Abstract

The growth of the solar energy industry depends on a strong relationship between science and engineering innovations, a vibrant financing and manufacturing sector, and cycles of policy design and advancement. The mixing pot of academic research and industrial entrepreneurship that is Silicon Valley, along with the strong overarching suite of environmental policies in place in California, work together to drive the solar energy industry. Together, they will keep the region a leader in a fast-changing industry as China, Europe, and other areas build their clean energy sectors. The globalized nature of solar energy is essential to building the energy sector needed as one vital element of a sustainable society.

Tesla founder and wide-ranging entrepreneur Elon Musk once described the sun as “that highly convenient and free fusion reactor in the sky, [that] radiates more energy to the Earth in a few hours than the entire human population consumes from all sources in a year” (Musk et al., 2014).

But plugging in to that free fusion reactor has been tricky. To be sure, great strides have been made in the basic physics and materials science of solar cells. In terms of pure technology, the direct conversion of photons from the sun into electrons for generating electricity—a process known as photovoltaics (PV)—has come a long way since the first panels of PV cells were used to power NASA satellites orbiting the Earth.

The economics of the technology have come a long way as well: The price of an individual solar PV panel has dropped 75 percent since 2008, while the power output per panel has gone up. Put another way, rooftop solar panels in 2012 cost about 1 percent of what they did in 1979 (Energy Department, 2013).

But turning the solar energy industry from a niche market into a major part of the global energy mix—essential for addressing climate change—is still a hurdle. Technological, financial, and business challenges must be overcome if it is to become truly widespread. Still, the potential of PV is enormous (Duke and Kammen, 1999); it could produce tens of times more electricity than is consumed by the entirety of human civilization.

A quick explanation of terms: The smallest unit of a photovoltaic system is the silicon wafer chip known as the “cell,” which directly converts incoming photons of light into electrons. When a group of cells are connected in series or in parallel and encapsulated in a clear protective laminate, they form a single “module”—the smallest unit producing useful power. A group of modules is usually packaged and pre-wired into a single “panel” at the factory; each panel is usually smaller than a single sheet of plywood and roughly the maximum size and weight that two workers can conveniently carry and lift onto a roof. A typical single-family home needs on its roof a minimum of four to six panels, called an “array,” to meet all its energy needs—maybe more if it is a large home, or if the system is meant to handle electricity-hungry items like plug-in electric vehicles. 1 In addition, the entire array system needs a power inverter, wiring, mounting, and an electric meter that can run backward—indicating when the system is producing more electricity than it is consuming from the local electric company.

Solar panels were originally most often paired with batteries to enable power when there’s no sunlight, and that arrangement is still used to provide power in remote areas or in specialty applications, such as lighting temporary highway construction signs. But increasingly, the panels are being put on a homeowner’s roof and hooked up directly to the local electrical utility’s existing power grid, with any excess that is generated sent to the grid. Anytime that the homeowner’s demand exceeds the capacity of the panels, the household simply draws upon the grid. In effect, the electrical grid acts as a giant battery.

Many innovative approaches have been introduced lately, in some cases drawing upon the experiences of Silicon Valley when it comes to start-ups, financing, and introducing new technologies. What is taking place in Silicon Valley and beyond to make this vision possible? What role can this community play in advancing laboratory research, government policy, and market innovation?

One example lies in the Mountain View, California-based firm Solar City. The firm’s business model is quintessentially Silicon Valley in nature: Rather than simply forecasting when solar energy will be “grid competitive” (estimated to be between now and 2020 across virtually all of the United States), Solar City is one of a handful of companies that have bypassed the simple sales-only model. Instead, Solar City will place panels it owns on your roof, so that you merely lease space to the company, and in return pay for the power it produces every month at a government-subsidized, locked-in, deeply discounted rate that is much less than the market rate for electricity from the local utility. 2 Sunrun (www.sunrun.com) and Sungevity (www.sungevity.com) are two other California-headquartered, aggressive, and innovative competitors in this arena, which promises to lower the homeowner’s residential utility bill the first month a solar system is in operation.

Such innovative thinking comes just in time for a promising technology. In fact, in a recent regional assessment of the potential of solar energy, my colleagues and I found that with a realistic model of the utility grid and conservative expectations for technological advances, photovoltaics alone could provide over one-third of the total energy needs across western North America (Mileva et al., 2013). This result, based upon data generated by the SWITCH open-access energy system analysis software developed by a member of our Renewable and Appropriate Energy Laboratory (http://rael.berkeley.edu/switch), highlights the potential of solar energy at a time when there is a dramatic need for a move to an entirely clean energy economy by mid-century (Kammen, 2006; Nelson et al., 2012; Wei et al., 2013).

To meet the long-term greenhouse gas mitigation target of an 80 percent reduction from the 1990 baseline by the year 2050, technology such as solar energy is needed to decarbonize electricity generation (European Commission, 2011). The deployment of solar photovoltaics technology at the terawatt scale has long been recognized as one of the most effective tools to mitigate climate change (Hoffert et al., 2002). 3 One thing to be aware of, however, is that the demand for energy is constantly growing; while the world needs 16 terawatts today, by 2050 it may need 30 to 50 terawatts, depending on how aggressive countries around the globe are in becoming energy efficient.

Consequently, effective energy policies aimed at mitigating carbon dioxide emissions will have to accommodate the developing countries’ growing need for affordable energy sources. This means it is imperative for the cost of photovoltaic technology to continue declining if it is to be deployed in both developed and developing countries.

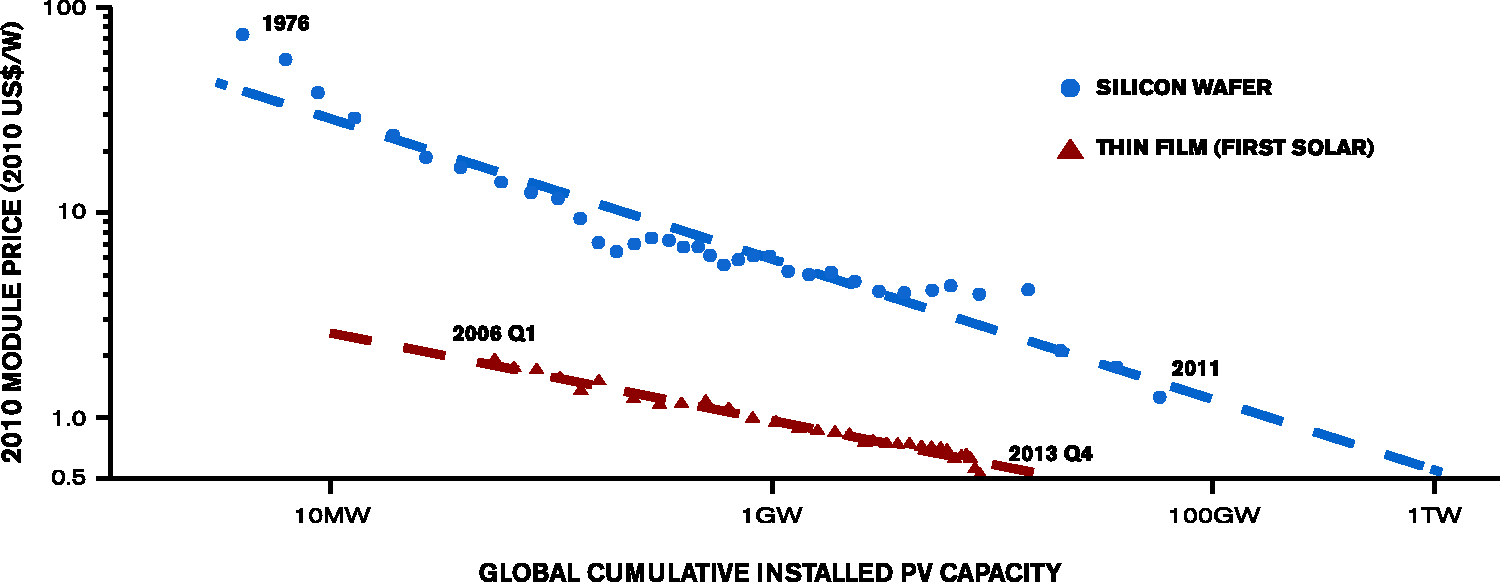

Any progress here can be greatly impeded by the market failures associated with innovation and carbon emissions (Jaffe et al., 2005). Policy interventions—mainly in the form of public spending on research and development, otherwise known as “technology-push,” and deployment incentives, referred to as “demand-pull”—are necessary to address these market failures (Nemet, 2006; Nemet and Kammen, 2007; Qiu and Anadon, 2012). As shown in Figure 1, energy policies aimed at developing PV technology into a globally affordable energy source are essential for deploying clean energy and mitigating climate change on the global scale. These innovations require sustained performance improvements and cost reductions (Duke and Kammen, 1999), and a vision of the widespread deployment of the most efficient use of the cleanest fuels (Williams et al., 2012).

Meeting CO2 emission targets requires further cost reduction in PV technology. The cost of photovoltaic technology has been decreasing steadily with increasing cumulative installations, but needs to continue. All prices are inflation-adjusted, in 2010 U.S. dollars

Unintended consequences of economies of scale

The more you do something, the better you get at it. According to economic theory, this also means that you will do it faster and more efficiently, using fewer resources in the process, and thereby bringing costs down—all of which translates into money. For example, an 80 percent learning curve means that the per-unit average cumulative cost in hours or dollars falls to 80 percent of the previous unit cost while the cumulative output doubles (Barbose et al., 2013; Sagar and van der Zwaan, 2006; Seel et al., 2013). 4

For PV, the learning curve shows roughly a 20 percent reduction in solar cell costs for each doubling of total global manufacturing. This means that as the market grows, the production of PV modules will benefit from accumulated operating experience, leading to innovation and cost reductions. (At the same time, economies of scale will also come into play, further reducing the price per module.) However, it is important to note that the learning rate can vary, and this uncertainty significantly affects the projected timing and cost of reaching cost-reduction milestones (Van der Zwaan and Rabl, 2004) and carbon dioxide mitigation targets.

In a recent study (Zheng and Kammen, 2014), we estimated that an annual market size of 56 terawatts and an estimated investment of about $25 trillion would be required to reach the target module price set by the SunShot Initiative (http://energy.gov/eere/sunshot/sunshot-initiative)—a national collaborative overseen by the Energy Department to make solar energy cost-competitive with other forms of energy—if the cost reduction is assumed to be driven by only economies of scale (Margolis et al., 2012). This implies that “demand-pull” policies focusing on further market scale-up are likely to be unrealistic, given the total market potential and the most expensive approach to achieve this goal.

A technology push is needed. A careful look reveals that a number of lead actors—including the country of Germany, Silicon Valley, the state of California, municipal governments, and a growing global manufacturing sector—play key roles in creating a “momentum of innovation.”

What are these roles? Each jurisdiction has its own incentives and its own subsidies for encouraging clean energy—a requirement for renewable energy in California, a special tariff to reward solar in Germany, and so forth. But the underlying goal is always the same: to create an expanding market with growing revenue that encourages manufacturers’ research-and-development activities. The idea is that the financial rewards of a growing market provide an incentive to commercialize important laboratory research results (Bettencourt et al., 2013).

Scholars have tried to precisely understand the various roles: how innovation brings new products into the market, and how the impact of economies of scale leads to cost reductions. It is important for policy makers to recognize that nothing stands still; the primary driving force underlying the reduction in the price of photovoltaics modules has evolved over time. And we are now at the point where economies of scale (Margolis and Kammen, 1999) are starting to show diminishing returns.

Today we are in a phase of the PV industry in which manufacturing innovations—often of technologies developed in Silicon Valley but brought to production scale across the globe—are driving further module cost reduction. The global PV market expanded nearly twelvefold from 2000 to 2013 (Rowe, 2014), and this scale-up has given birth to large-scale PV manufacturers, which could turn out to be an unintended barrier for new innovative technologies, especially in a market with serious oversupply problems.

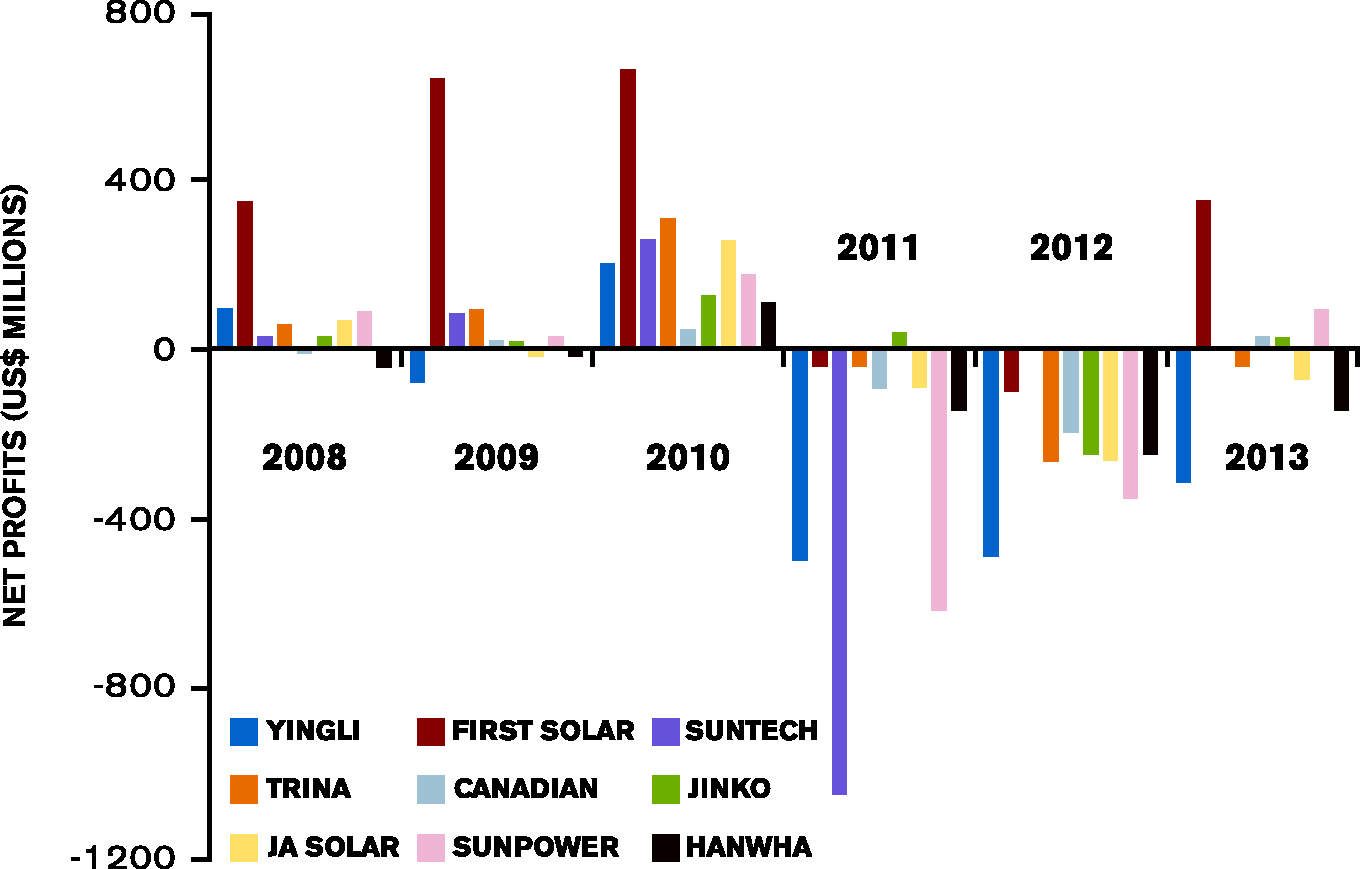

In recent years, this scale-up brought an overcapacity in PV module production that caused PV modules to be sold at unsustainably low prices. This imbalance pushed almost all major PV manufacturers into financial losses in 2011 and 2012 (Figure 2). Interestingly, while the huge ramp-up in manufacturing resulted in smaller and smaller profits for producers of solar modules—to the point where some China-based manufacturers were selling their modules at a loss—the places that built the overall systems and handled the financing (strengths of Silicon Valley firms) profited from the falling module prices. As a result, while the overall cost of a solar energy system a decade ago was dominated by the cost of a panel of solar modules, now it is the power inverter, electronics, and the other ancillary parts of solar array hardware that dominate the cost of a rooftop system.

Net profits or losses of nine major US-listed PV manufacturers, 2008–2013. The 2013 financial results have shown signs of industry-wide recovery from the dark periods during 2011–2012

This overcapacity situation made capital-intensive investment in expanding production capacity unattractive to investors. Lacking the opportunities to scale up production, early-stage PV companies with innovative technologies were forced to compete with incumbent large-scale manufacturers selling their modules at unsustainably low prices. As a result, the industry saw smaller PV manufacturers facing bankruptcy or acquisition.

This process, in turn, led to a further tightening of the capital flows into the industry, for a time causing some analysts to be pessimistic about solar’s future. This negative view still persists, but it has started to ease, partly because of the new wave of technical and deployment innovations. Today, thin-film solar panels with the potential for greatly reduced costs are set to shake up the industry, as are new financing and leasing innovations.

An innovation-focused policy framework for a path toward affordable PV

These waves of solar technological change highlight the need for an aggressive and sustained commitment to innovation.

A set of clearly targeted and long-term deployment policies is essential in the reinforcing dynamics among innovation, manufacturing, and market. First, clear, long-term deployment policies can reduce market uncertainties and encourage more efficient industry-wide consolidation, which contributed to the improved financial performance of major PV manufacturers in 2013. Second, as part of the market-driven innovation mechanism, a long-term and expanding market provides incentives to commercialize important laboratory results through channels such as venture capital funding.

The evolution of the PV manufacturing sector will depend on trade policies. Without trade barriers, surviving and excelling in a world of fierce international competition will require a rapidly innovating research and design sector, as well as economies of scale in manufacturing—and thus a critical size of the manufacturing sector. One possibility for PV manufacturing would have a handful of giant PV manufacturers make up most of the market share. In another version, small, boutique companies put new innovations into production and carve out specific niches; they will then either make it on their own or be acquired by larger firms. Recently, the trend has been toward the larger firms, whose greater manufacturing capacity has played a major role in driving price reductions. In my view, we will need both these large and small companies to survive, innovate, and push the industry.

At the moment, ongoing trade tariff battles, especially between the United States and China, are a cause for concern. Ideally, growing the overall industry will float all financial boats, and the tensions can ease. Giant incumbent manufacturers present large cost disadvantages and risks to start-up manufacturers, whose innovative technologies are yet to be scaled up. We need innovation and competition to drive new thinking, and a diversity of research approaches, business models, and experiments in policies to support clean energy deployment. With domestic and international market growth, waves of research and venture capital and large investment capital could dramatically build up the Silicon Valley model for PV. Already, my research shows that every dollar invested in the PV sector creates several times more jobs than does a similar amount invested in some fossil-fuel industries (Hoffert, 2010; Wei et al., 2010).

Elevated levels of public funding in research and development, and a focus on technological development in PV, are the other central piece of this conceptual model. “Demand-pull” policies will likely face problems on the national level in a globalized PV value chain. A study by the International Energy Agency (Kerr, 2010) identified the need to more than double the amount of publicly-funded research and development.

Innovation itself can be made more cost-effective by establishing a national program aimed at promoting collaboration in research and development and encouraging technology transfer among PV manufacturers. For example, the United States funded a shared research and development center in 2011 through the PV Manufacturing Consortium, which borrowed this pre-competitive model from the semiconductor industry.

An open-data model for the PV industry could also be adopted by the international community to aid research in policy and market development. Various data collection efforts already exist; however, variations in methodology are common. Compiling and continuously updating an official data set with well-documented methodologies—and making this information publicly available—would greatly reduce the cost and time involved in conducting policy and market research. A richer set of analyses and opinions would aid decision-making in both government and industry, and accelerate policy and business innovation.

Such efforts could put PV technology on a path to become cost-competitive with conventional electricity sources in less than a decade (Margolis et al., 2012).

Entering a clean energy era

The evolving economics of PV electricity in the US residential sector over the past two decades was a result of three main factors: increases in the price of electricity, increases in the price of gasoline, and decreases in the price of residential PV systems. With the remarkable drop in the price of PV modules, the ownership of a PV energy system to power the home has become much less costly. If one also plugs in an electric car to the rooftop array, the overall cost approaches the cost of a conventional household that uses grid electricity and a gasoline-powered car.

Furthermore, self-production of energy could help US households smooth out the sharp ups and downs in the prices paid for electricity, natural gas, and gasoline. For example, a recent International Energy Agency report (Priddle, 2014) found that the inflation-adjusted capital expenditure in oil, gas, and coal supply chains more than doubled between 2000 and 2013. And energy costs are projected to steadily increase in the future, as fossil fuels become increasingly more capital-intensive and expensive to extract.

Self-generated electricity would not have been possible without the confluence of a number of forces, many of which are present in Silicon Valley: university and industry research hubs tied closely to industry; mixtures of state and federal support; and a suite of state policies that strongly encourage different aspects of solar energy deployment. Silicon Valley is world-famous for its venture capital ecosystem, making it a global powerhouse for innovations in many business sectors, including solar power.

In this latest phase of the photovoltaics industry, energy policies are set to reward innovations, enabling a cost-efficient path to sustainable PV technology, which could be deployed globally on the terawatt scale. In this environment, the venture capital community can profit from finding and commercializing these PV innovations.

We have seen that innovation and scale-up of the solar industry work best when all the pieces work in concert. The current set of goals makes this interdependence clear; California aims to have one million solar rooftops and one million electric vehicles in use by 2020. This mixture should provide the technology push and demand pull needed to keep the industry growing at the same 50 percent annual growth rate that it has shown for the past 10 years.

We would all benefit by policies that put the California lessons into action, such as expanding the number of cities, states, and nations that set aggressive targets for clean energy education and deployment. We could establish incentives and standards for buildings that integrate solar energy, energy efficiency, and energy storage, turning our built environment into a network of energy power plants. Similarly, we should reward interdisciplinary energy innovations, such as tax incentives for solarized homes that come with electric vehicles paid for as part of the mortgage. (After all, an electric vehicle is in some ways a home appliance.) Policy makers could also reward creative innovations, such as clear solar panels for home and office-building windows, with fast-track permitting to bring down barriers to the new technology’s deployment. And state and federal accounting practices could include a carbon price as a business requirement, while employment reports that highlight job creation across the energy industry would make clear to all the value of green jobs.

Footnotes

Funding and acknowledgements

The author gratefully acknowledges the support of the Karsten Family Foundation, the Zaffaroni Family, the Class of 1935 of the University of California, Berkeley, and the California Energy Commission.

Notes

Author biography

![]() ) and director of the Transportation Sustainability Research Center.

) and director of the Transportation Sustainability Research Center.