Abstract

The Affordable Care Act (ACA) included financial and regulatory incentives and goals for states to bolster their health insurance rate review programs, increase their anticipated loss ratio requirements, expand Medicaid, and establish state-based exchanges. We grouped states by political party control and compared their reactions across these policy goals. To identify changes in states’ rate review programs and anticipated loss ratio requirements in the individual and small group markets since the ACA’s enactment, we conducted legal research and contacted each state’s insurance regulator. We linked rate review program changes to the Centers for Medicare and Medicaid Services’ (CMS) criteria for an effective rate review program. We found, of states that did not meet CMS’s criteria when the ACA was enacted, most made changes to meet those criteria, including Republican-controlled states, which generally oppose the ACA. This finding is likely the result of the relatively low administrative burden associated with reviewing health insurance rates and the fact that doing so prevents federal intervention in rate review. However, Republican-controlled states were less likely than non-Republican-controlled states to increase their anticipated loss ratio requirements to align with the federal retrospective medical loss ratio requirement, expand Medicaid, and establish state-based exchanges, because of their general opposition to the ACA. We conclude that federal incentives for states to strengthen their health insurance rate review programs were more effective than the incentives for states to adopt other insurance-related policy goals of the ACA.

Keywords

Introduction

The Affordable Care Act (ACA) sought to increase access to more affordable health insurance through a number of provisions. It expanded Medicaid eligibility and provided premium tax credits to households with incomes between 100% and 400% of the federal poverty level that purchased insurance within the ACA’s newly established health insurance exchanges (or marketplaces). These provisions increased access to insurance; however, that access is unaffordable to many individuals and small employers because of rising health insurance premiums. 1

To try to reduce the health insurance premium growth, some stakeholders wanted the ACA to give the federal government the authority to reject proposed health insurance rate increases determined to be unreasonable. But in the end, policymakers compromised by including incentives to strengthen states’ health insurance rate review programs and by establishing a federal medical loss ratio requirement. Since the ACA’s enactment, the Centers for Medicare and Medicaid Services (CMS) has made annual and ad hoc evaluations to determine whether each state’s rate review program is effective.2-5 CMS bases its determination on whether the state (1) receives sufficient data and documentation to determine the reasonableness of the proposed rate increase (whereby the rate is the unit price of insurance, and the premium is based on the rate coupled with the benefit design and allowable rating factors, such as age, geography, family composition, and tobacco use); (2) conducts a timely review that considers changes in factors such as medical cost, utilization, benefits, and cost sharing; and (3) bases its determination of the reasonableness of rate increases on a standard that is set forth in state statute or regulation. 6 Beginning September 1, 2011, in the individual and small group markets, non-grandfathered health insurance annualized rate increases of 10% or more must either be reviewed by the state or CMS for reasonableness. States with an effective rate review program conduct the review and make this determination, but CMS plays this role for states with ineffective rate review programs. The ACA allocated $250 million for states to bolster their rate review programs, including helping states to establish effective programs. The grants have been used by 44 states to hire and contract with actuaries, upgrade information systems, and enhance rate transparency.7,8

In addition to incentivizing states to impede unreasonable premium rate increases, the ACA encourages states to play a role in expanding insurance coverage. A number of studies have examined the factors that led states to decide whether to expand Medicaid or establish a state-based exchange.9-13 Politics loomed large in both decisions. Beland, Rocco, and Waddan found that Medicaid expansion and state-based exchange decisions required institutional coordination between the federal and state governments, further complicated by the fact that most states needed both the governor’s and legislature’s approval. 9 Jones and colleagues describe how several Republican-controlled states, which were initially receptive to establishing state-based exchanges, acquiesced in the face of intense political pressure to oppose the ACA in general. 10

However, politics was not the only factor in state decision making. Although Democratically controlled states were more likely to expand Medicaid than Republican-controlled states, economic circumstances, previous Medicaid expansion, and administrative capacity all played a role in states’ decisions to expand Medicaid. 11 Haeder and Weimer discuss the influence of state insurance commissioners and existing administrative capacity within states that established state-based exchanges. 12

To our knowledge, however, no studies have examined which states, by political party control, decided to establish an effective rate review program and create an anticipated loss ratio requirement that is consistent with the federal retrospective medical loss ratio requirement. In the remainder of this article, we first examine CMS’s determinations of the effectiveness of each state’s rate review program over time and highlight the states that took actions to become effective. Second, we report the share of states, by political party control, that made changes to become effective rate review programs, increased their anticipated loss ratio requirement to align with the federal medical loss ratio requirement, expanded Medicaid, and established a state-based exchange. We statistically test whether these 4 decisions differed by state political party control. Our hypothesis is that although Republican-controlled states generally oppose the ACA as a whole and chose to not emulate the federal medical loss ratio, not expand Medicaid, nor establish a state-based exchange, they would nonetheless establish effective rate review programs at a similar rate to non-Republican-controlled states, because reviewing rates has a relatively low administrative burden and doing so would prevent federal review of their carriers’ rates.

Data and Methods

Whereas several studies have documented states’ rate review and anticipated loss ratio laws at a point in time,14-21 we are the first to document changes over time between 2010 and 2013. Our sources included statutes, regulations, and insurance department bulletins. We also examined states’ cycle I and II grant applications “Grants to States for Health Insurance Premium Review” submitted to CMS, states’ medical loss ratio waiver applications submitted to the U.S. Department of Health and Human Services (DHHS), and the studies referenced above. After completing this legal research, we contacted state legislative librarians to review our findings. We then contacted the state agency that regulated health insurance to review our findings and to better understand their rate review programs. We received a full response from 47 state regulators and the District of Columbia, and a partial response from three state regulators, and thus relied on in-state health insurance experts to confirm our findings.

Since the enactment of the ACA, CMS has continually determined the effectiveness of each state’s rate review program (using the criteria discussed in the Introduction), and has published its determinations as of the following dates: July 1, 2011, 2 February 16, 2012, 3 May 3, 2013, 4 and April 16, 2014. 5 We classified each state into one of the following categories:

Always Had Effective Rate Review Program: States that CMS determined to have effective rate review programs for all major types of carriers (ie, for-profit insurers, non-profits, and health maintenance organizations [HMOs]) for each of its reviews, and based on our analysis, had already met CMS’s effectiveness criteria when the ACA was enacted.

Effective Rate Review Program via Changes: States that made changes to rate review statutes or regulations after the ACA was enacted to become effective rate review programs. Many of these states did not receive an “ineffective” determination from CMS, because the change was made prior to CMS’s first determination, effective July 1, 2011. We identified these states by linking their statutory and regulatory rate review changes to CMS’s effectiveness criteria, to determine which states met CMS’s effectiveness criteria as a result of the changes.

Ineffective Rate Review Program: States that had an ineffective rate review program as of April 16, 2014.

Prior to the ACA, many states established an anticipated loss ratio requirement within a law, regulation, or bulletin for the individual and small group markets. 20 The state loss ratios were strictly based on the share of premiums represented by medical claims, 22 whereas the federal medical loss ratio allows for quality improvement adjustments as well as tax, license, and regulatory fee adjustments, reducing the traditionally defined state loss ratio by a few percentage points. Therefore, we assumed that a 75% state loss ratio requirement was equivalent to the 80% federal medical loss ratio requirement. In the individual market, DHHS granted 7 of the 17 states that applied for temporary relief to lower the federal medical loss ratio threshold to between 65% and 75% for 2011 and 2012; however, each of these states had an 80% requirement by 2013. 23 Based on our research, 23 states in the individual market and 13 states in the small group market already had anticipated loss ratio requirements for their major types of carriers when the ACA was enacted; however, only 3 states in the individual market and 5 states in the small group market had a requirement of at least 75%. Hence, we examined whether the remaining states and the District of Columbia established or increased their anticipated loss ratio requirement to be at least 75% by December 31, 2013. Although the ACA did not have an explicit financial incentive for states to establish an anticipated loss ratio that is consistent with the federal medical loss ratio, increasing carriers’ loss ratios was a goal of the ACA. This goal creates an implicit incentive, because a state does not want to determine a rate increase to be reasonable and then systematically have carriers’ medical loss ratios exceed the 80% federal medical loss ratio threshold.

For Medicaid expansion and state-based exchange decisions, we relied on secondary sources. Twenty-seven states and the District of Columbia (or 55%) expanded Medicaid as of August 28, 2014. 24 Eighteen states and the District of Columbia (or 37%) established state-based exchanges as of October 1, 2013, the beginning of the first open enrollment period.25,26 Mississippi and Utah only established their exchanges in the small group market. Furthermore, Nevada, New Mexico, and Oregon have subsequently decided to have a federally supported state-based exchange in which they rely on the federal Web site and information technology; however, we based our analysis on their October 1, 2013, statuses. 27

We classified states’ political party control as of January 31, 2011, as follows: Republican or Democratic if the Republican Party or Democratic Party, respectively, controlled both houses and the governor’s office. 28 Otherwise states were considered divided.

We used a Fisher exact test to test whether the percentage of states that adopted these 4 policy goals differed by political party control. We used this test because the decision was binary and the expected frequency of particular cells was less than 5. 29 We used a McNemar exact test to test whether Republican-controlled states adopted these 4 policies at different rates, because the data were generated from the same sample of states, the decision was binary, and the expected frequency of particular cells was less than 5. This test included only the sub-sample of Republican-controlled states that had not adopted the policies being compared prior to the ACA. Results were considered statistically significant if the P value was less than .05 using a 2-tailed test.

Results

Status of the Effectiveness of States’ Health Insurance Rate Review Programs

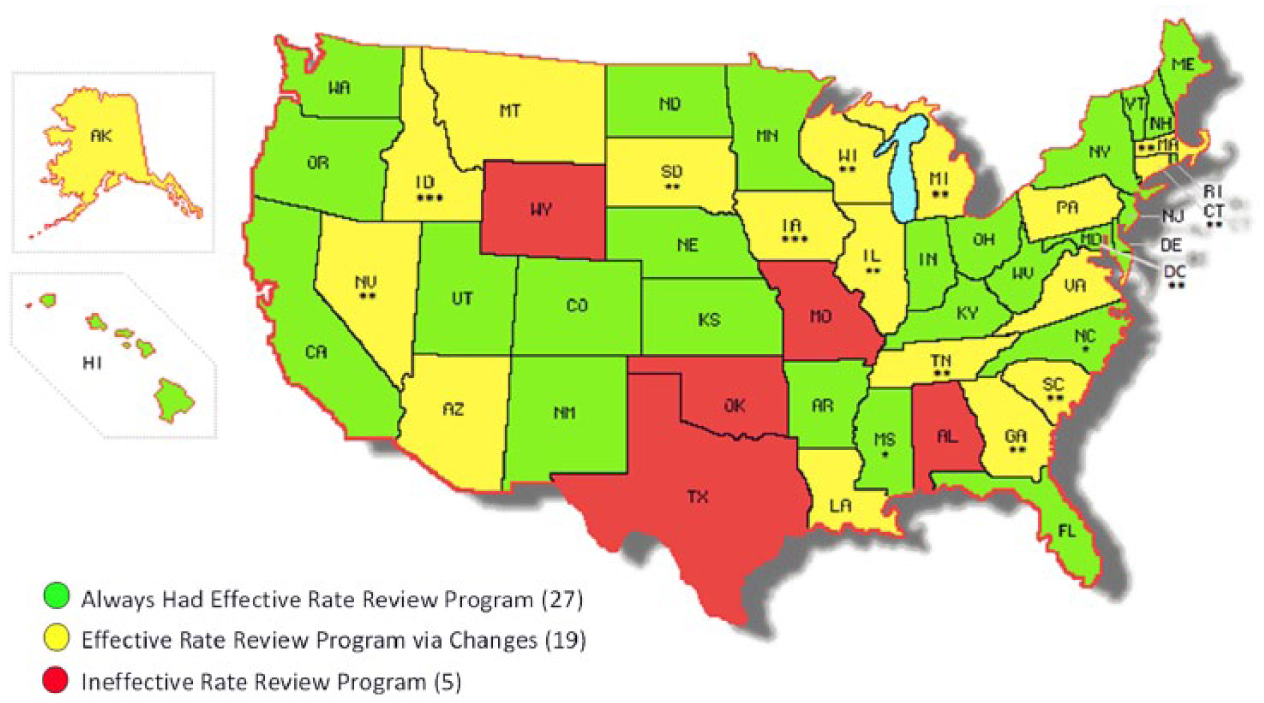

Figures 1 and 2 show the effectiveness status of each state’s rate review program in the individual and small group markets, respectively, from July 1, 2011, to April 16, 2014. These maps show that 37 states in the individual market and 27 states in the small group market that CMS determined to have effective rate review programs for each of its reviews, and based on our analysis, had already met CMS’s effectiveness criteria when the ACA was enacted. However, as we discuss below, altogether, 9 states in the individual market and 19 states in the small group market responded to the CMS incentive and became effective rate review programs.

Effective rate review program status in 2014 and changes in status since the enactment of the Affordable Care Act (ACA) by state in the individual market.

Effective rate review program status in 2014 and changes in status since the enactment of the Affordable Care Act (ACA) by state in the small group market.

Four states in the individual market and 13 states in the small group market took actions after the ACA was enacted that enabled them to have effective rate review programs by September 1, 2011, the date for which CMS or the state would review rate increases of 10% or more (see “Effective Rate Review Program via Changes” states with two or three asterisks in Figures 1 and 2). For example, Georgia had only an “informational only” filing requirement for most rate revisions in the individual and small group markets. In 2011, Georgia amended Rule Chapter 120-2-98 to require indemnity plans, preferred provider organizations, and Blue Cross Blue Shield plans to file rate increases of 10% or more, so that the state could review the reasonableness of those increases.

Meanwhile, 5 states in the individual market and 6 states in the small group market, which CMS initially determined to have ineffective rate review programs, took action after the September 1, 2011, deadline to become effective (see “Effective Rate Review Program via Changes” states with no asterisks in Figures 1 and 2). For example, although Pennsylvania had prior approval authority over all carrier types in the individual market as well as HMOs and non-profit carriers in the small group market, it had no rate filing requirements for for-profit insurers in the small group market, and thus, was considered ineffective. 2 However, in late 2011, Pennsylvania enacted Act 134 to give it prior approval authority over those insurers, enabling it to become an effective rate review program. 3

Finally, 5 states in both the individual and small group markets currently have an ineffective rate review program. This includes both Oklahoma and Texas, which had effective rate review programs in 2011, but decided to not comply with reviewing certain federal rate review requirements.

Comparison of States’ Reactions to the Affordable Care Act’s Health Insurance Policy Goals

Figures 3 and 4 show states’ reactions to the ACA’s health insurance policy goals in the individual and small group markets, respectively. The figures include a set of 4 bars each for Republican-controlled states, politically divided states, and Democratically controlled states. For each set, the first bar shows the percentage of states that did not meet the requirements of an effective rate review program when the ACA was enacted, but became effective since its enactment. The second bar shows the percentage of states that had an anticipated loss ratio requirement below 75% (including those states with no requirement) when the ACA was enacted, but established or increased their loss ratio requirement to this threshold or higher after its enactment. The third and fourth bars show the percentage of states that expanded Medicaid and established a state-based exchange, respectively.

Percentage of states that adopted Affordable Care Act’s health insurance policy goals by states’ political party control, individual market, 2010-2014.

Percentage of states that adopted Affordable Care Act’s health insurance policy goals by states’ political party control, small group market, 2010-2014.

Figure 3 shows states’ reactions to the 4 health insurance policy goals in the individual market. Republican-controlled states were moderately—but not statistically—less likely than non-Republican-controlled states to establish an effective rate review program (50.0% vs 83.3%, P = .301) and establish or increase their anticipated loss ratio requirement to be at least 75% (10.0% vs 25.0%, P = .271). However, Republican-controlled states were statistically less likely than non-Republican-controlled states to expand Medicaid (23.8% vs 76.7%, P < .001) and establish a state-based exchange (4.8% vs 53.3%, P < .001). Within Republican-controlled states, we compared the rate of establishing an effective rate review program with their rates of adopting the other 3 policy areas. (Only the 8 Republican states that did not already have an effective rate review program in place when the ACA was enacted were eligible to be included in these McNemar tests. The test with the anticipated loss ratio requirement to be at least 75% was not applicable, because none of the 8 states established or increased its anticipated loss ratio requirement to be at least 75%. For state-level detail on decisions in these 4 policy areas, see Table A1 in the appendix.) We found that these states were less likely to adopt the other policy areas, but the differences were not statistically different: establishing or increasing their anticipated loss ratio requirement to be at least 75% (50.0% vs 0.0%, P = not applicable), expanding Medicaid (50.0% vs 12.5%, P = .250), or establishing a state-based exchange (50.0% vs 12.5%, P = .250).

Figure 4 shows states’ reactions to the 4 health insurance policy goals in the small group market. Republican-controlled states were moderately—but not statistically—less likely than non-Republican-controlled states to establish an effective rate review program (69.2% vs 90.9%, P = .327). However, Republican-controlled states were statistically less likely than non-Republican-controlled states to establish or increase their anticipated loss ratio requirement to be at least 75% (5.3% vs 33.3%, P = .031), expand Medicaid (23.8% vs 76.7%, P < .001), and establish a state-based exchange (9.5% vs 56.7%, P = .001). Within Republican-controlled states, we compared their rate of establishing an effective rate review program with their rates of adopting the other 3 policy areas (Only the 13 Republican states that did not already have an effective rate review program in place when the ACA was enacted were eligible to be included in these McNemar tests. For the test with the anticipated loss ratio requirement to be at least 75%, only 12 of these states were included because one state already had an anticipated loss ratio requirement of at least 75% when the ACA was enacted. For the Medicaid expansion and state-based exchange tests, all 13 states were included. For state-level detail on decisions in these 4 policy areas, see Table A1 in the appendix.) We found that these states were less likely to adopt the other policy areas and the differences were statistically significant: establishing or increasing their anticipated loss ratio requirement to be at least 75% (66.7% vs 8.3%, P = .016), expanding Medicaid (69.2% vs 23.1%, P = .031), or establishing a state-based exchange (69.2% vs 7.7%, P = .008).

For example, South Carolina, a Republican-controlled state that neither expanded Medicaid nor established a state-based exchange, had prior approval authority over some types of plans in the small group market, but no filing requirement for most insurers, non-profit carriers, and HMOs. On June 29, 2011, it issued Bulletin 2011-03, giving itself prior approval authority over those carriers’ rates, effective September 1, 2011. This change enabled the state to become an effective rate review program. 2

Discussion

The ACA included financial and regulatory incentives and goals for states to bolster their health insurance rate review programs, increase their anticipated loss ratio requirements, expand Medicaid, and establish state-based exchanges. Both Republican-controlled and non-Republican-controlled states established effective rate review programs at a high rate: For Republican-controlled states, the rates were 50% and 69% in the individual and small group markets, respectively, and for non-Republican-controlled states, the rates were 83% and 91% in the individual and small group markets, respectively. However, Republican-controlled states were less likely than non-Republican-controlled states to establish or increase anticipated loss ratio requirement to be at least 75% (only in the small group market), expand Medicaid, and establish a state-based exchange. Particularly in the small group market, Republican-controlled states were more likely to establish an effective rate review program than to establish or increase their anticipated loss ratio requirement to be consistent with the federal retrospective medical loss ratio requirement, expand Medicaid, or establish a state-based exchange.

The ACA’s attempt to strengthen states’ health insurance rate review programs is reminiscent of the ACA’s Medicaid expansion. Under both policies, the federal government set minimum standards and provided financial incentives for states to pursue a federalist policy goal.

There is a notable difference, however. For rate review programs, the ACA created a clear federal role for non-compliant states. Specifically, CMS reviews non-grandfathered carriers’ rate increases of 10% or more in the individual and small group markets in states with ineffective rate review programs. This incentivized states, including Republican-controlled states that generally oppose the ACA, to establish effective rate review programs. For example, in April 2011, Idaho’s Republican governor issued Executive Order No. 2011-03 ordering executive agencies to not implement the ACA; however, in August 2011, the Idaho Department of Insurance received a waiver to begin conducting rate review in compliance with the ACA, in part, “to help preserve state oversight of rates.” 30 In contrast, there was no federal intervention for states that did not expand Medicaid, because the U.S. Supreme Court ruled that hinging all federal Medicaid funding on a state’s decision to expand Medicaid was overly coercive. 31

Although most Republican-controlled states bolstered their rate review programs to become effective, in part, to prevent federal review of their carriers’ rate increases, only 5% of all Republican-controlled states in the individual market and only 10% of all Republican-controlled states in the small group market established state-based exchanges to avoid the federally facilitated exchange. Establishing a state-based exchange, because of its visibility, could be construed as a tacit endorsement of the ACA. In fact, the American Legislative Exchange Council advocated for states to not establish state-based exchanges as a way to oppose the ACA. 32 Furthermore, the administrative burden to establish a state-based exchange is significant. DHHS grants totaled over $4 billion for states to establish state-based exchanges, 16-fold more than the $250 million in grants for states to bolster their rate review programs.7,8,25 This administrative burden has a greater impact on Republican states, which are more likely to have lower capacity state governments. 33

This study has 3 primary limitations. The small sample size of 50 states and the District of Columbia limits our power to detect statistical differences, potentially resulting in not rejecting the null hypothesis when there is a substantive difference. Notwithstanding the small sample size, we were able to detect important statistical differences.

Second, we do not incorporate how states reviewed health insurance rates sold through associations. Prior to the ACA, states often regulated associations’ rates in the large group market, or had less stringent requirements if they regulated them in the individual and small group markets.34,35 However, as of November 1, 2011, associations are subject to rate review regulations under the individual and small group markets. 36 Therefore, a few states with effective rate review programs were considered to be ineffective in reviewing associations’ rates. 4

Third, most states made decisions and changes related to rate review, loss ratios, Medicaid expansion, and state-based exchanges in 2011 and 2012. We classified states’ political party control as of January 31, 2011 to incorporate the November 2010 elections. Only Louisiana and Mississippi changed political party control in 2012, both from divided control to Republican control. In a few states, a policy change occurred in 2010, 2013, or 2014 under a different political party control than 2011; however, these rare events did not affect our main findings.

Conclusion

In principle, federalism combines state policy innovation and administration with federal financing and minimum standards, all of which are present in the ACA.37-39 The ACA sought to increase access to more affordable health insurance. It provided financial and regulatory incentives and goals for states to establish effective health insurance rate review programs, emulate the federal retrospective medical loss ratio requirement, expand Medicaid, and establish health insurance exchanges. Although the federalist goal for states to establish effective rate review programs was largely accomplished, including within Republican-controlled states, these states generally did not emulate the federal retrospective medical loss ratio requirement, expand Medicaid, or establish state-based exchanges, because of their general opposition to the ACA. Our findings suggest that federal incentives for states to strengthen their health insurance rate review programs were more effective than the incentives for states to adopt other insurance-related policy goals of the ACA.

Footnotes

Appendix

Table A1 shows each state’s and the District of Columbia’s status and change in the following 4 policy areas of the Affordable Care Act (ACA): rate review program effectiveness status and change since the enactment of the ACA, anticipated loss ratio requirement status and change since the enactment of the ACA, state-based exchange status, and Medicaid expansion status, all which were used to generate Figures 3 and 4 in the main article. The table is sorted by state political party control.

Acknowledgements

The authors are grateful to the state regulators who provided information on their rate review authority and programs, and the authors thank the following students at the Nicholas C. Petris Center on Health Care Markets and Consumer Welfare at the School of Public Health, University of California, Berkeley, who helped collect the rate review information: Rohini Behl, Shreya Chatterjee, Clare Connors, Camille Enriquez, Ada Gu, Ruslan Gurvitz, Sarah Levi, and Kathleen Sau. The authors thank Maureen Lahiff, PhD, lecturer, Division of Biostatistics, School of Public Health, University of California, Berkeley, for her helpful comments on the statistical methods; Shreya Chatterjee for creating the maps; and Kati Phillips, Program Manager, Nicholas C. Petris Center, for her help administrating this study.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors are thankful for funding provided by Robert Wood Johnson Foundation through its Changes in Health Care Financing and Organization Program (grant 69906). Pinar Karaca-Mandic also acknowledges funding from the National Institute on Aging (grant K01AG036740).