Abstract

The aim of the study is to examine the stationary properties of per capita energy use in the 19 Eurozone member countries by using yearly data in the 1960–2013 period. First and second generation of panel unit root tests are applied. Empirical findings show mixed results, since the evidence favors the panel stationarity of energy use per capita in all groups of countries for the specification with the constant only; on the contrary, in the specification with constant and trend, the null hypothesis that all series are non-stationary cannot be rejected. Therefore, policymakers should be cautious, paying attention to the energy use series’ properties, as different results conduct to opposite policy implications.

Introduction

The stationarity and unit root properties of per capita energy or electricity series are explored by an increasing amount of studies, which use different methodologies. Examining the time series properties of energy series is crucial both for researchers and for the policymakers, given the close link between energy and the real economy. In fact, if energy exhibits the presence of a unit root, this suggests that this series does not revert to its equilibrium level after being hit by a shock (Kula et al., 2012). Thus, if energy is a non-stationary process, then any shock to energy is likely to be permanent (Chen and Lee, 2007). On the contrary, if per capita energy is a stationary process, then the effect of the shock is transitory, and it is possible to forecast future movements in energy based on the past behaviors of the series. The series will be consistent and stable with path dependency. Path dependency of energy implies that world energy markets innovation will have permanent impacts. There is a large literature examining the causal relationship between energy and real output. Therefore, testing whether the energy use has a unit root is essential to any effective and sustainable energy policy. In the bargain, the issue of whether energy use is stationary has important implications for modelling. The findings from these studies have important policy implications (Mishra et al., 2009).

In addition, in this literature, an interesting aspect is related to the presence of cross-section dependence. In fact, only the more recent studies deal with it. Yet, taking cross-section dependence into account can completely change the tests results, conducting to opposite policy implications.

Moreover, to our knowledge, this is the first study that analyzes the topic of stationarity of energy series in the case of Eurozone member states in a panel context. In early 2007, the Commission put forth its ambitious energy-climate package, which unambiguously illustrated the role of the EU in leading the effort to create a climate-compatible energy system. The “20/20” package included the goals for 2020 of reducing GHG emissions by 20%, improving energy efficiency by 20%, achieving a 20% share of renewable energy, and a 10% share of biofuels (Eurostat, 2009).

Besides the “Introduction” section, the remainder of this article is organized as follows: “Literature review” section show a concise survey of the literature; “Samples selected and analytical methods” section presents the econometric strategy and data; and “Conclusions and policy implications” section gives the conclusions and policy implications.

Literature review

The topic of the stationarity properties of energy series is receiving a growing attention by applied analysts, because of its relevant implications on energy policies established by national authorities. Thus, testing for the unit root and cross-section dependence of energy variables emerged as a new branch of research in energy economics. Notwithstanding, empirical analyses for the Euro area member states are very few.

Comparison of empirical literature on stationarity of energy or electricity series in a panel data framework.

Source: Our elaborations.

GMM: Generalized Method of Moments; SURADF: Seemingly Unrelated Regressions Augmented Dickey-Fuller test.

Empirical analyses that concern also one or more Euro area member countries with a panel data approach are those of Lee and Chang (2007), Narayan and Smyth (2007), Hsu et al. (2008), Huang et al. (2008), Lee et al. (2008), Narayan and Smyth (2008), Lee and Lee (2010), Belke et al. (2011), Narayan and Popp (2012), and Shahbaz et al. (2012).

Samples selected and analytical methods

The econometric literature has proposed several unit root tests in a panel framework (Baltagi, 2013; Frees, 2004; Hsiao, 1989; Wooldridge, 2010).

The first generation of panel unit root tests here considered include Fisher-type test, IPS test (Im et al., 2003), and MW test (Maddala and Wu, 1999). The second-generation test is CADF (Pesaran, 2003). The main difference between two generations of tests lies in the cross-sectional independence assumption. In fact, first generation tests assume that all cross-sections are independent, whereas second-generation tests relax this assumption. Analogous to IPS test, Pesaran’s CADF is consistent under the alternative hypothesis that only a fraction of the series are stationary. Pesaran (2007) suggested modified IPS statistics based on the average of individual CADF, which is denoted as a cross-sectional augmented IPS (CIPS). In addition, second-generation tests are more useful when co-movements are observed in the national business cycles in a sample of countries in the same economic area (Hurlin and Dumitrescu, 2012). Cross-section dependence in macro panel data may arise from globally common shocks with heterogeneous impact across countries. Alternatively, it can be the result of local spillover effects between countries or regions (Eberhardt and Teal, 2011; Moscone and Tosetti, 2009). In this study, we employed several tests. The Pesaran (2004) CD-test employs the correlation-coefficients between the time-series for each panel member. The test is robust to nonstationarity, parameter heterogeneity, or structural breaks, and was shown to perform well even in small samples (Pesaran, 2006). Moreover, we present results of semiparametric Friedman (1937) test, as well as the parametric testing procedure proposed by Pesaran (2004), which test the hypothesis of cross-sectional independence in panel-data models with small T and large N.

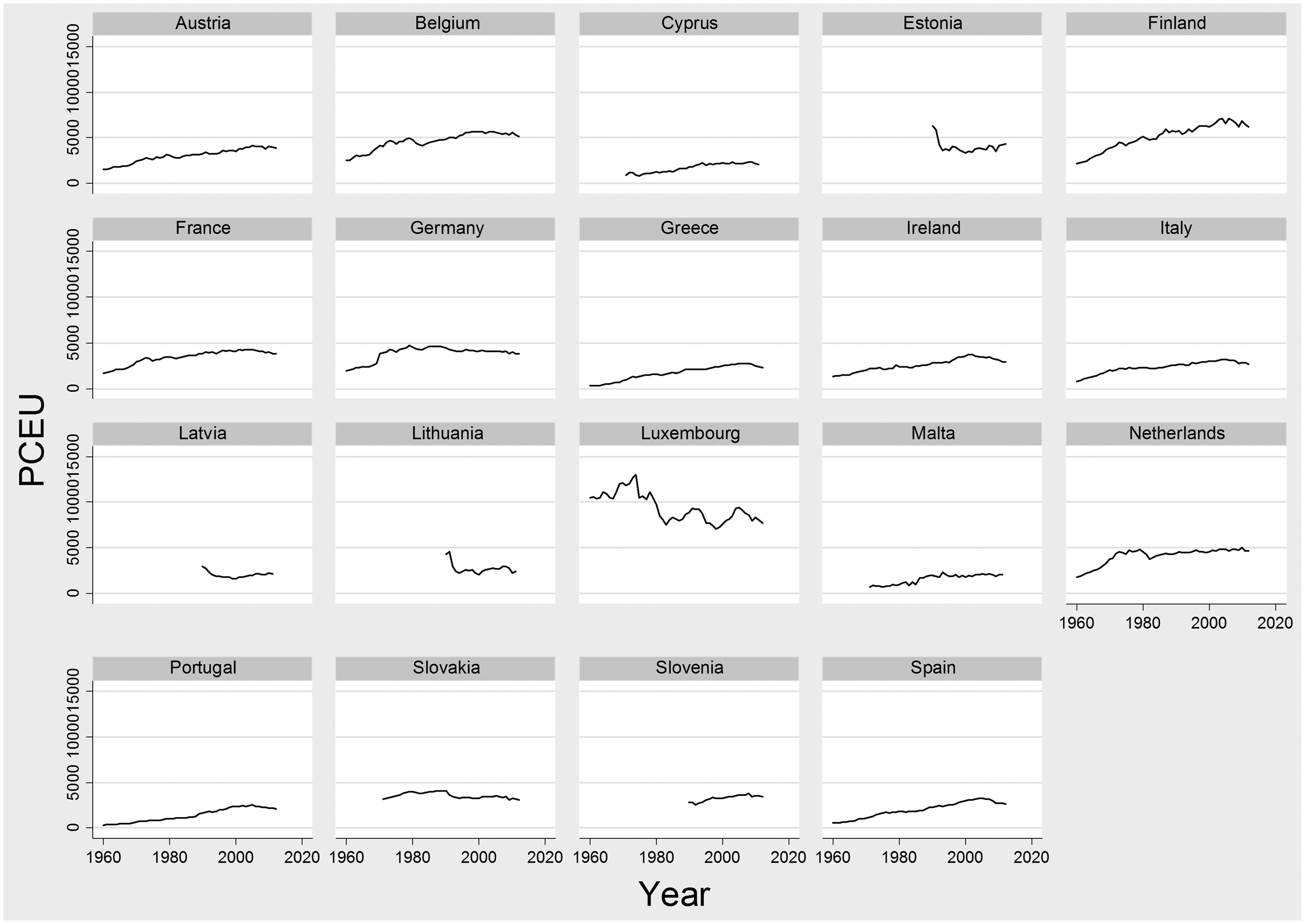

The energy use series are derived from the World Development Indicators (WDI) database by World Bank. The 19 Eurozone member countries considered in this study, for the 1960–2013 period, are Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Luxembourg, Luxembourg, Malta, Netherlands, Portugal, Slovakia, Slovenia, and Spain.

Figure 1 gives an initial graphical inspection of these series, showing the evolution of selected data: an upward trend seems to emerge.

Energy use in the EMU countries (1960–2013, kilograms of oil equivalent per capita).

Results and discussion

Exploratory data analysis.

Source: Our calculations on WB data.

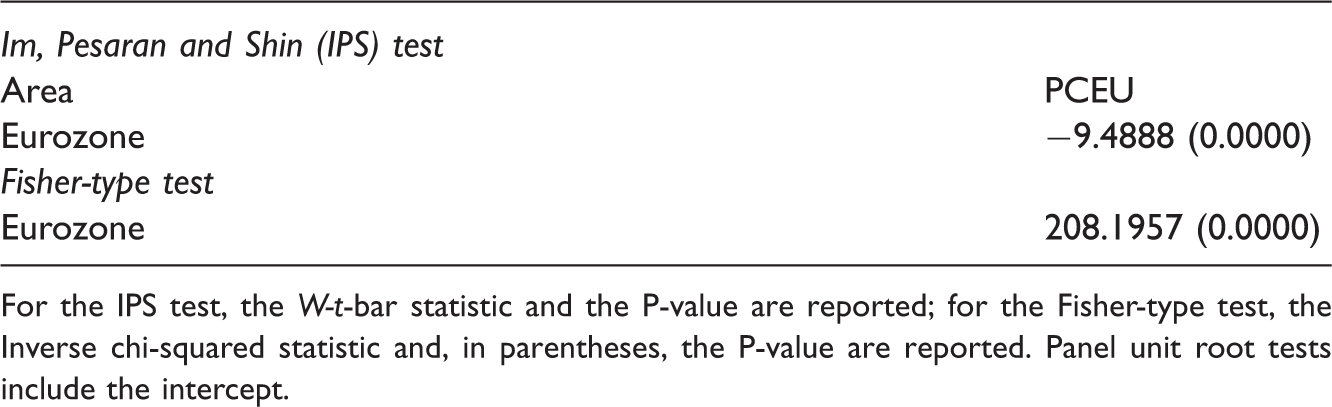

First generation panel unit root tests.

For the IPS test, the W-t-bar statistic and the P-value are reported; for the Fisher-type test, the Inverse chi-squared statistic and, in parentheses, the P-value are reported. Panel unit root tests include the intercept.

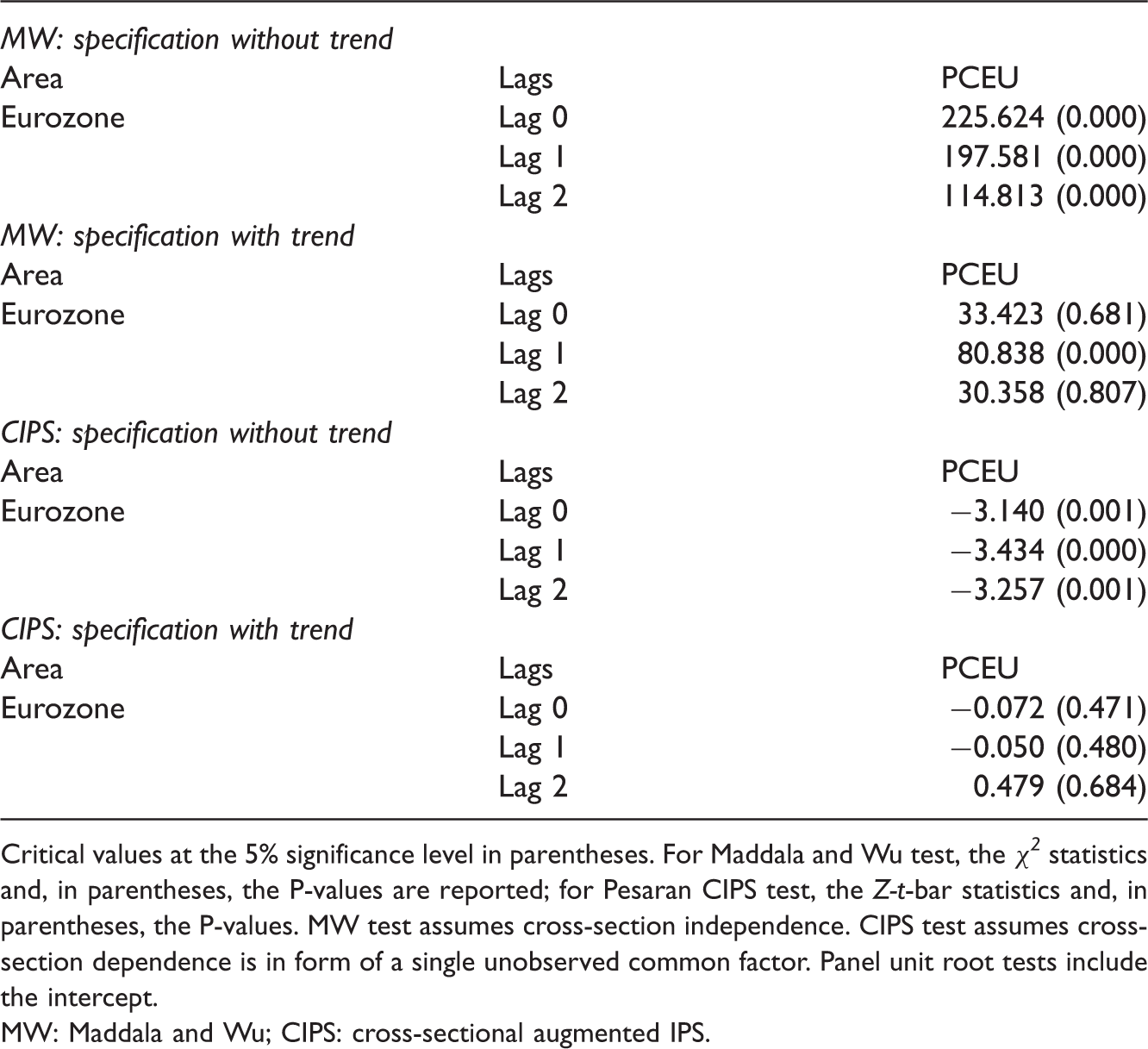

MW and Pesaran’s CIPS panel unit root tests.

Critical values at the 5% significance level in parentheses. For Maddala and Wu test, the χ2 statistics and, in parentheses, the P-values are reported; for Pesaran CIPS test, the Z-t-bar statistics and, in parentheses, the P-values. MW test assumes cross-section independence. CIPS test assumes cross-section dependence is in form of a single unobserved common factor. Panel unit root tests include the intercept.

MW: Maddala and Wu; CIPS: cross-sectional augmented IPS.

Panel cross-section dependence tests.

: Pesaran (2004) cross-sectional dependence in panel data models test; 2: Pesaran (2004) CD test for cross-section dependence in panel time-series data; 3: Friedman (1937) test for cross-sectional dependence by using Friedman’s χ2 distributed statistic. P-values in parentheses. Tests include the intercept.

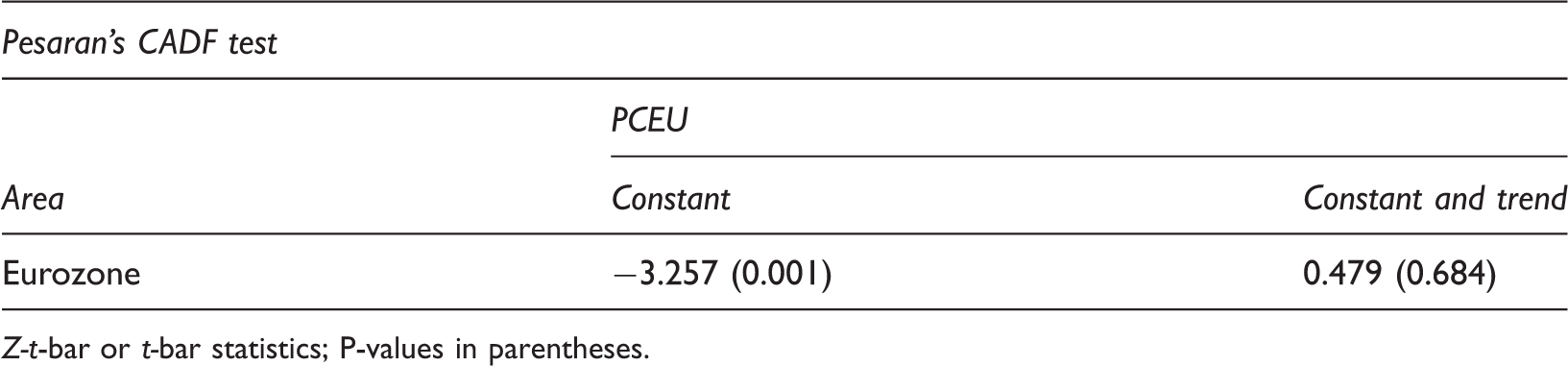

Panel unit root test in presence of cross section dependence tests.

Z-t-bar or t-bar statistics; P-values in parentheses.

Therefore, after we take the cross-sectional correlations into account, our results substantiate that the panel datasets for the 19 country-based panels are non-stationary. In fact, in the specification with constant and trend, the null that all series are non-stationary cannot be rejected, which is a clear sign of the non-stationary properties of the series; otherwise, it means that any shock may have a transitory effect on energy use. If most shocks to energy use were temporary, then a stabilization energy policy would have long-lasting effects in the selected panels according to our results. When energy use temporarily deviates from the mean value, the administrative policy of the government should not be to adopt unnecessary targets.

However, and this is relevant to note, when we consider the specification with the constant only, the evidence favors the panel stationarity of energy use per capita in all groups of countries. The fact that energy use shows stationarity indicates that it should be possible for the series to forecast future movements in energy use based on past behavior. Other macroeconomic variables linked to energy demand via flow-on effects, such as income, will not inherit that non-stationarity and transmit it to major economic variables, such as employment (Narayan and Smyth, 2007).

Conclusions and policy implications

In this study, we analyzed the properties of per capita energy use in 19 Eurozone member countries, using annual data for the 1960–2013 period. As regards the empirical strategy, first and second generation of panel unit root tests have been applied. As discussed above, we found mixed results. In fact, for the specification with constant and trend, we reach the conclusion that the series are non-stationary, meaning that any shock may have a transitory effect on energy use. On the other hand, the alternative specification with the constant only is in favor of stationarity, indicating that it should be possible for the series to forecast future movements in energy use based on past behavior.

Important policy implications emerge from our empirical results. Sustainable energy policies rely heavily on the forecasts of energy. In this regard, determining whether shocks to energy are permanent or transitory is important for setting feasible goals for sustainable energy policies. When energy use is non-stationary, then past behavior is of no value in forecasting future demand and one would need to look at other variables explaining energy use to generate forecasts of energy demand into the future. In fact, if shocks to energy use have permanent effects, such shocks will be transmitted to the other sectors of an economy, making energy policies based on forecasts invalid. Thus, for the policymakers, it is necessary to pay attention to energy use series.

Suggestions for future researches

Given the little amount of studies devoted to the analysis of the properties of energy series in the Euro area countries, it should be investigated the same properties with a time series approach. In fact, a limitation of most existing studies of the stationarity properties of energy, however, is that they do not adequately address the problem of unit root and/or allow for structural breaks in the data. Moreover, stationarity and cross-section dependence should be explored also for disaggregated data (i.e. different sources of energy) (Magazzino, 2012).

Footnotes

Acknowledgments

The author would like to thank two anonymous referees and the Editor for their valuable suggestions and helpful comments, which have greatly enhanced the quality of this article. Any remaining errors, of course, belong to the author.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.