Abstract

China will triple the number of nuclear power plants it has in operation by 2020 according to official plans, and the country’s nuclear fleet will increase 20-fold by 2050 under some not-yet-approved proposals. But how and where will China get the uranium to fuel them all? Will China need to resort to breeder reactors and reprocessing, with all the proliferation problems they incur? Or is there another way? The author suggests that between China’s domestic uranium mining, uranium purchased on the international market, and uranium mined by Chinese-owned companies overseas, China could meet even the most ambitious target, thus avoiding the troublesome and dangerous path of reprocessing.

Keywords

China leads the world in new reactor construction, with 26 new nuclear power reactors under way that are slated to produce a combined total of 27 gigawatts of electrical energy, or GWe (IAEA, 2014a). This is in addition to the 22 reactors the country already has, which currently produce a total of 20 GWe. (To give a sense of scale, Colorado’s Hoover Dam produces 2 gigawatts. Or, for another comparison, Georgia’s Plant Bowen, the largest coal-fired power plant in the United States, generates 3.5 gigawatts—enough electricity for about 1.9 million homes (Kenward, 2011)).

And even this will not be enough—at least according to China’s governing body in this field, known as the State Council. Consequently, since 2004 China’s official policy regarding the use of nuclear energy has changed from “moderate development” to “active development.” In 2012, the council’s “Medium- and Long-Term Nuclear Power Development Plan, 2011–2020” called for at least another 11 GWe by 2020, with more plants to come online in the coming decades (Zhang and Zhao, 2013). All told, that makes for a remarkable total of 58 GWe by 2020.

And some Chinese energy experts are even more bullish on the future, saying that China’s nuclear power industry could install as much as 400 GWe by 2050, or a 20-fold increase, making up about 15 percent of all of China’s electricity generation. A figure this large means that China would need a cumulative total of about a million metric tons of uranium between now and the year 2050, much more than its entire current reserves of uranium.

But where will all the uranium come from to feed the enormous appetite of these reactors? Some Chinese nuclear experts advocate that China pursue plutonium reprocessing and recycling, thereby “saving” uranium. Given the concerns about the relationship between reprocessing, unaccounted-for stocks of plutonium (Podvig, 2014), and nuclear weapons proliferation, the problem of supplying China’s reactors with enough fuel for civilian use may hold worldwide repercussions in the near future (Fissile Materials Working Group, 2013).

To meet its increasing demand for uranium to fuel its new nuclear power reactors, for the past 10 years the central government has adopted a strategy that combines domestic production, overseas exploitation, and purchases on the world marketplace in uranium. Known as the “Three One-Third” rule, one-third of its uranium comes from domestic supply, one-third from direct international trade, and another third from overseas mining by Chinese firms.

This outlook is promising for ensuring a long-term, stable supply and could avoid a situation in which China would have to stray into the dangerous waters of reprocessing, breeder reactors, and associated weapons-proliferation problems.

Domestic supply

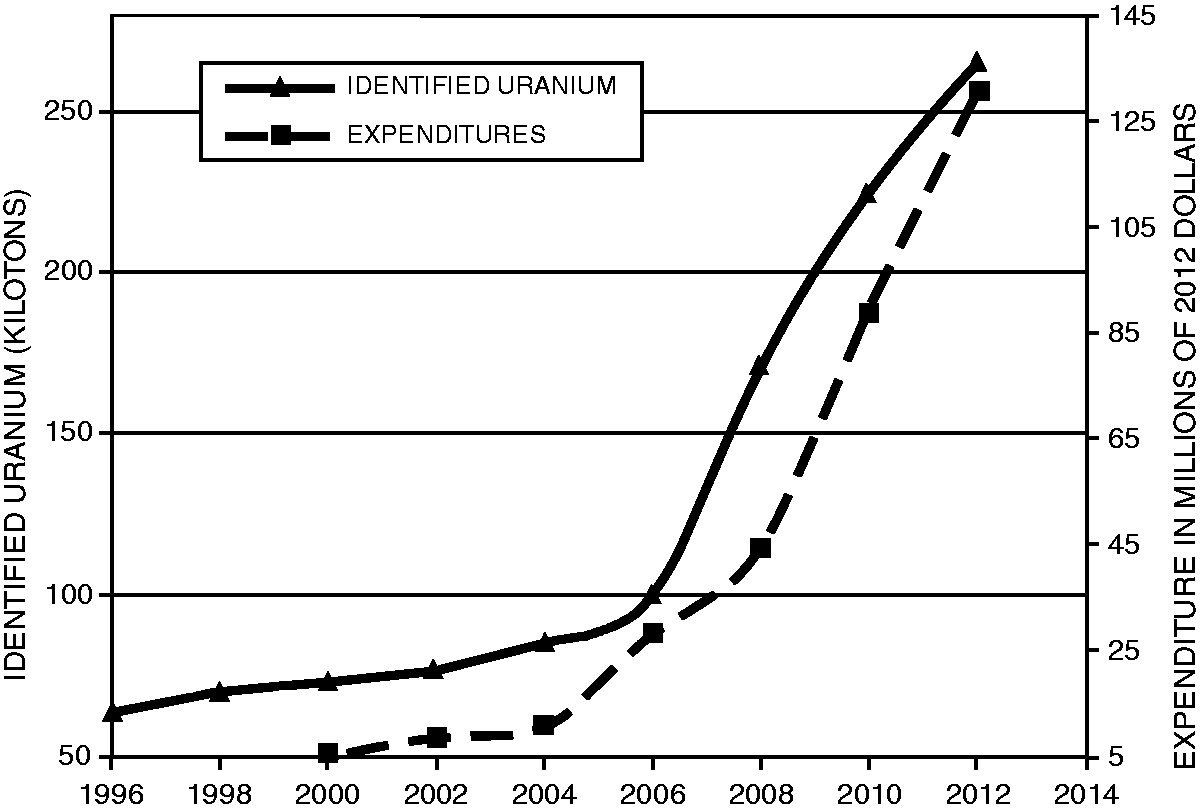

Since 2004, China has greatly accelerated the pace of its uranium exploration. A few brief statistics serve to illustrate this: In 2003, China spent about $9 million (in 2012 dollars) on searching for uranium and conducted exploratory drilling that totaled about 130 kilometers in the process. In contrast, in 2012 China spent $131 million and drilled 922.6 kilometers according to the International Atomic Energy Agency’s Uranium 2014: Resources, Production and Demand, commonly known as the Red Book (IAEA, 2014b). This tremendous effort paid off, and China’s identified reserves of uranium increased more than three-fold, from 77,000 metric tons of uranium in 2003 to 265,500 metric tons in 2012 (see Figure 1).

1

Since 2004, China’s identified uranium reserves have increased rapidly, paralleling its rising spending on exploration

In addition, Chinese authorities came up with new ways of predicting total uranium reserves in 2010, taking into account previously overlooked regions that have a different underlying geology, such as the belts of sandstone deposits in North China—which turn out to have a huge uranium potential. They also looked at the uranium potential of some formerly untouched areas such as Qinghai and Tibet and examined the potential for uranium to exist at greater depths—down to as deep as 1,000 meters below the Earth’s surface, instead of the usual focus on areas that are less than 500 meters deep. By looking in these new regions, using new models, and applying a greater understanding of the regional distribution of uranium, they were able to take a fresh look at existing exploration data from the past several decades. Their conclusion: China has more than 2 million tons of potential uranium reserves (Li, 2014).

The word “potential” is key, however. In geologists’ parlance, a uranium reserve that is “identified” or “proven” or “known” (the words are synonyms) means one in which its grades and tonnages have been determined fairly accurately. In contrast, uranium “potential” is a looser term based on what is roughly expected to occur from knowledge of previously discovered deposits and regionwide geological mapping. To cross the line from potential to proven uranium reserves requires significant amounts of exploration work.

Nevertheless, because of these technical advances China can expect to increase the volume of its estimated uranium reserves in the future. Much like calculating the amount of oil in the ground, uranium resources are a combination of economics (how much does a barrel of oil need to cost before fracking makes financial sense?), technology (how do we actually fracture shale to extract oil?), and policy (do we really want to allow fracking, given its costs to the environment and the drinking water supply?). Calculating how much uranium is realistically available to be mined is a dynamic process that depends on many factors, including engineering feasibility, exploration costs, uranium prices, and advances in technology. Inevitably, as the amount of money spent on uranium exploration increases, more uranium deposits will be discovered. And as the technology of exploration and mining improves, more of the previously nonfeasible, lower-grade ores will become usable, thus making the number of so-called “proven” reserves of uranium increase significantly.

All of which raises a question: As China continues its exploration efforts, how many more tons of proven reserves of uranium could be discovered? To answer this, I made a simple projection, assuming an average growth rate of 22,600 metric tons of uranium per year for the period between 2013 and 2050, based on the past rate of increase from 2004 (85,000 metric tons) to 2012 (265,500 metric tons). Based on this assumption, China could identify a total of proven uranium reserves of about 1.1 million metric tons by 2050—in other words, about half of its predicted uranium potential of 2 million tons. Hence, if China keeps finding uranium at the same annual rate that it did from 2004 to 2012, it would logically find enough uranium to meet all of its needs from domestic resources alone, even under the highest-growth scenario—which calls for the consumption of a cumulative total of 1 million tons of uranium from now through 2050.

Why use your own when you can buy someone else’s?

Given these statistics, an outside observer would be puzzled as to why China’s current uranium production is so much lower than its uranium demand. Yearly statistics routinely show that since 2004 China’s domestic production of uranium has lagged increasingly farther behind its annual uranium needs. For example, China upped its annual domestic uranium production from 840 metric tons of uranium in 2004 to 1,500 metric tons in 2014; however, during that same time period its annual need for uranium increased from 1,260 metric tons to 4,800 metric tons. These figures mean that in 10 years China was not able to even double its domestic production of uranium, while its demand more than tripled.

If anything, the trend has become more extreme; in recent years, China’s domestic uranium production only met about one-third of the country’s annual uranium requirements. Given the big gap between China’s domestic supply and demand, some Chinese experts have argued that the shortage in China’s uranium resources will crimp its development of nuclear power.

But they are missing a vital point: How much uranium you decide to go ahead and extract every year is not the same as how much your reserves have the capacity to supply. In a nutshell, China prefers to save its own proven domestic uranium reserves for a rainy day and instead buy what it needs for now on the worldwide open market for uranium. At a time when international uranium prices are historically low, it makes sense to make the most of the situation—especially when the majority of uranium ores discovered in China are of poorer quality, making them more costly to mine. Plus, China can always ramp up its mining and increase its domestic production of uranium, should it ever really need to do so in an emergency.

Hence, there are compelling reasons for China to want to get most (nearly two-thirds) of its uranium ore from overseas, either in the form of international trade or by having Chinese companies mine the ore themselves in countries overseas.

Direct international trade

China has recently secured a huge amount of overseas uranium resources—about three times the size of its own uranium reserves. And more could easily be added, which would make for more than enough to meet its most ambitious nuclear energy plan by 2050.

Since 2006, both the China National Nuclear Corporation, or CNNC (Zhang, 2012), and the China General Nuclear Power Corporation, or CGNPC (Wei, 2012), have been aggressively pursuing overseas uranium supplies. Based on available information, CNNC should have a total of approximately 60,000 metric tons of uranium available from international trading deals for the period between 2014 and 2050, coming from long-term supply contracts with companies such as Canada’s Cameco (10,000 metric tons of uranium over a 10-year period) and Kazakhstan’s Kazatomprom (30,000 tons from 2011 to 2020), among other contracts (Zhang and Bai, forthcoming).

Meanwhile, its rival, CGNPC, stated in 2014 that it secured an overseas uranium supply of 79,000 metric tons of uranium with the aid of international trading. But CGNPC did not give details, and part of that supply could have been consumed earlier. Therefore, based upon available information, I estimate that it should have a total of about 70,000 metric tons of uranium available for the period between 2014 and 2050 (Zhang and Bai, forthcoming). This uranium would come from a variety of sources, including a $3.5 billion, 10-year contract with Areva to supply about 20,000 tons of uranium by 2020; a contract with Canadian Cameco for 11,200 tons of uranium by 2025; a long-term contract with Kazatomprom for 24,200 tons of uranium by 2020; and a contract with Uzbekistan’s Navoi Mining & Metallurgy for about 12,000 tons by 2021. The remainder would come from a variety of sources, giving CGNPC a total of about 70,000 metric tons of uranium under contract to be imported to China.

Moreover, China has surplus uranium available from past imports, such as the 73,000 metric tons of uranium it imported from 2006 to 2013 (World Nuclear Association, 2015), a figure which is about three times more uranium than needed for its domestic energy use. When we include the uranium that came from Chinese mines during that same time period, we end up with a total surplus from imports of about 60,000 metric tons of uranium—which would be enough to supply the entire 2014 fleet of Chinese nuclear reactors for about 17 years.

Furthermore, when China purchases foreign reactors it often requires the foreign vendors to supply the first few loads of low-enriched uranium fuel, which ultimately means that China has to acquire much less uranium on its own. Eventually, the total saved uranium for China through these low-enriched uranium product deals would be worth about 40,000 metric tons of uranium.

Taken altogether, China would have a cumulative total of 230,000 metric tons of uranium acquired overseas by trading and deals in enriched uranium products.

Overseas mining by Chinese firms

Chinese nuclear corporations have also been actively developing their interests in direct uranium exploration and mining overseas. In 2006, CNNC established a wholly owned subsidiary, China Nuclear International Uranium Corporation (referred to as SinoU), responsible for the company’s overseas efforts in uranium exploration, evaluation, construction, mining, milling, production, and management in several countries, including Niger, Namibia, Zimbabwe, Mongolia, and Kazakhstan. By the end of 2009, SinoU announced that it had already secured more than 200,000 metric tons of uranium in overseas reserves and secured the import of about 6,000 to 8,000 metric tons of uranium each year through international trade. While SinoU’s leader did not disclose details about the size of the secured overseas reserves, estimates based on available information show that they contain about 198,000 metric tons (Zhang and Bai, forthcoming).

These efforts include the Azelik/Niger mine, whose uranium reserves total about 15,900 metric tons and which has an expected uranium production capacity of 700 metric tons of uranium annually for 20 years; the Imouraren/Niger mine, with a total uranium reserve of 83,870 metric tons, expected to produce 500 metric tons of uranium annually for 35 years; and the Langer Heinrich/Namibia mine, with an estimated 66,131 metric tons of uranium reserves and a production capacity of 2,030 tons annually in 2012.

Meanwhile, in 2006 a CGNPC subsidiary known as CGN Uranium Resources was established; it has been conducting uranium exploration and mining in Kazakhstan, Namibia, Australia, and Uzbekistan. In 2013, CGN Uranium Resources stated that it had secured approximately 308,000 tons of overseas natural uranium resources and that more would be acquired. Those mining projects include the Irkol and Semizbai/Kazakhstan mine, with a combined production capacity of 1,200 metric tons annually, and the Husab/Namibia mine, with 196,490 metric tons. (Recently the latter reported discoveries of more uranium deposits, increasing its estimated reserves to 248,000 metric tons.)

All told, eventually China would have access to about 500,000 metric tons of minable uranium lying in the ground. Assuming that it meets a rough industry average in which about 80 percent of raw ore is recoverable (i.e., not lost to mining and milling processes), that figure would mean that China has about 400,000 metric tons of uranium available from overseas exploration and mining. Combined with its domestic known recoverable uranium resources of 200,000 metric tons and the 230,000 metric tons of uranium available from trading on the international market and from low-enriched uranium fuel deals, that means that a cumulative total of 830,000 metric tons of uranium would be available for China’s nuclear power development from 2014 to 2050. That should be enough to feed the maw of China’s nuclear energy industry. Or will it?

Feeding China’s ambitious nuclear power development

Any estimate of China’s future uranium demand depends upon accurate projections of the number, size, and type of China’s nuclear power facilities in the future. Those figures in turn depend on whether China’s leaders decide to aim for a “high-growth” plan with many new reactors generating a lot of energy or for something more moderate.

Under a high-growth scenario, China’s nuclear-generating capacity would go from 20 GWe in 2014 to 58 GWe by 2020 and 400 GWe by 2050—or about 15 percent of all of China’s electrical generation. (For comparison’s sake, the generation of electricity by nuclear power only accounts for about 2 percent of China’s electricity at the moment; about 75 percent of the country’s electricity comes from the burning of coal.) The 400 GWe figure is a most optimistic projection, as it is about 20 times that of China’s capacity in the year 2014—four times that of current US capacity—and nearly the same as the output of all the world’s operational reactors combined. 2 If pressurized water reactors are used in the new nuclear power plants being built, refueling their reactors with low-enriched uranium fuel requires about 173 tons of natural uranium annually per GWe and about 150 tons per reactor for any new reactors built after 2020, due to a combination of technological advances and newer, more efficient designs. If that figure is added to the volume of fuel needed to fill the new reactors’ initial cores, then China’s will need a cumulative total of approximately 1 million metric tons of uranium by 2050.

Under a low-growth scenario, China’s nuclear fleet would go from a total installed capacity of 20 GWe in 2014 to 58 GWe by 2020; and 130 GWe by 2050 (about 5 percent of its total electricity generation). Then, China’s cumulative requirements for uranium will be approximately 500,000 metric tons through 2050.

Hence, the total supply of 830,000 metric tons of uranium that China has secured so far would easily meet the low-growth scenario; and it could even meet the high-growth scenario up until about 2045. While it would be insufficient to meet the needs of a projected 400 GWe of capacity by 2050 under high growth, this gap could easily be filled by China’s continual exploration of its known reserves and by continuing to pursue its overseas mining and trading operations. Hence, if China keeps to its current strategy the security of its uranium supply would not pose any serious challenges to China’s nuclear power development, even under the most ambitious scenarios, up to at least the middle of the 21st century.

At the same time, the most ambitious plans are becoming increasingly unlikely. As a matter of fact, there has been less momentum for developing China’s nuclear power ever since the Fukushima accident. While the country has resumed building on a few previously approved reactor projects, only one new reactor project has been approved at the time of writing. Many nuclear experts believe that it would be very difficult to achieve the target of 58 GWe by 2020, and some Chinese officials and nuclear experts now use the word “moderate” to describe the ideal pace of China’s nuclear power development. As a result, practical nuclear power deployment could be much smaller than under the projected high-growth scenario.

What the future holds

With all these considerations in mind, the supply of uranium should not constrain China’s development of nuclear energy for several decades. The latest issue of the Red Book estimates that the total identified global uranium reserve amounts to 7,635,200 metric tons of uranium, an increase of 7.6 percent compared with the total reported in 2011. Such an increase can add almost 10 years to the existing resource base. Based on the world’s uranium requirements in 2012 (about 61,600 metric tons of uranium per year), if there was no growth in nuclear power the total identified resources would be sufficient for about 124 years of supply to the global nuclear power fleet.

And it should be noted that the global identified uranium resources have more than doubled since 1975, in line with expenditures on uranium exploration, even while more than 2 million metric tons of uranium have been used from that date to today (World Nuclear Association, 2014).

Advocates of breeder reactors in China argue that China should not rely heavily on foreign uranium because the supply could be disrupted by political or economic change. But given that the uranium market is naturally an open and competitive one and that uranium suppliers in the international market are geographically and politically diverse, they are unlikely to collude to raise prices or limit supplies.

What’s more, history shows that past predictions of a steady rise in the price of uranium have been proved wrong. The 2011 MIT study “The Future of the Nuclear Fuel Cycle” emphasizes that “there are good reasons to believe that even as demand increases, the price of uranium will remain relatively low” (MIT, 2011). This is in line with other studies showing that the prices of most minerals have actually decreased in constant dollars over the past century, even while extraction has increased.

And even if uranium prices increased, the cost of uranium accounts for only a small fraction—about 2 to 4 percent—of the total production costs of nuclear-generated electricity.

What’s more, if China became seriously concerned about any potential disruptions of its uranium supply it could easily and inexpensively establish a strategic uranium stockpile, much like its strategic oil reserve. Such a uranium reserve is in fact under consideration as a national energy project in China’s 12th five-year energy plan (China National Energy Administration, 2011). This would be a much less expensive approach than a reprocessing and breeder reactor strategy, and from the point of view of nuclear weapons proliferation a much safer one.

The central government should have a long-term and comprehensive national nuclear energy development plan and a long-term uranium acquisition plan to go with it. China’s central government should intensify its uranium exploration and mining, both domestically and overseas, and continue to participate in the international trading of uranium.

Footnotes

Funding

This research was supported by a grant from the Carnegie Corporation of New York.