Abstract

Large CEO–employee pay gaps often elicit negative reactions, yet they have reached historic highs with limited resistance. How can this be explained? Developing a novel social comparison perspective, we propose that under specific circumstances pay inequality may yield positive reactions. We argue that perceived similarity with a CEO enhances acceptance of CEO pay, a process driven by elevated inspiration. We tested this prediction in four studies: a large international archival survey, a pre-registered survey of U.S. employees, and two pre-registered experiments. In the archival survey, we demonstrate that perceived similarity to CEOs, when measured indirectly, reduced support for income-inequality-reduction policies, and this effect appears-to-emerge across cultures. Converging experimental evidence reveals that employees who perceived greater similarity to their CEOs are more accepting of high CEO pay, due to feeling more inspired. These findings help elucidate why extreme pay disparities are often accepted, even though they may reinforce broader societal inequality.

Introduction

People have a keen sense of how their own fortunes compare to those of others (Festinger, 1954). Knowing that one has much less than others is not only experienced as aversive (Bolton & Ockenfels, 2000; Fehr & Schmidt, 1999), it also triggers strong emotional reactions of envy (Smith & Kim, 2007), and motivates behavior aimed at reducing the perceived inequality (Dawes et al., 2007). Large inequality, it seems, puts a sting in people’s hearts and minds (D. J. Brown et al., 2007). This sting may be especially salient in the domain of pay, given the meteoric rise of executive compensation relative to the moderate increase of employee compensation (Bivens & Kandra, 2022). For example, Satya Nadella—CEO of Microsoft—earned $96.5 million in 2025, 480 times the compensation of his median employee ($200,972; Microsoft Corporation, 2025). Such disparities are not unusual, as CEO‑to‑worker pay ratios are at historic highs (Bivens & Kandra, 2022; Chamberlain, 2015). Moreover, concrete information about CEOs’ high salaries and large pay inequalities in companies is becoming increasingly available to employees and outside observers alike (Securities and Exchange Commission, 2017).

Previous research has demonstrated that people typically react negatively to concrete information about large (vs. small) vertical pay inequality. They deem aggregate information about large CEOs-to-median worker inequality as aversive and unfair (Kiatpongsan & Norton, 2014). Consequently, employees and consumers alike view companies with extreme vertical pay inequality unfavorably, showing reduced willingness to work for or buy from them (Benedetti & Chen, 2018; Mohan et al., 2018). Related work further shows that elevated CEO pay can carry interpersonal costs, weakening followers’ identification with the CEO and reducing perceptions of leader charisma (Steffens et al., 2020). Although vertical pay inequality elicits well-documented negative reactions and public awareness has increased, pay inequality has persisted and become more pronounced over time (for a review of economic and institutional reasons, see Edmans et al., 2017). Yet, these widening gaps have provoked little public resistance. How can this paradox of limited public response to blatant, aversive (pay) inequality be explained?

Two prominent theoretical perspectives may shed light on this conundrum. First, at a macro-societal level, system justification theory argues that people are often motivated to support and defend existing political and economic systems, even when those systems produce inequality that disadvantages them (Jost & Hunyady, 2005). Because these inequalities are often less visible and more abstract, they may be easier for people to accept or justify. Importantly, however, this theoretical perspective offers limited insight into individuals’ reactions when confronted with concrete, proximal comparison information, such as realizing that their own earnings fall markedly short of their CEO. A second theoretical perspective, social comparison theory (Festinger, 1954), shifts the focus to the individual level by emphasizing how people respond to readily accessible information about others’ more or less favorable outcomes—namely, by engaging in upward and downward comparisons. This broad framework highlights how concrete comparisons between the self and a typically single referent shape self‑perception, affect, and behavior (for a review, see Gerber et al., 2018). Accordingly, social comparison theory offers a valuable lens for understanding how people react to concrete information about proximal income inequalities within their immediate social environments. The present research builds on and extends this perspective to better understand how extreme upward pay comparisons influence individual outcomes.

Specifically, we examine how, when, and why individuals react positively to concrete information about a higher-ranking person earning far more than their own salary (i.e., their CEO). In this way, we go beyond positive reactions to abstract and ambiguous information about inequality in socio-economic systems (Brown-Iannuzzi et al., 2015; Jost & Hunyady, 2005). Instead, we ask whether and when people can overcome the potential sting and envy, and react positively to concrete information about large vertical pay inequalities between themselves and others.

Understanding the proximal psychological processes that unfold in such situations is of great societal importance, as it would help explain the paradox of limited public response to blatant pay inequality. In turn, this may help to shed light on the factors that can foster acceptance of the inequality, thereby ultimately perpetuating corporate and societal inequality (Piketty, 2014). We develop and propose a novel social comparison perspective that counterintuitively suggests large disparities between one’s own pay as an employee and the CEO’s pay may, under specific conditions, be personally inspiring rather than detrimental. Instead of undermining employees’ relationships with their CEOs or fostering negative attitudes toward them (Steffens et al., 2020), we argue that disparities between CEO and one’s own pay can, under certain conditions, be perceived as acceptable.

Being Inspired by the Fortunes of Others

Social comparisons are so central to psychological functioning that they occur spontaneously, with little effort, even when objectively irrelevant (Gilbert et al., 1995; Mussweiler & Epstude, 2009). Upward comparisons are more likely than downward comparisons (Gerber et al., 2018). Typically, comparisons with upward standards lead to contrast effects—judgments that are shifted away from a comparison standard—on self‑perception, motivation, and affect (D. J. Brown et al., 2007; Gerber et al., 2018; Mussweiler et al., 2004), especially for comparisons with extremely discrepant standards (Barker & Imhoff, 2021). Indeed, in everyday social comparisons, in-the-moment upward comparisons to extreme standards are demotivating (Diel et al., 2021), leading to weaker motivations to improve (“pushing”) and greater intentions to give up (“disengagement”). Thus, comparing one’s own earnings to that of the extreme pay standard of Satya Nadella, for example, generally evokes dissatisfaction and diminished motivation.

Importantly, however, the effects of upward comparisons to extreme standards do not inevitably lead to adverse outcomes (Diel et al., 2021). Certain features of comparison standards can even elicit the opposite reaction, prompting motivational gains, affiliative responses, or positive attitudes. Specifically, if a person feels similar to the comparison standard on a dimension that is not directly related to the focal dimension of extreme difference, then assimilative tendencies result (e.g., Brewer & Weber, 1994; J. D. Brown et al., 1992; for suggestive meta-analytic evidence, see Gerber et al., 2018). So, if an individual perceives the comparison standard as similar, for example, having attended the same school, they may be more accepting of that person’s substantially higher pay.

This process can be understood based on the Selective Accessibility Model (SAM; Mussweiler, 2003), which proposes that comparison processes begin with a rapid, holistic assessment of target–standard similarity that is based on only a few salient cues, including non‑focal characteristics (E. E. Smith et al., 1974; Mussweiler, 2003). Although coarse (“Is this standard generally more similar or dissimilar to me?”), this initial judgment guides subsequent processing: when similarity is perceived, individuals test a similarity hypothesis and activate broad self‑knowledge that is consistent with the assumption that they resemble the standard (Mussweiler & Strack, 2000). In upward comparisons, even to extreme standards, this broad activation extends to general, positively valenced self‑possibilities, prompting individuals to envision improved versions of themselves and assimilate their self‑evaluations toward the standard (Mussweiler & Strack, 2000; Mussweiler et al., 2004). Notably, this bond of similarity can arise from many sources—belonging to the same social group (Mussweiler & Bodenhausen, 2002), being close friends (Pelham & Wachsmuth, 1995) or even being born on the same day (J. D. Brown et al., 1992). Regardless of its source, this heightened sense of similarity fosters assimilative tendencies.

Importantly, these assimilative self‑views are closely tied to motivational tendencies (Lockwood & Kunda, 1997). Judges who engage in similarity testing with an extreme upward comparison standard not only activate self‑knowledge consistent with this hypothesis but also trigger corresponding motivational responses, such as inspiration. To understand how perceived similarity shapes motivation, we draw on the dominant model of inspiration, which includes three key components (Thrash & Elliot, 2003; Thrash et al., 2014): evocation, becoming receptive to being influenced by an external source; transcendence, recognizing better possibilities exist as exemplified by the source; and approach motivation, the drive to pursue and approach those possibilities.

Integrating SAM with this model of inspiration clarifies how perceived similarity on a non‑focal dimension can render an extreme upward standard inspiring. First, judging an extreme standard as similar on a non‑focal dimension increases individuals’ openness to being influenced by the standard, reflecting evocation. Second, subsequent similarity‑hypothesis testing and the selective activation of positive self‑aspects enable individuals to transcend their current state by envisioning better future possibilities. Third, the combination of evocation and transcendence energizes the individual, fostering motivation to actively approach and pursue these newly perceived possibilities. In this way, the tripartite model helps explain how non‑focal similarity can transform an otherwise discouraging upward comparison into an inspiring one—an idea central to our research.

Applying these ideas to the context of large vertical pay inequality reveals an intriguing possibility. The pervasive negative consequences of exposure to extreme CEO pay documented to date may be limited to employees who perceive their CEOs as inherently dissimilar to themselves. Indeed, CEOs’ elevated pay levels themselves may further accentuate this sense of distance and weaken the potential social bond between leaders and followers (Steffens et al., 2020). In contrast, we believe that when employees perceive similarity with an extreme CEO standard, then positive consequences are likely. If employees see their CEO as similar on a dimension unrelated to the focal pay comparison—such as sharing a birthday or core values—this perception can foster heightened receptivity to the CEO standard’s influence. Such influence may take the form of elevated expectations about the attainability of more positive, general career outcomes (Cullen & Perez-Truglia, 2022; Steffens et al., 2020). As a result, employees may feel more motivated and energized to pursue enhanced future possibilities in their careers. This sense of inspiration, in turn, renders the CEO’s extremely high pay more acceptable. For example, perceiving oneself as similar to Satya Nadella could make him more inspiring and, consequently, increase one’s positive attitude toward his exceptionally high compensation.

In summary, we develop a novel social comparison perspective arguing that even exposure to large pay inequality can elicit positive reactions that ultimately make such inequality more acceptable. We examined the how, why, and when of positive responses to concrete, local pay disparities. Specifically, we hypothesized that perceiving greater similarity with a CEO enhances acceptance of large pay inequality, driven by feelings of inspiration.

Overview of Studies

We tested our hypotheses across four studies. Study 1 used a large international archival dataset to provide an initial, indirect test of whether respondents who perceived themselves as more similar to CEOs in social status were less supportive of policies aimed at reducing economic inequality. Study 2 sought to replicate this link among working adults evaluating their own CEO, while also testing inspiration as the theorized mediator. To assess the scope of the similarity effect and construct validity, we included two indicators of perceived similarity: an indirect measure (i.e., social-status similarity, as used in Study 1) and a more direct measure capturing general perceived similarity, allowing us to assess whether the predicted relationship emerged across different operationalizations of the construct. Studies 3–4 experimentally replicated the main and mediation effects to provide causal evidence. In these experiments, participants imagined themselves as new employees, perceived similarity to the CEO was manipulated on dimensions unrelated to pay, and we measured how inspired they felt and acceptance of their CEO pay. 1 Study 3 also manipulated pay-ratio magnitude and included perceived CEO competence as an alternative mediator. Finally, Study 4 tested a key theoretical boundary condition implied by social comparison theory: whether the effect of perceived similarity depends on the attainability of the CEO standard, operationalized through promotability within the organization.

In Study 1, we utilized all available International Social Survey Programme (ISSP) data relevant to our focal variables. This study was not pre-registered. Studies 2–4 were pre-registered. We report all measures, manipulations, and data exclusions in these studies. Target sample sizes were determined a priori, and we did not collect data after analysis. Informed consent was obtained from all participants, and we received institutional ethics approval. All experimental materials, pre-registrations, data, code, and supplementary analyses have been publicly posted in a public data repository: https://osf.io/xjz6v/overview?view_only=323b298310524146911f904db3e7baf2

Study 1

Study 1 used archival, cross-national survey data to examine whether respondents who indirectly indicated greater similarity to CEOs would express higher acceptance of pay inequality. This design allowed us to assess whether the relationship holds across societies that vary in their actual levels of pay inequality and in their broader inequality contexts.

Method

Data and Respondents

We analyzed data from the ISSP’s social inequality module, a cross-national collaboration collecting annual social science surveys (ISSP Research Group, 2024). This module included surveys of 35 countries with 157,446 respondents (Mage = 46.82, SDage = 17.18; 53% female and 47% male), a subset of whom answered the relevant questions: 36,982 respondents from 24 countries (without control variables), and 10,637 respondents from 14 countries (with control variables). We tested our main prediction that perceived similarity to a CEO is associated with lower support for income inequality reduction.

A multilevel sensitivity power analysis (α = .05; two-tailed, for Model 3, Table 2, Ncountries = 14 and Nresponses = 10,637) based on Monte Carlo simulations using the SIMR package (Green & MacLeod, 2016), showed 83% power to detect a coefficient of 0.015.

Measures

Outcome Variables

Support for Income Inequality Reduction

To capture the desire to reduce income inequality we gauged participants’ support for income inequality reduction, using a composite of four items (α = .68): Income differences in (R’s country) are too large (1 = Strongly agree, 5 = Strongly disagree; reverse scored); Government should reduce income differences (1 = Strongly agree, 5 = Strongly disagree; reverse scored); Should people with high incomes pay more taxes? (1 = Much larger share, 5 = Much smaller share; reverse scored); How are taxes in (R’s country) for those with high income? (1 = Much too high, 5 = Much too low). 2

Predictor Variable

Social-Status Perceived Similarity

To indirectly assess perceived similarity to a CEO in terms of social status, we used two items that captured respondents’ perceptions of their own social standing and that of a corporate chairman. Participants read, “In our society, there are groups which tend to be toward the top and groups which tend to be toward the bottom. Below is a scale that runs from top to bottom.” Respondents then indicated, separately, “where would you put yourself and your family now on this scale” and “where would you put a chairman of a corporation now on this scale” (1 = Top, 7 = Bottom). We calculated the absolute value of the difference between self- and chairman scores and reversed-scored this value, such that higher scores indicated greater social-status perceived similarity to a CEO.

Control Variables

To isolate the impact of social-status perceived similarity on support for income distribution, we controlled for various potential confounds derived from the ISSP. Specifically, since socioeconomic status and perceived societal inequality are known to shape attitudes toward redistribution (Brown-Iannuzzi et al., 2015, 2021; Cruces et al., 2013) and could influence social-status perceived similarity to CEOs, we included a comprehensive assessment of four different self-reports of objective and subjective social class as controls, namely: Education level (1 = Lowest formal qualification to 5 = University degree completed, graduate studies), Income level (1 = Low, 2 = Medium, 3 = High), Occupational status as a fixed effect (International Standard Classification of Occupations—ISCO-562 career/job classifications), and a Subjective social class measure (1 = Lower class/Poor/Bottom to 6 = Upper class). Importantly, we controlled for the potential confounding role of individuals’ perceived level of inequality in society at large. Participants were shown five diagrams depicting different types of societies and asked what type of society their country resembles today (1 = A small elite at the top, very few people in the middle and the great mass of people at the bottom to 5 = Many people near the top and only a few near the bottom). Finally, we included age, gender, and a fixed effect for political ideology.

Results

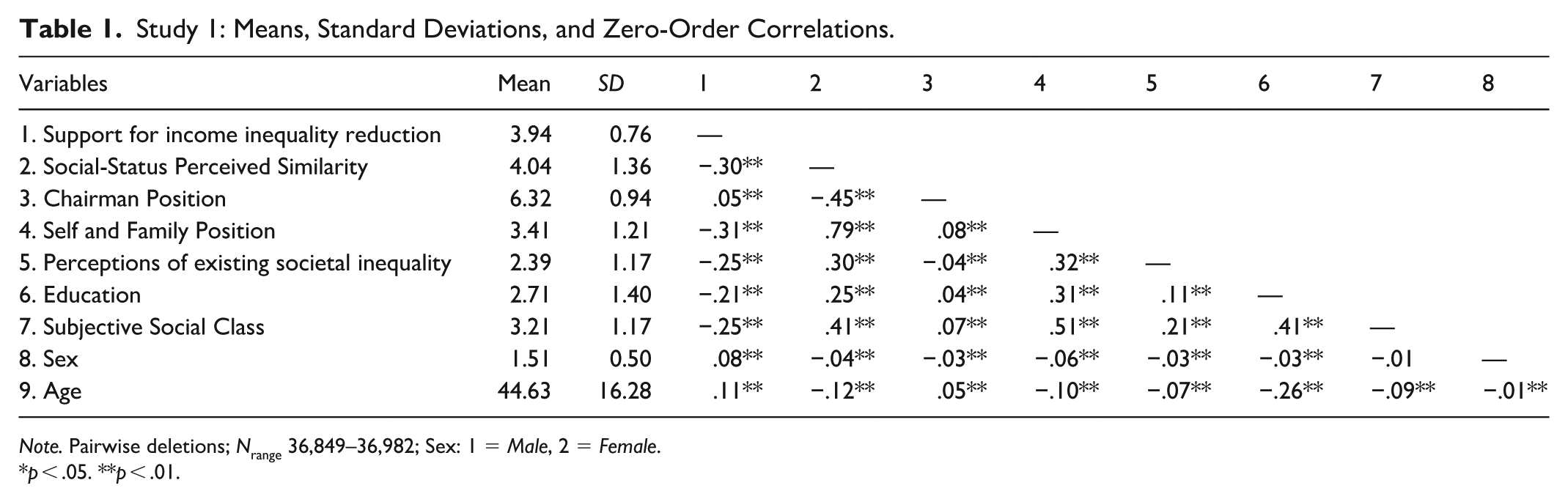

Descriptive statistics and correlations for key variables are presented in Table 1.

Study 1: Means, Standard Deviations, and Zero-Order Correlations.

Note. Pairwise deletions; Nrange 36,849–36,982; Sex: 1 = Male, 2 = Female.

*p < .05. **p < .01.

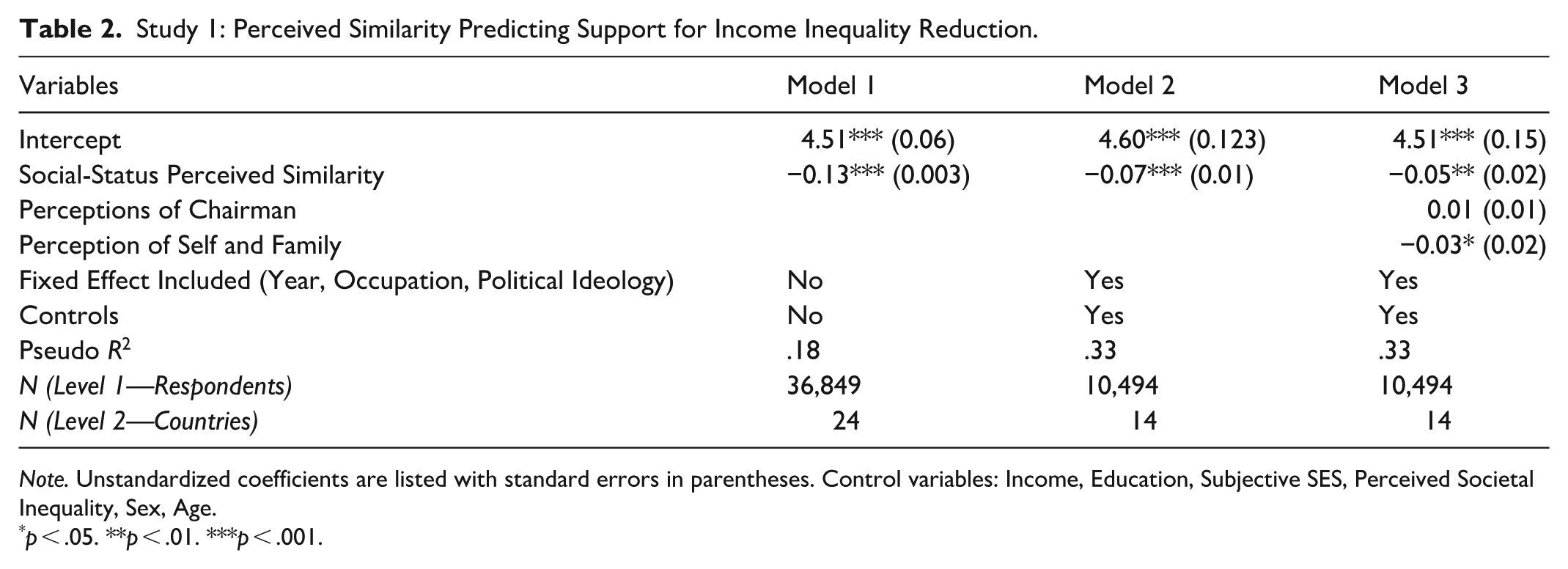

To test our main hypothesis, we performed several multilevel mixed-effects regression analyses on support for income inequality reduction. We modeled the country as a higher-level factor to account for shared national contexts. The first model included only our predictor variable social-status perceived similarity (Model 1, Table 1; Quoidbach et al., 2013). In Model 2, we added the control variables and fixed effects. As predicted, we found a negative association between social-status perceived similarity and support for inequality reduction: The more similar respondents perceived themselves to a CEO, the less they supported inequality reduction. This association was observed without controls (b = −0.13, SE = 0.003, t[36,847] = 46.54, p < .001, Table 2 Model 1), and with controls and fixed effects (b = −0.07, SE = 0.006, t[10,003] = 12.26, p < .001, Table 2 Model 2).

Study 1: Perceived Similarity Predicting Support for Income Inequality Reduction.

Note. Unstandardized coefficients are listed with standard errors in parentheses. Control variables: Income, Education, Subjective SES, Perceived Societal Inequality, Sex, Age.

p < .05. **p < .01. ***p < .001.

As additional robustness checks, we re‑estimated these models including country fixed effects and decomposed social-status perceived similarity into its within‑country and between‑country components. Reassuringly, the within-country component remained negatively associated with support for inequality reduction across specifications, indicating that the observed relationship reflects within-country variation rather than cross-national differences (See Supplemental Materials for the full analyses).

Furthermore, since absolute difference scores may also capture variance from the simple main effects of their components (Kenny, 1988; Murray et al., 2002), we also controlled for the two main effects of the similarity difference-score components (perceived self- and chairman-scores; see also Watson et al., 2004) and the effect held (b = −0.05, SE = 0.02, t[10,001] = 3.15, p = .002, Table 2 Model 3).

Taken together, these findings provide initial and suggestive support for perceived similarity breeding acceptance for pay inequality, beyond both actual and perceived social class levels, as well as distal perceptions of societal-level inequality.

Study 2

Study 2 had three primary goals. First, we sought to replicate the effect of perceived similarity on acceptance of high CEO pay ratios, focusing on how working adults evaluated their own CEOs. Second, we sought to enhance the construct and convergent validity of the suggestive Study 1 findings. Our theorizing holds that perceived similarity on different dimensions produces unitary effects. To test this, we used a broader, more explicit measure of perceived similarity, assessing both social-status similarity (Study 1) and general similarity. This allowed us to examine whether these measures converged and whether the predicted relationship with pay acceptance held across different operationalizations of perceived similarity. Finally, we sought initial support for our new hypothesized mediator, inspiration.

Method

Participants

We aimed to recruit 450 U.S. participants via Prolific Academic. The target sample size was guided by effect sizes observed in a preliminary pilot study. A total of 447 participants who reported working part-time or full-time completed the study (see pre-registration https://aspredicted.org/M19_HWF). In line with our pre-registered criteria, we excluded one participant who indicated they were not currently employed, five for having duplicate I.P. addresses, and five for using an autocompletion macro. The final sample consisted of 436 participants (46% female, 52% male; 2% non-binary or preferred not to report; Mage = 40.75, SDage = 11.98). The results hold for the entire sample. For linear multiple regression, sensitivity power analysis using seven predictors and standard criteria α = .05 and 1 − β = .80 revealed a minimum effect size that could be detected of f2 = 0.03.

Procedures

Participants first provided general information about the company they worked for. Next, they were informed that they would be asked questions about the head of their company, which may be titled CEO, President, or Managing Director. Participants provided either the person’s first name or initials and demographics to ensure they had a specific person in mind. This response was then inserted into all relevant questions.

Participants then provided what they either know or believe the CEO’s annual salary to be. They then completed two perceived-similarity measures with the CEO (order randomized), followed by how inspired they were by the person, and finally, how acceptable they viewed the person’s salary. Before completing the demographics, we asked participants to rate the accuracy of their estimate of the CEO’s salary, ranging from 0 (Not accurate at all) to 100 (Very accurate) with 10-point increments.

Measures

Perceived Similarity

Participants completed two measures of perceived similarity. One measured similarity in social status, similar to Study 1. Here, participants placed themselves and the head of their company on a 10-rung ladder on which those who are the best off are placed at the top and those who are the worst off are placed at the bottom. This self-report measure is commonly employed to evaluate subjective socioeconomic status (Adler et al., 2000). Again, we calculate the absolute value of the difference between self (i.e., their subjective SES) and head-of-company (i.e., perceived CEO’s SES) and reverse-scored this value, such that larger numbers indicate greater perceived similarity to the CEO.

The second measure gauged more directly perceptions of general similarity using three items (e.g., “Please indicate the extent to which you feel similar to the head [name inserted] of your company,” 1 = Not at all to 7 = Extremely; α = .96; Goldstein & Cialdini, 2007). The difference-based societal status similarity and direct general similarity measures were correlated, r(433) = .45, p < .001, providing evidence that the two indicators converge while still capturing different dimensions of perceived similarity (Funder & Ozer, 2019).

Inspiration

Participants indicated how much they felt: Inspired, Energized, and Motivated in relation to their CEO (1 = Not at all to 7 = Extremely; α = .97). 3

Acceptability of CEO Pay

Participants indicated the extent to which they agreed that the CEO’s salary is: Too High (reverse scored), Reasonable, Appropriate, and Acceptable (1 = Strongly disagree to 7 = Strongly agree; α = .93).

Results

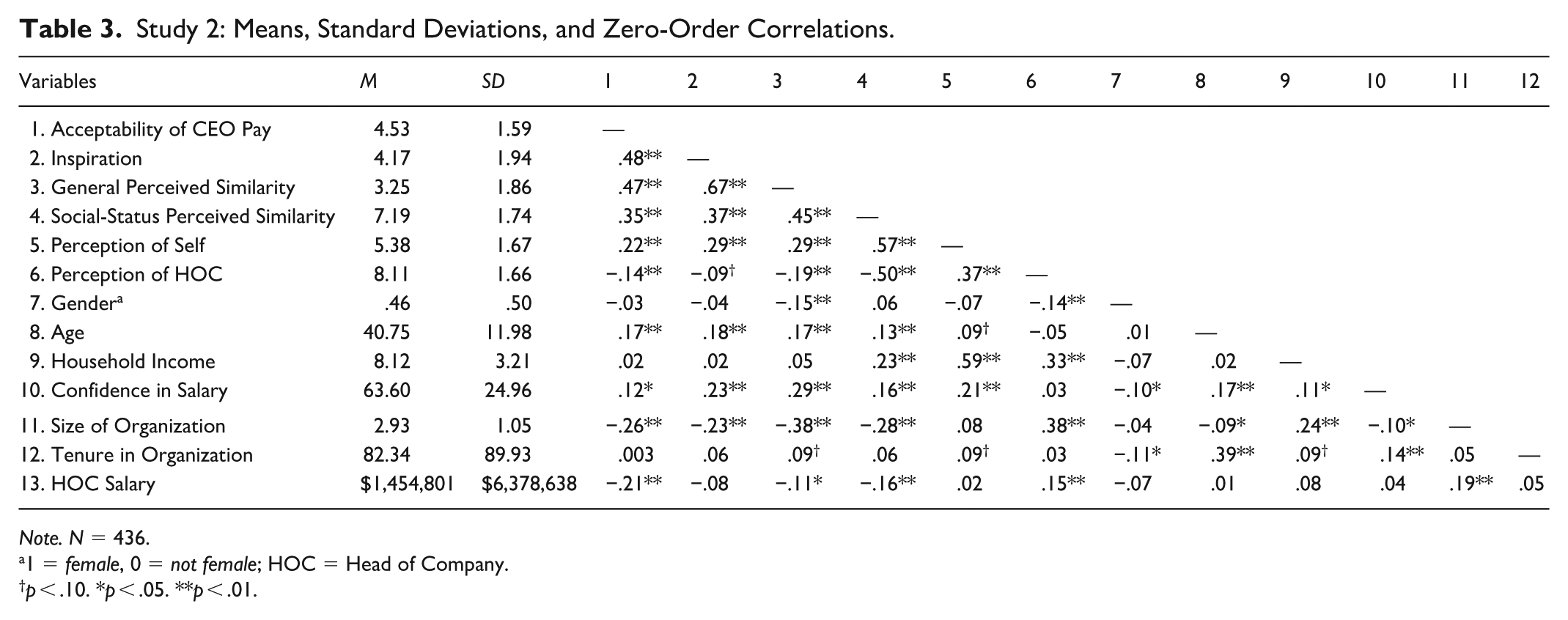

Descriptive statistics and correlations are presented in Table 3.

Study 2: Means, Standard Deviations, and Zero-Order Correlations.

Note. N = 436.

1 = female, 0 = not female; HOC = Head of Company.

p < .10. *p < .05. **p < .01.

In the analyses, we included the following controls: Gender, Age, Household income, Number of employees in the organization, Tenure in the organization (months), Confidence in their CEO’s salary prediction, and Estimation of the CEO’s salary. Similar to Study 1, for the social-status perceived similarity difference score, we included its two components as controls (Murray et al., 2002; Watson et al., 2004). The inclusion of all the control variables did not change the results. Specifically, we find that the results hold when controlling for subjective SES levels, as captured in the perceptions-of-self measure, which indicates one’s perceived position within society, as well as an objective measure of social class, namely, self-reported household income. 4 We report the results below without controls; however, Table 4 provides results with and without controls for reference—results do not change.

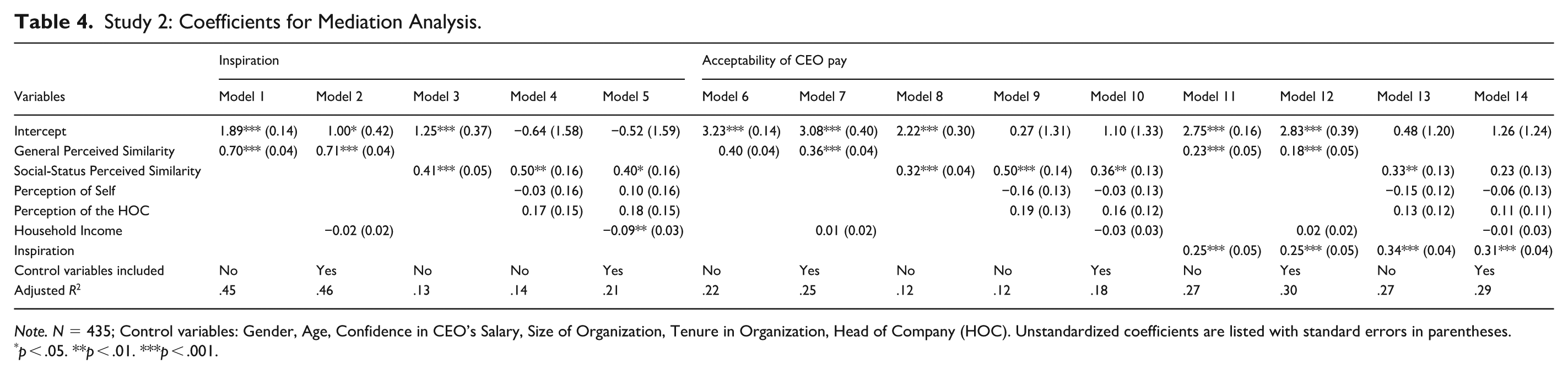

Study 2: Coefficients for Mediation Analysis.

Note. N = 435; Control variables: Gender, Age, Confidence in CEO’s Salary, Size of Organization, Tenure in Organization, Head of Company (HOC). Unstandardized coefficients are listed with standard errors in parentheses.

p < .05. **p < .01. ***p < .001.

Acceptability of CEO Pay

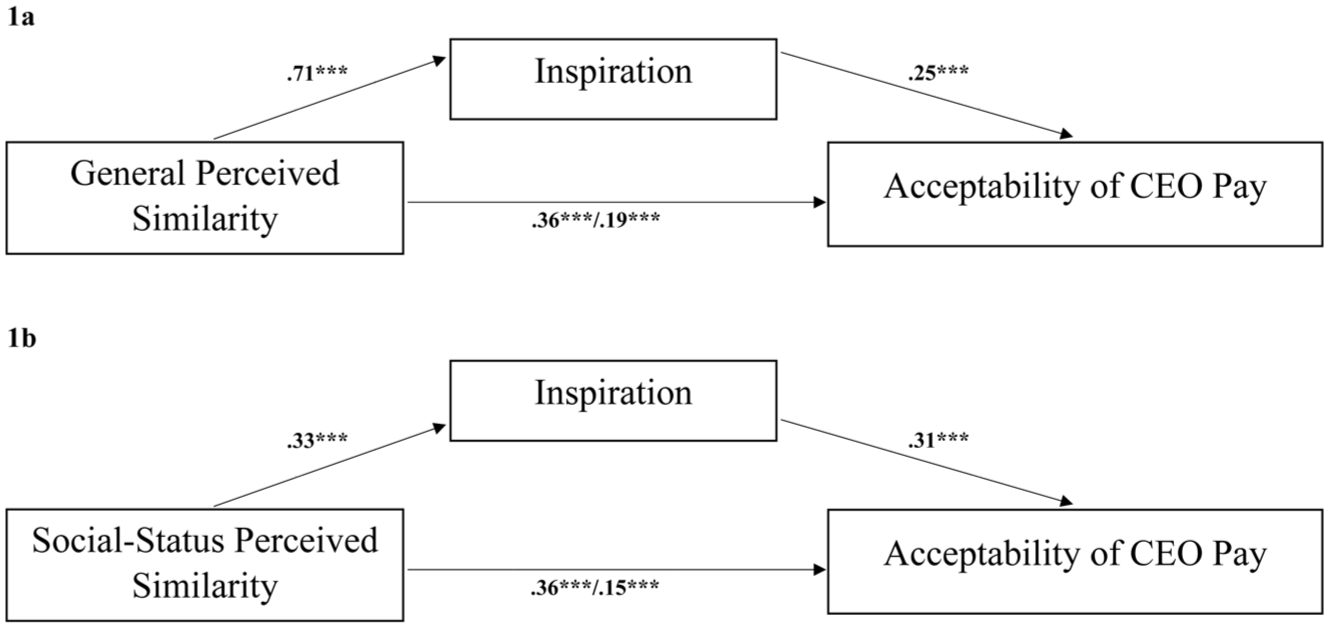

As predicted, an ordinary least squares regression indicated that direct measures of general perceived similarity (b = 0.40, SE = 0.04, t[434] = 11.07, p < .001, Table 4 Model 6) and of social-status perceived similarity (b = 0.32, SE = 0.04, t[434] = 7.83, p < .001, Table 4 Model 8) were positively related to viewing the CEO’s salary as being acceptable.

Indirect Effect

To test the mediating effect of perceived similarity on the acceptability of the CEO’s salary via inspiration, we ran a separate model for each of the two measures using PROCESS macro 4 for SPSS with 10,000 bootstraps. As predicted and as depicted in Figures 1a and 1b, we found a positive indirect effect for both general perceived similarity, a*b = 0.18, SE = 0.05, 95% CI [0.100, 0.257], and social-status perceived similarity, a*b = 0.14, SE = 0.04, 95% CI [0.092, 0.188].

Study 2: Mediation tests of two types of perceived similarity on the acceptability of CEO pay via inspiration.

Taken together, these findings provide initial support for perceived similarity in shaping acceptance of pay inequality. This pattern emerged for both indirect, status-based measures and direct, general measures of perceived similarity, and was mediated by inspiration. Importantly, these results also held when accounting for SES levels, both subjective and objective.

Study 3

Study 3 marked a shift from the observational designs used in Studies 1–2 to an experimental design, providing stronger causal evidence for the main and mediation effects. In this design, participants imagined working for a fictitious clothing company and read about an interaction with a CEO whose similarity to them was experimentally manipulated. A pre-registered version of this basic experiment (see Supplemental Materials) supported our predictions that perceived similarity enhanced the acceptability of CEO pay, via inspiration.

A central aim of this study was to examine whether the effect of perceived similarity is especially relevant when CEO–employee pay inequality is large rather than small. To test this, we orthogonally manipulated the size of the pay ratio between the participant and the CEO. Drawing on prior work showing that large pay disparities are particularly aversive, demotivating, and difficult to accept (Benedetti & Chen, 2018; Kiatpongsan & Norton, 2014; Mohan et al., 2018), we reasoned that perceived similarity and the resulting inspiration should be especially consequential for these reactions under high pay ratios, where there is more negativity to mitigate. In our 2 (similarity) × 2 (pay ratio) design, with inspiration and pay acceptability as outcomes, we predicted that similarity would increase inspiration across both pay ratios. However, we expected that this inspiration would be more likely to translate into greater acceptance of pay inequality under high ratios than under low ones, consistent with a second-stage moderated mediation.

A second aim of Study 3 was to examine a plausible alternative mechanism: that similarity increases pay acceptability because it leads participants to evaluate the CEO more favorably, particularly as more competent and thus more deserving of high pay. To assess this possibility, we included perceived CEO competence as a competing mediator. This allowed us to test whether the effect of similarity on pay acceptability operates primarily through inspiration as a motivational process rather than through more favorable evaluations of the CEO’s ability.

Method

Participants

Based on pre-tests, we expected a main effect size of δ = .20, and given our moderation hypothesis, we aimed to recruit 1,600 U.S. participants via Prolific Academic (see https://aspredicted.org/f647-2rqq.pdf). A total of 1,732 participants completed the study. Based on pre-registered criteria, we excluded 175 participants for failing an attention-check question, 18 for having a duplicate IP address, 12 for using an autocomplete macro, and 1 person who did not finish the study. The final sample consisted of 1,526 participants (58% female, 40% male, and 2% non-binary or preferred not to report; Mage = 41.38, SDage = 12.29; 99% full-time or part-time employees; 91% had college experience). The results do not change when run on the entire sample. A sensitivity power analysis (α = .05; two-tailed) showed that Study 3 has 80% power to detect an effect size of f2 = 0.07. We utilized a 2 × 2 between-subject design: Similarity (High, Low) by Ratio (High, Low).

Procedures

Participants were asked to imagine that they had joined an apparel company called WorkWear Inc. Importantly, they were told that the job would pay them $50,000 a year and allow them to utilize their skills and develop professionally. To increase engagement with the scenario, participants were prompted to reflect and write at least 100 characters regarding their professional strengths, values, and qualities that they could bring to the job. Next, participants were told that part of their onboarding required them to introduce themselves and select from a list of eight values the four they valued most: Loyalty, Self-Reliance, Humility, Compassion, Honesty, Kindness, Integrity, and Selflessness. Next, participants were informed that they would meet their CEO, Riley Banner, the following week. We used the name Riley, given its unisex nature, and thus we did not refer to the CEO’s specific gender (Flowers, 2015).

Participants were told they would be meeting the CEO because they had been put in charge of a new project. In preparation for the meeting, participants received background information. They were told that Riley had been CEO of the company for 5 years and is generally held in high esteem across the industry. Participants in the high CEO pay ratio condition were told that the CEO received an annual salary of $5,000,000 (a ratio of 100:1 compared to their salary); in the low CEO pay ratio condition, they were shown a pay ratio of 7:1 (the CEO received an annual salary of $350,000). As per our pre-registration, participants who failed to identify the CEO’s pay were removed from the study. We selected this pay ratio of 100:1 to strike a balance between laypeople’s underestimates of actual pay inequality (Kiatpongsan & Norton, 2014) and the even larger pay ratios typical of the most successful companies (Bivens & Kandra, 2022). We used a 7:1 for the low pay ratio because it was found to be the ideal ratio in the United States (Kiatpongsan & Norton, 2014).

Participants in the high-similarity condition were told they were from the same U.S. region and attended the same university. Those in the low-similarity condition were told they were from different regions in the United States and attended different universities. Participants were matched based on demographic survey items they completed at the beginning of the study. Next, Riley introduced themselves and asked the participant which values they selected and about their background more generally. In the high-similarity condition, participants further learned that Riley had selected beforehand the same four values and said, “Very interesting, it seems we are very similar.” In the low-similarity condition, Riley did not overlap in values and said, “Very interesting, it seems we are rather different.” In developing these manipulations, we ensured that Riley’s verbal and non-verbal behaviors were held constant across conditions, consistently reflecting pleasant and polite behaviors. Participants then completed the manipulation check, dependent measures, and were debriefed and paid.

Measures

Perceived Similarity and Inspiration

We used the same measures from Study 2 (αsimilarity = .96 and αinspiration = .96).

Acceptability of Pay Inequality

Participants indicated the extent to which they agreed that the CEO’s salary, compared to their salary, is: Too High (reverse scored), Reasonable, Appropriate, and Acceptable (1 = Strongly disagree to 7 = Strongly agree; α = .94).

Perceived CEO Competence

We used a 7-item competence measure (e.g., competent, confident, capable, efficient, intelligent, skillful, and hard-working) adapted from prior research on competence as a core dimension of social perception (1 = Strongly disagree to 7 = Strongly agree; α = .94; Abele & Wojciszke, 2007; Fiske et al., 2002).

Results

Descriptive statistics and correlations are provided in the Supplemental Materials.

Manipulation Check

We performed a 2 (similarity) × 2 (pay ratio) analysis of variance (ANOVA) on perceived similarity. The resulting analysis for perceived similarity indicated the intended main effect of the similarity manipulation, F(1, 1522) = 1,821.99, p < .001, η2p = .55. Participants in the high-similarity condition reported greater similarity (M = 5.49, SD = 1.18) than participants in the low-similarity condition (M = 2.71, SD = 1.37). There was also a smaller main effect of CEO pay ratio, F(1, 1522) = 15.70, p < .001, η2p = .01; Mhigh ratio = 3.99, SD = 1.89; Mlow ratio = 4.22, SD = 1.88). The interaction was not significant, F(1, 1522) = 0.01, p = .91, η2 p < .001.

Acceptability of Pay Inequality

We predicted that participants would be more accepting of their high CEO salary in the high-similarity condition relative to the low-similarity condition. We also explored the interaction between similarity and pay ratio on pay inequality acceptability. A 2 (similarity) × 2 (pay ratio) ANOVA revealed the predicted main effect for similarity, F(1, 1522) = 4.99, p = .026, η2 p = .003: participants were more likely to accept pay inequality when they were in the high-similarity condition (M = 3.68, SD = 1.64) compared to the low-similarity condition (M = 3.52, SD = 1.61). There was also a main effect for CEO pay ratio, with participants in the high CEO pay ratio condition indicating the relative pay was less acceptable (M = 3.02, SD = 1.54) than the low CEO pay ratio condition (M = 4.20, SD = 1.49), F(1, 1522) = 231.06, p < .001, η2 p = .13.

Finally, a marginally significant interaction emerged, F(1, 1522) = 3.48, p = .06, η2 p = .002. Planned contrasts revealed a pattern consistent with our theorizing. Consistent with the previous studies, in the high pay ratio condition, participants were more accepting of the relative CEO pay difference when they were in the high versus low similarity condition (Mhigh similarity = 3.18, SDhigh similarity = 1.56 and Mlow similarity = 2.86, SDlow similarity = 1.51), t(1522) = 2.91, p = .004, d = 0.21. In the low pay ratio condition, in contrast, there was no effect of similarity (Mhigh similarity = 4.21, SDhigh similarity = 1.55 and Mlow similarity = 4.18, SDlow similarity = 1.44), t(1522) = 0.26, p = .792, d = 0.02.

Moderated-Mediation Model

We predicted that the effect of similarity on the acceptability of pay inequality via inspiration would be moderated by pay ratio, and this moderation would occur between inspiration and acceptability. To test this second-stage moderated-mediation model, we used PROCESS macro 14 for SPSS with 10,000 bootstraps. We also included CEO perceptions as a simultaneous mediator.

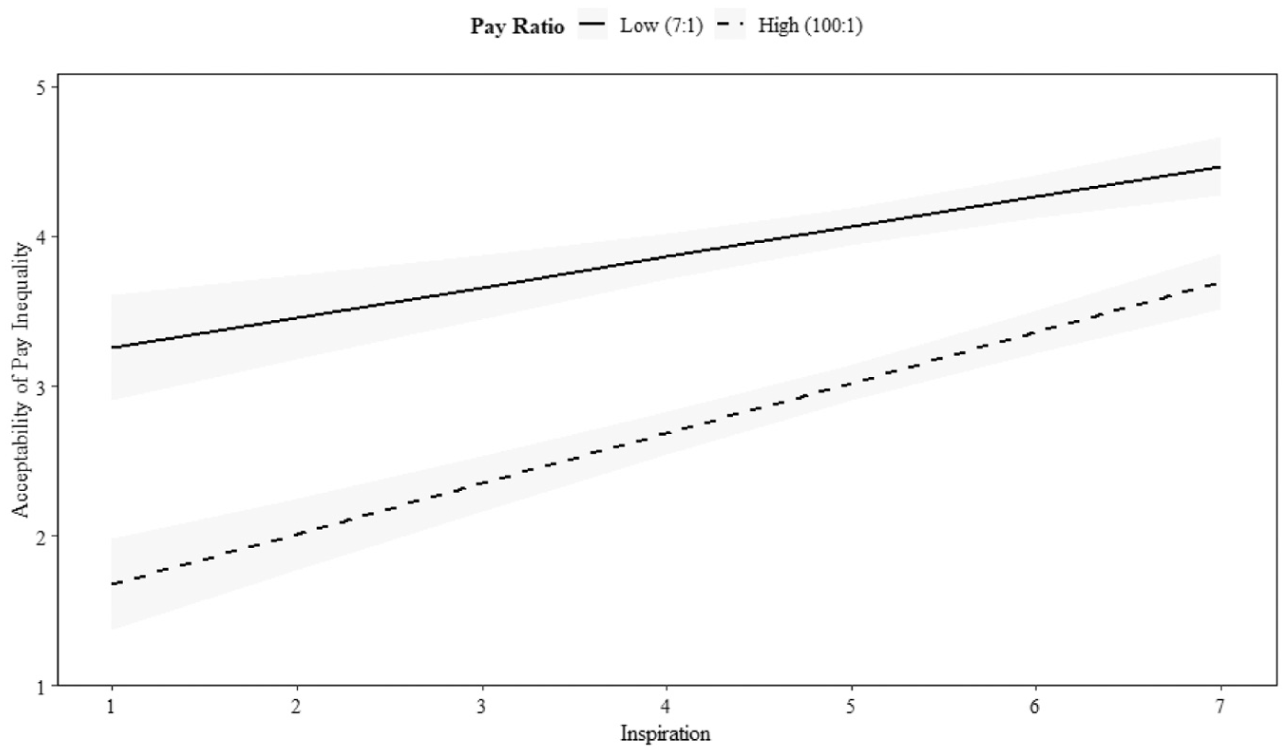

Consistent with our predictions, participants in the high-similarity condition reported greater inspiration (M = 5.49, SD = 1.31) than participants in the low-similarity condition (M = 4.02, SD = 1.63), b = 1.47, p < .001, f2 = 0.25. Additionally, participants in the high-similarity condition perceived the CEO as more competent (M = 6.06, SD = 0.72) than participants in the low-similarity condition (M = 5.67, SD = 0.87), b = 0.39, p < .001, f2 = 0.06. Results also revealed that, consistent with our second stage mediated moderation prediction, the interaction of inspiration by pay ratio on pay inequality acceptability was significant (see Figure 2), b = 0.13, SE = 0.05, 95% CI [0.021, 0.232].

Effect of inspiration and acceptability of pay inequality.

In support of our predictions, the extent to which inspiration influences views of pay acceptability was impacted by the CEO’s pay ratio, index of moderated mediation = 0.19, 95% CI [0.016, 0.357]. Specifically, the positive indirect effect of similarity on pay acceptability via inspiration was stronger for high CEO pay ratios, a*b = 0.48, SE = 0.07 [0.347, 0.605], than for low CEO pay ratios, a*b = .29, SE = 0.07 [0.161, 0.416]. In contrast, the moderated mediation was not significant for CEO perceived competence, b = −0.05 [−0.146, 0.039]. The indirect effect of similarity on pay acceptability via CEO competence was positive. However, it did not differ, whether for high CEO pay ratios, a*b = 0.08, SE = 0.03 [0.025, 0.155] or for low CEO pay ratios, a*b = 0.14, SE = 0.04 [0.071, 0.210].

Consistent with the unique effect and relative strength of our theorized mechanism, the indirect effect of inspiration on pay acceptance was significantly stronger than that of the viable alternative, perceived CEO competence, in the high pay-ratio condition, a*bdiff = 0.40, SE = 0.09, 95% CI [0.212, 0.571]. The two indirect effects did not differ in the low pay ratio condition, a*bdiff = 0.15, SE = 0.09 [−0.034, 0.324].

Study 4

Study 4 sought to strengthen causal evidence for the proposed underlying mechanism, this time through moderation as well as mediation, by testing a boundary condition: specifically, low attainability, operationalized as limited promotability within an organization. Previous research has demonstrated that perceptions of lower social mobility in the U.S. reduce people’s level of support for its current socio-political system, given the existing large levels of economic inequality in American society (Day & Fiske, 2017). We draw on this work to examine how participants’ perception of the promotability level in their immediate environment (i.e., their company) may moderate their positive reactions to their CEO’s high pay as a function of perceived similarity.

We theorized that if success in the company is perceived as largely unattainable (i.e., low promotability within the company), it would weaken the level of inspiration even for a CEO perceived as similar, resulting in lower acceptance of pay inequality across the board. In sum, we tested whether the indirect effect of similarity on pay acceptance via inspiration is moderated by attainability. To do this, we compared an average social mobility situation in which CEO achievements are (at least partially) potentially attainable, rendering a high-earning CEO likely to be more inspiring, with a low social mobility situation in which hierarchical advancement is largely unattainable, and as a result inspiration by the CEO is likely to be lower (Cullen & Perez-Truglia, 2022; Lockwood & Kunda, 1997).

Method

Participants

Based on pre-tests, we expected a main effect size of δ = .20, and given our moderation hypothesis, we aimed to recruit 1,650 U.S. participants via Prolific Academic (see pre-registration https://aspredicted.org/Y89_L1Q). A total of 1,661 participants completed the study. Based on pre-registered criteria, we excluded 417 participants for failing an attention-check question, 14 for having either duplicate or outside of the U.S. I.P. addresses, and 9 for using an autocompletion macro. The final sample consisted of 1,221 participants (52% female, 45% male, and 3% non-binary or preferred not to report; Mage = 36.04, SDage = 12.11; 98% full-time or part-time employees; 90% had college experience). The results hold for the entire sample. A sensitivity power analysis (α = .05; two-tailed) showed that Study 4 has 80% power to detect an effect size of f2 = 0.08. We utilized a 2 × 2 between-subject design: Similarity (High, Low) by Promotability (Average, Low).

Procedures

Participants engaged in the same procedure as in Study 3 with a few changes, see below. As before, participants were asked to imagine that they had joined an apparel company called WorkWear Inc., told that the job would pay them $50,000, and engaged in the same reflection task. Next, they selected from the list of eight values the four they valued most before receiving the background information, meeting their CEO, receiving the similarity manipulation, and completing its manipulation check. Unlike Study 3, CEO pay ratio was not manipulated. Rather, based on our findings from Study 3, we used the high 100:1 pay ratio for all participants.

Participants were also given information regarding the company’s internal promotion rates. To enhance external validity and keep CEO power high and constant, participants were told that Riley was largely uninvolved in promotion decisions directly; however, Riley had determined their procedures and guidelines. Participants in the low-promotability condition were told that the chances of receiving an internal promotion were low, with the company having the lowest rates in the industry, with practically zero internal promotion opportunities. Participants in the average-promotability condition were told that the chances of receiving an internal promotion were similar to the industry average, with some internal promotion opportunities. They then completed the promotability manipulation check, dependent measures, and were debriefed and paid.

Measures

Promotability Manipulation Check

To assess perceived promotability, participants indicated what they imagined their highest attainable job would be (1 = Current Position to 7 = CEO).

Perceived Similarity and Inspiration

We used the same measures from Studies 2–3 for these (α = .96 and α = .97, respectively).

Acceptability of CEO Pay

We used the same measure as in Study 2 (α = .95). 5

Results

Descriptive statistics and correlations are presented in the Supplemental Materials.

Manipulation Checks

We performed a 2 × 2 ANOVA on the self-other overlap and promotability manipulation checks, respectively. The resulting analysis for self-other overlap indicated the intended main effect of the similarity manipulation, F(1, 1217) = 1,554.88, p < .001, η2 p = .56. Participants in the high-similarity condition reported greater similarity (M = 5.43, SD = 1.22) than participants in the low-similarity condition (M = 2.64, SD = 1.24). There was no main effect of promotability, F(1, 1217) = 0.22, p = .64, η2 p < .001, and no interaction, F(1, 1217) = 0.27, p = .60, η2 p < .001. Overall, the similarity manipulation was effective.

A similar analysis for the perceived promotability revealed the intended main effect for promotability with its perception being higher in the average-promotability (M = 4.52, SD = 1.43) than in the low-promotability condition (M = 3.22, SD = 1.73), F(1, 1217) = 207.91, p < .001, η2 p = .15. There was also a much smaller, yet statistically significant, main effect of the similarity manipulation, F(1, 1217) = 9.01, p = .003, η2 p = .01. Promotability perceptions were higher in the high-similarity (M = 3.97, SD = 1.71) than in the low-similarity condition (M = 3.75, SD = 1.72). There was no interaction, F(1, 1217) = 0.07, p = .79, η2 p < .001. Thus, the promotability manipulation was successful.

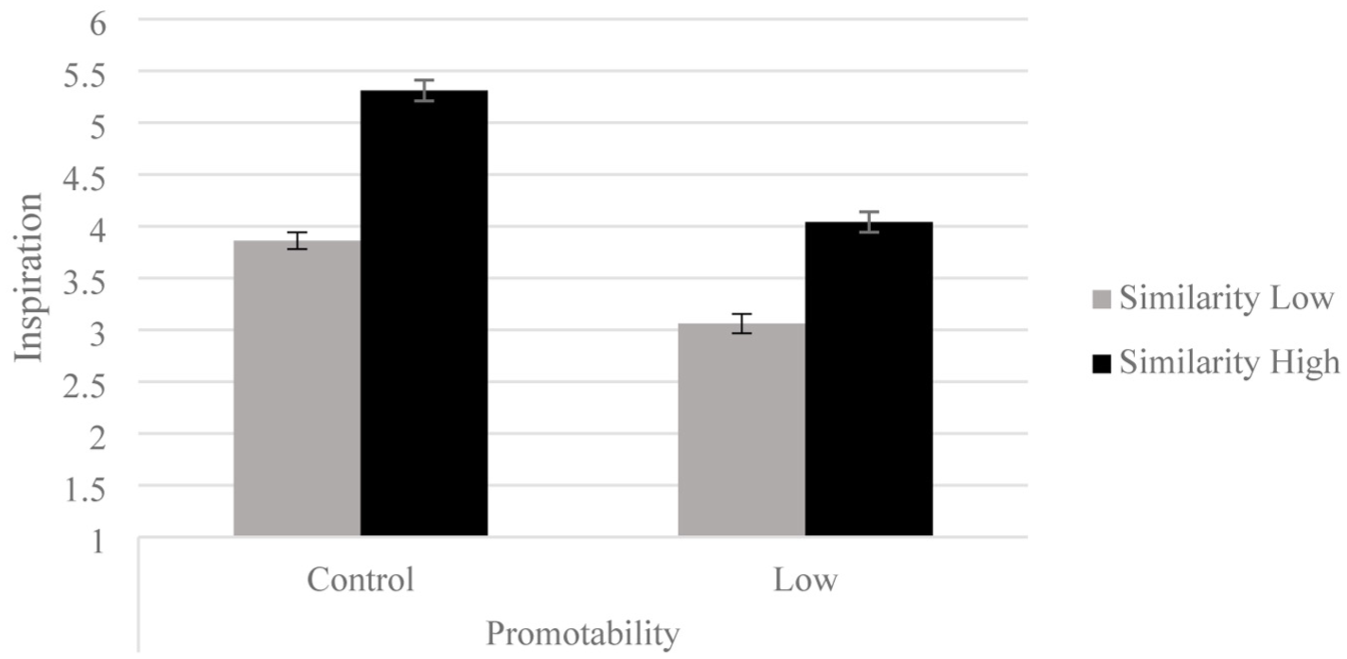

Inspiration

To test whether the effect of similarity on inspiration was conditional on promotability, we subjected inspiration to a 2 × 2 ANOVA. This resulted in significant main effects for similarity, F(1, 1217) = 167.79, p < .001, η2 p = .12, promotability, F(1, 1217) = 122.28, p < .001, η2p = .09, and importantly a significant interaction, F(1, 1217) = 6.58, p = .01, η2 p = .01 (see Figure 3). As predicted, planned contrasts revealed the impact of similarity on inspiration was stronger for average-promotability (Mhigh similarity = 5.31, SDhigh similarity = 1.41 and Mlow similarity = 3.86, SDlow similarity = 1.74), t(1217) = 10.96, p < .001, d = 0.92, than low-promotability (Mhigh similarity = 4.04, SDhigh similarity = 1.72 and Mlow similarity = 3.06, SDlow similarity = 1.64), t(1217) = 7.36, p < .001, d = 0.58.

Study 4: Interaction of similarity and promotability on inspiration.

Acceptability of CEO Pay

We predicted that participants would be more accepting of their high CEO salary in the high-similarity condition as compared to the low-similarity condition. A 2 × 2 ANOVA revealed a main effect for similarity, F(1, 1217) = 14.74, p < .001, η2 p = .01. Pay acceptance was significantly higher in the high-similarity condition (M = 3.15, SD = 1.48) than in the low-similarity condition (M = 2.83, SD = 1.44). There was also a smaller, yet significant main effect for promotability, with pay acceptance being higher in the average-promotability (M = 3.09, SD = 1.49) than the low-promotability condition (M = 2.91, SD = 1.45), F(1, 1217) = 5.07, p = .02, η2 p = .004. There was no interaction, F(1, 1217) = 0.51, p = .48, η2 p < .001. This pattern of findings shows that high (vs. low) perceived similarity enhances acceptability of CEO pay regardless of promotability.

Moderated-Mediation Model

To test the predicted first stage moderated-mediation model we examined the indirect effect of similarity on acceptability of CEO pay via inspiration as moderated by promotability, we used PROCESS macro 7 for SPSS with 10,000 bootstraps. 6 As predicted, we found that promotability moderated the indirect effect via inspiration, moderated-mediation index = −0.16, 95% CI [−0.289, −0.038]. As predicted, the positive indirect effect of similarity on pay acceptability via inspiration was stronger for average-promotability, a*b = 0.50, SE = 0.05 [0.393, 0.604] than low-promotability, a*b = 0.33, SE = 0.05 [0.233, 0.439].

Discussion

Across four studies, two observational and two experimental, we find consistent support that perceived similarity to a CEO enhances the acceptability of large pay inequality. In Study 1, using a large international sample, we found that an indirect measure of perceived social-status similarity to CEOs was associated with lower support for income-inequality-reducing policies. Study 2 showed this suggestive link was mirrored in employees reflecting on their own CEO: employees’ perceiving more similarity to their CEOs, captured indirectly via social‑status indicators and directly through broader, general perceptions, were more accepting of high CEO pay. Critically, the link between perceived similarity and pay acceptance could not be explained by subjective or objective SES (Studies 1–2) or perceived societal inequality (Study 1). Converging experimental evidence showed that increasing perceived similarity boosted acceptance of the CEO’s pay by elevating inspiration (Studies 3–4), especially for large pay ratios (Study 3).

Testifying to the construct, internal, external, and statistical validity of our empirical investigation, the findings proved robust across multiple forms of measured and manipulated perceived similarity, including indirect similarity based on social status and direct similarity based on general attributes, values, and background. Moreover, they held for both observers and employees across various measures of the acceptability of pay inequality. Study 1 further suggests that this relationship may emerge across diverse cultural contexts. Finally, statistical mediation and experimental moderation designs support the role of CEO inspiration as the underlying psychological mechanism driving these effects.

Our research offers broad theoretical and empirical contributions to diverse literatures, including pay inequality, social comparison, and leadership. First, it contributes to the relatively limited literature on the reactions to CEO-to-worker pay inequality. These pay disparities have been growing markedly (Bivens & Kandra, 2022), and have recently become transparent to employees and external observers alike (Securities and Exchange Commission, 2017). Research to date has highlighted negative reactions among employees and observers toward CEOs and companies with large CEO-to-worker pay ratios (Benedetti & Chen, 2018; Mohan et al., 2018). We extend this work by showing that such negative reactions are not inevitable. Rather, under conditions of high perceived similarity to the CEO, observers and employees may feel inspired and thus show positive reactions to high CEO pay. These findings contribute to a more nuanced view of how people react to large pay disparities.

Second, this article introduces a novel framework grounded in social comparison theory to elucidate how people experience and react to concrete information about proximal, large income inequalities within their immediate social environment. This theoretical perspective illuminates when, why, and how the typical negative reactions documented in the literature to CEO-to-worker pay inequality are mitigated. We theorize and demonstrate the importance of perceived similarity to a CEO in shaping people’s reactions to large pay inequality. Importantly, and in line with a large body of social comparison research (for a review see, Mussweiler, 2003), it is similarity on non-focal dimensions (e.g., attending the same university) that determines how people react to a social comparison standard who is strikingly different on the focal dimension (i.e., pay). If the CEO is perceived as dissimilar on such non-focal dimensions, then the negative reactions demonstrated by previous research ensue. If, however, the CEO is perceived to be similar, then more positive reactions such as inspiration result, and pay inequality becomes more acceptable.

Third, the present research makes notable contributions to the social comparison literature (Festinger, 1954), which has extensively examined how people react when confronted with extreme comparison standards. The upshot of this research is that people typically show negative reactions in terms of their self-views (Gerber et al., 2018; Mussweiler et al., 2004) and motivation (Diel et al., 2021; Lockwood & Kunda, 1997). Importantly, however, these negative reactions are not inevitable. For example, extreme upward comparisons typically reduce motivation to improve and increase tendencies to give up (Diel et al., 2021). However, when specific boundary conditions are present—such as a high perceived sense of control in the comparison domain—people are less likely to disengage when faced with an extreme standard. Extending Diel and colleagues’ logic, we show that exposure to extreme upward comparison standards generally diminishes inspiration and is thus demotivating, unless a specific boundary condition exists: perceived similarity to the comparison target.

Our focus on similarity aligns with its central role in social comparison theory (Mussweiler, 2003) and with empirical work, including a recent meta-analysis, showing that similarity shapes the direction of comparison outcomes toward assimilative tendencies (Gerber et al., 2018). Indeed, the findings of Study 4 further show that perceived similarity can even override attainability (Lockwood & Kunda, 1997) in shaping reactions to extreme upward standards. Specifically, we found that pay acceptability remained relatively low and comparable across both attainability levels when similarity was low. This pattern supports our theorizing that perceived similarity is a prerequisite for assimilation and inspiration toward an extreme upward comparison standard. Without similarity, individuals are not inspired by the standard.

Our research also echoes the multifaceted nature of similarity in social comparison. It highlights that similarity on non-focal dimensions that are not directly related to the comparison dimension itself critically shape the direction of social comparison effects. Prior research has largely treated non-focal similarity as a unitary construct, assuming that regardless of whether it stems from shared group membership (Mussweiler & Bodenhausen, 2002), close friendship (Pelham & Wachsmuth, 1995), or incidental characteristics like a shared birthdate (J. D. Brown et al., 1992), it consistently promotes assimilative social comparison processes (Mussweiler, 2003). Future research is needed to develop a more nuanced understanding of similarity, particularly by contrasting deeper, identity-related dimensions such as values and social class with more surface-level demographic variables like age, gender, or ethnicity. This distinction may reveal whether different types of similarity shape the consequences of social comparison in distinct ways.

Furthermore, a more nuanced understanding of the motivational outcomes of perceived similarity is needed. Although our studies show that perceived similarity enhances inspiration, we did not assess the content of that inspiration. We measured whether people felt inspired but not whether that inspiration is narrowly focused (e.g., on becoming a CEO) or more general (e.g., increasing effort, career development, or organizational commitment). Future research should clarify the approach-motivation component of inspiration—what people are inspired to pursue and whether those aspirations translate into concrete behaviors.

Finally, our research also contributes to the leadership literature. Much of this scholarship has highlighted the importance of personal relationships between followers and their leaders (Bass & Avolio, 1994; Graen & Uhl-Bien, 1995). In particular, followers’ personal identification with their leaders is a conduit through which leaders motivate and inspire (Kark et al., 2003; Wang & Howell, 2012). Recent work, however, shows that elevated CEO pay (relative to other CEOs) can undermine the perception of a shared identity (“we”) between leaders and followers, and as a result reduce the perception of the leader as inspiring and charismatic (Steffens et al., 2020). Our findings qualify this view by demonstrating that such disparities are not uniformly alienating: when a leader is perceived as similar to the self, the same inequality may be interpreted more favorably. In other words, perceived similarity renders the leader’s advantage psychologically relevant and thus potentially inspiring. In this way, our work introduces similarity perception as an important complement to the existing account of how elevated pay shapes leader–follower identification. Moreover, our findings suggest that CEOs and senior managers seeking to mitigate the negative effects of high pay or to enhance their inspirational impact may do so by intentionally highlighting their similarity to subordinates, even on incidental dimensions. Future research is needed to directly test this prediction and explore its broader implications.

By combining international archival data with pre-registered experiments involving U.S. working adults, our multi-method approach provides initial evidence that perceived similarity to CEOs may shape acceptance of pay inequality across varied contexts. Still, the generalizability of these findings should be interpreted cautiously. The experimental studies used hypothetical scenarios and self-reported attitudes, which may not map perfectly onto real workplace behavior. Moreover, the strongest cross-cultural evidence comes from Study 1, which relied on an indirect measure of perceived similarity. Accordingly, future research should examine these effects using more direct measures of similarity in culturally diverse field settings to better establish their scope and boundary conditions.

There are likely various boundary conditions that may magnify, diminish, or even eliminate our effect. For example, respondents who hold strong attitudes toward the CEO (e.g., due to knowing them well or based on vivid events) may be less affected by perceived similarity when deciding how much they support pay inequality (Petty & Krosnick, 1995). In addition, attributes of the CEO (e.g., gender, race; Biernat et al., 1991), of the respondent (e.g., social dominance orientation; Pratto et al., 1994) or of the context (e.g., the extent to which that country implements policies to reduce income inequality; Alesina & Angeletos, 2005) may shape the strength of the effect. It would be valuable for future research to examine such factors.

Our work echoes previous research demonstrating that inequalities within the broader socio-economic system can elicit positive reactions (Brown-Iannuzzi et al., 2015; Jost & Hunyady, 2005). We show that this logic is not limited to abstract, distal forms of inequality but also applies to concrete, proximal disparities between individuals, such as large pay gaps between employees and CEOs. More importantly, our theorizing and findings identify perceived similarity as a key factor shaping these broader reactions. When individuals see themselves as similar to a highly advantaged leader, they may respond more positively to that leader’s high pay and, at a broader level, become less supportive of efforts to reduce economic inequality. Consistent with this possibility, in Studies 2–4, perceived similarity was associated with greater acceptance of CEO pay, and in Study 1, an indirect measure of perceived similarity to CEOs was associated with reduced support for redistributive policies at the societal level. Taken together, our findings suggest that perceived similarity to highly advantaged leaders can help sustain acceptance not only of specific pay disparities but also of societal-level economic inequality more broadly.

In conclusion, our studies reveal that feeling similar to a CEO renders large pay disparities more acceptable. We illuminate why and when this effect emerges. Our findings highlight an interpersonal pathway through which extreme pay inequality can be tolerated, even when it is highly visible and personally disadvantageous. More broadly, these insights may help explain the paradox of muted public responses to stark societal inequality. Feeling “just like my CEO,” it seems, can soften the sting of substantial pay gaps, even when the CEO earns a hundred times more than I do.

Supplemental Material

sj-docx-1-psp-10.1177_01461672261449861 – Supplemental material for Just Like My CEO: When Perceived Similarity Makes Pay Inequality Acceptable

Supplemental material, sj-docx-1-psp-10.1177_01461672261449861 for Just Like My CEO: When Perceived Similarity Makes Pay Inequality Acceptable by Daniel Heller, Garrett L. Brady, M. Ena Inesi and Thomas Mussweiler in Personality and Social Psychology Bulletin

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by a London Business School Research and Materials Development (RAMD) grant awarded to Thomas Mussweiler.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Open Practices

Materials and data for Study 1 are publicly available on the ISSP website.

Studies 2, 3, and 4 were pre-registered (Study 2: https://aspredicted.org/M19_HWF; Study 3: https://aspredicted.org/f647-2rqq.pdf; Study 4: ![]() ).

).

Supplemental Material

Supplemental material is available online with this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.