Abstract

We examine the impact of governance on cost behaviors in the nonprofit sector. Analyzing operations data of 419,350 nonprofit organization-years for the period 2014–2019, we find that better governed organizations are more likely to reduce spending in response to revenue declines consistent with less cost stickiness. We also find that better governance attenuates administrative cost stickiness in response to declines in both program and donation revenues, however, program spending is notably different. While better governed organizations exhibit less cost stickiness in program spending in response to program revenue declines, when faced with declines in donations these organizations are less likely to reduce program spending, consistent with external stakeholder preferences for program over administrative spending. Taken together, our findings provide support for the significant role nonprofit governance plays on cost behaviors, prompting organizations to maintain program spending while curbing administrative spending in response to declining public support.

Introduction

Cost containment and resource management are critical factors for success in the nonprofit sector. Many nonprofit organizations operate with minimal operating reserves and prudent cost management is paramount to the long-term survival of these organizations. 1 Of particular interest is nonprofit managers’ ability to control expenses in the face of declining revenues, given that such times put additional strain on these organizations (Jones et al., 2013). 2 Despite pressure to contain costs, existing evidence points to the prevalence of cost stickiness in the nonprofit sector, sometimes to even greater degree than in the for-profit sector (e.g., Holzhacker et al., 2015a). Jones et al. (2013) find that organizations maintain costs in periods of declining revenues, often by using prior years’ savings. Additional studies confirm the asymmetric response to revenue changes and provide support for sticky cost behavior in German (Holzhacker et al., 2015a) and Canadian (Balakrishnan & Gruca, 2008) hospitals, as well as nonprofit organizations headquartered in New Zealand (Habib & Huang, 2019). In this study we aim to add to our understanding of factors driving the sticky cost phenomenon in the nonprofit sector by investigating the role of governance on organizational spending. That is, we test the moderating effect of governance on the behaviors of two major cost types: programmatic spending, that external stakeholders generally desire organizations to spend on, and administrative spending, which is often viewed as undesired costs, riddled with agency problems.

Managers, having considerable discretion over resource allocation adjustments in response to changes in demand (Chen et al., 2019), likely predicate their spending decisions on the extent of their alignment with principals. Managers, who lack sufficient oversight from principals, have been found to engage in empire building and/or divert resources for perquisite consumption (Jensen & Meckling, 1976; Zimmerman, 1979). Such managers would be more reluctant to reduce administrative spending in times of revenue declines and would overspend in times of revenue growth (Chen et al., 2012). In the nonprofit sector, mitigation of such agency costs where “management puts its own interests ahead of those of the organization, such as fraud, self-dealing, failures to carry out the nonprofit’s mission” is a key challenge for many organizations (Molk & Sokol, 2021, p. 1503). Governance plays an important role in monitoring managers’ spending decisions and keeping frivolous cost behaviors in check. Prior research shows that strong governance, in fact, is able to mitigate nonprofit asset diversions or financial fraud (Harris et al., 2017), but little is known about how effective good governance is in cost containment, especially in times of revenue declines.

Specifically, we study how governance impacts organizational administrative and program spending in response to revenue declines in the nonprofit sector. We hypothesize that better governance is helpful in attenuating cost stickiness in nonprofit organizations, especially with regard to administrative spending. External pressure through societal norms has been found to promote cost cutting behavior (Hartlieb et al., 2020), which leads to less sticky costs. Moreover, Van Puyvelde et al. (2012) suggest that nonprofit organizations’ degree of alignment between managers and principals is borne out in their spending decisions, while Habib and Huang (2019) posit that nonprofit managers, as agents to a variety of external stakeholders, approach cost cutting decisions from the perspective of the societal impact. Thus, well-governed managers likely act in the best interests of principals, for example, funders and other external stakeholders, while poorly governed managers may focus on personal benefits and perquisite consumption as a result of their divergent preferences.

The nonprofit setting is especially well-suited for research related to governance and cost behaviors. Nonprofit organizations have a principal-agent relationship distinct from the for-profit sector. On one hand, they operate free from shareholder oversight allowing managers greater discretion over how the organization will respond to changes in revenues (Holzhacker et al., 2015b; Jones et al., 2013). On the other hand, they are subject to considerable institutional pressures from external funders, such as donors and grantors (Holzhacker et al., 2015a; Krishnan & Yetman, 2011). These de facto principals may withdraw their support resulting in further revenue declines (via loss of donations and/or government grants) if spending decisions are not aligned with the interests of these external parties (Kitching et al., 2012; Parsons et al., 2017). It is not clear a priori how nonprofit organizations adjust costs in times of declining revenues where future revenues likely depend on external funders’ approval. Thus, the role of governance becomes even more important in this unique principal-agent setting.

Second, studying cost behavior in the nonprofit sector allows us to gain insight into potential differences in asymmetric cost behavior across two distinct cost categories, programmatic and administrative spending. In the absence of a profit maximization motive, external funders’ preferences are one of the driving forces behind nonprofit cost behavior. These are often centered around nonprofits’ dedication to achieving the objectives of their organization (namely, the organization’s mission) and could lead to reluctance to decrease programmatic spending even in the face of revenue declines. Despite external stakeholder preferences for more mission or program spending, proper cost management requires organizations faced with revenue declines to reduce spending across both administrative and program functions. In fact, we posit that better governed organizations are better able to match cost reductions across both administrative and program spending categories attenuating the impact of cost stickiness. Finally, we are interested in nonprofit managers’ cost management decisions in the face of declines in program revenues, derived from organizational goods and services rendered, verses public support from donors and grantors. Here we hypothesize that while well-governed organizations experience less cost stickiness in response to declines in program revenues, the opposite will be true for declines in donations. That is, we conjecture that nonprofits with good governance will maintain program spending levels in response to declines in donations in an effort to appeal to donors by providing for programs that fulfill the organization’s mission.

To test these predictions, we employ data from 2014 to 2019 available from the Internal Revenue Service (IRS) electronic-file (e-file) data obtained from Amazon Web Services (AWS) for 419,350 nonprofit organization-years. 3 All data come from IRS Informational Tax Form 990 which must be prepared by all 501(c)3 charity organizations reporting more than $25,000 in gross receipts annually. 4 Using this large, industry-diverse data set, we find that good governance attenuates sticky cost behaviors across both administrative and program spending categories. Further examination of sources of revenue declines indicates that well-governed nonprofits are more reluctant to reduce program spending in response to declines in donor support. We interpret these results to mean that well-governed managers faced with reductions in public support will continue investing in programs aimed at fulfilling the organization’s mission, to align with external supporters’ preferences.

Our paper makes several important contributions. First, we extend sticky cost research in the nonprofit sector to a large-scale, industry-diverse sample of U.S. nonprofit organizations. Prior literature is limited to investigation of cost stickiness in nonprofit organizations in either specific sectors or geographical regions (Balakrishnan & Gruca, 2008; Habib & Huang, 2019; Holzhacker et al., 2015a). In particular, Balakrishnan and Gruca (2008) and Holzhacker et al. (2015a) study the hospital industry, which is characterized by a mix of nonprofit, government-owned and for-profit organizations. These results may not generalize to the nonprofit sector as a whole and are based on Canadian and German hospitals, respectively. Habib and Huang (2019) find evidence of cost stickiness in the New Zealand charity sector which is relatively smaller than the U.S. nonprofit sector and geared toward “other” industry nonprofits (“other” industry nonprofits include economic development, employment, fundraising, promotion of volunteering, and religious activities which make up 29% of their sample).

In our comprehensive study we find that asymmetric cost behavior exists in U.S. nonprofit organizations, but the degree of cost stickiness depends on the governance mechanisms in place. Second, we add to the cost management literature (e.g., Chen et al., 2012; Liu et al., 2019) by directly studying how agency cost theory applies to cost behavior in the unique nonprofit sector setting. Using governance as a proxy for the external monitoring and alignment of managerial and principals’ interests, we find evidence of distinctive cost dynamics, driven by the alignment to external stakeholders’ preferences. The significant moderating effect of governance on nonprofit cost behaviors underscores the importance of aligning management’s interests to the mission of the organization, in the absence of implicit control by external stakeholders. Finally, our findings also help understand the drivers of asymmetric cost behavior for different types of costs in nonprofit organizations. By juxtaposing administrative and program spending, we find that better governance leads to adjustments of these costs in opposite directions when facing declines in donor support. Our results are consistent with more opportunistic managerial behavior with respect to administrative spending in poorly governed organizations (as predicted by agency costs theory), and more stable program spending in well-monitored organizations.

The remainder of this paper is organized as follows. Background and Hypotheses section reviews related theories to motivate hypotheses. Research Design section describes the research design, including sample data, measurement of variables, and estimation models. Empirical Results and Discussion section presents and discusses empirical results, including tests of robustness. Concluding Remarks section summarizes and concludes.

Background and Hypotheses

The Urban Institute’s NCCS (National Center for Charitable Statistics, 2025) survey on nonprofit leaders’ top concerns finds that 81% of respondents reported revenue as their main concern. Uncertain revenue streams also make navigating organizational spending especially difficult. Even with considerably less pressure on maximizing profitability than for-profit firms, nonprofit organizations must carefully manage their costs (Eldenburg & Krishnan, 2008; Kallapur & Eldenburg, 2005; Weidenbaum, 2009). In particular, excessive administrative spending has attracted scrutiny in the nonprofit sector. 5 These situations showcase agency problems and the need for keeping management and general expenses in check. Therefore, understanding cost behavior mechanisms in this sector of the economy is not only an important research question, but one with practical implications which impact public and community welfare as well.

To explain how costs behave in response to adversity (revenue declines) we summarize theories of asymmetric cost behaviors that have been empirically tested in the literature. Agency theory (Jensen & Meckling, 1976) proposes that managers’ interests are not perfectly aligned with those of other stakeholders, so that when managerial monitoring is not feasible, managers act in a manner which is at least partially inconsistent with stakeholder interests. Applying this theory to cost behaviors in the for-profit sector, firms with a greater degree of agency costs are assumed to engage in opportunistic behavior over-spending on administrative expenses and reluctant to reducing administrative spending in times of revenue declines (Chen et al., 2012). As a result, for-profit managers react asymmetrically to changes in total revenues, opportunistically retaining excess resource consumption in the form of administrative expenses, leading to a smaller proportionate decrease in these costs during total revenue declines than during total revenue increases. On the other hand, the sticky costs phenomenon could also be explained by the adjustment costs theory (Anderson et al., 2003). The subsequent literature on asymmetric cost behaviors (e.g., Banker & Byzalov, 2014; Chen et al., 2019) find that, when managers perceive a reduction in demand to be temporary, they are likely to avoid adjustment costs. These costs could be significant and relate to both current activity decline (disposal and layoff costs) and subsequent ramping up costs (hiring and acquisition) in the event of rebounding demand (Banker et al., 2013; Golden et al., 2020). In sum, extant literature identifies both rational, in an economic sense, adjustment-costs-driven, and problematic, agency costs-driven, explanations behind cost asymmetry in selling, general and administrative costs at for-profit enterprises.

In our study we aim to integrate existing theories and identify driving forces behind cost behaviors in the nonprofit sector. We focus on the nonprofit sector, because its unique institutional features play a role in management’s spending decisions and the resulting cost asymmetry. From the adjustment-costs point of view, nonprofit managers are motivated to maintain current administrative expense levels in a sector where decreases in employee morale and specialized work forces make employee layoffs particularly difficult. In addition, disposing of historic or donated property is more complex and even impossible for some nonprofit organizations compared to the disposition of operational fixed assets in for-profit firms (Cooper & Haltiwanger, 2006). Furthermore, excessively cutting overhead costs is argued to be detrimental to nonprofit organizations in the long-term (Arya & Mittendorf, 2015; Pallotta, 2008; Tinkelman, 2009). In sum, it may be prudent for nonprofit organizations to behave in a manner consistent with adjustment costs theory, that is, exhibiting sticky costs to a certain extent.

On the other hand, nonprofit organizations are subject to considerable institutional pressures. These pressures would dictate that spending and operational decisions conform to the expectations of external stakeholders and regulators (Balakrishnan et al., 2010). While institutional norms for nonprofits would generally aim at cutting costs (Eldenburg & Krishnan, 2008), external stakeholders, such as donors, grantors, regulators, and communities at large, are expected to distinguish between different expense types. They are likely to prefer the continuation of programmatic spending while disapproving of high administrative spending, especially in times of revenue declines. Furthermore, economic considerations, such as achieving target profitability via active cost management, are not likely to be as important for nonprofit organizations relative to their for-profit counterparts (see, for example, Holzhacker et al., 2015a). These features of the nonprofit sector suggest that nonprofit cost behaviors differ in important ways from their for-profit counterparts and that careful distinction should be drawn when considering which types of costs are to be adjusted—the core mission expenditures or the supporting costs (e.g., Balakrishnan & Gruca, 2008).

Surprisingly, despite a plethora of research studies related to asymmetrical cost behavior in the for-profit sector, there is limited research in other sectors of the economy. Prior studies find that cost stickiness exists in governmental organizations and government-owned public enterprises across the globe (Bradbury & Scott, 2018; Cohen et al., 2017; Nagasawa, 2018; Prabowo et al., 2018). In the nonprofit sector, most prior research focuses on the hospital industry, likely due to data availability and a mixed composition of the nonprofit, for-profit and governmental hospital organizations allowing for easy comparison across ownership structures. For example, Balakrishnan and Gruca (2008) show that operating costs are sticky in nonprofit Canadian hospitals over the 1986–1989 sample period and find that the degree of cost stickiness is greater for mission-related operating expenses, such as direct patient care, than for support services. These findings confirm differences in decision making for essential mission-related program expenses and nonessential administrative and support costs. Further, Holzhacker et al. (2015a) study German hospitals between 1993 and 2008 and find evidence of cost stickiness across all types of ownership; however, nonprofit hospitals are not as sensitive to regulatory changes in fixed pricing which negatively impacted revenues, as for-profit hospitals. This result suggests that nonprofit organizations are not as concerned with profitability decreases and are committed to providing community services even when revenues decline. Altogether, while research on cost asymmetry in the hospital industry is insightful, generalizability of these findings to the nonprofit sector as a whole is unknown. Citing accountability rationale, Habib and Huang (2019) is the only multi-industry study to date that finds evidence of cost stickiness in the New Zealand charity sector over the sample period of 2007–2014, with greater degree of cost stickiness for administrative costs than for service (program) expenditures. Habib and Huang (2019) interpret their findings as necessary actions by managers to maintain the trust and confidence of internal and external stakeholders, but do not test the role of alignment of these stakeholders’ preferences directly.

To reconcile the evidence and better understand cost behaviors in the nonprofit sector, we propose that external monitoring plays a key role in cost adjustment decisions in times of declining revenues. Institutional theory predicts that managerial cost adjustment decisions could be indirectly affected by societal norms (Hartlieb et al., 2020). Resource dependence theory suggests a more direct monitoring channel, such as supporters’ contributions, which constitute a major revenue source for many nonprofits (Froelich, 1999). In the latter case, external contributors’ approval is likely to result in higher future revenue, while their disapproval could lead to further reductions in revenue (Kitching et al., 2012; Parsons et al., 2017). That is, not sufficiently reducing spending, especially management and general expenses, might place organizations under scrutiny from donors and oversight agencies. Even in the for-profit sector, greater oversight and shareholder pressure leads to greater administrative cost cuts in U.S. and U.K. firms when revenues decline (Calleja et al., 2006). We employ governance as a proxy measure for external monitoring (Boland & Harris, 2023). Nonprofit boards play a stewardship role in the management of organizational resources and often serve as a link between external and internal stakeholders (Kugel & Mercado, 2024). We predict that the role of governance as a tool for aligning managerial and external stakeholder preferences becomes even more important in periods of declining revenues.

Building on prior research which has documented the presence of sticky cost asymmetries in the nonprofit sector, we posit that the degree of cost stickiness will be moderated by the governance structure of the organization. Specifically, we conjecture that in times of declining revenues, better governed nonprofits will reduce spending across both administrative and program spending categories mitigating sticky cost asymmetries prevalent in nonprofit organizations. This culminates in our first study hypothesis:

In periods of declining total revenues, organizations with better governance have less sticky costs. Next, we extend our analyses to examine the sources of revenue changes. Nonprofit organizations rely on three revenue sources: program service revenues, contributions (which include donations and grants), and other revenue (mostly investment income). A decrease in program service revenues indicates a shrinking of the organization’s core business. This type of activity decline may trigger sell-off of assets or personnel downsizing as the organization will likely experience underutilized capacities in production or service-related activities. We expect that well-governed organizations will attenuate the degree of cost stickiness for both administrative and program spending in the face of declining program revenues. We base this conjecture on the premise that this revenue stream is reliant on the operations of the business in providing a service or selling a product, which the nonprofit manager has control over. External contributions represent direct donor contributions, government grants, as well as indirect donor contributions, including those funneled through third party agencies such as the United Way. Organizations receiving this revenue type are those most subject to public scrutiny in competition for outside contributions and community support, and therefore most vulnerable to continued declines in external contributions, should administrative expenses not be controlled, or if program-related spending is reduced. That is, donors, grantors, oversight agencies, and the public at large prefer organizations that constrain administrative spending while continuing to spend on organizational objectives (Kitching et al., 2012; Parsons et al., 2017). Thus, in times of declining donations, we expect well-governed nonprofits to reduce administrative costs, however, maintain program spending, preferred by donors. We refrain from making predictions regarding other revenues, as they are not directly related to either administrative or program spending. This leads to our second set of hypotheses:

In periods of declining program revenues, organizations with better governance attenuate administrative and program cost stickiness.

In periods of declining contributions, organizations with better governance attenuate (exacerbate) administrative (program) cost stickiness.

Research Design

Sample Data

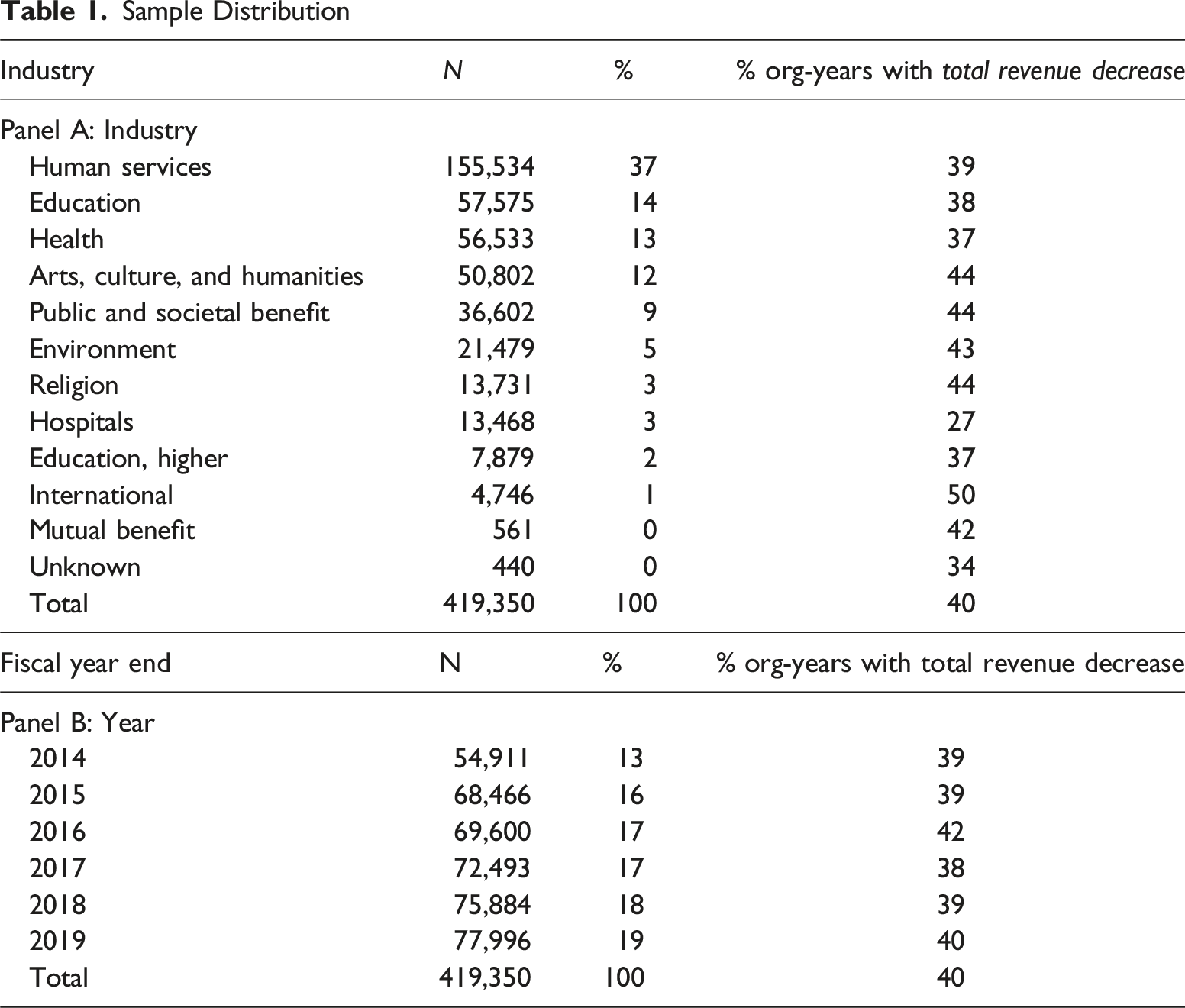

The sample is derived from the IRS e-file database and includes all public charities available for the period 2014–2019. The IRS e-file database includes all nonprofit organizations that have electronically filed their Informational Tax Form 990 with the IRS, made available through the Amazon Web Services data warehouse. Our initial sample consists of 1,296,053 organization-year observations.

From all accessible organizations, those agencies who report management and general expenses or program service expenses equal to zero (429,737) are removed from the sample as no meaningful comparison of costs can be made for such organizations. Further, those organizations that report total revenues equal to zero (106,924) are also excluded from the final sample for lack of meaningful interpretation. Our final screen is for organizations without two consecutive years of financial information required to calculate our change variables, leaving 419,350 nonprofit organization-year observations for our main analysis. See Appendix B for a tabular representation of our sample selection.

Sample Distribution

Measurement of Variables

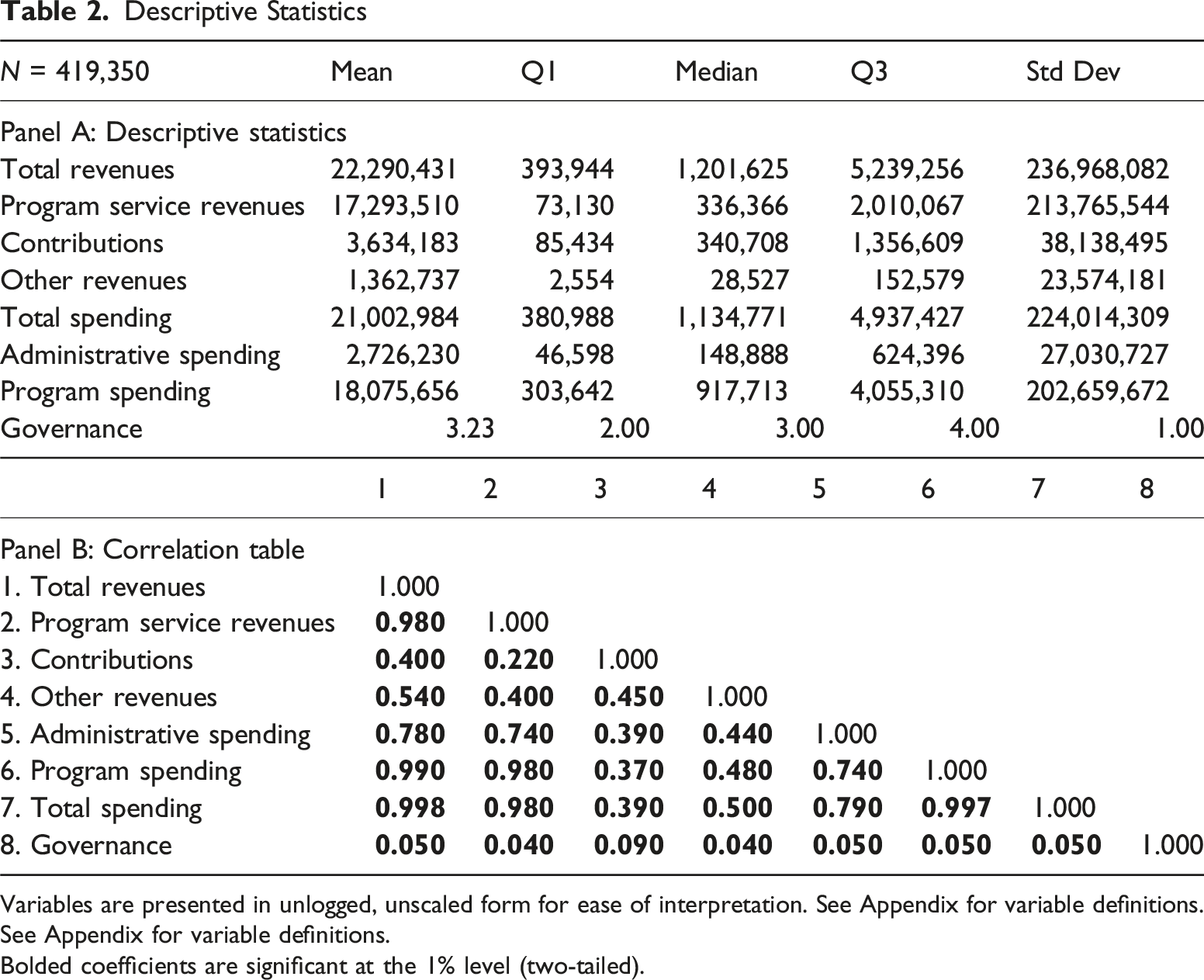

To measure changing levels of available resources, we initially focus on total revenues, followed by more detailed analysis of its components in nonprofit organizations: program service revenues, contributions, and other revenues. 6 Program Service Revenues are defined by the IRS as “…primarily those that form the basis of an organization’s exemption from tax.” These are the revenues earned from the agency’s primary business or purpose. While program service revenues provide a practical proxy for changes in nonprofit activity levels, it does face some limitations. Since nonprofit organizations are less price sensitive than for-profit firms (Lakdawalla & Philipson, 2006), a decline in program service revenues may capture a decline in product or service price rather than a deterioration of product or service demand. Contributions are defined as the total indirect and direct donations, as well as government grants received from the public. Other Revenues include all other sources of income not captured in our program service and contributions resource measures.

Administrative Spending (management and general expenses) as well as Program Spending (program service expenses) are both reported on the Statement of Functional Expenses in Part IX of the IRS Form 990. 7 Following Anderson et al. (2003) we calculate the natural log of the ratio of expenses in the current period deflated by expenses in the prior period, which is equivalent to calculating a change in these expenses, as the dependent variables in our analyses. To measure governance in our sample we follow Boland et al. (2020) who capture nonprofit governance using a simple index of five governance mechanisms reported in Section VI of Form 990. Boland et al. (2020) note that this index of five measures “perform(s) as well as, and in some cases better than, more complex indices.” Specifically, Governance is the sum the following five governance indicator variables coded one for organizations reporting: majority independent directors, audit committee, CEO salary setting process, no outsourcing of management duties, and providing financial information on the organization’s own website.

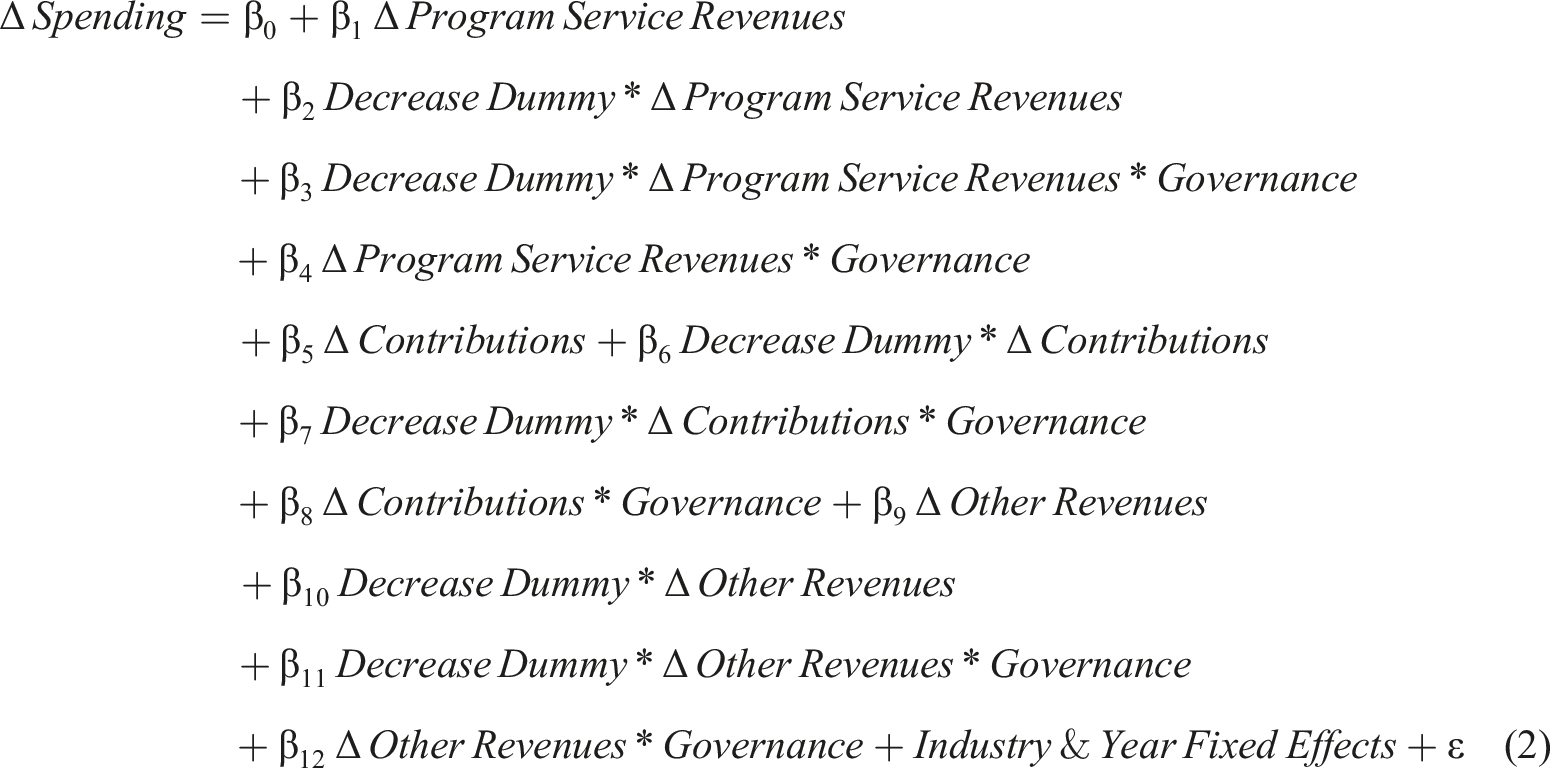

Estimation Models

To evaluate our hypotheses which predict the moderating effect of governance on nonprofit managers’ cost behaviors following declines in revenue, we add Governance, to the model developed by Anderson et al. (2003). Specifically, we estimate the following robust regression model:

The slope β1 provides an estimate of the percentage change in spending associated with a one percentage change in total revenues, coefficient β2 measures the extent of cost stickiness, and coefficient β3 captures the moderating effect of governance, on cost behavior. Based on hypothesis H1, coefficient β2 is predicted to be negative, while coefficient β3 is expected to be positive. Similar to Banker et al. (2013) and Chang et al. (2022), we interact changes in total revenues with our variable of interest, Governance, to account for the effect of governance on costs when revenue increases, captured by coefficient β4. 9

Next, we expand model (1) by decomposing total revenues into program service revenues, contributions, and other revenues:

Empirical Results and Discussion

Descriptive Statistics

Descriptive Statistics

Variables are presented in unlogged, unscaled form for ease of interpretation. See Appendix for variable definitions.

See Appendix for variable definitions.

Bolded coefficients are significant at the 1% level (two-tailed).

Regression Results

As discussed above, all study models are tested using robust regression techniques (iteratively reweighted least squares), identified by Leone et al. (2019) as the most effective method for mitigating the effects of extreme observations. Specifically, robust regressions assign a weight to each observation with higher weights given to observations which meet the assumptions underlying standard multiple regression. That is, robust regressions efficiently adjust for data outliers identified as a potential problem when working with IRS Form 990 data, from which we draw our sample (Tinkelman & Neely, 2011).

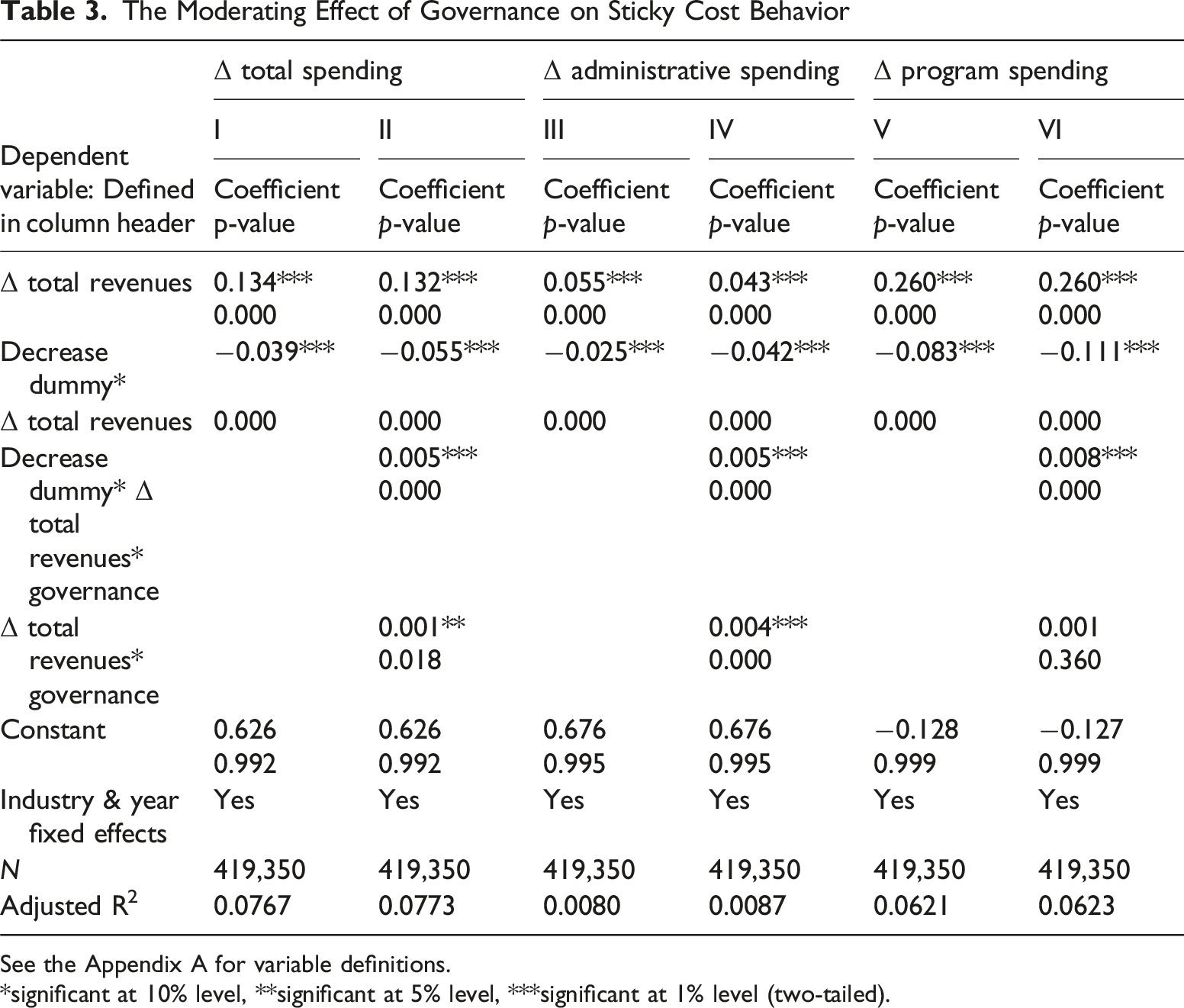

The Moderating Effect of Governance on Sticky Cost Behavior

See the Appendix A for variable definitions.

*significant at 10% level, **significant at 5% level, ***significant at 1% level (two-tailed).

Turning now to our models which include the moderating effect of governance, results reported in column II indicate that while we continue to document sticky cost behaviors in Total Spending (negative, significant coefficient on Decrease Dummy * Δ Total Revenues), we do find that better governance modestly attenuates these sticky costs (positive, significant coefficient on the three-way interaction term: Decrease Dummy * Δ Total Revenues * Governance). While this is consistent with our first hypothesis that better governed organizations exhibit a larger proportionate decrease in spending in response to revenue declines, we are careful to point out that the effect is somewhat small. Specifically, we note that the coefficient on our total spending measure (Decrease Dummy * Δ Total Revenues) indicates a stickiness effect of −0.055, while our governance moderating effect coefficient (Decrease Dummy * Δ Total Revenues * Governance) comes in at 0.005. We find the same is true in our column IV and VI results which indicate that both administrative as well as program spending exhibit a larger proportionate decrease, albeit not large in magnitude, at well-governed organizations during times of declining revenues.

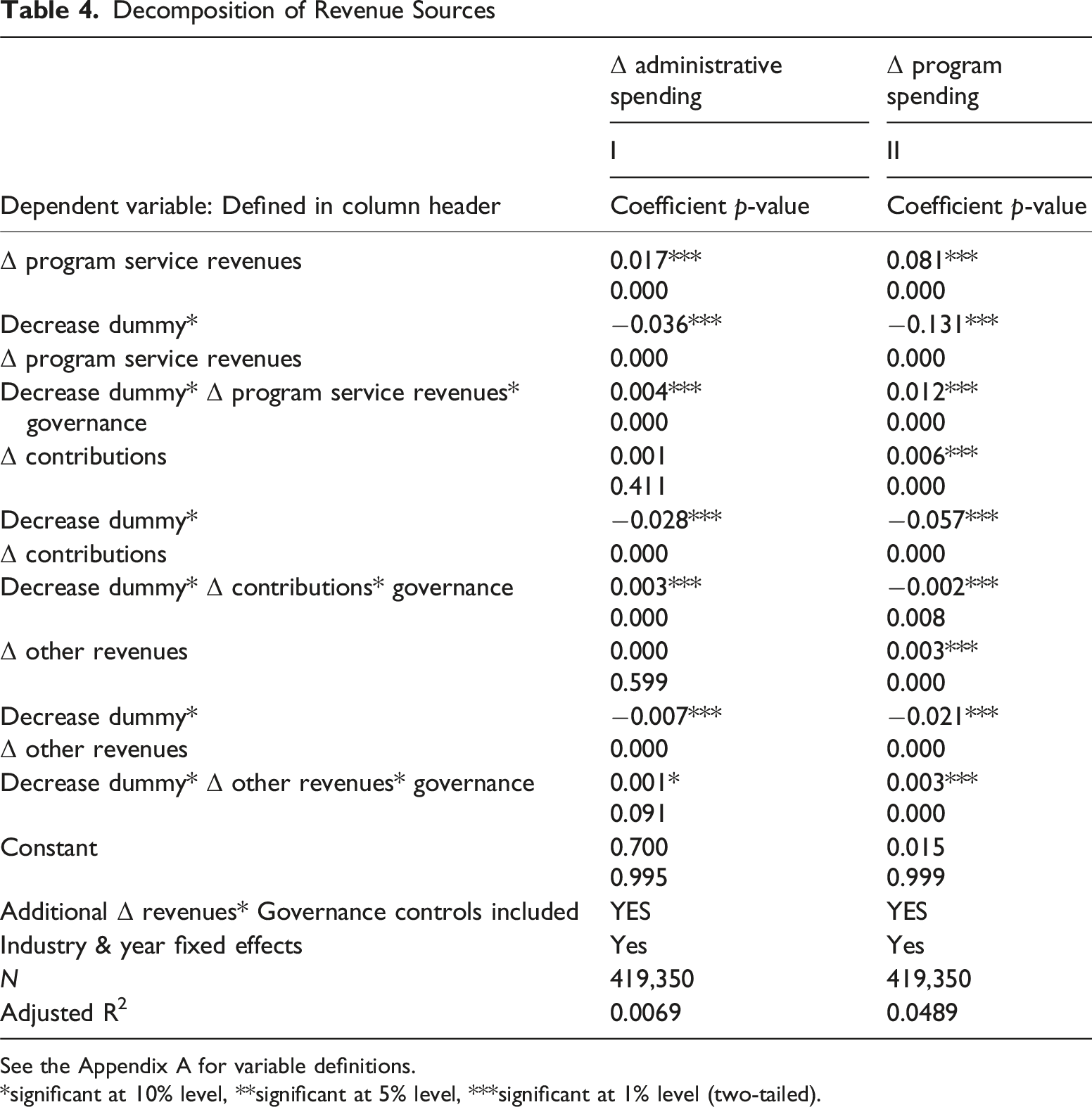

Decomposition of Revenue Sources

See the Appendix A for variable definitions.

*significant at 10% level, **significant at 5% level, ***significant at 1% level (two-tailed).

Moving to our tests of declines in Contributions, we find that while well-governed organizations are able to attenuate cost asymmetries in administrative spending in response to declines in donations, this is not the case for program spending. That is, we find that well-governed nonprofits with declines in contributions exhibit a smaller proportionate decrease in program spending (as indicated by the negative significant coefficient on the three-way interaction term), consistent with the second part of hypothesis 2 and the notion that organizations want to maintain mission spending preferred by donors, likely in an effort to rebound declining contributions.

Finally, we find results for declines in Other Revenues to be similar to our Program Service Revenues results. That is, good governance once again attenuates cost asymmetries in administrative and program spending in response to declining other revenue types.

Additional Analyses and Robustness Checks

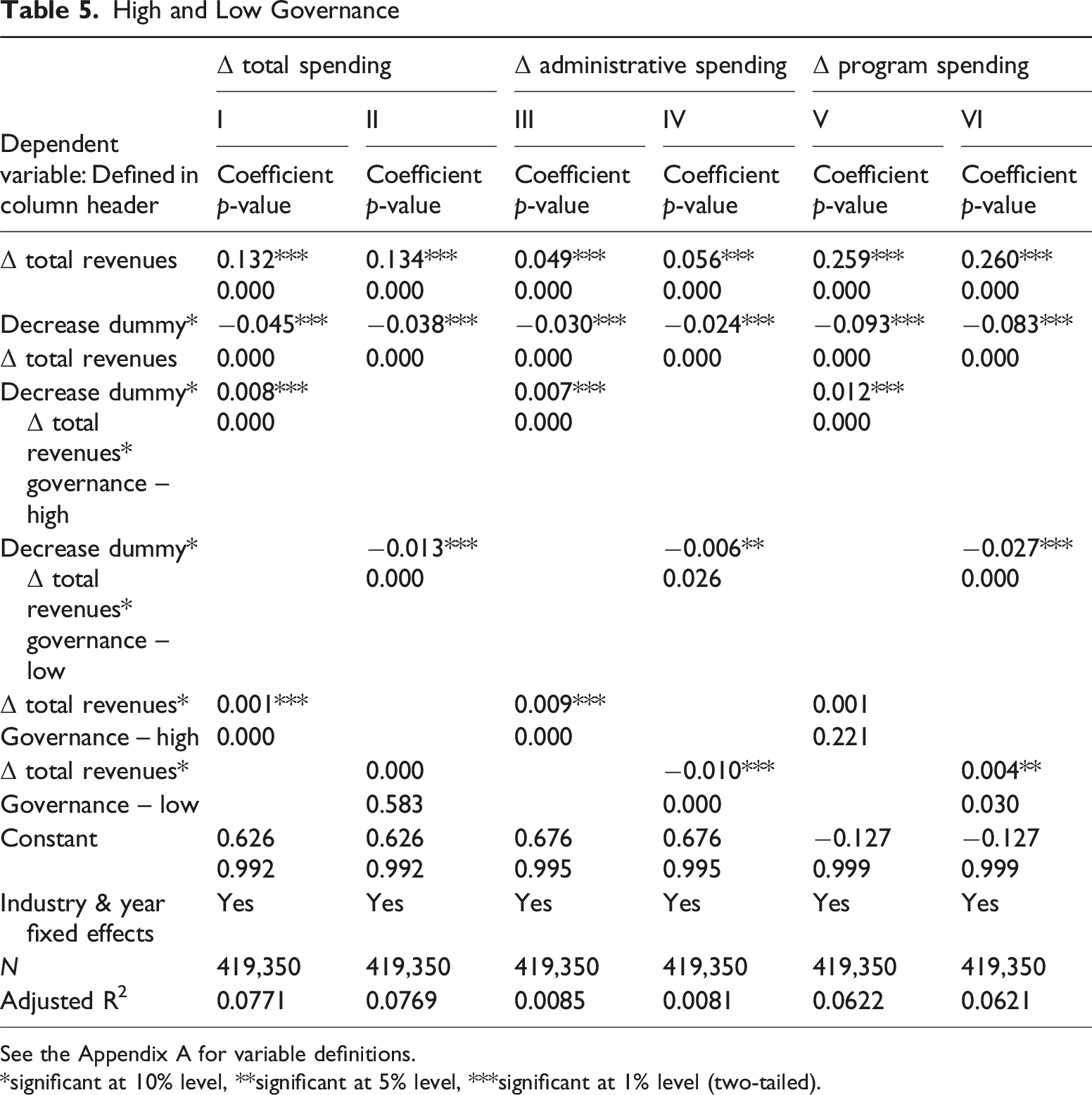

High and Low Governance

See the Appendix A for variable definitions.

*significant at 10% level, **significant at 5% level, ***significant at 1% level (two-tailed).

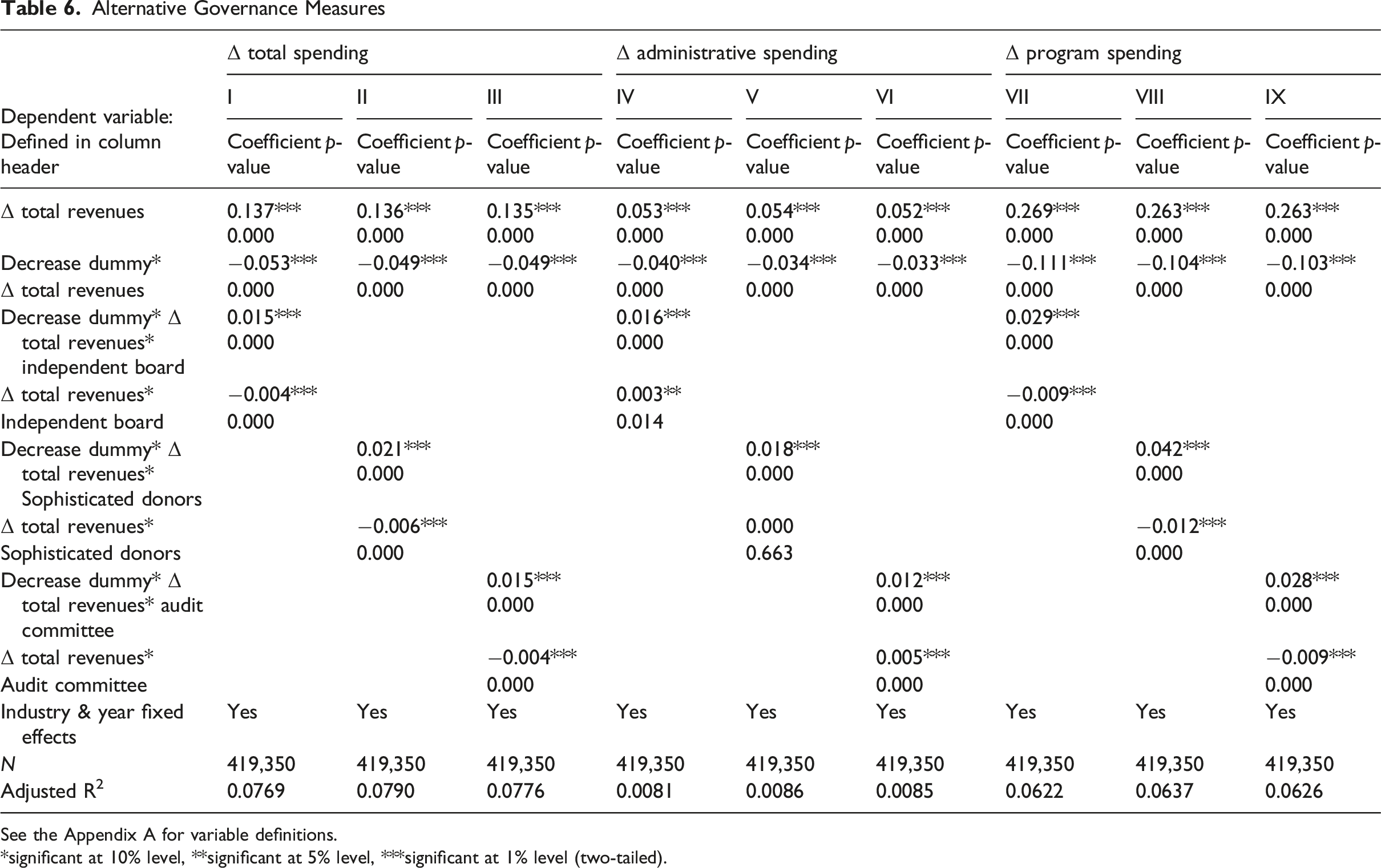

Alternative Governance Measures

See the Appendix A for variable definitions.

*significant at 10% level, **significant at 5% level, ***significant at 1% level (two-tailed).

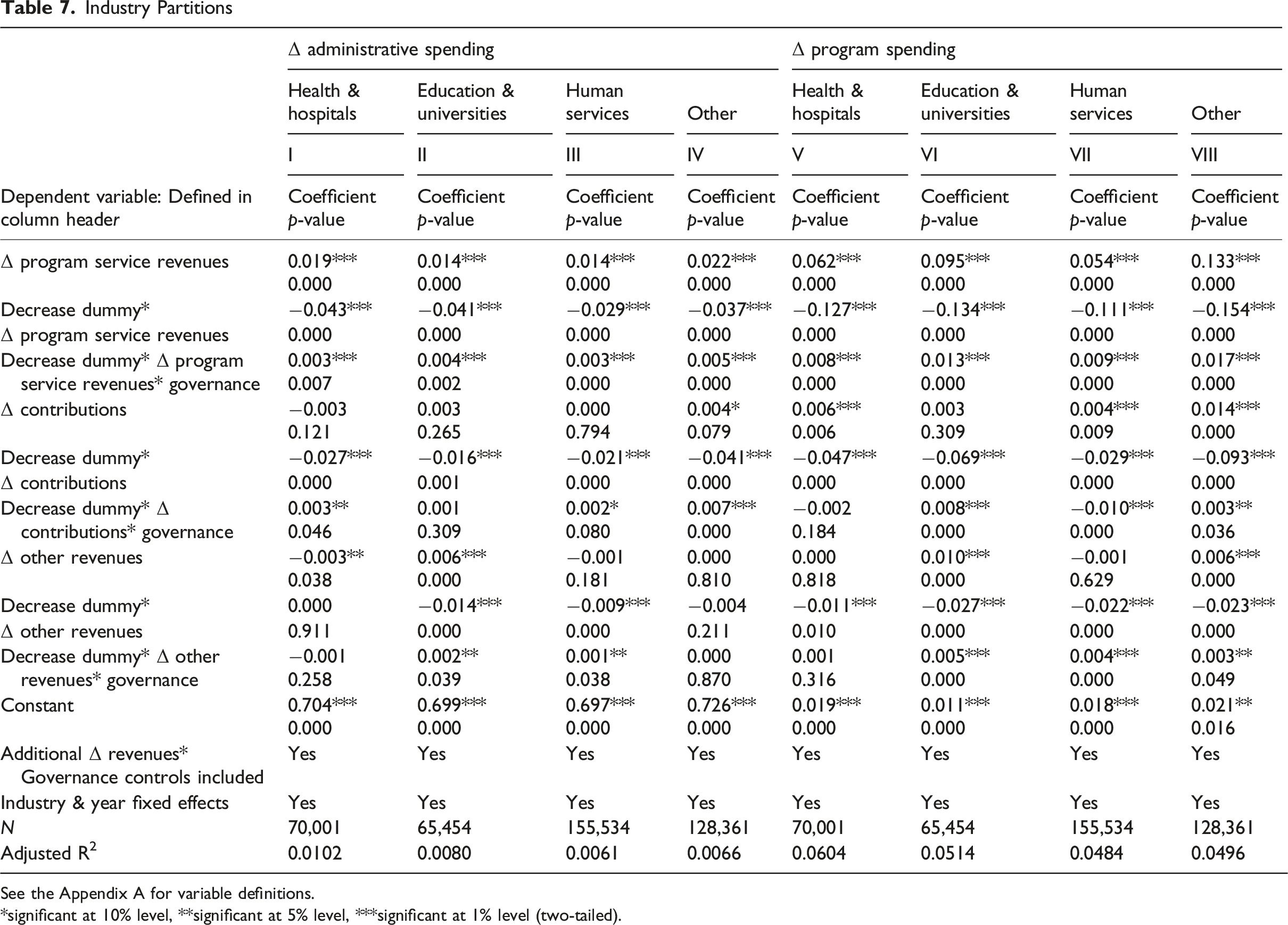

Industry Partitions

See the Appendix A for variable definitions.

*significant at 10% level, **significant at 5% level, ***significant at 1% level (two-tailed).

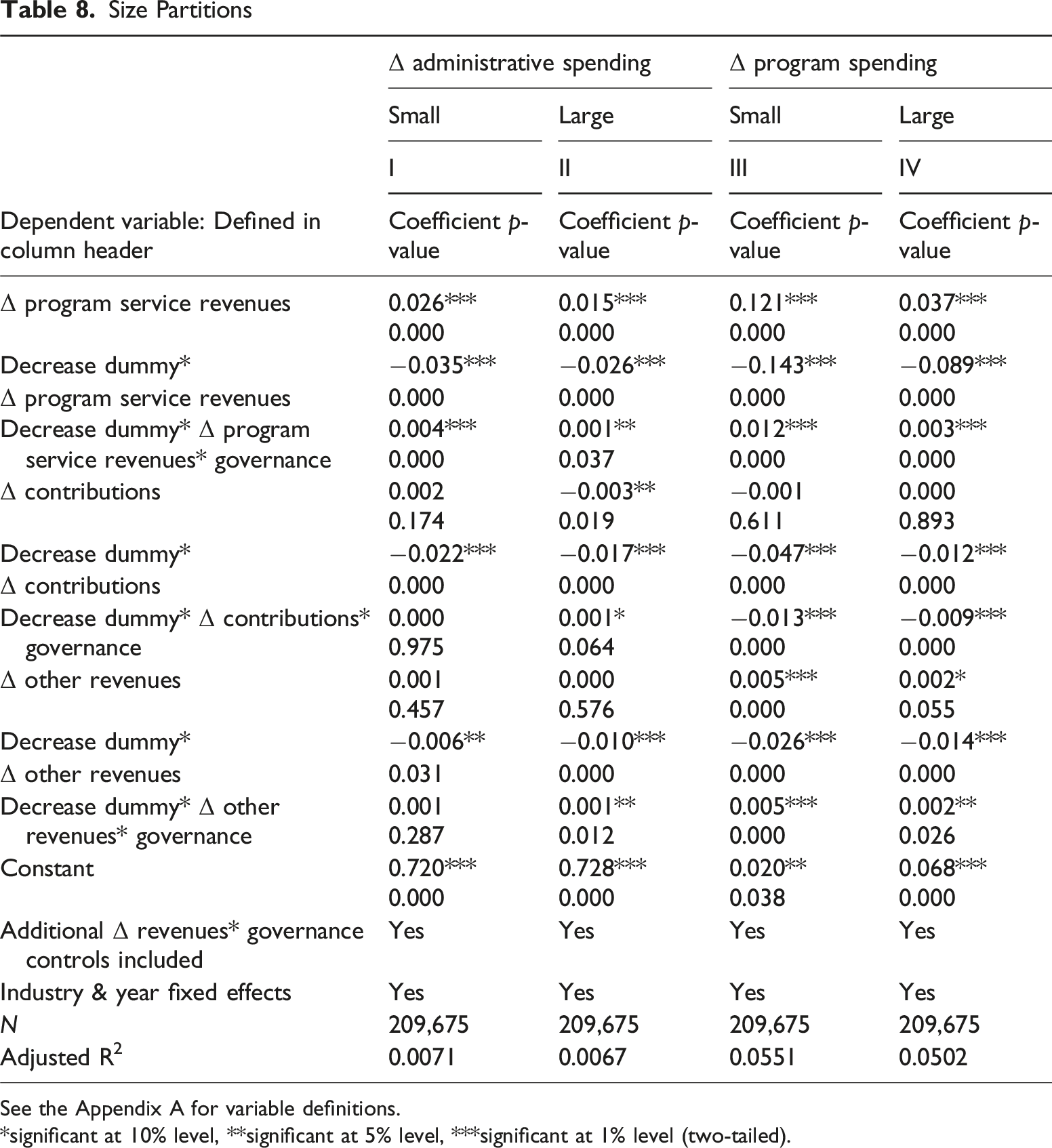

Size Partitions

See the Appendix A for variable definitions.

*significant at 10% level, **significant at 5% level, ***significant at 1% level (two-tailed).

In untabulated results, we analyze another expense category—fundraising expenses, commonly occurring in organizations relying on external funding. Due to expense classification shifting, a number of nonprofits report smaller or nonexistent fundraising expenses (see, for example, Krishnan et al., 2006). To address whether this affects our results, we first do a robustness check replicating our main analyses excluding organization-years reporting zero fundraising expense, where we find robust results. Next, we analyze fundraising expenses separately by employing changes in fundraising expenses as a dependent variable in models (1) and (2). In this untabulated analysis we find results consistent with our administrative spending behavior, that is, governance attenuates cost stickiness in fundraising expenses.

Next, we test the robustness of our models to various additional control variables for resources available to organizations which could play a role in cost behaviors during revenue downturns (Calabrese, 2018). First, we incorporate two measures common to the nonprofit sector which may impact managers’ spending: total assets and cash. We find robust results throughout all models when we include lagged, logged total assets as well as lagged, logged cash plus savings and temporary investments. Alternatively, Jones et al. (2013) employs two proxies for the resources available to the organization: net assets and savings (measured as a prior period’s surplus of revenues over expenses). Our results also hold when we control for these variables, however, for brevity they remain untabulated. 13

Finally, we confirm the robustness of all models to including firm fixed effects. If cost stickiness is driven by correlated omitted variables, firm fixed effects aid in mitigating these effects. Using this alternative model specification, we find results consistent with our main tabulated results and the significant effect of governance on cost stickiness. We find comfort in the robustness of our results to these additional variable and model specifications.

Alternative Explanation: Adjustment Costs Hypothesis

The asymmetric response to revenue changes is not necessarily an undesired by-product of underlying agency problems, as it might be optimal for an organization to not drastically reduce costs in response to revenue declines due to significant adjustment costs (Anderson et al., 2003; Banker & Byzalov, 2014). In the latter case, managers who are concerned with long-term value creation and acting in the interests of principals are not likely to act myopically when it comes to short-term spending adjustments (Banker et al., 2011). Following Anderson et al. (2003), we include prior period revenues change, asset concentration, and labor intensity as variables associated with adjustment costs. Our results persist after including these three variables in our models.

Concluding Remarks

In this paper, we examine the association between governance and cost behaviors in the nonprofit sector. Overall, our evidence documents that governance plays a key role in nonprofit managers’ cost decision making. Our results indicate that better governed nonprofit organizations reduce expenses at a greater rate than weaker-governed agencies during times of decreased revenues. This finding indicates that, consistent with agency theory predictions, governance mechanisms help reduce the effect of managers’ self-serving motivations related to management and general consumption, which may otherwise outweigh the preferences of external funders. Further, in our examination of the alternative sources of revenue declines in nonprofits, we find that well-governed nonprofits reduce both administrative and program spending in response to declines in program revenues, but are more reluctant to reduce program spending in response to declines in donor support. We interpret these results to mean that well-governed managers faced with reductions in public support will continue investing in programs aimed at fulfilling the organization’s mission, to align with external supporters’ preferences.

All told, the integration of the agency, cost allocation and sticky cost theories provides an interesting investigation into the nonprofit sector and organizations’ behaviors related to administrative expenses and program-related spending in an environment particularly sensitive to declines in revenues. The significant moderating effect of funder preferences proxied by organizational governance provides additional insights into our understanding of cost behaviors in the nonprofit sector. Additionally, the robustness of these results to various sources of revenue, industries, and sizes provides further generalizability of our findings in this diverse sector. Finally, we believe these are captivating results given the relatively little research conducted in this sector related to cost behaviors, particularly the role of organizational characteristics, such as governance, play in administrative and program cost decisions.

Footnotes

Acknowledgements

Authors would like to thank Associate Editor Stan Markov, anonymous referee, Rajiv Banker, Sudipta Basu, and participants of the 47th EAA Annual Congress, 2023 AAA MAS Section Mid-Year Meeting, and 2022 AAA Annual Meeting for useful comments and feedback.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.