Abstract

Two parallel strands of nonmarket strategy research have emerged largely in isolation. One strand examines strategic corporate social responsibility (CSR), and the other examines corporate political activity (CPA), even though there is an overlap between the social and political aspects of corporate strategies. In this article, we review and synthesize strategic CSR and CPA research published in top-tier and specialized academic journals between 2000 and 2014. Specifically, we (a) review the literature on the link between nonmarket strategy and organizational performance, (b) identify the mechanisms through which nonmarket strategy influences organizational performance, (c) integrate and synthesize the two strands—strategic CSR and CPA—of the literature, and (d) develop a multi-theoretical framework for improving our understanding of the effects of nonmarket strategy on organizational performance. We conclude by outlining a research agenda for future theoretical and empirical studies on the impact of nonmarket strategy on organizational outcomes.

Keywords

Nonmarket strategy refers to a firm’s concerted pattern of actions to improve its performance by managing the institutional or societal context of economic competition (Baron, 1995; Lux, Crook, & Woehr, 2011). Scholarly interest in nonmarket strategy has existed for more than four decades (Aguinis & Glavas, 2012; Hillman, Keim, & Schuler, 2004) and has come of age in recent years (Doh, Lawton, & Rajwani, 2012; Doh, McGuire, & Ozaki, 2015). However, two parallel strands of nonmarket strategy research have emerged largely in isolation. The first strand examines strategic corporate social responsibility (henceforth, CSR), while the other focuses on corporate political activity (henceforth, CPA). Strategic CSR refers to corporate actions that appear to advance some social good that allows a firm to enhance organizational performance, regardless of motive (McWilliams & Siegel, 2001; McWilliams, Siegel, & Wright, 2006). CPA concerns corporate attempts to manage political institutions and/or influence political actors in ways favorable to the firm (Hillman et al., 2004; Lux et al., 2011). The purpose of this article is to integrate and synthesize these two strands of the nonmarket strategy literature.

While scholars have long articulated the need for an integration of the two lines of research (Baron, 2001; McWilliams, van Fleet, & Cory, 2002; Rodriguez, Siegel, Hillman, & Eden, 2006; D. S. Siegel, 2009), there has been little exploration of the interactions between the social and political aspects of firm strategies until recently (den Hond, Rehbein, de Bakker, & Lankveld, 2014; Frynas & Stephens, 2015; Hadani & Coombes, 2015). Indeed, scholarship has fragmented into further silos, such as strategic environmental initiatives (Ambec & Lanoie, 2008; Dixon-Fowler, Slater, Johnson, Ellstrand, & Romi, 2013) and corruption (Doh, Rodriguez, Uhlenbruck, Collins, & Eden, 2003; Uhlenbruck, Rodriguez, Doh, & Eden, 2006), which can be viewed as distinct fields of study in their own right (Orlitzky, Schmidt, & Rynes, 2003; Rodriguez et al., 2006). Given that we cannot be exhaustive in our mapping of the literature, we treat such scholarship as either part of the CPA strand or the CSR strand.

The fragmentation of prior research is also due to a variety of disciplinary and theoretical lenses through which nonmarket strategy is examined. Scholars have drawn on theoretical perspectives from economics, management, and sociology to frame their research (Getz, 2001; Kitzmueller & Shimshack, 2012; Lim & Tsutsui, 2012). Many existing studies do not highlight synergies and/or tensions of various theories, nor do they attempt to integrate these disparate perspectives in their empirical research. Fortunately, some recent studies have started adopting multiple theoretical perspectives to examine nonmarket strategies. Therefore, multi-theoretical integration serves as a crucial lens that helps organize our review of the diverse body of the literature (Doh et al., 2012; Henisz & Zelner, 2012; Rodriguez et al., 2006). By so doing, we aim to synthesize the theoretically “siloed” literature into a multi-theoretical framework that moves us toward a more comprehensive understanding of the relationship between different nonmarket strategies and performance.

There have been several recent attempts to integrate the nonmarket strategy literature. Aguinis and Glavas (2012) provide an integration of the literature on the antecedents and effects of CSR. Also, Doh and colleagues (2012) integrate three prongs of institutional theory (new institutional economics, neo-institutional perspectives, and national business systems) with three strategic lenses (industrial organization, resource-based view, and network perspectives) to study nonmarket strategy.

Our review builds on and extends the extant literature in at least three ways. First, our review focuses on the performance consequences of nonmarket strategies. Thus, we do not review the vast research on the antecedents of nonmarket strategy, which were reviewed in Aguinis and Glavas (2012) for CSR research and in Hillman et al. (2004) and Lux et al. (2011) for CPA research. Second, unlike these reviews, our review aims to integrate and synthesize both strands of the literature. Third, our review examines all pertinent theories within the nonmarket strategy literature, and therefore its scope is broader than that of Doh et al. (2012).

An extensive body of the literature argues and demonstrates that an effective nonmarket strategy is of vital importance to firm survival, organizational performance, and possibly sustainable competitive advantage (Baron, 2001; Frynas, Mellahi, & Pigman, 2006; McWilliams et al., 2002; McWilliams & Siegel, 2011; Oliver & Holzinger, 2008; Sun, Mellahi, & Thun, 2010). As such, it is essential to provide a theoretical framework that explains the mechanisms by which nonmarket strategies influence organizational performance. Given the need “to develop theoretically grounded predictions regarding the performance of firm nonmarket strategy” (Bonardi, Holburn, & Vanden Bergh, 2006: 1210), we focus on theory-informed scholarship that seeks to explain the performance implications of the various nonmarket strategies and the associated mechanisms.

Our review is structured as follows. We begin by explaining the scope of the review and the literature survey process. Next, we analyze the evolution of the literature over the years, with a focus on the theoretical lenses used to explain the performance effects of nonmarket strategies. This is followed by an analysis of the factors that mediate and moderate the relationship between nonmarket strategy and organizational performance. Finally, we synthesize the findings of the review into a multi-theoretical framework and discuss avenues for future research.

Scope and Method of the Literature Review

We have modeled the journal selection process on two related review articles in the Journal of Management (Aguinis & Glavas, 2012; Laplume, Sonpar, & Litz, 2008). We have included all general management journals surveyed in both reviews (Academy of Management Review, Academy of Management Journal, Administrative Science Quarterly, Journal of Management, Journal of Management Studies, Organization Science, Organization Studies, Strategic Management Journal) and Journal of International Business Studies, known for scholarship on nonmarket strategy. We also included five specialist journals that are known for work on CPA and CSR (Business Ethics Quarterly; Business & Politics, Business & Society; Journal of Business Ethics; and Journal of Public Affairs).

We searched articles with words such as social responsibility or corporate political activity appearing in the title, abstract, or subject terms using ProQuest and EBSCO databases. In conducting our survey, we focused on two criteria for inclusion. First, we only selected articles that specifically addressed organizational performance. Second, we only selected articles where the application of at least one general theory was explicitly acknowledged. To confirm whether the articles address performance outcomes of nonmarket strategies or whether a theoretical perspective has been applied, we examined the main body of the papers to ensure that they were properly classified and coded.

We used an inductively derived formalized codebook. Our coding of the nature of the impact of nonmarket strategy on organizational performance—positive, negative, mixed, or insignificant—was based on authors’ interpretation of their own results. For example, we classified the association as positive if the author(s) of a paper state(s) that the study supports the positive association between the nonmarket activity studied and organizational outcomes. In order to increase reliability, the authors cross-checked each other’s coding, with discrepancies (e.g., whether a theory is classified as primary or secondary) providing an opportunity to further fine-tune the coding results. Once the process was finished, we carried out random checks, which suggested that there was high coding accuracy.

Given recent advancements in nonmarket strategy literature, the journal articles were surveyed over the most recent 15-year period, 2000-2014 (including papers in press in 2014). This resulted in a total of 214 articles, with 153 and 51 articles concerning the performance outcomes of CSR and CPA, respectively. In addition, we identified 10 articles that explicitly addressed both CSR and CPA in their research. We further consulted highly impactful papers on CSR and CPA published outside the study period and those outside the journals reviewed in this study. Using ISI Web of Knowledge, we identified the 25 most cited CSR papers and the 15 most cited CPA papers that were not included in our database and 17 recent CSR papers and 10 recent CPA papers published outside the journals reviewed in this study. We also consulted journal special issues dedicated to nonmarket strategies.

Analysis of the Literature

Overview of Nonmarket Strategy and Organizational Performance

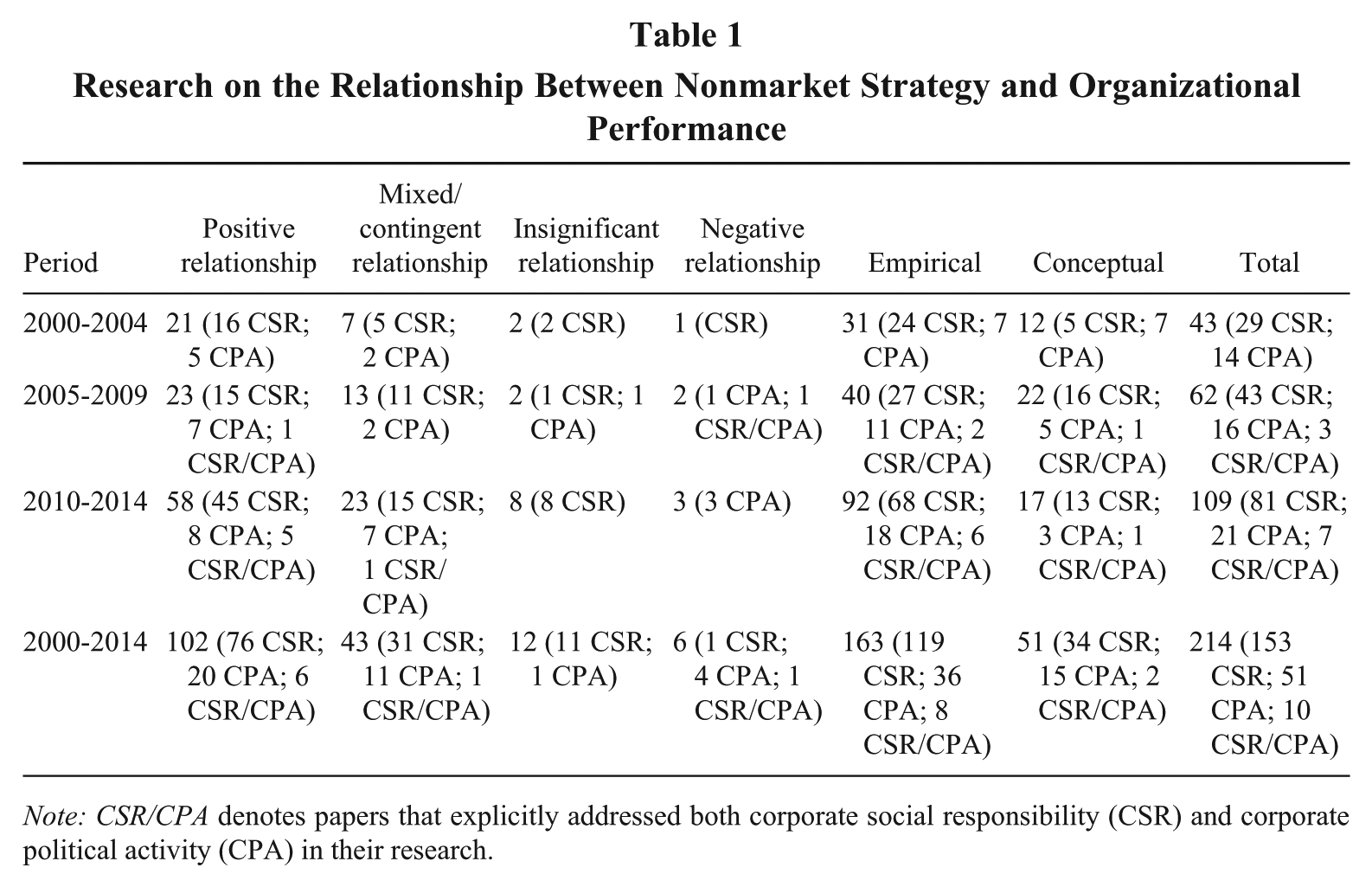

Table 1 presents a breakdown of the 214 articles and suggests several salient patterns. First, the theory-based nonmarket strategy literature has been burgeoning recently. We identified 109 articles during the past 5 years (2010-2014) compared to 105 articles during the 10-year period 2000-2009. Notably, this growth can be attributed to the proliferation of empirical studies in recent years (92 papers over 2010-2014 vs. 71 papers over 2000-2009), while the number of conceptual papers remains stable across the two periods (17 papers over 2010-2014 vs. 34 papers over 2000-2009).

Research on the Relationship Between Nonmarket Strategy and Organizational Performance

Note: CSR/CPA denotes papers that explicitly addressed both corporate social responsibility (CSR) and corporate political activity (CPA) in their research.

Second, a majority of empirical studies (102 out of 163) reported a positive association between nonmarket strategies and organizational performance. For instance, six out of the seven studies examining environmental initiatives reported a positive performance effect. However, 43 (26% of the total) empirical studies reported mixed relationships, 12 studies (7%) reported insignificant results, and 6 studies (4%) reported a negative association between nonmarket strategy and organizational performance. In other words, over one-third of the studies in our sample did not find positive performance effects of nonmarket strategies. It is noteworthy that each of the empirical papers was assigned equal weight. That is, we did not account for potential sampling or measurement errors in the survey process, which needs to be addressed in future research (Hunter & Schmidt, 2004). Also, these strategy-performance associations were not driven by the types of the data: The empirical results do not depend on whether the data analyzed in question were cross-sectional or longitudinal.

Third, while recent studies tend to subject the nonmarket strategy–performance hypothesis to more rigorous tests, the nature of the link remains elusive. Among the empirical papers published during 2010-2014, more than one-third of CSR studies (23 out of 68 papers) and more than one-half of CPA studies (10 out of 18 papers) did not find a positive relationship between nonmarket strategy and performance. Hence, these results add weight to the verdict over the years on the equivocal relationship between nonmarket strategy and performance (Margolis & Walsh, 2003; McWilliams & Siegel, 2000; Sun, Mellahi, & Wright, 2012).

A closer look at the studies in our sample reveals another two key issues. First, scholars are no longer satisfied with identifying a direct link between nonmarket strategies and performance. Many studies explore the underlying mechanisms through which nonmarket strategy impacts upon firm outcomes (e.g., Zheng, Singh, & Mitchell, 2015; Zhu & Chung, 2014). Studies also explore the moderating influences of various variables (Aguinis & Glavas, 2012; Goll & Rasheed, 2004). Second, studies point to a variety of links between nonmarket strategies and organizational outcomes that ultimately affect financial performance. They include consumer perceptions (Luo & Bhattacharya, 2006), access to finance (Madsen & Rodgers, 2015), preferential access to political resources (Frynas et al., 2006), or an improved relationship with the primary stakeholder (Hillman & Keim, 2001).

Overview of Theory Applications and Combinations in the Literature

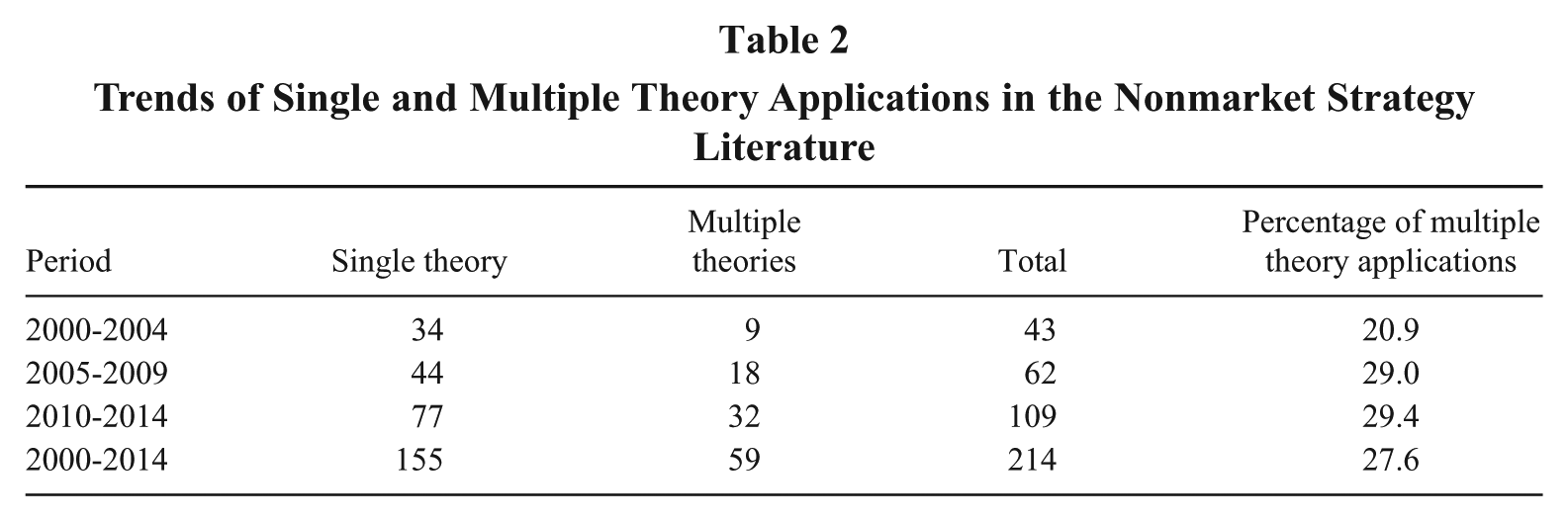

Table 2 shows that the majority of studies (155 out of 214 papers) draw on a single theoretical perspective. However, the intellectual pendulum seems to be swinging toward the use of multiple theories: The percentage of papers that have adopted multiple theories increased from just over 20% during the 2000-2004 period to about 30% during the 2005-2009 and 2010-2014 periods.

Trends of Single and Multiple Theory Applications in the Nonmarket Strategy Literature

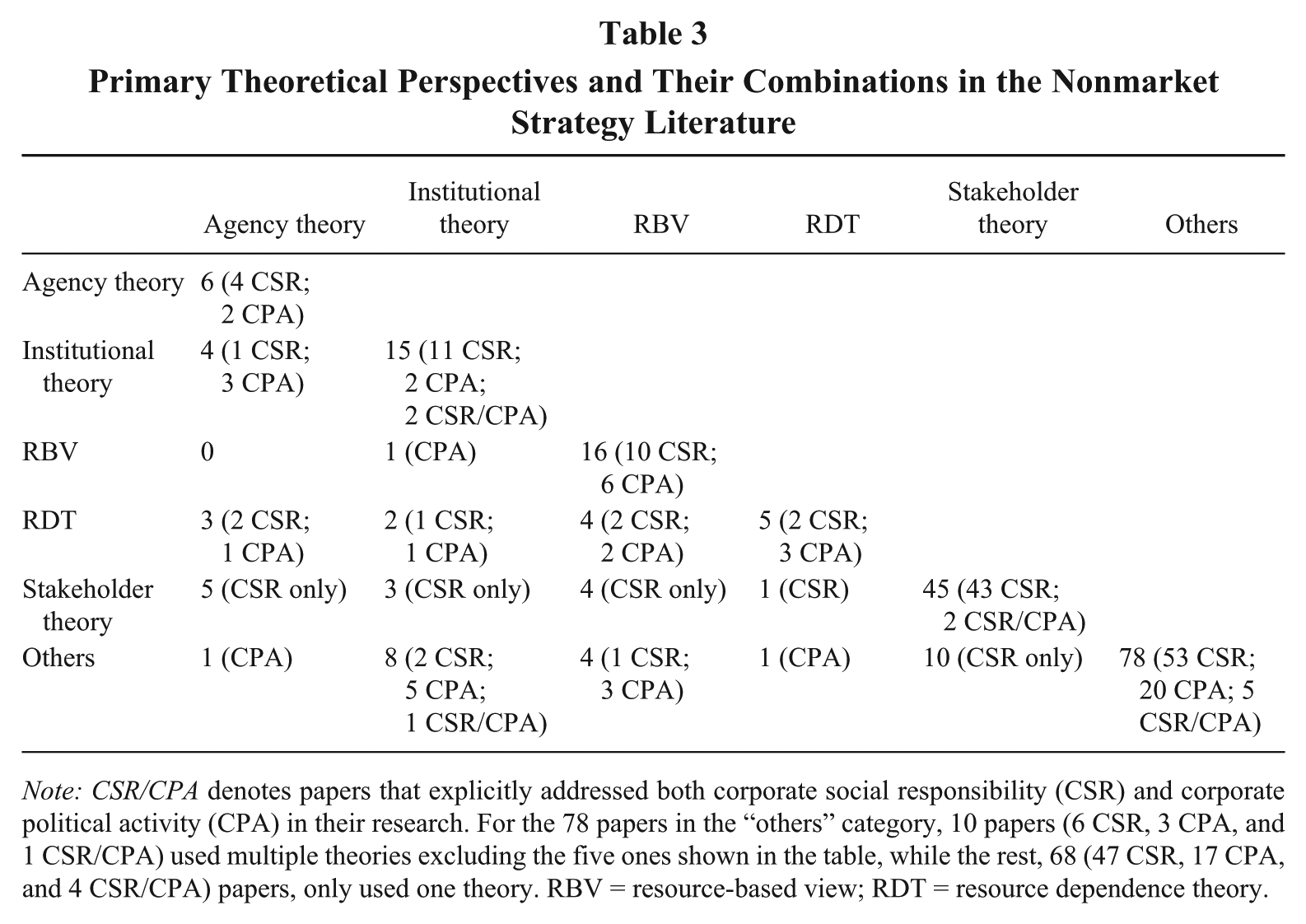

Scholars have primarily drawn on five theories to explore the link between nonmarket strategy and organizational performance: agency theory, institutional theory, resource-based view of the firm (henceforth, RBV), resource dependence theory (henceforth, RDT), and stakeholder theory. Table 3 shows that studies drawing on the five theories account for about 65% of the papers (136 out of 214) in our database. The remaining 35% draw on a wide variety of theories, such as public choice theory, signaling theory, social embeddedness/network theory, social identity theory, and transaction cost economics. Table 3 also presents the patterns of how various theories are applied and combined in the literature. Our analysis reveals that stakeholder theory is the dominant paradigm in CSR studies (45 papers). The dominant use of stakeholder theory holds through the various CSR subdisciplines. There are also notable combinations between stakeholder theory and other theories, such as agency theory, to assess the performance effects of strategic CSR.

Primary Theoretical Perspectives and Their Combinations in the Nonmarket Strategy Literature

Note: CSR/CPA denotes papers that explicitly addressed both corporate social responsibility (CSR) and corporate political activity (CPA) in their research. For the 78 papers in the “others” category, 10 papers (6 CSR, 3 CPA, and 1 CSR/CPA) used multiple theories excluding the five ones shown in the table, while the rest, 68 (47 CSR, 17 CPA, and 4 CSR/CPA) papers, only used one theory. RBV = resource-based view; RDT = resource dependence theory.

RBV is a popular lens for both CSR and CPA research. A total of 16 studies are found to just use RBV and its variants to examine the performance consequences of nonmarket strategies. We also identify a significant number of combinations of RBV with RDT and stakeholder theory. Similarly, institutional theory features prominently in the literature, especially in CSR studies, but scholars have yet to integrate it with other theories in a significant manner. Single applications of agency theory and RDT are less frequent. Rather, they are often combined with the other three theoretical perspectives.

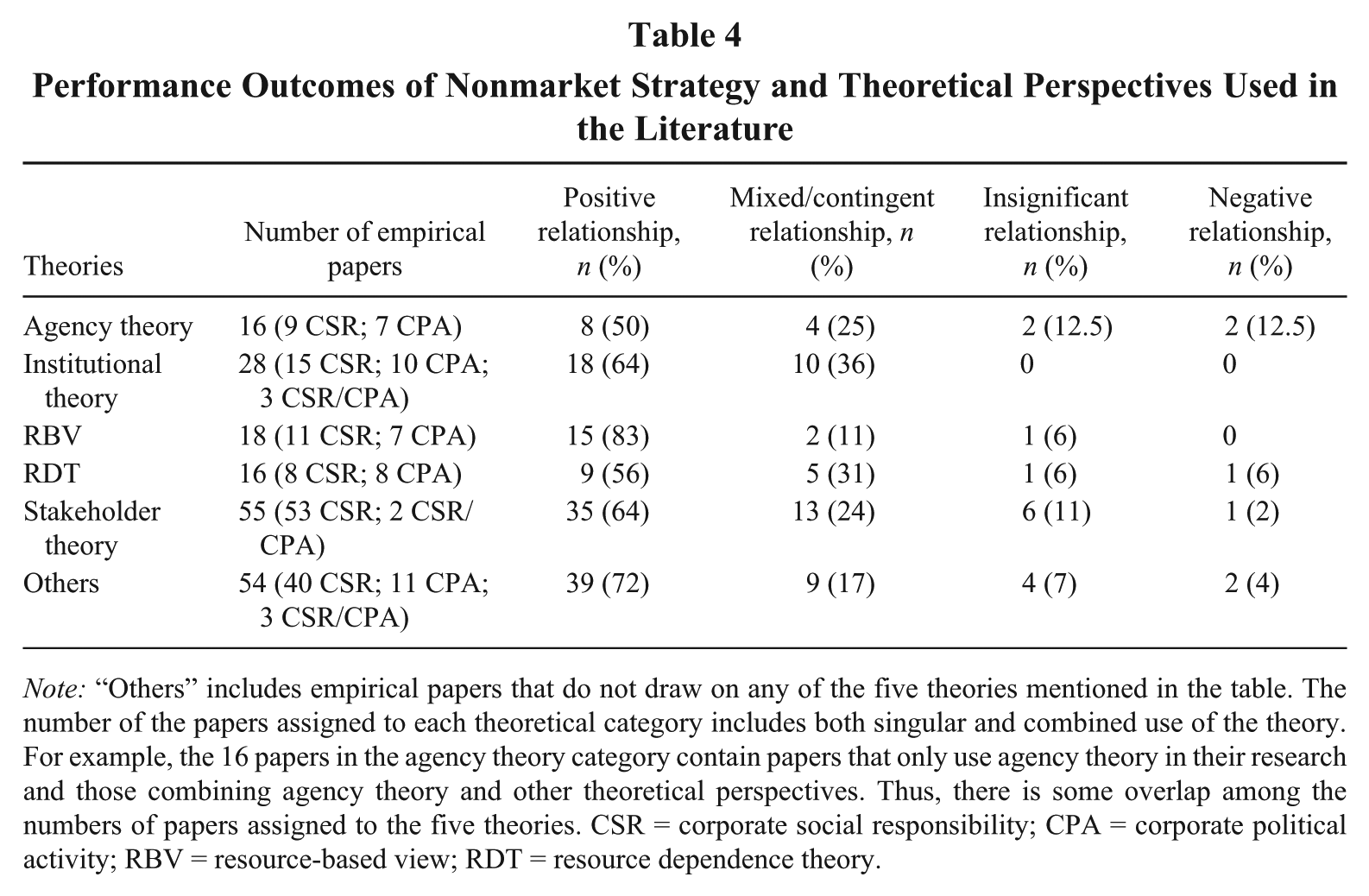

Table 4 reports how the strategy-performance relationship studied in empirical papers is associated with the five primary theories. Relatively speaking, the empirical evidence provides stronger support for RBV, institutional, and stakeholder theories’ predictions regarding the positive link between nonmarket strategy and organizational outcomes. In contrast, only 56% and 50% of RDT and agency theory applications, respectively, support such a positive association.

Performance Outcomes of Nonmarket Strategy and Theoretical Perspectives Used in the Literature

Note: “Others” includes empirical papers that do not draw on any of the five theories mentioned in the table. The number of the papers assigned to each theoretical category includes both singular and combined use of the theory. For example, the 16 papers in the agency theory category contain papers that only use agency theory in their research and those combining agency theory and other theoretical perspectives. Thus, there is some overlap among the numbers of papers assigned to the five theories. CSR = corporate social responsibility; CPA = corporate political activity; RBV = resource-based view; RDT = resource dependence theory.

With regard to the predictive power of theory, scholars (e.g., McWilliams & Siegel, 2011) have provided a sound rationale for a positive association between nonmarket strategy and organizational performance from the stakeholder, institutional, or RBV perspectives and why one should expect such association to be negative if one draws on agency theory (Hadani & Schuler, 2013; Petrenko, Aime, Ridge, & Hill, in press). However, our review of the literature suggests that nonmarket strategy research typically emphasizes the complementarity of theories rather than the tensions among them. This may be because nonmarket strategy scholars have been primarily interested in applying theoretical insights from diverse theories to come up with a set of empirical predictions. Under many circumstances, researchers incorporate macro- and organizational-level variables to weave together a tapestry of compatible and converging arguments from stakeholder theory, RBV, RDT, and other theoretical lenses to help develop their hypotheses. Relatively fewer research works have undertaken theoretical integration through addressing the underlying tensions among different theories. Notable among these are studies integrating agency theory with RDT or RBV to understand mixed or even negative performance effects of nonmarket strategy (Sun, Hu, & Hillman, in press; H. Wang, Choi, & Li, 2008).

Nonmarket Strategy and Organizational Performance

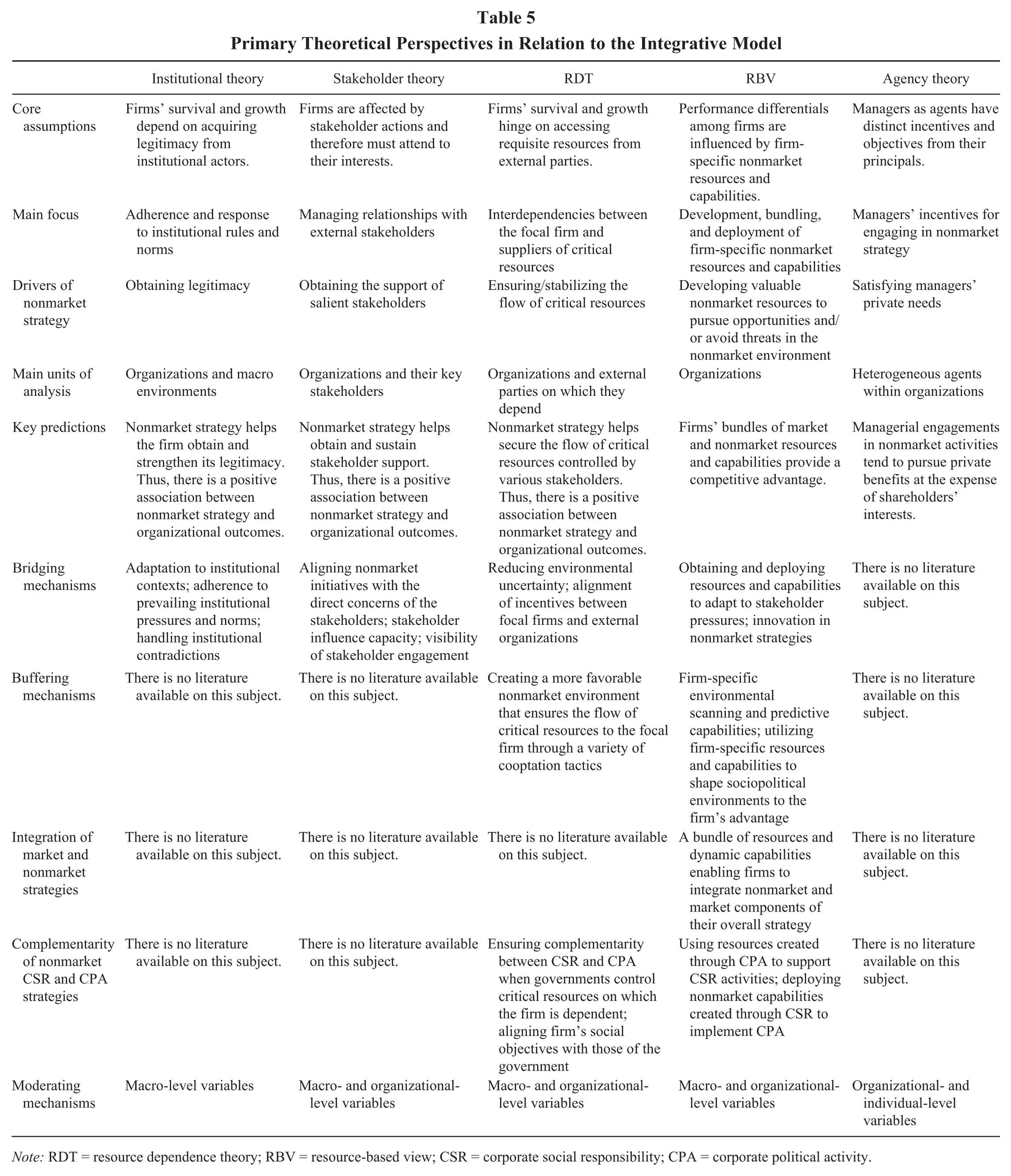

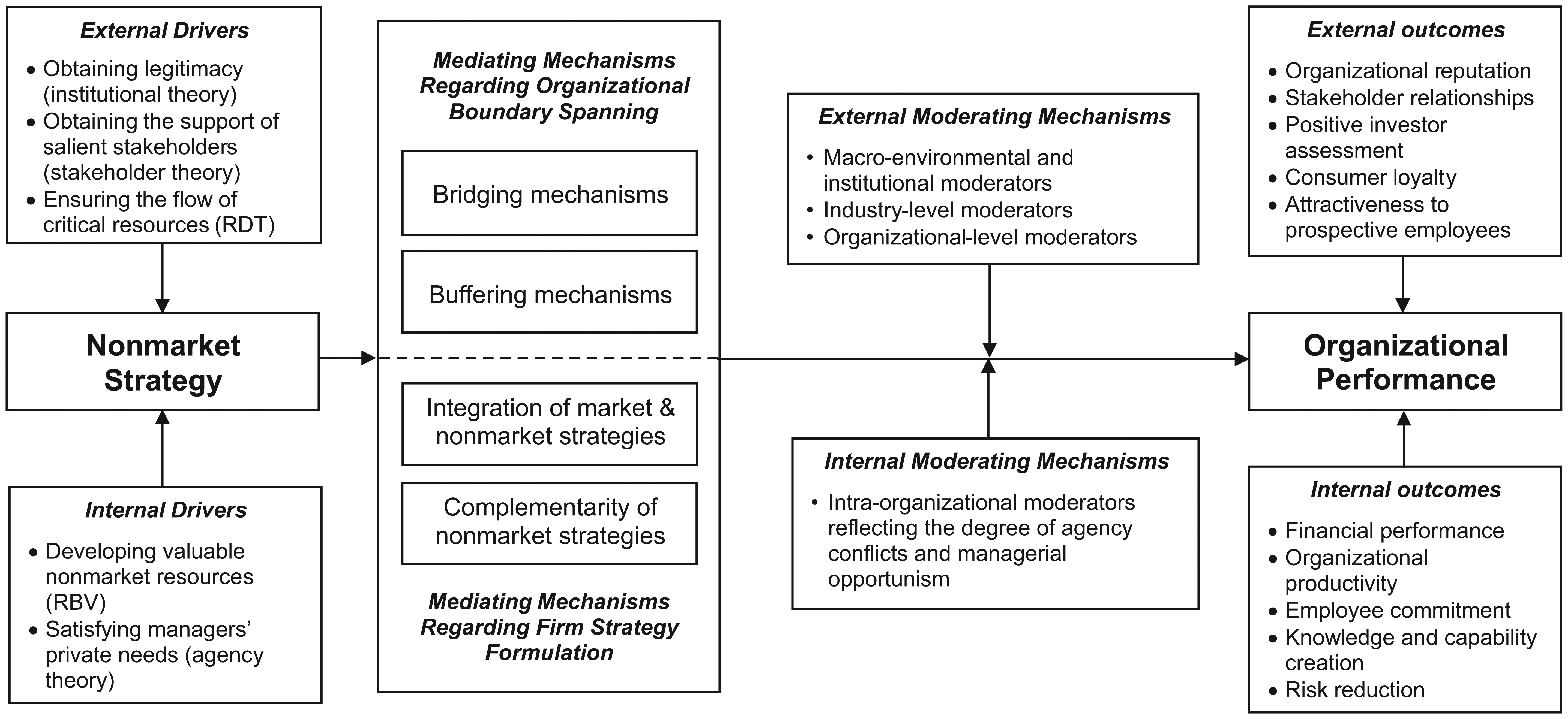

We start from the premise that a multi-theoretical framework is needed for a better understanding of the link between nonmarket strategy and organizational performance, as the quest for a single grand nonmarket strategy theory may not be fruitful (Hillman, 2002). Since the evidence is inconsistent on the direct link between nonmarket strategy and organizational outcomes (McWilliams & Siegel, 2000; Sun et al., 2012; Sun, Mellahi, Wright, & Xu, 2015; Surroca, Tribó, & Waddock, 2010), we identify the various mediating mechanisms and moderating variables that underlie this link. An integrative review of the mechanisms and variables from the five primary theoretical perspectives is summarized in Table 5. The integrative model explaining the nonmarket strategy–performance link is illustrated in Figure 1.

Primary Theoretical Perspectives in Relation to the Integrative Model

Note: RDT = resource dependence theory; RBV = resource-based view; CSR = corporate social responsibility; CPA = corporate political activity.

An Integrative Model of the Nonmarket Strategy–Performance Relationship

Managing the External Nonmarket Environment

The nonmarket environment structures a firm’s interactions with its nonmarket stakeholders. They include but are not limited to government actors and institutions, nongovernmental organizations, social and environmental activists, and local communities. Drawing on the five main theories, the literature explores how firms adapt to external demands, adhere to prevailing institutional pressures and norms, handle institutional contradictions to elevate their sociopolitical legitimacy, and secure critical resources from salient stakeholders. Table 5 summarizes different assumptions held by the five theories about why and how firms interact with their nonmarket stakeholders.

With respect to the mediating mechanisms that concern the means and approaches by which nonmarket strategies are implemented to enhance organizational performance, we distinguish the mechanisms related to organizational boundary spanning from those related to nonmarket strategy formulation. Consistent with the literature on organizational boundary spanning (Fennell & Alexander, 1987; Meznar & Nigh, 1995), we group the mechanisms related to the external nonmarket environments into the buffering and bridging activities, which are not mutually exclusive. Firms bridge with the external environment by seeking “to adapt organizational activities so that they conform with external expectations” (Meznar & Nigh, 1995: 976). In contrast, a firm resorts to a buffering strategy to protect itself from the external environment. To this end, the firm is “trying to keep the environment from interfering with internal operations and trying to influence the external environment” (Meznar and Nigh, 1995: 976; italics added). This classification is widely used in the nonmarket literature (Dieleman & Boddewyn, 2012; Zheng et al., 2015).

On the internal formulation of nonmarket strategies, we draw on the literature to highlight two key mechanisms. First, given the importance of alignment with market activities (Baron, 1995), we examine the literature with regard to mechanisms related to the integration between market and nonmarket strategies. Second, in line with the emerging literature on the CSR-CPA integration (den Hond et al., 2014; Frynas & Stephens, 2015; Rehbein & Schuler, 2015) and the consistency in nonmarket strategies (Tang, Hull, & Rothenberg, 2012; Vallaster, Lindgreen, & Maon, 2012), we examine the literature with regard to mechanisms related to the complementarity and consistency between strategic CSR and CPA.

Mediating Mechanisms Regarding Organizational Boundary Spanning

Bridging mechanisms

Scholars drew on stakeholder theory, institutional theory, RDT, and RBV to explain how bridging mechanisms mediate the link between nonmarket strategy and organizational outcomes. Nonmarket practices grouped under this mechanism involve activities complying with social and political expectations of stakeholders. The order in which the four theoretical perspectives are presented in the following is based on the breadth of the unit of analysis, moving from the broad to a more specific unit. Institutional theory looks at the interaction of firms with broad/national institutional contexts, stakeholder theory and RDT focus on stakeholders within or across contexts, and RBV deals with resources and capabilities within firms.

The bulk of the institutional theory literature explores the challenges facing firms, such as multinational enterprises (MNEs), in establishing legitimacy in various institutional contexts. MNEs operate in multiple institutional contexts and face a multitude of competing and possibly conflicting institutional pressures (Ioannou & Serafeim, 2012). An underlying theme in this line of inquiry is the adaptation of firms’ nonmarket initiatives to local institutional contexts and its impact on organizational outcomes. The core assumption here is that adaptation leads to legitimization and henceforth improves performance. In contrast, the divergence between MNEs’ nonmarket practices in the host country and local stakeholders’ expectations may delegitimize MNEs’ practices. The consensus here is that for firms to gain external legitimacy abroad, they need to manage local social pressures and priorities rather than transplant their home nonmarket practices within their network of subsidiaries (cf. Aguilera-Caracuel, Aragón-Correa, Hurtado-Torres, & Rugman, 2012). Although these studies suggest that performance depends on adaptability to local institutional contexts, one unresolved issue is whether MNEs should pay more attention to their home stakeholders or their host-country stakeholders. We argue that stakeholder theory and RDT would be best suited to tackle this question. Stakeholder theorists have long addressed the issue of stakeholder multiplicity and how firms should deal with stakeholder heterogeneity. Similarly, a resource dependence lens may help uncover tailor-made strategies for the various institutional contexts.

Additionally, firms have to deal with institutional contradictions where a “given action may be seen as socially responsible from one stakeholder perspective but irresponsible from another” (Keig, Brouthers, & Marshall, 2015: 92) or with institutional pressures to engage in corrupt practices (Lee & Weng, 2013). Institutional contradictions create a context where a particular nonmarket strategy may lead one stakeholder group to confer legitimacy to the firm but meanwhile may lead another group of stakeholders to withdraw its legitimacy. This implies that firms may need to abandon their established nonmarket practices in order to adapt to the host country’s institutional norms or they may employ ceremonial adoption without changing actual practices. Unfortunately, we found no studies that explicitly tested the performance impact of such strategies.

While institutional theory focuses on broad institutional contexts, stakeholder theory studies zero in on bridging strategies with specific stakeholder groups. The starting point of the stakeholder view is that some stakeholders matter more than others (Kassinis & Vafeas, 2006). Jia and Zhang (2014) found that stakeholders with a long-term investment horizon tended to pay less attention to negative media reports about a firm’s CSR activities than those with a short-term investment horizon. Relatedly, scholars have studied how certain nonmarket constituents’ responses influence firms’ performance. Ioannou and Serafeim (2015) found that because of the legitimization of CSR practices, sell-side analysts’ pessimism over high CSR scores diminished over time, and highly informed and experienced analysts were the first to be less pessimistic about firms with high CSR scores.

Another line of inquiry explores the alignment between nonmarket strategy initiatives and stakeholder concerns. Brammer and Millington (2008) noted that CSR is likely to have a positive impact on performance when it addresses issues important to salient stakeholders. Similarly, Lev, Petrovits, and Radhakrishnan (2010: 198) reported that firms can more easily justify CSR initiatives “if they can explain how corporate giving will enhance customer satisfaction and, in turn, sales growth.” Lankoski (2009) highlighted the importance of communication with stakeholders and visibility of firm’s nonmarket initiatives. That is, for firms wishing to generate goodwill and inhibit stakeholder skepticism, they need to be credited for their initiatives.

The third perspective, RDT, posits that bridging activities reduce uncertainties caused by focal firm’s dependence on external entities, thus reducing the potential negative effect of environmental dependence (Getz, 2001). In the context of the nonmarket strategy literature, RDT is often used in conjunction with stakeholder or institutional theory. For instance, Kassinis and Vafeas (2006: 146) supplemented the stakeholder perspective with RDT to highlight how within-group heterogeneity in terms of target firm’s varying dependencies impacts firms’ environmental performance. They argue that while stakeholder theory explains why and how stakeholders influence organizational conduct and performance, the answer to the question of “What gives stakeholders the ability to influence firm decisions?” is provided by RDT.

The thrust of an even smaller body of literature drawing on RBV is that firms are endowed with different resources and capabilities to influence or limit the influence of stakeholders. From an RBV perspective, bridging activities can help improve organizational efficiency by using firm-specific resources and capabilities to adapt to demands and changes in nonmarket environments (Hart, 1995). Drawing on stakeholder theory and RBV, Surroca and colleagues (2010) posited that the CSR-performance relationship is mediated by a bundle of intangible resources consisting of innovation, human capital, reputation, and culture.

In sum, the different theories provide complementary insights into bridging activities. The institutional perspective underscores the importance of institutional alignment and adaptation in organizational performance. However, the role of stakeholder heterogeneity and contradictions within and between institutional contexts remains to be empirically tested. The stakeholder literature accentuates the prioritization of salient stakeholders according to their power, legitimacy, and urgency (Mitchell, Agle, & Wood, 1997). The stakeholder theoretical prong is complemented by the RDT perspective, which emphasizes the management of interdependence between the firm and various salient stakeholders. The stakeholder response mechanism has also received support from scholars drawing on the RBV perspective. The most distinctive contribution of the RBV to the stakeholder response mechanisms is the shifting of emphasis toward the role of resources and capabilities in enabling the firm’s initiatives to entice stakeholder response.

Buffering mechanisms

Buffering mechanisms involve both defensive and proactive activities on the part of focal organizations to gain influence and control over their external nonmarket environments. These include lobbying, campaign contributions, public relations campaigns, and building personal and organizational ties to sociopolitical institutions and actors (Sun et al., 2012). Our literature review suggests that scholars draw primarily on RBV and RDT to examine the buffering mechanisms. From an RBV lens, defensive strategies can help companies establish a strategic advantage through firm-specific environmental scanning and predictive capabilities (Aragón-Correa & Sharma, 2003), while proactive strategies can provide a firm with an advantage by utilizing firm-specific resources and capabilities to shape the nonmarket environment to its advantage by, for instance, forestalling or manipulating additional regulation and raising rivals’ costs (McWilliams et al., 2002; Oliver & Holzinger, 2008). From an RDT lens, proactive activities can help the firm derive performance benefits from creating a more favorable nonmarket environment that ensures the flow of critical resources to the focal firm (Hillman, Withers, & Collins, 2009; Pfeffer & Salancik, 1978).

Our literature survey reveals that the CPA component of nonmarket strategy is often perceived from the buffering lens. Firms buffer themselves from unwanted political interferences and obtain access to and elicit support from political actors and institutions. This is achieved through gaining influence over regulations and receiving information and preferential treatments from government officials (Hillman et al., 2004).

RDT holds that organizational survival and growth are dependent on firms’ ability to procure resources from and manage uncertainties caused by external constituents. Since the government is “one of the most difficult environmental dependencies to control” (Hillman et al., 2009: 1412), firms may seek to co-opt political agencies and actors by a variety of tactics. Consequently, performance benefits accrue to firms that have successfully created co-optive linkages with the political environment. Informed by the RDT perspective, most studies in developed countries report a positive effect of political buffering activities on firm value (Hillman, 2005; Hillman, Zardkoohi, & Bierman, 1999). Lux et al.’s (2011) meta-analysis concluded that firms engaging in lobbying and campaign contributions achieved about 20% higher economic value.

In emerging economies where resource dependencies on the government are stronger, firms are expected to develop political connections to access critical political resources and to shield themselves from the perils of political extortions (Peng & Luo, 2000). While much of the research emphasizes the mechanisms through which firms generate value through political strategies, a more recent line of inquiry trend starts to note the vulnerabilities of nonmarket strategies through political buffering (J. Siegel, 2007; Sun et al., 2012). For example, J. Siegel (2007) highlighted the importance of political environment stability by reporting that politically connected South Korean firms suffered from discrimination and even expropriation and sabotage upon political shocks that caused a sudden loss of the power bases to which these ties were initially attached.

Studies drawing on RDT suggest that firm-level buffering activities may invite the risk of losing organizational autonomy. Depending on the nature and level of dependency, firms are exposed to varying pressures to divert their resources to help political actors achieve their goals that may in turn affect their organizational performance (Pfeffer & Salancik, 1978). Dieleman and Boddewyn (2012) examined how Indonesian business groups developed several interrelated buffering strategies to manage the contradictory and potentially predatory demands from sociopolitical stakeholders, such as preventing political ties from misappropriating resources.

Scholars drawing on RBV hold that companies can develop and deploy political resources and capabilities to generate economic returns (Boddewyn & Brewer, 1994; Holburn & Zelner, 2010). To the extent that firms’ ability to cope with political process is unevenly distributed, political resources and capabilities are frequently in scarce supply and are difficult for rivals to match. This underscores the importance of locking out competitors from accessing valuable political resources. Further, Oliver and Holzinger (2008) applied the dynamic capabilities approach to develop a typology of CPA and link them to different performance outcomes. Specially, proactive strategies, if effectively implemented, are more likely than reactive and defensive strategies to lead to sustainable competitive advantages. However, while social and environmental resources are unlikely to lead to a sustainable competitive advantage because CSR activities tend to be transparent and can be relatively easily imitated by competitors (McWilliams & Siegel, 2001, 2011), political resources fit the requirements of the RBV well in that “the most effective political behaviors are often covert in nature” and are more difficult to imitate (Boddewyn & Brewer, 1994: 136). McWilliams et al. (2002) argued that political strategies that capitalize on unique resources and block the availability of substitute resources to competitors by raising rivals’ costs help achieve a competitive advantage. Holburn and Zelner (2010) found that MNEs differ in their political capabilities in terms of assessing policy risks and managing policy processes; MNEs with superior political capabilities are more likely to succeed in countries with weak institutional constraints.

Integration between RDT and RBV perspectives can result in a more nuanced understanding of when and how firm-specific political resources impact on organizational outcomes. While RBV focuses on the creation and nurturing of resources and capabilities in relation to a firm’s social and political environments, RDT highlights how the value of these resources will be contingent on the power relationships and resource interdependences between focal firms and their sociopolitical stakeholders. Frynas and colleagues (2006) suggested that political resources can lead to first-mover advantages, but given changing resource interdependencies, sustaining these advantages requires additional market and nonmarket resources. Furthermore, late movers can also develop and use political resources to neutralize first-mover advantages. As another example, Zheng and colleagues (2015) examined how the buffering roles of political ties predicted by RDT might vary in accordance with firm-level heterogeneity, such as prior performance and types of ties, underscored by the RBV logic. They found that political ties helped firm survival but did not help generate more firm growth.

In sum, RBV and RDT provide complementary insights into buffering activities, but organic integration between RBV and other theoretical perspectives to study buffering activities remains rare. A notable exception combining RBV with the institutional perspective, C. Wang, Hong, Kafouros, and Wright (2012: 672) examined “the interaction between government involvement and firm resources,” suggesting that it is not the political linkages per se that lead to higher performance, but the “idiosyncratic manner” in which firms are affiliated with government actors and institutions; this was determined by a firm’s capability to respond proactively to institutional pressures. However, we found no study that explored the performance outcomes of nonmarket strategy using influential institutional concepts such as decoupling as buffering the formal structures to reconcile the conflicting isomorphic pressures imposed by different actors.

Mediating Mechanisms Regarding Nonmarket Strategy Formulation

Complementarity and tension between market and nonmarket strategies

The highly intertwined market and nonmarket environments facing a focal firm entail formulating a concerted strategy integrating both market and nonmarket components (Baron, 1995). RBV represents a dominant theoretical lens in this academic discourse. Firm-specific resources that can achieve integrative configurations in managing both market competition and nonmarket challenges are valuable, rare, costly to imitate, and non-substitutable (Clougherty, 2005; McWilliams et al., 2002).

Complementarity between market and nonmarket strategies is more likely in specific subfields such as environmental initiatives. Management tools, methods, and practices (e.g., quality management or performance management) are better suited toward making environmental improvements (compared with community development or human rights initiatives) as they share similar approaches to implementation and are close to core competencies of manufacturing and engineering firms (Molina-Azorín, Tarí, Claver-Cortés, & López-Gamero, 2009; Porter & van der Linde, 1995). These complementarities may help explain the high positive association between environmental initiatives and performance and underline the importance of studying specific nonmarket strategy subfields.

Nevertheless, compared to the bridging and buffering mechanisms, empirical studies exploring the relationship between nonmarket and market strategies are much less developed, particularly with regard to the CPA research. Among the small volume of empirical inquiries, a notable recent study in the U.S. electric utility industry found that firms tended to use campaign contributions to politicians strategically in association with their merger and acquisition activities (Holburn & Vanden Bergh, 2014). Utilities increased their contributions before they announced a merger to influence regulatory merger approvals, and the increase was more significant in states with greater political competition.

Ironically, some research has revealed the inherent tensions or negative interactions between market and nonmarket strategies. For instance, Li, Zhou, and Shao (2009) found that the positive performance effect of product differentiation strategy adopted by MNEs in China was weakened by the managerial political connections they developed with Chinese government officials. Theoretically, Ahuja and Yayavaram (2011: 1648-1649) postulated that rent-seeking nonmarket strategies “may well imply a weakening in the development of some other productive capabilities and thus weaken firms’ ability to earn other forms of rents such as efficiency and innovation rents.”

Consistent with this spirit, Sun and colleagues’ (2010) longitudinal study of the MNE political strategies in the Chinese auto industry delineated the underlying process in which erstwhile effective nonmarket activities may generate unintended adverse impacts on market-based competitive capabilities over time. Drawing on RDT, RBV, and social embeddedness perspective, they showed that in a dynamic business environment, strong connections developed between MNEs and local political institutions could turn into a liability as the original relationship-based strategies became increasingly obsolete and resulted in cost inefficiency and underdevelopment of market-based skills. In sum, our understanding of the role of complementarity and tension between market and nonmarket strategies remains limited, and we need more conceptual developments and empirical studies to investigate these issues.

Complementarity between strategic CSR and CPA

Historically, CSR and CPA were treated as separate activities. Recently, a growing body of research has started exploring the impact of alignment between and within CSR and CPA activities on performance (Liedong, Ghobadian, Rajwani, & O’Regan, 2015). Scholars have suggested that CSR may serve as a buffer to the potentially risky effects of CPA (Sun et al., 2012), the two practices are complementary and need to be aligned (den Hond et al., 2014), and the two may be mutually exclusive (Jamali & Mirshak, 2010). The combination of insights from the five theories can contribute toward a more differentiated understanding of this relationship.

Studies in the emerging economy context suggest that nurturing CSR activities can help strengthen an organization’s political connections, which in turn can lead to improved performance (e.g., Marquis & Qian, 2014). This perspective posits that CSR-CPA complementarity in response to government pressures can help strengthen a firm’s legitimacy and facilitate the inflow of critical government-controlled resources. Accordingly, as the firm seeks to align its nonmarket activities with institutional pressures, CSR activities are subservient to CPA in reaching their strategic goals.

Institutional theory, stakeholder theory, and RDT applications agree that the positive performance effects from the aforementioned complementarity are pronounced when governments control critical resources on which the organization is dependent and political legitimacy associated with access to government resources can be viewed as a strategic resource for firms. In particular, organizations with a high dependence on government actors may have to pursue social objectives in order to align their interests with those of the government, notwithstanding whether the key theoretical assumption concerns legitimacy within the institutional environment (Marquis & Qian, 2014), establishing the flow of critical resources (Kostka & Zhou, 2013), or obtaining the support of critical stakeholders (H. Wang & Qian, 2011).

While studies from the institutional, stakeholder, and RDT perspectives have frequently resorted to empirical evidence from China in exploring this alignment (Kostka & Zhou, 2013; Marquis & Qian, 2014; H. Wang & Qian, 2011), a recent study that simultaneously applied the three perspectives and was based on data from Switzerland found that the government had the weakest influence among primary stakeholders (Helmig, Spraul, & Ingenhoff, in press). Hence, we need more research to understand the interactions between CSR and CPA in institutional environments where political actors do not normally reward organizations for their alignment between nonmarket activities.

The focus on internal resources allows the RBV to theorize the complementarity of CSR and CPA in different institutional environments and permits a two-way causality: Firms may benefit from resources created through CPA to support their CSR activities or may benefit from resources created through CSR to support their CPA (den Hond et al., 2014). CPA can strengthen CSR activities through several mechanisms. Interactions with political actors can assist organizations in selecting CSR priorities by identifying significant social and political issues. CPA can provide critical information, support, or favorable regulation to enhance the economic viability of CSR activities. CPA may also help to increase the credibility and legitimacy of CSR activities (den Hond et al., 2014).

RBV can also be applied to theorize how CSR activities can strengthen CPA. CSR activities may strengthen human resources through improving personal relationships with political actors as well as improving organizational capital resources through enhancing organizational knowledge and external relationships. CSR activities can also improve geographic resources by establishing a geographic presence in a political constituency (Rehbein & Schuler, 2015). In short, RBV can theorize how the complementarity of nonmarket strategies enhances performance by developing different types of resources. Conversely, institutional, stakeholder, and RDT lenses may explain more satisfactorily the impact of the external context on performance.

However, some research on the interaction between strategic CSR and CPA points to the absence of complementarity. When managers are unable or unwilling to react to external pressures to improve CSR, CPA may substitute and weaken CSR activities. Studies show that stakeholder pressures to improve a firm’s CSR performance may prompt managers to engage in CPA to safeguard their discretion, thereby diverting resources away from CSR activities (David, Bloom, & Hillman, 2007), and that firms undertaking long-term relational CPA may challenge proposals by socially oriented stakeholders more than firms that do not (Hadani, Doh, & Schneider, 2013). In this sense, CPA can be used as a buffer to maintain the status quo when facing undesirable demands for CSR from activists.

The inconclusive research findings on complementarity between CSR and CPA may be related to the variable impacts of external stakeholder pressures on CPA and CSR. Social movement scholars have looked into how conflict plays out between social movements, civic groups, and business firms (de Bakker, den Hond, King, & Weber, 2013; Reid & Toffel, 2009). Social movements can either contend/disrupt or collaborate with business firms. Yaziji and Doh (2013) argue that resource providers to social movement organizations tend to shape the strategic interaction between social movements and firms. While research has explored why and how social movements and firms engage in private politics to achieve social and political goals (den Hond, de Bakker, & Doh, 2015; O’Connor & Shumate, 2014), we have very limited knowledge about the performance implications of interactions between firms and social movements in private politics. For instance, we know little about the capabilities that firms must possess (which could draw on RBV) and the critical resources that social movements must possess (which could draw on RDT) to facilitate the development of effective nonmarket strategies. This limited knowledge suggests an ample need for incorporating the social movement perspective in understanding CSR-CPA interactions and their performance impact.

Making Sense of Moderating Factors

The extant literature has examined a myriad of factors moderating the nonmarket strategy-performance link, ranging from individual, to organizational, and to environmental variables. Scholars drawing on RDT examined the moderating effects of industry regulations, which indicated the degree of mutual dependence between firms and the government (Hillman, 2005). Scholars drawing on stakeholder theory discussed the moderating effects of firm-level variables including size (Knox, Maklan, & French, 2005), reputation/status (Muller & Kräussl, 2011), and the visibility of nonmarket initiatives (Jia & Zhang, 2014). Literature from both theoretical perspectives explored the moderating role of market dynamism and munificence (Goll & Rasheed, 2004; Helmig et al., in press).

Institutional theory studies explored the moderating role of government policy and regulations (Vaaler & Schrage, 2009; Young & Makhija, 2014). Moreover, stakeholder influence capacity—a firm’s ability “to identify, act on, and profit from opportunities to improve stakeholder relationships” (Barnett, 2007: 803)—and the degree of institutional stability (Arya & Zhang, 2009) were identified as important moderators. Scholars drawing on RBV investigated the moderating roles of competitive dynamism; nonmarket engagement strategy in terms of pace, relatedness, and consistency (Tang et al., 2012); firm- and industry-level R&D, innovation, and product differentiation (McWilliams & Siegel, 2000); and ventures’ long-term orientation (T. Wang & Bansal, 2012).

Of particular importance in the literature is the role of agency theory in understanding how managerial factors moderate the performance effects of nonmarket strategies. The first four primary theories assume away the heterogeneity of agency concerns within business organizations. Nevertheless, it is top managers who make strategic decisions and exercise agency in firms’ market and nonmarket environments, and it is unlikely that they are equally accountable to their firms. Thus, the degree of managerial opportunism in undertaking nonmarket activities serves as a crucial moderating mechanism to regulate the performance effects of strategic CSR and CPA.

In the context of CPA research, scholars adopting the agency lens have posited that a large part of spending on CPA, such as lobbying and campaign contributions, are little more than managerial perquisites (e.g., Hadani & Schuler, 2013). Managers may sustain corporate political ties for personal reasons, boosting their personal reputations and advancing their careers by sustaining ties no longer valuable to the focal firm (Sun et al., 2012). Aggarwal, Meschke, and Wang (2012) failed to find any positive effect of investments in political donations on performance; instead, firms holding large amounts of free cash flows engaged in more political donations and less R&D and investment spending, which could be attributed to agency problems.

In the context of CSR, research has long recognized that senior managers may engage in self-serving philanthropic activities as a result of social pressures to gain approval from local business elites or to conform to wider societal expectations (Wright & Ferris, 1997). More recent CSR-related studies have investigated the performance outcomes of the agency conflicts involved in pursuing social and environmental objectives (e.g., Barnea & Rubin, 2010; H. Wang et al., 2008). H. Wang and colleagues (2008) found that the positive effect of corporate giving on financial performance leveled off when philanthropic activities reached an excessive level that generated considerable managerial self-serving opportunities. Such studies provide cumulative support for the agency problem in firms making an exceedingly large amount of social investments with negative performance outcomes.

Beyond a better understanding of moderating relationships, these agency studies support a reverse causality between nonmarket strategy and performance: High profits allow managers to invest in nonmarket strategies (rather than nonmarket strategies leading to positive financial performance). This argument was posited a long time ago—with regard to CSR—by Waddock and Graves (1997) and has been supported by studies applying the idea of slack resources as a source of agency problems to argue that firms use slack resources to spend on social and environmental causes (Amato & Amato, 2011; Seifert, Morris, & Bartkus, 2004).

An Integrative Framework for Nonmarket Strategy Research

We propose a novel classification of drivers, mediators, moderators, and performance outcomes of nonmarket strategy. Drawing on Aguinis and Glavas (2012), we distinguish between external drivers (why firms may feel compelled to develop nonmarket strategies) and internal drivers (why firms may willingly develop nonmarket strategies). We also distinguish between external outcomes (performance outcomes that primarily affect external stakeholders, e.g., reputation and consumer loyalty) and internal outcomes (performance outcomes that primarily affect shareholders and internal stakeholders, such as e.g., financial return and employee commitment). Departing from Aguinis and Glavas’s (2012) classification, we propose that the external-internal taxonomy be extended to classifying mediators and moderators. We distinguish between mediating mechanisms related to organizational boundary spanning and mediating mechanisms related to firm strategy formulation and between external moderating mechanisms and internal moderating mechanisms.

Underlying Doh and colleagues’ (2012) integrative model was the assumption that there are ample and unrealized opportunities for combining and integrating different strands of institutional theory and traditional strategy perspectives. Following a similar logic, we encompass a wider range of theoretical lenses and introduce the internal-external dichotomy to highlight conceptual complementarities in investigating the nonmarket strategy-performance nexus.

Our resulting integrative framework in Figure 1 underscores the contributions of the five theories in that institutional theory, stakeholder theory, and RDT primarily elucidate external drivers, while RBV and agency theory help elucidate internal drivers. Our framework suggests that the nonmarket strategy–performance relationship can be studied through a multi-theoretical lens that applies at least one theory related to external drivers and one related to internal drivers. Such an integrative approach is capable of providing satisfactory explanations of how the institutional context and social actors can constrain or enable nonmarket capabilities and managerial autonomy. Specifically, our framework can be used to fruitfully explore the following four key sets of relationships.

Context and nonmarket capabilities

A combination of institutional theory and RBV can explore how an organization’s ability to develop nonmarket capabilities is constrained by legal, political, and social contexts, given that certain types of lobbying, advocacy, or multi-stakeholder initiatives may be prohibited or permitted in some national contexts. Conversely, such a combination can help uncover how organizations are able to proactively develop and deploy nonmarket capabilities and even shape the institutional context, particularly in the presence of institutional voids or institutional duality through institutional entrepreneurship or ceremonial adoption of nonmarket practices in a foreign subsidiary.

Context and managerial discretion

A combination of institutional theory and agency theory can explore how the ability of managers to pursue private benefits in nonmarket activities is curtailed or augmented as a consequence of the legal, political, and social contexts. This may involve changes in corporate governance legislation or changing social norms. Conversely, such a combination can explore how managers are able to gain managerial autonomy and pursue private benefits in nonmarket activities by exploiting institutional voids or institutional duality. This may, for example, involve managers investing corporate funds in nonmarket initiatives to pursue idiosyncratic nonmarket initiatives in a foreign subsidiary.

Social actors and nonmarket capabilities

A combination of a relational perspective—stakeholder theory, RDT, or the neo-institutional strand of institutional theory—and RBV can explore how an organization’s ability to develop nonmarket capabilities is constrained by pressures from social actors, given that collective action, for example, through NGO coalitions or multi-stakeholder initiatives, can legitimize or delegitimize certain corporate nonmarket practices. Conversely, such a combination can help to uncover how organizations are able to develop and deploy nonmarket capabilities to counteract stakeholder pressures or even proactively influence social actors (e.g., through issue-specific associations or astroturfing).

Social actors and managerial discretion

Combining a relational perspective and agency theory can illustrate how managers’ nonmarket activities are curtailed as a result of pressures from social actors, since government action or collective stakeholder mobilization may legitimize or delegitimize certain practices. Conversely, such a combination can explore how agents are able to gain managerial autonomy in nonmarket activities by exploiting weaknesses of social actors, for example, the presence of multiple principals (e.g., dispersed share ownership), or conflicts of interest between stakeholder groups (e.g., conflicting interests of social movements or different perceptions of agency costs by social actors).

Integrative framework.

As the previous discussion has demonstrated, our integrative framework helps clarify the complementarities between the five theories that have guided nonmarket strategy scholarship. Note also that Figure 1 can be employed by researchers irrespective of what level of analysis or what specific topic is investigated. Our framework is by no means exhaustive, and additional factors may also be considered. However, this framework is intended to provide a basis from which future theory-informed scholarship can be conducted in a more systematic manner.

Discussion and Future Research

The purpose of this paper has been to review the literature on the nonmarket strategy–organizational performance link from multiple theoretical perspectives and integrate the two strands of the literature, namely, CSR and CPA. Our analysis reinforces the view that empirical evidence on the direct link between nonmarket strategy and organizational performance is inconsistent despite a majority of the studies in our sample reporting a positive association. To address these inconsistencies, we identified the mediators of the association between nonmarket strategy and organizational performance and categorized the mechanisms into those that deal with organizational boundary spanning and those that deal with internal strategy formulation.

Our integrative framework (Figure 1) highlights key drivers, mediators, moderators, and performance outcomes, which we have classified as either external or internal. Above all, our framework emphasizes the different mediators of the relationship between nonmarket strategy and performance. The boundary spanning mechanisms are organized into two broad categories: bridging and buffering mechanisms. Studies drawing on institutional theory to examine bridging strategies highlighted the issue of adaptation to institutional settings, the stakeholder literature emphasized alignment or congruence with the concerns of salient stakeholders, and the RDT literature highlighted the fit between the level and type of interdependencies and various nonmarket strategies, such as the alignment of incentives. The broad consensus is that the various types of alignments, drawn from the different theories predict nonmarket strategy–organizational performance link. What remains a blind spot is how firms grapple with institutional contradictions and nonmarket stakeholder heterogeneity. Empirical evidence on these issues is still limited. For example, in the case of institutional contradictions and hostile social movements, alignment may not be possible to achieve, and could even be pernicious, when stakeholders’ demands are in conflict with each other or when dealing with a social movement whose primary aim is to undermine the firm.

Our discussion of the buffering mechanisms highlights the complementarity between RBV and RDT in terms of understanding the rent-generating processes of nonmarket strategy. However, our knowledge is still relatively limited on how the effectiveness of buffering activities, or the sustainability of the rents, depend on environmental, interorganizational, and intraorganizational factors. For example, political and regulatory shocks and evolutionary changes can erode the effectiveness of the buffering mechanisms (J. Siegel, 2007; Sun et al., 2010), powerful politicians and stakeholders may appropriate the rents once created from the buffering mechanisms (Dieleman & Boddewyn, 2012), and agency considerations, rather than organizational-rent-generation motives, may drive the buffering activities (Hadani & Schuler, 2013). In short, we still have very limited knowledge about how the process in which the rent-generating buffering activities predicted by RBV and RDT interacts with subsequent rent appropriation to impact on performance across different institutional contexts (Coff, 1999; Sun et al., in press).

Whereas research on boundary spanning factors focused on the management of nonmarket stakeholders, a small but growing body of research concentrated on organizational strategic choices regarding strategy formulation. Relative to the former, this is a newer research theme. One important line of work emerging from this research is the integration of market and nonmarket strategies. Although the existing literature consistently points to the importance of integrating market and nonmarket strategies, the empirical evidence available on the impact of the integration on organizational performance is very limited. For instance, MNEs can adapt their market strategies to local idiosyncrasies, but how do stakeholders react when the MNE forsakes its nonmarket strategy at home to adapt to local institutional settings? It may also be useful to adopt a configurational approach in describing nonmarket strategies for MNEs (Short, Payne, & Ketchen, 2008).

Our survey reveals that work is also emerging with respect to mediators related to complementarities between CSR and CPA. However, despite the repeated calls for CSR-CPA integration in nonmarket research, very few empirical studies examined the impact of integrating CSR and CPA on performance. Conceptual research has been primarily directed at conceptualizing how complementarities between CSR and CPA strengthen the nonmarket strategy-performance link.

This brief discussion already highlights the need for a number of directions for future research, and our integrative framework in the preceding section can serve as a starting point for exploring key sets of relationships using different theoretical lenses. In the following, we summarize the main challenges that future scholarship on the nonmarket strategy–performance link needs to tackle: integrating CSR and CPA research, using different theoretical perspectives at different levels of analysis, and borrowing insights from other related disciplines.

Complementarity Between Strategic CSR and CPA

Although there is a broad consensus that complementarity between CSR and CPA matters for firm performance, the association between the two practices and its performance impacts are not yet clear. Studying the two practices in combination may yield unique insights on the value of a first-mover advantage for firms proactively pursuing integrated nonmarket strategies, substitution effects between political and social strategies of firms, or the outcomes of integrated nonmarket strategies for other stakeholder groups outside the organization. New perspectives emerging from this strand of inquiries can potentially reshape extant nonmarket strategy research agendas. In addition to the five theoretical lenses, scholars could borrow insights from social movement theory to explain when, how, and why firms implement different mixes of private and public politics to engage with social movements and what determines the effectiveness of the overall nonmarket strategy that result from these interactions. For instance, when are firms and social movements more likely to engage in private politics to enact practices consistent with the demands of social movements, and when do they resort to public politics to thwart their demands through CPA? And what are the performance implications thereof?

Given the significant CPA (Hillman & Wan, 2005) and CSR activities (Surroca, Tribó, & Zahra, 2013) in the foreign subsidiaries of MNEs, future research on CPA-CSR integration may fruitfully contribute new insights into MNE research. This can include exploring the integration of nonmarket activities at the subsidiary level, the subsidiary-headquarter relationship with regard to this integration, and the characteristics of institutional environments in different host countries that impinge on this integration. For example, an especially fruitful area of research would be to assess the variability of CPA-CSR integration among MNE subsidiaries in different emerging economies, given the wide differences in regulatory enforcement and approaches in different countries.

Scholars could consider the effects of internal (in)consistency within CSR and CPA practices. Some CSR practices may complement CPA activities, thereby diminishing stakeholders’ tendency to question the veracity of CSR activities. However, these CSR practices may not be aligned with other CSR initiatives, which increase stakeholders’ apprehension about the firm’s overall CSR strategy. An interesting future avenue would be to explore how the degree of complementarity affects organizational performance.

Future scholarship could investigate the extent to which this CSR-CPA complementarity differs among different types of CSR and CPA. For example, studies of environmental initiatives report a particularly high positive association between nonmarket strategy and performance, while other types of CSR may show a much lower positive association. Thus, while in this review we considered environmental initiatives and dealing with corruption as subsets of CSR and CPA, future studies could unpack the initiatives into specific types. For instance, scholars could distinguish between social responsibility and environmental initiatives when investigating complementarity.

Multi-Theoretical Approaches at Multiple Levels of Analysis

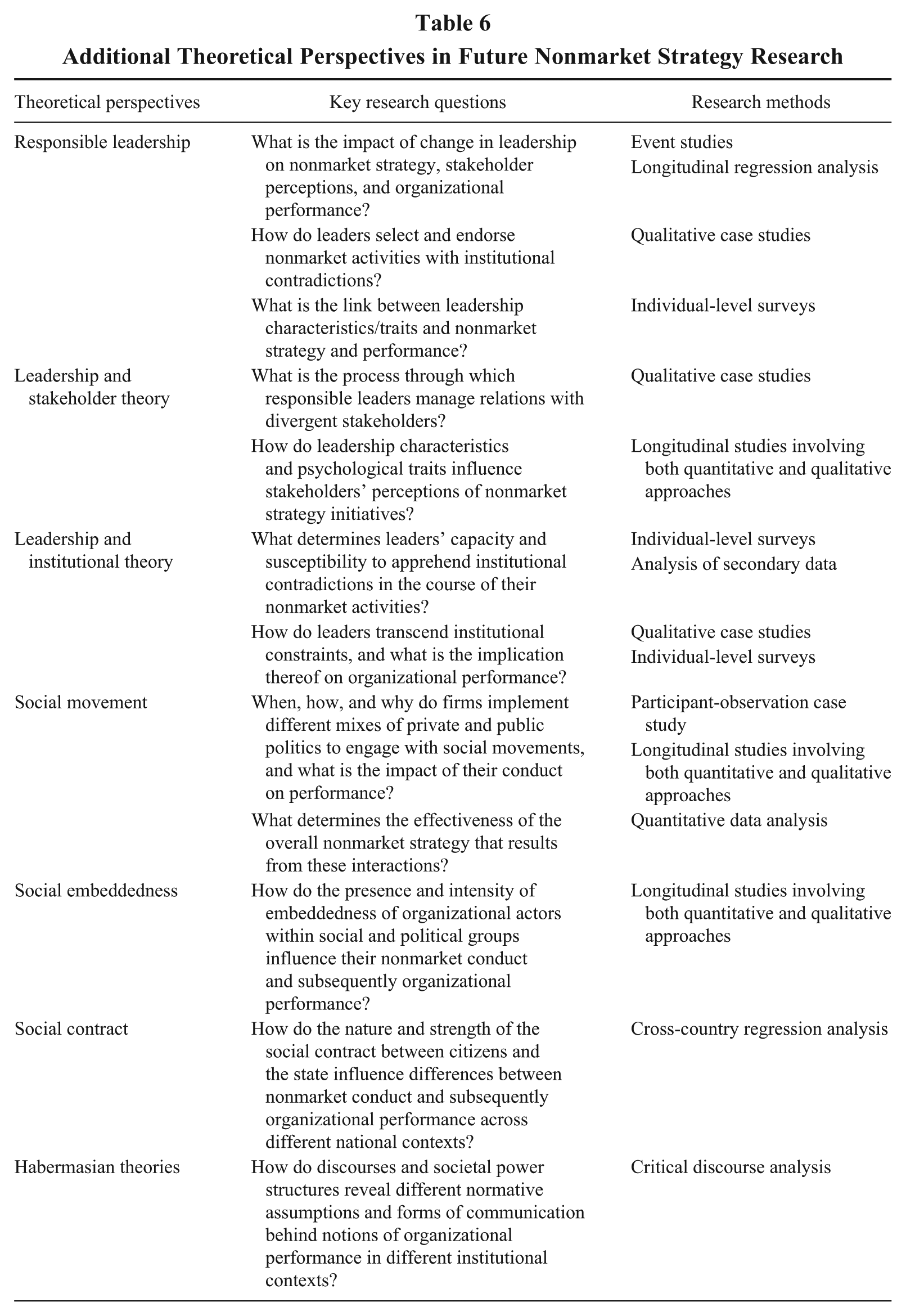

Our survey reveals that nonmarket strategy encompasses a mixture of reactive, anticipatory, and proactive elements. For example, firms may adopt nonmarket strategies in response to isomorphic or stakeholders’ pressures, or they may adopt proactive nonmarket strategies in order to exploit opportunities for value creation. Nonmarket strategy may be an outcome of factors at different levels of analysis: the macro (e.g., government tax incentives), the meso (e.g., specific business opportunities), and the individual level (e.g., cognition of individual CEOs). Therefore, in line with recent calls for a shift toward multi-theory and multilevel research on nonmarket strategy (Aguinis & Glavas, 2012; Frynas & Stephens, 2015), combining some of the five theories reviewed in the paper provides a convenient starting point for future nonmarket strategy research across different levels of analysis, though research may still benefit from additional insights and borrowings. Various strands of nonmarket strategy research would benefit from a multilevel and multi-theory lens, such as “private corruption” and other corporate illegal activities (e.g., tax evasion or anti-trust violations). Most of the research on corruption focuses on government corruption and its impact on company operations, namely, reactive strategies (Brouthers, Yan, & McNicol, 2008; Rose-Ackermann, 1999). But we know little about proactive strategies for addressing corruption, substitution effects between nonmarket strategies and corruption, and the influence of managerial cognition with regard to private corruption.

Future research should also attempt to bridge the micro-macro divide that pervades CSR and CPA research (and management research more generally). Most research on nonmarket strategy has been conducted at the macro or firm level and is largely silent about the impact of micro-level factors (Lawton, McGuire, & Rajwani, 2013; Morgeson, Aguinis, Waldman, & Siegel, 2013). A number of scholars (Aguinis & Glavas, 2012; Doh & Quigley, 2014) argue that more research is needed on the underlying psychological processes associated with CSR. Nonmarket strategy decisions are made by leaders whose motives, judgment, and choices may differ significantly. Therefore, research is needed on the role of heterogeneity of leaders and their interface with the nonmarket environment in driving firm performance. A growing literature on responsible leadership is starting to explore how managers’ intentions and choices influence firms’ nonmarket strategy and subsequently, performance. As argued by Waldman and Balven (2014), since CSR activities are consciously and deliberately initiated and endorsed by leaders of organizations, it makes sense to identify the micro-foundations of the practice. They explain that the study of responsible leadership “is not about whether organizations act responsibly, but about how individuals act and make decisions” (2014: 224).

As a starting point, scholars may want to integrate the proposed micro-foundation of nonmarket strategy with existing theories such as agency theory and stakeholder theory. Doh and Quigley (2014), for example, propose a theoretical framework that links stakeholder and leadership theories and unpacks the pathways through which responsible leaders are able to influence organizational outcomes. They argue that responsible leaders “who take an open and inclusive approach to understanding and incorporating the views of a diverse set of stakeholders into executive decision making may have a positive impact” (2014: 270). Particularly interesting is how responsible leaders can influence stakeholders through a psychological path that consists of trust, commitment, and ownership. And how do leadership characteristics and psychological traits influence stakeholders’ perceptions of nonmarket strategy initiatives? This line of inquiry will enrich the nonmarket strategy literature by focusing on the interaction between leaders and stakeholders.

As an alternative to stakeholder theory, the micro-foundation of nonmarket strategy brings human agency back into institutional theory. The key assumption here is that leaders are active agents within institutions and are sometimes able to break through the institutional blinders imposed by institutional arrangements (Marquis & Raynard, 2015). This raises several interesting questions: What determines the leader’s capacity and susceptibility to apprehend institutional contradictions in the course of their nonmarket activities? How do leaders transcend institutional constraints and implications thereof on organizational performance? Scholars may draw on the growing literature on embedded agency to better understand these intriguing issues.

In order to better understand managerial/leader choices with respect to nonmarket strategies, scholars may also draw on a range of other theories, including conventional theories of the firm and shareholder wealth maximization (see a debate on this issue in Waldman & Siegel, 2008) and theories from other disciplines including psychology and sociology.

Insights From Related Non-Business Disciplines

Similar to management research in general, nonmarket strategy scholars have successfully borrowed concepts and theories from adjacent disciplines such as sociology (e.g., RDT and institutional theory) and economics (e.g., agency theory) (Whetten, Felin, & King, 2009). We firmly believe that there is enormous value in continuing to borrow conceptual insights and methodologies from such related disciplines as sociology, political science, psychology, and history.

Recent contributions in top sociology journals show a growing interest of sociologists in different aspects of nonmarket strategy (Bartley, 2007; Lim & Tsutsui, 2012; Walker & Rea, 2014). Regarding the need for more micro-level analysis, the micro-foundation perspective is lined well with the sociological literature on social embeddedness. Given that managers’ actions are embedded in social relations (Uzzi, 1996), managers are most likely to support and be loyal to social or political groups to which they are most closely tied. That is, from the embeddedness perspective, stakeholders with strong ties to the manager may take precedence over demands of other stakeholders (Michelson, 2007). An interesting research question here is: How does the embedddeness (its presence and intensity) of organizational actors within social and political groups influence their nonmarket conduct and subsequently organizational performance (Sun et al., 2010)? Will political embeddedness on the part of focal firms lead to a backlash from other societal stakeholders over time? Insights from the social movement literature in sociology are extremely fruitful and can shed light on some blind spots in nonmarket strategy research (for a detailed discussion of why and how management scholars borrowed and applied social movement literature from sociology, see Whetten et al., 2009: 16-21).

In addition, recent scholarship on political CSR has introduced various political theories, including social contract and Habermasian theories (Frynas & Stephens, 2015). While these theories are currently not utilized in studies investigating the nonmarket strategy–performance link, linking nonmarket strategy research to theories from political philosophy or international relations could help explain political changes at domestic and global levels that affect the macro nonmarket environment within which firms operate, beyond the current insights that inter alia institutional theory is able to offer. This will in turn help explain performance differences between different institutional environments. Using social contract theories, future nonmarket strategy research could investigate, for example, how the strength of the social contract between the state and its citizens across a firm’s different host countries (measured, e.g., with the help of World Values Survey data) serves to legitimize or delegitimize different combinations of nonmarket strategies and hence affects the performance of such strategies. Going beyond the positivist focus on empirical facts, insights from Habermasian theories could help unpack the intersubjective validity of organizational performance, given the evidence that the link between CSR and organizational outcomes depends on social construction within different institutional contexts, including different forms of communicating performance in different countries and the publication outlet where the evidence on performance is published (Maignan & Ralston, 2002; Orlitzky, 2011).

In Table 6, we summarize the aforementioned discussion and outline some promising future research questions emanating from the integration of stakeholder theory and leadership and the proposed theories and perspectives, namely, responsible leadership, social movement, social embeddedeness, social contract, and Habermasian theory, together with appropriate research methods to address these questions. This list is by no means exhaustive, and other related disciplines such as business history and psychology can contribute further to a better understanding of the nonmarket strategy–performance link. Indeed, borrowing new insights from non-business disciplines may potentially lead to some of the greatest advances in our understanding of nonmarket strategy.

Additional Theoretical Perspectives in Future Nonmarket Strategy Research

Conclusion

Our analysis of the nonmarket strategy literature reveals a disconnection between scholars’ call for multi-theoretical perspectives and the overreliance on single theoretical lenses in empirical research. To address this gap, we have synthesized the two strands—strategic CSR and CPA—of the literature and outlined a framework that provides a theoretical foundation for future research on the nonmarket strategy–performance link by integrating institutional theory, stakeholder theory, RDT, RBV, and agency theory. As discussed in our review of the literature, the first four theories are well developed with regard to nonmarket strategy–performance mediators. The contribution of agency theory is concerned largely with nonmarket strategy–performance moderators. We suggest that intraorganizational- and individual-level factors, which are understudied in the current literature, play a vital part in capturing fully the interplay between nonmarket strategy and organizational performance. We make the case for greater theoretical, micro-macro integration in the nonmarket strategy literature to develop a better understanding of the impact of nonmarket strategy on organizational performance.

Footnotes

Acknowledgements

The authors would like to acknowledge and thank William Wan (Associate Editor) and two anonymous reviewers for their constructive and insightful remarks during the review process. Pei Sun is grateful for financial support from China’s National Natural Science Foundation (grant number: 71102014).