Abstract

The decision of the German government, post-Fukushima, to phase out the country’s nuclear power sector by 2022 builds on legislation in place since 2002. This earlier legislation was amended in 2010 to extend the lifetime of the nuclear plants, but the German parliament reversed this extension in the summer of 2011, slightly accelerating the original phase-out schedule; therefore, the market and the nuclear operators were prepared for the shutdown schedule. In this context, it is not surprising that the observed price impacts from the shutdown of 40 percent of the German nuclear power capacity in 2011 are smaller than some modeling exercises had projected. When empirical observation is analyzed in light of a range of economic models, the price effect of the nuclear phase-out can be expected to peak at 5 euros per megawatt-hour or less for a few years around 2020, a reasonably small increase compared with the uncertainties created by other fundamental determinants of Europe’s electricity prices. The macroeconomic effects attributable to the complete shutdown of nuclear power also appear likely to be relatively small, peaking at perhaps 0.3 percent of gross domestic product or less a few years before 2030. In the end, the management of the German transition to an energy mix dominated by renewable energies—and not the use of the existing nuclear reactor fleet for a decade more or less—will be the key determinant of whether that shift has larger or smaller effects on electricity prices or on the German economy overall.

The decision of the German government and, by a huge majority, the German parliament to restrict the lifetime of nuclear reactors and to phase out nuclear power generation in Germany by the end of 2022 was a political decision based on a fundamental risk assessment. On the one hand, such risk assessments must balance the size of potential damage and the probability of its occurrence under major uncertainties for both parameters; on the other hand, such assessments need to reflect political realities. But the wide range of cost estimates for severe nuclear accidents or disasters—from several hundred billion to several trillion euros 1 —makes a comprehensive and robust cost–benefit analysis extremely difficult to complete, leading ultimately to decisions based on fundamental ethical judgements. 2

This does not, however, mean that implicit and explicit economic considerations have not played a significant role in the German decision-making process. The variety of political decisions on the country’s existing nuclear fleet in the last decade has generated not only heated political debate, but also a broad range of quantitative analyses on cost issues. A comprehensive economic assessment of the final results of the phase-out does not yet exist, but the existing information does support some assertions on the economic dimensions of the phase-out, in both the short term and the longer term, and on the economic effects of past nuclear policy.

Especially in terms of politics, different cost issues have different significance. Some of the analyses of the German energy turnaround focus solely on macroeconomic efficiency or on impacts on gross domestic product, but distributional aspects and selected indicators—particularly electricity prices— are usually more significant in political terms and, therefore, often more meaningful to assess.

Although there are many perspectives on the economic dimension of phase-out, experience has already shown that the electricity price impact of shutting down 40 percent of German nuclear capacity was less significant than assumed in some earlier modeling exercises. The macroeconomic effects that could be attributed to the complete shutdown of nuclear power by 2022 also appear likely to be small. In the end, it is not the use of the nuclear reactor fleet for a decade more or less, but the management of the German transition to an energy mix dominated by renewable energies that will be the key determinant of whether that transition has larger or smaller effects on electricity prices or the country’s overall economy.

Economics in the nuclear past

At the turn of the century, nuclear power represented 29.4 percent of the total electricity supply in Germany. The production level of approximately 170 terawatt-hours marks the country’s peak level of nuclear power generation, reached between 1997 and 2001. The decline thereafter was a result of political decisions, of the sort that have shaped the industry since the introduction of nuclear power to Germany in 1961. Therefore, some aspects of past nuclear policy must be considered in order to properly understand the politics and the economics of the nation’s nuclear phase-out.

In the past 60 years, apart from major public spending on research and development and nuclear waste disposal, two major policy interventions made commercial nuclear power generation possible in Germany. First, the government made the first generation of commercial reactors attractive to electric utilities through broad government guarantees —including liability limits—that reduced the commercial risk of nuclear power plants to a level equivalent to the economic risk for investments in conventional coal-fired power plants (Müller, 1996). Also, the government’s strong support scheme for domestic coal production in Germany obliged power generators to use expensive hard coal from domestic mines for electricity generation, rather than cheaper hard coal from the international market. As a result, power generated from hard coal cost more than it otherwise would have, making investment in nuclear power plants economically more attractive. After-the-fact analysis shows that without this coal-support policy, investments in nuclear power plants would have been unattractive in Germany after 1984 (Bohn and Marschall, 1992; Kim, 1991).

When Germany reunified in 1990, 19 commercial nuclear reactors were operational in the western part of the country, representing a total installed net capacity of 20,800 megawatts. 3 The entire nuclear investment program in Germany—which stretched from 1968 to 1989—took place within the framework of a highly monopolized power market. Ever since 1935, the country’s power system had been shaped by regional monopolies and investment regulations that made investment decisions subject to regulatory approval. Once an investment had been approved, the electric utilities were allowed to include the respective investment costs and a fixed profit margin in electricity rates. An extreme case of this regime was the nuclear reactor of Mülheim Kärlich. The 1,200-megawatt reactor produced electricity for only one year, but the investment was entirely recovered from the ratepayers. This regulatory scheme ended in 1998, with a liberalization of the electricity market, driven mainly by the European Union, that resulted in competition among utilities within Germany as well as across borders and led to a situation where costs can be recovered only from sales to a competitive market.

Among many, three economic factors are of special importance for the nuclear phase-out attempts in Germany: First, an enormous amount of public spending went into the nuclear sector, totaling 88 billion euros from 1950 to 2012 (at 2012 prices), 4 a cost that was and is clearly perceived in the public debates over nuclear power. Second, the nuclear investment campaign was completely implemented within the framework of a monopolistic market, which allowed nuclear operators full recovery of investment costs that increased significantly over time; as a result, public and political confidence in nuclear power as a cheap source of power was low or nonexistent. Third, the nuclear fleet was, to a significant extent, written off when the electricity market was liberalized in 1998 and a coalition of Social Democrats and Greens—parties firmly opposed to continued use of nuclear power—took office for the first time.

The phase-out scheme of 2000 and 2002

Phasing out nuclear power has been a core issue in the politics of the Green Party since its establishment in 1980 and has been part of the political program of the Social Democrats in Germany since 1986, when the Chernobyl disaster occurred. As a logical consequence, nuclear phase-out was one of the political priorities of the new government in 1998.

The Social Democrat–Green coalition treaty of 1998 required the government to go for a phase-out strategy that would not lead to compensation for the owners and operators of the nuclear fleet. In the tradition of German corporatism, the government negotiated a contract with the nuclear industry in 2000 that included, among other aspects, a ban on any new licensing of nuclear reactors and a flexible phase-out scheme for the existing reactors. This model was based on an allowance for 32 years of operation for each reactor and the option of transfers of these entitlements among reactors.

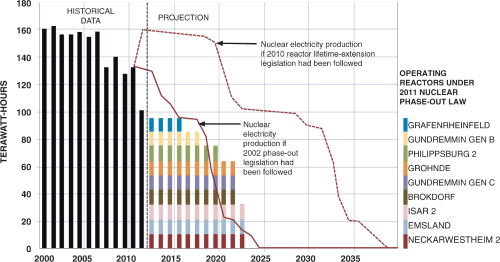

The key motivation for this model was the assumption that the legal risk would be very low if the operators were allowed to run the reactors for the full depreciation period and even accrue extra revenue from a few additional years of operation. This approach led to a phase-out trajectory that had some early plant closures and significant capacity shutdowns in the periods from 2011 to 2015, 2018 to 2020, and 2022 to 2024 (see Figure 1). The German government and the nuclear operators signed a contract in June 2000; it was translated into legislation by the end of 2001 and entered into force in January 2002. In 2003 and 2005, the first two reactors were closed under the new phase-out scheme. Although this phase-out was clearly policy-driven, it should be noted that economic interest in the nuclear industry decreased significantly after the liberalization of the electricity market, which resulted in extremely low wholesale market prices after the turn of the century. From 2000 to 2003, power traded at 20 to 25 euros per megawatt-hour in the German wholesale market, which made it difficult for nuclear power plants to cover the cost of operation, as well as make the necessary provisions for decommissioning, waste management, and profit.

Nuclear phase-out trajectories for Germany according to 2000, 2010, and 2011 decisions and legislation

Another result of the electricity market liberalization and the increasing integration of the northwestern continental electricity market (which includes Germany, France, Austria, the Netherlands, Luxembourg, and Belgium, with strong interconnector capacity to Switzerland) was a new kind of price formation. Electricity prices no longer depended on the average cost of power generation (and, therefore, the fuel mix used to generate that power). Prices were now set according to the short-term marginal costs of the marginal generation unit, which was a hard-coal or gas-fired unit in the continental regional market. As a result of this new method of price formation and increasing market integration, the power prices in the northwestern continental market converged, settling in France (with a 75 percent nuclear share of its power generation) at the same level as in Germany (with 30 percent nuclear) or Austria (which is nuclear-free). 5

Only a few years after the phase-out legislation entered into force, however, the economics in the continental European power market changed fundamentally. Hard coal and gas prices increased significantly; in 2005, the European cap-and-trade scheme for greenhouse gas emissions (the European Union Emissions Trading Scheme) was implemented and wholesale market prices increased significantly. By 2008, the wholesale market prices tripled to levels of 70 euros per megawatt-hour and maintained levels of 40 to 50 euros in 2009 and 2010. In this economic framework, the operation of nuclear plants became highly profitable (Matthes et al., 2011c) and the interest in extending the lifetime of the German nuclear plants grew significantly. This economic interest became even stronger when a series of reactors reached the limits of their production entitlements at the end of the first decade of this century, and the legal restrictions did not allow significant transfers of production allowances to these units.

The German political situation had allowed for no changes in the phase-out legislation before 2009; the Social Democrat–Green government that initiated the phase-out was re-elected in 2002, and in 2005, to create a governing majority, the conservative Christian Democratic Union (CDU) and Christian Social Union (CSU) had to go for a grand coalition with the Social Democrats. But political backing for the phase-out disappeared when the coalition of CDU/CSU and the liberal Free Democratic Party won the elections in 2009. Both parties were programmatic supporters of nuclear energy and strict opponents of the phase-out scheme of 2002.

The double U-turn of 2010 and 2011

The 2009 coalition treaty between the conservatives and the liberals included a clear agreement on the lifetime extension of the existing nuclear reactors in Germany. After a long debate, the government presented a decision embedded in a broad energy policy approach (BMU, 2011):

The lifetime of existing plants was extended for eight or 14 years, depending on the age of the reactors, without changing the 2002 implementation approach that allowed unused nuclear plant running times to be transferred to other plants. The ban on licensing of new reactors was not changed. To share the windfall profits from the lifetime extensions, the government and industry agreed to voluntary payments by nuclear operators to an energy and climate fund. As a result of the deal, the nuclear operators were able to gain extra profits from significantly larger production entitlements, and the government earned some extra income, which was earmarked for energy policy projects. The decisions on nuclear energy were embedded in a set of short-, medium-, and long-term targets for greenhouse gas emission reductions (40 percent by 2020, 55 percent by 2030, and 80 to 95 percent by 2050, compared with 1990 levels), the expansion of renewable energy production (increasing to 50 percent of the energy portfolio in 2030 and 80 percent in 2050), and greater energy efficiency (a 50 percent reduction of primary energy consumption by 2050).

Although the 2010 energy policy decisions were mainly motivated by the attempt to extend the lifetime of existing nuclear reactors, the complementary energy-policy decisions were of real importance. First, even as it was extending reactor lifetimes, the ruling coalition stated clearly that nuclear energy should only be a temporary option, and new nuclear investments would definitely not be allowed in the longer term. Second, the decarbonization of the energy system by the middle of the century was established as the new overarching paradigm of energy policy.

All in all, the nuclear plant lifetime extension in 2010 represented a net profit for the nuclear power generators of 42 billion to 64 billion euros, after taxes (Matthes, 2010), which created an enormous debate on the distributional aspects of the decision. The climate-policy dimension of the lifetime extension did not play a central role in this debate, given the fact that the emissions were already capped for long periods by the European Union Emissions Trading Scheme, and the nuclear decision in Germany would not impact the cap or have an additional impact on overall emission levels.

In the aftermath of the Fukushima disaster of March 2011, however, the German government issued an operating moratorium for the eight oldest reactors and initiated a fundamental change in nuclear policy. After debate, the German parliament approved new nuclear legislation with an overwhelming cross-party majority. 6 The new legislation essentially consisted of two parts: First, the extension of electricity generation entitlements was reversed and the original levels of the 2002 legislation were reinstated. Second, the nuclear production allowances were complemented by fixed plant-closure dates for each reactor. Effectively, this new legislation accelerated the original phase-out schedule by two to three years (see Figure 1). Although this political decision was taken in a very short time frame, the respective debate and the impact assessments relied on the very broad range of analysis that had been carried out in 2010 and before. More important, the nuclear operators, the market, and the network operators had had time to prepare for the gradual shutdown of the rectors over the course of a decade. This advance warning clearly had significant implications for the economic impacts of the accelerated shutdown schedule implemented in 2011.

Economic dimensions of the nuclear phase-out, and the longer perspective

The economic effects of nuclear phase-out have been the subject of a wide range of modeling-based analysis—during the debates in 2010 and before—and observed data have also been studied fairly extensively since March 2011. The electricity-pricing impact of nuclear plant lifetime extensions or restrictions has obviously been a major focus of analysis and debate. The macroeconomic impacts—e.g., on gross domestic product—have been discussed widely but in a much less heated way. 7 At any rate, in the absence of the option of new nuclear investments, all economic impacts of the nuclear phase-out will be temporary. In all the phase-out scenarios decided upon in 2000, 2010, and 2011, the most significant differences in terms of electricity prices and gross domestic product impact would occur by 2030 and disappear gradually after that.

The issue of compensation for the owners of the nuclear plants was not a serious issue in the debates of 2011. This is a result of the design of the 2000 agreement between the German government and the nuclear utilities, which was carefully crafted to prevent any need for compensation payments. 8 Nevertheless, three of the four nuclear operators (RWE, E.ON, and Vattenfall) took legal action to claim compensation payments after the 2011 phase-out decision (Rossnagel and Hentschel, 2012). Given the fact that this decision only re-introduced and slightly accelerated a legal status which had existed since January 2002, the chances of effectively obtaining any compensation must be assessed as rather low. 9

Nuclear plant owners will also, of course, face the issue of decommissioning. According to German legislation, however, the nuclear operators set aside decommissioning funds that were held on their balance sheets and allowed to be invested, generating additional returns. These decommissioning funds, amounting to about 28 billion euros (BReg, 2010), are probably sufficient for the full decommissioning of all plants.

Impact on electricity prices is probably the most important factor of the nuclear phase-out in terms of politics and the public perception. The broad range of modeling exercises carried out in 2010 and 2011 in regard to the phase-out and electricity prices can be summarized in this way: The price impacts peak at ranges of almost nothing to approximately 10 euros per megawatt-hour in the period from 2020 to 2030. The higher bound of this range (Fürsch et al., 2012; r2b/EEFA, 2010; r2b, 2011; Schlesinger et al., 2010, 2011) is equivalent to a 15 percent price increase for energy-intensive industries, a 4 percent increase for the service sector, and a 2 percent increase for small customers and households. Other modeling and analysis (Kunz et al., 2011; Loreck et al., forthcoming; Matthes et al., 2011a, 2011b) attribute power price increases of 5 euros per megawatt-hour or less to the nuclear phase-out—that’s to say, just half of the price increases indicated above.

A closer look at the modeling approaches and assumptions brings further insights:

In most of the modeling exercises, a large share of the price increase, post-phase-out, is projected to result from expected increases in the price of carbon-dioxide emission permits, which are difficult to estimate. In light of the observed market trends, the upper-range projections of electricity price increases after the phase-out clearly include overstated projections of increases in the price of carbon-dioxide permits. Cross-border interactions in the integrated continental European power market can be significant but are extremely difficult to assess. As a general trend, cross-border effects curb the electricity price impacts of changes in the market. Assumptions on the distribution of domestic and foreign investments form a decisive parameter for price equilibrium in the European power market. If the nuclear phase-out were to be complemented by only a few investments in conventional or renewable energy capacity, the shutdown of nuclear plants would lead to high price impacts; if there is significant investment, the price effects will be rather low. If these investments take place outside of Germany, this would increase electricity imports. Recent trends, however, show that Germany has maintained its role as a net electricity exporter, and significant new power plant capacities have been commissioned within its borders. These trends disprove economic models that assume the phase-out will cause the country to become an electricity importer and to make insufficient domestic investments in conventional and renewable capacities.

After the nuclear moratorium in March 2011, operational nuclear capacity decreased—as a result of the moratorium and long-time scheduled maintenance work—by 70 percent. For a few days, nuclear capacity was at a level that won’t be reached again until the end of 2021, according to the final phase-out arrangement. After this period, the long-term capacity loss still amounted to approximately 40 percent, or 8,300 megawatts, of the installed nuclear capacity of Germany. This special situation offers a unique opportunity to identify the wholesale market impact of a major capacity shutdown.

Calculations based on data from the European Energy Exchange show an increase of power prices before the nuclear moratorium, driven by rising fuel and carbon-dioxide allowance prices, and a significant price signal immediately after the first series of plant shutdowns. That signal, however, disappeared very quickly in subsequent weeks. After the summer of 2011, electricity futures prices were again predominantly driven by pre-Fukushima patterns, depending on fundamental fuel and carbon-dioxide price trends; because they are a component cost of overall power prices, increasingly weak carbon-dioxide emissions prices led to significantly decreasing electricity prices. A more detailed and methodologically advanced analysis (Thoenes, 2011) underlines the finding: The price signal from the nuclear shutdown in March 2011 could not be detected after the summer of 2011. The integrated continental European market obviously has adapted to the new supply structure and found a new equilibrium at price levels that do not differ significantly from the ones before the moratorium or are extremely low compared with the other fundamental determinants of the power market.

If these empirical observations are compared with the modeling done ahead of the phase-out, it’s clear that most of the modeled price effects, at least from the first tranche of plant shutdowns, exceed the observed impacts on electricity price significantly. Given all the uncertainties and interactions involved in electricity pricing, and considering the full range of estimates of the effects that Germany’s phase-out might have, a price increase of 5 euros per megawatt-hour for a few years is probably the maximum that can be attributed exclusively to the gradual phase-out of nuclear power. Furthermore, it should be noted that the uncertainties and volatilities for many relevant factors—the price of fuel and carbon-dioxide emissions permits, domestic and international investment activities, the level of economic activity, etc.—are probably much more significant for the longer-term price trends in the German and continental European power market than a restriction of the lifetime of nuclear reactors as implemented by the German phase-out legislation.

In terms of keeping electricity costs low, the most significant challenge will arise from the country’s long-term transition to renewable energies, a process that was in fact the ultimate goal even within the framework of the nuclear power plant lifetime extension in 2010. The effects of this transition cannot be seen as associated exclusively with the accelerated phase-out of nuclear power. But a carefully designed, robust, and flexible strategy of transition to renewable energies—with sufficient lead-times and a strong emphasis on straightforward implementation and practical learning—will make this transition more effective and efficient in the framework of an ambitious phase-out policy, particularly for a technology-based country like Germany.

Most estimates of the macroeconomic impacts of Germany’s accelerated nuclear phase-out have been made in models that reflect not only the nuclear energy sector, but also Germany’s entire decarbonization approach, which includes all its energy sources. This integrated transition toward an energy-efficient and renewable energy-based economy makes it extremely difficult to isolate the macroeconomic consequences of the nuclear phase-out strategy. The existing analysis on the very ambitious decarbonization strategies of Germany and the European Union does, however, indicate that their macroeconomic impacts will amount to significantly less than one percentage point below or above the business-as-usual case during the course of the next four decades (European Commission, 2011a, 2011b; Kirchner et al., 2009; Schlesinger at al., 2010, 2011). The impact of nuclear phase-out decisions peaks at 0.3 percent of total gross domestic product in the decade between 2020 and 2030 (Schlesinger et al., 2010, 2011). Even this relatively small decrease of GDP growth, however, is mainly premised on a high—and probably greatly overstated—electricity price impact of the nuclear phase-out.

These aforementioned analyses assumed that the only concerns were the timing of a nuclear phase-out and a policy that relies mainly on renewable energies to reach decarbonization goals by mid-century. This approach reflects the existing political debate but leaves out the possibility of use of nuclear power in the system, which would require major new investments in nuclear plants in coming decades.

Research conducted by the European Commission for the European Energy Roadmap 2050 (European Commission, 2011b; Matthes, 2012) shows a decision for or against an energy mix that includes or excludes new investments in nuclear power plants probably would not lead to major differences in terms of the cost impacts of a decarbonization program. Against this background, the strategic choices on the future shape of the electricity system should primarily rely on other issues—for example, the assessment of risk options and security of supply considerations. The transition to a decarbonized energy system without nuclear power needs well-designed strategies and policies. In the context of an energy system that will, in any case, need major investments, this transition could be achieved at comparatively low cost.

The surprisingly small cost of nuclear exit

Within the last decade, German nuclear policy has significantly changed course three times. The final decision in 2011 to pursue an accelerated shutdown of the German nuclear power industry actually marks the return to a phase-out schedule initially put into place in 2002, for which the nuclear operators and the market had prepared over the course of a decade.

As a result of this lead time, the electricity price impacts of the 2011 shutdown of the first 40 percent of nuclear capacity in Germany was much less significant than assumed in some of the broad range of modeling exercises that fueled nuclear debates in 2010 and 2011. If the empirical observations are considered with a range of model assessments, it seems likely the price effect of the nuclear phase-out will peak at 5 euros per megawatt-hour or less for a few years around 2020. Compared with the uncertainties and volatilities related to other fundamental determinants of the electricity price in continental Europe, this is a reasonably small effect. The same situation holds for the macroeconomic effects of the phase-out, which could peak at 0.3 percent of gross domestic product or much less a few years before 2030. Again, this increase is within the range of the usual uncertainties and relatively small.

The small economic effects of the German nuclear phase-out become even more obvious, if the ultimate goal of decarbonization of the energy system is factored into the equation. The management of this overarching transition to renewable energies by the middle of the century—and not the use of the existing nuclear reactor fleet for a decade, more or less—will be the key determinant of the electricity price changes or macroeconomic impacts. Recent European research underlines the point: Maintaining the nuclear energy pathway could not provide significant economic benefits. The accelerated and short-term nuclear phase-out, however, has the potential to provide an appropriate framework for a straightforward transition of the electricity system toward renewable energies, particularly because Germany has the technological base to support that transition. Furthermore, a strong push on sustainable technologies and innovative energy infrastructure systems has the potential to strengthen Germany’s position as a major technology-exporting country and create the macroeconomic benefits that derive from such front-runner status.

Footnotes

Acknowledgements

This article is part of a three-part series on the implications of phasing out civilian nuclear power in Germany, France, and the United States. Additional editorial services for this series were made possible by grants to the Bulletin of the Atomic Scientists from Rockefeller Financial Services and the Civil Society Institute.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.