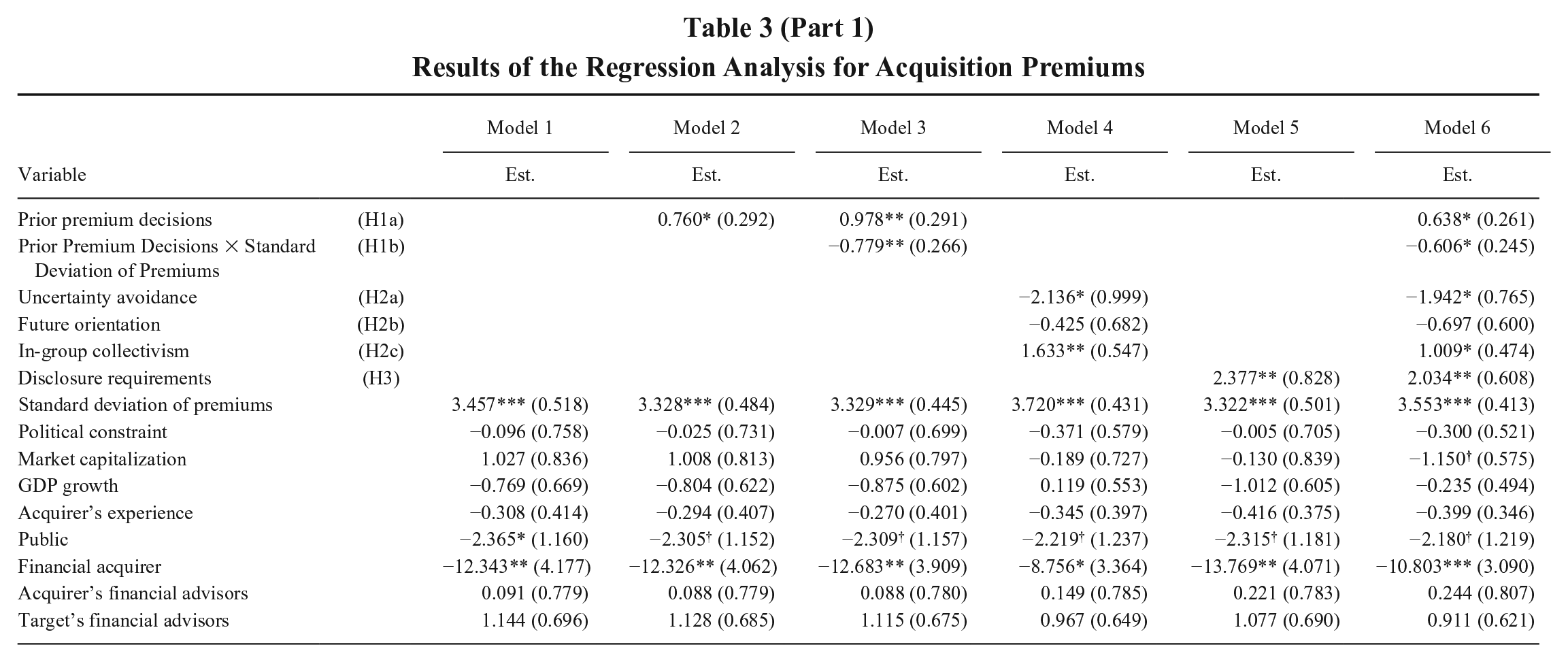

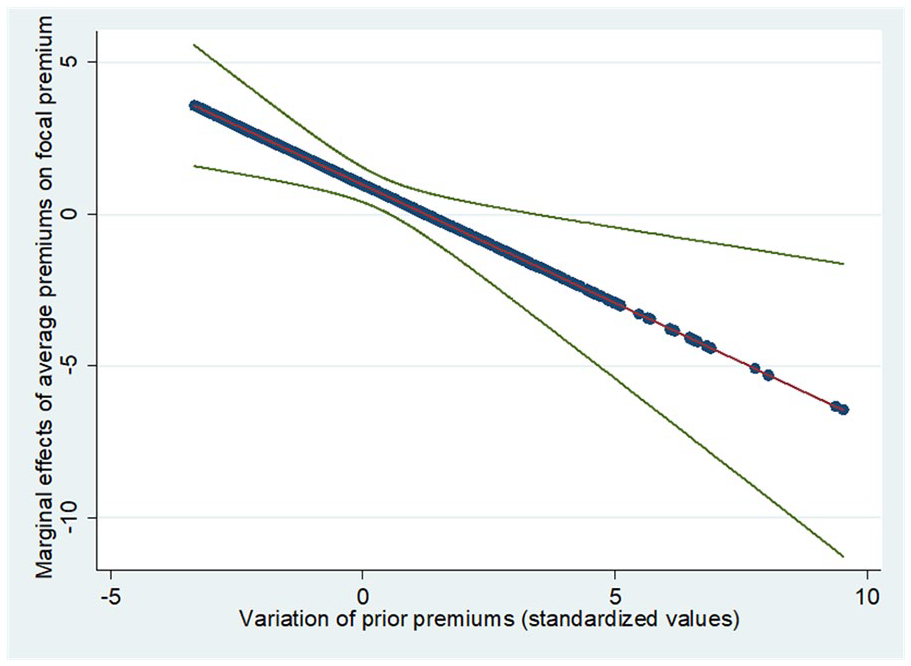

Table 3 reports the regression results for the dependent variable acquisition premium. Model 1 includes only the control variables. In Hypothesis 1a, we propose that prior premium decisions by industry peers in the same country positively relate to the focal acquisition premium. Thus, we enter the variable prior premium decisions in Model 2. In Hypothesis 1b, we hypothesize that the variation of prior premiums negatively moderates the relationship between prior premiums. Accordingly, we add the interaction term between prior premiums and the variation of prior premiums in Model 3. We find that prior premium decisions have a negative influence on acquisition premium (p < .020) in Models 2, 3, and 6 (the full model). Thus, Hypothesis 1a is supported. The coefficient for the interaction term between prior acquisition premiums and variation of prior premiums is negative (p < .019) in Models 3 and 6. Figure 1 shows the marginal effects plot (Meyer, van Witteloostuijn, & Beugelsdijk, 2017). The two outer lines give the 95% confidence range for the interaction line, which shows the marginal effect of prior premiums on premiums. Figure 1 demonstrates that the interaction effect is significant for nearly all values—that is, values smaller than (about) 1.0 and greater than 3.0. Therefore, Hypothesis 1b receives support.

Results of the Regression Analysis for Acquisition Premiums

Results of the Regression Analysis for Acquisition Premiums

Note: †p < 0.10, *p < 0.05, **p < 0.01, ***p < 0.001. Year and industry dummies are included. Robust standard errors are in parentheses.

Marginal Effects Plot for Variation of Prior Premiums

In Hypothesis 2a, we suggest that uncertainty avoidance negatively relates to acquisition premium, while we argue in Hypothesis 2b and 2c that future orientation and in-group collectivism positively relate to acquisition premiums, respectively. We enter the variables uncertainty avoidance, future orientation, and in-group collectivism in Model 4. We find that the coefficients for uncertainty avoidance, future orientation, and in-group collectivism are negative (p < .034), insignificant (p > .1), and positive (p < .041) in Models 4 and 6. Hence, Hypotheses 2a and 2c receive support. Finally, in Hypothesis 3, we postulate that a country’s disclosure requirements positively relate to acquisition premiums, and this variable is included in Model 5. We find that a country’s disclosure requirements have a positive influence on premiums in acquisition (p < .007) in Models 5 and 6. Hence, Hypothesis 3 receives support.

The institutional factors also have an economically meaningful impact on acquisition premium. Everything else being equal, premiums are US$4 million higher for a 1 SD increase in prior premiums paid by other firms in the past. Bidders offer, on average, US$13 million less or US$7 million more for a deal in countries that score 1 SD higher on uncertainty avoidance and in-group collectivism, respectively. Furthermore, bidding firms offer an additional US$14 million, on average, in countries that score 1 SD higher on disclosure requirements.

Sensitivity Tests

We conduct a number of supplementary analyses to assess the robustness of our results. First, we used alternative time periods to calculate the dependent variable, acquisition premium. In particular, we calculate deal premium as the ratio of the initial offer price to the closing stock price one week prior to the announcement date. We did the same for closing stock price one day prior to the announcement date. Our results continue to hold for these alternative specifications of the dependent variable.

Second, we excluded hostile takeover offers, tender offers, and both, as the premium for these types of offers is used to persuade the shareholders and is not necessarily an outcome of the negotiation between acquirer and target firms. While hostile takeover offers are made in the context of target management’s resistance (Schneper & Guillén, 2004), tender offers are made directly to all shareholders, with or without the approval of the target firm’s board (D’mello & Shroff, 2000). In both cases, the nature of the link between negotiation and acquisition premiums may differ. Even with these offers excluded, the results are very similar to those previously reported.

Third, we ran our analyses without premium decisions that were followed by a subsequent price premium change. That is, we excluded bids that resulted in a change between the initial offer price and final offer price. We removed such deals, as the follow-up negotiations that led to a change in price may contain dynamics that systematically differ from premiums that were publicly announced by the participating firms that subsequently remained unchanged. We also ran the analyses only with completed deals, as these deals may contain different underlying mechanisms and negotiations. The results again remain robust after such deals were eliminated.

Finally, we included country fixed effects to account for unobserved country-specific heterogeneities. However, since the cultural values and disclosure requirements scores are time-invariant (House et al., 2004; La Porta et al., 2006), we had to remove the three cultural values variables and the disclosure requirements variable from the model. The results for the time-variant cognitive factor, prior premium decisions, continue to support the original findings and show that both variables positively relate to acquisition premiums.

Discussion

Theoretical Implications

Our study draws on neo-institutional theory to shed light on how bid premiums for domestic acquisitions systematically vary across countries. Previous premium research has employed numerous theoretical frameworks to explain the antecedents of bid premiums in domestic settings, which has generated valuable findings in the process (e.g., Haleblian, Devers, McNamara, Carpenter, & Davison, 2009; Kim et al., 2011; Laamanen, 2007; Zhu, 2013). However, variations in premiums across countries have been largely ignored. Since the effect of national institutions on organizational decisions under uncertainty has been well established (DiMaggio & Powell, 1983; Scott, 2008) and premium decisions are mired in significant uncertainty (Beckman & Haunschild, 2002; Laamanen, 2007), we draw on institutional theory to derive hypotheses on the cognitive, normative, and regulatory nation-level institutional forces that result in systematic cross-country differences in bid premiums. Specifically, our work helps refine our understanding of institutional theory’s cognitive pillar, which exerts mimetic pressures on organizations (Scott, 2008), by helping to calibrate the level of taken-for-grantedness of prior decisions. We show that higher premiums offered for acquisitions in the past within the same industry and country increase focal premiums, and this increase is contingent on the deviation of prior premiums. In particular, the impact of prior premium decisions on focal premiums is stronger the less prior premiums deviate from each other. As a result, our work demonstrates that the legitimacy of a prior decision is reduced when alternatives to these decisions are prevalent. This finding may assist management scholars in examining continuous variables that exert mimetic pressures, as prior work on mimetic influences has predominantly focused on binary decisions, such as market entry (Haveman, 1993; Li et al., 2007; Xia et al., 2008), which are void of more than one alternative. Furthermore, our work complements Malhotra et al.’s (2015) anchoring perspective on premiums. While anchoring builds on the last decision before a focal decision, the institutional rationale suggests that the legitimacy of prior decisions, which develops over a lengthy process, determines focal decisions.

The findings further show that normative institutions influence acquisition premiums. More specifically, we find that greater country-level uncertainty avoidance results in lower bid premiums. This provides support for our argument that in higher uncertainty avoidance societies, bidders are more uncomfortable with the greater uncertainty associated with paying a higher price premium, as there is no guarantee that these investments can be recouped. This finding is noteworthy given that the target firms also seem to be open to lower premiums, even though they should be inherently interested in the largest possible offer price. Our results also show that greater country-level future orientation values do not drive up acquisition premiums. Furthermore, we find that greater in-group collectivism positively relates to bid premiums, which suggests that targets are more willing to accept offers that match their pride and concern for their firm (i.e., in-group) beyond economic factors. Interestingly, bidders in such societies are willing to oblige, as they also have greater confidence and pride that their organizations can extract sufficient synergy to offset the higher price. These findings demonstrate the impact of normative institutional forces on what otherwise can be viewed as rational investment (or buying/selling) decisions, which demonstrate the feasibility of studying these forces in other cost-benefit decisions that traditionally have been examined from value maximization and efficiency perspectives.

We also demonstrate that higher disclosure requirements positively relate to acquisition premiums resulting from regulatory influences. This positive relation suggests that acquirers have greater confidence in their assessment of acquisition gains in countries that have stricter disclosure mandates, as firms have more information on other organizations and their capabilities and potentials in such countries and are thus more willing to offer a greater premium. Our work adds to the growing number of studies that have examined the impact of different elements of the regulatory environment on, in particular, cross-border acquisition premiums, such as differences in investor protection (Bris & Cabolis, 2008), regulations in the banking sector (Palia, 1993), political affinity between acquirer and target countries (Bertrand et al., 2016), and host country corruption (Weitzel & Berns, 2006). Thus, we reveal that additional insights into bid premiums can be generated through the study of specific elements of the regulatory institutional environment.

In so doing, we respond to calls on how to advance research that examines how institutions matter beyond a catch-all concept (e.g., Aguilera & Grøgaard, 2019). In particular, our work untangles institutions by explicitly building on neo-institutionalism and its core premise that asserts organizations strive to be legitimate and conform to taken-for-granted norms (DiMaggio & Powell, 1983; Scott, 2008). In addition, we develop a more systematic and nuanced understanding of how institutions influence firms by systematically assessing the role of the three institutional pillars and by introducing a novel means to capture how variation in taken-for-grantedness moderates the influence of the cognitive dimension on organizational decisions in a country.

Furthermore, our study reinforces the notion that premium decisions are of a subjective and contextual nature as opposed to objective and (fully) rational as executives often claim in order to justify their decisions (Beckman & Haunschild, 2002; Hayward & Hambrick, 1997). Prior work has studied subjective antecedents of acquisition premiums, including social, psychological, and emotional dimensions of the executives and deal-makers involved (e.g., Aktas, De Bodt, Bollaert, & Roll, 2016; Chatterjee & Hambrick, 2011; Jenter & Lewellen, 2015). Our research complements this body of work by contributing an institutional, contextual perspective, which precisely builds on the assumption that organizations are driven by their intention to maintain or increase legitimacy rather than by purely economic efficiency considerations (Scott, 2008). In other words, our work complements emerging behavioral research on acquisition premiums that is based on bounded rationality. Our results confirm and establish that nation-level institutions indeed shape the size of acquisition premiums, even after we account for factors that can impact objective acquisition outcomes.

Lastly, we draw attention to potential institutional influences on other predictors of acquisition premium decisions. Given institutions’ impact on acquisition negotiations, institutional forces may restrict or facilitate how other predictors influence bid premiums, particularly those predictors whose underlying mechanisms are deeply rooted in the negotiation process leading up to the bid. In so doing, our study offers a jump-off platform that helps incorporate institutional theory into other theoretical lenses in future work on acquisition premiums. For instance, extant work suggests that the supply versus demand for a potential target, for example, in the form of the number of bidders, drives up bid premiums, as the target has a greater bargaining hand in these situations (Giliberto & Varaiya, 1989). Yet this relationship is likely weaker in countries characterized by higher levels of uncertainty avoidance, because bidders are less willing to take up the additional uncertainty associated with paying a higher price for the same target firm.

Managerial Implications

This study has managerial implications for acquirer and target managers. In particular, our work reveals how the institutional environment plays a profound role in determining the premium offered in acquisitions. Managers involved in such deals need to be aware that their institutional environment can drive up (or down) premiums. Acquiring managers should understand that they may use institutional pressures—for example, prior premium decisions by other firms—to lay out arguments that help them negotiate deals and constrain bid premiums. Target managers can use the same strategy to demand higher premiums. It is particularly important for managers to be aware of these implications, as they work in different countries in which institutional environments often vary and, thus, result in significantly different acquisition premiums.

Limitations and Avenues for Future Research

Our work also has limitations that invite interesting avenues for future research. First, we restrict our work to cross-country comparative analyses of domestic acquisitions in order to analyze the premium negotiation between two firms that are embedded in the same institutional context. We do not examine cross-border acquisitions, because acquirer and target firms are embedded in different nation-level institutional contexts and need to navigate these institutional differences (Meyer, Li, & Schotter, 2020; Meyer, Mudambi, & Narula, 2011). Further, these acquirer and target institutions can cancel, amplify, and interact with each other (van Hoorn & Maseland, 2016). Studying these interactions is beyond the scope of our work. However, we believe that examining how premium decision processes unfold for cross-border acquisitions and other international diversification strategies can prove quite fruitful (Hitt, Tihanyi, Miller, & Connelly, 2006; Li & Reuer, 2021). Thus, we encourage researchers to explore the differentiated impact of institutional profiles on the premiums offered in cross-border acquisitions in the future.

Second, we are not able to observe the underlying mechanisms that connect institutional forces with acquisition premiums due to data limitations. While we have carefully built our theoretical arguments on institutional theory and acquisition premium research, we ultimately can only speculate about the actual mechanisms, in line with prior literature that predominantly has relied on quantitative methods to examine bid premiums (e.g., Bertrand et al., 2016; Kim et al., 2011). Future research can attempt to use qualitative methods to shed light on what happens “behind closed doors” in premium negotiations. Such an approach can be particularly insightful to explore how cognitive pressures affect premium decisions. For example, scholars can explore whether decision-makers raise prior decisions made by other firms in their negotiation, question these prior decisions, and/or look for alternatives that are vastly different from established behaviors.

Third, our research builds on the assumption that nation-level institutions are relatively homogeneous within countries. While this assumption has been commonly made in extant research on institutions, within-country heterogeneities may exist, particularly, but not exclusively, with respect to normative institutions, such as cultural values (Shenkar, 2001; Stallkamp, Pinkham, Schotter, & Buchel, 2018). As a result, we may have overlooked institutional differences within a same country by using a broad-brush, albeit widely accepted, approach. This opening provides opportunities for scholars to use, for example, surveys or more fine-grained archival data to explore how regional, subnational institutional factors can affect acquisition premiums and related outcomes.

Lastly, our work links nation-level institutions with acquisition premiums, which contributes to the existing acquisitions literature that has tended to neglect the institutional environment. In fact, prior work has tended to focus on economics-driven theorizing and single-country research settings while downplaying the national institutional context that likely affects important predeal activities and decisions. For instance, institutional forces may affect the initiation phase of deals, which is subject to factors such as social comparison, cognitive behavioral patterns, and regulatory influences (Welch et al., 2020). Hence, a promising avenue for future research would be to examine the impact of nation-level institutions on the initiation of deals.

Conclusion

Although research has shown that premium decisions are subjective and contextual, this work has not yet explored how nation-level institutional forces affect acquisition premiums. By extending institutional theory to the literature on acquisition premiums, our findings reveal that cognitive, normative, and regulative factors influence bid premiums. Specifically, we find that prior premiums decisions made by other firms, moderated by their deviation from each other, the cultural values uncertainty avoidance and in-group collectivism, and the disclosure requirements in a country, significantly affect the bid premiums offered in acquisition deals. As such, our work reinforces the interesting notion that while premiums are often justified on expectations of objective acquisition outcomes, the underlying premium negotiations are systematically influenced by their institutional contexts. We hope that our study encourages additional research on bid premiums that helps connect institutional perspectives with the acquisition premium literature.