Abstract

Improving the residents’ health is an important strategy for addressing the declining population dividend in China under the new development paradigm. Based on the panel data of 290 prefecture-level cities in China from 2010 to 2021, this paper uses environmental tax as a quasi-natural experiment, and adopts a DID model to explore the impact of market-based environmental regulation on the residents’ health. The results show that the implementation of environmental tax can significantly reduce the population mortality rate, indicating an enhancement in residents’ health outcomes. Mechanism analysis shows that environmental tax mainly relies on air quality to improve the residents’ health. Also, the heath effect of environmental tax will be effective with the increase of income, and it’s stronger in administrative border areas. Heterogeneity analysis shows that the effect of environmental tax on residents’ health in western regions and resource-based cities is significantly stronger than those in central and eastern regions and non-resource-based cities. This paper provides new evidence for a comprehensive understanding of the impact of market-based environmental regulations on residents’ well-being, offering insights for the implementation of green development strategies.

The environmental tax, as an important environmental regulation, has been proved by scholars on its economic and environmental effects, which us known as “double dividends,” but there is relatively little research on its impact on resident’s health.

The contributions of this study are as follows: First, we explore the “health effect” of environmental tax. Extending the relevant research on the effect of market-based environmental regulation. Second, we provide a new research perspective that analyzing the policy impact from the view of the boundary effect.

The study extends the existing theory on the effect of environmental tax from traditional “double dividend” perspective to the residents’ welfare. We advise policy makers should continue to improve and optimize the environmental tax system to achieve Helah China 2030.

Introduction

Healthy ecology is not only a prerequisite for high-quality economic development, but also a basic guarantee for the public’s well-being. Since the reform and opening up, China’s economy has achieved rapid growth for more than 40 years, which has greatly raised the citizen’s material living standards. However, the traditional development model of “high energy consumption” and “high pollution” has seriously hindered China’s economy from shifting to the quality demographic dividend. According to the “Global Burden of Disease Report” in 2010, environmental pollution, especially air pollution, has become the fourth major risk factor threatening the health of Chinese citizens. In fact, the government has shown great concern for environment and and national health issues: the “Healthy China 2030 Planning Outline” has put environmental indicators into the national health security system, and explicitly stated that people’s health level should enter the ranks of high-income countries by 2030. On the one hand, China is facing severe challenges from population aging and childlessness, disappearing the traditional quantitative demographic dividend. Health capital, as an important source of quality demographic dividend, can not only lessen the labor shortage problem, but also promote unit labor productivity to help the economy develop in a high-quality direction. 1 On the other hand, due to the deterioration of the ecological environment, the shadow price of health has increased, causing the depreciation rate of health capital to accelerate, which has imposed tremendous costs on China’s economy.2 -4 Therefore, in order to solve the problem of ecological pollution and promote the construction of a “Healthy China,” the Chinese government has formulated a series of relevant laws and regulations. Among them, the “Law of the People’s Republic of China on Environmental Protection Tax” (hereinafter referred to as the environmental tax), as a vital step in the green tax reform, has attracted the concerns of many scholars.

To fully exert the advantage of the tax system in moderating the allocation of market resources, and to push green low-carbon development by price signals, China formally implemented the “Environmental Tax Law” in 2018. As one of the important administrative regulation tools for ecological protection, the environmental tax has been widely implemented in Western countries, and studies have successively confirmed its green effects on pollution prevention and the economic effects of stimulating green development at the regional and enterprise levels.5 -11 However, both ecological protection and economic development are closely related to the health and well-being of residents. Therefore, as China’s first single tax law to promote the construction of ecological civilization, can the implementation of environmental tax, a market-based environmental regulation, contribute to the construction of “Healthy China”? Is there any difference in the policy effect among different regions? If so, what is the mechanism behind it? Answering these questions is crucial to decoupling the causal links between environmental regulations and residents’ health, and can provide a reference for China to further optimize its green tax system.

Based on the above analysis, we use panel data of prefecture-level cities in China from 2010 to 2021, and adopt the difference-in-differences method to empirically test the causal link and mechanism channels between environmental tax and residents’ health. The possible marginal contributions of this paper are as follows: First, we extend the relevant research on the effect of market-based environmental regulation. In existing studies on the impact of environmental tax, most scholars have focused on its effects on enterprise performance and innovation, and some literature has also analyzed its impact on ecological protection and economic development from the regional perspective. However, there is little literature that applies a systematic causal identification method to analyze the impacts of market-based environmental regulations on the health of the public. Therefore, we extend the traditional “double dividend” perspective to the residents’ welfare, and explore the policy effects of market-based environmental regulations on residents’ health. Second, it provides a new research perspective for analyzing the theoretical mechanism of environmental regulation. In previous studies, the impacts of environmental regulation within a unit area are assumed to be averaged and homogenized. However, due to the existence of local protectionism in China, whether the local governments are lured by avoiding inspections or free-rider behavior, polluting enterprises are mostly scattered at administrative boundaries. This paper expands the micro-mechanism and realistic path of environmental tax affecting the residents’ health from the perspective of boundary effect. Third, we enrich the related literature on tax, income and health. We integrate environmental tax, residents’ income and health into a unified research framework. Mechanistically, we focus on the differences in the policy effects on residents’ incomes when facing the health effects brought by environmental regulations. It supplements the related research on the distributional effect of tax revenue from the ecological environment perspective.

The rest of this paper is structured as follows: Section 2 briefly reviews and summarizes the related literature; Section 3 proposes the research hypotheses on the basis of combining the policy evolution and related theories; Section 4 is the research design, including method selection and model construction, data sources, variable setting, etc.; Section 5 is the analysis of empirical results and the discussion of the mechanism of the effect; and finally, it concludes the whole paper.

Literature Review

The literature closely related to this paper can be organized into 2 branches: one is the research on the effects of environmental regulation. The other is the research on the factors affecting resident’s health.

The existing research on environmental regulations mainly focuses on 2 aspects: the green economic effect and the residents’ welfare effect. However, there has been comparatively less focus on the resident’s welfare in current research, especially the residents’ health effect, and has mainly focused on the green economy effect instead. Environmental tax is originated from Pigou’s “Welfare Economics,” which advocates the use of tax tools could regulate the negative externalities of enterprises, such as pollutant emissions, and is the theoretical foundation for realizing the “double dividend” effect. Existing studies generally agree that environmental tax has achieved significant performance in air pollution control. 12 It can not only eliminate backward production capacity and realize regional industrial upgrading, 13 but also enhance regional green total factor productivity in a long term.14,15 Meanwhile, according to Porter’s hypothesis, reasonable and strict environmental regulations can force enterprises to increase their green protection investment in a good market structure.16 -18 Thus, enterprises can use these financial supports to innovate green technology, help themselves to realize green transformation, and ultimately, improve enterprise ESG performance. 19 Regarding the welfare effects on residents, there have been studies focusing on the economic dimensions of environmental regulations, such as residents’ income, entrepreneurship, employment, etc., but there is relatively little research on the non-economic dimensions, especially the health. Chay and Greenstone 20 used air quality data caused by the Clean Air Amendment and found that the policy could significantly lower local infant mortality, and the decrease of air pollution was an important mechanism behind it. 20 Do et al 21 further support this argument using data from India. Furthermore, for China’s environmental regulations, Tanaka 22 found that the implementation of the “Two Control Zones” policy significantly reduced infant mortality by 20%. He et al 23 regarded the 2008 Beijing Olympics as a quasi-natural experiment, and found that temporary, phased, and mandatory emission reduction policies in some cities could significantly reduce PM10 concentration and decrease infant mortality by 8%. The most relevant literatures of our study are Williams24,25 and Mathieu-Bolh and Pautrel. 26 They brought the health into the interaction between pollution and environmental tax, and argued that environmental tax affect changes in health caused by pollution, which will magnificently affect labor productivity. However, the discussions on the impact of environmental tax on health were based in the context of developed countries, and in developing countries was relatively been neglected.

Another branch of literature closely related to this study is the analysis of factors that affect the health level of the public. Beginning with Grossman’s health production function, economists began to consider health as an essential component of human capital. Cropper 27 and Wagstaff 28 further considered the effects of the ecological environment and residents’ income on the basis of health production function, and concluded that, except for the natural growth of aging, environmental pollution and residents’ income are the 2 major factors affecting the depreciation of health capital. Generally, higher income levels not only improve personal living standards from the nutritional perspective, but also increase the accessibility of healthcare resources through the disparity of socio-economic status, and thus reduce the health risks they may face. In contrast, environmental pollution, such as air pollution, is an important source that undermines the inventory of health capital and accelerates its depreciation. Chen et al 29 found that air pollution caused by the differences in heating policy between northern and southern China would lead to a shortening of the average life expectancy of residents in northern China by about 5.5 years. In addition to these 2 factors, some scholars have also found that urbanization level, population size, medical conditions, and education level are also major factors affecting health risks.30 -33

Policy Evolution and Research Hypothesis

Policy Evolution

Since the reform and opening up, China’s pollution charge system has been in a constant process of reform and refinement. Its stages of development can be broadly generally divided into 3 stages: the construction and full implementation stage of the sewage fee system (1979-2002); the adjusting stage of the total amount sewage fee (2003-2017); and the official implementation of environmental tax (2018-present).

The sewage fee system was one of the longest-implemented market-incentive environmental regulations in China. In 1979, the official promulgation of the “Environmental Protection Law (Trial)” set the legal status of the sewage fee system. In 1993, the “Notice on the Collection of Pollution Discharge Fee” first reflected the idea of total control: the fees were charged for pollution that did not exceed the standard. Back in 2003, China changed the basis, scope, and standards of the fee system according to a series of laws and regulations. It could be noticed that the fee was not charged by single-factor exceeded concentration but by multi-factor total charges. Also, the charges standards were appropriately increased, and the objects of the collection were expanded from enterprises and institutions to all units and individual industries. This marked the completion of the most critical reform in the history of China’s pollution discharge fee system.

With the implementation of the “Environmental Tax Law” on January 1, 2018, China’s pollution discharge fee system, which has been in place for more than 30 years, has been succeeded by the environmental tax. To ensure a smooth transition from the fee system to the tax system, there are no significant differences between them in terms of collections standards, objects, and scope. However, to solve the problems of compulsory and enforcement problems that were criticized during the pollution discharge fee period and to better exert the double dividends effect of environmental tax, there are still some differences between the 2 systems: First, the legislation of the environmental tax. The execution of environmental tax is strengthened to improve to collection rate. For a long time, the central government continuously formulated and adjusted the fee system to better control pollutant emissions. Nevertheless, existing research believed that the expectation of fee system had not been achieved due to the phenomenon of “incomplete enforcement.” Compared with the fee system, the collection behavior of the environmental tax is guaranteed by legal obligation, and the legal effect is stronger. Second, by increasing the tax rate, the emission reduction of the polluting units is promoted. Another reason why the fee system failed to achieve the goal of enterprise pollutant reduction is that the collection standard was still too low compared with the cost of pollution control, and the economic stimulus for enterprise emission reduction behavior was insufficient. Hence, after the formal imposition of environmental tax law, some regions have taken the initiative to raise the tax rate to stimulate enterprise adjustment behavior, consciously control pollution, and internalize environmental externalities. Third, through the reform of the environmental tax, the tax system is greened. The inclusion of the pollution discharge fee into the tax system is undoubtedly a significant progress. The reform transforms the tax burden of labor factors to other production factors to reduce distortion of existing taxes in capital and labor factors, form more employment opportunities, and thus play the double dividends effect of environmental tax.

Research Hypothesis

The continuous environmental pollution crisis in China is ultimately the matter of production and lifestyle. As for production, various enterprises, especially polluting enterprises, have inescapable responsibilities. As the main source of pollution discharge, these enterprises should actively carry out their ecological construction duties and deeply participate in green development affairs. However, the “negative externality” of environmental pollution makes polluting enterprises lack sufficient motivation to engage in. Therefore, in the face of market failure in ecological protection, the government needs to intervene appropriately.

Theoretically, environmental tax can increase the cost of unit pollution emissions by levying tax, so that the private and social marginal cost of sewage behavior will be consistent. Thus, it can realize the internalization of negative externality of enterprises, and force them to control the scale of sewage emission while pursuing economic benefits. In reality, the original sewage fee system, as a market incentive environmental policy tool, lacks strict statutory support. Although it partly restrained the discharge behavior, its policy effects are quite weak under the idea of “exchanging environmental pollution for economic growth.” Unlike the former, the environmental tax not only establishes the compulsory nature of tax through legislation, but also effectively stops the government’s administrative intervention and enterprises’ rent-seeking behavior by changing the levying mode. In addition, some provinces have raised the environmental tax rate, which will significantly increase the pollution burden of polluting enterprises, forcing them to use renewable clean energy or make green technological innovations in the production process. Ultimately it will achieve the purpose of emission reduction.

And air pollution as the “top” environmental problem shows a significant negative correlation with resident’s health. On the one hand, with the reduction of air pollutants such as sulfur dioxide, nitrogen oxides and total suspended particulates, residents’ risk of suffering from asthma, lung cancer and other respiratory diseases will be greatly reduced, which directly enhances the health of residents. On the other hand, improved air quality will reduce government and household expenditure on healthcare, and the savings can be used to optimize nutritional intake and improve dietary structure. At the same time, improved air quality also facilitates people to increase outdoor exercise and community interaction, thereby reducing the possibility of common diseases such as obesity and depression, which indirectly enhances the quality of national health. Accordingly, In light of the above, we test whether:

Hypothesis 1: Environmental tax can improve the health level of residents by suppressing air pollution emissions.

Income is considered to be an important determinant of health level.31,34 According to the absolute income hypothesis,35,36 the intrinsic mechanism of income affecting health is mainly categorized into nutrition, medical level, and lifestyle. On the one hand, the increase in income not only enriches residents; dietary choices and optimizes their dietary structure; it also reduces the relative price of healthcare services and promotes residents’ investment in health capita. On the other hand, the environmental Kuznets curve shows that in the early stage of economic development, with the increase of per capita income, environmental pollution will continue to increase, but when economic development reaches a certain degree of relative stability, corresponding policy tools can improve environmental quality. Therefore, this paper puts forward the following hypothesis.

Hypothesis 2: The residents’ income can positively promote the improvement effect of environmental tax on the residents’ health level.

Administrative border areas are usually dual hollows of economic development and environmental protection. Due to China’s unique fiscal decentralization and servant promotion mechanism, serious local protectionism often develops among regions. And the invisible wall of administrative boundaries between different districts undoubtedly worsens interregional economic and trade exchanges, and cross-district collaborative governance. And then it would affect economic development, ecological protection, and cultural exchanges in the border areas, thus generating the “border effect.”37 -39 Based on the above theoretical framework, scholars further analyzed from the perspective of local protectionism, and found that due to the negative externalities of pollution and ecological benefits on the administrative boundaries cannot be internalized by the local governments, they would tend to adopt selective enforcement for ecological problems adjacent to the boundaries, resulting in border effect in environmental governance as well.

However, the implementation of environmental tax not only increases the actual tax burden of enterprises, but also significantly improves the collection efficiency. First, the promotion of the legal status enhances the enforcement rigidity of environmental tax, and the reform of the collection and management model also effectively reduces the information asymmetry between the collection department and the polluting enterprises, which significantly improves the collection efficiency of environmental tax. Second, the reform of the revenue sharing ratio between the central government and the local governments for the environmental tax directly increases the income sharing of local governments, which in turn prompts local governments to improve tax collection. Therefore, the implementation of environmental tax can effectively solve the “border effect” of local governments in the process of environmental governance. Thus, we hypothesize that:

Hypothesis 3: Regions with higher boundary ratios can strengthen the promotion effect of environmental protection tax on residents’ health.

Data Sources, Variables, and Models

Model Selection

Referring to Guo et al,10,16,40,41 we use the exogenous shock formed by some provinces raising the environmental tax rate after the implementation in 2018 to construct a difference-in-differences model, and empirically explore the impact of market-based environmental regulation on the residents’ health level. Therefore, this paper takes the criterion of whether cities raise the tax rate after the implementation of environmental tax as the basis of grouping, in which the treatment group is the 141 prefecture-level cities that have raised the tax rate, and the control group is the 149 prefecture-level cities that did not. The comparison of residents’ health level between the 2 groups is used to evaluate the impact of environmental tax on residents’ health level. The specific model is constructed as follows:

Where

Variables Selection

Explained variable

Residents’ health (Deathrate): The mortality rate of the population

Most existing studies use self-rated health as the research object, but the health status answers given by individuals mainly depend on individual subjective judgment, which are often not completely objective and rational. Therefore, considering the WHO definition of population health and the availability of data from prefecture-level cities in China, we choose the population mortality rate as the proxy variable for residents’ health level.

Explanatory variables

Regional dummy variables (Treat)

In the implementation process of the environmental tax, the central government only stipulates the upper and lower limits of the environmental tax rate, the specific tax rate of each province is determined by the local government itself according to the local economic development and ecological capacity. Among them, some provinces chose to smoothly transition the sewage fee system to environmental tax by keeping the tax rate unchanged; while other 14 provinces, including Guangdong, Sichuan, Beijing, Hunan, etc., increased the tax rate accordingly. Therefore, we set a regional dummy variable, which is the control group if the environmental tax rate in the province where the city is located is increased,

Time dummy variable (Time)

The “Environmental Tax Law of the People’s Republic of China” has been officially implemented since January 1, 2018. As a result, we set the time dummy variable,

Mechanism variables

Ecological environment: Air quality (Lnso2 and Lnsmoke)

Compared with water pollution, air pollution has a more direct and serious influence on residents’ health. To accurately measure the impact of environmental tax on environmental quality, we choose industrial sulfur dioxide emissions and industrial smoke emissions as its proxy variables.

Residents’ income: Average wage (Income)

As mentioned earlier, the increase in residents’ income can improve the health level of residents. Considering the availability and completeness of data, the average wage of employed workers was selected as the proxy variable for residents’ income.

Administrative boundaries: Border ratio ( Border_num and Border_Land)

Referring to Kahn et al, 42 we use the ratio of the number of counties located at the boundary of 2 provinces (including multi-provinces and national borders, coastlines) to the total number of counties under the same prefecture-level city to measure the border indicator. At the same time, we also use the ratio of the area of all border counties to the total area of the city to measure the border indicator. And all data we have collected comes from the administrative division map of China.

Control variables

To accurately identify the improvement effect of environmental tax on residents’ health, we refer to the existing literature and add the following control variables that affect residents’ health in the model:

Data sources

In this paper, annual panel data of 290 prefecture-level cities from 2010 to 2021 are selected as research samples to explore the impact of environmental tax on the residents’ health. Limited by the availability and completeness of the data, some provincial and city data such as Tibet, Haidong and Bijie are excluded. All the data in this paper come from the China Urban Statistical Yearbook, China Population and Employment Statistical Yearbook, China Industrial Statistical Yearbook, and statistical yearbooks of provinces and cities, and the missing data are replaced by linear interpolation method. It is worth noting that due to the lack of data on average employee wages in some autonomous regions, to ensure the representativeness of the sample, we exclude the corresponding cities that lack average employee wages when analyzing the moderating effect of residents’ income. The results of descriptive statistics for each variable are shown in Table 1.

Descriptive Statistics.

Results of Empirical Study

Results of DID

The different measures taken by different provinces for the environmental tax rate provide a perfect quasi-natural experiment for the DID method. Table 2 shows the estimation results of equation (1). Where column (1) is the result without adding control variables, and it can be seen that the estimated coefficient of the explanatory variable

Baseline Regression.

, **, and * are significant at the level of 1%, 5% and 10%, respectively. And the robust standard errors in parentheses are clustered at city-level level.

Robustness Tests

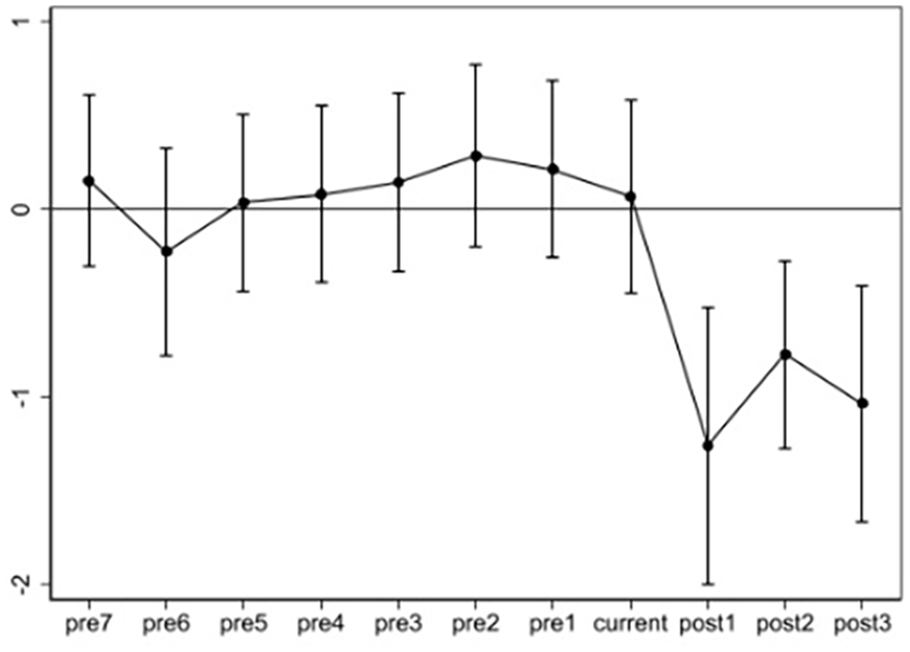

Parallel trend test

The credibility of the results drawn from the DID method depends on the comparability of the treatment and control groups before the event shock. As mentioned earlier, the specific environmental tax rate is decided by each province according to its own economic development and ecological carrying capacity, and grouping based on this standard may not meet the parallel requirement. Therefore, referring to Jacobson et al, 43 we adopt the event analysis method to test whether the population mortality rate of the 2 groups satisfies the parallel trend before the implementation of the “Environmental Tax Law.” To avoid the problem of complete collinearity, we take the first year of the sample period which is 2010, as the reference group for regression. The specific model is constructed as follows:

Where

Parallel trend.

As shown in Figure 1, before the official implementation of the “Environmental Tax Law,” the coefficients of

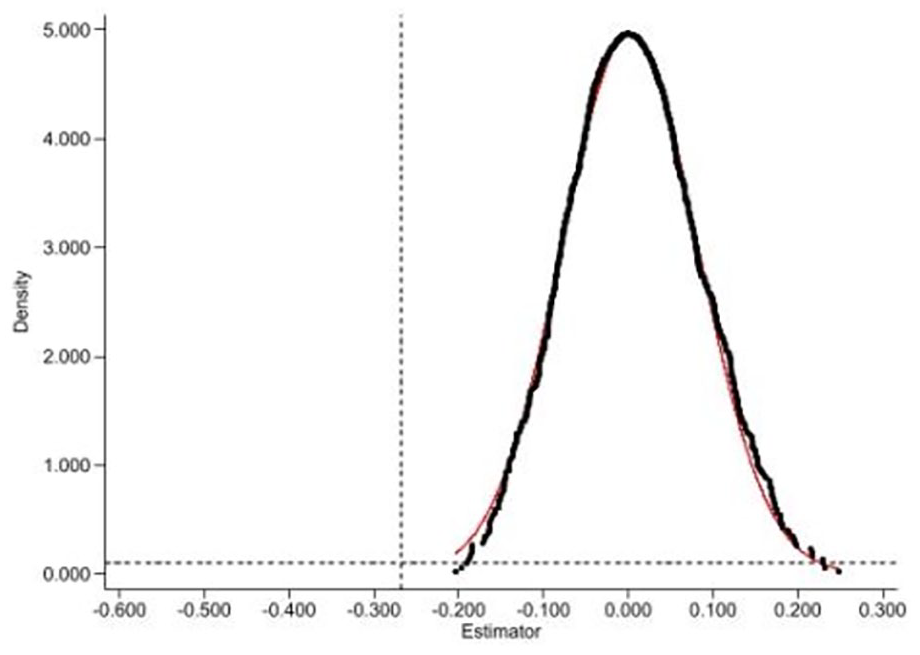

Placebo test

To avoid biased estimation of the baseline results caused by the interference of other unobserved variables, we refer to Guo et al

44

to conduct an individual placebo test in this paper. Specifically, we adopt the bootstrap method to randomly select 141 cities out of the total sample as the cities with increased environmental tax to generate a virtual treatment group, and regress according to equation (1). Meanwhile, to enhance the credibility of the randomized result, we repeat this process 1000 times. Figure 2 plots the kernel density distribution of the regression results, where the black dots are the estimated coefficient values of the virtual treatment group, the horizontal line is the 10% significance level, and the vertical line is the estimated coefficient of the baseline regression (ie,

Placebo test.

Interactive fixed effects

Since different provinces may launch some regional policies that vary over time according to their own conditions, these policies may have different influences on the ecological environment or the health status of the residents. Therefore, it may not be sufficient to eliminate these interferences by only adding city-fixed effect and time-fixed effect in the baseline regression. To control these features of each city that change over time, we add the interactive city-time fixed effect. The specific result is shown in column (1) of Table 3. After adding the interactive fixed effect, the significance of the explanatory variable’s coefficient is obviously increased and still negative. Therefore, the baseline regression results are robust.

Robustness Tests.

Note. Same as Table 2.

Exclusion of competing policy

Controlling the impact of low-carbon city pilot policies. China launched a total of 4 batches of low-carbon city pilot policies since 2011. Its stringent regulation on air pollutants may strengthen the constraints on enterprises and pollution emissions, which in turn affects local air quality and residents health. To control the impact of these policies, we add a dummy cross-term (

PSM-DID

The non-randomness of sample selection will cause systematic errors in the results of the baseline regression. To avoid that bias, we further adopt the propensity score matching method (PSM) to match the samples to ensure that the treatment group is as close as possible to the control group in other features. In this paper, the control variables mentioned earlier are selected in sample matching as covariances. Then, the propensity score as a distance function is used in the 1:1 nearest-neighbor matching method for matching. After dropping the samples that do not meet the matching conditions, the samples under the common support domain are selected to re-regress the equation (1). The results are shown in column (3) in Table 3. It can be found that the results are consistent with the baseline regression.

Other robustness tests

To further test the robustness of the baseline regression results, we perform the following additional robustness tests: First, two-sided trimming of continuous variables. The purpose is to exclude interference of possible extreme values. The result in column (4) of Table 3 shows that the coefficient of the explanatory variable is still significantly negative; Second, the samples of central cities such as municipalities, provincial capitals, and sub-provincial cities are dropped. To eliminate the interference of the differences between central cities and other cities in terms of economy and finance, we exclude the sample data of central cities and re-regress the rest. The result shows that the estimated coefficient of

Mechanism Channel Tests

The study above shows that the implementation of the “Environmental Tax Law” can significantly reduce the population mortality rate and improve the residents’ health. But what are the mechanism channels? And are there potential factors that affect the policy effect? According to the theoretical hypotheses, we divide the mechanism channels of which environmental tax affects regional population mortality into 2 forms: mediating and moderating effects. Mediating effect: The primary goal of environmental regulations such as environmental tax is to reduce pollutant emissions and improve ecological quality. And there are a lot of studies show that the improvement of ecological quality can significantly improve the health status of residents. Therefore, this paper argues that environmental tax can significantly reduce the emission of air pollutants, thereby reducing the regional population mortality rate. Moderating effect: On the one hand, the increase in residents’ income can significantly improve the standard of nutritional intake and healthcare, to improve physical fitness. Therefore, the change of residents’ income is also likely to influence the health effects of environmental tax. On the other hand, bordering areas are usually ecological protection hollows, but the implementation of environmental tax can significantly increase the incentives of local governments to collect tax, which in turn affects the ecological environment and residents' health in border areas. To verify the above mechanism channels, we will empirically explore the health effect mechanism of environmental tax by using equations (3) and (4). 45

Where

Mediating effect

From the perspective of environmental governance, to test whether the environmental tax affects the residents’ health by affecting regional air quality, the paper adopts the local industrial sulfur dioxide emissions and industrial smoke and dust emissions as 2 mechanism variables. Table 4 shows the results of the regression of the equation (3). As can be seen, the implementation of environmental tax significantly reduces industrial sulfur dioxide emissions and industrial smoke and dust emissions at the 99% confidence interval level. And in China’s theoretical and empirical research, the promotion effect of air quality improvement on the residents’ health has been widely confirmed. Therefore, this paper concludes that the implementation of environmental tax can improve the residents’ health by improving the air quality, which verifies Hypothesis 2.

Mediating Effects.

Note. Same as Table 2.

Moderating Effects

Residents’ income effect

While China'’s industrialization and urbanization are proceeding rapidly, the incomes of Chinese residents are also growing steadily. According to Maslow’s Hierarchy of Needs Theory, as incomes increase, people’s preference for their own health becomes more and more prominent, and it is also typical for people to place health as an important element of their welfare evaluation function. The increase in income, on the one hand, can give residents more diversified food choices, and the daily dietary structure will also be optimized. On the other hand, it is easier to access the healthcare resources through the socio-economic status differences. As a result, the differences in resident’s income will have an impact on the health effects of environmental tax.

We use the average salary of employed workers (

Moderating Effects.

Note. Same as Table 2.

Administrative border effect

Local governments are the main carriers of environmental regulations, which are the foundation and guarantee of ecological protection. The previous research suggests that there are obvious differences in the legal conditions between the administrative border and the administrative center in China. At the administrative border, the legal conditions are relatively weak, and phenomena such as collusion between government and enterprises, rent-seeking behavior, etc., are more frequent. Thus, the authority of laws and regulations is relatively small, plus the weak enforcement of the sewage fee system, its restrictive effect on the industrial pollution behavior is small. After the implementation of the environmental tax, its collection behavior is behind the “Environmental Tax Law” as the legal support, the rigidity of law enforcement compared to the sewage fee system has been greatly improved, and can more significantly limit the discharge of pollutants and improve the residents’ health. At the administrative center, the implementation of laws and regulations is already efficient, which can make up for the shortcomings of insufficient enforcement of the sewage fee system, so there is less room for the environmental tax to improve the residents’ health. If the mechanism of enhancing the enforcement rigidity holds, then in the administrative border areas, the effect of environmental tax on reducing the population mortality rate should be greater.

The results of columns (2) and (3) in Table 5 show that the coefficients of the interaction terms are all significantly negative at the 5% level, whether using the number ratio and the area ratio of border counties. It indicates that the improvement effect of environmental tax on the residents’ health is more significant and effective at the administrative boundaries.

Heterogeneity Analysis

Due to China’s vast territory and different natural environments, there are obvious discrepancies in resources and production methods in different regions. The consequent discrepancies in economic models and industrial structures can cause various degrees of pollution, which may lead to differences in the effect of environmental tax on the residents’ health. Based on this possibility, we divide China into East, Central, and West sub-samples according to geographic regions respectively, as well as 2 sub-samples of resource cities and non-resource cities, to conduct the heterogeneity tests.

The regression results in columns (1) to (3) of Table 6 show that the coefficient of the explanatory variables is significantly negative in the western region, while the coefficient values in the eastern and central regions fail the significance test. The above results show that the environmental tax’s improvement effect on the residents’ health is more significant in the western region. This result may be because compared with the western region, enterprises in the central and eastern regions pay more attention to solving environmental problems in their routine production, and their healthcare level and economic development are better than those in the western region. Therefore, the population mortality rate in the central and eastern regions is relatively stable and less sensitive to environmental policy shocks. On the contrary, the western region is in the stage of accelerating socio-economic development, and the priority of regional economic growth is higher than ecological protection. Moreover, the eastern coastal areas are in the process of adjusting and upgrading the industrial structure, they are gradually transferring some high-polluting industries to the western region, resulting in the acceleration of industrial pollution “westward migration.” Therefore, the impact of environmental tax on the population mortality rate in the western part of China is even stronger.

Heterogeneity Tests.

Note. Same as Table 2.

Similarly, the results in columns (4) and (5) of Table 6 indicate that the estimated coefficients of resource-based cities are significantly negative, while the coefficient of non-resource-based cities does not pass the significance test. A possible explanation lies in the fact that resource-based cities are more heavily exploited for natural resources compared to non-resource-based cities. Thus, their ecological environment is more fragile and relatively more responsive to environmental policy. So, environmental tax can better exert its health effect on residents in resource-based cities.

Conclusions and Recommendations

The “Healthy China,” as China’s key development strategy, has aroused widespread discussion in academia. However, the existing literature mainly discusses residents’ health from the perspectives of income, household registration, education, medical service, etc. Few studies explain how to promote the construction of a “Healthy China” from the logical chain of “environmental regulation-environmental quality-residents’ health.” Based on this, we empirically examine the health effect of the environmental tax on residents and its mechanism channels by using the DID method. The results show that the implementation of environmental tax can significantly reduce the population mortality rate by 0.267 units and thus improve the health level of residents, and this conclusion remains valid after a series of robustness tests such as propensity score matching, individual placebo test, and exclusion of competing policies. Mechanism analysis reveals that environmental tax can reduce regional population mortality rates by optimizing air quality. Meanwhile, residents’ income and administrative border areas have a significant positive moderating effect on the health effect of environmental tax. Furthermore, heterogeneity analysis also finds that compared with central-eastern cities and non-resource cities in China, environmental tax is more effective in improving the residents’ health in western cities and resource cities.

The conclusions of this paper have the following 3 policy implications. First, on the road of green tax reform, the implementation of environmental tax effectively solves the phenomenon of “incomplete enforcement” phenomenon of the sewage fee system and reduces the regional population mortality rate by suppressing the emission of industrial sulfur dioxide and industrial smoke and dust. Therefore, environmental tax can not only promote the green development of the economy, but also protect the people’s health and safety. The government should continue to improve and optimize the environmental tax system, formulate a more reasonable environmental tax rate, and improve the enforcement of environmental regulations. Second, while achieving high-quality economic development and improving people’s material living standards, it is necessary to further optimize China’s income distribution system, and give full play to the strengthening effect of income on the health effects of environmental regulations. Third, to reduce the asymmetric effect of the policy effect, local governments should adapt to local conditions and seek a balance between economic growth and ecological protection. They should formulate targeted and differentiated ecological policies, and strengthen the incentives for environmental protection behaviors in the central and eastern regions and non-resource cities. They should carefully prevent enterprises from taking negative behaviors such as production cuts in order to cater to the policy and reduce pollution emissions.

Footnotes

Acknowledgements

There are no additional acknowledgments.

Author Contribution Statements

Guo Bingnan designed the study and proposed the methodology. Feng Weizhe collected the data and analyzed it, and wrote the paper. Lin Ji checked the spelling of the paper and corrected the mistakes and verified the authenticity of the data analysis.

Data Availability Statement

The original data for this paper have been provided by the authors.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by the Philosophy and Social Sciences Planning Project of Zhejiang Province (Grant Numbers: 23NDJC214YB).

Ethical Statement

Our study did not require an ethical board approve because the data we used is from the statistical yearbook from prefecture-level city. There is no potential that it has ethical issue.

Informed Consent

Our study did not include patient experiments, there is no need for patient consent.

Trial Registration Number

Our study did not include medical trial, there is no need for trial registration.