Abstract

Tax havens are often connected to growth in tourism, as finance and tourism conveniently share infrastructural prerequisites. This paper addresses the detrimental impacts of a tax haven development strategy adopted by small open economies in relation to the development of their tourism industry. Utilizing the synthetic control method, we find that since the 2016 Panama Papers scandal, Panama’s tourism exports have fallen relative to an estimated counterfactual level that would have otherwise been attained. Moreover, based on an analysis of panel data drawn from 20 small open economies, we find that in the long run, the growth of the financial industry crowds out the tourism industry. Our findings warn tourism practitioners, based in tax havens, that they face an additional risk linked to potential tax scandals. Furthermore, the tourism industry may suffer reputational harm due to tax haven blacklisting and the crowding out of productive resources by the financial industry.

JEL classifications: F43, H26, O57, Z32

Introduction

In April 2016, millions of documents containing information on over 200,000 offshore entities were taken from Mossack Fonseca, a law firm based in Panama, and leaked to the world media via the International Consortium of Investigative Journalists (ICIJ). Those documents, which were subsequently dubbed the “Panama Papers,” garnered widespread media attention and showed that countless shell corporations had been set up and used for illegal purposes such as tax evasion, fraud, the evasion of international sanctions and money laundering. The initial response of Panama’s President at the time, Juan Carlos Varela, was to pronounce that the leak addressed tax evasion in general and not specifically Panama per se. However, commentators and politicians became concerned that Panama’s reputation as a tax haven could tarnish its impressive economic performance.

Along with Panama, the leak brought a group of small open economies (typically small islands) into the spotlight as jurisdictions used by Mossack Fonseca to set up these complex financial structures. Geographically, these locations, which are mostly concentrated in the Caribbean and Pacific regions, are generally characterized as small (in terms of population and land mass), remote, insular, and vulnerable to external shocks (United Nations, 2014). Quite often, they also possess substantial tourism assets thanks to their unique biodiversity and cultural richness (UNWTO, 2014). Consequently, many of them are categorized as “highly tourism developed” according to the Tourism Penetration Index (TPI) constructed by Mcelroy (2003) and are ranked high in the World Economic Forum’s (2022) league table of Travel & Tourism Development Index.

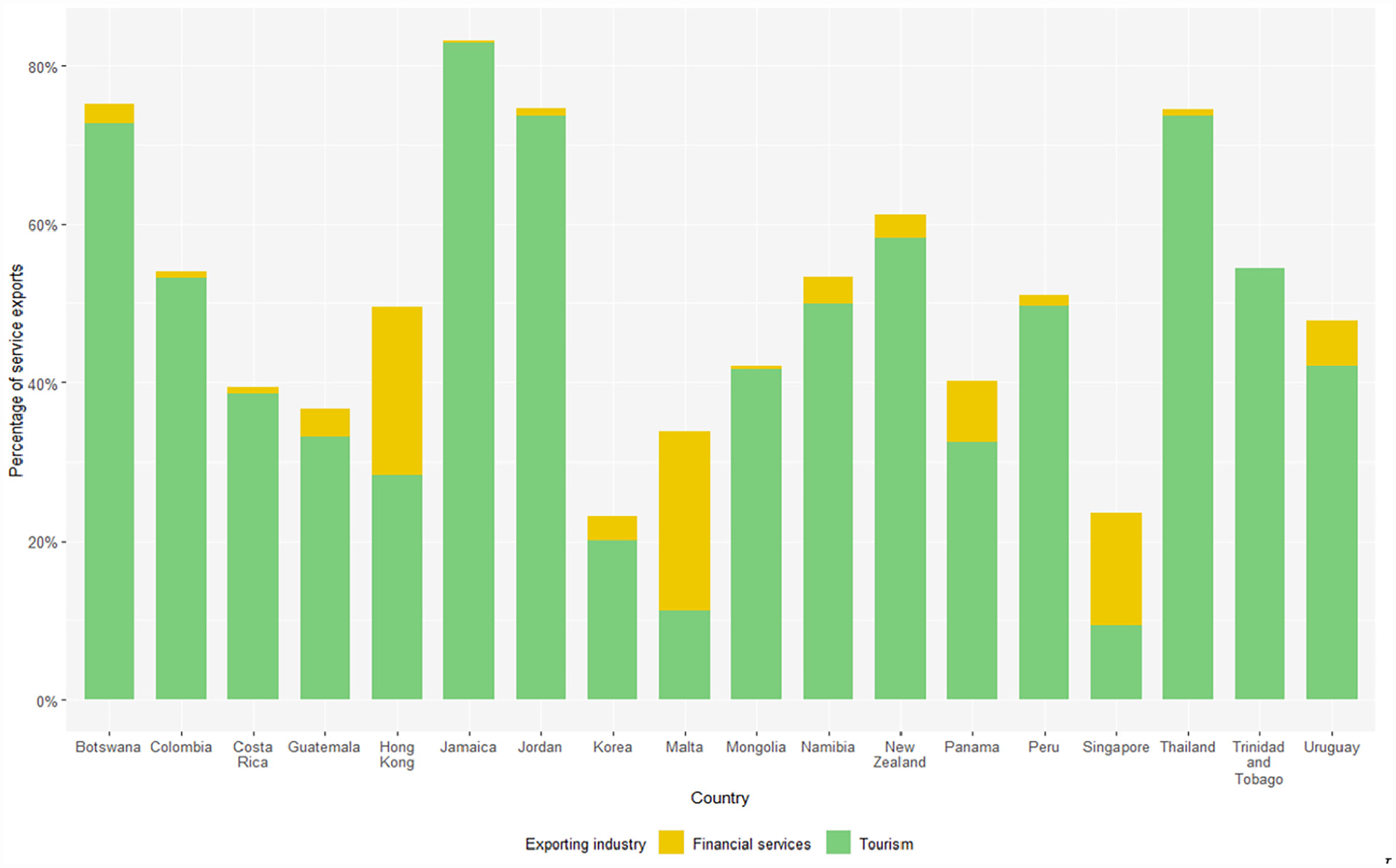

Figure 1 shows the relative importance of the tourism and financial services industries in some of the countries that were used by Mossack Fonseca (International Consortium of Investigative Journalists [ICIJ], 2021) or listed as tax havens by the European Union (European Commission, 2021). As of 2019, tourism and financial services jointly accounted for a significant proportion of total service exports for these countries, ranging from 23.5% to 83.2%. At the same time, the economic outcomes of the dominance of tourism and financial services have been remarkable, as many rank among the high-income or upper-middle-income categories, as per the The World Bank’s (2022) income level classification.

Tourism and financial services as percentages (%) of service exports, 2019.

The release of the Panama Papers represented a significant media event with unprecedented international coverage. The scandal led to the resignation of Iceland’s Prime Minister and implicated the heads of state and government leaders from Argentina, Saudi Arabia, Ukraine, and the UAE. Hence, from the standpoint of the tourism industry, which is prone to risk factors linked to media events (Brown, 2015; Liu et al., 2021), it is valid and vital to ask what repercussions the scandal had, particularly for a small open economy such as Panama.

In this paper, we present our investigation of whether this concern, with respect to Panama’s tourism exports, is observed by the economic data. Methodologically, we adopt the synthetic control method (SCM), where we compare the tourism variables of Panama with those of an artificially constructed control unit. Abadie et al. (2015) argue that this methodology “provides a systematic way to choose comparison units in comparative studies.”

More fundamentally, we question the development strategy underpinning the Panama Papers scandal—that is, the country’s reliance on the offshore finance industry for economic development. A possible scenario is that the growth of this industry has subjugated other pre-existing industries, such as tourism, by competing for productive resources. In the extant literature, numerous studies have explored this “Dutch disease” phenomena caused by the tourism industry—that is, its de-industrialization consequences (see, e.g., Copeland, 1991; Inchausti-Sintes, 2015; Nowak & Sahli, 2007). In contrast, this paper adds a fresh perspective to this strand of literature by examining the reverse direction of the Dutch disease. That is, the crowding out of tourism by a booming industry (financial services), a topic that has hitherto been scantly addressed in the literature (see, e.g., Dwyer et al., 2016; Forsyth et al., 2014).

To summarize, this paper addresses the detrimental repercussions of the tax haven development strategy adopted by small open economies on their tourism industries from the perspectives of (1) a one-off tax scandal, in relation to the extent to which the Panama Papers scandal negatively affected Panama’s tourism exports; and (2) the long-run crowding-out effect, whereby the thriving financial industries of small open economies may hinder growth in tourism.

Our paper makes three key contributions. Firstly, on methodological grounds, it is among only a few tourism studies that have applied the SCM to measure the impact of a major world event. In doing so, we demonstrate its relevance to the assessment of the impact on tourism and exemplify its potential for future application. Secondly, our findings enrich the tourism risk literature by highlighting the importance of the reputational risk a country may face if it chooses a development model predominantly based on financial secrecy. Thirdly, this paper contributes to a stream of research on tourism and “Dutch disease” by analyzing a distinct context in which services account for the majority of exports and examining the crowding-out effect of financial services on tourism. This is unlike past studies, which have focused on countries with well-established manufacturing sectors and tourism-induced de-industrialization.

The remainder of this paper is set out as follows. Section 2 provides a timeline of the Panama Papers and its subsequent impact. Section 3 outlines the theories underlying the repercussions of a country adopting a tax haven development strategy on tourism. Section 4 describes our methodology and outlines the data. Section 5 reports our results for both the SCM and the panel data analysis. Finally, Section 6 concludes and discusses future research directions.

The Panama Papers Scandal

Prior to the 2008 global financial crisis (GFC), the use of tax havens by multinational enterprises (MNEs) and wealthy individuals was not a salient issue. Although tax havens had been around for many years, their use was deemed a minor issue with respect to international business (IB). For example, IB scholars had typically focused on the four FDI motives (Cuervo-Cazurra & Narula, 2015; Dunning, 1993; Dunning & Lundan, 2008) resource seeking, market seeking, efficiency seeking, and strategic asset seeking FDI; whereas a possible fifth motive, identified by Dunning (1993), linked to escape FDI—a motive typically associated with the use of tax havens—has been somewhat neglected.

This all changed with the onset of the GFC, as the economic shock placed significant pressure on the public finances of several OECD and emerging market countries. For example, in the US, the Debt to GDP ratio grew from 62.6% in 2007 to 105.5% in 2018. Given the state of the public finances and the economic fallout that followed the GFC, the role played by tax havens in the global economy began to receive much greater media attention across the world. Furthermore, high-profile cases implicating some of the world’s biggest multinational companies—such as Amazon, Google, and Starbucks—generated significant global media attention. Recent estimates by Zucman (2015) show that around 55% of the foreign profits of US firms are located in tax havens. The Tax Justice Network estimates that around 25% of US firms’ global profits are shifted out of jurisdictions in which real economic activity takes place, resulting in a global revenue loss of around US$130 billion a year (Cobham et al., 2015). Furthermore, tax evasion fortifies inequality, as affluent households benefit disproportionally by hiding large sums of wealth in tax havens (Ahrens & Bothner, 2020).

The last major tax evasion and avoidance scandal prior to that of the Panama Papers hit the headlines in 2014. The so-called Luxembourg Leaks or “Lux Leaks,” revealed by the ICIJ, implicated over 300 companies with operations in Luxemburg that had reduced their tax bills by shifting profits around their corporate groups and, with the help of the big accounting firms, had secured favorable tax rulings (see Huesecken et al., 2018). But although this scandal started to put the issue of tax avoidance at the front and center of the political debate, it was not until the release of the Panama papers in 2016 that the world media really started to generate significant interest.

The Panama Papers leak scandal broke in April 2016, and it caused a global media sensation. The director of the ICIJ called the leak “probably the biggest blow the offshore world has ever taken because of the extent of the documents” (Bilton, 2016). The leak encompassed 40 years of data from a powerful Panama-based law firm called Mossack Fonseca, which also had offices in over 35 locations across the world. Mossack Fonseca specialized in the creation of shell companies that enabled individuals and firms to create corporate structures suited to hide their beneficial ownership of assets. This enabled individuals and firms to shift capital among corporate groups and into low-tax locations to avoid taxes and to benefit from a veil of secrecy. In total, the leak involved 11.5 million documents detailing financial and attorney-client information pertaining to more than 214,488 offshore entities. Furthermore, the ICIJ created a public database, allowing anyone to access and use it to investigate personal and corporate tax abuse. Using this database, Dominguez et al. (2020) map the network that linked interrelated individuals and companies monoscopically, at the level of countries and geographical regions. They find that the most prevalent offshore jurisdictions were the British Virgin Islands (VGB), Hong Kong (HKG), Singapore (SGP), Indonesia (IDN), the Cook Islands (COK), and Samoa (WSM).

In contrast to the Lux Leaks scandal, the Panama Papers placed a greater emphasis on the individuals who used complex tax avoidance schemes, rather than on the MNEs who also engage in tax avoidance. However, O’Donovan et al. (2019) find that the leak erased US$174 billion in market capitalization among implicated firms. Further scandals, such as the Paradise Papers and the Mauritius Leaks, have emerged since. However, the Panama Papers have undoubtedly had the biggest impact in generating widespread awareness of the scale and nature of the tax avoidance perpetrated by high net-worth individuals and MNEs.

Literature Review

This paper presents an examination of the detrimental impact of a tax haven development strategy adopted by small open economies on their tourism industry. In essence, this is a multifaceted topic. For tourism practitioners, the growth of offshore finance brings about reputational risk to the destination, rendering its tourism industry susceptible to one-off shocks. Furthermore, over the long run, the growth of the financial services industry in resource-constrained economies depresses and may even crowd out any growth opportunities for the tourism industry. To delineate these issues as thoroughly as possible, we draw from several strands of literature concerning Dutch disease, tourism risk, and impact assessment.

Tourism and Offshore Finance: Complementary or Competing?

The economic development of a tax haven appears to relate to a growth in tourism. Tourism and offshore finance conveniently share similar prerequisites, such as a favorable location, good transport links, and advanced information and communications technology (ICT) (Hampton & Christensen, 2007). Given the need for face-to-face meetings between offshore service providers and the wealthy clientele they aim to attract, the offshore finance industry requires the local economy to provide high-end recreational facilities, such as luxury hotels, spas, and golf courses. These enable wealthy individuals to make repeated visits, stay for extended periods, and even establish residence (Barber, 2015; Hampton & Christensen, 2002). In this sense, tourism and offshore finance would appear to complement one another.

From a historical perspective, the early tourism development of many islands has often been linked to the transformation of their economies (to shift away from traditional exports, such as sugar and copra, and toward mass tourism) and to their uptake as playgrounds of the rich (i.e., the “pleasure periphery”) (Hampton & Christensen, 2007; Mcelroy, 2003). Once settled, this first wave creates demand for a “pinstripe infrastructure” of specialist legal and financial services firms. This demand is met by bankers and tax accountants who are attracted to the islands by the climate and lifestyle (Hampton & Christensen, 2002), creating a skill pool for the subsequent development of offshore financial services. At the same time, many islands are encouraged by powerful financial institutions to diversify into non-traditional activities, such as offshore finance, as a development strategy and a means to capitalize upon the benefits associated with the capture of highly mobile capital (Barber, 2014; Mcelroy, 2003). The synergy between the needs of the wealthy for both an exotic playground and a sophisticated financial infrastructure generates a virtuous circle that strengthens the growth of the local economy through a positive feedback loop (Hampton & Christensen, 2007).

However, akin to the Dutch disease model developed by Corden and Neary (1982) and Copeland (1991), an alternative scenario is conceivable whereby the financial industry gradually “crowds out” the tourism industry, as they compete for scarce factors of production (this is the resource movement effect described in Corden & Neary, 1982; Forsyth et al., 2014). Generically, Dutch disease posits that a booming sector in an economy attracts factors of production from other sectors (i.e., lagging and non-tradable segments), generates foreign exchange earnings, and leads to a real appreciation in the exchange rate, eroding the external competitiveness of traditional exports (the lagging sector); meanwhile, to the disadvantage of the lagging sector, the income generated in the expanding sector increases domestic demand for non-tradable goods and, accordingly, increases the derived demand for factors of production, further shifting resources away from the lagging sector (Inchausti-Sintes, 2015). Hampton and Christensen (2007) explore the possibility of the crowding-out effect on tourism in the context of the British Channel Island of Jersey. They argue that one mechanism whereby the effect unfolds is through inter-industry wage differentials, whereby the high costs of human resources (caused by the generously paid financial industry) crowd out the scope for the development of tourism. Another mechanism is affected through the soaring prices of land (and of the housing market) brought about by its limited supply, which exacerbates the problem of retaining local labor in lower-paid industries, given the differentials between the purchasing power of financial industry workers and tourism employees. Notwithstanding, a further mechanism is linked to access to capital. Early in their development, investment in both industries is drawn mainly from local capital resources. As they both grow, there tends to be an increasing concentration of capital. This requires international capital to play a more prominent role that leads it to dominate the political economy of particular islands.

The extant literature on tourism and Dutch disease is predominantly centered on tourism-induced de-industrialization—that is, the crowding-out effect of tourism on the manufacturing sector (see Zhang & Yang, 2019). Notable exceptions to this literature investigate this issue in reverse. Dwyer et al. (2016) and Forsyth et al. (2014), estimate the effect of Australia’s mining boom on its tourism industry using a Computable General Equilibrium (CGE) modeling framework. In their study, a legacy of the mining boom saw the leisure and tourism industries face not only supply-side issues (attracting and retaining skilled labor, attracting sufficient capital/investment to meet the industries’ future growth and a contraction in the availability of airline seats and beds for tourists as they became fully occupied by mining workers), but also demand-side issues in relation to a reduction in inbound tourism and a rise in outbound tourism due to an appreciation in the Australian dollar. However, the literature has not investigated the Dutch-disease effects of finance (particularly illicit finance) on tourism, a gap this current study sets out to fill.

The Impact of Risks on Tourism in Tax Havens

The perception of risk is recognized as one of the main factors influencing tourist decision-making (Slevitch & Sharma, 2008; Williams & Baláž, 2015). Risks in tourism can be associated with natural disasters, disease, pollution, corruption, crime, riots, terrorist attacks, and even wars (Cao, 2022). Faced with a certain level of perceived risk, tourists (as consumers) adopt a range of strategies aimed at reducing such risk to tolerable levels (Fuchs & Reichel, 2006; Slevitch & Sharma, 2008). At the aggregate level, any changes in tourists’ travel intentions and behaviors in response to a rise in perceived risk can detrimentally impact the effective aggregate tourism demand for a destination.

A growing body of literature in tourism research examines the effect of country-level risk on aggregate tourism demand, especially from the perspective of institutional quality and political risk. One strand of such literature argues that good governance/institutions and a favorable political environment are crucial determinants in attracting international tourists (Ghalia et al., 2019). Accordingly, social unrest/protests, civil wars, perceived violations of human rights, or the perceived likelihood of these situations are all examples of instances that deter tourists. Conversely, another strand of literature argues that, under certain circumstances, lower institutional quality can be beneficial to tourism (Ghalia et al., 2019). Hence, there is ambiguity. For example, corruption can help facilitate business activity and increase the speed of transactions that lie outside of regulatory frameworks. In this respect, corruption may have a positive side effect of enabling tourists to enjoy goods and services that would have otherwise been unavailable. Unsurprisingly, this type of tourism is often associated with illicit or criminal activities.

Empirical evidence indicates that low levels of political risk (e.g., political stability) and high-quality institutions (e.g., low corruption, government effectiveness, and regulatory quality) are beneficial to the operation of tourism businesses and the inflow of tourists (Ghalia et al., 2019; Saha & Yap, 2014; Tang, 2018). However, as Lee and Chen (2021) do in a quantile regression framework, other kinds such as economic and financial risks can have a more salient effect than political ones, especially on those countries with high levels of tourist arrivals.

For small open economies, success in both tourism and offshore finance depends on external perceptions of political stability. Negative risk perceptions affect both tourism demand and the wealthy’s willingness to use an island as a tax haven (Hampton & Christensen, 2007). As Hampton and Christensen (2002) note, many tax haven governments have gone to great lengths to promote the growth of the offshore financial industry, often without properly considering the adverse impact (e.g., reputational effect, crowding-out effect) on other industries. Capó et al. (2007) make a similar point that over-reliance on an emerging, tradable sector can make the economy extremely vulnerable to external disturbances. Following this line of thought, we add quantitative evidence to the literature on tourism risk by demonstrating an additional risk factor not touched upon previously, that is, the reputational risk that a country may face should it opt for a development strategy predominantly based on financial secrecy.

Impact Assessment of Negative Events

The negative risk perceptions of a destination may be prompted by a variety of factors or sudden events, ranging from natural disasters, disease, social unrest, and terrorist attacks to a deterioration in the terms of trade and a rapid increase in commodity prices. Negative events create a negative image that decreases tourism demand and causes economic loss. Drawing from the Awareness-Perceived Egregiousness-Boycott (AEB) framework (Klein et al., 2004), Su et al. (2022) argue that the management of a tourism destination may lack ability or ethics, causing all stakeholders to suffer negative and harmful consequences. Through three experimental studies, they find that negative moral events (i.e., failures to meet quality/moral standards) produce stronger perceptions of betrayal and a greater propensity for tourism boycott than negative competence events (i.e., failures to fulfill the functional needs of stakeholders) would do. In the case of a negative moral event, tourists form a negative view of any wrong behavior that has occurred in a tourism destination and then judge the egregiousness of such behavior based on its possible consequences, which leads to a negative emotional shift. Furthermore, as Su et al. (2022) explain using the image-imagery duality model, individuals may associate any memories of negative events with a destination to form a negative perception that impacts such destination’s image as well as their own emotional and cognitive responses.

Empirical studies have investigated the effects of a wide range of negative events. For instance, Song, Gartner, and Tasci (2012) examined the effect of stricter visa restrictions in China in 1989 and 2008 and found there to be a 7% to 33% reduction in tourist arrivals across various source markets. In respect of terrorist attacks, Araña and León (2008) found that the 9/11 attacks in New York caused a significant decrease in the utility of tourists planning to travel to Mediterranean destinations and the Canary Islands; consequently, there had been an approximately 25% decline in the willingness to pay for an average holiday package. Wang (2009) investigated a series of crisis events that had taken place in Taiwan and found that the decline in tourist inflows had been greatest during the outbreak of a severe acute respiratory syndrome (SARS) pandemic, followed by the 1999 earthquake and the September 11, 2001 attacks, whereas the impact of the Asian financial crisis had been relatively mild.

Methodologically, the literature that investigates tourism impact assessment is commonly conducted by means of the input-output (I-O) and computable general equilibrium (CGE) methods, which are suited to estimate the economy-wide impact of any demand shocks (Li & Song, 2013; Song, Dwyer et al., 2012). Further, time series econometric methods, such as the autoregressive distributed lag (ARDL) models (e.g., Smeral, 2010; Song & Lin, 2010), are also adopted to delineate economic impact. A recent methodological development in impact assessment is the synthetic control method (SCM), developed by Abadie and Gardeazabal (2003) and Abadie et al. (2010) for policy analysis. This method is rarely applied in tourism research, with the exceptions of Biagi et al. (2017) and Albalate et al. (2022).

A tax scandal like the Panama Papers leak, which has attracted widespread global media coverage, is likely to affect Panama’s image negatively and is expected to diminish the country’s tourism activities. Cognitive appraisal theory (Lazarus, 1991) posits that an individual’s reaction to an event follows a cognition-emotion-behavior sequence. Tourists’ first impression of a destination is likely to originate from the media, which, by packaging news in ways that promote a particular understanding of reality, ignite particular feelings and can influence tourists’ travel intentions (Brown, 2015). In the wake of an unethical incident, Breitsohl and Garrod (2016) found that tourists’ first reaction will be to engage in cognitive evaluations, including their perceptions of the degree of severity of the incident, the image that is publicized by the destination and on whom they place the blame. Subsequently, an emotional response occurs. Tourists will likely develop hostile feelings (such as anger, contempt and disgust) toward the destination and opt to either avoid the destination on emotional grounds or even spread negative views of it. Therefore, once an unethical incident occurs, the subsequent tourism crisis harms not only the destination’s image but also the sustainable development of its tourism industry (Liu et al., 2021).

No studies appear to have hitherto specifically focused on unethical events in tax havens, and none have quantified Panama’s exposure following the huge data breach. Our research contributes to the literature on tourism impact assessment by providing evidence of the impact of a major tax scandal. Specifically, it demonstrates the suitability and relevance of SCM as a valuable additional tool for tourism impact studies.

Methodology

In this research, we perform two sets of analyses. The first involves the SCM, a tractable data-driven procedure designed to assess the impact of events and policy interventions—for example, that of terrorism in the Basque country (Abadie & Gardeazabal, 2003) and that of the introduction of a city tax on tourism demand in Italy (Biagi et al., 2017). As the Panama Papers scandal was a major world news event, we use the SCM to measure the extent to which it caused Panama to deviate from its original development trajectory. The second set of analysis utilizes panel data drawn from a sample of 20 small open economies over a period of 19 years to determine whether a booming financial industry crowds out growth opportunities for the tourism industry. Our panel data analysis enables us to determine whether this pattern is observed across several small open economies.

The Synthetic Control Method

In studying the effects of historical events and policy interventions on aggregate units, researchers often compare the outcomes of the unit affected by the event or intervention (i.e., the treated unit) with those of the unaffected units (i.e., the control units). The SCM involves a data-driven procedure that constructs a counterfactual synthetic control unit by taking the weighted average of a pool of control units, such that the synthetic control unit closely proxies the treated unit in terms of their economic profiles (characterized by outcome variables and relevant covariates) in the pre-intervention period. Henceforth, the values of the outcome variables of the synthetic control unit inferred for the post-intervention period represent the counterfactual values that the treated unit would have otherwise exhibited in the absence of the event or intervention. Accordingly, one can measure the effect of the event or intervention by calculating the difference between the outcome variables of the treated unit and the synthetic control unit for the post-intervention period.

Following Abadie et al. (2010, 2011), suppose we have observations for j + 1 units (j = 1, 2, …J + 1) for time periods t = 1, 2, …, T. We assume that j = 1 is the treated unit and j = 2, 3, …J + 1 the control units. The pool of control units is termed the donor pool. The intervention occurs at period T0 + 1. Hence, t = 1, 2, …T0 are the pre-intervention periods and T0 + 1, T0 + 2, …T the post-intervention periods.

Define Yjt as the observed outcome variable for unit j,

where

Consider that

where

Define a J × 1 vector of weights

In the implementation of SCM, let

For our study, we chose Panama, the country at the epicenter of the scandal, as the treated unit. To construct the synthetic control unit, we assembled a donor pool of control units each of which met at least one of the following criteria:

(i) The country was located in the Central America region (as defined by UNWTO, 2018) or neighbored Panama.

(ii) The country had at some point been on the European Union’s (EU) black and gray lists of non-cooperative tax jurisdictions (European Commission, 2021).

(iii) The country was mentioned in the Panama Papers (ICIJ, 2021) as one of the jurisdictions used by the compromised Mossack Fonseca law firm.

The control units, therefore, resemble Panama in terms of geography, level of economic development, and dependence on tourism and offshore financial services. The above criteria resulted in 20 countries being included in the donor pool. They were: Australia, Colombia, Costa Rica, Cyprus, Ecuador, El Salvador, Guatemala, Hong Kong, Jordan, South Korea, Malta, Mongolia, New Zealand, Nicaragua, Peru, Singapore, Thailand, Turkey, the United Kingdom, and Uruguay.

Regarding the estimation, we implemented the SCM on real tourism exports, the outcome variable (Yjt). For the observed covariates (

We collected quarterly data for Yjt and

Panel Data Analysis

We approach the crowding-out effect by estimating the causal effect of financial services exports on tourism. The export volumes of economies dependent on international trade provide a good indication of the size of the relevant industries. Given the absence of any readily available data directly linked to the scale of offshore financial services or illicit financial flows, we opted to use financial services exports as a proxy for offshore financial services. The volume of the financial services exports of tax havens embodies both the development of their financial industry and their ability to handle financial flows, including illicit ones.

Our sample includes many small open economies with dominant tourism industries, considerable offshore financial activities, or both. To identify those economies in which offshore financial activities were highly active, we referred to the EU’s black and gray lists of non-cooperative tax jurisdictions (European Commission, 2021) and the Panama Papers (ICIJ, 2021). Initially, we identified 40 such economies; however, we then had to discard 20 of them due to the unavailability of key data, leaving the following in the final sample: Australia, Botswana, Colombia, Costa Rica, Guatemala, Hong Kong, Jamaica, Jordan, Korea, Malta, Mongolia, Namibia, New Zealand, Panama, Peru, Singapore, Thailand, Trinidad and Tobago, the United Kingdom, and Uruguay.

To model the causal relationship, we follow the line of empirical research, reviewed in section 3.2, that examines the effects of macroeconomic variables and country risk on tourism (e.g., Ghalia et al., 2019; Lee & Chen, 2021; Tang, 2018) and thus specify our panel data model as the following equation:

where

Considering the possibility of reverse causality running from real tourism exports to real financial services exports (hence, real financial services exports potentially being an endogenous variable), we use automated teller machines (ATMs) per 100,000 adults as an instrumental variable (IV) for the estimation. This variable satisfies the validity requirements for an IV:

instrument exogeneity Cov(IV, u) =0: the number of ATMs in a country does not directly impact its tourism development, as the variable does not constitute a pull factor that attracts overseas tourists;

instrument relevance Cov(IV, x) ≠0: the number of ATMs in a country reflects the ease of access to banking services and can serve as an indicator of the development of the financial industry.

For the variables in the model, we collected annual data from international databases: the IMF’s International Financial Statistics, the IMF’s Balance of Payments Statistics, the World Bank’s World Development Indicators, and the PRS Group’s International Country Risk Guide (ICRG). The sample period is 2001 to 2019. The details of the variables, such as definitions and measurements, can be found in Table A1 in the appendix. Moreover, the descriptive statistics are reported in Table A2.

Results and Discussion

The Impact of the Panama Papers

Tourism is one of Panama’s pillar industries, contributing 14.5% of the country’s GDP and 14.4% of the country’s total employment in 2018 (WTTC, 2020). Panama attracts tourists because of its extraordinary landscapes, vast biodiversity, and rich cultural heritage; it is also a center of coastal, cultural, health, and eco-tourism (Klytchnikova & Dorosh, 2012). Compared with other tradeable goods industries, tourism has the highest multiplier effect on Panama’s economy (Klytchnikova & Dorosh, 2012).

As per the SCM procedure, we constructed a synthetic control unit by taking the weighted average of the control units in our donor pool. Table A3 in the appendix reports the weight allocated to each control unit. In carrying out our estimation, we chose 2016Q2 as the timing of the event T0 + 1, given that the first news stories pertaining to the scandal had been published at the beginning of April 2016. Accordingly, our sample’s pre-intervention period is 2012Q1 to 2016Q1, and the post-intervention is 2016Q2-2019Q4. Table A4 in the appendix provides a comparison between the treated unit (Panama) and the synthetic control unit. The closeness between their mean values, together with the small MSPE, indicates that our synthetic control unit is a good approximation for Panama.

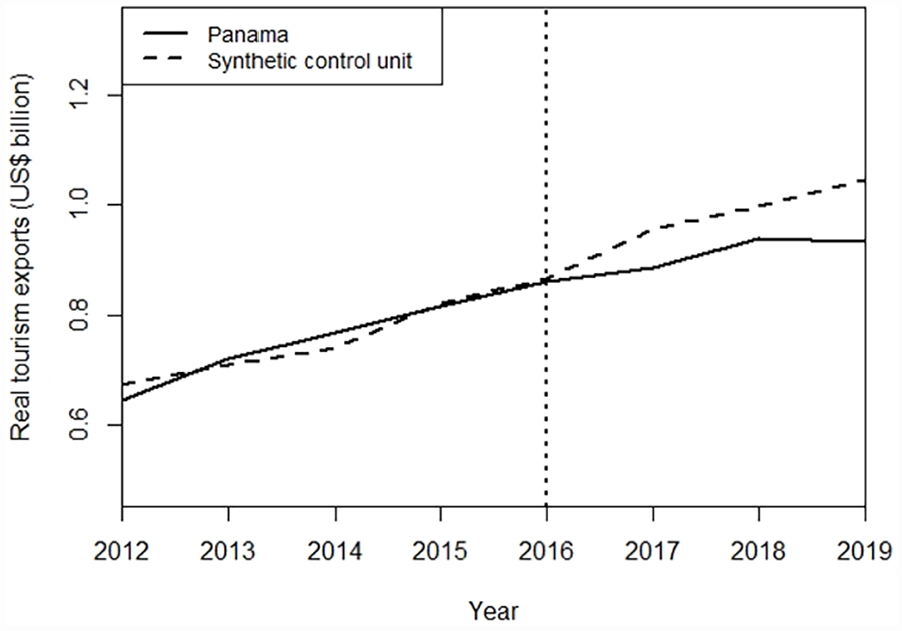

The effect of the Panama Papers scandal on the country’s tourism exports is visually captured in Figure 2, where the gap between the solid line (for Panama) and the dashed line (for the synthetic control unit) represents the unrealized tourism exports.

Growth path of tourism exports: Panama versus synthetic control unit.

As seen in Figure 2, in the wake of the release of the Panama Papers, Panama’s actual tourism exports trend (solid line) was still positive, gradually rising from US$ 0.85 billion (in real terms) in 2016Q2 to US$ 0.94 billion (in real terms) in 2018Q1 and reaching a plateau thereafter.

Despite the scandal, the push and pull factors of tourism in Panama have not significantly changed. The splendid landscapes, the rich cultural heritage and improved infrastructure still make the country a prime destination, with tourists keen to take advantage of those resources continuing to visit. Moreover, as Pizam and Smith (2000) discuss in the context of terrorism—as another type of negative event—travel arrangements may have been prepaid before an event and may be non-refundable. Hence, a considerable visitation volume may still be observed. Consequently, the tourism exports of a country may not immediately decline.

Nevertheless, compared with the synthetic control unit (dashed line), the actual values of Panama’s tourism exports (solid line) have been negatively affected, being 0.8%, 7.4%, 5.9%, and 10.7% lower than those observed for the synthetic control unit in 2016, 2017, 2018, and 2019, respectively. This suggests that, had the Panama Papers not been released, Panama’s tourism exports would have grown at a much faster pace. This finding corroborates the conjecture—presented in Section 3.3—that the Panama Papers scandal had negatively affected Panama’s tourism.

As noted in section 3.2, tourism is vulnerable to a variety of risks, with the extant literature tending to focus on those associated with natural disasters, diseases, terrorist attacks, and social unrest. The SCM results above confirm that a tax scandal constitutes an extra layer of risk to the tourism industry, one that is inherent to tax havens. The image of tax havens in the popular mind is largely associated with their role in facilitating tax evasion by individuals (Dharmapala, 2008). A tax scandal like the Panama Papers reinforces the popular perception of tax havens being unethical. Following the cognition-emotion-behavior mechanism (Breitsohl & Garrod, 2016; Su et al., 2022) described in section 3.3, it can be argued that, when faced with a tax scandal in a destination, some tourists may form a negative perception and change their travel decisions accordingly—for example, by postponing or canceling their visits—especially at times when public awareness of illicit activities (e.g., tax evasion and money laundering) is heightened and those activities are under strict scrutiny. Furthermore, some tourists may develop hostile emotions toward a destination (Van Fossen, 2003) or simply avoid any unnecessary visits, eventually dampening that destination’s tourism exports. In section 5.2, Table 1, we also present evidence of such a dampening effect. All in all, the SCM results corroborate Breitsohl and Garrod’s (2016) and Su et al.’s (2022) findings about tourists’ reactions toward an unethical destination incident, a largely underexplored issue.

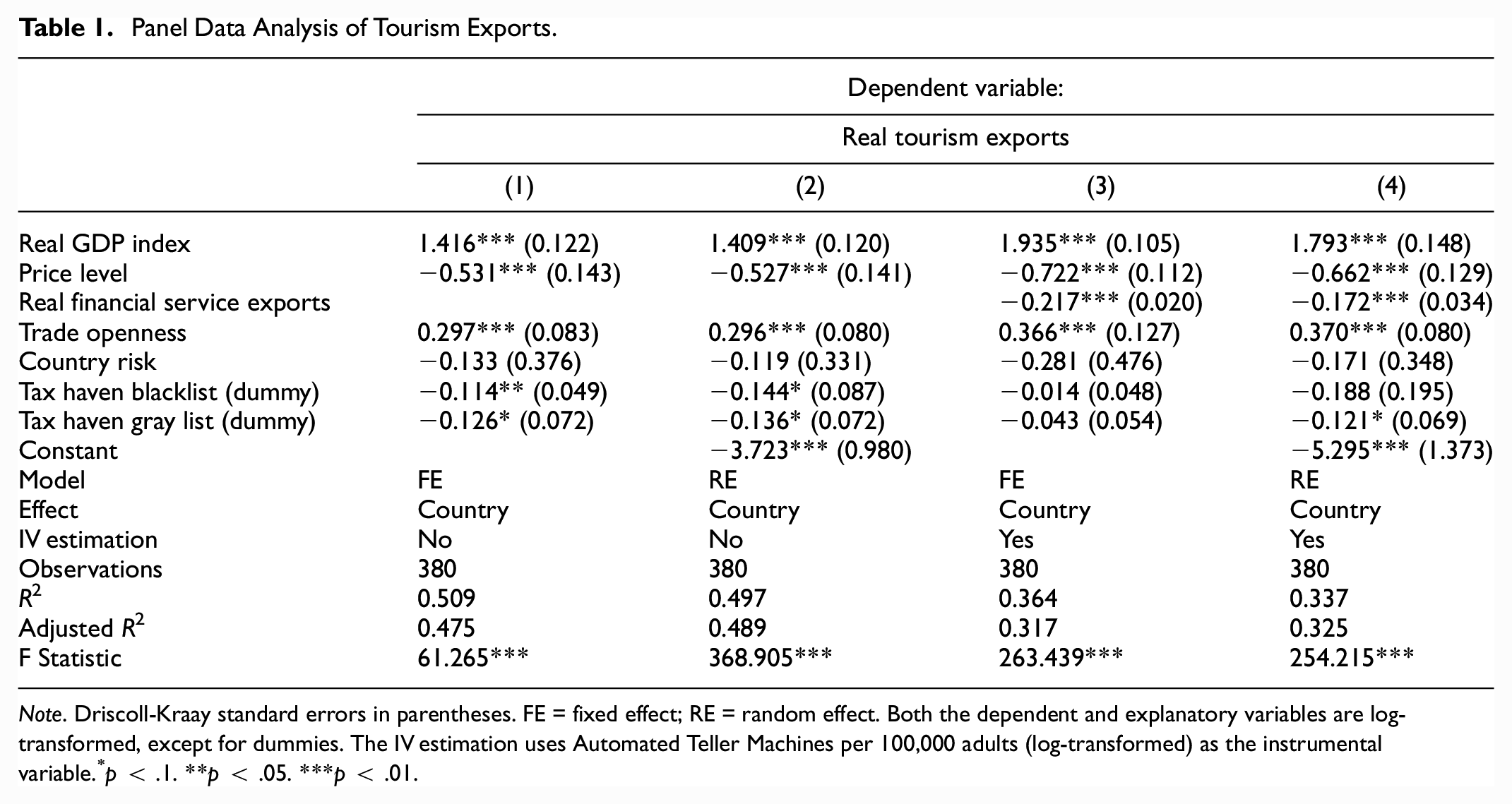

Panel Data Analysis of Tourism Exports.

Note. Driscoll-Kraay standard errors in parentheses. FE = fixed effect; RE = random effect. Both the dependent and explanatory variables are log-transformed, except for dummies. The IV estimation uses Automated Teller Machines per 100,000 adults (log-transformed) as the instrumental variable.

p < .1. **p < .05. ***p < .01.

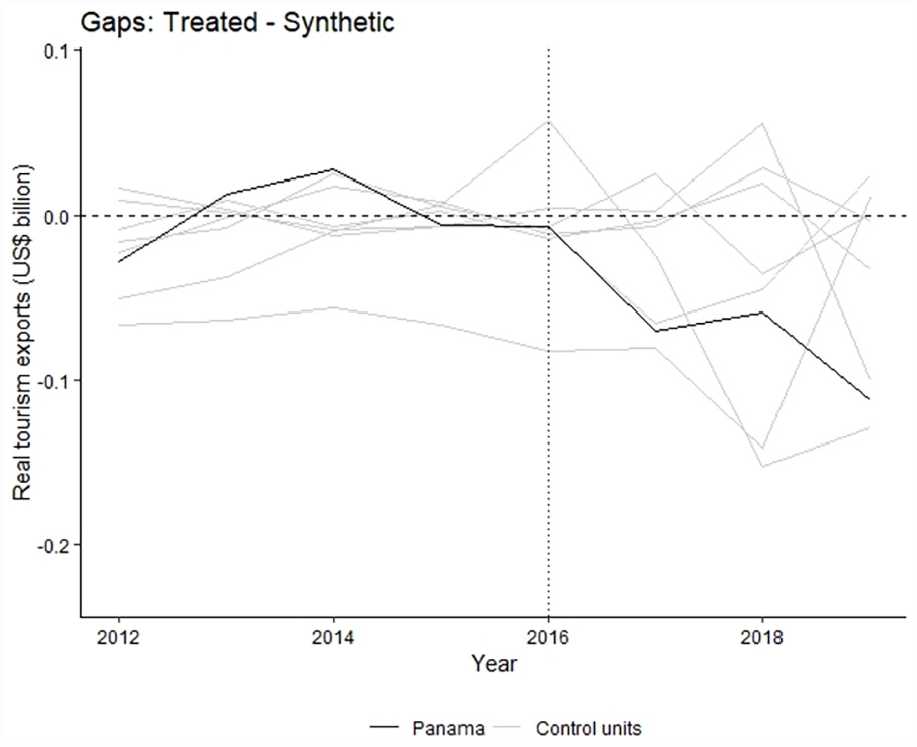

To further confirm our findings illustrated in Figure 2, we conducted a series of placebo tests where we reassigned the intervention to the control units in the donor pool, effectively measuring the equivalent effect of the scandal on their economies. We carried out these tests by iteratively replacing Panama with each economy in the donor pool (excluding Panama), one at a time, and re-estimating the SCM model to generate the placebo effect, which we calculated as the gap between the placebo and its corresponding synthetic control unit. We then compared the effect on each placebo with that of Panama. Ideally, the former should be trivial, whereas the latter should be much larger, so that we can be confident that the effect observed on Panama had not been driven by random chance.

Figure 3 presents the placebo effects (gray lines) and that of Panama (black line). Each line captures the gap between each economy and its synthetic counterpart, the wider the gap, the larger the effect of the event. For Panama, the absolute value of the gap since 2016 was found to be discernibly greater than zero, indicating a causal effect from the scandal. For most of the control units (as placebos), the gaps were found to fluctuate closely around zero, suggesting an absence of any effect from the scandal. We did however find that, in the case of Peru, the line peaked in 2016, before sharply declining to below −0.1 in 2018; a gap as large as that of Panama. This shows that the scandal may have had a spillover effect. Interestingly, like Panama, Peru is both a prominent tourism destination (for its landscape and cultural heritage) and a tax haven identified in the EU’s lists between 2016 and 2019 (the period over which the placebo effect was examined). In contrast, the placebo tests did not yield a dampening effect on the tourism exports of those countries in the proximity of Panama but not on the tax haven list—such as Costa Rica, Nicaragua, and Ecuador. Therefore, the spillover effect seems more likely to have been transmitted to other regional tax haven locations, in this case Peru, rather than non-havens.

Gaps in tourism exports between the treated unit and the synthetic control unit.

The Crowding Out of Tourism by Financial Services

Having found that the Panama Papers scandal hampered the growth path of Panama’s tourism, in our second piece of analysis we address the more fundamental question of whether the tax haven development model is detrimental to other pre-existing industries in small open economies.

Table 1 presents the results from the panel data analysis performed on 20 small open economies across the world for the 2001 to 2019 period. The dependent variable, real tourism exports, can be interpreted as an indicator of both inbound tourism demand and tourism development. The estimated coefficients were found to be generally consistent across the four models. Between Models 1 and 2, the Hausman test (χ2 = 3.5178, df = 6, p-value = .7416) was found to suggest the appropriateness of Model 2 (the random effects model). For Models 3 and 4, the Hausman test (χ2 = 15.481, df = 7, p-value = .0303) was found to be less clear-cut. If we used a significance level of 0.01, the null hypothesis that the random effect model—Model 4—is preferred was found to be accepted; if we used 0.05, the null hypothesis was found to be rejected. Considering that both models were found to report similar results, we mainly refer to Model 4 in the interpretation provided below.

Among the independent variables, the real GDP index, price level, and trade openness were found to be highly statistically significant. In particular, the real GDP index (a proxy for the level of economic development) and trade openness were found to be a positive influence on tourism exports, while the general price level was found to have a negative effect. These findings are consistent with those in the existing literature (for the latest review, see Rosselló Nadal & Santana Gallego, 2022).

The coefficients on country risk were found to be statistically insignificant. A possible explanation for this is that, as reviewed in section 3.2, the effect of country-level risk (especially with respect to institutional quality and political risk) is ambivalent at the very least. Good institutions and a stable political environment improve a destination’s image and attract more tourists. However, in those instances in which the nature of the visit is suspicious due to the possible involvement of illicit or criminal activities, higher institutional quality may not be favorable. In the extant literature—for example, Ghalia et al. (2019) and Lee and Chen (2021)—country risk-related variables are also observed not to be unequivocally significant.

In terms of the ways in which being a tax haven affects tourism, the two dummies tax haven blacklist and tax haven gray list provide an indication. The coefficients for both variables were all found to be negative—albeit not necessarily significant—across the four models. Being identified as a non-cooperative jurisdiction signifies that a destination’s economy has yet to comply with international tax standards and lacking good tax governance. In this respect, even though tourists may not be overly sensitive to wider institutional quality, as captured by the country risk variable, some may still be averse to being associated with unethical tax practices. Consequently, as suggested by the estimated coefficients, once a destination is recognized as a tax haven, it will experience a drop in its tourism exports of up to 14.4% below what could be otherwise expected. This finding is consistent with those found in the preprint by DePaul et al. (2022), who ascribe the reductions in tourism activities in the tax havens included in the EU’s lists to the reputational costs of such blacklisting.

As a destination continues to grow its financial industry to serve its wealthy clientele, resources will be diverted to this burgeoning sector, hindering the growth of others. Model (4) suggests that, across our 20 small open economies and over the 19-year sample period, a 1% rise in real financial services exports can cause a 0.172% decline in real tourism exports. This finding supports the hypothesis, made by Hampton and Christensen (2007, p.1013), that the process of “financial capital establishing itself as the political hegemon reinforces the process of crowding-out pre-existing competitor industries such as tourism” by virtue of the resource movement effect reviewed in section 3.1. Moreover, in the literature on Dutch disease, another mechanism underpinned by the spending effect is also noted (see Corden & Neary, 1982; Forsyth et al., 2014). A booming financial industry’s higher factor payments (e.g., wages, interests, rents, and profits) lead to a rise in real income and aggregate demand and, ultimately, in a real appreciation of the exchange rate, which reduces tourism exports.

An interesting observation we draw from the results presented in Table 1 is that the tax havens dummies appeared to lose their statistical significance when the real financial service exports variable was added to the model, which prompted our suspicion of potential multicollinearity issues. To check for such issues, we calculated the variance inflation factor (VIF). We found the VIF values for real financial service exports, tax haven blacklist, and tax haven gray list to be 1.202, 1.506, and 1.396, respectively. Similarly, we found the VIF values for other variables to also fall below the threshold level of 5. All this suggests an absence of any multicollinearity in the regression models. One possible alternative explanation for the observed phenomenon is that the crowding-out effect captured by the real financial service exports variable is common across all small open economies, not only tax havens. Hence, this variable serves as a stronger (statistically significant) factor than the tax haven dummies in terms of explaining the tourism exports of small open economies.

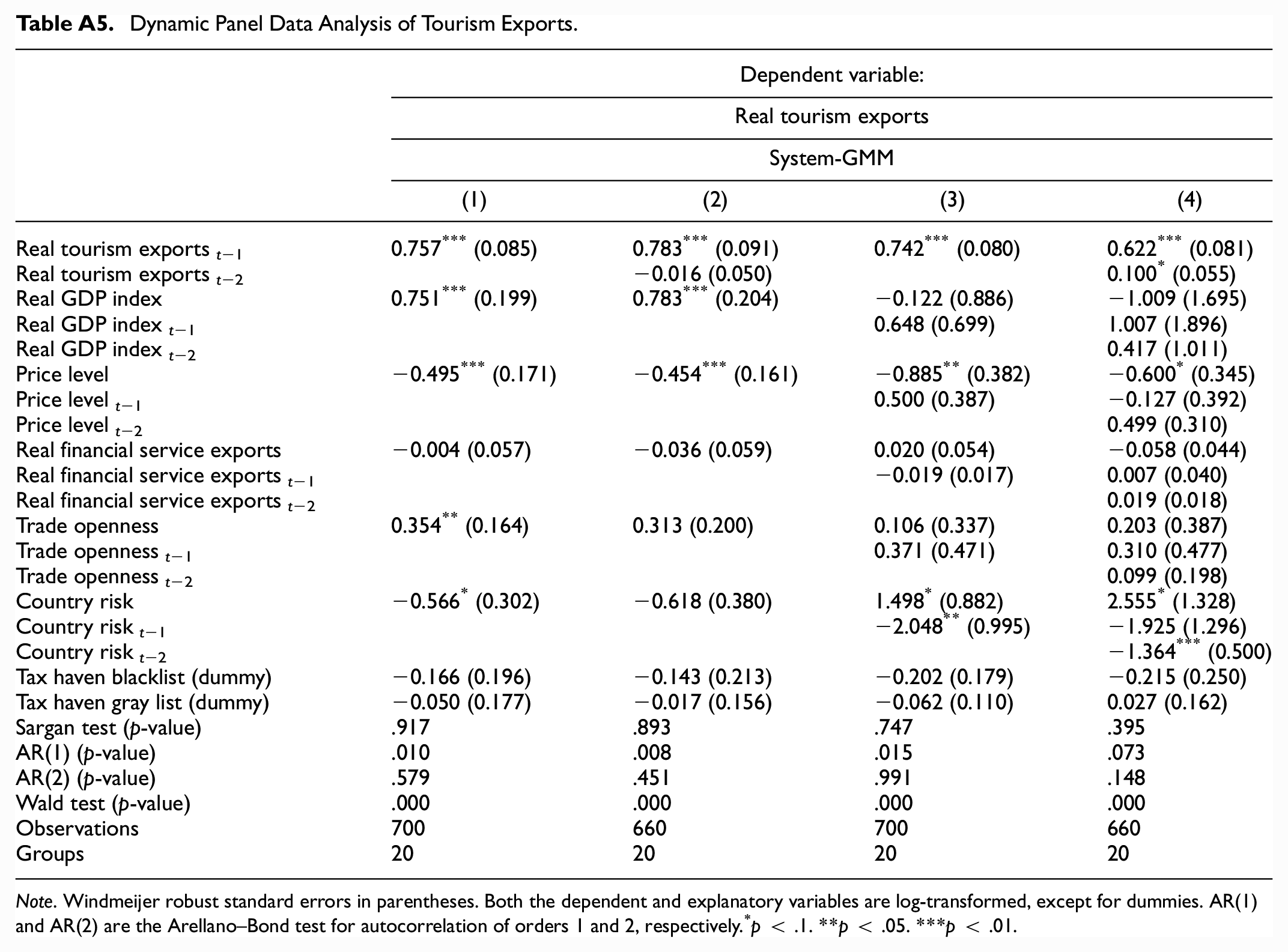

To supplement our static analysis in Table 1, we estimated additional dynamic panel data models, which augmented the static model of Equation (3) by including lagged dependent and independent variables. We followed the practice reviewed in Gallego et al. (2019) and used the system-GMM estimator, 1 which is considered to improve efficiency over other estimators such as the difference-GMM. The results are presented in AppendixTable A5. The Sargan test and the Arellano–Bond AR(2) test suggest acceptance of their respective null hypothesis, meaning there is no concern over overidentification and autocorrelation. A notable pattern is that the first lag of the dependent variable, Real tourism exports t−1, is statistically significant across all model specifications, whereas the independent variables recede into having smaller coefficients (in absolute values) and becoming less significant, or even insignificant; their lags also tend to be statistically insignificant. It is documented and discussed at length by Achen (2000) that the inclusion of lagged dependent variables often suppresses the original sensible substantive effects of other variables. This downward bias is common in time series applications in social sciences. Unfortunately, there is no definitive answer as to whether the significant lagged dependent variables have real explanatory power in this instance.

Nonetheless, the coefficients generally have the expected signs consistent with those obtained from the static models. The negative sign on the real financial service exports and the tax haven dummies variables indicates the possibility that the growth of financial services could crowd out tourism growth and the tax haven blacklisting could cause reputational harm. These effects are, however, not statistically significant from the short-run dynamic point of view; they are much stronger over the long-term horizon (as captured by the static models). A probable explanation could be that it takes time for the crowding out and the reputational costs to take effect. This resonates with our findings in section 5.1 from the SCM analysis, where we found that the harm to Panama caused by the Panama Papers was relatively small in the first 3 years and much bigger in the fourth year. Given that our aim is to establish the long-term interplay between financial services and tourism, we rely on the static models in Table 1 to draw conclusions and use Table A5 as a supplementary reference to gain additional insights.

The finding pertaining to the crowding-out effect of financial services on tourism offers a new perspective for the study of Dutch disease. As noted in section 3.1, the extant tourism literature tends to focus on the classic example of tourism-induced de-industrialization in a two-sector (manufacturing and tourism/services) or three-sector (agriculture, manufacturing, and tourism/services) model framework. Those studies were based on the implicit assumption that the economies they investigated had well-developed manufacturing sectors. However, our sample of tax havens constitutes a distinct context where there is an absence of a prominent and competitive manufacturing sector. Hence, our results make it worth considering the Dutch disease effects in a setting where services dominate.

Conclusions

The leak of the Panama Papers caused a global media sensation with far-reaching implications on the economic, political, and even cultural spheres of Panama. In our study, we address the repercussions of a tax haven development strategy adopted by small open economies on their tourism development from the perspectives of (1) a one-off tax scandal, investigating the extent to which the Panama Papers scandal had negatively affected Panama’s tourism exports; and (2) the long-run crowding-out effect, to determine whether a booming financial industry in small open economies hinders the growth of tourism exports.

In our study, we make several original contributions to the literature. First, to measure the impact of a media scandal, we applied the SCM—which is increasingly being used in the economics and social sciences literature—as a valuable addition to the set of tools for assessing the impact of tourism. Second, we analyzed the aftermath of the Panama papers scandal and found evidence of a negative reputational impact on the tourism exports of Panama. This finding adds to the literature on tourism risk factors by confirming that a major tax scandal can constitute an additional risk factor faced by countries that choose a development strategy linked to illicit financial flows. Finally, by analyzing the crowding-out effect of financial services on tourism, we bring a fresh perspective to the literature on tourism and Dutch disease. In contrast to the tourism-manufacturing settings adopted by the extant tourism literature, tax havens offer a distinct context for the study of the Dutch disease in service-based economies. We hope that our study will stimulate further discussions about the development strategy and inter-industry relations of small open economies.

Panama’s tourism exports grew sluggishly in the wake of the scandal. By using the SCM, we found that, compared with levels that could otherwise have been expected to be achieved, Panama’s tourism exports for 2016, 2017, 2018, and 2019 were lower by 0.8%, 7.4%, 5.9%, and 10.7%, respectively. The tax scandal caused some tourists to change their travel decisions by either postponing or canceling their visits to Panama; they may have done so due to the formation of a negative perception of the destination and a reluctance to be associated with unethical incidents, especially during a time when public awareness of illicit activities was heightened, and those activities were under tighter scrutiny.

Furthermore, the results of our panel data analysis of a sample of 20 small open economies over 19 years provide evidence that being identified as a tax haven (e.g., due to being in the EU’s black/gray list) entails reputational costs, lowering a country’s tourism exports by up to 14.4% over the long run, compared with the normal level it would have otherwise achieved. More fundamentally, our findings question the effectiveness of using a tax haven development strategy with an over-reliance on offshore finance as a pillar of the economy. Our panel data analysis confirms the crowding-out effect of a growing financial industry on other industries, such as tourism. We found that, for small open economies, a 1% rise in real financial services exports generally causes a 0.172% fall in real tourism exports.

Our findings highlight how a government’s prudential risk management can reduce the turbulence potentially experienced by the country’s tourism industry. The tourism industries of those economies profiting from financial secrecy could face additional risks in terms of unethical incidents and scandals, which entail reputational damage and even increased macroeconomic instability. The preliminary work by DePaul et al. (2022) also highlights a similar danger of being named and shamed by the blacklists of international organizations, which can hurt a country’s tourism exports. The COVID pandemic has yet again reminded us that economies (especially small open ones, as examined in Gounder & Cox, 2022) are constantly subject to vulnerabilities. As small open economies strive to revive their tourism industry in the post-COVID world, it is vital for tourism practitioners to assess the risk factors that they may face on their path to a full recovery and to consider the reputational risk inherent to their economic development models. Tourism businesses and destination management organizations (DMOs) should plan to mitigate any reputational costs by conducting marketing campaigns that raise tourists’ awareness of the attractiveness of the destinations.

Following this study, future research could investigate whether the governments of tax havens enforce stronger property rights protection and offshore financial secrecy activity, or reduce their reliance on offshore finance in order to minimize their exposure to the risk of future media scandals. Policymakers should rethink the long-run sustainability of their pillar industries. As governments across the world are set to ramp up their efforts to crack down on tax evasion and money laundering, any over-dependence on offshore financial services for economic development will likely continue to bring about reputational damage. To alleviate the risks linked to tax haven development strategies, policymakers should strive to encourage industrial diversification and facilitate the shift of productive resources (e.g., land, labor, and capital) to other industries.

Another aspect that future research may wish to address is the potential spillover effect of the Panama Papers and other similar tax scandals on locations other than the epicenter. As found in section 5.1, the Panama Papers scandal may have damaged not only Panama’s tourism industry but also other tax havens (such as Peru). Future research could employ spatial econometric techniques to investigate spillover effects from tax scandals and whether those effects are confined to regional locations or extend globally.

In relation to the crowding-out effect, future research could resort to a different modeling framework (e.g., CGE) to examine in greater detail the consequences of offshore finance at individual country levels—for example, rising labor costs, widening income disparity, chronic labor shortages, and severe pressure on both land and capital. Such investigations can be extended to incorporate dynamic elements in the models. Besides, researchers could continue to investigate this effect in a service economy context other than the usual tourism/manufacturing one. This new perspective resonates with the contemporary trend that sees many countries shifting toward service or knowledge-based economies, which entails new inter-industry dynamics.

Footnotes

Appendix

Dynamic Panel Data Analysis of Tourism Exports.

| Dependent variable: | ||||

|---|---|---|---|---|

| Real tourism exports | ||||

| System-GMM | ||||

| (1) | (2) | (3) | (4) | |

| Real tourism exports t−1 | 0.757 *** (0.085) | 0.783 *** (0.091) | 0.742 *** (0.080) | 0.622 *** (0.081) |

| Real tourism exports t−2 | −0.016 (0.050) | 0.100 * (0.055) | ||

| Real GDP index | 0.751 *** (0.199) | 0.783 *** (0.204) | −0.122 (0.886) | −1.009 (1.695) |

| Real GDP index t−1 | 0.648 (0.699) | 1.007 (1.896) | ||

| Real GDP index t−2 | 0.417 (1.011) | |||

| Price level | −0.495 *** (0.171) | −0.454 *** (0.161) | −0.885 ** (0.382) | −0.600 * (0.345) |

| Price level t−1 | 0.500 (0.387) | −0.127 (0.392) | ||

| Price level t−2 | 0.499 (0.310) | |||

| Real financial service exports | −0.004 (0.057) | −0.036 (0.059) | 0.020 (0.054) | −0.058 (0.044) |

| Real financial service exports t−1 | −0.019 (0.017) | 0.007 (0.040) | ||

| Real financial service exports t−2 | 0.019 (0.018) | |||

| Trade openness | 0.354 ** (0.164) | 0.313 (0.200) | 0.106 (0.337) | 0.203 (0.387) |

| Trade openness t−1 | 0.371 (0.471) | 0.310 (0.477) | ||

| Trade openness t−2 | 0.099 (0.198) | |||

| Country risk | −0.566 * (0.302) | −0.618 (0.380) | 1.498 * (0.882) | 2.555 * (1.328) |

| Country risk t−1 | −2.048 ** (0.995) | −1.925 (1.296) | ||

| Country risk t−2 | −1.364 *** (0.500) | |||

| Tax haven blacklist (dummy) | −0.166 (0.196) | −0.143 (0.213) | −0.202 (0.179) | −0.215 (0.250) |

| Tax haven gray list (dummy) | −0.050 (0.177) | −0.017 (0.156) | −0.062 (0.110) | 0.027 (0.162) |

| Sargan test (p-value) | .917 | .893 | .747 | .395 |

| AR(1) (p-value) | .010 | .008 | .015 | .073 |

| AR(2) (p-value) | .579 | .451 | .991 | .148 |

| Wald test (p-value) | .000 | .000 | .000 | .000 |

| Observations | 700 | 660 | 700 | 660 |

| Groups | 20 | 20 | 20 | 20 |

Note. Windmeijer robust standard errors in parentheses. Both the dependent and explanatory variables are log-transformed, except for dummies. AR(1) and AR(2) are the Arellano–Bond test for autocorrelation of orders 1 and 2, respectively. * p < .1. **p < .05. ***p < .01.

Acknowledgements

We thank our colleagues at Aston Business School Prof Tomasz Mickiewicz, Dr Matthew Olczak, Dr Michail Karoglou, Dr Anastasios Kitsos and Dr Johan Rewilak for their helpful comments on the draft of this paper and on our presentation at the EFE Entrepreneurship and Regional Development seminar. We also thank Prof Christos Pitelis (University of Leeds) for his helpful comments at the AIB MENA conference.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We thank the Leverhulme Trust for funding the research presented in this article (under Grant Number: RPG-2017-419).

Notes

Author Biographies

Zheng Chris Cao is a lecturer in economics at Aston Business School, UK. His research interests are in tourism economics, globalization, economic development, and applied macroeconometrics.