Abstract

In this study, we investigate how CEO narcissism, in combination with corporate governance practices, impacts organizational risk-taking and how this in turn affects organizations’ resilience to environmental conditions. We examine these issues in the context of the recent collapse (systemic shock) of the U.S. banking industry in September 2008, using a sample of 92 CEOs from 2006 until 2014. We find that before the shock CEO narcissism positively affected the riskiness of banks’ policies, especially when compensation policies that encourage risk-taking (stock options) are in place. The positive effect of narcissism was dampened, however, when board monitoring was more effective (because of the presence of knowledgeable outsider directors). Furthermore, we find that these preshock features hamper organizations’ resilience to (economic) shocks, as banks led by more narcissistic CEOs before the September 2008 collapse experienced a slower recovery to preshock performance levels afterwards. This effect was partially mediated by banks’ preshock riskiness of policies. We attribute these effects to the associated depletion of the organizations’ internal resources (beyond slack). Post-hoc analyses further underscore this idea, showing that the U.S. government’s capital injections through the Troubled Assets Relief Program (TARP)—resolving the “problem” of resource depletion—moderated these effects.

It’s only when the tide goes out that you learn who’s been swimming naked

“September 15, 2008 – the date of the bankruptcy of Lehman Brothers and the takeover of Merrill Lynch, followed within 24 hours by the rescue of AIG – marked the beginning of the worst market disruption in postwar American history” (Financial Crisis Inquiry Commission, 2011: 353). While a looming crisis in the U.S. banking industry already began to show at the start of 2006 with the gradual decline in housing prices in some parts of the U.S. (the “sandstone” states of Arizona, California, Florida, and Nevada), the crisis reached its climax in the “financial panic” of late 2008 (Hindmoor & McConnell, 2013: 543). September 2008 marked the moment that the subprime crisis, triggered by the burst of the housing price bubble, resulted in the collapse of the banking industry followed by a global financial crisis (Black & Hazelwood, 2013).

After the collapse, a common theme in popular outlets was that the “greedy” and “reckless” behavior of bank chief executive officers (CEOs), combined with poor corporate governance practices (such as risk-inducing compensation and lack of monitoring), produced a “dangerous cocktail” that led to the systemic shock and global crisis (DeYoung, Peng, & Yan, 2013; Financial Crisis Inquiry Commission, 2011). As is common in ex post causal attribution processes, these explanations are in all likelihood oversimplifications of reality (Hindmoor & McConnell, 2013), especially as they ignore the heterogeneity of banks and their CEOs. Indeed, although many banks failed or lingered after the September 2008 collapse, others showed remarkable resilience and recovered quite quickly. An intriguing question thus arises: What is the role of CEOs (and in particular their greed and recklessness) and corporate governance in shaping banks’ resilience to shocks such as the September 2008 collapse?

To answer this question, we develop a comprehensive model grounded in the upper echelons (UE) and corporate governance (CG) literatures. Building on these literatures, we argue that CEO narcissism, combined with CG policies that either incentivized CEO risk-taking (Wowak & Hambrick, 2010) or decreased monitoring vigilance (Cerasi & Oliviero, 2015), affected banks’ resilience to shocks. Here, we focus on CEO narcissism as growing evidence reveals that the more narcissistic—that is, self-loving and self-appraising—an organization’s CEO, the more it will engage in risky strategies and investments (e.g., Wales, Patel, & Lumpkin, 2013; Zhu & Chen, 2015b). Following repeated pleas to introduce an interactionist approach in UE research (e.g., Busenbark, Krause, Boivie, & Graffin, 2016; Wowak & Hambrick, 2010), we argue that the effect of CEO narcissism on risk-taking is moderated by the CG context in which CEOs operate. In particular, we expect the effect to be more pronounced when narcissistic CEOs are compensated with stock options, which are known to incentivize risk-taking behavior (Wowak & Hambrick, 2010), but less pronounced when firms have block ownership or independent and experienced directors, both of which affect the effectiveness of monitoring (Cerasi & Oliviero, 2015; De Haan & Vlahu, 2016; Hambrick, Misangyi, & Park, 2015).

Riskiness in strategies and policies (instigated by CEO narcissism in combination with poor CG practices) increases organizations’ vulnerability to external conditions (Aven, 2011) and is therefore especially relevant when assessing the impact of extreme events—such as the September 2008 collapse for U.S. banks—on organizational resilience. Starting from a central, but understudied tenet of the emerging literature on organizational resilience—that is, that preshock features of a system shape its subsequent ability to endure a shock, as well as to recover from it (Aven, 2011; van der Vegt, Essens, Wahlström, & George, 2015)—we argue that banks with a high level of riskiness in their policies before the September 2008 collapse depleted their resources and internal buffers, which, in turn, undermined their resilience. As a result, we expect that increased riskiness of policies and the associated depletion of resources caused drastic declines in performance immediately after the September 2008 collapse and difficulties in recovering to preshock performance levels afterwards.

We empirically test our ideas using a sample of 92 CEOs of U.S. commercial banks, which we followed from 2006 till 2014. Our findings provide general support for most of the hypothesized model: We found that the riskiness of bank policies before the systemic shock was positively associated with CEO narcissism, especially when CEO stock options were high and when there were no outsider directors with banking experience. While we do not find that preshock CEO narcissism or riskier policies affected banks’ drop in performance immediately after the collapse, our results do indicate that both CEO narcissism and riskiness of policies slowed down banks’ postshock recovery to preshock performance levels.

Our study makes several contributions. First, we contribute to the growing literature on organizational resilience by investigating its antecedents, a topic which has received insufficient attention in prior work (van der Vegt et al., 2015). Understanding why shocks differentially affect organizations in the long run is an important issue, as the continuity and survival of organizations also affects societal welfare (van der Vegt et al., 2015). Second, we extend both the UE and the CG literatures by our interactive approach (Busenbark et al., 2016)—that is, the combination of CEO narcissism and poor CG practices erodes organizations’ resilience to shocks. Third, we attend to the recurrent calls by CEO narcissism scholars to study its longer-run effects (e.g., Gerstner, König, Enders, & Hambrick, 2013; O’Reilly, Doerr, Caldwell, & Chatman, 2014). Scholars have repeatedly suggested, but not systematically tested, that because of their resource-depleting decisions and investments, narcissistic CEOs could have especially detrimental effects in the longer run (e.g., Engelen, Neumann, & Schmidt, 2016). The context of a systemic shock allows us to empirically test this often-made claim. Whereas Patel and Cooper (2014) have brought the relevance of environmental conditions to the fore by studying CEO narcissism’s effects during an economic crisis, we add to their work by specifically focusing on how the narcissistic CEOs’ preshock resource-depleting strategies have longer-lasting effects, damaging their firms’ capabilities to recover from the shock. Finally, in contrast to the claims in the more popular accounts, our study shows that not all banks and CEOs are the same; they are not all equally “greedy” and “reckless.” Our findings also suggest that good CG practices may mitigate the harmful effects of CEO narcissism and, in turn, strengthen organizations’ long-run resilience.

Theory and Hypotheses

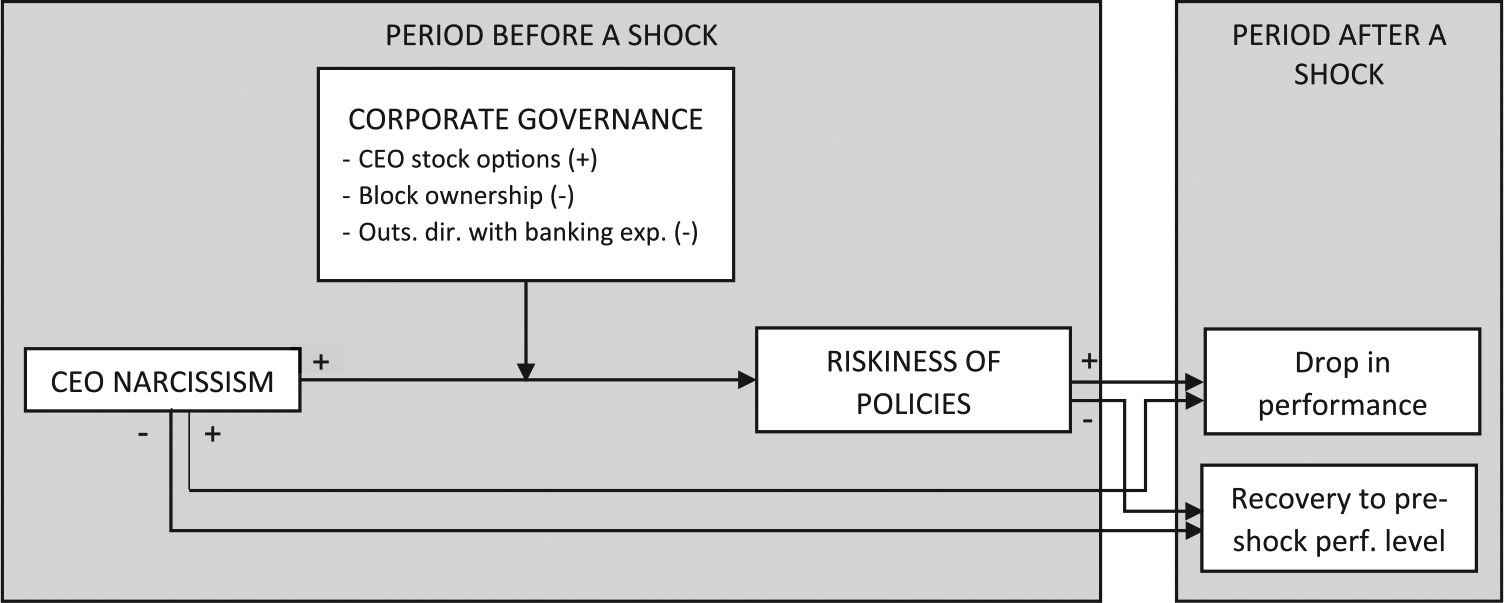

Figure 1 depicts our theoretical model. We propose that CEO narcissism increases the riskiness inherent in organizations’ policies, an effect that will be even more pronounced when combined with particular CG practices—high CEO stock options, low block ownership, and the absence of knowledgeable outsider directors. We further expect that higher preshock levels of CEO narcissism and/or riskiness will induce larger performance drops immediately after the shock, as well as slower recovery to preshock performance levels afterwards.

Research Framework

CEO Narcissism and the Riskiness of Banks’ Policies

UE scholars have repeatedly found that CEO narcissism is related to bold and risky (high-risk, high-return) strategies. For instance, CEO narcissism has been linked to forms of spending with highly uncertain returns: R&D, capital expenditures, and acquisitions (Chatterjee & Hambrick, 2011; Zhu & Chen, 2015b). Similarly, using a survey, Wales et al. (2013) found that narcissistic CEOs characterized their organizations as more entrepreneurially oriented—that is, with higher levels of innovativeness, proactiveness, and risk-taking in the pursuit of strategic opportunities. Gerstner et al.’s (2013) findings show that more narcissistic CEOs are prone to adopt novel and yet-unproven technologies, despite their inherent riskiness.

Three lines of reasoning, grounded in findings from the psychology literature (e.g., Emmons, 1987), are generally used to underscore the link between CEO narcissism and risky strategies. First, highly narcissistic CEOs have a strong desire to hold the spotlight by inspiring awe and admiration (Wales et al., 2013). This drives them to pursue strategies and policies that—in their opinion—will attract the audience’s attention and admiration and showcase their sense of vision and leadership (Gerstner et al., 2013; Wales et al., 2013). Second, narcissists’ excessive feeling of self-assurance and superiority (Emmons, 1987) leads to positively biased expectations that their decisions will have a positive outcome (Chatterjee & Hambrick, 2011; Gerstner et al., 2013; Wales et al., 2013). Third, narcissistic CEOs are also highly self-centered and self-interested (Emmons, 1987). Therefore, they are highly focused on securing personal rewards (Patel & Cooper, 2014), as well as less apprehensive about the outcome of their decisions on the fates of others, such as employees or other stakeholders (O’Reilly et al., 2014). This resonates with the characterization of narcissists as having a strong approach but weak avoidance motivation (Foster, Reidy, Misra, & Goff, 2011)—they are less likely to act as “a careful steward of organizational resources” (Patel & Cooper, 2014: 1530).

In line with prior work (DeYoung et al., 2013), we identify risky strategies in our setting of U.S. commercial banks as their investments in three types of policies: (a) commercial and industrial loans, (b) noninterest income activities, and (c) derivatives and off-balance sheet activities (including mortgage-backed securities). All of these policies have been found to increase banks’ inherent riskiness (Apergis, 2014; Black & Hazelwood, 2013; DeYoung & Torna, 2013; DeYoung et al., 2013). We expect banks with more narcissistic CEOs to invest more heavily in these risky policies, because of the above-mentioned three lines of reasoning. First, investing in these risky policies allows narcissistic CEOs to expose their boldness and strategic vision in banking to attract a “social stage” (e.g., Wales et al., 2013). Commercial loans are generally more lucrative and visible by others than loans to individual investors (Cole & White, 2012; DeYoung et al., 2013). Furthermore, similar to Gerstner et al.’s (2013) finding that narcissistic CEOs in the pharma industry were more prone to adopt technologies new to the industry, narcissistic CEOs in commercial banks may be more willing to engage in “novel,” “nontraditional” banking activities and “banking innovations,” such as noninterest income activities and/or derivatives and off-balance sheet activities (Apergis, 2014; Li & Marinc, 2014).

Second, all of these policies have been characterized in prior literature as carrying higher degrees of systematic risks—commercial loans due to their higher average rate of delinquency and default (Black & Hazelwood, 2013; DeYoung & Torna, 2013), and noninterest income activities as well as derivatives because they increase banks’ reliance on more volatile revenue streams (Apergis, 2014; DeYoung et al., 2013). However, due to their exaggerated self-confidence and sense of superiority (Emmons, 1987), narcissistic CEOs are convinced that they will be able to turn these policies into successes, and will thus pay less attention to the potential risks and downsides. In the same vein, their self-centeredness as well as their strong approach and weak avoidance motivation spurs narcissistic CEOs to focus (only) on the possibility of large rewards for themselves, while rendering them insensitive to the potential harmful consequences of increasing the inherent riskiness of banks for others, such as shareholders (e.g., Foster et al., 2011; Patel & Cooper, 2014). Based on these arguments, as a first hypothesis we propose

Hypothesis 1: CEO narcissism will be positively associated with the riskiness of a bank’s policies.

The Moderating Role of Corporate Governance Practices

Building on agency theory (e.g., Eisenhardt, 1989) CG scholars have identified two vital mechanisms to curtail (opportunistic) CEO behavior: incentives and control. Hence, we investigate three CG practices that either explicitly incentivize (narcissistic) CEOs to increase riskiness—that is, (a) CEO stock options—or give (narcissistic) CEOs more control through a lack of effective monitoring—that is, (b) reduced block ownership and (c) absence of knowledgeable and independent directors (see Figure 1).

CEO incentives

Both the popular press and academic studies have argued that certain compensation arrangements set by boards increase (bank) CEOs’ proclivity to pursue risk-enhancing strategies (e.g., Cerasi & Oliviero, 2015; DeYoung et al., 2013; Financial Crisis Inquiry Commission, 2011). A compensation arrangement that has been under particular scrutiny in this regard are stock options (Financial Crisis Inquiry Commission, 2011), as they reward CEOs for high performance but do not punish them for poor performance (e.g., Sanders, 2001; Tian & Yang, 2014). This, in turn, may make CEOs more likely to engage in strategies that have the potential (but not the guarantee) of big wins—such as strategies related to enhanced risk-taking. Nevertheless, the empirical evidence on the impact of executive compensation in general and stock options in particular is not clear-cut. In a conceptual piece Wowak and Hambrick (2010) proposed that because executives have diverging motives and drives, their reactions to the same compensation package might differ.

Drawing on Wowak and Hambrick (2010), we propose that a CEO’s tendency to increase the riskiness of policies when paid to a higher extent in stock options will be exacerbated the higher CEO narcissism, because of the specific features of a narcissistic personality—that is, a narrow-minded focus on personal rewards (Foster et al., 2011; Patel & Cooper, 2014), and an exaggerated self-confidence and assessment of one’s own abilities (Chatterjee & Hambrick, 2007; Emmons, 1987). Wowak and Hambrick (2010: 810) identify executives’ self-confidence as a critical factor affecting their responses to particular compensation packages noting that: “Highly confident executives will act vigorously in their attempts to attain rewards; those who lack confidence, or are unsure about whether their initiatives will bear fruit, may not respond to incentives as doing so entails extra effort, chances of setbacks, and career risks.”

Paying CEOs in stock options ties these CEOs’ personal wealth to their organization’s performance (Sanders, 2001). Hence, we would expect any CEO, but especially overconfident CEOs who are strongly driven by personal wealth, to engage in actions aimed at boosting firm performance (cf. Wowak & Hambrick, 2010). As narcissism combines overconfidence with a strong focus on personal rewards, we expect that stock options will represent a stronger incentive to increase risk, the more narcissistic the CEO. In line with this argument, Patel and Cooper (2014) found that option payoffs led CEOs that scored high on the narcissism scale to take greater risks. For bank CEOs, such risk-taking is likely to include higher investments in the more lucrative commercial loans (DeYoung et al., 2013) and increased involvement in financial innovations such as noninterest income (DeYoung & Torna, 2013) or derivatives and off-balance sheet activities (Li & Marinc, 2014). Taking these arguments together, we hypothesize

Hypothesis 2a: The relationship between CEO narcissism and the riskiness of policies will be more positive when the CEO’s amount of stock options is higher.

Monitoring

Numerous scholars have already indicated that individual CEOs’ degrees of freedom to affect organizational behaviors—that is, their managerial discretion—will be higher when these CEOs are not effectively monitored (e.g., Hambrick et al., 2015; van Essen, van Oosterhout, & Heugens, 2013; Zhu & Chen, 2015a). For instance, Tang, Crossan, and Rowe (2011) found that boards that effectively monitor weaken the ability of dominant CEOs to pursue deviant strategies. In the same vein, we expect that narcissistic CEOs will be more likely to increase the riskiness of their organizations’ policies when they are ineffectively monitored.

We examine the effects of block ownership, which is an especially relevant monitoring device as blockholders (De Haan & Vlahu, 2016)—that is, shareholders who hold at least five percent of outstanding shares (Grove, Patelli, Victoravich, & Xy, 2011)—can directly influence a firm’s decision-making because of the voting rights associated with their holdings. Thus, the higher the level of block ownership, the higher the chance that the CEO’s activities are actively and independently monitored (Cerasi & Oliviero, 2015). At the same time, block ownership results in concentrated ownership, which reduces the liquidity of the bank’s equity, leading to a higher risk exposure for the bank’s owners. Controlling owners—blockholders—then may seek ways to offset this increased risk exposure, for example, by restricting (narcissistic) CEOs’ tendency to pursue risky strategies (van Essen et al., 2013). As a result, we expect increased block ownership to reduce the ability of narcissistic CEOs to engage in risky policies. Thus, we hypothesize

Hypothesis 2b: The relationship between CEO narcissism and the riskiness of policies will be less positive when the level of block ownership is higher.

Zhu and Chen (2015b) introduce another monitoring-related factor that might mitigate narcissistic CEOs’ risk-taking strategies: directors’ background characteristics. In particular, they found that CEO narcissism led to more risk-taking spending when directors were more favorably disposed towards the CEO, for example, because of similarity in personality. In another study (Zhu & Chen, 2015a), they found that the combination of CEO narcissism and directors’ prior experience with acquisitions and international diversification negatively affected an organization’s engagements in these strategies. All of this underscores the relevance of studying directors’ characteristics as moderators of CEO narcissism’s effects.

In evaluating directors’ monitoring vigilance, CG scholars generally emphasize their independence, as well as their relevant expertise (e.g., De Haan & Vlahu, 2016). Following Hambrick et al.’s (2015) idea that the joint presence of multiple attributes increases individual directors’ monitoring vigilance, we propose that the presence of directors who are both outsiders and have experience in the banking industry will moderate the effect of CEO narcissism. Given the highly complex and opaque nature of banks (Grove et al., 2011), more knowledgeable directors—for example, because of their banking background—that are not part of the bank’s insider representation will be more successful in identifying potentially unsound and deviant strategies initiated by the bank’s CEO (Tang et al., 2011). As such, we expect that the presence of at least one of such knowledgeable outsider directors (Hambrick et al., 2015) will dampen narcissistic CEOs’ ability to pursue unduly risky strategies. In sum, we hypothesize

Hypothesis 2c: The relationship between CEO narcissism and the riskiness of policies will be more positive when there are no outside directors with banking experience.

Performance Consequences After the Shock

Irrespective of its underlying causes—exogenous or systemic—a substantial shock typically implies a severe drop in capital availability as well as a sharp plunge in market demand for all organizations affected by it (Chakrabarti, 2015). To explain the heterogeneity in firms’ abilities to still thrive despite the occurrence of such a shock, the literature on organizational resilience emphasizes the relevance of preshock features (van der Vegt et al., 2015) such as slack, in terms of resources that allow flexibility in rearranging and of “conceptual slack,” referring to “a willingness to question what is happening” (Sutcliffe & Vogus, 2003: 105). In the resilience literature (e.g., Aven, 2011), two distinct dimensions of resilience are commonly identified: (a) a system’s ability to endure a major disruption and (b) its capacity to bounce back. In line with this, we explore the effects of preshock CEO narcissism and riskiness of policies on two dimensions of resilience: the size of the drop in performance directly after the September 2008 collapse and the time it took to recover to preshock performance levels. Whereas the former is related to the immediate effects and reveals firms’ vulnerability to sudden disruptions, the latter refers to the longer-lasting effects and focuses on firms’ ability to restore their health.

Postshock performance drops

Chatterjee and Hambrick (2007) found that organizations with narcissistic CEOs had more extreme performance—big wins and big losses—and more fluctuating performance—big annual swings. They attributed this to narcissists’ preference for high-risk, high-return strategies. Similarly, Wales et al. (2013) found CEO narcissism to be related to greater performance variability, partially explained by their entrepreneurial orientation. In addition, given their low avoidance motivation, narcissistic CEOs are less inclined to hedge against potential threats, or to carefully monitor for potential signs of economic decline (Patel & Cooper, 2014). Hence, they manifest low levels of “conceptual slack” (Sutcliffe & Vogus, 2003).

All of this implies that contextual conditions, such as the macroeconomic environment, may strongly influence the performance of firms with highly narcissistic CEOs. Because of the high-risk, high-return strategies and limited hedging of these CEOs, they are probably the first to suffer from an economic shock (Aven, 2011; Patel & Cooper, 2014; Sutcliffe & Vogus, 2003). As an illustration, in an experiment that tracked the stock performance of participants’ investment portfolios during a stock market crash, Foster et al. (2011) found that highly narcissistic participants suffered more substantial losses shortly after the crash, precisely because they made more aggressive and riskier choices before the crash. We hypothesize

Hypothesis 3a: The higher preshock CEO narcissism, the larger its drop in performance immediately after a shock.

For the banks in our setting, one of narcissistic CEOs’ high-risk, high-return strategies is their enhanced engagement in risky policies (Hindmoor & McConnell, 2013). Scholars have indeed emphasized the high levels of systematic risks involved in these activities (e.g., Apergis, 2014; DeYoung et al., 2013). Large investments in noninterest income activities and off-balance sheet items (among which are mortgage-backed securities; DeYoung et al., 2013) are generally associated with higher earnings volatility and raise the risk of a bank not being able to cover its fixed costs of operating when revenues decline (DeYoung & Torna, 2013; Li & Marinc, 2014). Commercial loans, on the other hand, are associated with higher levels of credit risk and higher average rates of delinquency and default (DeYoung et al., 2013).

The September 2008 collapse represented a substantial economic shock—it caused capital markets to become squeezed (Bayazitova & Shivdasani, 2012) and banks’ revenue streams to run dry because of the high rate of failed loans (Financial Crisis Inquiry Commission, 2011). We expect that banks with more risky strategies before the collapse will have suffered worse performance losses afterwards. The higher investments in more risky policies intensified their vulnerability to sharp declines in revenues and capital accessibility. Hence, we hypothesize

Hypothesis 3b: The higher an organization’s preshock riskiness of policies, the larger its drop in performance immediately after a shock.

Postshock performance recovery

As for the ability to restore their performance levels, the resilience literature highlights the harmful effects of preshock strategies and investments that lock in organizations’ resources. Such strategies and investments often exhaust internal resources beyond slack, as well as limit their flexibility to restructure these resources (Sutcliffe & Vogus, 2003). However, a sufficient amount of internal resources and the ability to rearrange, transform, and adapt these resources to the uncertain and changed postshock economic conditions is crucial in enabling organizations to increase their performance levels again after a shock (Bayazitova & Shivdasani, 2012; Sutcliffe & Vogus, 2003). In a sample of manufacturing firms during the 1997 Asian economic shock, Chakrabarti (2015) indeed found that firms with lower slack resources experienced greater difficulties in growing after the start of the shock.

This reasoning comes close to a repeated (yet untested) claim in the CEO narcissism literature—that is, that narcissistic CEOs, with their risky strategies, tend to capitalize on short-term gains at the expense of long-run performance (O’Reilly et al., 2014). For instance, in their study in the pharma industry, Gerstner et al. (2013: 281) found that narcissistic CEOs were more prone to invest in biotechnology—at that moment an unconventional and alien, discontinuous, technology. This turned out to be a good investment, “but it is just as easy to picture narcissistic CEOs who invest aggressively in technologies that do not pan out and who severely damage their companies as a result.” Wales et al. (2013: 1047) call narcissistic CEOs “resource ‘hogs’ who take possession of whatever resources are accessible, even when such acquisitions might result in resource depletions that damage the effectiveness of firm objectives.”

Based on this, we expect that banks with more narcissistic CEOs before the shock found it harder to recover to preshock performance levels afterwards, because their preshock high-risk, high-return strategies locked in and depleted resources. In contrast, in a sample of manufacturing firms, Patel and Cooper (2014) found that CEO narcissism was associated with performance increases after an economic shock. They attribute this finding to the narcissistic CEOs’ riskier strategies and aggressive investments, even during the shock, which gave them a strategic advantage to recover in the postshock period. The authors do note, though, that the availability of slack resources and survival of the firm are important boundary conditions to their theory. These boundary conditions are, in fact, our point of departure—we argue that narcissistic CEOs will exhaust resources before the shock, making it harder for them to recover afterwards. Whereas lack of internal resources might not have been an especially challenging issue in industries where new capital could be raised from investors that value risky strategies, such as the industries in Patel and Cooper’s study, risk-taking (and aggressive investing) was heavily scrutinized and frowned upon in banking after the September 2008 shock (Bayazitova & Shivdasani, 2012). Hence, Patel and Cooper’s argument is unlikely to hold in our setting—that is, we anticipate that narcissistic bank CEOs will be less able to increase risk-taking after the shock because of resource depletion and lower risk-taking discretion for CEOs. We hypothesize

Hypothesis 4a: The higher preshock CEO narcissism, the slower its postshock recovery to preshock performance levels.

DeYoung et al. (2013: 180) described banks’ risky policies as requiring “fixed investments in expertise, location, interfirm contracting, marketing, and customer relationships.” Because of these fixed investments, preshock risky policies lock in and exhaust banks’ internal resources (Apergis, 2014), restraining banks’ flexibility after the shock (Sutcliffe & Vogus, 2003). While resource lock-in and depletion was not problematic when the economic outlooks were rosy (as banks could raise new capital in the public markets), the squeeze in the capital markets complicated this after September 2008 (Apergis, 2014; Bayazitova & Shivdasani, 2012). Hence, we expect preshock riskiness of policies to harm postshock recovery:

Hypothesis 4b: The higher an organization’s preshock riskiness of policies, the slower its postshock recovery to preshock performance levels.

Above we have suggested that both narcissistic CEOs and riskiness of policies will lead to larger performance drops (H3a-b) and slower recovery rates (H4a-b). Given that we hypothesized earlier that narcissistic CEOs will engage in riskier policies (H1), it is likely that the effect of CEO narcissism on both performance drops and recovery is partially mediated by riskiness of policies. We will investigate this possibility in our analyses below.

Setting and Sample

Setting and Timing: The U.S. Commercial Banking Industry

The setting of our study is the U.S. commercial banking industry (Standard Industrial Classification [SIC] codes 6021-6022). The riskiness in the policy portfolios of commercial banks displays a substantial degree of variance, as after the 1999 Gramm-Leach-Bliley Act many commercial banks engaged in investment banking activities to some degree (Cole & White, 2012).

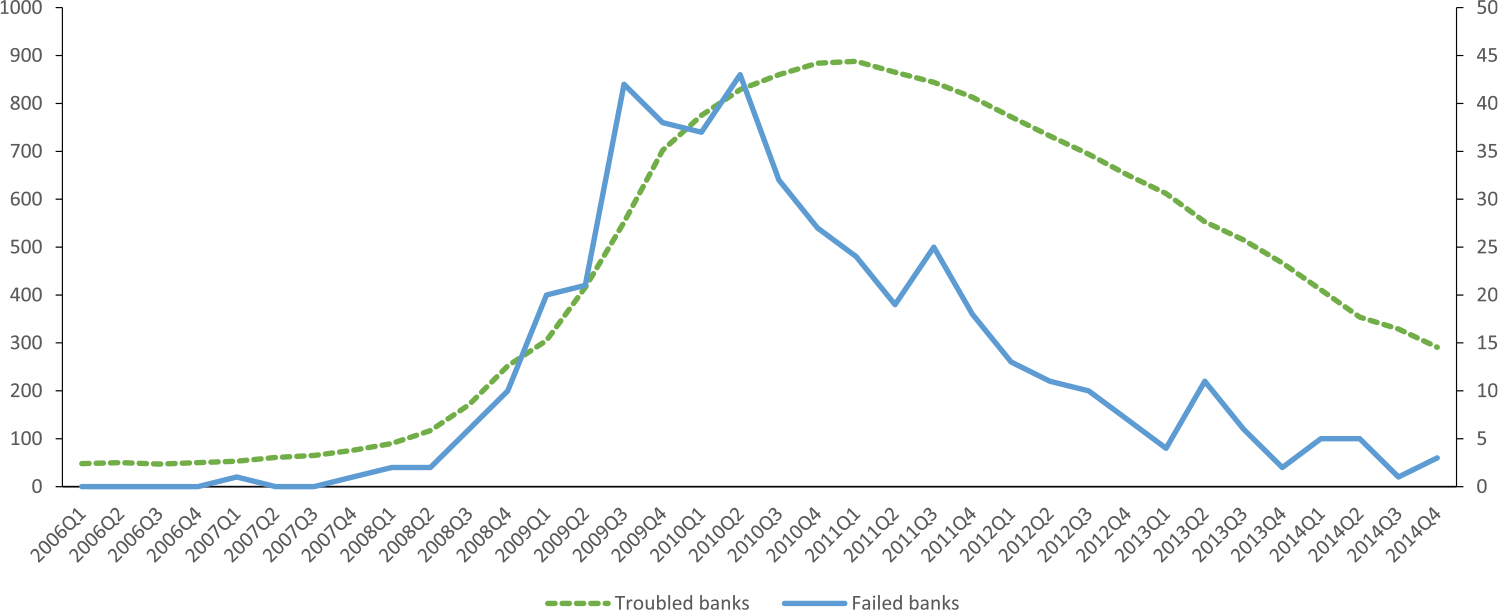

September 2008—with Lehman Brothers’ bankruptcy, Merrill Lynch’s takeover, and AIG’s rescue—marked the moment that the surging crisis turned into a collapse of the U.S. banking industry and a full-blown global crisis (e.g., Financial Crisis Inquiry Commission, 2011; Hindmoor & McConnell, 2013). September 2008 is therefore considered as the moment the systemic shock took place in our setting. Figure 2, which shows the numbers of troubled and failed banks, clearly exemplifies the September 2008 systemic shock: Both numbers started to increase sharply after the second quarter of 2008 (DeYoung & Torna, 2013). In October 2008, shortly after this shock, the U.S. government decided to support the banking industry with capital injections through the Troubled Asset Relief Program (TARP) (Black & Hazelwood, 2013).

Number of Troubled (left axis) and Failed (right axis) U.S. Commercial Banks

Sample

Consistent with past research, we restrict our sample to CEOs of banks in the Compustat (Banks) database with headquarters in one of the 50 U.S. states. We started data collection in the first quarter of 2006, 1 when signs of a looming crisis might have become evident for some players, but well before the actual systemic shock of September 2008 (Financial Crisis Inquiry Commission, 2011). We restricted our sample to banks that did not fail (went bankrupt or were acquired) before the systemic shock, and we followed these banks until 2014 (or until they failed if this was before 2014) so as to assess the performance consequences after the shock.

For the 484 banks that were in Compustat in the years 2006 to 2008, we sought to collect three yearly documents (annual reports containing a “letter to shareholders,” form 10Ks, and proxy statements) and complemented these with quarterly data from the Federal Reserve Y-9C database. The latter contains information based on the Y-9C reports, comprising quarterly data for large U.S. bank holding companies (DeYoung et al., 2013). As our independent variable, CEO narcissism, is based partially on information from banks’ letters to shareholders, we only retained banks in the sample if we were able to collect these documents. After an exhaustive search process on websites of the banks themselves and the SEC, this resulted in an initial sample of 105 banks. We further excluded seven more banks that had undergone a change in CEO in the pre-crisis period, and six banks because we were unable to collect quarterly data, setting our final sample at 92 bank CEOs. T-tests indicated that the size (in 2006) of these 92 banks was not significantly different from the 392 excluded Compustat banks but that they did perform slightly better in that year. However, the difference in performance was rather small (with an average ROA of 1.1% for the sample banks versus 1.0% for excluded banks). Our sample contains nine banks (9.8%) that failed in the period 2009 to 2011, which is lower than the 18.0% of banks that failed in the whole Compustat database (87/484). Hence, our sample might be biased towards better performing banks. To account for this, we control for selection bias in our analyses (see below). The average bank in our sample was 68.3 years old in 2006, had total assets of $42 billion in that year, and had a 56.3-year-old CEO with a tenure of 8.16 years.

Below, we present the empirical tests of our theoretical predictions. Because we set out to explain three different phenomena (preshock riskiness of policies, postshock drop in performance, and postshock recovery rate), and because we use different techniques and methods to do so, we present our methods and results for each dependent variable separately. Following these three sections, we conclude by discussing the whole set of results.

Empirics Part 1: Explaining Banks’ Riskiness Before the Shock

Measures

Dependent variable: Riskiness of policies

Consistent with prior research (e.g., Apergis, 2014; DeYoung et al., 2013; Li & Marinc; 2014), we identify three items related to the inherent riskiness of banks’ policies: commercial and business loans (relative to total assets), noninterest income (relative to net operating income), and derivatives and off-balance sheet items (relative to total assets). All items were measured on the quarterly level and were found in the Federal Reserve Y-9C database. As an illustration, in 2006 the banks in our sample had an average score of 0.12 (SD = 0.07) for the commercial and business loans measure, 0.24 (SD = 0.12) for noninterest income, and 0.20 (SD = 0.17) for derivatives and off-balance sheet items. We standardized each of the items relative to the banks in our sample, and we took the average of the three standardized items to compute our “riskiness of policies” index.

Independent variable: CEO narcissism

Chatterjee and Hambrick (2007, 2011) were the first to suggest using unobtrusive indicators from archival data to measure CEO narcissism. Several scholars (e.g., Engelen et al., 2016; Gerstner et al., 2013; Patel and Cooper, 2014) have replicated Chatterjee and Hambrick’s methods, while Rijsenbilt and Commandeur (2013) suggested several alternative measures, also based on objective and easily available information. Based on Chatterjee and Hambrick’s (2007, 2011) and Rijsenbilt and Commandeur’s (2013) suggestions, we identified six potential measures for CEO narcissism: (a) the prominence of the CEO’s photograph in the annual report (on a 4-point scale, depending on its size and whether it showed the CEO alone or together with others); 2 (b) the CEO’s cash compensation and (c) the CEO’s total compensation, both relative to that of the second most highly compensated executive; (d) the relative use of first-person singular pronouns (I, me, my, …) versus first-person plural pronouns (we, us, our, …) in the letter to shareholders; 3 (e) the number of signatures under the letter to shareholders (reversed); and (f) the number of words in the CEO’s Marquis Who’s Who biography. The former four items were suggested by Chatterjee and Hambrick (2007, 2011); the latter two were based on Rijsenbilt and Commandeur’s (2013) suggestions. In line with Patel and Cooper (2014), all items were measured in 2006.

A correlation analysis (available upon request), however, revealed a rather puzzling pattern. Though the CEO’s relative (cash and total) pay was a vital component of the scales of both Chatterjee and Hambrick (2007, 2011) and Rijsenbilt and Commandeur (2013), in our sample the pay-related items were either not or even negatively correlated with the other items. Moreover, in a nontrivial number of cases, the CEO actually earned less than the second most highly paid executive (14.5% for total pay). This peculiarity might be a consequence of the high amount of government regulations to which bank executives’ compensation packages are subject (Black & Hazelwood, 2013). Hence, executive compensation in the banking industry may be less under the (narcissistic) CEO’s discretion—or in any case less so than in other industries used in CEO narcissism studies, such as the computer (Chatterjee & Hambrick, 2007, 2011), biotech (Gerstner et al., 2013), or high-tech industry (Engelen et al., 2016), or in manufacturing firms (Patel & Cooper, 2014). A principal components analysis (available from the authors upon request) further suggested that the six items loaded on two different components, the first one comprising the four items not related to compensation, and the second one containing the two pay-related items. Therefore, we decided to exclude both pay-related items. We operationalized “CEO narcissism” as the average of the standardized values of the items (relative to the sample). In line with research in psychology that sees narcissism as a stable personality trait (Emmons, 1987) this measure was relatively constant over time and reactive to CEO succession. 4

To check the validity of our “CEO narcissism” measure, we used content analysis of banks’ letters to shareholders (signed by the CEO). First, using a dictionary developed and validated by Short, Broberg, Cogliser, and Brigham (2010), we see that our CEO narcissism measure is strongly correlated with “entrepreneurial orientation” in the letter to shareholders (.33; p < .001). This resonates with prior findings that narcissistic CEOs are more inclined to lead their organization towards such an orientation (Wales et al., 2013). Second, we used the standardized categories in LIWC, a content analysis software that has been used extensively to tap “the psychological meanings of words” (Pennebaker, Chung, Frazee, Lavergne, & Beaver, 2014). Our measure of CEO narcissism appears to be related to a more narrative and less facts-based style, 5 and also to more self-assurance. 6 Taken together, this corresponds to the image of the narcissistic CEO as a confident storyteller, who is concerned about passing on a story more than about precision and facts. The results also suggest that more narcissistic CEOs have slightly higher degrees of achievement orientation (.10; p < .10) and lower degrees of risk aversion (–.13; p < .10), which aligns with the idea of a narcissistic CEO who is focused on achieving successes and cares less about the potential negative consequences of risk-taking. This complements prior validation efforts, which show that CEO narcissism as measured by archival measures is highly correlated with stock analysts’ and clinical psychologists’ ratings of a set of randomly chosen CEOs (Patel & Cooper, 2014), as well as with psychology doctoral students’ ratings of video-clips of CEOs’ speeches (Petrenko, Aime, Ridge, & Hill, 2015).

Moderators: Corporate governance practices

First, we follow Hou, Li, and Priem (2013) and include a measure of CEOs’ accumulated stock options: “CEO options” represents CEOs’ number of unexercised exercisable options. Compensation data was collected manually from banks’ proxy statements. Given the skewness of the “CEO options” variable, we used a logarithmic transformation. Second, we obtained block ownership from banks’ proxy statements. Following prior scholars (e.g., Grove et al., 2011) we operationalized “block ownership” as the proportion of outstanding shares owned by all blockholders—that is, shareholders who hold at least 5% of a firm’s outstanding shares—together. Finally, the information needed to calculate the “presence of outsider directors with banking experience” was found under the individual directors’ biographies in banks’ proxy statements. Our measure is a dummy variable that equals one when at least one director is present who both is outside director and has prior experience in the banking industry (either as director or as employee) (cf. Grove et al., 2011; Hambrick et al., 2015). Note that in boards that counted at least one outsider director with banking experience, the total number of such directors is generally very low (in our sample, in 91% of the cases their number was two or less), which justifies our use of a dummy variable.

Control variables

We include control variables at different levels of analysis. First, we control for the bank’s riskiness of policies at the outset of our time frame (2006Q1), which represents the bank’s “starting conditions.” Second, to account for the overall economic conditions, we use the state-level quarterly growth in the Federal Housing Finance Agency’s house price index (“growth in house price index”), and we also include quarter-level time dummies. Third, we included three bank-level controls. In line with other researchers in the banking industry (e.g., DeYoung et al., 2013), we measured “bank size” as the natural logarithm of total assets. As theory on performance feedback suggests that the gap between historical and current performance levels instigates risk-taking (Greve, 2003), we control for “performance aspiration gap,” measured as banks’ current performance minus that in t – 1. Furthermore, prior studies in the U.S. commercial banking industry suggested that different institutional logics exist for banks (Marquis & Lounsbury, 2007). To capture this difference, we include a 6-point “urban/rural indicator” to assess the degree of urbanization of the county of the bank’s headquarters, based on the National Center for Health Statistics’ 2013 classification, which is related to the difference in logics. A lower value for this indicator refers to a higher degree of urbanization. Finally, we control for five variables related to banks’ executives and board: “CEO duality” (a binary variable equaling one if the CEO was also the chairperson of the board) as an indicator of CEOs’ power (Zhu & Chen, 2015b), and “CEO position tenure,” “top management team (TMT) tenure diversity” (the standard deviation of the years TMT members served in the bank), “board mean tenure” (the average years directors served in the board), and “board tenure diversity” (the standard deviation of the years board members served in the board) as prior research has indicated that executives’ and directors’ tenure is often related to their risk-taking inclinations (Grove et al., 2011).

Sample selection and endogeneity check

As our sample is only a subset of the total population of U.S. commercial banks in Compustat, and as our sample might be biased towards the better-performing banks (see above), we check for sample selection bias. We do this by using a two-stage self-selection model based on Heckman’s (1990) suggestions. In the first step, we use an indicator of bank size (natural logarithm of total loans) and performance (return on assets [ROA]) in a panel probit regression to predict inclusion in our sample. In the next step, we calculated the inverse Mill’s ratio derived from the predicted scores in the first step. This inverse Mill’s ratio is subsequently used as a “control for sample selection” in the regressions.

Furthermore, in line with other CEO narcissism studies (Chatterjee & Hambrick, 2007, 2011), we control for potential endogeneity. More precisely, we acknowledge that the decision to hire narcissistic CEOs might have correlated with the decision to build a more risky portfolio of policies. Hence, there may have been specific CEO- and firm-level variables that led to systematic differences in both the selection of narcissistic CEOs and the subsequent riskiness of bank policies. We account for this by trying to partial out that part of our narcissism measure that is the result of such variables (to get rid of unobserved heterogeneity). Following prior scholars (e.g., Chatterjee & Hambrick, 2011; Patel & Cooper, 2014), we regress our narcissism measure against carefully chosen CEO- and firm-level variables 7 related to the conditions that might have affected narcissistic CEOs’ selection in the first place and that, in turn, might be responsible for the riskiness of banks’ policies afterwards (analyses available from the authors). We then use the regression coefficients of the significant variables to calculate each CEO’s predicted narcissism score and include that value as an “endogeneity control” in all analyses.

Estimation Method

To test Hypothesis 1 and 2a-c, we used random-effects panel models with robust variance estimators to calculate the standard errors. Fixed-effects models were not appropriate because our key independent variable (“CEO narcissism”) is time-invariant. Given that the start of the time frame of our data collection was the first quarter of 2006, and given that the riskiness of banks’ policies is measured with a one-quarter lag, we were able to test Hypotheses 1 and 2a-c for 10 subsequent quarters (i.e., independent variables measured between 2006Q1 and 2008Q2, dependent variable between 2006Q2 and 2008Q3).

Results

Hypothesis tests

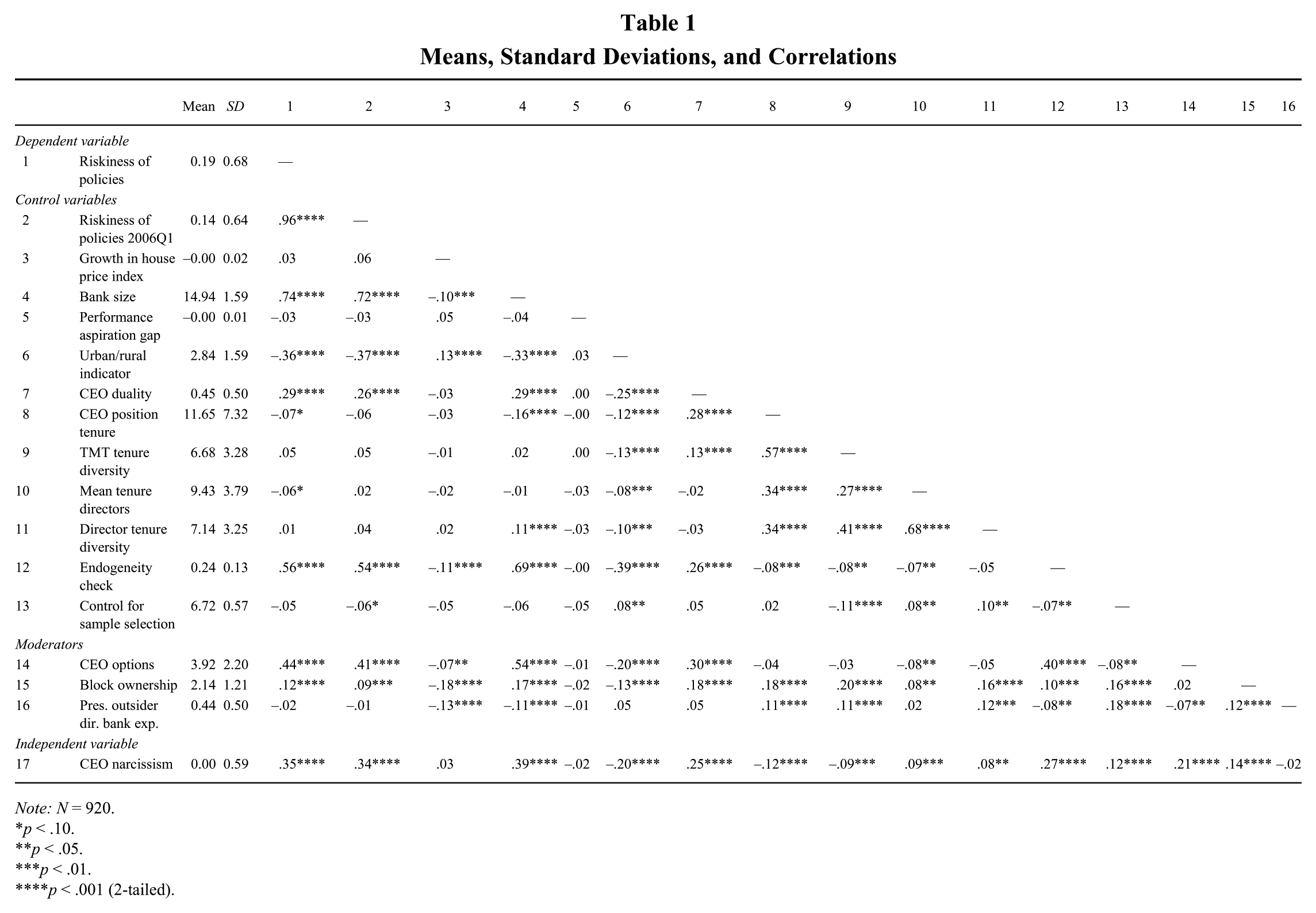

Table 1 shows the means, standard deviations, and correlations. The correlation between “CEO narcissism” and “riskiness of policies” is positive and significant (.35; p < .001), as expected. Table 2 presents the regression results. Model 1 includes control variables and moderators only. It appears that riskiness of banks’ policies in 2006Q1 is a strong predictor of its risky policies later on (B = .95; p < .001). Riskiness also increases with “TMT tenure diversity” (B = .01; p < .10) and decreases with “mean tenure directors” (B = –.01; p < .05).

Means, Standard Deviations, and Correlations

Note: N = 920.

p < .10.

p < .05.

p < .01.

p < .001 (2-tailed).

Random-Effects Regression Estimates of CEO Narcissism and Moderators on Riskiness of Policies

Note: Robust standard errors are in parentheses. N = 920.

p < .10.

p < .05.

p < .01.

p < .001 (2-tailed).

“CEO narcissism” is introduced in Model 2. As expected, “CEO narcissism” positively affects riskiness of policies (B = .06; p < .05), supporting Hypothesis 1. In practice, this means that a one-SD increase in CEO narcissism predicts a 5.40% SD increase in riskiness.

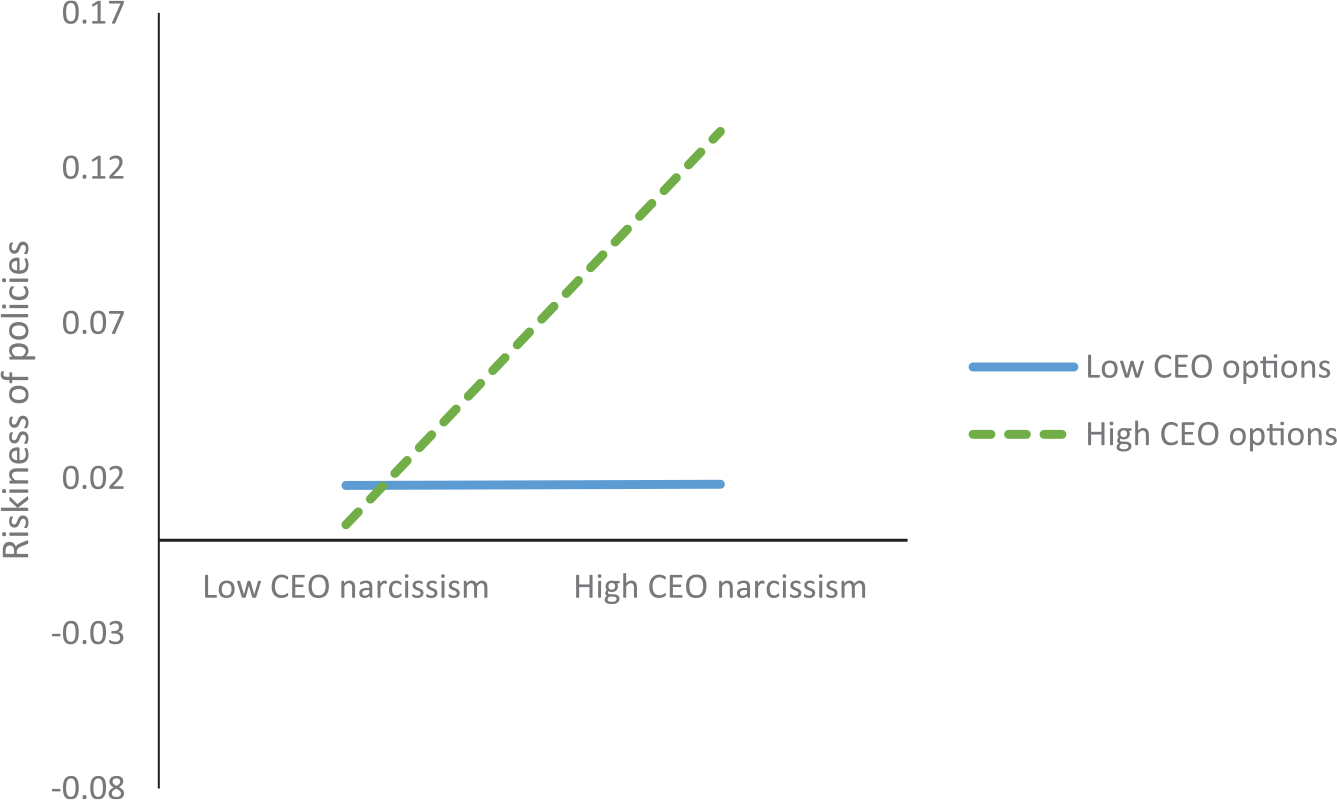

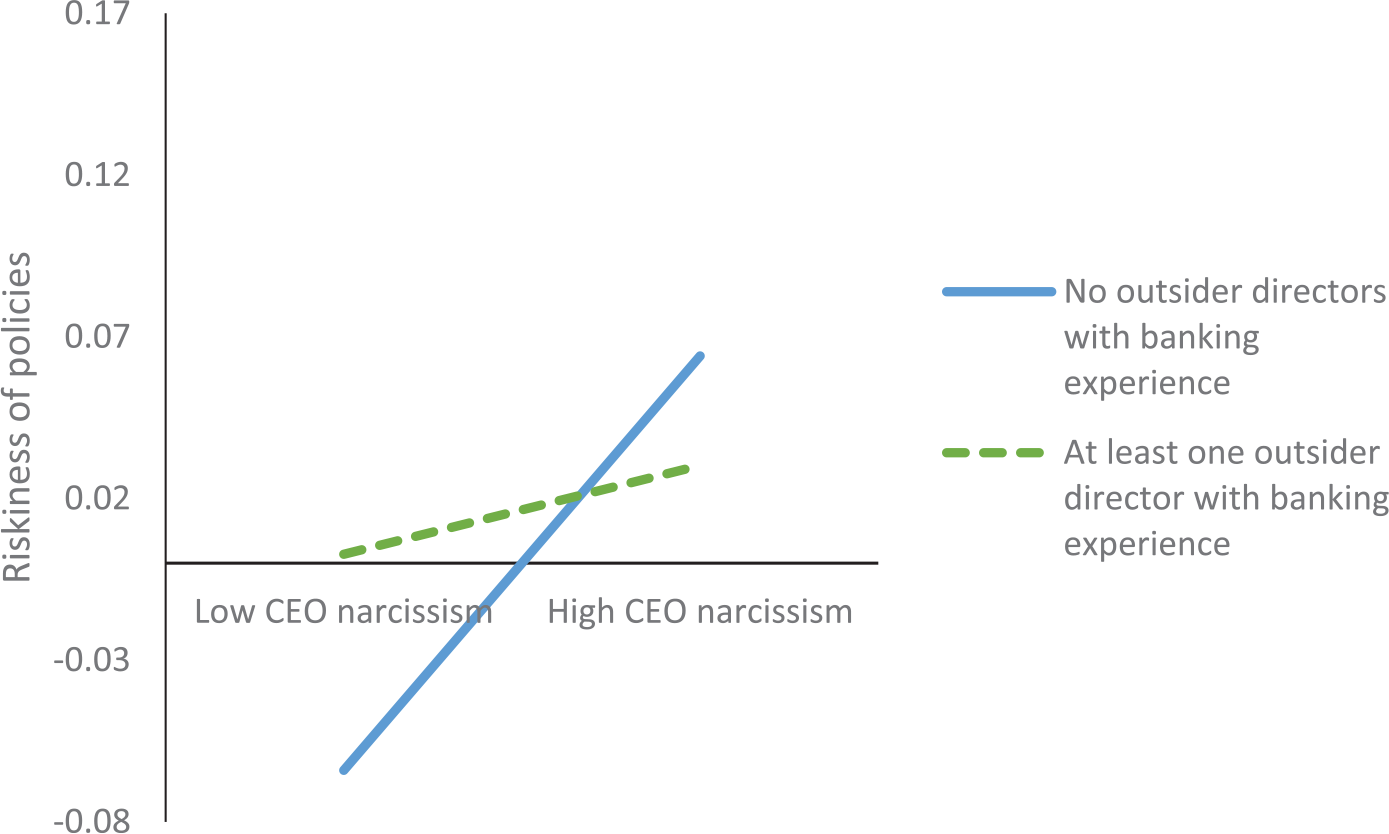

Hypothesis 2a, on the interaction of “CEO narcissism” and “CEO options,” is tested in Model 3. This hypothesis is supported, with a positive and significant interaction coefficient (B = .03; p < .10). Ceteris paribus, a one-SD increase in CEO narcissism relates to only a 0.87% SD increase in risky policies when CEO options are low (mean minus one SD), but a 10.62% SD increase when CEO options are high (mean plus one SD). We fail to find support for Hypothesis 2b. While the coefficient of the interaction of “CEO narcissism” and “block ownership” is negative as expected, it is only significant in the full model (Model 6), but not in Model 4. Model 5 supports Hypothesis 2c; the interaction coefficient of “CEO narcissism” and “presence of outsider directors with banking experience” is negative and significant (B = –.09; p < .05). All else equal, a one-SD increase in CEO narcissism predicts a 6.57% SD increase in banks’ risky policies when no outsider director with banking experience is present, but only a 2.84% SD increase otherwise. Both significant interactions also hold in Model 6, which includes all moderating effects simultaneously. Figures 3 and 4 plot both significant interactions. Together, the figures suggest that, as we expected, CEO narcissism is positively related to the riskiness of banks’ policies, and that this effect is stronger when CEOs are granted more stock options and when there are no outsider directors with banking experience.

Interactions of CEO Narcissism and Moderators on Riskiness of Banks’ Policies: CEO Options

Interactions of CEO Narcissism and Moderators on Riskiness of Banks’ Policies: Presence of Outside Directors with Banking Experience

Robustness checks

We performed two sets of robustness tests (all analyses are available upon request). First, we reran all models using a different approach for panel regressions: the (population-averaged) generalized estimating equations (GEE) method, which allowed us to specify the models with a first order autoregressive correlation structure. Second, we reran all analyses using different sets of control variables, such as board size. In addition, we ran the analyses without controlling for banks’ riskiness of policies at the outset of the time frame. Though in the robustness checks some of the significance levels drop slightly, the general pattern of our findings appears to be fairly robust. The analyses reported here include the control variables that led to the highest overall model fit (Wald χ2 and R2).

Empirics Part 2: Explaining Postshock Performance Drops

Measures

Dependent variables: Drop in performance

We operationalize bank performance as ROA, as has been done in numerous other studies (De Haan & Vlahu, 2016). An interview with a former board member of a large international bank as well as a careful read through of banks’ letters to shareholders also confirmed the relevance of ROA for banks. Because banks are highly leveraged institutions, their ROA numbers are generally substantially lower than those of companies in more classical industries. We therefore divided all ROA-related variables by 100 to facilitate our interpretation of the coefficients.

In our analyses to test Hypotheses 3a-b, the dependent variable is the drop in performance immediately after the September 2008 shock—or the end of the third quarter of 2008 (2008Q3). Due to substantial seasonality in banks’ ROA patterns—mostly driven by a parallel seasonality in interest rates—and in line with the standard guidelines (European Central Bank, 2010), we assess drops in ROA based on yearly, and not quarterly differences. Drop in performance is therefore operationalized as a bank’s ROA in 2008Q3 minus its ROA in 2009Q3. Note that 2009Q3 also corresponds to the lowest point in ROA in the U.S. commercial banking industry—2009 is generally seen as the year the industry hit rock bottom (Cole & White, 2012). To illustrate, the average ROA in our sample dropped 177% between 2008Q3 and 2009Q3, from 0.4% in 2008Q3 to −0.3% in 2009Q3, which represents a highly significant drop (p < .001).

Independent variables: CEO narcissism and riskiness of policies

“CEO narcissism” and banks’ “riskiness of policies” are operationalized as outlined above. As we are particularly interested in how preshock indicators affect banks’ performance after the shock, both independent variables were measured before the systemic shock—that is, “CEO narcissism” was measured in 2006, as explained above; and “riskiness of policies” was measured in 2008Q2.

Control variables

We use three sets of control variables. First, we include the “starting conditions,” referring to the value of several key variables at the start of the time frame—that is, the moment of the shock (2008Q3). They might have affected after-shock performance, by harming banks’ resilience to shocks (van der Vegt et al., 2015). For this reason, we include “ROA 2008Q3” (also to account for regression to the mean), “growth in house price index 2008Q3” at the state level, “bank size 2008Q3,” the “urban/rural indicator,” “CEO options 2008,” “block ownership 2008,” and “presence of outsider directors with banking experience 2008.” Second, we account for alternative explanations by including changes in several key variables from 2008Q3 to 2009Q3; we include the “drop in growth in house price index 08-09” to account for changes in the macroeconomic conditions, and “drop in bank size 08-09” as this might also be related to performance drops. Finally, to control for endogeneity and sample selection bias, we include the “endogeneity check” (see above) and an inverse Mill’s ratio as a “control for sample selection,” using the “logarithm of total loans” and “ROA” in the predict function (cf. Heckman, 1990).

Results

Hypothesis tests

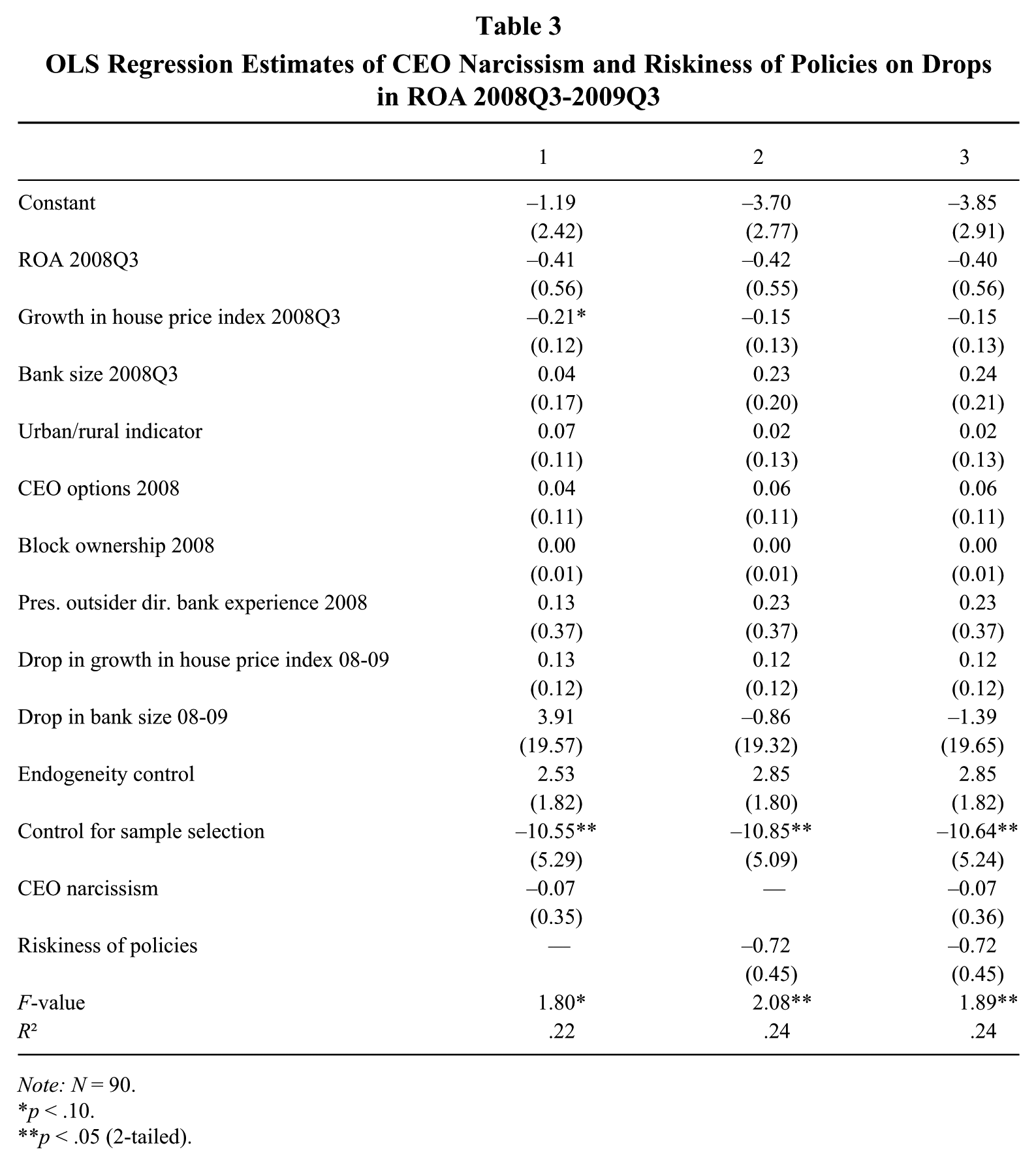

Table 3 depicts the ordinary least squares (OLS) regressions used to test Hypotheses 3a-b. Note that the sample size dropped to 90 because two banks failed between 2008Q3 and 2009Q3. We do not find support for our predictions; the coefficients of both “CEO narcissism” (see Models 1 and 3) and “riskiness of policies” (see Models 2 and 3) are not significant. Hence, Hypotheses 3a and 3b are rejected; neither the CEO’s degree of narcissism, nor the bank’s preshock riskiness of policies, appear to affect the performance drop shortly after the shock. One explanation for this lack of findings might be that the shock in our setting was so strong and the overall performance drop was so severe for the whole industry (as indicated above) that it applied to every bank in the short run (irrespective of CEO narcissism or riskiness of policies).

OLS Regression Estimates of CEO Narcissism and Riskiness of Policies on Drops in ROA 2008Q3-2009Q3

Note: N = 90.

p < .10.

p < .05 (2-tailed).

Robustness checks

To assess their robustness, we reran all analyses without preshock ROA (available upon request). Excluding this variable does not alter any of our results. We also checked whether the results remained the same if we used other quarters to assess ROA (e.g., 2008Q2 instead of 2008Q3 and 2009Q4 instead of 2009Q3), or yearly averages of ROA instead of quarterly performance levels to measure the drops in performance (analyses available upon request). Again, our results remained robust.

Empirics Part 3: Explaining Postshock Performance Recovery

Measures

Dependent variable: Recovery to preshock performance level

To test Hypotheses 4a-b, we assess how CEO narcissism and riskiness of policies affect the rate at which banks’ performance returns to preshock levels. We use a hazard model approach to see whether and when banks had recovered over the whole time frame after 2008Q3 (until 2014Q3—the last year for which data were available at the moment of data collection). Banks were seen as having experienced “recovery” at the first year that their ROA in the third quarter equaled or surpassed their ROA level in 2008Q3. Note that, as explained above, patterns in banks’ ROA should be evaluated based on yearly rather than quarterly differences (European Central Bank, 2010). This also means that the spells in our hazard models are defined at the yearly level. The total number of spells is 298, with 70 banks that recovered within the time frame under study and 6 banks that failed (went bankrupt) before recovering to their pre-crisis ROA level.

Independent variables CEO narcissism and riskiness of policies

Here, too, “CEO narcissism” and banks’ “riskiness of policies” were operationalized as outlined above, and both independent variables were measured before the systemic shock (2006 for “CEO narcissism” and 2008Q2 for “riskiness of policies”).

Control variables

Our set of control variables is similar to that in the second set of analyses: To account for banks’ starting conditions, we include “ROA 2008Q3,” “growth in house price index 2008Q3,” “bank size 2008Q3,” the “urban/rural indicator,” “CEO options 2008,” “block ownership 2008,” and “presence of outsider directors with banking experience 2008.” To account for the change in key variables, we include the contemporaneous (time-varying) “growth in house price index – cont.” and “growth in bank size – cont.” Moreover, to factor in changes in banks’ riskiness of policies after the shock, we also include “growth in riskiness of policies – cont.,” measured as the difference between banks’ contemporaneous riskiness of policies and that in 2008, relative to 2008. In addition, we also control for the U.S. government’s capital injections banks received through the Troubled Asset Relief Program (TARP) (Bayazitova & Shivdasani, 2012), as we conjectured that these capital injections might have affected their recipients’ ability to restore performance levels. Note that TARP was voluntary and did not only attract distressed banks. Some healthier banks saw the program as a relatively easy and cheap way to obtain new capital (Cornett, Li, & Tehranian, 2013). Our measure of “TARP funds” is the amount of funds received through TARP divided by the banks’ total assets.

Estimation Method

Parametric survival-time models (with an exponential distribution) are used to estimate the effects of “CEO narcissism” and “riskiness of policies” on the hazard of banks’ recovery to pre-crisis performance levels. We use robust variance estimators to calculate standard errors and a gamma frailty distribution to account for unobserved heterogeneity.

Results

Hypothesis tests

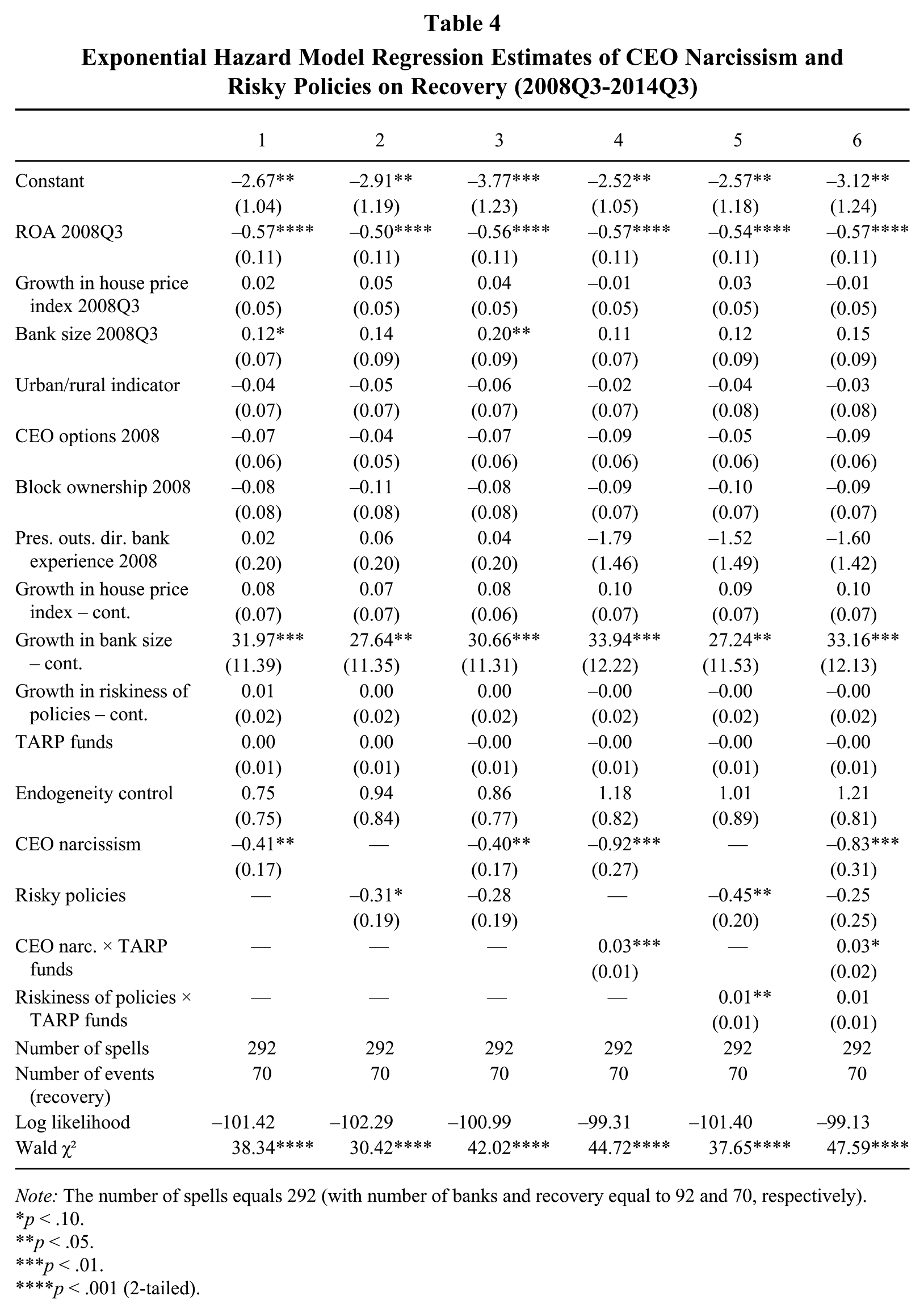

Table 4 shows that “CEO narcissism” has a negative and significant effect on the hazard of recovery (B = –.41; p < .05; Model 1), as expected. A one-SD increase of CEO narcissism corresponds to a drop in the recovery rate of 21.54%. 8 We also find a negative effect of banks’ preshock “riskiness of policies” (B = –.31; p < .10; Model 2)—meaning that a one-SD increase in riskiness relates to a drop in the recovery rate of 19.09%. 9 These results suggest that both preshock CEOs’ narcissism and riskiness of policies slow down and hamper banks’ recovery after the occurrence of the shock, in line with what we hypothesized.

Exponential Hazard Model Regression Estimates of CEO Narcissism and Risky Policies on Recovery (2008Q3-2014Q3)

Note: The number of spells equals 292 (with number of banks and recovery equal to 92 and 70, respectively).

p < .10.

p < .05.

p < .01.

p < .001 (2-tailed).

Though we did not formally propose that the effect of CEO narcissism would be mediated by the riskiness of policies, our argumentation implied partial mediation—that is, we argued that CEO narcissism would hamper recovery because of narcissistic CEOs’ more risky strategies (e.g., resulting in a more risky portfolio of policies). Model 3 (Table 4) suggests that “CEO narcissism” has a direct effect on recovery, as its coefficient remains significant when controlling for “riskiness of policies.” In addition, a Sobel test indicates the existence of a marginally significant indirect effect of “CEO narcissism” through “riskiness of policies” (z = −1.66; p < .10). Using Zhao, Lynch, and Chen’s (2010) decision tree, these results suggest partial, complementary mediation. Hence, increased riskiness of policies is one, but not the only way in which CEO narcissism debilitates organizations’ recovery. Narcissistic CEOs might be expected to pursue a variety of resource-depleting strategies and decisions, of which investments in risky policies is but one. Others could, for instance, involve bold (and expensive) acquisitions, or high levels of capital expenditures (see, e.g., Chatterjee & Hambrick, 2007, 2011).

Post hoc analysis: The role of TARP funds

To further explore the issue of resource depletion—which we saw as the main mechanism to explain the harmful effects of preshock CEO narcissism and riskiness on performance recovery—we take a closer look at the funds provided by the U.S. government to banks through TARP. Bayazitova and Shivdasani (2012: 377) wrote, “During a financial crisis, capital levels of banks are depleted and raising new capital in public markets is difficult. A government capital injection program can stabilize banks by providing a source of capital when public market alternatives are unavailable.” Hence, if resource depletion is indeed the mechanism that drives the negative effects of CEO narcissism and riskiness on banks’ recovery, the receipt of TARP funds should moderate the effects of “CEO narcissism” and “riskiness of policies” on recovery, so that the negative effects are less pronounced for TARP recipients—that is, the resource depletion issue should be (partially) solved when banks are bailed out through the injection of TARP funds.

We test this idea by including the interaction of “CEO narcissism” and “riskiness of policies” with “TARP funds” in Table 4. As expected, we find that “TARP funds” positively moderates both the effect of “CEO narcissism” (B = .03; p < .01; Model 4) and “riskiness of policies” (B = .01; p < .05; Model 5). These results indicate that CEO narcissism and preshock riskiness of policies will have less severe consequences for recovery to preshock performance levels when banks are bailed out through a governmental capital injection. In particular, for banks that did not receive a capital injection, a one-SD increase in CEO narcissism results in a 41.88% drop in the likelihood of recovery; while with a one-SD capital injection, it only results in a 19.09% drop. In the same vein, without capital injection, a one-SD increase in riskiness results in a 26.28% drop in recovery, as compared to a 17.15% drop with a one-SD capital injection. Model 6 includes the interactions of both “CEO narcissism” and “riskiness policies” with “TARP funds” simultaneously. Both interactions drop in significance. This might not be that surprising, given that they, in fact, represent two sides of the same coin—that is, both refer to the same process of resource depletion being “resolved” through a TARP capital injection.

Robustness checks

In order to assess their robustness, we reran all analyses without preshock ROA and controlling for changes in the three corporate governance indicators. We also redid the analyses using Cox proportional hazard models (all analyses are available from the authors upon request). Our results did not substantively change.

Discussion

Why were some U.S. commercial banks hit hard by the September 2008 collapse, while others managed to recover fast? What was the role of CEOs and CG practices in this respect? To answer these questions, we developed a theoretical model that integrated insights of the UE and CG literatures with the emerging literature stream on organizational resilience. As we expected, we found that CEO narcissism was associated with higher risk-taking—reflected in the riskiness of banks’ policies. Moreover, echoing classic agency theory predictions (e.g., Eisenhardt, 1989), we found that this baseline effect was even stronger when narcissistic CEOs were explicitly incentivized towards risk-taking (through stock options), but weaker when these CEOs were more effectively monitored (through the presence of knowledgeable outsider directors). Hence, our findings suggest that it is the combination of CEO narcissism and specific CG practices that leads towards (excessive) risk-taking. More positively, these findings also imply that an organization’s CG policies can make a real difference in reining in narcissistic CEOs.

We subsequently found that recovery after the September 2008 collapse was slower in banks with a more narcissistic CEO, and that this effect was partially mediated by banks preshock riskiness of policies. We explained these findings through the mechanism of the depletion of internal resources because of (risky) investments made before the shock. This was, in fact, backed by post hoc analyses that showed that the negative effects of CEO narcissism and riskiness of policies on the hazard of recovery were mitigated for banks that received a capital injection from the U.S. government. Indeed, following our logic, these capital injections allowed TARP recipients to (partially) replenish their depleted internal resources. We found no evidence, however, of an effect of either CEO narcissism or riskiness of policies on performance drops immediately after the shock. As mentioned above, this might be due to the gravity of the shock in our study—that is, the collapse was so grave that the whole industry suffered severe performance losses immediately afterwards, making the effects of differences in bank CEOs’ narcissism and/or riskiness of policies less relevant. In the longer run, however, the harmful effects of CEO narcissism and riskiness of policies kicked in, resulting in a slower recovery.

Contributions and Implications

With this study we contribute to different streams of literature. First, we add to the organizational resilience literature by exploring new sets of antecedents. Our findings suggest that CEOs, together with CG practices, are important predictors of organizations’ (long-run) resilience. Uncovering the antecedents of resilience is highly relevant, as it leads to a better understanding of organizational continuity and survival during adverse events (van der Vegt et al., 2015). While system-wide shocks, such as the one we studied, are relatively rare, shocks and events that damage single industries or even individual organizations occur far more often.

Second, by emphasizing the combined effects of CEO narcissism and CG practices, we add to both the UE and CG literatures. Several UE scholars (e.g., Busenbark et al., 2016) have already proposed that the effects of executive characteristics are generally not straightforward but are driven by contextual conditions. In the same vein, CG scholars have indicated that the performance effects of most CG are not unequivocal (e.g., Grove et al., 2011). Wowak and Hambrick (2010) even exactly called for empirical research on the interaction between executives’ characteristics and pay policies. Hence, we contribute to both the UE and CG literatures by exploring the interactive effects of CEO narcissism and CG practices.

Third, we also contribute to both the UE and the CG literatures by focusing on longer-run effects, which have been generally underexplored. For the growing CEO narcissism literature, the immediate (short-run) performance effects are a much debated topic, including the ongoing debate about the bright and dark sides of CEO narcissism (Wales et al., 2013). However, an increasing amount of scholars have (implicitly) alluded to the fact that CEO narcissism could also have important longer-lasting harmful effects (e.g., Chatterjee & Hambrick, 2007; Gerstner et al., 2013). With this study, we systematically test this assertion in the context of the recent collapse of the U.S. commercial banking industry.

Hence, our work complements Patel and Cooper’s (2014), who found that firms led by narcissistic CEOs suffered greater declines during the global financial crisis, but also experienced higher increases after the shock. As mentioned above, their main argument was that the riskier policy decisions taken by narcissistic CEOs, even during a crisis, gave them an edge to recover in the postcrisis period. This argument does not hold in our setting of commercial banks, where risk-taking was not valued and even strictly regulated after the September 2008 collapse. One advantage of our setting is, therefore, that we can more precisely test the longer-lasting effects of preshock CEO narcissism, as (narcissistic) CEOs’ discretion to engage in approach behavior after the shock (as in Patel and Cooper’s study) were severely constrained in our setting. Hence, it allows us to further unravel the underlying mechanisms of resource depletion.

In any case, both Patel and Cooper’s (2014) and our study underscore the importance of a longitudinal approach in studying the performance effects of CEO narcissism. The combination of both studies suggests that the long-run effects of CEO narcissism are complex, and that we need further theory development and testing about boundary conditions and moderators, such as the availability of slack resources and managerial risk-taking discretion. In line with the ongoing debate on its bright and dark (short-run) effects (see above), it appears that CEO narcissism also has bright and dark sides with respect to long-run performance effects: Narcissistic CEOs can boost long-run performance when slack resources are available and managerial discretion is high (see Patel and Cooper’s study), but they might harm their organizations’ resilience in the opposite case (see the current study).

Limitations and Future Research Avenues

As any study, ours has limitations that set the stage for future research avenues. First, this is an empirical study of only one industry and one shock. On the positive side, we can pinpoint the industry’s specificities and it allows us to use an industry-wide shock (a “once-in-a-generation crisis”; Patel & Cooper, 2014) as a natural experiment to test our propositions on resilience in a robust way (van der Vegt et al., 2015). However, it also limits generalizability. While we are convinced that our theoretical model is applicable to other settings, we cannot rule out the possibility that some of our findings might be contingent on the specific nature of the industry or shock under study—as also illustrated by the difference between our and Patel and Cooper’s (2014) findings (see above). For instance, our post hoc analyses on the moderating effects of TARP funds were informative as they supported our assumptions about the underlying logic for recovery. However, they might only be valid for the specific type of industry-wide shock used in this study, as for less wide-ranging shocks there will probably be no one to bail organizations out. Testing our framework in other settings would be a fruitful avenue for further research. Furthermore, we were only able to collect full information for 92 of the 484 banks that were listed in Compustat in 2006, which might also jeopardize generalization. We accounted for this potential sample selection bias by performing two-staged regression models (cf. Heckman, 1990).

Second, in our attempt to develop a comprehensive but parsimonious framework, we only included three salient CG indicators as moderators of the effects of CEO narcissism. We chose them carefully, based on CG scholars’ suggestions (e.g., Cerasi & Oliviero, 2015; De Haan & Vlahu, 2016), but other potential indicators that could enlighten our knowledge about the “dangerous cocktail” that potentially erodes an organization’s ability to recover from shocks would represent fruitful avenues for new research. Inspired by Hambrick et al.’s (2015) list of features of effective monitoring, these indicators could, for instance, be related to the two features not already included in our study: directors’ motivation (e.g., based on ownership stakes) or their ability to devote requisite time and attention to the firm.

To conclude, our study provides insights about the effects of CEO narcissism and CG practices on firms’ long-run resilience. We add to the extant knowledge in the resilience literature by indicating the importance of CEOs and CG practices as antecedents. However, many additional questions remain open for further exploration (e.g., What is the effect of other CEO characteristics, such as age, on resilience? Do other key players’ characteristics, such as the middle managers or employees, interact with those of the CEO in affecting resilience?). We also add to the ongoing debate on the performance effects of CEO narcissism by elucidating its effects on the longer term, but again several questions are left unanswered (e.g., Are the effects of CEO narcissism on resilience similar for all types of shocks? What are the long-run effects of CEO narcissism when no shock occurs?). With the present study, we hope to inspire future scholars to attend to these and other questions to further broaden our knowledge.

Footnotes

Acknowledgements

This article was accepted under the editorship of Patrick M. Wright. We wish to thank Sucheta Nadkarni (the associate editor) and the three anonymous reviewers for their insightful and supportive feedback. We would like to thank the participants of the “Innovation in Organizations” subtheme at the 2014 EGOS colloquium and the TMT track at the 2015 EURAM Conference in Warsaw for their comments on previous versions of the article. Moreover, we appreciate all feedback and comments received from the members of the ACED research group (University of Antwerp). We also gratefully acknowledge the Research Foundation – Flanders (FWO – Vlaanderen) for financial support through a post-doc grant for the first author.