Abstract

Over the past years, media coverage of firms has received significant scholarly attention. However, the resulting literature is spread across multiple disciplines and, therefore, varies with regard to its theoretical underpinnings and contextual settings. This makes it challenging for scholars to understand the contributions of this literature, to identify areas of inquiry, and to develop an encompassing research agenda. In this review, we address these issues by surveying the diverse literature on media coverage of firms to develop an integrative framework of the antecedents and consequences of media coverage that highlights paths for future research. Specifically, we identify the three theoretical perspectives—economic, institutional, and social-psychological—that the literature generally assumes on the news media. In addition, we highlight differences between strategy, finance, governance, and crisis contexts and review results from articles examining media coverage of firms in aggregate. In each context, we identify the primary functions of the news media as well as antecedents and consequences of media coverage. We proceed to develop an integrative framework for media coverage of firms by building on these findings and by examining the empirical methods used to measure media coverage, particularly regarding the measurement of specific coverage attributes. We highlight the gaps in current knowledge that our framework exposes and derive opportunities for future research that can further scholars’ and practitioners’ understanding of firm media coverage.

News media coverage of firms is ubiquitous. Whether in newspapers or magazines, online or on television, or in general or specialist publications, reporting on firms permeates most aspects of public, corporate, and private life (Dyck & Zingales, 2002). More importantly, as a result of the opaqueness of the inner workings of a firm to most outsiders, media coverage is often the main legitimate source for reducing information asymmetries about a firm’s actions (Deephouse, 2000). It is therefore not surprising that media coverage of firms has received significant scholarly attention in recent years. This scholarship provides substantial evidence that media coverage constitutes an important strategic asset (Deephouse, 2000) that can significantly affect the performance and valuation of firms (Ahern & Sosyura, 2014; Rogers, Skinner, & Zechman, 2016), as well as decisions regarding the allocation of resources (Desai, 2014), investors’ trading patterns (L. X. Liu, Sherman, & Zhang, 2014; Pollock & Rindova, 2003), and customers’ purchasing behavior (Berger, Sorensen, & Rasmussen, 2010; Stephen & Galak, 2012).

However, research on media coverage of firms is spread across business disciplines, including management (e.g., Bundy & Pfarrer, 2015; Graffin, Bundy, Porac, Wade, & Quinn, 2013; König, Mammen, Luger, Fehn, & Enders, 2018; Pollock & Rindova, 2003; Westphal, Park, McDonald, & Hayward, 2012), finance (e.g., Dyck, Morese, & Zingales, 2010; Dyck, Volchkova, & Zingales, 2008; Engelberg & Parsons, 2011), accounting (e.g., Kothari, Li, & Short, 2009; Robinson, Xue, & Yu, 2011), and marketing (e.g., Chen, Liu, & Zhang, 2011; Rinallo & Basuroy, 2009). Such fragmentation (Carroll & Deephouse, 2014) has resulted in a diversity of theoretical frames, settings, and empirical methods. As a result, a disparate body of research has emerged, and while certain aspects have been addressed by numerous scholars, such as the effect of news media coverage on CEO pay (e.g., Core, Guay, & Larcker, 2008; Kang & Kim, 2017), investor composition (e.g., Barber & Odean, 2008; Kalay, 2015), and stock market–related variables (e.g., Peress, 2014; Tetlock, 2007, 2011), most research is relatively insular and only loosely tied together, leaving management scholars and practitioners with a patchy understanding of the media coverage of firms.

Surprisingly, an in-depth review of this important but dispersed literature does not exist to date for management audiences. While consequential and well-cited reviews of various aspects of media coverage exist across disciplines such as sociology (Shoemaker and Reese’s, 2013, hierarchical model of influences on mass media), communications (McCombs, Shaw, and Weaver’s, 2013, review of the agenda-setting nature of media coverage), and journalism (Schudson’s, 2003, sociology of news), they do not adopt a focus on firms—or more specifically, on how firms influence their coverage and how media coverage influences their actions. To remedy this issue, management scholars have begun to review the general attributes of firm-specific media coverage (Carroll & Deephouse, 2014) and how media coverage influences specific constructs, such as firm reputation (Mariconda & Lurati, 2014). However, these reviews are far from comprehensive, focusing on only one or a few elements of firm media coverage. With our review, we aim to broaden the scope and provide a management-centric but interdisciplinary overview of research on media coverage of firms. In doing so, we seek to answer three interrelated questions: (1) Which theoretical lenses are applied to the news media in management and allied disciplines? (2) What are the primary functions of the news media, what are the antecedents and consequences of media coverage of firms, and what is the role of contextual influences highlighted by extant research? and (3) What are fruitful avenues for future research?

In an effort to answer these theoretical and empirical questions, we reviewed an extensive set of business-related peer-reviewed journals from the past 20 years with the aim of constructing an integrative framework of media coverage that can be used to shape future cross-disciplinary inquiries and advance scholars’ and practitioners’ understanding of firm media coverage and its impact on the management of firms. By providing a comprehensive account of this diverse and dispersed body of literature with regard to theoretical approaches, as well as context-specific perspectives on antecedents, attributes, and consequences of news media coverage of firms, we offer a holistic overview of the knowledge to date. Also, by highlighting methodological issues in the extant literature that limit the comparability and generalizability of empirical results and by offering potential remedies, we enable improvements to the theoretical and empirical quality of future research. Finally, by identifying promising directions for future research, we support researchers in contributing to the further development of this still-young field.

Scope and Methodology of the Review

Identification of the Relevant Literature

Following established procedures in the field (Fink, 2013; Short, 2009; Tranfield, Denyer, & Smart, 2003), we approached this review by defining a clear scope that is relevant to management scholars before conducting a systematic search across a comprehensive number of sources pertaining to the media coverage of firms. In defining our scope, we first focus on media coverage issued by professional news organizations, such as newspapers, magazines, online news platforms, or television channels. We exclude accounts published on other platforms, such as social media, where coverage is not exclusively generated by professional news workers. Second, we only investigate coverage of firms, that is, corporate organizations and their agents. Third, we are interested in earned media coverage and therefore exclude studies that focus solely on paid media content, such as advertising. While relaxing any of these boundaries would likely provide interesting insights, such an expansion of scope would mean a substantial trade-off with the depth of engagement with the specific drivers, attributes, and influences of media coverage of firms.

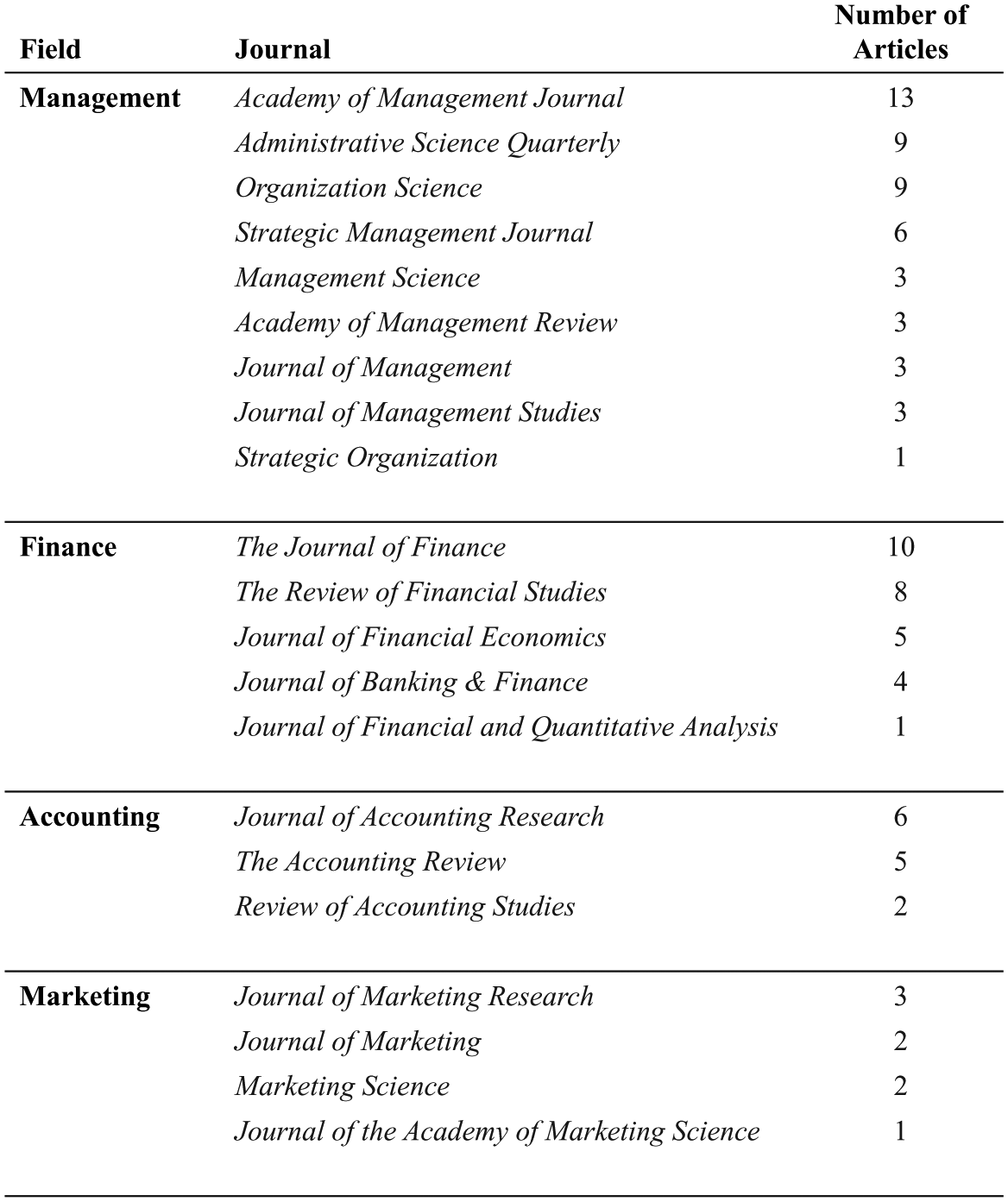

Following Short’s (2009) advice, we took a broad approach and selected a particularly extensive set of peer-reviewed journals. While we are cognizant that other disciplines such as communications, journalism, and public relations have provided valuable insights pertaining to firms and media coverage, we chose to narrow our selection of journals to those most relevant for the management community. As such, we focused on the top management journals and also expanded our focus to include other allied fields’ (organization, innovation and entrepreneurship, marketing, accounting, and finance) journals—in total, we considered 60 scientific journals, as listed in our online supplemental materials. 1 Furthermore, we limited our search to articles published over the past 20 years, that is, from 1997 to 2017. 2 Within the sample of journals, we conducted an abstract keyword search for variations of the words media, press, and journalist using the EBSCO database. We then screened the abstracts of the 911 identified papers and excluded all papers outside of the scope of this review and the inclusion criteria outlined above, which yielded a sample of 115 articles. We removed 35 more articles when full readings revealed that they did not match the research scope. Throughout the process, we identified an additional 57 promising articles through backward (searching references in the sample for relevant articles) and forward (investigating sources that cited the sample articles) snowballing search, 19 of which proved to be relevant after reading both the abstract and the full text. This way, we also included articles where media coverage was not the theorized variable (hence not referenced in the abstract) but was the empirical focus of the manuscript. In total, this procedure yielded a final sample of 99 peer-reviewed articles across four disciplines (21 journals) as depicted in Figure 1.

Distribution of Articles Across Disciplines

Classification of the Relevant Literature

Given the highly dispersed nature of the literature to date, we began our coding process by classifying the articles according to categories and concepts identified as relevant in the extant literature. First, focusing on one of the most comprehensive frameworks from the media literature, we used Shoemaker and Reese’s (2013) hierarchical model of influences on mass media to understand the antecedents of media content. 3 As such, we coded the articles on the basis of the antecedents of media coverage to isolate the characteristics of the media, the environment, and the organizations that drive coverage. Next, we coded articles on the basis of the only relevant framework specific to the management literature, Carroll and Deephouse’s (2014) organizational framework, which focuses on the attributes of media coverage, including the volume (amount of coverage), tone (expressed degree of support for a firm), topic (substantive content), and timing (sequential ordering) of coverage. During our coding, we realized that it would be helpful to consider three additional attributes of coverage, namely, language characteristics (e.g., linguistic tropes), the news segment (e.g., general newspapers vs. the financial press), and the regional scope of the coverage. Finally, we systematically coded all articles with regard to additional relevant categories, including the specific consequences of interest, descriptive information, underlying theoretical views of the news media, the contexts in which they examined the news media, the empirical results obtained, and the empirical methods applied to measure media coverage. Detailed results from this procedure can be found in our online supplemental materials.

Results

Descriptive Overview of the Relevant Literature

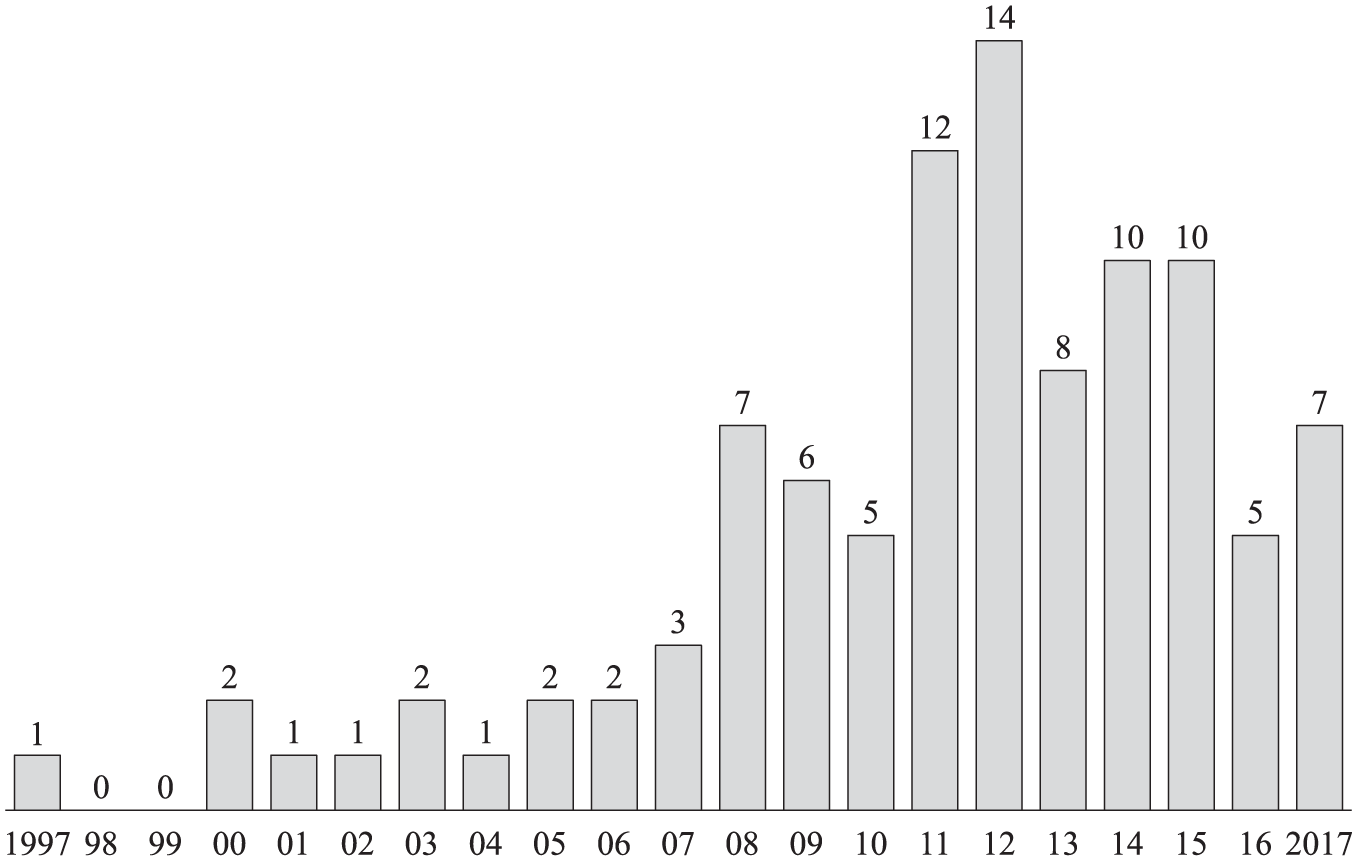

Figure 2 depicts the distribution of literature in the sample over time. A significant increase in scholarly attention to media coverage of firms over the past 10 years is immediately apparent. It is likely that the increasing accessibility of news media data through online databases, as well as the development of automated coding procedures (Loughran & McDonald, 2011; Pennebaker, Booth, & Francis, 2007), has contributed to researchers’ increased propensity to tackle the interesting research questions that can be answered by leveraging media reports. Overall though, it appears that now is an appropriate time to take stock of the literature to date. Below, we begin our review by identifying the dominant theoretical conceptualizations used in the literature. Then, drawing on the coding frameworks detailed above, we consider the varying contexts of coverage and the underlying functions, attributes, antecedents, and consequences of media coverage within each context. We end by integrating these varying perspectives into a comprehensive framework of media coverage of firms, and we detail future research opportunities from the framework.

Distribution of Articles Over Time

Theoretical Conceptualizations of the News Media

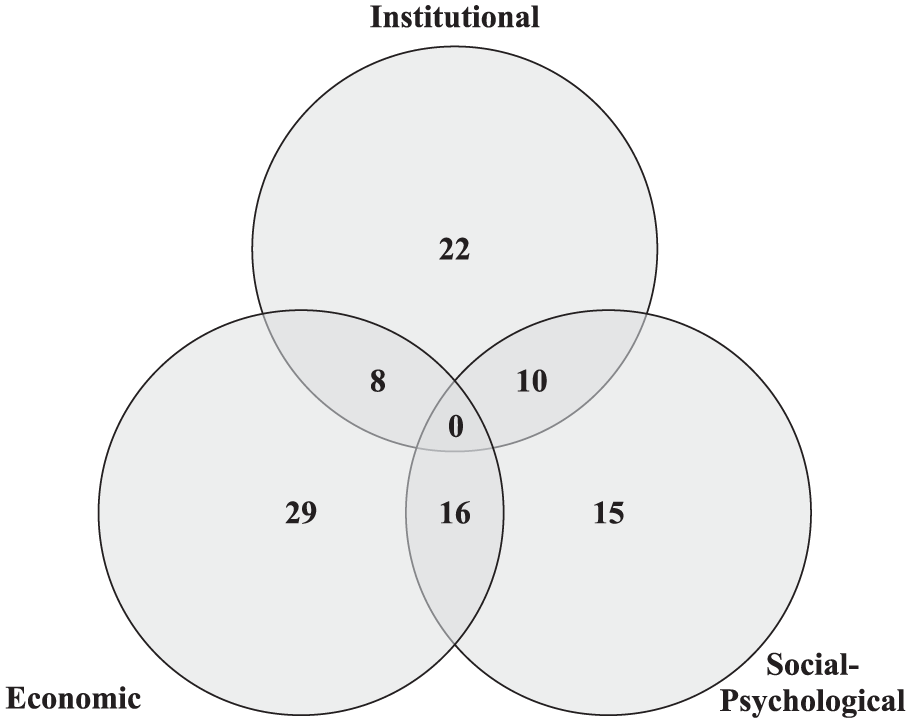

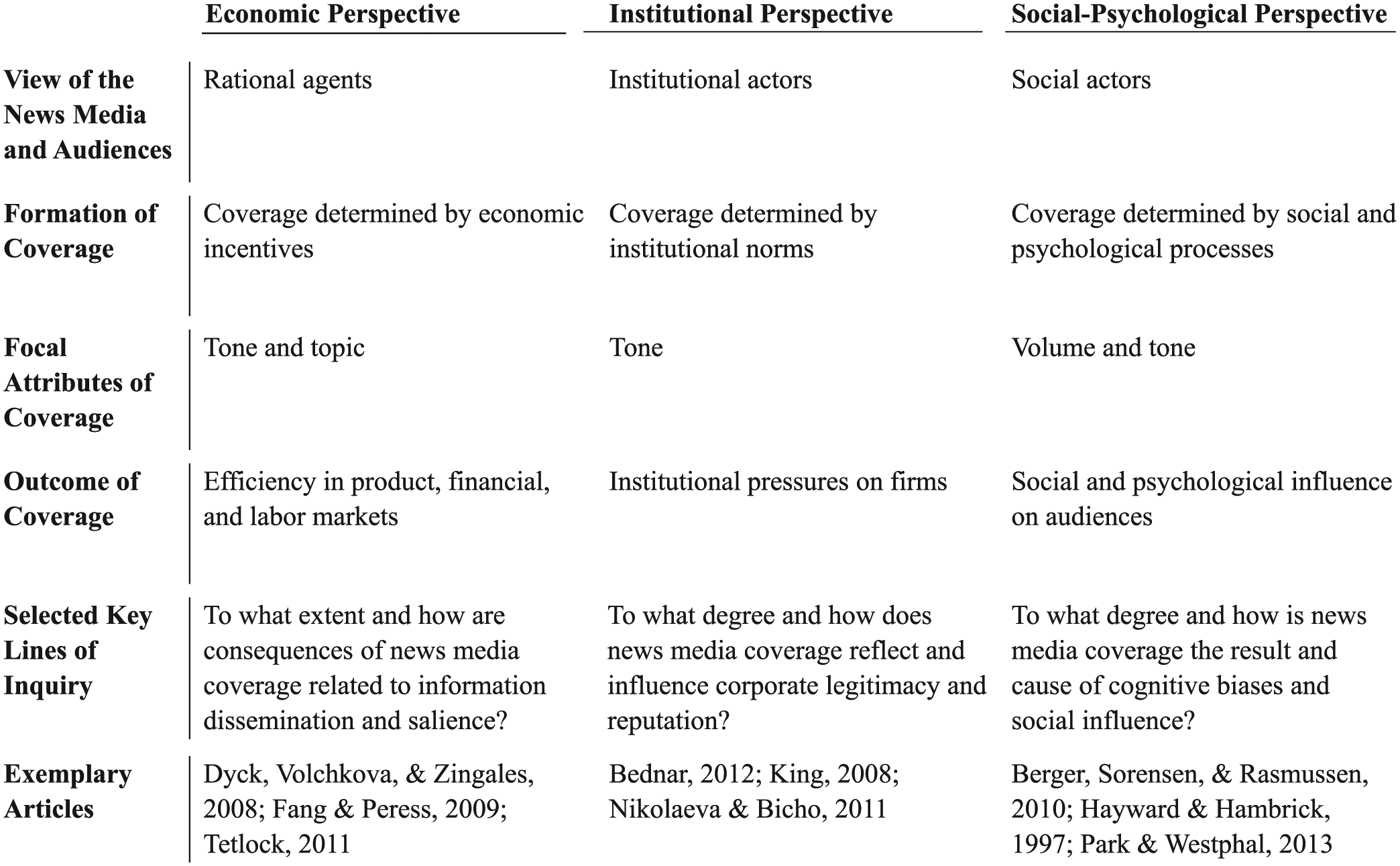

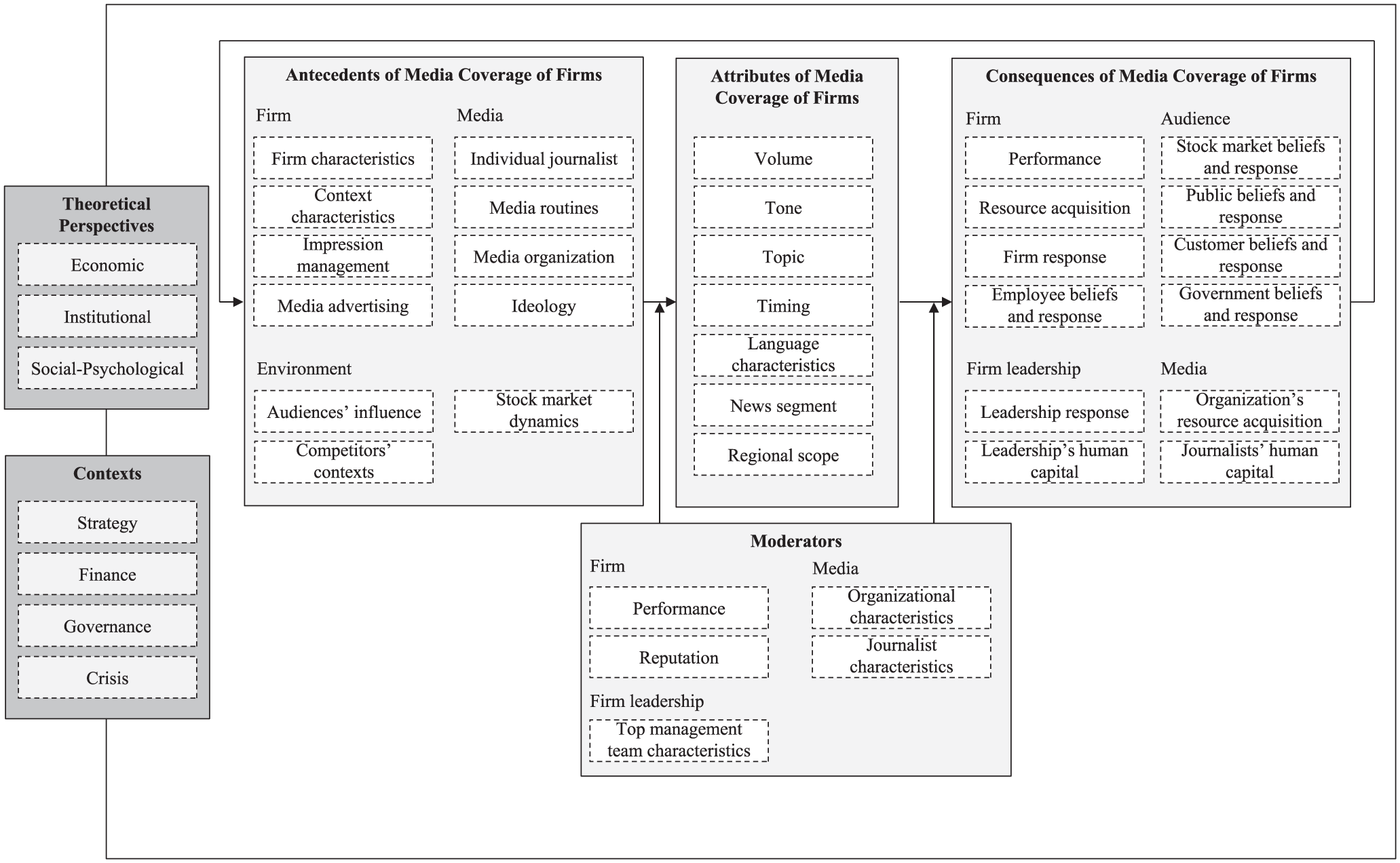

Given the discipline-spanning scope of this review and the dispersion of the literature across different fields, it is perhaps not surprising that the body of research on media coverage of firms rests on several different theoretical foundations. Indeed, we have uncovered three particularly prominent theoretical conceptualizations of the news media and their audiences among the sampled literature, namely, economic, institutional, and social-psychological. While in many ways not mutually exclusive—as demonstrated by numerous studies straddling different theoretical conceptualizations of the media (Ahluwalia, Burnkrant, & Unnava, 2000; Bednar, Boivie, & Prince, 2013; Core et al., 2008; Tetlock, Saar-Tsechansky, & Macskassy, 2008)—each of these perspectives focuses on distinct mechanisms through which media coverage is created and exerts influence. Each perspective also contains unique lines of inquiry. Therefore, the identified theoretical conceptualizations offer a useful means of structuring the diverse literature on media coverage of firms. An overview is provided in Figures 3 and 4.

Prevalence of Theoretical Perspectives on Media Coverage of Firms

Theoretical Perspectives on the News Media and Their Coverage of Firms

Economic Perspective

Scholars in the economic tradition generally see the news media as rational agents who engage in market transactions to maximize their own benefit and minimize cost (Houston, Lin, & Ma, 2011) and who perform a critical role in creating and disseminating information in markets (Drake, Guest, & Twedt, 2014; Dyck et al., 2008). Accordingly, this stream of research views the news media’s coverage of firms through the lens of economic incentives: the news media satisfy a demand for information and entertainment among their audiences and try to maximize their revenue by increasing readership and advertising income while controlling the cost of providing information (Core et al., 2008). Scholars in this stream view the news media as selecting those firms and events for coverage that they believe their audiences consider interesting in order to increase readership. Frequently, these firms are the ones that have been covered in the past, as they not only are familiar to audiences but also allow the media to leverage past reporting to economize on costs (D. Tan, 2016).

The economic perspective tends to focus on information dissemination as the news media’s primary role, especially in financial markets (L. X. Liu et al., 2014). As such, much of this research focuses on both the content and the tone of press coverage, assuming that these variables are proxies for fundamental firm information (Tetlock et al., 2008). Where biases in reporting by the news media are examined, these are explained by supply- or demand-side incentives, such as maintaining advertising revenues and access to information sources (Gurun & Butler, 2012). Most research from the economic perspective examines the effect that the news media’s coverage has on the efficiency of capital markets. For example, researchers have demonstrated that media coverage significantly influences stock prices (Griffin, Hirschey, & Kelly, 2011), stock turnover (Peress, 2014), and acquisition decisions (B. Liu & McConnell, 2013). However, effects other than those relating to financial markets, such as the influence of news media coverage on managers’ compensation, are also considered (Dyck et al., 2008).

In the economic tradition, two key lines of inquiry relate to potentially different reasons for why and how media coverage affects financial markets. On one hand, media coverage may make capital markets more efficient by reducing information asymmetries and increasing awareness of firms among stock market participants, as proposed by the information view (e.g., Bushee, Core, Guay, & Hamm, 2010; Fang & Peress, 2009). On the other hand, scholars adopting a salience view study how media coverage may lead to temporary overreactions in demand because it shifts investors’ attention to certain stocks (e.g., Joe, Louis, & Robinson, 2009; Tetlock, 2011). Both lines of inquiry have produced contrasting empirical evidence. In support of the information view, scholars have found that media-generated information has a lasting effect on stock returns (Bowen, Call, & Rajgopal, 2010) and that press coverage, in general, improves market liquidity (Bushee et al., 2010) and lowers the cost of capital for firms (Fang & Peress, 2009). Conversely, support for the salience view comes from evidence that individual investors overreact to media coverage of stocks; therefore, media-induced price changes tend to revert in the short term (Nocera, 2008; Tetlock, 2011).

Institutional Perspective

Scholars in the tradition of institutional theory emphasize the role of the news media as an important part of firms’ “institutional environment” (Nikolaeva & Bicho, 2011: 137). Scholars’ underlying assumption here is that “providing institutional and cultural accounts within which the appropriateness and desirability of actions can be evaluated . . . affects impression formation and the legitimation of firms” (Pollock & Rindova, 2003: 632). Moreover, these scholars assume that to arrive at their assessments of firms and firm actions, the media apply institutional logics held by their audiences (Bednar, 2012) and, thus, exert influential institutional pressures on firms (Bednar et al., 2013; Bitektine, 2011; Nikolaeva & Bicho, 2011).

Researchers in the institutional tradition frequently take a “macro” view in that they consider the news media as part of an institutional field of firm constituents for whom the media provide a stage for presenting their views on matters concerning a firm. Following Hilgartner and Bosk’s (1988) model of the media as an arena for public discourse where actors compete for attention, these researchers investigate how different constituents—and firms themselves—seek to exert influence over the media (Lamin & Zaheer, 2012; McDonnell & King, 2013). Given that the media are generally regarded as a credible source of information (Nikolaeva & Bicho, 2011), media coverage strongly influences how firm stakeholders view the firm (Pollock & Rindova, 2003) and, thus, constitutes an asset that can improve—or in the case of negative coverage, worsen—the performance of firms (Deephouse, 2000).

From an institutional perspective, particular attention is paid to the tone of media coverage and the degree to which it relates to certain social approval assets (Lange, Lee, & Dai, 2011). In fact, two key lines of inquiry within this stream of literature relate to how the news media passively “record” (Deephouse, 2000: 1094; Ferguson, Deephouse, & Ferguson, 2000) social approval (Bundy & Pfarrer, 2015) in the form of legitimacy, reputation, and/or celebrity (Lamin & Zaheer, 2012; Vanacker & Forbes, 2016; Zavyalova, Pfarrer, & Reger, 2017) and how they actively “influence” it (Deephouse, 2000: 1097; Durand & Vergne, 2015; McDonnell & King, 2013).

Social-Psychological Perspective

Scholars taking this perspective investigate media coverage of firms through more of a “micro” lens of individual social processes and cognition. In particular, they view journalists as individuals who are socially entrenched in a web of sources (Park & Westphal, 2013; Shani & Westphal, 2016), colleagues (Pollock, Rindova, & Maggitti, 2008), and audiences (Park & Westphal, 2013) who each exert influence on journalists’ coverage. In addition, scholars examine how media coverage is shaped by individuals’ cognitive constraints and biases—those of journalists themselves and those they anticipate in their audiences (Pollock et al., 2008; Westphal & Deephouse, 2011). Accordingly, these researchers tend to view media coverage as subjective or biased, reflecting social and cognitive influences on journalists, rather than representing objective reality (Bushee & Miller, 2012; Chatterjee & Hambrick, 2011).

Scholars taking a social-psychological vantage point tend to focus on both the volume and the tone of media coverage in their analysis (Core et al., 2008; Zavyalova, Pfarrer, Reger, & Shapiro, 2012), focusing their inquiry on the extent to which aforementioned social and cognitive influences shape coverage (Park & Westphal, 2013). Naturally, these scholars view the media’s audiences as influenced by both social and cognitive processes and point to related anomalies in the consequences of media coverage. For example, they find that customers may increase their purchases of a product even after negative reviews, because reviews move a product into a customer’s consideration set (Berger et al., 2010), and that auditors are biased towards putting excessive weight on media information when judging a company’s default risks (Joe, 2003).

Media Coverage in Context

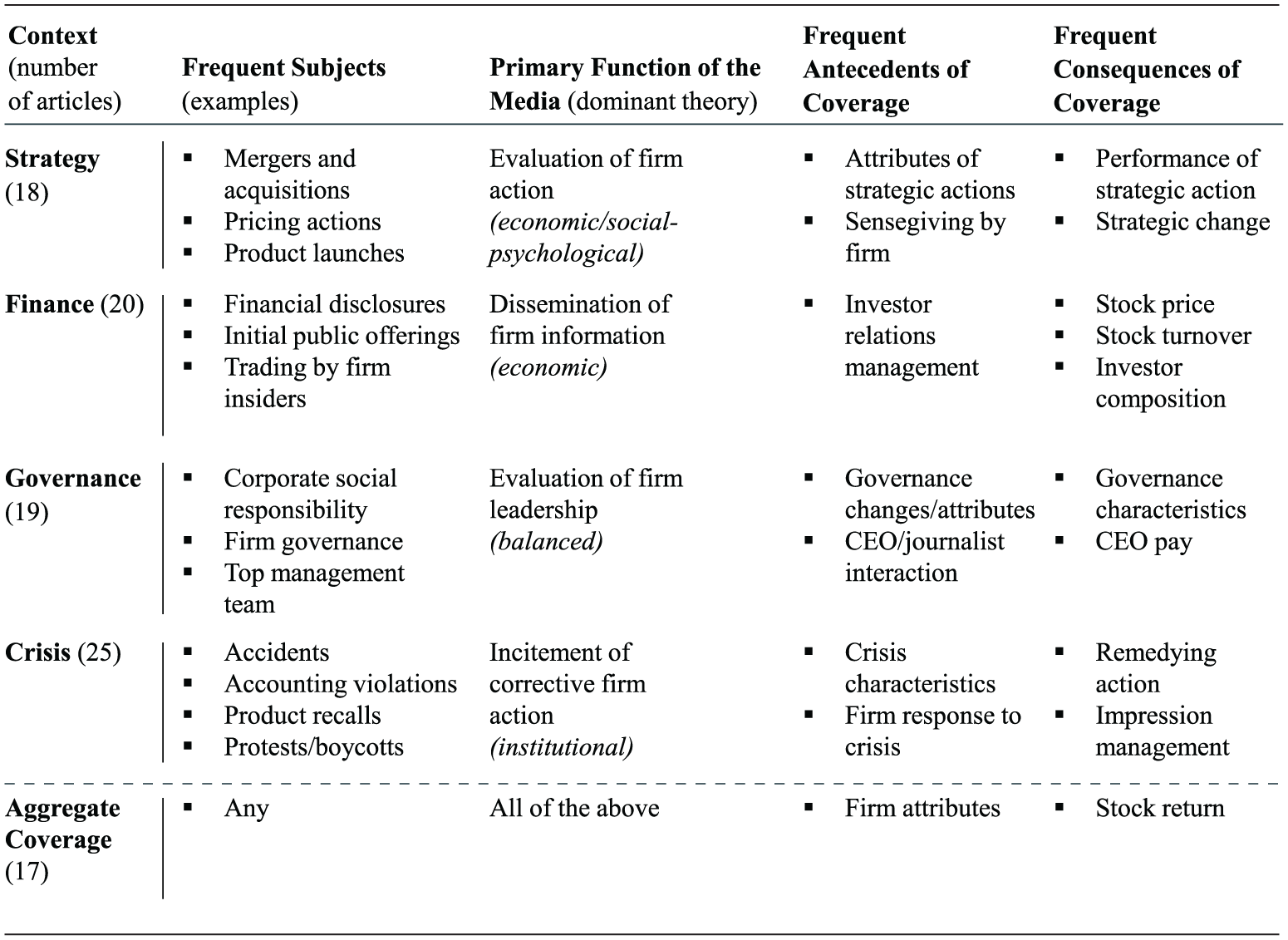

Apart from differences in the theoretical conceptualization of the news media, our review reveals the relevance of context in defining the primary functions of the news media and in describing the antecedents and consequences of media coverage. Context describes the circumstances that form the setting or environment in which coverage takes place. That is, context comprises the events, actions, and other elements that underlie the conditions in which the media coverage of firms occurs. In this way, context frequently, but not always, relates to what is covered by news media but may also describe an outcome or other critical element of coverage. Specifically, our review reveals four primary contexts: strategy, finance, governance, and crisis contexts. In addition, we found numerous studies examining contexts in aggregate or put simply, a firm’s media coverage across contexts. For each context, we identified (1) the primary functions ascribed to the media as informed by theoretical perspectives on media coverage of firms, (2) the antecedents of news media coverage, and (3) the consequences of news media coverage. Figure 5 presents a summary of our findings.

Description of Main Contexts of Media Coverage of Firms

Strategy Contexts

A recurring theme in media coverage of firms is focused on strategic actions taken by firms. Types of strategic actions that scholars have examined as contained in—or affected by—media coverage are strategic changes (Bednar et al., 2013); mergers, acquisitions, and other large investments (Ahern & Sosyura, 2014, 2015); product-related actions (Berger et al., 2010; Kaniel & Parham, 2017); pricing actions (Van Heerde, Gijsbrechts, & Pauwels, 2015); initiation of litigation against competitors (D. Tan, 2016); choice of exchange partners (Deephouse & Carter, 2005); and the establishment of new ventures or business units (Rindova, Petkova, & Kotha, 2007).

Primary function of the news media

Research on strategy contexts most often applies an economic or a social-psychological lens to the function of the news media as evaluating strategic initiatives. Taking product reviews by the media as an example of media coverage in strategy contexts, Kaniel and Parham evoke Merton (1987) in suggesting that “when search is costly, the mere appearance of a [product] in the media leads consumers to add the instrument to their limited consideration set” (2017: 338). Regarding the objectivity of these evaluations, Reuter and Zitzewitz argue that journalists are willing to accept low salaries because they “receive utility from providing a public good” (2006: 223) and that biasing evaluations of strategic actions towards advertisers would defeat this purpose, but they also acknowledge that this ethos is not upheld by all reporters. Others, however, stress social and cognitive influences on the media. For instance, Hayward and Hambrick emphasize a “striking propensity for the media to attribute organizational outcomes to individual leaders” (1997: 108) and a tendency to adhere to prior evaluations, even after performance diverges substantially.

Despite their differences, these perspectives share the view of the news media as an evaluator of firms’ actions. In choosing which actions to cover, the media simplify markets for their audiences and provide guidance regarding the quality of firms’ actions (Rinallo & Basuroy, 2009). Thus, the news media provide answers (or opinions) to address a variety of questions, such as Is an acquisition creating value? Is a firm’s strategic direction beneficial for external constituents? At the same time, news media coverage becomes a mirror for the evaluated firm and may entice it to adjust its strategic actions to garner positive coverage (Bednar et al., 2013).

Antecedents of news media coverage

Research on strategy contexts focuses mostly on the influence of specific attributes of firms’ strategic actions and sensegiving activities on the formation of coverage. Rindova et al. (2007), for example, examine the media coverage of a broad portfolio of strategic actions taken by both established and new ventures entering the online retail market. They find indications that the link between a firm’s actions and media coverage is particularly strong when the firm’s performance is not directly observable, as is the case for unlisted new ventures that do not disclose detailed financial results. Van Heerde and colleagues (2015) examine the antecedents of media coverage of a price war and find that deeper price cuts are more likely to be covered by the media, but less so the longer the price war lasts.

Other researchers examine variance in sensegiving activities undertaken by firms with regard to their strategic actions, particularly advertising and press releases. Ahern and Sosyura (2014) find that bidders can stimulate media coverage during merger negotiations by issuing press releases. At the same time, they find no evidence that the favorability of press releases improves the favorability of news media coverage. Other scholars point out that firms receive more attention (Rinallo & Basuroy, 2009) and more favorable evaluations (Van Heerde et al., 2015) from news outlets if they advertise in them. Researchers also suggest that the media cover strategic actions by firms more extensively when these are also covered by other media outlets, as well as when the focal firm is considered to provide an interesting narrative, such as being innovative (Rinallo & Basuroy, 2009).

Consequences of news media coverage

Within strategy contexts, scholars researching media coverage of firms point to numerous consequences of media coverage, with a particular focus on subsequent strategic change by firms and changes in firm performance. Bednar and colleagues (2013) show that negative press coverage of a firm is related to subsequent strategic changes. Conversely, Hayward and Hambrick (1997) and Chatterjee and Hambrick (2011) show that positive media coverage about a firm’s CEO leads to overconfidence, increasing firm risk-taking. This resonates with Gerstner, König, Enders, and Hambrick (2013), who find that firms led by narcissistic CEOs specifically dedicate more attention to, and invest more heavily in, discontinuous technologies if the news media show high engagement with the respective technology. Kaniel and Parham (2017) find that mutual funds close to the cutoff point of an important ranking by the Wall Street Journal changed their investment behavior to maximize their chances of being featured. Furthermore, D. Tan (2016) finds that firms are less likely to target competitors with patent litigation if their own media prominence is low, particularly when coverage about competitors has been positive.

Research also gives salience to the effect of media coverage on the performance of strategic actions and the firm in general, particularly with regard to sales. Positive media coverage of products as diverse as books, wines, and mutual funds drives sales of these products (Berger et al., 2010; Horverak, 2009; Kaniel & Parham, 2017; Solomon, Soltes, & Sosyura, 2014). This may also apply for tangential products, as Kaniel and Parham (2017) find evidence for spillover effects in cases where unmentioned funds still benefit from media coverage of funds managed under the same brand, and as Solomon and colleagues (2014) find that positive coverage of individual stocks drives inflows into funds that hold the mentioned assets. Interestingly, studying book reviews, Berger and colleagues (2010) find evidence that even negative media coverage can boost sales when an author is relatively unknown by moving a product into a consumer’s consideration set. Furthermore, media coverage of price cuts is associated with higher sales growth than can be explained by the price cuts alone (Van Heerde et al., 2015). Besides these most salient consequences, researchers have indicated that media coverage of strategic initiatives may also influence stock prices (Ahern & Sosyura, 2014, 2015), especially in the absence of other performance indicators (Chen et al., 2011).

Finance Contexts

The media frequently publish and comment on the financial performance of firms and their participation in financial markets. Frequent topics in finance contexts are earnings disclosures (Drake, Roulstone, & Thornock, 2012; Griffin et al., 2011) and initial public offerings (IPOs; L. X. Liu et al., 2014; Pollock & Rindova, 2003) and other forms of capital acquisition (Petkova, Rindova, & Gupta, 2013), as well as trading by firm insiders (Dai, Parwada, & Zhang, 2015) and investor relations (Bushee & Miller, 2012).

Primary function of the news media

Research in finance contexts is, perhaps unsurprisingly, primarily conducted through an economic lens. It is generally regarded that the media’s function in finance contexts is to reduce information asymmetries by providing information to market participants (Bushee et al., 2010). In addition, the news media are seen as a more credible source than managers or analysts, providing coverage that is “quite timely with an emphasis on factual reporting [as] news reporters and the business press typically do not have strong economic ties and relationships with individual firms” (Kothari et al., 2009: 1645). However, a number of works move beyond this view of the news media and their audience as rational actors and instead add elements from social and psychological theories. For example, Solomon (2012) finds that investor relations firms can affect media coverage about their clients if they have personal ties with journalists, highlighting social influences on journalists. Also, Barber and Odean (2008) explore how cognitive constraints on information processing lead individual investors to become net buyers in stocks that receive high media coverage of earnings news, explaining seemingly irrational reactions by part of the news media’s stock market audience.

Nevertheless, scholars in finance contexts generally emphasize the function of the news media as disseminators of firms’ (financial) information. Given the relative standardization of financial information, the news media act less as evaluators and more as transmitters of information that is already public (L. X. Liu et al., 2014; Rogers et al., 2016). Thereby, the news media’s discretion in finance contexts rather lies in their decision whether to cover or neglect a firm (Bushee & Miller, 2012; Pollock & Rindova, 2003). Also, compared to scholars studying other contexts, scholars in finance take a narrower perspective of the news media’s audiences, focusing particularly on the financial constituents of a firm (Bushman, Williams, & Wittenberg-Moerman, 2017; Griffin et al., 2011; L. X. Liu et al., 2014).

Antecedents of news media coverage

Few studies examine the antecedents of media coverage in finance contexts, but they provide interesting insights into media coverage following active media management by firms. Bushee and Miller (2012) and Solomon (2012) show that firms that hire an investor relations firm receive significantly more media coverage, particularly on dates when they disclose earnings. Relatedly, Petkova and colleagues (2013) show that new ventures attract more media coverage when they engage in many diverse sensegiving activities, such as issuing press releases or attending trade conferences. In addition, researchers highlight the influence of firm characteristics such as performance (Dai et al., 2015) and prior evaluations by both the media and investors on coverage (Pollock et al., 2008).

Consequences of news media coverage

Research on media coverage of firms in finance contexts is mostly concerned with outcomes regarding a range of capital market variables, such as stock prices or turnover, but also examines effects on investor composition and trading by firm insiders. For example, Griffin and colleagues (2011) find that media coverage of earnings is associated with significant changes in stock price volatility. Tetlock (2007) finds that negative sentiment in coverage leads to short-term pressure on returns and increased transaction volume. Dougal, Engelberg, Garcia, and Parsons (2012) confirm this result but highlight that different columnists influence the market in different ways.

On a stock level, Drake and colleagues (2014) find that coverage of a firm’s earnings by the business press reduces mispricing in the respective firm’s stock, but they trace this effect solely to better dissemination of the earnings information, rather than to editorial content. This stands somewhat in contrast to earlier findings by Kothari and colleagues (2009), who observe that favorable news dissemination by the business press reduces firms’ cost of capital, stock price volatility, and forecast error dispersion, while the reverse applies for negative coverage. Moreover, Solomon (2012) highlights that news disclosure by the business press is more impactful than that of firm executives or analysts.

Studies examining IPOs show that new firms that received higher media attention exhibit higher stock liquidity and less underpricing, as well as subsequently lower returns and higher price-earnings ratios than peers that were less prominently featured in the news media (B. Liu & McConnell, 2013; Pollock & Rindova, 2003). Similar results can be seen in other instances of capital acquisition: Bushman and colleagues (2017) provide evidence that firms who receive more favorable media coverage tend to attract more outside participants to syndicated loans and to pay lower interest spreads, while Petkova and colleagues (2013) show that firms that receive more coverage from industry media receive more venture capital funding.

Another significant stream of research examines the effect of news media coverage on investor composition. Engelberg and Parsons (2011) find evidence that links the publication of firms’ earnings in local newspapers to increased trading in that region. Kalay (2015) finds evidence of a less sophisticated investor base in firms whose disclosures frequently feature in the media—consistent with Barber and Odean’s (2008) assertion that individual investors are net buyers of stocks on earnings or dividend news days (as well as other news days). In this vein, Drake et al. (2012) find that media coverage of firms drives investor attention to their stock. However, there is evidence that larger investors are also affected by media coverage. For example, L. X. Liu et al. (2014) find that pre-IPO media attention attracts more institutional investors to an IPO. Moreover, Bushee and colleagues (2010) find that news media coverage of firms’ earnings releases increases trading not only by individual investors but also by large institutional investors. This is in line with Fang, Peress, and Zheng (2014), who find that mutual funds invest more in stocks of firms with a large media presence.

Finally, regarding trades by firm insiders, Rogers and colleagues (2016) find that newswire dissemination of insider purchases increases intraday stock returns and trading volume, even when the news release trails publication of the respective Securities and Exchange Commission (SEC) filing. In addition, Dai and colleagues (2015) find evidence for the claim that media coverage of trading activities by firm insiders reduces subsequent insider trading returns and volume.

Governance Context

Governance is another frequent subject in the news media coverage of firms. Research on governance contexts focuses on a distinct set of topics, including board quality (Joe et al., 2009; Johnson, Ellstrand, Dalton, & Dalton, 2005), attribution of firm performance to its executives (Westphal & Deephouse, 2011; Westphal et al., 2012), executive compensation (Core et al., 2008; Kang & Kim, 2017), firms’ corporate social responsibility (CSR; Kolbel, Busch, & Jancso, 2017; Nikolaeva & Bicho, 2011), and changes in governance (Bednar, 2012; Dixon-Fowler, Ellstrand, & Johnson, 2013).

Primary function of the news media

In governance contexts, the media and their audiences have been conceptualized to a similar extent using all three theoretical lenses. Bednar, for example, views the news media as “conduits of institutional pressure [who] prompt firms to conform to prevailing institutional logics” (2012: 137) in general and in the context of governance, to agency logic in particular. Other studies adopt slightly diverging perspectives. Using an economic-rational framework to study effects of media coverage, B. Liu, McConnell, and Xu argue that “the media can influence the human capital of managers by disseminating information about his actions and by shaping perceptions of those actions” (2017: 175). Conversely, Westphal and Deephouse stress that “journalists’ assessments of a firm’s leadership and strategy can be highly subjective, and their decisions about what information to report or emphasize in writing an article . . . can be similarly subjective” (2011: 1064), suggesting that journalists are susceptible to biases.

Nevertheless, a shared theme emerges from these perspectives with regard to the primary function of the media. Specifically, in governance contexts, the media emerge as evaluators of a firm’s leadership. By publicizing examples of both good and bad firm governance to a broad audience of firm stakeholders, the media address questions including, but not limited to, Is the firm’s leadership acting in constituents’ interest? Are governance mechanisms at the firm designed to align managerial and constituent interests? This evaluative function is consequential because the media can entice stakeholders to take corrective action against a badly governed firm and affect managers’ personal capital (Joe et al., 2009; B. Liu, McConnell, & Xu, 2017). However, caution must be exercised, as the media themselves are susceptible to social influence that may lower the efficacy of their evaluative function (Westphal & Deephouse, 2011; Westphal et al., 2012).

Antecedents of news media coverage

Studies examining antecedents of news media coverage in governance contexts focus primarily on the influence of governance changes and governance attributes as well as social interactions between CEOs and journalists. Bednar (2012) challenges the proposition that the media provide a supervisory function, showing that merely symbolic changes in governance structure result in more positive media coverage. Examining coverage of compensation, Core and colleagues (2008) find evidence that both total and excess compensation of boards lead to more media attention to the firm’s compensation practices.

In a series of studies examining the social fabric between journalists and CEOs, Westphal and colleagues highlight interesting dynamics that determine whether journalists attribute negative firm performance to firm leadership (i.e., governance failures) or to firm-external factors and events. Westphal and Deephouse (2011) provide evidence that following low performance, CEOs tend to ingratiate themselves with journalists and are rewarded with more favorable media coverage. Conversely, they find that journalists also respond to retaliation by CEOs against fellow journalists by issuing more favorable coverage, presumably to avoid losing access to a valuable source. Shani and Westphal (2016) come to similar conclusions regarding social distancing by CEOs from journalists who portrayed them unfavorably. Westphal et al. (2012) show that in addition to CEOs of the focal firms, CEOs of other firms may motivate journalists to decouple low firm performance from governance. Finally, Park and Westphal (2013) show that journalists pick up slant from their sources about outgroup CEOs (i.e., those of a different ethnicity or gender), unless they belong to the same outgroup themselves. In this vein, Dixon-Fowler and colleagues (2013) examine gender bias against female executives in the media and find that female CEOs are frequently mentioned in articles about appointments of other female CEOs, even if their firms do not share any other similarities. Finally, researchers have found evidence that CSR activities (Cahan, Chen, Chen, & Nguyen, 2015), firm size and performance (Bednar, 2012; Core et al., 2008), and prior media coverage (Bednar, 2012) influence the volume and tone of governance-related media coverage of a focal firm.

Consequences of news media coverage

Scholars investigating media coverage of firms in governance contexts have extensively studied the consequences of the news media’s coverage, especially with regard to governance characteristics and executive pay. Regarding board composition, Bednar (2012) suggests that positive coverage leads to reductions in formal board independence, whereas the reverse holds for negative coverage. This result is consistent with the findings of Joe and colleagues (2009), who, examining negative rankings of board quality, find that ranked firms initiate changes in governance and increase their share of outside directors.

Scholars have also devoted significant attention to the question of how news media coverage affects executive compensation. Bednar (2012) finds reductions in the share of CEO’s at-risk pay following positive media coverage and increases following negative media coverage but does not discern any effect on total compensation. This latter finding confirms Core and colleagues’ (2008) and Robinson and colleagues’ (2011) earlier results, which show that press coverage of executive compensation does not induce subsequent changes in pay, and Kuhnen and Niessen’s (2012) contemporaneous study, which finds that negative media coverage of executive pay does not affect total compensation levels. However, Kuhnen and Niessen show that in response to critical media coverage, option-based pay—a stigmatized form of compensation—is replaced with stock-based or salary compensation. While this seeming contradiction with Bednar’s work might be explained by different measures of media coverage, a more explicit contradiction arises from a recent study by Kang and Kim (2017). They find that CEOs who feature frequently in the media receive higher compensation, especially if they lead smaller firms with high performance and have not founded their firm. Therefore, despite a relatively wide body of research, evidence on media coverage and executive compensation is inconclusive. Another quite interesting finding is from a study by Robinson and colleagues (2011), who show that firms receiving negative media attention about CEO compensation are subsequently more likely to violate the SEC disclosure standards on executive compensation.

Relatedly, researchers have investigated long-term consequences of media coverage on executives’ human capital and employment prospects. B. Liu, McConnell, and Xu (2017) find that favorable media coverage of CEOs—as well as of the firms they manage—is associated with more nonexecutive board positions, longer board tenure, and higher compensation for these CEOs after their tenures. In addition, Farrell and Whidbee (2002) and Bednar (2012) find that the favorability of media coverage influences the CEO’s job security.

Furthermore, researchers have highlighted the relationship between media coverage and corporate governance as well as CSR. For instance, media coverage of governance practices was found to support the diffusion of said practices (Nikolaeva & Bicho, 2011). Moreover, both positive and negative coverage of board quality positively affects stock returns (Fang & Peress, 2009; Joe et al., 2009; Johnson et al., 2005), and low media ownership concentration and a low share of government ownership are associated with lower corruption in a country’s banking sector (Houston et al., 2011). Regarding the interplay of media coverage and CSR, research showed, for example, that positive coverage of a firm’s environmental governance reduces unsystematic risk (Bansal & Clelland, 2004), coverage of CSR leads to higher firm risk (Kolbel et al., 2017), and positive coverage following high CSR performance leads to higher Tobin’s q and lower cost of capital (Cahan et al., 2015).

Crisis Contexts

A final context that features prominently in the news media coverage of firms concerns crises, that is, salient individual events or practices that typically result from wrongdoing, whether actual or perceived, by the firm or its agents. Crisis contexts tend to arise around a certain set of issues, including incidents of environmental violations and product failure (Desai, 2014; Hoffman & Ocasio, 2001), firms’ involvement in stigmatized industries or practices (Durand & Vergne, 2015; Lamin & Zaheer, 2012; Vergne, 2012), protests against the firm (King, 2008), or engagement in fraud, corruption, and related illegal practices (Dyck et al., 2008; Wiersema & Zhang, 2013).

Primary function of the news media

Extant research on crisis contexts leans heavily on institutional theory and is largely concerned with how media coverage of firms’ malpractice reflects or affects their legitimacy or reputation (Durand & Vergne, 2015; Lamin & Zaheer, 2012). Nevertheless, social-psychological and economic perspectives on the news media and their audiences have also taken hold in crisis contexts. For example, Zavyalova and colleagues (2012) point to cognitive biases in journalists’ reporting in crisis contexts; they argue that a “safety-in-numbers effect” shields firms from negative coverage after wrongdoing in the presence of wrongdoing by competitors, as their actions will be less salient for journalists. Conversely, Miller (2006) stresses a rational bias in the news media’s selection of corporate frauds to cover, as they tend to report more frequently on cases associated with a low cost of information acquisition and processing.

Despite such differing perspectives on the representativeness of crisis contexts covered in the media, what unifies them is a view of the media’s function as agitators for corrective action. By reporting on the misdeeds of firms, the media disseminate this information widely among firm constituents, giving prominence to stakeholders already taking action (King, 2008) or enticing them into action (Tang & Tang, 2016) and pressuring firms to conform with corrective demands (Desai, 2014; Piazza & Perretti, 2015).

Antecedents of news media coverage

Research on crisis contexts emphasizes the importance of crisis characteristics and firms’ responses to a focal crisis on media coverage. In relation to events that constitute a crisis context, Miller (2006) finds that accounting violations attract more media coverage when the violation constitutes theft, was committed by individuals, or is large in magnitude. In a similar vein, Gomulya and Boeker (2014) find that the unfavorability of the media’s response to an accounting restatement is proportional to the magnitude of the restatement. Dyck and colleagues (2008) add that shareholder activism regarding governance violations may also lead to more media coverage of the incidents. Briscoe and Murphy (2012) highlight the fact that the media are more likely to report on firms’ curtailment of retiree health benefits when the impact is large, the curtailment is transparent, and interest groups make corrective demands. Finally, Zavyalova and colleagues (2012) find interesting dynamics between firm and industry wrongdoing in the context of product recalls: while firm wrongdoing and—to a lesser extent—industry wrongdoing independently lead to (a spillover of) negative media coverage about a firm, their interaction results in an attenuating effect.

Evaluating the effects of firm responses in crisis contexts, Lamin and Zaheer (2012) find that following accusations of sweatshop labor, denial and defiance responses by firms increase the unfavorability of media coverage, while no form of response can improve the favorability of media coverage. Zavyalova and colleagues (2012) reach a somewhat different conclusion, finding that technical responses by firms attenuate negative media coverage after firm wrongdoing, whereas ceremonial actions prove effective after wrongdoing by industry peers. One possible explanation for this divergence might lie with the fact that product recalls are typically the result of unintentional errors and relatively frequent occurrences in many industries, whereas the use of sweatshop labor may carry more stigma. Gomulya and Boeker (2014) in turn highlight that following accounting restatements, media coverage of a firm is more positive if the firm appoints a new CEO with significant (turnaround) experience and an elite educational background. Finally, several studies affirm the influence of firm size and prior media coverage on coverage of crisis contexts (Dyck et al., 2008; Lamin & Zaheer, 2012; Miller, 2006).

Consequences of news media coverage

The consequences of media coverage in crisis contexts have received significant attention from scholars. In particular, a large body of research has examined how firms are prompted to engage in rectifying actions or impression management in response to crises covered by the media. This is consistent with Hoffman and Ocasio’s (2001) finding that media coverage of an environmental incident related to firms was a sufficient condition for the incident to garner widespread industry attention. Regarding reactions Durand and Vergne (2015) find that firms tend to divest from sin industries following negative media coverage about their own or their peers’ engagement in such industries. Piazza and Perretti (2015) confirm this finding, showing how firms were more likely to disengage from nuclear power plant projects following negative media coverage about the technology. Dyck and colleagues (2008) find reversals of severe governance violations by Russian firms only after coverage by the international and not the domestic Russian press. Similarly, B. Liu and McConnell (2013) find that firms are more likely to abandon acquisitions that triggered a negative stock market response if they receive substantial negative media coverage. King (2008) observes that firms are more likely to concede to consumer boycotts when these are covered by the media, and studies by both Briscoe and Murphy (2012) and Desai (2014) find that media coverage of firms’ malpractices or crisis incidents may trigger corrective behavior even in competitors. Some researchers point to more indirect firm responses, especially those involving changes in governance. Both Bowen and colleagues (2010) and Wiersema and Zhang (2013) find that media coverage concerning financial wrongdoing by firms increases the likelihood of CEO turnover at the affected firms. In addition, these firms tend to reduce the size of their boards, allocate more board seats to outsiders, and appoint directors with fewer outside mandates (Bowen et al., 2010).

Other studies assert that in addition to such substantial actions, news media coverage also affects the impression management activities of targeted firms (Rhee & Valdez, 2009). McDonnell and King (2013) show that media coverage of a boycott entices the target firm to issue prosocial statements in response. In addition, Desai (2011) finds that firms in the railroad industry engaged in anticipatory impression management by releasing defensive statements following safety incidents at competitors that received significant media attention.

Finally, scholars point to negative reactions among audiences towards focal firms following media coverage in crisis contexts. These include reactions from financial constituents (Bowen et al., 2010; King & Soule, 2007; Miller, 2006), auditors (Joe, 2003), customers (Jonsson & Buhr, 2011; Y. Liu & Shankar, 2015; Tang & Tang, 2016), managers at other firms (Bednar, Love, & Kraatz, 2015), and governments (Tang & Tang, 2016). All of these findings have implications for a firm’s reputation following a crisis as well (Rhee & Valdez, 2009). Given this strong influence of media coverage in crisis contexts, Dyck and colleagues (2010) find that whistleblowing journalists are promoted more frequently, highlighting journalists’ incentives to engage in investigative research on firm wrongdoing.

Research on Aggregate Coverage

While distinctions exist between the above contexts, some scholars have advanced our understanding of the media coverage of firms by studying coverage and its consequences in aggregate, irrespective of the underlying context.

Antecedents of news media coverage

In research on aggregate coverage, scholars have focused on the relationship between firm characteristics and general news coverage. In particular, they find that media coverage is higher for firms that have greater market capitalization (Bushee et al., 2010; Fang & Peress, 2009; Hillert, Jacobs, & Müller, 2014), higher returns and more employees (Bushee et al., 2010), higher individual ownership and stock volatility (Fang & Peress, 2009), and are members of the S&P 500 (Hillert et al., 2014) or are located in the same area as the respective media outlet (Gurun & Butler, 2012). These studies further emphasize that firms’ press releases (Bushee et al., 2010) and advertising (Gurun & Butler, 2012) also influence the aggregate volume and tone of media coverage.

Consequences of news media coverage

The majority of research on aggregate coverage investigates the effect of news media coverage on stock market variables, indicating that volume and favorability of media coverage affect stock prices and returns (Fang & Peress, 2009; Gurun & Butler, 2012; Huang, 2015; Tetlock, 2011; Tetlock et al., 2008). Consistent with the notion that the media function as disseminators of information, they find that this effect is particularly strong for firms that are small, are illiquid, have a low analyst following, or are mostly held by individual investors (Fang & Peress, 2009; Gurun & Butler, 2012). Peress (2014) further supports this view by showing that on newspaper strike days, turnover and volatility of small stocks are significantly lower than on days when the news is disseminated regularly, while documenting no such effect for large stocks. A more nuanced view emerges from the work of Hillert and colleagues (2014). They do not find any direct connection between volume of coverage and stock returns but instead assert that momentum and reversal effects are pronounced for high-attention firms, especially when stock returns and the favorability of media coverage match. On a market level, looking at stock price synchronicity and future earnings incremental explanatory power (FINC) as proxies for efficient capital markets, Kim, Zhang, Li, and Tian (2014) find that countries with more press freedom and lower state ownership in the press exhibit lower synchronicity and higher FINC. Deephouse (2000) adds that firms with more positive media coverage exhibit higher returns on assets, suggesting that media coverage may also be linked to performance.

Finally, two studies investigate the consequences of news media coverage on firms’ current and prospective employees. Kjaergaard, Morsing, and Ravasi (2011) follow the case of a Danish firm that achieved “celebrity status” in the media and find that enthusiastic media reports aligned employees’ beliefs and actions with the portrayal of the firm in the media through a form of “celebrity seduction.” Similarly, Vanacker and Forbes (2016) find that new ventures that are backed by venture capital firms with large media coverage attract more talent than those backed by relatively unknown funds.

An Integrated Framework of Media Coverage of Firms and Directions for Future Research

Figure 6 depicts our holistic framework for media coverage of firms. Our framework aims to transcend the theoretical boundaries erected by economic, institutional, and social-psychological conceptualizations of the news media by integrating antecedents, attributes, consequences, and moderators from an interdisciplinary body of research. As we have seen, scholars using different theoretical lenses tend to differ on the mechanisms underlying the formation of, and influence exerted by, media coverage of firms. However, this mostly results in different explanations for the same phenomena, rather than contradicting predictions. For example, scholars have variously explained firms’ propensity to take remedying actions in critical contexts in response to news media coverage by economic incentives (Dyck et al., 2008) or institutional and social pressures (Durand & Vergne, 2015; King, 2008). Examples like this not only demonstrate the value of our framework that cuts across perspectives but also make clear that one major avenue for future research is to determine which of multiple competing explanations for the same phenomenon holds the greatest explanatory power. Similarly, the holistic view that our framework provides highlights that future research might tackle questions that pertain to how firms’ media coverage might be simultaneously a cause and a consequence of, for example, social approval (Bundy & Pfarrer, 2015).

An Integrated Framework of Media Coverage

Moreover, our framework emphasizes the important role of context on the formation and consequences of news media coverage. As outlined before, both the type and characteristics of a specific context may substantially influence the formation of news media coverage (Miller, 2006; Rindova et al., 2007), as well as its consequences (King, 2008; B. Liu & McConnell, 2013). In some cases, context may even reverse relationships. For example, while in most contexts firms with negative performance receive more coverage, in some cases, such as trading by firm insiders, firms with positive performance attract more attention from the media (Dai et al., 2015). Bearing this in mind, our framework recognizes that context moderates the relationships of antecedents with attributes and consequences of news media coverage.

Ultimately building on the body of research in this review as well as selected other frameworks (Carroll & Deephouse, 2014; Shoemaker & Reese, 2013), our framework aims not only to provide a concise overview of our current knowledge about media coverage of firms but also to identify knowledge gaps that could be exploited by future research.

Antecedents of Firm-Related News Media Coverage and Related Research Opportunities

A multitude of factors related to the firm, the media, and their environment may influence media coverage. In relation to firms, factors include firm characteristics, context characteristics, as well as impression management and media advertising by the focal firm. For example, large firms are more likely to be covered than small firms (Fang & Peress, 2009; Hillert et al., 2014), and actions carried out by individual firm members attract more coverage than those without discernible decision makers (Miller, 2006). Firms experiencing a crisis or poor performance also attract coverage (Hoffman & Ocasio, 2001; Y. Liu, Shankar, & Yun, 2017). Furthermore, firms may be represented differently by the media depending on their impression management (Ahern & Sosyura, 2014) or advertising (Gurun & Butler, 2012).

Concerning the media, and consistent with Shoemaker and Reese’s (2013) theory of influences on mass media content, we identify multiple different spheres of influence on media coverage, including influences from individual journalists, media routines, the media organization, and ideology. 4 Examples of influences of individual media workers would be journalists’ gender or ethnic background (Park & Westphal, 2013). Media routines refer to established practices shared across members of the journalistic profession that shape how an individual journalist creates coverage. Examples of such media routines include reliance on newswires, fellow journalists, and other sources for cues regarding potential objects of coverage (Shoemaker & Reese, 2013). Influences from the media organization may derive, for example, from business considerations and can define the degree of audience orientation or propensity to advertiser bias (Gurun & Butler, 2012). Finally, ideology refers to the norms, beliefs, and values widely shared in society and internalized by both journalists and their audiences, such as the old adage “if it bleeds, it leads,” driving journalists to seek out dramatic news (Arpan & Pompper, 2003). Such influences on media coverage become particularly apparent in cross-country comparisons where differences in ideology are most salient (Dyck & Zingales, 2002).

In relation to the environment, we distinguish between relevant firm-external characteristics and dynamics of the contexts that trigger news media coverage. For example, activism by stakeholders may be an important factor influencing media coverage decisions and leading to more unfavorable reporting (Dyck et al., 2008). Similar influence may come from the stock markets (Fang & Peress, 2009) and competitor firms (Durand & Vergne, 2015).

Overall, it is clear that research on the antecedents of news media coverage of firms has received relatively little attention by scholars, and knowledge gaps exist regarding all mentioned antecedents. We highlight three areas that may warrant particular attention. First, the field would likely benefit from a cross-context perspective that explicitly contrasts the antecedents of media coverage in different contexts. While some prior studies venture in this direction, they tend to focus on only the consequences in general and not on antecedents or an explicit comparison between contexts (Bushee et al., 2010).

Second, research about media coverage of firms would benefit from a more nuanced understanding of how firms’ impression management influences coverage by the news media. Most research to date has focused strongly on the volume and favorability of press releases (Ahern & Sosyura, 2015; Kalay, 2015). However, we know from research on strategic public language (Gao, Yu, & Cannella, 2016) that firms’ impression management can be measured using far more intricate dimensions than just positive and negative language. Application of this knowledge in research on media coverage of firms, especially in empirical studies, however, is rare. Laudable exceptions to this include studies in crisis contexts (Lamin & Zaheer, 2012; McDonnell & King, 2013). Furthermore, Westphal and Deephouse (2011) and Westphal et al. (2012) undertook various sophisticated measurement efforts in their examination of how CEOs exert social influence on the media. While they also focus on positive language, they measure, for example, positive statements by CEOs in press articles, conference calls, letters to shareholders, and annual reports in relation to firm performance, strategy, and leadership and governance. They further capture external attributions of firm performance in these materials, as well as CEOs’ impression management efforts through surveys among firm members and journalists.

Third, research should begin to recognize the media as part of a larger organizational context. Media organizations are often owned and controlled by nonmedia owners (Shoemaker & Reese, 2013). For example, in a world where GE once owned NBC, how does Amazon’s Jeff Bezos’s ownership of the Washington Post influence its coverage of firms? Furthermore, what are the implications of board interlocks between media firms and other corporations in terms of coverage and firms’ impression management strategies? As media outlets are facing mounting economic pressure to consolidate, becoming some of the largest firms in their own right, answers to these questions will be critical to understanding firms’ future media coverage.

Attributes of Firm-Related News Media Coverage and Related Research Opportunities

In characterizing attributes of news media coverage of firms, we build on Carroll and Deephouse’s (2014) framework—volume, tone, topic, and timing—but extend it by adding the necessity to consider language characteristics, the news segment, and the regional scope of the coverage. Volume of coverage is probably the most straightforward (and most frequent) of these attributes and refers to the amount of media coverage a firm receives, such as the number of articles (Dai et al., 2015). Measurement of the volume of media coverage is relatively uniform, relying on the count of articles (Bednar et al., 2015) or on strongly related variables such as counts of statements (Park & Westphal, 2013) or counts of words (Bushee et al., 2010).

Tone of coverage “refers to the level of support for [a firm] expressed in a news article” (Carroll & Deephouse, 2014: 84) and is typically conceptualized as a composite of favorable and unfavorable tone (Carter, 2006). As a result of its evaluative power, it is not surprising that tone has received much of the scholarly attention to date. Regarding the measurement of favorable or unfavorable coverage, the main fault line runs between studies using manual coding of their sources and those relying on computerized word counts or other automated procedures. Among management scholars, coding tone based on the Loughran and McDonald (2011) dictionaries and Linguistic Inquiry and Word Count (LIWC; Pennebaker et al., 2007) positive and negative emotion dictionaries has emerged as the most established automated practice. While both manual and automated approaches have their respective merits, the former allowing for more exact and nuanced coding, the latter allowing for far greater volumes of source material and yielding largely objective measures, relatively few studies acknowledge the inherent limits of either procedure or employ both methods in robustness checks (for an exception, see Zavyalova et al., 2012). The literature also varies with regard to the operationalization of tone. Studies use word counts and ratios (positive, negative, or both) at various levels of aggregation (article, event, year) by firm or industry, leaving scholars with a vast array of operationalizations. Some studies even take the inverse of unfavorable media coverage to denote favorable media coverage (Gurun & Butler, 2012), which is problematic, as ample evidence exists that favorable and unfavorable coverage is by no means symmetric (Bednar, 2012; Gomulya & Boeker, 2014).

The topic of coverage denotes the substantive representation of a certain subject of coverage, as well as the specific information contained in the coverage. For example, studies compare coverage of the CEO with other coverage of a firm (Kang & Kim, 2017), examine consequences of news stories on the basis of their similarity with prior news (Tetlock, 2011), analyze differences between regular media coverage and awards bestowed by the media (Chatterjee & Hambrick, 2011), or compare coverage of different firm action types (Rindova et al., 2007).

Timing refers to a sequential ordering of information (Carroll & Deephouse, 2014). Such ordering can take many forms, but most prominent are the position of information within an article, that is, its salience (Gurun & Butler, 2012); the longitudinal timing of the article relative to the actual events; and prior media coverage carrying the same information, that is, its timeliness and novelty (Tetlock, 2011). Other studies examine the effect of timing of media articles relative to other events (Ahern & Sosyura, 2014; Chen et al., 2011).

Another attribute of news media coverage is what we call language characteristics. Research on firms’ strategic public language has identified a plethora of characteristics beyond tone, such as characteristics of narrative and frame or rhetorical devices (Gao et al., 2016). As is the case for such firm communication, it is only reasonable to assume that language characteristics in news media coverage may have specific antecedents (e.g., characteristics of journalists, media outlets, and the covered firms) and consequences (e.g., effects on comprehension and perceived credibility). While research on language characteristics in news media coverage of firms is nascent at best, some initial evidence of its relevance exists: Ahern and Sosyura (2014) find that in the context of merger rumors, the degrees of experience and specialization of journalists and the readership appeal of the involved firms are predictive of sensationalist reporting that uses ambiguous language. This ambiguity in language is, in turn, a predictor of the accuracy of the reporting. Future research could study further language characteristics such as readability, concreteness, or the use of metaphors and other tropes, all of which have been demonstrated to potentially have consequences for audience reception (König et al., 2018; Pan, McNamara, Lee, Haleblian, & Devers, 2018; H.-T. Tan, Wang, & Zhou, 2014).

The media also consist of countless different outlets across numerous segments resulting in potential differences due to the news media segment. Sources used in research on media coverage of firms in the United States alone comprise general national newspapers such as the New York Times (King & Soule, 2007), financial newspapers such as the Wall Street Journal (Jensen & Roy, 2008), local newspapers such as the Cleveland Plain Dealer (Hoffman & Ocasio, 2001), newswire services such as Dow Jones Newswires (Bushman et al., 2017), and magazines as diverse as the Hollywood Reporter (Chen et al., 2011) and Fortune (Chatterjee & Hambrick, 2011).

While the use of a broad set of sources is commendable, issues may arise where differences in sources are not accounted for. In the small number of studies that explicitly contrast coverage in different segments of the press, significant variances come to light. For example, Gurun and Butler (2012) find that unlike local newspapers and magazines, national newspapers are not biased towards advertisers. Similarly, Bushee and Miller (2012) suggest that active media management through investor relations firms is more effective at local rather than national newspapers. Drake and colleagues (2014) find that only coverage in newswires, represented by the Dow Jones Newswire, but not in national newspapers, represented by the Wall Street Journal, reduced stock mispricing. Additionally, Petkova and colleagues (2013) find evidence that coverage by industry media, but not by general media, increases venture capital investment in new ventures. Therefore, research that does not account for potential differences in antecedents or consequences of the coverage in specific news media segments may dilute any effects it hopes to observe.

Finally, we focus on the regional scope of coverage. Extant research shows a tendency to focus on coverage of firms by media outlets in the United States. Eighty-two studies, accounting for more than 80% of the sample reviewed here, focus on U.S. news media alone. Only a small number of studies focus on other countries or include media coverage from outlets across multiple countries. In addition, three metastudies examine the antecedents and consequences of country-level media variables (Griffin et al., 2011; Houston et al., 2011; Kim et al., 2014). However, even among multicountry studies, media coverage from different countries is frequently simply aggregated in order to increase the sample size (Durand & Vergne, 2015; Nikolaeva & Bicho, 2011).

The few studies that actually examine cross-country variations in specific media coverage suggest interesting dynamics. Dyck et al. (2008) find that media coverage of governance violations was consequential only when it appeared in the Western financial press but not when it was featured by Russian newspapers, even when these were joint ventures with the very Western news outlets whose coverage sparked firm responses. Rinallo and Basuroy (2009) find bias in fashion magazines towards home companies akin to Gurun and Butler’s (2012) finding about local news media slant, but only in France.

Focusing on the various attributes of media coverage provides scholars with ample avenues for future theoretical and empirical refinement. First, it is surprising that individual articles often focus on either volume or tone in isolation (less than half focused on both). Studies examining both volume and tone of coverage provide ample evidence of how these variables reinforce each other and how their consequences are intricately linked (B. Liu & McConnell, 2013; B. Liu, McConnell, & Xu, 2017). Particularly noteworthy in this regard are those studies that investigate only the tone of media coverage (14 articles), as they implicitly gathered all necessary data to construct a volume variable but chose not to do so (Deephouse, 2000; Gomulya & Boeker, 2014; Lamin & Zaheer, 2012). Moreover, many of the studies exploring the consequences of both volume and tone consider the two variables as independent constructs in their statistical models, not allowing for a reinforcing interaction between them (Bednar et al., 2015; Desai, 2014) and further limiting our theoretical and empirical understanding of their relationship. As such, research about media coverage of firms may benefit from the use of more multifaceted deconstructions and the simultaneous examination of multiple attributes of media coverage (Carroll & Deephouse, 2014).

Second, there appear to be plenty of opportunities for methodological advancement, especially with regard to measuring the tone of media coverage. While arguably most accurate, manual coding is rarely feasible with today’s large data sets, which often contain several hundred thousand or even millions of articles (Ahern & Sosyura, 2014; Hillert et al., 2014). At the same time, word count methods that are in use today are crude, as they cannot determine whether a word describing a firm or another entity is used ironically and cannot differentiate between ambiguous meanings of a word (e.g., whether good is used as a noun or as an adjective). Scholars with an interest in methods innovation should find many opportunities to advance research on media coverage of firms (and, frankly, research about language in organizational contexts in general). To give just one example of potential for innovations, computational approaches for word sense disambiguation have been described for more than a decade (Sebastiani, 2002) and if carefully developed, should eventually be able to remedy many of the aforementioned drawbacks of automated coding procedures. Ultimately, the significant differences in methodologies for measuring tone, particularly between disciplines, severely limit generalizability and comparability of results (for an exception, see Kuhnen & Niessen, 2012).

Third, research about media coverage of firms stands to benefit from explicit comparisons of media coverage by news outlets from different segments and regions. Extant studies are split between those that consider only a small set of media sources (Huang, 2015; Tetlock, 2007) and those that aggregate sources as broadly as “Major Newspapers, Journals and Magazines, and Trade Magazines databases of Lexis-Nexis” (Pollock & Rindova, 2003: 635) or “major US and world publications, major world publications (non English), news wire services, TV and radio broadcast transcripts, company and SEC filings” (Nikolaeva & Bicho, 2011: 146). However, a few studies indicate that characteristics of media outlets, such as segment or region, in fact strongly influence the formation and consequences of media coverage (Dyck et al., 2008; Petkova et al., 2013). Relatedly, Carter and Deephouse (1999) compared investor, supplier, and customer perspectives on Walmart using financial press, trade press, and general newspapers, respectively. Future research could examine whether such differences hold for other settings, taking advantage of online databases and automated coding. Future research may thus benefit from taking a more differentiated perspective of news media sources when designing studies.

Consequences of Firm-Related News Media Coverage and Related Research Opportunities

In relation to consequences of news media coverage, we distinguish between effects on the firm, firm leadership, audience, and media. At the firm level, media coverage particularly influences firms’ performance, resource acquisition, and direct responses by the firm and its employees. For example, media coverage may lead to improvements in firms’ return on assets (Deephouse, 2000) and acquisition of equity (L. X. Liu et al., 2014), debt (Bushman et al., 2017), and human capital (Vanacker & Forbes, 2016). In addition, media coverage may support the accumulation of intangible resources, such as reputation or legitimacy (Bednar et al., 2015; Love, Lim, & Bednar, 2017). More directly, media coverage may also contribute to immediate responses from firms, ranging from verbal statements (McDonnell & King, 2013; Pfarrer, Pollock, & Rindova, 2010) to major strategic shifts (B. Liu & McConnell, 2013).

The consequences of media coverage are also felt by the leadership team of a firm and by CEOs in particular. Specifically, media coverage may contribute to—or endanger—managers’ human capital (Kang & Kim, 2017) and employment prospects (B. Liu, McConnell, & Xu, 2017). Also, CEOs may engage in more individual responses to coverage by individual journalists than firms could do, such as social distancing from these journalists (Shani & Westphal, 2016).