Abstract

The cost of building new nuclear reactors receives a great deal of attention in market economies, including the United States, Japan, and Germany. But in a post-Fukushima era of additional safety regulations, the economics of keeping a fleet of aging reactors online may command just as much attention. The author reviews the experience of the US nuclear reactor fleet in light of the post-Fukushima scrutiny of nuclear safety and describes the factors that have influenced, and will likely influence, future decisions about whether to own and operate nuclear reactors. He shows that safety has been the driver of nuclear costs and that the inability of the industry to deliver safe reactors at affordable costs is an endemic, long-standing problem. Nuclear power, he writes, is a complex technology based on a catastrophically dangerous resource that is vulnerable to natural events and human frailties, which suggests that nuclear safety and affordable reactors are currently incompatible and are likely to remain so for the foreseeable future.

Keywords

Has the heralded “nuclear renaissance” finally arrived? In February 2012, for the first time in more than 30 years, the US Nuclear Regulatory Commission (NRC) issued a license to build two new nuclear reactors. In March, the NRC approved a license for two more new reactors, and utilities have submitted applications for 23 additional reactors. Two of those reactors would be at a brand-new nuclear power plant in Florida’s Levy County, where Progress Energy Florida recently agreed to a settlement that will allow the utility to collect $350 million from customers over the next five years as a down payment.

Look more closely at what’s happening in Levy County, however, and you’ll see that the nuclear industry’s slump is not over yet. The new Levy County reactors will not start operating for at least another decade, if ever. It’s all a question of money: The utility estimates that the reactors will cost between $17 billion and $22 billion—not counting financing charges and cost overruns, which have plagued the nuclear industry. (Progress originally estimated that the reactors would cost $5 billion and would commence operation in 2016.) With the demand for electricity growing at a snail’s pace, and natural gas prices at a fraction of what the utility expected when it filed its application for a new plant in 2008, opposition to the project has mounted, threatening a rerun of the 1970s and 1980s, when the majority of nuclear construction plans were canceled or abandoned.

The questionable economics of building new nuclear reactors are only part of the problem that the nuclear industry confronts today. It also faces the challenge of keeping its fleet of old reactors online. Just eight miles south of where Progress plans to build its new reactors, the company is struggling to get its aging Crystal River reactor back in service. The reactor has been offline since September 2009, when engineers cut into its containment building to replace steam generators—work that exposed structural flaws in the building’s concrete panels. Attempted repairs have only created new cracks. Replacing the panels, or perhaps the entire containment building, will take years and cost more than $2 billion, if indeed the plant ever comes back online.

At many sites around the United States, the costs of building new nuclear reactors have received a lot of attention, but the economics of existing nuclear reactors have come under far less scrutiny. Severe accidents like Three Mile Island, Chernobyl, and Fukushima shine a spotlight on safety issues, which creates a major challenge for nuclear economics, because safety can be extremely expensive. Suddenly, old reactors do not look like the cash cows that they are believed to be. In fact, they may be financial disasters waiting to happen.

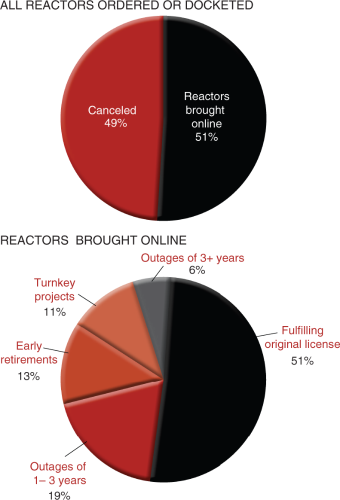

As shown in Figure 1, the assumption that nuclear reactors hum along, once they are online, is not consistent with the US experience (Cooper, 2012). About half of all reactors ordered or docketed at the Nuclear Regulatory Commission have been canceled or abandoned. Of those that were completed and brought online, 13 percent were retired early, 19 percent had extended outages of one to three years, and 6 percent had outages of more than three years. In other words, more than one-third of the reactors that were brought online did not just hum along. Another 11 percent were turnkey projects, which had large cost overruns that were never revealed or documented.

The financial and online status of US nuclear reactors.

Too expensive to build

A brief review of the economics of new nuclear reactor construction is helpful, because the pattern of construction costs is one indicator of the pattern of subsequent capital expenditures—particularly for the repair or replacement of major components. From the point of view of an investor in a market economy, the decision to build or buy a nuclear reactor involves a financial analysis of risk and reward (Cooper, 2009b). Although that calculation has historically been heavily influenced by a number of policies and large subsidies that affect the prospects of nuclear power, it remains, at root, an economic decision.

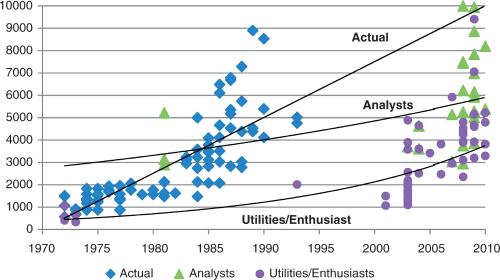

Shortly after the start of the twenty-first century, nuclear enthusiasts began to hype a renaissance in nuclear power that would lead to the construction of hundreds of new reactors, based on bold assumptions about the dramatically reduced cost of construction for standardized, modularized reactors. As shown in Figure 2, those projections proved to be as far off the mark as the projections that typified the building boom of the 1970s and 1980s.

Overnight costs of reactor construction (2009 dollars/kilowatt).

During the US construction boom, nuclear reactors suffered severe cost escalation (Cooper, 2010). The final reactors cost more than seven times as much as the initial reactors brought online and exceeded the original projections by an even wider margin. The result was a series of lengthy regulatory and court proceedings that contested large potential rate increases and made nuclear power a lot less profitable than the utilities had hoped.

The pattern repeated itself in the cost projections offered during the past decade. Rising cost estimates in the United States, and uncertainty surrounding several projects undertaken by the French, seem to have derailed the so-called renaissance (Cooper, 2009a). As a result, in the United States, more than 80 percent of the license proceedings that were opened at the NRC during this time period are dormant, if not dead, and more than half of those that are still active appear to be unlikely to result in actual construction of new reactors (Cooper, 2009b).

The current difficulties of nuclear reactor construction are reflected in the fact that, despite the long-standing socialization of liability for a nuclear accident (Cooper, 2011e) and efforts to streamline the licensing process, utilities require a combination of federal loan guarantees, early cost recovery from ratepayers, and public entity support to proceed with projects (Cooper, 2011a). Even then, it is not certain a project will be successful. Aside from the socialization of liability, the other subsidies are not generally available to support retrofit or repair costs for existing reactors. Also, it’s likely there will be more regulatory scrutiny in the future, not less, for both old and new reactors.

Too costly to fix

The US nuclear industry has complained that the cost escalation was driven by unnecessary regulation—regulation that the NRC believed was vital to ensure the safety of the growing fleet of nuclear reactors in the 1970s.

1

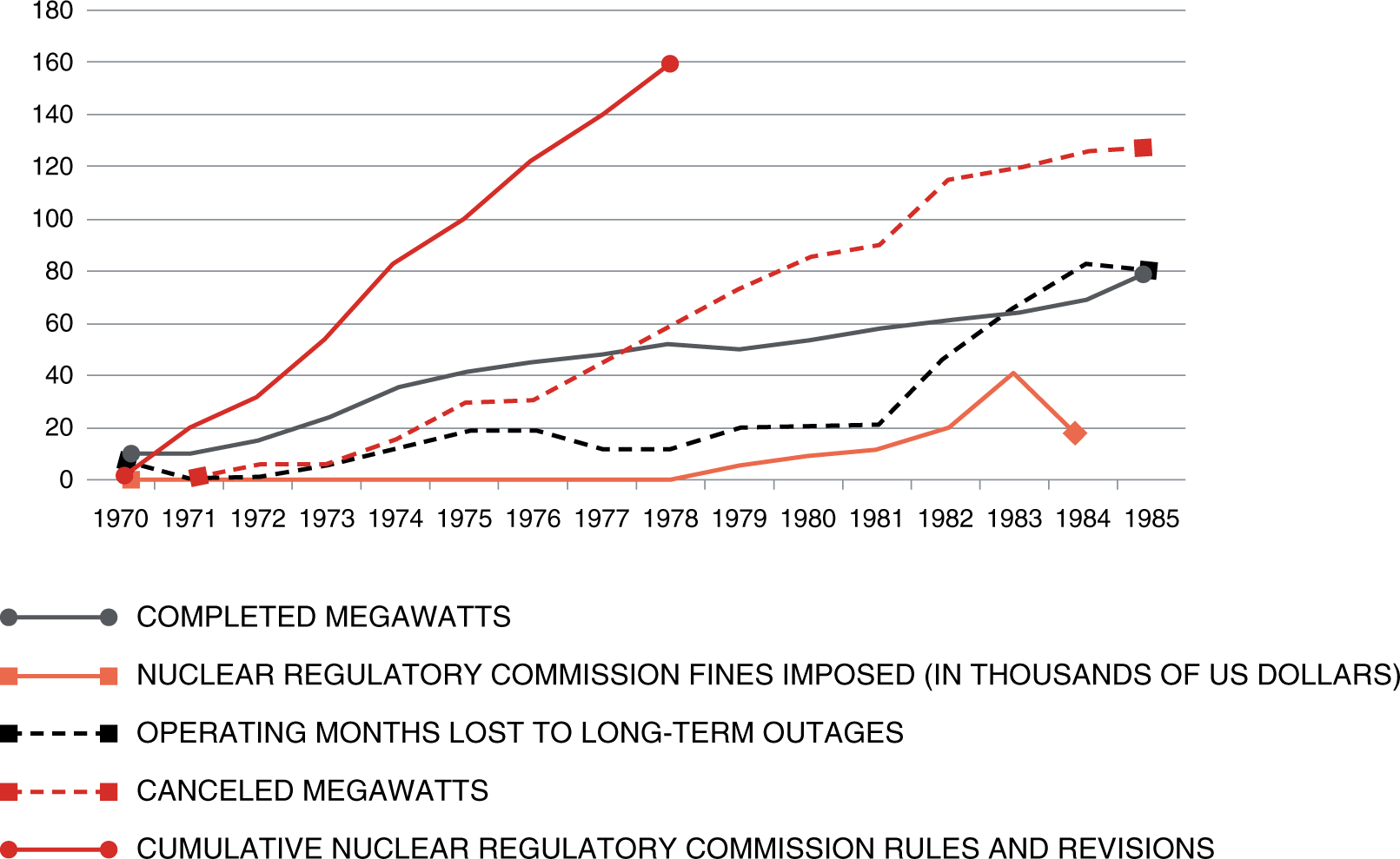

One thing history shows clearly is that the link between safety regulation and economics existed before the 1979 accident at Three Mile Island (Cooper, 2012; Koomey, 2011). Figure 3 covers the construction boom-and-bust period before Chernobyl. By 1985, the status of more than 90 percent of all reactors (canceled or completed) had been decided. Figure 3 shows that the growth of standards and guidelines was dramatic, from three in 1970 to 143 by 1978, with an even higher total when rules plus major revisions are counted. Enforcement came after the Three Mile Island accident, when the NRC felt compelled to ensure compliance with its rules, and long-term outages ramped up.

2

Enforcement altered the economics of existing reactors.

Safety regulation and the disposition of nuclear reactors.

Ultimately, since the start of the commercial industry, one-quarter of all US reactors have had outages of more than one year. There are three causes of these outages:

Replacement—to refresh parts that have worn out Retrofit—to meet new standards that are developed as the result of new knowledge and operating experience (e.g., beyond-design events) Recovery—necessitated by breakage of major components

The reactors that had extended outages were twice as likely to have been completed before Three Mile Island, and therefore they were caught in the transition to greater safety regulation. Construction of these reactors began with half as many regulations in place as for reactors that did not suffer such outages, and the number of regulations that were applied to these reactors more than tripled during their construction period. The average cost of an outage (in 2005 dollars) was more than $1.5 billion, with the highest cost topping $11 billion (Lochbaum, 2006).

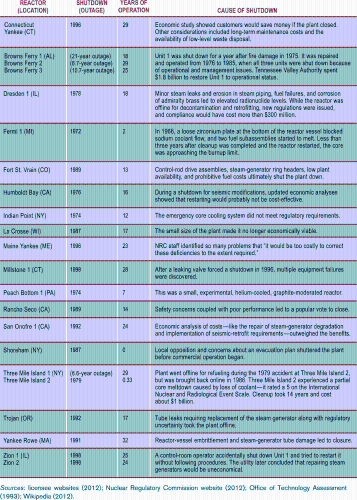

Significantly early retirements and reactors with outages exceeding 5 years.

Quantitative and qualitative analysis of the early retirements provides insight into the decision to retire reactors. Early retirement reactors are typically older, smaller reactors built before the ramp-up in safety regulation. They are not worth repairing or keeping online when new safety requirements are imposed, or when the reactors are in need of significant repair. On average, compared with reactors that were not retired early, early retirements were:

Less likely to be pressurized water reactors (53 percent vs. 63 percent) Brought online earlier (on average, 1972 vs. 1979) Much more likely to have been brought online before Three Mile Island (82 percent vs. 50 percent) Smaller (558 megawatts vs. 964 megawatts) Less likely to have suffered a safety-related outage (12 percent vs. 33 percent) More likely to have suffered damage or a component-related outage (24 percent vs. 11 percent)

Qualitatively, the decision to retire a reactor early usually involves a combination of factors, such as major equipment failure, system deterioration, repeated accidents, and increased safety requirements. Economics is the most frequent proximate cause, and safety is the most frequent factor that triggers the economic reevaluation. Although popular opposition inspired a couple of early retirements (a referendum in the case of Rancho Seco; state and local government in the case of Shoreham), this was far from the primary factor, and in some cases local opposition clearly failed (referenda failed to close Trojan or Maine Yankee). External economic factors, such as declining demand or more-cost-competitive resources, can render existing reactors uneconomic on a stand-alone basis or (more often) in conjunction with one of the other factors.

Under the post-Fukushima microscope

Fukushima highlights the fact that nuclear reactors do not age gracefully. Time not only causes wear and tear; it also exposes reactors to events that occur only rarely and reveals design issues that were not recognized or never addressed when the reactor was constructed (Cooper, 2011b). Retrofitting old reactors is costly, so the trade-off between safety and economics is put under a microscope.

This scrutiny means more people looking more carefully at a reactor’s track record, but even more importantly, more people paying attention to the ongoing struggle with safety. The problem is compounded by the fact that reviewing nuclear reactor safety after an accident reveals an endemic tendency to undervalue safety before an accident—namely, past violations of standards that did not result in enforcement actions (Onishi and Fackler, 2011) but instead in lowered standards to avoid increased expenses related to safety (Donn, 2011; Sullivan, 2011).

The United States, Japan, and the European Union have issued safety recommendations in response to the Fukushima accident (Eurosafe Forum, 2011; Nakagome, 2011; Nuclear Regulatory Commission, 2011). By the first anniversary of Fukushima, 96 percent of the reactors in Japan were offline (Fackler, 2012). Every reactor in France was undergoing mandatory upgrades for backup power and venting, and the overall cost of meeting new safety requirements there will add billions to the cost of electricity. 3 Germany began closing aging reactors and ultimately decided to abandon nuclear power. All of this suggests that license extensions will be harder to come by, and additional plants will be retired (Lekander et al., 2011). Implementation will vary from nation to nation, but “cost increases are inevitable,” according to former Exelon CEO John Rowe (Malik, 2009).

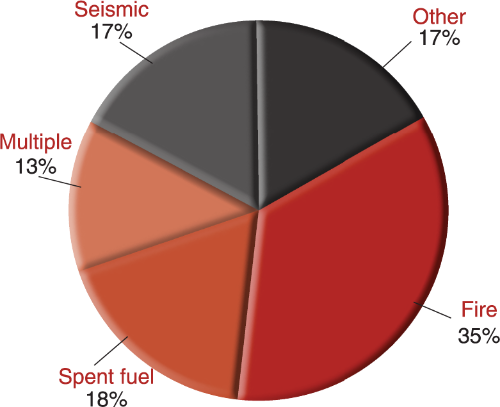

In the United States, the concerns expressed about safety affect a large part of the fleet. The Union of Concerned Scientists (2012), which tracks ongoing safety issues at operating nuclear reactors in the United States, has found that leakage of radioactive materials is a pervasive problem at almost 90 percent of all reactors, as are issues that pose a risk of accidents. Figure 4 shows three issues that have been highlighted by Fukushima: seismic risk, fire hazard, and elevated spent fuel storage. More than 80 percent of US reactors face one or more of these issues. All boiling water reactors (like those at Fukushima) have at least one of these issues. Three-quarters of US pressurized water reactors have an issue. Half of those that do not exhibit one of these issues had a near miss in 2011. Clearly, safety remains a challenge in the United States, one that has been magnified by Fukushima.

Significant ongoing safety issues.

Too big to fail

Operating an old nuclear reactor, like building a new one, can be a bet-the-farm proposition for a utility. The scale of an accident like the one at Fukushima (and Chernobyl before it) is so large that, notwithstanding insurance schemes that socialize the risk of nuclear power, it can force even the largest utility instantly into virtual, if not actual, bankruptcy. Considering the expense associated with such an accident, old reactors may simply be too risky—financially—to operate. It appears that severe accidents typically cost hundreds of billions of dollars (Cooper, 2012). Even a utility as big as the Tokyo Electric Power Company (Tepco), the fourth largest in the world, cannot sustain such a massive blow to its bottom line without help.

The fact that governments will step in may be a mixed blessing, from the investor point of view, and it is definitely problematic from the societal point of view. Companies such as Tepco may be seen as “too big to fail,” like the banks that received government bailouts in the financial meltdown of 2008. This may create a perverse incentive for a utility to take risks it should not, although the zombie-like condition of Tepco, and the intense scrutiny that nuclear utilities endure post-accident, suggest there is a significant price to pay after the fact. Unfortunately, it’s questionable if this price will be factored into decisions about whether to continue operating existing reactors that are facing safety issues.

The too-big-to-fail concept is generally applied to financial institutions and fits within a broader class of economic dilemmas known as moral hazard. The theory is that, when an outside party (like the government) absorbs some of the risk of a transaction, the original parties to the transaction (like banks and energy companies) have an incentive to do things that they would not do if they bore all of the risk (like slack off on safety standards to save money). In the case of financial institutions, the government fears that letting a bank fail might undermine confidence in the financial market, putting the entire system at risk. And the financial institutions count on this fear and assume the government will not let them sink—and so banks feel freer to take a few more risks. Hence, systemic risk motivates governments to bail out banks and, more recently, to impose greater requirements for safety and soundness on institutions that pose systemic risk since the institutions themselves have less incentive to do so.

Whether investors in utilities should count on this concept as a way to protect their investments in nuclear reactors is unclear. In one sense, no nuclear reactor or even nuclear power station in the United States is too big to fail. They make up too small a part of a highly interconnected grid to bring down the whole grid, but the magnitude of a severe accident may be sufficient to undermine the economic viability of the utility. Clearly, Tepco is struggling with the financial aftermath of Fukushima and exists only because of the intervention of the Japanese government.

In another sense, the magnitude of the Fukushima accident has been so great that it demonstrates how a nuclear power plant can be too big to fail. An accident of this severity calls into question the entire technology, which poses a challenge to the national grid and has a large impact on the broader national economy. With utility disruption, grid disruption, and economic disruption, society may feel compelled to step in, thereby absorbing the risk that the utility should take.

Lessons for decision makers

Journalists and policy makers frequently insist on simple answers to complex questions, such as the question of whether the world can have nuclear safety and affordable reactors. Writing just after Chernobyl, Tomain (1987) posed the question somewhat differently: “Is nuclear power not worth the risk at any price?” These are extremely complex questions, but if a simple answer must be provided, it is this: If we use a market standard, nuclear power is neither affordable nor worth the risk. If the owners and operators of nuclear reactors had to face the full liability of a nuclear accident and meet alternatives in a competition unfettered by subsidies, no one would have built a nuclear reactor in the past, nor would they build one today, and they likely would exit the nuclear business as quickly as they could.

The combination of a catastrophically dangerous resource, a complex technology, human frailty, and the uncertainties of natural events make it extremely difficult and unlikely that the negative answer can be changed to a positive. By bringing intense scrutiny to bear on aging reactors, Fukushima prompts policy makers and the public to ask tough questions about whether aging reactors should be retired or not have their licenses extended—the same questions that have generally been asked about the construction of new reactors. In formulating the answer, the lessons of half a century of nuclear power should be kept in mind. Among the most important of these lessons:

Nuclear power is a non-market phenomenon

Nuclear socialism is an appropriate description of the economics of nuclear power. It is certainly true that economics have decided, and will likely continue to decide, the fate of nuclear power, but the fiction that investors and markets can make decisions about nuclear power in a vacuum is dangerous. Given the massive economic externalities of nuclear power (not to mention the national security and environmental externalities) and the massive subsidies on which it has always depended, policy makers decide the fate of nuclear power by determining the rate of profit through subsidies.

Match risks and rewards

If the goal is to have cost-efficient decisions, risks must be shifted onto those who earn rewards. By reducing the rate of profit that utilities earn from subsidized projects, policy makers can offset the bias that subsidies (such as loan guarantees and advanced cost recovery) introduce into utility decision making.

Buy time

Given the severe problems that retrofitting nuclear reactors pose, and the current conditions of extreme uncertainty about changes in safety regulation, it is prudent to avoid large decisions that are difficult to reverse or modify. Flexibility is a valuable attribute of investments, and mistakes should be kept small (Cooper, 2011c, 2011d).

Learn from history

Sound economic analysis requires that sunk costs be ignored, but the mandate for forward-looking analysis does not mean that the analyst should ignore history. Utilities claim that the cost of completing a new reactor or repairing an old one (the cost “to go”) is lower than the cost of pursuing an alternative from scratch. The problem is that utilities are just as likely to underestimate and be unable to deliver on the promised “to-go” costs as they have been when they tried to estimate and deliver on the cost to build nuclear reactors. Regulators must exercise independent judgment and take the risk of cost overruns into account.

The Fukushima disaster, the worst nuclear accident ever to occur in a market economy, punctuated half a century of tension between nuclear safety and nuclear economics. Intense post-Fukushima scrutiny has highlighted the endemic problems that afflict the underlying technology. The prospects for both new and old nuclear reactors are much dimmer now, possibly signaling an end of an era in the so-called nuclear renaissance proclaimed just a decade ago.

Footnotes

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.