Abstract

To counter the escalating threat of direct conflict with rogue nations, the use of sanctions packages has become a preferred tactical response. However, although targeted, there are significantly elevated spillover effects that can generate sectoral damage. While the literature on sanctions has focused on analyzing the effectiveness and the impact on the sanctioned and sanctioning country, spillover effects have not been addressed in the tourism and travel industry. Based on behavioral decision theory and modern portfolio theory, this study states hypotheses and confronts two potential results derived from each theory regarding the way negative consequences of sanctions spill over into airlines. Using the aviation sanctions packages derived from the Russia-Ukraine war in 2022 in different regions worldwide, the results indicate greater spillovers flow into airlines than other aviation-related corporations, into big firms than small firms, and with significant differential effects on each analyzed region.

Introduction

In response to the Russia-Ukraine war that began on 24 February 2022, the European Union, Canada, and the United States made the joint decision to implement a range of sanctions, including the outright exclusion of Russian aircraft from their respective airspace from 27 February. Similar targeted decisions followed such bans by corporations such as AerCap Holdings, Boeing, and Airbus, each of whom halted the supply of parts, maintenance, technical support, and leasing activity to Russian aviation corporations. 1 Traditional research surrounding the implementation of sanctions has mainly focused on analyzing their effectiveness (Bianchi & Sosa-Padilla, 2022) and the consequential effects upon the sanctioned country (Sturm & Menzel, 2022). Interestingly, potential unintended consequence effects or spillover effects have attracted less attention (Hatipoglu et al., 2023). It is in this context, wherein our study contributes to the literature by analyzing the spillover effects of sanctions on the travel industry. Based on behavioral decision theory and modern portfolio theory, this study proposes hypotheses and confronts two potential results derived from each theory regarding the way negative consequences of sanctions spill over into airlines. Additionally, the study unearths potential asymmetries among regions. Also, from a practical viewpoint, while the implementation of sanctions is a critical tool to fight against tyranny and rogue nations, it is crucial that we further develop our understanding of contagion effects upon indirectly exposed sectors and corporations.

Note that, for this specific case, aircraft sanctions have significant impacts not only upon flight plans through the extension of routes between the west and east but also on the confidence of tourists in both directly affected regions and those regions with regional boundaries close to both Russia and Ukraine. Further, while such exposure to the Russian market would have been quite minimal before the beginning of the Russia-Ukraine war, the additional influence of continued lockdowns in China to mitigate the effects of the COVID-19 pandemic proliferated an environment which greatly exposed airlines to significant downside risk (Dube et al., 2021). The changes in the market value of airlines, as measured through a robust methodology mitigating the influence of international effects, can greatly enhance our understanding and ability to better coordinate targeted sanctions packages in the future, supporting the decision-making of both policymakers and governments.

For this purpose, this research specifically analyses the influence of the alluded sanction packages on the international aviation sector in several distinct ways: firstly, through a comparison of worldwide airline share price and volatility behavior when compared to other transportation stocks as a control group, secondly focusing on distinct differentials in response between Chinese, European, Russian, and United States domiciled aviation corporations, which in turn will allow us to identify potential asymmetric effects; and thirdly, by looking into the firm size and the differential spillover effects. 2

Overall, the study finds that the negative consequences of sanctions spill over much more into airlines than other publicly traded aviation-related companies, with differential effects on each examined region and a greater impact on larger firms than small firms. Theoretically, two frameworks have emerged as leading contenders to explain investor behavior in such situations; behavioral decision theory and modern portfolio theory. Regarding the potential “battle” between the two, the latter seems to beat the former. According to behavioral decision theory, familiarity with a big name favorably conditions investors’ decision-making toward that big name as investors form high expectations regarding their potential. One would expect that, in the context of sanctions, big firms should be more protected. The desire to maximize returns given a specific level of risk, as assumed by modern portfolio theory, seems to prevail: large airlines generally linked to long-haul routes are expected to be more affected by increasing energy costs as a consequence of sanctions packages.

The remainder of this paper is structured as follows: the previous literature and theory that guides the development of our research are summarized in Section 2. Section 3 presents a thorough explanation of the wide variety of data used in this analysis while also presenting a concise overview of the methodologies used. Section 4 specifically presents evidence of the wide-reaching influence of Russian-targeted aviation sanctions and the subsequent contagion effects generated therein. Section 5 concludes.

Literature on Sanction Research: Spillover Effects

The literature that has analyzed political sanctions focuses mainly on the effectiveness of such drastic measures and the effects on the targeted country. The research line that focuses upon the effectiveness of sanctions was pioneered by Hufbauer et al. (1985), who analyzed the design elements and implementation that lead sanctions to accomplish their goal. Such work was further developed by Baldwin (2000), which focused on several different positions in the debate concerning whether sanctions are useful; McLean & Whang, 2010],which find that the cooperative attitude of the sanctioned country’s main trading partners is a major determinant for the success of the sanction; Morgan & Schwebach (1997),which propose a model to measure the efficacy of sanctions; Pape (1997), which presents the reasons for which sanctions fall short of the expected effects; and more recently, Gholz and Hughes (2021) who find that the inclusion of key elements of market structure is critical to assess the effectiveness of sanctions. We further considered research that focused on the effects of government-imposed sanctions on tourism, particularly that which has recently focused on the behavior of tourism considering restrictions due to COVID-19 (Seyfi et al., 2023). Gorji et al. (2023) identified that sanctions influence both affective and cognitive images and enhance tourist risk perceptions, while the continued re-introduction of sanctions can paralyze regional tourism (Khodadadi, 2016; Seyfi et al., 2022; Seyfi & Hall, 2020). When focusing on the effects of sanctions on tourism experience using a sample of Russian tourists in Cyprus, Farmaki (2023) identified that animosity within tourist destinations represents a complex construct evolving from media representation and the passage of time post-event. While Ivanov et al. (2016) identified that international sanctions had significantly damaged regional tourism in Crimea.

The research thread on the effects of the targeted country not only has attempted to assess the impact of sanctions (Eaton & Engers, 1992) but also the criteria that should be employed to judge such an impact (Cortright et al., 2000) and the effects of distinct types of sanctions such as “smart” sanctions (Drezner, 2011). Within this second line of research, a group of studies look at potential spillover effects within the targeted country, such as the impact on human rights (Drury & Peksen, 2014; Peksen, 2009) or on democracy (Peksen & Drury, 2010). Interestingly, besides the research that examines potential backfiring effects on the sender country (Gordon, 2016; McLean & Roblyer, 2016; McLean & Whang, 2010), the literature has not paid much attention to potential contagion effects on other countries (Bachmann et al., 2022; Hatipoglu et al., 2023). Hatipoglu et al. (2023) claims to be the first systematic investigation of spillover derived from the impact of international economic sanctions on third countries. In addition to the investor perspective, it is essential to also consider the consumer perspective in analyzing the effects of international aviation sanctions. Investors, who play a crucial role in financial decision-making, base their investment choices on their expectations of consumer behavior. Consequently, understanding the actions and choices of prospective travelers becomes vital as it significantly shapes the financial performance of airlines and related industries, an area that has not received significant attention to date. Incorporating the consumer perspective allows for a deeper understanding of how international aviation sanctions impact consumer confidence, travel preferences, and the overall demand for air travel services. 3

Our study, framed in the context of the beginning of the Russia-Ukraine war, contributes to the literature by looking into the effects of sanctions on the travel industry of the targeted country as well as different regions of the world, thereby analyzing for the first-time spillover effects in the travel and tourism industry. The unfolding of the recent events regarding the Russia-Ukraine war has sparked interest in the analysis of sanctions. Bianchi and Sosa-Padilla (2022) attempt to find the optimal restrictions to be imposed, Sturm and Menzel (2022) identify the economic sanctions that maximize the economic cost for the targeted country and minimize the cost for the sanctioning country, while Sturm (2022) analyzes the effects of constrained imports of oil and gas from Russia, and Lorenzoni and Werning (2022) and Itskhoki and Mukhin (2022) look into the factors that influence the equilibrium exchange rate. Interestingly, Lorenzoni and Werning (2022) suggest that exchange rates are not the best signals to look at to analyze how effective sanctions are.

Tourism and travel sectors are extremely sensitive to events that bring about uncertainty and that, as Wut et al. (2021) point out, “create vulnerability.” Thus, it is obvious that sanctions imposed on Russia will affect its economy in general and its travel in particular (Yap et al., 2023); however, third countries are not immune to these consequences either (Plzáková & Smeral, 2022).

Considering this extreme sensitivity in tourism, it is expected that aircraft sanctions—beyond their effects on flight plans through the extension of routes between the west and east –will significantly impact the confidence of tourists in both directly affected regions. We hypothesize that this erosion in tourists’ confidence can spill over into investors’ conduct. In line with the behavioral decision theory, people tend to invest in those stocks whose uncertainties are under control or, at least, are more familiar and confident with (Heath & Tversky, 1991). Consequently, we state the following hypothesis:

In addition to the empirical investigation, our research is underpinned by two key theoretical frameworks: behavioral decision theory and modern portfolio theory. While we acknowledge that these theories have broad applicability across various domains, we want to emphasize their specific relevance to our study on the effects of international aviation sanctions on the airline industry. Behavioral decision theory provides insights into how individual investors’ psychological biases and heuristics influence their investment decisions, particularly in times of economic uncertainty and geopolitical events. By considering this theory, we aim to shed light on the role of investor expectations and sentiment in shaping the financial performance of airlines. Modern portfolio theory guides our understanding of how investors optimize their portfolios to balance risk and return, considering factors such as firm size, industry dynamics, and market conditions. Applying this theory allows us to examine the differential impacts of sanctions on airlines compared to other aviation companies. By explicitly integrating these theoretical frameworks into our research, we provide a solid foundation for understanding the dynamics of the aviation industry during periods of geopolitical turmoil.

Asymmetric Spillover Effects Between Regions

Beyond logical influential factors such as physical distance between the sanctioned country and third countries (i.e., whether the third country is a neighboring country), the targeted country tends to get prepared for the potential consequences. For this specific case, it is important to notice that, in response to the broad range of international sanctions imposed, Russia’s central bank immediately more than doubled its key policy rate to 20% while simultaneously imposing capital controls and halting the sale of foreign currency, closing domestic exchanges, and adding significant liquidity to underpin both the ruble and domestic stock markets simultaneously. Further regulatory support was implemented by imposing a ban on short-selling while banning international investors from exiting Russian-owned positions. International aviation corporations not only had to contend with aviation sanctions, but also with significant volatility within energy commodity markets, much of which had transitioned into direct difficulty when hedging fuel price movements and raising working capital, where such practices become quite difficult in periods of turmoil (Carter et al., 2006; Weiss & Maher, 2009). On 5 March 2022, Vladimir Putin visited the employees of state-owned Aeroflot, announcing that the imposed sanctions were “an act of war” and reciprocated such sanctions by banning Western airlines from Russian airspace. Further financial supports were provided in April 2022, when the Kremlin announced the provision of 100 billion rubles to support regional aviation, where demand had been negatively affected, falling by up to one-third year-on-year. Further issues have also been generated within aircraft leasing markets, where Russian-based lease agreements have been broken; however, the planes remain trapped within Russia. This situation has not only breached the Chicago Convention but also exposed many Irish-based leasing companies when considering the estimated USD$10 billion valuation of planes based within Russia. Sanctions also stifled the flow of planes manufactured within Russia, where orders of the Irkut MS-21 were reported to have been delayed until at least 2024. In June 2022, the Russian government announced a support package of 770 billion rubles to support domestically manufactured aircraft, generating knock-on effects upon international supply and demand structures.

Consequently, because of the physical distance between countries and the targeted country’s preparedness, we state that:

Firm Size

As mentioned earlier, sanctions have significant effects on flight plans as well as on tourists’ confidence. We hypothesize that this impact can also spill over into investor conduct through two theories that can bring about confronted results: behavioral decision theory and modern portfolio theory.

Behavioral decision theory encompasses a set of “descriptive theories to explain the psychological knowledge related to people’s decision-making behavior” (Takemura, 2014), with multiple applications in tourism (J. Kim et al., 2020; E. E. K. Kim et al., 2022). It has been widely applied to behavioral economics and behavioral finance, wherein Heath and Tversky (1991) observe that individuals show a preference for betting in familiar areas in which they have certain knowledge about the potential risks and uncertainties so that they feel more confident than in other areas they are unfamiliar with. Accordingly, the literature shows that investors favor “big names.” Interestingly, despite empirical evidence that these strong brand names do not necessarily produce increased short-term returns, investors prefer them over less powerful brands (Frieder & Subrahmanyam, 2005). These authors justify this result by arguing that investors have superior expectations of “appreciation potential” in those big firms with strong brand names. In the context of sanctions, the expectations are that these big firms are more protected, thereby increasing the demand for shares of these firms. To reinforce this argument, it is also important to recall that, based on the resource-based view (J. Barney, 1991; J. B. Barney & Arikan, 2005), firm size has been widely used in the tourism and travel literature 4 as a determinant factor for a company to navigate adversities (Nicolau & Sharma, 2022); hence, large airlines should be in a better position to protect their business.

Regarding modern portfolio theory, while widely adapted to destination management (Jang & Chen, 2008; Johar et al., 2022), it represents a framework where a portfolio of stocks maximizes their expected returns considering a specific risk (Markowitz, 1952). Sharpe (1964) put forth the market model in which a share’s return is linearly dependent on the market’s return, where the market risk (systematic risk) is driven by general conditions of the market (such as the Russia-Ukraine war) and the firm-specific risk depends on the uniqueness of the firm and its characteristics. Accordingly, investors will only favor those stocks with a certain level of return for a given level of risk if there is no other stock with a higher return for the same level of risk. In this framework, there should be no room for preferences based on familiarity issues such as those suggested by the behavioral decision theory. However, Huberman (2001) observed that this is not the case and found that investors prefer familiar assets, thereby ignoring the main tenets of modern portfolio theory.

Consequently, while large airlines should be in a better position to protect their business (based on the resource-based view) and investors being generally more familiar with these big names tend to favor these stocks (behavioral decision theory), modern portfolio theory postulates that investors will objectively assess the information available in the market and their decisions will be contingent upon the market’s risk and the firm-specific risk. Therefore, the final reaction would depend on how much of the firm’s business investors find that can be affected. At this point, it is important to consider that larger airlines are generally associated with long-haul routes that entail higher costs and, therefore, are more affected by increasing energy costs. Because of this argument, we expect that modern portfolio theory will win over behavioral decision theory so that:

Data and Methodology

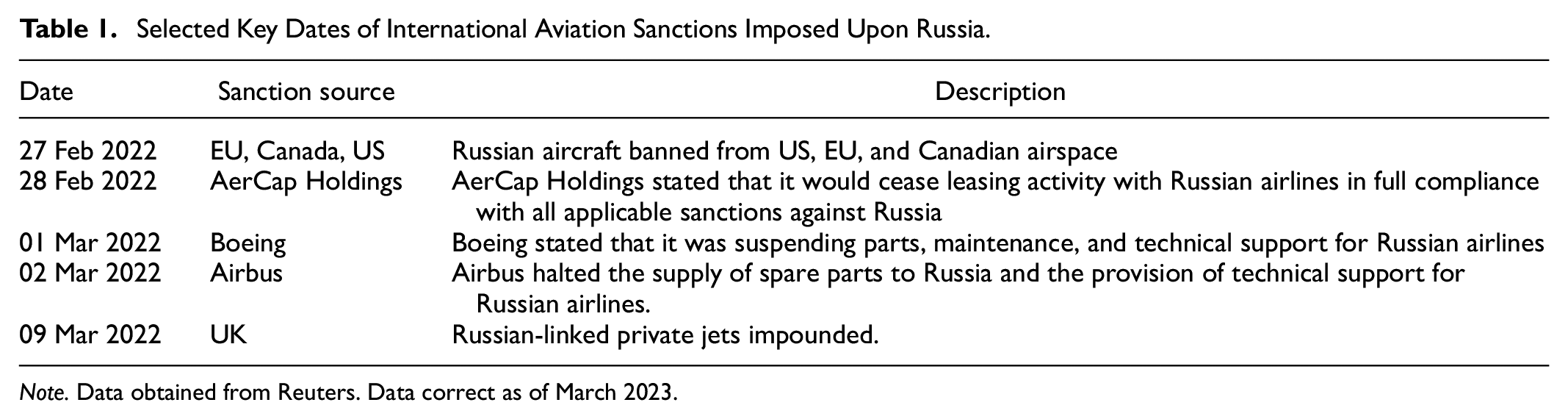

Data used in the analysis is obtained from the Thomson Reuters Eikon database, where stock market ISIN codes were obtained for 682 worldwide transportation companies as denoted by their respective TRBC sector. For the following analysis, we separate the identified TRBC sectors specifically into two groups consisting of (1) Airlines; and (2) All Other Companies, where specifically, the group identified as Airlines represent the TRBC sectors inclusive of Airlines, whereas the group All Other Companies includes the TRBC sectors including Airline Catering Services; Airport Fueling Services; Airport Operators; Airport Operators & Services; Charter Bus Services; Commuter Ferry Operators; Highways & Rail Tracks; Marine Passenger Transportation; Marine Port Services; Passenger Transportation, Ground & Sea; Port Operators; Rail Services; Railway Operators; and Specialized Aviation Services. Where data was unavailable due to market closure, respective international Depository Receipts were utilized. The sample period 1 January 2019 through 31 March 2023 is examined, where the use of a substantial period of analysis before the imposition of Russian sanctions supports the identification of traditional behavioral patterns 5 within the airlines and control sample analyzed. 6 Data relating to the 2022 sanction packages imposed upon the Russian economy, specific Russian corporations, and the aviation sector at large due to the Russia-Ukraine war are obtained from Reuters. The inclusion of data prior to the beginning of the COVID-19 pandemic supports our methodological structure through the provision of a period of relative financial market stability in advance of the onset of both the COVID-19 pandemic and the Russia-Ukraine war. Specifically focused on the aviation sector were those events leading to the banning of Russian aircraft from the US, EU, and Canadian airspace on February 27 and the impounding of Russian-linked private jets, such as that in the UK on March 9. Selected key dates of international aviation sanctions placed upon Russia are presented in Table 1. Further relevant examples to this study include the cessation of leasing activities by AerCap Holdings with Russian airlines on February 28, the suspension of supply, maintenance, and technical support for Russian airlines by Boeing on March 1 and a similar decision by Airbus, which was implemented on March 2.

Selected Key Dates of International Aviation Sanctions Imposed Upon Russia.

Note. Data obtained from Reuters. Data correct as of March 2023.

This research sets out to establish the specific effects that such broad sanctions had upon the international aviation industry as separated by sector and by geographical location. We first calculate the natural logarithm of returns

where on day

The abnormal and cumulative returns averaged over all airlines and companies analyzed

For our event study, we calculate corresponding t-statistics to determine the significance of each event window. We compute the t-statistic as:

To specifically analyze the return and volatility differentials due to the international sanctions imposed on Russia, we utilized an EGARCH(1,1) methodology, which was selected after using several goodness-of-fit testing procedures.

9

The EGARCH(1,1) structure is used to specify the conditional variance

while we express the variance equation of our EGARCH(1,1) model as follows:

We include an additional

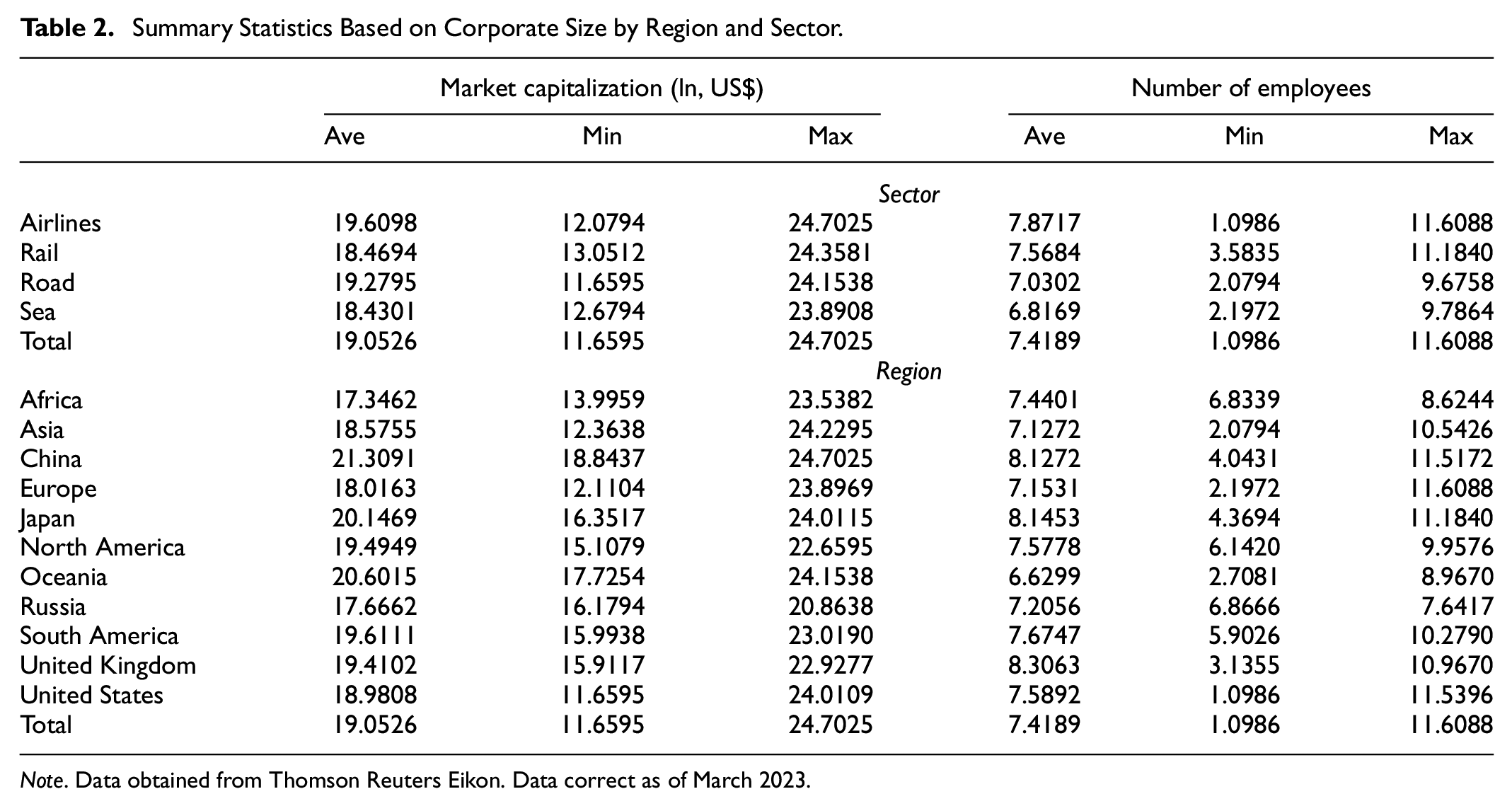

To provide detailed insights into the sectoral and regional differentials, data is separated by sector (airlines, rail, road, and sea) and again by region (Africa, Asia, China, Europe, Japan, North America, Oceania, Russia, South America, United Kingdom, and the United States of America). Associated summary statistics are presented in Table 2, focusing specifically on the market capitalization and the number of employees in the included companies. Methodological processes are separated based on transportation stocks (rail, road, and sea) and airline stocks. Such separation of the data allows for direct comparison of the results, therefore providing more substantiative detail surrounding the international effects of sanctions.

Summary Statistics Based on Corporate Size by Region and Sector.

Note. Data obtained from Thomson Reuters Eikon. Data correct as of March 2023.

Results

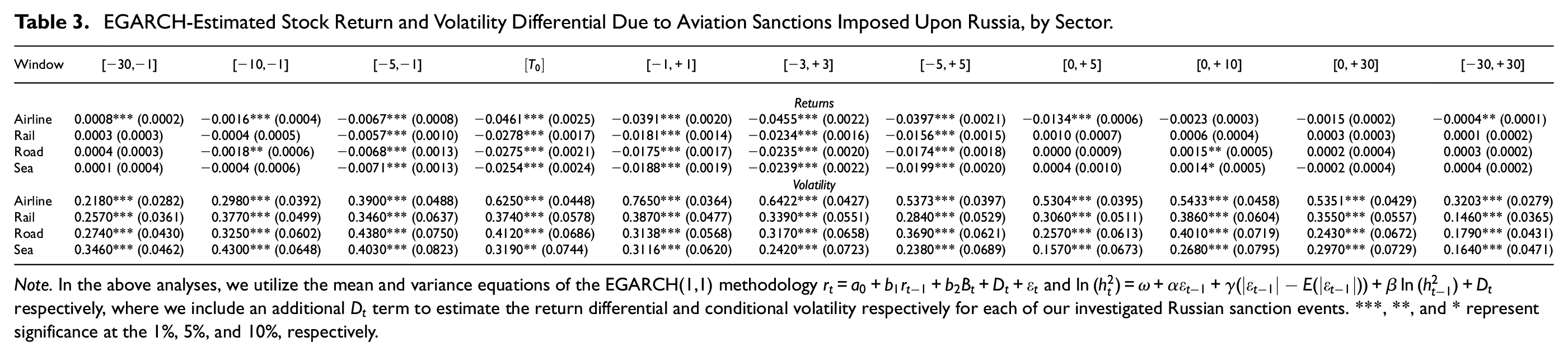

First, we differentiate between return and volatility differentials, as a direct result of the imposed aviation sanctions due to the beginning of the Russia-Ukraine war in Table 3. When considering airlines as separated by TRBC section and geographical location, respectively, noting that the presented results indicate corporate response more than each respective domestic exchange, several distinct differentials are identified. In the period before

EGARCH-Estimated Stock Return and Volatility Differential Due to Aviation Sanctions Imposed Upon Russia, by Sector.

Note. In the above analyses, we utilize the mean and variance equations of the EGARCH(1,1) methodology

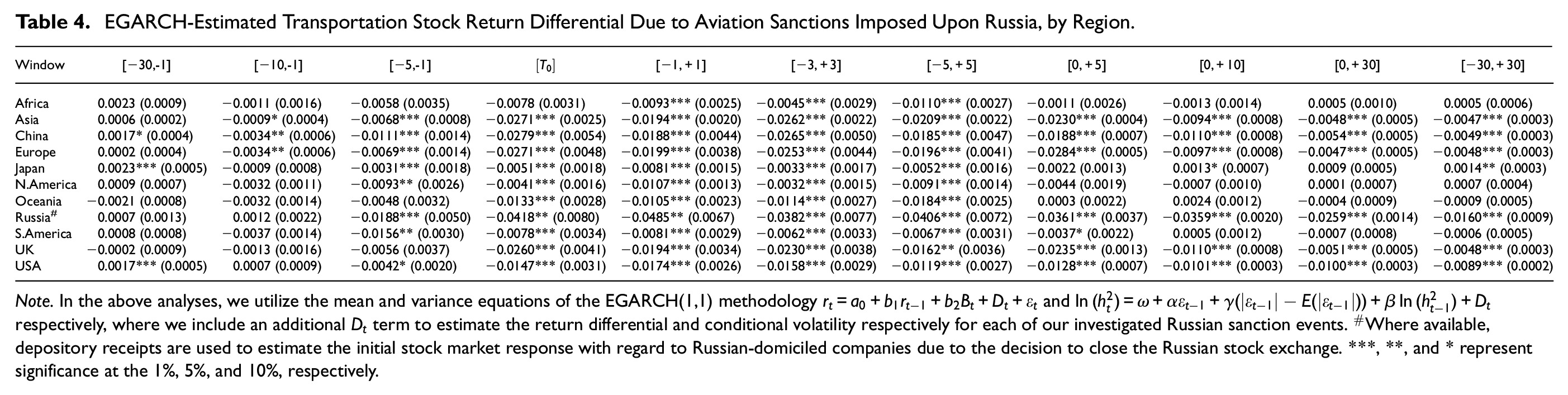

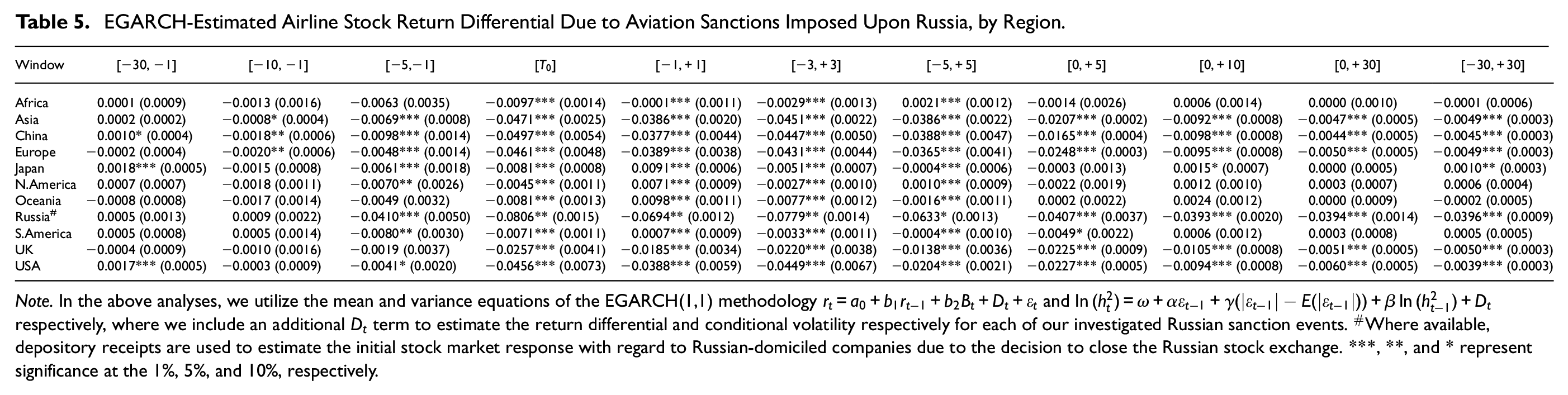

Regional differentials of transportation and airline-related returns, because of aviation sanctions, are presented in Tables 4 and 5, respectively. As theoretically expected, Russia is the most negatively influenced nation regarding estimated influence for transportation corporations and airlines, where returns on the sanctions date are −4.2% and −8.1% at time

EGARCH-Estimated Transportation Stock Return Differential Due to Aviation Sanctions Imposed Upon Russia, by Region.

Note. In the above analyses, we utilize the mean and variance equations of the EGARCH(1,1) methodology

EGARCH-Estimated Airline Stock Return Differential Due to Aviation Sanctions Imposed Upon Russia, by Region.

Note. In the above analyses, we utilize the mean and variance equations of the EGARCH(1,1) methodology

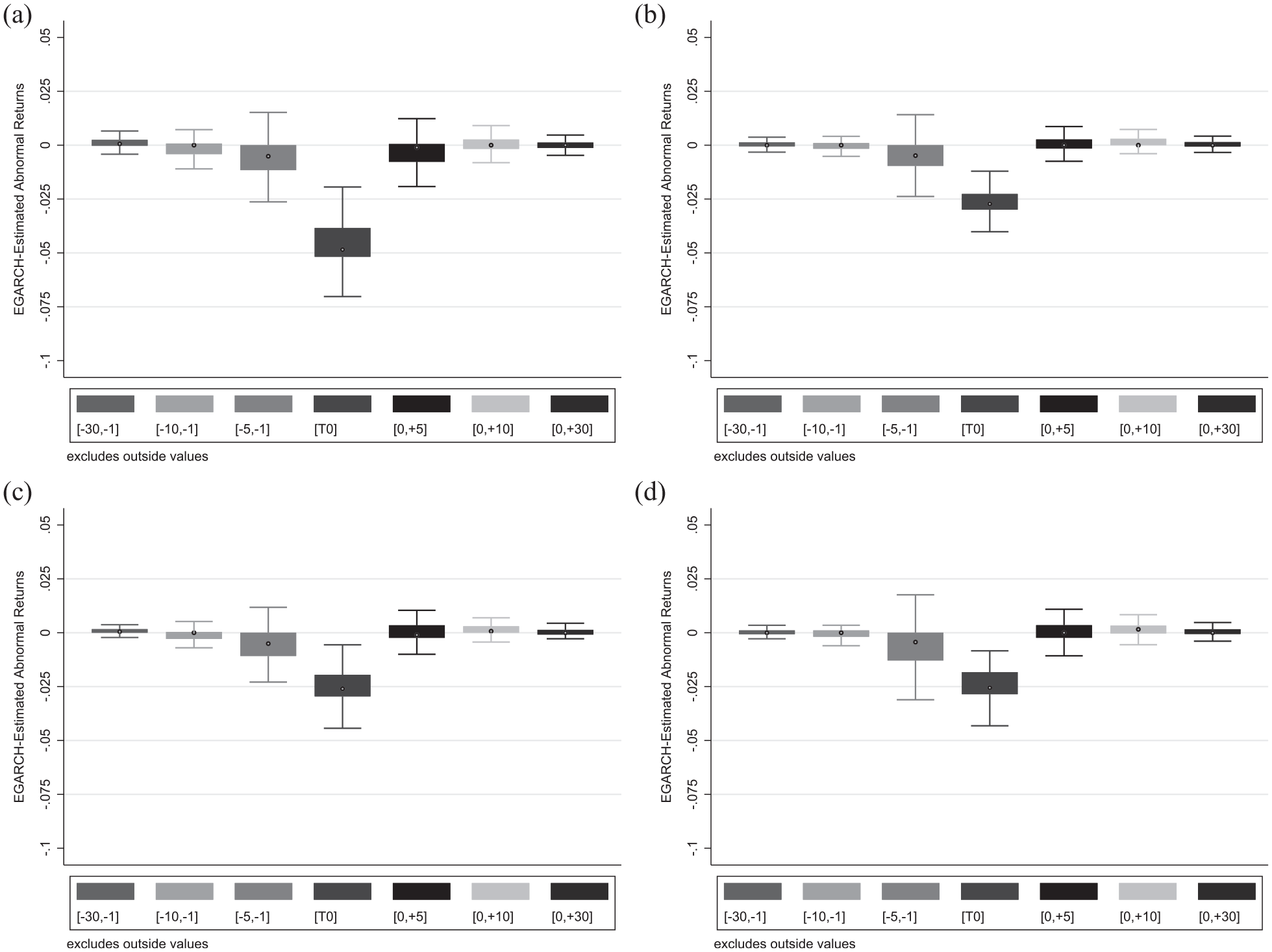

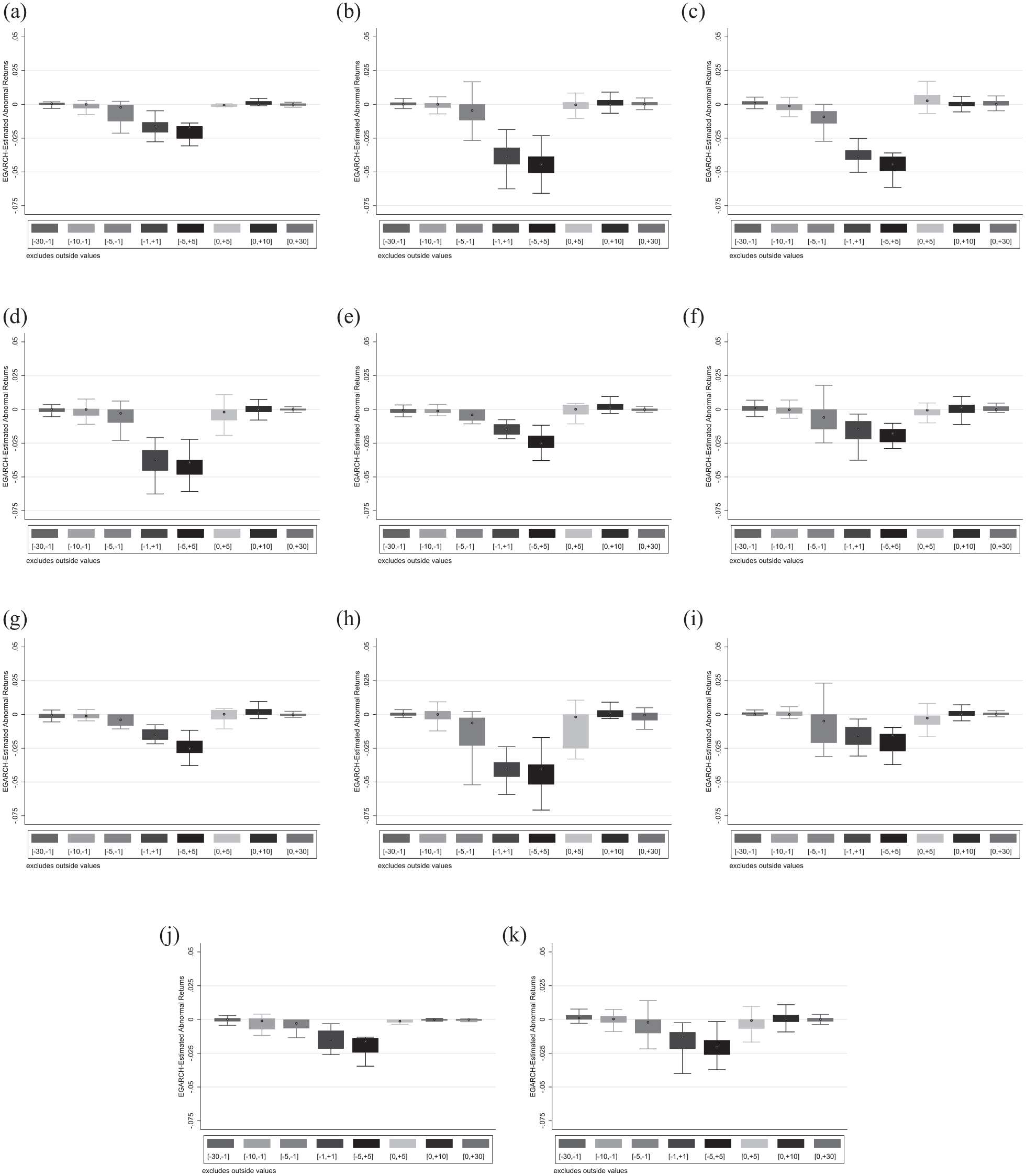

Figures 1 and 2 further verify the observed results presented in Tables 3 to 5 respectively, where evidence suggests that airlines experienced sharper, more persistent negative returns when compared to other aviation companies, thereby supporting hypothesis 1 that the negative consequences of sanctions spill over greater into airlines than other aviation companies. Note, however, that airlines in the United States do not experience negative median returns at the same depth as that experienced by their Chinese and European counterparts. This result supports hypothesis 2 regarding spillovers with asymmetric effects among the different regions. The rapid return of industry performance to that which is in line with broad market conditions is quite an interesting observation, indicating that investor response surrounding an immediate re-evaluation of corporate performance was immediate, with European and Chinese companies perceived to be most exposed to collateral damage related to targeted sanctions.

Corporate abnormal returns surrounding international aviation sanctions: (a) airlines, (b) rail, (c) road, and (d) sea.

Regional aviation-related abnormal returns surrounding international aviation sanctions: (a) Africa, (b) Asia, (c) China, (d) Europe, (e) Japan, (f) North America, (g) Oceania, (h) Russia, (i) South America, (j) United Kingdom, and (k) United States.

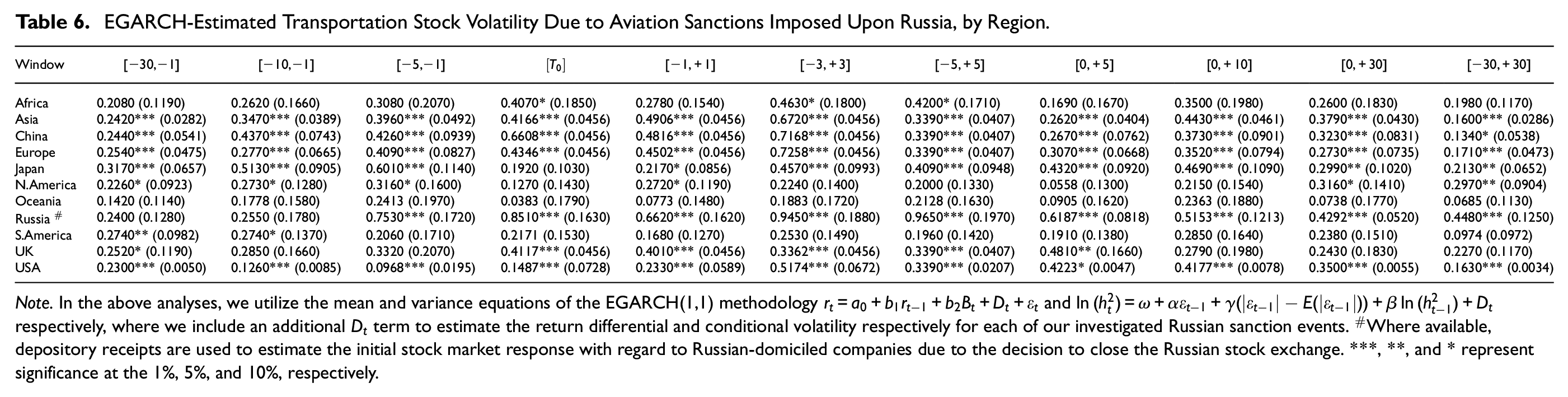

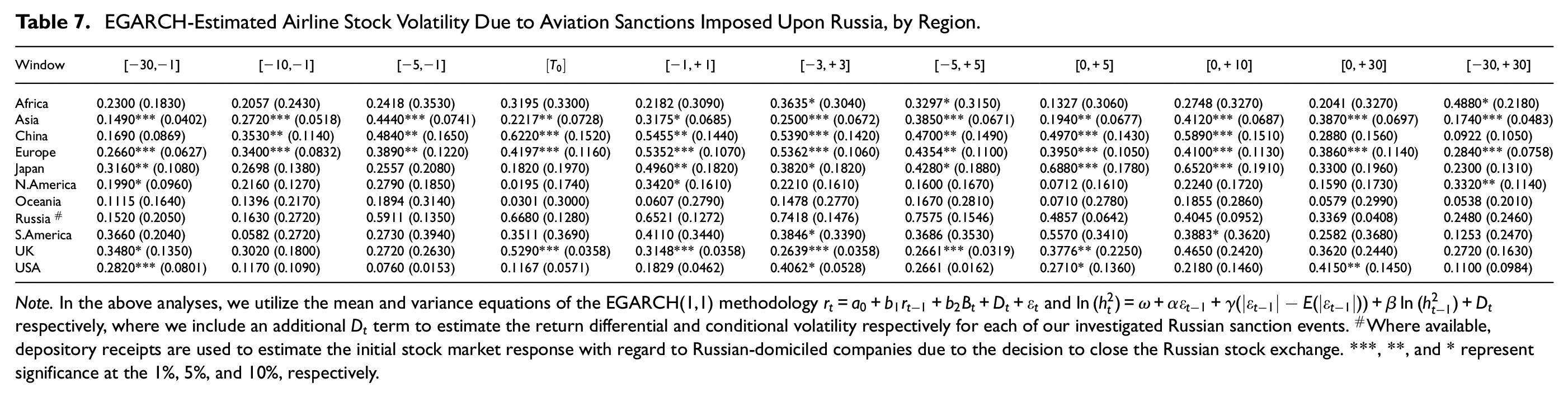

Evidence of related financial market volatility effects specific to the implementation of aviation sanctions on Russia are presented in Tables 6 and 7, respectively. Specifically, Table 6 relates to all analyzed publicly traded transportation corporations by region, whereas Table 7 focuses on airlines in isolation. Several significant effects have been identified that complement the results identified when focusing on regional return differentials because of international sanctions. Significantly elevated and persistent levels of volatility of both transportation and airline-related stocks are identified in Russia. However, it is interesting to note that the Asian, European, South American, and United Kingdom-based corporations present evidence of persistently elevated transportation and airline sector financial market volatility. The United States, Africa, North America (consisting of Canada and Mexico), and Oceania each present evidence of significant shelter from the influence of international sanctions.

EGARCH-Estimated Transportation Stock Volatility Due to Aviation Sanctions Imposed Upon Russia, by Region.

Note. In the above analyses, we utilize the mean and variance equations of the EGARCH(1,1) methodology

EGARCH-Estimated Airline Stock Volatility Due to Aviation Sanctions Imposed Upon Russia, by Region.

Note. In the above analyses, we utilize the mean and variance equations of the EGARCH(1,1) methodology

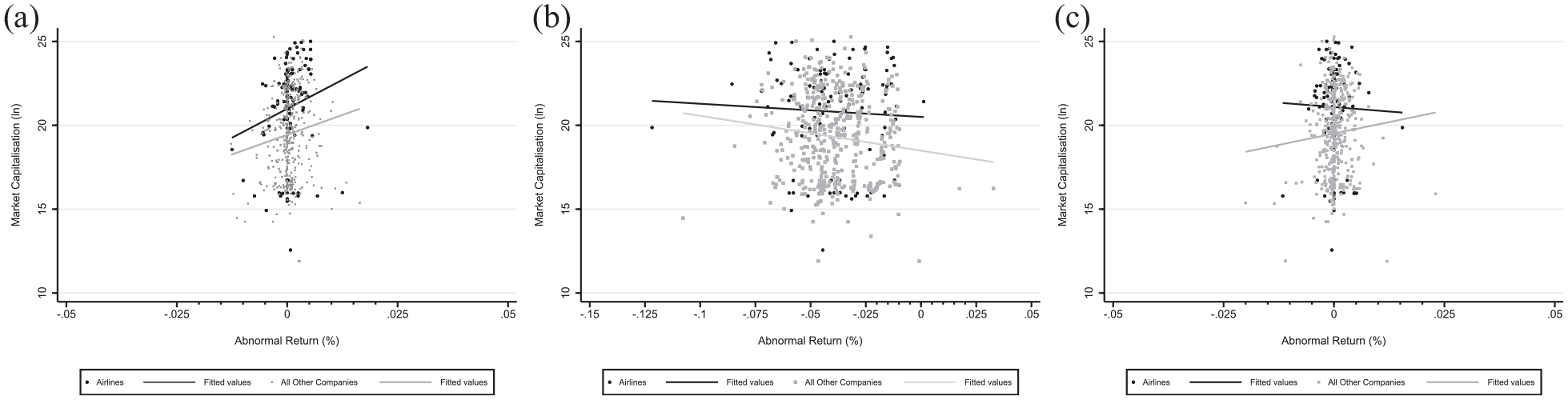

We further evaluate the relationship in the period surrounding each event between abnormal returns and company size in Figure 3. When considering the 30 trading days period to each announcement, we observe that, on average, analyzed airlines within the sample are larger than the comparable sample of transportation companies, where both groups present evidence of a strong positive relationship between larger companies and elevated abnormal returns. However, considering the 10 days surrounding the implementation of aviation sanctions at time

Relationship between abnormal returns and corporate size (market capitalization): (a) Time [−30,−1], (b) Time [−5,+5], and (c) Time [0,+30].

Such findings highlight the crucial role that firm size plays in shaping airlines’ response to international sanctions. Larger airlines, with their greater resources and established market presence, tend to exhibit distinct patterns of resilience and adaptation compared to smaller airlines. Our analysis reveals that larger airlines are better equipped to mitigate the adverse effects of sanctions through diversification strategies, alternative route planning, and financial resilience. However, we also observe that the relationship between firm size and performance is not linear, with some smaller airlines demonstrating remarkable adaptability and innovation in the face of sanctions. These findings underscore the need to consider firm size as a key determinant of an airline’s ability to navigate the challenges presented by international sanctions.

Building upon the theoretical foundations of behavioral decision theory and modern portfolio theory, our study provides valuable insights into the complex interplay between investor behavior, market dynamics, and the effects of international aviation sanctions on the airline industry. The incorporation of behavioral decision theory allows us to capture the role of investor expectations, sentiment, and decision-making biases in shaping stock returns and market reactions to sanctions announcements. Our findings highlight the importance of considering the psychological factors that drive investor behavior in understanding the financial performance of airlines during periods of geopolitical turmoil. Further, the interdependence between investor decisions and consumer behavior should not be overlooked in the context of aviation sanctions. Investors closely monitor consumer preferences, as shifts in consumer demand significantly impact the financial performance of airlines and related sectors. Changes in consumer behavior, such as reduced travel willingness or shifts in destination preferences, can have direct implications for revenue and profitability. Therefore, understanding the interplay between investor expectations and consumer behavior allows for a comprehensive assessment of the effects of sanctions on the aviation industry.

Such results also give rise to two key points that merit further consideration: first, the lack of persistence of abnormal returns could potentially indicate those market participants did not credibly identify a pathway to further aviation sanctions, attributed to a key international concern surrounding the lack of cohesion, conviction, ruthlessness, and timeliness when implementing targeted sanction packages; and secondly, while Russian corporations are found to exhibit sharp negative returns, and simultaneously considering the influence of the closure of Russian stock exchanges in an attempt to calm domestic investors, the implementation of Russian government stability supports as a counter-measure to international sanctions appears to have significantly reduced broad volatility. This latter finding should be of interest to policymakers in the future. However, such perceived “stability” achieved when counteracting sanctions should be considered little more than synthetic and simply a short-term mechanism to shroud deep-rooted fragility and stress. Overall, the ability of nations to circumvent the effects of targeted sanctions packages through market intervention undermines their existence. Secondary contagion resulting from targeted sanctions packages is found to be significant, and negative side effects must be considered in detail before full implementation. The probability of success of such packages appears to be directly correlated with the credibility of the depth of sanction one side is willing to impose upon others.

Concluding Comments

While the literature on sanctions has mainly focused on the analysis of their effectiveness and the impact on the sanctioned country, the effects of potential unintended consequences have not attracted much attention, let alone in the tourism and travel industry. This study contributes to the literature by analyzing the spillover effects of sanctions on the tourism and travel industry. Based on the tenets of behavioral decision theory and modern portfolio theory, this research investigates the influence of aviation sanctions packages imposed due to the beginning of the Russia-Ukraine war in 2022, on the airline industry in different regions of the world: Europe, the United States and China. The study finds that the negative consequences of sanctions spill over greater into airlines than other aviation companies, with differential effects on each region and a greater impact on larger firms than small firms. Drawing on behavioral decision theory, familiarity with a big name favorably conditions investors’ decisions toward that big name as investors form high expectations regarding their potential. In the context of sanctions, these expectations would lead investors to regard big firms as more protected, with the consequent increase in the demand for shares of these firms. However, modern portfolio theory seems to take over in this environment as the desire to maximize the expected returns, given a certain level of risk, leads investors to consider all the available information and look at it objectively without psychological traits, such as familiarity, having an influence on their decisions. It seems that larger airlines are generally associated with long-haul routes that entail higher costs and, in turn, are more affected by increasing energy costs.

Our findings have important policy and regulatory implications for the international aviation industry and the entities involved in sanctioning activities. The existence of asymmetric spillover effects of sanction on different regions and sub-sectors means that the sanctioning entity must take these potential differential effects into account to ensure that all the necessary informative measures are communicated to and anticipated by the potentially affected third parties, regions and sub-sectors. Accordingly, when sanctions are announced, airlines that can be particularly affected by “collateral effects” such as energy costs (on account of their association with long-distance flights) should be prepared and implement plans that alleviate these negative consequences via diversification strategies. Further, our study provides valuable insights into the role of firm size in understanding the effects of international sanctions on the aviation industry. By treating firm size as a significant variable rather than a control variable, we shed light on the unique dynamics and the varying responses exhibited by airlines of different sizes. Our findings demonstrate that firm size significantly influences an airline’s ability to withstand and adapt to the challenges posed by sanctions.

Further, several avenues for future research can further enhance our understanding of this complex phenomenon. Firstly, expanding the analysis to include other countries that have experienced similar sanctions could provide comparative insights and deepen our understanding of the broader implications of sanctions on the global aviation landscape. Additionally, investigating the long-term effects of sanctions on the financial performance and strategic decisions of airlines and aviation companies would contribute to a comprehensive understanding of the lasting impacts of sanctions. It is also important to better understand the role of corporate governance structures and risk management practices in mitigating the adverse effects of sanctions on the aviation industry could provide valuable insights for policymakers and industry practitioners. Further, considering the dynamic nature of geopolitical conflicts using higher frequency financial market and social media sentiment data could greatly improve our understanding of the interaction and contagion effects associated with such geopolitical shocks. By addressing these research gaps, future studies can provide a more comprehensive and nuanced understanding of the implications of sanctions on the aviation industry and contribute to effective policy formulation and strategic decision-making. Future research should further explore the consumer perspective by examining the effects of sanctions on consumer confidence, travel intentions, and the overall demand for air travel. Such research would provide a more comprehensive understanding of the complex dynamics between investor decision-making and consumer behavior, offering valuable insights for policymakers, industry practitioners, and investors in the aviation sector.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.