Abstract

The US Department of Veterans Affairs (VA) healthcare system is dedicated to preventing veteran homelessness, but there is limited research on the specific sources of financial debt among homeless veterans. We investigated the proportion of veterans seeking VA homeless services reporting any debt and specific types of outstanding debt, associations between homelessness experiences and debt, and whether these associations vary by sex. Using VA administrative data, we cross-sectionally evaluated various types of outstanding debt among 118 594 homeless and at-risk veterans in the VA healthcare system from fiscal years 2023–2024. Multivariable logistic regression models were constructed for history of homelessness experiences in relation to any and different types of financial debt, overall, and by sex. About 48% of veterans in VA homeless programs had outstanding debt, with credit cards being the most prevalent contributors to debt. Outstanding debt related to student loans, child support, medical expenses, and tax bills were significantly associated with greater episodes of recent homelessness. Medical expenses, fines, or other legal obligations were significantly associated with lifetime homelessness duration. Housing loans were associated with shorter duration and fewer episodes of homelessness (over the past 3 years). Similar patterns were observed among male and female veterans. Financial debt is linked to prolonged homelessness among veterans, necessitating increased social services for financial literacy, debt consolidation, and other interventions to mitigate risks.

Introduction

The total financial debt among households within the United States (US) was over $18 trillion in 2025, which, on average, exceeded $100 000 per US household. 1 Whereas credit card debt has reached a record level, 2 medical debt has been established to be among the most common reasons for personal bankruptcy.3 -6 A growing body of research studies have evaluated the relationships of financial debt with incarceration,7,8 homelessness,7 -19 and psychosocial traits (eg, substance use,9,20 mental health,9,10,21 suicidality7,11 -13), yet few of these studies have been focused on specific types of financial debt, including legal 8 and medical 14 debt. There has also been increasing interest in financial literacy training and development of other financial-based interventions to improve money management and address debt for various populations, including adults with behavioral health and social problems. 22 It is worth noting that these interventions often emphasize the need to understand financial structures, such as interest rates, which often serve lenders’ profit motives and can be predatory, and, instead, the target of these interventions should be on empowering individuals with knowledge and skills to assess their financial decisions.

Current evidence suggests that financial concerns, in general, and money mismanagement potentially leading to financial debt, in particular, are key risk factors for homelessness in veteran and non-veteran populations.8,16 It has been established that US veterans have access to unique financial, social, and healthcare benefits that are not available to their civilian counterparts, and the US Department of Veterans Affairs (VA) is heavily invested in preventing veteran homelessness and operates a continuum of VA homeless programs. Although previous studies have shown that financial concerns, such as debt, are major risk factors for veteran homelessness,7,20 the relationship between financial debt and homelessness is likely bi-directional and cyclical. Furthermore, there has been limited examination of distinct sources of financial debt among homeless veterans, and the share of US veterans experiencing distinct types of financial debt has yet to be determined. A recent national survey found that many homeless and at-risk veterans may need access to financial and credit counseling to help with managing debt.23,24 As such, it would be informative to characterize distinct types of financial debt and their relationships with homelessness experiences among US veterans to guide programming and policy efforts.

In this quality improvement project, we performed cross-sectional analyses of VA administrative data on US veterans who used VA homeless program services to examine any reported outstanding debt at the time of program intake and distinct types of outstanding debt in relation to their histories of homelessness including total lifetime duration, recent episodes, and recent duration of homelessness. Given that sources of financial debt may vary between male and female veterans, that the VA primarily serves male veterans, and that there is growing interest in understanding the specific needs of female veterans, we also conducted analyses stratified by sex. The purpose of this project was to address the following questions among veterans seeking VA homeless program services: (1) What proportion of veterans who use VA homeless program services report any outstanding debt and specific types of debt? (2) Is there a relationship between homelessness experiences and outstanding debt? (3) Does the relationship between homelessness experiences and outstanding debt vary by sex?

Methods

Database

This quality improvement project was sponsored by the Homeless Programs Office in response to an informational request from the Government Accountability Office (GAO). All data management and analysis tasks were conducted on the VA network on a secure VA operations server behind the VA firewall. The project followed VA’s Program Guide 1200.21 for non-research activities and institutional review board approval was waived. Furthermore, this quality improvement project was reported in accordance with the Strengthening the Reporting of Observational Studies in Epidemiology (STROBE) guidelines. The VA Homeless Operations Management and Evaluation System (HOMES) captures data on veterans participating in homeless programs, as documented by VA homeless service staff. Each veteran entering VA homeless programs completes an intake assessment – captured by the VA HOMES Assessment Form – which includes questions that ask about any significant outstanding debt [‘Do you have any significant outstanding debts?’]. Veterans who answer ‘Yes’ are further asked a series of ‘Yes’ or ‘No’ questions about different types of significant outstanding debt (‘housing loans’, ‘student loans’, ‘other loans’, ‘credit card debt’, ‘child support’, ‘alimony’, ‘medical expenses’, ‘fines or other legal obligations’, ‘outstanding tax bills’, and ‘other’). Each veteran is allowed to report multiple types of outstanding debt.

The HOMES Assessment Form also includes questions pertaining to history of homelessness experiences with 3 indicators: (1) Lifetime duration of homelessness experienced (‘How long have you been homeless?’ with response options including ‘at least one night but less than one month’, ‘at least one month but less than 6 months’, ‘at least 6 months but less than 1 year’, ‘at least one year but less than 2 years, and ‘two years or more’; (2) Number of episodes of recent homelessness (‘What is the total number of times you have been homeless on the street, in Emergency Shelter [ES], or Safe Haven [SH], in the past 3 years’) with response options of 0; 1; 2; 3; 4+ times); and (3) Duration of recent homelessness (‘How many months in total have you been homeless in the past 3 years’) with a response option that allows input of up to a 2 digit number that ranges from 0 to 36. Background characteristics including fiscal year of the assessment (2023 or 2024), region of residence, sex, age, race, ethnicity, marital status, and years of education were also obtained from the HOMES Assessment Form. To examine clinical characteristics, we extracted diagnostic data from VA electronic health records that are stored in the VA Corporate Warehouse (CDW) and linked to the HOMES database. We calculated the 17-item Charlson’s Comorbidity Index (CCI)25 -30 based on the International Classification of Diseases, Tenth Revision, Clinical Modification (ICD-10-CM) codes that correspond to major chronic conditions and predicts cumulative 1-year mortality risk. 30 Similarly, ICD-10-CM codes from outpatient and inpatient records were used to identify substance use and mental health disorder diagnoses covering the period 1 month before or after the first visit between 1 April 2022 and 31 December 2024, that is, 6 months before and after fiscal years 2023 to 2024. This methodology has been used in previous studies to broadly capture psychiatric diagnoses among homeless veterans who are often transient and may be diagnosed in the VA healthcare system at different entry points. 31 Figure 1 presents a directed acyclic graph for the relationship between homelessness, financial debt, and covariates.

Directed acyclic graph.

Participants

Data from the HOMES Assessment Form were captured using Microsoft’s Structured Query Language Server Management System (SSMS) [Redmont, WA, USA] and transferred into the Statistical Analysis System (SAS) Grid [Cary, NC, USA] for further data management and analysis tasks. As of 23 July 2025, the HOMES Assessment Form included 1 252 888 records for 680 149 distinct US veterans who sought homeless program services. Of those, 165 697 records for 131 754 distinct veterans were kept because they corresponded to a date of HOMES Assessment that took place during fiscal years 2023 to 2024, that is, between 1 October 2022 and 30 September 2024. Specifically, we evaluated outstanding debt, homelessness, demographic, and socioeconomic data using the latest available HOMES Assessment Form for each veteran within fiscal years 2023 to 2024, and clinical data within the pre-specified period based on linked HOMES and CDW databases. Of 131,754 distinct veterans, we excluded 13 160 veterans who self-reported their sex as ‘Other’ (n = 460) or ‘Unknown’ (n = 17), as well as those with missing data on age (n = 100), race (n = 7600), ethnicity (n = 7148), marital status (n = 6539), and education (n = 1895), yielding a total of 118 594 veterans who were male or female with no missing data on demographic and/or socioeconomic characteristics.

Statistical analysis

Complete case analyses were performed whereby subsamples of 118 594 veterans to examine outstanding debt in relation to homelessness experiences, before and after stratifying by sex. Bivariate relationships were examined using independent samples t-tests and χ2 tests, as appropriate. Multivariable logistic regression models were constructed to estimate odds ratios (OR) with their 95% confidence intervals (CI) for demographic, socioeconomic, clinical, and homelessness characteristics as predictors of overall and distinct types of outstanding debt, before and after stratifying by sex. Interaction terms within multivariable logistic regression models were used to evaluate differences by sex in associations between homelessness characteristics and outstanding debt. Two-sided statistical tests were evaluated at α = .05.

Results

Of 118 594 veterans who used VA homeless programs in the analytic sample, 105 669 were male and 12 925 were female. As detailed in Supplemental Table S.1, male veterans were older, less educated, more likely to report their race as white, and more likely to be diagnosed with medical or psychiatric disorders than female veterans, whereas female veterans were more likely than male veterans to report multiple sources of significant outstanding debt. Conversely, lifetime duration of homelessness, number of episodes of recent homelessness, and duration of recent homelessness were higher among male versus female veterans. Furthermore, 56 546 (47.7%) reported they had any type of outstanding debt, and the most frequently observed type of debt was credit card debt (21 666 (18.3%)) followed by other loans [besides housing and student loans] (19 501 (16.4%)). The prevalence of any outstanding debt was significantly lower among male versus female veterans (46.4% vs 58.3%, P < .001), with distinct patterns by sex in terms of types of outstanding debt. Specifically, male veterans were more likely (P < .001) than female veterans to report child support (8.1% vs 2.0%), whereas female veterans were more likely than male veterans to report housing loans (3.5% vs 3.3%), student loans (20.8% vs 8.7%), other loans (23.7% vs 15.6%), credit card debt (27.1% vs 17.2%), and medical debt (9.5% vs 6.6%). Among the 105 669 male veterans (89.1% of the total sample), 46.4% reported having any debt with the most frequent types of debt being credit card (17.2%), other loan (15.5%), and child support (8.1%). Among the 12 925 female veterans (10.9% of the total sample), 58.3% reported any debt with the most frequent types of debt being credit card (27.1%), other loan (23.7%), and student loan (20.8%; Supplemental Table S.2).

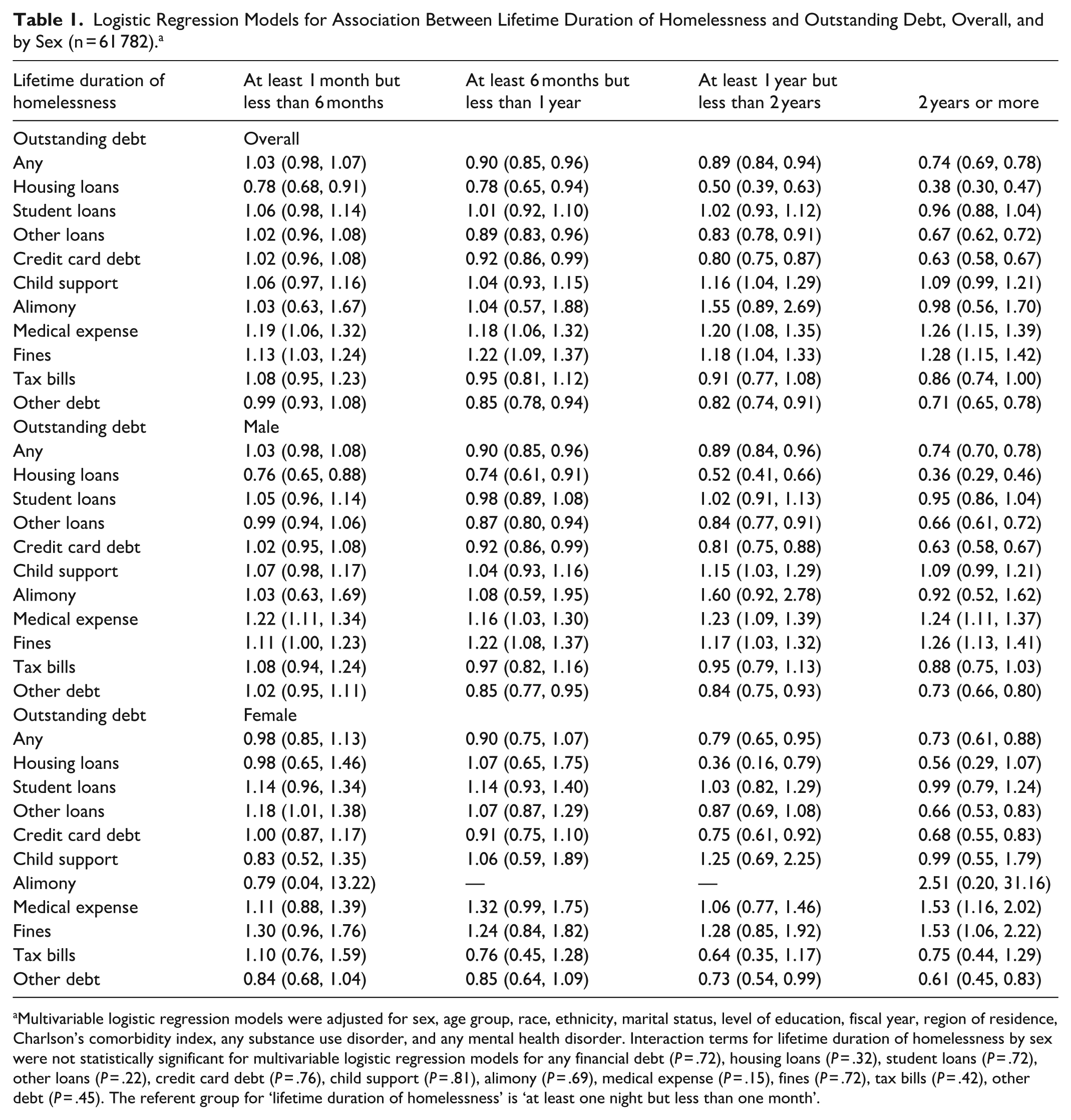

Using a subsample of 61 782 veterans with valid data on lifetime duration of homelessness, we constructed a series of multivariable logistic regression models for this exposure variable in relation to any type and each type of outstanding debt, overall, and by sex (Table 1). As indicated by OR > 1 and 95% CI that did not include the null value of 1, a longer lifetime duration of homelessness was related to significant outstanding debt, especially when the source of debt was medical expenses and legal fines. Conversely, having housing loans was associated with a shorter lifetime duration of homelessness, as indicated by OR < 1 and 95% CI that did not include the null value of 1. Using a subsample of 113 898 veterans with valid data on number of episodes of recent homelessness, we constructed a series of multivariable logistic regression models for this exposure in relation to any type and each type of outstanding debt, overall, and by sex (Table 2). Whereas housing loans were associated with fewer episodes of recent homelessness, that is, over the past 3 years, any outstanding debt, student loans, other loans, credit card debt, child support, medical expenses, tax bills, and other sources of debt were associated with more episodes of recent homelessness, that is, over the past 3 years. Using a subsample of 77 190 veterans with valid data on duration of recent homelessness, we constructed a series of multivariable logistic regression models for this exposure in relation to any type and each type of outstanding debt (Table 3), suggesting that 1-month longer duration of recent homelessness, that is, over the past 3 years, was not related to significant outstanding debt. Results displayed in Tables 1 to 3 suggest similar patterns for male and female veterans, and that there were no statistically significant interaction terms by sex with few exceptions (eg, number of episodes of recent homelessness as a predictor of student loans and fines). However, these associations were less frequently statistically significant among female veterans given sample size limitations.

Logistic Regression Models for Association Between Lifetime Duration of Homelessness and Outstanding Debt, Overall, and by Sex (n = 61 782). a

Multivariable logistic regression models were adjusted for sex, age group, race, ethnicity, marital status, level of education, fiscal year, region of residence, Charlson’s comorbidity index, any substance use disorder, and any mental health disorder. Interaction terms for lifetime duration of homelessness by sex were not statistically significant for multivariable logistic regression models for any financial debt (P = .72), housing loans (P = .32), student loans (P = .72), other loans (P = .22), credit card debt (P = .76), child support (P = .81), alimony (P = .69), medical expense (P = .15), fines (P = .72), tax bills (P = .42), other debt (P = .45). The referent group for ‘lifetime duration of homelessness’ is ‘at least one night but less than one month’.

Logistic Regression Models of the Association Between Number of Episodes of Recent Homelessness in the Past 3 Years Associated with Outstanding Debt (n = 113 898). a

Multivariable logistic regression models were adjusted for sex, age group, race, ethnicity, marital status, level of education, fiscal year, region of residence, Charlson’s comorbidity index, any substance use disorder, and any mental health disorder. Interaction terms for homelessness frequency by sex were not statistically significant for multivariable logistic regression models for any financial debt (P = .13), housing loans (P = .33), other loans (P = .25), credit card debt (P = .18), child support (P = .89), alimony (P = .14), medical expense (P = .69), tax bills (P = .84), other debt (P = .25), but were statistically significant for student loans (P = .03) and fines (P = .01). The referent group for ‘number of episodes of recent homelessness in the past 3 years’ is zero.

Logistic Regression Models for Duration of Recent Homelessness in the Past 3 Years as Predictor of Outstanding Debt Characteristics (n = 77 190). a

Multivariable logistic regression models were adjusted for sex, age group, race, ethnicity, marital status, level of education, fiscal year, region of residence, Charlson’s comorbidity index, any substance use disorder, and any mental health disorder. Interaction terms for duration of recent homelessness by sex were not statistically significant for multivariable logistic regression models for any financial debt (P = .52), housing loans (P = .86), student loans (P = .29), other loans (P = .53), credit card debt (P = .44), child support (P = .09), alimony (P = .14), medical expense (P = .47), fines (P = .39), tax bills (P = .33), other debt (P = .53).

Discussion

Based on national data, we found that nearly half of veterans who used VA homeless programs had some type of outstanding debt, with credit card debt being the most common. Female veterans were significantly more likely to report any outstanding debt and were more likely to report multiple sources of debt. When we examined how outstanding financial debt was related to homelessness experiences, we found some strong associations with lifetime duration of homelessness and number of episodes of recent homelessness associated with various types of debt. Some sources of debt, such as debt from medical expenses, fines, and other legal obligations, were more strongly associated with lifetime duration of homelessness than with duration of recent homelessness. Debt from housing loans were associated with less extensive histories of homelessness, which might be expected since individuals able to obtain a home loan likely reached a certain level of income and assets at least at some point. Similarly, participation in the VA Home Loan Program among eligible veterans may be protective against future experiences with homelessness.

The importance of debt in relation to homelessness seems obvious, although the temporal relationship between these 2 experiences has yet to be evaluated. For instance, it is likely that debt can lead to homelessness, but it can also prolong or increase the duration and number of episodes of pre-existing homelessness. In this project, even though we evaluated homelessness as exposure and debt as outcome of interest, directionality remains uncertain within a cross-sectional design. Our findings align with the broader literature reporting financial debt as a factor related to recent homelessness,20,32 and indebtedness along with financial crises, unemployment, reduced income, and past homelessness can mediate the relationship between severe mental illness and homelessness. 16 Our findings may also have program implications as many studies have suggested that legal assistance and debt advice, along with temporary income supports, may be effective in addressing pathways to homelessness, such as preventing evictions, resolving financial issues before they worsen, and offering proper timely supports.9,17,21

A limited number of studies have examined specific types of financial concerns in relation to homelessness, including legal and medical debt. For instance, a cross-sectional study analyzed the impact of incarceration and legal financial obligations on the duration of homelessness by interviewing 101 adults who lived in city-sanctioned encampments and tiny house villages in Seattle, WA, US, with more than 25% reporting that they currently owed legal fines, and those with legal fine debt experiencing 22.9 months of additional homelessness. 8 Another study of 60 homeless individuals in Seattle found that most had at least 1 type of debt, with two-thirds reporting current medical debt. 14 More than half with medical debt incurred this debt while covered under insurance, and individuals with trouble paying medical bills experienced a more recent episode of homelessness 2 years longer than those without trouble, even after controlling for race, education, age, gender, and health status. 14

Financial debt and homelessness among veterans have been linked to a wide range of health outcomes, but studies focused on homeless veterans have been limited so far. A study conducted in 2021 and involving 1004 low-income US veterans found an interaction between a history of homelessness and current debt, with 40% of veterans with both past homelessness and higher debt reporting suicidal ideation. 7 Another study involving a sample of 48 965 veterans who separated from active duty in fall 2016 examined the financial status of newly transitioned veterans over a 3-year period found that 13% of veterans disclosed troubled financial status and veterans with troubled financial status reported greater difficulty adjusting to civilian life, while women were less likely to report difficulty. 33 There have been similar findings from other studies. 15 It is worth mentioning that our findings indicate that male veterans were less likely to report any outstanding debt than female veterans, but not by much. Importantly, there were no sex differences in associations between outstanding debt and histories of homelessness, suggesting that debt is an important factor in pathways to homelessness, and vice versa, for both sexes as supported by various lines of research.22,34

Although this analysis is among the first to examine the link between specific types of financial debt and homelessness characteristics among veterans seeking homelessness assistance, a few important caveats are worth mentioning. First, missing data on demographic and clinical characteristics in the HOMES database may have resulted in selection bias or affected the analyses in other ways. Second, data on outstanding debt was collected during intake assessments based on veteran self-report and may not always be accurate or properly documented. Also, information on various debt categories were collected but there was no data available on the amount of each type of debt which would have been relevant to judge the scope and magnitude of this issue within this population. Third, the cross-sectional design precluded us from establishing a temporal relationship between homelessness and financial debt experiences, and theoretically, the relationship among these 2 experiences is likely bi-directional and cyclical. Fourth, the observational study design and the reliance on existing administrative data may have precluded our ability to adjust for important confounders, potentially resulting in residual confounding. Fifth, sample size limitations precluded our ability to examine relationships stratified by race, ethnicity, and VA-connected disability rating. Thus, further studies with larger sample sizes and advanced designs are needed to expand on findings from this quality improvement project.

Conclusion

Credit card debt and various loans are among several sources of outstanding debt affecting nearly half of veterans seeking VA homeless services. Distinct types of outstanding debt were associated with longer duration (eg, medical expenses and legal fines) and a greater number of homelessness episodes (eg, student loans, credit card debt, child support, medical expenses, tax bills) among these veterans. Housing loans may be associated with shorter duration and fewer episodes of homelessness. Irrespective of sex, financial debt may be associated with longer and more frequent homelessness, highlighting the need for increased support and resources for homeless male and female veterans facing financial challenges. Specifically, increased support for financial literacy, debt consolidation, and other interventions may be necessary to mitigate homeless risks.

Supplemental Material

sj-docx-1-inq-10.1177_00469580261440182 – Supplemental material for Medical Debt, Credit Card Debt, and Other Financial Debt Among Veterans Who Receive Homeless Assistance in the Veterans Affairs Healthcare System

Supplemental material, sj-docx-1-inq-10.1177_00469580261440182 for Medical Debt, Credit Card Debt, and Other Financial Debt Among Veterans Who Receive Homeless Assistance in the Veterans Affairs Healthcare System by Hind A. Beydoun, Dorota Szymkowiak and Jack Tsai in INQUIRY: The Journal of Health Care Organization, Provision, and Financing

Supplemental Material

sj-docx-2-inq-10.1177_00469580261440182 – Supplemental material for Medical Debt, Credit Card Debt, and Other Financial Debt Among Veterans Who Receive Homeless Assistance in the Veterans Affairs Healthcare System

Supplemental material, sj-docx-2-inq-10.1177_00469580261440182 for Medical Debt, Credit Card Debt, and Other Financial Debt Among Veterans Who Receive Homeless Assistance in the Veterans Affairs Healthcare System by Hind A. Beydoun, Dorota Szymkowiak and Jack Tsai in INQUIRY: The Journal of Health Care Organization, Provision, and Financing

Footnotes

Acknowledgements

We thank the Homeless Programs Office, US Department of Veterans Affairs, for their support of this study. Disclaimer: The views expressed in this article are those of the authors and do not reflect the official policy of the U.S. Department of Veterans Affairs, or the U.S. government.

Ethical Considerations

Ethical approval was waived given the non-human subject nature of this quality improvement project sponsored by the Homeless Program Office at the U.S. Department of Veterans Affairs.

Consent to Participate

Informed consent was waived given the non-human subject nature of this quality improvement project sponsored by the Homeless Program Office at the U.S. Department of Veterans Affairs.

Author Contributions

Hind Beydoun, PhD, MPH: Conceptualization; Data curation; Formal analysis; Methodology; Software; Visualization; Writing – original draft. Dorota Szymkowiak, PhD: Investigation; Data curation; Validation; Writing – review & editing. Jack Tsai, PhD, MCCP: Conceptualization; Investigation; Project administration; Resources; Supervision; Writing – review & editing.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The study’s datasets are not publicly available, but the code can be obtained from the corresponding author upon reasonable request.

Supplemental Material

Supplemental material for this article is available online.