Abstract

Although medical debt has been associated with housing instability, almost no research has connected homelessness to medical debt. We interviewed 60 individuals experiencing homelessness in Seattle, selected from those participating in self-governed encampments organized by a homeless advocacy organization. Most respondents reported having at least one kind of debt, with two-thirds reporting current medical debt. Almost half reported trouble paying medical bills for themselves or family members. Almost one-third believed medical debt was in part responsible for their current housing situation. More than half with medical debt incurred this debt while they were covered under insurance. People who had trouble paying medical bills experienced a more recent episode of homelessness 2 years longer than those who did not have such trouble, even after controlling for race, education, age, gender, and health status. People of color who had trouble paying medical bills reported almost 1 year more homelessness than whites.

Keywords

Medical debt and medical debt-related bankruptcy are common: more than 1 in 4 Americans are paying off medical debt and even more struggle to pay medical bills, while more than 60% of U.S. bankruptcies have been stubbornly linked to medical causes, even after the 2010 Affordable Care Act expanded access to Medicaid and private insurance.

Study participants with medical debt had a longer most recent episode of homelessness on average (22.4 months) than those without medical debt; those whose medical debt case was sent to collections had, on average, 15.5 years of homelessness overall, compared to 4.4 years of homelessness for those not sent to collections. The effect of debt on homelessness was particularly strong for people of color.

We were surprised at how even small amounts of debt were associated with longer duration of homelessness; we also found insurance was not protective—more than half of respondents with medical debt reported having insurance at the time they incurred the most medical debt.

Introduction

Prevalence of Medical Debt

Medical debt and medical debt-related bankruptcy are common.1-9 In 2016, roughly 16% of U.S. consumers’ credit reports included medical debt, defined as unpaid medical bills in collections, with more than $81 billion owed. 10 A 2017 study reported more than 1 in 4 Americans are paying off medical debt and more than a third struggle to pay medical bills. 11 In 2018, 31% of adults with a credit bureau record had debt in collections, and 16% had medical debt in collections. 12

Low income, lack of health insurance, and poor health have been associated with difficulty paying medical bills after controlling for demographic covariates. 13 The uninsured are about 3 times more likely to incur medical debt than those with private insurance.1,8,14,15 Common causes of medical bankruptcy include hospital bills, prescription drug costs, doctors’ bills, insurance premiums, medical equipment, cost of nursing homes, and income loss from illness.4,7,16

Bankruptcy, Especially Post-Affordable Care Act

More than 60% of U.S. bankruptcies have been stubbornly linked to medical causes, even after the 2010 Affordable Care Act (ACA) expanded access to Medicaid and private insurance.2,3,17 A 2015 survey of beneficiaries of ACA-related Medicaid expansion reduced the probability of being worried and stressed related to paying bills, 18 but the underinsured report more medical debt, 19 and health insurance rarely provides complete protection from medical bankruptcy. Although current ACA policies mandate insurance plans cover 60% of expected medical care costs, and most medical debtors have coverage, insurance rarely covers all costs.3,6,17,20

Inequities Associated With Medical Debt

America’s large income inequality problem is exacerbated by the U.S. market-based health system, generating inequitable health outcomes. 21 Lichtenstein and Weber found disproportionately high rates of medical debt among black Americans living in racially distinct neighborhoods and that medical debt was a driver of foreclosure and racial disparities in homeownership. 22

Medical Debt Is Associated With Housing Instability

Several studies have linked medical debt or medical debt-related bankruptcy with housing instability,5,8,20,23-25 but only one identified homelessness as an outcome. 23 Fifty-six percent of people with medical bill problems reported making significant trade-offs as a result of medical bill payment or pressure to pay, including forgoing necessities such as food, rent, or heat; spending their savings; incurring credit card debt; and declaring bankruptcy. 8 A 2007 study exploring a previously undocumented association between medical debt and its effects on “low-income families’ efforts to own, rent, or maintain their homes” 5 found 25% of respondents said their medical debt led to housing problems; furthermore, individuals with medical debt on their credit reports were twice as likely to have housing problems than those whose credit reports did not include medical debts. 5 Nine percent of homeowners facing foreclosure in Philadelphia cited illness or medical costs as the primary reason for being behind on mortgage payments.24,25 In the same study, half of survey respondents listed a health-related cause as contributing to the foreclosure of their home. The study was small, and the response rate was 7%, but it suggests a link between medical costs and housing instability. 25 Houle and Keene 24 examined the risk of default and foreclosure using data from a nationally representative longitudinal study of older middle-aged adults, finding worsening health increased the risk of default and foreclosure.

Owing to burgeoning homelessness on the West Coast, and competing narratives about the origins of this problem, we sought to understand how one large trigger for financial instability might also be linked to housing instability. We aimed to understand whether trouble paying medical bills could be associated with length of homelessness in a population experiencing homelessness in Seattle.

Methods

We surveyed 60 people living in encampments and shelters in Seattle and King County to examine the relationship between debt, especially medical debt, and length of homelessness. After obtaining University of Washington human subjects research approval (#50806), we worked with Seattle’s Tent City 3 (TC3), under the umbrella of Seattle Housing and Resource Effort (SHARE), to develop the questionnaire for our survey. We tested several prototypes with residents of TC3 before beginning formal data collection.

Our sample was restricted to people older than 18 and currently experiencing homelessness in Seattle and King County, Washington, and to those who were currently staying in encampments and/or shelters (n = 60). Over the course of a 4-month period, the lead author (J.B.) made repeated visits to 9 shelters, encampments, and basic services organizations, conducting between 1 and 3 interviews per visit in a private location on the grounds of the shelter, encampment, or organization.

To recruit subjects, we gained permission in advance from each shelter or encampment. This required us to attend the weekly camp meeting and having the residents vote on whether to participate. In all cases, camps voted to invite us in to conduct interviews. When we arrived, we alerted the front desk of our presence, and word was circulated that we were in camp. People then approached the interviewer, rather than the interviewer approaching the prospective participant. Owing to this recruitment method, we are unable to tally the number of individuals who “declined” the survey.

Nonmonetary incentives were offered to the shelter, encampment, or organization as a whole, rather than providing incentives to specific respondents. These included blankets, toiletries, body-warmers, cold and flu medicines, and coffee. The governing bodies of the camps advised us to give nonmonetary incentives to the group as a whole, rather than to individuals. This way, the entire encampment, shelter, or service organization benefited from the research, rather than only responding individuals. This was intended to reinforce the community-oriented ethic of Seattle’s self-governing, democratic encampments.

When compared with data from the City of Seattle’s 2016 Homeless Needs Assessment, 5 conducted concurrently with this study and with a sample size of 1050, we found our sample was slightly older, more educated and white. Our questionnaire is available upon request.

We collected 5 types of self-reported information: length of housing instability and homelessness, health status, access to and utilization of health care, financial information, and socio-demographic factors. Questions regarding health care access, quality, and subjective health measures were taken from previously validated survey tools.1,14,26-29 The questionnaire included between 32 to 44 questions, depending on skip patterns. Data were captured using Open Data Kit software on an e-tablet. All participants provided consent as required by our human subjects approval. Each interview lasted, on average, 37 minutes. We collected demographic information about each respondent. For the purposes of our regression model, sex and race were treated as binary. Self-reported length of housing instability and homelessness was calculated from 2 questions asking in which year the individual first experienced homelessness and how long the person had been staying at their current location. A person’s health status can predict the consumption of health care services, and, therefore, medical costs. 19 We examined 5 self-reported health factors, using questions from previously validated questionnaires. First, we simply asked respondents to rate their health status on a scale from 1 to 5. 30 We asked which medical conditions they had experienced, using a checklist of 17 common health issues adapted from the 2008 Arizona Health Survey,14,31 including chronic physical conditions, mental health problems, trauma, physical disability, and drug and alcohol use. We assessed well-being using standardized depression and fatigue scales. 30

We measured debt and medical debt using 8 variables, as informed by measures used in 2 national and 1 state-based surveys.1,14,26 We asked about trouble paying medical bills for self or family members, current responsibility for medical bills, dollar amounts of medical bills owed, whether a medical bill was sent to collection, if medical debt was in part responsible for the current housing situation, whether bankruptcy had ever been declared, and if there was other debt including student loan, credit card, pay day loan debt, or other debt.

We examined 6 medical access and utilization factors: insurance coverage, number of doctor and dentist visits in the past 6 months, usual source of care, and problems attending doctor’s office visits or picking up prescriptions in the last 6 months.

All analyses were conducted using R Version 1.0.136. We used Fisher’s exact tests and 2-tailed t-tests to assess average length of current episode in months and years since the participant was first homeless in relation to predictor variables. Tables present sample sizes and valid percentages; respondents omitting answers to any question were excluded item-by-item from analyses.

We built our regression model by first calculating univariate statistics to examine the independent variables associated with length of homelessness. We examined continuous variables to determine if they were normally distributed. We plotted variables on scatterplots with LOESS curves to examine their association with length of homelessness. We used t-tests for continuous variables and Fisher’s Exact or chi-square tests for categorical variables to determine if any independent variables were associated with length of homelessness. Variables with associations with p-values at .25 or lower were included in our models with variables indicated as needed based on our conceptual model. After constructing multiple models, we compared the likelihood ratios to determine if additional independent variables contributed to the model. We dropped 5 cases from the regression analysis as those cases did not have complete information on the independent and dependent variables in our final model (n = 55). Our final linear regression model predicted length of homelessness with “trouble paying medical bills,” with binary responses “no trouble” compared to “any trouble.” We controlled for health status and 4 demographic variables (white compared to non-white, 4 levels of education, sex, and 2 levels of health status).

Results

The profile of the typical respondent in our Seattle-based study was a 48-year-old white male whose last stable housing was in Washington State, and whose most recent episode of homelessness was slightly more than a year in length (despite having first experienced homelessness, on average, 11 years prior). Our “average” person-in-profile graduated from high school or had a 2-year degree. This person had medical debt, though it amounted to less than 1000 dollars, quite possibly in collections. He was currently covered under Washington’s expanded Medicaid program, AppleHealth, which became available to low-income individuals without children in 2010 as part of the ACA. Our typical respondent had one or more doctor visits in the last 6 months, had experienced trauma, had at least one mental health diagnosis, and had about 3 chronic health conditions (Table 1).

Respondent Demographics.

Note. Survey of (N = 60) individuals living in homeless encampments and shelters in Seattle, Washington, between January 1, 2017, and April 5, 2017 (interviews conducted by the author J.B.). GED = General Educational Development.

The average length of the most recent episode of homelessness was 17 months, but the average first experience of homelessness was 12 years ago. Most participants reported having at least one kind of debt (82%), with 68% of the total sample reporting current medical debt. Almost one-third of participants (30%) believed medical debt was in some part responsible for their current housing situation. Of those who reported having current medical debt, 40% responded they thought medical debt was in some part responsible for their current housing situation. Almost half of the sample reported having trouble paying medical bills for themselves or for their family members, and of those, 74% of cases were sent to collections. More than half (56%) of respondents with medical debt incurred debt while they were covered by insurance. Almost half (47%) of respondents with medical debt reported debt in amounts under 1000 dollars, and 31% reported debt in amounts under 300 dollars (Table 2).

Respondent Self-Reports of Personal Debt.

Note. Survey of (N = 60) individuals living in homeless encampments and shelters in Seattle, Washington, between January 1, 2017, and April 5, 2017 (interviews conducted by the author J.B.). GED = General Educational Development.

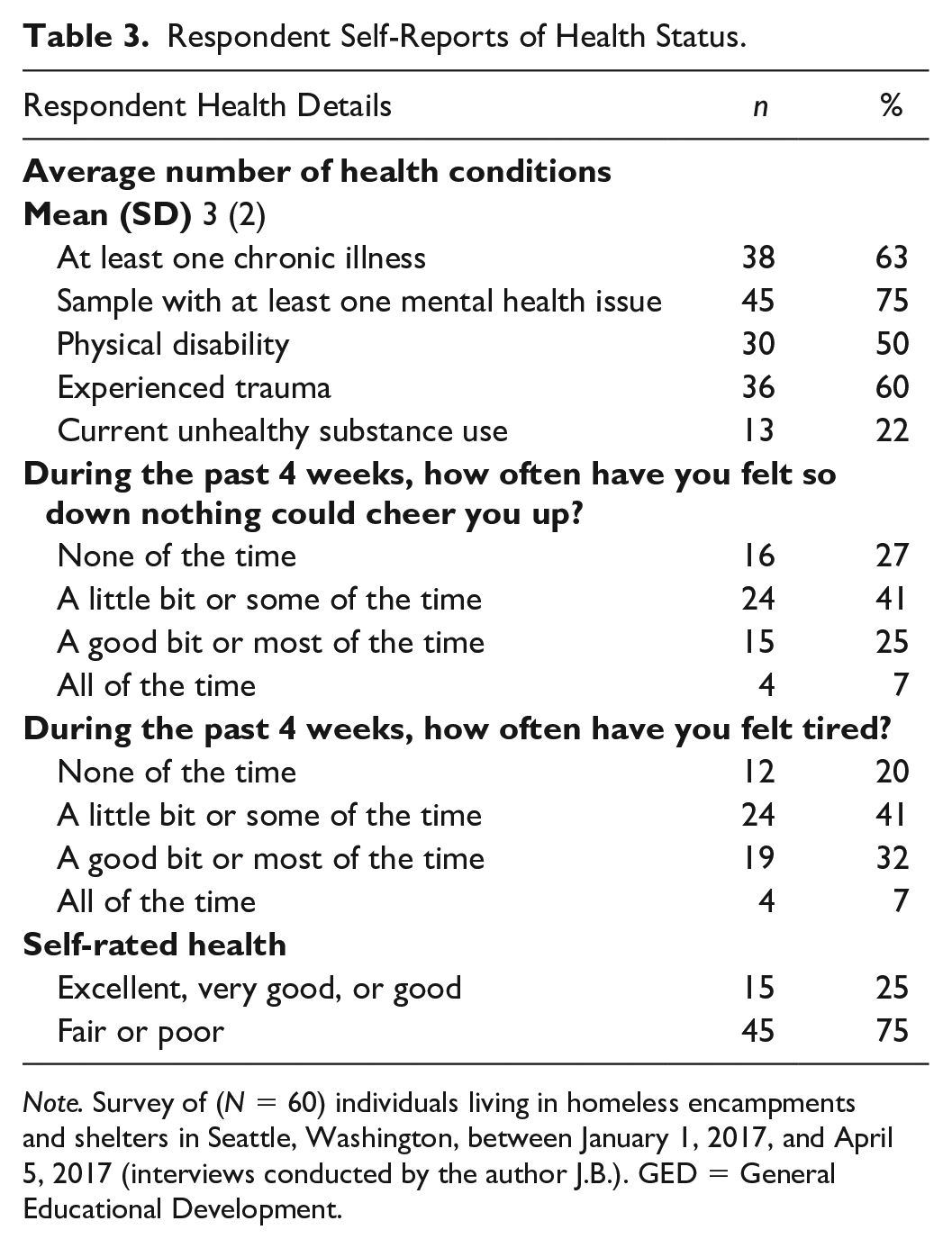

Just fewer than 95% of respondents reported having at least one of the 17 medical issues we asked about, with an average number of 5 health conditions. Almost two-thirds of respondents had at least one self-reported chronic illness (63%), and 75% had at least one self-reported mental health issue. Half of respondents reported at least one physical disability and 60% reported having experienced trauma. Three quarters of respondents reported fair or poor self-rated health (Table 3).

Respondent Self-Reports of Health Status.

Note. Survey of (N = 60) individuals living in homeless encampments and shelters in Seattle, Washington, between January 1, 2017, and April 5, 2017 (interviews conducted by the author J.B.). GED = General Educational Development.

The majority of respondents (83%) had insurance at the time of the survey, with 62% covered under Medicaid/AppleHealth. One quarter of respondents reported lacking coverage at some point in the last 12 months, and almost half the sample reported avoiding medical care and filling a prescription at some point in the last 6 months. On average, respondents reported having 4 doctor appointments and 1 dentist appointment in the last 6 months. Two in 5 respondents (40%) had 3 or more doctor’s visits (Table 4).

Medical Access and Utilization.

Note. Survey of (N = 60) individuals living in homeless encampments and shelters in Seattle, Washington, between January 1, 2017, and April 5, 2017 (interviews conducted by the author J.B.). GED = General Educational Development.

Emergency room visits are not included.

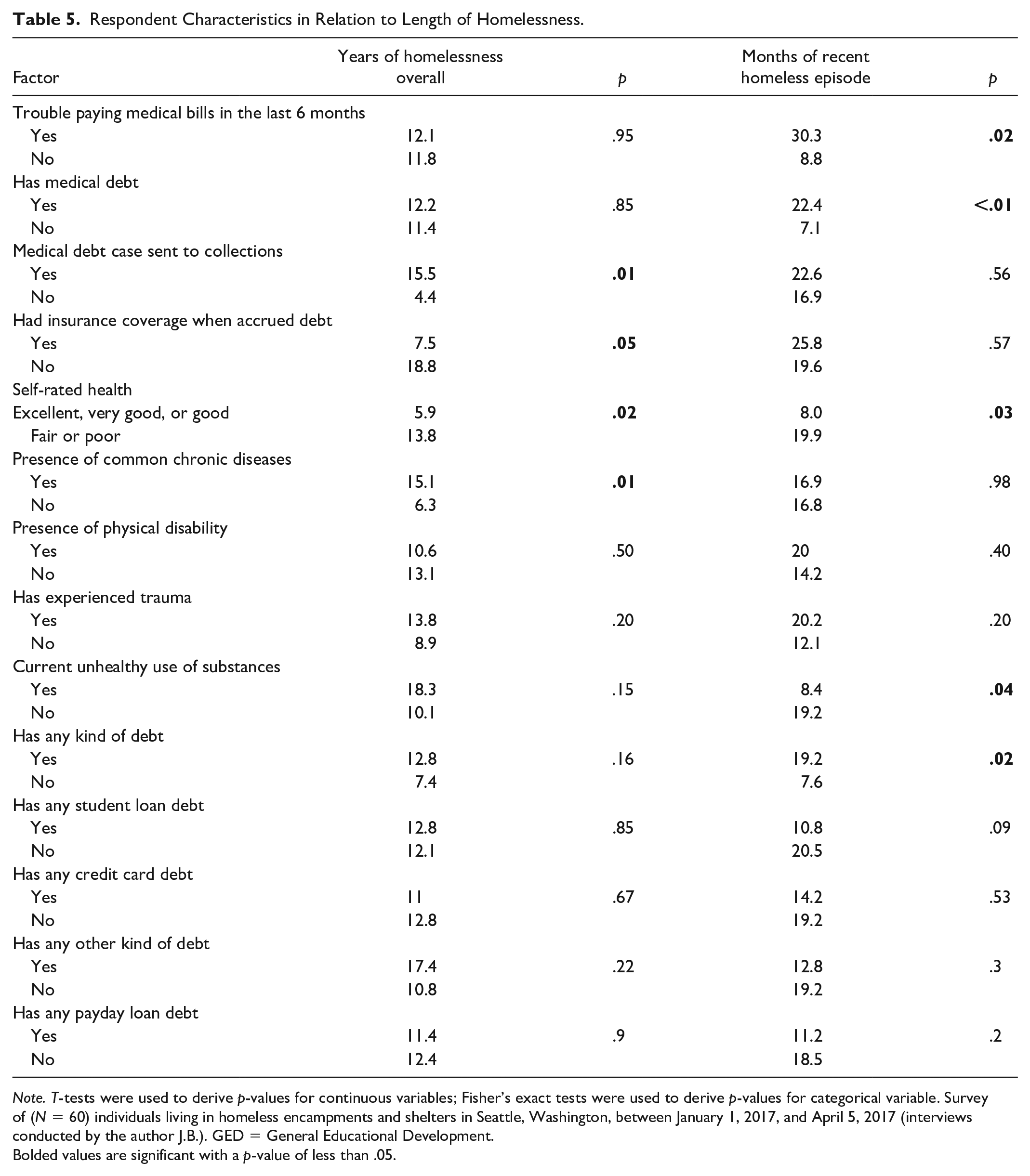

Using 2-tailed t-tests, we found a significant association between the presence of any kind of debt and length of most recent episode of homelessness (p = .02), with those who had any kind of debt reporting, on average, 19.2 months of homelessness and those without any kind of debt reporting 7.6 months. Those whose medical debt case was sent to collections had, on average, 15.5 years of homelessness overall, compared to 4.4 years of homelessness overall among those who did not have their case sent to collections (p = .01), and respondents with medical debt had a longer most recent episode of homelessness on average (22.4 months) than those who did not have medical debt (7.1 months, p = .008). Respondents who had trouble paying medical bills for themselves or family members also reported a longer recent episode of homelessness on average (30.3 months) than those who did not report trouble paying bills (8.8 months, p = .02). Respondents reporting at least 1 chronic condition had more time since first homelessness (15.1 years) than those who did not report having a chronic condition (6.27 years, p = .01). Respondents reporting current unhealthy use of substances had shorter average length of most recent episode of homelessness (8.4 months) than those who did not report unhealthy substance use (19.2 months, p = .04), though this result was not significant when examining the length of time since a person was first homeless. Unsurprisingly, respondents reporting fair or poor health appeared to have both longer average lengths of homelessness (19.9 months, p = .02) and longer most recent episodes of homelessness (13.8 years, p = .03) than those reporting better health (8.0 months and 5.9 years, respectively). We determined respondents who did not have insurance coverage when they incurred medical bills reported more years since first homeless (18.8 years) than those who did have medical coverage (7.5 years, p = .047), though this finding was not significant when examining length of current episode of homelessness (Table 5).

Respondent Characteristics in Relation to Length of Homelessness.

Note. T-tests were used to derive p-values for continuous variables; Fisher’s exact tests were used to derive p-values for categorical variable. Survey of (N = 60) individuals living in homeless encampments and shelters in Seattle, Washington, between January 1, 2017, and April 5, 2017 (interviews conducted by the author J.B.). GED = General Educational Development.

Bolded values are significant with a p-value of less than .05.

Even though the following findings were not significant, the effect sizes are interesting and future designs including the sequence of exposure and outcome will improve our understanding. Respondents with student loan debt reported shorter current episodes of homelessness (10.8 months) than those who did not have student loan debt (20.5 months, p = .09). Similarly, those with credit card debt reported shorter current episodes of homelessness (14.2 months) than those who did not report having credit card debt (19.2 months, p = 0.53), and those with payday loan debt reported both shorter current episodes of homelessness (11.2 months) and a lower number of years spent homeless overall (11.4 years) than those who did not report having any payday loan debt (18.5 months of current episode of homelessness, p = .2; 12.4 years of overall homelessness, p = .9).

In our regression model, we predicted length of homeless with a simple binary yes/no variable, “trouble paying medical bills” for themselves or family members in the last year, controlling for demographic factors and health status. Our model predicted slightly less than 25 months of additional homelessness for those who reported having trouble paying medical bills. This association was significant at p ≤ .001, even after controlling for race, education, age, gender, and health status (Table 6).

Predictor of Length of Homelessness in Regression Analysis.

Note. Survey of (N = 55) individuals living in homeless encampments and shelters in Seattle, Washington, between January 1, 2017, and April 5, 2017 (interviews conducted by the author J.B.). Interpretation: the coefficient reflects the effect size and its direction. After controlling for the other demographic factors in the model, people who had trouble paying medical bills experienced significantly more months of homelessness (24.86 months). p < .001. The adjusted R2 can be interpreted to indicate our model explains a meaningful amount of variation, about 19% of the outcome. GED = General Educational Development.

p < .001.

Discussion

Our analysis contributes to the small body of evidence on the relationship between debt, especially medical debt, and homelessness, while considering health status and health coverage as important confounders. Our findings show a significant association between the length of a person’s current episode of homelessness and trouble paying medical bills. While other forms of debt also were associated with length of homelessness, trouble paying medical bills was an independent factor, even after controlling for health status and demographic variables. Previous research8,19-21,32 has associated housing instability and medical debt, but our findings clarify medical debt is independently associated with elongating the time between losing a home and once again becoming stably housed.

We were surprised at how even small amounts of debt were associated with longer duration of homelessness. Our study sample reported relatively small amounts of debt (<300 dollars) were associated with current homelessness, consistent with a 2014 finding that foreclosure was associated with even small amounts of medical debt. 23 A 2016 study of medical debt in collections found more than half were for less than $600. 10 A 2004 study also found relatively small amounts of debt (<500 dollars) led to housing problems, and that health insurance was not protective. 5

We also found insurance was not protective—more than half of respondents with medical debt reported having insurance at the time they incurred the most medical debt. Despite full implementation of the ACA, several studies in various cities suggest even small amounts of debt seem highly destabilizing, though noting a large degree of regional variation in this finding.3,14,22,25

Herman et al 14 demonstrated medical debt was more important than insurance status in predicting delayed or missed medical care in 2011. A survey conducted by The Access Project found more than 25% of survey participants with medical debt said the “debt resulted in housing problems such as the inability to . . . make mortgage or rent payments, or to secure or maintain a home.” 5 In 2008, Doty et al 1 determined 79 million adults had current medical bills or debt, 21 million of whom reported they were unable to pay for basic necessities due to their medical debt burden.

We found associations between length of homelessness and credit card debt, student loan debt, and payday loan debt with meaningful effect sizes even if not statistically significant. These types of debt may be protective against homelessness, if only in the short term. Those with credit cards may use them to stave off homelessness, if only in the short term by charging goods, saving liquid assets for the rent or mortgage. The presence of student loan debt suggests the debtor has received an education, perhaps enabling positions with higher earning power. Payday loans may be protective, as these short-term, high-interest, and unsecured loans give users access to quick cash, despite saddling users with debt.

Previous studies found medical debt affected all demographic groups, with communities of color affected disproportionately. 22 Our Seattle study found similar results. Although Seattle’s American Indian and Alaskan Native populations comprise 0.6% of the population, and blacks are 7.2%, our study of people living in tent cities and shelters found both races/ethnicities disproportionately represented, making up 7% and 15% of our sample, respectively. Other authors have reported the effect of medical debt on individuals across health status as well,1,5,23 as those with better health had, on average, greater amounts of medical debt than those with poor health. This may occur because those with good health are spending more money on health care, resulting in better health outcomes.

It is difficult to determine at what point a person began having difficulty paying medical bills—before or after the current or first experience of homelessness. Our data suggest if an individual happens to have trouble paying medical bills and is also currently experiencing homelessness, they are likely to be homeless significantly longer—more than 2 years. To better distinguish between the relative contributions of medical debt and health conditions, which are likely entangled (although, in our regression model, debt trumped health status), we recommend a longitudinal study.

Limitations

While we piloted several versions of our questionnaire, our instrument could still be improved. We did not collect information on personal income (we believed the variation was too small to matter), incarceration history (this has been done in a subsequent paper), 33 attitudes toward health care, sexual orientation, and other possible predictors of health or medical care utilization. We would have liked more specific information on payday loan debt and types of other debt frequently mentioned, including child support and back-rent, especially since Bickham and Lim found medical debt was associated with increased payday loan debt in 2015. 34 Our data were self-reported, based on respondent memory. To derive 4 predictor scores, we made decisions about grouping factors that may not be simply additive in their predictive value. A larger data set would have improved the predictive power. We collected data during Seattle’s rainiest winter on record, thus restricting our sample size: respondents may have been reluctant to sit outside their tents to answer questions (visits to encampments landed only 1 or 2 interviews, on average). We did not use personal incentives. The experiences of Seattle’s population, where the visible homeless population is growing rapidly and is driven in part by the very high cost of living, may not be generalizable to populations elsewhere.

Policy Implications

Our study provides insight into the role of even small amounts of medical debt on length of homelessness in a Seattle sample. We found strong relationships between homelessness and type of debt, presence of medical debt, and trouble paying medical bills. The association between length of homelessness and trouble paying medical bills remained true after controlling for health status and demographic variables. Our findings show if someone had trouble paying medical bills, length of homelessness was extended by more than 2 years. The effect of debt on homelessness was particularly strong for people of color. Further research would help us learn more about the causal of role debt—medical debt as well as other student and payday loan debt—in homelessness.

Supplemental Material

INQ_SAGEI_5_3_Infographic_Sep_11_2020 – Supplemental material for Presence of Any Medical Debt Associated With Two Additional Years of Homelessness in a Seattle Sample

Supplemental material, INQ_SAGEI_5_3_Infographic_Sep_11_2020 for Presence of Any Medical Debt Associated With Two Additional Years of Homelessness in a Seattle Sample by Jessica E. Bielenberg, Marvin Futrell, Bert Stover and Amy Hagopian in INQUIRY: The Journal of Health Care Organization, Provision, and Financing

Footnotes

Acknowledgements

The authors appreciate Seattle’s democratically run self-governed encampment organizations, SHARE and Nickelsville, for collaborating on this research. They also appreciate the time each respondent spent to answer our questions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The lead author (J.B.) received a stipend from the Northwest Public Health Training Center to support this research, in her role as a graduate student.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.