Abstract

Isolation facilities are essential to pandemic response, yet the economic trade-offs of repurposing existing hospitals remain poorly characterised. This study quantifies both the operational costs and the revenue foregone from converting Tigoni Level 4 Hospital (TL4H) into Kiambu County’s sole COVID-19 isolation centre. Our study focused on estimating recurrent and labour costs, considering only capital costs incurred during the study period. We conducted a cost analysis at the facility level, assessing all expenditures incurred by TL4H between June 2020 and February 2022, using an activity-based costing approach to allocate costs to specific operational activities. Sensitivity analyses, including one-way and 10,000-draw Monte Carlo PSA, estimated uncertainty in total and per-patient costs. The total operational cost of the isolation centre over the 21 months was KES 489,220,113.98 (USD 4,181,011.14). This translates to an annual operating cost of KES 279,554,350.85 (USD 2,389,149.23). The average cost of managing one COVID-19 patient regardless of severity was estimated as KES 337,626.03 (USD 2885.45). The revenue foregone by waiving user fees for COVID-19 patients was KES 160,678,901.00 (USD 1,374,236). Sensitivity analysis indicated that HRH costs (78.9% of total expenditure) had the largest influence: a ±20% change shifted total costs by ±KES 77.6 million (USD 663,191.18). PSA results showed a mean total operational cost of KES 489,212,852 (USD 4,180,949.08; 95% UI: 414,803,680-573,687,849), and a mean cost per patient of KES 337,621.02 (USD 2885.40; 95% UI: 286,268.93-395,919.84). Repurposing TL4H as a COVID-19 isolation centre was resource-intensive, highlighting the importance of strategic budget planning and resource allocation for future preparedness.

In Kenya, national policy directed county governments to set up isolation facilities to manage COVID-19 cases. In Kiambu County, Tigoni Level 4 Hospital, a 104-bed facility, was converted into the main isolation centre for 21 months (June 2020 to September 2022).

Our work provides a facility-level cost analysis of converting a Kenyan public hospital into a COVID-19 isolation centre and quantifies both the operational costs and the revenues foregone as a result of this conversion.

Our work enhances understanding of the cost dynamics of hospital repurposing by linking operational cost structures to real-world facility management. It informs hospital managers and planners about key cost drivers during health emergencies and provides evidence to support budget planning, workforce deployment, and emergency preparedness.

Background

When Kenya’s first COVID-19 case was confirmed in March 2020, 1 the government faced an urgent challenge: to care for and isolate infectious patients without overwhelming the overall health system. Establishing isolation facilities became a critical part of Kenya’s Ministry of Health pandemic response, enabling safe patient care while limiting community transmission. 2 This approach mirrored strategies adopted globally for managing SARS-CoV-2, the novel coronavirus first reported in Wuhan, China, in December 2019 and later declared a public health emergency of international concern by the World Health Organization.3 -5

In Kenya, the national government rapidly issued treatment protocols and public health measures, including social distancing, mask mandates, stay-at-home orders, curfews, and travel restrictions. 6 County governments were advised to designate isolation facilities to meet the medical and basic needs of COVID-19 patients during recovery. 2 Tigoni Level 4 Hospital (TL4H), a 104-bed facility in Kiambu County, was converted into the dedicated county COVID-19 isolation centre in June 2020, at the height of the first wave, and remained in this role until September 2022. This period coincided with escalating case numbers in Kiambu and neighbouring Nairobi, as well as stringent national restrictions.

Kenya’s public healthcare system is structured into 6 tiers, with Level 4 hospitals (such as TL4H) providing a wide range of outpatient, inpatient, surgical, diagnostic, and maternity services. 7 These facilities usually charge user fees under the Facility Improvement Fund programme, which contributes to their operational budgets. However, following the government’s declaration of COVID-19 as a national public health emergency, all user fees for COVID-related services were waived at the point of care.

Previous research by Barasa et al 8 estimated the per-patient cost of managing COVID-19 in Kenyan hospitals or isolation centres at KES 80,639 (USD 764.41) for mild-to-moderate cases, KES 157,645 (USD 1494.38) for severe cases, and KES 758,917 (USD 7194.07) for critical cases. These estimates, derived from resource use data in 3 public hospitals, national treatment guidelines, and market prices, provide valuable benchmarks for estimating patient-care costs. However, they do not capture the total operational costs of converting and running an entire hospital exclusively for COVID-19 care, nor the financial impact of lost revenue from waived user fees.

While isolation facilities are vital for infection control, their establishment requires substantial resources and may displace other essential services, creating both direct costs and indirect economic losses. In a health system where many facilities rely on user fees for operational sustainability, understanding these costs is critical. This study aimed to quantify the full operational costs of running TL4H as a public COVID-19 isolation facility, and to estimate the revenue foregone during its months of exclusive operation. This dual perspective provides evidence to guide resource allocation, health financing, and emergency preparedness in Kenya and comparable settings.

Methods

Local Context

(a) Healthcare funding

Healthcare services in Kenya are provided by both public, private healthcare facilities and faith-based organisations. Following the promulgation of the new constitution in 2010, management of health roles was split into the 2 levels of government: county and national. 9 The management of public health facilities up to level 5 has been placed under the county government. Level 6 facilities fall under the National Government. TL4H is 1 of the 14 public hospitals under the management of the county government of Kiambu.

Kenya’s health system is funded by: the government (national and county) through taxes, the National Hospital Insurance Fund (NHIF) through member contributions, donor funds, and individuals’ out-of-pocket payments. 10 In the financial year 2015/2016 household out-of-pocket payment constituted 26.1% of the total health expenditure. 11 In 1989, Kenya introduced user fees in public hospitals. These user fees form the facility improvement fund. 12

In June of 2020, TL4H was converted into an isolation centre dedicated to serving COVID-19 patients. During this period, patients received all services at the isolation centre free of charge; thus, funding for the hospital was primarily from the government, that is, the county and national, as well as donors.

(b) Kiambu County health budget

In the financial year 2019/2020, the County Government of Kiambu allocated KES 5,052,933.672 to health services out of a total county budget of KES 15,638,800,000. This represented approximately 32.3% of the total budget for that year. In the subsequent financial year 2020/2021, the county’s health expenditure increased to KES 5,752,309,420; while the total county budget rose to KES 17,894,726,836.13,14 This amounted to about 32.1% of the total budget. Despite the increase in absolute health spending, the proportion of the budget allocated to health services slightly decreased compared to the previous year.

Part of this was allocated for the establishment of the COVID-19 Isolation Centre at TL4H. This facility was established in June 2020 and served as the isolation facility until February 2022.

Study Design

This was a retrospective, facility-based costing study that estimated the financial resources required to convert and operate TL4H as a COVID-19 isolation centre between June 2020 and February 2022.

A bottom-up (micro-costing) approach was used to quantify recurrent and capital costs from a facility-level perspective. Costs were assessed using an activity-based costing approach, which allocated expenditures to specific operational activities across the facility. This study followed the Consolidated Health Economic Evaluation Reporting Standards (CHEERS) 2022 guidelines, 15 and the completed checklist can be found in Supplemental File 1.

Data Collection

Data were collected directly from TL4H via relevant department heads and administrative records. Costs included expenditures on human resources, health products and technologies, medical engineering, equipment, overheads, and infrastructure constructed during the study period. Aggregate facility-level data were compiled, focusing on incurred costs rather than patient-level resource use. The underlying data for this study are provided in Supplemental File 2, and a complete table listing all data collection sources is available in Supplemental File 3.

Inclusion and Exclusion Criteria

Cost data were included if they were directly related to the operation of TL4H as a COVID-19 isolation centre between June 2020 and February 2022.

Costs were excluded if they were incurred outside the study period, unrelated to the isolation centre operations, based on individual patient-level resource use, or lacked verification in administrative records.

Estimation of Resource Costs

(a) Supplies

The costs of pharmaceuticals, non-pharmaceuticals, laboratory commodities, medical engineering, and catering supplies were established via supplier quotations. Medical engineering costs were due to the oxygen utilised. The total cost was obtained by determining the quantity of supplies utilised and the unit cost. It was derived as follows: Total costs = Quantity of resources × unit cost.

The consumption data was consolidated by the respective departments. This data was obtained from the stock control cards, and in instances, the stock control cards were unavailable, then delivery notes for the same period were used to estimate consumption. Commodities such as pharmaceuticals and non-pharmaceuticals were mainly procured from the Kenya Medical Supplies Authority (KEMSA). The KEMSA price list 2021 was used to determine the cost of the commodities procured from KEMSA. For commodities not procured from KEMSA, the costs were obtained from the prequalified suppliers list issued by the procurement department.

(b) Costing Human Resources for Health (HRH)

To obtain labour costs, the staff returns, which documented the number of staff stationed at the facility with their details such as cadre and job group, were used to identify HRH at the isolation centre. For periods where staff returns were not available, posting orders, which document transfers in and out of facilities within Kiambu County, were used to track the HRH in Tigoni isolation centre throughout the period under review. The salaries of the HRH were obtained from the payroll database. Since all the staff were fully dedicated to the isolation centre, they were assigned 100% full-time equivalent (FTE). For employees of the same cadre and job group, the average salary for the job group was utilised to cost for the human resources.

The total cost for each cadre was computed as:

HRH costs were disaggregated into: basic salaries, allowances, overtime payments, and agency/temporary staff.

(c) Costing for medical equipment and infrastructure

The capital costs considered during the study were the additional investments made for the establishment of a COVID-19 isolation centre. The useful life of the capital items was assumed to be 5 years. In addition, a discounting rate of 3% was used in the analysis.16,17

(d) Costing for overheads

In order to determine the overhead costs for the review period, the billing statements from service providers were used. No allocation was required as the whole facility was utilised for COVID-19 services.

Establishing User Fees Foregone

To establish user fees foregone, billing data was obtained from the accounts department that documented the service utilisation per patient admitted in Tigoni isolation centre from the period of establishment to disbandment as a COVID-19 isolation centre. The billing data was differentiated into costs such as admission fees, laboratory fees, and accommodation fees.

Cost data for pharmaceuticals, non-pharmaceuticals, laboratory consumables, and oxygen use were obtained from bin cards, the KEMSA price list, and tender documents. Infrastructure and equipment costs came from tender documents and delivery notes, while human resource costs were compiled from staff returns, posting orders, and payroll records. Overhead costs were derived from service provider statements.

Cost Drivers and Probabilistic Sensitivity Analysis

(a) Probabilistic Sensitivity Analysis (PSA)

PSA was conducted on 3 major cost drivers: HRH, medical engineering (oxygen), and non-pharmaceutical supplies. Each driver was modelled using a log-normal distribution (to ensure positive draws) with parameters derived from the baseline mean and an assumed coefficient of variation (CV): HRH CV = 10%, medical engineering CV = 20%, non-pharmaceutical supplies CV = 30%. Monte Carlo simulations recalculated total operational costs and per-patient costs over multiple iterations to generate 95% uncertainty intervals. This analysis was conducted using R version 4.3.0 (C) 2023; The R Foundation for Statistical Computing. The draws and simulation code are available as Supplemental Files 2 and 4, respectively.

(b) Univariate sensitivity analysis

One-way sensitivity analyses evaluated the impact of ±10% and ±20% changes in key cost drivers while holding other components constant. The tabulated sensitivity analysis results can be found in Supplemental File 5.

Foreign Exchange Considerations

The cost in Kenyan shillings was converted to United States dollars using the exchange rate of 1 USD for KES. 117.01, which was the average exchange rate for 2022 as obtained from the Central Bank of Kenya’s average prevailing rates for the period under study.

Results

Patient Admissions and Length of Stay

Over the study period, there were a total of 1449 patients admitted to the isolation centre. August 2021 had the most patients admitted to Tigoni (n = 358), while January and November 2021 had the fewest patients (n = 5) during the entire 21-month period of operation. The average length of stay was 9.28 days.

Costs Incurred Operating the Isolation Centre

The total cost of operating the isolation centre over the 21 months was KES 489,220,113.98 (USD 4,181,011.14), and is tabulated in Table 1. This translates to an annual cost of operation of KES 279,554,350.85 (2,389,149.23). The average cost of managing 1 COVID-19 patient was estimated as KES 337,626.03 (USD 2885.45). The highest cost drivers were human resources (79.3%), medical engineering (8.3%) and non-pharmaceutical supplies (4.4%).

Total operational expenditure for Tigoni Isolation Centre over the 21-month COVID-19 period, disaggregated by major cost categories (in KES and USD) with proportional contributions.

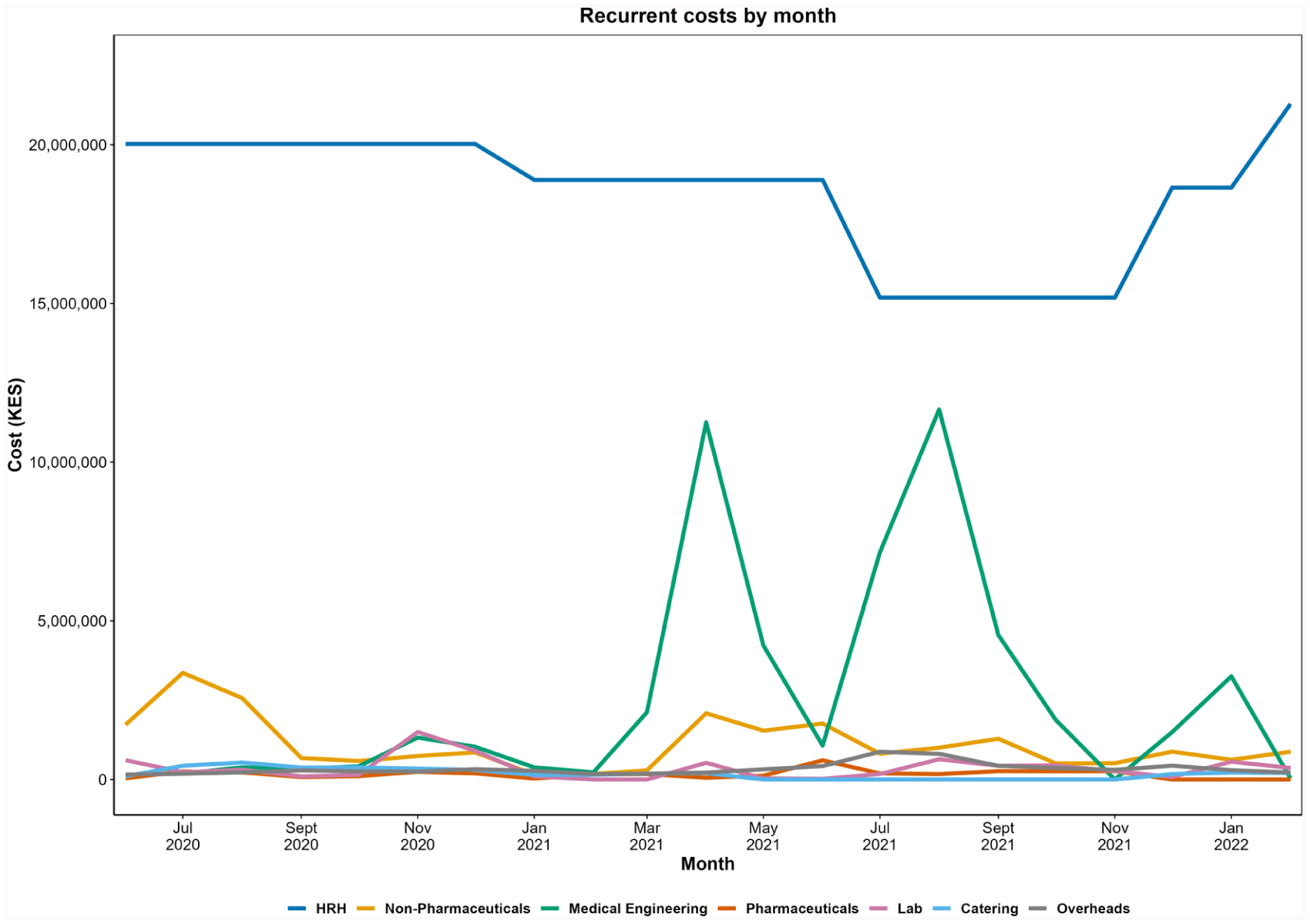

The recurrent costs by month over the review period are illustrated in Figure 1. Human resources for health (HRH) remained the dominant cost driver, 20M KES per month through late-2020, dipping to 18.9M, then falling to about 15.0M in June to November 2021, and increasing to 21.3M by February 2022. Medical Engineering showed episodic surges, most notably in April and August 2021, while Non-Pharmaceuticals peaked early in July 2020 at KES 3,359,543.00 (USD 28,711.59) and otherwise was generally less than 1.5M KES per month. Pharmaceuticals, Laboratory, Catering, and Overheads contributed comparatively small amounts (typically less than 1M KES per month). August 2021 also recorded the highest Laboratory (KES 635,546.12; USD 5,431.55), Medical Engineering (KES 11,657,992; USD 99,632.44), and Catering (KES 481,787.88; USD 4,117.49) costs. Across the period, the three most costly commodities were oxygen (KES 7,877,390.00; USD 67,322.37), surgical masks within Non-Pharmaceuticals (KES 2,670,493.00; USD 22,822.78), and GeneXpert cartridges (KES 2,256,422.88; USD 19,284.02).

Monthly recurrent costs for the Tigoni Isolation Centre over 21 months (June 2020–February 2022) across major expenditure categories. The x-axis shows the respective month, and the y-axis shows the total cost in Kenyan shillings (KES). Human resources for health (HRH, blue); Non-Pharmaceuticals (orange); Medical Engineering (green); Pharmaceuticals (vermillion); Lab (purple); Catering (sky); Overheads (grey).

Similarly, August 2021 was also the month of the highest medical engineering costs and catering costs at KES 11,657,992 (USD 99,632.44) and KES 481,787.88 (USD 4117.49) respectively.

The three most costly commodities utilised were oxygen (KES 7,877,390.00, USD 323,710.71), surgical masks for non-pharmaceuticals (KES 2,670,493.00, USD 22,822.76) and GeneXpert cartridges (KES 2,256,422.88, USD 19,284.02).

User Fees Foregone

The exact fees for each patient were ascertained through hospital billing data. The average user fees per patient, regardless of severity, during the study period were KES 110 889.51 (USD 947.69). Of the patients admitted, 1037 (71.5%) required critical care, which constituted the major contributor to billing charges (47.2%). This was followed by personal protective equipment (PPE; 28.9%) and oxygen therapy (6.75%). The billing items costing the least included branulae, laboratory tests and charges for inpatient files. Table 2 illustrates the total charges per billing item over the study review period.

User fees foregone at Tigoni Isolation Centre from June 2020 to February 2022, disaggregated by billing item, with totals presented in KES and USD and proportional contribution to overall charges.

Operational Cost in the Context of the County Health Budget

When expressed as a share of Kiambu County’s health budget, the annualised operational cost of the Tigoni Isolation Centre represented 5.53% of total health expenditure in FY 2019/2020 and 4.86% in FY 2020/2021.

Cost Drivers

The total HRH cost over the 21-month study period represented 79.3% of total operational costs. The largest HRH subcomponent was basic salaries (KES 321,142,555.55; USD 2,745,921.30, 82.7% of HRH), followed by allowances (KES 29,736,121.00; USD 254,084.26, 7.7%), overtime (KES 18,622,755.00; USD 159,190.26, 4.8%), and agency/temporary staff (KES 18,706,648.00; USD 159,840.75, 4.8%). The top 3 cadres by cost were nurses (KES 154,437,080; USD 1,320,213.59; 39.8% of HRH), medical specialists (KES 34,187,972.50; USD 292,106.35; 8.8%), and pharmacists (KES 22,872,751.52; USD 195,433.48; 5.9%).

Medical engineering expenditure was dominated by oxygen, totalling KES 40 637 335.00 (USD 347 218.68). Bulk oxygen purchases accounted for 93.2% (KES 37 890 000; USD 323 966.92), cylinder oxygen 6.7% (KES 2 721 335; USD 23 255.38), and small cylinders < 0.1% (KES < 40 000; USD < 342.00). Pharmaceutical costs were driven by essential medicines for COVID-19 supportive care and treatment of comorbidities, and changes in these are seen in response to patient admissions.

Probabilistic Sensitivity Analysis (Monte Carlo)

Simulated total operational cost had a mean of KES 489,212,852 (USD 4,181,035.33), median KES 486,845,208 (USD 4,161,967.21), with a 95% uncertainty interval of KES 414,803,680 to 573,687,849 (USD 3,545,579.50-4,900,756.16; SD = KES 40,148,075; USD 343,262.25). Cost per patient had a mean of KES 337,621.02 (USD 2886.68); median KES 335,987.03 (USD 2872.84), 95% uncertainty interval KES 286,268.93 to 395,919.84 (USD 2448.75-3382.33; SD = KES 27,707.44; USD 236.87). Variance decomposition indicated that most simulated cost uncertainty originated from HRH, given its dominant share of baseline expenditure.

One-Way Sensitivity Analysis

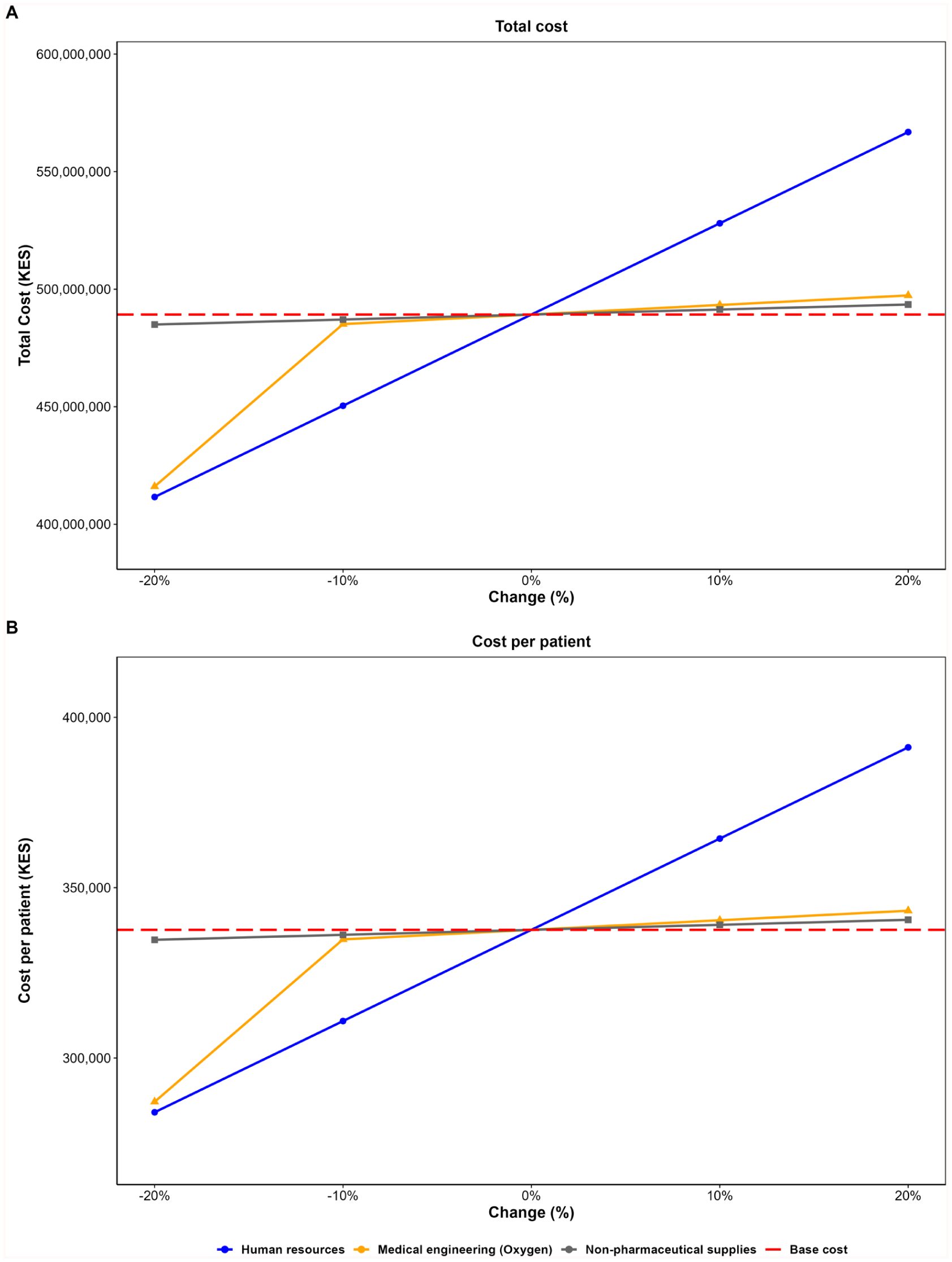

A univariate sensitivity analysis assessed the impact of ±10% and ±20% independent changes in the 3 largest cost drivers (HRH, oxygen, pharmaceuticals) on total operational cost and cost per patient (Figure 2).

One-way sensitivity analysis of major cost drivers. The figure illustrates the impact of ±10% and ±20% independent changes in the 3 largest cost drivers on total operational costs and cost per patient at TL4H COVID-19 isolation centre.

Using the exact baseline values from the cost file, HRH (KES 388,028,495.60; 78.9% of baseline; USD 3 316,209.42) produced the largest absolute variation in total operational cost: a ±20% change in HRH resulted in a change of ±KES 77.61 million (USD 663,696.12; new total range KES 411.61M-566.83M; USD 3,518,140.73-4,845,999.15), corresponding to cost-per-patient values from KES 284,067.92 to KES 391,184.14 (USD 2429.41-3344.83). Medical engineering (oxygen) and non-pharmaceutical supplies produced much smaller absolute effects (±KES ≈7.83M and ±KES ≈2.05M, respectively, for ±20%; USD 66,948.49 and 17,521.36).

Discussion

This study provides a facility-level cost analysis of a COVID-19 isolation centre in a low- and middle-income country (LMIC) setting. By disaggregating costs into their constituent drivers and quantifying the uncertainty around these estimates, we offer not only a historical account of pandemic resource allocation but also a decision-support tool for future health emergencies.

The overwhelming dominance of human resources for health (HRH), nearly four-fifths of all operational expenditure, underscores the labour-intensive nature of hospital-based outbreak response. This is consistent with existing literature, where personnel expenditure often eclipses consumables and infrastructure costs, particularly in settings with sustained patient care needs over prolonged periods. 18 Our HRH breakdown further reveals that basic salaries consumed the largest share of funds. This suggests that the cost burden may stem less from temporary emergency hiring and more from the redeployment or retention of existing staff under standard pay structures. Such dynamics could limit fiscal flexibility: without agile staffing models or adaptable pay mechanisms, governments might face high fixed labour costs even when demand fluctuates.

Oxygen, the primary medical engineering cost, illustrates the logistical vulnerabilities exposed by COVID-19. Bulk oxygen purchases accounted for over 93% of oxygen-related expenditure, highlighting both the achievement of securing large-volume supply contracts and the risk of overreliance on a single delivery modality. Although essential for severe COVID-19 care, bulk supply chains remain vulnerable to transport constraints and supplier bottlenecks, underscoring the need to develop hybrid oxygen-generation capacity in future planning.

Pharmaceutical expenditure, while modest in proportion to HRH and oxygen, was highly elastic to patient volumes. This demand-linked pattern reflects the predictable surge-spend relationship in outbreak settings, and aligns with evidence from other LMIC COVID-19 wards where medication procurement closely mirrored epidemic curves. In budgetary terms, such elasticity suggests that pharmaceutical costs can be anticipated and scaled with a degree of precision, a relative advantage for forecasting.

The study also calculated user fees foregone, which totalled KES 160.7 million (USD 1.37 million), attributed to critical care, PPE, and oxygen. These findings highlight the significant human and material resource investments required for pandemic response and the fiscal implications of free, publicly funded care during a health emergency. These figures are considerable given the fact that only 1449 patients were admitted throughout the period.

TL4H provided services similar to COVID-19 isolation facilities in Sri Lanka and New Zealand.19,20 Other countries, however, converted hotels, gymnasiums and sports centres into isolation facilities or built new structures from scratch, which further increased the operational costs. For instance, a study from a hospital-turned-isolation centre in Egypt reported a total operational cost of USD 3.75 million over 9 months for 2543 patients, giving an approximate cost-per-patient of USD 1474.63. 21 By contrast, the operation of Tigoni isolation centre worked out to an average cost-per-patient of KES 337,626.03 (USD 2885.45). This difference may be due to the Egyptian study focusing primarily on patient care and hospitalisation, without fully accounting for the costs to run the facility, such as utilities and infrastructure maintenance. Previous Kenyan studies on COVID-19 isolation facilities reported per-patient management costs ranging from KES 80,638.86 (USD 764.41) to KES 758,917.30 (USD 7194.07), 8 indicating that the Tigoni figures fall well within the expected range for the country.

However, allocating nearly 5% of the county’s annual health budget to a single facility highlights the magnitude of the county-level investment made to contain COVID-19. While necessary under emergency circumstances, such concentration of resources inevitably constrains the budgetary flexibility for other essential health programmes. Linking these findings to our sensitivity analysis, targeted efficiency measures in major cost drivers, particularly human resources, could free up 1% to 2% of the county’s health budget for reinvestment in broader service delivery.

We found that even modest changes in HRH costs could shift total operational expenditure by more than 15%, far exceeding the proportional effects of oxygen or pharmaceuticals. The probabilistic Monte Carlo simulations reinforced this dominance: HRH was the principal source of uncertainty in total cost, with variance decomposition showing its outsized role in shaping the plausible cost envelope. Together, these results suggest that HRH efficiency reforms, such as flexible staffing rosters, cross-trained personnel pools, and adaptive pay structures, may deliver the highest potential cost savings without compromising care quality. This analysis also has methodological value. By integrating deterministic and probabilistic sensitivity analysis, we were able to distinguish between influence (which driver has the greatest effect on cost if changed) and uncertainty (which driver’s variability most contributes to cost unpredictability). This dual perspective allows for translating retrospective cost data into actionable preparedness strategies.

From a strategic perspective, the implication is clear: if governments wish to maintain surge capacity without incurring unsustainable costs, the next generation of pandemic preparedness plans must be designed around workforce adaptability. While investments in oxygen and medicines remain vital for clinical outcomes, the fiscal sustainability of future isolation facilities will hinge on labour management innovation.

We commend the Kiambu County government for mitigating a potential healthcare-associated economic catastrophe by absorbing these costs rather than passing them on to patients. Indeed, a 2018 study in Kenya showed that out-of-pocket healthcare payments increase the proportion of people living below the poverty line by 2.2%, affecting at least 1 million Kenyans. 10 Parallelled to the fact that the pandemic already had devastating effects at the household level (such as increased unemployment and decreased household income),22,23 waiving the costs becomes even more substantial. In our view, therefore, this effort propounded a significant financial risk management for the people of Kiambu, and this is further compounded by modelling studies showing that institutional-based isolation facilities are more effective (albeit less economical) in reducing COVID-19 transmission. 24

It is concerning that so much was spent to isolate and manage a few patients – only 5 were admitted during case troughs in the 104-bed facility. While the full-building conversion was prudent, future decisions could consider patient caseloads and home-based care, which is more economical. 8 During periods of low case numbers, only a designated area or floor could be used for isolation, allowing the rest of the hospital to operate normally and generate income.

Our work underscores the essential role and high staffing levels required for patient care. Managers and policymakers should prioritise HRH in cost-containment and efficiency analyses, focusing on interventions such as optimising rostering, reducing unnecessary overtime, task-shifting where clinically appropriate, and adjusting staffing mixes. Agency and casual staff, though a modest share of HRH costs (4.8%), can provide surge capacity if integrated strategically rather than recruited ad hoc.

In addition, attention to oxygen, PPE, and pharmaceuticals can yield incremental savings. Bulk oxygen usage indicates reliance on continuous supply chains, suggesting that investment in on-site oxygen generation could reduce long-term costs and buffer against market fluctuations. Improvements in procurement, stock management, and usage protocols for PPE and pharmaceuticals can reduce expenditures, though absolute savings are smaller. These interventions are typically easier to implement quickly and can complement HRH-focused strategies.

Our work has limitations to consider. First, it used a one-way approach, varying each cost driver independently, which does not capture potential correlations or interaction effects; for example, reducing staff could affect supply use or patient throughput. Second, we assumed linear cost responses, where proportional changes in inputs (e.g., HRH) lead to equivalent cost changes; in reality, some costs are fixed and cannot be reduced proportionally. Third, any reductions in HRH or supplies must be balanced against clinical quality and safety, as cost savings may compromise patient care or facility capacity. Fourth, the findings are context- and time-specific: they reflect baseline costs at a single regional facility in 1 county of Kenya, limiting generalisability. While analysing a single facility allowed precise estimation of unit costs and personnel expenses, our study did not account for lost revenue from preexisting services (eg, outpatient care, surgery, or well-baby clinics), which would influence overall financial outcomes. Finally, we did not perform a cost breakdown by patient severity level, nor did we have epidemiological data on the admitted patients, which could have provided additional insights into cost drivers across different patient groups.

Conclusion

Between June 2020 and February 2022, the total cost of operating TL4H as a COVID-19 isolation facility was KES 489,220,114 (USD 4,181,011). During this period, the Kiambu County Health Department waived KES 160,678,901 (USD 1,374,236) in user fees for the 1449 patients admitted, with the facility’s conversion accounting for approximately 5% of Kiambu county’s budget. Human resources and non-pharmaceutical commodities constituted the largest cost components, suggesting that targeted workforce planning, strategic resource allocation, and increased local production could enhance cost efficiency. The waiver of user fees contributed to advancing universal health coverage by ensuring access to essential care during a public health emergency. These findings highlight that cost-containment opportunities are concentrated in the design and deployment of the health workforce and underscore the importance of integrating cost-driver and uncertainty analyses into health emergency preparedness, enabling policymakers to identify both fiscal requirements and the most effective levers for operational efficiency.

Supplemental Material

sj-pdf-1-inq-10.1177_00469580251381969 – Supplemental material for Operational Costs and Revenue Dynamics of Repurposing a Public Hospital into a COVID-19 Isolation Centre in Kenya: A Facility-Based Case Study

Supplemental material, sj-pdf-1-inq-10.1177_00469580251381969 for Operational Costs and Revenue Dynamics of Repurposing a Public Hospital into a COVID-19 Isolation Centre in Kenya: A Facility-Based Case Study by Magoma Mwancha-Kwasa, Brenda Onyancha, Agnes Wambui Karita, Gerald Kwoba Mang’eni, Emily Ngonyo Muiruri, Hillary Kagwa, Patrick Nyaga, Janefer Maina Kinyanjui, Mike Mulongo, Lizah Nyawira, Prabhjot Kaur Juttla, Moses Ndiritu and Ryan Nyotu Gitau in INQUIRY: The Journal of Health Care Organization, Provision, and Financing

Supplemental Material

sj-pdf-3-inq-10.1177_00469580251381969 – Supplemental material for Operational Costs and Revenue Dynamics of Repurposing a Public Hospital into a COVID-19 Isolation Centre in Kenya: A Facility-Based Case Study

Supplemental material, sj-pdf-3-inq-10.1177_00469580251381969 for Operational Costs and Revenue Dynamics of Repurposing a Public Hospital into a COVID-19 Isolation Centre in Kenya: A Facility-Based Case Study by Magoma Mwancha-Kwasa, Brenda Onyancha, Agnes Wambui Karita, Gerald Kwoba Mang’eni, Emily Ngonyo Muiruri, Hillary Kagwa, Patrick Nyaga, Janefer Maina Kinyanjui, Mike Mulongo, Lizah Nyawira, Prabhjot Kaur Juttla, Moses Ndiritu and Ryan Nyotu Gitau in INQUIRY: The Journal of Health Care Organization, Provision, and Financing

Supplemental Material

sj-pdf-4-inq-10.1177_00469580251381969 – Supplemental material for Operational Costs and Revenue Dynamics of Repurposing a Public Hospital into a COVID-19 Isolation Centre in Kenya: A Facility-Based Case Study

Supplemental material, sj-pdf-4-inq-10.1177_00469580251381969 for Operational Costs and Revenue Dynamics of Repurposing a Public Hospital into a COVID-19 Isolation Centre in Kenya: A Facility-Based Case Study by Magoma Mwancha-Kwasa, Brenda Onyancha, Agnes Wambui Karita, Gerald Kwoba Mang’eni, Emily Ngonyo Muiruri, Hillary Kagwa, Patrick Nyaga, Janefer Maina Kinyanjui, Mike Mulongo, Lizah Nyawira, Prabhjot Kaur Juttla, Moses Ndiritu and Ryan Nyotu Gitau in INQUIRY: The Journal of Health Care Organization, Provision, and Financing

Supplemental Material

sj-xlsx-2-inq-10.1177_00469580251381969 – Supplemental material for Operational Costs and Revenue Dynamics of Repurposing a Public Hospital into a COVID-19 Isolation Centre in Kenya: A Facility-Based Case Study

Supplemental material, sj-xlsx-2-inq-10.1177_00469580251381969 for Operational Costs and Revenue Dynamics of Repurposing a Public Hospital into a COVID-19 Isolation Centre in Kenya: A Facility-Based Case Study by Magoma Mwancha-Kwasa, Brenda Onyancha, Agnes Wambui Karita, Gerald Kwoba Mang’eni, Emily Ngonyo Muiruri, Hillary Kagwa, Patrick Nyaga, Janefer Maina Kinyanjui, Mike Mulongo, Lizah Nyawira, Prabhjot Kaur Juttla, Moses Ndiritu and Ryan Nyotu Gitau in INQUIRY: The Journal of Health Care Organization, Provision, and Financing

Footnotes

Acknowledgements

We extend our heartfelt gratitude to Idah Kinya (Strathmore University) for her invaluable assistance with the probabilistic sensitivity analysis.

Ethical Considerations

Ethical approval was obtained from the Research Ethics Committee (REC) of the University of Eastern Africa Baraton (Approval Number: UEAB/REC/10/06/2020). The study involved secondary data collection only, and all information was de-identified at the point of collection. As no patient-identifiable information was used, informed consent from patients was not required.

Author Contributions

MMK, BO, and RNG conceived and designed the study. MMK, BO, RNG, MM, and LN developed the methodology. Data curation and collection were carried out by BO, AWK, GKM, ENM, HK, PN, and JMK. Formal analysis was performed by MMK, BO, MM, and PKJ. The original draft of the manuscript was written by MMK, BO, and PKJ, with review and editing contributions from MMK, PKJ, and MM. Project supervision and administration were overseen by MN, who also contributed to funding acquisition along with MMK and RNG.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data is available as the S1 File in the Supplemental Information.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.