Abstract

The impact of the pandemic has diminished, and while it is still present, it no longer causes the same degree of societal disruption as before. The nature of this disruption has also shifted. Considering the psychosocial and economic disruption triggered by COVID-19, this study explores the adverse financial consequences of COVID-19 restrictions and its mental health impact on household heads. The study employed a quantitative cross-sectional survey research design. A questionnaire was distributed to a nationally representative sample of individuals (N = 1580) through computer-assisted telephone interviewing and self-completion. From this dataset, 550 household heads who were employed before the implementation of COVID-19 regulations were selected for inclusion in this study. Findings reveal that while there were no discernible gender differences in terms of financial distress experienced during COVID-19, females were more prone to psychological distress compared to males during this period. These results offer insights into gender disparities concerning the mental health and economic repercussions of COVID-19. Policy initiatives and interventions should consciously address the specific needs of females, aiming not only to mitigate the current pandemic’s impact but also to fortify resilience against potential future crises.

Introduction

The coronavirus pandemic (COVID-19) has taken an overwhelming toll on the world’s population, with economic and social impacts continuing to reverberate globally as the pandemic recedes (World Bank, 2022a). In the wake of the COVID-19 outbreak, the world economy was jolted into the largest recession in over a century, resulting in a dramatic upsurge in inequality within and between countries (World Bank, 2022b), which continues to be felt in the aftermath of the pandemic. Similarly, there have been significant economic and psychosocial consequences due to the COVID-19 pandemic on the South African population. As a result, large and unequal impacts have been felt within and across the country. While lockdowns were implemented worldwide to curb the virus, studies internationally, including in South Africa, have documented the detrimental influence of the pandemic on the mental health of the world’s population, especially among the more vulnerable (Kim et al., 2020; Naidu, 2020).

Both global and local research studies have revealed the adverse impact on psychological well-being caused by the COVID-19 pandemic and the ensuing economic downturn (Gong et al., 2022; Holmes et al., 2020; Stevensen & Wakefield, 2021). During the pandemic, individuals experienced significant setbacks in accessing economic resources due to widespread unemployment, which may have contributed to higher levels of depressive symptoms among adults during the initial phases of the pandemic (Oyenubi & Kollamparambil, 2020). Individuals further commonly experience mental health issues and health sequelae such as frustration, acute stress, anxiety, depression, post-traumatic stress disorder (PTSD), insomnia and suicidal behaviours (Alqahtani et al., 2022; Gong et al., 2022). In addition, individuals from marginalised communities were at a higher risk of encountering stressors and exhibited greater vulnerability to stress, given their constrained access to psychosocial coping resources (Ryu & Fan, 2023). To some extent, these effects stem from shifts in employment patterns and financial strain (Gong et al., 2022; Stevensen & Wakefield, 2021). It is thus critical to mitigate both short- and long-term negative effects of psychological distress within these marginalised contexts that are plagued by structural impediments.

Furthermore, the pandemic has brought to the fore the long-standing structural determinants of health inequities, such as precarious employment conditions, growing economic disparities, high unemployment rates, and anti-democratic political institutions and processes (Nwosu & Oyenubi, 2021; Paremoer et al., 2021; Posel & Hall, 2021). Paremoer and colleagues (2021) argue that the pandemic particularly drew attention to the role of precarious work, exploitative working conditions, migrant status, class, and gender in determining who was most susceptible to being negatively impacted by COVID-19 (i.e., financial difficulties, income loss, emotional distress). These social vulnerabilities have been exacerbated at both a community and societal level as these drivers of health intersect with status, ethnicity, gender, and education level during this period. The disproportionate economic impact of the COVID-19 pandemic on individuals from marginalised backgrounds, as well as other vulnerable groups such as women, has been driven by these structural determinants (Chaudhury & Banerjee, 2020; Tsai et al., 2017). These individuals inevitably have limited access to health services, basic amenities and services, and their low income hampers their ability to afford adequate food, let alone benefits such as taking sick leave (Macleod et al., 2021; Statistics South Africa, 2020).

According to Carli (2020), females have experienced a higher job loss rate than males. Females have also been disproportionately represented in essential roles that expose them to both infection and psychological stress. Females faced an increase in household chores and childcare responsibilities during the pandemic, which resulted in females experiencing higher levels of psychological distress compared to males (Borrescio-Higa & Valenzuela, 2021; Xue & McMunn, 2021). In addition, they were also at a higher risk of losing their jobs or suffering income reductions compared to men. Research conducted by Etheridge and Spantig (2022), Hwang and Shin (2023), and Mudiriza and De Lannoy (2020) indicate that the loss of employment or income can have adverse effects on mental health, particularly affecting females and young individuals.

Considering the potential adverse outcomes resulting from increasing financial strains and unemployment, particularly for vulnerable groups such as females, it is essential to grasp the specific responsibilities and roles that females undertake within the household. In recent decades, because of social, structural, and economic changes, the increasing experience of poverty by females has been accompanied by a growth in the number of female-headed households (Milazzo & Van de Walle, 2017). According to Goldscheider et al. (2015), females seem more likely than males to be named the household head. As a result, these female-headed households are more economically vulnerable than their male counterparts (Chant, 2006).

The high rates of unemployment in South Africa also disproportionately affect females more. Females are more disadvantaged and experience higher unemployment rates as opposed to males (Casale et al., 2021). Posel et al. (2023) further contend that poorer outcomes for females in the workplace (and more unpaid care work) contribute to higher rates of poverty in female-headed households. In addition, females’ increasing share of poverty is related to the rising incidence of single-mother households (Posel et al., 2023; Posel & Hall, 2021). Most children living in households without both their parents (Posel & Hall, 2021) are more likely to live with their mother than their father. Consequently, females often take on the double role of primary physical caregivers and primary financial providers for their children, thus the potential for greater vulnerability (Hatch & Posel, 2018).

South Africa provides a unique backdrop to assess the association between the financial consequences of COVID-19 and psychosocial distress, particularly by gender. The country is plagued by high levels of unemployment, poverty, and inequality, which were exacerbated during the pandemic (Simon & Khambule, 2021), and records among the highest inequalities in the world, where around 20% of the population lives in poverty (World Bank, 2022b). South Africa further enforced one of the most stringent COVID-19 lockdown regulations globally (Greyling et al., 2021). As a result of the ‘hard’ lockdown and suspension of economic activity, between 2.2 and 2.8 million South African adults lost their jobs (Casale et al., 2021; Jain et al., 2020; Statistics South Africa, 2020). Poorer households, with less education, black, 1 and female, were disproportionately affected by job or income losses (Casale & Posel, 2020; Simon & Khambule, 2021; United Nations Development Programme, South Africa, 2020).

This trend of increasing inequality in living standards between males and females due to the widening gender gap in poverty is referred to as the feminisation of poverty. This phenomenon largely links to how females and children are disproportionately represented within the lower socioeconomic status community in comparison to males within the same socioeconomic status. This is corroborated by Chant (2006), who postulates that several factors contribute to prevailing perceptions of the feminisation of poverty, for example, inequalities in rights, entitlements, and feminisation of labour. A lack of income does not solely contribute to the causes of feminisation of poverty. However, it is also a result of the deprivation of choices and opportunities as well as the gender biases within societies and governments females face.

Accordingly, the current study aims to explore the adverse financial impact of the COVID-19 pandemic on the mental health of household heads. It further explores the gendered impact of the pandemic as related to financial distress and mental health. Household heads are typically responsible for the financial running of the household, and thus, should they lose their jobs or income, the negative impact will be greater than for those who do not have such responsibilities. Most households are headed by the oldest person in the household, and headship is strongly associated with the highest income earner (Posel, 2001). The burden of responsibility for the household typically falls on the head, and thus the loss of income may be more anxiety-provoking because of their responsibility. The burden of responsibility is particularly acute in female-headed households (Posel, 2001). Generally, the household head is responsible mainly for the household’s economic well-being, and females have a disadvantage when it comes to gaining access to society’s economic resources (Posel & Casale, 2018). In addition, recognising the necessity to prioritise mental health interventions in pandemic policy responses (Nguse & Wassenaar, 2021; Posel et al., 2021), effective policy development requires understanding the correlation between the pandemic’s financial impact and mental health outcomes. It is thus important to explore the adverse financial consequences of COVID-19 restrictions and its mental health impact on household heads.

Methodology

Design

The study employed a cross-sectional survey research design. A cross-sectional survey provides a snapshot of a population’s characteristics and the country’s status at a particular time (Babbie, 2016).

Participants and procedure

This study forms part of a broader study investigating the social, economic and psychological impacts of the COVID-19 pandemic in South Africa. South Africa was experiencing the second wave of the COVID-19 pandemic at this time, with the result that lockdown measures were more restrictive. Data for this study were collected from December 2020 to March 2021 by administering a national COVID-19 survey. The survey was conducted via computer-assisted telephone interviewing (CATI), with households situated in both urban and rural areas across South Africa. Before conducting the interview, each respondent provided verbal informed consent. For each province, the relative sample sizes were adjusted to ensure that each sub-cluster population consisted of a minimum of 30 respondents to adequately cover the towns and villages representing urban and rural areas.

A stratified random sample of 2118 adults (81% response rate) aged 18 years and older were recruited using the number of households in each province as a weighting factor. Following the elimination of cases with missing values, the nationally proportionate sample included 1580 respondents recruited via the CATI platform. Out of the 1580 respondents, we extracted data on 550 household heads who had been employed prior to the enforcement of COVID-19 regulations. These individuals constitute the sample for the present study.

Data-collection instrument

The national COVID-19 survey was developed by the Institute for Social and Health Sciences to collect information on perceptions of the pandemic and the related restrictions, socioeconomic status, and the financial and psychological impact of COVID-19. The questionnaire comprises 73 items assessing 11 domains (Swart et al., 2022; Taliep et al., 2023). Internally, a team of six researchers assessed the questionnaire for face validity. Subsequently, the survey underwent a review by the Bureau of Market Research (BMR), the organisation contracted to collect the data, to ensure alignment with study objectives, appropriate wording, smooth flow, and suitable duration. A pilot study was conducted in Gauteng, covering a span of 3 days, involving 20 respondents aged 18 and above, to evaluate the feasibility of the survey using the CATI method.

Outcome and explanatory variables

The outcome variable for the study was psychological distress. Psychological distress was measured on a scale consisting of six items, each prepositioned with ‘In the last seven days, how often have you . . .’. Each item asked about a specific emotive or behavioural state, consisting of ‘felt anxious’, ‘felt sad’, ‘felt hopeless’, ‘felt isolated’, ‘felt angry’, and ‘had trouble sleeping’. Responses were rated on a 3-point frequency scale ranging from ‘rarely or none of the time (less than one day)’ to ‘most or all of the time (5–7 days)’. The scale constructed was measured by creating the mean score for each participant out of three, with a higher score indicating more psychological distress.

Our explanatory variables included sociodemographic characteristics and the experience of financial distress. The sociodemographic variables included gender, age, education and household size. The gender variable was measured through two categories namely ‘Female’ and ‘Male’, where females were coded as 2 and males as 1, 2 with males indicated as the reference category for the multiple regression. Participant age was recorded on five-year intervals ranging from 18 years to 65 and older. Responses were grouped into 11 age categories, ‘18–19; 20–24; 25–29; 30–34; 35–39; 40–44; 45–49; 50–54; 55–59; 60–64; and 65 years and older’. Highest level of education was measured through nine categories ranging from ‘no schooling’ to ‘post-graduate degree completed’. Household size consisted of the number of household members.

The level of financial distress was measured in terms of financial insecurity and financial instability. Financial insecurity comprised two variables, ‘Poverty experienced during COVID-19’ and the ‘Percentage of income lost’. The variable ‘Poverty experienced during COVID-19’ comprised six items and was adapted from the Afrobarometer Lived Poverty Index (Bratton, 2006). The items asked how often, since the start of lockdown, the household experienced any of the following: ‘gone without enough food to eat’, ‘gone without enough clean water for home use’, ‘gone without medicines or medicinal treatment’, ‘gone without a cash income’, ‘gone without electricity’, and ‘gone without shelter’. Responses were recorded on a 5-point frequency scale ranging from ‘never’ to ‘always’, with a higher score indicating a greater prevalence of household poverty. The ‘Percentage of income lost’ variable measured the loss of household income since the start of the lockdown, and participants were asked to indicate how much of their total household income was lost during this period. Responses ranged in quartiles from ‘0% lost’ to ‘100% lost’.

Financial instability consisted of three variables, each prepositioned with ‘Since the beginning of the lockdown, have you done any of the following’. Each variable asked about a specific financial behaviour, that is, the accessing of savings, meeting bill payments and the borrowing of money. Responses were dichotomous with ‘yes’ coded as 2 and ‘no’ options coded as 1.

Data analyses

The data analysis was conducted using the IBM Statistical Package for Social Sciences for Windows (v.28) (IBM Corp., Armonk, NY, USA). Descriptive statistics including percentages and means were computed to describe the study variables. Chi-square and t-tests were used to assess differences between males and females. In addition, multivariate linear regression was utilised to examine the associations between the explanatory variables (sociodemographic and adverse financial experiences) and the dependent variable (psychological distress) among employed household heads during COVID-19. A significance level of p = .05 was applied to all statistical tests, while the 95% confidence interval (CI) was applied to all regression parameter estimates.

Ethical considerations

Ethical clearance for this study was obtained from the Unisa College of Human Sciences and Research Ethics Committee in 2020.

Results

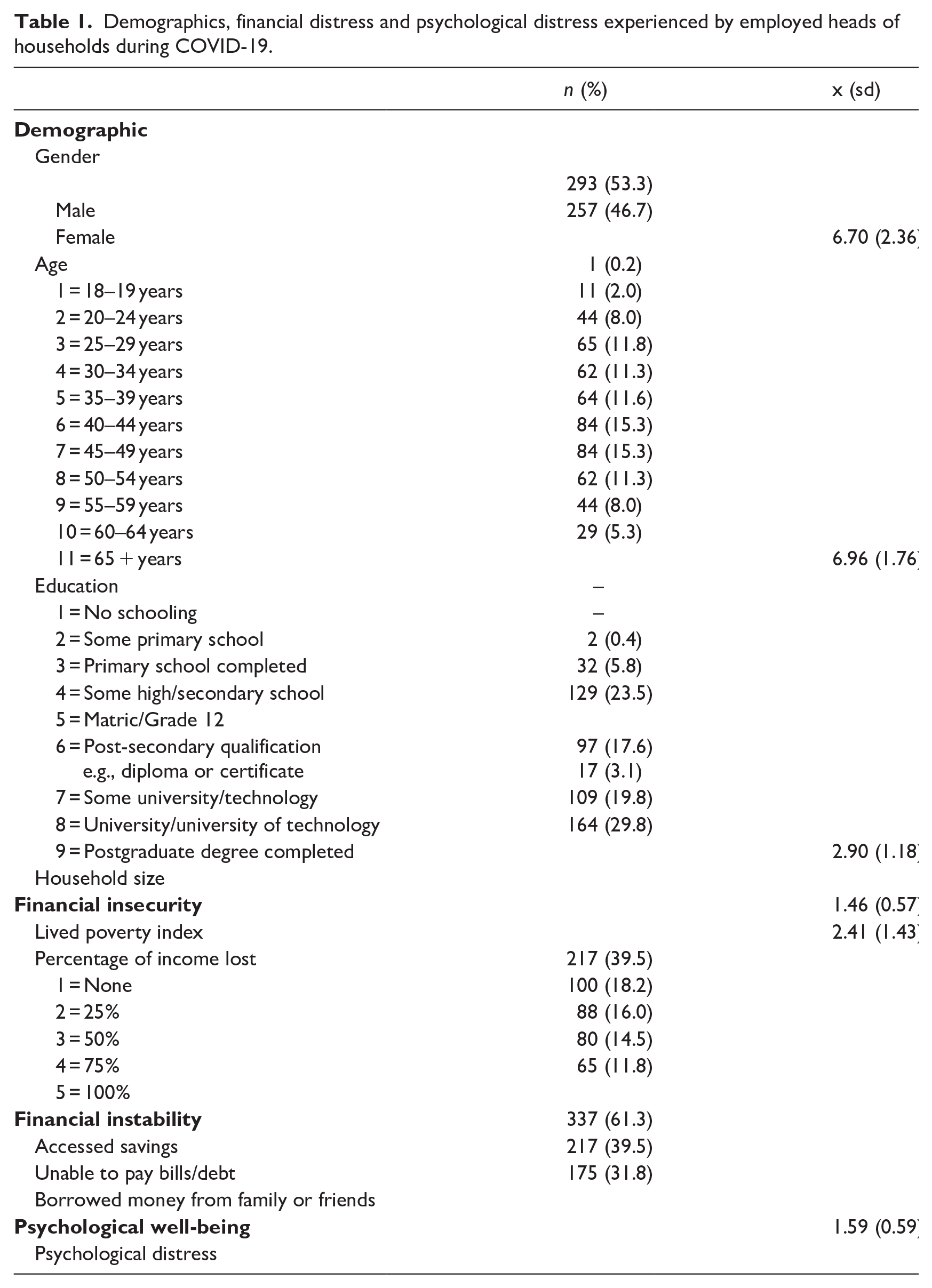

The sociodemographic, financial experiences, and psychological distress characteristics of the sample are presented in Table 1. The sample was predominantly male (53.3%), with an average age of 40–44 years. Most participants held a post-secondary qualification or higher (70.3%) and resided in households with an average size of about three members.

Demographics, financial distress and psychological distress experienced by employed heads of households during COVID-19.

Concerning financial insecurity, the mean score of 1.46 for the lived poverty index indicates that, on average, respondents’ households had never or just once or twice gone without food, water, medicine, medical treatment, electricity, or shelter since the implementation of the lockdown, and approximately 60.5% having lost some or all their income. Regarding financial instability, 61.3% of the household heads had accessed their savings, 39.5% could not pay their bills, and 31.8% borrowed money from family or friends. A mean score of 1.59 for psychological distress indicates that, on average, respondents occasionally or moderately felt anxious, sad, hopeless, isolated, angry, or had trouble sleeping over the past 7 days.

Table 2 reflects the gendered comparison of demographics, financial distress and psychological distress experienced by heads of households during COVID-19. The findings indicate that males were significantly more likely to possess higher levels of education (i.e., some university education) than females, who were more likely to have post-secondary education (t = −3.572, df = 548, p < .001). There were no significant differences between males and females with respect to age and size of household. Concerning financial distress, there were no differences between males and females regarding poverty experienced during COVID-19, percentage of income lost, being unable to pay bills or debt, or having borrowed money from family or friends. However, males were significantly more likely (65.2%) than females (56.8%) to have accessed savings (χ2 = 10.713, df = 1, p = .001). Females were also significantly more likely to have experienced psychological distress than males (x̄ = 1.68 vs x̄ = 1.51) (t = 3.282, df = 548, p < .001) during this period.

Gendered comparison of demographics, financial distress and psychological distress.

Table 3 represents the influence of demographics and financial distress on the mental health status of heads of households during COVID-19. A multilinear regression modelling was performed sequentially, generating and testing two models with new explanatory variables entered at both stages of progression, resulting in a single set of results. In the first model (Table 3), we looked at the sociodemographic characteristics of the household heads in terms of explaining psychological distress. The two variables, gender and education, were significantly related to psychological well-being. Females (compared to males) (β = 0.155, p = .002) and those with lower levels of education (β = −0.031, p = .032) were more likely to experience psychological distress.

Influence of demographics and financial distress on the mental health status of employed heads of households during COVID-19.

p < .001; **p < .01; *p < .05.

In the second model, we introduced five variables: lived poverty index and percentage of income lost, which relate to financial insecurity and accessed savings, unpaid bills, and borrowed money from family or friends, which is related to financial instability. In this model, the age and gender variables were significant, as were accessed savings and unpaid bills. Taken together, model 2 testing indicates that psychological distress increases among household heads who were (1) female (β = 0.156, p = .001), (2) older (β = 0.029, p = .004), (3) experienced greater poverty (β = 0.204, p = < 0.001), (4) accessed their savings (β = 0.101, p = .043), and (5) were unable to pay their bills or debt (β = 0.141, p = .013).

Table 4 presents the results of the multivariate linear regression of sociodemographic and financial distress on the mental health status of household heads, separately for males and females. For male heads of households, age, poverty, and accessed savings were significantly related to the experience of psychological distress. Male household heads who were older (β = 0.035, p = .018) experienced more significant levels of poverty (β = 0.181, p = .004), and accessed savings (β = 0.135, p = .002) reported greater levels of psychological distress. Among female heads of households, those who experienced greater levels of poverty (β = 0.241, p < 0.001) and were unable to pay bills (β = 0.245, p = .005) evidenced higher levels of psychological distress.

Gendered influence of demographics and financial distress on the mental health status of employed heads of households during COVID-19.

p < .001; **p < .01; *p < .05.

Discussion

Given the study’s emphasis on examining the adverse financial repercussions of COVID-19 alongside its mental health effects on household heads, the data primarily targeted this demographic. Household heads were singled out due to their perceived roles as primary decision-makers and providers within their households. Considering that their household’s welfare is among their top priorities, we postulated that any distress encountered within the household would directly impact them. We, therefore, specifically targeted household heads, as all variables related to financial distress were analysed at the household level. This approach acknowledges that such concerns would significantly influence the head of the household.

The data indicated that when the household suffered from financial distress (instability/insecurity), it negatively affected the psychological distress of the head of the household. These findings align with growing evidence that financial stresses and worries negatively impact the mental health of individuals (Asebedo & Wilmarth, 2017; Marshall et al., 2020). A study by Ryu and Fan (2023) confirms that psychological distress is positively and significantly associated with financial worries. Furthermore, several factors have been identified as contributing to poor mental health, including poverty, financial indebtedness, and borrowing of money (Marshall et al., 2020; Oyenubi & Kollamparambil, 2020; Sun, 2023). Results of this study revealed that individuals who were placed in the precarious position of having to access their savings had higher levels of psychological distress in contrast to individuals who were able to pay their accounts, experiencing less psychological distress. It can thus be deduced that regardless of whether individuals could pay their bills, if they needed to access their savings, their psychological stress levels increased. The converse was also true in that regardless of whether an individual was accessing their savings, if individuals could pay their bills, they experienced less psychological stress. It is, therefore, probable that individuals experiencing reduced psychological stress from bill payments either refrain from tapping into their savings or feel relieved about settling their bills while experiencing distress related to accessing their savings.

Regarding female levels of psychological distress, it was anticipated that the risk of psychological distress among females involved in unpaid work would increase during the pandemic due to heightened exposure to heavier and more stressful workloads (Seedat & Rondon, 2021). The results of this study show that during the pandemic, females experienced higher levels of psychological distress as opposed to males regardless of levels of financial distress. The literature echoes these findings, suggesting that females tend to report elevated stress levels compared to men. Specifically, Xue and McMunn (2021) as well as Ausín et al. (2021) found that when having to contend with the dual role of household head and carer, females experience feelings of greater pressure and responsibility attributed to their dual obligations of managing household finances alongside providing care for household members. An increased rate of unemployment among females during the pandemic also adversely affected their employment and economic prospects and increased the pressure on families to take on caring roles because of the closures of schools and elderly care facilities (Priola & Pecis, 2020; Wenham et al., 2020).

Concerning age, older household heads encountered increased levels of psychological distress amid COVID-19, likely due to the more multi-generational nature of their households. Conversely, younger household heads tended to preside over less multi-generational households.

The data further revealed that older females serving as heads of households experiencing higher levels of poverty and facing greater pressure to cover expenses and bills or accounts, while facing diminishing savings reported experiencing higher levels of psychological distress compared to their male counterparts. Dziak et al. (2010) postulate that female heads are at a mental health disadvantage because of the feminisation of poverty in addition to social stressors associated with single-parent responsibilities. The study shows that female household heads suffered more and had a much heavier burden to carry during COVID-19 than their male counterparts. This may be attributed to females having lower levels of education, leading household heads to earn less income, resulting in less savings and potentially higher levels of deprivation.

Conclusion

The preceding results are not unexpected during COVID-19, as existing literature suggests that female household heads typically experience heightened levels of psychological distress. This aligns with research by Patel et al. (2022), which revealed that females exhibited significantly higher distress levels and experienced more pronounced deterioration during the pandemic compared to males. This may be attributed to increased childcare duties, more severe economic repercussions, and reports indicating substantial increases in gender-based violence. Therefore, the results from the COVID-19 data reflect an intensification of the pre-existing crisis rather than a reversal of it.

Many households during the pandemic were impacted by financial distress, which will take a long time to recover. As a result, these higher levels of psychological distress, which were exacerbated during COVID-19, will persist. In addition, after the pandemic, most households are in an even more precarious position than they were before COVID-19, and psychosocial distress and anxiety were now heightened because of the pandemic. While the R350 social relief of distress (SRD) grant was implemented to alleviate some of the financial distress people were suffering, it is not keeping pace with inflation post-COVID, affecting the overall quality of life of the household. The government may need to consider exploring options to introduce a more sustainable intervention to address the needs of the working-age population and recognise the more vulnerable groups.

Limitations

The study found that the pandemic’s impact on financial distress and mental health differed between males and females. However, it is important to note that the sample used was not representative of the entire population; it had more men, mostly with post-secondary qualifications, and was limited to those with telephone access. Thus, the findings may not fully reflect the socioeconomic disparities present in the population, particularly regarding access to resources. The findings offer insights into gender differences during the pandemic, but they only represent a specific subgroup of South Africans, not the majority. Policy efforts should prioritise addressing the needs of females to mitigate the pandemic’s impact effectively.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The author(s) received Unisa funding for the research of this article.

Availability of data and materials

The datasets used during the current study are available from the corresponding author upon reasonable request.