Abstract

In this study, we explore how top executives affect the well-being of multiple stakeholders and long-run organizational outcomes. In the context of the 2008 global financial crisis (GFC), we examine how CEO greed impacts firms’ stance toward corporate social responsibility (CSR) prior to the onset of the GFC and how this, in turn, shapes firms’ fate during and after the GFC. We argue that CEO greed will be negatively associated with CSR, because in their unbridled pursuit of personal wealth, greedy CEOs are more likely to exhibit myopic behaviors and neglect investment in CSR. We also adopt a person-pay interactionist logic to theorize that the willingness of greedy executives to invest in CSR will be especially sensitive to different types of pay instruments. Next, we build on recent findings from research on CSR that suggest that stakeholder engagement is a defining feature of resilient organizations. We expect that, due to low CSR investment, firms led by greedy CEOs will experience greater losses in the short run and will take longer time to recover from the 2008 GFC. For a sample of 301 CEOs of public U.S. organizations, we analyzed the stock prices and found general support for our hypotheses.

Keywords

Reflecting on the devastating consequences of the 2008 global financial crisis (GFC) in his address to General Motors employees, President Obama (2009) condemned the corporate “attitude that’s prevailed in Washington and Wall Street . . . for far too long; an attitude that valued wealth over work and selfishness over sacrifice and greed over responsibility.” Echoing this sentiment, both scholars and the media have suggested that the unbridled selfishness of top executives may be detrimental to the livelihood of organizations and to the welfare of broader society (Haynes, Hitt, & Campbell, 2015; Haynes, Josefy, & Hitt, 2015; Wang & Murnighan, 2011). Greed, defined as “the pursuit of excessive or extraordinary material wealth” (Haynes, Campbell, & Hitt, 2017: 556), is an individual-level motive characterized by an extreme form of self-interested behavior and a low concern for the well-being of others (Haynes, Josefy, et al., 2015). 1 Despite the existence of widespread agreement on the destructive consequences of executives’ greed, however, there is surprisingly little empirical evidence to corroborate these concerns. Although management scholars have recently taken some initial steps to explore the influence of CEO greed on organizational outcomes and documented its negative impact on shareholder returns (Haynes et al., 2017), systematic evidence of how executives’ greedy behavior affects multiple stakeholders and long-run organizational outcomes is still lacking.

We address this issue. We explore how CEO greed shapes firms’ stances toward corporate social responsibility (CSR) and how this, in turn, affects firms’ resilience to systemic shocks, of which the 2008 GFC was a prime example. CSR is an umbrella term for firms’ actions that yield benefits for multiple stakeholders beyond legal requirements (McWilliams & Siegel, 2001). Because executives are directly involved in formulating CSR strategies (Waldman, Siegel, & Javidan, 2006), a burgeoning stream of research that builds on the upper-echelons (UE) perspective (Hambrick & Mason, 1984) suggests that the immense variance in CSR reflects the heterogeneity in corporate leaders’ motives (Chin, Hambrick, & Treviño, 2013; Petrenko, Aime, Ridge, & Hill, 2016; Wowak, Mannor, Arrfelt, & McNamara, 2016).

Relying on the UE perspective, we argue that CEOs’ greed will be reflected in their firms’ diminished level of engagement with stakeholders. Stakeholder engagement, as expressed through CSR, is a long-term-oriented strategic investment with limited immediate payoffs (Kang, 2016). Because greedy CEOs excessively focus on maximizing short-term profitability (Haynes, Josefy, et al., 2015), we assume that they will be more likely to neglect stakeholders’ needs. Moreover, because executive behavior is shaped not only by intrinsic but also by extrinsic motives (Wowak, Gomez-Mejia, & Steinbach, 2017), we also theorize that the relationship between CEO greed and CSR will be contingent on the type of executive pay arrangements that are in effect (Wowak & Hambrick, 2010). Scholars have relied on agency theory (Eisenhardt, 1989) to argue that monetary incentives are a powerful tool for channeling CEOs’ focus toward stakeholders’ needs (Deckop, Merriman, & Gupta, 2006; Flammer, Hong, & Minor, 2019; McGuire, Dow, & Argheyd, 2003). As the insatiable acquisition of wealth is a hallmark of greed (Wang & Murnighan, 2011), we suggest that the willingness of greedy CEOs to invest in CSR will be especially sensitive to different types of pay instruments, such as bonuses and restricted stocks.

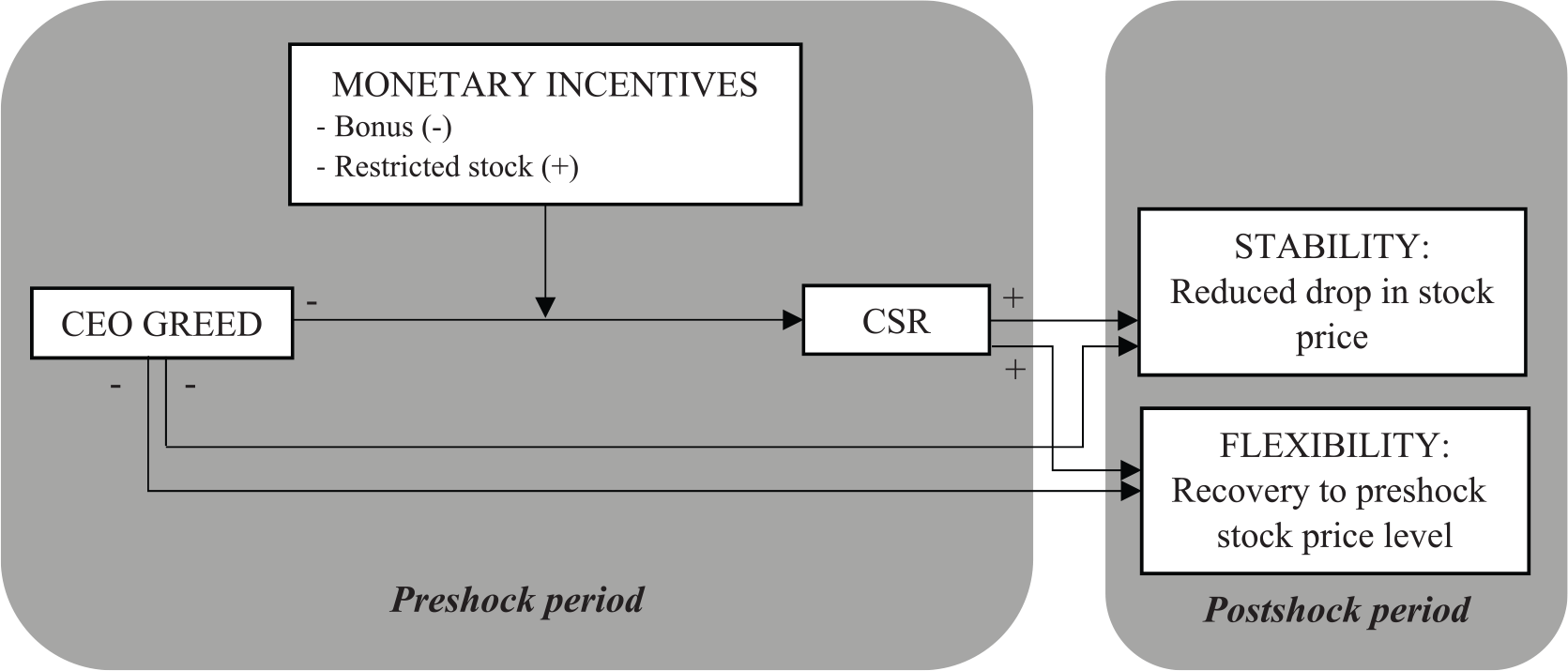

To examine the long-run consequences, we investigate whether firms with greedy CEOs and reduced investments in CSR are also less resilient to environmental disturbances. Organizational resilience is the latent “ability of organizations to anticipate, avoid, and adjust to shocks in their environment” (Ortiz-de-Mandojana & Bansal, 2016: 1615). We build on recent findings from research on CSR that suggest that stakeholder engagement is a defining feature of resilient organizations (DesJardine, Bansal, & Yang, 2019; Flammer & Ioannou, 2018; Ortiz-de-Mandojana & Bansal, 2016). Investment in CSR contributes to organizational resilience in two ways: First, it builds stability by creating interdependencies and strengthening relationships between the firm and its stakeholders, thereby fostering firms’ capacity to absorb exogenous shocks; second, it gives rise to greater flexibility, because firms with broad stakeholder engagement gain access to diverse and distinctive points of view, thereby increasing the set of possible adjustments to external changes (DesJardine et al., 2019). On the basis of these insights, we expect that, due to low CSR investment, firms led by greedy CEOs will experience greater losses in the short run, as manifested in a drop in these firms’ stock price in the immediate aftermath of a systemic shock, and they will need more time to recover.

Figure 1 depicts our research framework. Working with a sample of 301 CEOs of publicly listed U.S. companies, we analyzed CSR before and resilience during and after such a systemic shock: the 2008 GFC. Our results suggest that CEO greed was indeed negatively associated with CSR in the preshock (2003-2008) period and that this relationship was amplified when executive pay was linked to short-term targets. Furthermore, although we do not find that firms with low CSR investment or greedy CEOs experienced greater drops in stock price in the postshock period, our findings do indicate that both CEO greed and low CSR investment are associated with longer recovery times.

Research Framework

Our study makes a number of contributions. First, we contribute to the literature on the drivers of executive behavior (Busenbark, Krause, Boivie, & Graffin, 2016; Wowak et al., 2017). By integrating the UE perspective and agency theory to predict why and how CEOs shape firms’ CSR profiles and long-run performance, we respond to calls to integrate CEOs’ pecuniary and nonpecuniary motives as antecedents of strategic decision making (Wowak et al., 2017). Second, we complement the CSR literature on organizational resilience (DesJardine et al., 2019; Ortiz-de-Mandojana & Bansal, 2016) by illustrating how CEOs promote socially responsible initiatives and, in turn, affect their firms’ ability to cope with systemic shocks. There is growing evidence that CSR investments yield long-term benefits, yet this line of research has stopped short of examining its antecedents. We extend this literature by pointing out that consideration of executives’ motives for investing in CSR is essential for a more complete understanding of the drivers of organizational resilience. Third, we contribute to the body of UE research that explores the impact of executives’ characteristics on organizational outcomes in the context of systemic shocks (Buyl, Boone, & Wade, 2019; Patel & Cooper, 2014). These studies have examined how executives adopt (reckless) risk-taking strategies and thereby affect the long-run fate of their organizations. We add to this research by proposing that CEOs may also impact firms’ capacity to endure and bounce back from systemic shocks by neglecting investment in CSR due to their excessive focus on current earnings. Finally, we contribute to the growing management literature that investigates the organizational consequences of executive greed (Haynes et al., 2017; Haynes, Hitt, et al., 2015; Haynes, Josefy, et al., 2015; Wang & Murnighan, 2011). This research has examined how CEO greed impacts short-run organizational outcomes, such as shareholder wealth (Haynes et al., 2017). We extend this scholarship by providing evidence that CEO greed also has important long-run consequences: It jeopardizes organizations’ resilience to systemic shocks.

Theory and Hypotheses

CSR Perspectives

In this study, we add to the long-standing but ongoing debate (e.g., Smith & Rönnegard, 2016) between two classical views on the purpose of the firm and executives’ responsibility. On the one hand, advocates of the shareholder view argue that executives should act solely to the benefit of their firms’ owners, the shareholders. Going back to Friedman (1962), they argue that in a free economy, the only social responsibility for executives should be to maximize the firm’s profits, within the rules of the game—that is, without deception or fraud. Executives thus have a fiduciary duty to follow the interests of their firms’ owners (N. Smith & Rönnegard, 2016).

Conversely, the stakeholder view proposes that there are various other parties—stakeholders—that should also be considered during strategy development and decision making (Freeman, 1984). Stakeholders are commonly defined as “any group or individual who can affect or is affected by the achievement of the organization’s objectives” (Freeman, 1984: 46). This implies that executives’ social responsibility is directed not only toward the shareholders, and not even only toward their organizations’ primary stakeholders—those with whom they have a contractual arrangement, such as employees, customers, and shareholders—but also toward their secondary stakeholders; this latter group does not enter into formal contractual arrangements or direct transactions with the firm, and it includes entities such as community groups or nongovernmental organizations (Thijssens, Bollen, & Hassing, 2015). In line with this view, CSR is generally defined as encompassing all voluntary organizational actions that generate benefits for all stakeholders, beyond the firm’s owners alone (McWilliams & Siegel, 2001). CSR does not inevitably preclude the maximization of shareholder value (Smith & Rönnegard, 2016), but it generally drains short-term profits in favor of long-run value creation—for example, through the development of good relationships with stakeholders (Kang, 2016).

Despite their opposing stances on executives’ responsibility, both the shareholder view and the stakeholder view are normative in nature (Donaldson & Preston, 1995): They stipulate what executives should do. At the same time, they do not account for what executives want to do. Yet a growing stream of research shows that there is an immense heterogeneity in executives’ motives to attend to shareholders’ and/or stakeholders’ benefits (Chin et al., 2013; Gupta, Briscoe, & Hambrick, 2017; Kang, 2016; Tang, Qian, Chen, & Shen, 2015; Wowak et al., 2016). In this study, we focus on a key motive for executives: greed. This is a very relevant motive for our study, as we argue that high levels of executive greed violate the normative assumptions of both the shareholder and the stakeholder view. Haynes et al. (2017) have already convincingly shown that executive greed, as a manifestation of managerial opportunism, negatively affects shareholders’ interests. They found that instead of caring for the maximization of shareholder wealth, greedy CEOs directed more of their firms’ resources to themselves, resulting in lower shareholder returns (Haynes et al., 2017). We add to this finding by proposing that greed will also negatively affect executives’ willingness to act in the best interest of other stakeholders. More specifically, we expect greedy CEOs to reduce investments in CSR and to expose their organizations to the harmful consequences of systemic shocks, acts that therefore go against what is assumed in the stakeholder view.

Greed

Owing to its origins in Adam Smith’s (1776/1977) The Wealth of Nations, self-interest is traditionally seen as the driving force behind executives’ decision making in classical economic theories. Although this idea has inspired a view of uniformly self-interested executives (Hirschman, 1977), abundant evidence indicates that self-interest is subject to systematic individual differences (Declerck & Boone, 2016; Haynes, Josefy, et al., 2015). Greed, which is most commonly defined as an excessive materialistic desire to acquire personal wealth (Wang & Murnighan, 2011), can be seen as the “dark” end of the self-interest continuum—that is, hyper-self-interest (Haynes et al., 2017). Whereas “healthy” self-interest generally comes with positive externalities, as A. Smith (1776/1977) discussed, this is not the case for hyper-self-interest. The unbridled, purely self-serving pursuit of personal wealth that is associated with greed is not aligned with collective interests—the “greater good” (Haynes et al., 2017). In a similar vein to the way in which executives’ positive self-concept (core self-evaluation) turns into hubris when it reaches very high levels (Hiller & Hambrick, 2005), greed could be seen as an “unhealthy” excess of self-interest (Haynes et al., 2017). While self-interest is morally neutral, greed carries a moral charge (Posner, 2003). As such, it is closely related to moral identity, which refers to individuals’ inherent tendency to abide to socially constructed rules of moral conduct (Aquino & Reed, 2002). Indeed, the pursuit of self-interest at the expense of the well-being of others associated with greed is regarded as immoral in most societies (Posner, 2003).

Greed by definition implies a lack of concern for the well-being of others (Wang & Murnighan, 2011). A long tradition of research in social psychology supports this. For instance, it has repeatedly shown that in prisoners’ and social-dilemma games, greedy individuals tend to opt for defection, which endows them with short-term gains at the expense of group welfare (Bogaert, Boone, & Declerck, 2008; Declerck & Boone, 2016). Conversely, individuals’ moral identity positively affects volunteerism and donation behavior (Aquino & Reed, 2002). Translating these findings to an organizational context, we expect that greed will reduce CEOs’ readiness to attend to stakeholders’ interests in strategic decision making, bringing about decreases in CSR and in long-run resilience. In support of this, Ormiston and Wong (2013) found CEOs’ moral identity to be a key driver of corporate social irresponsibility.

Greed is related to but distinct from another CEO characteristic that has been featured in both the CSR (Petrenko et al., 2016) and organizational resilience literatures (Buyl et al., 2019): narcissism. Narcissists are “those who have very inflated self-views and who are preoccupied with having those self-views continuously reinforced” (Chatterjee & Hambrick, 2007: 351). Narcissists constantly strive to increase their “narcissistic supply”—that is, they seek to reinforce their inflated self-image by engaging in exhibitionistic acts that attract external praise and awe (Chatterjee & Pollock, 2017). Narcissism relates to greed because both concepts heavily draw on the notion of self-interest. However, whereas greed is defined in economic terms, narcissism is not: With narcissism, the extreme pursuit of wealth transforms into an extreme pursuit of an ideal and grandiose self-image. Because of this distinction, the two characteristics may produce opposite behaviors. That is, narcissistic CEOs have been shown to favor CSR investment because furthering some social good brings about admiration from external audiences (Petrenko et al., 2016). This increased engagement in CSR, however, stands in contrast to what can be expected from greedy CEOs. We explain why below.

CEO Greed and CSR

We expect a negative association between CEO greed and firms’ CSR (see Figure 1) due to greedy CEOs’ diminished concern for how their strategic decisions affect the well-being of the firm’s stakeholders. In their unbridled pursuit of financial wealth, greedy CEOs may seize firm resources that could have otherwise been allocated to social issues, or they might compromise the safety of workers and engender devastating consequences for the natural environment, as was the case in the 2010 BP oil spill in the Gulf of Mexico (Haynes, Josefy, et al., 2015). Moreover, even though firms face increasing pressures from diverse institutional actors to contribute to social welfare (Wang, Tong, Takeuchi, & George, 2016), greedy executives are less likely to be receptive to arguments about the organizational benefits of employee satisfaction or community engagement (Haynes, Josefy, et al., 2015) as long as these pressures do not endanger CEOs’ wealth. Greedy CEOs’ opportunistic tendencies are also at odds with a commitment to the long-run fate of their organizations or to the building of strong stakeholder relations, given that these executives are more likely to leave the firm in pursuit of greater material wealth in the form of higher compensation or prestige elsewhere (Haynes, Josefy, et al., 2015).

In addition, we argue that the negative association between CEO greed and CSR is especially likely in the contemporary business environment. Today’s corporate milieu is in general geared toward the short term and away from activities that benefit larger communities (Hambrick & Wowak, 2012). In recent years, the combination of rising quarterly-earnings pressures and steeply declining CEO tenures has led to an increased emphasis on short-term decision making (Mizruchi & Marshall, 2016). In addition, CEO pay is closely tied to firm performance, and firms typically experience declines in market value for failing to meet quarterly targets (Mizruchi & Marshall, 2016). This implies that CEOs with an excessive desire to accumulate material wealth are expected to have especially pronounced short-term interests. Hence, they are less likely to invest in CSR because committing resources to social issues requires a short-term financial sacrifice that primarily pays off only in the long run (Kang, 2016). Taken together, this leads us to hypothesize the following:

Hypothesis 1: CEO greed will have a negative impact on a firm’s CSR.

Monetary Incentives, CEO Greed, and CSR

Scholars in the agency theory tradition have repeatedly established the relevance of monetary incentives as instruments for influencing CEO behavior (Eisenhardt, 1989). In particular, CEOs’ compensation packages are generally designed so that they reward CEOs for attaining particular (desired) outcomes. CSR scholars have used this insight to argue that certain pay packages can steer CEOs to adopt longer time horizons, which may lead them to establish and strengthen relationships with the firm’s stakeholders (Deckop et al., 2006; Flammer & Bansal, 2017). In this respect, two CEO pay components are of particular relevance: (a) bonuses, which focus on short-term-oriented performance outcomes (Hou, Li, & Priem, 2013), and (b) restricted stocks, which can be cashed only after a particular time period (Johnson & Greening, 1999).

However, the empirical evidence on the effects of CEO pay on CSR is not clear-cut (Hart, David, Shao, Fox, & Westermann-Behaylo, 2015). In the case of firms’ environmental performance, for instance, researchers have found that long-term-oriented executive pay has both positive (Berrone & Gomez-Mejia, 2009) and negative (Berrone, Cruz, Gomez-Mejia, & Larraza-Kintana, 2010) effects. Given this ambiguity, we build on a person-pay logic (Wowak & Hambrick, 2010) to theorize that CEOs’ tendency to invest in CSR when provided with short- or long-term incentives is contingent on their motives (here, CEO greed; see Figure 1).

Bonus

Annual bonuses are outcome-based instruments that tie CEO pay to generally financial objectives (McGuire et al., 2003). They have an asymmetric payoff structure: CEOs are rewarded for attaining year-end performance targets, but they are not penalized for failing to achieve them (Hou et al., 2013). This represents a strong incentive for (greedy) CEOs to boost short-term firm performance so as to maximize their personal wealth. Because stakeholder engagement requires long-term horizons for financial benefits to accrue (Flammer & Bansal, 2017), scholars have argued and found that CEO pay based on a high proportion of bonuses is negatively associated with investment in CSR (Fabrizi, Mallin, & Michelon, 2014). Due to the asymmetric payoff structure of bonuses, the focus of CEOs who have a strong desire to accumulate personal wealth—that is, greedy CEOs—on short-term strategic actions will be exacerbated when their pay heavily depends on annual bonuses, potentially even at the expense of damaging stakeholder relations. We expect that the greedier the CEO, the more strongly large bonus-based pay relative to total compensation will incentivize the CEO to maximize short-term returns. Therefore, we hypothesize the following:

Hypothesis 2a: The relationship between CEO greed and a firm’s CSR will be more negative if a higher proportion of the CEO’s pay is an annual bonus.

Restricted stock

In contrast, restricted stock ownership compels CEOs to adopt long-term horizons. Under such pay arrangements, CEOs hold stock that cannot be sold until certain conditions—usually, continued employment for a period of time—are met (Johnson & Greening, 1999). This implies that a sizable portion of the CEO’s wealth becomes tied to long-term performance outcomes, and at the same time it reduces the pressure to maximize earnings in the short run (Deckop et al., 2006). Longer time horizons, in turn, may motivate CEOs to become more cognizant of the importance of continued stakeholder support and legitimacy (Johnson & Greening, 1999). Hence, restricted stock that cannot be sold for a longer period of time incentivizes CEOs to treat stakeholders fairly (Hambrick & Wowak, 2012). Empirical evidence supports the idea that long-term-oriented executive compensation leads to increased investment in CSR (Deckop et al., 2006; Flammer et al., 2019; Flammer & Bansal, 2017).

This suggests that the negative association between CEO greed and CSR might be contingent on whether executive compensation contains long-term incentives. If a considerable portion of CEO pay consists of restricted stock, executives who have a strong desire to acquire material wealth might especially become attuned to the well-being of stakeholders. Because restricted stock ties a CEO’s wealth to long-term firm valuations, we expect that the greedier the CEO, the more strongly large proportions of restricted stock will incentivize the CEO to consider long-term strategic investments such as CSR. This leads us to hypothesize the following:

Hypothesis 2b: The relationship between CEO greed and a firm’s CSR will be less negative if a higher proportion of the CEO’s pay is restricted stock.

CEO Greed, CSR, and Organizational Resilience

Organizational resilience is a system’s latent ability to endure despite adversity and to recover and maintain its existing structure after a shock (Gunderson & Pritchard, 2002). Two essential properties give rise to resilient systems: stability and flexibility (DesJardine et al., 2019). Stability includes a set of capabilities that enable a firm to preserve its key organizational attributes, such as its core functions and structure, in the face of disturbances (Weick, Sutcliffe, & Obstfeld, 2008), whereas flexibility entails a stock of flexible and diverse resources that facilitate the development of alternative solutions to the same disruption (Sanchez, 1995). Resilient organizations are thus better able (a) to preserve their core structures and (b) to bounce back from setbacks, because they excel at anticipating, absorbing, and adjusting to environmental changes (Ortiz-de-Mandojana & Bansal, 2016). In line with DesJardine et al. (2019), we assess both facets of resilience in terms of stock behavior, since market valuations reflect all relevant and new information about the firm. To examine stability, we evaluate the drop in stock price immediately after a severe systemic shock. To assess flexibility, we consider the time it takes a firm’s stock price to recover to preshock levels (DesJardine et al., 2019).

Research on organizational resilience emphasizes that it is essential to consider a firm’s features prior to a systemic shock if one is to understand how it will react to the shock (Buyl et al., 2019). Therefore, we explore how both CSR and CEO greed in the preshock period contribute to firms’ stability and flexibility in the postshock period (see Figure 1) and therefore play a vital role in the creation of resilient organizations. Investment in CSR fosters resilience through mechanisms that are primarily external to the firm. For example, due to increased stakeholder support and reciprocity, firms become more strongly embedded in their social and natural environment (Ortiz-de-Mandojana & Bansal, 2016). CEO greed is not only expected to decrease stakeholder engagement, but it also relates to resilience through its impact on organizational culture and practices. Because CEOs’ greedy behavior may inspire a culture of cupidity across the entire organization and because it may lead to resource depletion (Haynes et al., 2017; Haynes, Josefy, et al., 2015), it makes firms more vulnerable to environmental shocks.

Stability

CSR fosters a firm’s ability to absorb exogenous disturbances by creating “interdependencies between the organizational system and the social and natural systems in which the organization is embedded” (DesJardine et al., 2019: 5). These interdependencies result from repeated interactions with stakeholders and regularly involve the sharing of resources, values, and information (Albert, Kreutzer, & Lechner, 2015). Firms that engage in CSR are thus more steadily anchored in their environment. For example, not only do employees tend to be more committed to organizations with strong CSR programs (Flammer & Luo, 2017), but CSR also signals conformity to institutional demands, which leads to increased legitimacy and a diminished exposure to unsystematic market risks (Bansal & Clelland, 2004). If firms have high CSR investment in the period before a systemic shock, they are more likely to exhibit greater stability immediately after that shock, because they are strongly embedded in their environment and have deeper relationships with their stakeholders. We expect that this will be reflected in less severe drops in the stock price. Hence, we hypothesize the following:

Hypothesis 3a: The greater the firm’s CSR in the preshock period, the smaller the drop in its stock price following a shock.

In addition to a detrimental effect on stakeholder relations, we propose that CEO greed might also affect firms’ ability to absorb external shocks in other ways. Greedy CEOs are likely to shape organizations so that they develop individualistic cultures (Haynes, Josefy, et al., 2015) that foster increased competition and self-serving behaviors in the top management team (TMT) (Fredrickson, Davis-Blake, & Sanders, 2010) and among lower-level employees (Connelly, Haynes, Tihanyi, Gamache, & Devers, 2016). In individualistic organizations, employees are motivated and incentivized to compete with their colleagues (Lazear & Rosen, 1981), and this can give rise to several undesirable behaviors, such as conflict (Fredrickson et al., 2010) and a manipulation of or an unwillingness to share information (Milgrom & Roberts, 1988). This implies that CEO greed might contribute to the creation of individualistic organizations that fare worse in the long run, because sharing of information is one of the key mechanisms that resilient firms use to sense and interpret changes in the environment (Ortiz-de-Mandojana & Bansal, 2016). Firms can detect problems in the environment only when there is sufficient attentional capacity throughout the entire organization. Individualistic organizations are less likely to integrate their members’ multiple perspectives as a result of their diminished levels of information sharing, and so they compromise their ability to anticipate and adjust appropriately to emerging problems (Sutcliffe & Vogus, 2003). In light of this, we argue that CEO greed in the period before a shock will be associated with a diminished stability that will be reflected in higher losses following that shock. Therefore, we hypothesize the following:

Hypothesis 3b: The greater CEO greed in the preshock period, the larger the firm’s drop in stock price following a shock.

Flexibility

Increased interdependencies between the organization and its stakeholders in the preshock period not only lead to greater stability but also foster greater flexibility after the shock (DesJardine et al., 2019). On the one hand, CSR initiatives positively affect stakeholder motivations. For example, employees in firms with positive labor relations will be more willing to adjust their working time and wages, while fair treatment of the supply chain might facilitate the development between the firm and its suppliers of trust and common efforts focused on bringing about recovery (Ortiz-de-Mandojana & Bansal, 2016). Moreover, firms with strong stakeholder relations also gain access to diverse points of view and information. For instance, reciprocal transactions with customers may lead to faster detection of changes in customer tastes, and repeated interactions with other stakeholders can help firms better identify new technologies or environmental threats (Harrison, Bosse, & Phillips, 2010). Furthermore, the resulting increase in knowledge diversity is conducive to firms’ ability to navigate uncertain and complex environments (Ferrier, 2001), and it stimulates creativity and innovation (DesJardine et al., 2019) in such forms as the cutting of costs through waste reduction or transportation improvements (Ortiz-de-Mandojana & Bansal, 2016). Hence, we expect that firms with high levels of CSR investment before a shock will exhibit greater flexibility in the postshock period due to the increased collective will and information sharing among stakeholders. These firms not only depend on stakeholders who are more willing to adapt but also are more likely to develop novel solutions when faced with adversity. Therefore, we expect that they will take less time to recover from systemic shocks:

Hypothesis 4a: The greater the firm’s CSR in the preshock period, the shorter its recovery time following a shock.

Besides because of its negative effect on CSR, we anticipate that CEO greed in the preshock period will also affect a firm’s ability to recover from systemic shocks because it will exhaust the firm’s internal resources. That is, greedy CEOs strive to appropriate excess returns from the firm to satisfy their material desires (Haynes et al., 2017). In addition, to the extent that CEOs’ greedy behavior is overt, TMT members and lower-level employees are also more likely to engage in greedy acts, thereby further exacerbating agency costs (Haynes, Josefy, et al., 2015). In extreme cases, the cultivation of such an individualistic organizational culture might even lead employees to steal from the firm (Greenberg, 1990). This implies that CEO greed results in a depletion of firms’ resources, which can profoundly limit their ability to recover from a shock (Sutcliffe & Vogus, 2003). This is because “a sufficient amount of internal resources and the ability to rearrange, transform, and adapt these resources to the uncertain and changed postshock economic conditions” are the key ingredients of flexibility (Buyl et al., 2019: 9). We thus anticipate that firms with greedy CEOs in the preshock period will take a longer time to recover from this shock. Hence, we hypothesize the following:

Hypothesis 4b: The greater CEO greed in the preshock period, the longer the firm’s recovery time following a shock.

Sample

We constructed a panel data set of CEOs who served at public U.S. corporations listed on the S&P 1500 index prior to the onset of the GFC. Consistent with prior work, we identify September 17, 2008, as the start of the GFC, which unfolded immediately after Lehman Brothers’ fall and AIG’s bailout by the U.S. Federal Reserve (DesJardine et al., 2019). The ensuing economic meltdown resulted in significant corporate losses across industries and affected all aspects of the business environment (Flammer & Ioannou, 2018). These aspects make the 2008 GFC an ideal natural setting in which to examine organizational resilience.

Our data set was compiled from several sources. Compensation and other CEO-related data were retrieved from Execucomp and the U.S. Federal Election Commission, while data on boards of directors and CEOs’ past employment were gathered from BoardEx. All firm-level accounting data and industry classifications were obtained from Compustat, and information on institutional ownership came from the Thomson-Reuters Institutional Holdings (13F) database. For stock prices, data were drawn from the Center for Research in Security Prices (CRSP) database, while data on CSR came from the Kinder, Lyndenberg, and Domini and Co. (KLD) database. KLD is an independent investment firm that has been providing annual ratings for CSR strengths and concerns under several categories (e.g., environment, community, product quality) for publicly traded U.S. firms since 1991. KLD is the most widely used data source for empirical research on CSR (Mattingly, 2017) and has repeatedly been employed in UE studies (Chin et al., 2013; Petrenko et al., 2016; Wowak et al., 2016) and organizational resilience (DesJardine et al., 2019; Ortiz-de-Mandojana & Bansal, 2016).

To construct the final sample, we applied several conditions. Our baseline population covered all CEOs of firms included in the S&P 1500 in the year 2008 (at the onset of the GFC). We then merged the data from all sources (KLD, Compustat, Execucomp, BoardEx, CRSP, and Thomson-Reuters Institutional Holdings) and dropped observations with missing variables. Subsequently, we excluded observations with missing data and from highly regulated sectors (e.g., public and financial) where managerial discretion might be severely curbed (McNamara, Aime, & Vaaler, 2005). Finally, for a CEO to be included in the sample, we required that he or she could be observed for the three consecutive years of 2006, 2007, and 2008 so that we could capture more than just a snapshot of preshock CEO greed. 2

Applying these criteria left us with a sample of 301 CEOs, each from a different firm. 3 We used the same matched CEO-firm sample in three sets of analyses that cover different time periods. In Part 1, we examine how CEO greed affected CSR during the preshock period. Our observation period started in 2003, when KLD expanded its firm coverage, and ended in 2008, prior to the onset of the GFC. The sample for this first set of analyses comprised 1,419 yearly observations for the 301 CEOs. In Part 2, we analyze how CEO greed and CSR before the GFC (preshock CEO greed and CSR) affected firms’ ability to absorb exogenous shocks in the year following September 17, 2008, for our sample of 301 CEOs. Finally, in Part 3, we study how preshock CEO greed and CSR affected firms’ ability to recover during the 2009-to-2011 period. For this third set of analyses, we excluded 32 CEOs that left the organization in the 2009-to-2011 period. This left us with 5,164 yearly observations for a sample of 269 CEOs. Because our theoretical predictions rely on the explanation of different phenomena (CSR, stability, and flexibility) and require different estimation techniques, we present the methods and results in three separate sections.

Empirics Part 1: Explaining CSR in the Preshock Period

Method

Dependent variable

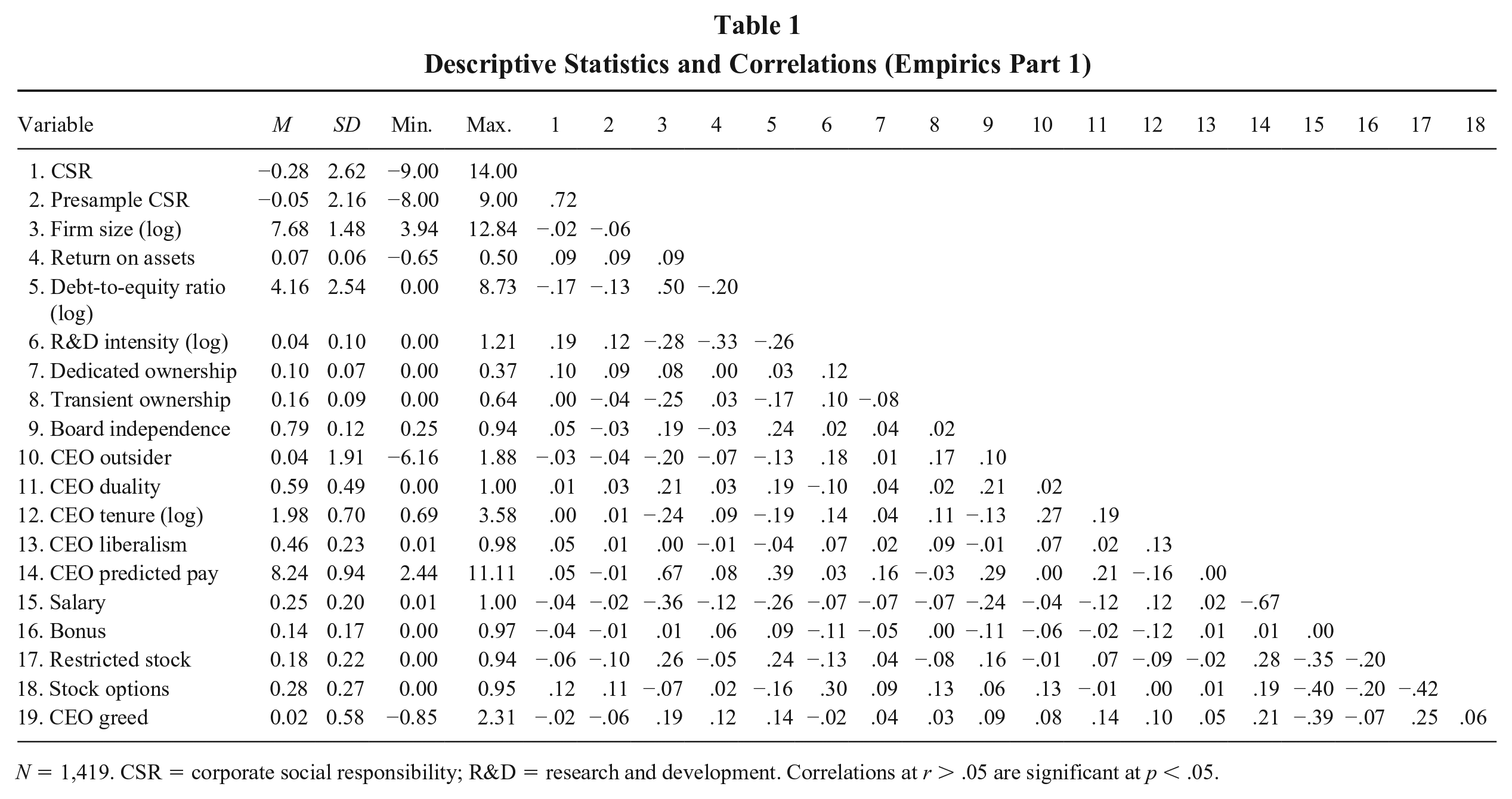

To measure firms’ CSR engagement, we used all of KLD’s rating categories (community, diversity, employee relations, environment, human rights, and product quality) except for the corporate governance category, because the latter relates more to mechanisms that enable shareholders to monitor and control managerial behavior in order to maximize their returns (Servaes & Tamayo, 2013). Hence, our measure assesses firms’ engagement with both primary stakeholders—employees, customers (product quality)—and secondary stakeholders—the community and environmental and human rights stakeholder groups (Thijssens et al., 2015). Following the common approach taken in research on CSR (Gupta et al., 2017; Kang, 2016), we measured CSR as the sum of all binary strength items minus the sum of all binary concern items across all stakeholder categories. On average, the resulting composite CSR score of the firms in our sample was ‒0.28 (SD = 2.62), with a minimum of ‒9 and a maximum of 14. The use of such a composite CSR measure reflects the idea that stakeholder relations can improve both by increasing stakeholder engagement and by minimizing negative externalities (Chin et al., 2013). 4

Independent variable

To operationalize CEO greed, we carefully followed Haynes et al. (2017). These authors recently developed a novel procedure for obtaining an unobtrusive measure of CEO greed. They went to great lengths to establish the construct’s discriminant and predictive validity. For example, they conducted several interviews with senior executives, industry analysts, and experts. In addition, they provided empirical evidence to demonstrate that greed is distinct and independent from related constructs, such as hubris.

We used three proxies of extraordinary compensation to operationalize CEO greed (Haynes et al., 2017); they capture different aspects of abnormal compensation with respect to (a) the market’s view on the appropriate form of compensation, (b) the pay of the next-highest-paid executive in the same firm, and (c) the pay that would be expected based on known predictors of executive compensation. All three measures represent actualized extraordinary wealth, which is an outcome of the latent variable in question, namely, greed, or the pursuit of or desire to acquire excessive material wealth. Assessing actualized forms of compensation to measure greed allows us to rely on unobtrusive indicators from archival data. In contrast, the success of primary data collection on a sample of large corporations not only is implausible due to low response rates but also can be expected to be subject to severe social desirability bias due to the sensitivity of the topic. Moreover, in the context of executive pay, weak pursuit of wealth is unlikely to be reflected in abnormally high compensation, because one of the key duties of the board of directors is to evaluate and set executive pay arrangements (Gupta & Wowak, 2017). This implies that a high score on the compensation-based measure of greed more likely results from an actual pursuit of wealth rather than its being an accidental outcome.

The first proxy is the dollar value of perquisite compensation—that is, annual compensation not properly categorized as salary, bonus, or long-term incentives (Haynes et al., 2017). This variable captures the use of perks and various personal benefits, which tend to reflect agency costs and rent extraction, because shareholders do not consider such forms of compensation to reflect pay for managerial ability (Yermack, 2006). The fact that the majority of executives at S&P 1500 firms receive zero perquisite compensation and the fact that the correlation between perks and firm size is negligible lend support to this view (Haynes et al., 2017). The second proxy is pay disparity, which takes the form of the CEO’s cash pay divided by that of the next-most-highly-paid officer (Haynes et al., 2017). CEOs yield considerable influence over the pay of their TMT (Chatterjee & Hambrick, 2007). Hence, large pay gaps are highly indicative of the presence of greedy CEOs, because uneven distribution of resources is a key outcome of greed (Wang & Murnighan, 2011). 5 The third proxy is CEO overpayment—the excessive portion of CEO compensation that cannot be explained by firm and contextual factors (Haynes et al., 2017). This proxy consist of residuals from a CEO-pay regression (Fong, Misangyi, & Tosi, 2010). Following the standard approach in the literature, we regressed the log of total annual CEO pay on CEO age, CEO tenure, CEO duality, percentage of independent directors on board, firm size, firm risk, sales growth, return on assets (ROA), and firm and year fixed effects. All explanatory variables were lagged by 1 year. The resulting adjusted R2 was .67, which is comparable with that from prior studies. Because we wanted to capture the excessive portion of executive compensation, CEO overpayment was measured as the residual from the CEO-pay regression if the residual was positive and 0 otherwise (Haynes et al., 2017).

To construct the CEO greed variable, we combined the three proxies by using principal component analysis with varimax rotation (Haynes et al., 2017). The results revealed significant loadings of all three compensation-based measures of greed on a single factor (eigenvalue = 1.36; 45% variance explained). 6 Hence, we used factor weightings to compute a single measure of CEO greed, which we winsorized at the 1% and 99% levels to mitigate the impact of outliers. The distribution of CEO greed is shown in Figure A in the online supplement.

Moderator variables

Bonus is the ratio of the annual value of bonus to the total value of all CEO compensation (McGuire et al., 2003), and restricted stock is the ratio of the annual value of restricted stocks to the total value of all CEO compensation (Deckop et al., 2006). 7

Control variables

We include year and industry dummies (based on two-digit Standard Industrial Classification codes) to account for macroeconomic fluctuations and industry membership. We control for a number of firm-level covariates, all of which have been found in prior work to be associated with CSR. We include presample CSR, measured as the value of the firm’s CSR in the year prior to when the CEO was observed in the sample for the first time (Wowak et al., 2016). 8 We also control for firm size, measured as the logarithm of firm sales (Gupta et al., 2017), and ROA, measured as the ratio of income before extraordinary items to the book value of assets (Tang et al., 2015). In addition, we include slack resources, measured as the logarithm of the ratio of long-term debt to market value of equity, as such excess resources increase the opportunity for managers to invest in other-than-economic goals (Stevens, Moray, Bruneel, & Clarysse, 2015). Research and development (R&D) intensity, measured as the logarithm of the ratio of R&D expenses to sales plus 1, is included because previous research has shown that R&D and CSR are highly correlated (McWilliams & Siegel, 2000). 9 Furthermore, previous research has shown that institutional investors play an important role in pressuring CEOs to pursue short-term- versus long-term-oriented strategies (Zhang & Gimeno, 2016). More in particular, transient investors generally have short-term investment horizons, while dedicated investors focus on the longer term (Connelly et al., 2016). Because of this, we control for dedicated ownership, measured as the number of shares owned by dedicated institutional investors divided by the total number of shares outstanding, and transient ownership, measured as the number of shares owned by transient institutional investors divided by the total number of shares outstanding. 10 Finally, we control for board independence, measured as the percentage of independent directors on the board, as the independence and composition of boards of directors has been linked to CSR in prior studies (Hart et al., 2015).

At the CEO level, we account for several variables related to CEOs’ power and human capital: CEO outsiderness, measured as the sum of the inversed standardized firm and industry tenure that the focal CEO attained prior to assuming the post (Karaevli & Zajac, 2013); CEO duality, measured as a dummy that equals 1 if the CEO is also the chairman of the board (Wowak et al., 2016); CEO tenure, measured as the logarithm of the number of years that the CEO was in his or her position (Petrenko et al., 2016); and CEO liberalism, measured as a CEO’s individual political contributions to the Democratic Party (for a detailed description of the measure, see Chin et al., 2013). Previous research has found that liberal, compared with conservative, CEOs engage more in CSR initiatives (Chin et al., 2013). Moreover, when analyzing the effects of CEO greed, it is important to separate them from those of the CEO’s pay level and pay structure (Haynes et al., 2017). Because of that, we include CEO predicted pay (based on the CEO-pay regression from the third CEO greed proxy) to control for CEO pay level, and salary and stock options, measured as a ratio of the CEO’s total compensation to—together with moderators bonus and restricted stocks—control for CEO pay structure.

Estimation

Because our data consist of cross-sectional time series covering the 2003-to-2008 period, we used panel data analysis. The Hausman test failed to reject the null hypothesis, indicating that the random-effect estimator was consistent and therefore appropriate. In our sample, the number of firms equaled the number of CEOs, hence firm-CEO match was used as the grouping variable. To account for heteroscedasticity and intragroup correlations, we clustered standard errors within the panel. All independent, moderator, and control variables were lagged by 1 year. This research design alleviates concerns about endogeneity resulting from reverse causality and is in line with our theorized causal direction.

Results

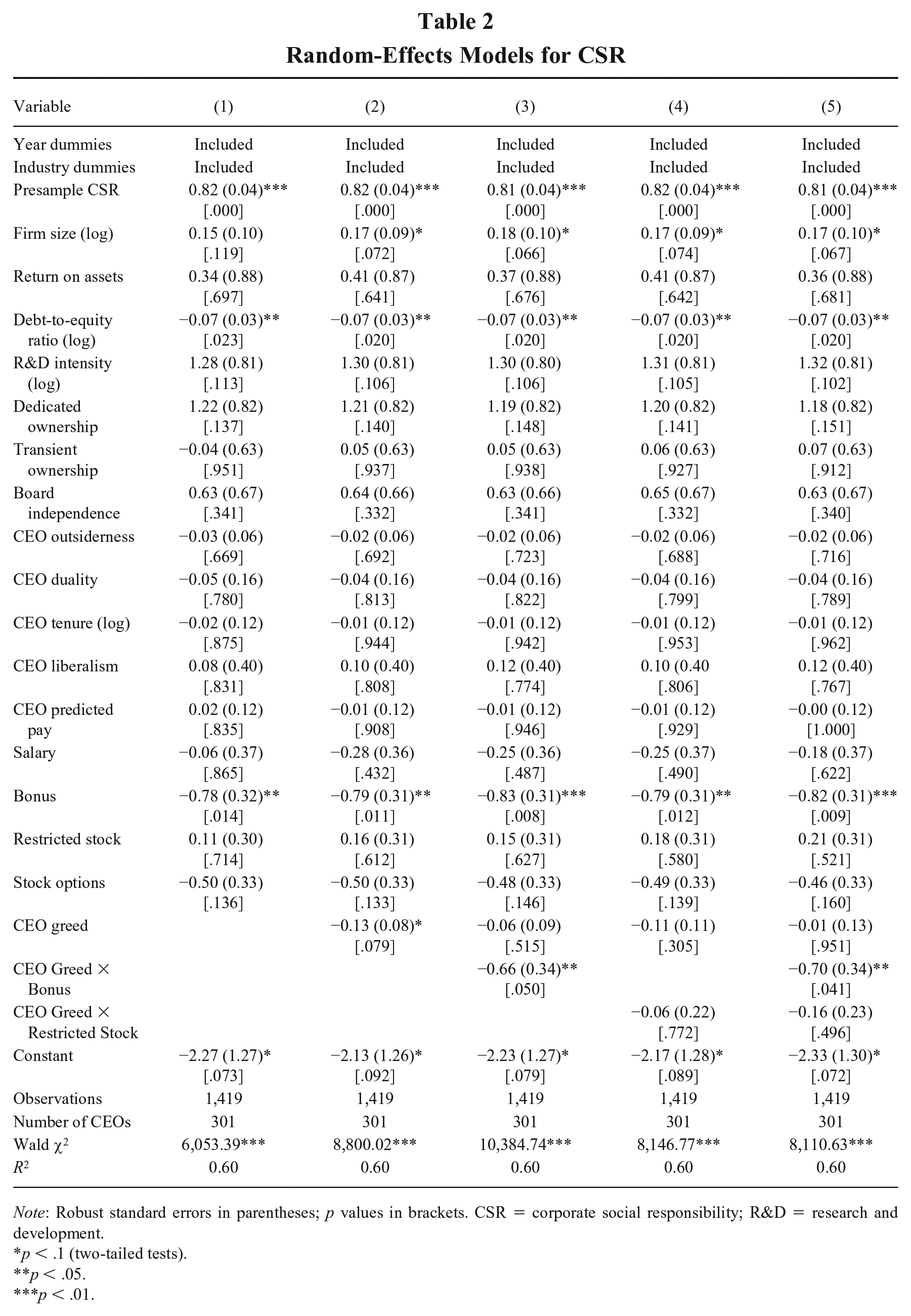

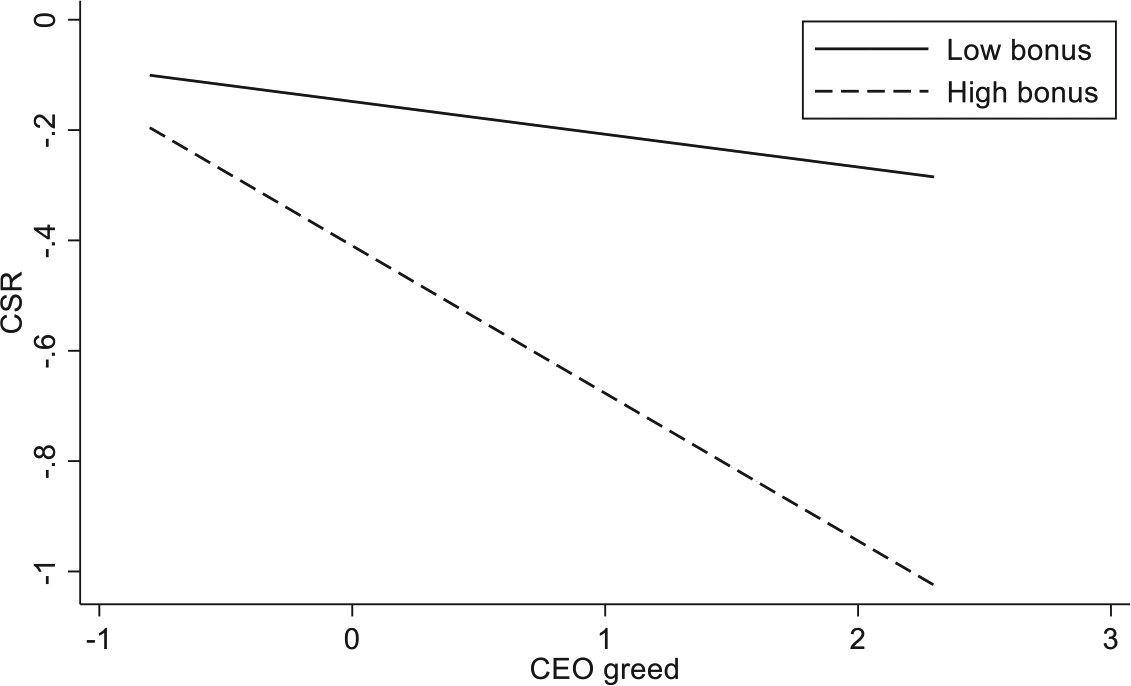

The correlations and descriptive statistics are shown in Table 1. Table 2 reports the regression results. Model 1 includes control and moderator variables only. The results indicate that presample CSR is a strong predictor of CSR (β = 0.82, p = .000). Additionally, firms with abundant slack resources (β = ‒0.07, p = .023) invest more in CSR. In line with theoretical expectations, bonus is negatively associated (β = ‒0.78, p = .014) with it. In Model 2, we introduce CEO greed and find a negative and significant coefficient (β = ‒0.13, p = .091), providing support for Hypothesis 1. A one-standard-deviation (SD) increase in CEO greed results in a 2.9% SD decrease in CSR. In Model 3, we introduce the interaction term between CEO greed and bonus to test Hypothesis 2a, which stated that the negative impact of CEO greed on a firm’s CSR will be more pronounced if the CEO is paid to a larger degree in bonuses. Hypothesis 2a is supported with a negative and significant coefficient on the interaction term (β = ‒0.66, p = .050). All other things being equal, a one-SD increase in CEO greed is associated with a 1.3% SD decrease in CSR when the proportion of bonus is low (mean − 1 SD) and with a 6.0% SD decrease in CSR when the proportion of bonus is high (mean + 1 SD). To visualize this interaction, we plotted the association between CEO greed and CSR in Figure 2 at low and high levels of bonus. In Model 4, where we introduce the interaction term between CEO greed and restricted stock, we fail to find support for Hypothesis 2b. Finally, Model 5 includes all variables and yields further support for the expectation that the combination of CEO greed and short-term-oriented compensation (bonus) has a negative impact on stakeholders. 11

Descriptive Statistics and Correlations (Empirics Part 1)

N = 1,419. CSR = corporate social responsibility; R&D = research and development. Correlations at r > .05 are significant at p < .05.

Random-Effects Models for CSR

Note: Robust standard errors in parentheses; p values in brackets. CSR = corporate social responsibility; R&D = research and development.

p < .1 (two-tailed tests).

p < .05.

p < .01.

The Joint Effect of CEO Greed and Bonus Pay on Corporate Social Responsibility

Robustness checks

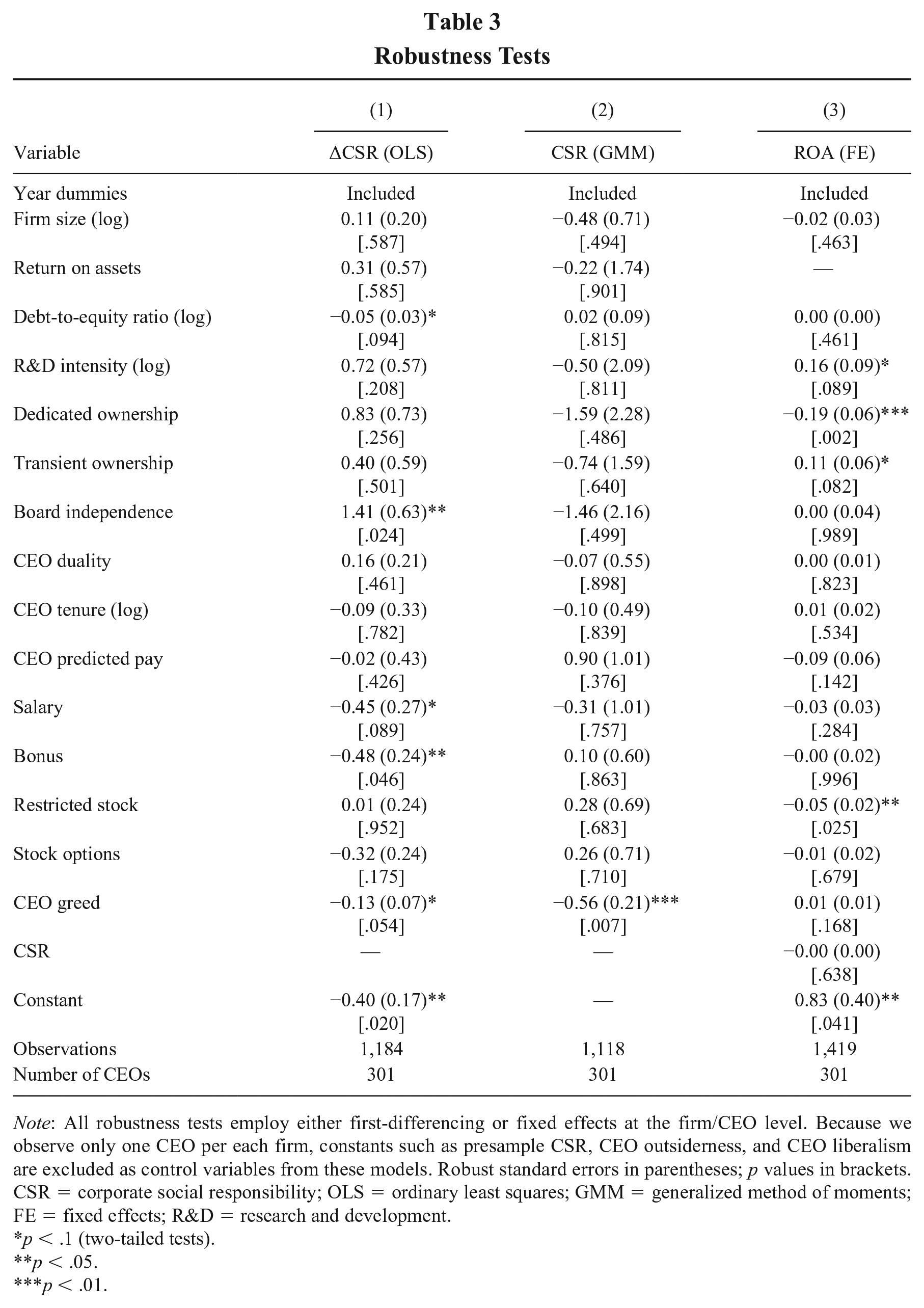

We conducted two tests to address endogeneity concerns. First, we specified an ordinary least squares (OLS) model with robust standard errors to regress the change in CSR (CSR t – CSRt–1) against the change in CEO greed (CEO greedt–1 – CEO greedt–2), controlling for the change in all control variables and year fixed effects. The sample size was reduced to 1,184 CEO-year observations due to the additional data requirements. The regression results shown in the first column of Table 3 indicate that the coefficient of change in CEO greed remains negative and significant (β = ‒0.13, p = .054). Second, we employed the generalized method of moments (GMM) approach (Arellano & Bond, 1991), which handles endogeneity by incorporating internal instruments consisting of first differences of multiple lags on all right-hand-side variables. We used lags of t ‒ 2 and t ‒ 3 as instruments to avoid the problems arising from instrument proliferation that are associated with longer lags (Roodman, 2009). Due to the lag structure, the sample size for this analysis was reduced to 1,118 CEO-year observations. Both the Sargan and the Hansen test for overidentifying restrictions indicated that the internal instruments were exogenous. We specified a two-step first-difference GMM estimator and applied Windmeijer-corrected standard errors to control for downward bias in the estimator (Windmeijer, 2005). The negative and significant coefficient on CEO greed (β = ‒0.56, p = .007) in the second column of Table 3 provides further support for our findings and suggests that endogeneity has not introduced a bias into our results.

Robustness Tests

Note: All robustness tests employ either first-differencing or fixed effects at the firm/CEO level. Because we observe only one CEO per each firm, constants such as presample CSR, CEO outsiderness, and CEO liberalism are excluded as control variables from these models. Robust standard errors in parentheses; p values in brackets. CSR = corporate social responsibility; OLS = ordinary least squares; GMM = generalized method of moments; FE = fixed effects; R&D = research and development.

p < .1 (two-tailed tests).

p < .05.

p < .01.

Furthermore, our argument that CEO greed leads to a decrease in CSR engagement due to a greedy CEO’s myopic focus on the maximization of short-run profits suggests that CEO greed should be positively associated with short-term firm performance. To strengthen our theoretical arguments, we investigated this implication. Following Connelly et al. (2016), we operationalized short-term performance as ROA in year t. We regressed ROA on the same set of lagged covariates as those used in our main analyses, except that we replaced lagged ROA with lagged CSR as a predictor. The Hausman test rejected the null hypothesis; hence we specified a fixed-effects model with clustered standard errors. The coefficient of CEO greed in the third column of Table 3 is positive, as expected, but did not reach statistical significance (β = 0.01, p = .168).

Finally, one might argue that our measure of CEO greed (based on abnormally high compensation) may be driven by the CEO’s human capital—that is, CEOs with a college or MBA degree, or who studied at an elite school, might be able to reap higher compensation. We reran the analyses including control variables to account for these CEO features (see Table C in the online supplement) and found that this did not change our results. Similarly, our findings hold if we exclude insignificant CEO-level control variables (see Table D in the online supplement).

Empirics Part 2: Explaining Postshock Stability

Method

Dependent variable

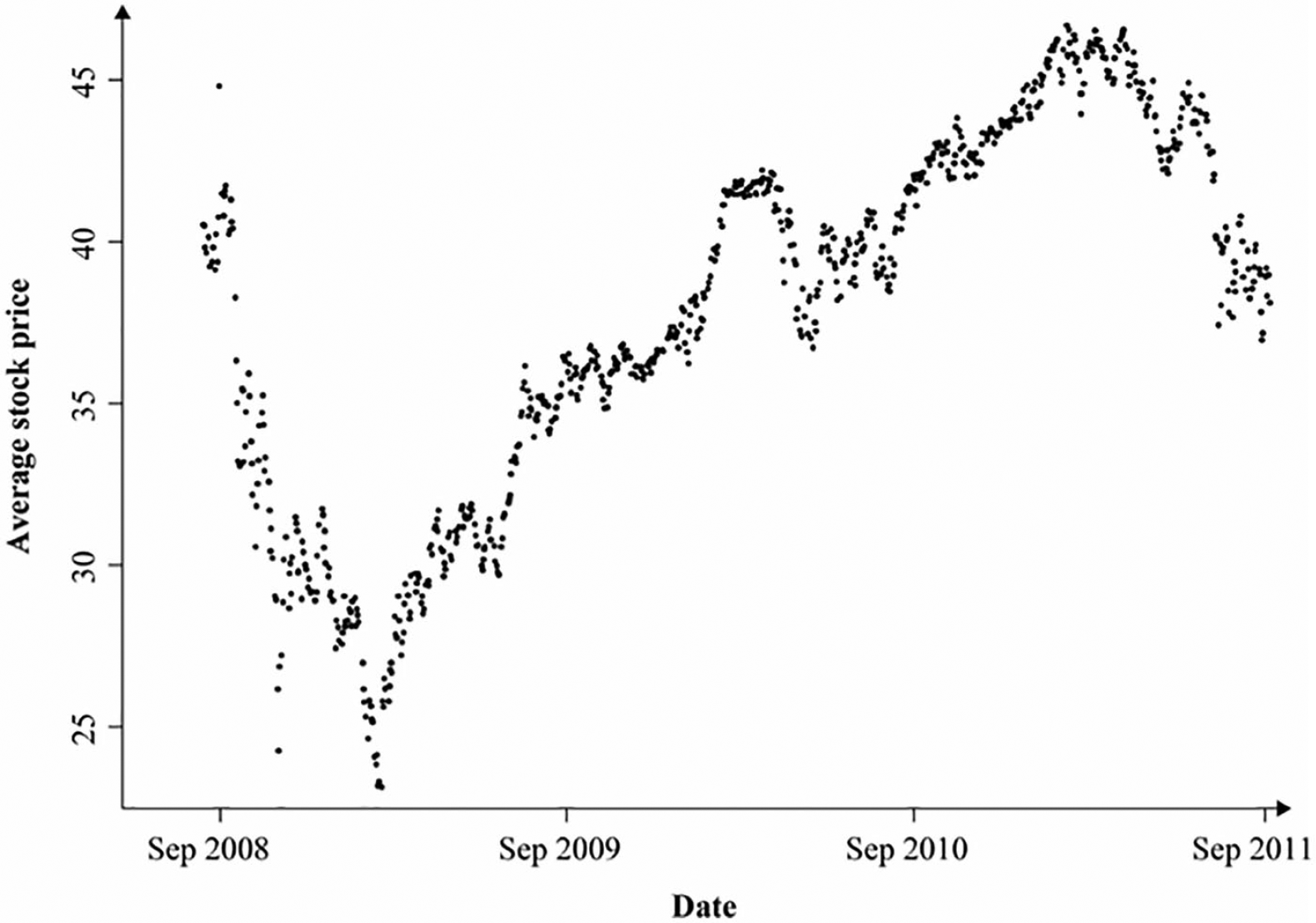

We follow DesJardine et al. (2019) and measure a drop in a firm’s stock price as the absolute percentage change between the closing price just before the onset of the GFC on September 17, 2008, and the lowest closing price that the stock reached within a 12-month period. 12 A high value on this measure reflects a large drop. A window of 1 year is the standard boundary in related studies (Buyl et al., 2019; DesJardine et al., 2019) and reduces the likelihood that drops in stock price are driven by other events. Additionally, a visual inspection of the average daily stock price movements (see Figure 3) confirms that the severest drop in stock price following the economic meltdown occurred in the first quarters of 2009.

Average Daily Stock Price During the Period September 2008 to September 2011

Independent variable

Both CSR and CEO greed are operationalized as described earlier. However, we measured both variables prior to the GFC (preshock CSR and CEO greed). We took the average value during the 2 years before the shock (2007-2008) to ensure that we capture more than just a snapshot of preshock CSR and CEO greed.

Control variables

We included industry dummies to control for industry-level stock price drops and used the same set of control variables as in Part 1. In line with the independent variables, all control variables were computed as the average of their 2007 and 2008 values to capture stable preshock tendencies. Additionally, we control for several firm-level factors that might have affected the drop in stock price immediately after the shock (DesJardine et al., 2019): firm age, measured as the logarithm of the number of years since the firm was first covered by Compustat; intangible assets, measured as the logarithm of market-to-book ratio; operational efficiency, measured as the ratio of sales to total assets; and capital intensity, measured as the ratio of capital expenditures to total assets. To account for regression to the mean (Buyl et al., 2019), we also control for preshock stock price, measured as the closing price on September 16, 2008.

Estimation

Because our data were a cross-section, we specified OLS models with robust standard errors.

Results

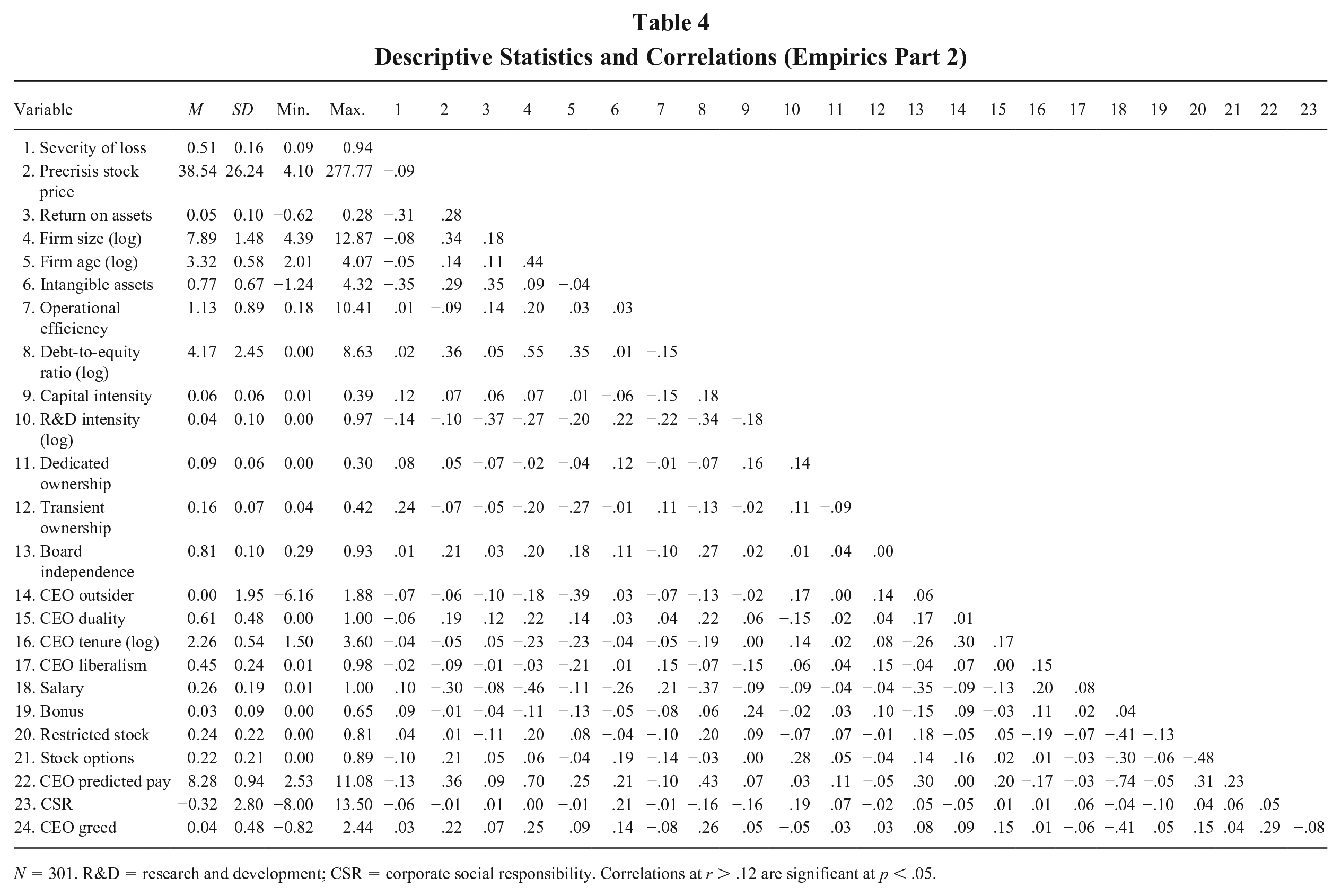

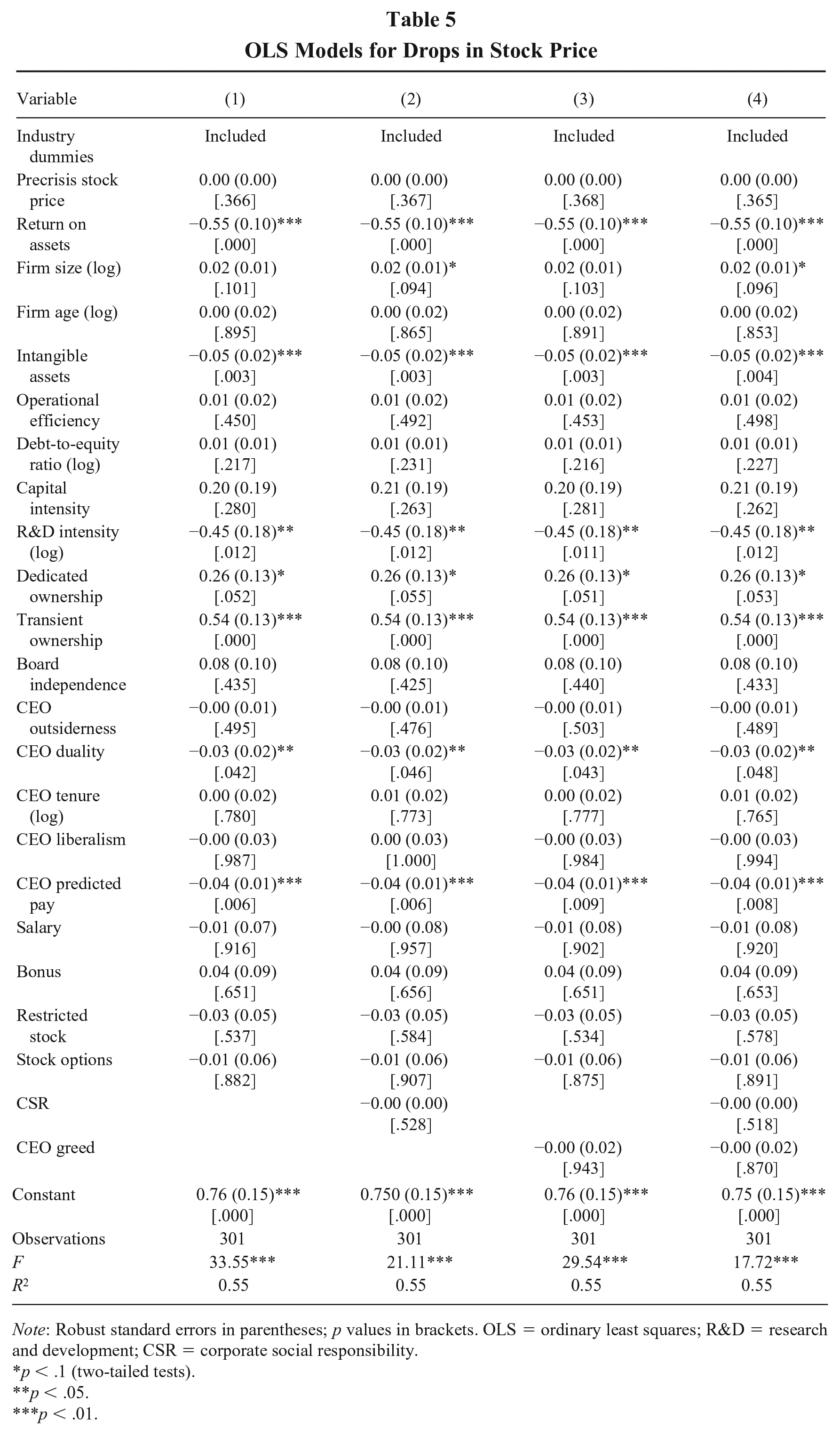

The correlations and descriptive statistics are shown in Table 4. Table 5 reports the OLS regression results. Model 1 includes control variables only and indicates that firms with better performance (β = ‒0.55, p = .000), more intangible assets (β = ‒0.05, p = .003), higher R&D intensity (β = ‒0.45, p = .012), and CEO duality (β = ‒0.03, p = .042) prior to the shock experienced smaller drops. Surprisingly, both types of institutional ownership are associated with larger drops, although the effect of transient ownership (β = 0.54, p = .000) is roughly double the effect of dedicated ownership (β = 0.26, p = .052). Models 2 and 3 introduce preshock CSR and preshock CEO greed, respectively. Model 4 contains all variables. Overall, we find no support for Hypotheses 3a and 3b, suggesting that preshock CSR and greed did not affect the drops in stock price immediately after the 2008 GFC.

Descriptive Statistics and Correlations (Empirics Part 2)

N = 301. R&D = research and development; CSR = corporate social responsibility. Correlations at r > .12 are significant at p < .05.

OLS Models for Drops in Stock Price

Note: Robust standard errors in parentheses; p values in brackets. OLS = ordinary least squares; R&D = research and development; CSR = corporate social responsibility.

p < .1 (two-tailed tests).

p < .05.

p < .01.

Robustness checks

To assess whether the results are sensitive to the temporal measurement of preshock features, we ran several analyses where all the explanatory variables were measured either only in 2008 or only in 2007 or as the average value during 2006 and 2007. The results remained consistent. Next, we specified a model that did not include preshock stock price, but excluding this covariate did not affect our findings. We also explored different operationalizations of preshock CSR. CSR scholarship often makes a distinction between CSR strengths and concerns (Mattingly, 2017) or between strategic and tactical CSR (Bansal, Jiang, & Jung, 2015). For instance, DesJardine et al. (2019) find that strategic CSR, which involves significant resource commitments, provides greater benefits for organizational resilience in comparison to tactical CSR, which can be implemented relatively quickly. The additional analyses reconfirmed no association between any of these CSR operationalizations and drops in firms’ stock prices. Researchers also increasingly explore the impact of individual stakeholder dimensions (e.g., employee relations) on organizational outcomes (Wang et al., 2016). We documented a negative and significant effect of diversity on drop in stock price (β = ‒0.02, p = .030). In practical terms, a one-SD increase in firm diversity initiatives results in a 15.8% SD decrease in stock price. All robustness analyses are available upon request.

Empirics Part 3: Explaining Postshock Flexibility

Method

Dependent variable

To test Hypotheses 4a and 4b, we examined the amount of time it took firms’ monthly closing stock price to fully recover to preshock (i.e., September 16, 2008) levels after the GFC (DesJardine et al., 2019). The dependent variable is the hazard rate, representing the probability that a firm recovers at time t. To allow for sufficient recovery times, the observation period spanned a 36-month window (September 2008 to September 2011).

Independent variable

The independent variables, CSR and CEO greed, are both operationalized as earlier. In line with Part 2, CSR and CEO greed are measured prior to the systemic shock. We again took the average value of the 2007-to-2008 period to make sure we do not just capture a snapshot of preshock CSR and CEO greed.

Control variables

We include three sets of control variables. First, to account for starting conditions (i.e., 2007-2008 CEO or firm average tendencies), we include all control variables already employed in Part 2. Second, we control for changes in several key firm variables: growth in ROA, growth in firm size, and growth in intangible assets. These are time-varying covariates, measured as the difference between firms’ contemporaneous value and that in 2008 (e.g., in 2010, growth in ROA is measured as ROA2010 – ROA2008). Third, because some of the firms in our sample experienced CEO turnover prior to recovery, we excluded those firms from the sample to ensure that we tracked the same population of CEOs across all analyses. (Note that we include firms with CEO turnover in one of our robustness checks.) This implies that the resulting sample might be biased toward certain types of CEOs who are less likely to exit during recovery, which might also affect organizational resilience. To control for such potential bias, we employ Heckman’s (1979) two-stage selection model. In the first-stage probit model (Table E in the online supplement), we use preshock firm and CEO features (i.e., 2007-2008 CEO or firm average tendencies) to predict the likelihood of CEO turnover in the postshock recovery period. After consulting the literature on CEO turnover (e.g., Flickinger, Wrage, Tuschke, & Bresser, 2016; Hubbard, Christensen, & Graffin, 2017), we included the following explanatory variables: transient ownership, dedicated ownership, firm size (logged), ROA, intangible assets, CSR, CEO tenure (logged), CEO duality, CEO outsiderness, CEO liberalism, CEO age, and CEO greed (all measures are based on the total sample, including CEOs that left in the postshock period). We used the predicted scores to calculate the inverse Mills ratio, which we then used in the regressions to control for sample selection.

Estimation

To estimate how preshock CSR and CEO greed impact firms’ recovery times, we specified Cox proportional hazard models. A positive coefficient on a covariate in the survival model indicates a higher probability of a faster recovery, hence pointing to a contribution of the covariate toward greater firm flexibility. Survival analysis is suitable for our data, as it can accommodate right censoring and skewness of survival data (DesJardine et al., 2019). During the observation period, 37 sample firms did not recover from the systemic shock, while none failed. The spells in our survival models were defined at the monthly level. The origin was September 2008, and we continued to observe the firm until it either fully recovered or until the end of the observation period. We specified robust standard errors.

Results

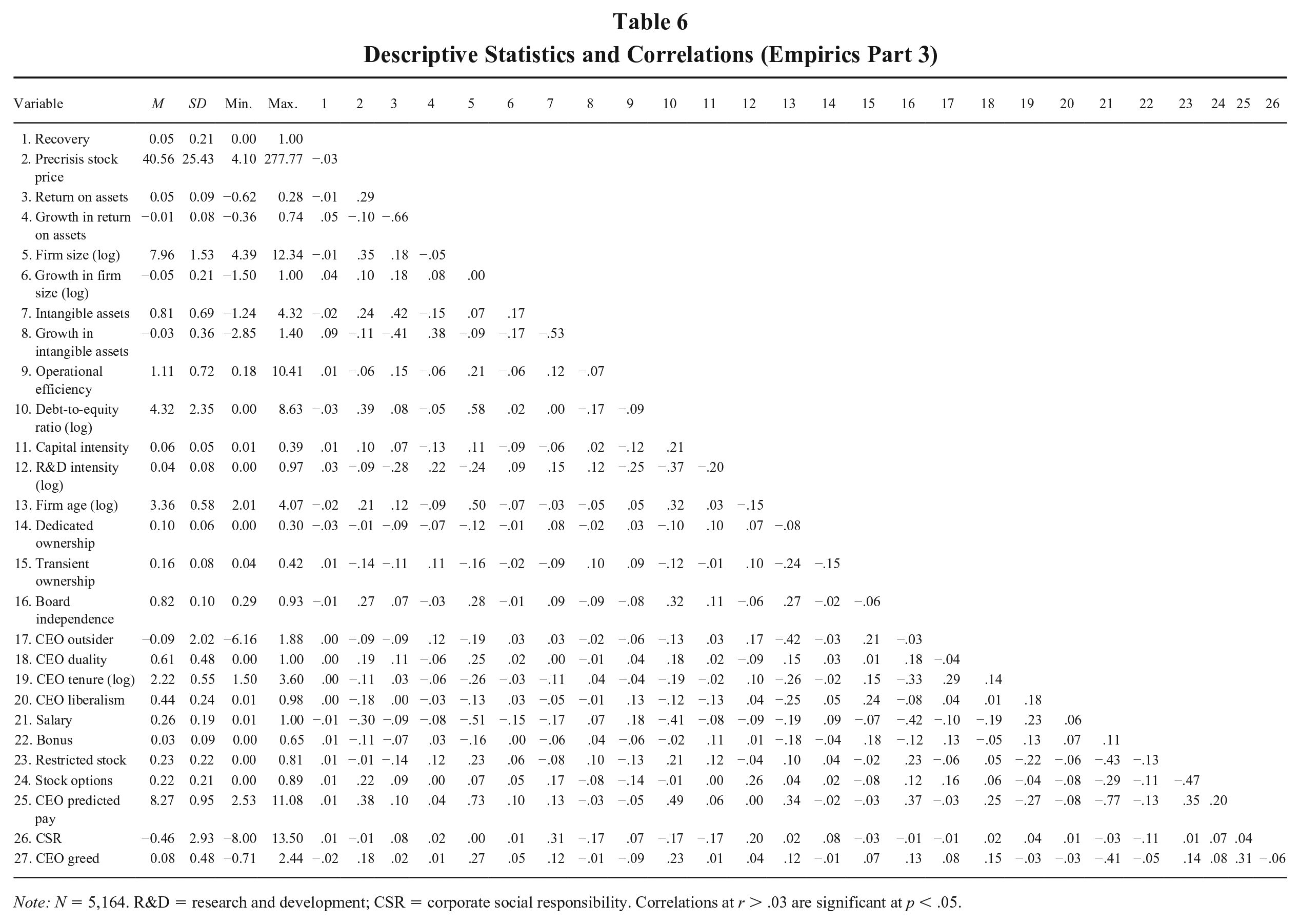

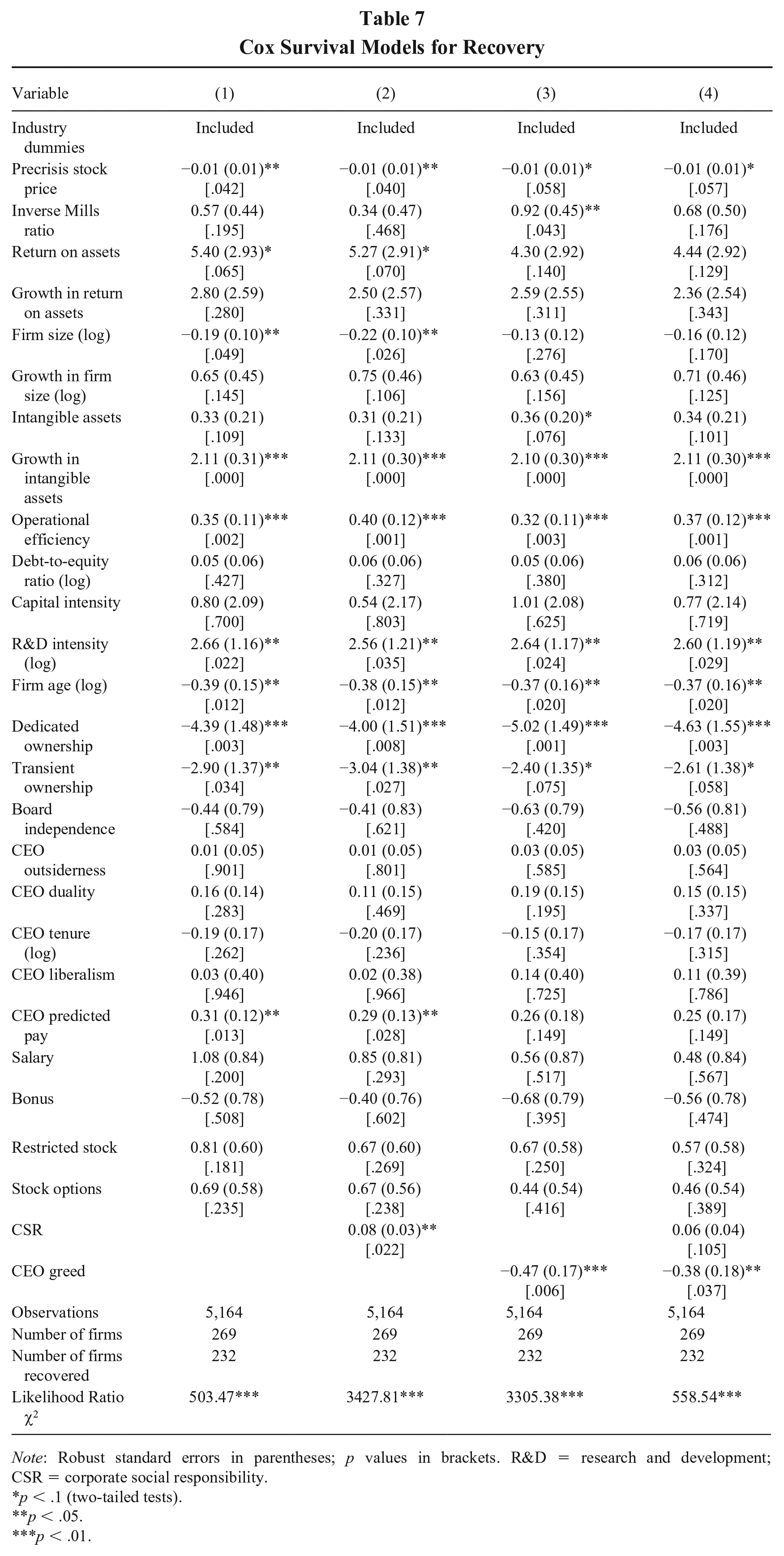

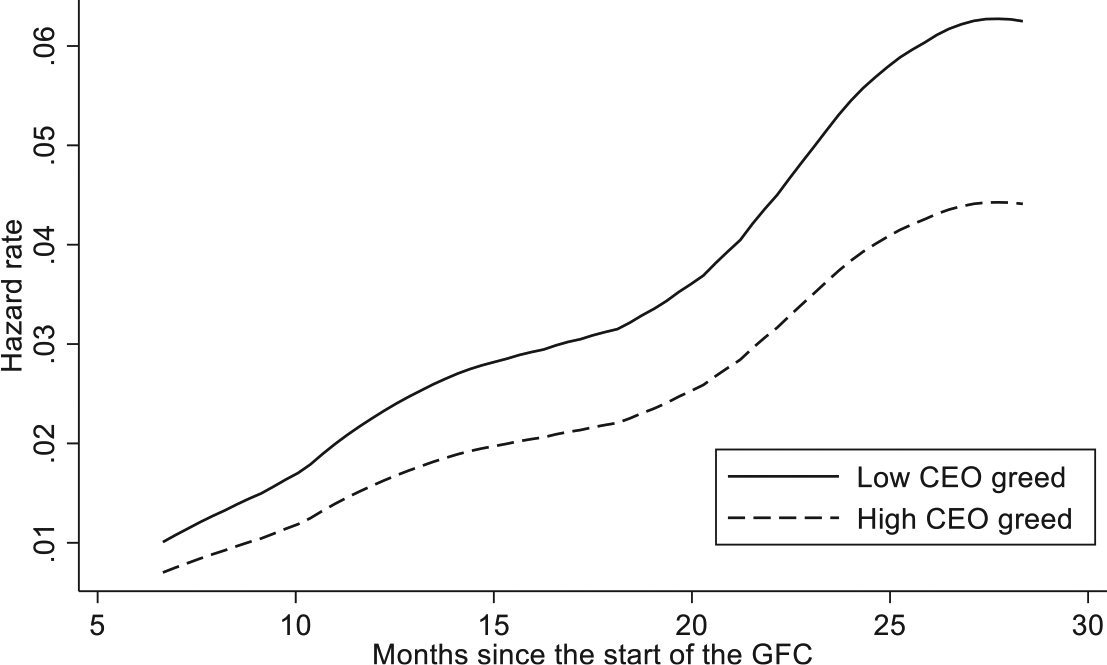

The correlations and descriptive statistics are shown in Table 6. Table 7 displays the results for our survival analysis. Model 1 includes control variables only and indicates that firms with better performance (β = 5.40, p = .065), greater growth in intangible assets (β = 2.11, p = .000), better operational efficiency (β = 0.35, p = .002), higher R&D intensity (β = 2.66, p = .022), and higher predicted CEO pay (β = 0.31, p = .013) are more likely to recover. By contrast, firms that were valued highly prior to the GFC (β = ‒0.01, p = .042), that are larger (β = ‒0.19, p = .049), and that are older (β = ‒0.39, p = .012) are associated with a diminished likelihood of recovery. Consistent with Part 2, both types of institutional ownership negatively contribute to resilience, with dedicated ownership (β = ‒4.39, p = .003) having a stronger effect compared to transient ownership (β = ‒2.90, p = .034). In Model 2, we find that firms with higher preshock CSR engagement are significantly more likely to recover faster (β = 0.08, p = .022), thereby providing support for Hypothesis 4a. This means that a one-SD increase in preshock CSR initiatives results in a 24.6% increase in probability of recovery. 13 In Model 3, we find support for Hypothesis 4b. The coefficient of CEO greed is negative and significant (β = ‒0.47, p = .006), which relates to a drop in the recovery rate of 20.2% as a function of a one-SD increase in preshock CEO greed. This relationship is illustrated in Figure 4, which shows that the conditional probability that a firm will recover at time t given that it has not recovered before (i.e., the hazard rate) is higher for firms that are led by less greedy (i.e., mean − 1 SD) compared to greedier (i.e., mean + 1 SD) CEOs. Model 4, in which we include all variables, yields additional support for the pattern of our findings. Interestingly, controlling for preshock CSR results in a 16.7% decrease in the negative impact of CEO greed on the recovery rate (β = ‒0.38, p = .037), a pattern that suggests partial mediation. 14

Descriptive Statistics and Correlations (Empirics Part 3)

Note: N = 5,164. R&D = research and development; CSR = corporate social responsibility. Correlations at r > .03 are significant at p < .05.

Cox Survival Models for Recovery

Note: Robust standard errors in parentheses; p values in brackets. R&D = research and development; CSR = corporate social responsibility.

p < .1 (two-tailed tests).

p < .05.

p < .01.

The Effect of CEO Greed on Firm’s Recovery to Pre–Global Financial Crisis Stock Price Level

Robustness checks

We did several tests to assess the robustness of our findings. First, in a postestimation analysis, we investigated whether the effects of the explanatory variables are proportional over time, because Cox proportional hazard models are based on the key assumption that the relationship between predictors and time to recovery is not a function of time. The test of the proportional hazards assumption on the basis of Schoenfeld residuals failed to reject the null hypothesis, suggesting that time-dependent effects were not likely to have affected our results. Second, we estimated Cox proportional hazard models with shared frailty. Shared-frailty models are the survival-data analog to random-effects models. A frailty is a latent random effect that is used to model within-group correlation, thereby accounting for unobserved group heterogeneity. Our findings remained the same after the specification of shared frailty. Third, we also lengthened the observation period to a 5-year window and found no significant changes in our results. All analyses are available upon request.

Finally, we redid the analyses, this time including the set of firms with CEO turnover during the recovery period. We replaced the control for sample selection with a dummy variable that equals 1 if the firm experienced CEO turnover during our observation window. We labeled this variable “CEO turnover.” The results of these analyses are shown in Table F in the online supplement. We document a positive but insignificant effect of preshock CSR on recovery time (β = 0.04, p = .190), thereby failing to provide additional support for Hypothesis 4a. However, we reaffirm our prior finding that preshock CEO greed is negatively associated with time to recovery, with a negative and significant coefficient (β = ‒0.33, p = .049).

Discussion

Why do firms differ so much in their ability to overcome adversity, and what are the antecedents of this heterogeneity? To answer these questions, we integrated literatures on UE, CSR, and organizational resilience to theorize and test how CEO greed affects firms’ capacity to absorb and recover from systemic shocks. In line with our expectations that greedy CEOs exhibit a diminished concern for the welfare of their firms’ stakeholders and tend to forgo long-term investments that require short-term financial sacrifices, we found a negative association between CEO greed and CSR. Moreover, we combined agency theory’s insight that monetary incentives steer CEO behavior (Eisenhardt, 1989) with the person-pay interactionist logic (Wowak & Hambrick, 2010) and found that especially greedy CEOs are more likely to neglect stakeholder concerns when their pay heavily depends on annual bonuses. This finding suggests that because bonuses reward CEOs for the firm’s short-term financial success (Hou et al., 2013), CEOs with a strong desire for the accumulation of personal wealth are particularly more likely to tone down long-term investments, such as CSR, when they are rewarded with bonuses. However, while we consistently find a positive direct effect of restricted stock on CSR, we document no evidence of an interaction between CEO greed and such long-term monetary incentives. A possible explanation could be that although greedy CEOs might be more responsive to pay arrangements that entail a long-term focus compared to their less greedy peers, this may manifest itself in the adoption of long-term strategies other than CSR, such as R&D investments or capital expenditures (Flammer & Ioannou, 2018).

We additionally found that the stock prices of firms with strong stakeholder relations (high CSR) were associated with higher recovery rates following the 2008 GFC, whereas firms led by greedy CEOs were less likely to bounce back from the economic shock. This result corroborates the view that investment in CSR contributes to organizational flexibility due to its positive effect on stakeholder motivations and the increased knowledge diversity that stems from interdependencies between the firm and its social and natural environment (DesJardine et al., 2019; Ortiz-de-Mandojana & Bansal, 2016). To explain the negative impact of CEO greed on recovery rates, we argued that greedy leaders shape individualistic organizations where subordinates are also inspired to free-ride (Haynes, Josefy, et al., 2015). Because the resulting increase in agency costs across the entire organization leads to resource depletion, these firms exhibit a diminished ability to recover from adversity (Sutcliffe & Vogus, 2003).

Contrary to our predictions, we found no evidence of an effect of CSR or CEO greed on the drop in stock prices immediately after the 2008 GFC. When we unpack CSR and assess the impact of individual stakeholder dimensions on firm stability, we do find that firms with strong diversity practices are associated with smaller drops. This result partially aligns with DesJardine et al. (2019), who documented a positive effect of strategic CSR on firms’ ability to absorb systemic shocks. 15 However, when we examine the impact of strategic CSR on firm stability, we fail to fully replicate their results. While we remain agnostic about this discrepancy, it is important to note that their sample is roughly 3 times the size of ours. Hence, a plausible explanation might be that the authors were better able to detect relationships between variables, because the precision of estimates increases with sample size (Wooldridge, 2013). A more theoretically driven explanation for not finding an effect might be that the sudden economic collapse may have been so grave that it rendered the impact of heterogeneity in executive motives and stakeholder engagement immaterial (Buyl et al., 2019). For instance, even if the CEO has good relations with the firm’s stakeholders, when the purchasing power of customers and other businesses in the supply chain suddenly takes a drastic hit, nothing can save the firm from a sharp drop in its stock price. Moreover, in such times of crisis, stock markets are driven not necessarily by economic fundamentals or rationality but rather by emotions and herd-following behavior. By contrast, the lingering effects of CEO motives and good stakeholder relations might become perceptible in the long run, for example, through different recovery rates. For instance, strong collaborations with employees and other stakeholders may help to bounce back faster, for example, by introducing innovative solutions or by increasing the willingness to make sacrifices.

Contributions

Most broadly, we contribute to the research on the drivers of executive behavior. The fast pace at which this field is progressing has led to a proliferation of diverse explanatory constructs and increasing fragmentation (Wowak et al., 2017). We add to this literature by demonstrating how the concept of CEO greed can be utilized as a characteristic that facilitates the synthesis of different disciplinary perspectives on executive behavior—for example, the UE perspective and agency theory. Because greed has long been a major subject of economic, psychological, political, ethical, and philosophical literatures (Wang & Murnighan, 2011), it represents a core personal motive that can help scholars to build richer models that bridge theoretical silos.

Next, we extend the literature that explores how strong stakeholder relations contribute to organizational resilience (DesJardine et al., 2019; Flammer & Ioannou, 2018; Ortiz-de-Mandojana & Bansal, 2016). These studies have shown, for example, that investment in CSR fosters employees’ motivations, engagement, and commitment while mitigating adverse behaviors, such as shirking and absenteeism (Flammer & Luo, 2017). All of these behaviors, whether they are positive or negative, have profound consequences for organizational resilience in times of crisis. Although this research has made great strides in understanding the link between CSR and organizational resilience, it has stopped short of examining the sources of the immense heterogeneity in CSR practices. By building on the UE perspective to argue that firm CSR practices reflect executives’ motives (Hambrick & Mason, 1984), we add to this literature by proposing that CEOs play a central role in shaping organizational resilience.

Finally, our work complements UE research that focuses on the role of CEO characteristics in organizational resilience (Buyl et al., 2019; Patel & Cooper, 2014). These studies have relied on the concept of CEO narcissism to explain firms’ capacity to endure and bounce back from systemic shocks. Because narcissistic CEOs are more prone to adopt risk-taking strategies due to their strong desire to inspire awe (Wales, Patel, & Lumpkin, 2013), they may endanger their firms’ long-run fate (Buyl et al., 2019). We contribute by showing that greed is an important characteristic for understanding how CEOs impact organizational resilience in ways other than risk taking—that is, due to their excessive focus on current earnings, greedy executives build firms with weak stakeholder support and individualistic cultures.

Our results also reveal important implications for practice. Whereas Haynes et al. (2017) previously described the harmful effects of executive greed for shareholders, we extend this observation to the whole set of firms’ stakeholders by showing that greedy CEOs invest less in CSR—especially when they are heavily incentivized with bonuses—and jeopardize firms’ resilience to systemic shocks. Restraining such behavior is relevant for society at large, as firms’ survival and continuity affects societal welfare (Sutcliffe & Vogus, 2003). Moreover, our findings suggest that greedy CEOs’ selfish behaviors cannot even be curbed with what—at least according to agency theory—should motivate them the most: long-term incentives.

Nevertheless, an important message for boards and compensation committees is to be cautious in negotiating and designing executive compensation arrangements. They should ensure that CEOs receive “fair” compensation, and they should avoid the combination of (relative) overcompensation with high bonuses. High levels of CEO compensation are probably unavoidable nowadays (and, fortunately, they are not always driven by unbridled greed), but boards can at least attempt to safeguard stakeholders’ interests by avoiding the combination of exceptionally high compensation, perks, and (short-term-oriented) bonuses.

Limitations and Future Research

Our study is not without limitations. Several of these are related to our measurement of CEO greed. First, although we conducted several robustness checks to address endogeneity concerns, we did not control for other CEO features that have been linked to CSR in prior studies—narcissism (Petrenko et al., 2016) and hubris (Tang et al., 2015), for instance—due to the labor-intensive data collection efforts that doing so would have required. We have argued that CEO greed is sufficiently distinct from CEO narcissism, especially in the context of CSR, where the two explanatory constructs are expected to lead to opposite firm outcomes. Additionally, Haynes et al. (2017) have empirically shown that CEO greed is distinct from CEO hubris. Nonetheless, future studies may want to control for a greater number of constructs when studying CEOs’ impact on long-run firm outcomes to better account for other reasonable alternative explanations.

Second, along the same lines, CEO greed (in terms of abnormally high compensation) might be the result of CEOs’ power, managerial discretion, or human and social capital, implying that these features might have driven our results. Though we included several control variables to account for such alternative explanations in the main analyses (e.g., tenure, duality, outsiderness) and robustness checks (e.g., MBA, elite college), future researchers might undertake efforts to more directly discern CEO greed from these features. Finally, we defined and measured “executive greed” at the CEO level. Given Hambrick and Mason’s (1984) call to study the characteristics of the whole dominant coalition, it would be fascinating to explore executive greed at the TMT level and study, for example, how the effects of CEO greed might be curbed or exacerbated by the greed levels of other executives.

To explain the lack of support for our prediction that restricted stocks attenuate the negative impact of CEO greed on CSR, we proposed that long-term incentives might spur greedy CEOs to commit to long-term investments other than CSR. If one were to extend this idea, it could emerge that we failed to detect the interaction effect because restricted stocks do not tie a CEO’s wealth directly to stakeholder engagement. In contrast, CSR contracting is a recent corporate governance innovation that aims to integrate CSR targets (e.g., CO2 emissions) into executive pay (Flammer et al., 2019). Given the dramatic increase in CSR contracting in recent years (Flammer et al., 2019), future scholars may want to study whether CSR contracting is effective at curbing the potentially detrimental effects of CEO greed.

Although our findings suggest a partial mediation effect of CEO greed on firm flexibility via CSR, we also document a robust direct negative effect of preshock CEO greed on recovery after the 2008 GFC. Our rationale was that by engaging in selfish behavior, greedy leaders foster a culture of greed. Because such firms may exhibit exacerbated agency costs and experience resource depletion across the entire firm, they are less able to bounce back from adversity. However, a potential concern is that we did not directly explore these mediating mechanisms, and this limits our causal account. Nevertheless, the robustness and the size of the effect highly warrant further investigation and present ample opportunities for future work.

Finally, despite the fact that even critics of the efficient-market hypothesis accept the idea that stock prices reflect all relevant information about the firm, our exclusive reliance on stock price data to gauge organizational resilience might limit the generalizability of our findings. Hence, we encourage future scholars to examine different ways of operationalizing organizational resilience. This could include not only measurement of different types of firm outcomes, such as the reliability of firm performance (Sørensen, 2002) or long-term sales growth (Ortiz-de-Mandojana & Bansal, 2016), but also examination of different types of shocks—for instance, natural disasters, such as Hurricane Katrina (Muller & Kräussl, 2011).

Conclusion