Abstract

The board of directors of a nonprofit proprietary hospital is responsible for supervising and managing major operational matters and reviewing operational results. This study investigates how hospital financial performance is influenced by director and supervisor characteristics among the board members of nonprofit proprietary hospitals in Taiwan. Data were obtained from the Division of Medical Services of the Ministry of Health and Welfare. A generalized linear model was used to evaluate 32 non-profit proprietary hospitals for the years 2006 to 2017, totaling 363 observations. The empirical results revealed a significant positive correlation between the proportion of directors with management qualifications and hospital financial performance. Moreover, the results represented that a higher proportion of board members with a medical background did not correspond to higher hospital financial performance. Although doctors accounted for the highest proportion of board members, indicating their key role in hospital management, the need for board members with management expertise cannot be ignored. Therefore, a balance between directors with management experience and medical knowledge on the board of directors is beneficial for hospital financial performance.

Hospital boards have a central role in strategic financial decision, thus, understanding the characteristics of board members is essential.

This study found that hospital financial performance is related to the board members’ characteristics.

This study can hopefully serve as a reference for hospital administration and policy making based on the board structure.

Introduction

Board directors are the agents supervising hospital operations on behalf of the hospital owners. For the board of directors to operate properly, suitable individuals must be recruited as the directors. Goodall and Pogrebna 1 argued that expert leadership depends on familiarity and experience with the core business, and directors with different professional backgrounds influence hospital financial performance. Therefore, whether board composition, including the backgrounds and qualifications of board members, is an important factor influencing hospital financial performance is a topic worthy of discussion.

In general, the main board members are physicians. They can use their medical expertise to enhance organizational operation and improve hospital quality.2-4 However, some research has suggested that directors with a background in management have financial knowledge as well as cost-control, organization, and integration abilities; accordingly, they have the advantage over doctors due to their financial management experience and can enhance hospital performance. 5 In a word, directors have different influences on hospitals’ operational performance because they have different professional backgrounds and characteristics and can adopt different approaches to management supervision, which is a core aspect of hospital governance.

The relationship between the characteristics of hospital directors and hospital operational performance has been explored.6-8 However, financial aspects have been less studied in relation to operational performance. 9 Sound financial performance can ensure the future operation sustainability of the hospital, and financial performance is therefore an important aspect for hospital management. Therefore, the aims of this study were to elucidate the characteristics of board members of nonprofit proprietary hospitals in Taiwan and examine the influences of these characteristics on hospital financial performance. Moreover, hospitals were classified into large and small ones and relationships were separately explored between 2 sizes.

The rest of the paper is organized as follows. Section 2 presents the literature review, including the theory of hospital governance. Section 3 briefly describes the data set and presents the methods. Section 4 conducts the empirical study and presents the estimation results. Section 5 discusses and analyzes the empirical results, while the last section concludes the paper.

Literature Review

According to agency theory 10 and resource dependence theory, 11 the main functions of a board of directors are to supervise management and provide resources. Agency theory describes the contractual relationship between enterprise capital providers and managers and the agency relationship formed as a result of owners (principals) entrusting managers (agents) to run enterprises on their behalf. However, agency problems easily arise when both parties pursue different profits, and agency costs are incurred accordingly. A board of directors not only offers management supervision but also reduces agency costs, 12 which is the main internal control mechanism. Thus, the functions of a board of directors are crucial for improving corporate governance.13-15

Resource dependence theory holds that the board of directors can provide important resources for enterprises, including providing necessary information for enterprises, assisting managers in obtaining key resources, and maintaining close contact with external environments. 11 The resources offered by the board of directors are based on the experience and expertise of the board members. A board of directors composed of members with diverse professional backgrounds can provide not only a variety of valuable resources but also awareness of changes in external environments.16,17 Moreover, a large board of directors can offer diverse resources and professional knowledge to improve the breadth of perspectives contributing to decision-making processes, which is positively related to corporate performance. 18 Thus, companies can benefit from board members with distinct characteristics who provide a diversity of resources. 19

In conclusion, it has been mentioned in the literature that the functioning of the board of directors is an important part of improving corporate governance. This study deeply explored the relationship between the characteristics of hospital board members and financial performance. Hence, we establish the following base hypothesis.

Hypothesis: Hospital financial performance relates to the characteristics of the board of directors.

Materials and Methods

To understand the characteristics of the board of directors and explore their influence on hospital financial performance in Taiwan, the present study considers board composition (with respect to the gender, educational background, professional background, and duty characteristics of board members) in terms of financial performance, gross operating profit margin, return on assets, net operating profit margin, net income before tax, and net income after tax. Data were sourced from the financial statements of nonprofit proprietary hospitals compiled by the Division of Medical Services of the Ministry of Health and Welfare. Since 2001, when the requirement was first introduced for nonprofit proprietary hospitals to disclose their financial statements, 59 nonprofit proprietary hospitals have been in operation. Because the financial statements from earlier years were incomplete, samples from 12 years were selected (from 2006 to 2017). This study mainly focused on comprehensive hospitals and excluded hospitals that did not provide director lists or financial data in their financial statements. The final samples consisted of 32 nonprofit proprietary hospitals, with a total of 363 observations.

The regression model of the director characteristics and financial performance of the nonprofit proprietary hospitals is as follows:

where the dependent variable Yi, i = 1, 2, 3, 4, 5 represent financial performance. Y1 is the gross operating profit margin, Y2 is the return on assets, Y3 is the net operating profit margin, Y4 is the net income before tax, and Y5 is the net income after tax. The independent variables are as follows: FE is the proportion of women, MAS is the proportion of directors with a master’s or doctoral degree, UNI is the proportion of directors with a university degree, MED is the proportion of directors who were doctors, MAN is the proportion of directors with a management background, SUP is the proportion of supervisors, CHA_MED is the proportion of chairperson with a medical background, and CHA_DE is the proportion of individuals concurrently serving as chairperson and deans. The control variables are as follows: DEBT is the debt ratio, ASSET is the log of the total assets, COM represents corporate hospitals, REL represents religious hospitals, GEN represents general hospitals, which serve as the reference group and are used as the dummy variable. If the hospital attribute does not belong to a corporate or religious organization, then it is classified as a general hospital. Detailed definitions of the variables are provided in Table 1.

Definitions of Board Member Characteristics and Variables.

Source. Financial statements of non-profit proprietary hospitals compiled by the Division of Medical Services of the Ministry of Health and Welfare.

This study explored the relationship between the characteristics of boards of directors and hospital financial performance using the generalized linear model. This model is a flexible generalization of ordinary linear regression, which allows the response variables to have error distribution models with a non-normal distribution.

Results

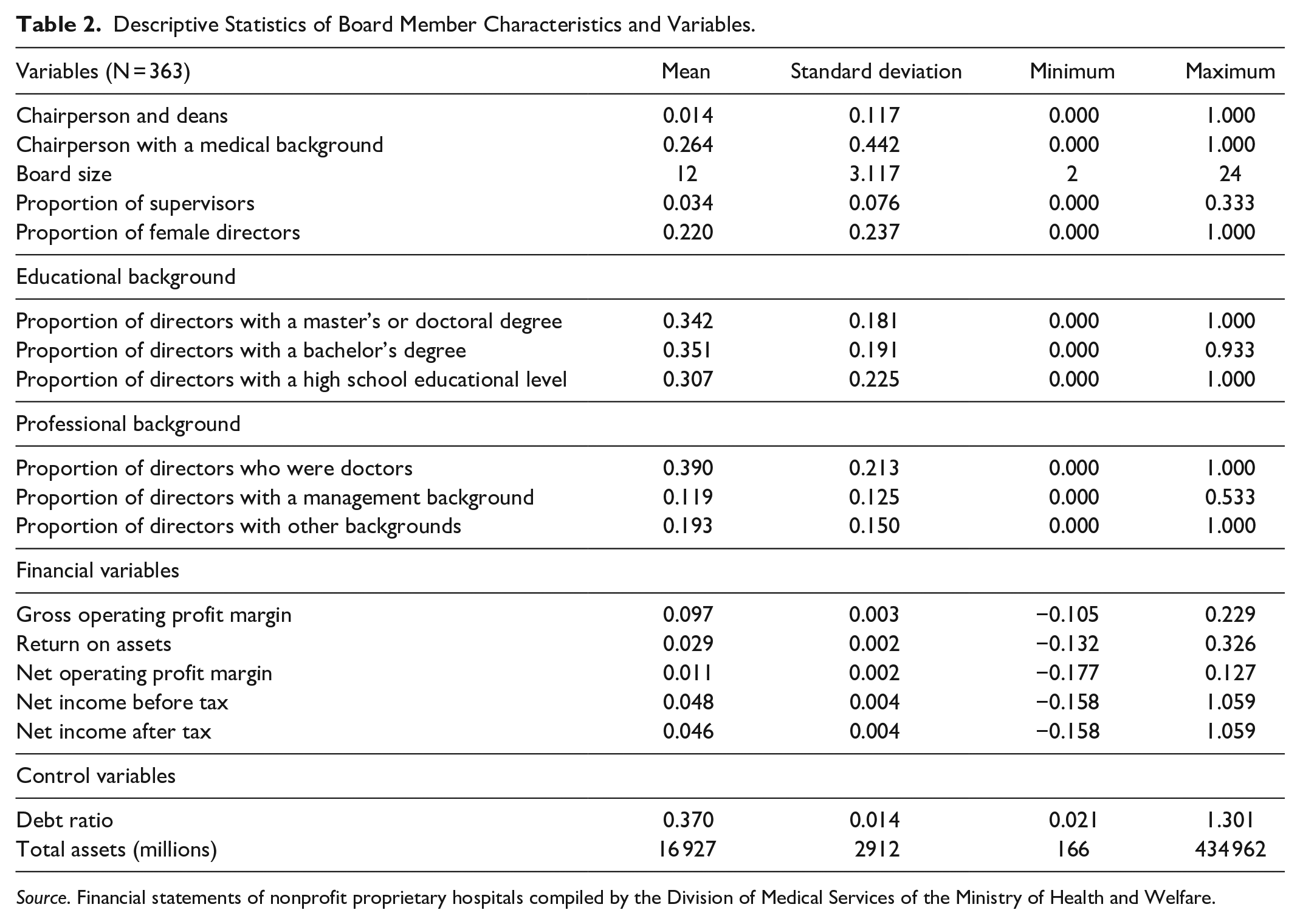

The descriptive statistics of the board member characteristics of the 32 nonprofit proprietary hospitals are summarized in Table 2. The mean of the board members concurrently serving as chairperson and deans was 0.014, and the mean of chairperson with a medical background was 0.264. The mean proportion of supervisors was 3.4%, the average proportion of female directors was 22%, and the average number of directors on a board of directors was 12. These statistics are consistent with Article 43 of the Medical Care Act, which states that a board should be composed of 9 to 15 members. Regarding board composition, the proportion of doctors was the highest (39%), and the proportion of board members with a management background was the lowest (11.9%). Regarding educational background, the proportion of directors with a university degree was the highest (35.1%). The proportion of female directors was 22%, and the proportion of supervisors was 3.4%.

Descriptive Statistics of Board Member Characteristics and Variables.

Source. Financial statements of nonprofit proprietary hospitals compiled by the Division of Medical Services of the Ministry of Health and Welfare.

The regression results are presented in Table 3. The proportion of doctors (−0.140, P < .001) and chairperson with a medical background (−0.050, P < .001) had significant negative influences on gross operating profit margin, and the proportion of directors with a management background had a significant positive influence on return on assets (0.043, P < .01). However, chairperson with a medical background (−0.012, P < .05) and the proportion of directors with a master’s or doctoral degree (−0.039, P < .01) had significant negative influences on return on assets. Chairperson with a medical background (−0.012, P < .05), the proportion of directors with master’s or doctoral degree (−0.050, P < .01), and the proportion of doctors (−0.065, P < .001) had significant negative influences on the net operating profit margin. When the dependent variables were the net income before and after tax, the main independent variables had a nonsignificant influence. Overall, the proportion of directors with a management background was significantly and positively related to hospital financial performance, and the proportion of directors with a master’s or doctoral degree, proportion of directors who were doctors, and chairperson with a medical background were significantly and negatively related to hospital financial performance.

Multiple Regression Analysis of Board Member Characteristics and Hospital Financial Performance.

Note. N = 363. Religious nonprofit propriety hospitals were used as the control group.

P < .10. *P < .05. **P < .01. ***P < .001.

The proportion of doctors (−0.140, P < .001) and chairmen with a medical background (−0.050, P < .001) has significant negative influences on gross operating profit margin, and the proportion of directors with a management background has a significant positive influence on return on assets (0.043, P < .01). The coefficient of both the proportion of female directors and the proportion of supervisors is negative but not significant. In sum, we find evidence in support of the hypothesis that an association exists between the characteristics of the board of directors and financial performance.

As to the control variables, the coefficient of the total assets shows a significant negative effect on gross operating profit margin but a significant positive effect on net income before tax and net income after tax. In addition, both corporate hospitals and general hospitals have significantly higher gross operating profit margin and net income before tax and net income after tax than religious hospitals.

Nonprofit proprietary hospitals were classified according to their asset sizes. Those with total assets of more than NT$10 billion were classified as large hospitals, and those with total assets of less than NT$4 billion were classified as small hospitals. No general hospitals were classified as large hospitals, and no company hospitals were classified as small hospitals. The results of multiple regression analysis for large and small hospitals are displayed in Tables 4 and 5, respectively.

Multiple Regression Analysis of Board Member Characteristics and the Financial Performance in Large Hospitals.

Note. N = 82. Religious nonprofit propriety hospitals were used as the control group.

P < .10. *P < .05. **P < .01. ***P < .001.

Multiple Regression Analysis of Board Member Characteristics and the Financial Performance in Small Hospitals.

Note. N = 197. Those with total assets of less than NT$4 billion were defined as small hospitals. Religious nonprofit propriety hospitals were used as the control group.

P < .10. *P < .05. **P < .01. ***P < .001.

According to Table 4, in large hospitals, only the proportion of directors with a master’s or doctoral degree had a significant negative influence on financial performance; other director characteristics had no significant influence on financial performance. In small hospitals, chairperson with a medical background and the proportion of doctors had significant negative influences on financial performance but the proportion of directors with a management background had a significant positive influence on financial performance (Table 5); this is consistent with the regression results for all of the samples (Table 3).

Discussion

For a board of directors to effectively exercise its supervisory and management duties, its members must have professional knowledge, skills, and experience. 11 Educational level is often regarded as a proxy for measuring an individual’s knowledge and professional skills. 20 Someone with a higher level of education has demonstrated their ability to learn how to use analytical tools and develop logical thinking, organization, and integration skills. People from different professional backgrounds have different values and views, which influence their judgments and decisions.6,21 The different perspectives offered by hospital board members with different professional backgrounds can improve a hospital’s health care quality, operating efficiency, and financial performance. 22 Directors’ behaviors and governance also influence the operation decisions of hospitals.23,24 Literature on hospital management has mainly classified directors’ professional backgrounds into the 2 categories of medicine and management.25,26 The Organization for Economic Cooperation and Development reported that an increasing number of doctors are involved in hospital management, 27 and considerable attention has been paid to the influence of doctors serving as managers on hospital operating efficiency. 28

This study investigates the relationship between hospital financial performance and director and supervisor characteristics among the board members of nonprofit proprietary hospitals in Taiwan. The empirical results showed that the proportion of directors with a management background was significantly and positively related to hospital financial performance, while the proportion of directors who were doctors, and chairperson with a medical background were significantly and negatively related to hospital financial performance.

Directors with a background in management generally have organization-management, financial-planning, responsibility-accounting, or cost-control abilities 29 ; these directors provide financial knowledge, have the abilities to make organizational decisions and solve problems, and pay attention to overall operational performance.30,31 Hospital board members without sufficient financial knowledge or attention to hospital performance are less likely to agree on goals—inconsistent with the best interests of hospitals. This study discovered that a high proportion of directors with a management background is helpful for improving hospital financial performance, which is consistent with the previous results.29-31

Moreover, directors with a medical background have a strong influence on an organization because of their familiarity with major medical procedures as a result of their medical education and clinical experience.3,29,32-34 Directors with a medical background can provide clinical knowledge and insight into health care policies, thereby enriching board meetings.7,35 Weiner et al 36 pointed out that these directors can establish communication mechanisms among doctors, managers, and the board of directors and gain the trust of clinical staff in decision making through their professional values and common goals, which demonstrates the importance and necessity of doctor leadership. Veronesi et al 37 identified a positive relationship between directors with a medical background and continuous improvement in health care quality; additionally, they discovered that doctor-led hospitals have reduced mortality rates and higher levels of patient satisfaction, which is significantly and positively related to health care quality improvement.4,38,39

By contrast, Agarwal et al 40 found that the number of doctors serving on a hospital’s board of directors is unrelated to management performance because doctors are primarily responsible for clinical quality rather than hospital management. Thus, some researchers believe that board members concurrently serving as doctors and directors reduce the effectiveness of a hospital’s board of directors. 41

In agreement with the previous findings,42,43 the present study found that the proportion of doctors on a hospital’s board of directors was negatively related to hospital financial performance, probably because doctors’ expertise lies primarily in medicine. Doctors focus on providing medical services and improving health care quality, whereas managers emphasize increasing income from patient services and controlling operating costs. Therefore, a high proportion of doctors on the board of directors does not benefit hospital financial performance.

Although this study pointed out that having more doctors on the board of directors results in worse financial performance, it does not mean that having fewer doctors on the board would be better for hospital performance. In view of the current distribution of a higher proportion of doctors on the board of directors, if the number of doctors on the board of directors is further increased, it may be detrimental to the financial performance of the hospital.

Regardless, doctors are still needed on the boards of directors of hospitals. According to Article 43 of the Medical Care Act, the number of directors with medical qualifications should be no less than 1/3 of the total, with at least 1 doctor. The Medical Care Act highlights the necessity of doctors as hospital board directors, but the empirical results of this study demonstrate the importance of management expertise. Thus, the combination of management expertise and medical knowledge in a board of directors can help in achieving the full effects of knowledge management to improve hospital operational performance.

The influence of chairperson characteristics on organizational performance has been explored in many studies. This study indicated that chairperson with a medical background had significant negative influences on hospital financial performance. The main responsibility of chairperson is to ensure that the board of directors has appropriate human capital and that all board members are competent directors, thereby jointly meet the requirements of management teams in terms of goals, resources, regulations, rights, and liabilities. Hence, chairperson serve a crucial role as board leaders. 44 Orlikoff 45 pointed out that chairperson serving concurrently as deans can receive the latest information regarding the operation and management decisions of the board of directors in a timely manner, provide direct instructions for making timely and sound judgments, and implement operation principles. Brickley et al 46 suggested that having chairperson who serve concurrently as deans can help improve organizational performance.

However, some studies have proposed that this may cause conflicts of interest between internal managers and stakeholders, making it difficult to make clear judgments. 47 Wang et al 48 pointed out that the professional knowledge and work experience of chairperson have a significant positive influence on organizational performance and that chairperson with a medical background are positively related to hospital performance. Prybil 8 discovered that in the United States, hospitals with better performance had a higher proportion of doctors on their board of directors. Similarly, research has indicated that the proportion of doctors on the board of directors is significantly and positively related to return on assets 9 and that hospitals that have board directors with a medical background perform better than those that have board members with a management background. 6 Offering a different perspective, Kuntz et al 9 suggested that such directors are negatively related to financial performance (net income, earnings before interest, and tax).

Although some studies have reported that directors with a medical background can improve financial performance,4,37,48,49 Sarto et al 50 argued that such directors have a negative influence on hospital financial performance. Alexander and Morrisey 42 and Succi and Alexander 43 argued that directors with a medical background are prone to conflict due to divergent interests, which is unfavorable for doctors’ outpatient services, increases medical costs, and reduces hospital operating efficiency.

On average, 22% of the board of directors of the non-profit proprietary hospitals are women, indicating that the gender of board members is not unitary. Female directors are conservative and cautious in governance, have objectivity and reflect a sense of responsibility, which improves the efficiency of supervision 51 and helps to improve the performance of the organization.52-55 However, no significant results are obtained in this study. In addition, supervisors in the board of directors account for only 3.4% on average. Supervisors only perform supervisory duties and are not responsible for financial management, and currently, Taiwan’s Medical Law does not mandate the establishment of supervisors in hospitals, therefore the sample of supervisors in the board of directors is small, resulting in an insignificant impact on the financial performance of the hospital.

As for the control variables, total assets have a positive and significant impact on net income before tax and net income after tax, but they have a negative and significant impact on gross operating profit margin. Generally, hospitals with larger scales have more severe illnesses. The cost of treating these patients is high, which is not conducive to the gross operating profit margin, but in terms of overall profitability, the larger scale still helps hospital financial performance. In addition, the debt ratio has a negative and significant impact on net income before tax and net income after tax, showing that the higher the debt ratio, the higher the operating risk, which is not conducive to the financial performance of the hospital. Finally, the financial performance of corporate hospitals and general hospitals is better than that of religious hospitals, which is consistent with the results of Chang, 56 and which shows that corporate hospitals are more profitable than other types of non-profit propriety hospitals.

From the empirical results, most of the director characteristics had no significant influence on financial performance in large hospitals. However, in small hospitals, the proportion of doctors had significant negative influences on financial performance but the proportion of directors with a management background still had a significant positive influence on financial performance. To save labor costs, most small hospitals directly select their board members from medical staff currently employed at the hospital. This may explain why most of the board members of the small hospitals in this study were doctors. However, to deliver effective management supervision, board directors should possess operation management, supervision, and auditing abilities. Therefore, small hospitals should aim to employ professional directors in of their board of directors and increase the number of members with a management background, which would help in making decisions concerning hospital management and improve hospital financial performance.

This study was subject to some limitations that could not be overcome. The first is that an empirical model was adopted to explore the relationship between the director characteristics and financial performance of nonprofit proprietary hospitals, but the causal relationship was not explored. The second limitation is that the director characteristics considered in this study were based on information obtained from the director lists of registered nonprofit proprietary hospitals, but complete information regarding the background and education of hospital directors could not be obtained from online platforms because of the Personal Information Protection Act. The third limitation is that this study only used nonprofit proprietary hospitals as the subjects and excluded other private hospitals. A comprehensive study on all hospitals in Taiwan can only be carried out if these hospitals disclose complete financial statements to the public in the future.

Conclusions

Operation of the board of directors is a key aspect of hospital governance, and competent authorities have paid increasing attention to strengthening board functions. This study explored the characteristics of members of the boards of directors of nonprofit proprietary hospitals in Taiwan to understand their influence on financial performance and thus the importance of their role in hospital governance. The empirical results revealed that a high proportion of directors had a management background, which was positively related to hospital financial performance. However, the proportion of directors who were doctors were negatively related to hospital financial performance, indicating that although including people with a medical background on a hospital’s board of directors is necessary, a higher proportion of such directors is less beneficial for hospital financial performance. Therefore, according to the findings of this study, a balance between the proportions of board directors who have a management background and those who are doctors can help to improve hospital financial performance.

Compared with corporate governance systems, hospital governance systems have not yet matured. The empirical results of this study can hopefully serve as a reference for nonprofit proprietary hospitals and competent authorities to understand and recognize the importance of the member characteristics and board structure of hospital boards of directors. Accordingly, these authorities can ensure that hospital boards can provide strategic guidance and effective supervision at the management level, thereby strengthening their role in hospital governance. Other types of hospitals should be included in future studies to explore the relationship between hospital board member characteristics and financial performance, and family ties among board members can also be explored in depth.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.