Abstract

This study examines whether auditors’ task-specific expertise acquired during the initial recognition and valuation of goodwill influences clients’ subsequent goodwill accounting. Given the complexity of goodwill valuation, the high degree of managerial discretion involved, and the potential for auditor bias, we hypothesize that auditors-in-charge who serve during a client’s acquisition year and thereby acquire client-specific expertise affect the timeliness and magnitude of subsequent goodwill impairments during their remaining tenure. Using data on Swedish auditors and their publicly-listed clients, we find that both the likelihood and magnitude of goodwill impairments increase with the client-level task-specific expertise of the auditor-in-charge. In contrast, evidence for portfolio-level or audit firm-level expertise is weaker and less consistent. However, portfolio-level and audit firm-level expertise are more relevant in homogeneous industries, within the largest audit firm, and among auditors with pre-IFRS regulatory experience. Overall, our findings suggest that audit quality in goodwill accounting is primarily driven by client-level skill acquisition of the individual auditor, whereas the transferability of task-specific knowledge across engagements depends on the industry structure, audit firm scale, and auditors’ regulatory training.

Introduction

The auditing literature has long established that auditor expertise is an important determinant of audit outcomes. Although early research primarily focused on industry specialization, more recent studies examine how task-specific expertise in particular accounting domains that often transcend industry boundaries affects audit outcomes, including fair value accounting, multinational accounting, and taxation (e.g., Ahn et al., 2020; Christensen et al., 2015; Goldman et al., 2022; Gunn & Michas, 2018; Stein, 2019). A related and emerging strand of the literature investigates event-specific specialization, such as auditors’ expertise in mergers and acquisitions, and how this expertise influences clients’ accounting for acquisition-related transactions (Gal-Or et al., 2022; Mao & Yin, 2017). Across these settings, prior studies consistently find that aggregated expertise at the audit office or audit firm level is associated with beneficial audit outcomes. Reflecting this emphasis, the Public Company Accounting Oversight Board (PCAOB) in the United States (US) encourages audit clients to consider auditor expertise by asking, for example, “Does your auditor have the expertise necessary to address the audit issues that may arise from the reporting requirements related to business combinations as well as other effects of a business combination…?” (PCAOB, 2015b). Notably, however, the PCAOB does not specify whether this expertise should be assessed at the level of the individual auditor responsible for the engagement or at the level of the audit firm or office. Despite the growing interest in task-specific and event-specific specialization, audit research to date provides limited evidence on whether and how the expertise of individual auditors with complex accounting items or events translates into audit outcomes (Amel-Zadeh et al., 2023).

In this study, we investigate whether auditors’ task-specific expertise influences clients’ financial reporting outcomes. Specifically, we examine whether auditors-in-charge who serve during a client’s acquisition year, thereby acquiring client-level expertise, influence the timeliness of subsequent goodwill impairments during their remaining tenure. 1 We also examine the effects of portfolio-level expertise of auditors-in-charge and the expertise of audit firms. Because the initial recognition and valuation of goodwill involve unverifiable assumptions and substantial audit effort, auditors who participate in acquisition-date discussions may be better positioned to evaluate subsequent goodwill valuations. At the same time, their prior involvement may shape later impairment assessments, analogous to evidence that managers responsible for acquisitions are more likely to delay subsequent goodwill impairments (Beatty & Weber, 2006; Ramanna & Watts, 2012). Although auditors do not share managers’ bonus-related incentives, they may nonetheless face reputational concerns or dismissal risks associated with the recognition of goodwill impairments (Ayres, Neal, et al., 2019).

We use data on Swedish auditors and their publicly listed clients from 2005 through 2019. The Swedish setting is particularly well suited for these analyses because auditors-in-charge sign audit reports with their names and affiliations both before and after the adoption of International Financial Reporting Standards (IFRS) in 2005. This feature enables us to track individual auditors over time and examine how they develop task-specific expertise at both the client and portfolio level. To capture client-level expertise, we measure the cumulative amount of goodwill recognized during an auditor’s tenure with a given client, scaled by the client’s reported goodwill balance. For clients with goodwill, this measure equals zero if the auditor was not responsible at the time of the initial recognition. The measure increases with expertise and equals one if the auditor is in charge for all of the client’s acquisition-related activities. We also capture task-specific expertise at the portfolio level based on an auditor’s cumulative involvement in the initial recognition of goodwill across all other clients. These measures are constructed separately for auditors-in-charge and for audit firms. This design allows us to decompose task-specific expertise into two components that capture skill acquisition at the individual auditor level as well as knowledge dissemination across clients and within audit firms.

Our main results show that client-level task-specific expertise of the auditor-in-charge is positively associated with both the likelihood and the magnitude of goodwill impairments. When restricting the sample to impairment-years, we also find that portfolio-level task-specific expertise of the auditor-in-charge and client-level task-specific expertise of the audit firm are positively associated with the magnitude of goodwill impairments. As such, we find broad evidence of skill acquisition at the individual auditor level, and some support for the view that client-level expertise acquired by an auditor-in-charge can be transferred to other clients. In addition, we find limited evidence of knowledge transfer within the audit firm influencing other clients’ subsequent goodwill accounting. Cross-sectional analyses further indicate that the knowledge-sharing effect is stronger in more homogeneous industries. We also find that knowledge sharing within the audit firm is most pronounced in the largest audit firm, and that auditors who began their careers before IFRS adoption rely more on audit firm-level and portfolio-level knowledge. Collectively, these results indicate that, although client-level expertise of the auditor-in-charge is the dominant driver of goodwill impairments in our setting, the extent to which task-specific knowledge is transferred across clients and within audit firms depends on industry context, audit firm size, and the auditor’s regulatory training background.

Our study makes several contributions to the accounting literature. First, we contribute to the growing literature on task-specific expertise in auditing by examining whether expertise in a complex accounting domain that transcends industries is primarily client-specific or is transferable across clients at the portfolio level. Recent studies document that auditors can develop expertise in domain-specific or event-specific accounting issues, such as fair value accounting, taxation, or mergers and acquisitions, and that this expertise is distinct from industry specialization (e.g., Ahn et al., 2020; Gal-Or et al., 2022; Goldman et al., 2022). Prior evidence generally suggests that this expertise is transferable across clients through knowledge sharing across client portfolios within the audit firm or audit office. We add to the literature by showing that goodwill impairment outcomes in the Swedish setting are primarily driven by the task-specific client-level expertise of the auditor-in-charge.

Second, we contribute to the literature examining whether audit quality is primarily driven by individual auditors or by collective expertise and knowledge spillovers within an audit firm. Much of the prior auditing literature measures expertise at the audit firm or office level and emphasizes the role of aggregated experience and organizational learning in improving audit outcomes (e.g., Shepardson, 2019). In contrast, more recent evidence highlights the importance of individual-level experience in enhancing monitoring effectiveness (e.g., Myers et al., 2023). Our results show that the individual auditor-in-charge is the dominant driver of audit quality in goodwill accounting, even after controlling for audit committee expertise. At the same time, consistent with Shepardson (2019), we find that collective expertise at the audit firm and portfolio level can matter in settings that facilitate knowledge sharing, such as larger audit firms and more homogeneous industries. Thus, we extend the literature by reconciling firm-level and individual-level perspectives, showing that audit firm expertise improves audit quality primarily through the expertise of individual auditors, with knowledge spillovers arising under specific organizational and institutional conditions.

Finally, we contribute to the literature on external monitoring of goodwill-related reporting decisions by highlighting the role of auditors. Prior studies show that institutional investors (Glaum et al., 2018), analysts (Ayres, Campbell, et al., 2019), and independent valuation experts (Gietzmann & Wang, 2020) can constrain managerial discretion in goodwill accounting, and analyst pressure may also induce opportunistic impairment behavior (Han et al., 2021). We show that incumbent auditors-in-charge with greater client-level involvement in the initial recognition of goodwill play a central role in mitigating managerial misuse of discretion in subsequent impairment decisions. Clients with auditors who possess greater client-specific goodwill expertise impair goodwill more frequently and in a timelier manner, underscoring the importance of auditor continuity and task-specific expertise in complex accounting judgments.

Setting and Hypotheses

The Swedish Institutional Setting and Goodwill Accounting

Our study focuses on Swedish firms listed on Nasdaq Stockholm from 2005 through 2019. A key advantage of this setting is that audit reports are personally signed by the auditor-in-charge, which allows us to track individual auditors and their goodwill-related expertise at both the client and portfolio level over an extended period, beginning with the adoption of the impairment-only approach. Although much of the audit work may be delegated, the auditor-in-charge retains full responsibility and legal liability for the engagement. In Sweden, both the auditor-in-charge and the audit firm are formally appointed at the client’s Annual General Meeting, and most engagements are conducted by Big 4 audit firms. In addition, signing auditors are not necessarily partners (Sundgren & Svanström, 2014). Another distinctive feature of the Swedish audit market is that clients may, but are not required to, appoint two separate audit firms and two separate signing auditors. However, the prevalence of joint audits has declined over time. Finally, most publicly-listed firms have their headquarters in the Stockholm area, where the Big 4 maintain central offices that provide specialized support to local offices across the country.

In 2005, the European Union mandated the use of IFRS for all publicly-listed firms domiciled in its member countries. 2 As a consequence, listed firms in Sweden were required, in accordance with IFRS 3 and International Accounting Standard 36, to apply the acquisition method to business combinations and to annually test recognized goodwill for impairment. The process of identifying, recognizing, and subsequently testing goodwill for impairment relies heavily on managerial judgment, particularly with respect to valuation assumptions. Although standard setters’ intention in allowing for managerial judgment was to make goodwill accounting more uniform and informative (Sundvik, 2019), inspections in the US by the PCAOB (2015a) indicate that auditors struggle with determining its fair economic value at the acquisition date. Specifically, auditors are required to evaluate the reasonableness of management’s assumptions underlying goodwill valuations both at initial recognition and in subsequent impairment tests. Prior literature documents that goodwill valuations frequently reflect factors beyond underlying economic fundamentals, suggesting the presence of bias. For example, Shalev et al. (2013) finds that managers misuse discretionary judgment when recognizing goodwill following mergers and acquisitions to inflate goodwill balances, potentially enhancing future earnings and managerial compensation. Bartov et al. (2021) shows that the introduction of the impairment-only approach led to overbidding in mergers and acquisitions and inflated goodwill balances. However, using a sample of firms reporting non-GAAP (Generally Accepted Accounting Principles) earnings, Ashby et al. (2024) finds that firms excluding amortization from non-GAAP earnings recognize more of the purchase price as definite-lived intangible assets and less as goodwill. Other studies provide evidence that managers exercise discretion in goodwill impairment decisions for reasons unrelated to underlying economics (e.g., Glaum et al., 2018; Li & Sloan, 2017; Ramanna & Watts, 2012).

Development of Hypotheses

Audit verification relies on complex and subjective judgments that require auditors to assess both technical compliance with accounting standards and whether reported figures reflect a client’s underlying economics (DeFond & Zhang, 2014; Nelson & Tan, 2005). A large body of archival research documents that auditors’ industry specialization improves audit quality (e.g., Balsam et al., 2003; Bratten et al., 2020; Krishnan, 2003; Reichelt & Wang, 2010). However, because the complexity of accounting standards increasingly transcends industry boundaries, expertise in specific accounting domains may also play an important role in improving audit quality.

Although the literature on task-specific expertise beyond industry specialization remains relatively sparse, prior studies show that auditors exert substantial influence over clients’ accounting choices in domains aligned with their expertise, including taxation (Christensen et al., 2015; Goldman et al., 2022), research and development (Godfrey & Hamilton, 2005), mergers and acquisitions (Gal-Or et al., 2022), and reverse mergers (Mao & Yin, 2017). Ahn et al. (2020) further demonstrates that auditors’ task-specific expertise related to fair value measurement is associated with higher audit quality. Collectively, these studies suggest that expertise in complex accounting domains may improve audit outcomes even when this expertise is not industry-specific.

Although much of the prior literature measures expertise at the audit firm or office level, several studies argue that the incentives, competencies, and judgments of the auditor-in-charge play a critical role in determining audit outcomes (e.g., Aobdia et al., 2015; Carcello & Li, 2013; DeFond & Francis, 2005; Reynolds & Francis, 2000). Although audit work is typically performed by teams, task-specific learning tends to be more pronounced among higher-ranked auditors (Bonner, 1990; Causholli, 2016). This is particularly relevant for goodwill accounting, which is highly material, judgment-intensive, and closely scrutinized at senior levels of the audit. The auditor-in-charge is responsible for planning the audit, interacting with client management, reviewing teamwork, and resolving complex accounting issues in coordination with a review partner (Emby & Favere-Marchesi, 2010). Given the complexity of goodwill valuation, the auditor-in-charge is likely to be directly involved in acquisition-date discussions and in evaluating management’s assumptions regarding goodwill recognition and valuation. This direct involvement is most pronounced at the time of the acquisition, suggesting that client-specific expertise regarding goodwill is primarily accumulated by the auditor-in-charge rather than by junior team members. Despite extensive evidence that auditor expertise affects audit outcomes, limited research examines how individual auditors’ task-specific expertise influences the audit of complex accounting items such as goodwill. Goodwill valuation involves substantial discretion and estimates that are difficult to verify efficiently (Griffith et al., 2015), suggesting that the expertise of the auditor-in-charge may be particularly important in constraining biased reporting and ensuring that impairments reflect underlying economic conditions.

At the same time, competing arguments exist. Although skilled auditors have incentives to deliver high-quality audits to protect their reputation and avoid penalties (Knechel et al., 2013), behavioral biases and independence concerns may reduce auditors’ willingness to challenge goodwill valuations they were involved in initially recognizing. This concern is particularly salient given evidence that goodwill impairments are associated with an increased risk of auditor dismissal (Ayres, Neal, et al., 2019). Reflecting these concerns, the PCAOB has argued that mandatory auditor rotation may improve independence and audit quality, whereas the audit profession has emphasized the importance of client-specific knowledge and the potential costs of rotation (e.g., Rapoport, 2012). Consistent with these opposing views, the literature documents mixed evidence on the association between auditor tenure and audit quality where some studies find that client-level expertise, often proxied by tenure, improves audit quality (Chen et al., 2008; Chi et al., 2017; Gul et al., 2009; Myers et al., 2003), but others report lower audit quality (Carey & Simnett, 2006; Hamilton et al., 2005).

Furthermore, independence issues have been highlighted in the context of auditing goodwill. Carcello et al. (2020) shows that higher non-audit fees are associated with a lower likelihood of goodwill impairments. Lobo et al. (2017) finds that, in the French joint-audit setting, clients combining two Big 4 audit firms are less likely to impair goodwill and report smaller impairments than clients combining Big 4 and non-Big 4 auditors. Experimental evidence further suggests that auditors are more likely to accept a client’s decision not to impair goodwill when the Chief Financial Officer (CFO) has prior Big 4 audit experience (Favere-Marchesi & Emby, 2018). In a related vein, Beatty and Weber (2006) shows that managers responsible for the original acquisition are less likely to impair goodwill, presumably to avoid signaling a failed acquisition. Analogously, auditors-in-charge may be reluctant to require impairments that would signal that they had previously accepted inflated goodwill valuations. Although auditors do not share managers’ compensation incentives, impairment decisions may still expose them to reputational costs and the risk of losing goodwill-intensive clients (Beatty & Weber, 2006; Ramanna & Watts, 2012). Accordingly, greater involvement in the initial recognition of goodwill could reduce auditors’ willingness to require subsequent impairments, potentially lowering audit quality.

Taken together, these arguments yield conflicting predictions regarding the effect of auditor-in-charge client-level goodwill expertise on subsequent impairment outcomes. Skill acquisition and professional incentives suggest that greater expertise should lead to more timely and larger impairments when economically motivated, whereas behavioral biases and independence concerns suggest the opposite. Because we are unable to establish a clear directional expectation, we formulate our first hypothesis in null form as follows:

Auditor-in-charge client-level goodwill expertise is not associated with a client’s subsequent goodwill impairments.

Although H1 focuses on skill acquisition in the form of task-specific expertise through first-hand experience at the focal client, expertise may also develop and operate through broader learning and knowledge-sharing mechanisms. For individuals or groups to acquire expertise, learning can occur either through direct experience or through the transfer of others’ experiences via formalized channels or informal spillovers within the organization. Research in cognitive psychology emphasizes the role of analogical reasoning in this process, whereby individuals organize prior experiences, recognize similarities between past and current decision environments, and evaluate current alternatives by applying accumulated knowledge (McDonald et al., 2008; Sternberg, 1977).

Consistent with this perspective, Shepardson (2019) shows that audit committee members’ prior first-hand experience with goodwill impairments increases the likelihood of future impairments, suggesting that expertise in goodwill accounting can be abstracted into decision schemes that are applicable beyond a single firm or engagement. This evidence indicates that individuals with task-specific experience may disseminate abstract knowledge related to goodwill accounting and impairment testing to new contexts. At the same time, evidence from Myers et al. (2023) suggests that client-specific experience of individual monitors remains particularly important, because after controlling for general expertise, internally recruited audit committee chairs exhibit more effective monitoring than externally recruited chairs. Taken together, these studies suggest that although task-specific knowledge can be transferable, its effectiveness may depend on the nature of the expertise and the context in which it is applied.

As such, it remains unclear whether task-specific goodwill expertise acquired by an auditor-in-charge is primarily client-specific or whether it can be transferred to other clients through the auditor’s portfolio or disseminated more broadly within the audit firm. Prior audit research provides mixed evidence. Some studies suggest that expertise is uniquely held by individual partners and cannot be uniformly distributed across offices or clients (Chi & Chin, 2011; Chin & Chi, 2009), implying limited spillovers. In contrast, other studies document that audit expertise developed at the firm or office level improves audit outcomes, indicating that audit firms can facilitate effective knowledge sharing across engagements and ranks (Ahn et al., 2020; Hux et al., 2023).

The efficiency of knowledge transfer may depend on whether the underlying expertise is primarily explicit or tacit. Explicit knowledge can be codified and disseminated through documentation and training, whereas tacit knowledge is embedded in personal experience and is more difficult to transfer across individuals and engagements (Duh et al., 2020; Huang et al., 2023). Given the judgment-intensive and context-specific nature of goodwill valuation, task-specific goodwill expertise is likely to contain a substantial tacit component, potentially limiting its transferability across clients or within audit firms.

Because prior literature provides conflicting evidence regarding the extent to which task-specific audit expertise can be disseminated beyond the focal engagement, and because the complexity of goodwill accounting may constrain the transfer of tacit knowledge, we refrain from making directional predictions. Accordingly, we formulate the following hypotheses for the auditor-in-charge as well as the audit firm in the null form:

Auditor-in-charge portfolio-level goodwill expertise is not associated with a client’s subsequent goodwill impairments.

Audit firm client- and portfolio-level goodwill expertise is not associated with a client’s subsequent goodwill impairments.

Research Design

Measuring Task-specific Expertise at the Client and Portfolio Levels

To capture task-specific expertise of auditors, we introduce four variables representing expertise at different levels, where higher values indicate higher expertise. First, we test H1 with TSE_CL_AIC (task-specific expertise at the client level of the auditor-in-charge). This variable is defined as the cumulative amount of goodwill recognized by the focal client during the auditor-in-charge’s tenure (

To capture portfolio-level expertise and examine H2a, we construct TSE_PL_AIC (task-specific expertise at the portfolio level of the auditor-in-charge), defined as the cumulative amount of goodwill recognized across all other clients (j) of the auditor-in-charge during their respective tenures, excluding the focal client i. We scale this cumulative amount by the total reported goodwill balances of those same clients in year t.

4

Accordingly, TSE_PL_AIC reflects the extent to which the auditor-in-charge has accumulated task-specific expertise from engagements with other clients. Higher values indicate greater exposure to goodwill recognition at the portfolio level, independent of the focal client. We express the variable in equation (2) as follows

For audit firms, we test H2b using two measures constructed in direct analogy to the auditor-in-charge measures in equations (1) and (2). First, TSE_CL_AF is defined as the cumulative amount of goodwill recognized by the focal client during the tenure of its current audit firm, scaled by the client’s reported goodwill balance in year t. This measure captures the extent to which the focal client’s goodwill was recognized while being audited by the same firm, irrespective of which individual auditor-in-charge signed the engagement. Similarly, TSE_PL_AF mirrors the portfolio-level measure for the auditor-in-charge presented in equation (2). It is defined as the cumulative amount of goodwill recognized across all other clients of the audit firm during its respective tenures with those clients (excluding the focal client), scaled by the total reported goodwill balances of those clients in year t. Accordingly, TSE_PL_AF reflects the degree of task-specific expertise accumulated at the portfolio level by the audit firm. The construction of the task-specific expertise variables, especially TSE_PL_AF, follow the logic of the fair value expertise measures in Ahn et al. (2020) where expertise is fair value assets and liabilities under audit within an audit office’s portfolio, divided by the fair value assets and liabilities within the office’s city-industry market in the US setting. 5

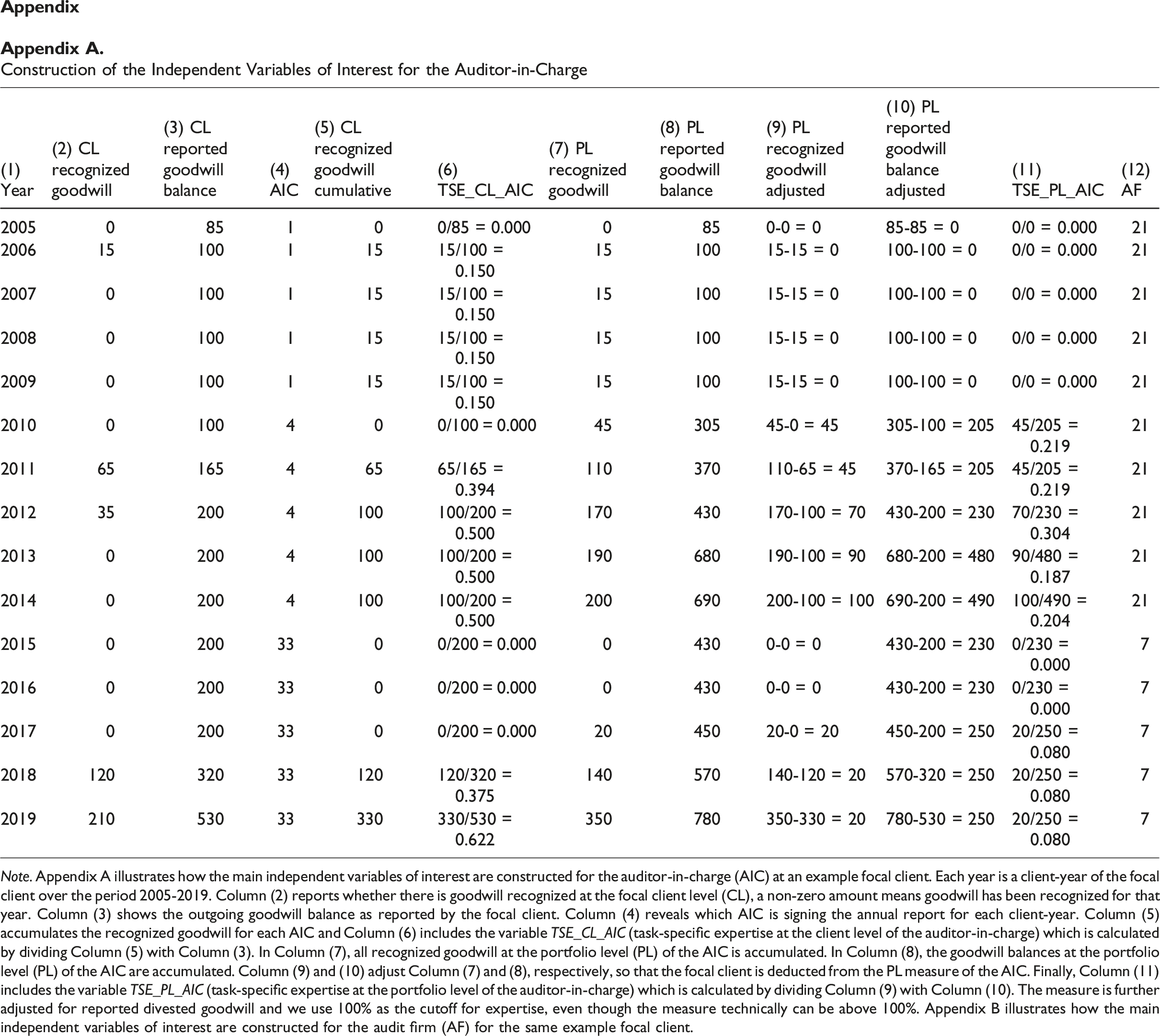

Appendix A illustrates how the auditor-in-charge variables are constructed during the sample period 2005–2019 for a focal client and its three different auditors-in-charge. In 2005, the first individual (AIC #1) has zero TSE_CL_AIC because no goodwill was recognized that year. If the full goodwill balance of the client would have been recognized this year, TSE_CL_AIC would be one. In 2006, goodwill is recognized at the client level which generates 0.150 in TSE_CL_AIC. For TSE_PL_AIC, the measure is still zero because we exclude the focal client and no other clients in the portfolio of the first individual has recognized goodwill. In 2010, the client changes its auditor-in-charge so that TSE_CL_AIC starts from zero. However, the new individual (AIC #2) has a broader portfolio which generates 0.219 in TSE_PL_AIC. Appendix B illustrates how the variables are constructed during the sample period 2005–2019 for the same focal client as in Appendix A but here the focus is on audit firms. We follow the same logic in the calculations for audit firms as with auditors-in-charge. In year 2010, we note that TSE_CL_AF remains at 0.150 for the client-level expertise of the audit firm because the new auditor-in-charge (AIC #2) was affiliated with the same audit firm as the previous auditor-in-charge (AIC #1). If task-specific expertise matters, there will be a difference in the outcomes of impairment tests between higher and lower values of the expertise measures.

Empirical Models and Control Variables

In our main tests, we augment established models predicting both the likelihood and the magnitude of goodwill impairments (e.g., Beatty & Weber, 2006; Ramanna & Watts, 2012) with variables capturing client-level and portfolio-level task-specific expertise. We first estimate the likelihood of goodwill impairment using the following multivariate logistic regression model

Using the same set of right-hand-side variables as in equation (3), we estimate the magnitude of goodwill impairments using the following linear regression model

Sample Selection

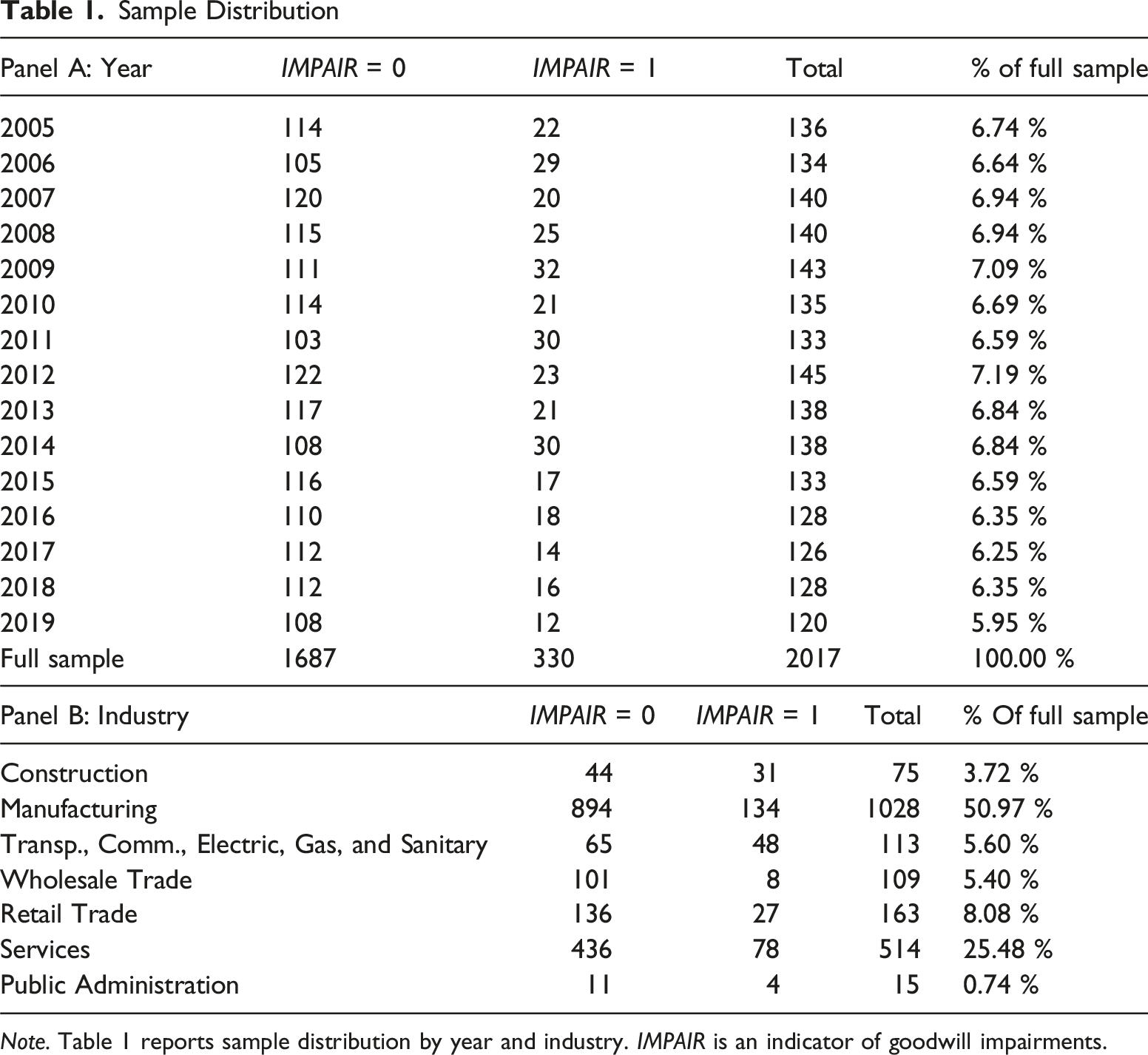

Sample Distribution

Note. Table 1 reports sample distribution by year and industry. IMPAIR is an indicator of goodwill impairments.

Results

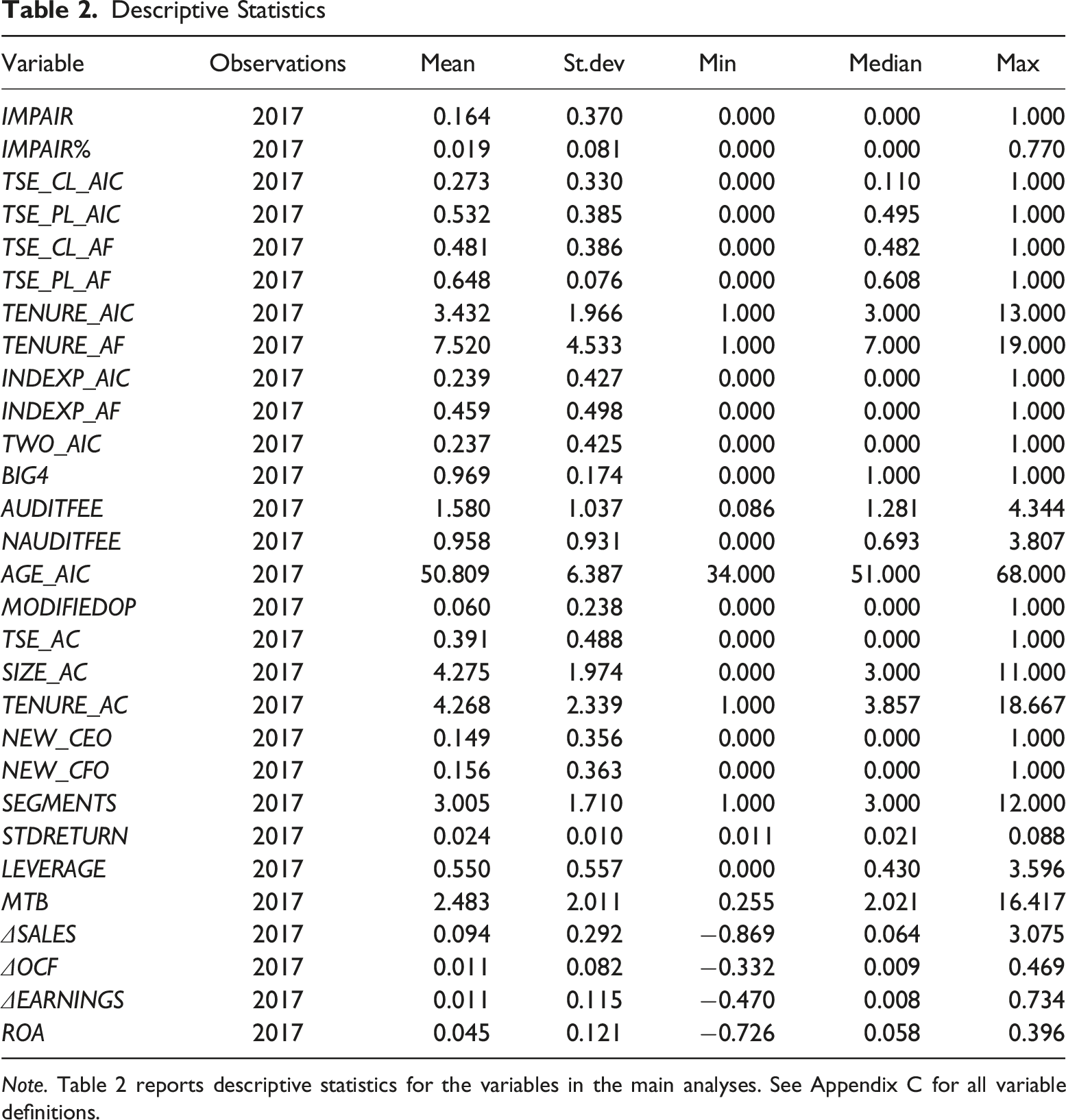

Descriptive Statistics

Descriptive Statistics

Note. Table 2 reports descriptive statistics for the variables in the main analyses. See Appendix C for all variable definitions.

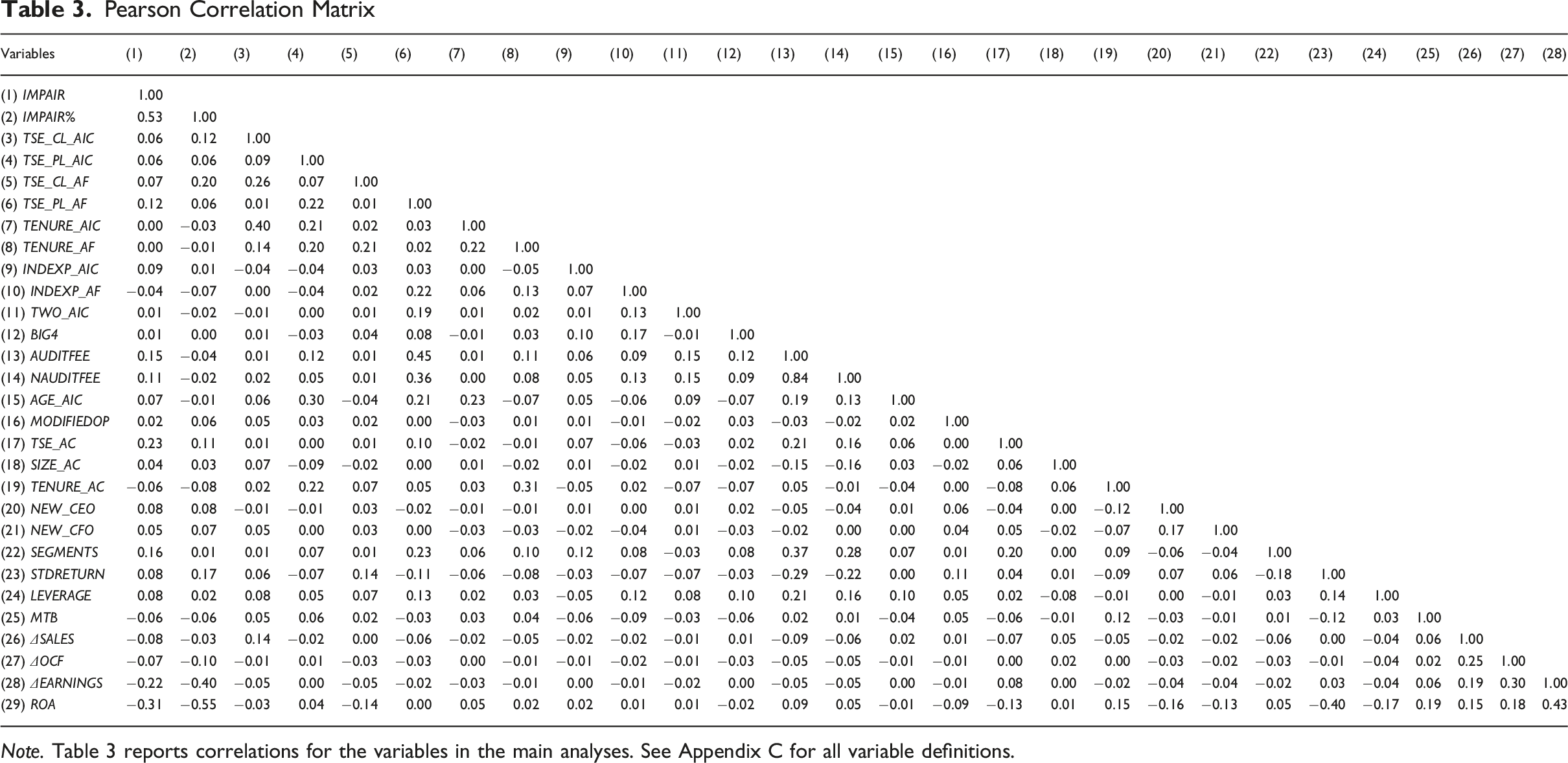

Pearson Correlation Matrix

Note. Table 3 reports correlations for the variables in the main analyses. See Appendix C for all variable definitions.

Main Results

Auditor Task-Specific Expertise at the Client and Portfolio Levels and Goodwill Impairments

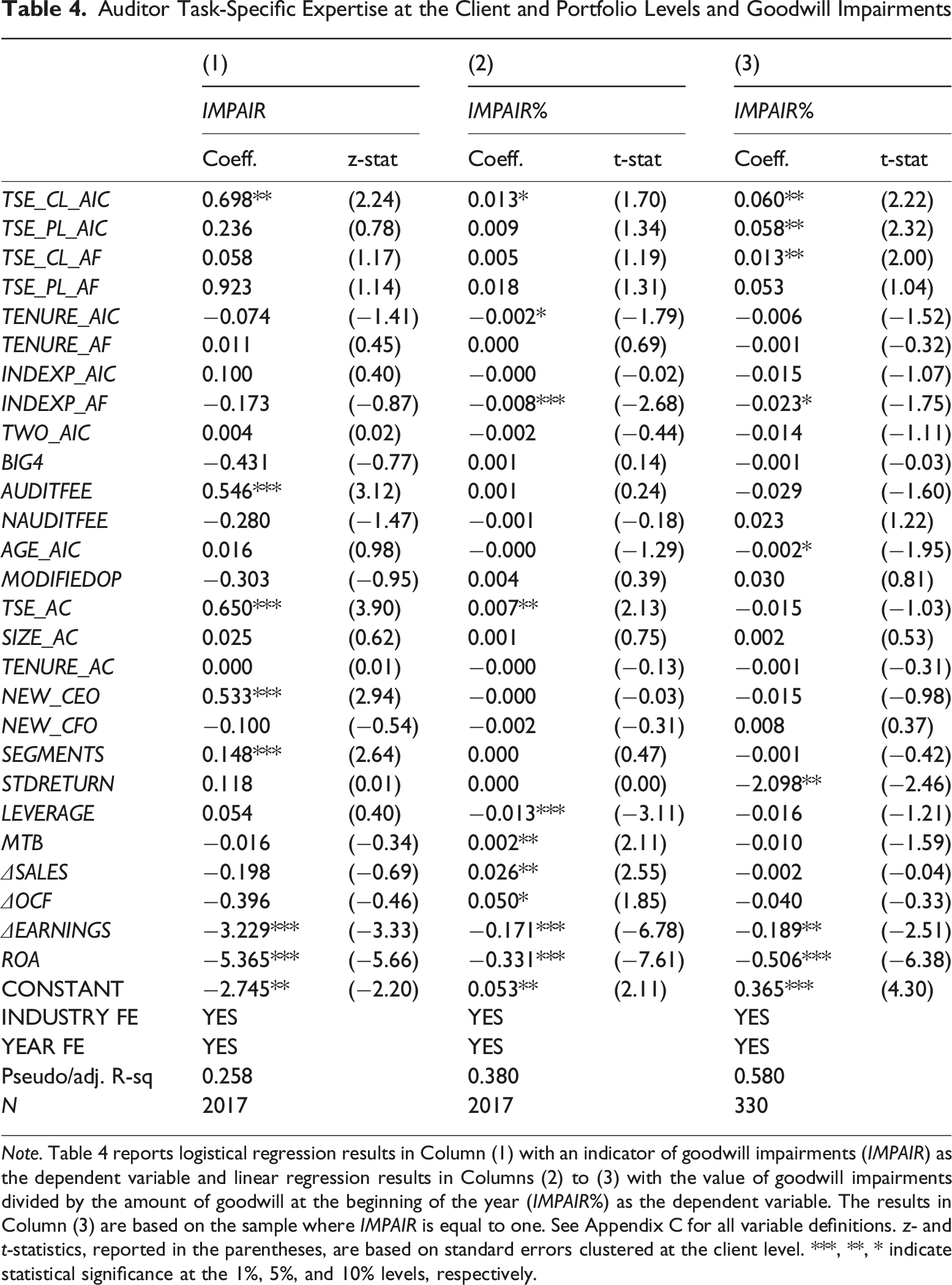

Note. Table 4 reports logistical regression results in Column (1) with an indicator of goodwill impairments (IMPAIR) as the dependent variable and linear regression results in Columns (2) to (3) with the value of goodwill impairments divided by the amount of goodwill at the beginning of the year (IMPAIR%) as the dependent variable. The results in Column (3) are based on the sample where IMPAIR is equal to one. See Appendix C for all variable definitions. z- and t-statistics, reported in the parentheses, are based on standard errors clustered at the client level. ***, **, * indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

Column (2) of Table 4 reports the main regression results for the magnitude of goodwill impairments based on equation (4). The coefficient on TSE_CL_AIC is positive and statistically significant at conventional levels (coeff. 0.013, t-stat 1.70), indicating that goodwill impairments are larger when clients engage auditors-in-charge with greater client-level goodwill expertise. Consistent with the results for impairment incidence, we find no statistically significant effects at the audit firm level or portfolio-level effects of the auditor-in-charge, providing no evidence of knowledge dissemination in this specification. The coefficient on TENURE_AIC is negative and statistically significant (coeff. −0.002, t-stat −1.79). This is consistent with consistent with Ferramosca et al. (2017) that the magnitude of goodwill impairments decreases with auditor tenure. The positive coefficient on TSE_AC (coeff. 0.007, t-stat 2.13) corresponds to the case in Shepardson (2019) and suggests that having audit committees with impairment experience is associated with larger impairments. We re-run the analyses of impairment amounts using a Tobit regression model because the dependent variable is bounded at zero and find consistent results (untabulated).

Next, we restrict the sample to observations in which IMPAIR equals one, thereby excluding client-years without impairments and focusing on the subsample in which the magnitude of impairments is observed. Under this specification, we find positive and statistically significant coefficients on TSE_CL_AIC (coeff. 0.060, t-stat 2.22) and TSE_PL_AIC (coeff. 0.058, t-stat 2.32). Evaluated over the full range of auditor-in-charge expertise, these estimates imply that the magnitude of goodwill impairments increases by approximately six percentage points when expertise is derived either from the focal client or from the auditor’s portfolio. Accordingly, we reject the null hypotheses H1 and H2a in this specification. At the audit firm level, the coefficient on TSE_CL_AF is positive and statistically significant (coeff. 0.013, t-stat 2.00), indicating that impairment magnitudes increase by 1.3 percentage points when client-level expertise is held at the audit firm level. In contrast, we find no statistically significant effect of portfolio-level audit firm expertise. Thus, although we reject H2b with respect to client-level audit firm expertise in this specification, this result is sensitive to model choice. We fail to reject H2b for portfolio-level audit firm expertise.

Taken together, the evidence supports a skill acquisition effect across the specifications, whereby greater client-level expertise of the auditor-in-charge is positively associated with goodwill impairments. In addition, within the subsample of firms that recognize an impairment, we find evidence consistent with a knowledge dissemination effect operating through both the auditor-in-charge’s client portfolio and the audit firm’s client-level expertise.13,14

Results from Cross-Sectional Analyses

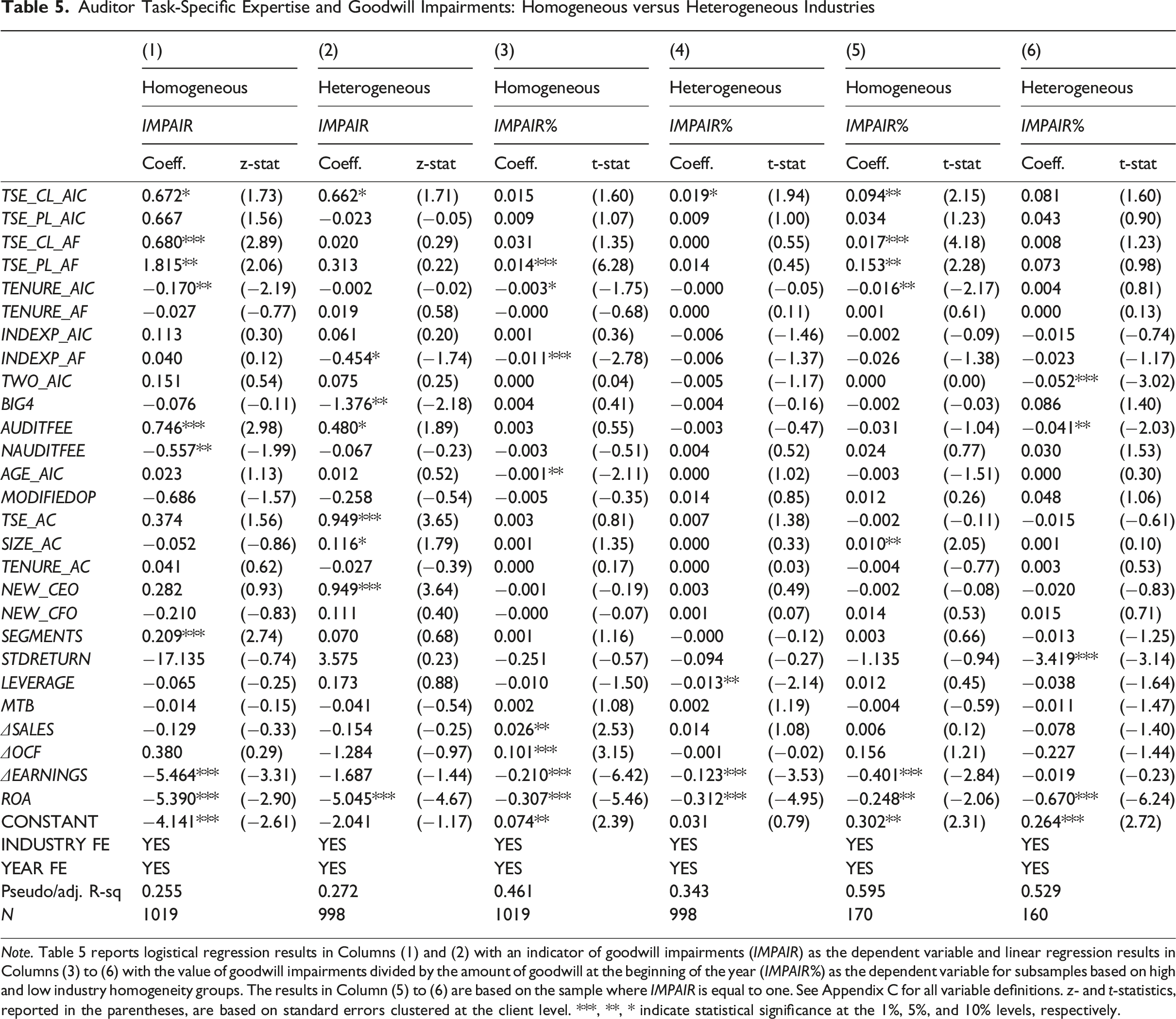

Auditor Task-Specific Expertise and Goodwill Impairments: Homogeneous versus Heterogeneous Industries

Note. Table 5 reports logistical regression results in Columns (1) and (2) with an indicator of goodwill impairments (IMPAIR) as the dependent variable and linear regression results in Columns (3) to (6) with the value of goodwill impairments divided by the amount of goodwill at the beginning of the year (IMPAIR%) as the dependent variable for subsamples based on high and low industry homogeneity groups. The results in Column (5) to (6) are based on the sample where IMPAIR is equal to one. See Appendix C for all variable definitions. z- and t-statistics, reported in the parentheses, are based on standard errors clustered at the client level. ***, **, * indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

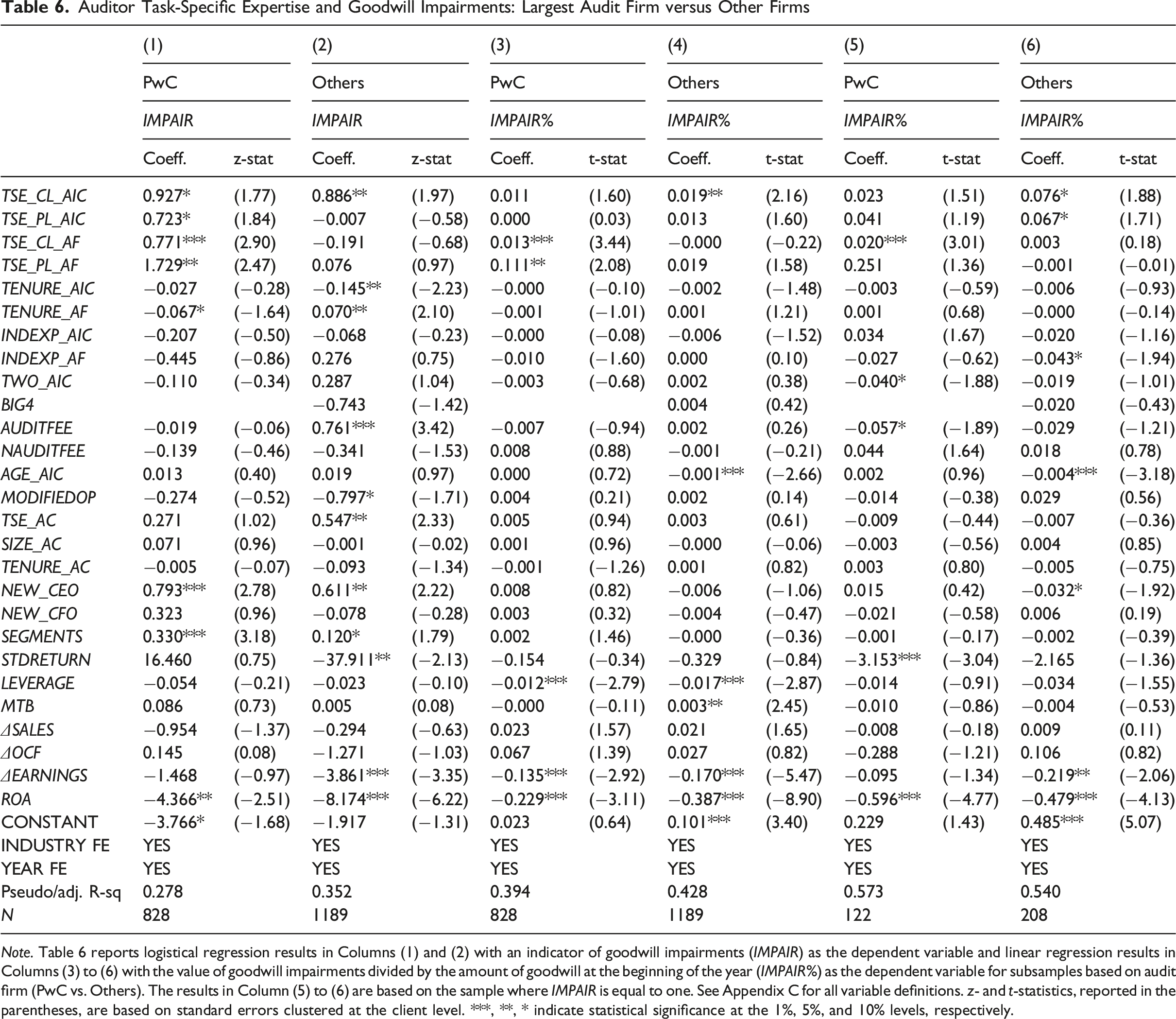

Auditor Task-Specific Expertise and Goodwill Impairments: Largest Audit Firm versus Other Firms

Note. Table 6 reports logistical regression results in Columns (1) and (2) with an indicator of goodwill impairments (IMPAIR) as the dependent variable and linear regression results in Columns (3) to (6) with the value of goodwill impairments divided by the amount of goodwill at the beginning of the year (IMPAIR%) as the dependent variable for subsamples based on audit firm (PwC vs. Others). The results in Column (5) to (6) are based on the sample where IMPAIR is equal to one. See Appendix C for all variable definitions. z- and t-statistics, reported in the parentheses, are based on standard errors clustered at the client level. ***, **, * indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

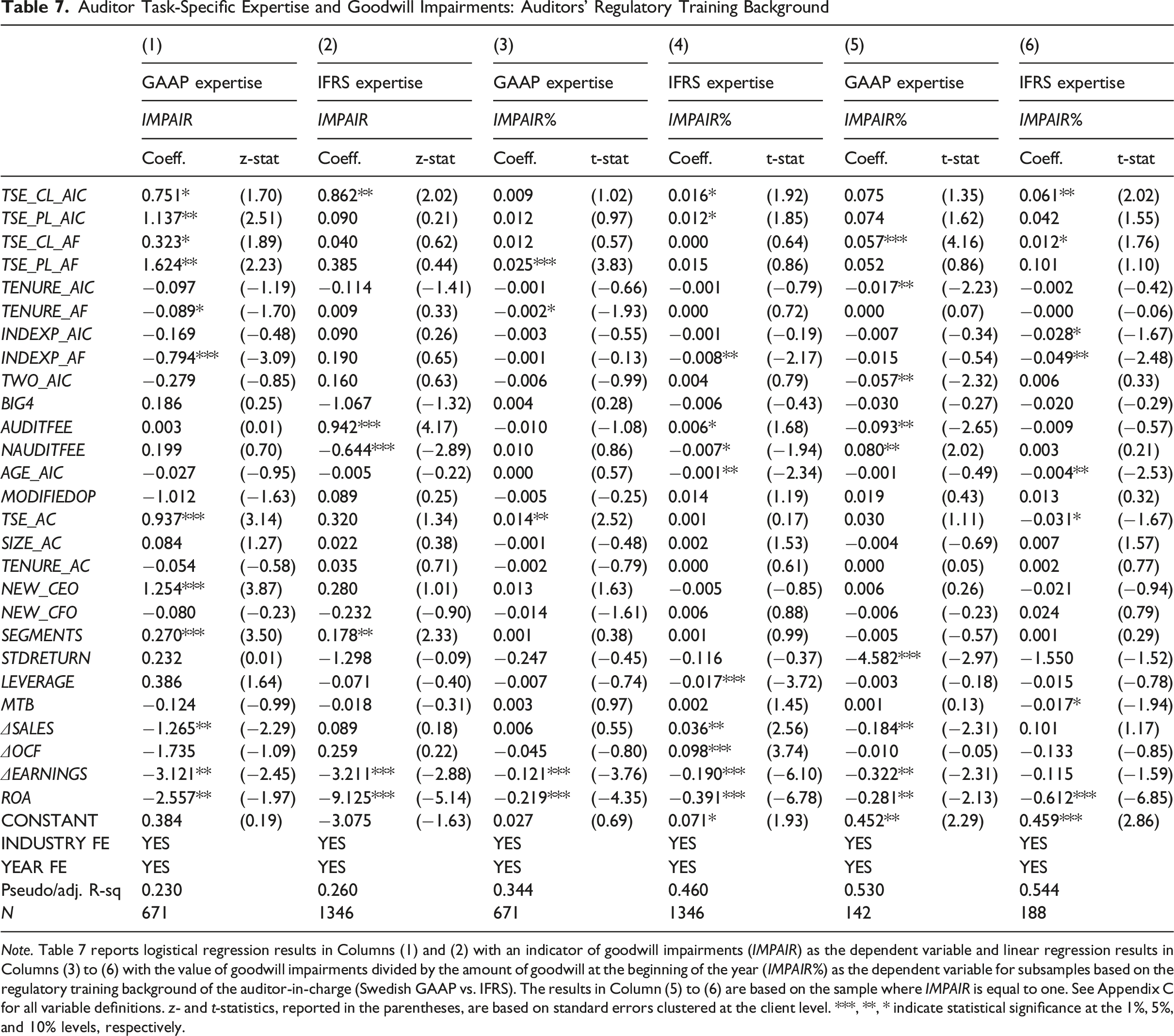

Auditor Task-Specific Expertise and Goodwill Impairments: Auditors’ Regulatory Training Background

Note. Table 7 reports logistical regression results in Columns (1) and (2) with an indicator of goodwill impairments (IMPAIR) as the dependent variable and linear regression results in Columns (3) to (6) with the value of goodwill impairments divided by the amount of goodwill at the beginning of the year (IMPAIR%) as the dependent variable for subsamples based on the regulatory training background of the auditor-in-charge (Swedish GAAP vs. IFRS). The results in Column (5) to (6) are based on the sample where IMPAIR is equal to one. See Appendix C for all variable definitions. z- and t-statistics, reported in the parentheses, are based on standard errors clustered at the client level. ***, **, * indicate statistical significance at the 1%, 5%, and 10% levels, respectively.

Sensitivity Analyses

We conduct four additional sets of tests to investigate the robustness of our inferences and potential confounding factors. First, we recognize that establishing any causal relation is challenging due to unobserved omitted variables, reverse causality, and functional form misspecifications. Our main findings could, for example, be confounded if auditors-in-charge who remain with clients differ systematically from those who are replaced. To help to mitigate this concern, we account for innate heterogeneity of the auditors-in-charge by using alternative estimation models based on propensity score matching (PSM). Here, we form a dummy variable based on the median of TSE_CL_AIC to create a treatment group. We then use PSM to generate a control group based on all control variables in equation (2). We rely on one-to-one matching without replacement and a caliper of 0.01 but find similar results with a caliper of 0.005 (Rosenbaum & Rubin, 1983). The (untabulated) results indicate a positive and statistically significant coefficient on TSE_CL_AIC. The magnitude of the coefficients is larger than in the baseline regressions, mitigating the previously discussed concern. 16 Across all three specifications, we find that the coefficient on TSE_CL_AIC is positive and statistically significant, both for the likelihood of impairment and for the magnitude of impairments. We also find a positive and significant effect for TSE_CL_AF regarding the magnitude of impairments, suggesting that client-level expertise accumulated elsewhere within the audit firm also influences impairments. This latter finding provides some support for a knowledge dissemination effect regarding the audit firm’s client-level expertise. Taken together, the main inferences are robust to matching.

Second, we test whether the inferences hold after excluding the global financial crisis of 2009, when most impairments occurred. With this reduced sample, we continue to find positive and statistically significant coefficients on TSE_CL_AIC in all (untabulated) specifications, whereas the coefficients on TSE_PL_AIC and TSE_CL_AF are only statistically significant and positive within the sample of impairments. The coefficients on TSE_PL_AF are always positive, but insignificant. Overall, our main inferences are not sensitive to excluding this specific year.

Third, we examine the likelihood of goodwill impairments when economic conditions are indicative of impairment. Following prior literature (e.g., André et al., 2016; Carcello et al., 2020; Ramanna & Watts, 2012), we construct alternative measures of economic impairment at the client level and replace the dependent variable IMPAIR in equation (3) with a variable which equals one when a firm carries economically impaired goodwill and recognizes a goodwill impairment in the same year, and zero otherwise. As such, this dependent variable captures a subset of IMPAIR. The purpose of this analysis is to assess whether our main inferences are sensitive to restricting attention to economically meaningful impairment recognitions, while avoiding additional sample restrictions that would lead to sample attrition in our Swedish setting. Following Ramanna and Watts (2012) and Carcello et al. (2020), we first classify goodwill as economically impaired when MTB is below one. Using this definition, the mean of the dependent variable is 0.067 and the coefficient on TSE_CL_AIC (coeff. 0.554, z-stat 1.83) remains positive and statistically significant, indicating that greater client-level expertise is associated with a higher likelihood of impairing economically impaired goodwill. Next, consistent with EFRAG (2016), we define economic impairment based on negative Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA). Under this definition, the dependent variable has a mean of 0.060 and the association with TSE_CL_AIC (coeff. 0.687, z-stat 2.19) remains positive and statistically significant. We also consider negative operating cash flows as an indicator of economic impairment. Using this definition, the mean of the dependent variable is 0.088 and the coefficient on TSE_CL_AIC (coeff. 0.641, z-stat 1.93) continues to be positive and statistically significant. In addition, we find a positive and statistically significant coefficient on TSE_CL_AF (coeff. 0.092, z-stat 1.84), providing evidence of a knowledge dissemination effect at the audit firm level.

Finally, we re-estimate the main tests using client fixed effects following Minutti-Meza (2013). Including client fixed effects absorbs all time-invariant client characteristics, such that the coefficients are identified from within-client variation over time. The (untabulated) results show that the coefficients on TSE_CL_AIC remain positive and marginally significant both regarding the incidence and magnitude of clients’ goodwill impairments, but the magnitude of the coefficients is reduced compared to the main results, and the effect is insignificant in the impairment subsample. For TSE_CL_AF, we find one marginally significant coefficient with IMPAIR% as the dependent variable in the full sample, suggesting that there is some evidence of knowledge transfer once time-invariant client characteristics are accounted for. The coefficients on the portfolio-level measures of the auditor-in-charge and audit firm are all positive but insignificant.

Conclusions

In this study, we investigate auditor task-specific expertise at the client and portfolio level. We posit that for complex accounting items such as goodwill, audit quality is influenced by the extent to which auditors-in-charge and audit firms possess task-specific expertise. Using data for Swedish publicly-listed firms, where auditors-in-charge have signed audit reports for decades, we construct measures that capture the proportion of the goodwill balance initially recognized during the tenure of the incumbent auditor-in-charge and the incumbent audit firm.

Our results show that client-level task-specific expertise of the auditor-in-charge is positively associated with both the likelihood and the magnitude of goodwill impairments. These findings indicate that client-specific expertise accumulated by the auditor-in-charge during the goodwill recognition year contributes to higher audit quality in subsequent goodwill accounting. Cross-sectional analyses further suggest that knowledge sharing and transfer of expertise occur under specific conditions, such as in more homogeneous industries where expertise is more readily transferable across clients and within the largest audit firm.

This study contributes to auditing literature in several ways. First, we add to the literature on task-specific expertise by showing that specialization in complex accounting items that transcend industry boundaries improves audit quality, and that these effects are primarily driven by client-level expertise of the auditor-in-charge. Second, we extend the literature examining whether audit quality is primarily driven by individuals or by collective knowledge spillovers. We show that the client-level expertise of the auditor-in-charge is the dominant driver of audit quality in goodwill accounting, whereas audit firm- and portfolio-level expertise matter more in settings that facilitate knowledge sharing, such as larger audit firms and among auditors with pre-IFRS regulatory training. Finally, we contribute to the literature on external monitoring of goodwill reporting by showing that incumbent auditors-in-charge with client-level goodwill expertise are well positioned to constrain managerial discretion.

Our study is subject to several limitations. First, we are generally unable to link subsequent goodwill impairments to the specific goodwill initially recognized during the period in which the auditor-in-charge acquired expertise. This limitation arises when our expertise measure is below one and reflects the lack of sufficiently granular impairment disclosures by clients, rather than a constraint of the Swedish setting, which is otherwise advantageous due to the availability of individual auditor identifiers. Therefore, we cannot fully disentangle the underlying mechanisms through which auditor expertise affects impairment decisions. Second, we are only able to observe the signing auditors-in-charge and not the full audit team composition for each engagement. It is therefore possible that newly appointed auditors-in-charge already possess client-level expertise through prior involvement as team members. Nevertheless, given that auditing is a team-based activity, it is noteworthy that the signing auditor-in-charge continues to exert a pronounced influence on subsequent goodwill accounting outcomes.

These limitations point to several avenues for future research. One direction is to examine how audit firms allocate audit team members to goodwill-related tasks and how auditors-in-charge prioritize goodwill relative to other complex accounting areas. Another avenue is to study task-specific expertise in other domains, such as taxation or fair value accounting, to assess whether the limited evidence on knowledge transfer within audit firms is specific to goodwill or reflects features of our institutional setting. Future studies could also more directly examine the unlearning process among auditors that we discuss in one of our cross-sectional tests by combining archival data with survey or experimental approaches to capture how individual auditors adapt (or fail to adapt) to major accounting regime changes such as IFRS adoption. Finally, we encourage future studies to examine other institutional contexts, such as the US, where audit partners are now identifiable, to assess the generalizability of our findings of the importance of task-specific knowledge to larger economies and to further explore differences between auditor and managerial behavior across settings.

Footnotes

Acknowledgments

We would like to thank Xiao-Jun Zhang (Editor in Chief), Linda Myers (Associate Editor) and two anonymous reviewers for their constructive feedback throughout the review process. We are also grateful for comments on earlier versions received from Cristina Florio (discussant), Qing Liu, Partha Mohapatra, Kjell Ove Røsok (discussant), Chia-Hsiang Weng as well as participants at the 2021 Nordic Accounting Conference in Copenhagen, 2022 Audit Practice Meet in Umeå, 2022 Botnia Accounting and Auditing Seminar in Helsinki, 2023 Joint Midyear Meeting of the AIS, SET and International Sections of the AAA in Las Vegas, and 2023 JAAF Conference in Helsinki. We gratefully acknowledge financial support from Handelsbanken Research Foundation, Hanken Support Foundation, Liikesivistysrahasto, Peter Wallenberg Foundation, and research assistance from Frans Grönholm. All remaining errors are the authors’ responsibility.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Jan Wallander and Tom Hedelius Foundation (Frii), Hanken Support Foundation (Sundvik), Liikesivistysrahasto (Sundvik), Peter Wallenberg Foundation (Sundvik).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Notes

Author Biographies

Appendix

Construction of the Independent Variables of Interest for the Auditor-in-Charge Note. Appendix A illustrates how the main independent variables of interest are constructed for the auditor-in-charge (AIC) at an example focal client. Each year is a client-year of the focal client over the period 2005-2019. Column (2) reports whether there is goodwill recognized at the focal client level (CL), a non-zero amount means goodwill has been recognized for that year. Column (3) shows the outgoing goodwill balance as reported by the focal client. Column (4) reveals which AIC is signing the annual report for each client-year. Column (5) accumulates the recognized goodwill for each AIC and Column (6) includes the variable TSE_CL_AIC (task-specific expertise at the client level of the auditor-in-charge) which is calculated by dividing Column (5) with Column (3). In Column (7), all recognized goodwill at the portfolio level (PL) of the AIC is accumulated. In Column (8), the goodwill balances at the portfolio level (PL) of the AIC are accumulated. Column (9) and (10) adjust Column (7) and (8), respectively, so that the focal client is deducted from the PL measure of the AIC. Finally, Column (11) includes the variable TSE_PL_AIC (task-specific expertise at the portfolio level of the auditor-in-charge) which is calculated by dividing Column (9) with Column (10). The measure is further adjusted for reported divested goodwill and we use 100% as the cutoff for expertise, even though the measure technically can be above 100%. Appendix B illustrates how the main independent variables of interest are constructed for the audit firm (AF) for the same example focal client.

(1) Year

(2) CL recognized goodwill

(3) CL reported goodwill balance

(4) AIC

(5) CL recognized goodwill cumulative

(6) TSE_CL_AIC

(7) PL recognized goodwill

(8) PL reported goodwill balance

(9) PL recognized goodwill adjusted

(10) PL reported goodwill balance adjusted

(11) TSE_PL_AIC

(12) AF

2005

0

85

1

0

0/85 = 0.000

0

85

0-0 = 0

85-85 = 0

0/0 = 0.000

21

2006

15

100

1

15

15/100 = 0.150

15

100

15-15 = 0

100-100 = 0

0/0 = 0.000

21

2007

0

100

1

15

15/100 = 0.150

15

100

15-15 = 0

100-100 = 0

0/0 = 0.000

21

2008

0

100

1

15

15/100 = 0.150

15

100

15-15 = 0

100-100 = 0

0/0 = 0.000

21

2009

0

100

1

15

15/100 = 0.150

15

100

15-15 = 0

100-100 = 0

0/0 = 0.000

21

2010

0

100

4

0

0/100 = 0.000

45

305

45-0 = 45

305-100 = 205

45/205 = 0.219

21

2011

65

165

4

65

65/165 = 0.394

110

370

110-65 = 45

370-165 = 205

45/205 = 0.219

21

2012

35

200

4

100

100/200 = 0.500

170

430

170-100 = 70

430-200 = 230

70/230 = 0.304

21

2013

0

200

4

100

100/200 = 0.500

190

680

190-100 = 90

680-200 = 480

90/480 = 0.187

21

2014

0

200

4

100

100/200 = 0.500

200

690

200-100 = 100

690-200 = 490

100/490 = 0.204

21

2015

0

200

33

0

0/200 = 0.000

0

430

0-0 = 0

430-200 = 230

0/230 = 0.000

7

2016

0

200

33

0

0/200 = 0.000

0

430

0-0 = 0

430-200 = 230

0/230 = 0.000

7

2017

0

200

33

0

0/200 = 0.000

20

450

20-0 = 20

450-200 = 250

20/250 = 0.080

7

2018

120

320

33

120

120/320 = 0.375

140

570

140-120 = 20

570-320 = 250

20/250 = 0.080

7

2019

210

530

33

330

330/530 = 0.622

350

780

350-330 = 20

780-530 = 250

20/250 = 0.080

7

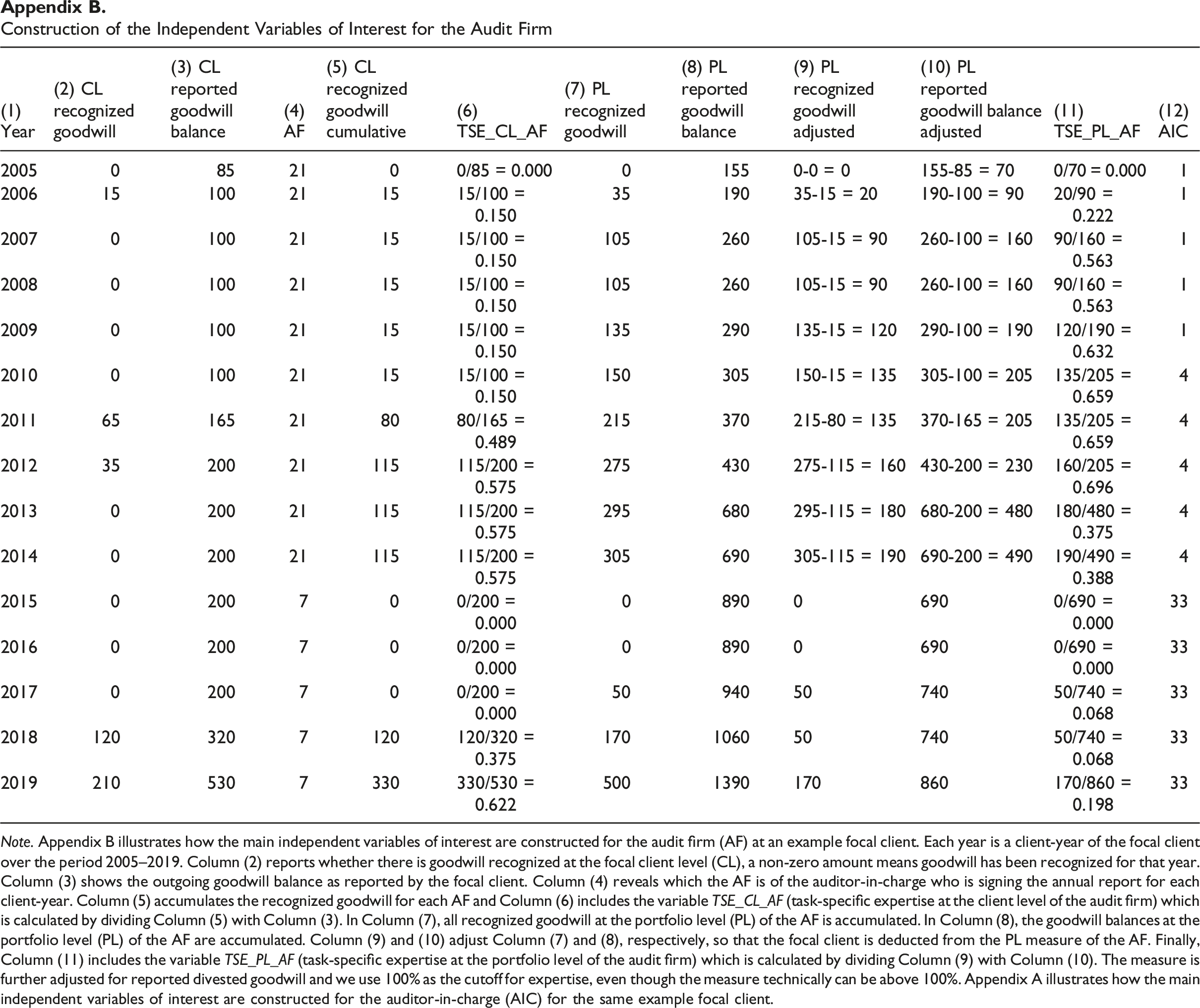

Construction of the Independent Variables of Interest for the Audit Firm Note. Appendix B illustrates how the main independent variables of interest are constructed for the audit firm (AF) at an example focal client. Each year is a client-year of the focal client over the period 2005–2019. Column (2) reports whether there is goodwill recognized at the focal client level (CL), a non-zero amount means goodwill has been recognized for that year. Column (3) shows the outgoing goodwill balance as reported by the focal client. Column (4) reveals which the AF is of the auditor-in-charge who is signing the annual report for each client-year. Column (5) accumulates the recognized goodwill for each AF and Column (6) includes the variable TSE_CL_AF (task-specific expertise at the client level of the audit firm) which is calculated by dividing Column (5) with Column (3). In Column (7), all recognized goodwill at the portfolio level (PL) of the AF is accumulated. In Column (8), the goodwill balances at the portfolio level (PL) of the AF are accumulated. Column (9) and (10) adjust Column (7) and (8), respectively, so that the focal client is deducted from the PL measure of the AF. Finally, Column (11) includes the variable TSE_PL_AF (task-specific expertise at the portfolio level of the audit firm) which is calculated by dividing Column (9) with Column (10). The measure is further adjusted for reported divested goodwill and we use 100% as the cutoff for expertise, even though the measure technically can be above 100%. Appendix A illustrates how the main independent variables of interest are constructed for the auditor-in-charge (AIC) for the same example focal client.

(1) Year

(2) CL recognized goodwill

(3) CL reported goodwill balance

(4) AF

(5) CL recognized goodwill cumulative

(6) TSE_CL_AF

(7) PL recognized goodwill

(8) PL reported goodwill balance

(9) PL recognized goodwill adjusted

(10) PL reported goodwill balance adjusted

(11) TSE_PL_AF

(12) AIC

2005

0

85

21

0

0/85 = 0.000

0

155

0-0 = 0

155-85 = 70

0/70 = 0.000

1

2006

15

100

21

15

15/100 = 0.150

35

190

35-15 = 20

190-100 = 90

20/90 = 0.222

1

2007

0

100

21

15

15/100 = 0.150

105

260

105-15 = 90

260-100 = 160

90/160 = 0.563

1

2008

0

100

21

15

15/100 = 0.150

105

260

105-15 = 90

260-100 = 160

90/160 = 0.563

1

2009

0

100

21

15

15/100 = 0.150

135

290

135-15 = 120

290-100 = 190

120/190 = 0.632

1

2010

0

100

21

15

15/100 = 0.150

150

305

150-15 = 135

305-100 = 205

135/205 = 0.659

4

2011

65

165

21

80

80/165 = 0.489

215

370

215-80 = 135

370-165 = 205

135/205 = 0.659

4

2012

35

200

21

115

115/200 = 0.575

275

430

275-115 = 160

430-200 = 230

160/205 = 0.696

4

2013

0

200

21

115

115/200 = 0.575

295

680

295-115 = 180

680-200 = 480

180/480 = 0.375

4

2014

0

200

21

115

115/200 = 0.575

305

690

305-115 = 190

690-200 = 490

190/490 = 0.388

4

2015

0

200

7

0

0/200 = 0.000

0

890

0

690

0/690 = 0.000

33

2016

0

200

7

0

0/200 = 0.000

0

890

0

690

0/690 = 0.000

33

2017

0

200

7

0

0/200 = 0.000

50

940

50

740

50/740 = 0.068

33

2018

120

320

7

120

120/320 = 0.375

170

1060

50

740

50/740 = 0.068

33

2019

210

530

7

330

330/530 = 0.622

500

1390

170

860

170/860 = 0.198

33

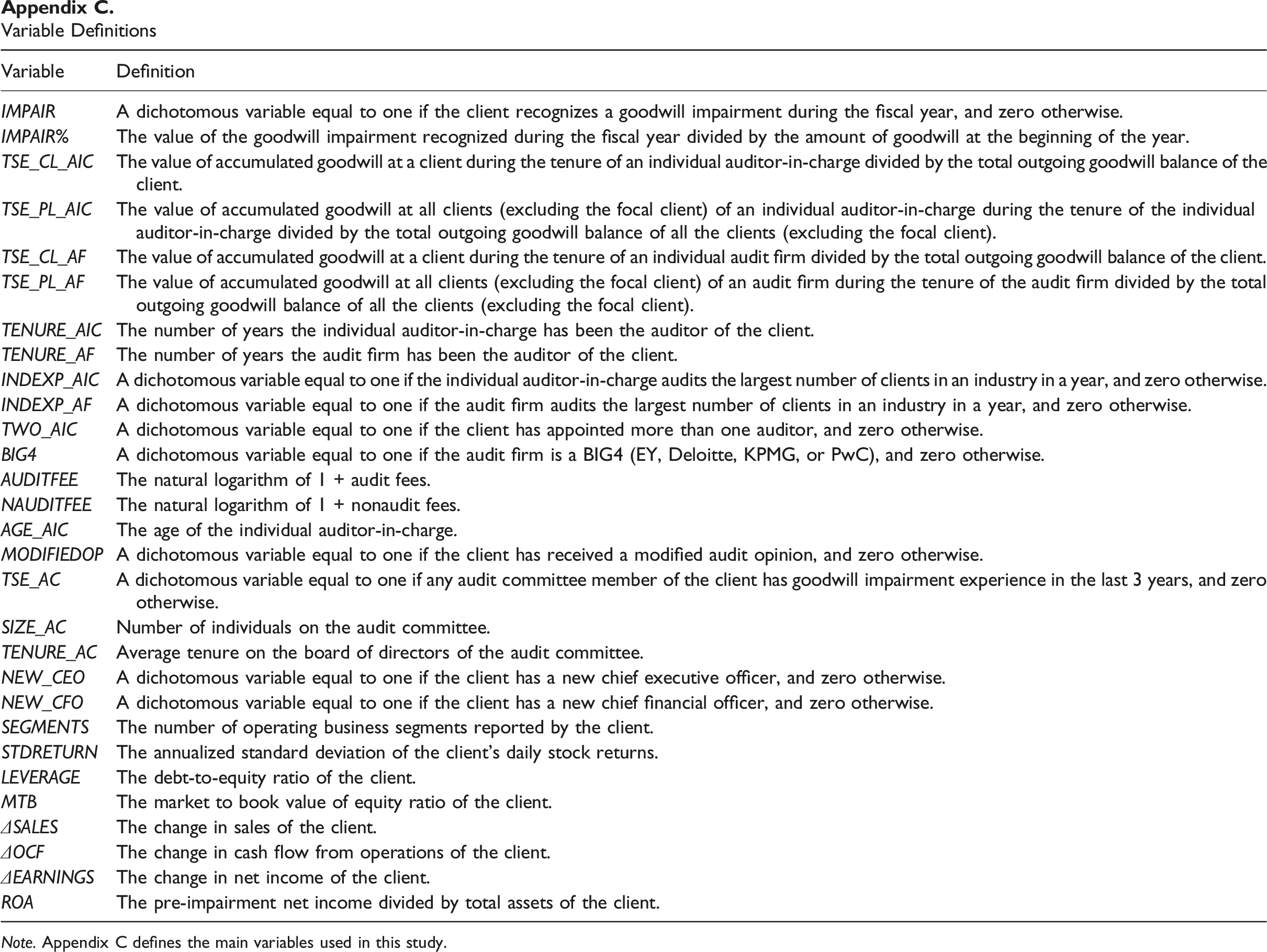

Variable Definitions Note. Appendix C defines the main variables used in this study.

Variable

Definition

IMPAIR

A dichotomous variable equal to one if the client recognizes a goodwill impairment during the fiscal year, and zero otherwise.

IMPAIR%

The value of the goodwill impairment recognized during the fiscal year divided by the amount of goodwill at the beginning of the year.

TSE_CL_AIC

The value of accumulated goodwill at a client during the tenure of an individual auditor-in-charge divided by the total outgoing goodwill balance of the client.

TSE_PL_AIC

The value of accumulated goodwill at all clients (excluding the focal client) of an individual auditor-in-charge during the tenure of the individual auditor-in-charge divided by the total outgoing goodwill balance of all the clients (excluding the focal client).

TSE_CL_AF

The value of accumulated goodwill at a client during the tenure of an individual audit firm divided by the total outgoing goodwill balance of the client.

TSE_PL_AF

The value of accumulated goodwill at all clients (excluding the focal client) of an audit firm during the tenure of the audit firm divided by the total outgoing goodwill balance of all the clients (excluding the focal client).

TENURE_AIC

The number of years the individual auditor-in-charge has been the auditor of the client.

TENURE_AF

The number of years the audit firm has been the auditor of the client.

INDEXP_AIC

A dichotomous variable equal to one if the individual auditor-in-charge audits the largest number of clients in an industry in a year, and zero otherwise.

INDEXP_AF

A dichotomous variable equal to one if the audit firm audits the largest number of clients in an industry in a year, and zero otherwise.

TWO_AIC

A dichotomous variable equal to one if the client has appointed more than one auditor, and zero otherwise.

BIG4

A dichotomous variable equal to one if the audit firm is a BIG4 (EY, Deloitte, KPMG, or PwC), and zero otherwise.

AUDITFEE

The natural logarithm of 1 + audit fees.

NAUDITFEE

The natural logarithm of 1 + nonaudit fees.

AGE_AIC

The age of the individual auditor-in-charge.

MODIFIEDOP

A dichotomous variable equal to one if the client has received a modified audit opinion, and zero otherwise.

TSE_AC

A dichotomous variable equal to one if any audit committee member of the client has goodwill impairment experience in the last 3 years, and zero otherwise.

SIZE_AC

Number of individuals on the audit committee.

TENURE_AC

Average tenure on the board of directors of the audit committee.

NEW_CEO

A dichotomous variable equal to one if the client has a new chief executive officer, and zero otherwise.

NEW_CFO

A dichotomous variable equal to one if the client has a new chief financial officer, and zero otherwise.

SEGMENTS

The number of operating business segments reported by the client.

STDRETURN

The annualized standard deviation of the client’s daily stock returns.

LEVERAGE

The debt-to-equity ratio of the client.

MTB

The market to book value of equity ratio of the client.

ΔSALES

The change in sales of the client.

ΔOCF

The change in cash flow from operations of the client.

ΔEARNINGS

The change in net income of the client.

ROA

The pre-impairment net income divided by total assets of the client.