Abstract

Previous literature on the engagement quality (EQ) review argues that EQ reviewers should provide more efforts into the review process when fieldwork auditors’ judgments and conclusions on the financial statements are potentially biased. Little empirical study has been done, however, partly due to the confidentiality of the detailed data on EQ reviewers’ audit hours. The purpose of the article is to shed light on the existing literature by conducting an empirical investigation using a unique actual data set available in Korea. The results show that the EQ review hours are positively associated with CEO turnovers, a proxy for the audit risk, which supports the prediction of the theory on the EQ review. Additional analyses show that such results are stronger under (a) the upward earnings management and (b) the forced CEO turnover. The article extends the existing literature on the EQ review process and enhances the understanding of the engagement-level quality control in the volatile audit environment by providing empirical evidence to the analytic discussions on the EQ review.

Keywords

Introduction

The engagement quality (EQ) review is a process of reviewing the auditor’s works for each individual audit engagement. An independent reviewer who is not directly involved in the audit conducts the EQ review at the final phase of audit procedure (Arens et al., 2012). 1 An EQ reviewer assesses the appropriateness of auditors’ judgments and conclusions on financial statements as well as the sufficiency of audit evidence collected during the fieldwork. 2

The EQ review is considered as one of the most effective means of quality control in auditing (Mautz & Matusiak, 1988). The Public Company Accounting Oversight Board (PCAOB) Standing Advisory Group acknowledges that the EQ review is the contemporaneous audit procedure for quality control that prevents audit failure more effectively than other post hoc in-house inspection or external oversight (PCAOB, 2004). The EQ review receives a new attention in the aftermath of the high-profile accounting scandals in the early 2000s.

Prior studies on the EQ review have focused primarily on the value of the EQ review or its task description and requirements (e.g., independence, responsibilities, and qualifications). For example, Matsumura and Tucker (1995) develop an analytic model to show the value of the EQ review with emphasis on its role in mitigating auditors’ judgment bias. Epps and Messier (2007) compare and analyze the EQ review guidance in the audit manuals across six major audit firms to delineate the differences and similarities of EQ review practices.

This article discusses how the EQ reviewers’ efforts change when the fieldwork auditors’ judgments and conclusions are potentially biased in a new audit environment (e.g., CEO turnover). The possible biases may come from two different and competing reporting incentives by managers in the year of the CEO turnover. On one hand, the incoming CEOs have an incentive to manage earnings positively to eliminate the doubt thrown on managerial ability. On the other hand, the incoming CEOs want to make an accounting reserve for future profits by reporting as much accounting losses as possible.

In either situation, it is difficult for fieldwork auditors to make a request for the adjustments on reported earnings. First, the tremendous changes in the year of the CEO turnover create a new audit environment that increases the level of inherent risk (Whittington & Pany, 2003). Second, the economic dependence on the clients makes the fieldwork auditors hard to be free from the increased pressure from clients. Finally, the cognitive limitation on human information processing prevents the fieldwork auditors from the recognition of biased estimates because the CEO turnover brings the structural changes in business strategy and governance.

Given the possibilities of the fieldwork auditors’ biases, the theory on the EQ review argues that the EQ reviewers should put additional efforts into review process in response to the increased engagement risk (Matsumura & Tucker, 1995). The prediction of the theory provides the following testable empirical question: Do the EQ reviewers change the level of review hours in response to the increased risk upon CEO turnover?

So far, little empirical research has been done, however, partly due to the lack of real-life data. 3 In South Korea, since 2014, The Act on External Audit of Stock Companies requires firms to disclose the detailed audit hours on the audit report including the EQ review hours and the engagement team’s fieldwork hours. Using this unique real-life data set from Korea, the article empirically investigates whether the EQ reviewers respond to potential engagement risk created by CEO turnover.

The main result of the article shows that the EQ review hours are positively associated with CEO turnovers, which supports the prediction of the theory. Besides the main analysis, we performed two additional subgroup analyses: (a) the signs of discretionary accruals and (b) the forced versus non-forced CEO turnover.

The results of the first additional analysis show that the positive relation between the EQ review hours and CEO turnovers is stronger under the income-increasing earnings management than that of the income-decreasing earnings management. The results may imply that the EQ reviewers consider the overstated earnings as high litigation risk environment and, as a result, put more efforts into reviewing the fieldwork auditors’ collected evidence and conclusions when the reported earnings have positive reporting bias.

The results of the second additional analysis show that the EQ review hours in a group of the forced CEO turnover are significantly higher than those in a group of non-forced CEO turnover. That is, the EQ reviewers perceive higher level of audit risk on the engagement team’s works when the CEOs are involuntarily changed.

The article contributes to the literature as follows. First, unlike prior studies, the article discusses the quality control at the level of audit engagement. Most prior studies have focused on how audit risk is reflected in the pricing of audit service (Simunic, 1980) or how total audit hours (that includes both EQ review and fieldwork hours) vary in response to a certain audit risk (Caramanis & Lennox, 2008; Deis & Giroux, 1996). By distinguishing the EQ review efforts from the engagement team’s audit efforts (i.e., fieldwork effort), the article enhances the understanding of two different audit efforts. Second, the article highlights that the CEO turnover increases the perceived engagement risk and should be considered as one of the most important factors in the auditing studies. Huang et al. (2014) argue that the CEO turnover has been neglected in the field of auditing research although it is a significant factor to change the assessment of audit risk.

Background and Hypothesis Development

Quality Control at the Audit Engagement Level

Mautz and Matusiak (1988) argue that top priority should be given to improving quality control rather than imposing additional regulations because the current accounting and auditing practices already bear substantial regulatory costs. Previous studies show that total quality cost decreases as prevention cost increases (Garrison et al., 2015). Therefore, audit scholars and practitioners should pay attention to the importance of the review at the level of individual audit engagement (i.e., EQ review) as means of providing quality control.

Audit procedure generally follows the following four phases: (a) planning and designing audit approaches, (b) performing tests of controls and substantive tests of transactions, (c) performing analytical procedures and tests of details of balances, and (d) completing and issuing an audit report (Arens et al., 2012). In the last phase of audit procedure, the financial statements and the audit files are reviewed before the issuance of an audit report. An EQ reviewer should evaluate carefully and objectively the judgments and conclusions made by auditors in auditing the financial statements or in preparing an audit report (PCAOB, 2017: AS 1220). Thus, the EQ review process plays an important role in monitoring auditors’ works and audit files at an individual engagement level. PCAOB (2009), in this sense, emphasizes that the EQ review can serve as an important safeguard against erroneous or insufficiently supported audit opinion.

Regarding the institutionalization of the review of audit works, Mautz and Matusiak (1988) argue that the EQ review has been conducted by a few audit firms in practice even long before the EQ review was required by regulation. 4 Because the AICPA SEC Practice Section required the review of audit works as membership requirement, the related provisions have been established and revised to meet the needs of the changing audit environment. In 1999, the requirement is revised to include a 2-year cooling-off period (Schneider et al., 2003). That is, a partner is banned from serving as an EQ reviewer for at least 2 years after serving as an engagement partner. After the passage of the Sarbanes-Oxley Act of 2002, the audit environment moves from self-regulation (e.g., peer review program) to government regulation and oversight (Messier et al., 2008). Thus, the auditing standards for quality control—including the EQ review requirements—are established and enforced by PCAOB. Assuming and improving the preexisting standards and guidance, the PCAOB auditing standard (i.e., AS 1220) specifies the objective of the EQ review and the qualifications and responsibilities of the EQ reviewers which should be abided by in the review process.

Theory and Practice of the EQ Review

Matsumura and Tucker (1995) posit that the value of the EQ review is to mitigate the auditor’s bias in the judgment and decision-making in audit procedure. They argue that the EQ reviewer induces an auditor to maintain an objective and rigorous stance during the audit. They develop an analytic model of audit reporting in which an auditor (i.e., engagement team) makes sampling and reporting decisions (e.g., unqualified vs. qualified). An EQ reviewer, then, also makes sampling and decides whether to go with an auditor. In the model, to express an audit opinion, an auditor compares the audit evidence (i.e., the mean from audit sample) to the reference point that an auditor sets (i.e., the threshold of decision-making).

A biased auditor makes a decision threshold that is away from the unbiased expectation. Matsumura and Tucker (1995) point out that two factors can make an auditor biased: (a) an economic incentive caused by client’s pressure and (b) inherent risk of an audit. A client may put a heavy pressure on an auditor to accept the accounting choices that bias the earnings in favor of a client, and under the client’s pressure, it is not easy for the auditor to reject the biased accounting information. In the audit environment where an auditor is biased, an effective EQ reviewer induces an auditor’s critical value to move toward the unbiased expectation. In the model, for example, a reviewer’s veto penalty (i.e., internal penalty that an auditor bears when the reviewer’s disagreement turns out to be right) is expected to induce an auditor to make an unbiased decision.

Tucker and Matsumura (1997) empirically support the expectations by the Matsumura and Tucker’s (1995) model. Using 152 student subjects, they test whether the introduction of the EQ review decreases the subjects’ judgment bias in audit reports. The results show that the EQ review significantly decreases the percentage of unqualified opinion in a biased situation. They also find that the bias reduction effect achieved by the EQ review process is statistically similar to that achieved by additional audit sampling.

Luehlfing et al. (1995) empirically examine whether EQ review serves as a quality control mechanism for audit-related risks. Using 44 observations obtained from three Big-Four firms, they test the relation between the EQ review hours and the client and auditor characteristics. The results show that the client’s industrial membership (i.e., financial and manufacturing industry) is negatively associated with the EQ review hours whereas client size and reviewer’s experience are positively associated with the EQ review hours. The other audit-risk related factors—such as net loss, initial audit, audit opinion, client special risk situations—are statistically insignificant.

Epps and Messier (2007) review the EQ review guidance and practice aids in the audit manuals from six major audit firms to examine the similarities and differences across the audit firms. They find that the EQ review guidance shares lots of common characteristics: written policies, reviewer’s qualifications, review process, and documentation requirement. They also identify substantial differences in the contents and extensiveness of practice aids and the participation of the EQ reviewers in an audit engagement.

The Financial Reporting Incentives and Biases Upon CEO Turnover

The CEO turnover may create two contradicting types of reporting incentives: income-increasing or income-decreasing earnings management. The high level of uncertainty in the year of the CEO turnover may give the incoming CEOs more income-increasing incentives while previous big bath theory may give them income-decreasing incentives. The following section discusses more fully about these possible incentives.

The incentive for income-increasing earnings management

The McKinsey Report in 2018 shows that nearly half of executive transitions are regarded as failures or disappointments (Zucker, 2020). Knowing that the stakeholders keep their eyes on the new management, the incoming CEOs may want to show superior performance in the year of the CEO turnover to eliminate the doubt cast on managerial ability. In this case, the incoming CEOs have an incentive to manage the reported earnings upward because an accounting measure (e.g., reported earnings) is preferred to a market measure (e.g., stock price) in managerial performance evaluation (DeAngelo, 1988).

The CEO turnover brings tremendous structural changes in business strategy and governance. Even though the extent of changes may depend on new CEO’s leadership style and personal characteristics such as professional competency and personal preference, these changes create the uncertainty about the estimates on business prospects such as firm performance, strategic direction, and managerial policies, ending up with the acceptance of optimistic accounting estimates.

For example, Clayton et al. (2005) posit that the assessment about the future cash flows of a firm will be changed following the CEO turnover. They hypothesize that the stock-return volatility is increased by two sources of uncertainty: the substantial change in business strategy (or a firm’s course) and the doubt about the new CEO’s professional ability. They find that the stock-return volatility increases upon the CEO turnover and such increased volatility lasts for about 2 years following the turnover.

The incentive for income-decreasing earnings management

The incoming CEOs argue that the firm’s poor performance is the predecessors’ responsibilities and try to take a big bath in the year of the transition. They may want to make an accounting reserve for future profits, using the attribute of accrual accounting, because the understated earnings in current period can be effortlessly reversible in future periods. Thus, upon CEO turnover, the income-decreasing earnings management is expected and many previous studies support this argument.

DeAngelo (1988) examines how accounting earning is used in a proxy contest by the incoming CEOs and finds that unexpected accruals (cash flows) are significantly negative (positive) when a new CEO comes in. The result indicates that an incoming CEO tries to report decreased earnings with managerial accounting discretion although profitability is actually increased after the proxy contest. Denis and Denis (1995), using the operating income measure, report similar financial reporting behavior observed in the year of top management turnover. Pourciau (1993) also points out that the incentives and opportunities for earnings management can be greater in nonroutine executive turnover than in routine executive turnover.

The Audit Environment Under the CEO Turnover: Potential Biases by the Fieldwork Auditors

Upon CEO turnover, fieldwork auditors should evaluate the possibilities of biases in financial reporting (either upward or downward) and design and conduct audit procedures accordingly to reach unbiased conclusions. But, the new audit environment of executive transitions may make the fieldwork auditors’ judgments biased for the following reasons.

First, the CEO turnover increases the inherent audit risk, which in turn increases the possibilities of the biased judgments and conclusions by the fieldwork auditors. Inherent risk is the likelihood that material misstatements exist in financial statements before considering the effectiveness of internal control (Messier et al., 2008). The level of inherent risk is affected by business environment and firm-specific factors such as the nature of client’s business, management judgments and estimates to record account balances, nonroutine transactions, and factors related to fraudulent reporting (Arens et al., 2012).

Inherent risk lowers the persuasiveness of audit evidence. That is, when the level of inherent risk is high, the auditors need to provide additional efforts to be convinced that the judgments and conclusions to financial statements are correct. If the efforts for enhancing the persuasiveness of audit evidence are limited (e.g., the limitation on efforts for increasing appropriateness and sufficiency of audit evidence), however, the increased inherent risk inevitably makes auditors biased. In this sense, Whittington and Pany (2003) point out that the substantial turnover of management is indicative of high level of inherent risk.

Inherent risk is closely related to the uncertainty about client’s business prospects, and the increased uncertainty weakens the reliability and relevance of the accounting judgments and conclusions. Thus, the possibilities of material misstatements in account balances may increase. Huang et al. (2014) examine whether the situation of the CEO turnover is perceived as a risk factor that affects the audit pricing. They argue that the CEO turnover increases the uncertainty that results in higher business risk, and thus higher audit risk. They further find that forced CEO turnovers are positively associated with audit fees. This shows that CEO turnover serves as a risk factor that increases the risk of material misstatements (i.e., inherent risk).

Second, the disagreement between incoming CEOs and auditors about accounting issues is likely to drive the auditors to allow a biased financial reporting. It may not be easy for an engagement partner to modify an audit opinion by rejecting the managerial estimates that deviate from economic substance. According to Matsumura and Tucker (1995), a client may threaten to change the audit firm (i.e., opinion shopping) to avoid the adverse economic consequences resulting from qualified opinion. The incoming CEO’s dissatisfaction serves as the pressure to the auditors to accept the biased financial statements.

Finally, according to the theories of human information processing, a human being has the limited cognitive ability that cannot fully and instantaneously adjust judgment rules under the changed circumstance. This may exacerbate auditor’s judgment bias. Functional fixation hypothesis says that a decision maker has difficulty in adjusting decision process in response to the underlying changes in accounting process (Ashton, 1976). Thus, even in the environment of the CEO turnover, where the client firm is unchanged while underlying decision structures are changed, auditor may still be fixated to the audit evidence (i.e., decision data) before the CEO turnover.

In sum, in the audit environment of the CEO turnover, the auditor’s appropriate judgments and conclusions may be hindered due to following reasons: (a) inherent audit risk caused by the uncertainty about business prospect-related estimates, (b) clients’ pressures and auditors’ economic dependence on the clients, and (c) auditor’s limited cognitive ability.

EQ Reviewer’s Response to Potentially Biased Works by the Fieldwork Auditors

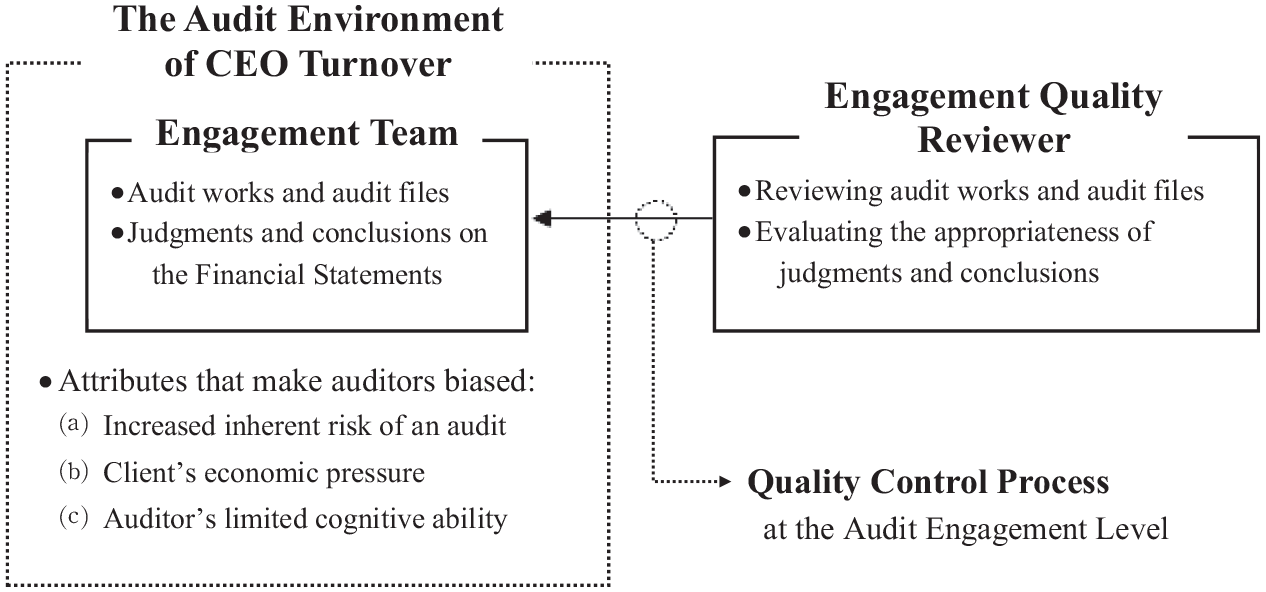

The EQ reviewers are responsible for reviewing the engagement team’s works and audit files to make sure that the audit is adequately performed. Specifically, the EQ reviewers investigate whether the audit evidence collected during fieldwork is sufficient and whether the conclusions made on audit procedures are appropriate. If auditors are biased, then the auditors’ works and working files are also biased. It means that the EQ reviewers’ efforts should vary depending on the extent of the biases in the auditors’ judgments. Luehlfing et al. (1995) posit that the EQ review needs to be conducted more extensively when the deficiencies in financial statements (or audit report) are hard to be detected through the normal audit procedures.

The increased possibility of the auditors’ biased judgments in the year of the CEO turnover may cause the EQ reviewers to perceive the engagement risk embedded in auditors’ works and audit files as relatively high. As a result, the EQ reviewers need to provide more efforts into review process. Figure 1 depicts what makes the engagement team biased in the audit environment of the CEO turnover, and how the EQ reviewers respond to the increased engagement risk through the quality control process at the level of audit engagement.

EQ reviewer’s risk assessment in the audit environment of CEO turnover.

In sum, the theory predicts that the EQ reviewers increase the level of effort when there exists a possibility of bias in the fieldwork auditors’ judgments and conclusions. Based on the discussion above, we develop the following hypothesis:

Model Specification and Measurement

Endogeneity of CEO Turnover: Self-Selection Bias

The literature on top executive changes documents that the primary reason for the CEO turnover is firm performance. In a situation where the CEO turnover is likely to be influenced by business risk (e.g., firm performance and financial distress), there can be a possibility that the main variable of the study (i.e., CEO turnover [TURN]) is endogenous. To mitigate the self-selection bias, we used a two-stage approach by Heckman (1979). In the first stage, we calculated the inverse Mills ratio with the selection model using a probit model. After that, we included the inverse Mills ratio as an additional control variable in Equation 2 and conducted the regression model to test the hypothesis.

As the literature shows, overall firm performance in the prior year of the CEO turnover could be a key indicator of the CEO turnover. Thus, we included the accounting performance (ROA), stock market performance (RET), debt covenant restriction (DEBT), and percentage change in market capitalization (CHMV) in the prior period of the CEO turnover as instrumental variables. The selection model used in the first stage is as follows:

The dependent variable TURN is an indicator variable that takes 1 for the CEO change, and 0 otherwise. ROA is calculated by dividing net income by beginning total assets. RET is the cumulative stock return over 12 months in a given period. DEBT is calculated by dividing total liabilities by total assets. CHMV is the percentage change in the market value of equity. Finally, CONTROLS indicate all control variables of the research model (i.e., Equation 2).

Research Model

We constructed the following Equation 2 to test the relation between the EQ review hours and the CEO turnovers:

We used two alternative measures for the EQ reviewers’ audit efforts in Equation 2. EQR1 represents the level of the EQ review hours (the natural logarithm of EQ review hours). EQR2 represents the proportion of the EQ review hours (EQ review hours divided by total audit hours). The variable of interest in Equation 2 is TURN. If an EQ reviewer views the CEO turnover as a factor that makes the fieldwork auditors biased in the audit procedure, then the estimated coefficient β1 is expected to be positive. Because the regression residuals could be correlated across firms and over time, we adjusted the standard errors of the coefficients on independent variables by two-way cluster at both firm and year.

Control Variables

Previous research shows that EQ review hours are affected by (a) client’s characteristics (e.g., client size, leverage, firm performance), (b) audit-related characteristics (e.g., audit firm type, size of receivables, size of inventory, industry characteristics), and (c) corporate governance (e.g., business group affiliation, ownership by foreign investors).

Deis and Giroux (1996) argue that auditors spend more audit hours for large organizations because large organizations deal with numerous transactions. Thus, we included the client size (SIZE) as a control variable, and we expect a positive association with the EQ review hours. We used the natural logarithm of total assets as a proxy for the client size.

Prior studies also show that the leverage and firm performance affect the inherent risk of an audit. For example, Kalelkar and Khan (2016) and Luehlfing et al. (1995) assert that poor firm performance increases audit risk. DeFond and Jiambalvo (1994) find that the high level of leverage increases the possibility of debt covenant violation, which provides the managerial incentive for earnings management. Higher leverage is likely to be related to higher audit risk because earnings management increases the auditor litigation risk (Heninger, 2001). Thus, we expect a positive (negative) association between the EQ review hours and the leverage (firm performance). We calculated leverage (DEBT) by dividing total liabilities by total assets, and firm performance (ROA) by dividing net income by beginning total assets.

Palmrose (1989) finds that the audit firm type is associated with audit hours. A “Big” audit firm is likely to have sufficient knowledge, experience, and audit resources that help reduce audit-related risk. Thus, we expect that audit firm type is negatively associated with the EQ review hours. Audit firm type (BIG) is an indicator variable that takes 1 if an audit firm is affiliated with the U.S. “Big-Four” audit firms, and 0 otherwise.

The audit complexity increases as the size of accounts receivable and inventories increase. According to Simunic (1980), the valuation of receivables and inventories is a complex task and it increases audit risk. Complex audit task requires an auditor to exert more audit effort along with the increased audit fee because it increases the litigation risk (Kalelkar & Khan, 2016). Thus, we expect the size of receivables and inventories to be positively associated with the EQ review hours. We calculated the size of receivables (RECV) by dividing accounts receivable by beginning total assets, and we calculated the size of inventories (INVT) by dividing inventories by beginning total assets.

Previous EQ review literature argues that the industrial membership is an audit-related risk factor. Luehlfing et al. (1995) find that the manufacturing and financial industrial membership is negatively associated with the EQ review hours. Industrial membership (IND) is an indicator variable that takes 1 if a client is in the manufacturing industry, and 0 otherwise. 5

The characteristics of corporate governance also affect audit effort because it influences the accounting environment where the managerial discretion on financial reporting is executed. Prior studies show that the business group affiliation and the ownership by foreign investors are important corporate governance factors that affect the financial reporting environment in Korea.

Kim and Yi (2006) find that the firms affiliated with large Korean business group (so-called “Jaebeol”) manage earnings more intensively than do the nonaffiliated firms. Thus, we expect that the business group affiliation to be positively associated with the EQ review hours due to the opportunistic financial reporting behavior observed in a business group. The business group affiliation (BGROUP) is an indicator variable that takes 1 if a firm is affiliated with a large Korean business group, and 0 otherwise.

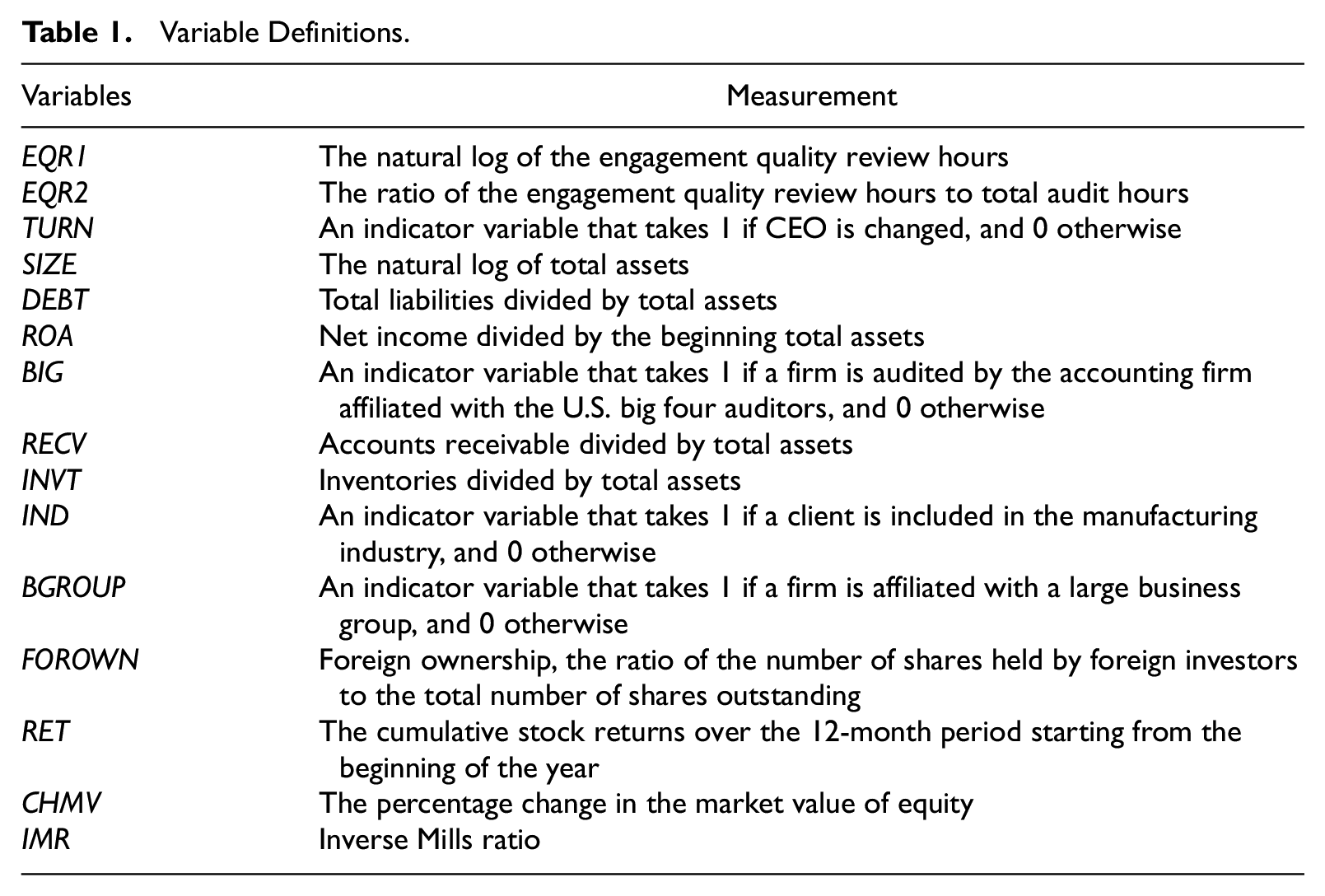

Kang and Kim (2014) stress that the equity investments by foreign investors in Korea grew rapidly in recent years and the foreign ownership significantly influences the corporate governance in Korea. To protect their own interests, foreign investors may establish both internal (e.g., board of directors) and external (e.g., external auditors) governance mechanism. As for the audit procedure, it is likely that foreign investors request high quality auditing from external auditors which increases the EQ review hours. Thus, we expect a positive association between foreign ownership (FOROWN) and the EQ review hours. Table 1 summarizes the definitions of all the variables.

Variable Definitions.

Data and Sample Selection

We analyze the financial statements data of the firms listed on the Korea Composite Stock Price Index (KOSPI) market of Korea Exchange (KRX). We use a database called KisValue which provides the financial and disclosure information of the firms listed on the KRX. We use the consolidated financial data because Korea has fully adopted the International Financial Reporting Standards (IFRS) since 2011. The data for detailed audit hours are hand-collected from the audit reports.

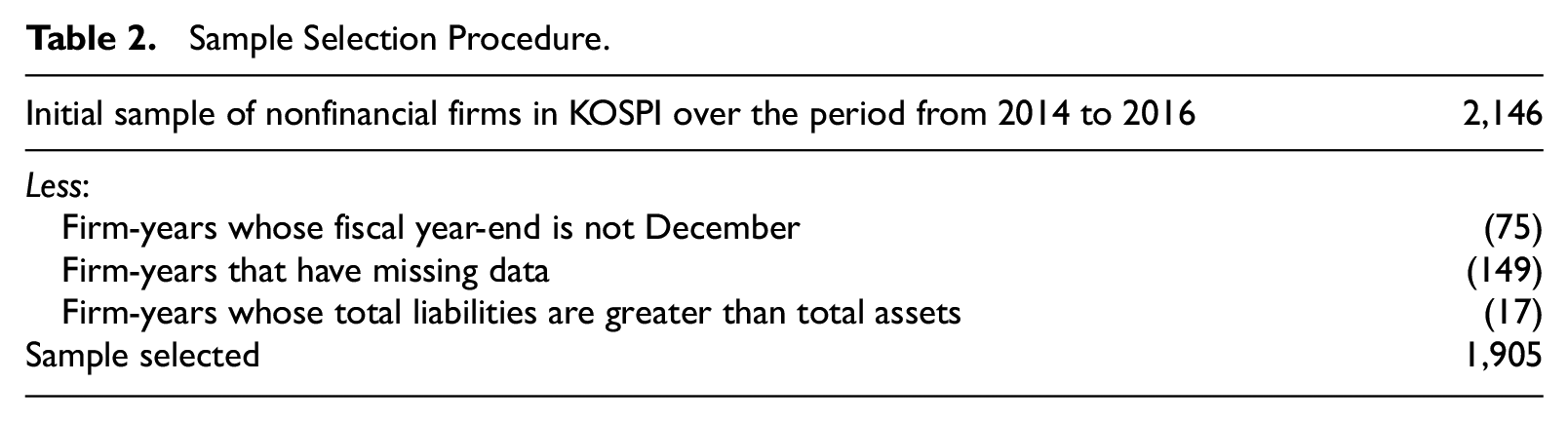

Table 2 shows the sample selection procedure. Initially, 2,146 firm-year observations in nonfinancial sectors are collected over the period from 2014 to 2016. Then, we excluded (a) the firms whose fiscal year-ends are not December (75 observations), (b) the firm-year observations with missing values (149 observations), and (c) the firm-year observations whose total liabilities are greater than total assets (17 observations). The procedure results in 1,905 firm-year observations for the analyses.

Sample Selection Procedure.

Results

Descriptive Statistics

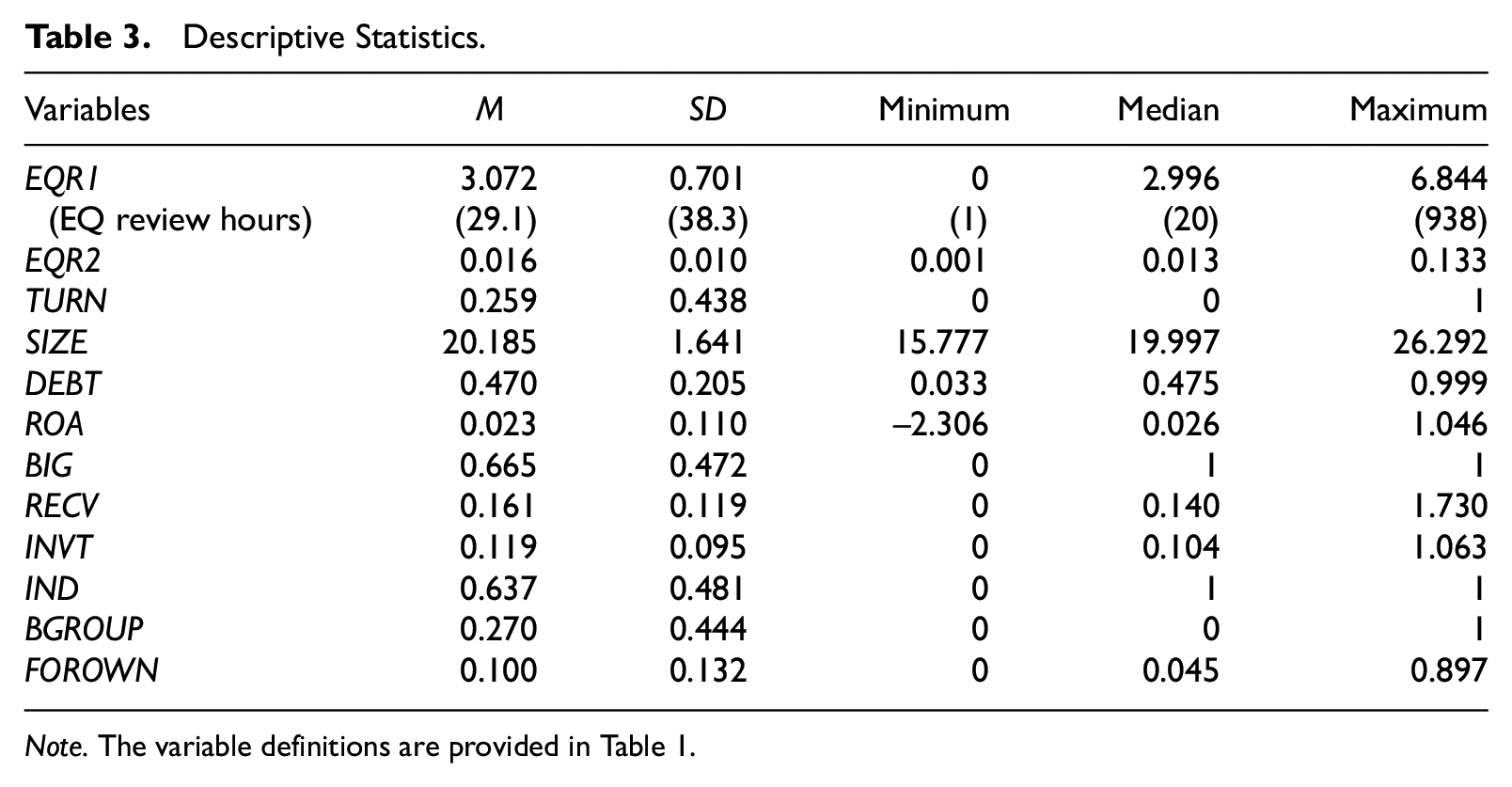

The mean value of EQR1 is 3.072, which means that the average EQ review hours are 29.1 hr. The minimum and the maximum values of EQR1 are 0 and 6.844, respectively. This means that the minimum EQ review hours are 1 hr (conducted by one reviewer) and the maximum EQ review hours are 938 hr (conducted by nine reviewers). The mean value of EQR2 is 0.016, which means that the EQ review hours are on average about 1.6% of total audit hours (i.e., the sum of the EQ review hours and the fieldwork audit hours).

The mean value of TURN shows that 25.9% of sample observations report CEO turnovers. The mean value of BIG indicates that 66.5% of sample observations are audited by Big-Four audit firms. The mean value of IND and BGROUP are 0.637 and 0.270, respectively. These values indicate that 63.7% of sample observations are classified into manufacturing industry and 27% of sample observations are affiliated with large business groups. Table 3 summarizes descriptive statistics of variables.

Descriptive Statistics.

Note. The variable definitions are provided in Table 1.

Characteristics of Accounting Accruals and Audit Hours During the CEO Turnover

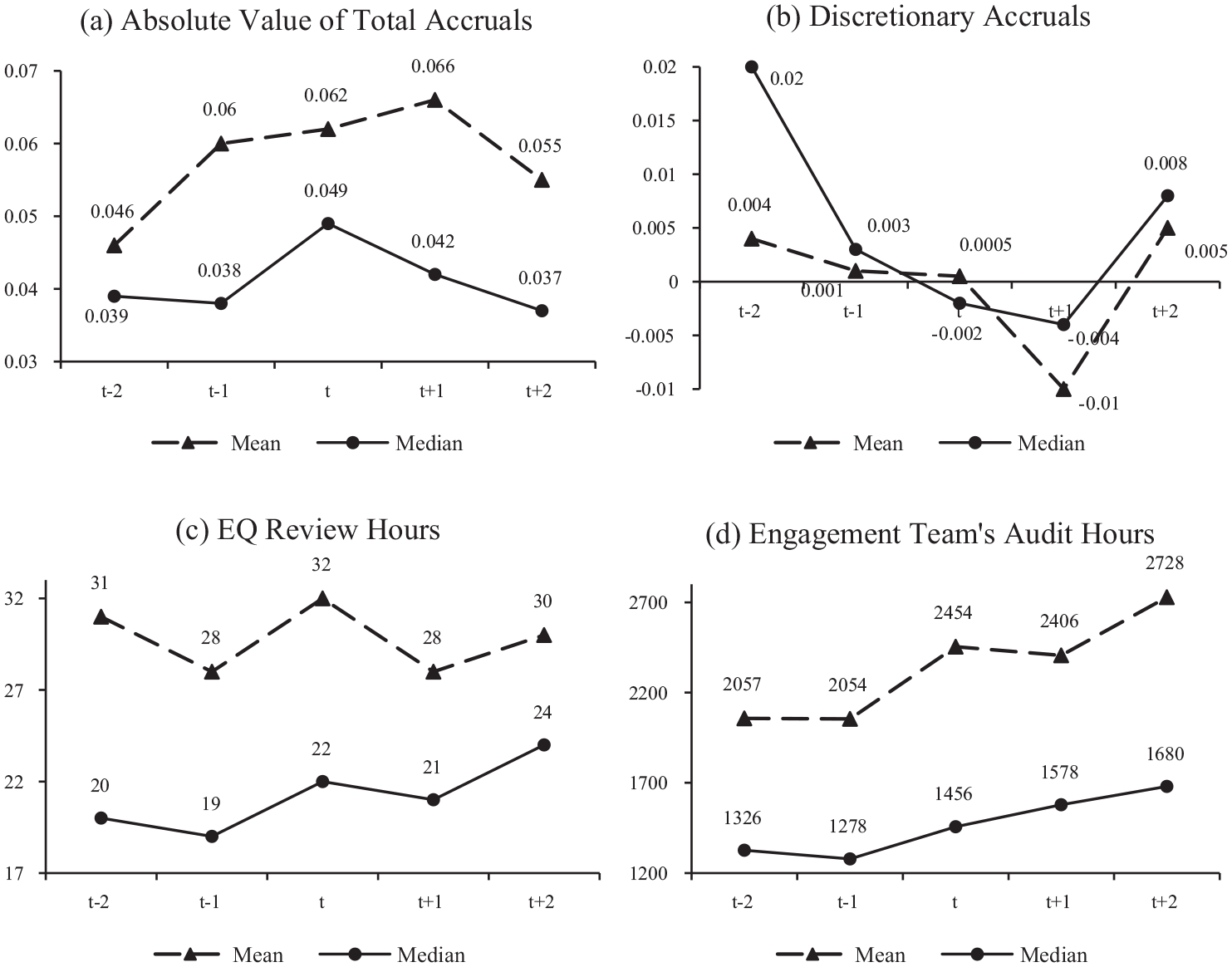

Figure 2 shows visual descriptions of the mean and the median values of accounting accruals, EQ review hours, and audit hours over time from t – 2 to t + 2 surrounding the year of the CEO turnover.

Trends of accruals and the audit efforts surrounding CEO turnover.

Figure 2a shows the change in total accruals (i.e., the absolute values of positive or negative accruals) surrounding the year of the CEO turnover. The highest mean and median values are found in t + 1 (M = 0.066) and t (median = 0.049), respectively. It means that the size of total accruals increases surrounding the CEO turnover. Figure 2b shows the change in discretionary accruals surrounding the year of the CEO turnover. In the year of CEO turnover, the mean and median values of discretionary accruals are 0.0005 and –0.002, respectively, which means that, contrary to those in other periods, the discretionary accruals in t are on average close to 0. Also, the standard deviation, minimum, and maximum values in t are 0.079, –0.249, and 0.46, respectively. Considering the increased level of total accruals in t (Figure 2a), the high standard deviation and the wide range of the level of discretionary accruals imply that the two types of reporting incentives (i.e., income-increasing vs. income-decreasing earnings management) are competing in the year of the CEO turnover. Thus, this descriptive figure indicates that separate tests for those two different types (positive vs. negative) of discretionary accruals would help understand more clearly the relation between EQ review hours and CEO turnovers.

Figure 2c shows the EQ review hours (i.e., review hours) spent by EQ reviewers surrounding a CEO turnover. The EQ review hours in t (M = 32 and median = 22) is greater than those in t – 1 or t + 1 (M = 28 and median = 19 in t – 1; M = 28 and median = 21 in t + 1). It implies that the EQ reviewers perceive the audit environment of the CEO turnover as an audit risk factor. Figure 2c shows the results of a simple trend analysis for EQ review hours without considering other factors which may affect EQ review hours. In the sections of regression analyses, we present the results of multiple regressions and provide their interpretations. Figure 2d shows the trend of the fieldwork audit hours surrounding CEO turnover. The results indicate that the engagement team’s audit hours increase over time, which implies that the fieldwork auditors perceive higher audit risk in the audit procedures after the CEO turnover.

Correlation

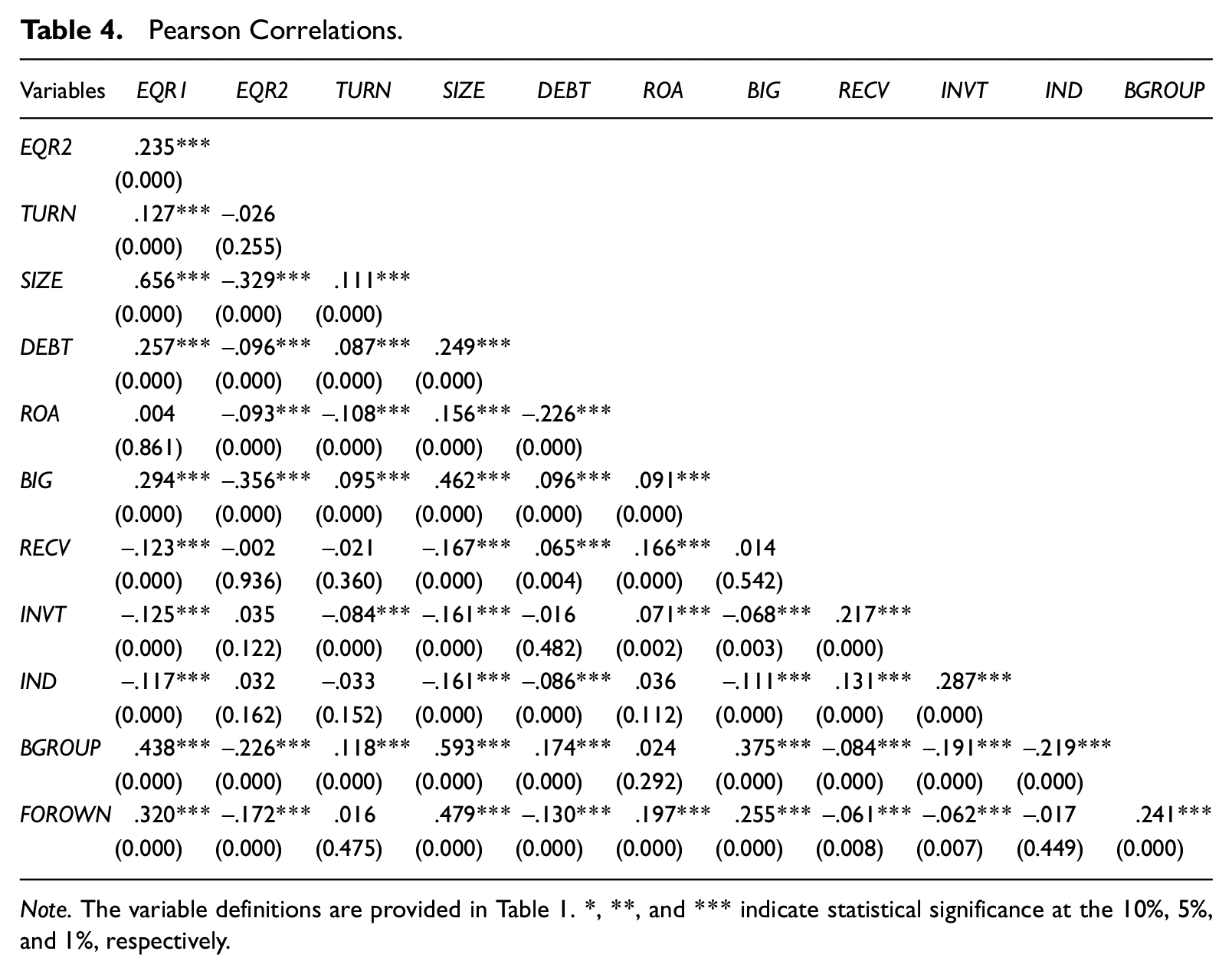

Table 4 presents the Pearson correlation coefficients among key variables. The table shows the correlations between the two alternative measures for EQ review hours and TURN in the second row. The level of EQ review hours (EQR1) is positively correlated with CEO turnovers (p < .01) whereas the ratio of EQ review hours (EQR2) is not (p = .255).

Pearson Correlations.

Note. The variable definitions are provided in Table 1. *, **, and *** indicate statistical significance at the 10%, 5%, and 1%, respectively.

The Regression Results for Testing Hypothesis

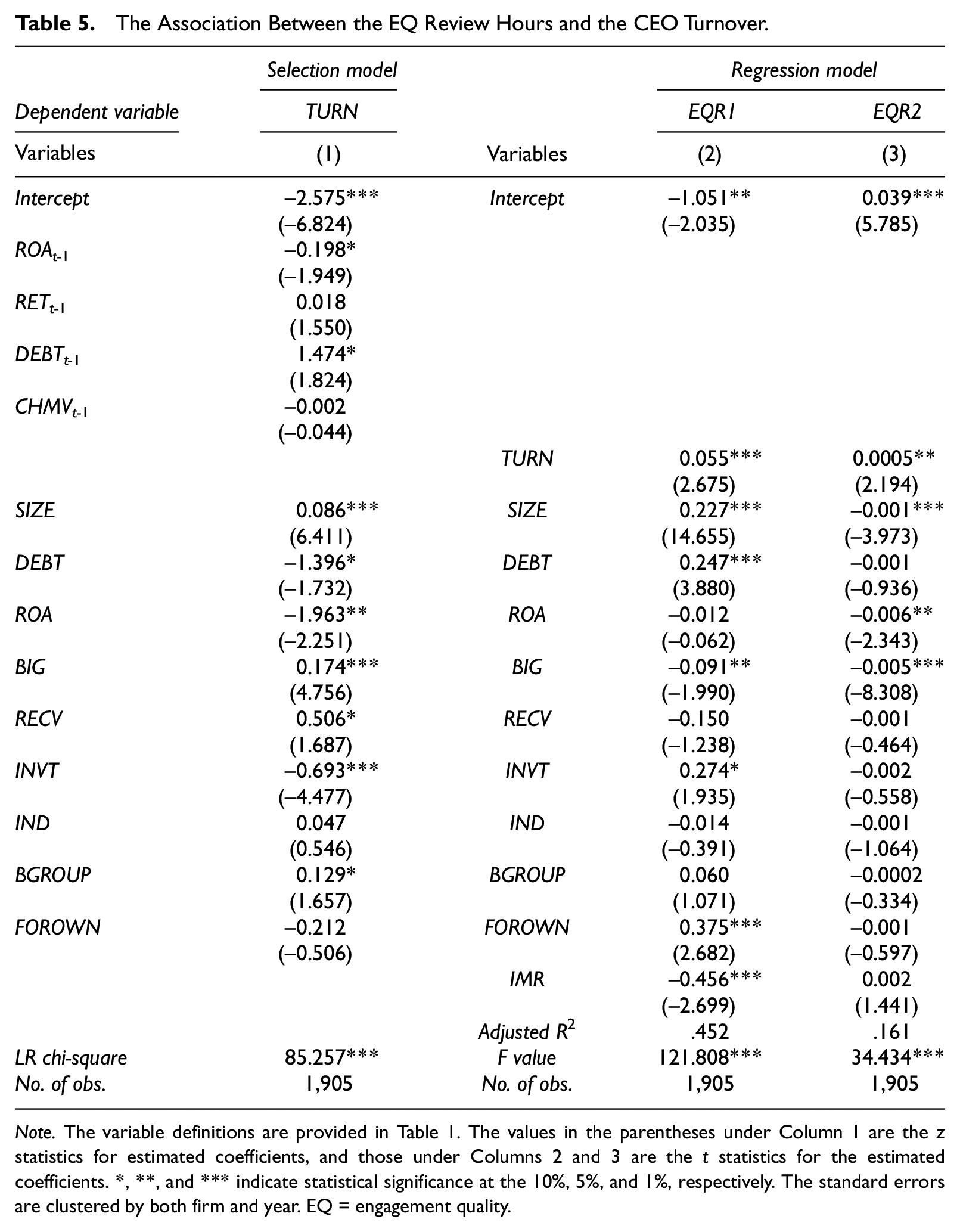

Table 5 provides the results of the regression analyses for hypothesis testing. The table shows the probit results of the selection model in Column 1 and the results for the associations between the EQ review hours and the CEO turnovers in Columns 2 and 3. The estimated coefficients on instrumental variables in Column 1 indicate that both the performance in prior period (ROAt–1) and the financial distress in prior period (DEBTt–1) are significant drivers of the CEO turnover. The coefficients of the variable TURN in both Columns 2 and 3 are positive and statistically significant (t = 2.675, p < .01 and t = 2.194, p = 0.028, respectively). This means that the EQ reviewers put audit efforts into the review process more for the clients with CEO turnovers than for the clients without turnovers.

The Association Between the EQ Review Hours and the CEO Turnover.

Note. The variable definitions are provided in Table 1. The values in the parentheses under Column 1 are the z statistics for estimated coefficients, and those under Columns 2 and 3 are the t statistics for the estimated coefficients. *, **, and *** indicate statistical significance at the 10%, 5%, and 1%, respectively. The standard errors are clustered by both firm and year. EQ = engagement quality.

The results of the variable Inverse Mills ratio (IMR) show that there is an endogeneity issue for EQR1 (the level of the EQ review hours), but not for EQR2 (the proportion of the EQ review hours). The statistically significant control variables include SIZE (+), DEBT (+), BIG (–), INVT (+), FOROWN (+) in Column 2, and SIZE (–), ROA (–), BIG (–) in Column 3. The signs of the coefficients on these variables are consistent with the prediction of the model, except for the SIZE. Specifically, the sign of the coefficient on SIZE in Column 2 is positive whereas that in Column 3 is negative. Because the measure of EQR2 contains fieldwork hours in the denominator, the results show the possibility that the fieldwork hours are increased more than the EQ review hours as the size of clients increases. The signs of the coefficients on ROA (in Column 3) and BIG (in both columns) are negative, which implies that the firm performance and the auditors’ expertise (or resources) lower the level of assessed engagement risk by the EQ reviewers. The signs of the coefficients on DEBT, INVT, and FOROWN in Column 2 are positive, which indicate that the leverage and audit complexity increase the level of engagement risk assessment, and the foreign ownership may serve as a governance mechanism leading to the increased EQ review hours.

The Signs of Discretionary Accruals and the EQ Review Hours

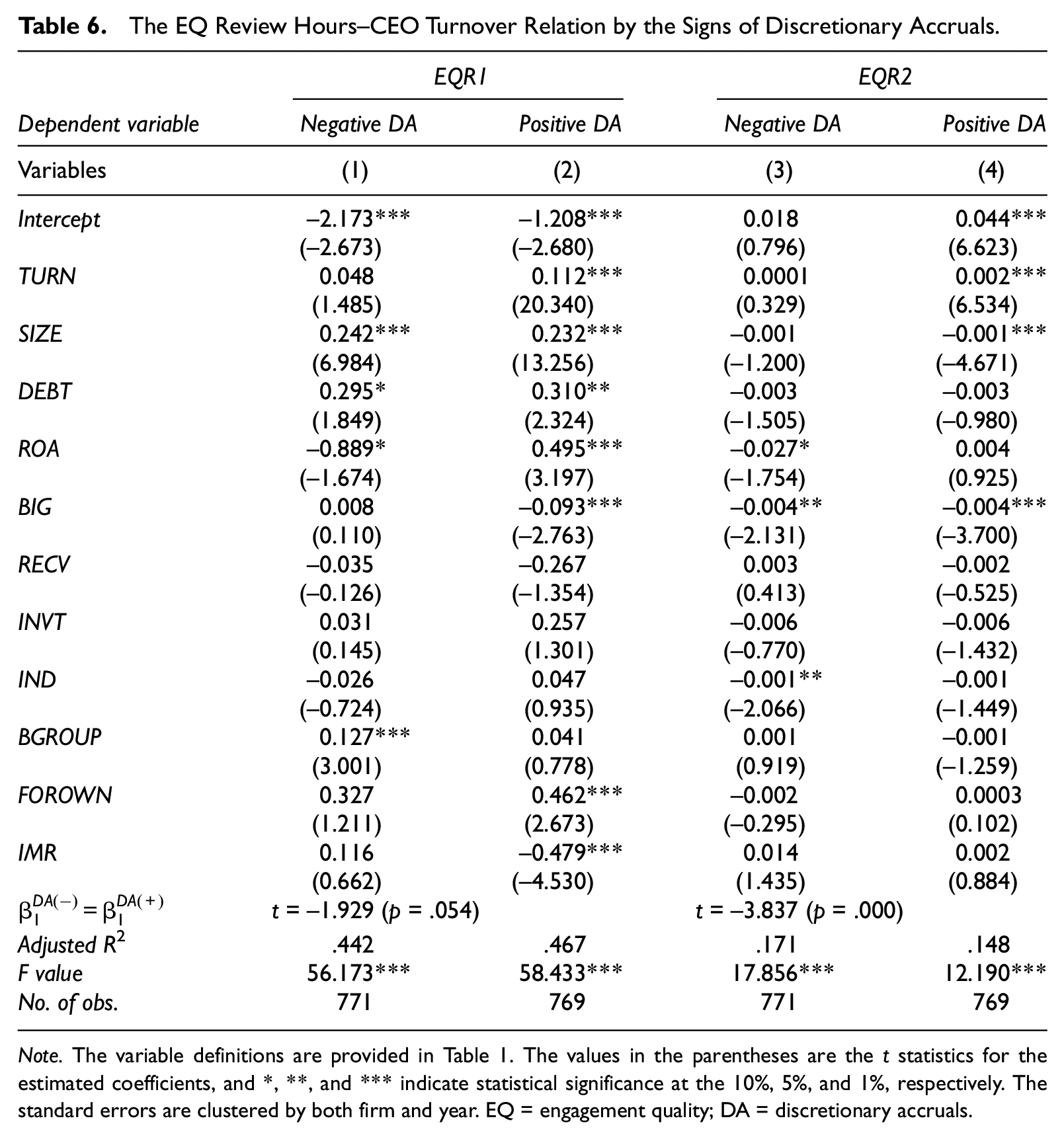

In the year of the CEO turnover, as discussed in the literature review section, two contradicting incentives for earnings management may compete: income-increasing (upward) or income-decreasing (downward) earnings management. We conduct additional analyses to investigate which incentive is more influential to the “EQ review hour–CEO turnover” relation. We examine the association between the EQ review hours and the CEO turnover by the signs of discretionary accruals. Table 6 presents the regression results of the EQ review hours (EQR1 and EQR2) on CEO turnovers (TURN) by the signs of discretionary accruals.

The EQ Review Hours–CEO Turnover Relation by the Signs of Discretionary Accruals.

Note. The variable definitions are provided in Table 1. The values in the parentheses are the t statistics for the estimated coefficients, and *, **, and *** indicate statistical significance at the 10%, 5%, and 1%, respectively. The standard errors are clustered by both firm and year. EQ = engagement quality; DA = discretionary accruals.

The results show that the EQR1–TURN relation is statistically significant (insignificant) in the group of positive (negative) discretionary accruals. The coefficient on TURN, β1, in Column 2 is greater than that in Column 1, and the difference of the coefficients on β1 between the two groups is statistically significant (p = .054). The results indicate that the EQ reviewers perceive the upward bias in the fieldwork auditors’ collected evidence and conclusions as riskier than the downward bias (potentially because of the litigation risk), and as a result, the EQ reviewers put more efforts into reviewing the engagement team’s works when earnings are managed upward. The insignificant results for the negative discretionary accruals may be interpreted in line with accounting conservatism. Roychowdhury and Watts (2007) argue that conservative accounting is one of the efficient means in reducing the agency problem that comes from information asymmetry. The conservatism may serve as mechanism to prevent the potential problems arising from overstated earnings by reflecting instantaneously bad news (i.e., expected losses) into financial reports. The EQ reviewers may expect the mechanism of accounting conservatism to play a role in reducing the audit risk on the works of the fieldwork auditors, and as a result, they pay less attention to the fieldwork auditors’ works when earnings are managed downward.

The Columns 3 and 4 report the regression results of EQR2 on TURN, and the results are similar to those in Columns 1 and 2. The coefficient on TURN is positive and significant only in the group of positive discretionary accruals (Column 4) while it is not statistically significant in the group of negative discretionary accruals (Column 3). The test for the difference in the coefficients on TURN between the two groups indicates that the difference is also strongly significant (p < .01). Overall, the findings in Table 6 indicate that the “EQ review hour–CEO turnover” relation is more pronounced when there is an income-increasing earnings management rather than when there is an income-decreasing earnings management.

Forced Versus Non-Forced CEO Turnover

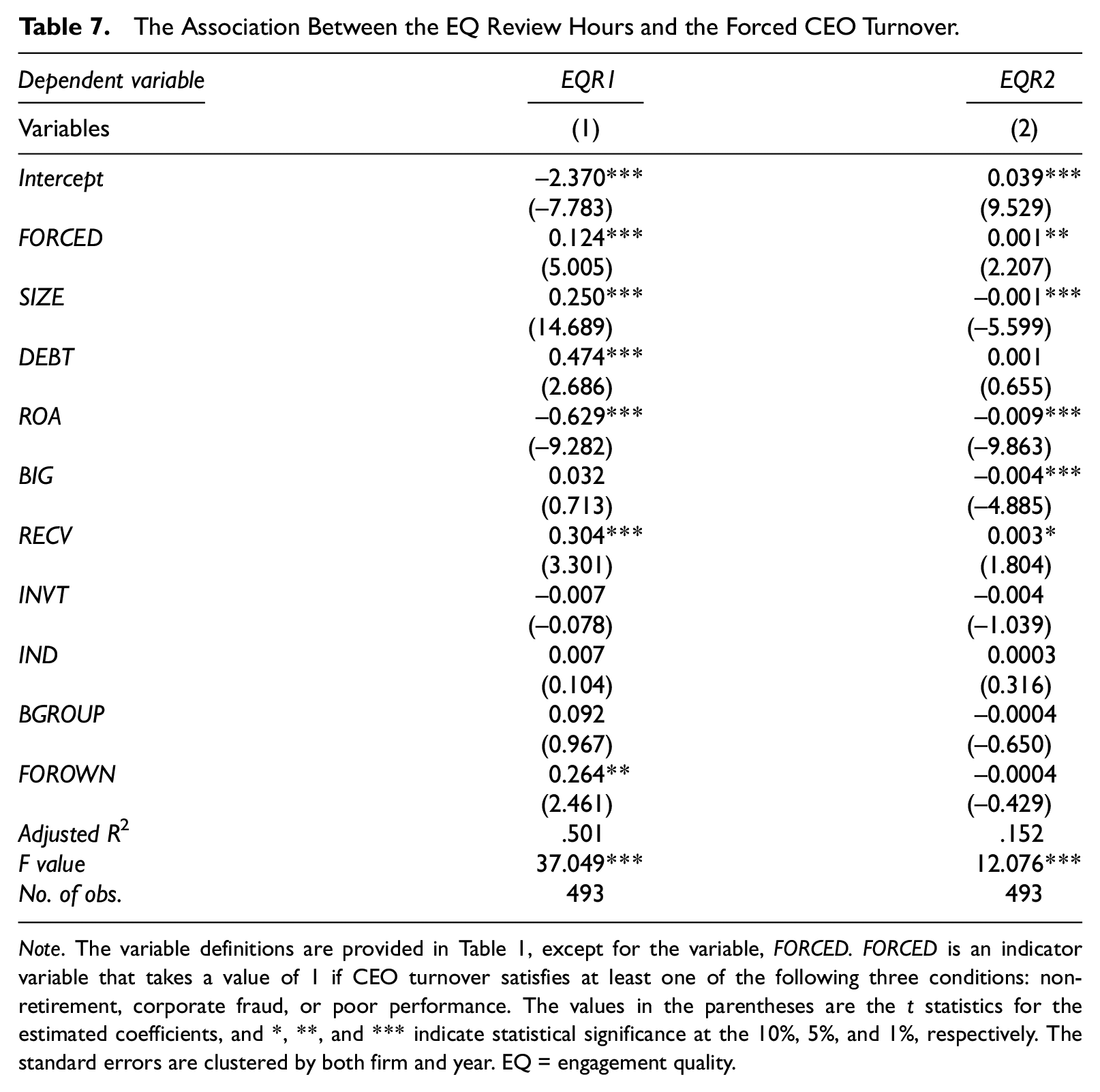

The literature shows that the forced CEO turnover brings more drastic changes in business and accounting environment than does the non-forced CEO turnover (Huang et al., 2014). Such drastic changes make the EQ reviewers to perceive the level of risks on the fieldwork auditors’ works as high and, in turn, it is expected that the EQ reviewers increase their review hours.

Similar to Huang et al. (2014), we define a CEO turnover as a forced turnover if at least one of the following three reasons are satisfied: (a) non-retirement, (b) corporate fraud, or (c) poor performance. Following the retirement age bracket (i.e., 64–66 years) by Jenter and Lewellen (2015), we consider that the non-retirement condition is satisfied if the age of outgoing CEOs is below the retirement age bracket. Following the suggestions of Huang et al. (2014), we consider that the corporate fraud condition is satisfied if an asset misappropriation, breach of trust, or accounting manipulation is disclosed in a timely disclosure report either in the current period or in the previous period. 6 Finally, we consider the poor performance condition is satisfied if a negative operating income (or negative change in operating income) is reported in the period prior to a CEO turnover. The forced CEO turnover (FORCED) is an indicator variable that takes 1 if at least one of the three conditions mentioned above is satisfied, and 0 otherwise.

Table 7 reports the regression results of EQR1 and EQR2 (the EQ review hours) on FORCED (forced vs. non-forced CEO turnover). The results show that the relation between the EQ review hours and the indicator variable for forced CEO turnovers is positive and statistically significant for both EQR1 and EQR2 (t = 5.005, p < .01 and t = 2.207, p = .028, respectively). These results indicate that the EQ reviewers put more efforts in their review process when the CEO turnovers are involuntary, which is consistent with the implication of Huang et al. (2014).

The Association Between the EQ Review Hours and the Forced CEO Turnover.

Note. The variable definitions are provided in Table 1, except for the variable, FORCED. FORCED is an indicator variable that takes a value of 1 if CEO turnover satisfies at least one of the following three conditions: non-retirement, corporate fraud, or poor performance. The values in the parentheses are the t statistics for the estimated coefficients, and *, **, and *** indicate statistical significance at the 10%, 5%, and 1%, respectively. The standard errors are clustered by both firm and year. EQ = engagement quality.

Conclusion

After experiencing many audit failures in the early 2000s that lead to enormous economic losses, scholars and practitioners start recognizing the importance of establishing the quality control policies and procedures within audit firms at both firm and engagement levels. For the engagement-level quality control, prior studies have well documented how valuable the EQ review is and what the EQ reviewers should do in the review process to achieve the accuracy and integrity of financial reporting. However, little empirical research has been done to investigate how the EQ reviewers respond to the expected potential audit risk partly due to the difficulty of obtaining real-life detailed audit data (e.g., the confidentiality issues).

In South Korea, since 2014, The Act on External Audit of Stock Companies requires firms to disclose the detailed audit hours on the audit report including the EQ review hours and the engagement team’s fieldwork hours. Huang et al. (2014) argues that the CEO turnover is one of the most important audit risk factors, but it has been neglected in the field of audit research. In this regard, this article empirically examines the response of EQ reviewers to the increased audit risk caused by the CEO turnover.

The results are consistent with the prediction by the theory on the EQ review. The EQ review hours are positively associated with the CEO turnovers, which means that the EQ reviewers provide more audit efforts into the review process in response to the increased audit risk caused by the CEO turnover. Additional analyses indicate that the EQ reviewers respond more to an income-increasing earnings management than to an income-decreasing earnings management, and they perceive the audit risk to be higher when there is an involuntary CEO turnover than a voluntary CEO turnover.

The article extends the existing literature of descriptive or analytic discussions on the EQ review process by providing empirical evidence based on the unique actual data on EQ review hours. The article also enhances the understanding on how the engagement-level quality control works in the volatile audit environment such as top executive turnovers. Because the results of the article are based on the sample of 1,905 observations over the 3-year testing period, however, a caution is needed before generalizing the results.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.