Abstract

Board members with multiple directorships develop reputational capital as decision experts. Prior studies based on public firms suggest that such directors would use higher quality auditors to improve the quality of financial reporting and, thereby, protect their reputational capital. This study is the first large-scale study that investigates whether multiple directorships influence auditor choice in the setting of private firms. The result indicates a significant positive association between the proportion of board members with outside directorships and audit quality. Furthermore, it shows that the propensity to hire a higher quality auditor is significantly influenced by directors’ network. Finally, the results indicate that the incentives to invest in higher quality auditors are largely influenced by the size of the companies in which board members have their outside directorships.

Introduction

This article examines whether outside directorships of board members affect their demand for audit quality in private firms. By serving on multiple boards, directors have developed reputational capital as decision experts and the value of their human capital depends on their performance in different organizations (Fama & Jensen, 1983). Presumably, such directors would use higher quality auditors to improve the quality of financial reporting and, thereby, protect their reputational capital (Carcello et al., 2002; Fredriksson et al., 2020). Also, outside directorships enable executives to establish a network with other directors (Fahlenbrach et al., 2010). The information from directors’ personal networks can influence their decisions regarding auditor choice (Johansen & Pettersson, 2013). However, prior studies on how corporate governance characteristics influence the choice of higher quality auditors are predominantly focused on public firms. Because private firms differ from public firms on a number of important aspects (Langli & Svanström, 2014), it is not obvious without testing that the results from public firms will generalize to private firms.

An audit is used by firms to create a separating equilibrium (Jensen & Meckling, 1976). The empirical findings (e g., Carcello et al., 2002; Fredriksson et al., 2020) suggest that in equilibrium, we observe firms with higher reputational boards and higher audit quality and vice versa. This equilibrium is intuitive from an economic perspective and may imply that shareholders who are more concerned about the reputation of their firms would choose directors with higher reputational capital. Therefore, the auditor-choice decision might be indirectly influenced by shareholders. In this study, I seek evidence to better understand the influence of the board on the auditor-choice decision in private firms.

The reputational capital of directors with multiple directorships is not associated with only one company but instead is associated with a number of companies where those directors are serving. Thus, any negative news related to the firm from a director’s portfolio can have a substantial impact on the director’s reputational capital (Fredriksson et al., 2020). However, compared with public firms, private firms have a considerably lower profile and they are not scrutinized by market participants to the same extent as public firms (Van Tendeloo & Vanstraelen, 2008). Therefore, the reputational cost of directors serving in multiple boards in private firms may be lower than those serving in public firms. The lower reputation cost may negatively affect directors’ incentives to pay for differentially higher quality audit services.

On the contrary, the value of reputational capital will likely not be less important for directors serving in private firms. Directors with multiple directorships are viewed more favorably in directorship markets because of their high competence (Shivdasani, 1993). High reputational capital is vital for career advancement and provides greater opportunities on the labor market. In addition, in the setting of private firms, the reputational capital might need even more protection because of the following reasons. First, in private firms the board composition and structure are not subject to regulation. This can result in the lack of mechanisms within the board that can ensure a high quality of financial reporting. For this reason, the choice of a high-reputation auditor can give the board members with higher reputational capital a greater protection and confidence in the quality of financial information.

Second, unlike public firms where the information is readily available because of the higher disclosure requirements and the information provided by stock prices (e.g., Lennox, 2005), private firm setting is more informationally opaque. In such a setting, the appointment of a high-reputation auditor can serve as a signal for the directorship market that the company where the director is sitting has the high quality of financial reporting and, thus, serves as a protection of the director’s reputation.

The Swedish private firm setting offers an advantageous research opportunity because of the following reasons. First, in Sweden the regulation regarding the board composition and structure is more relaxed. For instance, there are no formal requirements for private firms to have audit committees or independent board members, characteristics that are proved to be associated with higher quality of financial information (e.g., Abbott et al., 2004; Carcello et al., 2002; Knechel & Willekens, 2006; Sultana et al., 2019). Private firms have, therefore, a greater flexibility to define their own governance strategy. This will likely provide a large variety of governance characteristics and result in a greater variation of financial reporting practices compared with public firms. Thus, the impact of different board features on audit quality demand may be more pronounced in such a setting. Second, unlike public firms where auditing is mostly conducted by Big 4 auditors, private firms in Sweden are characterized by a greater variation of auditor choices. Third, although the Swedish audit market differs substantially from the U.S. audit market (which is used in many audit studies), it is largely dominated by private firms and, thus, is very similar to other European countries. In addition, the Swedish institutional setting is characterized by lower litigation risk (compared with Anglo-Saxon countries) and, in this regard, is also similar to many European countries (e.g., Hope & Langli, 2010; Kinney, 1994; Vanstraelen, 2003). Given these similarities, it is reasonable to assume that the results of this study can be generalized to private firms in other European markets.

This study extends prior studies (Carcello et al., 2002; Fredriksson et al., 2020) that examine the effect of multiple directorships on audit quality in public firms in a number of important ways. First, this study is based on a large sample of private firms and, therefore, provides further insight into the auditor selection in private firms and makes an important contribution to the literature on audit quality. Second, prior studies use audit fees (Carcello et al., 2002; Fredriksson et al., 2020) and auditors’ client portfolios (Fredriksson et al., 2020) to differentiate audit quality in public firms. In private firms, however, there is a larger variety of auditor choices (Chaney et al., 2004) and the market share of high-reputation auditors is considerably lower compared with public firms that are predominantly audited by Big 4 auditors. The selection of a Big 4 or Second-tier auditor in a private firm suggests a considerably higher price for audit services and will properly capture the demand for higher audit quality in such a setting. Therefore, Top 6 auditors (Big 4, Grant Thornton and BDO) are used to capture higher audit quality (Sundgren & Svanström, 2013). Third, I extend the studies of Carcello et al. (2002) and Fredriksson et al. (2020) by examining the effects of directors’ networks on auditor choice.

More importantly, in terms of the incremental contribution, this study is the first to examine how the variation in the value of reputational capital (depending on the size of companies in which directors are serving) influences the demand for audit quality.

Using a sample of 37,292 Swedish private companies over 2006–2015, this study investigates whether boards with greater proportions of outside directorships protect their reputational capital that is manifested by the demand for higher audit quality. Because only small quality differences are found between Big 4 and Second-tier auditors in the Swedish private firm market (Sundgren & Svanström, 2013), Top 6 is used as a proxy for audit quality in this study.

The results provide support for the hypothesis that the demand for audit quality increases with directors’ outside directorships, consistent with the greater need to protect their reputational capital in the private firm setting. Furthermore, I find that the propensity to hire Top 6 auditors is significantly influenced by directors’ network. Finally, I show that the incentives to protect the reputational capital depend on the size of firms where directors have their outside directorships.

This study contributes to the existing literature in several ways. First, it contributes to the growing stream of studies on the association between corporate governance characteristics and audit quality (Fredriksson et al., 2020; Lai et al., 2017; Nekhili et al., 2020; O’Sullivan, 2000; Sultana et al., 2019). Prior studies are predominantly focused on public firms. Nevertheless, smaller companies represent a greater proportion of business worldwide (Chen et al., 2011) and there is a lack of evidence from this considerably different sector. This study is one of the first in this area to use a large sample of private firms and show the role of board structure on the demand for audit quality. Second, this study contributes to elucidating the effects of network on audit quality (Johansen & Pettersson, 2013; Sun et al., 2020) by showing that the presence of a large auditor in the board member network positively influences audit quality in other firms where the directors are serving. Finally, this study adds to the literature on audit quality demand in private firms (Fortin & Pittman, 2007; Francis et al., 2011; Hope et al., 2012; Niskanen et al., 2011).

The reminder of this article is organized as follows. The next section provides information about the Swedish institutional setting. “Literature Review and Research Expectations” section reviews the relevant literature and develops the study predictions. “Research Design” section introduces the sample and empirical models. The main results are reported in the “Results” section. Section “Additional Analysis” includes the supplementary tests and sensitivity analyses. The final section concludes the article.

Institutional Setting

Swedish corporate governance is regulated by legal rules—mainly the Companies Act—as well as complements to legislation (self-regulation), such as the Swedish Corporate Governance Code and the Stock Exchange’s requirements. Two later provisions are mandatory for all Swedish firms listed on the Swedish regular market.

The Companies Act contains provisions for private and public limited liability firms. Chapter 8 includes the provisions concerning the board of directors. Regardless of whether the firm is public or private, the responsibilities of the board of directors include the same principal issues. In particular, the board shall regularly evaluate the firm’s financial position as well as ensure satisfactory monitoring. The rules regarding the board composition, managing director, and chair are less restrictive for private companies. In particular, private firms are allowed to have a board comprising one or two members. If the board includes two or more members, one of the board members must be appointed as a chair of the board. Also, private firms are not required to appoint a managing director. If the firm has the managing director, he or she is not prohibited to serve as a chair of the board. The Swedish regulation for public firms is consistent with the European Union (EU) regulation and includes the latest requirements regarding Audit Committee (the Companies Act) and board independence (the Swedish Corporate Governance Code).

Limited liability firms are required to appoint an auditor. Starting from 2010, small firms are exempted from this requirement. A firm must appoint an auditor if it meets at least two of the following criteria in the last two financial years: (a) more than three employees; (b) a balance sheet total exceeds SEK 1.5 million; and (c) a net turnover exceeds SEK 3 million (The Companies Act, Chapter 9).

Sweden has a two-tier system of auditor qualification: an approved auditor and an authorized auditor. The total number of qualified auditors in Sweden at the end of 2019 was 3,075, of which 2,726 are authorized and 349 are approved (Swedish Inspectorate of Auditors, 2019). Both authorized and approved auditors are entitled to audit all private and public companies. The audit market in Sweden is dominated by the Big 4 audit firms. The fifth and sixth largest audit firms are Grant Thornton and BDO. Sweden also has a large number of small audit firms.

Literature Review and Research Expectations

Prior academic research has found that weaknesses in corporate governance are associated with earnings manipulations, poor financial reporting quality, and internal controls (e.g., Beasley, 1996; Beasley et al., 2000; Carcello & Neal, 2000; Dechow et al., 1996; Klein, 2002; Krishnan & Visvanathan, 2007). The positive audit quality outcomes are related in prior studies to the existence of an audit committee as well as board members’ greater independence and expertise (e.g., Carcello et al., 2002; Clatworthy & Peel, 2013; Fredriksson et al., 2020; Knechel & Willekens, 2006; Sultana et al., 2020).

The rational expectation for the relationship between the quality of corporate governance and investments in external auditing could be that good corporate governance provides a better control environment that would reduce the need for external auditing and result in lower audit fees (Knechel & Willekens, 2006). Contrary to the intuition, many studies have reported a positive association between governance quality and audit fees (e.g., Carcello et al., 2002; Fredriksson et al., 2020; Hay et al., 2008; Knechel & Willekens, 2006; O’Sullivan, 2000; Sultana et al., 2019). The prevalent explanation is that higher quality boards may require more auditing to protect their reputational capital against financial reporting misstatements and possible liability. Hay et al. (2008) conclude in their study that the relationship between the quality of corporate governance and external auditing is complementary rather than substitutional. The studies on the association between governance quality and auditor selection have also found evidence consistent with this argument. Abbott and Parker (2000) use a sample of 500 firms listed in the United States and find that audit committees that are both independent and active are positively associated with the choice of a specialist auditor. They explain the finding by the higher reputational cost of litigation for outside directors. Beasley and Petroni (2001) study 681 public and private property-liability insurers during 1991–1992 and find that more independent boards are more likely to select a specialist Big 6 auditor. However, they do not find any difference between nonspecialist Big 6 and non-Big 6 auditors. The recent study of Fredriksson et al. (2020) based on the sample of public Finnish firms reports that the directors who sit in multiple boards are more likely to choose auditors with higher client portfolios to improve the quality of internal controls and financial reporting and, thereby, protect their reputational capital.

The studies on the association between corporate governance characteristics and the demand for audit quality are predominantly focused on public firms. Despite the great number and economic importance of private firms, they are largely neglected in corporate governance research and recommendations. Given the important differences between public and private firms, it can be questioned whether “better” corporate governance is associated with higher demand for audit quality in private firm settings.

This study investigates how the presence of directors with outside directorships in the board is associated with the choice of larger auditors. Directors who serve on the boards of multiple firms are more sophisticated experts in their fields (e.g., Brown et al., 2019; Carcello et al., 2002). They can bring to the organization their knowledge, expertise, and, also, their networks. Board networks provide valuable information on industry trends, market conditions, and best practices (Brown et al., 2019; Mol, 2001). Multiple directorships are associated with superior firm performance and greater firm value (Larcker et al., 2013; Masulis & Mobbs, 2011). They are also better advisors because of their greater experience and connections (Field et al., 2013). Directors with multiple directorships have developed reputational capital as decision experts that signal to the external labor market of directors (Fama & Jensen, 1983). They have incentives to perform well in each organization to maintain the high value of reputational capital and to be rewarded in the director labor market (Srinivasan, 2005). Prior research suggests that such directors invest in higher quality auditing to protect their reputational capital. They use external auditing to improve the quality of internal controls and financial reporting and thereby reduce the risk of potential fraud and misstatements (Fredriksson et al., 2020). Prior studies on public firms find that multiple directorships are associated with greater audit fees and larger auditors (Carcello et al., 2002; Fredriksson et al., 2020). Private firms, however, represent a different environment. Specifically, private firms have a considerably lower profile and are not scrutinized by shareholders as much as public firms. Therefore, the reputational cost of directors serving in multiple boards of private firms may be lower, which implies less pressure on directors to protect their reputational capital.

However, there are several important reasons for greater auditing demand. The considerably more relaxed requirements to the board composition and structure in private firms may result in the lack of mechanisms within the board to ensure the high quality of financial reporting. The higher level of expertise and advisory capacity of directors with multiple directorships will likely contribute to higher quality decisions. However, a greater workload of such directors does not allow them to be involved in the firm monitoring to the same extent as other board members. Given considerably more relaxed control mechanisms in private firms, the reasonable way to compensate for insufficient control and protect the reputational capital is to invest in a higher audit quality (Abdel-Khalik, 1993). Also, private firms are characterized by lower transparency compared with public firms that have higher disclosure requirements (e.g., Lennox, 2005). In such an environment, an appointment of a larger auditor can signal the higher quality of financial information for directorship markets and can, therefore, positively influence the director’s reputational capital. This leads to the first hypothesis:

Boards with multiple directorships create connections between firms. Their network serves as an important source of business information for connected firms (Larcker et al., 2013) and may contribute to spread of ideas, methods, and potentially influence board decisions (e.g., Bizjak et al., 2009; Ortiz-de-Mandojana et al., 2012; Shropshire, 2010). Johansen and Pettersson (2013) draw on the social network literature and suggest that directors with multiple directorships can use the information from their personal networks to reduce uncertainty in making decisions regarding auditor choice in public Danish firms. They find support for this hypothesis. Based on this evidence, it can be expected that board members with multiple directorships might influence an auditor choice decision through knowledge and experience obtained from other firms. This leads to the second hypothesis:

Private companies vary in their size and are divided into the following categories: micro, small, medium-sized, and larger firms (EU recommendation 2003/361). The value of directors’ reputational capital may depend on the type of companies in which those directors are serving. The larger the company is, the more knowledge and expertise it requires. Greater reputational capital of directors serving in larger firms suggests larger reputational threats compared with directors serving in smaller private companies and needs, therefore, a higher degree of protection. This leads to the third hypothesis:

Research Design

Sample Selection

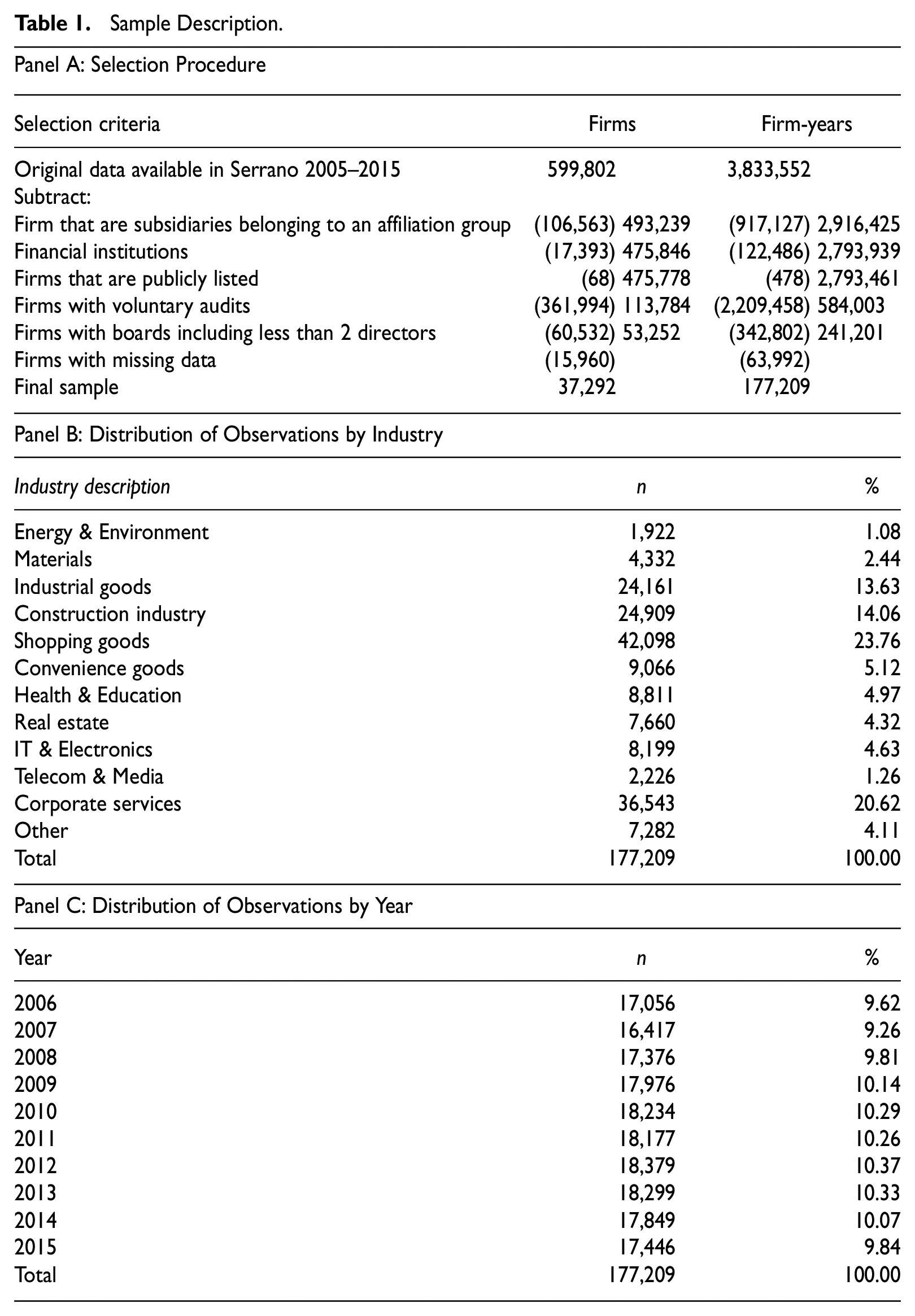

The sample includes privately held firms between 2006 and 2015. The financial data are obtained from the Serrano database, including financial information on all Swedish companies. These data were merged with auditor data obtained from the Swedish Inspectorate of Auditors (SIA) and board data provided by the Bisnode company for the same period.

The original data set included 3,833,552 observations for 599,802 limited liability firms. The subsidiaries were excluded (917,127 observations for 106,563 firms) because their choice of auditor is likely to be influenced by the parent company. The sample includes only parent firms and independent firms. Financial institutions were excluded (122,486 observations for 17,393 firms). Listed firms (478 observations for 68 firms) were eliminated. Furthermore, 2,209,458 observations representing 361,994 firms defined as ones with voluntary audits were excluded. Small unlisted companies often have small boards consisting of one person. To increase board variation, firms that include less than two board members were eliminated (342,802 observations for 60,532 firms). Finally, 63,992 observations for 15,960 firms were excluded because of missing data. Table 1 provides detailed information on the sample selection and distribution. The final data set used for this study includes 177,209 observations for 37,292 firms.

Sample Description.

Empirical Model

To test the study hypotheses, I estimate the following model 1 :

where TOP6 is a binary measure when a firm is audited by a Top 6 auditor (PwC, Ernst & Young, Deloitte, KPMG, Grant Thornton, and BDO). The descriptions of the variables included in the model are provided in the appendix. To minimize the effect of outliers, all continuous variables in Equation 1 are winsorized at 1% and 99%.

Measurement of the Variables

A Dependent Variable

The measure of audit quality used in this study is auditor choice. Prior literature commonly associates higher audit quality with the affiliation to Big 4 firms (e.g., Ferguson et al., 2003; Hope et al., 2012; Minnis, 2011; Simon & Francis, 1988) because of their stronger incentives (due to larger client base) arising mostly from reputation and litigation concerns (DeAngelo, 1981), higher quality employees (DeFond & Zhang, 2014), and more resources spent on training their employees (Firth, 1985). Second-tier auditors represent the fifth and the sixth largest firms worldwide. Although their market share is still lower than that of Big 4 auditors, they have considerably developed reputational capital and the incentives similar to Big 4 auditors to provide high-quality audits (Boone et al., 2010). Empirical evidence from European private firm sector provide rather weak support (Maijoor & Vanstraelen, 2006; Van Tendeloo and Vanstraelen, 2008) or cast doubt regarding superior quality of Big 4 firms in the sector of private firms (Hardies et al., 2018; Sundgren & Svanström, 2013). The study of Sundgren and Svanström (2013) suggests audit quality distinction between Top 6 and other auditors in the private firm market because of similar audit quality levels among six larger firms. Following this study, audit quality is proxied by a binary variable TOP6 that equals 1 if the auditor is a Big 4 or Second-tier audit firm, and 0 otherwise.

Independent Variables

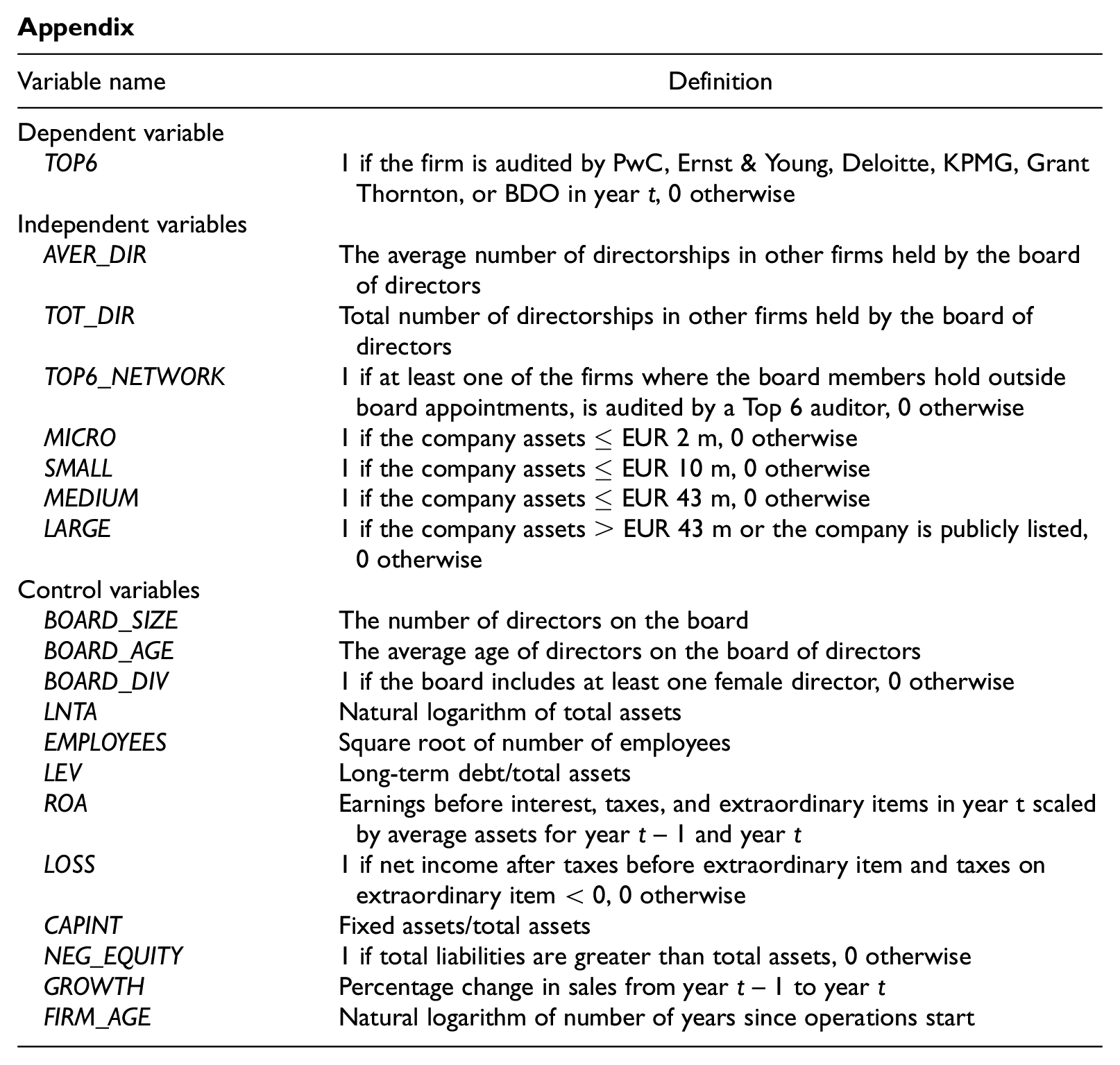

The test variables for H1, directors’ reputational capital, is measured following prior studies (Carcello et al., 2002; Fredriksson et al., 2020) as the average number of outside directorships held by the board members (AVER_DIR) and the total number of outside directorships held by board members (TOT_DIR).

The test variable for H2, the presence of Top 6 in the auditor’s network, equals 1 if at least one of the firms where board members hold outside board appointments, is audited by Top 6 auditor, and 0 otherwise (TOP6_NETWORK).

To test H3, I construct three variables to proxy for the value of directors’ reputational capital. These variables represent the directorship in each firm category: micro, small, medium and larger firms. First, I calculate mean assets per assignment of outside directorships held in other firms by the board members. This is calculated as the sum of assets in other companies where the board directors are serving divided by the sum of outside directorships. Then, using mean assets per assignment, I contract four indicator variables representing four company categories according to EU definition: MICRO (≤ EUR 2 m), SMALL (≤ EUR10 m), MEDIUM (≤ EUR 43 m), and LARGE (> EUR 43 m or the firm is publicly listed). 2 I use the interaction of each company category with the variable AVER_DIR in the model.

Control Variables

The choice of control variables is guided by prior research. I include board size (BOARD_SIZE) and directors’ age (BOARD_AGE) that are expected to positively affect audit quality (Nekhili et al., 2020; Lee et al., 2019). The presence of females in the board is found to be associated with higher audit fees and the choice of specialist auditors (Lai et al., 2017). To control for the effect of gender-diverse boards, I include an indicator variable board diversity (BOARD_DIV) denoting the presence of at least one female director on the board (Lai et al., 2017). Furthermore, I include the natural logarithm of total assets (LNTA) to control for firm size (Fan & Wong, 2005; Lai et al., 2017). Following Fortin and Pittman (2007), firm complexity is proxied by a square root of number of employees (EMPLOYEES). Leverage (LEV) is included to control for possible agency conflicts between shareholders and debtholders (DeFond, 1992; Lennox, 2005). To control for differences in the firms’ financial conditions, return on assets (ROA), negative earnings (LOSS), and negative equity (NEG_EQUITY) are included (Forst & Hettler, 2019; Hope et al., 2012; Lai et al., 2017; Niskanen et al., 2010). More profitable firms use internally generated resources to finance future projects and, therefore, less likely to hire larger auditors (Lennox, 2005). Profitability is captured by a variable sales growth (GROWTH). Companies arguably require less monitoring when their assets are mostly fixed (e.g., Lennox, 2005). This is controlled by a capital intensity variable (CAPINT). Demand for audit quality is expected to decrease with a firm’s age (FIRM_AGE; Mansi et al., 2004). Finally, I include the set of indicator variables for years to control for the year fixed effects and indicator variables for industry that control for the industry fixed effects.

Results

Descriptive Statistics

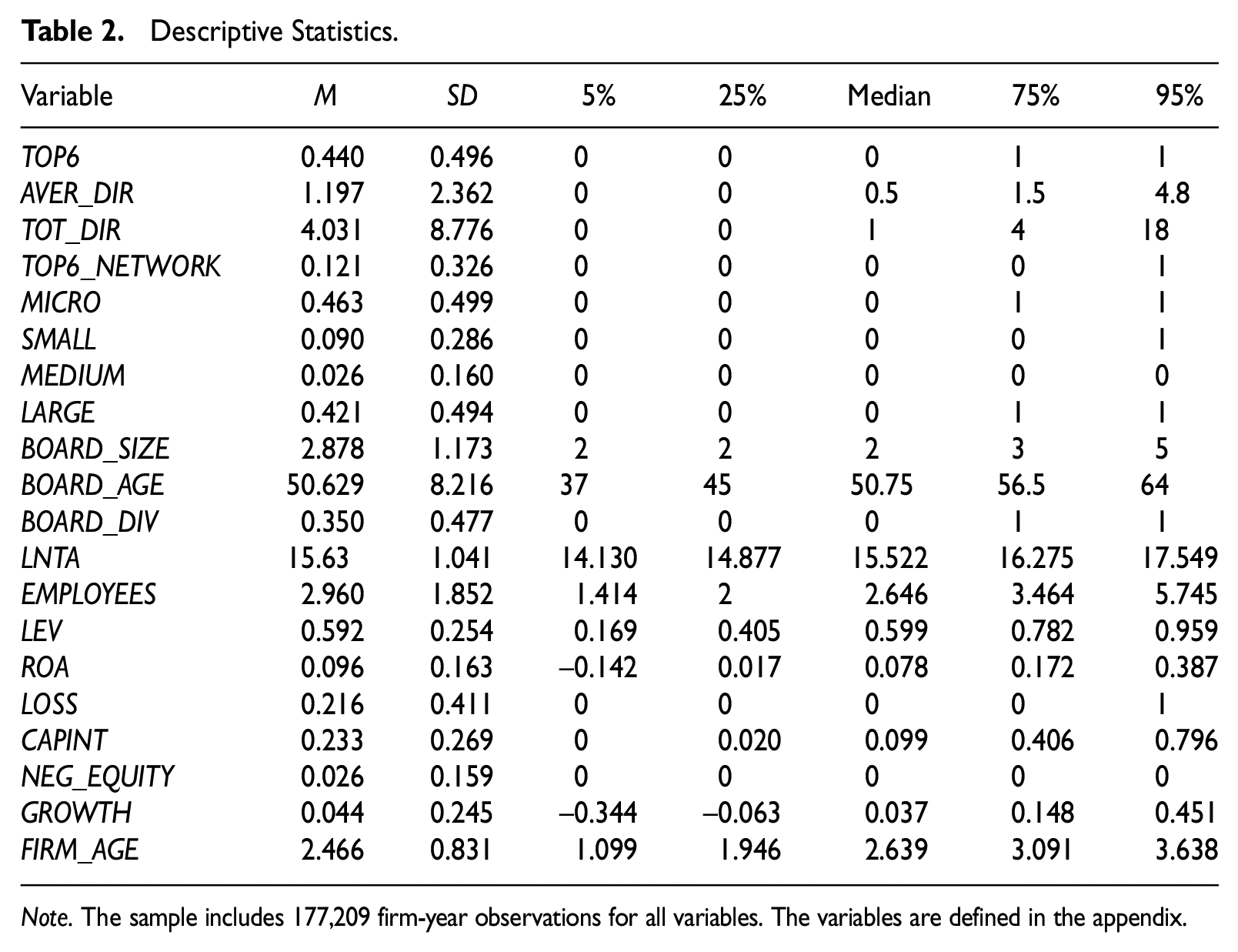

Table 2 presents descriptive statistics for the final sample. As shown in the table, 44% of private firms employ Top 6 auditors (TOP6). The table also indicates that board members have on average 1.2 directorships in other companies. In the sample, 46.3% of boards have their outside directorships in micro firms and 42.1% in larger private firms or listed firms. The mean (median) age of directors is 50.6 (50.8). The mean percentage of the boards that include at least one female director is 35%.

Descriptive Statistics.

Note. The sample includes 177,209 firm-year observations for all variables. The variables are defined in the appendix.

The logarithm of total assets (LNTA) has a mean (median) of 15.63 (15.52). The mean (median) value of the square root of employees (EMPLOYEES) is 2.96 (2.65). This means that an average firm has about nine employees. Almost 22% of the private firms experience losses (LOSS) and only 2.6% have negative equity (NEG_EQUITY). The firms have in general quite high leverage (LEV) with mean (median) of 0.59 (0.60).

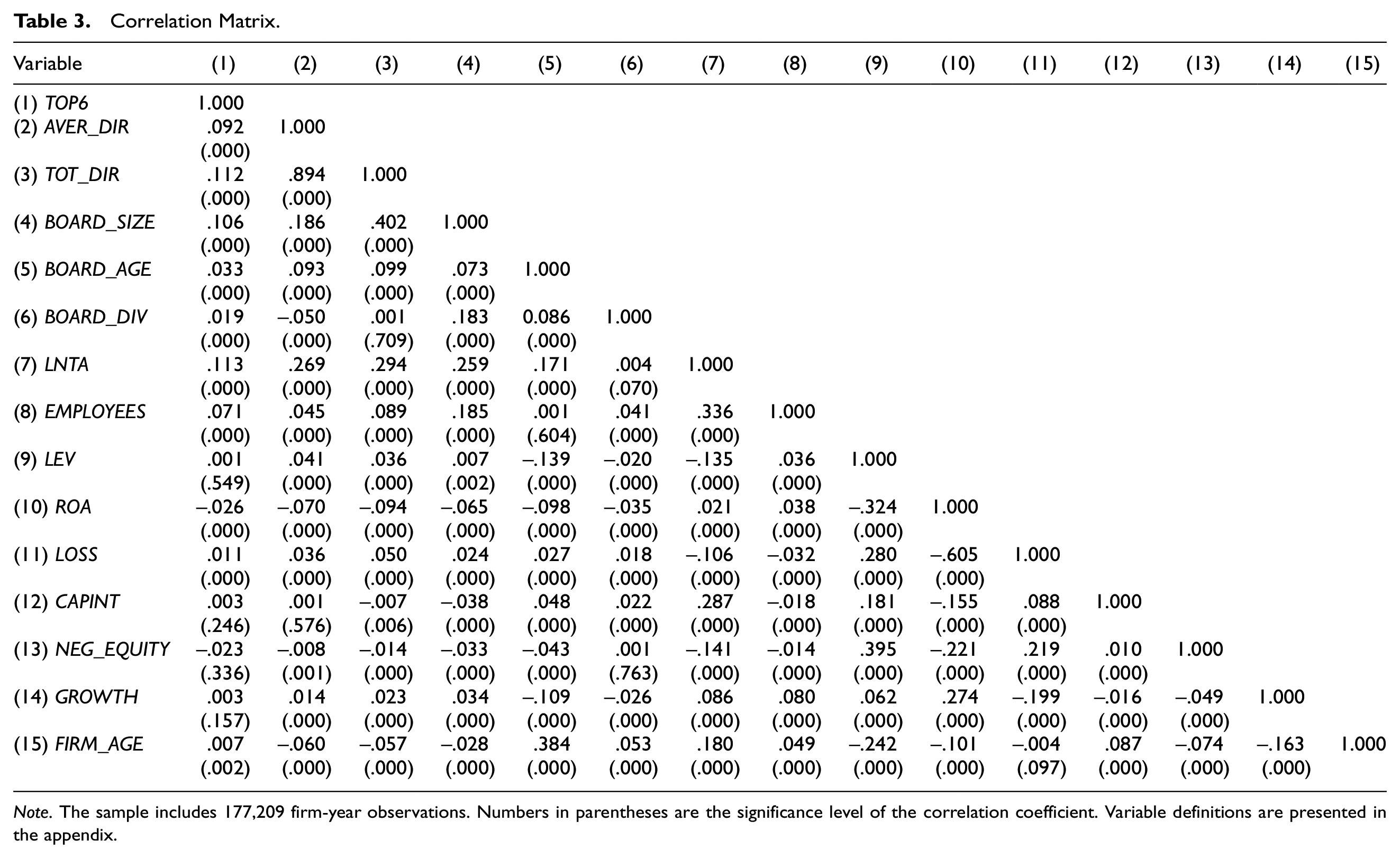

Table 3 presents the Pearson correlation matrix of the variables. The table shows a significantly positive correlation between TOP6 and the test variables. Most of the other variables are also significantly correlated. However, unreported variance inflation factors (VIFs) do not indicate any multicollinearity problems. Specifically, no VIF is above 1.83 and mean VIF is 1.33.

Correlation Matrix.

Note. The sample includes 177,209 firm-year observations. Numbers in parentheses are the significance level of the correlation coefficient. Variable definitions are presented in the appendix.

Test of Hypotheses

The Impact of Board’ Outside Directorships on Auditor Choice

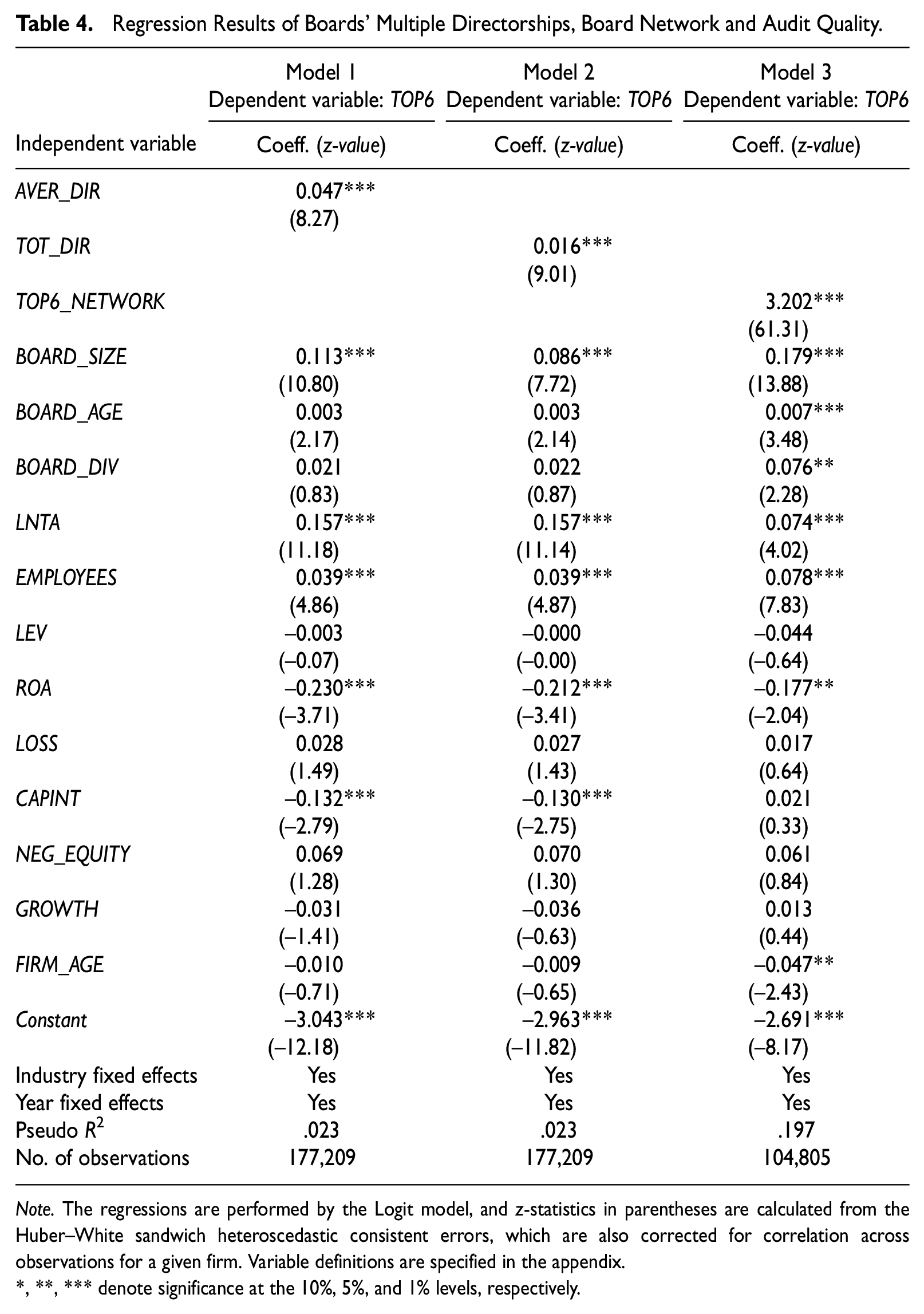

The results of the analyses that measure the demand for higher quality auditing by board members with multiple directorships are reported in Table 4. The results in Columns (1) and (2) show that the coefficients on the two variables that capture board expertise, AVER_DIR and TOT_DIR, are positive and significant (p < .001). This is consistent with the prediction in H1 that higher percentage of outside directorships requires greater protection of directors’ reputational capital, resulting in the choice of higher quality auditors.

Regression Results of Boards’ Multiple Directorships, Board Network and Audit Quality.

Note. The regressions are performed by the Logit model, and z-statistics in parentheses are calculated from the Huber–White sandwich heteroscedastic consistent errors, which are also corrected for correlation across observations for a given firm. Variable definitions are specified in the appendix.

, **, *** denote significance at the 10%, 5%, and 1% levels, respectively.

The Effects of Board Network on Auditor Choice

Table 4, Column (3) illustrates the result of H2. The result provides strong evidence (p < .001) that board networks matter in auditor choice. The results show that among firms that have board members with outside directorships, the probability to choose a Top 6 auditor increases considerably if at least one firm in the board members’ networks is audited by a Top 6 auditor.

Reputational Capital Value and the Demand for Audit Quality

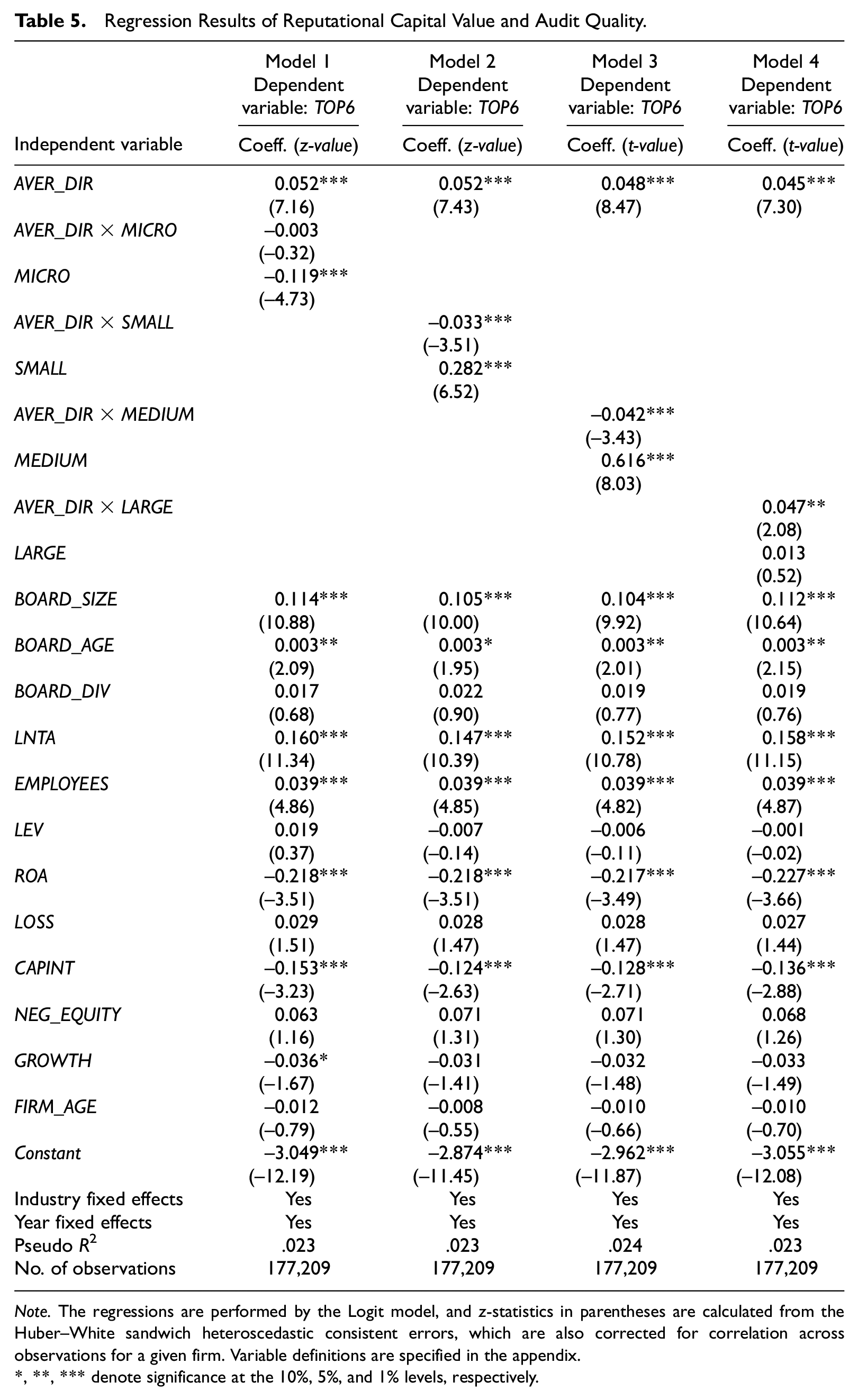

The results of the analyses of the effects of multiple directorships in different company categories are reported in Table 5, Columns (1) to (4). Columns (2) and (3) show that the coefficient of the interaction terms SMALL*AVER_DIR and MEDIUM*AVER_DIR has a negative sign and is significant (p < .01). The interaction term MICRO*AVER_DIR (Column [1]) has a negative sign but is not significant. The result reported in Column (4) show that the interaction term LARGE*AVER_DIR is positively and significantly (p < .05) associated with TOP6, indicating that a higher fraction of the directors serving in larger firms or listed firms is positively associated with the demand for higher audit quality. The results in Table 5, therefore, are consistent with the notion that greater reputational capital needs a higher degree of protection and provide support for H3.

Regression Results of Reputational Capital Value and Audit Quality.

Note. The regressions are performed by the Logit model, and z-statistics in parentheses are calculated from the Huber–White sandwich heteroscedastic consistent errors, which are also corrected for correlation across observations for a given firm. Variable definitions are specified in the appendix.

, **, *** denote significance at the 10%, 5%, and 1% levels, respectively.

Additional Analyses and Sensitivity Tests

Financial Reporting Quality and Financial Position

Abnormal Accruals

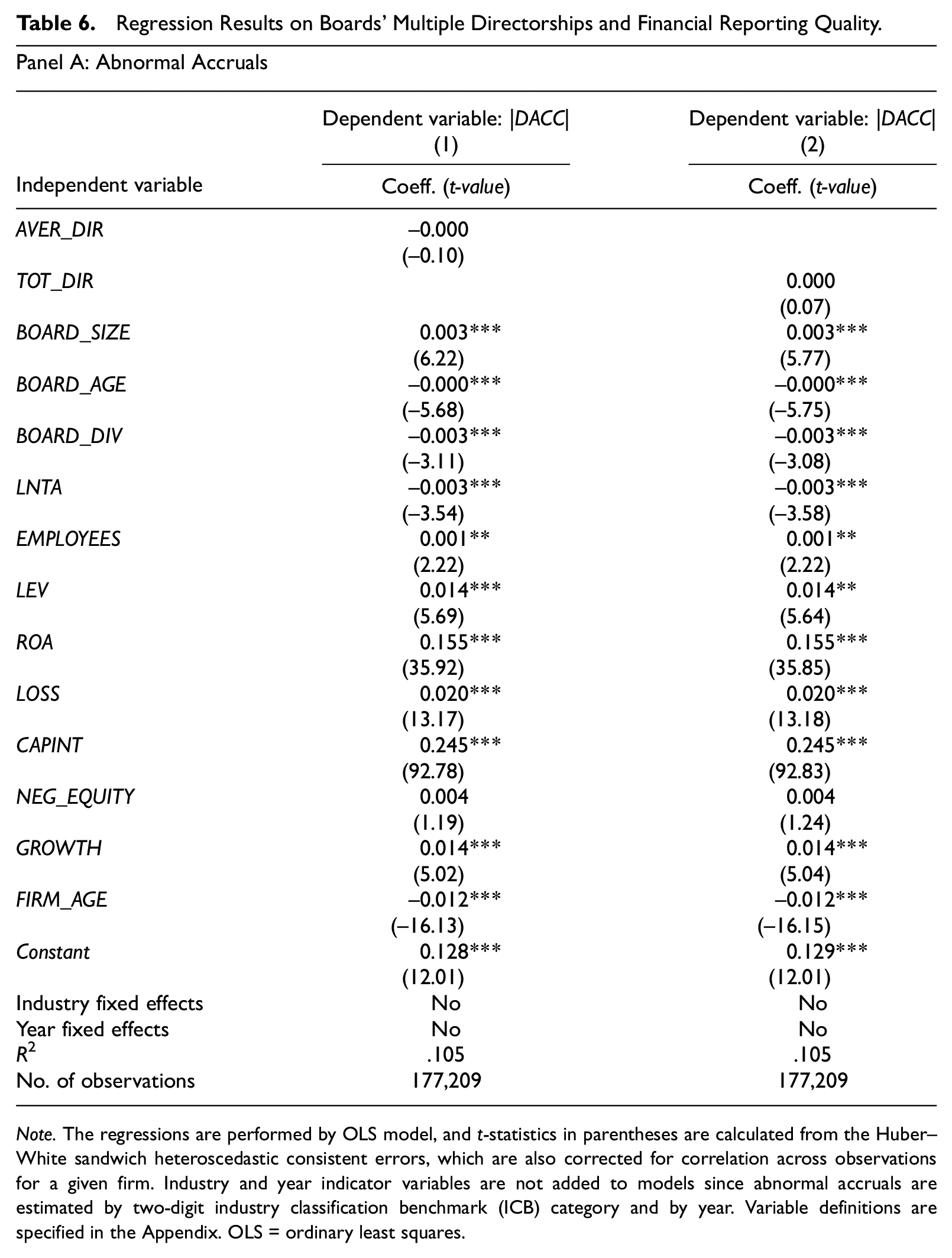

As the next step of the analysis, I examine whether directors sitting in multiple firms are associated with higher financial reporting quality. Directors with outside directorships are willing to perform well in each organization to maintain the high value of their reputational capital. However, greater workload of such directors may prevent them from devoting sufficient time to their duties in each firm. Therefore, it is an open question how the quality of financial information is associated with multiple directorships in private firms.

To analyze financial reporting quality, I use abnormal accruals. Prior literature suggests that audit quality is higher if firms’ earnings are of higher quality, expressed in lower abnormal accruals (e.g., Balsam et al., 2003; Krishnan, 2003; Lee et al., 2019; Lim & Tan, 2008; Reichelt & Wang, 2010). I estimate performance-adjusted abnormal accruals following Kothari et al. (2005). The following equation is estimated for each year and industry: TAit = α (1/Ai,t– 1) +β1 (ΔSALESit–ΔARit) +β2 PPEit+β3 ROAit+ε it . Expected total accruals (ETAs) are the fitted values for each observation from the above regression The abnormal accruals (DACC) represent the difference between total accruals and ETAs and are used as a proxy for earnings quality Audit quality is proxied by the absolute value of abnormal accruals |DACC| suggested by Reichelt and Wang (2010). The higher the value, the higher the reported earnings.

To analyze the effect of multiple directorships on abnormal accruals, I estimate the ordinary least squares (OLS) regression model with the dependent variable |DACC|, independent variables AVER_DIR and TOT_DIR, and firm control variables. The regression result is presented in Table 6, Panel A. Columns (1) and (2) show that both coefficients AVER_DIR and TOT_DIR are not significantly associated with |DACC.| The result, thus, does not reveal significantly different financial reporting quality in the firms that have larger proportions of board members with multiple directorships.

Regression Results on Boards’ Multiple Directorships and Financial Reporting Quality.

Note. The regressions are performed by OLS model, and t-statistics in parentheses are calculated from the Huber–White sandwich heteroscedastic consistent errors, which are also corrected for correlation across observations for a given firm. Industry and year indicator variables are not added to models since abnormal accruals are estimated by two-digit industry classification benchmark (ICB) category and by year. Variable definitions are specified in the Appendix. OLS = ordinary least squares.

Note. The regressions are performed by the Logit model, and z-statistics in parentheses are calculated from the Huber–White sandwich heteroscedastic consistent errors, which are also corrected for correlation across observations for a given firm. Variable definitions are specified in the appendix.

, **, *** denote significance at the 10%, 5%, and 1% levels, respectively.

Internal Control, Delayed Reporting and Auditor Opinion

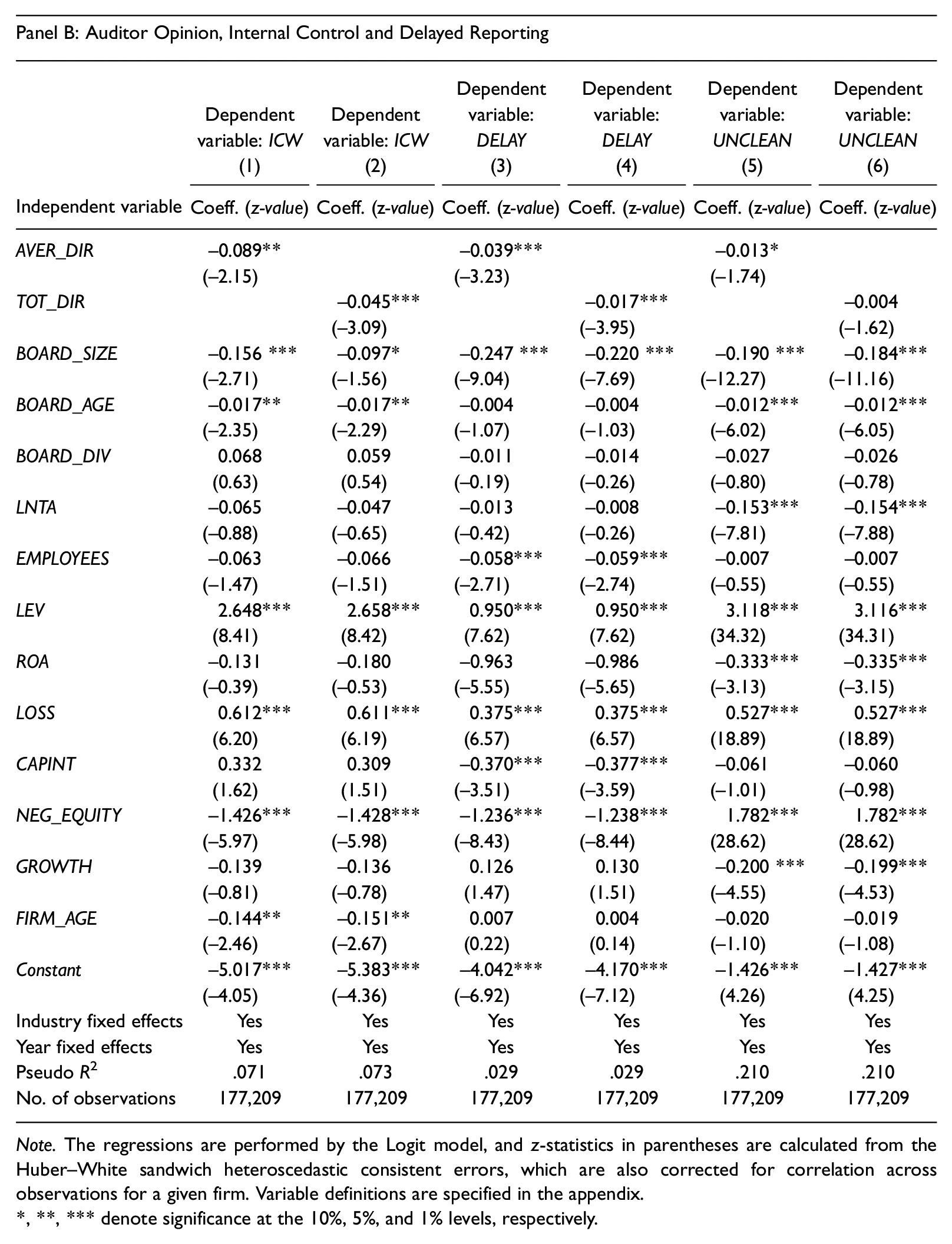

To capture further aspects of financial reporting quality, I use the incidence of an internal control weakness and a delayed filing of an annual report as measures. Moreover, I analyze companies’ financial positions using auditor opinion. The data for these variables are provided by the Swedish Inspectorate of Auditors. If the accounting has deficiencies, the auditor can include an internal control remark in the audit report. A binary variable internal control weaknesses ICW indicates the presence of an internal control remark in the auditor report and signals that a firm has poor quality of internal control. Next, I include a binary variable reporting delay DELAY coded as unity for firms filing their annual statements beyond the statutory deadline, which is expected to signal underlying firm-specific problems (Dyer & McHugh, 1975). Finally, I include a binary variable unclean auditor opinion UNCLEAN indicating that the audit report includes a going concern paragraph. Unclean auditor opinion indicates that there is substantial doubt about the entity’s ability to continue as a going concern. This suggests, therefore, that an entity experiences severe problems.

The results of the analyses are reported in Table 6, Panel B. Columns (1) and (2) show the results on internal control weaknesses. Both AVER_DIR and TOT_DIR are negatively and significantly related to ICW. The results regarding reporting delays are presented in Columns (3) and (4). Both variables of interest have a negative sign and are significant. The results related to auditor opinion are presented in Columns (5) and (6). AVER_DIR is negatively and significantly associated with UNCLEAN. TOT_DIR has a negative sign but is not significant. The aggregated results indicate that directors serving in multiple boards are associated with a higher quality of financial information and are less likely to receive a modified auditor’s opinion.

Propensity Score Analysis

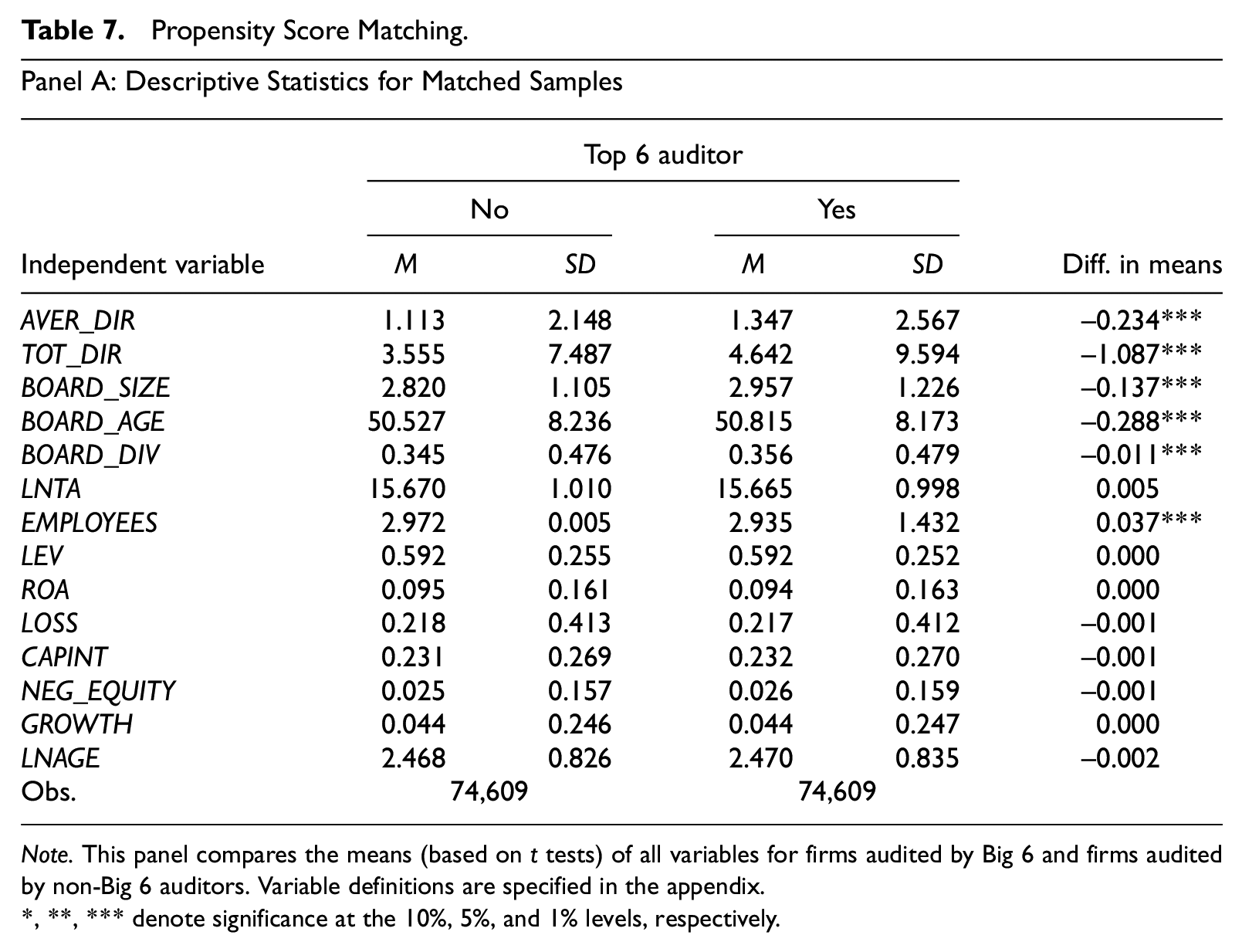

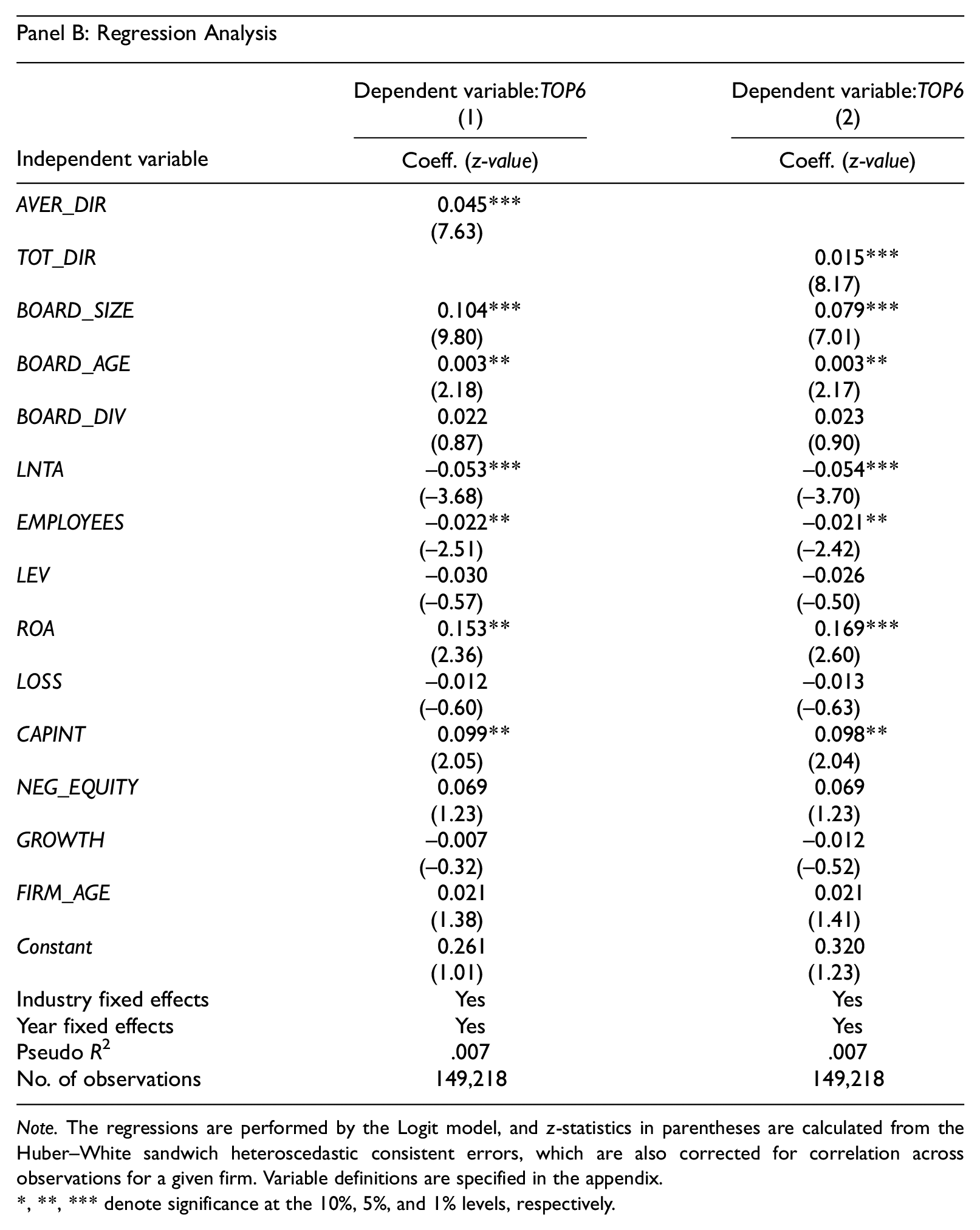

Firms employing Top 6 auditors might be systematically different from other firms. This could result in potential self-selection bias in the main sample. To overcome this possible problem, I use the propensity score matching (PSM) technique (Rosenbaum & Rubin, 1985) to construct a matched sample of companies audited by non-Top 6 auditors and having the same predicted probabilities as companies audited by Top 6. In the first stage, I estimate the propensity scores of companies having Top 6 auditors. I run a logistic regression including all firm characteristics (i.e., control variables): LNTA, EMPLOYEES, LEV, ROA; LOSS, CAPINT, NEG_EQUITY, GROWTH, LNAGE, and industry dummy. In the second stage, I employ one-to-one nearest neighbor matching within a caliper. Nearest neighbor matching within a caliper is an appropriate method for this study because of two reasons. First, it is particularly useful if the outcome variable is non-normal non-continuous. Second, it allows multivariate post-matching analyses (Guo & Fraser, 2014). To apply this method, a company audited by a Top 6 auditor i is matched with a company audited by a non-Top 6 auditor j if the absolute difference of propensity scores between i and j falls into a predeterminant caliper ε and is the smallest among all pairs of absolute differences of propensity scores between i and j within the caliper (Guo & Fraser, 2014). The caliper size is calculated as a quarter of a standard deviation of the sample estimated propensity scores (Rosenbaum & Rubin, 1985). 3 The propensity score-matching produces a matched sample of 74,609 control firm observations, resulting in a combined sample of 149,218 firm observations. Panel A of Table 7 shows the covariate means after matching for the treated and control samples. Most covariate means differ significantly before matching, but after matching, they are similar. In the third stage, I estimate the main regression presented earlier. The results of the post-matching regression analyses are presented in Panel B of Table 7. This analysis, therefore, offers strong support for the main findings, confirming that greater fractions of multiple directorships have a substantial impact on audit quality demand.

Propensity Score Matching.

Note. This panel compares the means (based on t tests) of all variables for firms audited by Big 6 and firms audited by non-Big 6 auditors. Variable definitions are specified in the appendix.

, **, *** denote significance at the 10%, 5%, and 1% levels, respectively.

Note. The regressions are performed by the Logit model, and z-statistics in parentheses are calculated from the Huber–White sandwich heteroscedastic consistent errors, which are also corrected for correlation across observations for a given firm. Variable definitions are specified in the appendix.

, **, *** denote significance at the 10%, 5%, and 1% levels, respectively.

Impact Threshold for a Confounding Variable

Control variables and propensity score analysis help to mitigate the influence of observable differences between treatment and control observations. To further evaluate the influence of correlated omitted variables, I follow prior research (Cahan et al., 2022; Christensen, 2016; Frank, 2000; Larcker & Rusticus, 2010) and estimate the impact threshold for a confounding variable (ITCV). This method approximates to which extent a hypothetical omitted control variable would have to be correlated with the test variables (AVER_DIR and TOT_DIR) and the dependent variable (TOP6) to invalidate the results.

The result (untabulated) of the analysis of the model including AVER_DIR indicates that ITCV is 0.0454. The result of the model including TOT_DIR shows that ITCV is 0.0498. This suggests that partial correlations between multiple directorships and Big 6 with a hypothetical additional control variable must be at least .213 (the square root of .0454) and .223 (the square root of .0498), respectively.

According to Larcker and Rusticus (2010), it is important to consider the ITCV in relation to the impact of the control variables. The result of the model including AVER_DIR indicates that the control variable with the largest impact on the coefficient for multiple directorship is LNTA, with a value of 0.0209. The result of the model with TOT_DIR shows that the control variable with the largest impact is BOARD_SIZE, with a value of 0.0228. Therefore, the impact of an omitted variable on the choice of Big 6 auditors would need to be more than 2 times greater than the strongest control variable in each respective model. In sum, the measures of multiple directorship have the largest ITCV value relative to the control variables. Assuming that the model includes a wide set of control variables, this test provides some confidence in the estimation of the effect of multiple directorships on the choice of higher quality auditors.

Big 4 Instead of Top 6

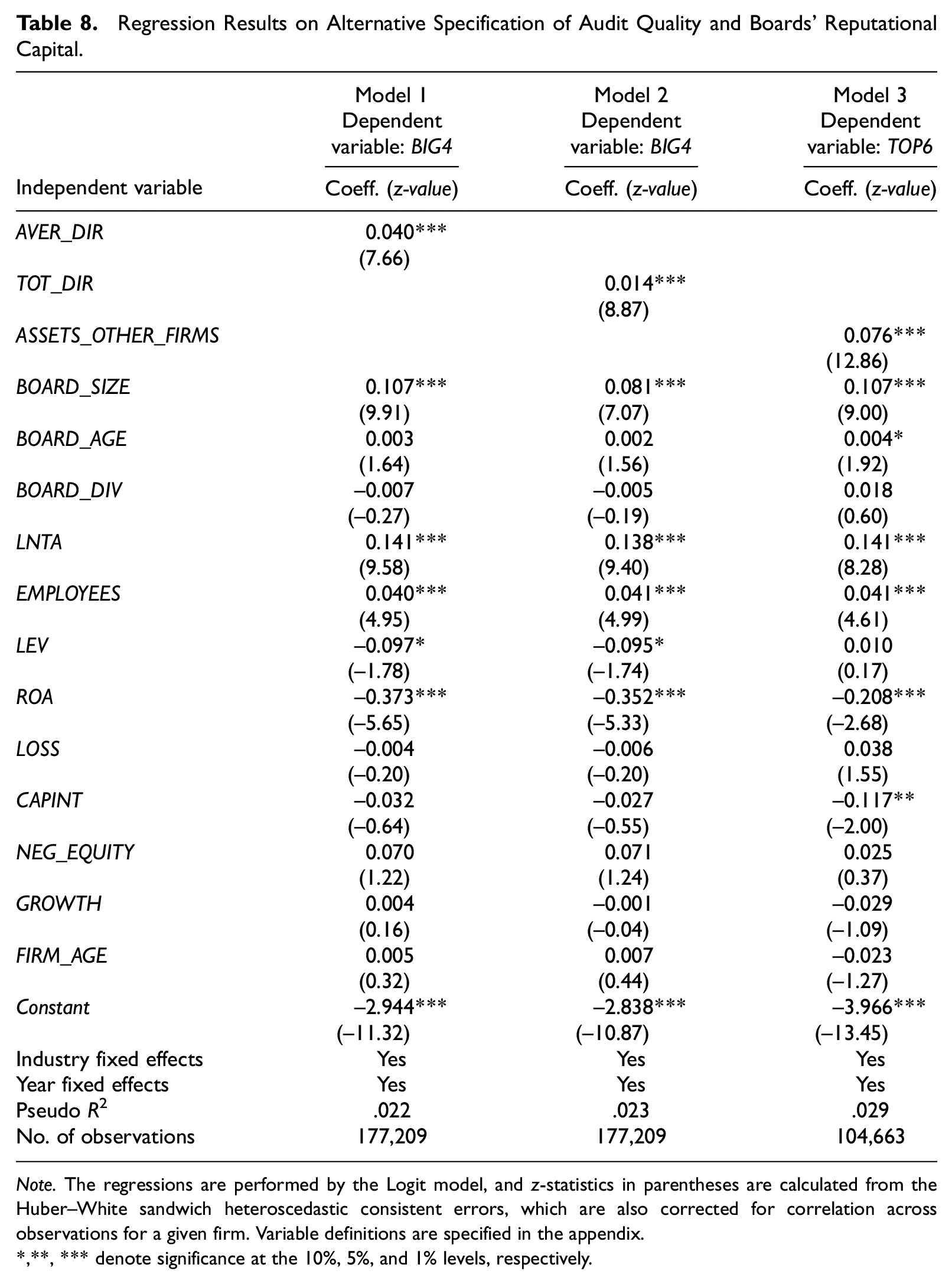

The market share of Big 4 audit firms is relatively small among private firms (33.7% in the studied sample); as a supplementary test, I replace Top 6 with Big 4 (PwC, Ernst & Young, Deloitte, and KPMG). The results of the tests on auditor choice are reported in Table 8, Columns (1) and (2). The results of this test are similar to the main results.

Regression Results on Alternative Specification of Audit Quality and Boards’ Reputational Capital.

Note. The regressions are performed by the Logit model, and z-statistics in parentheses are calculated from the Huber–White sandwich heteroscedastic consistent errors, which are also corrected for correlation across observations for a given firm. Variable definitions are specified in the appendix.

,**, *** denote significance at the 10%, 5%, and 1% levels, respectively.

Alternative Specification of Board Expertise

Multiple directorship in larger firms that often are more complex may be associated with greater expertise. This can provide higher incitement for directors to protect their reputation capital. I construct the alternative measure of board expertise as a natural logarithm of the average assets of outside directorships held in other firms by board members (ASSETS_OTHER_FIRMS). Table 8, Column (3) reports the results for this proxy for demand for audit quality. The finding indicates that ASSETS_OTHER_FIRMS is positively related to Top 6. The result is, therefore, consistent with the main finding on the positive association between boards’ multiple directorships and audit quality.

Effect of Firm Size

Finally, I consider the role of firm size in the auditor choice. It could be that the probability to choose a higher quality auditor increases as company size increases. I address this issue by reestimating Equation (1) for subsamples of smaller and larger firms based on the median of total assets (LNTA). The results (untabulated) for these sensitivity tests are highly significant and are similar to the main results.

Conclusion

Although the effects of corporate governance characteristics on audit quality have received considerable attention from legislators and researchers, the relation between corporate governance and audit quality demand in private firms is less examined. To the best of my knowledge, this is the first large-scale study on the effect of board structure on auditor choice in private firms.

Using a comprehensive sample of 37,292 Swedish privately held firms spanning the period 2006–2015, this study establishes several key findings. First, the result indicates that boards with greater proportions of directors serving in multiple boards seek to protect their reputational capital and demand higher quality audit services. Second, the finding indicates that the propensity to employ a larger auditor is considerably influenced by the board network. Third, the result reveals that only directors with outside directorships in larger private or public firms are more likely to invest in higher audit quality. This finding suggests that the value of reputational capital increases with the size of companies where directors are serving and accordingly influence their incitement to protect their reputational capital. Finally, in additional analyses I do not find any significant difference in abnormal accruals of firms with a greater proportion of directors serving in multiple boards. However, further analyses have shown that such directors are associated with a higher quality of internal controls, lower probability of delayed reporting, and lower probability of receiving a modified auditor’s opinion.

This study suggests that board structure considerably influences private companies’ demand for higher quality auditing and makes, thereby, an important contribution to the generalizability of previous empirical studies based on public companies. The findings of this study enhance our understanding of the effects of board characteristics on the choice of higher quality auditor and financial reporting aspects.

The research suggests that boards’ multiple directorship is a significant determinant of audit quality and provides policymakers and researchers with important insight into auditor selection criteria in private firms. This finding warrants further research. It could be investigated whether board characteristics influencing audit quality demand are similar across different categories of private firms.

The study is not without limitations. This is a study of association, not causation. It suggests that unobserved factors that are correlated with both audit quality and board characteristics can influence the result. To mitigate this potential problem, I use multiple proxies of studied factors. Furthermore, I conduct additional tests using alternative variable specifications. Moreover, I use propensity score analysis to control for potential self-selection bias. In addition, the use of the impact threshold of a confounding variable addresses the influence of omitted variables. Although the results do not provide evidence for the existence of other unobserved factors, it cannot be completely ruled out that such factors do exist. One of such intuitive factors may be the fact that shareholders indirectly influence the choice of auditors through the selection of higher quality boards.

Footnotes

Appendix

| Variable name | Definition |

|---|---|

| Dependent variable | |

| TOP6 | 1 if the firm is audited by PwC, Ernst & Young, Deloitte, KPMG, Grant Thornton, or BDO in year t, 0 otherwise |

| Independent variables | |

| AVER_DIR | The average number of directorships in other firms held by the board of directors |

| TOT_DIR | Total number of directorships in other firms held by the board of directors |

| TOP6_NETWORK | 1 if at least one of the firms where the board members hold outside board appointments, is audited by a Top 6 auditor, 0 otherwise |

| MICRO | 1 if the company assets ≤ EUR 2 m, 0 otherwise |

| SMALL | 1 if the company assets ≤ EUR 10 m, 0 otherwise |

| MEDIUM | 1 if the company assets ≤ EUR 43 m, 0 otherwise |

| LARGE | 1 if the company assets > EUR 43 m or the company is publicly listed, 0 otherwise |

| Control variables | |

| BOARD_SIZE | The number of directors on the board |

| BOARD_AGE | The average age of directors on the board of directors |

| BOARD_DIV | 1 if the board includes at least one female director, 0 otherwise |

| LNTA | Natural logarithm of total assets |

| EMPLOYEES | Square root of number of employees |

| LEV | Long-term debt/total assets |

| ROA | Earnings before interest, taxes, and extraordinary items in year t scaled by average assets for year t– 1 and year t |

| LOSS | 1 if net income after taxes before extraordinary item and taxes on extraordinary item < 0, 0 otherwise |

| CAPINT | Fixed assets/total assets |

| NEG_EQUITY | 1 if total liabilities are greater than total assets, 0 otherwise |

| GROWTH | Percentage change in sales from year t– 1 to year t |

| FIRM_AGE | Natural logarithm of number of years since operations start |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The study was supported by Jan Wallanders och Tom Hedelius stiftelse samt Tore Browalds stiftelse (W18-0023).