Abstract

The purpose of this study is to understand how one of the most non-renewable countries is acting concerning the global challenge of energy supply vs. resources for energy generation. Saudi Arabia is registering the highest energy consumption per capita in the world with its fastest population growth and the rapid pace of industrialization. Its electricity consumption is expected to be more than doubled by 2025, and the carbon emission is supposed to be on the rise. In that backdrop, Saudi Arabia has taken many steps to shift its dependency from oil to solar, wind and nuclear sources of energy, and plans to secure half of the country’s electricity needs from the alternative sources of energy in coming 20 years. The government has announced an ambitious plan to install 41 Giga Watt of solar capacity and invest $108.9 billion by 2032. This exploratory study reviews the steps undertaken in this regard to promote the solar energy initiative as envisaged by the government. This paper discusses the issues and challenges in shifting from oil to solar energy in Saudi Arabia. It documents and discusses the drivers that push Saudi Arabia to adopt solar as an alternative source of energy that can be used to reduce oil dependency and to improve environmental sustainability. A multi-pronged approach involving all stakeholders is the key to success in making the solar project sustainable in Saudi Arabia.

Keywords

Introduction

Saudi Arabia’s economic growth has increased exponentially over the past three decades largely due to the rich and accessible oil and natural gas endowments. Saudi Arabia has the highest level of GDP amongst the Gulf Cooperation Council (GCC) but also emits the highest level of carbon dioxide (CO2) with evidence suggesting an increasing dependence on oil and gas for power generation. Saudi Arabia being the largest economy in GCC whose economic growth is seen highly dependent on non-renewables, and there is a pressing need for Saudi Arabia to explore an alternative source of energy. Experts also suggest that Saudi Arabia can emerge as the most competitive manufacturing location for photovoltaic (PV) solar energy. European Commission Institute for Energy reported that 0.3% of light falling on the Sahara and the Middle East deserts would be enough for the whole of Europe.

Among the six GCC countries, Saudi Arabia has emerged as one of the biggest markets accounting for most of the projects for the PV market and is expected to contribute to making the region a hub for solar expansion. The current electricity prices in Saudi Arabia are also set well below the long-run marginal costs, and from a customer perspective, there is little economic incentive to either conserve electricity or to use it more efficiently (Al-Natheer, 2005). On the other hand, despite having all the resources, some major economies are not so committed to carbon emission reduction causing serious pollution resulting into various diseases. Saudi Arabian initiative towards the green power exports will not benefit the participating countries from the production of energy but also strengthen their local expertise and employment as well. In this background, the present study aims to explore, understand and analyse how the solar can be an alternative source of energy in Saudi Arabia.

Saudi Arabia: Challenges of the current energy system

Saudi Arabia has a total area of 2,149,690 km2, half the size of EU or six times size of Germany (Al-Jarboua, 2009). It has got two main seasons of summer and winter (Rehman et al., 2007), and 85% of the population are living in the urban areas (Vincent, 2008). In GCC, 26 out 39 million people are residing in the KSA (Reiche, 2010), and it is rated as the world’s 20th largest economy with a GDP of $528.3 billion largely accounting from oil exports. Saudi Arabia has got world’s second largest oil reserves estimated at 268.3 billion barrels, roughly one-fifth of the world’s total proven conventional oil reserves (Worldatlas, 2017). According to British Petroleum Statistical Review of World Energy, the Saudi Arabia is the world 2nd largest holder of proved oil reserves representing 15.9% of the total and sixth largest holder of proved natural gas reserves (Al-Jarboua, 2009). In 2015, it was also the second largest producer of oil in the world with 11.7 million barrels per day (CNN Money, 2016). Saudi Arabia is OPEC’s biggest oil producer and has oil consumption much higher than the global average. There are predictions that if the existing rate of consumption continues by 2038, it might be importing oil for itself. It consumes a billion barrels a year, or about 40 barrels per capita which are recorded as the highest per capita rate in the world. The electricity consumption in Saudi Arabia is four times greater than the United States, five times that of South Korea and eight times to the consumption in Japan (Estimo, 2016; Sughai, 2014).

Power consumption in Saudi Arabia is three times more than the world average, and it has grown at a compound annual growth rate (CAGR) of 6% over the last 5 years. Recent statistical data shows a significant rate of growth regarding domestic consumption with an annual growth of 14.8% (Al-Ajlan et al., 2006). The housing sector in Saudi Arabia is a major consumer of electricity with 70% as most of the structures in the Kingdom lack insulation. The total power transmission of Saudi Electricity Company (SEC) has increased by almost 50–60%, transmission lines by nearly 75% and the number of customers by over 70% between 2000 and 2010 (Ghafour, 2014a; Taha, 2012). Future demand for electricity and water in Saudi Arabia is set to grow with a high growing population, increasing urbanization and with the fast pace of industrialization.

Electricity generation in Saudi Arabia causes major environmental consequences that include an impact on air, climate, water and land (Al-Natheer, 2006). As per 2012 data, Saudi Arabia has been the world’s ninth largest CO2 emitter with 2.8% of global emissions. Due to heavy reliance on fossil fuels, the electricity and heat production contributes 56.34% of internal CO2 emissions in Saudi Arabia. Despite recent efforts of the government to diversify its economy, as of December 2015, the petroleum sector accounts for roughly 80% of budget revenues, 45% of GDP and 90% of export earnings (Forbes, 2016). The current energy supply is exclusively sustained by fossil fuel with no input from any source of renewable energy (RE) despite having longest sunshine hours and highest solar radiation intensity in the world (Rehman, 2010). Jeddah, Riyadh, and Dammam, the three big cities of Saudi Arabia are having an average of 5.78 kWh/m2/day insolation which is much higher than the global scale of 1.36 kWh/m2/day (Frohlich, 2006). The availability of raw material also makes Saudi Arabia, an attractive destination for solar energy. There is availability of silicon oxide for the PVs in the white rock/sand with the highest ratio of 99.5% compared to red sand and limestone having 86.7% and 13.5%, respectively (Elani and Bagazi, 1998).

Research methodology

The present research documents and discusses a country-specific explorative case study of the solar energy scenario existing in Saudi Arabia. It aims at documenting and discussing the current situation of the solar energy initiatives undertaken by the different stakeholders in Saudi Arabia. The data covered are mostly secondary in nature collected from various sources of published data in the form of government reports, published articles, books, reports by different institutions, and other documents accessible from the government sources. The study got its impetus from the government plan adopted in 2012 to shift to the RE in a big way in coming years. The Kingdom’s solar industry is aiming to achieve 24 GW of solar capacity by 2020 and 41 GW by 2032 and the government plans to invest more than $108.9 billion in the solar industry and has announced incentives which includes financing up to 50% of project costs and a generous tax break (Alyahya and Irfan, 2016a).

Government’s recent decision to implement the solar energy strategy and save the Saudi Arabia up to 520,000 barrels of oil a day by 2032 is a gigantic step, and it needs to be discussed and analysed to understand its impact on the economy as a whole. Matara et al. (2017) also reckon with the view that the alternative energy policy if successfully adopted in the Kingdom may lead to a more cost effective and efficient energy system with nuclear and renewable technologies constituting 70% of the electricity supply by the year 2032. It is important to evaluate and discuss the requisite business and economic scenario existing to achieve this ambitious goal and to discuss the kinds of barriers and challenges being faced by the various stakeholders of the solar energy sector. The study aims at shedding lights on the solar energy project initiatives undertaken in the Saudi Arabia so far, its preparedness, and what needs to be done to achieve the huge solar energy goals envisaged by the government. The current study is developed based on an exploratory approach, based on the secondary data from various stakeholders and institutions relevant to the solar energy development in Saudi Arabia.

Rationale to diversify to alternative source of energy: Potential of solar energy in Saudi Arabia

Despite its huge oil production and possession, Saudi Arabia faces a different structural problem related to its stagnant oil-production-per-citizen rates worsened by the rapidly increasing population and a high unemployment rate (Bahrain Tribune, 2007). Recently, the government reported 11.6% of the level of unemployment in Saudi Arabia in its national transformation program 2020 (NTP, 2020). Its per capita income has decreased by more than half between 1980 and 2000 (from $16,650 to $7239) and likely to reach an unsustainable level of the welfare redistribution in the long term (Kumetat, 2009). In a nutshell, the Saudi Arabia is registering the world’s highest energy consumption per capita, fastest population growth, and fast pace of industrialization that translates into a 7–8% rise in the energy demand. In fact, according to the government estimate, demand for electricity generation will exceed 120 GW by 2032. Saudi Arabia’s electricity consumption is expected to be more than doubled by 2025 with most being produced from the diesel and a very nominal portion from the RE (Ramli et al., 2015). Thus, the CO2 is expected to be on rising proportionately if no RE and green energy are used (Mansouri et al., 2013). To overcome this adverse situation, it would be highly required to use a renewable and sustainable source of energy system (Bkayrat, 2013; Rasooldeen, 2012; Tago, 2014a).

It is important for Saudi Arabia to be self-dependent and rely on a self-sustained method of energy development. As the oil prices have gone down globally in the recent past, there is a huge requirement for giving impetus to the alternative sources of energy like renewable and solar. It should account for 20–25% within the next 10 years, and Saudi Arabia plans to shift its dependency to solar, wind and nuclear sources of energy, and secure half of the country’s electricity needs in coming 20 years. A decentralized and stabilized power supply with sustainable tariffs is required which warrants a paradigm shift for the future of the Saudi economy (Al-Fawaz, 2014; Hassan, 2015). Though Saudi Arabia has abundant wind and solar radiation, 53.85% of Saudi Arabia’s electricity come from oil and rest from the natural gas (WDI, 2012). The average solar radiation falling on the Arabian Peninsula is about 2200 kWh/m2 (Al-Awaji, 2001) with Saudi Arabia being located in one of the world’s rich solar region receiving most strong sunlight (Dargin, 2009). Al-Natheer (2005) suggests that compared to geothermal energy, RE source like solar and the wind are more cost-effective in the Saudi Arabia. The research, development and demonstration (RD&D) work conducted by the Energy Research Institute (ERI) at King Abdulaziz City for Science and Technology (KACST) confirms that solar energy has a multitude of practical uses in Saudi Arabia (Abdurabb, 2014).

Having a peak electricity load of 57 GW, being totally dependent on oil and gas provides an excellent opportunity for the generation of solar energy because of available high rate of daily sunshine. The city of Medina reflects a linear and polynomial correlation between ambient temperature and global irradiation data, respectively, from sunrise to midday and midday to sunset (Benghanem and Joraid, 2007), with lowest albedo values recorded in summer and highest in winter (Maghrabi and Al-Mostafa, 2009). Followed by correlations predicting annual average of daily global solar radiation with excellent accuracy for Jeddah (El-Sebaii et al., 2009). A Solar Radiation Atlas developed by KACST in collaboration with the US National Renewable Energy Laboratory (NREL) in 2013 to monitor and map Saudi Arabia’s solar, the wind, geothermal and waste-to-energy resources. The purpose was to monitor data based on recordings from approximately 70 stations established throughout the country. Based on data, it has been found that direct normal radiation exceeds 30 MJ/m2/day in some regions in the summer, and is not less than 24 MJ/m2/day anywhere in the country even in the month of January (NREL, 2000). Bushnak (2006) also found that the number of hours of natural sunshine received by the Saudi Arabia was among the highest in the world which increases its potential for the use of solar energy.

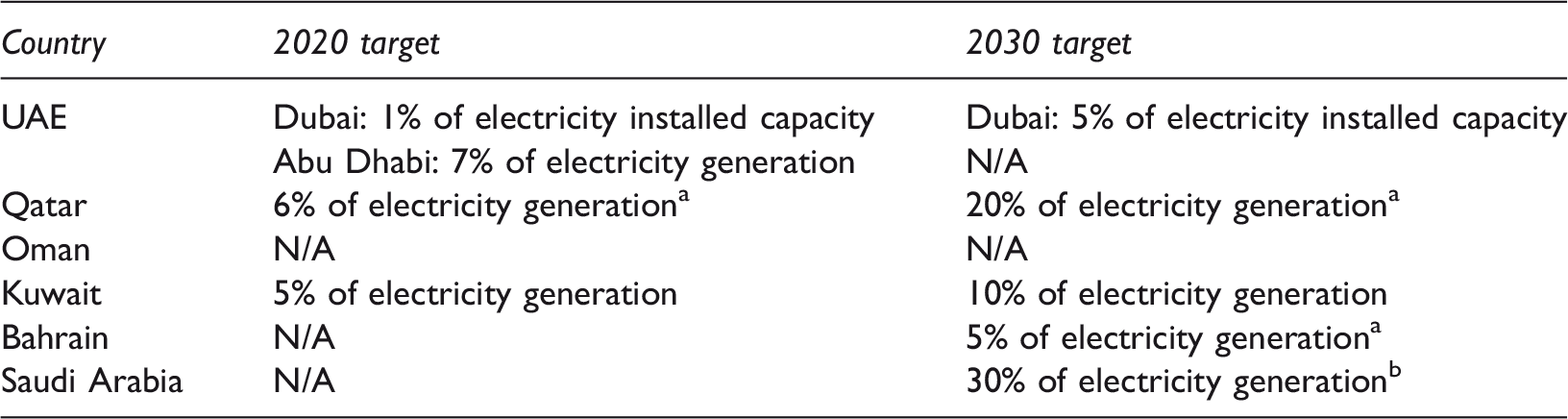

Renewable energy targets conceived for Saudi Arabia and other GCC countries.

Source: Kuwait, Saudi Arabia and Yemen from League of Arab States (2013); RCREEE (2013a, 2013b); REN21 (2013); Dubai and Qatar (2020) from EU-GCC Clean Energy, and Masdar Institute (2013); Qatar (2030) from Eversheds, and Ernst and Young (2013); Kuwait 2030 target from Alsayegh et al. (2012).

Unofficial targets.

2032 target.

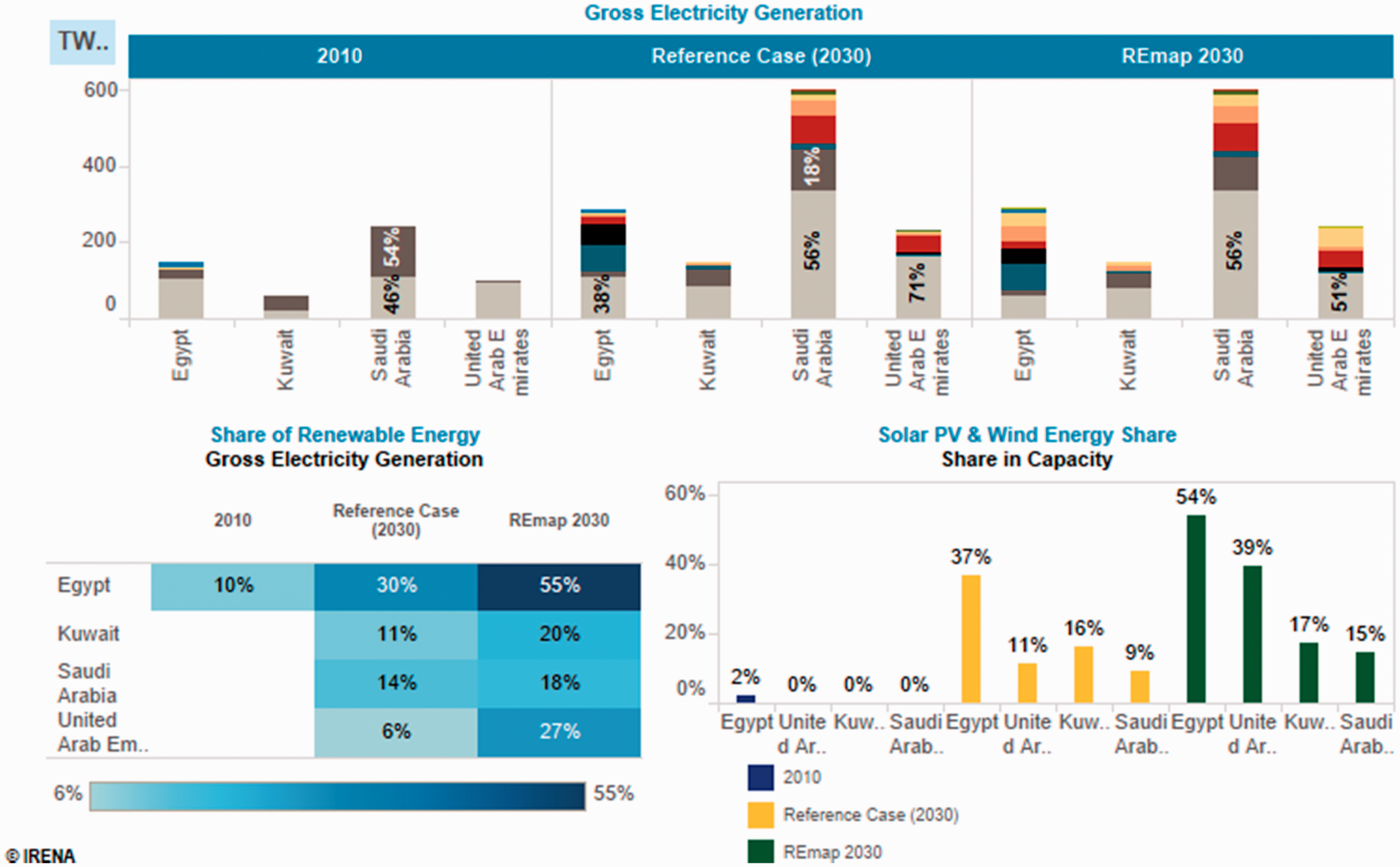

Comparative data of Saudi Arabia and other GCC countries for RE, solar and wind energy. Source: IRENA (2016a).

Some studies have been conducted to evaluate the RE potential of Saudi Arabia. Some of these are Government policies for solar investment (Alyahya and Irfan, 2016a), development of talent for Saudi solar industry (Alyahya and Irfan, 2016b), development of solar atlas by Saudi Arabia (Alyahya and Irfan, 2016c). Solar PV and another efficiency improvement for sustainable residential buildings (Taleb and Sharples, 2011), RE options and economic viability of Solar PV within the residential sector (Al-Saleh and Taleb, 2009). Delphi approach examining of renewables (Al-Saleh, 2009), barriers to geothermal resources (Taleb, 2009) and sustainable development policies for energy conservation (Al-Ajlan et al., 2006). Most of the studies investigated the high potential of Saudi Arabia for exploiting the solar energy source. Saudi Arabia is the home to the world’s largest continuous sand desert, ‘Al-Rub Al-Khali’ or the Empty Quarter which receives enough daily solar radiation capable of powering two Earths with its massive solar energy potential (Oettinger, 2011).

Assumptions reflect that the energy-related technologies will continue to flourish with varied development and penetration in the market in all scenarios, and such technological changes will not be affected by the policies and actions of Saudi leaders. Furthermore, it is assumed that technological growth does not depend on innovators but probably upon the implementation choices made by the demand domain users (Geels, 2006; Wolsink, 2000). The government has mandated Saudi investment funds to make use of their liquidity in partnering with the international RE providers to cope up with the rapidly growing energy sector. Moreover, the Saudi RE investors and project owners are instructed to capitalize in and conduct business with sustainable solar business around the world. Alike the Desertec project (power supply from Africa to Europe) which is worth approximately 400 billion Euros (US $512 billion). Saudi Arabia is planning to export energy to Europe as well which has been found to be technically feasible and might take 5–10 years duration, provided proper finance be available (Estimo, 2014a). There has been much impetus for developing solar energy in other GCC countries as well, and it is widely established that developing renewable and solar energy infrastructure will lead to a lot of socio-economic benefits in the long run for the country and the region at large. Figure 2 provides data about the social and economic benefits for the Middle East vis-a-vis other countries of the world.

Solar energy expansion in the Middle East and its socioeconomic benefits. Source: IRENA (2016a).

Solar energy initiatives in Saudi Arabia: Key findings

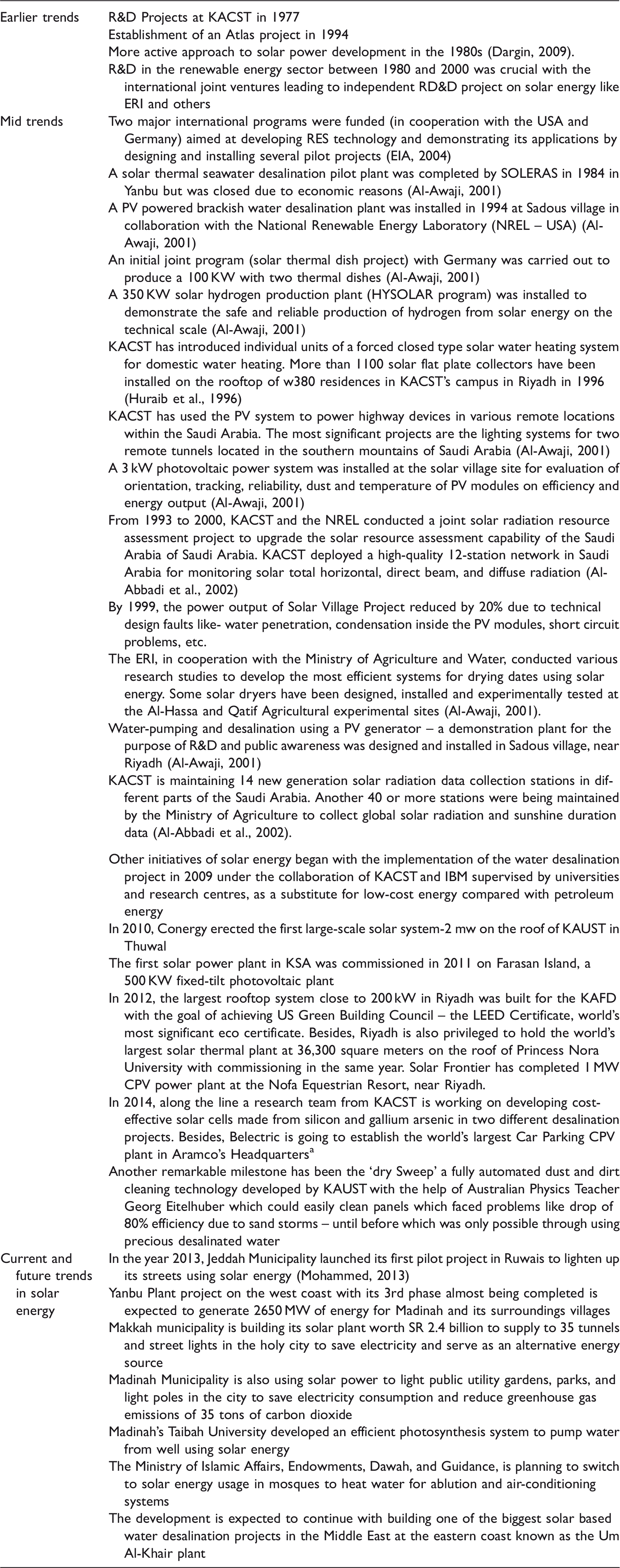

The journey of solar energy began in the KSA in the early 1960s with the first PV beacon established by a French company at the airport of Madinah Al-Munnawara (Sakr, 1987). It was followed by small-scale research projects initiated in 1969 and leading to systemized R&D projects undertaken by KACST in 1977 (Al-Awaji and Hasnain, 1999). One of the earlier initiatives taken in the solar energy development in Saudi Arabia was to establish an Atlas project in 1994. It was an R&D joint venture for the measurement of solar radiation between Energy Research Institute (ERI) of KASCT and National Research Energy Laboratory (NREL), USA. It connected 12 cities – Riyadh, Qassim, Al-Ahsa, Al-Jouf, Tabuk, Madinah, Jeddah, Qaisumah, Wadi Al Dawasir, Sharurah, Abha, and Jizan to the central unit for data collection, and was calibrated on a yearly basis to derive reliable and accurate data (Al-Awaji, 2001). Following the initial failure of HYSOLAR program in 1986, government’s interest in RE was revived with King Abdullah University of Science & Technology (KAUST) establishing two rooftops solar PV plants in its northern and southern laboratories. Later on, King Abdullah City for Atomic and Renewable Energy (KACARE) was established in April 2010 by a royal decree (Al-Saleh, 2011), it is in charge of developing the nation’s RE sector and plays a major role in this arena. KACARE, based on Saudi’s economic and natural resource abundancy, estimated that 80% of industrial and service components for RE could be sourced internally. The opportunity cost of domestically consuming hydrocarbon resources at subsidized rates instead of exporting them is huge. From an economic perspective, investing in RE will help to reduce the consumption of valuable oil and natural gas for power generation, and it will free up resources for export (Bkayrat, 2013).

The government adopted an exhaustive solar energy strategy in 2012, and the current 0.003 GW of installed solar energy capacity is planned to be expanded to 24 GW of RE by 2020, and 54 GW by 2032. The new energy policy scenario leads to the construction of 131 GW of additional capacity, of which 110 GW are supposed to be nuclear and renewables. It requires a massive $392 billion in capital investment including $356 billion for nuclear and renewables (Matara et al., 2017). KACARE has earlier suggested a revision of the National Energy Plan to implement 41 GW of solar power (25 GW of Concentrated Solar Power (CSP) and 16 GW of PV), and the initiative to set up solar power for water desalination plants was taken by it. Studies based on 3, 5 and 10 GW capacity export to Europe has been undertaken which demonstrate that it is economical and unlike Desertec (power from North Africa to Europe) it would not require a third party to install generation capacity since KACARE would lead the production and connection investment (Arab News, 2013a, 2014).

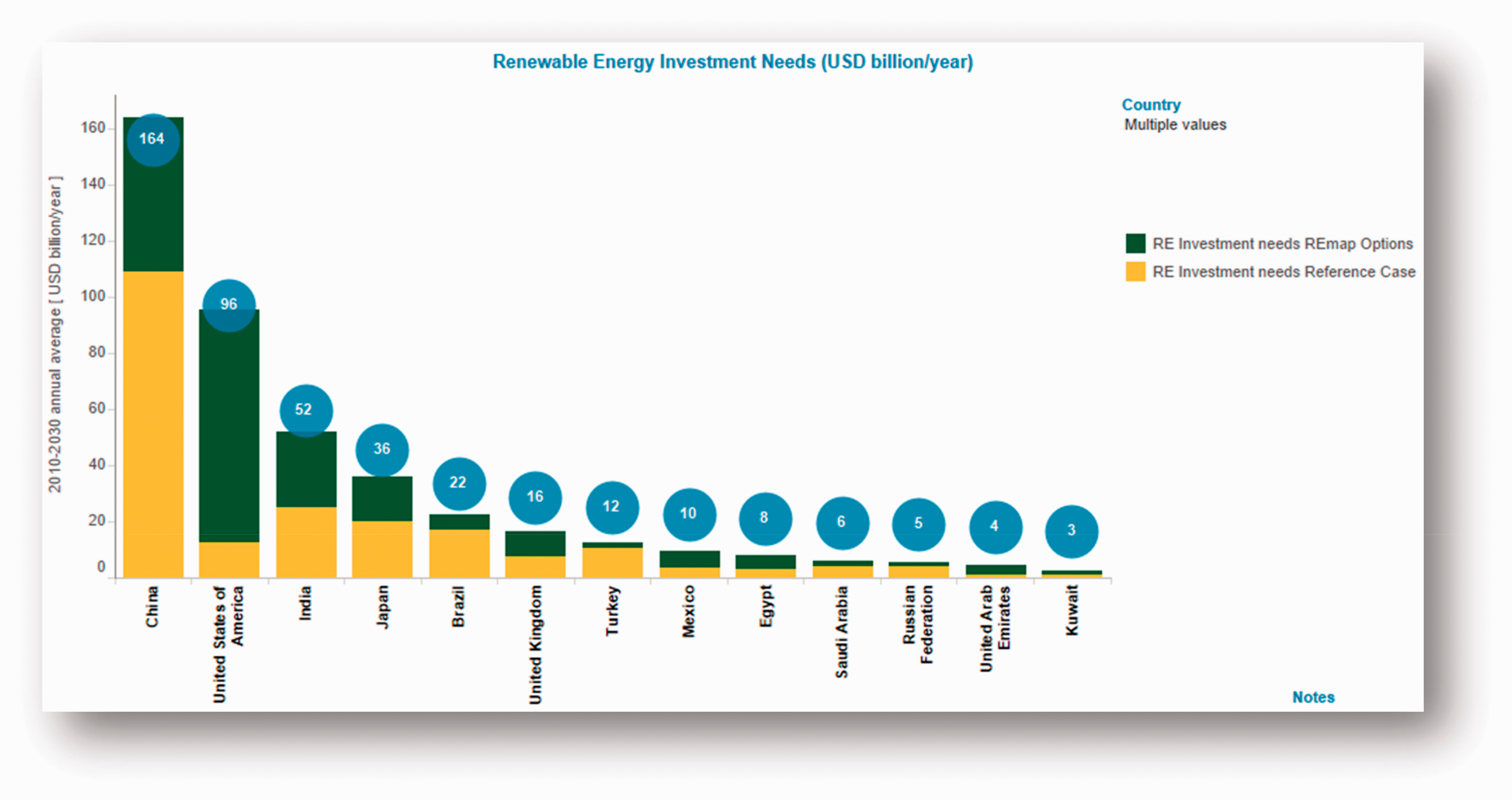

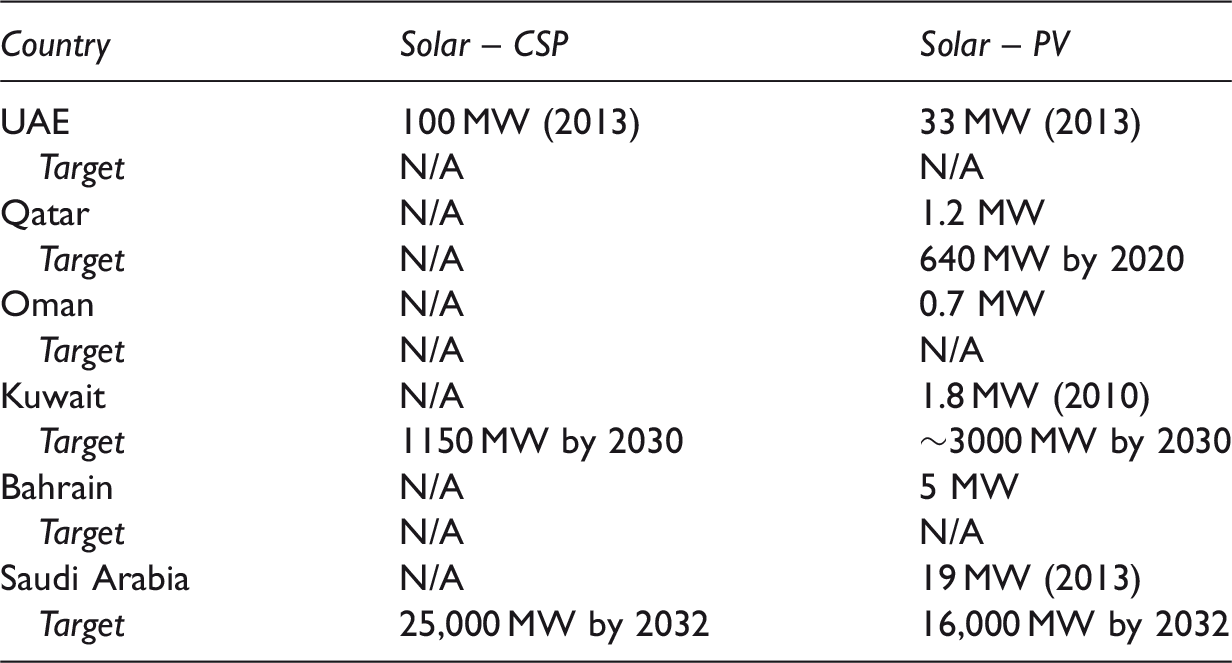

In March 2008, ex-oil minister, Ali Al-Naimi, informed the French Newsletter ‘Petro strategies’ that Saudi Arabia’s strategic plan was to sharpen its solar expertise and to emerge as the solar energy research centre in coming 30–50 years. It aims to be a major megawatt exporter (Al-Fawaz, 2014; Estimo, 2014b). The existing capacity in the RE sector in Saudi Arabia is almost non-existent (Clercq, 2013). With the vision of becoming the world’s leading RE market, KSA plans to invest $109 billion (equivalent to SR 408.75 billion) over the next 20 years. Figure 3 provides the required fund needed to attain the RE map for Saudi Arabia and some other countries (Figure 3). With the goal of generating one-third of the domestic electricity consumption of RE, Saudi Arabia plans to install 24 GW of renewable power capacity by 2020. Table 2 provides the details about the solar energy production and the future targets for Saudi Arabia vis-a-vis other GCC countries. Very recently, in April 2016, Saudi Arabia adopted its Vision 2030. The vision document puts a huge emphasis on developing the RE sector. It sets an initial target of generating 9.5 GW of RE. Saudi Arabia has an impressive natural potential for solar and wind power, and its local energy consumption is going to increase three-fold by 2030. It lacks a competitive RE sector at present, but the new Saudi vision 2030 aims to localize a significant portion of the RE value chain in the Saudi economy, including research and development, and manufacturing, among other stages (Government of Saudi Arabia, 2016).

Investment requirement for developing RE in Saudi Arabia vis-a-vis other selected countries for the years 2010–2030 (in USD billion). Source: IRENA (2016a). Solar energy installed capacity and its future targets for Saudi Arabia vis-a-vis other GCC countries. Source: RCREEE (2013b); REN21 (2013); Alsayegh et al. (2012).

With the objectives set out by the solar strategic plan, KACARE has embarked on a national project to conduct all kinds of research on the RE within Saudi Arabia. In addition to KACARE, other existing institutions also play a major role in Saudi Arabia. Center of Research Excellence in Renewable Energy (CoRE-RE), Saudi’s first national research centre was established in the year 2007 with a vision to be the national centre contributing to the advances in research and commercialization of RE technologies in the KSA and the region (CoRE-RE, 2016). Following this, another initiative was taken by Late King Abdullah for climate research with the establishment of the King Abdullah Petroleum Studies and Research Center (KAPSARC) in 2010 which is a non-profit global institution dedicated to independent research into energy economics and policy making. Alongside, few solar projects are under construction with a total capacity of some 15 MW (Hanware, 2014a). Another government agency, playing an important role in solar energy research and development and policy formulation is KACST. KACST was established in 1977 as an independent scientific agency; it helps in developing solar power technology by adopting compatible science and technology policy making, data collection, funding external research and providing services such as the patent registration (KACST, 2010). It launched a national energy efficiency program denoting solar energy as the key to reducing the cost of water desalination and power generation (Hepbasli and Alsuhaibani, 2011). It also expected that new technologies’ energy efficient systems could be created and implemented across the KSA and the world.

Saudi Aramco, the national petroleum and natural gas company, is playing a critical role in solar energy development in the Saudi Arabia. Saudi Aramco targets RE to contribute 20–30% of its energy needs. Besides, Saudi Electricity Company and Aramco have undertaken collaborative efforts with the help of international experts in establishing beneficial partnerships in meeting the Saudi Arabia’s objectives. Most of the policy research and strategic proposals for the Supreme Petroleum Council (chaired by the King) emerge from Saudi Aramco, and the Ministry of Petroleum is also dependent on them for the research initiatives (Hertog, 2013). The role of the Saudi Aramco becomes more prominent, and the CEO confirmed that they would be looking into the issue where KACARE can achieve short term goals. It seems at variance role where in one hand they want to establish short term solar projects, and on the contrary, they want to focus on Nuclear energy (Abdurabb, 2014; Estimo, 2014a; Mahdi, 2014). Very recently, the oil ministry has been restructured, and its role has become more pervasive across energy and industrial sectors in Saudi Arabia. The ministry got new nomenclature as Ministry of Energy, Industry, and Mineral Resources, and Khalid Al-Falih, the chairman of Saudi Aramco was appointed as the new energy minister on 7 May 2016 (AFP, 2016).

KACST also collaborated with IBM by establishing a Nanotechnology Center of Excellence focusing on new materials for converting solar energy to electricity (Hertog and Luciani, 2009). KACST has adopted a German BMFT joint program on thermal dish project generating 50 kW from a single concentrator dish, considered the largest of its type in the world (Bhutto et al., 2014). In another initiative, it had collaborated with US National Renewable Energy Laboratory for establishing the Solar Radiation Atlas (Zell et al., 2015). In the past, KFUPM has also collaborated with ERI for establishing the Solar Energy Atlas in 1983, and the Saudi Arabian Wind Energy Atlas in 1986 (Woertz, 2008).

Some of the important initiatives undertaken in the Solar energy sector in Saudi Arabia have been listed below. It includes the initiatives undertaken in the past as well as the ongoing, and future scope of solar energy projects in Saudi Arabia:

Trends and gradual development of solar energy projects in Saudi Arabia.

Currently, the area of prioritization for the RE has been the large utility-scale renewable power plants, but the small off-grid plants also need to be encouraged down the line. There is a huge opportunity for private sectors, and to reap the benefit out of it, incentive plans need to be laid down. Sustainable development and growth through building huge projects need to be backed up by strategic plans as well. As visible in the case of Gobi desert, Cooper and Sovacool (2013a, 2013b) suggested that large projects not be enough, careful consideration of myriad logistical, economic, environmental and social concerns must be considered as well. The Saudi Arabia is spending a lot on the power sector, besides the local participation could lead to more cost-effective strategies. Though high-level plans are already in place, a detailed timeline for a clear and gradual shift with long-term policies to provide a predictable and reliable framework to support renewable deployment is necessary to cope with the slow adoption and advancement in the RE sector. Findings from Al Saleh (2011) revealed that the government has the intention to increase the role of both the private sector and foreign investors. Besides, a niche market for RE is being made in the western part of the country in four expensive economic cities with a cost of more than US$60 billion before mass markets evolve throughout the Saudi Arabia. Demirbas et al. (2017) also find that the KSA government approach in developing an energy policy aimed at diversifying energy sources and its suppliers and attracting private sector.

KACARE is encouraging the businessmen to invest in the Saudi Arabia’s energy scheme, an ecosystem in the country with global initiatives. On the other hand, with an exclusive partnership with Manz, a German based leading manufacturer, it is expected to have access to matured German world-class technology. The increased personal incomes and bank deposits in GCC countries, particularly in the KSA, UAE and Qatar have led to policies where banks are expanding their credit line. KACARE plans to export 10 GW (equivalent to 10 nuclear plants) in Europe in winter via North Africa, Italy or Spain (Estimo, 2014b; Tago, 2014a; Taha, 2013). The new Saudi Vision 2030 adopted in April 2016 also talks about public–private partnership (PPP) to facilitate the flow of private investment and to encourage competitiveness and to promote the localization of RE (Government of Saudi Arabia, 2016).

According to Pazheri et al. (2012), the efficient use of renewables through smart grid can reduce oil consumption for electricity and dependency on oil. To utilize the renewables in remote locations, the infrastructural development requires about ten years. Saudi Arabia has the potential to become a major exporter of electric power. According to Solar Energy Authority (Solar DirectX), the cost competitiveness of the Saudi Arabia is expected to surpass the USA in the renewable power. E-magazine, Cleantechnica quoted that by 2019 the ratio of the price of solar energy between US and KSA is estimated to be $130–243 per MW hour and $70–100 per MW hour, respectively. KACST team has already treasured high-quality patents and inventions with advancements such as three-link solar cells. Also, localization of manufacturing, production and developing of solar PV panels have been in progress with milestones in the areas of alternative energy production (Khan, 2012).

Saudi Arabia can be a leading producer and exporter of solar energy in the form of electricity if it achieves a breakthrough in solar energy conversion (Al-Awaji, 2001; Hepbasli and Alsuhaibani, 2014). It requires a shift to the new investment energy forms which can contribute numerous public benefits like, enhanced environmental quality and protection, increased energy security, and local economic development (Al-Natheer, 2005; Patlitzianas et al., 2006). Global environmental awareness has led to the innovation for more sustainable technological and institutional processes and systems in the field of RE, referred in other words as sustainable innovation (Foxon and Pearson, 2008). Thus, the sustainability transition dynamics need to be closely examined between theory and practice by applying innovation systems (Al-Saleh, 2010; Foxon and Pearson, 2008). It is a systemic view of interaction among different actors (Edquist, 2005), and can be explained from a socio-technical perspective (Shackley and Green, 2007). Alternately, a multi-level perspective (Geels, 2002) or more accredited broader approach which allows a transition of the rationale for policy intervention – an approach of systems failures over market failures (Al-Saleh, 2010).

Barriers and challenges for solar energy development in Saudi Arabia

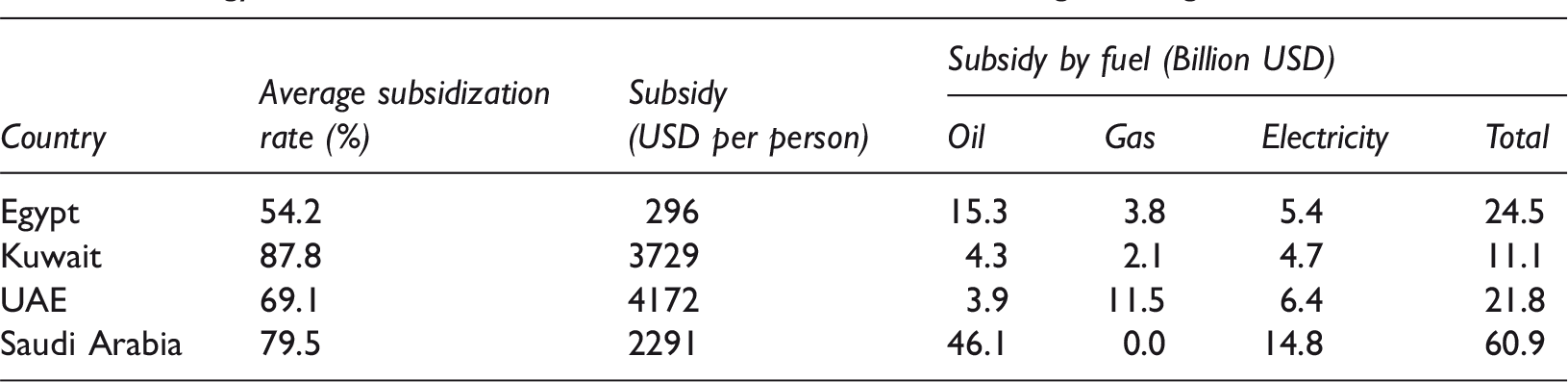

Energy subsidies in Saudi Arabia vis-a-vis other GCC and neighbouring countries.

Source: MENA Renewables Status Report, Paris: IRENA; 2013 and Alyahya and Irfan (2016a).

The current strategies and policies for developing RE in Saudi Arabia warrant bringing new legislation, signing new international treaties, providing incentives for investment, targeted energy generation, developing guidelines for energy conservation. Resulted in making strategies to stimulate the energy sector by adopting appropriate taxation and other public policy measures (Bhutto et al., 2014).These need to be addressed by creating a level playing field to promote the RE infrastructure. The April 2016, new Saudi vision attempts to deal with these issues by proposing public–private partnership (PPP) for promoting investment in RE infrastructure in Saudi Arabia. Based on the practices in other countries, Saudi Arabia may also include feed-in-tariff (FIT), renewable portfolio standards, incentives, pricing laws, and quota systems (Saidur et al., 2010). A small-scale local initiative has to be jointly carried out by the civil society, communities and small businesses (Al-Badi et al., 2011; Schroeder, 2014). The FIT scheme policy is required to be adopted in two stages for Saudi Arabia as it has been proven to be efficient incentive model. First by introducing market independent FIT for market restructuring like fixed price, and second, when the competition is up, to present the market dependent FIT model to reap the comprehensive benefit of the FIT model (Ramli and Twaha, 2015)

There is no immediate pressure to seek and secure alternative sources of energy which makes the Saudi Arabia less reluctant to invest in non-conventional energy (Al-Jarboua, 2009). Also Blazquez et al. (2017) argued that significantly high amount of oil export to the global market might negatively impact the oil price and thus will offset the potential gains from the RE. According to the former Saudi Arabian Oil Minister, at the current production rates, Saudi oil reserves will last for about 80 years, and the business scenario shows less concern for energy securities through the use of renewables in the Saudi Arabia (Patel, 2009). The strong trader mentality from the traditional Arab culture inhibits the innovation, and they focus on short-term financial returns which lack long-term perspective for potential gains from R&D and entrepreneurship (Vidican et al., 2012). KACST has reported that the monkeys, which are considered a part of the eco-system, are damaging the solar panels in KSA in many places, however, no recent statistics available on their numbers. Another barrier includes obstacle from the public resistance to the high voltage line to all long-distance grid projects. PV is limited to sunny periods only. However, CSP which is more expensive can provide electricity storage. Many local contractors are not familiar with the PV technologies yet in Saudi Arabia as well. Decades ago, the water and power had been centralized causing transportation and other cost add-ons to go up, which is now decentralized to be cost effective. The subsidized rate is enjoyed by all sections of society in the Saudi Arabia whereas it is advisable to make it accessible to the poor only and the rich should bear the actual cost to help recover the cost involved in the production process.

In Saudi Arabia, seeing the benefits and plausibility of the solar energy projects, it is imperative to overcome the barriers to expanding the penetration of the solar energy project base. Renewable energy resources tend to be capital intensive due to its upfront investment nature; it is also seen as financially riskier. For example, a new gas turbine generating plant can be installed in the Saudi Arabia for about $800 kW whereas renewable technologies currently range from about $1000 to $2500 kW. The lack of information on the part of customers, vendors, manufacturers and government policymakers as well as the lack of institutional capacity (experience and information) plays a major role in discouraging the appropriate coordination among different institutional entities, and its stakeholders. Besides higher capital costs, other factors such as higher perceived risks, low investor interest, high transaction costs and unreliable policy regimes make the cost of financing generating technologies that use renewable fuels higher with cases charging interest rates upward of 20%. The energy price distortion is an important impediment in this regard. At subsidized energy prices, pay-back periods for RE technologies appear to be less attractive. From a societal perspective, excluding environmental and social cost in the energy price leads to suboptimal energy investments (Al-Natheer, 2005). The operational barriers also need to be eliminated for facilitating the integration of renewable generation technologies with the existing grids.

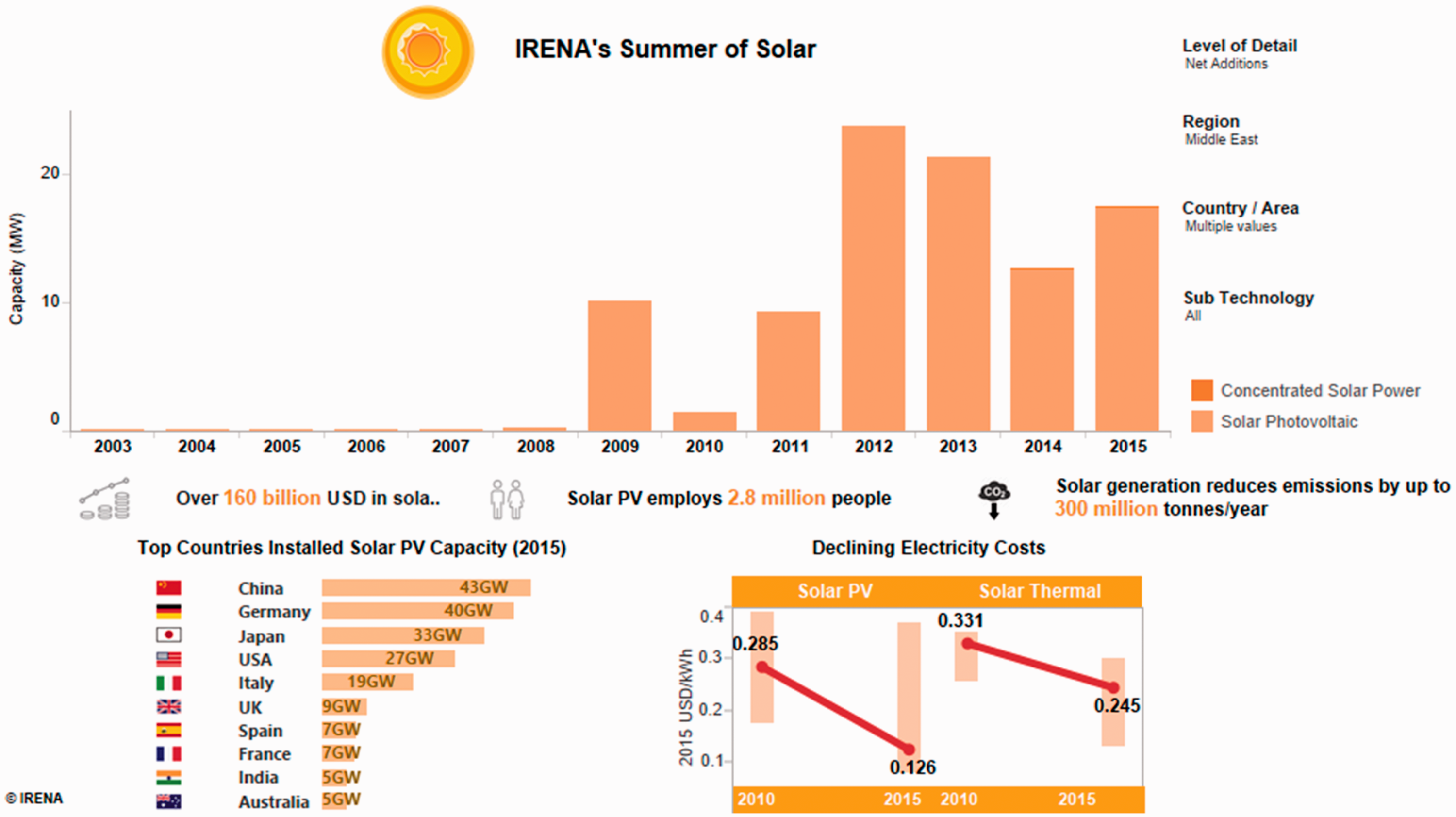

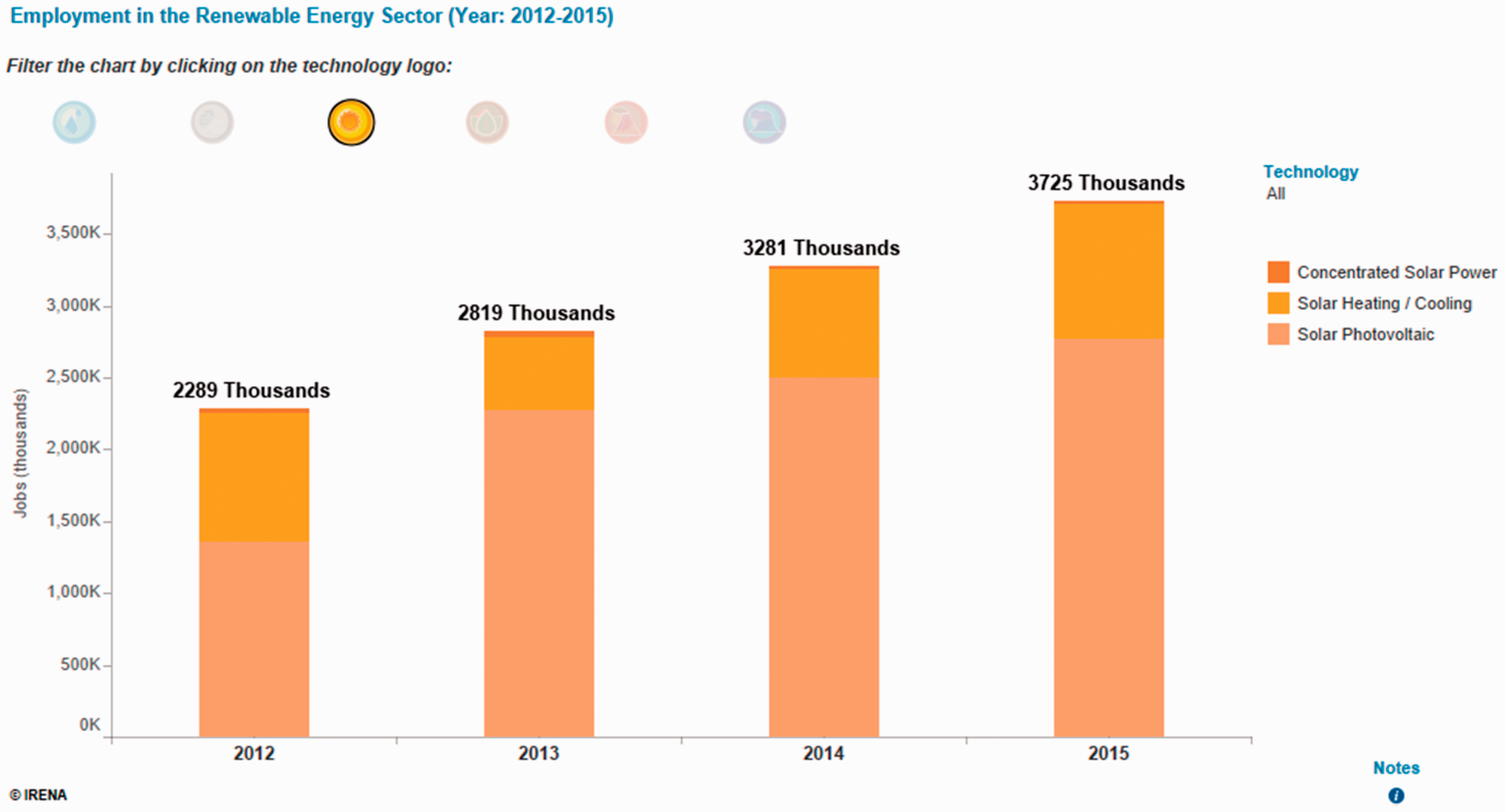

The concern of Saudization, the localization of the workforce and lack of skilled and trained workforce is another issue which needs to be handled properly to make the solar projects successful. Though, the government has taken many steps to upgrade the skill of its people and talent development one of the key performance indicators for the government in its National Transformation Plan 2020 adopted in 2016 to serve the objectives of Vision 2030. The plan envisages creating 450,000 jobs in the non-governmental sector by 2020. Developing the skill and talent of Saudi employees will remain a key issue to fill these jobs. Worldwide, the solar energy sector has been a source of providing gainful employment to its citizens. These solar projects can be of great use for generating employment. In 2015, the total number of global employment in this sector was 3725 million as shown in Figure 4. Alyahya and Irfan (2016b) also argue that Saudi Arabia will need a technical workforce of 218,650 by the year 2030 (i.e. 14 years from now). This would create a demand for 14,577 graduates per year for the next coming 14 years (Table 5). This figure is far above the present capacity of local universities providing technical graduates. With an assumed 50% import of expatriate workforce, the requirement of Saudi graduates becomes 303 per university per year which is still on a higher side. It needs the proper attention on the skill development by the universities and other educational institutions to cater to these requirements. Skill development of the required workforce is a pre-requisite for meeting the demand of the trained and skilled workforce to be deployed in the solar energy sector.

Global employment in various solar energy sectors (years 2012–2015). Source: IRENA (2016a). Estimated workforce requirement with import of workforce. Source: Alyahya and Irfan (2016b).

Conclusion, recommendations and policy implications

There is a need to reinforce the Saudi Arabia’s intent to utilize RE in coming years fully, and being the frontrunners in developing, deploying and implementing the RE source for Saudi Arabia in the GCC. This can be achieved through joint ventures in collaborations with universities, and by adopting pilot projects like the solar project with KAUST, enabling students to have hands-on training, encouraging educational development system tailored to meet local needs, planning of establishing an in-depth knowledge on Nanotechnologies, etc. Among the six GCC countries, Saudi Arabia has emerged as one of the biggest market accounting for PV projects and is expected to contribute to making the region a hub for solar expansion.

Current electricity prices in Saudi Arabia are set well below the long-run marginal costs, and there is little economic incentive to either conserve electricity or to use it more efficiently for consumers. Thus, less subsidization is an issue which needs to be handled as a comprehensive approach to the energy policy aimed at reducing the cost disparities through less subsidization of conventional energy. If it is done judiciously, it can quickly change the equation for the RE (Al-Natheer, 2005; Baltimore, 2008). In that regard, there is a need to adopt a planned increase in the energy cost over several years combined with a more balanced investment strategy which can bridge the gap between conventional and non-conventional energy and make sources like solar and wind viable economically in Saudi Arabia (see also Al-Jarboua, 2009). An efficient use of fossil fuels and an increased share of renewable energies would have several benefits not only for Saudi Arabia but also for other GCC countries. If the domestic use of fossil fuels is reduced, more oil and natural gas could be exported, and it will aid in the stability and security of Gulf region (Reiche, 2010). Saudi initiative towards green power exports will benefit the participating countries from the production of energy and it will also strengthen the local expertise and will generate employment. Green Gulf, the first localized project is expected to extend the solar energy value chain with backward linkage contributing to building the sustainable climate and environment in that regard.

Development of the solar projects will add to the talent development of youths in Saudi Arabia (Alyahya and Irfan, 2016b; Hanware, 2014a). Large scale developments are expected to open gateways to locals through technology transfer and training in the RE technologies. The technology transfer developed under the SOLERAS agreement with the installation of Solar Village Project and solar thermal seawater desalination plant in Yanbu City on the Red Sea are examples of comparatively successful initiatives in the solar sector in this regard (Al-Saleh, 2010).In the solar energy sector, the job market is expected to flourish and more jobs are to be made available in this sector giving an opening to the Saudization process as 95% of employees to be benefited will be Saudi nationals. KACARE, Saudi electricity company (SEC) and Saudi Aramco along with the manufacturing and delivery modules are also working on the know-hows which need to be transferred to semi-government and private sectors for establishing full integrated manufacturing facilities. The help of foreign partners and investors are required to learn from their experiences and expertise, and the localized technology which is lagging behind needs to be strengthened by developing a self-sustainable model based on a value based partnership. The new Vision 2030 catapults the public–private collaboration in this regard. It will surely help in creating a win-win situation by creating a public–private partnership in Saudi Arabia.

The partnership and expertise sharing in RE need to be extended across the globe. Efforts have been made to establish world-class laboratories to support PV and RE related research. Further market mechanisms like CDM (Clean Development Mechanism) have been initiated to reduce carbon emission. A national atlas is required to be established in the Saudi Arabia to provide a one-stop solution. This may include dust, humidity, the wind, soil, rust-causing factors, the degree of tilt of the earth, an abundance of water, natural shade of mountains, etc. To cater the RE needs of the Saudi Arabia (Alyahya and Irfan, 2016a). ISO certifications (ISO 9001-2008) have also made a major landmark in the development of the solar energy projects in the Saudi Arabia. Advancements in Nanotechnology, with trusteeship of 49 patents reflect the depth of research in this field. KACST is further committed to building a generation of technicians and researchers in this area (Al-Awaji, 2001).

There is a need to disseminate more information through media to expand the educational awareness for expanding the RE knowledge base. Research, Development & Demonstration (RD&D) plays a vital role in transferring technology to a country like Saudi Arabia. There is a need to pay attention to the solar energy education, and effective dissemination of solar power technologies (Al-Awaji, 2001; Hasnain et al., 1995; Hassan, 2015). The politics and corruption are also thought to be the knowledge vacuum with a tradeoff of cheap electricity and low water prices to keep the citizens away from the awareness of the energy matters. Besides the tight control of media and authorities about the knowledge distribution contributes to the cause as well. These issues need to be addressed as well (Al-Saleh, 2011). There is a need for a paradigm shift in the government structure to develop more sustainable tariffs which seem to be likely addressed with the adoption of new Vision 2030. The characteristics of the Arab culture such as the high levels of risk avoidance, fear of blame, high centralization of authority, and great respect for authority. These may impede the creativity and transition to an innovation-based economy in the Gulf region, and it needs to be addressed in the long-term (Al-Saleh and Vidican, 2013).

Use of solar applications (especially PVs) is regarded as the best and least expensive means of providing the basic energy services in the region. This can be encouraged by providing solar home systems to provide power for indoor lighting and other DC appliances such as TVs, radios, sewing machines, etc. PV modules can be adopted for lighting especially for homes and community buildings as well as for the telecom towers. Solar cooling systems can be encouraged for commercial applications such as supermarkets, theatres, and cinemas since air-conditioning is one of the largest electricity consumers in the region. Solar water heaters can reduce electricity consumption in water heating sectors for many hot water domestic and industrial applications. There is a possibility of developing large solar power plants supplying off-grid for the desert communities as well (Doukas et al., 2006). All these steps will go a long way in contributing towards the government’s decision to implement the solar energy strategy and save the Saudi Arabia up to 520,000 barrels of oil a day by 2032 which appears to be a large step. There is a need to adopt a multi-pronged approach and integrate the efforts of all stakeholders involved in the energy sector to expedite the process of realization of the solar energy goal. There is a high hope with the new Saudi Vision 2030 adopted very recently which specifically deals with the RE issues. The oil ministry being revamped as the energy, industry and mineral resources have expanded its scope for effectively pushing the development agenda. It will surely boost the solar energy sector in a great way if the bureaucracy is cut down, and efficient implementation of the proposed strategy is done. Bringing public–private partnership for a long-term stake in this sector seems to be a very positive step. It is required to wait and watch for the finer details on this area to come, and its consequent impact on the restructuring of the solar energy sector.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.