Abstract

Several states are considering competitive procurement to help shape Medicaid managed care markets. In New York state, the focus of our study, regulators propose contracts that reward quality improvement and simplify state administration by rewarding plans that operate across several of the state’s 62 counties. This case analysis uses novel regulatory data from New York state, obtained via public records request, to examine incentives underlying Medicaid markets and help inform contracting design. The data report plan enrollment by county and plan spending across administrative activities for all 16 Medicaid plans in New York state for 2018. We examine the counties in which plans operate, profitability, and administrative resource allocation. We compare outcomes by tertile of plan profitability, measured as net income per member-month. Plan profitability ranged widely, with the most profitable plan realizing nearly $30 per member-month while the least profitable 5 plans realized net negative earnings. Operational differences across plan profitability emerged most clearly in administrative spending. The most profitable plans reported greater spending on salaries overall and for executive management, and taxes, while the least profitable plans spent more on operational functions including utilization management/ quality improvement, claims processing, and informational systems. We observe modest differences in county rurality and little in geographic breadth. Procurement design that rewards capacity-building in key administrative functions might impact market evolution, given that on average, highly profitable firms spent less on these activities in New York’s Medicaid managed care market in 2018.

Existing knowledge indicates that Medicaid managed care markets vary widely in terms of plan profitability and resource allocation.

Our research contributes by providing novel data analysis from New York state, revealing how plan profitability impacts administrative spending and shedding light on the implications for market evolution and procurement design.

The implications of our research suggest that incentivizing firms to invest in key administrative functions can impact market evolution, potentially influencing policy decisions regarding Medicaid managed care contracts.

Introduction

Medicaid is the largest healthcare coverage program in the United States, covering approximately one-fifth of the nation. Its beneficiaries are primarily poor, disproportionately rural, and otherwise vulnerable populations priced out of private markets. Most states administer most beneficiaries’ coverage through a managed care organization, usually a private insurer, who is responsible for critical aspects of delivering this coverage. Medicaid insurers finance and authorize each episode of care and bear financial risk above the per-member-month capitation fee received from the state. It is thus in the public interest that the private market for Medicaid insurance is fiscally sustainable; viable across the geographies in which beneficiaries reside and seek care; and encouraging of responsible fiscal stewardship that emphasizes adequate investment in medical care and quality improvement. 1

Yet, as private organizations, regulators have little insight into the operations and resource allocation of Medicaid firms, which complicates efforts at improving contract design. 2 This study uses novel data obtained from a Freedom of Information Act request to evaluate the financial performance and resource allocation of New York Medicaid insurers. We put these data into the context of broader trends in the regulatory and market environment to generate insights into potential implications of contract design choices.

Several states are incorporating financial incentives into Medicaid contracts to advance public priorities. While states take a variety of approaches,3(pp. 25–26) competitive procurement, wherein states evaluate invited bids from insurers based on a range of state-defined criteria, such as cost-effectiveness and capacity to serve Medicaid beneficiaries, is the most common, though New York is a notable exception. States are at varying stages of implementation, many are early in the process, some have been successful, while others have faced legal challenges.3,4

In New York, the governor’s office aims to release a request for proposals in late 2023 that will be used to selectively award contracts in coming years.5,6 The aims for procurement design include reducing administrative duplication, by contracting with a smaller number of firms that offer coverage across several of the state’s 62 counties; and favoring firms that demonstrate a commitment to quality improvement.4,5

Perhaps equally as powerful as regulators at shaping the future of Medicaid insurance markets is a co-occurring trend of industry consolidation. Indeed, the number of plans in New York state’s Medicaid market fell nearly in half from 29 to 15 between 2008 and 2023, even amidst Medicaid expansion grew the program’s enrollment. Evidence suggests that the most profitable firms the most likely to survive consolidation, while they either acquire or overpower their profitable peers. 6 Thus, to the extent that there are clear winners within the market, and those highly profitable firms already operate in ways that align with the state’s priorities, the market may naturally evolve toward regulators’ desired ends. By contrast, if profitable plans fail to emphasize state priorities, then contracting incentives could prove more powerful for shaping the market’s evolution. We use the New York data to investigate these questions. First, are there clear winners in plan profitability? Second, to what extent do the operations of profitable firms align with the 2 public aims of geographic breadth and quality improvement?

Methods

Data

This study uses data from New York state’s Managed Medicaid Cost and Operating Reports (MMCOR) and obtained through a Freedom of Information Act request. The data cover the universe of managed care plans operating in the state of New York in calendar year 2018. The sample size is N = 16 plans.

These data reflect mandatory plan reporting unique to New York. 2 Each firm enumerates a total of 87 tables entirely or in part specific to Medicaid on financial and operational outcomes including (our primary focus) categorized administrative spending and profits. In this study, the term “profits” represents net income, defined as the residual amount after deducting all operating expenses, taxes, and costs from total revenue. We use “profits” for its neutrality in applicability to both non-profit and for-profit entities. For non-profit plans, it’s important to note that “profit” refers to surplus funds that are reinvested into the organization to support their healthcare mission, not distributed as shareholder dividends. We also note the distinction in tax structures between these plan types. Non-profits benefit from tax exemptions, reducing operational costs, while for-profits pay corporate income taxes, influencing their cost structures and pricing strategies.

Administrative expense categories include utilization management and quality improvement (listed together), claims processing, and information-management systems. Additionally, expenses on occupancy, depreciation, and amortization of physical capital; and rent and real estate, are listed, as are totals spent on salaries across administrative categories and plan profits, or surplus for non-profit firms.

Finally, firms must report enrollment counts, listed as the total number of member-months covered statewide and by county. Dividing the reported total of member-months by twelve, we estimate that our data represent an annualized enrollment of 4 332 981 managed Medicaid beneficiaries in New York state, corresponding to 98.71% of state-reported enrollment for that year.

To these MMCOR reports, we incorporate data on county characteristics from “Quickfacts” produced by the Census Bureau. We collect county-level social and economic characteristics (proportion female; proportions White, Black, and Hispanic; high school graduation rate; population per square mile; median household income; and poverty rate). We then weight these outcomes according to the percentage of plan enrollees from each county to construct a weighted average of each outcome for each plan. We use these to evaluate demographic characteristics of those counties in which higher-profit plans have a stronger presence.

Analysis

Our analyses are descriptive, with a limited sample size but universal data coverage. We present means of demographic characteristics, weighted by county enrollment as described above. We present administrative spending by category for each firm across the top 7 administrative spending categories, defined market wide. Dollar amounts are presented per enrollee per month, representing the number of dollars received from state Medicaid revenues for each beneficiary’s monthly premium that is then allocated to each administrative category. We present these outcomes by profitability tertiles, which indicate those plans more likely to remain over time amid consolidation (the most profitable) and those more likely to exit the market or to be acquired by their competitors (the least profitable).

Results

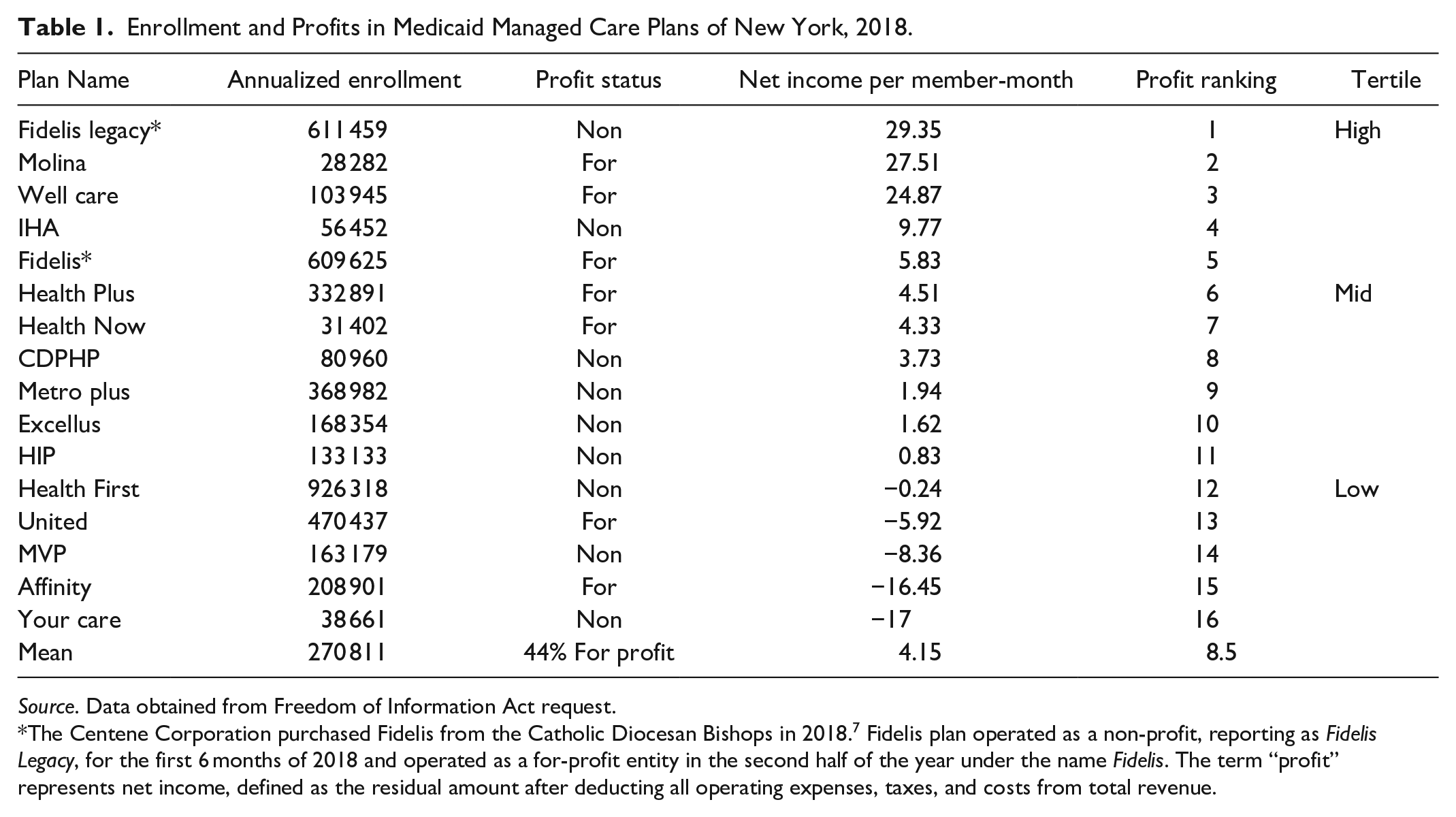

The market for Medicaid managed care plans in New York state has 16 plans for 2018 (Table 1). Annual enrollments range from approximately 28 000 (Molina) to over 926 000 (Health First). Fidelis Legacy operated only in the first half of 2018, was acquired by the Centene Corporation mid-year, 7 then began reporting as “Fidelis” the remainder of that year. At any point during the year, Fidelis comprises the largest plan.

Enrollment and Profits in Medicaid Managed Care Plans of New York, 2018.

Source. Data obtained from Freedom of Information Act request.

The Centene Corporation purchased Fidelis from the Catholic Diocesan Bishops in 2018. 7 Fidelis plan operated as a non-profit, reporting as Fidelis Legacy, for the first 6 months of 2018 and operated as a for-profit entity in the second half of the year under the name Fidelis. The term “profit” represents net income, defined as the residual amount after deducting all operating expenses, taxes, and costs from total revenue.

Levels of profit ranged widely across plans (Table 1). The lowest-ranked tertile, consisting of 5 firms, each realize net negative earnings per member-month. The top 3 plans realized between approximately $25 and $30 per member month in net income. The highest-ranked plan in per-member-month net income was Fidelis Legacy, a non-profit plan that became for-profit after its acquisition. The following 2 highest-profit plans were for-profit. For profits appear generally over-represented among the more profitable plans, with 5 of the top 8 but only 2 of the bottom 8 ranked plans being for-profit.

County characteristics wherein plans operate vary less by profitability (Figure 1). Profitable plans serve more counties on average (29.4 vs 18.8). However, 2 of the 5 most profitable plans were offered in only 2 and 4 counties, respectively (not shown). Furthermore, we observe a pattern in which more profitable plans draw their enrollees from counties that are somewhat more rural on average: with lower population density (11.7 vs 16.7 persons per square mile), lower median household income ($65 700 vs $71 900) and fewer Black and Hispanic, and more White residents on average. At the least, the result does not provide evidence of a lack of profitability in rural counties.

Demographic characteristics of plan enrollee counties, by tertile of profitability.

Figure 2 presents a clearer pattern between profitability and plan spending across administrative functions. Per member-month, profitable plans allocated fewer resources toward operational tasks of claims processing ($0.71 vs $2.44), Utilization Management/ Quality Improvement ($1.35 vs $4.28), and Management Information Systems ($2.88 vs $3.71). By contrast, higher profit plans reported more spending on Occupancy, Depreciation and Amortization; taxes; salaries; and salaries of executive management.

Administrative spending activities per-member-month, New York State Medicaid Managed Care 2018.

On average, each member-month contributed approximately 50 cents toward each executive manager’s salary in high-profit firms, but only approximately half that amount (27.6 cents) in low-profit firms (Figure 2). We should note, these figures reflect salary and fringe benefits but do not include stock options or other equity payments that may add disproportionately to executive earnings in more profitable plans within for-profit firms.

Discussion

This case study yielded several novel insights into the characteristics of profitable plans in New York State’s Medicaid managed care market. The data reveal wide-ranging plan profitability, ranging from approximately $30 per member-month to a $17 loss. The most profitable 5 plans were disproportionately owned and operated by for-profit firms, though we note that both all plans strive to optimize financial performance to sustain operations and fulfill their missions.

Wide variation in profitability carries implications for state regulators amidst ongoing market consolidation. Poor performers were well-differentiated from others and are thus more likely to exit the market or to be acquired by peers capable of generating greater productivity from their assets. 6 In this environment, market evolution is likely to mirror the operations of highly profitable plans to the extent they function differently from poor performers.

The clearest differences between the most and least profitable plans’ operations were the amounts they allocated across administrative activities. The least profitable plans allocated more resources toward operations including claims processing; quality improvement and utilization management; and management information systems. By comparison, the most profitable plans spent more on average on salaries overall, executive management salaries more specifically and franchise and ACA taxes. Additionally, the most profitable plans reported greater administrative losses to occupancy, depreciation, and amortization.

These data point to the potential for incentives to be particularly impactful that reward firms for investing in operational capacity in key administrative activities, particularly those in which Medicaid has fallen behind provider network quality and review of authorization denials.8,9 This could influence more profitable plans to reallocate resources toward these functions or better enable less-profitable plans or mid-tier plans already making these investments to survive industry consolidation.

While the most profitable plans served a greater number of counties at the mean, some nevertheless served only a handful of counties or less. State regulators signaled a preference for the contracting ease associated with plan breadth, given the smaller number of contracts required when each firm covers a wider swath of beneficiaries. In that case, this study suggests regulators may want to explicitly build this into their procurement, as there is no clear evidence that the evolution toward consolidation will clearly favor breadth. Though, this would mean that regulators are effectively rewarding bigger businesses for being big. Given a pattern wherein more profitable plans operated in less urban counties on average, we did not find evidence that market evolution will necessarily lead to “bare” rural counties, which could have been the result if only unprofitable firms, at risk of market exit, served these areas. Instead, the result indicates that rewarding breadth may not necessarily influence access to managed care for rural beneficiaries relative to the outcome with no policy change.

This study’s primary limitation stems from its descriptive nature and the restricted sample size of sixteen plans. Despite these constraints, the unique data source provides a valuable glimpse into the financial operations of all managed care plans in New York’s Medicaid market.

Conclusion

State regulators have the capacity to shape the Medicaid managed care market through well-designed incentives. This case study, covering the universe of plans in New York Medicaid managed care for 2018, provides evidence that the most profitable plans invested less in operations including quality improvement and claims payments in favor of executive management salaries and reported depreciation and amortization. More research is needed to determine if changes in procurement design could be more impactful in shaping market evolution by rewarding critical activities not rewarded by market incentives or by states setting participation standards on finance and quality goals.

Footnotes

Author Contributions

Naomi Zewde: Conceptualization, methodology, data collection, writing—original draft preparation.

Victoria Perez: Data analysis, writing—review and editing, supervision.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical Approval

The authors extend their gratitude to colleagues and reviewers for their insightful comments and suggestions. The study adheres to ethical standards and principles. Our study did not require an ethical board approval because only publicly-available firm-level data.