Abstract

When public administrators resolve disputes between citizens and other state officials, are they truly impartial? The question is imperative for evaluating resolutions made by street-level bureaucrats whom citizens often perceive as the face of public administration. This study examines the relationship between public accreditation and the tendency of street-level bureaucrats’ resolutions to accept the state’s arguments or the citizens’ claims. Using quantitative analysis of administrative lower-court rulings in Israeli tax disputes, the findings link public accreditation to state favoritism in street-level resolutions. Such an outcome, if not accounted for, may jeopardize procedural fairness and erode public trust in government.

Introduction

Street-level bureaucrats are major implementers of public policy (Portillo & Rudes, 2014; Thomann et al., 2018). Serving at the front-lines of public administration, they use their broad discretion when allocating public benefits and imposing public sanctions (Lipsky, 2010; Tummers & Bekkers, 2014). Despite the diversity in their jobs—teachers, police officers, low court judges, social workers, and more—they are seen as belonging to the same group of public servants that interact with citizens directly and on a regular basis, exercise considerable discretion while doing so (Hupe & Buffat, 2014), and develop similar coping mechanisms to balance their lack of information and resources (Gofen, 2014). The decisions they make concern important issues that affect the outcomes of governance (Brodkin, 2012; Edlins & Larrison, 2018) and reflect the administration to citizens (Davidovitz & Cohen, 2022a).

At the core of the social contract between citizens and the government is the belief that the former will be treated fairly and with dignity (Rawls, 1971). In return for their participation in collective decision-making and paying of taxes, citizens expect fair treatment from authorities (Beeri et al., 2022; Van Ryzin, 2011). Some scholars view the concept of bureaucratic neutrality as a myth (Portillo et al., 2020); yet procedural values, such as fairness, equity, and respect continue to constitute a significant driver of trust in government (Mazepus & van Leeuwen, 2020; Mcloughlin, 2015; Moynihan et al., 2015). Therefore, citizens who believe they received unbiased treatment from public administrators and generalize their personal experiences (Kumlin & Rothstein, 2005) are more likely to develop trust in the administration and follow administrative decisions and rules (Kang, 2022).

People expect fair treatment from street-level bureaucrats (Raaphorst & Van de Walle, 2020) whom they perceive as the symbolic face of the government (Lipsky, 2010). It is therefore essential for street-level bureaucrats’ decisions to be considered unbiased, especially when resolving disputes between the state and its citizens. Still, the literature is equivocal regarding street-level bureaucrats’ dual role as state employees serving citizen-clients. They sometimes are viewed as citizen agents who consider themselves advocates for the public (Glyniadaki, 2022; Maynard-Moody & Musheno, 2000; Tummers, 2017), while at other times they are described as state agents, adopting the state’s narratives (Prendergast, 2007). 1

This study focuses on situations in which street-level bureaucrats are called upon to resolve disagreements between citizens and other state officials. In such administrative disputes, the likelihood of their resolutions to support public claims or state arguments can expose their pro-citizen or pro-state tendencies (Cohen & Gershgoren, 2016; Raaphorst, 2018).

Many factors can influence the tendency of street-level bureaucrats to make state-friendly or citizen-friendly resolutions. Some factors are shaped by the special circumstances in each dispute. Other general, environmental, organizational, social, and personal factors also may affect their use of discretion (Jilke & Tummers, 2018; Kinsey & Stalans, 1999; Visser et al., 2024), collide with their obligations to various accountability forums (Hupe & Hill, 2007; Thomann et al., 2018), and counter or amplify their personal narratives (Maynard-Moody & Musheno, 2000).

The study here investigates the potential relationship between public accreditation and street-level bureaucrats’ willingness to accept the state’s or the citizens’ claims in their resolutions. 2 Some street-level bureaucrats may be publicly accredited through formal certification and membership in public organizations, while others may serve without such public accreditation. Like formally certified schoolteachers and police officers who work alongside unaccredited assistants and volunteers, this study extends the scholarly view of lower-court judges as street-level bureaucrats (Biland & Steinmetz, 2017; Cowan & Hitchings, 2007; Dallara & Lacchei, 2021; Jain, 2018; Lipsky, 2010) to uncertified lay adjudicators with whom they collaborate in mixed administrative tribunals.

The article proceeds as follows: first, we set theoretical background for exploring street-level bureaucrats’ pro-citizen or pro-state tendencies in their resolutions. Two hypotheses follow, focusing on the relationships among such tendencies, formal certification, and membership in public organizations. Then, the context and method for testing the hypotheses are described. The hypotheses are tested, using statistical tools to examine all lower-court rulings issued in Israeli tax appeal committees between 2005 and 2021. Formally certified lower-court judges’ rulings that resolved such tax disputes are compared to those made by uncertified lay adjudicators, and those made by judges who are also active members of the district court are compared to those decided by judges who have retired their membership in the district court. After presenting and discussing the results, we conclude by highlighting the study’s limitations of the study and potential future research directions.

Pro-Citizen and Pro-State Tendencies in Street-Level Resolutions

Scholars have emphasized how crucial discretion is to the efforts of street-level bureaucrats (Evans, 2016; Thomann et al., 2018). Discretion is generally defined as freedom of choice that can be exercised within a specific context (Evans, 2011). This study focuses on such freedom of choice as manifested in street-level bureaucrats’ resolutions and explores its relationship to their pro-citizen or pro-state tendencies.

The terms “pro-citizen tendencies” and “pro-state tendencies” refer to street-level bureaucrats’ discretionary preferences for the claims of citizens in disputes with other state officials. In their pro-citizen resolutions, they reject the state’s arguments and accept those of the citizens and, vice versa, in their pro-state resolutions. Public administration theory is equivocal in terms of whether street-level bureaucrats tend to favor the state or its citizens. The classic distinction between politics and administration (Rohr, 1987) views them as state agents acting in its favor (Prendergast, 2007) and condemns their deviations from public policy as shirking responsibility or sabotage (Brehm & Gates, 1997). In contrast, some scholars have suggested, based on the self-descriptions of street-level bureaucrats, that they may see themselves as citizen agents, using their discretion to implement procedures and laws that help those they consider worthy and punish those they deem unworthy (Glyniadaki, 2022; Maynard-Moody & Musheno, 2000; Tummers, 2017). Real-world resolutions that resolve such disputes can expose the antecedent pro-state or pro-citizen tendencies of street-level bureaucrats.

“Resolutions” or “street-level resolutions” refer to the settling of disputes (Burton, 1990) between citizens and other state-officials. Citizens can take their claims against state officials to a variety of appeal agencies (Buck, 2004; Currie & Goodman, 1975). Indeed, many of those with the authority to accept or reject such claims – such as mediators, arbitrators, specialized tribunals, and administrative adjudicators – are street-level bureaucrats themselves. They use their discretion to make resolutions, but who will they side with?

Scholarship provides insights into the numerous personal, organizational, and environmental factors that influence the use of discretion by street-level bureaucrats (for a comprehensive description, see Cohen, 2018). Most studies focus on their use of discretion in making decisions about their own conduct. Little attention has been paid, however, to street-level resolutions that affirm or reject arguments presented by other state officials. Such resolutions can be made by publicly accredited deciders or by those without such accreditation. This study focuses on two types of public accreditation: formal certification and public organization membership.

“Formal certification” confirms the public role of a street-level bureaucrat. Formal certification confers public authority and recognizes public expertise by affirming that the certified individual has met the necessary level of compliance and completed the needed steps to be designated, systemically, as a formally certified state servant. Public-organization membership is another type of public accreditation that indicates that a public organization determined the street-level bureaucrat to be competent enough to become a member of the organization. The question that arises is whether publicly accredited street-level bureaucrats accept more or fewer citizen claims in their resolutions than those who are not publicly accredited.

Hypotheses

The Relationship between Street-Level Bureaucrats’ Formal Certification and Their Pro-State Tendencies in Their Resolutions

Formally certified street-level bureaucrats may feel more compelled than their uncertified counterparts to support the state that accredited them (Bolino et al., 2013). People have many reasons for making decisions that affect themselves and others (Lavee, 2021; Van Lange et al., 2013). Yet scholars have observed that bureaucrats often make decisions based on professional preferences (Bhatti et al., 2009) and that formally certified street-level bureaucrats may develop feelings of (professional) accountability toward their public profession/vocation (Hupe & Hill, 2007). In addition, they may be more socialized to meet the standards required for their formal certification as state servants (Feldman, 1981; Morrison, 1993; Moyson et al., 2018), which may compel them to internalize and adopt state-oriented standards. Furthermore, they may interact with other formally certified state servants (e.g., in vocational associations, Hupe & Hill, 2007) more intensively than their uncertified counterparts, strengthening formally certified officials’ state-oriented indoctrination both informatively and normatively (Keulemans & Van de Walle, 2020; Raaphorst & Loyens, 2020; Tummers et al., 2012).

Last, but not least, formal certification also may result in role-induced bias (Simon et al., 2008, 2009). The assignment of roles can influence people’s attitudes and behaviors (Janis & King, 1954; Zimbardo, 1965). Hence, individuals may reach conclusions that are mandated by their role (Janis & King, 1954; Simon et al., 2008, 2009; Zimbardo, 1965) or look up information to support the outcomes they believe their role requires (Betsch et al., 2001), as shown in a German study where participants assigned to the role of legal prosecutor were more likely to convict suspects than those who were assigned to the role of defense counselor (Engel & Glöckner, 2013). Consequently, formally certifying street-level bureaucrats as state servants may induce them to prefer standards they perceive as supporting their state-servant role, such as conforming to administrative opinions and adopting the administration’s narratives (Baumeister & Leary, 1995; Cialdini & Goldstein, 2004; Cohen & Gershgoren, 2019).

The stronger tendency of formally certified street-level bureaucrats to express state favoritism (Bolino et al., 2013), strengthened by their socialization (Moreland, 2006; Moyson et al., 2018), public professional accountability (Hupe & Hil, 2007), and potential role bias as state servants (Engel & Glöckner, 2013) may shift their attitude toward favoring the state. Consequently:

H1. Resolutions made by formally certified street-level bureaucrats will be less likely to reflect pro-citizen tendencies than resolutions made by those who are not formally certified.

Formal certification is postulated to be related to state favoritism in the resolutions of street-level bureaucrats. What effect will other types of public accreditation have on their use of discretion?

The Relationship between Street-Level Bureaucrats’ Public Organization Membership and Their Pro-State Tendencies in Their Resolutions

Public accreditation also can be obtained through membership in a public organization, indicating that the public organization deemed the individual competent enough to become a member. Such a form of public accreditation has the potential to compel street-level bureaucrats to adopt their public organization’s standards and develop feelings of (professional) accountability toward the organization and their peers within it (Hupe & Hill, 2007).

Peers are a major part of street-level bureaucrats’ social networks (Lotta & Marques, 2020), providing additional sources of learning (Foldy & Buckley, 2010) through the “collective schema” (Vinzant et al., 1998), occupational culture (Alcadipani et al., 2020), and attitudes they hold, including attitudes toward clients (Keulemans et al., 2020; Sandfort, 1999). Hence, it is widely accepted that public organizations change the opinions of their street-level bureaucrat members (Cohen & Gershgoren, 2016; Ottati et al., 2005) as well as those they hold toward outgroups (Davidovitz & Cohen, 2022a; Hughes et al., 2017). Peers’ normative influence, also known as peer pressure, is expected to diminish when members of the organization make decisions on their own outside of the organization; however, peer informative influence (Foldy & Buckley, 2010) may persist. If the convincing standards upheld by organizational peers are internalized (Vygotsky, 1980), they can influence resolutions made by street-level bureaucrats outside their public organization.

Finally, like the postulated influence of formal certification, membership in a public organization also may generate role-induced bias (Simon et al., 2008, 2009). Thus, street-level bureaucrats who are members of public organizations may prefer standards that they perceive as supporting their public-organizational role (Janis & King, 1954; Zimbardo, 1965).

Taking the preceding into consideration, if street-level bureaucrats are publicly accredited as members of public organizations, they may be more favorable to state arguments other state officials make. Consequently:

H2. Resolutions made by street-level bureaucrats who are members of a public organization will be likely to exhibit less pro-citizen tendencies than resolutions made by those who are not public organization members.

Methodology

The Context: Lower-Court Judges and Lay Adjudicators’ Rulings in Tax Disputes

The study looks at actual lower-court judges’ and lay adjudicators' rulings in Israeli Appreciation Tax and Acquisition Tax disputes as test cases for street-level bureaucrats’ resolutions. According to Lipsky’s (2010) definition, lower-court judges are street-level bureaucrats. This view has inspired the use of street-level bureaucracy theory in studies of U.K. district judges (Cowan & Hitchings, 2007), French and Canadian family court judges (Biland & Steinmetz, 2017), U.S. immigration judges (Jain, 2018), and Italian asylum judges (Dallara & Lacchei, 2021). We contend that uncertified lay adjudicators serving in decision teams alongside formally certified judges also fit the definition of street-level bureaucrats. Like their formally certified counterparts (and other street-level bureaucrats), they experience heavy workloads, enjoy considerable discretion and exercise it to manage their responsibilities. Possess a measure of expertise, handle their work in accordance with their own preferences, develop coping mechanisms to ease stress, and interact with their clients (litigants) on a regular basis in situations that vary in complexity.

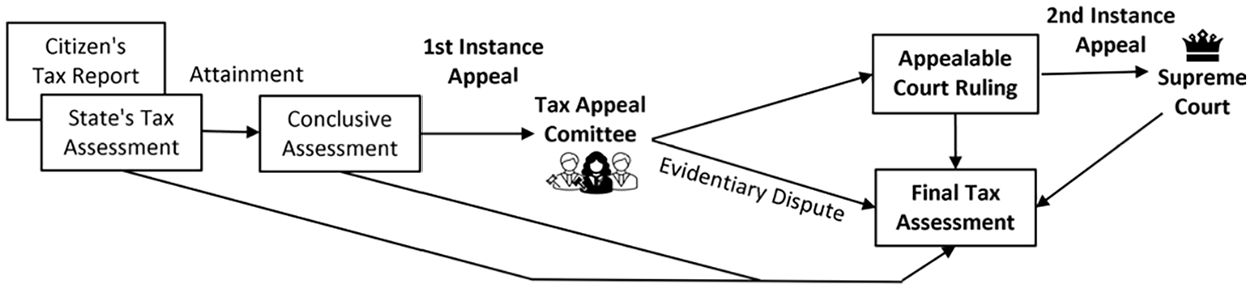

Resolutions made by both formally certified lower-court judges and uncertified lay adjudicators in Israel resolve first instance civil tax disputes between citizen taxpayers and the state treasury. 3 As Figure 1 shows, after a multistage process of tax reporting, evaluation, and negotiations, state officials working for the Israeli Tax Authority may decide to counter the taxpayer’s Appreciation Tax and Acquisition Tax reports by issuing the state’s conclusive tax assessment (Cohen & Gershgoren, 2019). Citizen taxpayers who decide to challenge the state’s conclusive assessment present their counterclaims before administrative tax appeal committees that have judicial authority limited to the determination of such tax disputes. 4 The tax appeal committees are composed of three members: a formally certified judge who is an active member of the district court where s/he also presides (hereafter, “Dual Judge”) or a formally certified judge who is not a member of the district court 5 (hereafter, “Committee Judge”), and two private individuals who are neither formally certified judges nor members of the district court (hereafter, “Lay Adjudicators”), one of whom usually is a private real-estate appraiser and the other a private accountant or lawyer. 6

Israeli appreciation tax and acquisition tax dispute system.

At trial, the judges and lay adjudicators assigned to the case elicit information from the parties; after hearing their claims, a separate ruling is recorded by each committee member for each tax dispute the case entails. If their decision is not unanimous, the tax dispute is resolved in accordance with the majority opinion. Should a case involve multiple claimants with similar tax disputes, one ruling may resolve them all. 7

According to Israeli jurisprudence, only rulings resolving normative disputes (that is, addressing questions of law) can be appealed to the Supreme Court. 8 Therefore, based on the arguments detailed in the state’s tax assessment and the taxpayers’ counterclaims, the tax committee members know in advance whether the ruling they will make potentially could be appealed to the Supreme Court.

Extra-Legal Factors

Judicial theory postulates extra-legal factors that may influence lower-court judges’ decision making (Rachlinski & Wistrich, 2017). Some of these factors, such as the deciders’ gender (Oren-Kolbinger, 2018; Steffensmeier & Hebert, 1999), age (Fox & Van Sickel, 2000; Manning et al., 2004), claimant type (an individual or a corporation; Gliksberg, 2015), the number of claimants, and the number of tax disputes in each case were included in the models used to test the research hypotheses.

Other extra-legal factors, such as the deciders’ political ideology, electoral accountability, race, and religion, are not relevant to the examined context. Israeli lower court judges are not elected to office but rather formally certified by an independent committee (Basic Law: The Judiciary). Likewise, tax appeal committee members (i.e., judges and lay adjudicators) are appointed periodically by the Minister of Justice, and almost all of those included in the data panel shared the same race and religion. 9

Furthermore, it is important to note that between 1995 and 2006, the discretionary space governing Israeli courts’ use of legal interpretations when filling gaps in judicial norms (Barak, 1989) was dramatically extended (Posner, 2007). Since then, the Supreme Court has allowed court rulings to be based on flexible legal terms, such as “reasonableness,” “balance of values,” and “purpose” (Kedar, 2002; Salzberger, 2007).

These various factors were used to filter the data and as control variables in the statistical analysis that follows.

Quantitative Data, Filtering, and Coding

The data were gathered from two public databases: the MISIM Taxes-Online database (“the MISIM database”) and the Israeli Judicial Authority’s Public Archive. The MISIM database is the main source of professional information for Israeli tax practitioners holding detailed rulings in tax cases. The Judicial Authority’s Public Archive is managed by the state and contains the curriculum vitae of formally certified judges, including their date of birth and year of appointment.

From the cases involving Appreciation Tax and Acquisition Tax disputes included in the MISIM database, only those addressed by tax appeal committees during the 15 years since 2005 were chosen. This was done to reduce heterogeneity (Keele, 2015), centering on rulings made within extended discretionary space (Salzberger, 2007) because, as past research suggests, discretionary space relates to Israeli lower-court judges’ pro-citizen tendencies in their rulings (Gershgoren & Cohen, 2023a).

All 475 cases were analyzed to construct a novel database that contained managerial decisions and detailed rulings for each of the 505 tax disputes that these cases entailed. The parameters coded for each tax dispute include the legal reference number of the case; the date the tax disputes it contained were resolved; the nature of each resolution (whether a managerial decision, an appealable ruling, or a final ruling); the winning party; the number of claimants involved; the number of tax disputes presented in the same case; the claimant type (whether a corporation or an individual); and the name of the judge or lay adjudicator. Using information from the Judicial Archive, the formally certified judges’ age and seniority at the time of their rulings were added. 10

After finalizing the collection and coding, 65 managerial decisions (e.g., granting statute of limitations, permission to join new claims or setting of court fees) were discarded, as these are part of the dispute determination process (Kim, 2007) and do not address the core arguments detailed in the contested state’s tax assessment and in the taxpayers’ counterclaims. Furthermore, 194 unappealable rulings were set aside, as the potential appealability of the resolution might influence the decider’s use of discretion (Gershgoren & Cohen, 2023a; Klein & Hume, 2003). 11 Such rulings were used for robustness testing of the main statistical model.

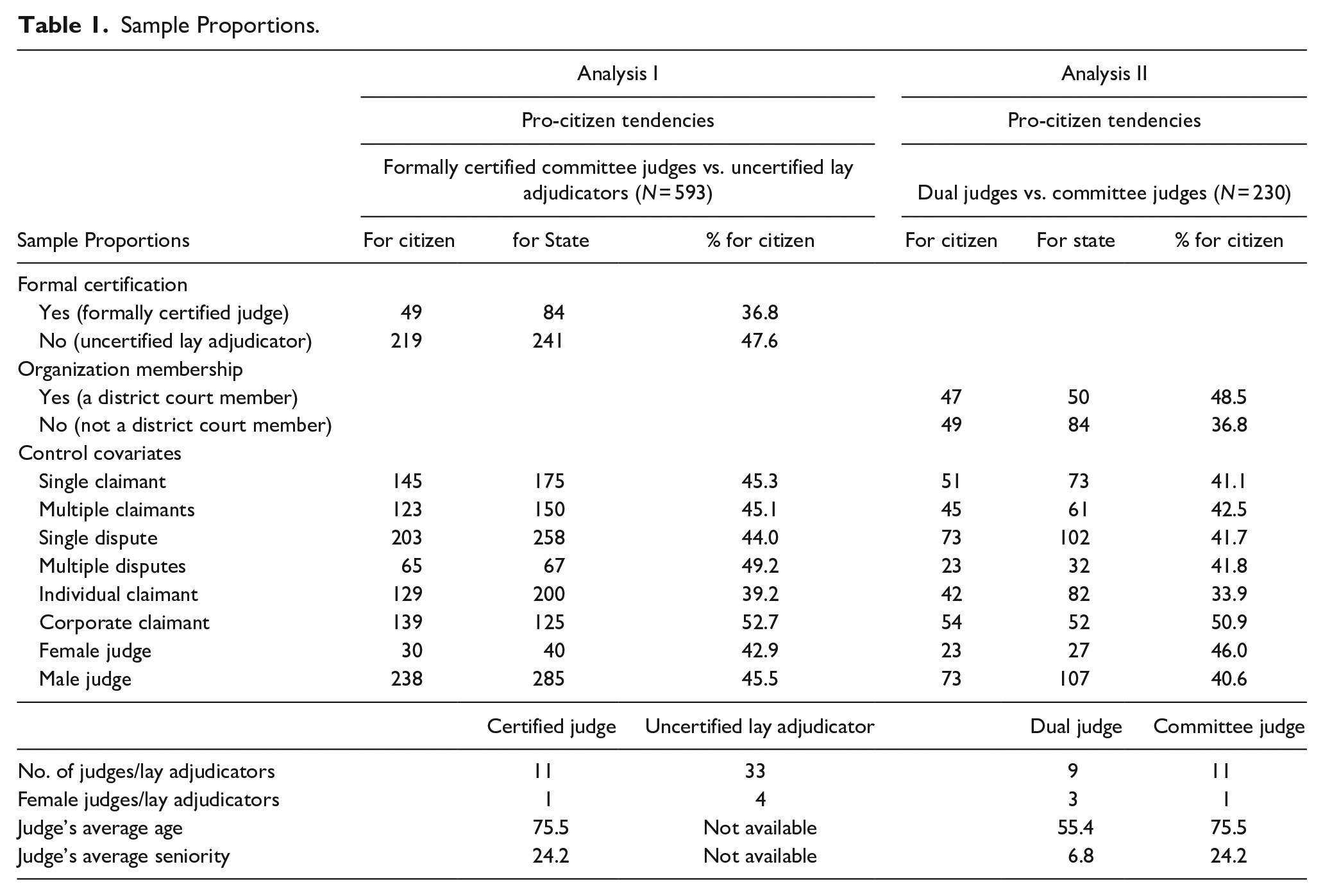

The filtered and coded data panel included 738 rulings (addressing 246 tax disputes), dual judges made 103 rulings, committee judges 143, and lay adjudicators 492.

Of these, 48 partial rulings that neither fully accepted nor fully rejected the citizens’ claims (10 made by committee judges and 32 by lay adjudicators) were set aside to be used for robustness testing of the main statistical model. The final data panel includes conclusive rulings that either fully accepted or fully rejected the citizens’ claims. Of these rulings, dual judges made 97, committee judges 133, and lay adjudicators 460. (Coding reliability measures are detailed in Appendix A.)

Models and Variables

Hypothesis H1 was tested by comparing the 133 rulings that formally certified committee judges made to the 460 rulings of uncertified lay adjudicators (N = 593). The 97 rulings made by dual judges were excluded from this analysis to control for the potential influence of the dual judges’ membership in the district court (a public organization)—as postulated in Hypothesis H2. [H2 is tested by comparing those 97 rulings to the 133 rulings made by committee judges who are not members of the district court (N = 230).]

Given that the dependent variable is binary, a logistic regression was used with each of the following specifications 12 . Analysis I tests Hypothesis H1, and Analysis II tests Hypothesis H2:

Analysis I:

Analysis II:

The models predict

Formal certification is the binary independent variable for Analysis I (used for testing Hypothesis H1). It was set to 1 when the ruling was made by a formally certified committee judge and to 0 when it was made by an uncertified lay adjudicator.

Organization membership is the binary independent variable for Analysis II (for testing Hypothesis H2). It was set to 1 when the ruling was made by a dual judge who is a member of the district court and to 0 when made by a committee judge who has retired from the district court.

The errors

Data Analysis Tools

The data were analyzed using R (version 4.0.1) software with the glmmTMB software package (Brooks et al., 2017) and the Excel XLMiner add-in.

Findings

Sample Proportions and Cross-Correlations

Table 1 details sample proportions and pro-citizen tendency rates, comparing conclusive rulings that either fully accepted or fully rejected the citizens’ claims formally certified committee judges made to those made by lay adjudicators who are not formally certified judges (Analysis I). It also presents comparisons of conclusive rulings made in such committees by (formally certified) dual judges who also are members of the district court (a public organization) to those made by (formally certified) committee judges who resigned their membership in the district court (Analysis II).

Sample Proportions.

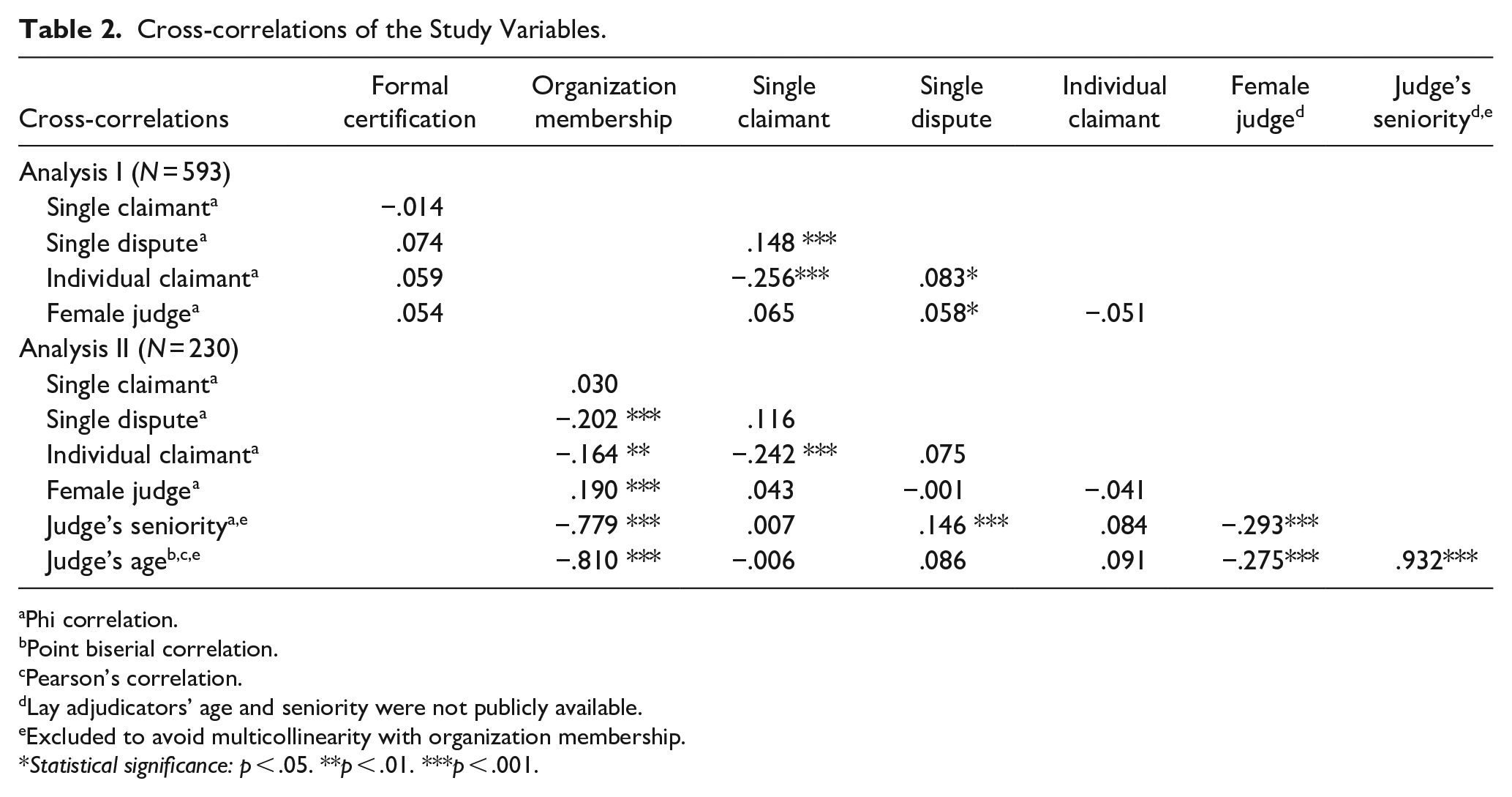

Table 2 presents bivariate correlations between all variables and covariates. As the Table shows, in Analysis II, the relationships between judges’ seniority and age and organization membership are statistically significant and strong; we excluded them from Analysis II to avoid multicollinearity. The remaining variables and covariates display negligible collinearity of 0.256 or less, within accepted limits (Coakes, 2005).

Cross-correlations of the Study Variables.

Phi correlation.

Point biserial correlation.

Pearson’s correlation.

Lay adjudicators’ age and seniority were not publicly available.

Excluded to avoid multicollinearity with organization membership.

Statistical significance: p < .05. **p < .01. ***p < .001.

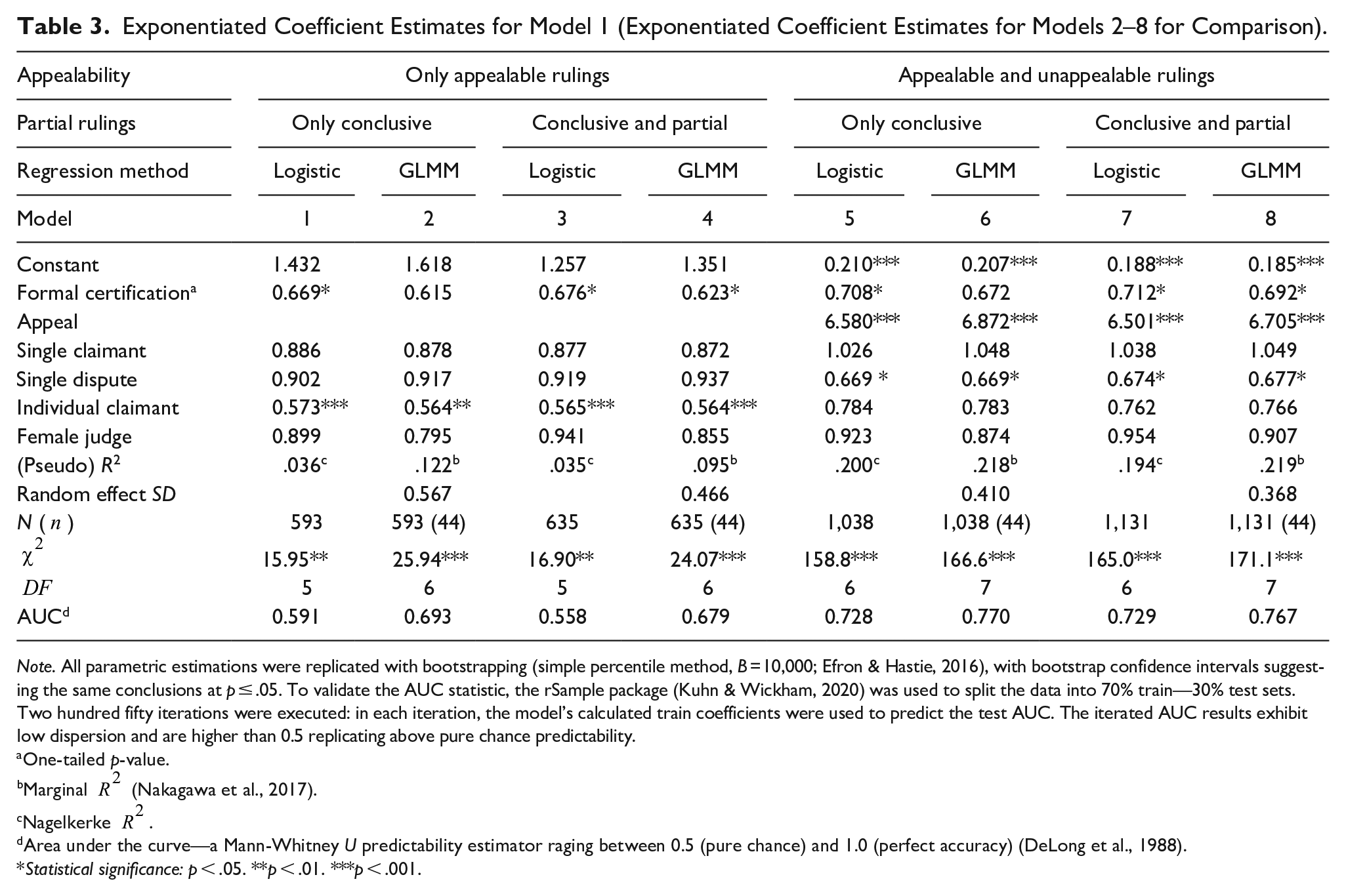

Analysis I: Logistic Regression

Model 1, the main model used for Analysis I in testing Hypothesis H1, is a logistic regression that examines conclusive rulings that either fully accepted the citizen’s claims or fully rejected them. To ensure the statistical robustness of Model 1, seven comparison models were fitted. Comparison Models 2, 4, 6, and 8 apply a generalized statistical mixed model (GLMM): a logistic regression with a random intercept (Brooks et al., 2017) that considers the possible dependencies between rulings made by the same lower court judge or lay adjudicator, using the decider’s name as an intercept. Comparison Models 3, 4, 7, and 8 add partial rulings (that neither accepted nor rejected the citizens’ claims) that were not included in Models 1, 2, 5, and 6, conservatively marked as fully rejecting citizens’ claims.

14

Moreover, in Models 5 to 8 the unappealable rulings that were discarded from Models 1 to 4 were added, tapped by the binary independent variable Appealability (1 when ruling could be appealed to the Supreme Court. 0 when unappealable). Table 3 details the exponentiated coefficient estimates (

Exponentiated Coefficient Estimates for Model 1 (Exponentiated Coefficient Estimates for Models 2–8 for Comparison).

Note. All parametric estimations were replicated with bootstrapping (simple percentile method, B = 10,000; Efron & Hastie, 2016), with bootstrap confidence intervals suggesting the same conclusions at p ≤ .05. To validate the AUC statistic, the rSample package (Kuhn & Wickham, 2020) was used to split the data into 70% train—30% test sets. Two hundred fifty iterations were executed: in each iteration, the model’s calculated train coefficients were used to predict the test AUC. The iterated AUC results exhibit low dispersion and are higher than 0.5 replicating above pure chance predictability.

One-tailed p-value.

Marginal

Nagelkerke

Area under the curve—a Mann-Whitney U predictability estimator raging between 0.5 (pure chance) and 1.0 (perfect accuracy) (DeLong et al., 1988).

Statistical significance: p < .05. **p < .01. ***p < .001.

In Model 1, the exponentiated coefficient estimate for formal certification is statistically significant and less than one, indicating that formally certified committee judges display less pro-citizen tendencies than their uncertified lay adjudicator counterparts, supporting Hypothesis H1.

The exponentiated coefficient estimate for formal certification is statistically significant in Models 3, 4, 5, 7, and 8, also supporting Hypothesis H1.

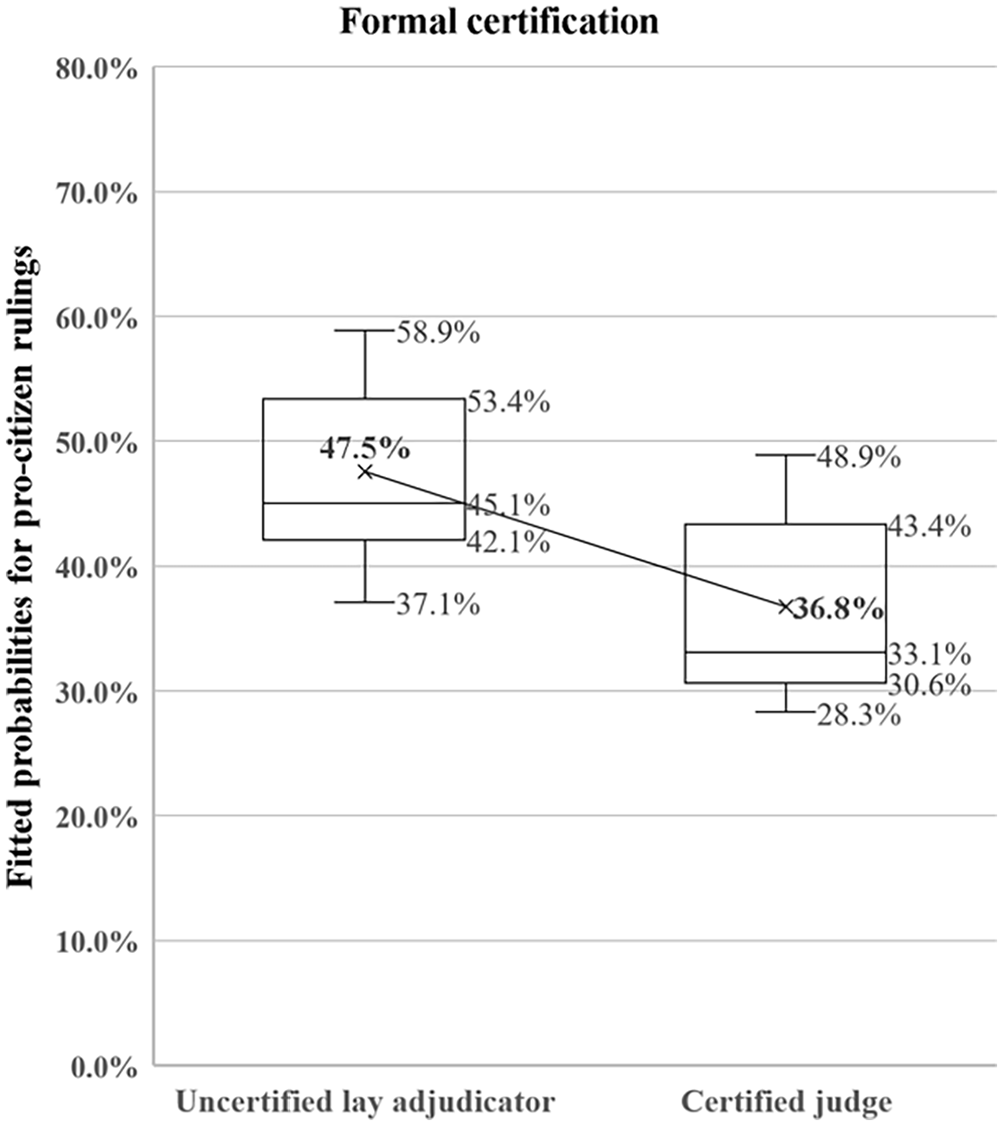

Figure 2 shows the fitted probabilities of pro-citizen rulings (means, full, and interquartile ranges, and medians), based on Model 1 for rulings made in tax appeal committees by formally certified committee judges and uncertified lay adjudicators. As shown, the average fitted probability of rulings being pro-citizen when made by formally certified judges (36.8%) is 10.7% lower than the average of those made by uncertified lay adjudicators (47.5%), again supporting hypothesis H1.

Fitted probabilities of pro-citizen rulings.

Analysis II: Inconclusive Results

Despite using records gathered over 15 years (between 2005 and 2021) that included all relevant publicly available rulings made by committee judges and dual judges in tax appeal committees, we were unable to statistically confirm or reject Hypothesis H2. Given a calculated odds-ratio (OR) of 1.61, a Prx of 0.42 (the portion of the compared group’s sample from the total data panel), a Pry of 0.37 (the compared group’s success rate), and a confidence level of 0.05 (one-tailed), a statistical-power analysis (Demidenko, 2007) of the limited data scope (N = 230) indicates that only extreme mean differences of 58% (or more) between the compared groups could be evaluated; hence, additional data are required to support more subtle mean differences. 15 Furthermore, the high collinearity (detailed in Table 2) between the judges’ age, seniority, and public organization membership as well as the statistically significant difference between committee judges’ average age and seniority (75.5 and 24.2) and the average age and seniority of dual judges (55.4 and 6.8) suggest that the committee judges’ long tenure on the district court may continue to impact their pro-state tendencies even after retirement.

Indeed, none of the statistical examinations used for Analysis II was statistically significant, suggesting no evidence for a mean difference (of 58% or more) between committee judges and dual judges average pro-citizen tendencies. Therefore, based on the present limited scope of empirical data, Hypothesis H2 cannot be sustained or rejected (below a mean difference threshold of 58% that was not indicated using the limited data). 16

Discussion

The goal of the study was to examine potential relationships between public accreditation via formal certification and membership in public organizations and pro-citizen or pro-state tendencies in resolutions made by street-level bureaucrats. Focusing on their use of discretion in resolving disputes between citizens and other state officials, the findings show that formally certified lower-court judges were significantly more likely than their uncertified lay adjudicator counterparts to reject citizens’ claims that contested the state’s arguments in tax disputes. The results indicate that resolutions made by formally certified street-level bureaucrats are less likely to reflect pro-citizen tendencies than resolutions made by those who are not formally certified (confirming Hypothesis H1). Alas, based on the present limited scope of empirical data and due to low statistical power (Demidenko, 2007), the prediction that street-level bureaucrats who are members of public organizations tend to favor the state in their resolutions more than those who are not, could not be supported or rejected.

Relying on all publicly available Israeli court rulings in Appreciation Tax and Acquisition Tax disputes between 2005 and 2021 and adopting the scholarly view of lower-court judges as street-level bureaucrats (Biland & Steinmetz, 2017; Cowan & Hitchings, 2007; Dallara & Lacchei, 2021; Jain, 2018; Lipsky, 2010), the findings provide a more nuanced picture of how discretion is used in making street-level resolutions. They contribute to previous knowledge in two ways: first, the findings demonstrate, both theoretically and empirically, the unfavorable effect that public accreditation (via formal certification) may have on the use of discretion by street-level bureaucrats, which can result in a systematic bias toward accepting the state’s arguments and rejecting the citizens’ counterclaims in their resolutions. Policymakers and street-level managers should consider such outcomes in order to reduce the risk of undermining procedural fairness that can erode public trust in government (Edri-Peer & Cohen, 2023; Mazepus & van Leeuwen, 2020).

Second, the findings improve understanding of the dual role street-level bureaucrats play as citizen or state agents. While some scholars suggest that street-level bureaucrats should be committed to the state (Brehm & Gates, 1997) and serve citizens on its behalf, other scholars adopt the “professional-agency narrative” (Cecchini & Harrits, 2022) suggest that street-level bureaucrats solve problems using their practical and professional knowledge of “what works.” The findings here suggest that public accreditation (through formal certification) of street-level bureaucrats may bring state-oriented favoritism to their resolutions.

The findings highlight normative consideration of the part that public accreditation and especially formal certification of street-level bureaucrats plays in public policy implementation and governance. The analysis points to the need to account for potential anti-citizen tendencies in resolutions made by front-line civil servants who are formally certified. Policymakers and street-level managers should be aware that the (often unavoidable) formal certification of street-level bureaucrats may compel these front-line workers to favor the state over its citizens in their resolutions.

If procedural fairness is to be maintained, policymakers should consider devising methods to promote attention to citizen perspectives and counterbalance pro-state tendencies in street-level resolutions. Such methods could include specific administrative regulations, vocational training for formally certified personnel, or the promotion of citizens’ participation in administrative decision-making (Bennett et al., 2022; Gershgoren & Cohen, 2023b) by incorporating citizens and formally certified street-level bureaucrats in mixed administrative decision forums.

Limitations and Future Research

Notwithstanding its contributions, the study has limitations that open avenues for future research. The main limitation stems from the decision to restrict the surveyed data to actual court rulings made in tax appeal committees by lower-court judges and lay adjudicators. Future research should employ comparative analysis to validate the model, using additional types of resolutions and other types of street-level bureaucrats and including factors such as the street-level bureaucrats’ political ideology, electoral accountability, race, and religion, and the claimants’ trustworthiness (Davidovitz & Cohen, 2022b), race (Maranto et al., 2024), or social group (Raaphorst & Groeneveld, 2018) that could not be extracted from the public data used here. Furthermore, the disputes surveyed involved payments that citizens are obliged to make to the state. The results might have differed had they involved payments the state is obliged to pay to its citizens, such as public subsidies or governmental grants. Additionally, the study was conducted in Israel. Research carried out in different settings would contribute to the growth of additional knowledge. Finally, since “real-world” data were used, the study did not benefit from the more controlled conditions of a lab.

Conclusion

The study’s findings contribute to the field by underscoring the important role that public accreditation plays in shaping street-level bureaucrats’ use of discretion. As we expected, formally certified street-level bureaucrats were more likely to favor the state in their resolutions that settled disputes between the state and its citizens. Such outcomes, if not accounted for, may undermine procedural fairness and erode public trust in government.

We urge policymakers and street-level managers to consider these findings, and we hope they encourage further studies that will broaden the understanding, both theoretically and empirically, of what motivates street-level bureaucrats’ pro-citizen or pro-state tendencies. The study may also encourage further use of publicly available data in assessing how discretion is used by those serving on the frontlines of public administration.

Footnotes

Appendix A: Coding Reliability Measures

The study relied on all actual data that were available (Pollitt, 2017). This reduced common source bias (Favero & Bullock, 2015). Yet, there might be other biases, such as the researchers’ halo effect (Viswesvaran et al., 2005) in the categorization of the tax disputes as managerial, appealable, or final. To reduce such risks, the MISIM database was used to verify that the rulings that were categorized as final had not been appealed to the Supreme Court. In addition, a team of five Israeli tax experts, consisting of two tax lawyers, two accountants, and a former tax assessor analyzed 10% of the original cases to validate the inter-rater reliability of the categorization scheme. The examiners were asked to independently evaluate the cases, categorize the tax disputes they identified, and code each of the rulings therein. The resulting inter-rater reliability scores were all greater than 0.9, indicating almost perfect agreement.

Acknowledgements

We are grateful to the Editor, Karen Hult, and to the anonymous reviewers of this manuscript for their insightful comments. We would also like to acknowledge the support of the Research Fund of the Open University of Israel.

Data Availability Statement

The datasets generated during and/or analyzed for the current study are not publicly available due to anonymity and data sharing conditions under the ethical guidelines on which this study was conducted. They are available from the corresponding author on reasonable request.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.