Abstract

Microfinance institutions (MFIs) have been promoted worldwide as developmental platforms that can help eliminate some of the major global challenges such as poverty and economic development. The effectiveness of using MFIs to fulfil such expectations depends on their performance, which can be affected by a range of institutional factors such as corruption, rule of law and financial sector development. However, there is a lack of clarity on whether these factors are performance inhibitors or promoters. Using gender as a mediating factor, this study develops and tests these relationships on MFI performance, with the aim of contributing to research on institutions and corruption in the Global South. Drawing on the MFI performance model, the study uses data on MFIs operating in 33 African countries. The results reveal that the control of corruption reduces MFIs’ operating expenditure, while it increases MFIs’ operating income. Drawing from the essentialist perspective of the theory of social construction of gender, it is argued that female borrowers from MFIs are shown to have a mediating impact on the relationship between the variables tested (such as control of corruption) and MFI performance. The study also has public policy relevance for nations seeking to use MFIs as means of fostering entrepreneurship and economic development.

Introduction

Organizational performance literature has covered factors such as corruption (Fisman and Svensson, 2007; Van et al., 2018), rule of law (North, 1990; Scott, 2013), financial sector development (Vanroose and D’Espallier, 2013) and gender (Swamy et al., 2001), among others, as performance inhibitors or promoters. However, the relationships between these factors and organizational performance within the context of microfinance institutions (MFIs) has yet to be empirically explored. In particular, corruption, which is defined as ‘a role behavior in any institution (not just government or public service) that violates formally defined role obligations in search of some private gains’ (Luo, 2002: 407), remains a potent force in most of the Global South nations, leading to misallocation of resources and forcing firms to reposition their operations (Rose-Ackerman, 2002, 2016; Shleifer and Vishny, 1993). Traditionally, much of what has been established by scholars revolves around the notion that corruption is a disruptive force in discouraging foreign direct investment (Brouthers et al., 2008; Cuervo-Cazurra, 2006; Habib and Zurawicki, 2002). Besides having negative effects on economic growth, corruption also has potential to erode public confidence in the legal and political systems (Rose-Ackerman, 2016; Shleifer and Vishny, 1993).

In spite of the growing lines of research on corruption and corrupt practices (Misangyi et al., 2008; Rose-Ackerman, 2016), there are two major deficiencies with the current research. First, although MFIs are important and legitimate organizations that offer valuable avenues for scholarly enquiry (see Gul et al., 2017), few scholars have sought to examine the effects of corruption on their operations, including expenditure and operating income. Second, although corruption and local institutions influence the activities of MFIs, the two research streams have grown in isolation, despite the potential linkage between the pursuit of noble objectives of MFIs, and the corrupt practices in a given country.

Against this background, our main purpose is to examine how the control of corruption, rule of law and financial sector development affect MFIs in terms of input (expenses) and output (income) in Africa. To accomplish this objective, we utilize a data set on MFIs operating in 33 African countries to test this relationship.

In addressing the gaps in the literature, we contribute to several streams of literature on business ethics, institutions and corruption in various ways. First, we extend the existing literature on the institutions-based view (Meyer et al., 2009; Peng et al., 2008) that focuses almost exclusively on the effects of formal and informal institutions on multinational enterprises (MNEs), state-owned enterprises and some small and medium enterprises (SMEs). Thus, there is also a need to extend our understanding of the effects of corruption beyond large private firms to include MFIs in the developing world. This study departs from current literature by offering robust analysis on the effects of corruption, rule of law and financial sector development on MFIs.

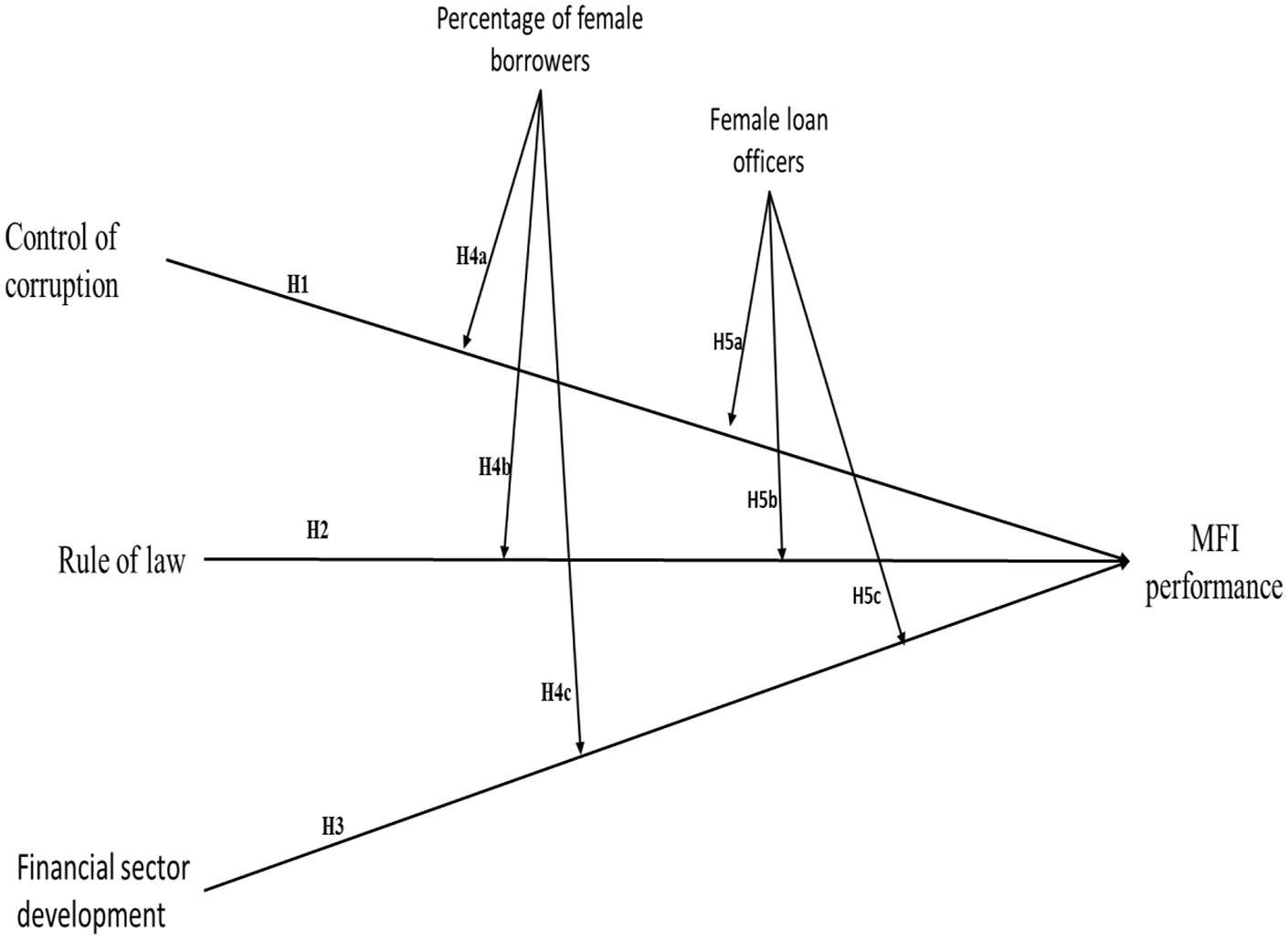

Second, we develop a model (see Figure 1) which captures the effects of corruption, rule of law and financial sector development on MFIs’ operating expenditure and operating income. Thus, we offer an emerging African perspective on this issue. Moreover, this article advances the understanding of the corruption literature (Cuervo-Cazurra, 2006; Rose-Ackerman, 2016) by examining how corruption affects the operations of MFIs. Thus, the study constitutes one of the first empirical works in the African setting examining and deepening our understanding of the effects of corruption beyond MNEs and state-owned organizations. After reviewing the literature on institutions, corruption and MFIs, we present our conceptual model and research methods. This is followed by the key findings of the study. The final section sets out both the theoretical and policy implications of the study.

Conceptual model.

Literature review

Theoretical foundations: Institutions, corruption and governance

The institution-based view contends that organizations’ ability to operate and achieve success or failure is shaped by institutions (Meyer et al., 2009; Peng et al., 2008). Defined as ‘the rules of the game in a society or, more formally, the humanly devised constraints that shape human interaction’ (North, 1990: 3), institutions play a pivotal role in outlining the political, social and legal constraints that shape organizations’ operations (North, 1990; Peng et al., 2009). Institutions are conceptualized to include formal and informal institutions (North, 1990; Peng, 2017). Formal institutions include legal systems, political systems and economic systems, whereas informal institutions capture norms, cultures and ethics in the society (Peng, 2017). The wider institutional framework, such as the rule of law, not only shapes but also governs individuals and organizations’ behaviour in terms of what is right or wrong within the society (North, 1990; Scott, 2013). Thus, organizations may adopt ‘local ways of doing things’ to respond to the normative, cognitive and regulatory pressures to gain and maintain legitimacy (Amankwah-Amoah and Debrah, 2017; DiMaggio and Powell, 1991). For example, although bribery is illegal in advanced nations, in developing and corrupt nations it may be seen as a legitimate means of doing business (Cuervo-Cazurra, 2016). Nevertheless, organizations may be forced to comply or adopt new approaches in order to be perceived as legitimate (Cuervo-Cazurra, 2016).

Another perspective comes from the persuasive school of thought which considers how the internal and external institutions (including political and cultural systems) determine and prevent corruption (Brunetti and Weder, 2003; Misangyi et al., 2008). Whilst internal institutions seek to engender anti-corruption practices through systems and procedures, external institutions operate as a check on public sector and government appointees (Peltier-Rivest, 2018). Political institutional frameworks such as watchdogs, anti-corruption and independent governmental institutions have been set up to combat corruption (Head, 2012; Spigelman, 2004; Vibert, 2007), minimize waste and improve accountability systems for better democratic governance (Melo et al., 2009). Formal political institutions influence political stakeholders’ exercise of power and ensure that public officials are held accountable (Fjelde and Hegre, 2014; Tavits, 2007). It has also been found that political institutional trust serves as a key influence on individual attitudes towards corruption (Sööt and Rootalu, 2012).

Despite overwhelming evidence that political institutions play a key role in minimizing or exacerbating the influence of corruption (Ferraz and Finan, 2011; Myerson, 1993; Torsten et al., 1997; Yerrabati and Hawkes, 2016) most of the studies have been based on corruption perception indices, examples being Transparency International’s Corruption Perceptions Index (CPI) and the World Bank’s Control of Corruption Index. Beyond the practical difficulties associated with researching actual corruption cases, Ferraz and Finan (2011) opined that the predominant cross-country analysis of the role of political institutions on corruption has focused on macro-level analysis. As a result, this has impeded the unravelling of the full complement of political institutional architecture that promotes or inhibits corruption at country, industry or organizational levels. Nevertheless, it is important to reiterate that the influence of corruption on political institutions has been established in the extant literature (see Anderson and Tverdova, 2003; Chang and Chu, 2006; Cho and Kirwin, 2007; Mishler and Rose, 2001; Pellegata and Memoli, 2016; Seligson, 2002).

Effects of corruption

Corruption has received much research attention, from various subject areas including anthropology, history, sociology and psychology, and organizational studies, and from sub-disciplines such as organizational behaviour, business ethics and management (Engels, 2010; Fein and Weibler, 2014; Treviño et al., 2006; Von Alemann, 2005). Despite its broad coverage in many academic disciplines, the concept of corruption depends on different perceptual underpinnings of researchers and other stakeholders (Johnston, 2005; Pellegata and Memoli, 2016). This has led to some variances on what is generally accepted as a corrupt action (Brei, 1996). For this reason, some corruption academics suggest that the well-known Transparency International’s Corruption Perceptions Index (CPI) and the World Bank’s Control of Corruption Index (CC) do not offer a comprehensive insight into corruption as the indices are based on the views of metropolitan populations and the private sector stakeholders (Andersson and Heywood, 2009; Pellegata and Memoli, 2016). This point of view is well articulated by Von Alemann (2005) to the effect that as a concept, corruption relies on the perceptual predisposition of the investigator of a ‘given’ corruption incidence. Such has been the position of the corruption literature for many decades. Indeed, Senturia (1930) asserted that insight into corruption is reliant on the views of the researcher and the prevailing major political and public moral ethos. Corruption is therefore best understood within a given social and cultural context (Dalton, 2005; Fein and Weibler, 2014).

Despite the definitional and contextual limitations, the existing literature has established the effects of corruption on organizations. Earlier inertia on the part of liberal economists who detested any form of market regulation relegated ethical consideration within business organizations to the background (Fein and Weibler, 2015). However, as the business sector continues to embrace ethics there has been a corresponding increase in research interest in business ethics and corruption (Kuhn and Weibler, 2012; Rendtorff, 2016; Rose-Ackerman, 2005; Sroka and Lőrinczy, 2015). The connection between corruption and organizational performance has been established (see Fisman and Svensson, 2007; Van et al., 2018) and there is agreement in the existing literature that corruption affects organizations. However, the literature is sharply divided on the direction of impact of corruption on performance either as a promoter or inhibitor (Van et al., 2018). The only exception is a paper by Cheung et al. (2012), whose findings demonstrate that corruption, particularly bribery activities, generates both benefits and costs to firms in many developed countries.

Other studies have mainly focused on corruption as an inhibitor, particularly in terms of organizational performance, diverting critical resources for innovation and the resultant reputational damage (Hung, 2008; Luo, 2002); reduced profit and inefficient use of firms’ human and technological resources (Murphy et al., 1993); stifled competition through high costs of new entry imposed by corrupt industry players (Rose-Ackerman, 1997); reduction of employment in firms (Beltrán, 2016); and impediment of firms’ adoption of quality standards (Paunov, 2016) and firms’ financial performance (Kim et al., 2017; Van et al., 2018). The alternative point of view is that corruption enables organizations to resolve bureaucratic and regulatory challenges and hence acts as a promoter of organizational performance (De Jong et al., 2012; Lau et al., 2013; Lui, 1985; North, 1990; Vial and Hanoteau, 2010). Studies on corruption further show that the impact of corruption (positive or negative) does affect types of organizations differently. For instance, Paunov (2016) found that corruption impedes the performance of smaller organizations but does not impact on exporters or foreign- and publicly-owned companies. Similarly, Faruq et al. (2013) reported that organizations that are less productive have a higher tendency to engage in corruption as compared to more productive business counterparts.

A critical examination of studies on the effects of corruption on organizational performance further reveals that the effect of corruption on financial performance has yet to receive much research attention, with just a few empirical studies conducted (see Donadelli et al., 2014; Van et al., 2018) in comparison with the research focus on its effects on organizational productivity and growth. Fein and Weibler (2015) further point out the lack of depth and focus and unsubstantiated generalization within behavioural ethics, organizational behaviour and management studies literature on corruption. Specifically, they question how generalizable the western views of corruption are, given the different conceptualization of corruption across the world, and especially Africa. While there is growing interest in corruption research in Africa, there are limited systematic empirical studies that shed light on the influence of corruption and other performance-related factors on MFIs. Based on the above analysis, we hypothesize the following:

H1. The control of corruption increases MFIs’ performance.

H2. Rule of law increases MFIs’ performance.

H3. Financial sector development increases MFIs’ performance.

Moderating effects of gender

The recent launch of the new International Standard Organization (ISO) anti-corruption standard (ISO37001) reinforces the understanding that corruption has been identified as one of the main unethical business practices in the business environment, which needs to be tackled (Institute of Business Ethics, 2012; Rose-Ackerman, 2002). Contemporary research and debate on corruption have also examined its role and impact as mediated by gender differences. Frank et al. (2011) explain that research on the gender–corruption nexus has taken three main directions. Firstly, whether there are gender differences with respect to willingness to engage in corrupt practices. Secondly, evaluating the effects that corruption may have on the policy goal of enhancing gender equality. Lastly, whether men and women experience corruption differently when faced with it within the same context.

The current study does not seek to examine the impact of the gender–corruption nexus on gender policy (second research agenda) or whether men or women experience corruption differently (the third research agenda). Rather, this study is placed within the research context of the first view, by seeking to examine whether there are any gender-related differences with respect to willingness to engage in corrupt practices and whether an increase in women within microfinance organizations as loan officers (internal agents) reduces corruption or otherwise, and the impact on MFI performance. Further to this, the study also seeks to explore whether female loans borrowers in microfinance organizations (external agents) also moderate corruption or otherwise within such organizations, and their impact on MFI performance.

Scholarly scrutiny of the gender–corruption nexus has been characterized by disagreements and intellectual tensions (Frank et al., 2011; McCabe et al., 2006). For instance, Swamy et al. (2001) undertook a cross-country analysis to investigate the relationship between gender and corruption. Using micro-data, they established that women are less involved in bribery, and are less likely to condone bribe-taking. Similar research findings have been reported by, inter alia, Dollar et al. (2001) and Rivas (2013). Some proponents of this view have argued that institutional logics mediate to explain this gendered difference with corruption. Stensöta et al. (2015) argued that the stronger the bureaucratic principles are in the administration processes within the institution, the less gender matters. In the microfinance sector, Azim et al. (2017) highlighted some governance-based bureaucratic principles and mechanisms which can help diminish opportunities for corruption. These include factors such as decentralization of authority, strong monitoring and review of decision-making processes, high internal audit intensity, impersonal punishment, anti-corruption cultures and transparency. What is unclear, however, is the level at which MFIs have adopted such governance and bureaucratic principles which mediate against corruption in developing regions such as Africa. Consequently, research such as this, which seeks to examine issues around gender and institutional factors (such as the control of corruption and the rule of law) and their effect on microfinance institutions in Africa, has become not just important but also timely.

Opposed to the ‘females are less corrupt’ views are other research studies that accentuate that there are no gender differences towards corruption. For instance, Azfar and Nelson (2007) report that women are not necessarily more intrinsically honest or averse to corruption than men, but rather they react more strongly to a given risk of detection. Beyond the two contradicting extreme views on corruption and gender, Alatas et al. (2006) suggest that gender differences found in previous studies are not universal as stated and that they may be more culturally specific. Their studies used experimental analyses from data collected from different regions and cultures, such as Australia, India, Indonesia and Singapore. Recently, others, including Alhassan-Alolo (2007) and Armantier and Boly (2008), have echoed the stance by Alatas et al. (2006) by also stating that the attitudes and behaviours of women concerning corruption depend on institutional and cultural contexts. For instance, Alhassan-Alolo (2007) reported that other factors can affect the attitudes and behaviours of women towards corruption, such as the level of restraint towards corrupt opportunities, their networks, as well as the sector under investigation (public or private). The questions which therefore arise are: within the context of microfinance organizations in developing countries, are women less prone to corruption? Does their engagement in such institutions as internal agents (loan officers) and external agents (loan borrowers) positively influence the financial performance of such organizations? The literature remains unclear and hence the basis for the development of Hypotheses 4 to 5, below.

The arguments used to support the notion that women are less inclined to engage in corruption than men are usually based on predisposed assumptions and stereotypes that men are more individually oriented (selfish) while women are more socially orientated (selfless) (Eckel and Grossman, 1998). In addition, it is generally reported that women exhibit ‘helping’ behaviour (Eagly and Crowley, 1986), and score higher on ‘integrity tests’ (Ones and Viswesvaran, 1998) and on moral development tests than their male counterparts (White, 1999). Beyond these, the social construction of gender offers an insightful theoretical lens to examine the relationship between gender and corruption.

The social construction of gender posits that gender roles are reflective of ‘status’ within a society (Lindsey, 2020) and that gender roles implicitly and explicitly categorize people and therefore motivate social behaviours (Gilligan and Attanucci, 1988). The theory of social construction of gender can be classed as essentialist or non-essentialist (Mikkola, 2017). While the essentialism perspective of gender dictates that identity (male or female) is defined by a set of attributes, the non-essentialist perspective of gender postulates that gender identity is not defined by specific traits. Consequently, in the social construction of gender, the perspective which assumes a clear biological division between male and female and their respective roles when considering the social creation of masculinity and femininity, is essentialist. Within this perspective, gender identity and gender role are congruous. The contrasting view (that is, non-essentialist) is that an outward expression of gender identity does not necessarily correspond with gender role (Witt, 1995). The resulting argument from a non-essentialist perspective of social construction of gender is that a male identity is not necessarily harmonious with a male role just as a female identity is not necessarily harmonious with a female role. This is in line with feminist ethics of the contemporary ethical theory school of thought (Tong, 2003).

As opposed to traditional or western modernist ethical theories, which are rooted in the ethical absolutism school of thought and so propose the view that right and wrong are objective qualities that can be rationally determined, feminist ethics is an alternative or contemporary ethical theory. Also known as the ethics of care, feminist ethics is an ethical theory that prioritizes empathy, harmonious and healthy social relationships, care for one another, above abstract principles that characterize the traditional or western modernist ethical theories (Koehn, 2012). In effect, feminist ethics has gone beyond narrow issues of gender and focuses more on the traits that underline it. Based on the feminist ethics theory, it can be argued that a person may identify as a male in terms of gender identity but demonstrates feminist ethics characteristics such as care and empathy. Accordingly, that person is less likely to engage in corrupt practices. While the role of gender identity and gender trait is worth exploring within the context of corruption and MFIs, this article assumes the position of an essentialist perspective of social construction of gender, by arguing that gender identity is what might moderate willingness to either engage or not engage in corrupt practices. Alolo (2006) reinforces this point by highlighting that for women, their gendered ethics encompasses the exhibition of personality traits that define femininity, such as emotion, compassion and care in the exercise of judgements.

In addition to the above discussion, which reviews and highlights disagreements on the nature of the relationship between gender and corruption, the literature on gender and firm performance remains unresolved. Some studies report that a greater representation of the female gender in organizations enhances firm performance (Liu et al., 2014; Lückerath-Rovers, 2013), and as such countries such as Sweden, Norway and Spain have initiated efforts to make minimum representations of gender diversity in the boardroom a legal requirement; see for instance Medland (2004) and Wang and Kelan (2013). Contrary to this stance, Adams and Ferreira (2009) reported that, on average, firms perform worse when there is greater gender diversity of the board. This supports the argument also put forward by Almazan and Suarez (2003) that too much board monitoring through gender diversity can decrease shareholder value. The varying views and disagreements on the interaction between gender and institutional factors such as the control of corruption and on firm performance form the basis of Hypotheses 4 to 5 in this study. As argued above, drawing from the essentialist perspective of the social construction of gender, it is argued in this article that gender identity is what may moderate the willingness to engage in corrupt practices or otherwise. Based on the above arguments, the following hypotheses are offered and tested within the context of MFIs:

H4a. Percentage of female borrowers has no effect on the relationship between the control of corruption and MFIs’ performance.

H4b. Percentage of female borrowers has no effect on the relationship between the rule of law and MFIs’ performance.

H4c. Percentage of female borrowers has no effect on the relationship between financial sector development and MFIs’ performance.

H5a. Percentage of female loan officers has no effect on the relationship between the control of corruption and MFIs’ performance.

H5b. Percentage of female loan borrowers has no effect on the relationship between the rule of law and MFIs’ performance.

H5c. Percentage of female loan officers has no effect on the relationship between financial sector development and MFIs’ performance.

Research methodology

Data used

The data for this article are obtained from three different sources. The Microfinance Information Exchange database MFI-specific information is obtained from MIX market, a platform containing financial and non-financial information on MFIs. The MIX market has been used extensively for MFI-related research (see Mersland et al., 2011; Tchakoute Tchuigoua, 2014, 2016) because of its extensive worldwide coverage. The country-specific information is obtained from the World Development Indicators (World Bank), The Global Economy and Hofstede and Hofstede (2001). Given that the focus of this article is mainly on Africa, we start with all MFIs operating within the African continent from 2006 to 2015 (10 years). We then exclude firms’ year observations with inconsistent financial information such as negative assets, revenue and MFIs missing substantial information. As a result of these filters, the final sample consists of 425 MFIs across 33 African countries.

Dependent variable

The main dependent variable, which measures the financial performance of MFIs, is the operating self-sufficiency ratio. The operating self-sufficiency ratio is the main measure of MFIs’ performance because it shows how an MFI is able to cover its operating expenses with available financial revenue (Cull et al., 2007; Hartarska, 2005). This measure has been used extensively in the MFI literature (see Assefa et al., 2013; Tchakoute Tchuigoua, 2014, 2016). Variable definitions are contained in Appendix A.

Main independent variables

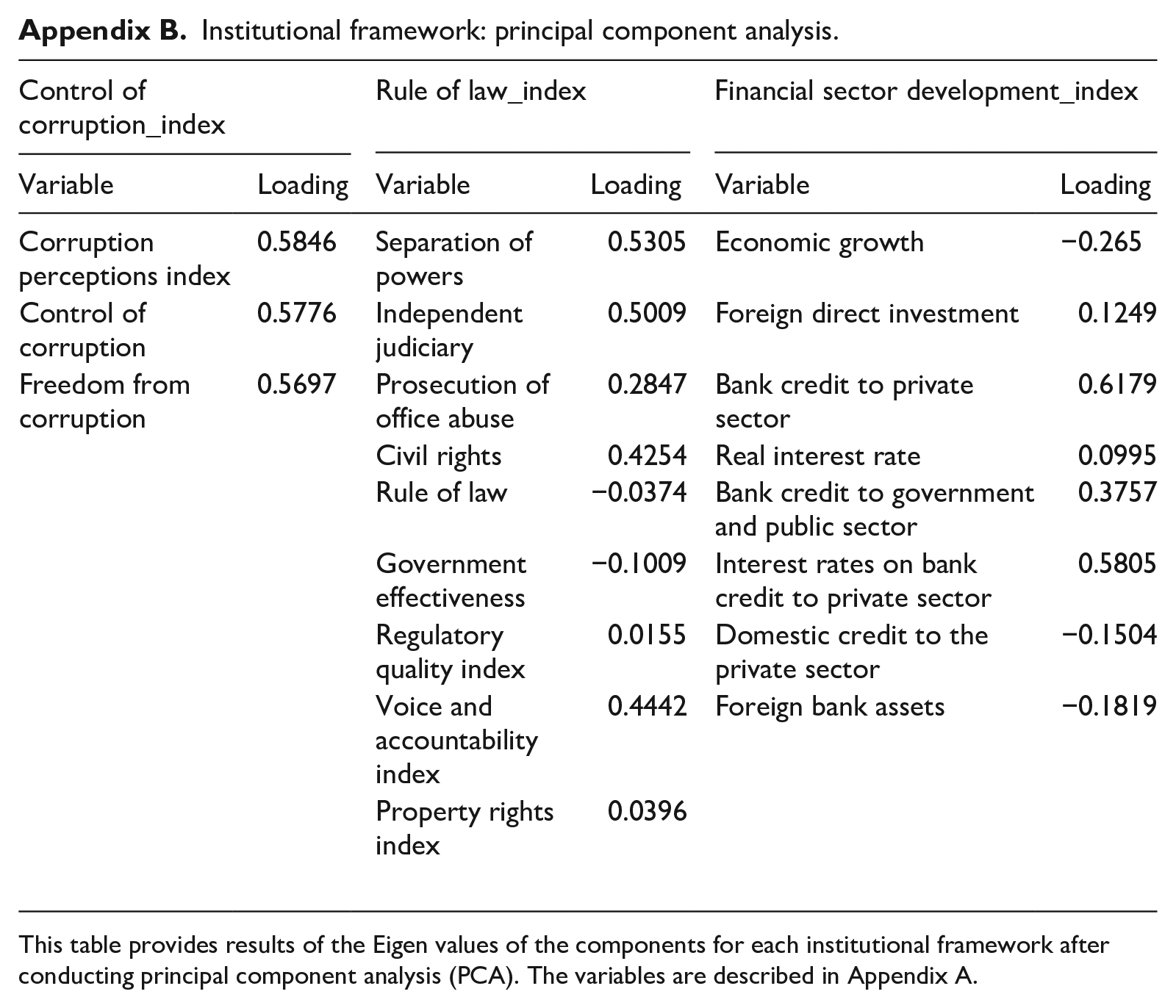

We use three main independent variables, including control of corruption, rule of law and financial sector development. These variables have been widely used in the literature to examine the effects of corruption and institutions on both financial and non-financial firms. However, there is a major problem with choosing the appropriate measure because these variables are defined in several ways, as noted, and different authors have used different definitions to measure corruption and institutions (see Ahlin et al., 2011; Chikalipah, 2017; Tchakoute Tchuigoua, 2014; Vanroose and D’Espallier, 2013). The variation of definitions presents two main concerns. First, it encourages cherry picking, where different authors choose different definitions to meet their objectives. Second, the use of a single measure only examines the effect of one dimension of corruption or institution on performance. Thus, a cluster of definitions is appropriate to examine the effect of each of the institutional variables on MFI performance.

To overcome the limitations in previous studies, we follow Jellema and Roland (2011) and Li and Sun (2017) and apply principal component analysis (PCA) to construct an index for each of the institutional variables using measures commonly found in the extant literature. The PCA identifies linear combinations that best embody the variation in measures used for each of the institutional variables (see Greene, 1990). One main advantage of building an index is that it captures the multiple dimensions of each institutional variable (Jellema and Roland, 2011). The procedure followed in constructing indexes for each of the three institutional variables is as follows. First, we identify the appropriate measures for each institutional variable from the extant literature. Second, we perform the PCA with varimax rotation for all measurements of each institutional variable. We use the first principal component after running the PCA to represent each of the institutional variables (see Li and Sun, 2017). Following previous studies, we only include factor loadings of 0.30 or above. Third, we focus on the first principal component for each institutional variable (Li and Sun, 2017).

To construct an index for the control of corruption, we use three definitions including corruption perception, control of corruption and freedom from corruption. These three measures have loadings above 0.30. For the rule of law index, we use nine measures including separation of powers, independent judiciary, prosecution of office abuse, civil rights, rule of law, government effectiveness, regulatory quality, voice of accountability and property rights. Out of these, four measures have loadings above 0.30 including separation of powers, independent judiciary, civil rights and voice of accountability. Finally, the financial sector development index is constructed with eight measures including economic growth, foreign direct investment, bank credit to private sector, real interest rate, bank credit to government and public sector, interest rates on bank credit to private sector, domestic credit to private sector and foreign bank assets. There are three measures with loadings above 0.30, including bank credit to private sector, bank credit to government and public sector and interest rates on bank credit to private sector. Appendix B contains the factor loadings from the first principal component of the PCA for all three institutional variables.

Interactive variables

Two variables including the percentage of female borrowers and female loan officers are interacted with each of the three institutional variables separately to examine whether they positively or negatively affect the relationships between the institutional variables and MFI performance. The percentage of female borrowers is defined as the total number of female borrowers to the total number of borrowers. Similarly, the percentage of female loan officers is defined as the total number of female loan officers to the total number of loan officers.

Control variables

To account for omitted variable bias and country-specific differences, we employ two different sets of control variables including MFI-specific variables and country-specific variables.

MFI-specific variables

The variables controlled for are MFI age, size of loan portfolio, MFI size and regulation. MFI age is measured as the number of years since incorporation. Gross loan portfolio is measured as the total outstanding loan portfolio to total assets. MFI size is measured as the natural logarithm of total assets. Regulation is a dummy variable equal to 1 if an MFI is subjected to prudential regulation and zero otherwise.

Country-specific variables

The country-specific variables included as control variables are inflation, legal origin and uncertainty avoidance. Inflation is deflated by GDP. Legal origin is a dummy variable which equals 1 for common-law systems and zero otherwise. Uncertainty avoidance is Hofstede’s cultural index on uncertainty avoidance, which reflects the extent to which individuals attempt to minimize uncertainty (see Hofstede, 2011).

Econometric specification

In this article, the Hausman–Taylor (1981) estimator for error-components model is used because we have three time-invariant but important variables included in all our regressions. These variables are legal origin, regulation and uncertainty avoidance, which are considered important to MFIs’ operational performance (Afrifa et al., 2019; Hartarska and Nadolnyak, 2007; Tchakoute Tchuigoua, 2016). However, the inclusion of these three variables means that the use of the fixed-effects method is precluded (Li and Sun, 2017). Two methods that could be employed are generalized method of moments (GMM) and random-effects; however, legal origin, regulation and uncertainty avoidance are highly likely to be correlated with the unobserved individual effects because they are time-invariant (Li and Sun, 2017).

The Hausman–Taylor test is used frequently in the literature to accommodate time-invariant variables (see Li and Sun, 2017; Tchakoute Tchuigoua, 2014) because it allows the time-invariant regressors to be correlated with the unobserved individual effects. It also uses both the within-variation and between-variation time-varying independent variables to serve as instruments for endogenous time-invariant variables. This method has an advantage over both the fixed- and random-effects methods because it is more efficient and generates estimated coefficients for the time-invariant variables (Greene, 2003; Li and Sun, 2017; Oh et al., 2016).

To test Hypotheses 1 to 3, we use the Hausman and Taylor model as follows:

Where:

All variables are as defined in Appendix A.

Results

Descriptive statistics and correlation matrix

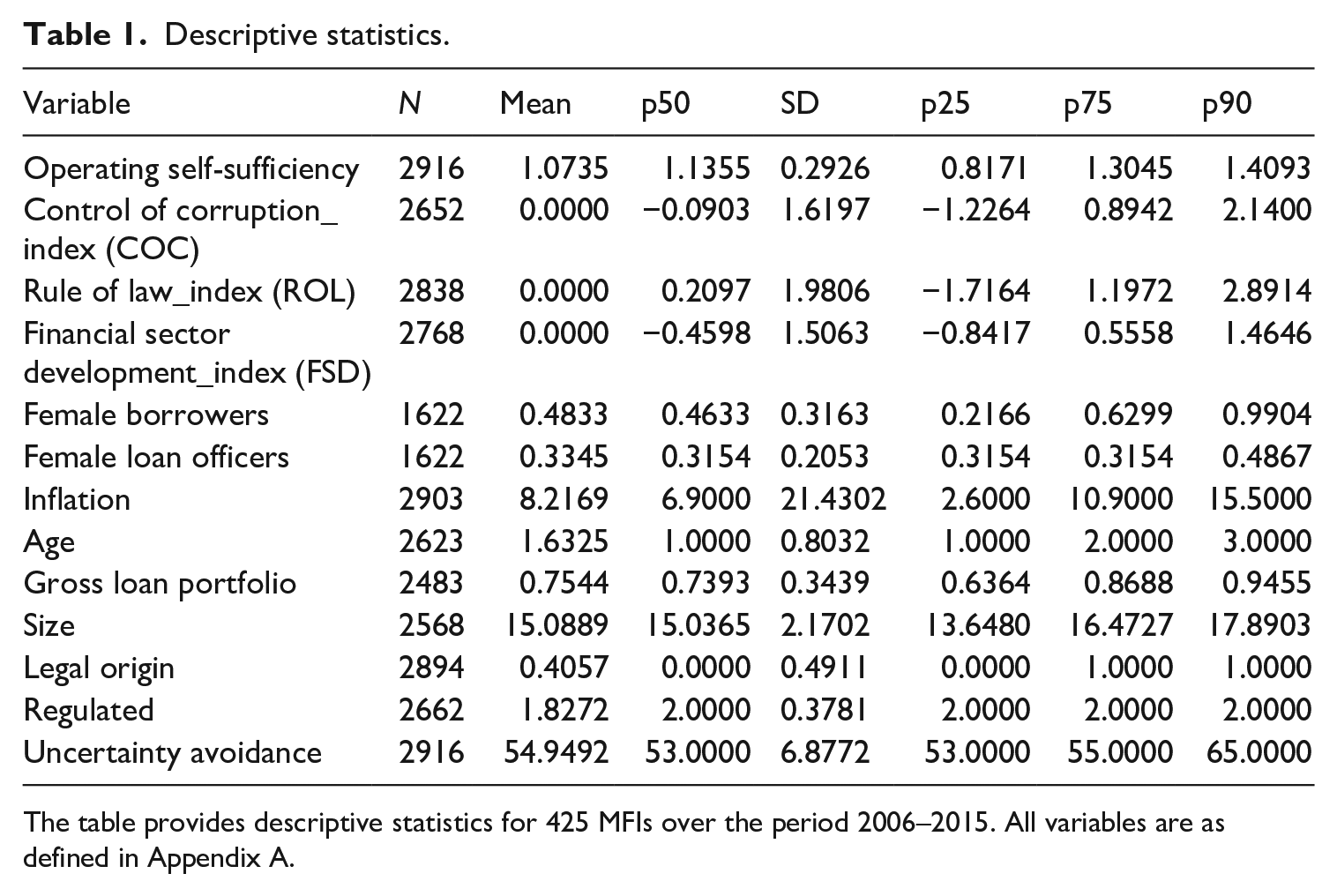

The descriptive statistics are displayed in Table 1. The operating self-sufficiency of the average firm is 1.0735, meaning MFIs in the African continent are only just able to cover their operating expenses. This figure is considered low compared with studies conducted around the world (Tchakoute Tchuigoua, 2014). The average indexes for control of corruption, rule of law and financial sector development are 0.0000, by construction (see Li and Sun, 2017). The percentage of female borrowers of the average firm is 63.33%, which is similar to the 66.55% in Abdullah and Quayes (2016). On average, the percentage of female loan officers in the sample is 33.45%. The percentage of MFIs located in common-law countries is 40.57%, compared with 59.43% in other countries. The percentage of MFIs under regulation is 82.72%, compared with the unregulated percentage of 17.28%. The average country’s uncertainty avoidance is 54.9492.

Descriptive statistics.

The table provides descriptive statistics for 425 MFIs over the period 2006–2015. All variables are as defined in Appendix A.

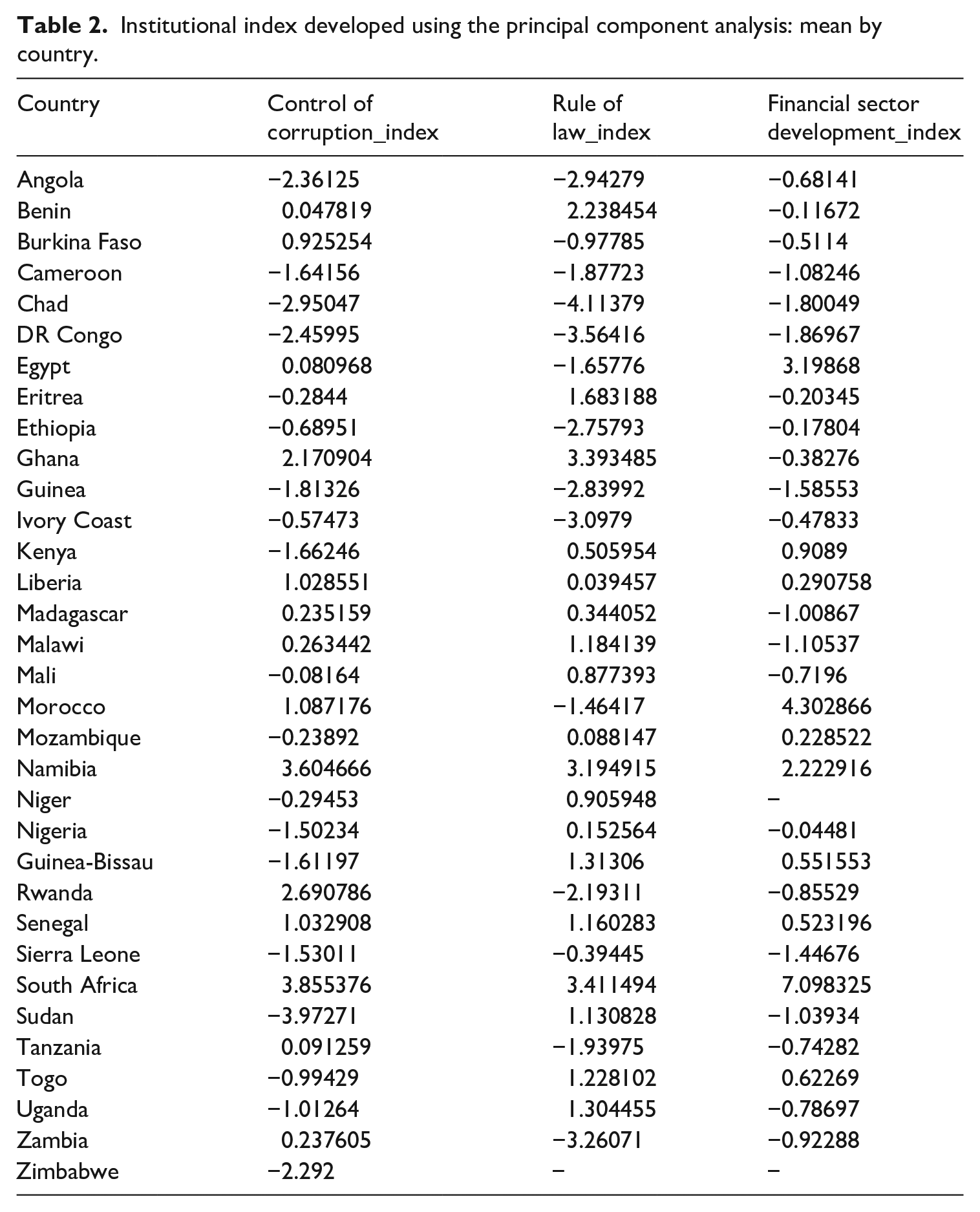

The country level indexes developed using the PCA for control of corruption, rule of law and financial sector development are contained in Table 2. In terms of control of corruption, the three countries with the highest scores are South Africa (3.8554), Namibia (3.6047) and Rwanda (2.6908). The three countries with least control of corruption are Sudan (3.9727), Chad (−2.9505) and DR Congo (−2.4600). The top three countries with better rule of law are South Africa (3.4115), Ghana (3.3935) and Namibia (3.1949); whereas Chad (−4.1138), DR Congo (−3.5642) and Zambia (−3.2607) have the lowest rule of law. South Africa (7.0983), Morocco (4.3029) and Egypt (3.1987) have the highest financial sector development; while DR Congo (−1.8697), Chad (−1.8005) and Guinea (−1.5855) recorded the lowest score in financial sector development.

Institutional index developed using the principal component analysis: mean by country.

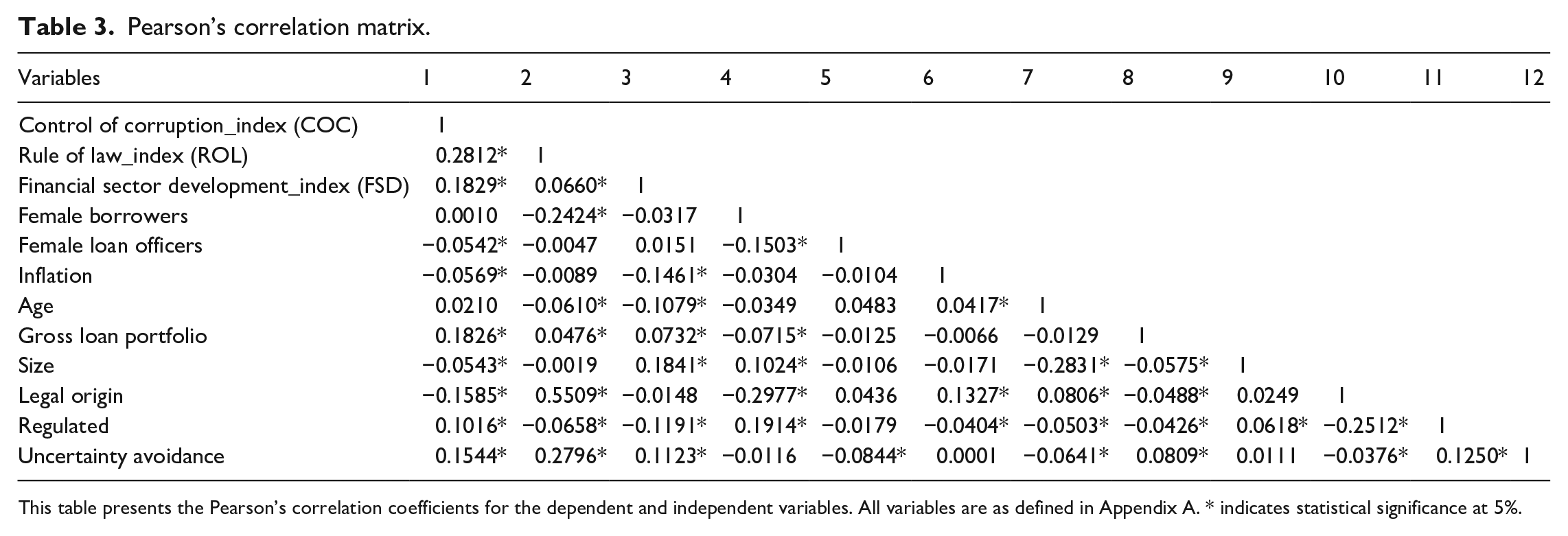

The results of the Pearson correlation matrix, which are contained in Table 3, are performed to assess the presence of multicollinearity among explanatory variables before regression estimation. According to the results, all the correlations among explanatory variables are below the 80% threshold prescribed by Field (2005). Therefore, multicollinearity is not a serious issue for the estimates.

Pearson’s correlation matrix.

This table presents the Pearson’s correlation coefficients for the dependent and independent variables. All variables are as defined in Appendix A. * indicates statistical significance at 5%.

Multivariate regression results and discussion

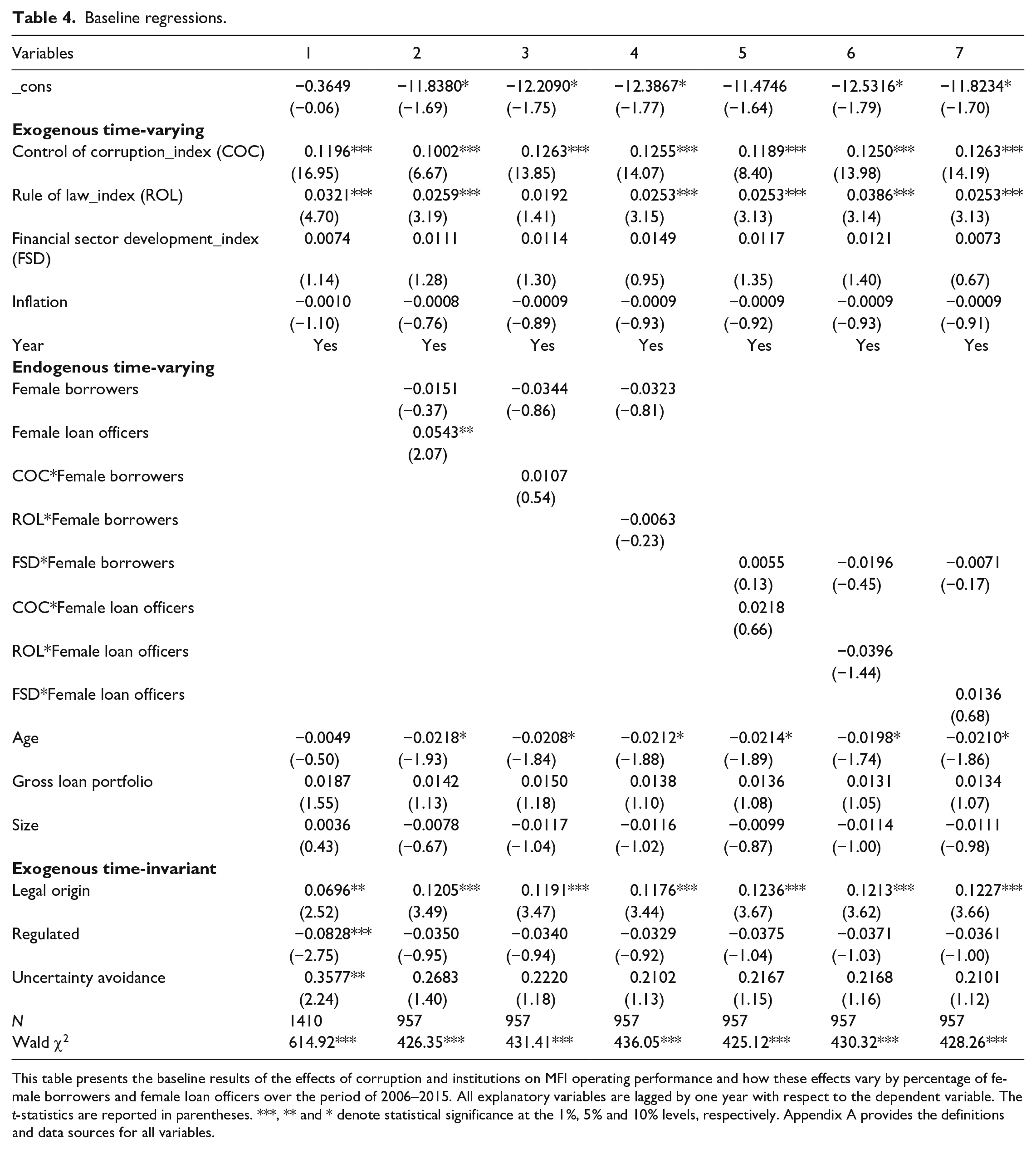

Table 4 presents the results to test Hypotheses 1 to 5. Column 1 contains all the hypothesized and control variables. Columns 2 to 4 contain the interaction of the percentage of female borrowers with control of corruption, rule of law and financial sector development, respectively. The last three columns (5 to 7) contain the interaction of the percentage of female loan officers with control of corruption, rule of law and financial sector development, respectively. The dependent variable in all the columns is the operating self-sufficiency.

Baseline regressions.

This table presents the baseline results of the effects of corruption and institutions on MFI operating performance and how these effects vary by percentage of female borrowers and female loan officers over the period of 2006–2015. All explanatory variables are lagged by one year with respect to the dependent variable. The t-statistics are reported in parentheses. ***, ** and * denote statistical significance at the 1%, 5% and 10% levels, respectively. Appendix A provides the definitions and data sources for all variables.

Control of corruption and MFIs’ performance

In column 1, the first hypothesized variable, control of corruption, has a positive and statistically significant coefficient (0.1196, t-stat = 16.95) at 1%. This is consistent with Hypothesis 1. This indicates that MFIs enjoy higher performance when measures are put in place to control corruption. Specifically, the result shows that a 10% increase in the control of corruption leads to a 1.196% increase in MFI performance.

A fundamental explanation for the positive association between control of corruption and MFIs’ performance is that, in economies where more effective measures have been put in place to combat corruption practices, there will be better performance in the rates of loan repayments. Consequently, this would impact positively on MFI performance.

Theoretically, this finding is consistent with the Institutional Theory Perspective on Corruption (Pillay, 2014). The theory holds that corruption at the organizational level is caused by lack of institutional support from the tax environment, poor comprehension of the regulations as well as execution and practices of these regulations. However, if these structures are effectively put in place through institutional logic (Misangyi et al., 2008), then they can help control corruption and consequently lead to better performance. The result is also consistent with the empirical findings. As reported by Luo (2005), through a well-developed institutional logic within organizations exhibited by cultural, structural and behavioural practices, the control of corruption can help address organizational development and performance or else may result in the following damage, namely: evolutionary hazard, strategic impediment, competitive disadvantage and organizational deficiency.

Rule of law and MFIs’ performance

The second hypothesized variable, rule of law, has a positive and statistically significant coefficient (0.0321, t-stat = 4.70), consistent with Hypothesis 2. This indicates that MFIs in environments with better rule of law experience higher performance. Specifically, a 10% increase in rule of law leads to a 0.321% increase in MFIs’ performance. A plausible explanation for this finding is that in countries where there is better and effective rule of law, MFIs’ capital levels are safeguarded through loan repayment rates (Godquin, 2004). This is because in strong legal environments, MFIs can readily seek redress from the courts to recoup amounts owed by clients. As such, it is more likely that MFIs operating in environments with stronger rule of law can be expected to enhance their performance through the enforcement of contracts. This would consequently lead to higher MFI performance. Qian and Strahan (2007) have reported on how a stronger rule of law may increase performance through easy access to external finance and the cost of borrowing.

The Economic Analysis of Law (Posner, 2014), which attempts to explain and predict the behaviour of participants in and persons regulated by the law, can be used to theoretically explain this result. In effect, the theory explains the influence of rule of law on behaviour and so expounds on how persons (or agents) consider the consequences of violation of a legal rule in choosing their actions (corruption in this instance). Empirically, this finding is in consonance with the central theme of the Heritage Foundation’s Annual Index of Economic Freedom (Miller et al., 2015), which reports with evidence from over 120 countries that economic performance and freedom depend on rule of law (which is characterized by factors such as the quality of political and legal institutions) and that erosion of the rule of law usually reflects an increased level in perceived corruption.

Financial sector development and MFIs’ performance

The third hypothesized variable to be considered is financial sector development. The coefficient is not statistically different from zero (0.0074, t-stat = 1.14), meaning that the developments in the financial sector have no effect on MFIs’ performance. Although this result is contrary to Hypothesis 3, it is not surprising, given the conflicting reasons provided in the extant literature. Proponents of a positive relationship between financial sector development and MFI performance argue that a well-developed financial sector provides a conducive environment in which MFIs are able to flourish and increase their efficiency and profitability. Developments in the financial sector that have been cited as positively impacting on MFIs and which lead to improved efficiency and performance are varied. They include factors such as spillover effects of modern banking techniques, like the use of modern technology (Aboagye and Otieku, 2010), stimulation of MFIs to reduce costs, increased efficiency, improved quality of service due to competition from commercial banks (Drake and Rhyne, 2002), increased regulation and supervision of financial institutions (Steel and Andah, 2003).

For a negative proposition, Vanroose and D’Espallier (2013) report that a major external factor or macroeconomic and institutional environmental feature that affects MFI performance is the financial sector development of the country. In the study of 1073 financial institutions from six developing regions of the world, Vanroose and D’Espallier (2013) reported a negative relation between a country’s financial sector development and MFI performance. Their study sought to argue that MFIs reach more clients and consequently are more profitable in countries where access to the traditional financial system is low. Similar studies to this negative relationship have been reported. Hermes et al. (2009) argue that the direct competition between MFI and traditional commercial banks is the underlying reason, which explains the prediction of a negative relation between MFIs and the development of the formal banking sector. This argument seeks to explain that in a very well-developed financial sector, commercial banks are able to become more efficient and benefit from economies of scale. They are also able to diversify by becoming more flexible and serving different groups of people, such as clientele and markets that otherwise would be served by MFIs in a less developed financial sector. On the flip side, the high competition forces MFIs to focus on the unbanked segment of the market (Christen et al., 2004; Vanroose and D’Espallier, 2013), which may result in higher loan default rates and consequently lower MFI performance.

Market Failure Theory has also been used as an argument to explain the negative relationship between MFI performance and financial sector development. Proponents of this argument (see for instance Khandker, 2005) argue that MFIs are substitutes for the commercial banking sector and they solve the limitations of the traditional banking sector by serving a clientele that is not served by banks. As such, in places where the traditional banking system is well established, the microfinance sector is expected to be less developed and so would yield lower performance and vice versa.

Interaction of percentage of female borrowers with control of corruption, rule of law and financial sector development effect on MFIs’ performance

The results of the interaction of control of corruption and percentage of female borrowers (COC*Female borrowers) effect on MFIs’ performance are reported in column 2. The coefficient of the interaction variable (COC*Female borrowers) (0.0543, t-stat = 2.07) is positive and statistically significant at 5%. This is consistent with Hypothesis 4a and shows that the effect of control of corruption on MFIs’ performance is higher in the presence of female borrowers. Specifically, a 10% increase in control of corruption for MFIs with no female borrowers results in a 1.002% increase in performance, but increases to 1.056 (1.002 + 0.543) for MFIs with female borrowers. This shows a higher performance of control of corruption for firms with female borrowers.

Theoretically, these findings can be explained by the essentialist perspective of the theory of social construction of gender: a perspective that dictates that identity (male or female) is defined by a set of attributes. In relation to corruption, this theory argues that women (female borrowers, in this instance) more generally exhibit a higher ‘integrity test’ score (Ones and Viswesvaran, 1998) and score higher on moral development (White, 1999). This perspective assumes, therefore, that they would be less prone to corrupt practices as opposed to men. Empirically, the findings support the view reported by Azfar and Nelson (2007), who stated that the adverse behaviour of women towards corruption may be explained by the understanding that women react more strongly to the risk of detection were they to engage in corruption, and so desist from corrupt practices.

As shown in columns 3 and 4, respectively, the interaction of the percentage of female borrowers with the other two hypothesized variables, rule of law and financial sector development, shows no statistically significant results. The coefficients are: ROL*Female borrowers (0.0107, t-stat = 0.54) and FSD*Female borrowers (−0.0063, t-stat = −0.23). These results show that the effects of rule of law and financial sector development on MFIs’ performance are not affected by the borrowing percentages between female and male. These two findings are consistent with Hypotheses 4b and 4c, respectively.

Interaction of percentage of female loan officers with control of corruption, rule of law and financial sector development effect on MFIs’ performance

The interactions of the percentage of female loan officers and the three hypothesized variables, control of corruption, rule of law and financial sector development, are contained in columns 5 to 7, respectively; however, none of the coefficients is statistically significant. The coefficients of the three interaction variables are as follows: COC*Female loan officers (0.0218, t-stat = 0.66), ROL*Female loan officers (−0.0396, t-stat = −1.44) and FSD*Female loan officers (0.0136, t-stat = 0.68). These results show that the variation of percentage of female loan officers within an MFI has no influence on the effects of control of corruption, rule of law and financial sector development on MFIs’ performance.

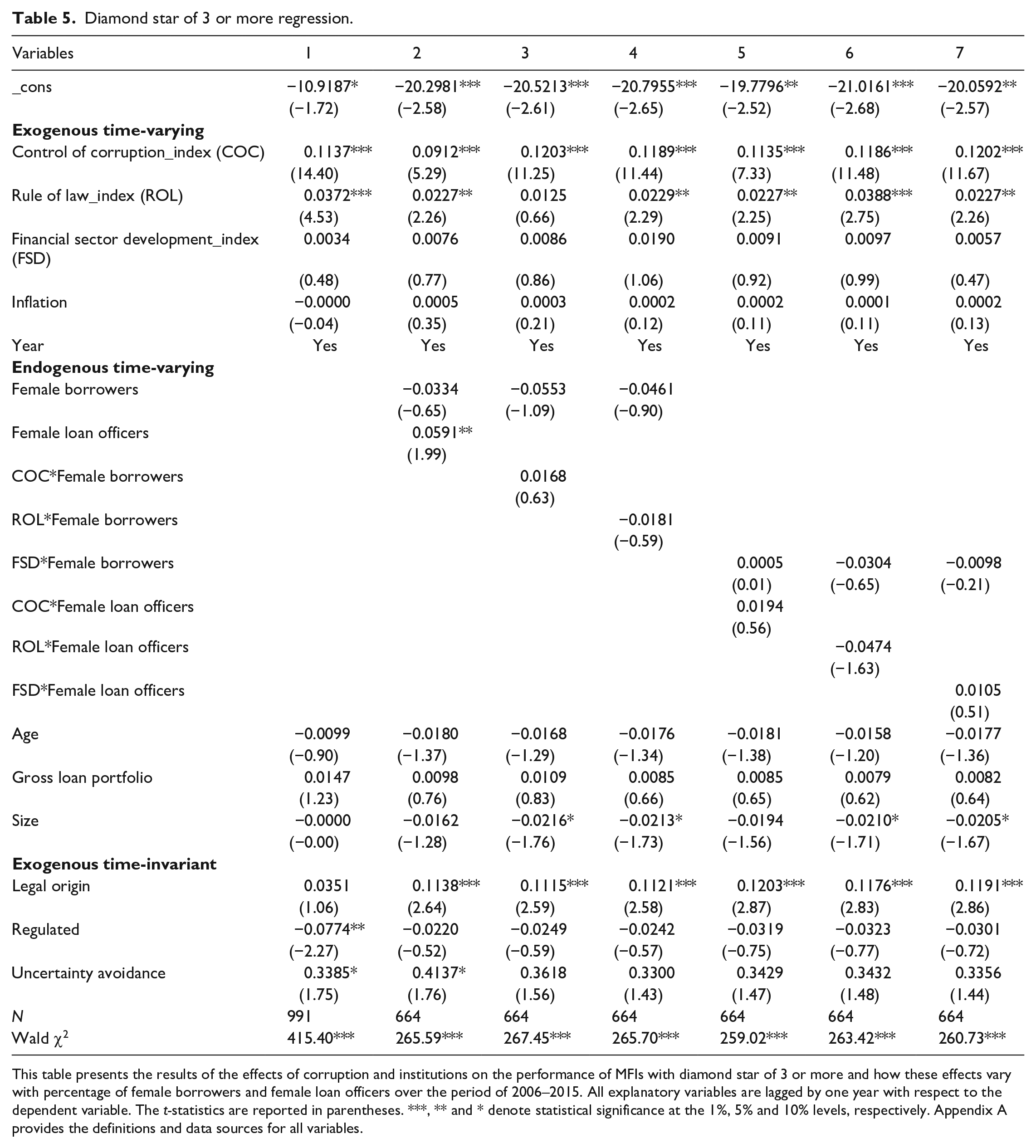

Robustness test

Diamond star greater than 3

The MFIs’ financial information contained in the MIX market database is classified into 5 diamond star categories. This is because MFIs self-report their information voluntarily, and not every MFI’s financial information is independently verified by a third party. Thus, there could be reliability issues with the information used in this article. The diamond star measures the level of reliability of an MFI’s financial information, 5 indicating highly reliable and 1 indicating unreliable financial information. A diamond star of 5 indicates that an MFI’s financial information is certified and audited or rated by a reputable rating agency (see Assefa et al., 2013; Louis and Baesens, 2013; Quayes, 2012); whereas a diamond star of 1 shows that the particular MFI’s financial information is unaudited. Because of these potential reliability issues, some previous studies have exclusively focused only on MFIs’ financial information with a 3 or more diamond star (see Assefa et al., 2013; Louis and Baesens, 2013; Quayes, 2012; Tchakoute Tchuigoua, 2016). However, focusing on only MFIs with certified and audited financial information introduces the problem of selection bias. To prevent this issue and to improve the power of the tests, we used the full dataset in estimating the baseline regression results. For comparability purposes however, we re-estimate the baseline regression results by only focusing on MFIs with diamond star 3 or above attached to their financial information.

The results, which focus on diamond star 3 or above, are presented in Table 5. The results are qualitatively consistent with the baseline regression results in Table 4. Similar to the baseline regression results, the results in column 1 of Table 5 show that the operating self-sufficiency of MFIs with diamond star 3 or above increases with control of corruption (0.1137, t-stat = 14.40) and better rule of law (0.0372, t-stat = 4.53). In terms of the interaction effect of the percentage of female borrowers, the results in column 2 of Table 5 once again show that the effect of control of corruption on MFIs’ performance is higher with an increase of female borrowers (0.0591, t-stat = 1.99). The comparability of the baseline results and the diamond star 3 or above results rules out the possibility of unreliable data driving the baseline results because of the self-reporting nature of the MIX database.

Diamond star of 3 or more regression.

This table presents the results of the effects of corruption and institutions on the performance of MFIs with diamond star of 3 or more and how these effects vary with percentage of female borrowers and female loan officers over the period of 2006–2015. All explanatory variables are lagged by one year with respect to the dependent variable. The t-statistics are reported in parentheses. ***, ** and * denote statistical significance at the 1%, 5% and 10% levels, respectively. Appendix A provides the definitions and data sources for all variables.

Conclusions

The article sets out to advance our understanding of research on MFIs by examining how the control of corruption affects MFIs in terms of input (expenses) and output (income) in Africa, and how gender acts as a mediating factor. Using analyses of MFIs operating in 33 African countries, we found that control of corruption forces MFIs to conserve operating income and expenditure. The present findings suggest that the control of corruption increases MFIs’ performance. Thus, the findings support the theoretical contention that control of corruption can exert positive effects on organizational performance.

From a theoretical standpoint, we draw on and extend multiple streams of research. First, we extend the traditional application of the institution-based view (Peng, 2017; Peng et al., 2008) beyond firms to incorporate not-for-profit organizations such as MFIs. In addition, we shed light on gender research and microfinance organizations (Boehe and Cruz, 2013) by exploring the effects of gender in mediating the relationship between the control of corruption and MFIs’ performance. Furthermore, our study advances the understanding of the challenges of doing business in the emerging market context (Boso et al., 2018; Khanna et al., 2005) by examining the mechanisms through which systemic or perceived corruption shapes the activities of MFIs. Thus, we shed light on how corruption can hinder or facilitate the functioning of MFIs. In addition, our study contributes to research on MFIs (Ledgerwood and White, 2006) and corruption (Brouthers et al., 2008; Rose-Ackerman, 2016) by deepening our understanding of the moderating influences of the links between control of corruption and MFIs’ performance, through exploring the effects of gender of loan officers and borrowers. In addition, we contribute to the new research on African management (Amankwah-Amoah, 2016; Zoogah et al., 2015) by emphasizing the importance of corruption and its effects on MFIs in this discourse.

The results provide evidence suggesting some managerial and public policy implications. First, they clearly point towards the importance of gender in moderating the relationship between control of corruption and MFIs’ performance. Given that MFI actors demonstrating male identities are deemed more aggressive risk-takers (Boehe and Cruz, 2013: 133), mainly due to certain conditions that favour this, it might be worthwhile to consider positive interventions that encourage female actors in MFIs as an effective means of improving their financial welfare.

Limitations and directions for future research

Notwithstanding the theoretical and practical contributions, caution should be exercised in interpreting the results. First, we limited our analysis to a small sample of 33 African countries. Given that there are 54 nations in Africa, our analysis cannot be generalized to other emerging or developing countries’ settings. To address this limitation, future studies could target a much larger sample of developing nations not only in the Global South, but also across the world. Second, although we moderated for the percentage of female borrowers and loan officers, this is far from complete in developing our understanding of the moderating factors at play. It might be useful for future studies to account for factors such as age of the borrowers and loan officers, as well as their levels of education and industry expertise. Further to this, since this article assumed the essentialist perspective of the social construction of gender, future research could focus on the non-essentialist perspective and investigate whether gendered traits, and not gender identity as investigated in this article, are what may moderate willingness to engage in corrupt practices within MFIs.

It is also important for future research to consider the impacts of lax control of corruption on the long-term survival chances of MFIs and other organizations. Such analysis could shed additional light on the wider impacts of corruption within countries and their economic activities. Accordingly, additional research is necessary to elevate these important issues and advance new discourse on African management.

Footnotes

Appendices

Institutional framework: principal component analysis.

| Control of corruption_index | Rule of law_index | Financial sector development_index | |||

|---|---|---|---|---|---|

| Variable | Loading | Variable | Loading | Variable | Loading |

| Corruption perceptions index | 0.5846 | Separation of powers | 0.5305 | Economic growth | −0.265 |

| Control of corruption | 0.5776 | Independent judiciary | 0.5009 | Foreign direct investment | 0.1249 |

| Freedom from corruption | 0.5697 | Prosecution of office abuse | 0.2847 | Bank credit to private sector | 0.6179 |

| Civil rights | 0.4254 | Real interest rate | 0.0995 | ||

| Rule of law | −0.0374 | Bank credit to government and public sector | 0.3757 | ||

| Government effectiveness | −0.1009 | Interest rates on bank credit to private sector | 0.5805 | ||

| Regulatory quality index | 0.0155 | Domestic credit to the private sector | −0.1504 | ||

| Voice and accountability index | 0.4442 | Foreign bank assets | −0.1819 | ||

| Property rights index | 0.0396 | ||||

This table provides results of the Eigen values of the components for each institutional framework after conducting principal component analysis (PCA). The variables are described in Appendix A.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.