Abstract

Drawing on prior literature on audit fees, client reputation, and corporate governance, we posit that a material adverse event at a firm, such as a financial fraud allegation, leads to an increase in the audit fees of firms connected to the former by a board interlock. We propose two possible mechanisms to explain the upward pressure on audit fees: a client-side effect, where the client demands additional audit services, and an auditor-side effect, where the auditor raises its audit fees due to a perceived increase in audit engagement risk. The results indicate an average marginal increase of 12.86% in audit fees in the year following the public revelation of financial fraud. Additional analyses suggest that an auditor-side effect is in place, while we cannot find clear evidence supporting the client-side effect. Furthermore, we document that the positive effect on audit fees persists for up to at least 2 years after public disclosure of the event when the interlocked director serves as a member of the audit committee.

Introduction

Board interlocks occur when the same director sits simultaneously on the boards of two firms. 1 This study addresses whether audit fees increase following financial fraud allegations at firms to which the audit client is connected by a board interlock. Extant research (Fich & Shivdasani, 2007; Kang, 2008; Srinivasan, 2005) reports that if a firm or its executives allegedly engaged in manipulations of financial information, investors penalize not only the fraudulent firm but also firms in its board network. This evidence suggests that investors tend to attribute the incidence of financial fraud to lax board monitoring and perceive it as a signal of potential irregularities or inadequate corporate governance at connected firms as well. 2

While prior research provides strong empirical evidence that investors penalize firms merely because they are connected by a board interlock to an alleged fraud perpetrator, to our knowledge, there is no direct evidence on whether connected firms experience longer-lasting economic effects due to their interlocks with a fraudulent firm, neither is there evidence on the mechanisms through which such effects take place. Our article sheds light on this issue by investigating whether firms’ audit fees increase following financial fraud allegations at a connected firm. We propose two mechanisms that could apply upward pressure on audit fees. First, auditors could adjust their assessment of engagement risk if a firm’s board member also serves on the board of a fraudulent firm. We argue that evidence of possible law violation at an interlocked firm could be taken as an indicator of board failure; that is, if a specific board member is not serving effectively at one firm, that individual might not be serving effectively at the other firms either. In addition, the auditors might be concerned that questionable practices transferred from the scrutinized firm to connected non-fraudulent firms, in line with studies on contagious behavior (e.g., Bizjak et al., 2009; Chiu et al., 2013; Davis, 1991). Such concerns could lead to an upward reassessment of perceived client risk and, consequently, to greater audit effort and higher audit fees. Finally, auditors face litigation and reputation risk in case of audit failure (e.g., Bar-Yosef & Sarath, 2005). If the involvement of a firm’s director in financial fraud at a different firm increases the perceived risk of the engagement, auditors might charge the client a higher litigation premium.

Second, board members involved with the fraudulent firm could demand more audit services from the auditor of the interlocked firm. Carcello et al. (2002) suggest that high-quality boards require greater audit quality to protect their reputation capital and enhance accounting quality assurance. In addition, theoretical (Fama & Jensen, 1983) and empirical research (Brochet & Srinivasan, 2014; Fich & Shivdasani, 2007; Srinivasan, 2005) suggests that poor monitoring results in labor market penalties for directors. While failure to prevent and detect financial fraud at one firm hurts a director’s reputation, involvement with a second fraudulent firm could be detrimental for the director’s career prospects. Hence, we argue that interlocking directors have incentives to demand more auditing to mitigate the reputational penalties due to their position at a fraudulent firm by preventing questionable behavior at the connected firm.

Our main prediction is that a material adverse event such as allegations of financial fraud at a firm is associated with higher audit fees for firms connected to the former by board interlocks.

We use enforcement actions initiated by the U.S. Securities and Exchange Commission (SEC) in the period between 1999 and 2014 to proxy for financial fraud. Our main sample consists of 580 firm-year observations related to 290 unique firms connected through 208 directors to 107 firms investigated by the SEC for alleged violations related to reporting and disclosure issues. 3 We find support for the hypothesis that the revelation of financial fraud is associated with an increase in audit fees. Specifically, we document a 12.86% increase in audit fees, on average, in the year following the revelation of financial fraud at a connected firm with respect to the year before the announcement, after controlling for a battery of audit fee determinants and industry and year fixed effects. We gauge the sensitivity of our results to different model specifications, to the use of different proxies for some of our variables, and to the inclusion of additional control variables. In all cases, the results remain qualitatively unchanged. Furthermore, to address the concerns that the results are driven by time trends or other factors that could be affecting the audit fees of both the interlocked firms and their peers, we supplement our main tests with a matched-sample analysis. While the audit fees of the interlocked firms and the matched control firms are not significantly different in the year before the event, the audit fees in the year after the event are about 10.63% higher for the sample of interlocked firms providing further support to the hypothesis that connections to fraudulent firms exert an upward pressure on the audit fees of the connected firms. We next document that the increase in audit fees is greater for those cases where the interlocking director is a member of the audit committee of either the fraud or the connected firm, or both.

Such documented increase in audit fees is consistent with both an auditor-driven (supply- driven) and a client-driven (demand-driven) mechanism. To better understand the drivers of the increase in audit fees, we carry out three tests aimed at verifying whether an auditor-driven or a client-driven mechanism is likely in place. The first test is based on whether directors resigned preemptively from the fraud company. The rationale behind this test is that directors who resign are likely those who are most concerned about reputation and career, as suggested by prior literature (e.g., Fahlenbrach et al., 2017; Gao et al., 2017). If a client-side mechanism is in place, we expect that audit fees increase more when the interlocking directors preemptively resign. The results do not provide supporting evidence to this expectation. A second test explores the role of gender. Based on prior literature, we expect female interlocking directors to be the most concerned about reputation risk and, therefore, the most likely to demand higher audit quality. This test does not provide support to a client-driven mechanism either. Finally, prior studies (e.g., Carcello et al., 2002; Hay et al., 2008; Knechel & Willekens, 2006) suggest that corporate governance quality is positively associated with audit fees. Hence, a client-driven mechanism would predict that the increase in audit fees is more pronounced for firms with strong corporate governance. We do not find evidence that the increase in audit fees is greater for better governed firms. Instead, we observe the opposite effect—strong corporate governance mechanisms seem to be associated with a lower increase in audit fees. All in all, while we cannot directly differentiate between the two mechanisms, our results are more consistent with an auditor-driven mechanism. 4 In addition, we document significantly higher probability of modified opinions for the interlocked firms after the event, providing some evidence for increased audit effort. Finally, we investigate the persistence of the increase in audit fees. Our results indicate no significant increase in audit fees 2 years after the financial fraud becomes publicly known indicating that the effect is likely transient. However, we find that for the subsample of firms whose director serves on the audit committee of either firm, the effect persists for at least 2 years after the event.

This study contributes to the extant literature in two main ways. First, we contribute to studies on the real effects of connections to allegedly fraudulent firms (e.g., Fich & Shivdasani, 2007; Srinivasan, 2005). Our results indicate that connected firms experience higher audit fees following the revelation of financial fraud, in particular when the interlocked director serves on the audit committee of either or both firms. Second, the study contributes to the literature on the effects of board interlocks on audit outcomes (e.g., Johansen & Pettersson, 2013). To the best of our knowledge, it is the first study to provide direct evidence that material adverse events at companies connected by a board interlock impact a firm’s audit fees.

The remainder of the article is organized as follows. The next section provides background information regarding SEC enforcement actions. We then review the literature on board interlocks and the determinants of audit fees followed by a discussion of our methodology. We next report the results of the analysis, sensitivity checks, and additional analyses. The final section concludes.

SEC Enforcement Actions

In this article, we use the SEC enforcement actions as a proxy for likely financial fraud. Prior studies (e.g., Beasley, 1996; Farber, 2005; Feroz et al., 1991; Files, 2012) suggest that the SEC has limited resources and cannot investigate every potential financial reporting violation and therefore focuses instead on high-profile cases that are likely to lead to sanctions. Generally, the initiation of an SEC investigation is triggered by a specific event, such as a restatement, an unexpected executive or director turnover, or an auditor’s resignation (Karpoff et al., 2008a, 2008b) The SEC first initiates an informal inquiry, which typically constitutes a detailed review of the firm’s financial statements. The inquiry is upgraded to a formal investigation upon uncovering evidence of potential wrongdoing. The investigation period can span several years. 5 Upon completion of the case, the SEC issues a litigation release (LR) and/or administrative proceeding (AP), which could be given a secondary designation of Accounting and Auditing Enforcement Release (AAER) if it involves accountants (or auditors) and/or could be of interest to accountants (or auditors). Therefore, SEC enforcement action releases capture likely financial fraud cases. Restricting the sample to these cases reduces the risk of scope limitations and extraneous event biases embedded in other commonly used misconduct databases such as the Government Accountability Office’s restatement data (Karpoff et al., 2017). In addition, SEC allegations of financial fraud are indicative of corporate governance failure, which could have a negative impact on connected firms’ market value (e.g., Kang, 2008). Hence, they represent a suitable setting for the purposes of this study.

Prior Literature and Hypothesis Development

Our study builds on the literature on the spillover effects arising from board connections and the literature on the determinants of audit fees.

Role of Board Interlocks on Firm Behavior and Reputation

Early research in organizational sociology suggests that board interlocks are an important conduit for information transfer that affects organizational practices, norms, values, and corporate policies (Mariolis & Jones, 1982). Board interlocks with more prominent firms serve as a signaling mechanism and help less visible firms build their reputation (Certo, 2003; Mizruchi, 1996). Prior research has also explored the role of board interlocks on the spread of corporate practices such as stock-option backdating and expensing (Bizjak et al., 2009; Reppenhagen, 2010), disclosure (Cai et al., 2014; Chan et al., 2017), and tax avoidance (Brown & Drake, 2014). Taken as a whole, these studies provide evidence that board interlocks are a powerful source of information that can influence firms’ corporate reputation, practices, and behavior. An emerging body of literature analyzes the effect of material adverse events at a firm on the market value of firms connected by a board interlock, documenting a negative investor reaction, which indicates negative reputation spillover effects. For example, Fich and Shivdasani (2007) report that, if a firm is subject to a class action lawsuit for financial misrepresentation, connected firms experience negative abnormal market reactions even if they are not directly involved in or associated with any misstatement or other wrongdoing. Similarly, Kang (2008) argues that the negative reputation effect following the announcement of SEC investigation spills over to interlocked firms in the form of negative stock market reactions. Drawing on signaling and attribution theory, the author suggests that investors tend to attribute behaviors such as financial manipulations to internal causes (e.g., the quality of the board) rather than to situational factors, thus holding the board members responsible for failing to prevent financial fraud. The negative reputation spills over to interlocked firms and creates uncertainty about their corporate governance quality and effectiveness.

Engagement Risk and Audit Fees

Firms’ external auditors play a key role in validating the integrity of reported financial information. Numerous studies have advanced our understanding on the determinants of audit effort and, more specifically, audit fees. 6 Much of the research on audit fees is influenced by the seminal work of Simunic (1980) and is concerned mainly with the auditor- and client-specific characteristics that affect audit fees, such as client size and complexity. There is also evidence that audit fees are positively related to the perceived risk of the audit engagement (e.g., Bell et al., 2001; Gietzmann & Pettinicchio, 2014; Hogan & Wilkins, 2008; Lyon & Maher, 2005; Morgan & Stocken, 1998; Raghunandan & Rama, 2006; Seetharaman et al., 2002). Engagement risk consists of three separate components: (a) the client’s business risk; that is, the risk that certain events and circumstances can adversely affect firm operations and performance (American Institute of Certified Public Accountants [AICPA], 2014, AU 315.04); (b) audit risk; that is, the risk that the auditor might fail to detect a material misstatement in the client’s financial statements and modify the audit opinion accordingly (AICPA, 2006, AU 312.02); and (c) the auditor’s business risk, which includes litigation risk, the risk of reputation loss, and the risk of sanctions by regulatory bodies such as the SEC (Brumfield et al., 1983). Higher audit fees are justified by a higher risk of error, which requires more extensive and specialized procedures.

The client’s reputation is also an important factor in determining audit fees. Asthana and Kalelkar (2014) examine the effect of “improved” client reputation on audit fees. They use inclusion in the S&P 500 index as a proxy for improved reputation and observe that audit fees are discounted when firms enter the index but increase upon exit. In addition, Jha and Chen (2015) provide evidence that firms headquartered in high social capital counties pay lower audit fees. They suggest that a firm’s location can be an indicator of the trustworthiness of the management and the integrity of its financial reporting.

Connections to Fraudulent Firms and Audit Fees

In this article, we investigate the effect of adverse material events at one firm on the audit fees of firms in its board network. We base our expectations on studies in accounting, finance, and management that document the presence of reputation spillover effects to interlocked firms when the focal firm is allegedly involved in financial fraud (Fich & Shivdasani, 2007; Kang, 2008; Srinivasan, 2005), studies on the effect of client reputation and engagement risk on audit fees (e.g., Asthana & Kalelkar, 2014; Lyon & Maher, 2005), and the literature on the relation between corporate governance and the demand for audit services (Carcello et al., 2002; Hay et al., 2008; Knechel & Willekens, 2006; Zaman et al., 2011). We propose two main mechanisms that could drive the effect of material adverse events on audit fees: an auditor-side mechanism (i.e., the auditor adjusts audit fees to reflect increased engagement risk) and a client-side mechanism (i.e., the client requests more audit services, which results in higher audit fees).

First, we argue that auditors have incentives to adjust their assessment of audit engagement risk and increase their fees if a client is connected to a fraudulent firm. Financial fraud allegations indicate corporate governance failure and can hurt the reputation of involved executives and directors (Karpoff et al., 2008a). If board members were not successful at preventing fraud at one firm, then they might not serve effectively as monitors also at the other firms on whose board they sit. This is even more true when the board members are part of the audit committee, whose interlocks have been associated with poor financial reporting quality in prior literature (e.g., Sharma & Iselin, 2012; Tanyi & Smith, 2015). Auditors might be especially concerned about such a possibility because prior studies indicate that they face both litigation and reputation penalties in case of audit failure (e.g., Beasley et al., 1999, 2010; Feroz et al., 1991). Indeed, Beasley et al. (2010) report that, in 23% of the AAER cases between 1998 and 2007, the audit firm was also sanctioned. In addition, studies on auditor’s reputation suggest that, in case of audit failure, the reputational penalties are considerably greater than the litigation risk (Irani et al., 2015; Skinner & Srinivasan, 2012). Thus, auditors have strong incentives to ensure the financial reporting integrity of connected firms to reduce the probability of audit failure. If external auditors suspect that the monitoring at an interlocked firm is compromised, they would spend more hours and effort in auditing the firm’s financial statements to reduce the risk of audit failure, which would be reflected in higher audit fees. 7 This is also consistent with the arguments of prior literature that auditors plan the engagement and price their services based on a critical assessment of the client’s risk (e.g., Bell et al., 2001; Gietzmann & Pettinicchio, 2014; Johnstone & Bedard, 2003; Lyon & Maher, 2005; Morgan & Stocken, 1998) and reputation (Asthana & Kalelkar, 2014; Jha & Chen, 2015).

Second, it is possible that the client demands additional audit services, which results in higher audit fees. Research in organizational reputation and legitimacy suggests that board connections to reputable firms serve as a signaling mechanism to potential investors and business partners (e.g., Certo, 2003; Mizruchi, 1996). However, connections to a fraudulent firm could hurt organizational reputation and provide connected firms with incentives to mitigate the perceived reputational damage. These reputation concerns are likely to be even stronger for interlocking board members. Prior studies suggest that board members are often held accountable (Brochet & Srinivasan, 2014) and incur substantial labor market penalties (Fich & Shivdasani, 2007; Srinivasan, 2005) following material adverse events at a firm on whose board they serve. While directors generally do not lose all outside appointments following corporate financial fraud allegations at one firm, any subsequent involvement with a fraudulent firm could be detrimental to their careers. 8 Thus, we argue that the reputational concerns of interlocking directors will motivate them to demand additional audit services to reduce the risk of fraudulent behavior and protect their own and the connected firm’s reputation (Carcello et al., 2002; Hay et al., 2008; Knechel & Willekens, 2006; Zaman et al., 2011).

Taking into account both the auditor- and the client-side mechanisms, we expect a firm connected to an allegedly fraudulent firm to pay higher audit fees after the revelation of accounting fraud at a connected firm. More formally, this hypothesis is stated in its alternative form as follows.

Data and Research Design

Sample and Data

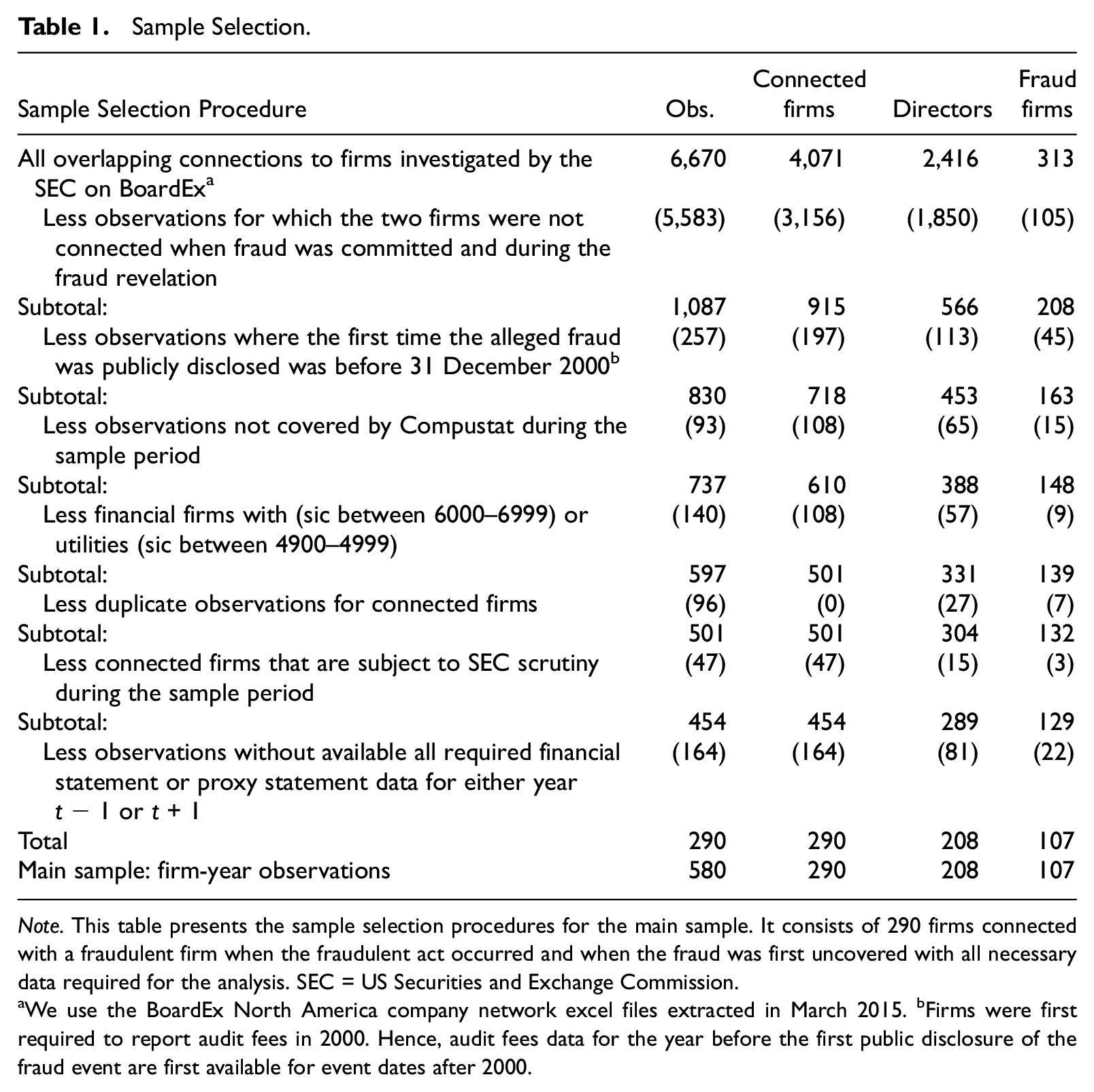

We follow a two-step procedure to select our sample. As a first step, we identify all firms that have been subject to SEC enforcement actions classified by the SEC as related to issuer financial statements and reporting. 9 In total, we find 2,215 LRs, APs, and AAERs that the SEC has classified as such between 1999 and 2014. 10 These cases generally involve violations of federal securities laws, such as premature revenue recognition, the misstatement of assets and liabilities, under/overstating expenses, and misleading disclosures. We limit our analysis to these cases because they involve the issuance of misleading or fraudulent financial reports and are violations that could and should have been prevented and detected by the firm’s board members and would be of interest to the firm’s external auditors. We focus only on the first release regarding a specific event and eliminate subsequent related releases. In addition, we eliminate cases that do not involve violations of Generally Accepted Accounting Principles (GAAP), such as sanctions against auditors for lack of independence or noncompliance with Public Company Accounting Oversight Board (PCAOB) rules, violations of the Foreign Corrupt Practices Act, and cases involving subsidiaries resulting in a sample of 607 unique firm events. 11 Related board network information on overlapping connections to firms with Compustat identifier (gvkey) is available from BoardEx for 313 firms. 12

As a second step, we identify the board networks of the allegedly fraudulent firms using detailed information available from BoardEx. We further restrict the sample to network connections where the interlocking individual serves on the boards of both firms at the same time during the fraud period—that is, when the bad act occurs—and when the bad act is revealed. This sample selection procedure ensures that we capture individuals whose oversight failed to prevent the bad act from occurring in the first place and who have the opportunity to influence connected firms’ audit fees after the revelation of the alleged fraud through both the client- and the auditor-side mechanisms. 13 We eliminate observations where the alleged fraud is disclosed for the first time before December 31, 2000, because firms were not required to disclose their audit fees prior to 2000, and firms not covered by Compustat North America during the sample period. Consistent with prior research on the determinants of audit fees (e.g., Krishnan & Wang, 2015), we eliminate connected firms that operate in the financial services industry (Standard Industrial Classification, or SIC, codes 6000–6999) and utility firms (SIC codes 4900–4999). We ensure no duplicate observations in terms of connected firms—that is, each connected firm enters our sample the first time it is connected to a firm investigated by the SEC—because we expect that subsequent connections to allegedly fraudulent firms could have different implications for the firm’s and auditor’s decision making. 14 Furthermore, we drop connected firms that are subject to SEC scrutiny during the sample period to reduce the risk of spurious correlations due to their own poor financial reporting rather than a board connection to an allegedly fraudulent firm. Data on audit fees and internal control problems are hand-collected from firms’ proxy statements (form DEF 14A) and annual financial reports (forms 10-K and 10KSB) available through SEC’s EDGAR. We require each firm in the sample to have all the financial and audit fee data required for the analysis for both the year before and the year after the event. The final sample for our main analysis consists of 580 firm–year observations related to 290 unique firms connected to 107 fraudulent firms through 208 interlocking directors. Table 1 presents the collection procedure for this sample.

Sample Selection.

Note. This table presents the sample selection procedures for the main sample. It consists of 290 firms connected with a fraudulent firm when the fraudulent act occurred and when the fraud was first uncovered with all necessary data required for the analysis. SEC = US Securities and Exchange Commission.

We use the BoardEx North America company network excel files extracted in March 2015. bFirms were first required to report audit fees in 2000. Hence, audit fees data for the year before the first public disclosure of the fraud event are first available for event dates after 2000.

Variables

To test our hypothesis, we collect data on audit fees for the firms in the connected firm sample in the 2-year window around the first public disclosure of the alleged financial fraud and use the logarithmic transformation of audit fees (AUDIT_FEE) as our dependent variable. The main independent variable is Y1, which is one for all observations in year t + 1 and zero in year t − 1. Year t is the year in which the fraud first becomes revealed, which is the earliest of the SEC investigation disclosure, the restatement (if any), or the class action lawsuit filing (if any). To identify the earliest date when information about the financial fraud first becomes publicly available, we utilize several sources. First, we search the company’s annual and quarterly reports and LexisNexis for the company’s press releases or articles in the business press indicating that the allegedly fraudulent company is investigated by the SEC. Second, we collect data on class action lawsuit filings available through the Securities Class Action Clearinghouse provided by Stanford Law School. Third, we utilize data on restatements. Based on these different sources, we use the earliest revelation of financial fraud to identify year t. 15 Figure 1 in the Online Appendix illustrates a typical SEC enforcement action and provides further details on our identification strategy.

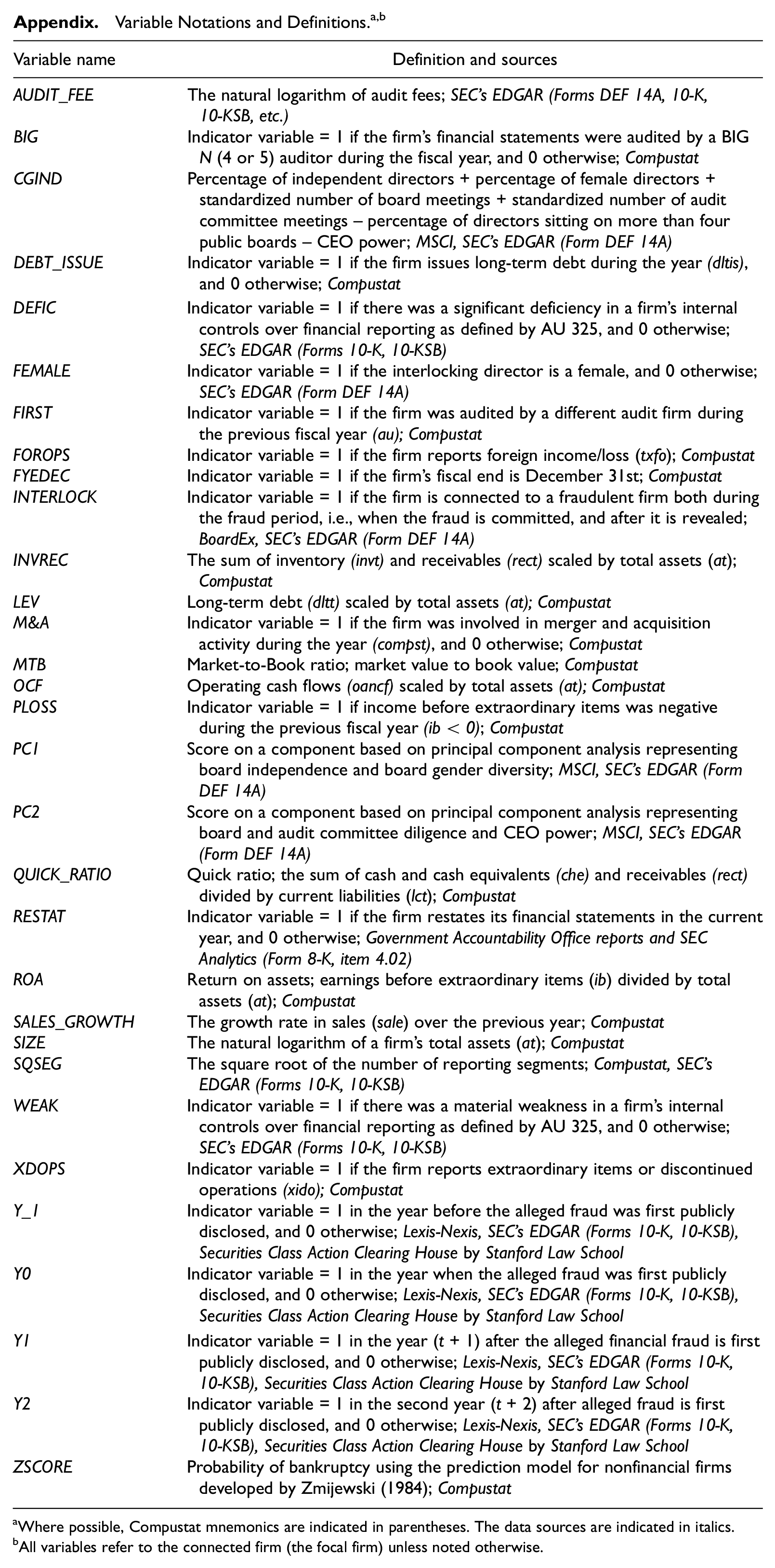

We follow prior studies on the determinants of audit fees and include firm-specific controls that are likely to affect the resources the auditor allocates to the audit engagement, as well as the litigation premium arising from the perceived engagement risk. Generally, larger, less profitable, more leveraged clients pay higher audit fees (e.g., Simunic, 1980). Thus, we control for the firm’s size (natural logarithm of total assets; SIZE), profitability (ROA), market-to-book ratio (MTB), leverage (long-term debt to total assets; LEV), and prior-period financial distress (PLOSS). In addition, current non-cash assets (e.g., inventory and receivables) might be more difficult to audit (Hay et al., 2006; Simunic, 1980). We include the sum of inventory and receivables scaled by total assets (INVREC) to proxy for this inherent engagement risk. Firms in need of new external financing are perceived as riskier (Krishnan et al., 2013). Thus, we add an indicator variable equal to one if the firm raised new long-term debt during the year (DEBT_ISSUE). Firms experiencing financial distress have an incentive to use questionable practices to inflate earnings and avoid covenant violations. To control for financial distress and liquidity constraints, we include the Zmijewski (1984) score (ZSCORE), the quick ratio (QUICK_RATIO), and operating cash flows (OCF). Growth could be another factor affecting audit fees, because it could serve as an indication of business risk. Thus, we expect sales growth (SALES_GROWTH) to be negatively related to audit fees. In addition, auditors might exert additional effort if the firm does not maintain adequate internal controls. 16 Accordingly, we control for the presence of material weakness (WEAK) and significant deficiency (DEFIC) in the firm’s internal controls over financial reporting and expect them to be positively correlated with audit fees. 17 If the firm restates previously issued financial statements (RESTAT), the auditors are required to also audit the restated financial statements in addition to the current fiscal year’s filings, which results in higher audit fees. Complex organizational structures require additional audit effort. Thus, we control for the complexity of the client by including indicators for whether the firm had significant foreign operations (FOROPS), merger or acquisition activity (M&A), and the number of reporting segments (the square root of the number of reporting segments, SQSEG). Big N audit firms generally charge an audit fee premium, which we control for by adding the variable BIG to indicate for whether the firm is audited by a Big N audit firm or not. Audit tenure can also affect audit fees, as one of the reasons firms change auditors is to reduce audit fees (Hay et al., 2006). We control for recent auditor change by including a dummy variable (FIRST) equal to one if the audit tenure is one year or less. We also add an indicator for whether the firm’s fiscal year-end is December 31 (FYEDEC) as audits conducted in January and February could require overtime and be more costly. All variables included in the regression are described in the Appendix.

Main Model

We employ a panel ordinary least squares (OLS) regression approach that compares the audit fees of the connected firms before the alleged fraud becomes public to the audit fees of the same firms after the event. This approach allows each firm in the sample to be used as its own control, thus reducing endogeneity concerns (Ettredge et al., 2012; Hail & Leuz, 2009). More specifically, we compare the audit fees of each firm in the year prior to the public disclosure of the alleged fraud (year t − 1) to the year after (year t + 1). We use year t − 1 as the base year because information about the financial fraud is not likely to be available then. 18 Even if the board members or the auditor had private information, it would have taken time for the auditor to adjust the audit procedures and thus the fees. We contrast the base year to year t + 1 rather than to year t to allow enough time for the new information to be reflected in the client risk assessment and/or audit effort. 19 In addition, choosing year t + 1 over t + 2 has the advantage of mitigating the effect of additional unobservable events that could have influenced the connected firms’ audit fees after the revelation of financial fraud. In a supplementary analysis, we determine the persistence of the effect by testing whether there is also an effect in year t + 2.

To test the consequences of financial fraud allegations on connected firms’ audit fees, we regress AUDIT_FEE on Y1 and include a list of control variables as discussed above. The following model is estimated using OLS regression with year and industry—Fama and French (1997) 17-industry classification—fixed effects on the connected firm sample:

where AUDIT_FEE is the natural logarithm of firm i’s audit fees in year t and Y1 is an indicator variable equal to one the year after the revelation of financial fraud and zero the year before. The control variables are as described above. To account for the correlation between the standard errors of same-firm observations, we cluster the standard errors by firm. Our main hypothesis predicts that β1 is positive and significant.

Empirical Results

Descriptive Statistics

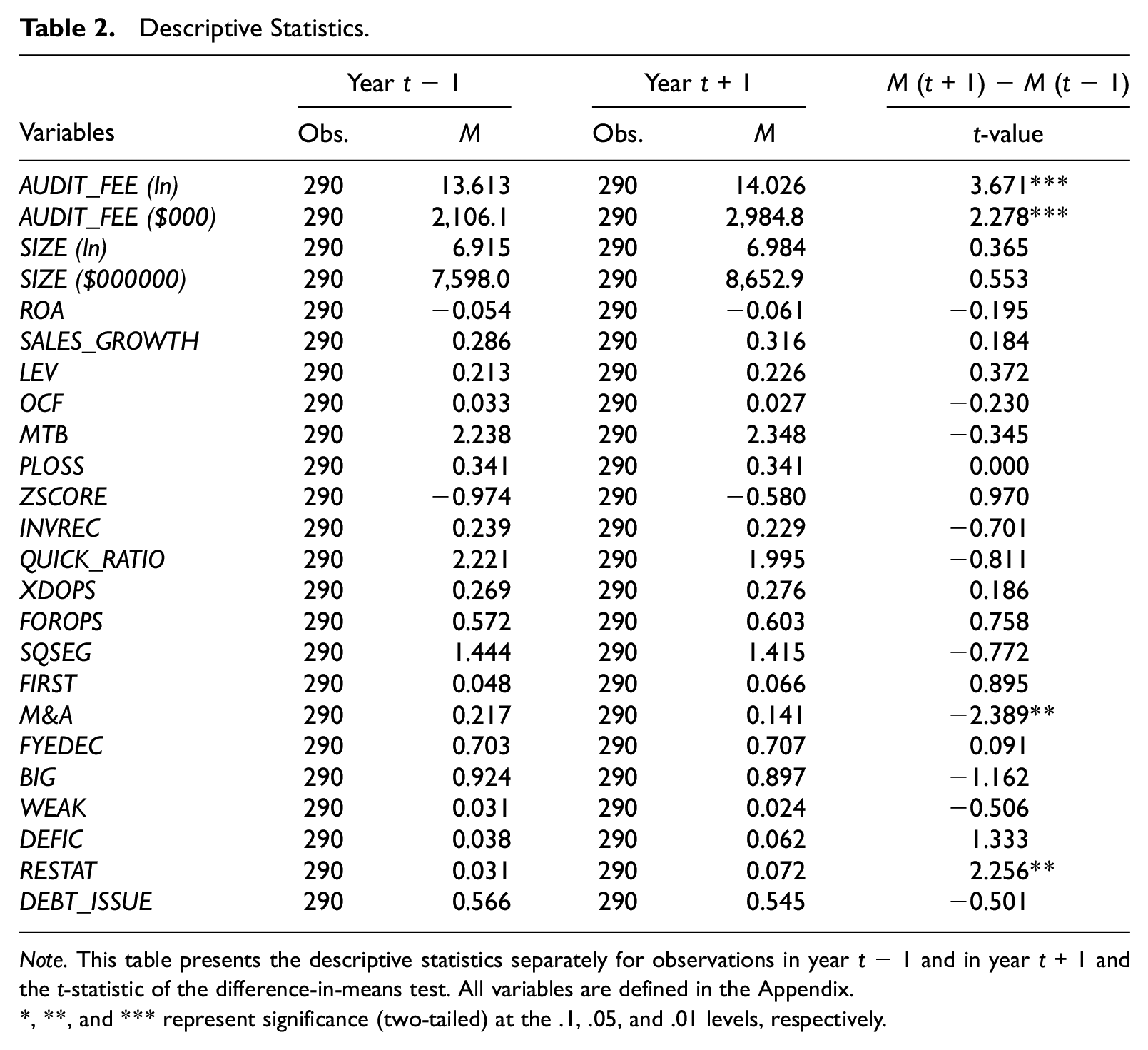

The average firm in our sample has around $8.1 billion in assets and has paid around $2.5 million in audit fees, 70.5% of the firms have a December year-end, and 91% have a Big N auditor. Table 2 presents the descriptive statistics separately for years t − 1 and t + 1. On average, audit fees (AUDIT_FEE) are significantly higher in year t + 1 than in year t − 1 for the firms included in the sample (the mean is around $2.1 million in year t − 1 and around $3 million in year t + 1), whereas average total assets (SIZE) remain relatively unchanged. Firms are less likely to be involved in mergers and acquisitions (M&A) and more likely to restate their earnings (RESTAT) in year t + 1. There do not appear to be other notable differences between t − 1 and t + 1.

Descriptive Statistics.

Note. This table presents the descriptive statistics separately for observations in year t − 1 and in year t + 1 and the t-statistic of the difference-in-means test. All variables are defined in the Appendix.

, **, and *** represent significance (two-tailed) at the .1, .05, and .01 levels, respectively.

The pairwise Pearson’s correlation coefficients between the variables included in the analysis are presented in the Online Appendix. The correlation between audit fees (AUDIT_FEE) and total assets (SIZE) is high (0.839), positive, and significant (at the 5% level or above), indicating that a firm’s total assets are a primary driver of its audit fees, consistent with prior studies (for a meta-analysis, see Hay et al., 2006). In addition, there is a high correlation between the number of segments (SQSEG) and audit fees (0.522) and between foreign operations (FOROPS) and audit fees (0.470). As predicted, audit fees are significantly positively correlated with our main variable of interest, Y1. All other correlation coefficients are generally below 40%, suggesting that multicollinearity is not a main concern in this analysis. 20

Main Results

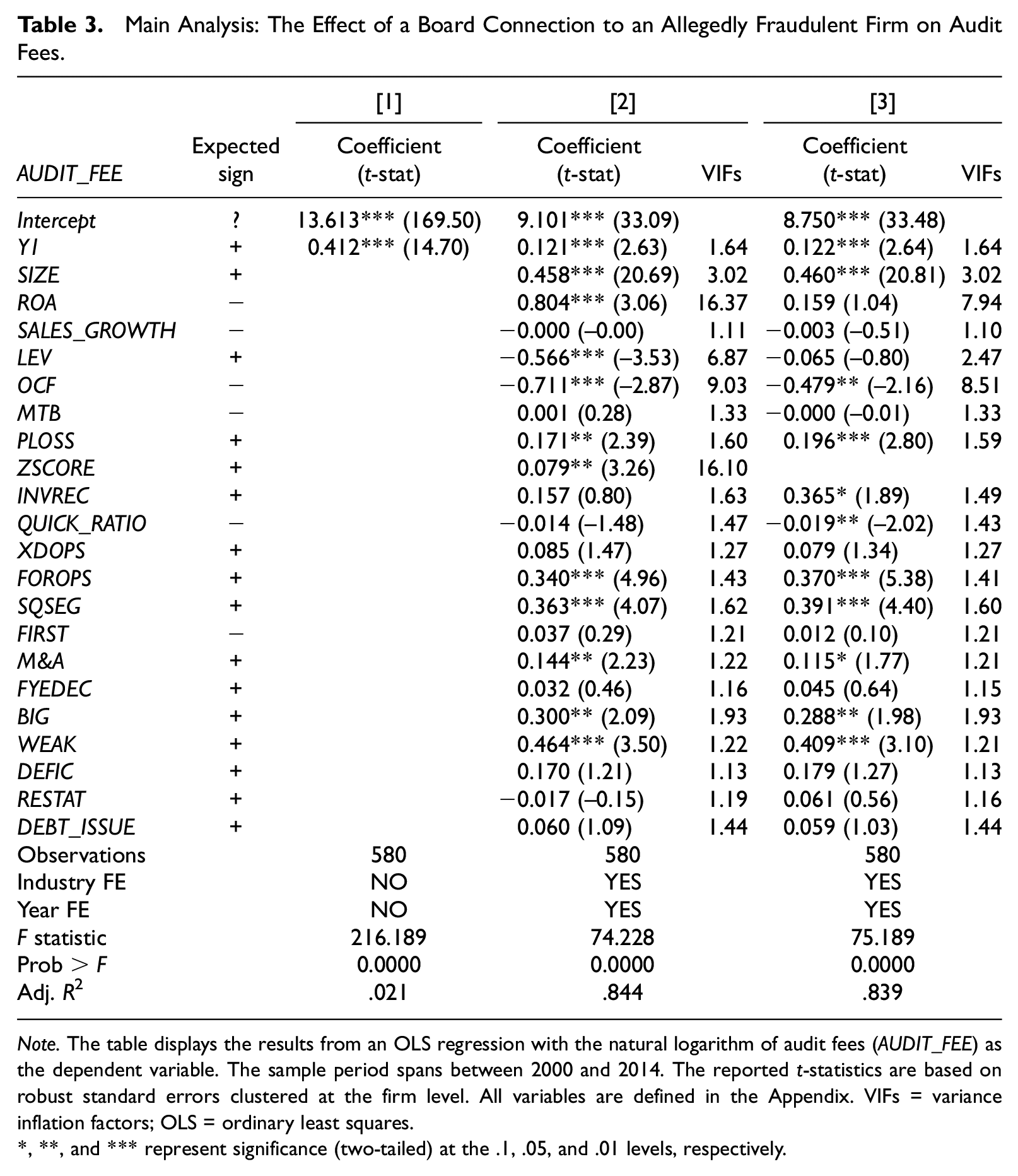

The results of the main regression are reported in Table 3. In column [1], we provide the results of the univariate analysis. The coefficient of Y1, which is an indicator variable that takes the value of one the year after the revelation of a financial fraud at a connected firm, is positive and significant (β1 = 0.412; t-statistic = 14.70), consistent with the t-test on the difference in means reported in Table 2. After we add the full set of control variables and industry and year fixed effects to the model (column [2]), the coefficient of Y1 is positive and significant at the 1% level for a two-tailed test (β1 = 0.121; t-statistic = 2.63), suggesting that, on average, the revelation of financial fraud is positively associated with the audit fees of interlocked firms, in support of our prediction. The marginal effect on audit fees is 12.86%. 21 The signs and magnitudes of the coefficients of the control variables are generally consistent with prior literature. For example, bigger and riskier firms pay higher audit fees, whereas firms with higher operating cash flows (OCF) pay lower fees to reflect their lower risk of liquidity problems. The complexity of firms’ operations also positively affects their audit fees, as indicated by the positive and significant coefficients of foreign operations (FOROPS), and the squared root of reporting segments (SQSEG). In addition, more problematic audits require more audit effort, which translates to higher fees. Accordingly, the coefficient of WEAK (equal to one if there was material weakness in the firm’s internal controls) is positive and significant. Finally, experiencing a loss over the previous year and being audited by a Big 4 auditor is positively associated with audit fees. 22

Main Analysis: The Effect of a Board Connection to an Allegedly Fraudulent Firm on Audit Fees.

Note. The table displays the results from an OLS regression with the natural logarithm of audit fees (AUDIT_FEE) as the dependent variable. The sample period spans between 2000 and 2014. The reported t-statistics are based on robust standard errors clustered at the firm level. All variables are defined in the Appendix. VIFs = variance inflation factors; OLS = ordinary least squares.

, **, and *** represent significance (two-tailed) at the .1, .05, and .01 levels, respectively.

As noted previously, some of the variables included in the analysis are highly correlated. To test whether multicollinearity biases our results, we perform a variance inflation factor (VIF) analysis. All VIFs are under 10 except for ROA (16.37) and ZSCORE (16.10). To address concerns that our results could be affected by the multicollinearity between ROA and ZSCORE, we next repeat the analysis, omitting ZSCORE as a covariate. 23 The results are reported in column [3] of Table 3. The coefficient of Y1 is qualitatively and quantitatively similar to that reported before, but the coefficient of ROA becomes insignificant. 24 A subsequent VIF analysis indicates that no VIFs are higher than 10 in the adjusted model. 25

Robustness

To gauge the sensitivity of our results, we conduct a number of robustness checks. We repeat the analysis with different specifications of industry fixed effects (i.e., Fama–French 12- or 48-industry classification, or two-digit SIC codes) and firm fixed effects. 26 The results remain robust.

We also test the sensitivity to the inclusion of additional variables in the analysis, such as having a pension plan, above-median industry sales, accounting quality measured as the absolute value of total accruals, and variables designed to capture the severity of financial fraud (i.e., duration, type, and, perceived damage to investors). 27 Untabulated analysis shows that the coefficients of these variables are not significant and the coefficient of our main variable of interest remains qualitatively and quantitatively similar to our main results. In addition, to test whether the increase in audit fees could be explained by the increased risk environment at the restating firms, we rerun the main analysis by omitting the restating firms from the sample. The results (untabulated) remain robust after excluding the firms with the highest misstatement risk (i.e., the firms that actually restate their earnings during the year).

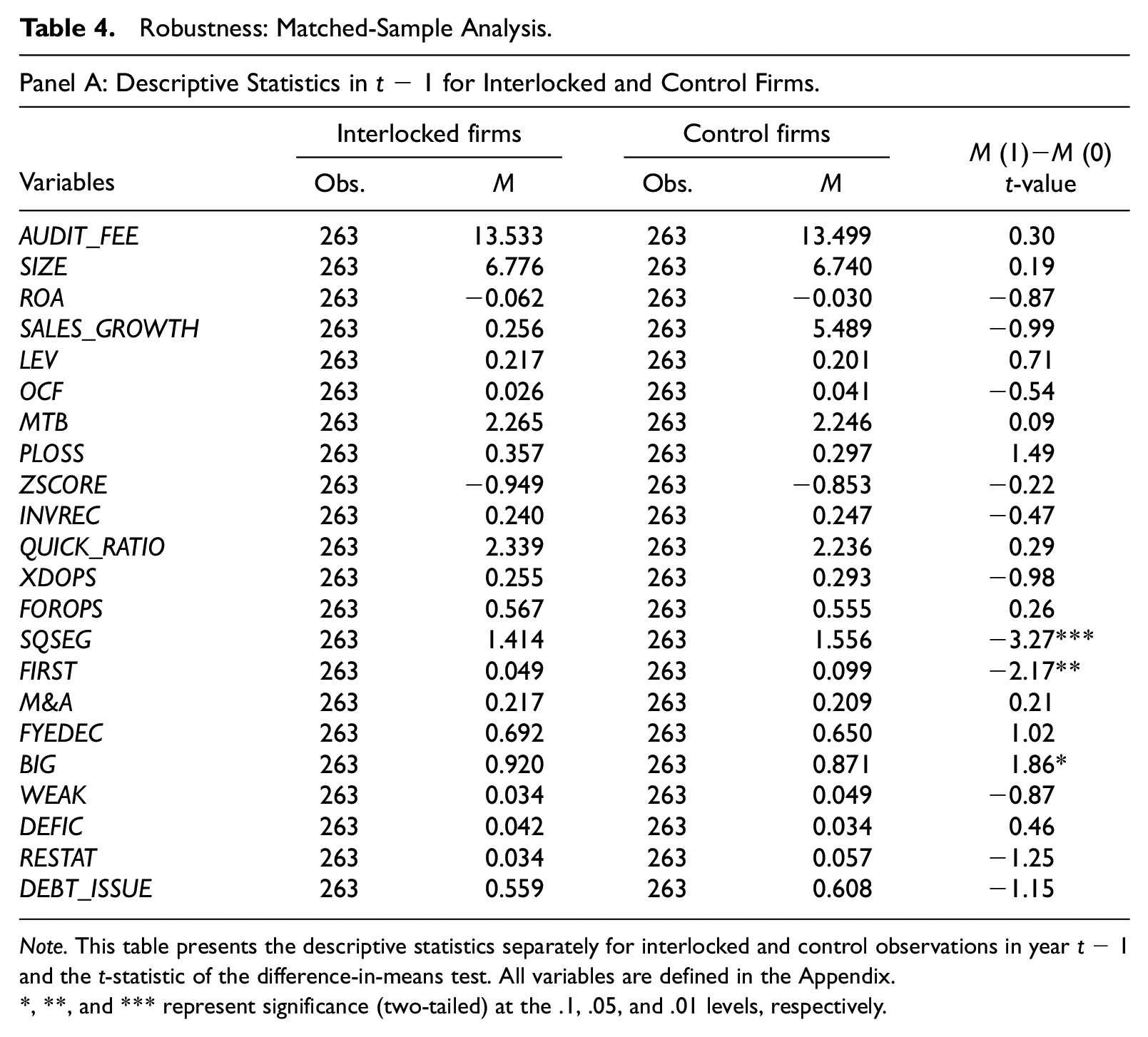

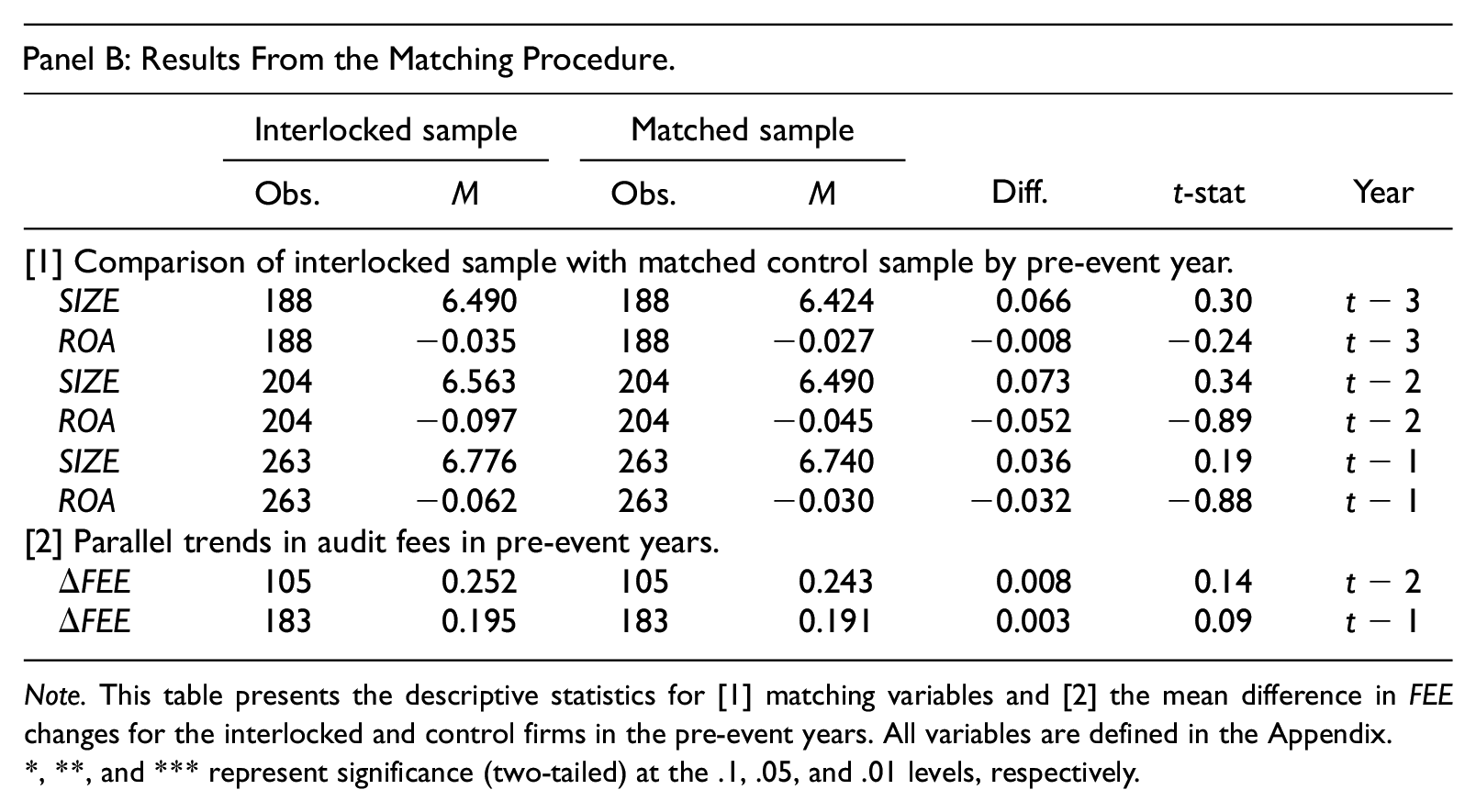

While the panel OLS regression analysis presented earlier indicates that firms experience an increase in audit fees following allegations of financial fraud at a connected firm, it is possible that the results are driven by some other factors that impact simultaneously not only the interlocked firms but also their peers. To address this concern, we match each firm in our interlocked firm sample to a firm operating in the same industry and of similar size and profitability in the year before the allegations of financial fraud become public. 28 The choice of variables to match on is consistent with prior literature (e.g., Sharma & Iselin, 2012). We employ a coarsened exact matching technique introduced by Iacus et al. (2011) and require that the control firms have no interlock connections to a fraudulent firm. 29 We successfully match 280 interlocked firms to 280 control firms in year t − 1. Audit fees for the control firms both in year t − 1 and t + 1 are available for 263 control firms, which reduces the number of matched pairs to 263 firms. Table 4, Panel A, reports the descriptive statistics of the matched sample of firms in year t − 1 and the t-statistic of the t-test of the difference in means between the interlocked and control firms. The differences between the means of both samples are insignificantly different from zero except for SQSEG, which is the square root of reporting segments, FIRST, which is an indicator equal to one if the firm changed its auditor in a given year, and zero otherwise, and BIG, which is an indicator variable equal to one if the firm is audited by one of the Big 4 audit firms, and zero otherwise. We include SQSEG, FIRST, and BIG as control variables in the multivariate regression, thus effectively accounting for any differences in the audit fees that could be due to these covariates. As an additional check, we follow Kausar et al. (2016) and compare the average values of our matching variables (i.e., SIZE and ROA) and the pre-event trends in audit fees (AUDIT_FEE) for the interlocked firms and the matched control sample in the 3-year period before the event. 30 Table 4, Panel B, shows that there is no statistically significant difference between the means of the matching variables for the two samples. In addition, the insignificant difference in the mean changes in audit fees for the two subsamples suggests that the interlocked and control firms follow parallel trends in audit fees in the pre-event years.

Robustness: Matched-Sample Analysis.

Note. This table presents the descriptive statistics separately for interlocked and control observations in year t − 1 and the t-statistic of the difference-in-means test. All variables are defined in the Appendix.

, **, and *** represent significance (two-tailed) at the .1, .05, and .01 levels, respectively.

Panel B: Results From the Matching Procedure.

Note. This table presents the descriptive statistics for [1] matching variables and [2] the mean difference in FEE changes for the interlocked and control firms in the pre-event years. All variables are defined in the Appendix.

*, **, and *** represent significance (two-tailed) at the .1, .05, and .01 levels, respectively.

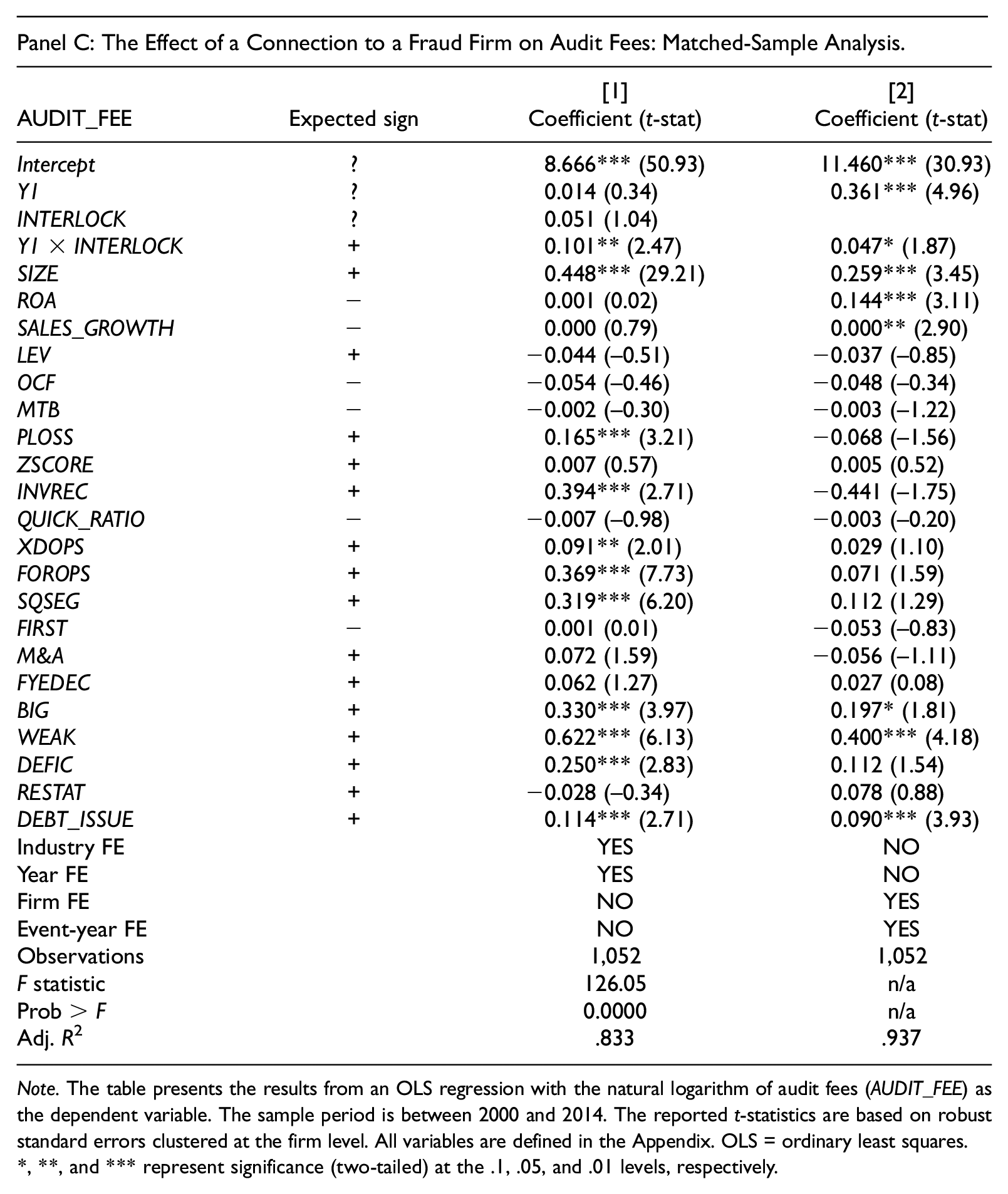

Panel C: The Effect of a Connection to a Fraud Firm on Audit Fees: Matched-Sample Analysis.

Note. The table presents the results from an OLS regression with the natural logarithm of audit fees (AUDIT_FEE) as the dependent variable. The sample period is between 2000 and 2014. The reported t-statistics are based on robust standard errors clustered at the firm level. All variables are defined in the Appendix. OLS = ordinary least squares.

, **, and *** represent significance (two-tailed) at the .1, .05, and .01 levels, respectively.

Table 4, Panel C, column [1] reports the results of a multivariate regression analysis on the matched sample of firms, where the main variable of interest is the interaction between Y1 and INTERLOCKED (which is one for firms connected to a fraudulent firm, and zero otherwise). We find that, while the coefficients of Y1 and INTERLOCKED are not significantly different from 0, the coefficient of the interaction between the two variables is positive and significant (β1 = 0.101; t-statistic = 2.47) providing evidence of higher audit fees that cannot be explained by the observable covariates and time trends, consistent with the expectation that connections with allegedly fraudulent firms impose upward pressure on audit fees. In column [2], we report the results of a multivariate regression with firm fixed effects instead of industry fixed effects and event-year fixed effects instead of year fixed effects. The coefficient of the interaction between Y1 and INTERLOCKED is positive, albeit weakly significant. 31

Additional Analyses

Conditioning on audit committee memberships

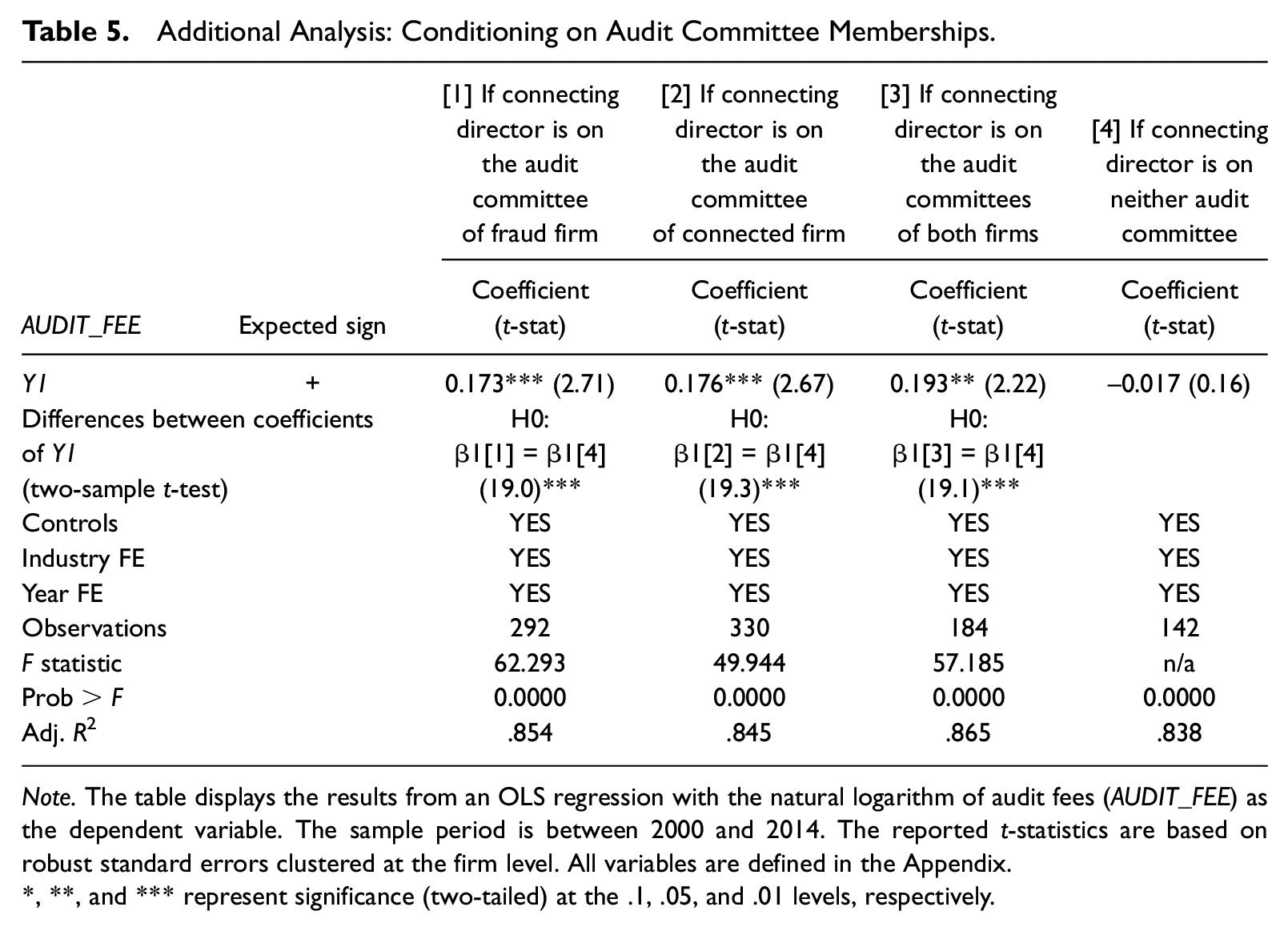

Audit committee members are directly involved in monitoring management, ascertaining the integrity of financial reporting, and assuring compliance with regulatory and legal requirements that can materially affect a firm’s financial statements. In addition, they have key responsibilities with respect to the performance of external auditors and the effectiveness of the internal audit function and are more likely to be held accountable by investors and other stakeholders for failing to prevent financial fraud (Brochet & Srinivasan, 2014; Srinivasan, 2005) or to spread questionable practices to other firms (e.g., Chiu et al., 2013). In our setting, interlocking directors serving on the audit committees of the fraudulent firms are likely to be blamed for failing to prevent the bad act or suspected of transferring some questionable practices, while if serving on the audit committees of connected firms, they are likely to undermine stakeholders’ confidence in the financial reporting practices of the connected firms. Therefore, we expect the perceived engagement risk for the auditors to be greater in cases where the interlocking director serves on the audit committee of either the fraudulent firm, the connected firm, or both. In addition, audit committee members might be more concerned about the possibility of earnings management contagion (Chiu et al., 2013) and demand additional audit services.

To test these predictions, we collect data on audit committee memberships of the interlocking directors from firms’ proxy statements (forms DEF 14A) available on SEC’s EDGAR and BoardEx. The interlocking director serves on the audit committee of the fraudulent firm in 146 firms (292 observations, or around 50% of the main sample), on the audit committee of the connected firm in 165 firms (330 observations, or around 57% of the main sample), on the audit committee of both firms in 92 firms (184 observations, or around 32% of the main sample). Finally, the interlocking director does not serve on either audit committee in 71 firms (142 observations, or around 24.5% of the main sample). We run Model (1) separately for each subsample and present the results in Table 5.

Additional Analysis: Conditioning on Audit Committee Memberships.

Note. The table displays the results from an OLS regression with the natural logarithm of audit fees (AUDIT_FEE) as the dependent variable. The sample period is between 2000 and 2014. The reported t-statistics are based on robust standard errors clustered at the firm level. All variables are defined in the Appendix.

, **, and *** represent significance (two-tailed) at the .1, .05, and .01 levels, respectively.

Table 5, column [1], reports the results for the subsample of firms where the interlocking director serves on the audit committee of the fraudulent firm when the bad act occurred. 32 The coefficient of Y1 is positive and significant, indicating a marginal increase in audit fees of 18.89% following allegations of financial fraud at a connected firm. Table 5, column [2] presents the results for the subsample, where the director serves on the audit committee of the connected firm. In line with the expectations, the coefficient of Y1 is positive and significant, indicating a marginal increase in audit fees of 19.24% in year t + 1, which cannot be explained by the control variables. While the marginal increase in audit fees for this subsample appears slightly higher than for the subsample of firms where the director serves on the audit committee of the fraudulent firm, the two coefficients are not significantly different. Next, we rerun Model (1) for the subsample of firms where the director serves on both committees forming an audit committee interlock and report the results in Table 5, column [3]. Similarly to the findings for the other two subsamples, the coefficient of Y1 is positive and significant at the 5% level (β1 = 0.193; t-statistic = 2.22), which corresponds to a marginal increase in audit fees of 21.29%, significantly higher (based on a two-sample t-test) than the coefficients of Y1 for the other two subsamples. Finally, Table 5, column [4], shows the results for the subsample, where the interlocking director serves on neither audit committee. The coefficient on Y1 is not significant, indicating no incremental change in audit fees for this subsample. Hence, the evidence provided thus far suggests that the results are driven by audit committee members.

Indirect tests of the auditor-side and client-side mechanisms

Next, we conduct additional tests to shed light on the mechanisms that drive the increase in audit fees following allegations of financial fraud at a connected firm. Drawing on prior research, we argue there are two potential mechanisms that could explain the increase in audit fees: an auditor-side mechanism (i.e., the auditor charges higher fees to reflect increased engagement risk) and a client-side mechanism (i.e., the client requests additional services to ensure the integrity of its financial reporting and preserve its reputation). The results presented thus far are consistent with both mechanisms. While we cannot directly test the two mechanisms, to gain further insights into the main driver of the relation between a firm’s audit fees and revelations of financial fraud at a connected firm, we conduct three additional tests based on (a) preemptive resignations, (b) corporate governance mechanisms, and (c) the gender of interlocking directors.

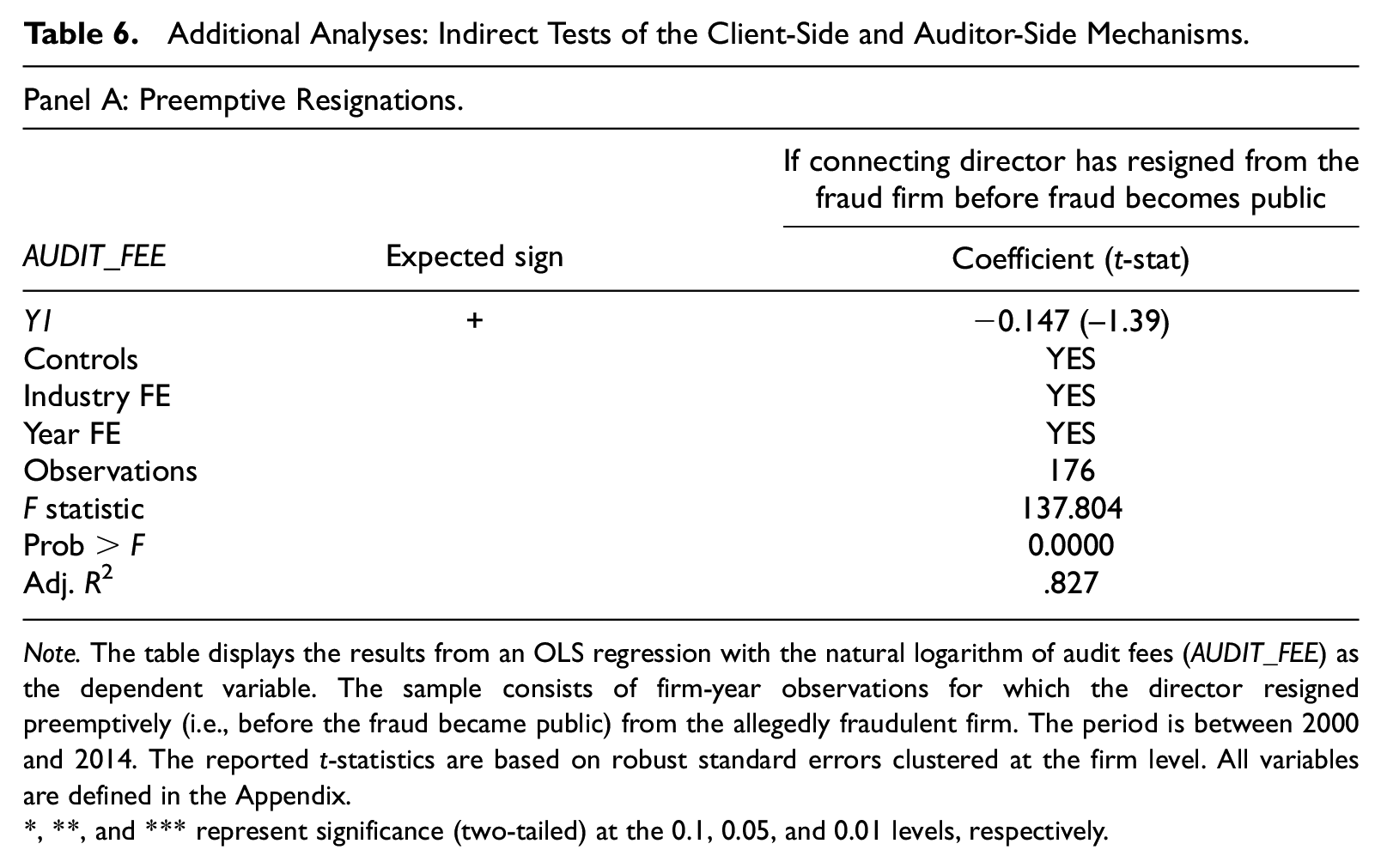

We utilize preemptive resignations of directors, that is, cases where the interlocking director serves on the boards of both firms when the bad act occurs but resigns from the board of the fraudulent firm before the bad act is publicly revealed, to indirectly test the client-driven effect. Prior research (e.g., Dou, 2017; Fahlenbrach et al., 2017; Gao et al., 2017) indicates that independent directors resign in anticipation of negative events such as restatements to protect their reputational capital. Drawing on prior literature, we propose that leaving the board of the fraudulent firm before the bad act is publicly disclosed serves as an indication of strong reputation and career concerns and an effort to mitigate reputational damage by disassociating from the fraudulent firm. 33 Accordingly, we expect directors who preemptively resign from the boards of the allegedly fraudulent firms to have greater incentives to ensure connected firms’ financial reporting quality by requesting more auditing services. We empirically test this prediction by estimating Model (1) for a sample of 176 firm-year observations, where the firms are connected when the fraud is committed but the director resigns from the board of the fraudulent firm before the fraud becomes first publicly disclosed. 34 If a client-side mechanism is in place, we would expect coefficient β1 to be positive and significant. Table 6, Panel A presents the results of this analysis. The coefficient of Y1 is not significantly different from 0, failing to provide support for the prediction that the audit fees increase for the subsample of firms whose directors preemptively resign from the boards of the allegedly fraudulent firms. The coefficients of the control variables are not reported for brevity reasons.

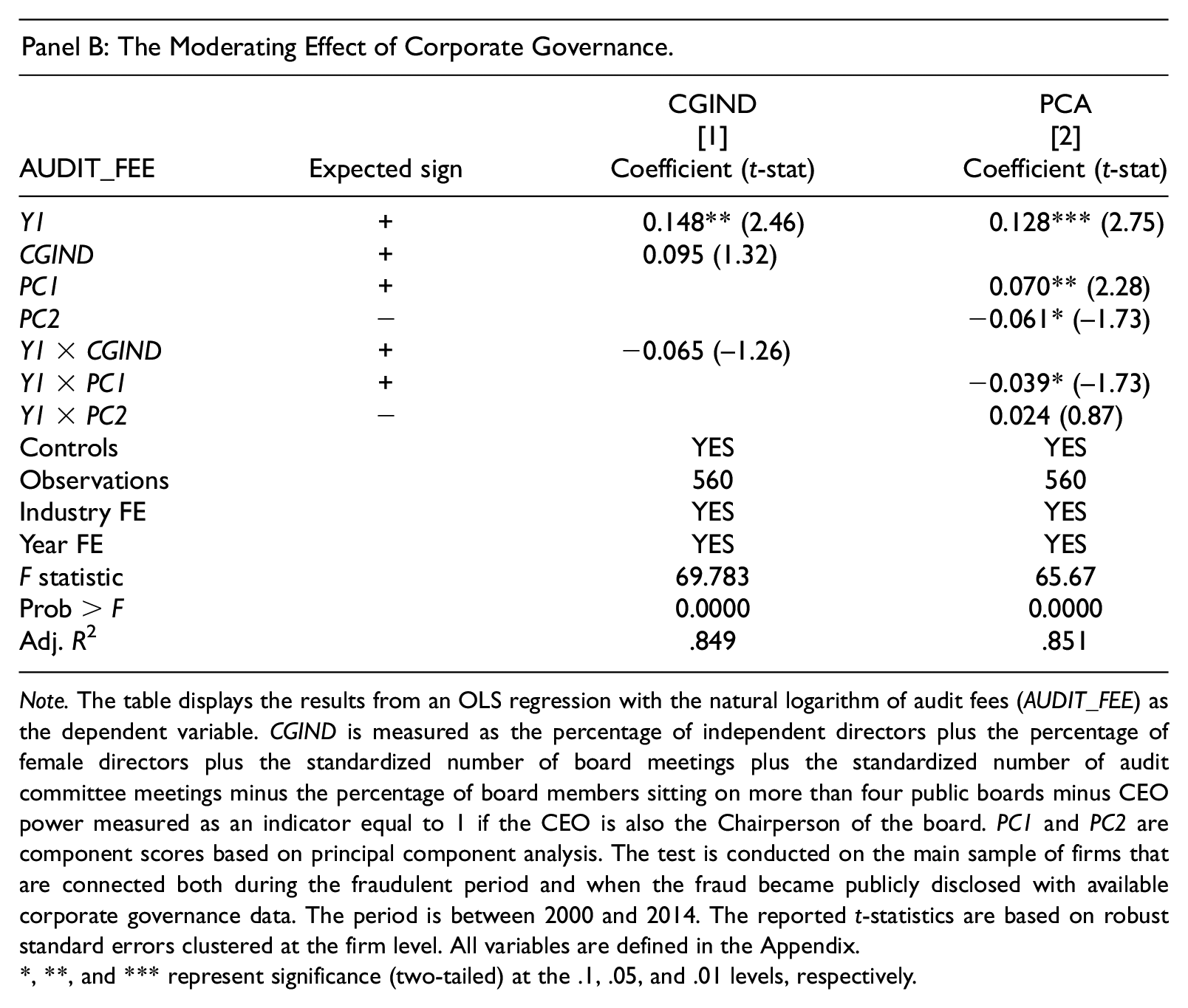

Next, we test whether the corporate governance quality moderates the association between board connections to a fraudulent firm and audit fees. Prior research (e.g., Carcello et al., 2002; Hay et al., 2008; Knechel & Willekens, 2006) documents positive association between audit fees and different corporate governance characteristics such as director independence, diligence, and expertise. In our setting, we expect that if a client-side mechanism dominates, this will manifest in a greater increase in audit fees for the better governed firms. To test this assertion, we collect data on structural indicators of corporate governance quality such as the number of independent directors, number of female directors, number of board and audit committee meetings, CEO/Chairperson duality, number of directors serving on four or more boards, and audit committee independence from MSCI and firms’ proxy statements. 35 These data are available for 280 firms in our main sample. We follow Srinidhi et al. (2014) and construct an index, CGIND, that aggregates these variables to assess a firm’s corporate governance strength. 36 We then interact the resulting index variable with our main variable of interest, Y1. If higher quality boards demand more audit services after the revelation of financial fraud at a connected firm, we expect the coefficient of the interaction to be positive and significant. Table 6, Panel B, column [1] presents the results. While the coefficient of Y1 remains positive and significant, in line with the previously reported results, neither the coefficient of CGIND nor the coefficient of the interaction between CGIND and Y1 is significant, failing to provide support for a client-driven effect. We next construct an alternative measure of corporate governance quality to address potential concerns arising from assigning equal weights to different corporate governance dimensions and from the high correlation between such dimensions (Larcker et al., 2007). In particular, we complement our analysis with an alternative approach, which relies on principal component analysis, and reduce our corporate governance indicators to components that are uncorrelated with each other. We follow Larcker et al. (2007) and retain the components which have eigenvalues greater than one. The first retained factor has two relevant indicators with significant loadings: board independence and board gender diversity both of which load positively, while the second component has three relevant indicators: board and audit committee diligence, which load negatively and CEO power, which loads positively. We then incorporate the two component scores in our estimation model by interacting them with Y1. The results presented in Table 6, Panel B, column [2] indicate a positive and significant correlation between the first component and audit fees. Interestingly, the coefficient on the interaction between Y1 and the first component (Y1 × CP1) is negatively, albeit weakly, associated with audit fees. This suggests that more independent and diverse boards demand more audit services consistent with the evidence provided by prior literature (Carcello et al., 2002; Hay et al., 2008; Knechel & Willekens, 2006), yet the increase in audit fees after the revelation of financial fraud at a connected firm is somewhat less pronounced for these firms. That is, corporate governance quality mitigates the effects due to associations with a fraudulent firm, which is more in line with an auditor-side effect than with a client-side effect. The second component score is negatively associated with audit fees again in line with the expectations that more powerful CEOs and less diligent boards and audit committees tend to demand less audit services. The coefficient on the interaction variable between the second component score and Y1 is not significant. The coefficient of Y1 remains qualitatively and quantitatively similar to the previously reported results. Overall, these tests fail to provide support for a client-side effect.

Additional Analyses: Indirect Tests of the Client-Side and Auditor-Side Mechanisms.

Note. The table displays the results from an OLS regression with the natural logarithm of audit fees (AUDIT_FEE) as the dependent variable. The sample consists of firm-year observations for which the director resigned preemptively (i.e., before the fraud became public) from the allegedly fraudulent firm. The period is between 2000 and 2014. The reported t-statistics are based on robust standard errors clustered at the firm level. All variables are defined in the Appendix.

, **, and *** represent significance (two-tailed) at the 0.1, 0.05, and 0.01 levels, respectively.

Panel B: The Moderating Effect of Corporate Governance.

Note. The table displays the results from an OLS regression with the natural logarithm of audit fees (AUDIT_FEE) as the dependent variable. CGIND is measured as the percentage of independent directors plus the percentage of female directors plus the standardized number of board meetings plus the standardized number of audit committee meetings minus the percentage of board members sitting on more than four public boards minus CEO power measured as an indicator equal to 1 if the CEO is also the Chairperson of the board. PC1 and PC2 are component scores based on principal component analysis. The test is conducted on the main sample of firms that are connected both during the fraudulent period and when the fraud became publicly disclosed with available corporate governance data. The period is between 2000 and 2014. The reported t-statistics are based on robust standard errors clustered at the firm level. All variables are defined in the Appendix.

, **, and *** represent significance (two-tailed) at the .1, .05, and .01 levels, respectively.

Panel C: The Moderating Effect of Gender.

Note. The table displays the results from an OLS regression with the natural logarithm of audit fees (AUDIT_FEE) as the dependent variable. FEMALE is an indicator variable equal to 1 if the interlocking director is female, and 0 otherwise. The test is conducted on the main sample of firms that are connected both during the fraud period and when the fraud became publicly disclosed. The period is between 2000 and 2014. The reported t-statistics are based on robust standard errors clustered at the firm level. All variables are defined in the Appendix.

, **, and *** represent significance (two-tailed) at the .1, .05, and .01 levels, respectively.

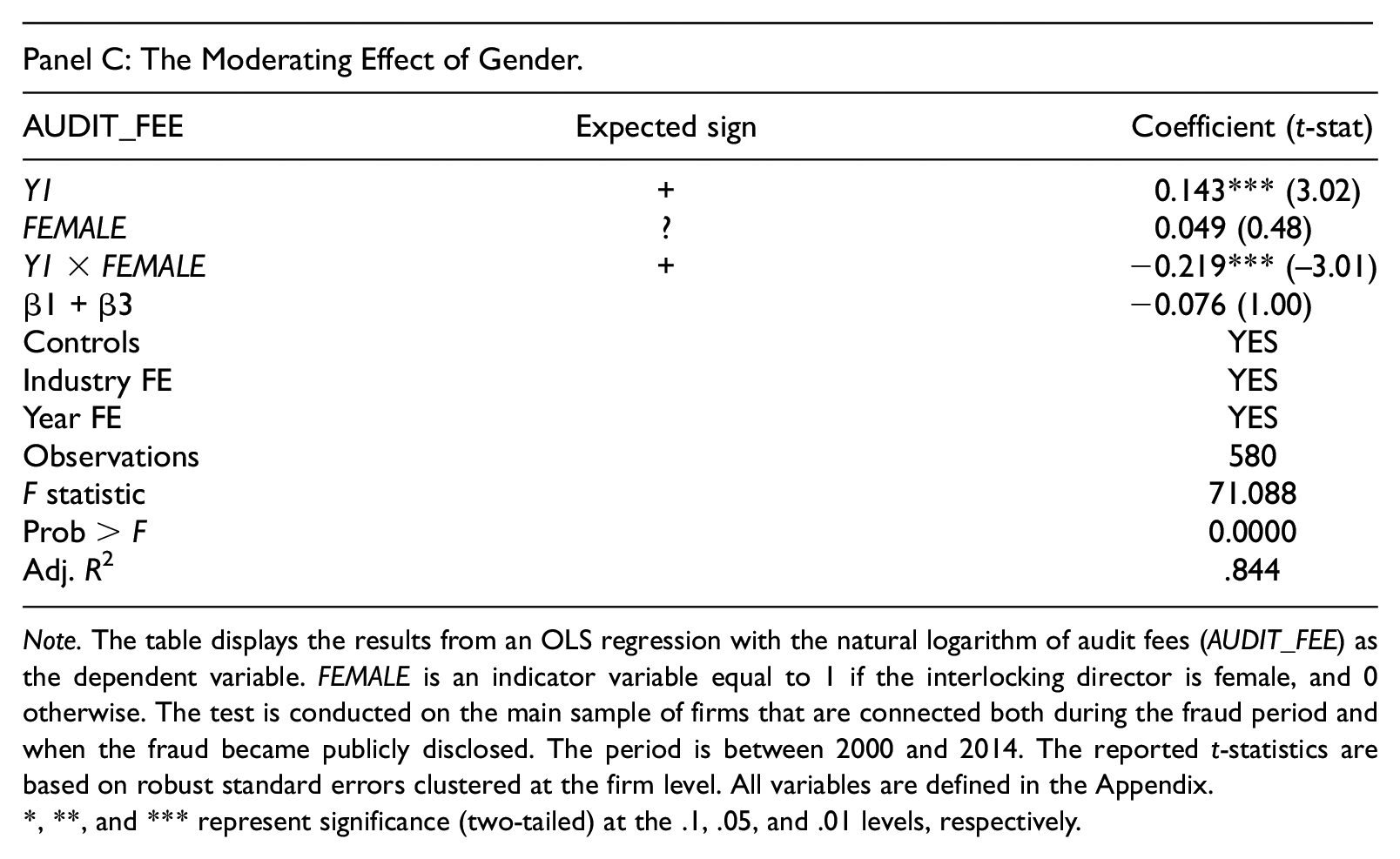

As a third indirect test, we explore whether gender moderates the association between being connected to a fraudulent firm when the fraud is revealed and audit fees (i.e., the association between Y1 and AUDIT_FEE). Prior literature suggests that women are more risk-averse in financial decision-making than their male counterparts (e.g., Powell & Ansic, 1997; Sunden & Surette, 1998) and are less tolerant to litigation and reputation risk (Srinidhi et al., 2011). Thus, we expect female interlocking directors to be more concerned about their own and the connected firm’s reputation and more likely to request additional audit services than their male counterparts. To this end, we introduce a new variable—FEMALE—to Model (1) which is one if the interlocking director is female, and zero otherwise. We are particularly interested in the interaction between Y1 and FEMALE. If a client-side effect is in place, we expect both the coefficients of Y1 and the interaction Y1 × FEMALE to be positive and significant.

Table 6, Panel C, presents the results of this analysis. Surprisingly, while the coefficient of Y1 is positive and significant consistent with the previously reported results, the coefficient of the interaction between Y1 and FEMALE is negative and significant, indicating that the audit fees for firms where the interlocking director is female are significantly lower (not higher as predicted in line with the client-side effect) than the audit fees for firms with male interlocking directors. Furthermore, this analysis shows that the audit fees do not significantly change in t + 1 with respect to t − 1 for firms with female interlocking directors (β1 + β3 = −0.076, which is not significantly different from 0). A potential explanation for this interesting finding is that female directors might not be considered culpable in the financial fraud cases (or at least not as culpable as their male counterparts). Indeed, Steffensmeier et al. (2013) conduct an in-depth analysis of 83 corporate fraud cases between 2002 and 2009 and note that women were seldomly involved in the conspiracy networks to commit fraud. Other studies also suggest that gender diversity on corporate boards improves the quality of financial reporting (e.g., Srinidhi et al., 2011), suggesting that it is unlikely that poor oversight of the female directors failed to prevent the bad act.

All in all, our indirect tests based on preemptive resignations and the moderating effects of corporate governance and gender fail to provide evidence in support of a client-side effect. Rather our results suggest that the positive association between the revelation of financial fraud and audit fees is more consistent with an auditor-side effect. 37

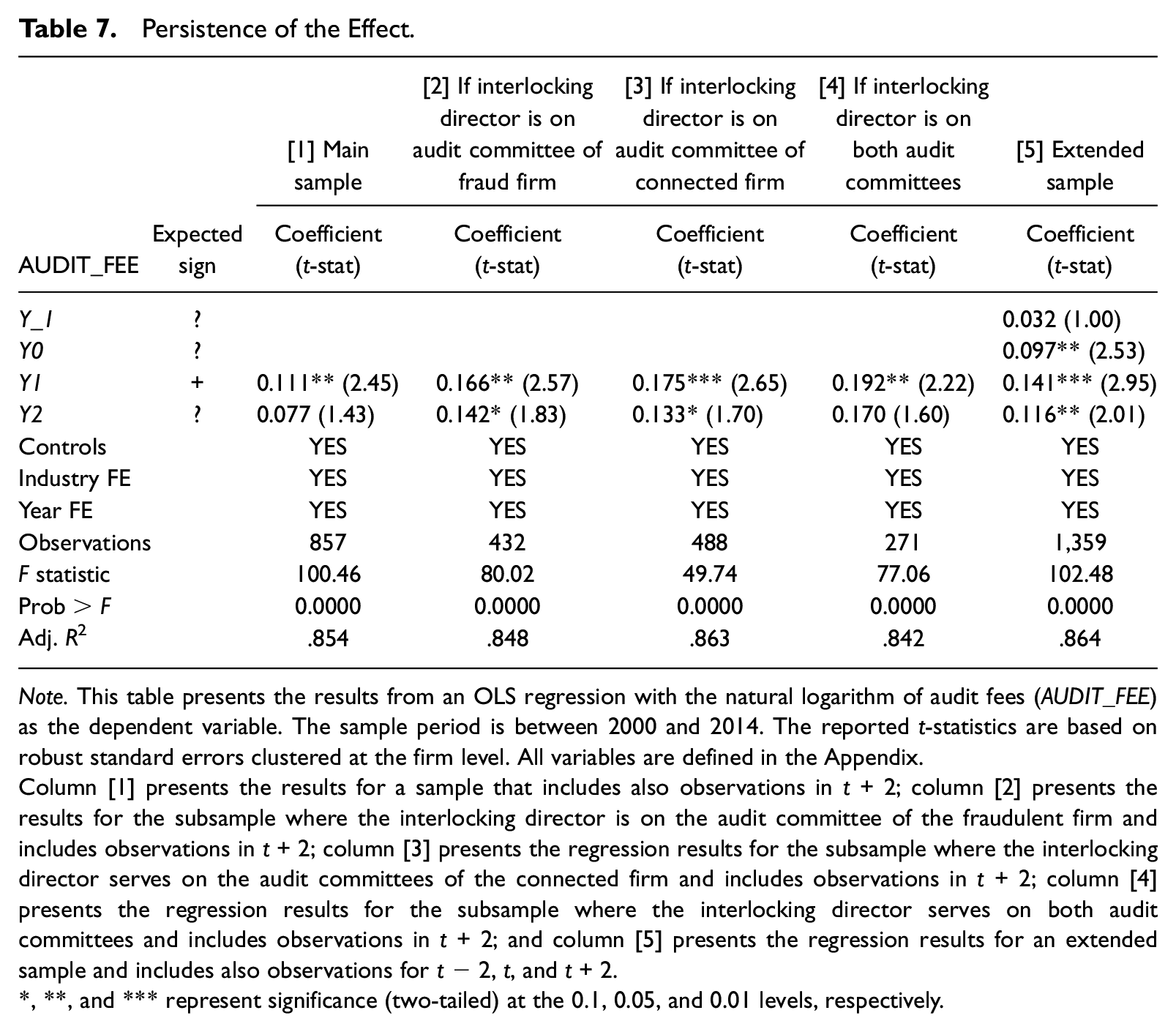

Persistence of the increase in audit fees

Thus far, our analysis has focused on the change in audit fees in the year after the allegations of financial fraud vis-à-vis the year before it. A further question to explore is whether the observed increase in audit fees is due to a one-time reaction or it persists in the subsequent year (i.e., year t + 2). To capture the persistence effect (if any), we add an indicator variable, Y2, equal to one in year t + 2 and zero in years t − 1 and t + 1. The result presented in Table 7, column [1] indicates that on average the effect does not persist in year t + 2. Next, we condition the analysis on whether the director serves on the audit committee of either the fraudulent firm (column [2]), the connected firm (column [3]), or both firms (column [4]). We document a positive and significant effect on audit fees in t + 1 consistent with the results reported previously across all subsamples, and a positive, albeit weakly significant effect on audit fees in t + 2 for the subsample where the director serves on the audit committee of the connected firm or the fraudulent firm, but not on both. This finding suggests that the effect that we observe persists for some firms for at least 2 years after the allegations of financial fraud become public. Finally, in column [5], we present the results for our sample extended 2 years before the event and 2 years after, resulting in a total sample of 1,359 observations. The coefficients on Y0, Y1, and Y2, but not Y_1 are all positive and significant indicating an increase in audit fees with respect to t − 2.

Persistence of the Effect.

Note. This table presents the results from an OLS regression with the natural logarithm of audit fees (AUDIT_FEE) as the dependent variable. The sample period is between 2000 and 2014. The reported t-statistics are based on robust standard errors clustered at the firm level. All variables are defined in the Appendix.

Column [1] presents the results for a sample that includes also observations in t + 2; column [2] presents the results for the subsample where the interlocking director is on the audit committee of the fraudulent firm and includes observations in t + 2; column [3] presents the regression results for the subsample where the interlocking director serves on the audit committees of the connected firm and includes observations in t + 2; column [4] presents the regression results for the subsample where the interlocking director serves on both audit committees and includes observations in t + 2; and column [5] presents the regression results for an extended sample and includes also observations for t − 2, t, and t + 2.

, **, and *** represent significance (two-tailed) at the 0.1, 0.05, and 0.01 levels, respectively.

Increased audit effort or higher litigation risk premium

The findings presented in this article indicate that adverse events at interlocked firms are associated with higher audit fees and the additional tests suggest that the increase is more consistent with an auditor-side mechanism. This may be due to the fact that the auditors perform additional audit services and/or charge higher litigation premiums. Disentangling these two effects is challenging in our setting as direct measures of litigation premium or audit effort such as hours spent on the engagement are not available. We, however, shed some light on this issue by indirectly examining changes in audit quality, which should increase as a result of additional audit effort. In particular, we consider two proxies of audit quality—the probability of issuance of a modified opinion (e.g., Lennox, 2005) and the probability of misstatements measured as the subsequent restatement of the current year financial reports (e.g., Kinney et al., 2004). We observe a significantly higher probability of a modified opinion for connected firms after the revelation of financial fraud, consistent with increased audit effort, but no significant differences in the probability of misstatements. 38 Thus, while there is some evidence of increased audit effort, the results are not conclusive, and we cannot dismiss the possibility that the increase in audit fees documented earlier is attributable to both increased audit effort and higher risk premium.

Conclusion

This study examines whether material adverse events such as egregious GAAP violations at a firm have an effect on the audit fees of firms connected to the former by a board interlock. We observe a significant positive effect on audit fees following the revelation of financial fraud at a connected firm. The results are robust to a battery of sensitivity checks and a matched-sample analysis. We also show that the effect is predominantly driven by cases where the interlocking director is an audit committee member. Furthermore, we distinguish between two potential mechanisms that could drive the increase in audit fees: an auditor-side mechanism (i.e., the auditor reassesses the client’s engagement risk) and a client-side mechanism (i.e., the client demands more audit services). Our analyses suggest that a client-side mechanism is not clearly in place. We also find some evidence of an increased probability of modified audit opinions for the connected firms suggesting that at least some of the increase in audit fees can be explained by increased audit effort.

This study contributes to the literature in two important ways. First, it provides evidence that board connections to fraudulent firms have implications for a firm’s audit fees. Prior studies (e.g., Fich & Shivdasani, 2007; Kang, 2008) have focused on the stock market reactions following public allegations of financial fraud of a connected firm and involved directors’ labor market penalties (Fama & Jensen, 1983; Fich & Shivdasani, 2007; Srinivasan, 2005). Our article shows that board connections to fraudulent firms have additional important economic effects. Second, we contribute to the emerging literature on the effects of board connections on audit fees. We complement prior literature (e.g., Johansen & Pettersson, 2013) on the effect of board interlocks on auditor choice and audit fees by suggesting that material adverse events at one firm influence the audit fees of firms to which they are connected by a board interlock.

The study has several caveats. First, our research design does not allow us to directly differentiate between the two mechanisms. Our indirect tests of the client-side effect fail to provide support along this line of reasoning. An informal conversation with a former audit partner of a Big 4 auditor also suggests that the results are likely driven by higher audit engagement risk. However, while our results are more consistent with an auditor-side effect, we recognize that it is hard to draw final conclusions. Second, our research design is subject to the usual endogeneity concerns. While the results are robust to the inclusion of firm fixed effects and a matched-sample analysis, endogeneity concerns cannot be fully excluded. Third, our results should be generalized with caution. We focus on SEC enforcement actions as a proxy for financial fraud cases. The results presented in this article might not be fully generalizable to less severe cases of financial misstatement. Future research may investigate whether similar results apply to less severe cases such as restatements. Finally, in our study, we exclude from the sample connected firms that are investigated by the SEC during the sample period. An interesting question for future research could be whether connections to a fraudulent firm increase the probability of SEC scrutiny.

Supplemental Material

sj-pdf-1-jaf-10.1177_0148558X20971947 – Supplemental material for The Effects of Board Interlocks With an Allegedly Fraudulent Company on Audit Fees

Supplemental material, sj-pdf-1-jaf-10.1177_0148558X20971947 for The Effects of Board Interlocks With an Allegedly Fraudulent Company on Audit Fees by Mariya N. Ivanova and Annalisa Prencipe in Journal of Accounting, Auditing & Finance

Footnotes

Appendix

Variable Notations and Definitions.a,b

| Variable name | Definition and sources |

|---|---|

| AUDIT_FEE | The natural logarithm of audit fees; SEC’s EDGAR (Forms DEF 14A, 10-K, 10-KSB, etc.) |

| BIG | Indicator variable = 1 if the firm’s financial statements were audited by a BIG N (4 or 5) auditor during the fiscal year, and 0 otherwise; Compustat |

| CGIND | Percentage of independent directors + percentage of female directors + standardized number of board meetings + standardized number of audit committee meetings – percentage of directors sitting on more than four public boards – CEO power; MSCI, SEC’s EDGAR (Form DEF 14A) |

| DEBT_ISSUE | Indicator variable = 1 if the firm issues long-term debt during the year (dltis), and 0 otherwise; Compustat |

| DEFIC | Indicator variable = 1 if there was a significant deficiency in a firm’s internal controls over financial reporting as defined by AU 325, and 0 otherwise; SEC’s EDGAR (Forms 10-K, 10-KSB) |

| FEMALE | Indicator variable = 1 if the interlocking director is a female, and 0 otherwise; SEC’s EDGAR (Form DEF 14A) |

| FIRST | Indicator variable = 1 if the firm was audited by a different audit firm during the previous fiscal year (au); Compustat |

| FOROPS | Indicator variable = 1 if the firm reports foreign income/loss (txfo); Compustat |

| FYEDEC | Indicator variable = 1 if the firm’s fiscal end is December 31st; Compustat |

| INTERLOCK | Indicator variable = 1 if the firm is connected to a fraudulent firm both during the fraud period, i.e., when the fraud is committed, and after it is revealed; BoardEx, SEC's EDGAR (Form DEF 14A) |

| INVREC | The sum of inventory (invt) and receivables (rect) scaled by total assets (at); Compustat |

| LEV | Long-term debt (dltt) scaled by total assets (at); Compustat |

| M&A | Indicator variable = 1 if the firm was involved in merger and acquisition activity during the year (compst), and 0 otherwise; Compustat |

| MTB | Market-to-Book ratio; market value to book value; Compustat |

| OCF | Operating cash flows (oancf) scaled by total assets (at); Compustat |

| PLOSS | Indicator variable = 1 if income before extraordinary items was negative during the previous fiscal year (ib < 0); Compustat |

| PC1 | Score on a component based on principal component analysis representing board independence and board gender diversity; MSCI, SEC’s EDGAR (Form DEF 14A) |

| PC2 | Score on a component based on principal component analysis representing board and audit committee diligence and CEO power; MSCI, SEC’s EDGAR (Form DEF 14A) |

| QUICK_RATIO | Quick ratio; the sum of cash and cash equivalents (che) and receivables (rect) divided by current liabilities (lct); Compustat |

| RESTAT | Indicator variable = 1 if the firm restates its financial statements in the current year, and 0 otherwise; Government Accountability Office reports and SEC Analytics (Form 8-K, item 4.02) |

| ROA | Return on assets; earnings before extraordinary items (ib) divided by total assets (at); Compustat |

| SALES_GROWTH | The growth rate in sales (sale) over the previous year; Compustat |

| SIZE | The natural logarithm of a firm’s total assets (at); Compustat |

| SQSEG | The square root of the number of reporting segments; Compustat, SEC’s EDGAR (Forms 10-K, 10-KSB) |

| WEAK | Indicator variable = 1 if there was a material weakness in a firm’s internal controls over financial reporting as defined by AU 325, and 0 otherwise; SEC’s EDGAR (Forms 10-K, 10-KSB) |

| XDOPS | Indicator variable = 1 if the firm reports extraordinary items or discontinued operations (xido); Compustat |

| Y_1 | Indicator variable = 1 in the year before the alleged fraud was first publicly disclosed, and 0 otherwise; Lexis-Nexis, SEC’s EDGAR (Forms 10-K, 10-KSB), Securities Class Action Clearing House by Stanford Law School |

| Y0 | Indicator variable = 1 in the year when the alleged fraud was first publicly disclosed, and 0 otherwise; Lexis-Nexis, SEC’s EDGAR (Forms 10-K, 10-KSB), Securities Class Action Clearing House by Stanford Law School |

| Y1 | Indicator variable = 1 in the year (t + 1) after the alleged financial fraud is first publicly disclosed, and 0 otherwise; Lexis-Nexis, SEC’s EDGAR (Forms 10-K, 10-KSB), Securities Class Action Clearing House by Stanford Law School |

| Y2 | Indicator variable = 1 in the second year (t + 2) after alleged fraud is first publicly disclosed, and 0 otherwise; Lexis-Nexis, SEC’s EDGAR (Forms 10-K, 10-KSB), Securities Class Action Clearing House by Stanford Law School |

| ZSCORE | Probability of bankruptcy using the prediction model for nonfinancial firms developed by Zmijewski (1984); Compustat |

Where possible, Compustat mnemonics are indicated in parentheses. The data sources are indicated in italics. bAll variables refer to the connected firm (the focal firm) unless noted otherwise.

Acknowledgements

We thank the two anonymous reviewers, Sasson Bar-Yosef, Pietro Bianchi, Mara Cameran, Limei Che (discussant), Kim Ittonen, Juha-Pekka Kallunki, Linda Myers (Associate Editor), Marleen Willekens (discussant), the seminar participants at the 2016 EIASM Workshop on Audit Quality, 2017 EAA Annual Congress, and the 2019 JAAF Conference for their helpful and constructive comments on earlier versions of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Data Availability

Data are available from the sources identified in the article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.