Abstract

Despite the significant increase in interest in sustainable business practices, decisions on switching to more environmentally friendly input materials are understudied. In a conjoint experiment, we presented 267 Finnish manufacturing firms with an opportunity to acquire an alternative, more ecological input material and investigated their willingness to switch to that material. We find that in general, firms are willing to substitute their current principal input with a more ecological alternative under conditions of functional parity. However, such willingness is contingent on the firm’s value creation structures. Specifically, if the products and processes driving the firm’s value creation rely more on tangible materials (high materiality), firms anticipate higher input-switching costs, which leads to inertia and slows the adoption of alternative, environmentally friendlier inputs. However, if a firm’s value creation is driven more by intangible assets, like intellectual property and amortizable development costs, input-switching costs appear lower. Such firms not only find it easier to adopt ecological inputs but may also derive greater benefit from leveraging the positive reputation effects associated with ecological improvements. By exploring how willingness to switch to an alternative input material is constrained by organizational structures, our findings contribute to research on input substitution and theories of external influence, like demand-side research, stakeholder theory, and ecological responsiveness.

Keywords

While the contribution of the manufacturing sector to global GDP has steadily declined, its negative impact on the environment has risen since 2002 (World Bank, 2019). One way in which manufacturing companies can decrease their environmental footprint is by switching to more ecological (e.g., recycled, biodegradable, or carbon-neutral) input materials. Examples of companies looking to substitute their current input materials with more environmentally friendly alternatives include Lego replacing plastics in bricks with plant-based materials (Tabary, 2018), Ikea (n.d.) aiming to reach 100% sustainable wood purchases in 2020 and to use only renewable and recycled materials by 2030, and fashion house Marimekko using wood-based fibers instead of cotton in its recent collection of clothes (Binlot, 2020). We interpret environmental friendliness in terms of a reduced negative impact on the natural world. While we recognize that adopting environmentally friendly inputs could either enhance or reduce the quality of the end product, we presume functional parity in order not to confound the effect of environmental friendliness with changes in quality. In other words, our research design presumes that a change in environmental friendliness does not alter the core functionality and performance of the input.

In spite of the practical relevance of environmental friendliness as a driver of input material substitution decisions, management research has not yet systematically addressed the topic. This is an important gap because the choice of input materials is vital to the sustainability of the end product, as the material determines which natural resources and ecosystems are depleted and influences the carbon and water-usage footprint of products and their production processes (Ljungberg, 2007). We propose that manufacturing firms have a strong incentive to switch to more environmentally friendly input materials. We base this proposition on Bansal and Roth’s (2000) ecological responsiveness framework, according to which firms have intrinsic incentives, like the moral responsibility to do the right thing, as well as extrinsic incentives, rooted in competitiveness and legitimacy, to source environmentally friendly inputs to respond to growing ecological pressure from diverse stakeholders (Berrone, Fosfuri, Gelabert, & Gomez-Mejia, 2013; Demuijnck & Fasterling, 2016; Gond, Kang, & Moon, 2011).

Nevertheless, firms do not simply respond to stakeholder preferences without considering how their response may affect the firm’s ability to create value. Substituting a familiar input with a new one is associated with switching costs and risks (Suh & Kim, 2018) whose magnitudes hinge on structural dependencies that affect how components are interlinked and how they are connected to externally acquired inputs (Kraaijenbrink, Spencer, & Groen, 2010). Such structural dependencies manifest in the product, the production process, and the firm’s entire asset base. We draw on inertia thinking (Rumelt, 1995) to present contingencies that alter the salience of environmental friendliness as a factor considered in input-material-switching decisions.

We suggest that the adoption of environmentally friendly inputs is less likely in firms whose products and processes are highly dependent on tangible materials—which would create what we call product-input and process-inputs dependencies—because perceived switching costs and risks associated with input substitution increase inertia (Hannan & Freeman, 1984; Li, Madhok, Plaschka, & Verma, 2006; Messner, 2002). Moreover, we propose that inertia may be reduced for firms that at the macro level (firm asset base) rely strongly on intangible assets, such as almost-market-ready development projects, intellectual property, and acquired brand value. Such organizations display evidence of market-oriented development and market responsiveness, making them more susceptible to external influence (Cucculelli & Bettinelli, 2015; Lev, 2019). They also derive more value from aligning themselves with stakeholders by leveraging the benefits of being perceived as an ecological firm owing to positive effects on reputation and brand equity (Levinthal & Wu, 2010).

Acknowledging the difficulty of obtaining observational data on rare events, such as input material substitutions, we opted for a conjoint experiment as our empirical strategy. We presented 267 managers of Finnish manufacturing firms who had strategic authority over input choices with six different scenarios and asked them how willing they would be to substitute the primary input of their most important product with an alternative one, given the presented scenario. The scenarios in the experiment varied in terms of the relative environmental friendliness of the alternative input compared with the current material, the cost implications of input switching, the sources of stakeholder pressure, and the types of business risk associated with switching. The same managers also completed a survey about the firm, which generated variables that we use as controls. In addition, we obtained the financial records of all small and medium-sized firms in the Finnish manufacturing sector to create industry-controlled moderators.

Our study adds to the literature in the following ways. Despite research on the make-or-buy and where-to-buy decisions (Leiblein, Reuer, & Dalsace, 2002; Parmigiani, 2007; Suh & Kim, 2018), few studies direct attention to the acquisition of tangible inputs (what to buy; G. George, Schillebeeckx, & Liak, 2015). Our study demonstrates that while environmental friendliness is an appealing attribute, wide-scale adoption requires firms overcome strong inertial tendencies rooted in product-input and process-inputs dependence while firm-intangibles dependence alleviates inertia. We propose that these dependencies on various organizational structures alter the perceived value of environmental opportunities and help explain why organizations would not align decisions with stakeholder preferences even when those preferences are homogenous (Priem, 2007) and those stakeholders have power, urgency, and legitimacy (Mitchell, Agle, & Wood, 1997). Accordingly, studying such dependence can contribute to theories of external influence, such as stakeholder theory (Freeman, 1984; Freeman & McVea, 2001), demand-side research (Priem, 2007; Priem, Wenzel, & Koch, 2018), and theories of ecological responsiveness (Bansal & Roth, 2000). We propose that theories of external influence should consider structural dependencies as foundational to their perspectives on the firm (Freeman, 1984; Freeman & McVea, 2001; Priem, Li, & Carr, 2012).

Input Material Substitution: Theory and Hypotheses

External Influence and Ecological Responsiveness

Theories of external influence, including stakeholder theory and demand-side research, argue that firms respond to external interests to improve their value creation ability. In their seminal article, Bansal and Roth (2000) propose that firms want to mitigate a firm’s impact on the natural environment by aligning their activities with three drivers of ecological responsiveness: competitiveness, legitimation, and environmental responsibility.

Bansal and Roth (2000) understand competitiveness in terms of long-term profitability and competitive advantage. Substantial evidence suggests that engaging in environmentally friendly practices is good for business (Ambec & Lanoie, 2008; Ameer & Othman, 2012; Margolis & Walsh, 2003). Evolving stakeholder preferences are making the business case for ecological materials and green manufacturing processes increasingly clear, which strengthens their role as sources of competitive advantage (Landrum, 2018; Landrum & Ohsowski, 2018). For instance, ecological actions influence the investment recommendations of financial analysts (Ioannou & Serafeim, 2015), and investor decisions are increasingly influenced by climate risk, sustainability metrics, and sustainable sourcing (Fink, 2020). Accordingly, a firm scoring well on sustainability scorecards might find it can access capital at favorable rates. Environmental aspects are also being used as criteria in the majority of public-sector calls to tender such that ecological responsiveness may broaden market access (Brammer & Walker, 2011; Lindgreen, Swaen, Maon, Walker, & Brammer, 2009; Nissinen, Parikka-Alhola, & Rita, 2009). In addition, more sustainable firms find it easier to hire employees and experience lower rates of employee turnover (Lamm, Tosti-Kharas, & King, 2015; S. Lee & Ha-Brookshire, 2017).

Perhaps most importantly for competitiveness, consumers increasingly care about how products are made and what they contain (McWilliams & Siegel, 2001; Siegel, 2009). This trend affects not only consumer-facing organizations because “even pure business-to-business firms must ultimately contribute to some consumer benefit” (Priem, 2007: 222). Even if the benefits derived from environmental friendliness were purely symbolic or emotive—not affecting the product’s price or quality—they could still influence the subjective value consumers derive from the ownership and/or use of a product (Bowman & Ambrosini, 2000). Hence, improving environmental friendliness can increase downstream demand and willingness to pay for products (Kim & Mauborgne, 2014; Miltton, 2017; Priem, 2007) and can generate reputational rewards that enable differentiation from competitors (Deephouse & Suchman, 2008; Philippe & Durand, 2011). In addition, ecologically responsive firms can find opportunities for new value creation and innovation (Berrone et al., 2013), and develop valuable new capabilities (Sharma & Vredenburg, 1998).

While legislation and industry regulation force firms to make certain environmental decisions (Giunipero, Hooker, & Denslow, 2012; Walsh & Skjoldal, 2011), organizations also proactively adopt ecological business practices in pursuit of legitimation: aligning operations with the set of regulations, norms, values, and beliefs prevalent in the business environment (Bansal & Roth, 2000; Deephouse & Suchman, 2008). Although some firms do so by taking symbolic action to comply nominally with regulations, norms, and stakeholder expectations (Crilly, Zollo, & Hansen, 2012), a more substantive engagement can enable a firm to shape future regulation, avoid fines and penalties, and earn a social license to operate (Berrone et al., 2013; Demuijnck & Fasterling, 2016; Gond et al., 2011).

Environmental responsibility motivations differ from the other two drivers of ecological responsiveness. They are rooted in an internal, intrinsic concern for the social good, while competitiveness and legitimation derive from external influence and acting out of (enlightened) self-interest (Bansal & Roth, 2000). Ethical considerations and doing the right thing outweigh the potential (short-term) profit implications of the action. Prior research offers abundant evidence from business owners and managers prioritizing the pursuit of social and environmental goals (Drumwright, 1994; Fauchart & Gruber, 2011; Muñoz & Dimov, 2015). As the champions of these initiatives derive personal satisfaction from their implementation, the firm is rewarded with improved employee morale as a spillover effect because many employees appreciate being part of an organization that engages in environmentally responsible conduct (Bansal & Roth, 2000). A recent study investigating the cultural attitudes to the natural environment across 78 countries also concludes that “an overwhelming majority of the world’s population supports environmental protection and identifies with the value of ‘looking after the environment’” (Milfont & Schultz, 2016: 194).

These arguments suggest that concerns about competitiveness, legitimacy, and environmental responsibility spur firms to be ecologically responsive. In our context, competitiveness and associated stakeholder concerns are likely to be the most salient driver because competitiveness spurs firms to create greener products (Bansal & Roth, 2000), and greener products require environmentally friendly inputs. Accordingly, the development of green products demands some external influence. Because consumer and other stakeholder preferences are homogeneously aligned in favor of environmental sustainability, switching to an input material that is more environmentally friendly than the current option conforms to stakeholder expectations (Priem et al., 2012). Since alignment with stakeholder preferences is associated with improvements in competitiveness and legitimacy, firms have an incentive to respond accordingly:

Hypothesis 1: Manufacturing firms’ willingness to substitute an existing input for an alternative one will increase in line with the environmental friendliness of the alternative input material.

Reproducing Structures and Switching Inertia

Theories of external influence argue that in order to be successful, firms must align the tangible (e.g., products and processes) and the intangible (e.g., image and knowledge) structures they consistently reproduce with the interests of external actors. However, firms also consider “how new resources are selected and how they are matched with the existing resources in place in the organization” (Kraaijenbrink et al., 2010: 262). Tangible and intangible structures, such as products, processes, and the firm’s asset base, increase switching costs and expectancy value (Suh & Kim, 2018), thereby altering the willingness to respond to external influence. We juxtapose theories of external influence with inertia thinking to outline conditions that affect a firm’s willingness to adopt a more environmentally friendly input material.

The Austrian economist Lachmann (1956) arguably laid the foundations for inertia thinking in management. He explained that the dichotomy between labor and capital in classic economic models, such as the Cobb-Douglas production function, obscured the reality that productive capital is actually a structure of interlinked assets that are never fully fungible. Burns and Stalker (1961) and Stinchcombe (1965) later recognized that organizational structures must imply some form of inertia, following which inertia gained ground as a core construct in population ecology (Hannan & Freeman, 1977, 1984, 1989). Population ecologists identified internal and external factors that could lead to inertia among populations of organizations. Internal sources include specialized assets; information and political constraints; and historical, normative agreements that lead to standardized procedures. External sources comprise factors such as legal and fiscal barriers, legitimacy constraints, and information acquisition costs (Hannan & Freeman, 1984). We are interested in how structures such as product, production process, and the firm’s broader asset base, and their dependence on tangible inputs, affect the decision to replace the current input material with a more environmentally friendly option.

Given the relative lack of research on input substitution, we draw on the literature on supplier switching (Li et al., 2006). This literature suggests that for a buyer, the output of an alternative supplier needs to supersede the value of specialized assets (Riordan & Williamson, 1985), like existing routines, relational rents, and trust developed with the existing supplier (Dyer & Singh, 1998; Gulati, 1995). Moreover, the offering must be sufficiently attractive to overcome general buyer inertia rooted in path dependence and bounded rationality (Rumelt, 1995). This leads Li et al. (2006) to suggest that alternative suppliers ought to develop distinct resource bundles in order to offer products of higher value to possible buyers. While insightful, these explanations focus on changing the buyer–supplier relationship and not on input material substitution, which need not involve a new supplier.

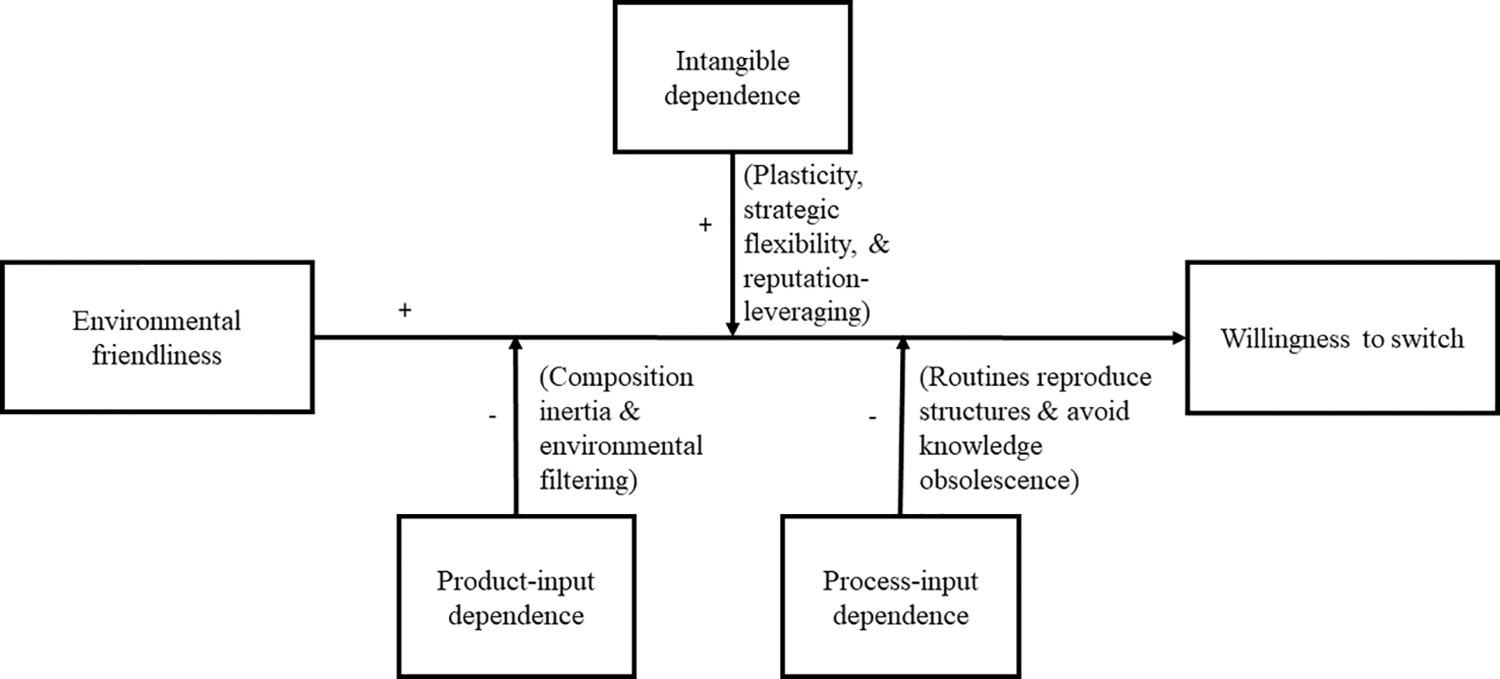

Even when there is no need to switch suppliers, buyers could be influenced by existing structures in ways that could significantly affect the salience of external influence. Our contention is that willingness to switch will be affected by the firm’s resources in place at three complementary levels (Kraaijenbrink et al., 2010). At the micro level, we consider the salience of the input itself in the firm’s product. At the meso level, we look at the salience of input materials in the firm’s productive process. Finally, at the macro level, we investigate the salience of intangible assets in the firm’s asset base. We thus juxtapose the external influence that pushes firms toward change (Bansal & Roth, 2000) with the internal need to consistently reproduce structures, which opposes change (Nelson & Winter, 1982). At the micro and the meso levels, we focus on material structures, which make switching harder, while at the macro level, we take the counter perspective and focus on immaterial structures, which should make switching easier. Figure 1 provides a schematic overview of our hypotheses.

Overview of the Hypothesized Effects

Micro level: Product-input dependence

The Danish company Lego recently announced it would start making some of its famous Lego blocks from polyethylene, a bioplastic derived from sugarcane. While Lego explicitly acknowledged that “plant-based polyethylene has the same properties as conventional polyethylene” (what we call “functional parity”), the company committed to source only 1% to 2% of its plastic needs from sustainable sources (Tabary, 2018). Why would the adoption level be so low despite the environmental friendliness of polyethylene aligning with growing external influence? One explanation is product-input dependence, which captures how important an input is in the use value of a product. For Lego, for instance, significant use value is derived by the satisfactory click sound when connecting two bricks; by the safety of the ABS plastic for children, who will inevitably put the bricks in their mouths; and by the bricks’ durability (Kundu, 2019). When a product’s structure is highly dependent on a specific input material, a firm’s input-switching decisions may be less sensitive to the positive attributes of alternative input materials.

At the micro level, firms are reluctant to change a material composition that they have used successfully in the past (Messner, 2002). This is because historical success creates path dependencies that make adaptation more difficult. Changing a key input used in an important product may also create a need for organizational learning and associated costs, which reduces the benefit to the firm. In addition, path-dependent thinking leads to myopia and the filtering out of environmental information that could affect the salience of ecological attributes in input material decisions (Foerstl, Meinlschmidt, & Busse, 2018). Hence, we propose that firms will consider the trade-off between the anticipated benefits of adopting a more environmentally friendly input and the imagined difficulties and switching costs caused by the transition (Bansal & Roth, 2000; Siegel, 2009). A high level of product-input dependence invokes difficulties and switching costs, which reduce the salience of environmental friendliness in the input-switching decision. We therefore hypothesize the following:

Hypothesis 2: The positive relationship between an alternative input’s environmental friendliness and the firm’s willingness to substitute the original input for the alternative one becomes weaker when product-input dependence increases.

Meso level: Process-inputs dependence

Another possible explanation of Lego’s low adoption level of bio-polyethylene is that switching to bio-based plastics entails potential risks to the production process. A firm like Lego will compare the durability, moldability, supply stability, and other properties of bioplastics with those of the familiar ABS plastic and investigate whether input switching would affect how the production process creates value (Barrett, 2020; Kundu, 2019). Switching to bioplastics may necessitate process changes, like the replacement or retooling of existing machinery and the retraining of employees who may need to acquire new skills to work with the alternative input. These changes disrupt existing process structures and make the firm reluctant to adopt a new material as the firm risks losing specialized investments (Lieberman & Montgomery, 1988).

At the meso level, process-inputs dependence exists because a manufacturing firm’s value creation structure is often optimized to handle specific tangible inputs. The essence of a production process is to deploy routines and practices to repeatedly reproduce structures that consistently add value (Nelson & Winter, 1982). The more material these structures are, that is, the more they rely on tangible inputs, the more complex changing even a single input would be. Any change that alters such an efficiently planned, often highly automated production process may inflate a manager’s inertia because it heightens the risk of the firm not being able to reproduce the well-functioning structures for value creation with a high degree of fidelity (Hannan & Freeman, 1984). Substituting even a single input may result in changes to how the components of the production process are linked together and may require architectural innovation (Henderson & Clark, 1990). This increases complexity and lengthens the change process, thus reducing responsiveness to ecological prompts (Hannan & Freeman, 1984; Pérez-Valls, Céspedes-Lorente, Martínez-del-Río, & Antolín-López, 2019). Because substitution is always imperfect, any input change may make knowledge held within the firm obsolete, as specialized knowledge on how to acquire, handle, or transform the changed input material may no longer be valid. Such knowledge vacuums can create uncertainty on how best to organize production (Lewin, 2012).

Consequently, any change of a key input material can disrupt the firm’s production process structure. Anticipating such disruptions causes inertia, which, in the context of an opportunity to switch to a new input material, is likely to reduce the perceived importance of certain desirable attributes, like environmental friendliness, compared with essential ones, such as moldability in plastics. The greater the role of physical inputs in the firm’s value creation structure, the more complex making any change to the underlying processes becomes (Rumelt, 1995). Inertia thinking stipulates that changing core technology that is essential to the production process happens rarely and is associated with high switching costs and heightened risk of failure (Hannan & Freeman, 1984; Kelly & Amburgey, 1991). Firms will anticipate these risks and consider them in a cost-benefit analysis against the increased environmental friendliness. Therefore, if process-inputs dependence is high, firms are more likely to focus on core business activities (Miller & Friesen, 1983) and less likely to engage in environmental initiatives (Martinez-del-Rio, Antolin-Lopez, & Cespedes-Lorente, 2015). As such, a high level of process-inputs dependence reduces the salience of environmental friendliness in input switching decisions. We hypothesize the following:

Hypothesis 3: The positive relationship between an alternative input’s environmental friendliness and the firm’s willingness to substitute the original input for the alternative one becomes weaker when process-inputs dependence increases.

Macro level: Firm-intangibles dependence

Why does Lego persist in searching for alternatives to ABS plastic? If the product- and process-level structural dependencies overshadow the benefit of environmental friendliness, could there be a counteracting force at play? We surmise that firms with a strong intangible asset base are more likely to align their operations to stakeholder preferences than are firms with a predominantly tangible asset base. Firms with proven development and design capabilities and a strong reputation face higher levels of stakeholder scrutiny, are more capable of responding to stakeholder preferences, and can capture more value by doing so (Barrett, 2019; S. George & McKay, 2018; Kundu, 2019). In short, firms with a sizable intangible asset base capture more value when they are responsive to external influence. Lego’s value creation is arguably mainly driven by its intangible assets: Even though the basic idea of making compatible interlocking pieces that can be reassembled to build different things is easy to copy, no other company offering similar products has achieved the same level of success as Lego. Moreover, Lego has purchased licenses for many popular culture themes, such as Star Wars, Harry Potter, and Minecraft, which indicates investments in a strong intangible asset base that allows the company to remain attuned to its stakeholders’ preferences.

A firm’s existing asset base, tangible or intangible, reflects its historical decisions and is “an exogenous constraint on the ability of a manager to change the organization” (Suddaby, Coraiola, Harvey, & Foster, 2020: 533). While intangibles are becoming increasingly important because of the rising importance of knowledge and the dematerialization of manufacturing activities (Bonfour, 2003), accounting for intangibles remains complex and differs across regions (Cañibano, 2018). In management, intangible assets are all resources that have no immediate physical embodiment. Within the International Accounting Standard (IAS), intangibles are the licenses, patents, goodwill, trademarks, and other intellectual property rights a firm acquired, and the term also encompasses development costs for economically feasible and well-identified projects (Cucculelli & Bettinelli, 2015; Lev, 2019). Intangibles (in IAS) can thus be construed as evidence of successful, market-oriented experimentation (advanced development of well-identified and feasible projects) and market responsiveness (the scanning and execution capability to acquire resources that are valued in the market). Consequently, we propose that firms that depend more on intangibles than their competitors will be more sensitive (higher capability and stronger potential for value capture) to external influence and hence be more interested in environmentally friendly materials. Additionally, firms with more intangibles are presumed to be more confident about the future because they dare to enlist positive future expectations on their balance sheet.

In structural terms, intangibles have a higher level of plasticity—an ability to respond to environmental opportunities (Rumelt, 1995). Firms whose asset base consists of proportionally more intangibles than that of their competitors have a history of successful experimentation and market responsiveness (Lev, 2019) and thus have more malleable structures within which it is easier to integrate distinct material inputs. Relatedly, intangibles are associated with greater strategic flexibility, which enables a firm to better deal with changing customer expectations and environmental changes (Ferreira, Vila, Mariussen, Singh, Oberoi, & Ahuja, 2013). Firms whose intangible assets are derived from advanced and economically feasible projects show evidence of capabilities for market-oriented development. These capabilities enable firms to adapt their products and processes to changes in the external environment (Yi, Knudsen, & Becker, 2016). Moreover, one of the main reasons why manufacturing firms might buy licenses or acquire other firms is to obtain knowledge they do not possess (Vermeulen, 2005). Firms that own such intangible assets thus demonstrate a capability to integrate complex assets in the organization. That capability may also alleviate managers’ concerns about input substitution. The flipside of such capability is that it is likely to increase stakeholders’ expectations that the firm acts accordingly, which further increases the likelihood of a firm responding to external influence.

Another intangible structure to consider is the firm’s reputation or image. Firms with a high brand value can view switching to a more environmentally friendly input as a reputation-enhancing investment. Intangibles such as reputation (even if acquired in factor markets) can be leveraged across a wide spectrum of products and services because they are scale-free structures that can efficiently be applied to an evolving or expanding product portfolio (Levinthal & Wu, 2010). Therefore, even if switching to an environmentally friendly new input material for one product comes at a cost, the firm might find that cost outweighed by the reputational benefits accrued across its product range. In conclusion, firms with a strong reputation and those with strong market-oriented development and market responsiveness—as evident in their intangible asset base—may be more susceptible to external influence. Such firms’ intangible asset base not only makes them more capable of responding to external influence but also increases the likelihood they will be held to account. The preceding arguments support our final hypothesis:

Hypothesis 4: The positive relationship between an alternative input’s environmental friendliness and the firm’s willingness to substitute the original input for the alternative one becomes stronger when firm intangibles dependence increases.

Data and Methods

Our data are derived from a conjoint experiment, a primary survey, and financial statement data obtained from Bureau van Dijk’s Orbis database. The target group was small and medium-sized enterprises (SMEs) in the Finnish manufacturing sector (NACE2 Section C). We identified candidate firms in the Orbis database and followed the European Union SME definition for inclusion, that is, that SMEs have between 10 and 249 employees and either a turnover of between €2 million and €50 million or total assets of between €2 million and €43 million. This Boolean search identified 1,620 eligible firms for which we downloaded financial statement data.

The survey was conducted in collaboration with a professional research agency using a survey instrument designed by the authors. The first and second authors referred to relevant literature when composing the survey instrument in English. It was then translated by the second author into Finnish and checked and translated back by the third author, after which the first author compared both versions. The translations were refined iteratively, and only the second author had access to both versions to ensure consistency and accuracy. After this process, the Finnish version of the survey was professionally edited by the research agency, and three industry experts verified its relevance and understandability.

To identify suitable respondents, all 1,620 firms identified in the Orbis search were contacted by telephone and procurement decision makers were identified. The survey agency ensured that the respondent had the knowledge and autonomy to influence not only the choice of supplier but also what was procured. We reached 568 such decision makers who promised to participate in the survey. A link to a web-based survey instrument was emailed to them immediately, and after three reminders, 267 managers submitted a complete set of responses (response rate: 47%). Typical job titles of the respondents included operations manager, purchasing manager, product manager, R&D manager, production manager, and occasionally, CEO. Finally, we merged the survey data with the financial statement data and grouped the firms into 14 industry clusters based on their NACE2 code.

Using financial data, we controlled for nonresponse bias by comparing measures related to firm size (total assets and number of employees), liquidity (current ratio), and performance (profit margin and return on equity before tax) among the 267 firms that responded to the survey and those remaining 1,353 that were eligible but did not participate (Rogelberg & Stanton, 2007). The differences in the means showed that the firms in our sample are somewhat larger than in the general population, whereas there were no significant differences in the means of the liquidity and performance measures using conventional statistical thresholds (the highest t value for the test of equality of means was t = 1.27, p = .20). An examination of the distribution of the firms across the NACE2 categories does not suggest a systematic bias toward certain industries within the manufacturing sector. Given the modest asymmetry in the sample toward larger SMEs, it is possible that our findings would not hold for smaller entities.

Conjoint Experiment

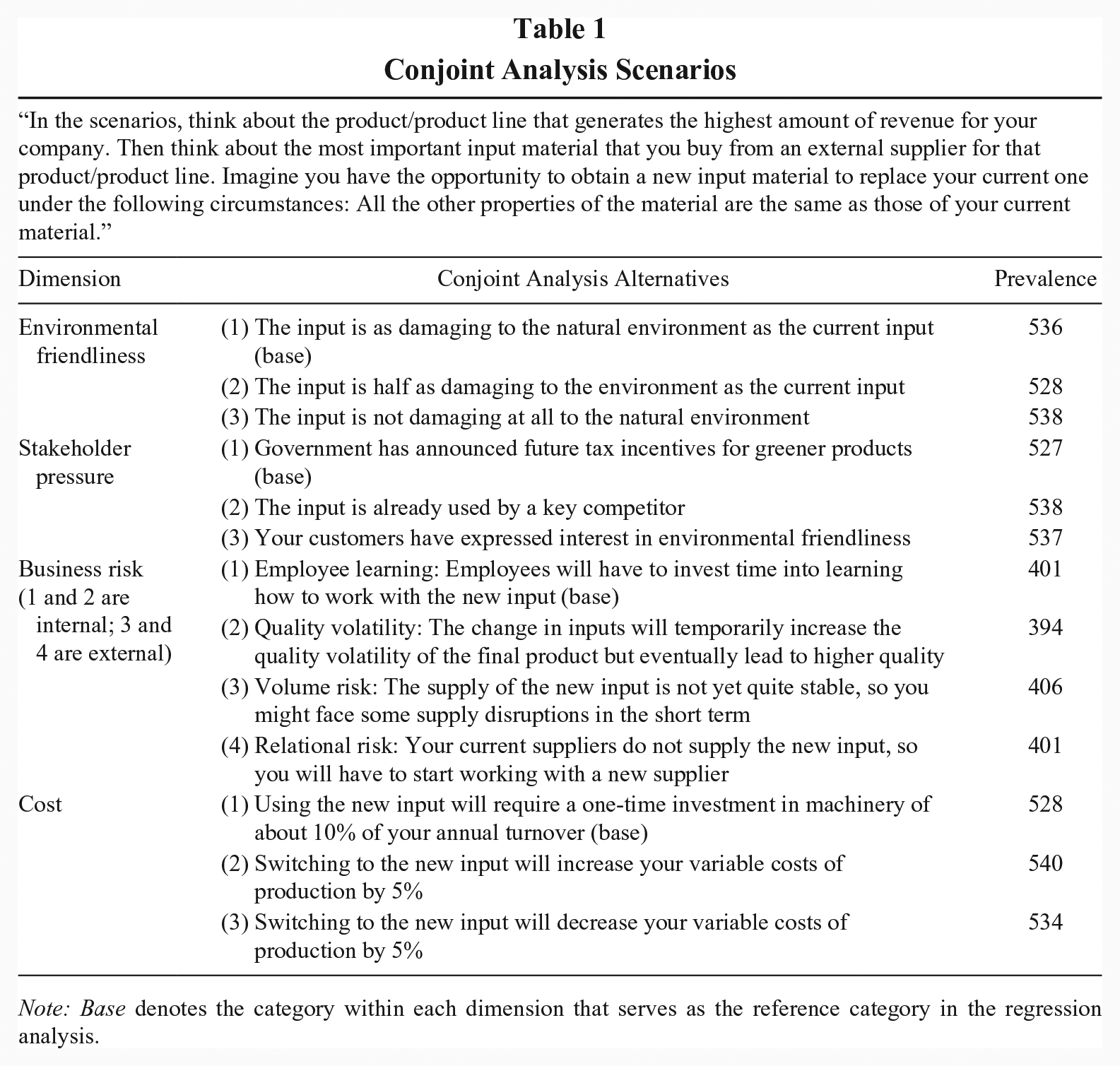

We chose a conjoint experiment as the core component of our empirical strategy because it allows us to study a rare event—such as input material substitution, for which observational data would be very difficult to collect—while being able to manipulate a number of relevant strategic parameters influencing such decisions. Accordingly, the dependent, independent, and key control variables used in this study were derived from the conjoint experiment. Our strategy was to apply a conjoint analysis block design to gauge the relative impact of four distinct dimensions that affect input material substitution (for a similar approach see, Schillebeeckx, Chaturvedi, King, & George, 2016). We presented respondents with six distinct scenarios and asked them to rate their willingness to switch to the new input material described in the scenario. The respondents were instructed the new material would be functionally equivalent to the current one. Specifically, the dependent variable, the likelihood of switching to a new input material, was captured by asking respondents, “How likely are you to purchase this new input at the same price as your current input?” Respondents chose between very unlikely, unlikely, likely, and very likely.

The focal dimension in our design was environmental friendliness, which comprised three items: The new input material is either (a) as damaging to the environment as the current material, (b) half as damaging as the current material, or (c) not at all damaging to the environment. The remaining three dimensions included in the conjoint design were used to contextualize the input material substitution decision. Accordingly, we included competitors, customers, and government as different sources of stakeholder pressure (Achrol, Reve, & Stern, 1983; Meixell & Luoma, 2015; Sarkis, Gonzalez-Torre, & Adenso-Diaz, 2010). In addition, substituting an input material entails various business risks (Falkner & Hiebl, 2015; Helbig, Wietschel, Thorenz, & Tuma, 2016; Srinivasan, Mukherjee, & Gaur, 2011), which we operationalized as four items: the need for employees to invest time to learn to work with the new material, a risk of temporary volatility of quality, a volume risk due to supply disruptions, and the relational risk of having to start working with a new supplier. Finally, we included three different fixed and variable cost implications of using the new input material. The 13 (3 + 3 + 4 + 3) different statements and the exact instructions given to the respondents are presented in Table 1.

Conjoint Analysis Scenarios

Note: Base denotes the category within each dimension that serves as the reference category in the regression analysis.

This design resulted in 108 (3*3*4*3) distinct scenarios that were split into 18 mutually exclusive groups of six, known as a block design (Li et al., 2006). Each respondent was presented with one block of six distinct scenarios. Before seeing the scenarios, the respondents were asked to focus on the most important externally acquired input material for the most important product in their portfolio. They were informed that the scenarios described an alternative input material.

Moderators

Product-input dependence captures how much of the total product cost is driven by the focal input. In the primary survey after the conjoint experiment, respondents selected from five options: 0% to 19%, 20% to 39%, 40% to 59%, 60% to 79%, and 80% to 100% of the total cost. We recoded these options into a continuous 1-to-5 variable and then normalized the variable by withdrawing the mean and dividing by the standard deviation (for each NACE2 category). The normalization serves to facilitate the interpretation of the marginal effects and to make the effects comparable across industries within the manufacturing sector.

Process-input dependence was operationalized in two steps. We first took a firm’s average material costs (MC) over the preceding 5 years and divided this by the firm’s average added value (AV) created over the same period

Firm-intangibles dependence was construed by dividing the firm’s 5-year intangible asset value by the firm’s fixed (tangible + intangible) asset value, averaged over the preceding 5-year period. While the definition of intangible assets in accounting differs from the interpretation of intangible assets in strategic management, research has shown that the accounting value of intangible assets under the IAS is informative in terms of the total value of intangibles (as they are understood in the strategy literature). Notably, the accounting value of intangibles is a strong predictor of a firm’s stock price and thus company valuation (Sahut, Boulerne, & Teulon, 2011). In the absence of market valuation data, as many companies in our sample are private, this measure gives a good indication of overall firm intangibles. 1 We normalized this variable by reducing the fraction with the industry mean (NACE2 level) and divided that by the industry’s standard deviation for the same reason as explained earlier.

Control Variables

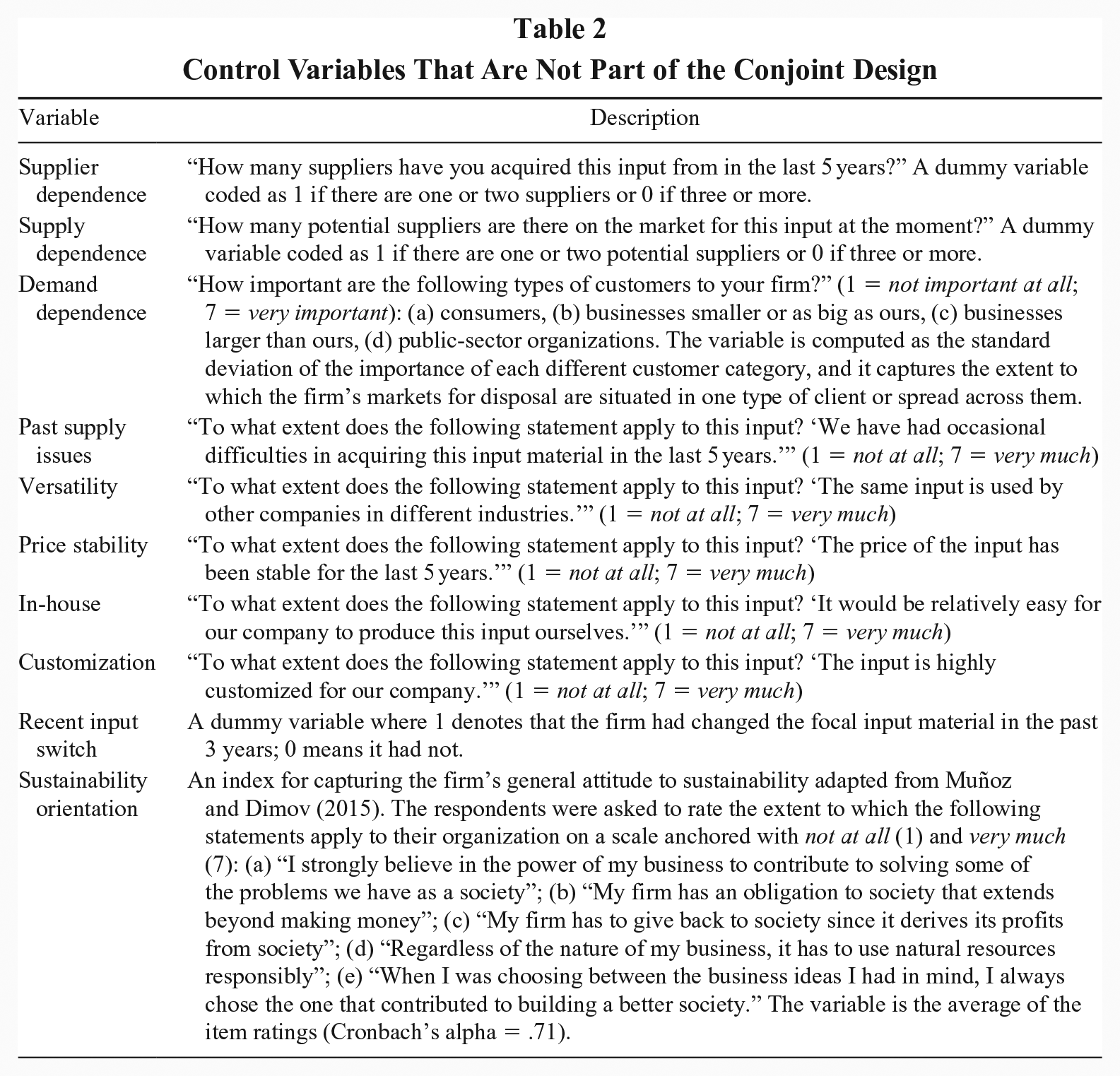

In addition to those variables included in the conjoint experiment (stakeholder pressure, financial implications of switching, and internal and external business risks), our regression models incorporate a number of other controls drawn from the survey that followed the conjoint experiment (see Table 2). All the reported controls are based on answers elicited from the same respondents who took part in the conjoint experiment. First, we control for organizational and relational dependence (recent input switch, supplier, supply, and demand dependence) because we want to separate those types of dependence from our focus on input dependence as a source of inertia and to control for power in the supply chain. We also control for asset specificity by asking respondents how customized the focal input is. Second, we control for sustainability orientation as a proxy for environmental responsibility, which Bansal and Roth (2000) argue could also prompt ecological responsiveness; that argument revolved around firms that abide by a social responsibility logic not conducting a cost-benefit analysis on initiatives targeting sustainability. By controlling for sustainability orientation, we sought to isolate those organizations that would be less susceptible to forms of input dependence. Furthermore, we controlled for recent supply issues, resource versatility, resource price stability, and whether or not the firm could produce the input in-house. The purpose of those controls is to isolate other potential factors that could make a manager more or less likely to switch inputs. Furthermore, we tried a variety of other industry controls, survey design controls, and controls at the respondent level, but none of those changed our results, nor did they generate substantial insights; hence we excluded reporting them to improve parsimony.

Control Variables That Are Not Part of the Conjoint Design

Results

Descriptive Statistics

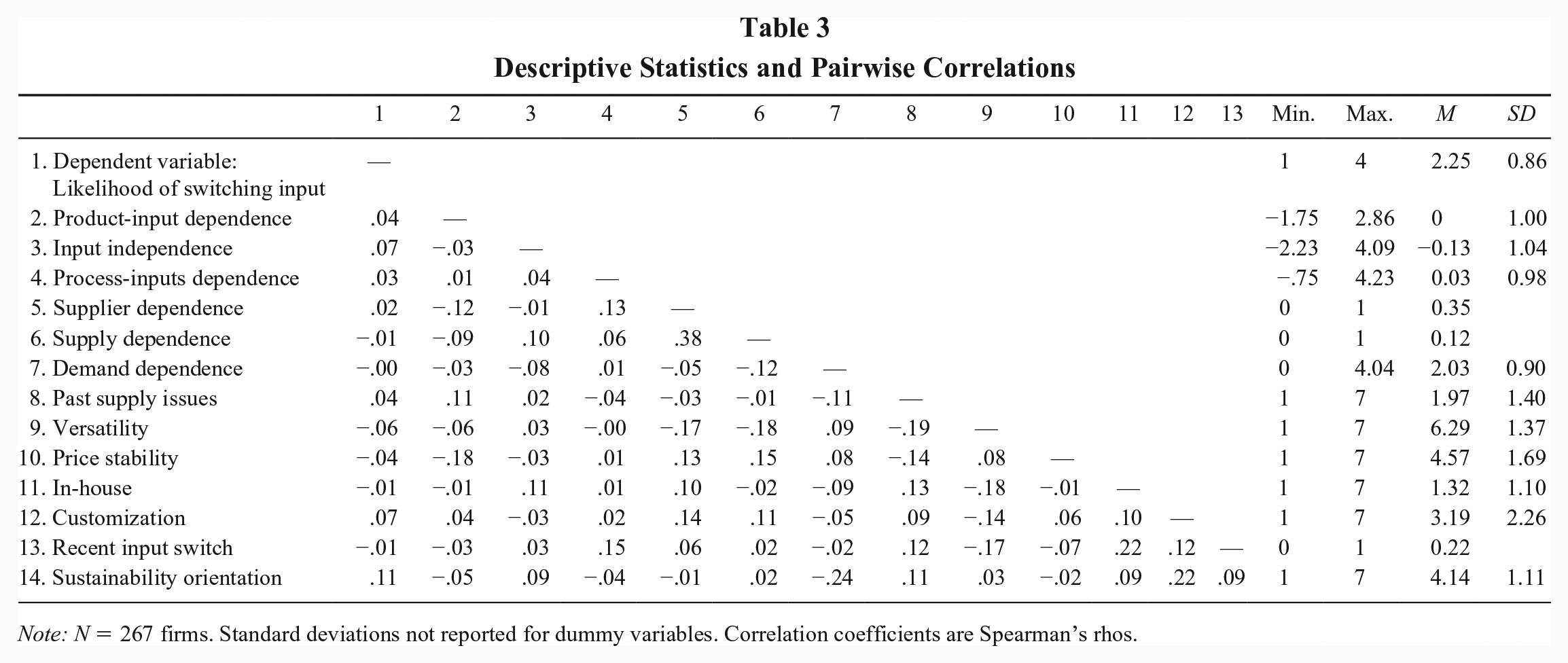

Table 3 provides descriptive statistics and a correlation matrix of all variables that were not part of the conjoint design. Because the dependent variable is ordinal, the correlation matrix reports Spearman’s rank correlation coefficients. The correlations are moderate, suggesting that multicollinearity is not a serious issue in our analysis.

Descriptive Statistics and Pairwise Correlations

Note: N = 267 firms. Standard deviations not reported for dummy variables. Correlation coefficients are Spearman’s rhos.

Unconditional Effects

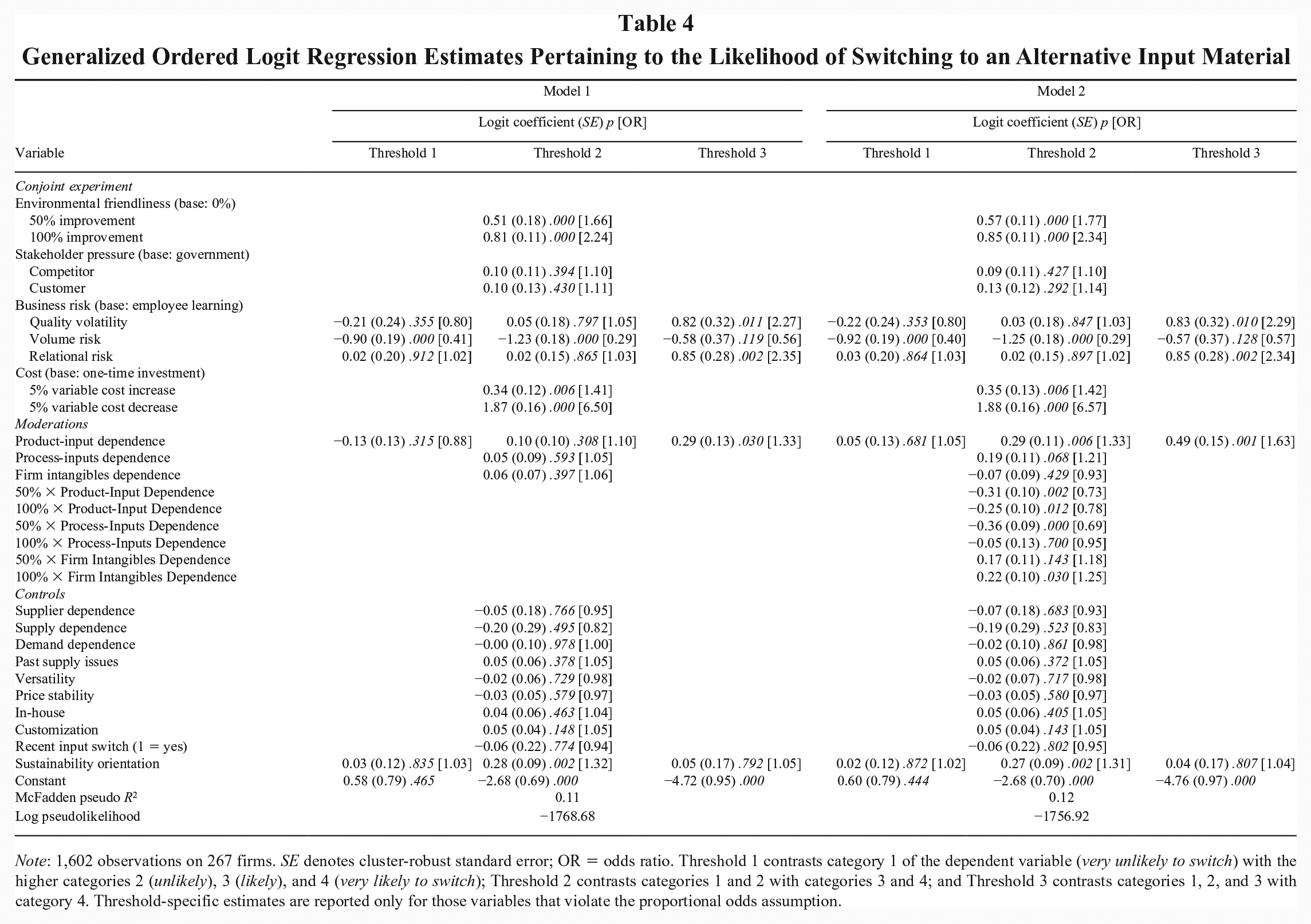

Because the dependent variable comprises four non-normally distributed values, we used ordered logit regression. We estimated cluster-robust standard errors as each respondent rated six scenarios in the conjoint experiment and the within-respondent ratings are not independent of each other. Ordered logit models are based on the proportional odds assumption, which imposes the restriction that all the category probabilities in the dependent variable have different thresholds but share the same regression coefficients. We used the Brant test of parallel regression to establish if this assumption holds in our model. We ran the test separately for model specifications with and without interaction terms. The chi-square test statistics clearly suggest that our model violates the proportional odds assumption (90.71 with 44 degrees of freedom for the model without interaction terms and 104.47 with 56 degrees of freedom for the model including the interactions; both significant at the p < .001 level). A closer inspection revealed that three variables caused the violation: business risk, sustainability orientation, and product-input dependence. In order to allow the regression coefficients for these three variables to vary between the categories of the dependent variable, we estimated a generalized ordered logit model, which imposes the parallel regression restriction on all variables except for the three aforementioned ones, for which the coefficients were estimated separately for each threshold. Note that although the moderating variable product-input dependence violates the parallel regression assumption, the interaction terms involving it do not. Therefore, the parallel regression restriction was applied to the interaction terms.

Table 4 reports the logit coefficients, their cluster-robust standard errors, the p values, and the odds ratios (exponentiated logit coefficients) as effect size measures that are in the metric of the dependent variable. The odds ratio expresses the effect of a one-unit increase or decrease in the predictor on the odds of switching to a new input material. Values above 1 are associated with positive change, while values below 1 indicate a reduction in the odds of switching. For variables that meet the parallel regression criterion, we present only one set of estimates that applies to all three thresholds in the model. For the variables that violated this criterion, we present separate estimates for each threshold. Model 1 in Table 4 presents the results for a model specification that includes the unconditional effects of all variables, whereas the interaction terms for testing the moderation effects are added in Model 2.

Generalized Ordered Logit Regression Estimates Pertaining to the Likelihood of Switching to an Alternative Input Material

Note: 1,602 observations on 267 firms. SE denotes cluster-robust standard error; OR = odds ratio. Threshold 1 contrasts category 1 of the dependent variable (very unlikely to switch) with the higher categories 2 (unlikely), 3 (likely), and 4 (very likely to switch); Threshold 2 contrasts categories 1 and 2 with categories 3 and 4; and Threshold 3 contrasts categories 1, 2, and 3 with category 4. Threshold-specific estimates are reported only for those variables that violate the proportional odds assumption.

Hypothesis 1 suggested a positive relationship between environmental friendliness and willingness to switch to a new input material. Both dummy variables capturing this dimension of the conjoint design are statistically significant at the p < .001 level. Compared with when the new input material is as damaging to the environment as the current material, the odds of switching to a new input material are higher by a factor of 1.66 when the new material is half as damaging to the environment as the current material and by a factor of 2.24 when the new material is not damaging to the environment at all. These results are robust in the face of the addition of respondent fixed effects, a test that addressed potential endogeneity concerns due to omitted variable bias at the respondent level (Kibler et al., 2017). Therefore, we find strong support for Hypothesis 1.

An examination of the other dimensions of the conjoint experiment reveals no differential effect between the different types of stakeholder pressure. This finding does not necessarily mean that stakeholder pressure is irrelevant in absolute terms; it might be that different stakeholder pressures are considered equally important, or alternatively that when considering the available option set captured by the scenario, the source of stakeholder pressure does not feature heavily in the decision-making process.

In terms of the risks, the respondents deemed the volume risk caused by temporary supply problems to be the most problematic, which seems to confirm that respondents were focusing on their firm’s most important input material as requested. Compared with the need for employees to learn new skills (base category), volume risk was a far more pressing concern for our respondents. With odds ratios ranging from 0.29 to 0.56 (depending on the specific threshold in the dependent variable), the firm is clearly less likely to switch to an alternative input material if there is a risk of supply problems. Interestingly, the effect on switching of temporary quality problems or the requirement to start working with a new supplier does not differ from that of the need for employee learning with respect to any other threshold than the highest, where the greatest likelihood of switching is contrasted with the three lower categories. The risk of temporary quality problems and the relational risk of having to switch to a new supplier appear to positively predict a high likelihood of switching. The most plausible interpretation is that decision makers will be more inclined to switch to an alternative input material as long as the firm can avoid requiring significant employee learning or incurring a volume risk. With regard to the three financial conditions in the conjoint experiment, it was clear that the base category of a one-off investment of 10% of annual revenue to adapt equipment was considered a less appealing option than a 5% variable cost increase, while, not surprisingly, a 5% variable cost decrease was a notably more appealing alternative compared with the base category.

In order to further gauge the effect sizes of the different dimensions within the conjoint experiment, we followed Luchman (2014) in using general dominance statistics. Expressed in percentages, they are more straightforward to interpret than odds ratios, whose scaling makes it difficult to gauge the relative importance of positive (odds ratio higher than 1) and negative (odds ratio less than 1) effects. They are also well suited to generalized ordinal regression models because they distill the contribution of a predictor to the dependent variable into a single value in spite of the coefficient (and odds ratio) being estimated separately for each threshold (Luchman, 2014).

We used the Stata routine domin (Luchman, 2015) to estimate the general dominance statistics for the conjoint experiment. Since we already report the odds ratios for the individual variables in Table 4, we opted to compute the dominance statistics for the four dimensions in the conjoint experiment as a whole; that is, we computed one dominance statistic for environmental friendliness, rather than separate statistics for 50% and 100% improvements in environmental friendliness and followed the same procedure with stakeholder pressure, business risk, and cost considerations. The procedure involves estimating separate ordinal logit models for each of the 15 possible combinations of the four dimensions in the conjoint experiment, 2 recording the McFadden pseudo R2 as a measure of model fit, and averaging the marginal contributions to model fit attributable to each dimension.

The general dominance statistic for environmental friendliness is 0.0126; for stakeholder pressure, 0.0008; for business risk, 0.0221; and for cost considerations, 0.0622. These can be converted into percentages to assist interpretation. Accordingly, environmental friendliness explains 1.3% of the recoverable information about the model, or in other words, it brings the model 1.3% closer to perfect prediction given the comparison point of an intercept-only model (Luchman, 2014). The percentages for stakeholder pressure, business risk, and cost considerations are 0.08%, 2.2%, and 6.2%, respectively. This means that managers with procurement responsibility are most likely to consider switching to an alternative input material if it is cheaper than the current one, which supports the validity of the conjoint experiment. They are also more likely to switch if the new input material does not threaten to disrupt supply in the short term. The third most salient criterion for switching is the new input material being more environmentally friendly than the current option.

Interaction Effects

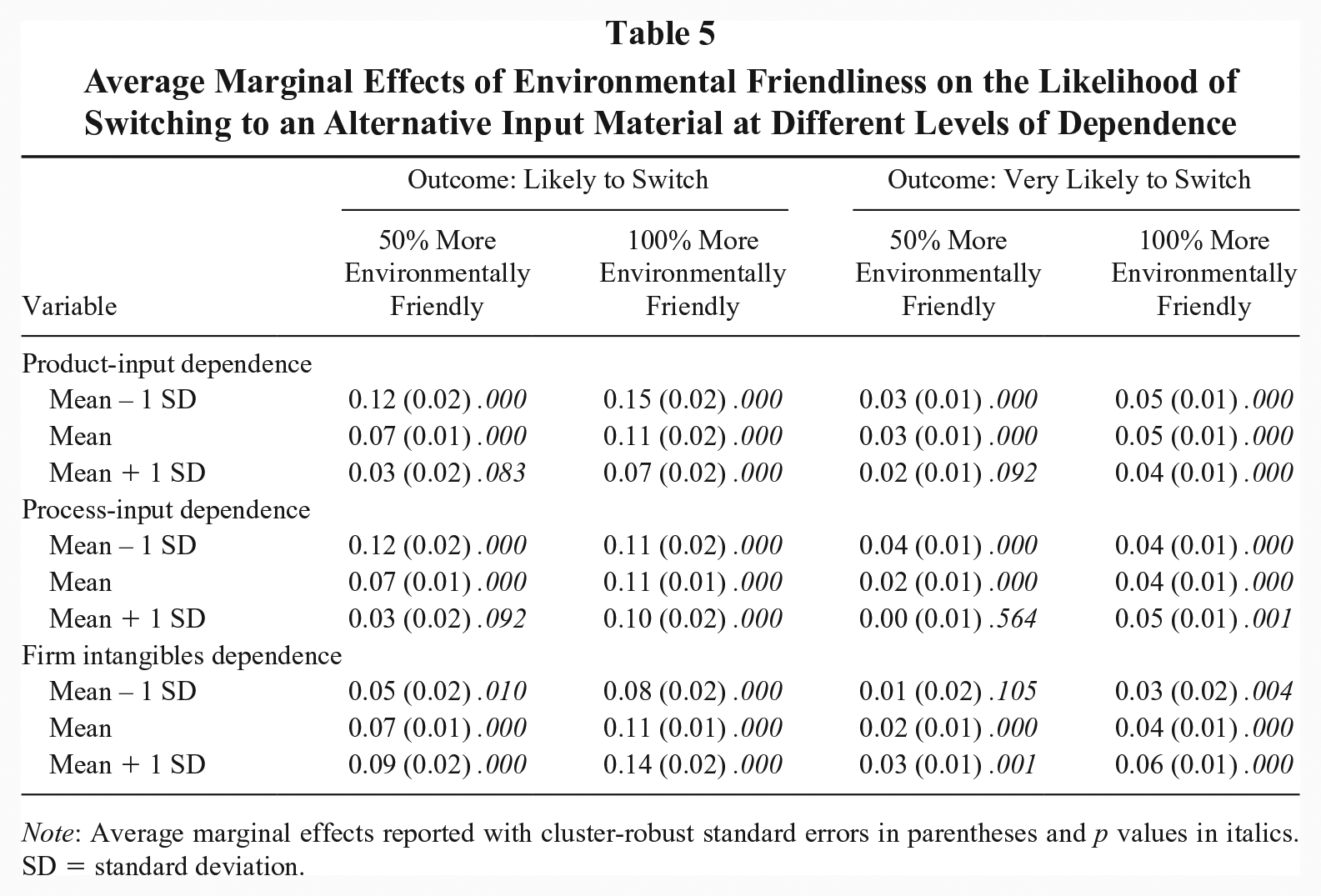

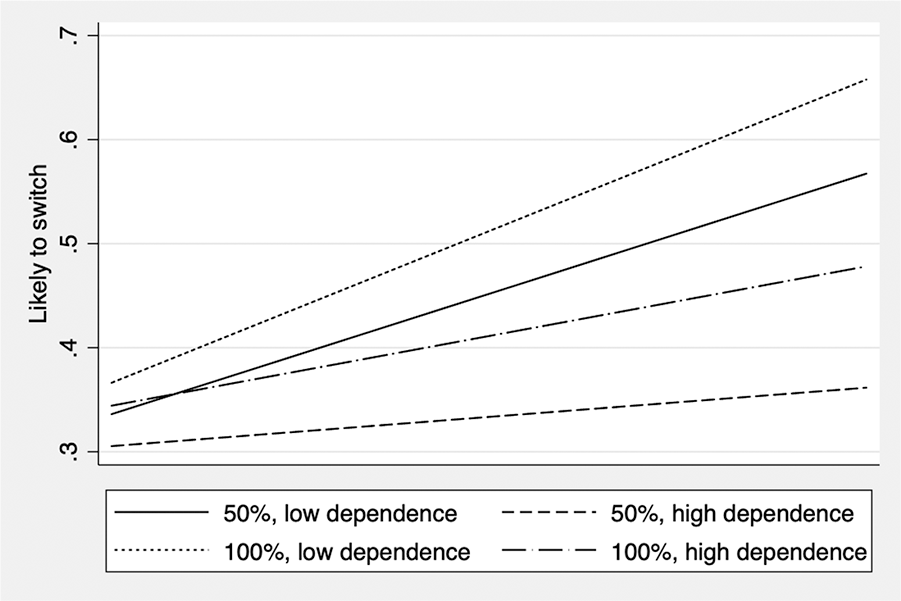

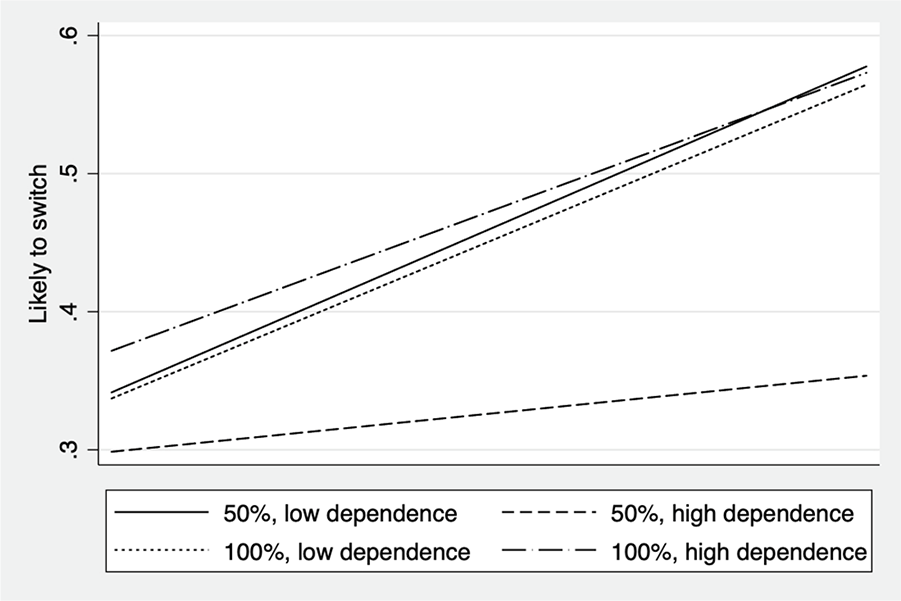

Model 2 in Table 4 adds the interaction terms to the regression equation. The results show significant interaction effects for each moderator with (inverse) odds ratios ranging from 1.05 to 1.45. 3 Therefore, compared with the unconditional effects of the variables constituting the conjoint experiment in Model 1, the effect sizes of the interaction terms are moderate. However, it is not advisable to interpret moderating effects based only on the interaction terms (Brambor, Clark, & Golder, 2006). Consequently, in order to examine Hypotheses 2 through 4, we computed the average marginal effects of environmental friendliness on predicting the transition from a response of unlikely to one of likely and the transition from a response of likely to one of very likely to switch to the alternative input material for different values of the moderating variables. We omit the transition from very unlikely to unlikely because it is not of substantive interest. Table 5 reports the marginal effects of the independent variable when the moderators are set at their means and at one standard deviation unit below and above their means. Figures 2 through 4 provide graphical illustrations of the same effects. To improve the readability of the graphs, we plotted only the transition from unlikely to likely responses.

Average Marginal Effects of Environmental Friendliness on the Likelihood of Switching to an Alternative Input Material at Different Levels of Dependence

Note: Average marginal effects reported with cluster-robust standard errors in parentheses and p values in italics. SD = standard deviation.

Average Marginal Effect of Environmental Friendliness on the Outcome “Likely to Switch” When Product-Input Dependence Varies

Average Marginal Effect of Environmental Friendliness on the Outcome “Likely to Switch” When Process-Input Dependence Varies

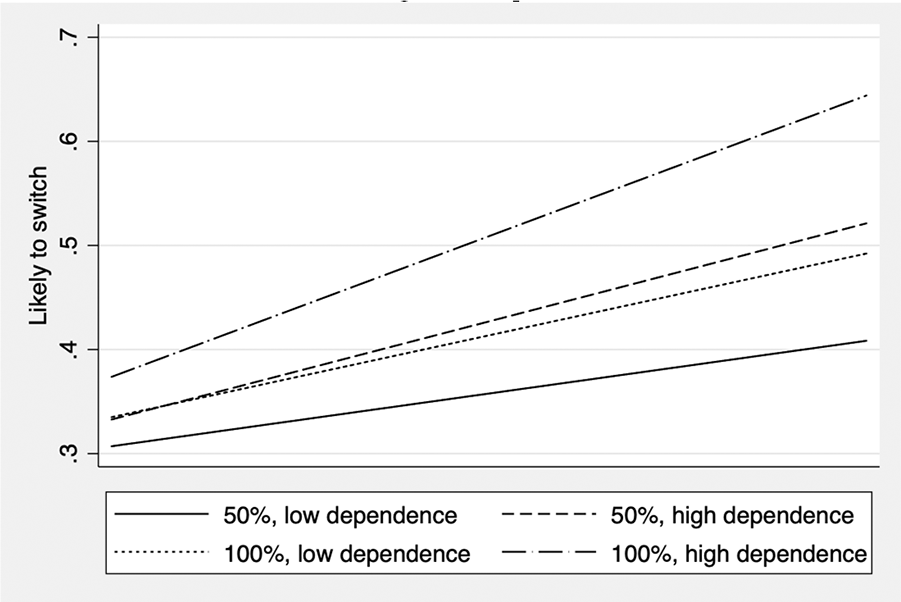

Average Marginal Effect of Environmental Friendliness on the Outcome “Likely to Switch” When Firm Intangibles Dependence Varies

Figure 2 clearly shows that an increase in the value for product-input dependence is associated with a decline of the marginal positive effect of environmental friendliness. This finding supports Hypothesis 2. Figure 3 shows a similar effect for process-inputs dependence when the new input material is half as environmentally damaging as the current one. However, process-input dependence does not reduce the effect of environmental friendliness on the likelihood of switching when the new material is not at all damaging to the environment; thus, a high level of environmental friendliness is resistant to inertia originating from process-inputs dependence. This partially supports Hypothesis 3. In the case of firm intangibles dependence, we see an opposite effect, with an increasingly positive impact of environmental friendliness as firm intangibles dependence is augmented. This supports the argumentation underpinning Hypothesis 4 around intangibles enhancing the salience of external influence and thus boosting the effect of environmental friendliness on the switching decision.

Robustness Checks

We conducted a variety of unreported statistical tests to examine the robustness of our findings. Most importantly, we used an alternative dependent variable for all of the model specifications reported in Table 4. This variable captures the respondent’s willingness to pay for the alternative input material, and it was measured with an additional question posed immediately after that relating to the principal dependent variable (willingness to switch to an alternative input material) in each scenario of the conjoint experiment.

Respondents who answered that they would be (very) unlikely to switch were asked how much cheaper the input would need to be to make them change their mind. Those responding they would be (very) likely to switch were asked how much more expensive the input could be before they were dissuaded from switching. Based on these responses, we constructed a seven-step ordinal variable coded from 0 to 6 in the following order: the respondent is not willing to switch at any price; the input has to be 40%, 30%, 20%, or 10% cheaper for them to consider switching; they would be willing to switch at price parity; and they would be willing to switch even if the input were 10% to 20% more expensive. Replacing willingness to switch in the models in Table 4 with willingness to pay generates substantively similar results. We also created a normalized variable that subtracts the respondent’s average response to the willingness-to-pay question from each response. This allows us to control for a general (un)willingness to switch/pay on the part of the firm and learn whether the same predictors are significant. Again, the results are consistent with those in Table 4.

Moreover, because most prior research focuses on switching suppliers rather than on substituting inputs, we checked whether our findings remained consistent if we looked only at those scenarios requiring a new supplier. While the power of this model is significantly smaller (only 397 observations), we found the same significant effects except for the interaction with firm intangibles dependence. The finding seems to imply that the compounded difficulty of changing both input and supplier lowers the salience of macrolevel firm structures, like the asset base. Interestingly, when we isolate those scenarios in which temporary supply problems occur, none of the interactions are significant. We also see that for those scenarios, the average willingness to switch (pay) is significantly lower. The salience of practical supply stability may be one of the reasons why many firms have started to address environmental and social problems within their existing supply chains (Kogg & Mont, 2012).

Discussion

Despite the growing importance of intangibles, like brands and knowledge (Lev, 2019), the economy still relies on many tangible materials and physical objects that are manufactured from natural resources, and this area has received significantly less managerial research attention (G. George et al., 2015). As concerns about climate change and natural resource depletion have made their way onto corporate agendas, managing natural resources sustainably is increasingly being recognized as a key managerial challenge and a necessary component of achieving sustainable development (G. George, Merrill, & Schillebeeckx, 2020; Schillebeeckx, Workman, & Dean, 2018). While some scholars have adopted a holistic perspective, arguing for a stronger anchoring of economic systems within the natural world and recognizing the need for strong sustainability (Landrum, 2018; Landrum & Ohsowski, 2018; Tashman, 2020), our approach is focused on a specific strategic and practical question most purchasing managers have been asked and will be asked in the future: “Do you want to buy more environmentally friendly inputs?”

Ecological Responsiveness and Input Substitution

While make-or-buy and where-to-buy decisions have been studied before (Jauhar & Pant, 2016; Leiblein et al., 2002; Li et al., 2006; Vahidi, Torabi, & Ramezankhani, 2018; Walker & Weber, 1984), management research has been noticeably silent on the related what-to-buy question. The current study opens up this debate by investigating managerial willingness to substitute an existing input for a more ecological alternative. We anchored our thinking in theories of external influence, such as ecological responsiveness (Bansal & Roth, 2000), stakeholder theory (Freeman, 1984), and demand-side research (Priem, 2007), and hypothesized that when all sources of external influence are aligned, as is the case in our empirical context, managers concerned with their firm’s competitiveness and legitimacy should favor switching to environmentally friendly inputs when the opportunity emerges (Bansal & Roth, 2000).

Our research design depicts an almost ideal scenario, in which respondents were presented with a functionally equivalent alternative input material at price parity. The parameter of interest in those scenarios was the environmental friendliness of the alternative input. Given the condition of functional parity, environmental friendliness can be understood as an extrafunctional attribute—one that does not affect the core function of the input but is nevertheless perceived positively in purchasing decisions. Other examples of extrafunctional attributes include country of origin, labor standards, and the source of the energy used in manufacturing (Balabanis, Diamantopoulos, Mueller, & Melewar, 2001; Canavari, Centonze, Hingley, & Spadoni, 2010; Drumwright, 1994). The demand-side perspective suggests that consumer preferences for such extrafunctional attributes influence not only firms operating at the consumer interface but also upstream firms that anticipate downstream changes in consumer willingness to pay that provide opportunities for additional value creation (Priem et al., 2012, 2018).

Our findings make three important contributions to the seminal work of Bansal and Roth (2000) on ecological responsiveness. First, in their advanced model of corporate ecological responsiveness (Bansal & Roth, 2000: 729), the authors suggested that intrinsically motivated environmental responsibility would prompt firms to donate to and undertake unpublicized environmental initiatives but not to develop greener products. However, we found that sustainability orientation (a proxy for environmental responsibility) increased the likelihood that someone would switch to a more environmentally friendly input, a step toward making greener products. An additional analysis of a subsample of respondents with a strong sustainability orientation (available upon request) shows a stronger effect for environmental friendliness that is also less affected by the moderators. This suggests that respondents who might be described as “true believers” are less easily dissuaded by structural dependencies and make decisions more from a moral vantage point. This finding offers grounds for optimism because it shows that 20 years after the publication of Bansal and Roth’s article, environmentally responsible firms not only are engaging in pro-environmental initiatives that do not require changes to existing business processes (e.g., donations, employee volunteering) but are significantly more likely to make changes in core business processes (such as input switching) to align with their convictions.

Second, Bansal and Roth (2000: 729) proposed that issue salience—the strength and homogeneity of external influence—will be positively associated with legitimation and the competitiveness motivation of the firm, and this could lead to greener products, even in the absence of environmental responsibility. Indeed, a subsample analysis of firms with low sustainability orientation (available upon request) showed that such respondents are still motivated to respond to external influence and engage in input substitution, which adds credence to the instrumentalist cost-benefit trade-off logic presented in our arguments.

Third, our theorization of extrafunctional attributes allows us to extend Bansal and Roth’s (2000) model of ecological responsiveness to a more generic model of responsiveness to external influence. We suggest that our findings are also replicable when the competitiveness and legitimation motivations are anchored not in salient ecological issues, like environmental friendliness, but in social justice issues (e.g., fair wages, or the absence of gender or racial discrimination) or nationalist tendencies (e.g., country of origin). As long as the context of a salient issue (care for the natural world) that aligns with the opportunity (input switching) to achieve an outcome (green products) under conditions of functional parity can be replicated, a generalization of our findings from environmental friendliness to other extrafunctional attributes seems plausible.

Structural Dependencies and Theories of External Influence

Switching decisions do not take place in a vacuum. Firms are constrained by the resources in place (Kraaijenbrink et al., 2010), such that existing organizational structures affect the probability of acting on stakeholder preferences. Theories of external influence on value creation (e.g., Freeman, 1984; Freeman & McVea, 2001) often fail to explain why firms would not respond to external influence when consumer and other stakeholder preferences are aligned and salient. We theorized that it is important to explicitly consider the effects of firm structures—like product, process, and asset base—on how managers evaluate external influence.

To increase the explanatory power of theories of external influence, we contend that their perspective of the firm can be meaningfully rooted in the micro, meso, and macro structures that give rise to inertia. Put differently, the value logic of demand-side and stakeholder theories (Parmar, Freeman, Harrison, Wicks, Purnell, & De Colle, 2010; Priem et al., 2012) and the counteracting forces of inertia anchored in the firm’s existing structures (R. Lee & Neale, 2012; Li et al., 2006; Rumelt, 1995) are inextricably linked. Prior demand-side research and stakeholder theory, however, have mainly focused on the positive implications of stakeholder value creation while downplaying inertia types (Huang, Lai, Lin, & Chen, 2013), inertia of cognitive representations (Tripsas & Gavetti, 2000), structural inertia (Hannan & Freeman, 1984), and even asset-specific investments (Riordan & Williamson, 1985), all of which problematize the very idea that firms ought to respond to external influence. Indeed, our finding that managers require a strong stimulus before breaching the inertia inflection point for input material substitution aligns with findings on inertia associated with strategic learning (Sirén, Hakala, Wincent, & Grichnik, 2017).

In our context of homogenous stakeholder preferences (virtually every stakeholder, ceteris paribus, values environmental friendliness), inertia helps explain why firms would not realign their structures with the interests of external stakeholders. If managers are indeed influenced by existing structures when dealing with external influence, we should consider how that affects preferences to respond to one stakeholder instead of another when their preferences are not aligned. Rather than explicitly focusing on which stakeholder is more powerful, is more legitimate, and/or makes the more urgent demand (Mitchell et al., 1997), managers faced with such decisions may simply choose the path of least structural resistance. An exciting avenue for future research would then be to explore how material structures in particular amplify or silence the voice of specific stakeholders.

Relatedly, a value-centric interpretation of our findings, as advocated by the demand-side perspective (Priem, 2007; Priem et al., 2012), suggests that the same change may reduce value in use (due to product-input dependence) and jeopardize value creation (due to process-inputs dependence) while supporting value capture (owing to firm intangibles dependence). The result of this balancing exercise explains why many firms may not pursue input substitution, even under the optimistic experimental condition of price and function parity applied in our study. Future research could expand the benefit set of the environmentally friendlier alternative, add price reductions or functionality improvements to the decision-making scenarios, and explore whether such changes would alter the moderating effects of the focal structures.

Limitations and Future Research

As is common with survey research, our findings cannot be interpreted as proof of causality. By virtue of asking the same respondent to rate various alternative scenarios, the conjoint experiment did manage to control for many forms of response bias; however, longitudinal panel research or an in-depth historical case study of actual input selection and switching decisions would be needed to verify our findings and mechanisms and to eliminate the possibility that the determinants of planned behavior (e.g., willingness to switch) do not drive actual action (Ajzen, 1991). Replacing environmental friendliness with another extrafunctional attribute, like country of origin, would enable researchers to use a longitudinal design to study whether structural dependencies have moderated the willingness to switch suppliers. For example, researchers could study how preferences for products “made in the USA” (or another country) evolve with changes in government administration and policy discourses.

We framed environmental friendliness as an extrafunctional attribute of input materials that is measurable in discrete increments and entirely separable from functional attributes. Our scenarios provide a somewhat extreme case where the improvements in environmental friendliness countenanced are large (50% or 100%) and are assumed to have no functional implications. Rigorous interview and/or observational case study research could explore managers’ views on the difference between functional and extrafunctional attributes, whether there is a gray zone, or whether attributes could evolve from being extrafunctional to become functional over time as consumer preferences evolve. Moreover, experiments and qualitative research could also delve deeper into the proposed mechanisms. A key weakness of the blocked conjoint design is that it remains hard to identify individual differences in decision makers’ causal cognitions. Other types of conjoint design (e.g., repeated-measures metrics or fully crossed designs) could possibly address this more accurately.

Our conjoint design also highlighted that temporary supply problems are a key barrier in the context of input-switching decisions. This is perhaps not surprising given that novel materials often lack well-functioning, high-volume markets from which they can be sourced (Bellmann & Khare, 2000). This finding is important for policy makers and producers of ecological inputs as it suggests such companies should prioritize ensuring a stable supply and sufficient volumes to increase their chance of market success. How innovative suppliers resolve this chicken-or-egg problem is an important area for future research.

Finally, structural dependence as a complement to theories of external influence opens diverse research avenues. Rather than focusing on organizational inertia in terms of population survival (Hannan & Freeman, 1977, 1984), scholars might build on our work and investigate how specific firm structures could create a form of situational inertia in the face of specific opportunities or threats. Future research could explore how our focal structures interact and whether they influence supplier switching rather than input switching. Like products and processes, supplier relationships can be understood as structures that are more or less dependent on specific inputs. Our findings suggest that managers making decisions may consciously or unconsciously be invoking extant structures. Switching decisions may be influenced by micro, meso, or macro structures that further calcify with each decision. In doing so, we invite further research on how structural dependencies may be linked to the microfoundations of structural inertia. To close, our focus on micro and meso material and macro immaterial structural dependencies could be turned around. In the market for technology transfer, for instance, researchers could investigate whether dependence on a specific knowledge input (tied to a product), knowledge domain (tied to the firm’s overall research process), or tangible asset base influences merger decisions.

Conclusion

We explored the understudied what-to-buy decision required of manufacturing firms and found input-switching decisions are positively influenced by environmental friendliness. However, even in a beneficial scenario of a newly available input that can perform exactly the same function at the same price as the current one, many firms do not choose to switch lightly. To explain that reluctance, we propose that inertia thinking is a natural complement to theories of external influence, like ecological responsiveness, demand-side research, and stakeholder theory. We find that the salience of environmental friendliness of an alternative input is influenced by firms’ micro (product), meso (process), and macro (asset base) organizational structures. Managers consider these structures, either consciously or unconsciously, when deciding on their willingness to switch to an alternative input material.