Abstract

This study examines the stationary properties of per capita energy use in the 19 Eurozone member countries by using annual data over 1960–2013 period. We utilize the Clemente et al. unit root test that determines structural breaks. Empirical results show that most of the country series does not reject the unit root null hypothesis at the 5% significance level, both in the case of additive outlier and of innovative outlier. Therefore, our empirical findings provide significant evidence that energy use is nonstationary in almost all Eurozone countries. For the policy makers, it is necessary to pay attention to energy use series.

Introduction

The stationarity and unit root properties of per capita energy or electricity series are explored by an increasing amount of studies, which use different methodologies. Examining the time series properties of energy series is crucial both for researchers and for the policy makers, given the close link between energy and the real economy. In fact, if energy exhibits the presence of a unit root, this suggests that this series does not revert to its equilibrium level after being hit by a shock (Kula et al., 2012). Thus, if energy is a nonstationary process, then any shock to energy is likely to be permanent (Chen and Lee, 2007). On the contrary, if per capita energy is a stationary process, then the effect of the shock is transitory, and it is possible to forecast future movements in energy based on the past behaviors of the series. The series will be consistent and stable with path dependency. Path dependency of energy implies that world energy markets innovation will have permanent impacts. There is a large literature examining the causal relationship between energy and real output. Therefore, testing whether the energy use has a unit root is essential to any effective and sustainable energy policy. In the bargain, the issue of whether energy use is stationary has important implications for modeling. The findings from these studies have important policy implications (Mishra et al., 2009). If energy series is nonstationary and is characterized by hysteresis or path dependency, innovations in the world oil market will have permanent effects on energy used. In addition, understanding the correct series behavior of energy use might be vital to distinguish among theories that most accurately describe observed behavior. Energy is known to influence the productivity of labor and capital, among other things. In other words, energy consumption has always aligned relationships with an economic system and is vitally correlated with the economic system (Hsu et al., 2008).

However, in this literature, an interesting aspect is related to the effect of structural breaks. When we conduct research into energy series and the relationship between energy variables and macroeconomics is estimated, we should take structural breaks into account as they can reflect the true current status (Chen and Lee, 2007). In fact, the majority of the studies about the stationarity of energy found that this series is nonstationary when the structural breaks are not considered. While, when structural breaks are taken into account, most of the studies show that energy is stationary. Thus, taking structural breaks in the energy use series will significantly increase the power of the unit root tests. Moreover, to our knowledge, this is the first study that analyzes the topic of stationarity of energy series in the case of Eurozone member countries (Magazzino, 2016). Previous studies that focus exclusively on whether or not energy use is stationary have yielded mixed results.

Besides the Introduction, the remainder of this paper is organized as follows. The second section gives a brief survey of the literature. The third section describes the econometric methodology and the data used. The fourth section summarizes the conclusions we draw and briefly the policy implications that emerge.

Literature review

As clarified before, the issue of the stationarity properties of energy series is receiving a growing attention by applied researchers, also thanks to the relevant implications on economic growth. In fact, it is crucial to fully understand the stationary properties of the energy series since there is a close link between energy variable and real economy. Therefore, testing for the integrational properties of energy variables has emerged as a new branch of research in energy economics. Thus, a clear motivation of the present research is centered in our interest in whether shocks to the time path of per capita energy use are transitory or permanent. Nevertheless, few researches have been devoted to the Eurozone case.

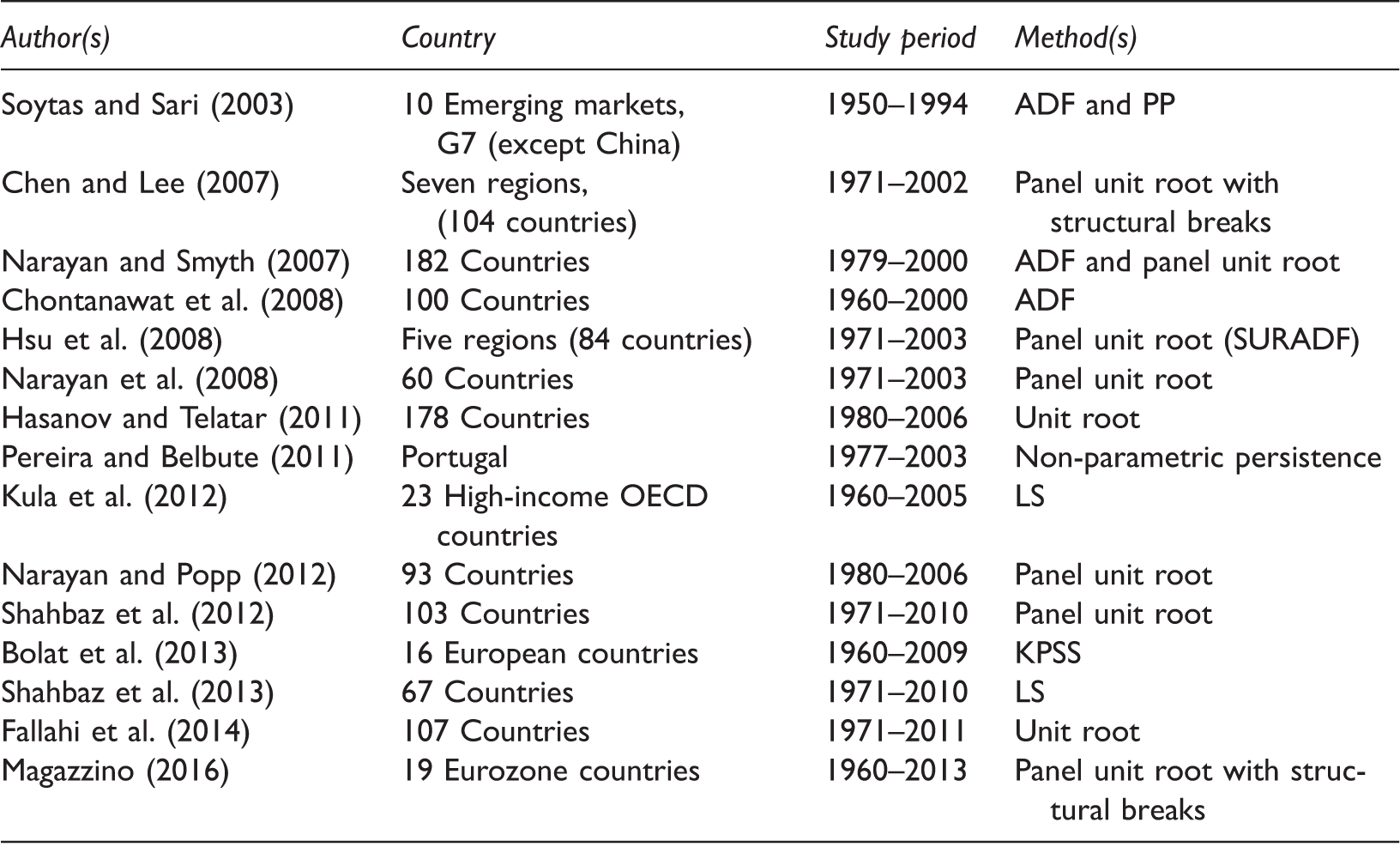

Comparison of empirical literature on stationarity of energy or electricity series for EMU countries.

ADF: Augmented Dickey-Fuller test; KPSS: Kwiatkowski, Phillips, Schmidt, and Shin test; LS: Lee and Strazicich test (Lee and Strazicich, 2003), PP: Phillips-Perron test; SURADF: Seemingly Unrelated Regressions Augmented Dickey-Fuller test.

Source: our elaborations.

Applied studies that include also one or more Eurozone member with a time series approach are due to Fallahi et al. (2014), Bolat et al. (2013), Shahbaz et al. (2013), Kula et al. (2012), Pereira and Belbute (2011), Hasanov and Telatar (2011), Chen and Lee (2007), and Soytas and Sari (2003).

As regards similar studies in the context of panel data, we found those of Magazzino (2016), Narayan and Popp (2012), Shahbaz et al. (2012), Hsu et al. (2008), Narayan et al. (2008), and Narayan and Smyth (2007).

Methodology and data

The econometric literature has proposed several unit root tests with structural breaks. Yet, one obvious weakness of the Zivot and Andrews (1992) strategy, relating as well to similar tests proposed by Perron and Vogelsang (1992), is the inability to deal with more than one break in a time series. Addressing this problem, Clemente et al. (1998) proposed tests that would allow for two events within the observed history of a time series, either additive outliers (the additive outlier [AO] model, which captures a sudden change in a series) or innovational outliers (the innovative outlier [IO] model, allowing for a gradual shift in the mean of the series). This taxonomy of structural breaks follows from Perron and Vogelsang’s (1992) work. However, in that paper the authors only dealt with series including a single AO or IO event (Baum, 2001; Becketti, 2013; Enders, 2014; Franses et al., 2014; Lütkepohl, 2005; Lütkepohl and Krätzig, 2004).

The AO is the type of outliers that affects a single observation. After this disturbance, the series returns to its normal path as if nothing has happened. The IO is the type of outliers that affects the subsequent observations starting from its position or an initial shock that propagates in the subsequent observations. An AO affects only the t observation, whereas an IO affects all observations beyond time t through the memory of the system.

The double-break additive outlier model involves the estimation of the following equation

The equivalent model for the innovational outlier leads to the formulation

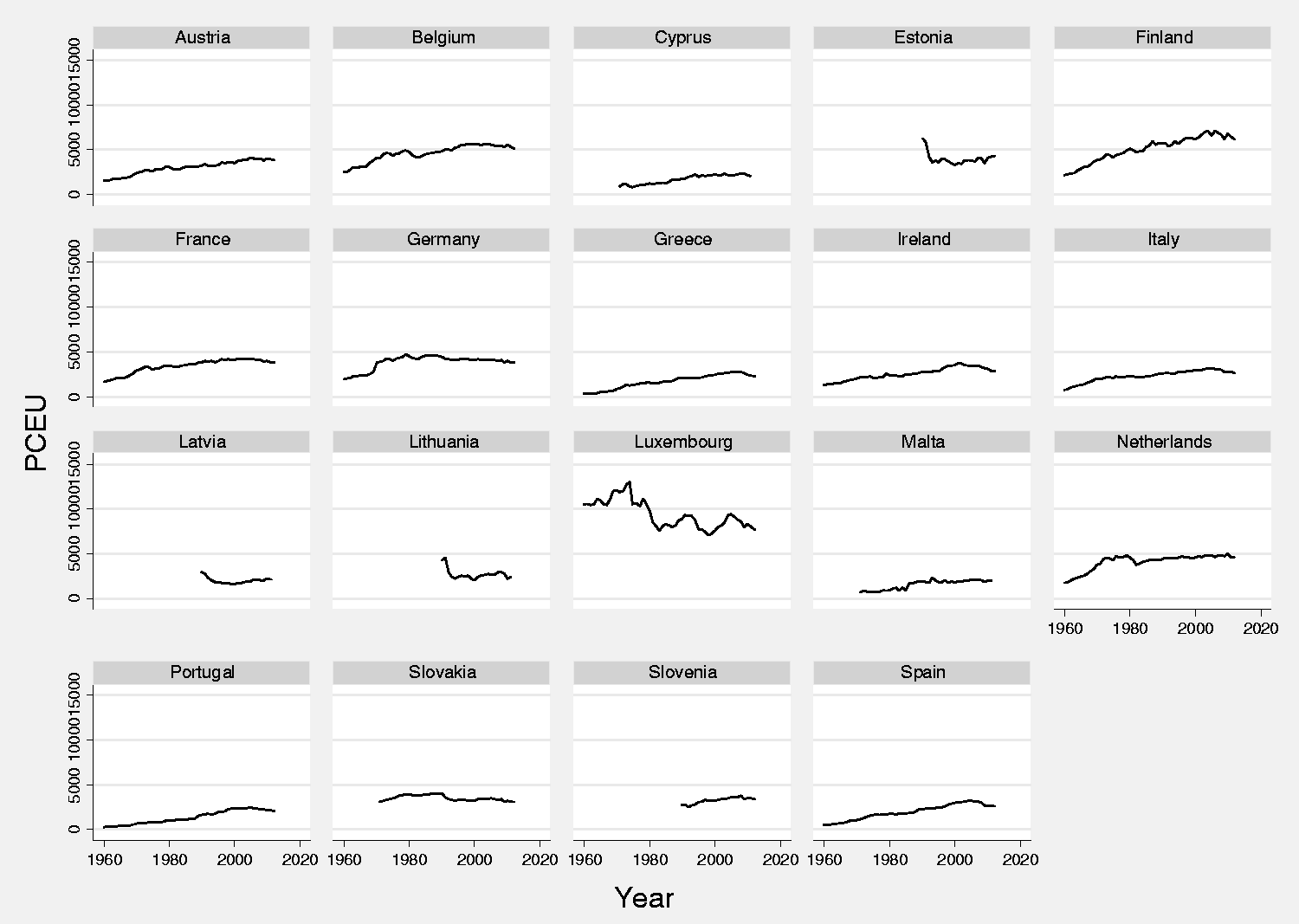

The data of energy use are obtained from the World Bank’s World Development Indicators (WDI) database. The 19 Eurozone member countries considered in this study, for the 1960–2013 period, are Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Luxembourg, Luxembourg, Malta, Netherlands, Portugal, Slovakia, Slovenia, and Spain.

A first graphical inspection is offered by Figure 1, which shows the evolution of these variables, suggesting a general upward trend.

Energy use in the EMU countries (1960–2013, kg of oil equivalent per capita). Source: WB data. Available at: http://data.worldbank.org/indicator/EG.USE.PCAP.KG.OE.

Empirical results

A standard approach in time series studies of energy demand is to first test for the stationarity of energy use and, conditional on the finding of the order of integration, proceed to examine whether energy use is cointegrated with other variables of interest. If energy use is mean reverting, then this series should return to its trend path over time, and it should be also possible to forecast future movements in energy use based on past behavior. To address the low power of univariate unit root tests, recent developments in unit root testing have progressed in two directions. The first is to take into account the structural breaks. A second method concerns the development of panel data unit root tests.

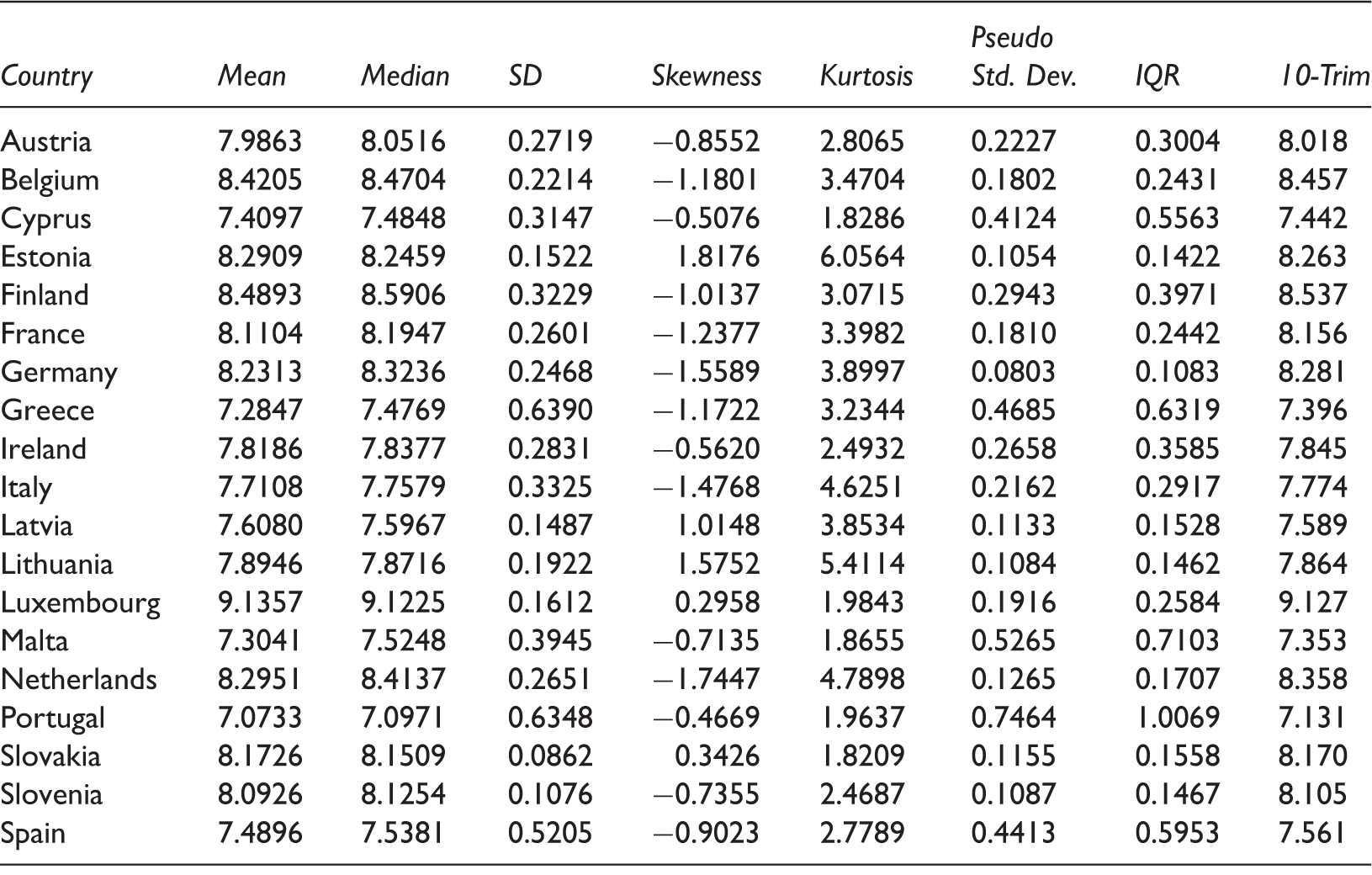

Exploratory data analysis.

IQR: inter-quartile range.

Source: Our calculations on WB data.

Given the fact that for each variable, 10-Trim values are near to the mean, and standard deviation to the pseudo standard deviation, the inter-quartile range (IQR) shows the absence of outliers in the observed sample.

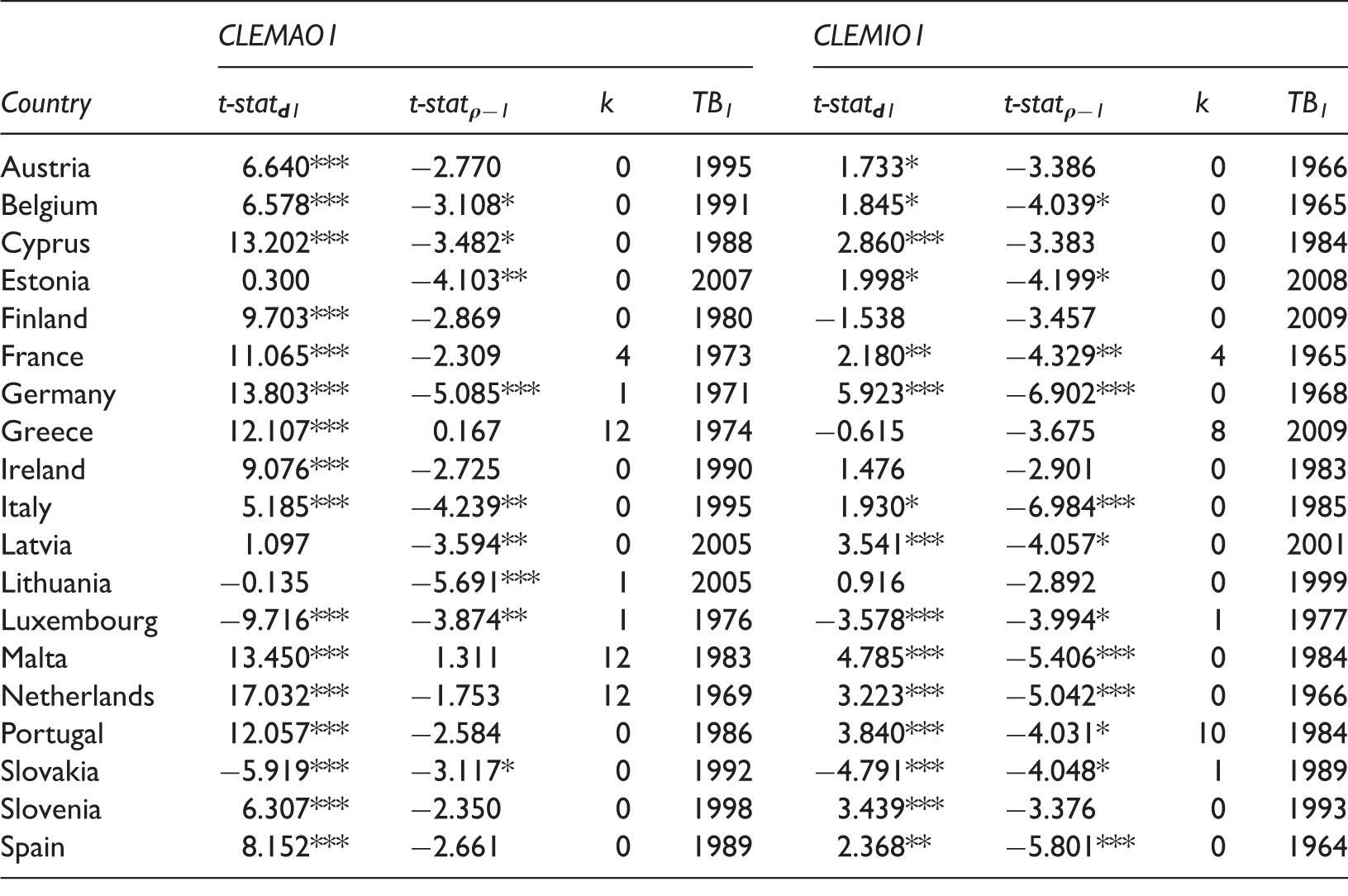

Results for unit root test that allow for one structural break (additive or innovative outlier).

Note: k denotes the lag length. 5% Critical value: −3.560 for CLEMAO1 and −5.490 for CLEMIO1.

p < 0.10. **p < 0.05. ***p < 0.01.

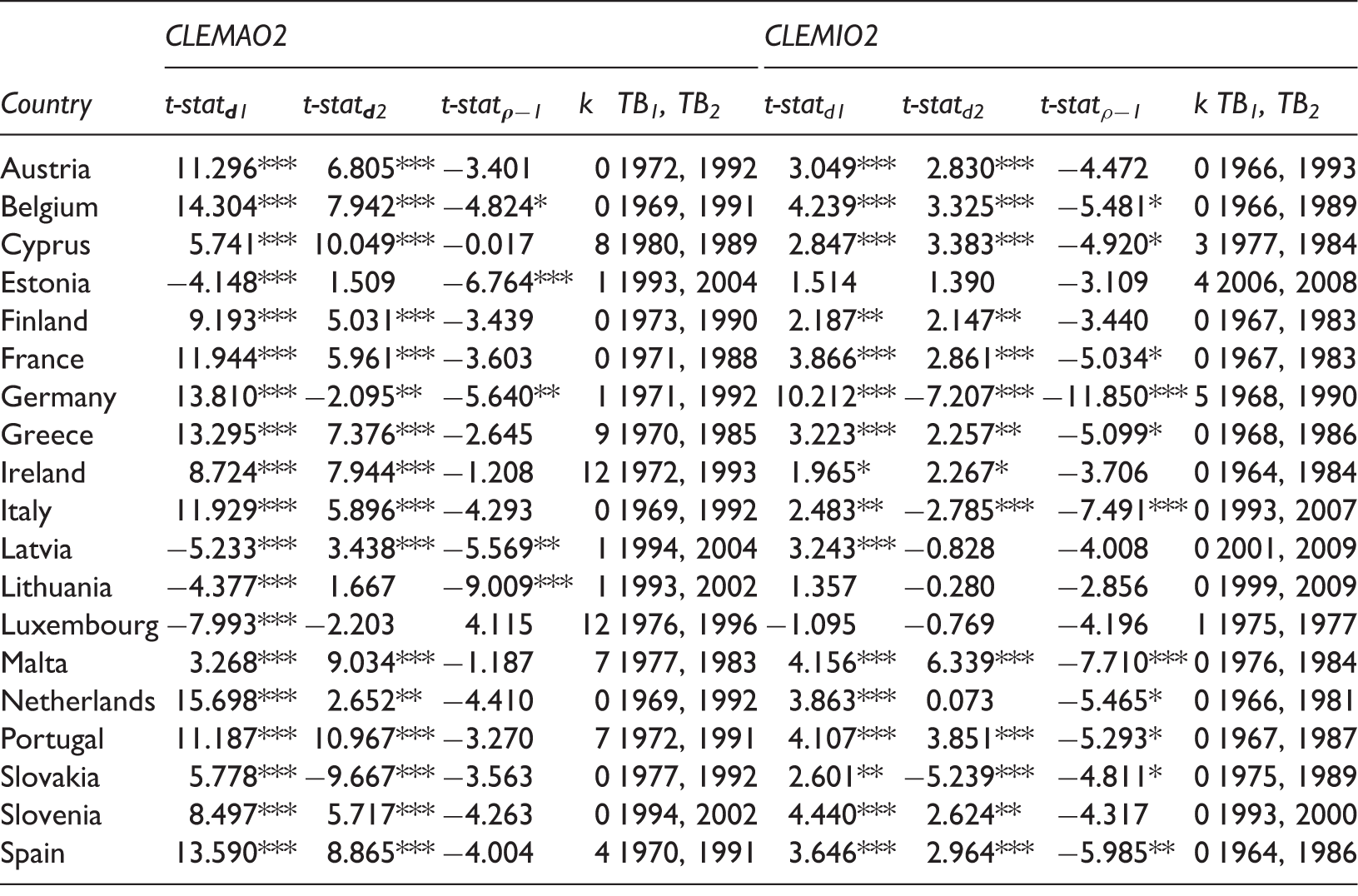

Results for unit root test that allow for two structural breaks (additive or innovative outliers).

Note: k denotes the lag length. 5% Critical value: −5.490 for CLEMAO2 and CLEMIO2.

p < 0.10. **p < 0.05. ***p < 0.01.

Despite the structural break, we are unable to reject the null hypothesis of a unit root in these series for most of the countries, especially in the additive outlier context. In addition, an examination of the break points in Table 4 reveals some clustering of the break dates. It is apparent that most structural breaks in the series occur around the crises (notably the oil shocks and the First Persian Gulf War). This preponderance of break points may reflect recessions during this period, which leads to large shifts in the economic activity. Some policy implications do emerge from our results.

The stationarity properties of energy series have important implications for economic policies, given the effect of structural changes in oil markets on macroeconomic variables. In fact, if energy use is non-stationary, the unit root will be transmitted to other macroeconomic variables. Failure to reject the null hypothesis implies a non-stationary series where innovations in energy use have permanent effects. Thus, if there was a shock to energy series, given the importance of this variable to other sectors in the economy, other key macroeconomic variables would inherit that nonstationary. One source of innovation in energy use is through sudden increases in the price of energy (Narayan and Smyth, 2007). Hamilton (1983) showed that oil price shocks, via their effect on a country’s energy consumption, are responsible for almost for every recession in the USA since World War II. Hamilton (1996) linked oil price shocks to output and inflation.

Conclusions and policy implications

In the current paper, we investigated the stationary properties of per capita energy use in 19 Eurozone member states by using yearly data over the 1960–2013 period. The empirical strategy has used the Clemente et al. (1998) tests. According to the unit root test results, we found that most of the country series does not reject the unit root null hypothesis at the 5% significance level, both in the case of additive outlier and of innovative outlier. The study’s contribution is that we apply the unit root tests with structural breaks to examine the stationarity properties of energy use, thus providing new insights into energy series for Eurozone countries. When we applied the single additive outlier unit root test, we find a unit root in per capita energy use for 53% of the countries, whereas applying the single innovative outlier unit root test only 37% of the sample exhibits a unit root. Therefore, to sum up, our empirical findings provide significant evidence that energy use is nonstationary in almost all Eurozone countries. Our findings from unit root tests in this study suggest that shocks to per capita energy use are permanent. This result implies that following major structural change in the world oil market, per capita energy use will not return to its original equilibrium over a short amount of time. Impact of shocks on energy variable can be permanent or transitory according to its unit root properties. If energy use follows a nonstationary process (i.e., contains a unit root), shocks will be permanent. These results are in contrast with those in Bolat et al. (2013), where a different statistical methodology was employed, whilst partially confirmed those in Magazzino (2016), which contains a panel data analyses of energy use series for the EMU countries. These results are particularly relevant, since almost all Eurozone countries are net oil and gas importers.

Important policy implications emerge from our empirical results of the unit root test with structural breaks. From an economic viewpoint, if key macroeconomic variables are nonstationary, business cycles theories describing output fluctuations as temporary deviations from long-run growth trends lose their empirical support (Cochrane, 1994). Sustainable energy policies rely heavily on the forecasts of energy. In this regard, determining whether shocks to energy are permanent or transitory is important for setting feasible goals for sustainable energy policies. When energy use is nonstationary, then past behavior is of no value in forecasting future demand and one would need to look at other variables explaining energy use in order to generate forecasts of energy demand into the future. In fact, if shocks to energy use have permanent effects, such shocks will be transmitted to the other sectors of an economy, making energy policies based on forecasts invalid. For the policy makers, it is necessary to pay attention to energy use series.

Suggestions for future researches

Given the little amount of studies devoted to the analysis of the stationarity properties of energy series in the Eurozone case, it should be investigated the same properties with a panel approach. In fact, a limitation of most existing studies of the stationarity properties of energy, however, is that they either do not adequately address the problem of cross-sectional correlation and/or allow for structural breaks in the data.

Footnotes

Acknowledgements

Comments from Mauro Costantini (Brunel University), as well as the anonymous referees and the editor are gratefully acknowledged. However, the usual disclaimer applies.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.