Abstract

We use a sample of 248 tax strategies published by U.K. companies listed on the Financial Times Stock Exchange (FTSE) 100 and FTSE 250 to examine (a) how companies present themselves—more as “responsible taxpayers” who view taxes as a meaningful contribution to society, or more as “tax planners” who view taxes primarily as a cost, and (b) whether these presentations correspond to actual tax avoidance behavior. Our results show that, on average, firms tend to portray themselves as “responsible taxpayers,” but that this portrayal is consistent with firms’ tax avoidance behavior only when firms are subject to above-average external monitoring by financial analysts. The results suggest that firms manage the content of qualitative tax disclosures to sway public opinion as long as the probability of detecting misstatements is sufficiently low. This raises doubts as to whether mandatory qualitative information provides added value for stakeholders if it is not under external review.

Introduction

In 2016, the U.K. government passed a law that requires companies (exceeding specific size thresholds) to publicly disclose their tax strategy (UK Parliament, 2016). The U.K. government is thus reacting to the increasing global demand for tax transparency, which has caused several legislators to implement regulations to drive public tax disclosure (Müller et al., 2020). In addition to the U.K. law change, a variety of other recent regulations also address the disclosure of firms’ tax strategies. The Australian Tax Transparency Code (TTC)—although voluntary—demands large business to provide information on their approach to tax strategy for financial years ending after May 3, 2016 (Australian Taxation Office, 2021). Furthermore, the Global Reporting Initiative (GRI, 2019)—a framework for sustainability reporting—incorporates information on tax strategies in the framework for reports as of January 1, 2021. The growing interest in firms’ tax strategies raises the question of the costs and benefits of mandatory qualitative disclosure. To this end, we examine what information firms disclose about their strategy and whether the information is useful to stakeholders, that is, whether the information disclosed reflects firms’ actual tax policies.

We investigate the content of tax strategy disclosures published by U.K. firms listed on the Financial Times Stock Exchange (FTSE) 100 and FTSE 250 indexes. Finance Act (FA) 2016, Schedule 19, requires tax strategy disclosures that inform stakeholders about (a) risk management and governance structures, (b) the firm’s attitude toward tax planning, (c) the level of risk the firm is prepared to accept for U.K. taxation, and (4) the firm’s approach to its dealings with the U.K. revenue agency (HM Revenue and Customs (HMRC), 2015b; UK Parliament, 2016). As these disclosures are qualitative, we apply a textual analysis. Because few domain-specific word lists exist in tax research, we generate a tax-specific word list that measures whether a firm presents itself as a “responsible taxpayer” who considers taxes a meaningful contribution to society or as a “tax planner” who considers taxes primarily as a cost factor. We generate a word-frequency measure, the tax strategy “tone,” which captures how firms position themselves.

We find that, on average, firms present themselves as “responsible taxpayers” (i.e., they use more words in their tax strategies that classify them as “responsible taxpayers” than as “tax planners”). Using cross-sectional regressions, we then estimate whether the tone of the strategy disclosures can be explained by actual tax policy behavior measured by the firms’ long-run Cash and GAAP ETRs. We find that the tone of strategy disclosures reflects firms’ actual tax policy only for firms with an above-average number of financial analysts following or firms in industries subject to governmental oversight. For other firms, tax strategy disclosures are not informative enough to differentiate between tax avoiders, aggressive tax planners, or nonplanners. These findings indicate that firms manage the content of published tax strategy disclosures as long as the probability of detecting misstatements is low. Moreover, over time, firms increase the length of tax strategy disclosures as well as the “tone” of their strategy, that is, they are increasingly portraying themselves as responsible taxpayers.

This study makes several contributions. First, we add to the evolving research stream examining the effects of qualitative tax disclosures. Prior research shows that qualitative disclosures can contain valuable information (e.g., Campbell et al., 2014, 2019; Hardeck et al., 2020; Inger et al., 2018). Whether tax strategy information also provides useful information is currently unclear. Xia (2020) finds that firms with lower effective tax rates use less boilerplate language in their initial tax strategy disclosures and provide more information. In contrast, Dunker and Willkomm (2022) as well as Belnap (2023) find that firms with lower effective tax rates provide poorer disclosures (less detailed and more similar) which the authors interpret to mean that tax avoiding firms exploit the discretion of qualitative disclosure rules to lower transparency levels. Finally, Bilicka et al. (2022) find that the length of tax strategies described in the annual reports of U.K. firms increased after the introduction of mandatory tax strategy disclosure, but that information quality (as measured by the volume of boilerplate language) decreased. None of the previous studies investigated how firms present themselves in their strategy disclosure and whether the presentation is related to actual tax avoidance behavior. However, this is important to understand if the tax strategies are informative at all. This study addresses this research gap. To this end, we develop a new keyword list to capture whether a firm presents itself as a “responsible taxpayer” or a “tax planner” and relate this measure to firms’ actual tax avoidance behavior.

Second, we contribute to research on the effect of information intermediaries on disclosure behavior. Belnap (2023) studies the effect of nongovernmental organizations and the media on the quality of disclosed tax strategy information. He finds that attention by nongovernmental organizations and the media increases the probability that firms comply with the U.K. rules and publish their tax strategy but that the disclosures are of low quality. We complement this research by examining the effect of financial analysts on the quality of tax strategy disclosures. In contrast to the results regarding the effect of media and nongovernmental organizations, our results suggest that attention from financial analysts improves the quality of tax strategy disclosure.

Third, our results contribute to the discussion among researchers on the benefits and costs of increased tax transparency. One potential benefit of disclosing tax strategies is that the qualitative information is easier for the public to process. For example, instead of studying several years of annual reports to determine whether a company is located in a tax haven, whether its tax rate is above or below the industry average, or whether there are uncertain tax benefits (UTBs), readers of tax strategy disclosures are directly informed about the firm’s tax planning approach. But this assumes that disclosed tax strategies are sufficiently informative to allow the public to distinguish between different forms of tax behavior (e.g., “responsible taxpayer” versus “tax planner”). Our results, however, confirm the conjecture of Oats and Tuck (2019). For many companies, there is no association at all between the actual tax avoidance policy pursued by the firm and the presentation in the disclosed tax strategy. Requiring disclosure of useless information is costly because addressees may not be able to review important other information due to limited resources (Freedman, 2018). Moreover, in such cases, the perceived transparency is detrimental because it potentially misleads the public and may even impair the ability of stakeholders to identify aggressive tax avoiders (e.g., Dierynck et al., 2022).

Our study has important implications for research, consumers, and investors and for public policymaking regarding tax disclosures. First, the observed tax misreporting behavior informs public policymakers about an important limitation of recent tax transparency initiatives (e.g., Australian Taxation Office, 2021; GRI, 2019). Firms are required to be more transparent in their public tax reporting to create public pressure on firms to reduce their tax planning to avoid potential reputational damage. In this vein, the aim of the U.K. tax strategy disclosure requirement was to create greater transparency about companies’ tax approaches among the U.K. revenue agency, shareholders and consumers, thus leading to a change in tax planning behavior and improving tax compliance (HMRC, 2015b). However, by managing the content of published tax information, firms can avoid public shaming, which could explain why recent studies find little support for the effectiveness of the U.K. disclosure requirements in curbing tax avoidance (Bilicka et al., 2022; Xia, 2020). 1 Overall, this calls into question the value of enforced qualitative tax information that is not subject to mandatory external audits, as it has no meaning for the majority of stakeholders. Second, our findings are of relevance for consumers and investors who are interested in buying products and stocks of firms that match their own ethical values by having a “good” tax policy. Our results show that these consumers and investors cannot rely on the content of published tax strategy disclosures except when the firm is subject to high external monitoring.

The remainder of this article is organized as follows: In the next section, we present institutional background information regarding the U.K. tax disclosure rules. In the section “Hypothesis Development,” we review the relevant literature and derive our hypotheses. In the “Research Methodology” section, we present the sample selection, estimation method, and variable measurement. The results are described in the “Empirical Results” section. The following section includes robustness checks, and the last section discusses the results and implications for future research.

The U.K. Disclosure Requirement

As part of the FA 2016, Schedule 19, the U.K. parliament passed an annual disclosure requirement for firms’ tax strategies to create greater transparency and improve large business tax compliance (HMRC, 2015a, 2015b; UK Parliament, 2016). The regulation applies to groups, subgroups, and companies that are domiciled in Great Britain and that generated either a total turnover of more than GBP 200 million or had an aggregated balance sheet of more than GBP 2 billion in the previous financial year. In addition, foreign companies and groups that are part of a multinational enterprise group, as defined by the Organisation for Economic Co-operation and Development (OECD), and that are or would be affected by the British country-by-country reporting obligation are obliged to publish their tax strategies. 2 For a firm to be subject to the requirement of country-by-country reporting, it must reach a global turnover of GBP 750 million. With regard to this turnover threshold, no specific threshold for British companies is set by the law, so minimal activity is sufficient to make British companies subject to the disclosure requirement.

The FA 2016 became law in September 2016 and has been in effect for each financial year starting after September 15, 2016. Strategy disclosure has to be available before the end of the current financial year and needs to be renewed at least after 15 months. It must be published on the internet and be accessible free of charge. By law, the published tax strategy disclosure must contain four mandatory components: (a) risk management and governance structures, (b) attitude toward tax planning, (c) the level of risk the company is prepared to accept for U.K. taxation, and (d) the approach of the company toward its dealings with HMRC. A detailed description of taxes paid, on the other hand, is not required, although the strategy disclosures can include, on a voluntary basis, other information related to taxation. In case of noncompliance with the law, that is, not providing a strategy disclosure, publishing an incomplete strategy disclosure, or publishing a strategy disclosure that is not free of charge, the government charges an initial penalty of GBP 7,500. If the company does not fulfill the requirements after 6 months, another fee of GBP 7,500 is charged. From this point on, each month, a GBP 7,500 fee becomes due until the correct strategy disclosure is published free of charge.

Hypothesis Development

There are different incentives for managers to either report information that accurately reflects the actual tax policy or to report information that is intended primarily to affect the firm’s public reputation. Firms usually face a trade-off between signaling to their shareholders high performance by their tax department, that is, the successful use of tax avoidance strategies, and the risk of being declared by the public as “aggressive tax avoiders” or of attracting the attention of the revenue agency. While shareholders may anticipate benefits (e.g., higher after-tax profits) from tax avoidance, evidence is rising that the general public perceives tax avoidance as negative (e.g., Christian Aid, 2017; Dyreng et al., 2016; Pagg, 2017). This could be attributed to the fact that the payment of the “fair” share of taxes has become increasingly an aspect of corporate social responsibility (CSR). Academic research supports not only the relation between tax payments and CSR (e.g., Hoi et al., 2013; Huang et al., 2017; Lanis & Richardson, 2015), but also the GRI (2019) has recently added tax information to their sustainability framework, suggesting that they consider tax payments an important contribution to society. A unique characteristic of tax disclosures is that they may contain additional information for the revenue agency. 3 Nevertheless, tax avoidance schemes already must be disclosed to the U.K. revenue agency (disclosure of tax avoidance schemes, “DOTAS”) (HMRC, 2014), and U.K. companies are subject to a risk assessment by the agency. Thus, in our opinion, the shareholders and the general public are the main addressees of the published tax strategy disclosures, and avoiding increased tax enforcement should thus not be a main motive to dilute information in published tax strategy disclosures. Nevertheless, there are other motives for diluting the tax information in published tax strategies.

Motives to Dilute Information in the Published Tax Strategy

First, providing stakeholders with information about the firm’s tax strategy is associated with proprietary costs (Dye, 1986; Prencipe, 2004; Verrecchia, 1983; Wagenhofer, 1990). Not only stakeholders but also competitors obtain access to firm information. Prior research shows that competitors respond to changes in a firm’s tax policy (Bird et al., 2018). Competitors can use the information on the firm’s strategy and mimic the behavior, which may lead to a loss in competitive advantage (Deng et al., 2021; Kubick et al., 2015). Since competitors are likely to be most interested in tax planning strategies, the level of tax avoidance is often used as a proxy for proprietary costs (Deng et al., 2021; Osswald, 2018; Robinson & Schmidt, 2013).

Second, tax disclosures can be used to manage a firm’s reputation. Although the evidence with respect to reputational costs of tax avoidance is mixed in the existing research (e.g., Austin & Wilson, 2017; Chen et al., 2019; Gallemore et al., 2014; Hanlon & Slemrod, 2009), Graham et al. (2014) find that 69% of corporate tax executives rate reputational concerns as an important factor explaining why a firm does not engage in a specific tax planning strategy. In line with this, Dyreng et al. (2016) find evidence that public pressure on U.K. firms has reduced tax avoidance. Thus, firms might have an incentive to present themselves as “responsible taxpayers” to avoid potential reputational costs. Support for this motive is also provided by the CSR literature. Hardeck et al. (2020) find evidence that firms from liberal market economies use socially responsible tax disclosure to green-wash their tax avoidance behavior. Similarly, Davis et al. (2016) show that CSR performance is negatively related to tax payments. The idea to present the firm as a “responsible taxpayer” to protect or build reputation corresponds to legitimacy theory. The fundamental idea is that there exists a social contract between the firm and society. The firm has no inherent right to exist if not conferred by society (Deegan, 2002; Magness, 2006). For this right to earn, the firm has to behave in a socially acceptable manner (O’Donovan, 2002). Society has to consider the company as legitimate. Through disclosures, the company can signal its legitimacy and influence society’s perception of its actions (Deegan, 2002; Hummel & Schlick, 2016; Magness, 2006; Watson et al., 2002). Thus, to be perceived as legitimate by the public, the firm could have an incentive to disclose a tax strategy disclosure that presents the firm as a responsible taxpayer that is not engaged in tax avoidance (even if this does not reflect the true facts). In line with this rationale, Dyreng et al. (2020) find that some firms strategically fail to disclose their subsidiaries when they are located in tax haven countries. Lanis and Richardson (2013) confirm legitimacy theory in the context of taxes. The authors find that tax aggressive firms disclose more CSR information in their annual reports than nonaggressive firms. Thus, firms with low ETRs have an incentive to dilute information to avoid reputational damage.

However, firms with high ETRs may also have a corresponding incentive, as they could face potential reputational damage from their shareholders if it becomes clear that they are not successfully using tax planning strategies. In line with this reasoning, Inger et al. (2018) find a positive (negative) association between tax avoidance and tax footnote readability for firms with tax avoidance below (above) the industry-year median.

Motives to Provide Reliable Information in the Published Tax Strategy

On the contrary, there are also motives to report information that relates to the actual tax policy. First, an incentive to provide valid information is to reduce information asymmetries to lower agency costs in line with agency theory or to signal above-average performance in line with signaling theory to differentiate oneself from other companies with lower quality (Prencipe, 2004). Hence, firms with high tax rates justify tax payments by pointing out that they are good corporate citizens and believe in paying the “fair share” of taxes, whereas firms with low tax rates justify their behavior by pointing out the importance of taking tax advantages. Blaufus et al. (2019) show that the stock market responds positively to news on legal tax planning (as long as firms’ tax risk is low). Thus, firms with high tax department performance (successful use of tax planning strategies) have an incentive to communicate this performance to their shareholders to differentiate themselves from firms with poorer performance and promote their reputation with their shareholders.

Second, another potential incentive to not present misleading information is the risk of litigation; the fear of legal actions due to inadequate or untimely disclosure can enhance voluntary disclosure (Healy & Palepu, 2001). In a tax context, a potential litigation risk might occur if a firm declares in its tax strategy disclosure that it does not pursue aggressive tax avoidance when it actually conducts high-risk tax planning.

As the aim of the U.K. tax strategy disclosure requirement was to create greater transparency about a firm’s approach to tax, firms should be urged to only disclose reliable information. However, the above discussion illustrates that there are motives for both to disclose information that reflects the actual tax policy or to disclose information that does not reflect the actual tax policy. The identification of such misleading reporting behavior is important because companies can avoid “public shaming,” and the goal of regulation—to curb tax avoidance—is not achieved. Moreover, the information that tax strategies are not reliable is important for customers and their purchase decisions. In line with the results of Dyreng et al. (2020) and Inger et al. (2018), who provide evidence of misleading tax disclosures, we assume that the incentives for tax misreporting predominate; thus, we state our first hypothesis as follows:

Moreover, the probability of detection is influenced by the degree of external monitoring. We assume that the degree of external monitoring is best captured by the number of analysts following the firm. Jensen and Meckling (1976) suggest that security analysts possess comparative advantages in monitoring activities. Dyck et al. (2010) also note that financial analysts have an important role in detecting fraud. Empirical support for this argument is provided by Mauler (2019), who finds that firms increase their level of tax transparency (qualitative and quantitative information) if they receive analysts’ tax coverage. Hence, analysts’ tax coverage can be interpreted as additional monitoring and scrutiny. Yu (2008) finds support that the number of analysts following lowers the level of earnings management. The author interprets this result as in line with the hypothesis that analysts act as external monitors. In line with these results, Bradley et al. (2017) find that the intensity of analyst coverage is negatively related to financial misreporting. Thus, we state our second hypothesis as follows:

Research Methodology

Data

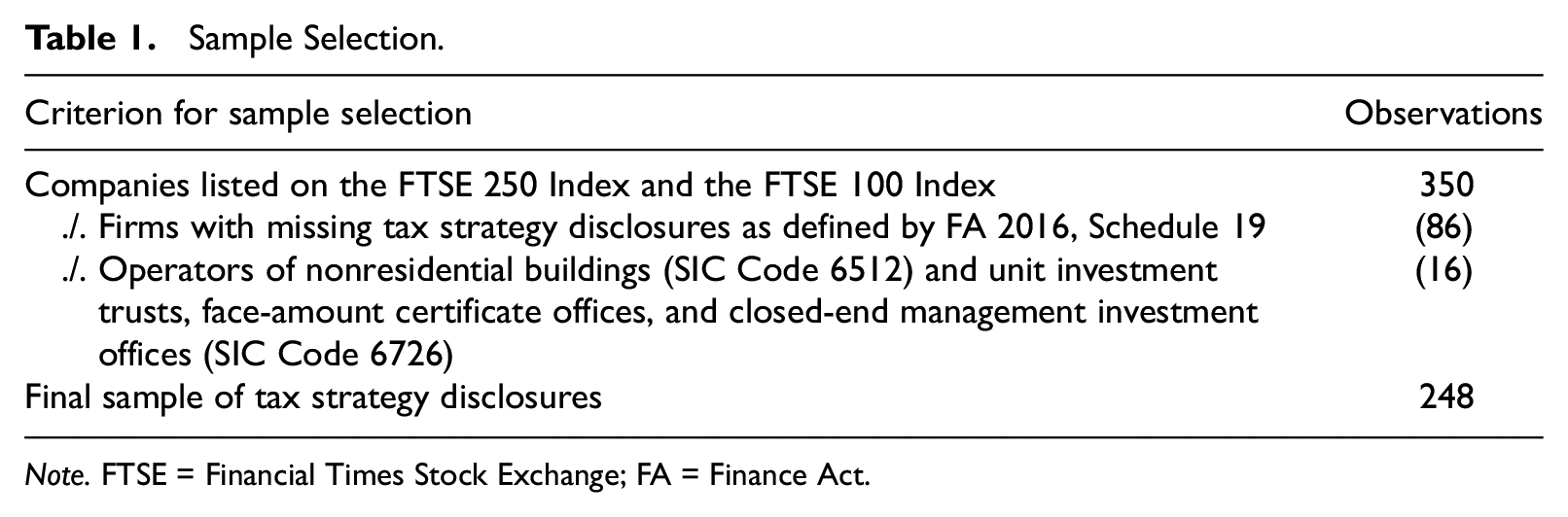

The following cross-sectional analysis is based on the tax strategy disclosures of companies listed on the FTSE 100 Index and the FTSE 250 Index (status as of April 16, 2019). The disclosures of the firms’ tax strategies were manually collected from the company’s websites between April and May 2019. Therefore, the most recently available strategy was used. In total, we gathered tax strategy disclosures from 264 of the initial 350 companies. For the remaining companies, there are either no published tax strategies at all (e.g., due to exemptions or due to the firm falling below the size criteria or being covered by a strategy disclosure at a higher level (UK Parliament, 2016) or no published strategies in the sense of the specifications of the FA 2016, Schedule 19. 4 Furthermore, we eliminate firms that are (a) operators of nonresidential buildings Standard Industrial Classification (SIC) Code 6512), because the status of real estate investment trust (REIT) leads to tax exemption of property rental business profits and gains or (b) unit investment trusts, face-amount certificate offices, and closed-end management investment offices (SIC Code 6726) because these companies are exempted from the obligation to publish a tax strategy disclosure. We end up with a final sample of 248 firms (97 from the FTSE 100 Index and 151 from the FTSE 250 Index).

Many strategy disclosures refer to an explicit fiscal year. For the strategy disclosures that refer only to a date, we assign the strategy disclosure to the fiscal year in which the date falls. Some strategy disclosures do not refer to any fiscal year/date at all or refer to a fiscal year prior to 2018, but since no new strategy disclosures were published until spring 2019, we assume that these strategy disclosures also apply to fiscal year 2018. We end up with 50 tax strategy disclosures that are allocated to fiscal year 2019 and 198 tax strategy disclosures that we assign to fiscal year 2018. Table 1 displays the sample selection process. Financial data are taken from Thomson Reuters.

Sample Selection.

Note. FTSE = Financial Times Stock Exchange; FA = Finance Act.

Variable Measurement and Estimation Strategy

Variables of Disclosed Tax Strategy

To measure the firm’s attitude toward tax, we apply textual analysis that allows us to convert the qualitative information into a numerical value: the disclosure tone (TONE). Owing to the increased possibilities in the field of computational linguistics, there is a growing stream of literature using textual analysis. Although general word lists exist (e.g., General Inquirer, Diction software), Elaine Henry and Leone (2016) show that domain-specific word lists better predict market reactions to earnings announcements than general word lists. General word lists have the risk of polysemy, that is, the risk that a single word has several meanings (Elaine Henry & Leone, 2016). In line with these findings, we develop our own tax-specific list of keywords to directly identify the firm’s attitude toward taxes. Following the research agency TNS BMRB (2015), we differentiate between two types of taxpayers: “responsible taxpayers” and “tax planners.”

Firms that present themselves as “responsible taxpayers” emphasize that they view taxes as a meaningful contribution to society and to the communities in which the companies operate. Taxes are seen as part of CSR (Lanis & Richardson, 2012). Moreover, they pursue open, constructive, and transparent relationships with tax authorities.

Firms that present themselves as a “tax planner,” on the contrary, emphasize that they view taxes primarily as a cost that should be optimized like any other business expense to achieve financial efficiency and to maximize shareholder value (e.g., by using tax incentive schemes). However, this differentiation does not divide firms into “good” and “bad” but refers to different tax policy approaches only.

Our keyword search methodology consists of multiple steps: (1) Based on domain expertise and prior research on word lists (Hardeck et al., 2020), we create an initial keyword list to identify responsible taxpayers and tax planners; (2) two of the authors checked the initial keyword list for false hits. Owing to the small sample size, all hits were checked. A success rate of 85% is required. (3) To ensure that our keyword list is complete, a random sample of 30 strategies is drawn, and new keywords are looked for in this sample (step 2 is repeated for the new keywords). (4) Finally, we checked the reliability of our keyword list by providing it to five PhD students (specialized in company taxation) who had to assign the keywords from our list to the categories. The Krippendorff

In contrast to prior tone measures (e.g., Elaine Henry & Leone, 2016), we do not distinguish between positive and negative words (thus not measuring the sentiment) but rather capture the firm’s attitude toward tax. The higher the value of TONE is, the greater the firm presents itself as a “responsible taxpayer.” If a company does not use any keywords, we code the tone as zero. This is the case for only one observation. As a final step, we control our codification by reading the 10 tax strategies with the lowest and the highest tone.

Variables of Tax Avoidance Behavior

To capture the firms’ tax avoidance behavior, we use the cash effective tax rate (CASH_ETR) and the GAAP effective tax rate (GAAP_ETR) 7 (Dyreng et al., 2008; Hanlon & Heitzman, 2010). The CASH ETR is defined as the cash taxes paid divided by the pretax book income. It is affected by tax deferral strategies. The GAAP ETR, on the contrary, is calculated by dividing the total income tax expenses by the pretax book income. The numerator includes the current and deferred tax expenses. Thus, the GAAP ETR does not reflect deferral strategies (Hanlon & Heitzman, 2010). We require positive values for the numerator as well as the denominator. Furthermore, we winsorize the tax rates to values between 0 and 1. Owing to the limitations of annual-based tax rates (year-to-year variation, undefined tax rate in case of negative pretax book income), we use the long-run ETRs (CASH_ETR3 and GAAP_ETR3) over a horizon of 3 years (Dyreng et al., 2008), which also allows us to measure current as well as past tax behavior. The long-run CASH ETR (GAAP ETR) is defined as the sum of the cash taxes paid (total income tax expenses) over a 3-year period (t to t− 2) divided by the sum of the pretax book income over the same 3-year period (Dyreng et al., 2008).

Regression Design and Control Variables

To test our first hypothesis, we examine whether the disclosure tone (TONE) is associated with the firm’s ETR. The following regression equation is estimated:

ETR3 is either CASH_ETR3 or GAAP_ETR3. CONTROLS is a vector of the following firm-specific control variables: LN_ANALYSTS, defined as the number of analysts following (proxied by the number of estimates for earnings per share); SIZE, defined as the natural logarithm of total assets reported; PTROA, defined as the pretax book income scaled by lagged total assets; INTANG, intangible assets scaled by lagged total assets; LEV, defined as long-term debt scaled to lagged total assets; FOREIGN_DUMMY, defined as a binary variable indicating whether the percentage of foreign sales in total sales exceeds 10%; HQ, defined as a binary variable indicating whether the headquarters of the ultimate parent is in the United Kingdom; and industry-fixed effects (based on SIC codes). 8

Using LN_ANALYSTS, we capture the extent of external monitoring (Bradley et al., 2017; Mauler, 2019; Yu, 2008). 9 With the firm-specific control variables, we capture size effects (SIZE), firm profitability (PTROA and LEV), firm operations (FOREIGN_DUMMY), and the tax-reporting environment (INTANG). The choice of control variables is based on prior research on disclosure behavior (e.g., Akamah et al., 2018; Campbell et al., 2014; Dyreng et al., 2020; Erin Henry et al., 2016; Higgins et al., 2015; Hope et al., 2013; Law & Mills, 2015; Li, 2010; Lisowsky et al., 2013). HQ controls for a potential homeland bias (TNS BMRB, 2015). 10

To test our second hypothesis, we repeat the regressions including an interaction effect of LOW_ANALYSTS and the tax policy variables. LOW_ANALYSTS is an indicator variable that takes the value of 1 for firms with a below-average number of analysts following and 0 otherwise.

Empirical Results

Descriptive Statistics

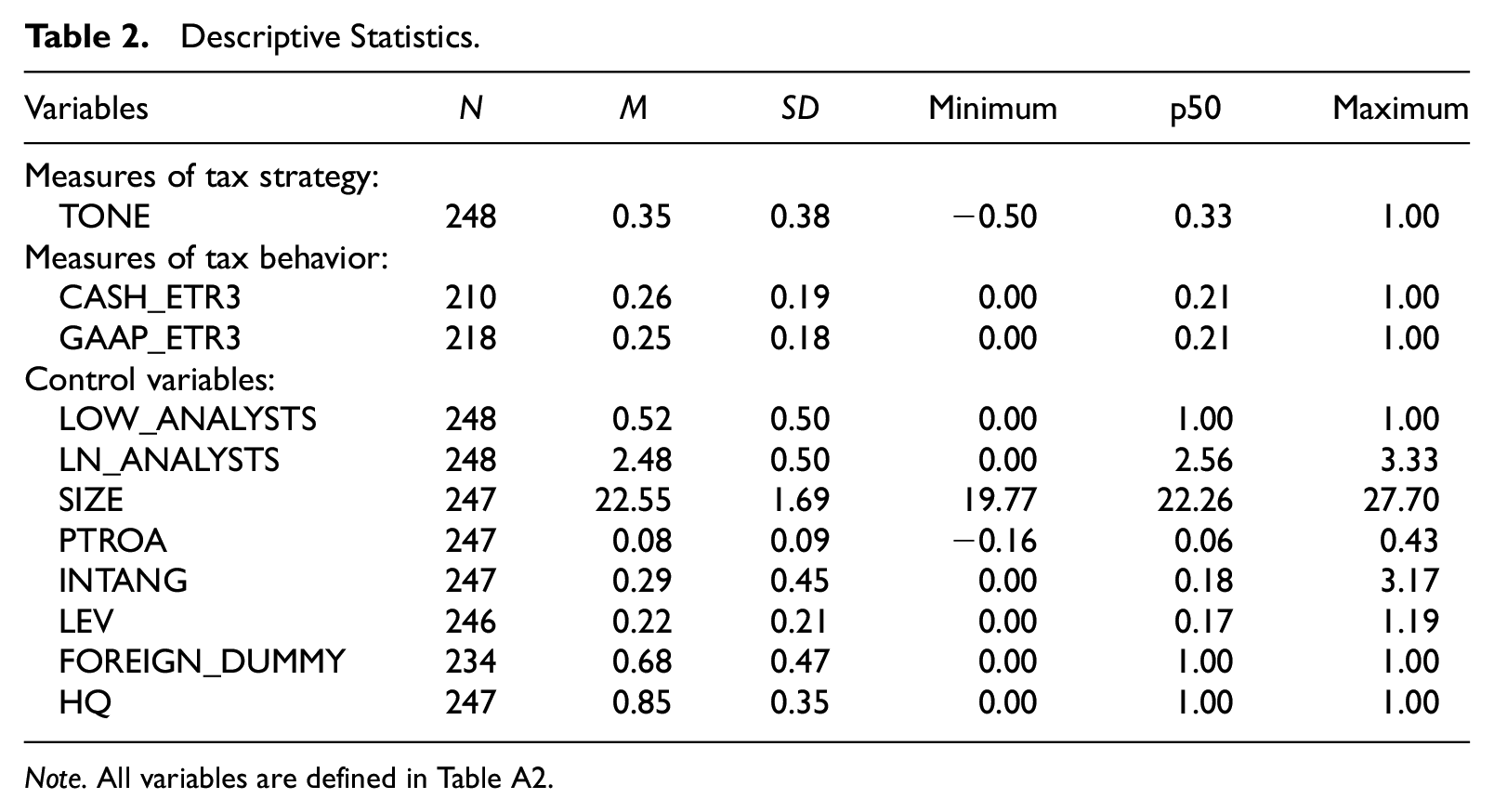

The descriptive statistics for our variables are presented in Table 2. By construction, TONE is bounded to [−1, 1]. In our sample, the mean of TONE amounts to 0.35. This means that, on average, the firms use more keywords in their tax strategies that classify them as “responsible taxpayers” than as “tax planners.” While the maximum of TONE equals 1 (27 companies), the minimum amounts to −0.5 (two companies).

Descriptive Statistics.

Note. All variables are defined in Table A2.

The companies that are assigned as fully “responsible taxpayers” (TONE = 1) present themselves using formulations such as the following: Tesco is a responsible taxpayer. We are one of the most significant contributors of tax in the UK and recognise the importance of the tax payments that we make in all of the communities we serve. [. . .] Where we are uncertain as to how tax law applies we look to discuss this with the relevant tax authority to achieve certainty for Tesco and the tax authority concerned.—Tesco PLC, Tax strategy for the accounting period ending 23 February 2019 The Group seeks to protect its reputation as a responsible corporate citizen by ensuring that it acts in accordance with the letter and the spirit of current tax legislation so that it pays the right amount of tax when it falls due.—Travis Perkins PLC, Tax strategy dated 3rd December 2018 Every day we change lives within the communities we operate in around the world. We believe that how we deal with our tax affairs is an important element of our approach to corporate social responsibility. We gladly accept that we pay taxes to the governments where we do business and where our people live and work.—PageGroup PLC, Tax strategy (no date) The Group is committed to acting with integrity and transparency on all tax matters, and complying fully with UK tax law. It does not pursue any aggressive tax planning schemes and pays its taxes as and when they become due.—Fresnillo PLC, Tax strategy for the for financial year ending 31 December 2018

In contrast to these firms, others clearly state that they make use of tax advantages or even state that they are rated as “not low risk” from the HMRC: We seek to maximise the benefits available from tax credits and other incentives offered by governments (eg R&D credits, intellectual property incentives, tax holidays etc).—Meggitt PLC, Tax strategy approved by the Board of Directors on 30 October 2018 DLG will make use of available tax incentives, reliefs and exemptions and will endeavour to structure its business / operations in a tax efficient manner. DLG will only enter into a transaction that is commercially driven and will not undertake any tax planning that is inconsistent with legislation.—Direct Line Insurance Group PLC, Tax strategy 2018 It will consider opportunities to structure its arrangements in a tax efficient manner, for example, the use of legitimate tax incentives. Such arrangements are carefully evaluated by the Group as it aims to comply with all relevant tax legislation.—Sports Direct International PLC, Tax strategy for the financial year ending on 29 April 2018 HMRC’s most recent rating for the Group is Not Low Risk.—Imperial Brands PLC, Tax strategy dated February 2019

These examples illustrate the differentiation between “responsible taxpayers” and “tax planners” and show that firms indicate the use of tax planning; however, they also emphasize that these strategies are in compliance with the law. It raises the question of whether U.K. tax strategy disclosures contain information that is in line with actual tax policy or whether firms misreport to manage their public reputation.

Regression Results

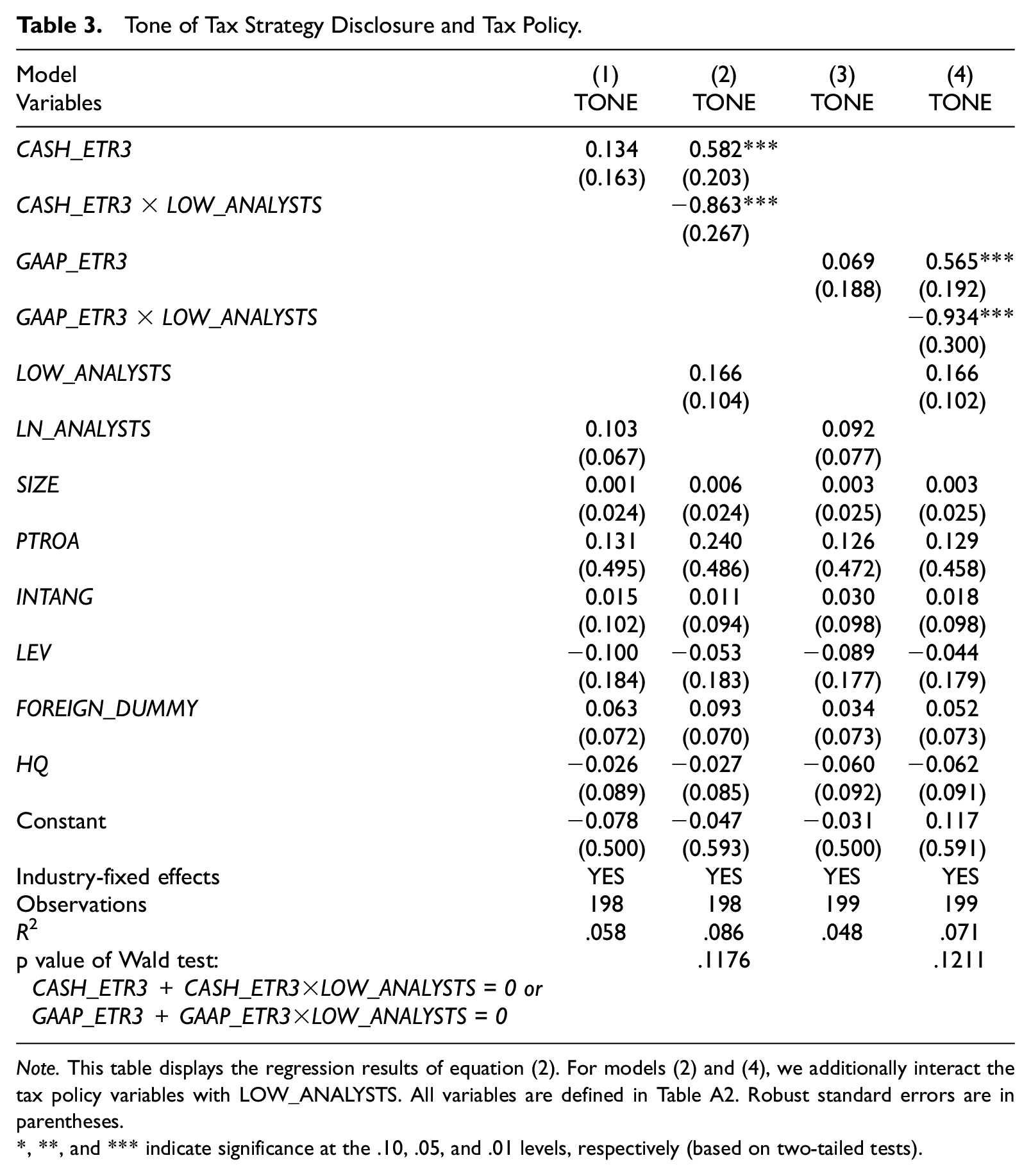

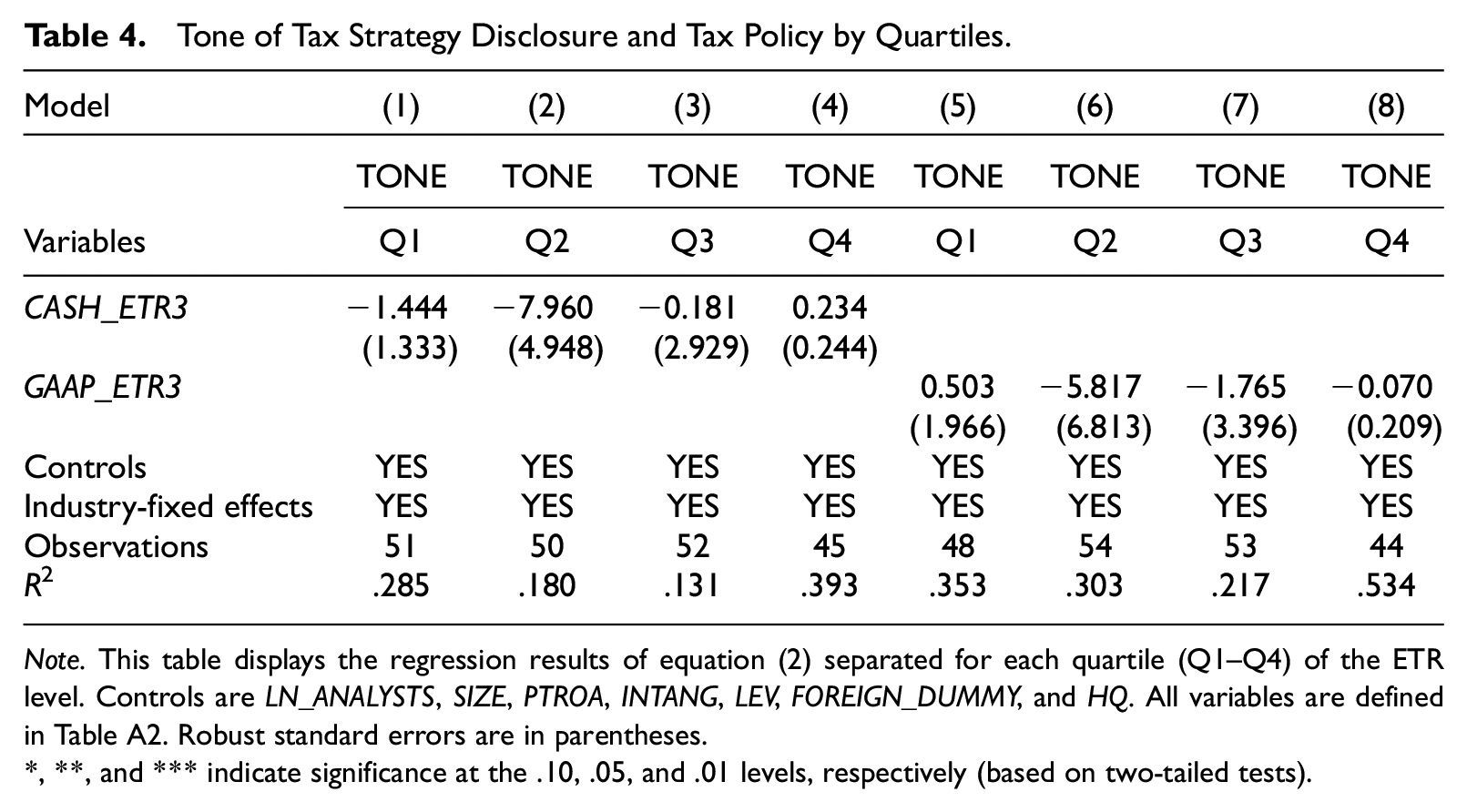

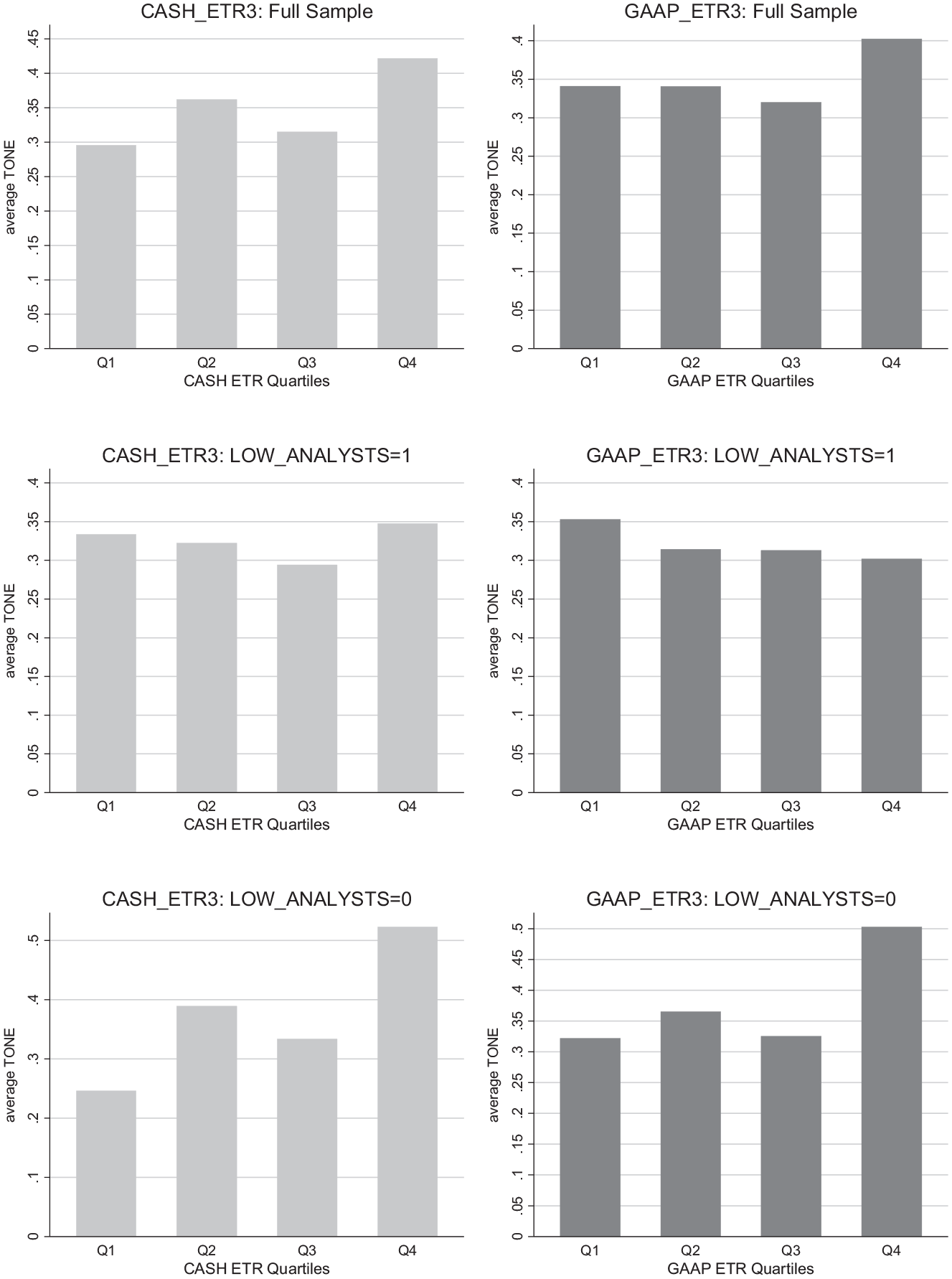

Table 3 reports the regression results of equation (2). 11 Overall, we do not find a significant association between the disclosure tone and the tax avoidance level (models (1) and (3) in Table 3). An increase in the long-run ETR (t to t− 2) does not significantly affect the tone. The results support H1. Tax strategy disclosures may not be informative enough to differentiate between tax avoiders, aggressive tax planners, and nonplanners. Dividing the ETR levels into quartiles, we do not find that our results change within these subsamples (see Table 4). This finding is supported by Figure 1, which plots the average disclosure tone by quartiles of ETRs. An (untabulated) regression reveals that, on average, the disclosure tone is not significantly larger in the fourth quartile than in the first quartile.

Tone of Tax Strategy Disclosure and Tax Policy.

Note. This table displays the regression results of equation (2). For models (2) and (4), we additionally interact the tax policy variables with LOW_ANALYSTS. All variables are defined in Table A2. Robust standard errors are in parentheses.

, **, and *** indicate significance at the .10, .05, and .01 levels, respectively (based on two-tailed tests).

Tone of Tax Strategy Disclosure and Tax Policy by Quartiles.

Note. This table displays the regression results of equation (2) separated for each quartile (Q1–Q4) of the ETR level. Controls are LN_ANALYSTS, SIZE, PTROA, INTANG, LEV, FOREIGN_DUMMY, and HQ. All variables are defined in Table A2. Robust standard errors are in parentheses.

, **, and *** indicate significance at the .10, .05, and .01 levels, respectively (based on two-tailed tests).

Average TONE by ETR Quartiles.

However, we find that if the number of analysts following a company is high, an increase in the long-run ETR is positively associated with a higher disclosure tone (models (2) and (4) in Table 3). In contrast, if the number of analysts following a company is low, the effect is insignificant. We interpret the results as evidence for misreporting if external monitoring is low. In this case, the opportunities to report misleading information and not being detected are lower. Firms facing high external monitoring, on the contrary, do not misreport with respect to the level of tax avoidance but inform in line with their actual tax policy. Hence, we find that the effect of the long-run ETR on the disclosure tone is significantly moderated by the degree of external monitoring. Figure 1 supports this finding. In sum, our results support H1 and H2.

Supplemental Analysis

In this section, we investigate whether firms’ strategy disclosure differs from year to year. We hand-collected 193 tax strategies for the year 2021. Again, we removed firms that are (a) operators of nonresidential buildings (SIC Code 6512) because the status of REIT leads to tax exemption of property rental business profits and gains or (b) unit investment trusts, face-amount certificate offices, and closed-end management investment offices (SIC Code 6726) because these companies are exempted from the obligation to publish a tax strategy disclosure. We end up with 179 firms where we examine the change of the tax strategy tone.

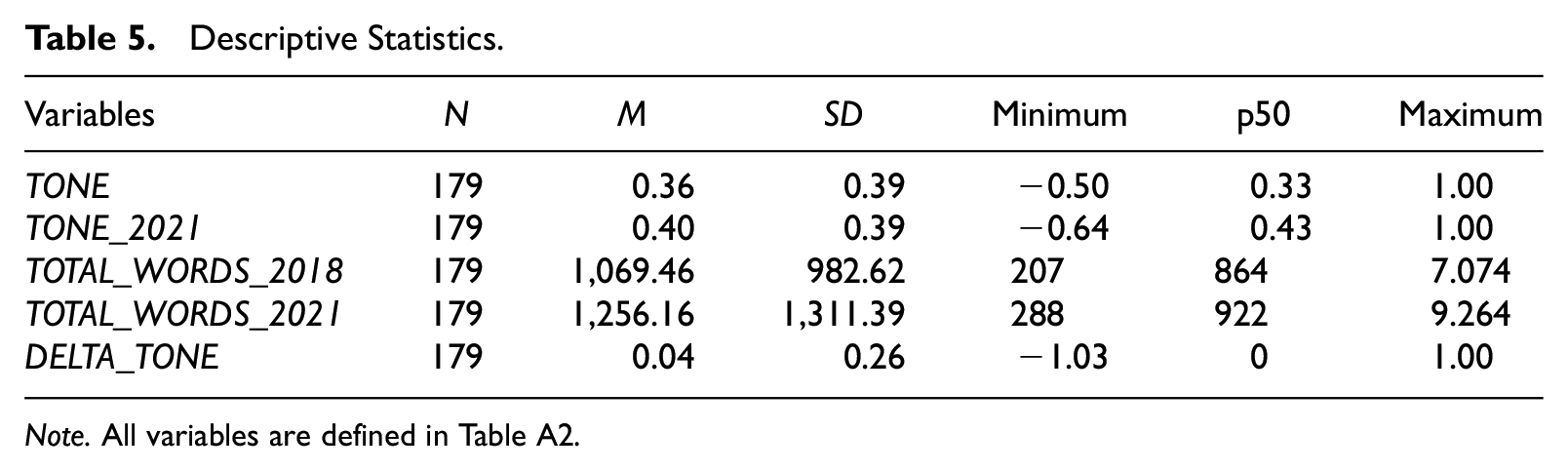

We find that 127 firms increased, and 51 firms lowered the total number of words in their tax strategy. On average, the firms raised the total number of words from 1,069 in 2018 by 17.49% to 1,256 in 2021. Regarding the tax strategy tone, we find that 70 firms increased and 43 decreased their relative representation as a responsible taxpayer. On average, the tone increased from 0.3578 by 10.87% to 0.3967. We generated two dummy variables for the change of the tone and the change of the total number of words, which are 1 if the change is positive and zero otherwise. Using t-tests we find that both the change in the tone and the total number of words are significantly different from zero. We show the descriptive statistics for the years 2018 and 2021 variables for these strategies as far as we have data for both years in Table 5:

Descriptive Statistics.

Note. All variables are defined in Table A2.

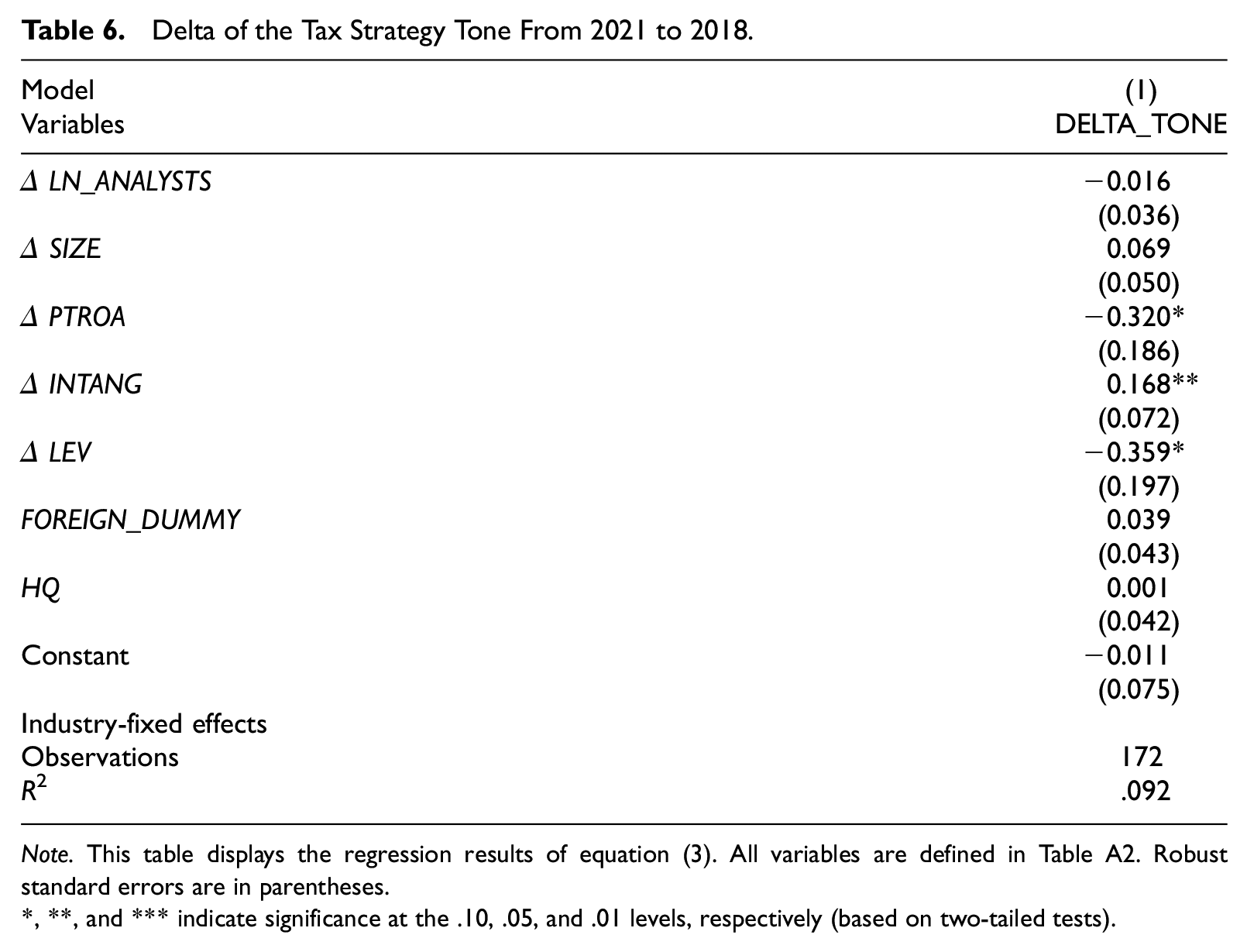

Furthermore, we estimate the following regression model to analyze the change of the tone: 12

where DELTA_TONEi is the change of our tax strategy tone from 2018 to 2021, Δ LN_ANALYSTS is defined as the change of the number of analysts following (estimated by the number of estimates for earnings per share) from 2018 to 2021; Δ SIZE, defined as the change of the natural logarithm of total assets reported from 2018 to 2021; Δ PTROA, defined as the change of the pretax book income scaled by lagged total assets from 2018 to 2021; Δ INTANG, the change of intangible assets scaled by lagged total assets from 2018 to 2021; Δ LEV, defined as the change of the long-term debt scaled by lagged total assets from 2018 to 2021. Furthermore, we included FOREIGN_DUMMY, defined as a binary variable indicating whether the percentage of foreign sales in total sales exceeds 10%; HQ, defined as a binary variable indicating whether the headquarters of the ultimate parent is in the United Kingdom and industry-fixed effects (based on SIC codes). 13

The results are displayed in Table 6. We find that for firms with an increasing profitability and with increasing long-term debt, the tone decreases. In contrast, firms with increasing intangible assets increase their tone.

Delta of the Tax Strategy Tone From 2021 to 2018.

Note. This table displays the regression results of equation (3). All variables are defined in Table A2. Robust standard errors are in parentheses.

, **, and *** indicate significance at the .10, .05, and .01 levels, respectively (based on two-tailed tests).

Robustness Checks

We perform several robustness checks to validate our results (see the Online Appendix). First, we use a different proxy for the degree of external monitoring to test H2. The banking and insurance industry is a highly regulated sector and subject to governmental oversight. Thus, we test whether misreporting behavior is moderated by the finance and insurance sector (SIC codes between 6000 and 6499). We find confirmative evidence. Firms in the finance and insurance sector disclose information that corresponds to their actual tax policy, as they face high external monitoring.

Second, to test the validity of LOW_ANALYSTS as a proxy for the degree of external monitoring, we compare the similarity of the tax strategy disclosures. 14 We find that the similarity is higher for firms with a low number of analysts following (two-sided t-test; p < .05). This result was confirmed by multivariate regression. We regress SIMILARITY on LOW_ANALYSTS, SIZE, PTROA, INTANG, LEV, FOREIGN_DUMMY, HQ, and industry-fixed effects. Thus, firms with a high number of analysts following use less “boilerplate” language than other firms.

Third, we control whether our results are influenced by the measurement of the disclosure tone. In the Online Appendix, we provide examples of firms that position themselves as both responsible taxpayer and tax planners at the same time. Instead of offsetting the number of keywords for “responsible taxpayers” and “tax planners,” we repeat the regression for the two categories separately. We use the number of keywords for “responsible taxpayers” or “tax planners” as two separate dependent variables. Overall, we find that tax avoidance behavior is associated neither with the keywords for “responsible taxpayers” nor with the keywords for “tax planners.” However, while the effect does not depend on the number of analysts following for the “responsible taxpayer” keywords, the interaction terms are significant if we regress only the keywords for “tax planners.” If the number of analysts following a company is high, the long-run ETR is negatively related to the number of “tax planner” keywords, that is, firms with a higher ETR use fewer “tax planner” keywords. This finding is in line with our main results and suggests that the results are driven by the keywords of “tax planner.”

Fourth, we change the calculation of the tax policy variables. Instead of considering only 3 years (t to t− 2), we expand the horizon of the long-run ETR to 5 years (t to t− 4). The results remain qualitatively unchanged.

Fifth, we examine the effect of outliers using robust regressions as recommended by Leone et al. (2019) and find qualitatively unchanged results for our main analyses.

Sixth, the measurement of the constructs “responsible taxpayer” and “tax planner” is designed so that the word list used is complete to ensure the validity of the measurement instrument. However, this has resulted in a different number of words for the two constructs. To test whether the different number of words affects our results, we eliminated randomly nine keywords regarding tax planning. 15 This left us with 22 keywords regarding a “responsible taxpayer” and 22 keywords for a “tax planner.” We find the results qualitatively unchanged and therefore conclude that they are not biased by the different number of words for the two categories.

Seventh, we repeat regression (2) only for the firms, where the ultimate parents headquarter is in the United Kingdom to address the risk, that our results are driven by non-U.K. firms, which might have different tax strategies for different countries, as for U.K.-headquartered firms, the obligation applies to the whole firm and not just the U.K. portion of its operation (Bilicka et al., 2022). 16 In this case, we again find that the tone reflects actual tax avoidance behavior only for firms with an above-average number of analysts following.

Conclusion

This study is the first to examine how companies portray themselves—more as “responsible taxpayers” who view taxes as a meaningful contribution to society, or more as “tax planners” who view taxes primarily as a cost—and whether these portrayals correspond to actual tax avoidance behavior. On the one hand, firms have an incentive to disclose successful tax planning activities to their shareholders; on the other hand, firms might fear the negative reputational costs of being accused by the public of not paying their fair share of taxes. Using textual analyses, we measure the tone of tax strategy disclosures from FTSE 100 and FTSE 250 firms. The tone indicates whether a firm presents itself more as a “tax planner” or as a “responsible taxpayer.”

Our findings provide evidence of significant misreporting in qualitative tax disclosures. The content of tax strategy disclosures reflects firms’ actual tax avoidance behavior only if firms are monitored by an above-average number of financial analysts or if they are subject to governmental oversight. Consequently, managers seem to dilute the information content of published tax strategy disclosures, and thus, stakeholders should not rely too much on these strategy disclosures when making investment or consumption decisions.

Moreover, the opportunity to manage the content of tax disclosures limits the ability of governments to reduce tax avoidance via public shaming. In light of the increasing number of tax transparency initiatives, policymakers should consider that these initiatives will be successful only when qualitative tax disclosures such as tax strategies are subject to external monitoring. Moreover, policymakers might consider including a requirement of additional quantitative information on actual tax behavior in tax strategy disclosures to decrease management’s discretion. Otherwise, tax transparency initiatives bear the risk that stakeholders’ perception of a firm’s tax policy is biased due to firms’ disclosure management. Without an effective monitoring mechanism, forced qualitative disclosures impose costs for firms and information receivers but do not provide useful information to the majority of stakeholders. However, whether it is worth in terms of costs and benefits to require a mandatory audit of qualitative tax disclosures is an open question.

When interpreting our results, one should, however, keep in mind some limitations. First, we study tax strategy disclosures published by U.K. firms. Prior research shows that attitudes toward taxes vary by culture (e.g., Kountouris & Remoundou, 2013). Thus, future research should study whether our results hold for different countries. Second, we measure firms’ actual tax policies using GAAP and CASH ETRs because other measures, such as UTBs, are not available for U.K. firms. Although ETRs are widely used measures in empirical tax research, these measures are subject to some biases (e.g., Drake et al., 2020). Future research could thus examine whether UTBs better explain the tone of tax strategy disclosures than the measures used in this study.

Supplemental Material

sj-docx-1-jaf-10.1177_0148558X231200913 – Supplemental material for Public Disclosure of Tax Strategies and Firm’s Actual Tax Policy

Supplemental material, sj-docx-1-jaf-10.1177_0148558X231200913 for Public Disclosure of Tax Strategies and Firm’s Actual Tax Policy by Kay Blaufus, Janine K. Jarzembski, Jakob Reineke and Ilko Trenn in Journal of Accounting, Auditing & Finance

Footnotes

Appendix

Variable Definitions

| Variable | Description |

|---|---|

| Measures of tax strategy: | |

| TONEi | (# Keywords ‘responsible taxpayer’ - # Keywords ‘tax planner’)/(# Keywords ‘responsible taxpayer’+ # Keywords ‘tax planner’) for the year 2018 |

| TONE_2021i | (# Keywords ‘responsible taxpayer’ - # Keywords ‘tax planner’)/(# Keywords ‘responsible taxpayer’+ # Keywords ‘tax planner’) for the year 2021 |

| TONE_ADJUSTEDi | (# Keywords ‘responsible taxpayer’ - # Keywords ‘tax planner’)/(# Keywords ‘responsible taxpayer’+ # Keywords ‘tax planner’), where the adjusted wordlist for ‘responsible taxpayer’ and ‘tax planner’ contain the same number of words |

| TOTAL_WORDS_2018i | Total number of words in the tax strategy 2018 |

| TOTAL_WORDS_2021i | Total number of words in the tax strategy 2021 |

| DELTA_TONEi | Difference between TONE_2021 and TONE |

| Measures of tax behavior: | |

| CASH_ETR3i | Sum of cash taxes paid (year t to t-2) divided by the sum of pretax book income (year t to t-2). The nominator and denominator have to be positive. Data from at least two periods are required and a value is only calculated if the annual CASH_ETR is also available for at least two periods. The variable is winsorized to values between 0 and 1. |

| GAAP_ETR3i | Sum of total income tax expenses (pretax book income minus after-tax book income) (year t to t-2) divided by the sum of pretax book income (year t to t-2). The nominator and denominator have to be positive. Data from at least two periods are required and a value is only calculated if the annual GAAP_ETR is also available for at least two periods. The variable is winsorized to values between 0 and 1. |

| Control variables: | |

| LOW_ANALYSTSi | 1, if the number of analysts (EPS1NE) is below the mean; 0 otherwise. We set missing values for the number of analysts to zero. |

| LN_ANALYSTSi | Natural logarithm of one plus the number of analysts (EPS1NE). We set missing values to zero. |

| SIZEi | Natural logarithm of total assets reported |

| PTROAi | Pretax book income scaled by lagged total assets reported |

| INTANGi | Intangible assets (WC02649) scaled by lagged total assets reported |

| LEVi | Long-term debt scaled by lagged total assets reported |

| FOREIGN_DUMMYi | 1, if the percentage of foreign sales of total sales (WC08731) is greater than 10% |

| HQi | 1, if the headquarter of the ultimate parent is in the United Kingdom; 0 otherwise (data as of November 2020) |

Note. All continuous control variables (except LN_ANALYSTS) are winsorized (yearly) at the 1st and 99th percentiles.

Acknowledgements

The authors gratefully acknowledge the helpful comments and suggestions from Ralf Maiterth, participants of the 2022 Tax Meeting of the Schmalenbach Society for Business Administration and an anonymous reviewer. They also thank Julian Bock, Nadine Graf, Tjard Marx, and Julian Simon for their support in data collection.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplementary Material

Supplemental material for this article is available online.

Notes

Author Biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.