Abstract

The current study examined financial stress, career-related optimism, and psychological distress from the age of 19 (2013; n = 5,787), until the age of 25 (2019; n = 2,933) using the Longitudinal Surveys of Australia Youth (2009 cohort). Longitudinal mediation using latent growth curve modeling observed trajectories of change across young adulthood, whereby financial stress and career-related optimism decreased, while psychological distress increased across time. The inclusion of regression parameters in the analyses indicated that participants with shallower reductions in financial stress reported steeper increases in distress, and this effect was mediated by shifting career-related optimism. With ongoing financial pressures around the world disproportionately impacting young people, our work further illustrates how these stressors can shape the life course via shifts in vocational optimism and subsequent mental health. Moving forward, policies and timely clinical interventions should be implemented to assist young adults in navigating this pivotal developmental period.

Any period of growth and change across the lifespan can instigate functional and psychological challenges. Emerging adulthood (originally defined as 19-to-25-years-of-age) is a critical developmental stage where independence and autonomy grow, with both positive and negative effects on psychological well-being (D. Wood et al., 2018). Arnett (2006) described this developmental stage as characterized by open possibilities for the future and a sense of hope and expectation. However, researchers in high-income countries have found emerging adulthood is a time of uncertainty and instability that can foster increased psychological distress (Kessler et al., 2005; Rohde et al., 2013). Psychological distress, defined as a state of emotional suffering often accompanied by symptoms of depression and anxiety (Belay et al., 2021), can play a pivotal role in shaping one’s life course (Kessler et al., 2005; Ravens-Sieberer et al., 2015). Specific data from Australia reveals poor mental health during emerging adulthood can precipitate unemployment, interpersonal difficulties, substance use and can increase the risk of self-harm and suicide later in life (Lawrence, 2015). Thus, public health policies and timely interventions are crucial during emerging adulthood.

In the current study, we consider the vocational, educational, and structural constraints impeding young people from gaining financial independence to unpack how financial stress can precipitate a decline in mental health functioning. Although psychological distress typically increases in adolescence, wellbeing is then higher during adulthood (Jones & Meredith, 2000; Kessler et al., 2005; Petersen et al., 1991; Pettit et al., 2011; Schulenberg & Zarrett, 2006; Solmi et al., 2022). Indeed, some Australian estimates indicate that 75% of mental health issues will develop before 25-years-of-age (Brennan et al., 2021). Therefore, it is expected, following increases in psychological distress during adolescence, the typical trajectory would see a period of recovery and solidification during emerging adulthood, but this effect will not be universal. The current study will model trajectories of financial stress, career-related optimism, and psychological distress across 6 years to explore who is susceptible to ongoing psychological ill-health across emerging adulthood.

Financial Stress During Emerging Adulthood

Emerging adults face significant difficulties in achieving financial independence (Chesters & Cuervo, 2019), especially in advanced capitalist economies. In these settings, young people are increasingly delaying full time work to continue advanced post-school education—potentially attracting significant levels of debt in the process. Financial difficulties also emerge among emerging adults transitioning into the workforce because employment opportunities have become increasingly casualized, offering reduced security (Campbell & Burgess 2018; De Stefano 2016; A. J. Wood et al., 2019). The soaring cost of living and hypercompetitive housing market further compound the impact of employment instability. While many emerging adults in high income nations remain or become financially dependent upon their families (D. Woodman et al., 2023), others who cannot rely on financial support often experience elevated levels of financial stress.

Emerging adults in Australia face similar difficulties to those in other high-income countries. The casualization of work through the rise of “gig work” (i.e., on demand work) has resulted in approximately half of all young Australians adopting short term transitory employment (Chesters & Cuervo, 2019; Department of the Senate, 2022). At the same time, a ‘housing affordability crisis’ has been a part of Australia’s zeitgeist since the turn of the millennium (Jacobs, 2015). A recent survey found 70% of young Australians reported housing affordability as their top concern (Walsh et al., 2023), with census data indicating 19-to-24-year-olds are disproportionately more likely to be homeless (Australian Bureau of Statistics [ABS], 2021b).

Australian emerging adults are also spending prolonged periods of time in education, with recent estimates indicating 88% of 15- to 24-year-olds are studying (Australian Institute of Health and Welfare, 2021). While the Australian Government provides welfare payments to financially support Australian students, Davidson et al. (2020) found these student support payments to be $168 per week below the poverty line. Other policies designed to support emerging adults in navigating their studies are more effective. The higher education contribution scheme allows students to defer their tuition fees to be later paid back through their tax. This policy reduces financial barriers that impede access to higher education (Aungles et al., 2002) and has features that may reduce Australians’ financial stress relative to people in other systems. As an income-contingent loan tied to inflation, it only becomes repayable once students cross pre-specified income thresholds (Barr et al., 2019). This differs from countries where tuition fees are paid upfront, such as the United States of America, where many emerging adults have large, interest-generating debts (Barr et al., 2019; Zhan, 2022).

Taken together, emerging adults follow diverse pathways toward financial independence. Yet, regardless of the individual educational and vocational decisions made by young people, emerging adulthood is characterized by delaying or being shut out of full-time work and proportionally high income-to-housing costs. This has resulted in a growing number of young adults reporting high financial stress (O’Keeffe et al., 2022; Prime et al., 2020), which we define as difficulty meeting basic financial commitments due to a shortage of money (Australian Government Department of Employment and Workplace Relations, 2022).

Financial stress is a common experience for emerging adults who gain independence (Blinn-Pike et al., 2008; Heckman et al., 2014), particularly if they are studying full time and or moving out of home (Baum & Ma, 2012; Kroll, 2013; Oseguera & Rhee, 2009). Despite this, when entering adulthood from adolescence, the mean level of income tends to increase as people age (Easterlin, 2001) inferring financial stability typically increases (i.e., due to more consistent work hours, cessation of studying obligations, and higher salaries). This suggests that the typical trajectory for financial stress reduces with age across emerging adulthood.

An extensive literature base has highlighted the connection between financial stress and psychological distress (Cheng et al., 2020; DeVaney & Lytton, 1995; Frankham et al., 2020; Netemeyer et al., 2018). Accordingly, we argue that developmentally typical reductions in financial stress should be associated with concurrent decreases in psychological distress. Yet, current worldwide economic conditions and psychological challenges that emerging adults encounter make understanding this relationship more important than ever. It is worthwhile knowing more about what factors might mediate this relationship, and how these factors might co-occur over time. Additionally, most of the current literature focuses on the impacts of growing up in lower socioeconomic households and the negative impacts this can have on mental health outcomes (Frankham et al., 2020; Fryers et al., 2003). Accordingly, there is a lack of research looking at how financial independence, and the financial stress that can coincide with this, impact mental health during emerging adulthood.

The Cognitive Impact of Financial Stress: Altered Future Expectations

Despite the changes in financial stress and psychological distress that can unfold in emerging adulthood, Arnett (2000) suggested this developmental period is met with high levels of optimism. Research by Kerpelman and Mosher (2004) suggests optimism for the future can lead to increased mental wellbeing among rural African American adolescent populations, due to feelings of efficacy and responsibility for one’s decisions and life. This suggests that optimism might act as a protective factor for the mental health of emerging adults in circumstances of increased financial stress. Schwaba et al. (2019) found that optimism typically increases throughout early and middle adulthood in samples of American and Dutch respondents, before plateauing at 55 years of age. In part, these changes emerge from shifts in autonomy during this time that increase confidence in accomplishing desired outcomes (Deci & Ryan, 2000; Kerpelman & Mosher, 2004).

Indeed, financial stress has been found to predict future outlook and goal setting, likely impacting career-related optimism. Career-related optimism has been defined as the belief in a favorable outcome and a focus on the positive aspects of future career growth (Rottinghaus et al., 2005). Morton (2017) found when finances are tight, individuals prioritized short-term goals to meet current needs, but when finances were adequate, long-term goals were prioritized. Eshelman and Rottinghaus (2015) supported this, finding that American midwestern high school students from low socioeconomic backgrounds had lower occupational aspirations. Correspondingly, researchers found that undergraduate students facing financial hardship perceive they have fewer occupational choices and accept poorer fitting jobs and lower salaries (Allan et al., 2019; Hausdorf, 2007). This demonstrates how financial stress can influence career-related optimism and highlights the critical nature of emerging adulthood for future outcomes.

Emerging adults increasingly think about themselves as future workers, shifting their focus toward vocational aspirations and goals that form their self-identity (Erikson, 1968; Gottfredson, 1981; Super, 1980). These educational and vocational aspirations continue increasing in the years immediately following high school (Mau & Bikos, 2000). Indeed, this period of development is where aspirations begin to be formed based on interests, abilities, perceived prestige, and level of difficulty for career paths (Creed et al., 2007; Gottfredson, 1981). It is likely that financial stability plays a role in the appraisal of these factors, and it seems plausible that these future career prospects could influence one’s psychological wellbeing (Sinclair et al., 2010).

The Current Study: Predicting Change in Psychological Distress

Throughout the period of emerging adulthood, financial stress, career-related optimism, and psychological distress outcomes are known to change. Whether these changes co-occur, however, remains an open question. Thus, the goal of the current project is to investigate the dynamic interrelationships among these outcomes during a pivotal developmental period. Using latent growth curve mediation, the proposed research will explore patterns of change in financial stress, career-related optimism, and psychological distress in a nationally representative sample of emerging Australian adults (aged 19–25). Therefore, this study will use responses from participants over a 6-year period to conduct latent growth curves, establishing the starting point (the “intercept”) and rate of change over time (the “slope”) for each key variable before explicating their interdependencies over time.

This research contributes to our understanding of social and developmental psychology and could play a role in identifying time points for interventions in a clinical setting. Indeed, mental health disturbances during emerging adulthood are likely an ongoing issue worldwide. Normative developmental variations in wellbeing are compounded by changing social expectations around housing and employment, which are set in high-income international policy contexts with “unfriendly” welfare regimes toward younger people (Arundel & Lennartz, 2017; Bricocoli & Sabatinelli, 2016; Wilkinson & Ortega-Alcazar, 2017). Therefore, understanding the processes that interconnect developmental changes in financial stress, career-related optimism, and psychological distress in emerging adults may prove beneficial not only for clinical intervention but also for public policy. Relating to the forementioned literature, this paper will test the following hypotheses:

Method

Openness and Transparency

This study used data from the Longitudinal Surveys of Australian Youth (LSAY), which is publicly available. Interested readers may find information about data access, guidelines, and measures at https://www.lsay.edu.au/data/lsay-quickstats. Supplementary materials, including analytical code, were made available on the Open Science Framework (OSF). The analyses were not pre-registered; however, the method and hypotheses underwent peer-review by a Masters theses panel, with the original research proposal viewable on OSF. A broader range of career-related optimism items were originally included in the proposal, however 2 items were removed after conducting a confirmatory factor analysis. These results and our decision-making processes are outlined in the supplementary materials (https://osf.io/bh7n2/?view_only=da327e491303466fad906513a769c9d0).

Sample and Study Design

The sample consisted of the 2009 cohort from the Longitudinal Surveys of Australian Youth (LSAY). In total, 11 waves of data collection occurred for this cohort, over a 10-year period (from 2009 until 2019). In wave one (2009), a nationally representative sample of 15-year-old students were selected to participate in the study (n = 14,251). The sample were derived from 353 secondary schools across all states and territories in Australia, stratified to represent students across Australia. The sampling used state and territory, school sector and geographical location as the main strata. Additionally, gender composition and community socioeconomic status were also considered during stratified sampling. Oversampling was conducted for smaller jurisdictions and for Aboriginal and Torres Strait Islander students to ensure that reliable results can be produced by state and indigenous status (see Rothman & Herbert, 2009 for a full outline of the LSAY sample design). The initial project had ethical approval from a human research ethics committee, with ongoing review by the Australian Institute of Family Studies Human Research Ethics Committee.

Annual surveys were completed from 2009 until 2019 via telephone interviews or online (commencing in 2012). Participants could miss up to one survey wave and remain in the study. The surveys took approximately 20 minutes to complete. Depending on which wave was being collected, different domains of questioning were used to ensure the study captured the transitory period from secondary school into early adulthood. For the current study, relevant questions were taken to analyze the changes in financial stress, career-related optimism, and psychological distress for young Australians.

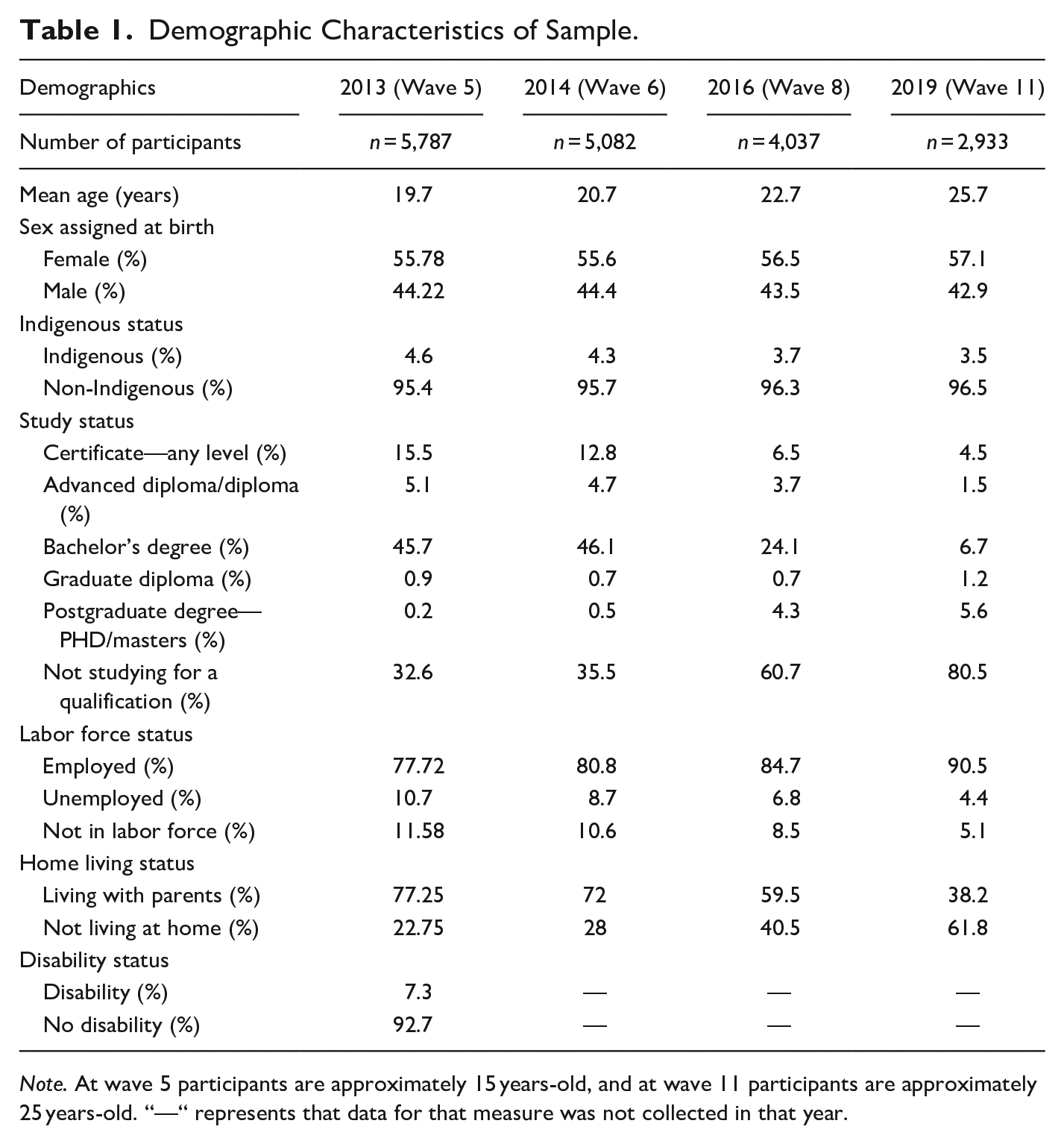

The data analyzed for this study will come from waves 5 (n = 5,787), 6 (n = 5,082), 8 (n = 4,037), and 11 (n = 2,933). These waves were selected as they capture both the measures and developmental stage of interest. Demographic information collected included sex assignment, indigenous status, study status, current qualification level, labor force status, disability status, and living at home status. Demographic statistics for the data waves used in the current study can be viewed in Table 1.

Demographic Characteristics of Sample.

Note. At wave 5 participants are approximately 15 years-old, and at wave 11 participants are approximately 25 years-old. “—“ represents that data for that measure was not collected in that year.

Measures

Financial Stress

Participants were provided with a list of 10 scenarios that may occur due to a shortage of money and were asked to indicate whether any had happened to them in the previous year. Example scenarios included skipping meals, borrowing money, and not having funds to cover bills (e.g., “have you over the past year because of a shortage of money went without meals?”). Responses were provided on a binary scale (0 = No, 1 = Yes). Items were summed to create a total financial stress scale, with higher scores indicating greater financial stress. Similar measures have been used in other research on young adults (O’Donnell et al., 2023) and is regarded as a useful and age-appropriate indicator of financial outcomes among young adults (De New et al., 2020). The financial stress data was collected from wave 5 until wave 11 for the 2009 LSAY cohort; the period of interest for this study were waves 5, 6, 8, and 11.

Psychological Distress

Participants’ mental health was assessed using the self-reported Kessler Psychological Distress Scale (K-6, Kessler et al., 2010). Validated within both clinical and general populations, the K-6 is a non-diagnostic indicator of general distress that maps onto experiences of depression and anxiety using 6 items (1 = none of the time to 5 = all of the time). Similar to previous research (Easton et al., 2017), the K-6 was found to be internally consistent across time in the current sample. Specifically, participants were asked if they felt the following indicators of distress during the previous month; (1) Nervous, (2) Hopeless, (3) Restless or fidgety, (4) That everything was an effort, (5) So sad that nothing would cheer you up, and (6) Worthless. The items were aggregated, with higher scores indicating greater psychological distress. The K-6 data was collected in waves 6, 8, and 11.

Career Related Optimism

Career-related optimism was measured by three self-report questions that related career optimism. These included, “thinking about my career inspires me,” “I get excited when I think about my career,” and “I am eager to pursue my career dreams.” These questions were measured on a scale of 0 to 10 (where 0 = strongly disagree and 10 = strongly agree) whereby higher scores indicated more career-related optimism. The 3-item measure was internally consistent across time and were averaged. The career-related optimism data was collected in waves 5, 8, and 11 for the 2009 LSAY cohort. An outline of the items in each measure can be viewed on the OSF.

Covariates

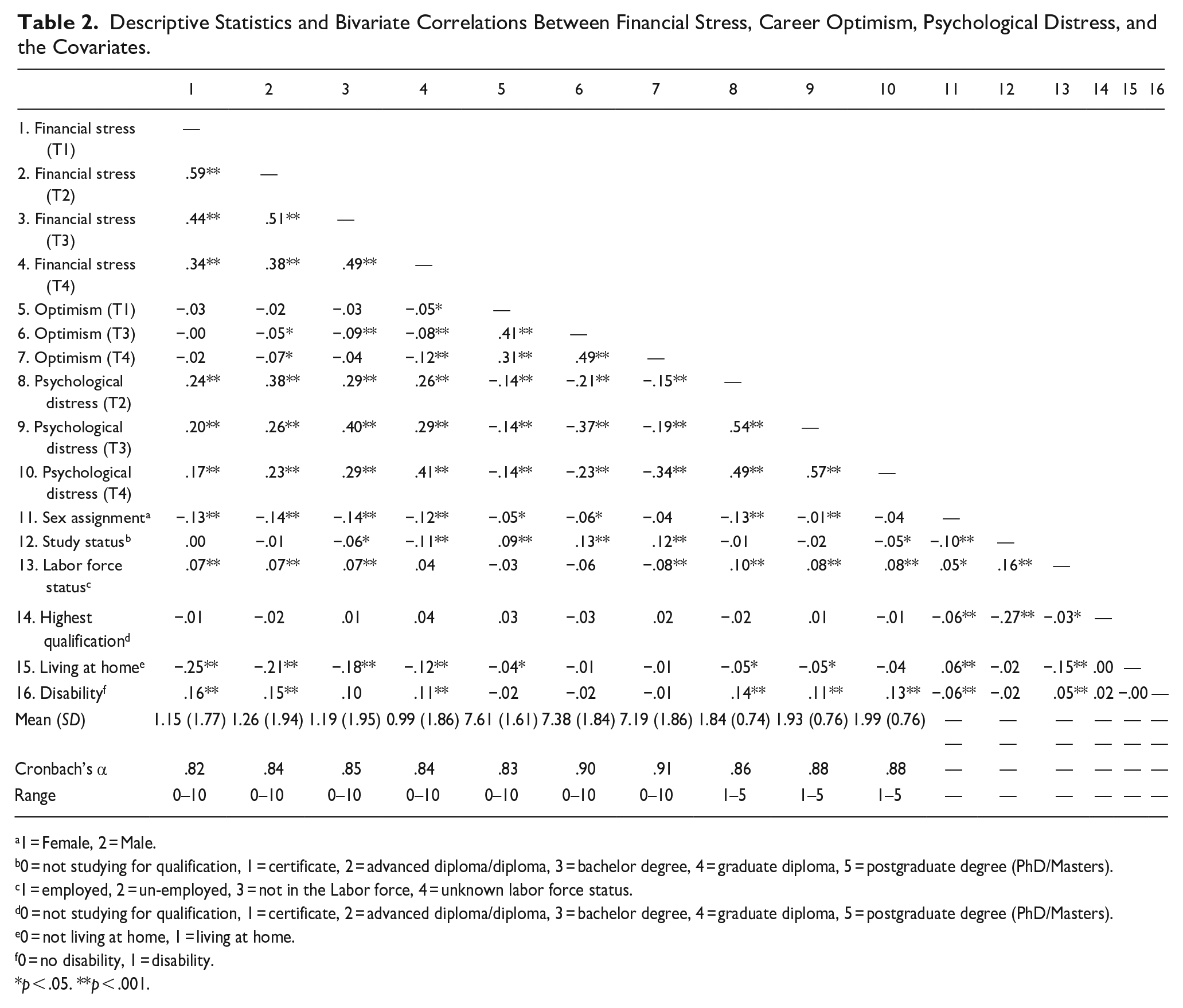

Several demographic and psychosocial factors were controlled for in the current study, to account on their potential influence on life outcomes during emerging adulthood. This included sex assigned at birth, disability status, indigenous status, labor force status, study status, and living at home status. The descriptive statistics for each factor and evidence of internal consistency across measures are in Table 2.

Descriptive Statistics and Bivariate Correlations Between Financial Stress, Career Optimism, Psychological Distress, and the Covariates.

1 = Female, 2 = Male.

0 = not studying for qualification, 1 = certificate, 2 = advanced diploma/diploma, 3 = bachelor degree, 4 = graduate diploma, 5 = postgraduate degree (PhD/Masters).

1 = employed, 2 = un-employed, 3 = not in the Labor force, 4 = unknown labor force status.

0 = not studying for qualification, 1 = certificate, 2 = advanced diploma/diploma, 3 = bachelor degree, 4 = graduate diploma, 5 = postgraduate degree (PhD/Masters).

0 = not living at home, 1 = living at home.

0 = no disability, 1 = disability.

p < .05. **p < .001.

Analytic Strategy

Analyses were conducted using R (Version 4.0.5; R Core Team, 2021). First, bivariate correlations and descriptive statistics were reviewed. Second, a series of unconditional latent growth curve (LGC) models were conducted using a structural equational modeling framework. These initial unconditional models were conducted separately for financial stress, career-related optimism, and psychological distress. Each observed indicator across time were initially used to create an “intercept” latent variable, with factor loadings constrained to be 1. This intercept variable represented average scores across time, without allowing for increases or decreases. Thus, this unconditional means model assumes no change in the construct of interest across time. Next, a latent “slope” was added to the model to represent linear change in each construct of interest. Factor loadings were constrained to be proportional to the intervals between measurement periods. Model comparisons were conducted to determine the overall presence and shape of change over time (testing hypothesis 1).

Following this, the best fitting unconditional models were entered concurrently into a predictive model. Directional hypotheses were explored by regressing the intercept and slope of financial stress (predictor) onto the intercept and slope of career-related optimism (mediator), and finally onto psychological distress (outcome). LGC modeling is an established method of testing longitudinal mediation effects (Preacher et al., 2008) based upon a priori conceptualization of variable ordering (Cheong et al., 2003). Bi-directional effects and alternative processes were also accounted for, by regressing each slope onto all intercept factors (i.e., does initial levels of one variable predict subsequent changes in another). The indirect effects were estimated (the a*b pathway) and evaluated using 5,000 bias corrected bootstrapped confidence intervals (hypothesis 2).

At time 1 for this study (2013), there were 5,787 participants who completed the study. This represented 40.6% of the original sample. Subsequent waves retained approximately 90% of participants from the previous wave. A missing data analysis indicated that missing responses were not completely at random, Little’s MCAR test, χ2 (259) = 556.03, p < .001 (Little, 1988). Subsequent correlations using an aggregated number of missing datapoints indicated that females (r = 0.08, p < .001) and students (r = −0.21, p < .001) were significantly less likely to attrite out of the study. Accordingly, full information maximum likelihood (FIML) was used to account for missing data. FIML relies on the assumption that the probability of missing data is dependent on other observable variables, therefore all observed variables are used to estimate the coefficients (Enders & Bandalos, 2001). Scholars have argued FIML is less biased than other approaches (e.g., multiple imputation) when data is not missing completely at random (Enders & Bandalos, 2001).

Results

Descriptive Statistics and Bivariate Correlations thesis

Bivariate correlations (Table 2) revealed that psychological distress was significantly correlated with both career-related optimism and financial stress across all time points. However, the relationship between financial stress and career-related optimism was weak and mostly not significant across time. Moreover, sex assignment and living at home status was found to be significantly negatively correlated with financial stress across all timepoints. Correspondingly, disability status was found to be significantly positively correlated with financial stress across the first two timepoints and study status was significantly negatively correlated with financial stress across the final two timepoints. Additionally, labor force status was found to be significantly positively correlated with financial stress (across the first three time points), and for psychological distress (across all time points).

Unconditional Latent Growth Curve Models

Compared to the general means model of financial stress, the inclusion of a linear slope significantly improved the model fit Δ χ2 (3) = 148.42, p < .001. When observing the LGC, participants at T1 had few financial stressors on average (intercept = 1.18, p < .001; on of a 10-point scale), and then typically decreased slightly across time as evidenced by the negative slope (slope = −0.028, p = .001). This suggests financial stress, on average, is relatively low for emerging adults in Australia around the age of 19, and as they age to 25 years-old, financial stress typically decreases.

Similar to our unconditional model on financial stress, there was evidence for linear change in career-related optimism Δ χ2 (3) = 172.78, p < .001. Participants scores started off reasonably high (7.596, p < .001; out of a 10-point scale), but then decreased across time (−0.068, p < .001). This suggests that although participants are optimistic during the start of early adulthood, there are minor reductions across adulthood on average.

Compared to the general means model for psychological distress, the inclusion of a linear slope significantly improved the model fit Δ χ2 (3) = 78.558, p < .001. Although experiences of distress started off relatively low (1.869, p < .001; out of a 5-point scale), they typically increased across emerging adulthood (0.026, p < .001).

Parallel Latent Growth Curve

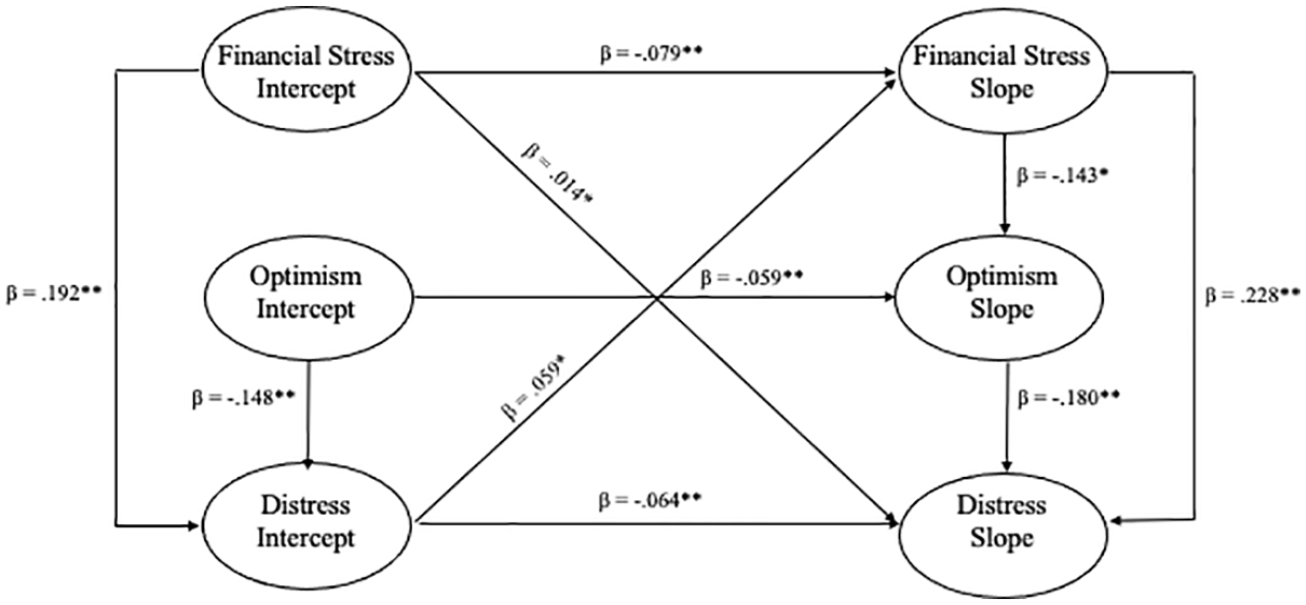

Evidence for a Cross-Sectional (Intercepts) Mediation Effect

Subsequently, a parallel growth curve analysis was conducted in line with the analytical strategy, χ2 (52) = 416.34, p < .001; RMSEA = 0.06; SRMR = 0.03; CFI = 0.94. The intercept of financial stress was found to be significantly and positively associated with the intercept of psychological distress (β = .192, p < .001). Although higher intercepts of career-related optimism, was found to be significantly associated with lower intercepts of psychological distress (β = −.148, p < .001), the financial stress intercept was not significantly associated with starting levels of career-related optimism (β = −.033, p = .332). Hence, the cross-sectional mediation model (intercepts only) was not statistically significant (β = .005, CI 95% [−0.015, 0.039], p > .05).

Evidence for a Longitudinal (Slopes) Mediation Effect

The intercept of each construct was found to negatively predict the slopes for the same construct, suggesting that participants higher in financial stress (β = −.079, p < .001), career-related optimism (β = −.059, p < .001), and psychological distress (β = −.064, p < .001), were more likely to report slight deductions in each construct across time (likely due to a ceiling effect). When exploring bi-directional associations, participants with higher financial stress at the start of the study reported steeper increases in psychological distress (β = .014, p < .05) and higher intercepts of psychological distress predicted the increasing financial stress across emerging adulthood (β = .059, p < .05). No other significant bi-directional associations were found.

There was evidence of a significant longitudinal mediation effect in the model. Specifically, it was found that increasing levels of financial stress was found to be associated with increasing levels of psychological distress (β = .228, p < .001). Increasing levels of career-related optimism also predicted decreasing psychological distress (β = −.180, p < .001) over time. With experiences of financial stress, future-oriented optimism, and psychological distress all decreasing on average across the sample, the association between the slopes indicates that greater psychological recovery is possible when financial stressors are lessened, and participants can maintain higher levels of optimism across emerging adulthood. Finally, increasing levels of financial stress was associated with decreasing levels of career-related optimism (β = −.143, p < .05) over time. Accordingly, participants with steeper reductions in financial stress exhibited more shallow reductions in their career-related optimism. Consistent with these direct effects, a significant indirect effect was observed, β = .026, CI 95% [.006, .127], p < .05. Accordingly, individuals with decreasing levels of financial stress are less likely to report negative trajectories of career-related optimism, and therefore have corresponding decreases in psychological distress across emerging adulthood. See Figure 1 for the longitudinal mediation results. All possible indirect effects were calculated and uploaded in the supplementary materials on the OSF.

Parallel latent growth curve mediation pathway model.

Discussion

Emerging adulthood is a developmental period known to introduce challenges that shape life outcomes. This study tracked the developmental trajectories of salient factors in this life stage to examine potential co-occurring relationships among them. Namely, financial stress, future-orientated cognitions, and psychological distress were measured from the ages of 19 to 25. The results indicate that, for emerging adults in Australia, career-related optimism and financial stress decreased from 2013 to 2019, while psychological distress increased. Furthermore, the study aimed to determine if career-related mediated the relationship between financial stress and psychological distress over time. As our longitudinal modeling demonstrates, changes in career-related optimism explain the association between the trajectories of financial stress and psychological distress across emerging adulthood. The discussion of the results below broadens our understanding of how to enhance positive outcomes for emerging adults.

Developmental Changes in Financial Stress, Career Optimism, and Psychological Distress

Consistent with our hypothesis, financial stress decreased over time. As emerging adults age, they typically settle into more stable work hours, receiving salary increases, and greater financial literacy during this life stage (De New et al., 2020; Easterlin, 2001). Our descriptive statistics show that approximately two-thirds of our nationally representative Australian sample were studying at the onset of the study, but less than 20% were still engaged in their studies by the age of 25. Concurrent increases in employment were also observed. These trends across emerging adulthood are widely observed around the industrialized world and characterize this developmental period (D. Wood et al., 2018). However, it’s worth noting that the welfare support provided to students by the Australian Government (albeit limited), combined with the income-contingent and interest-free student loans, ensures that our sample’s experiences might not generalize to other nations with more generous or restrictive social welfare and education regimes.

In contrast, the decreasing levels of career-related optimism and increasing experiences of psychological distress were inconsistent with our expectations. Previous research on optimism, broadly defined, indicated that shifts in autonomy during adulthood instigates subsequent increases in optimism (Deci & Ryan, 2000; Kerpelman & Mosher, 2004; Schwaba et al., 2019). Accordingly, career-related optimism may have a different trajectory to optimism for the future. Individualistic norms in Australia motivate emerging adults to forge their own career paths amid shifting market demands. These shifts may impact young peoples’ ability to predict future job opportunities and can result in emerging adults needing to adjust to careers that may differ from their initial expectations (Csikszentmihalyi & Schneider, 2000; Mortimer & Larson, 2002). In line with this, research has suggested that career aspiration and expectations can become more reality-based after adolescence (Gottfredson, 1981). The rise of insecure gig-work among Australian emerging adults may further expedite this process of realignment. With approximately half of Australian emerging adults engaged in precarious work, participants may struggle to be inspired by the employment landscape before them (Cuervo & Chesters, 2019).

This sample of Australian emerging adults also exhibited an increasing trajectory for psychological distress across 5 years. These results are inconsistent with findings by Pettit et al., (2011) and Schulenberg and Zarrett (2006) who both suggested, as one transitions from adolescence into adulthood, mental wellbeing typically increases. These results may indicate that the current lifestyles and demands placed on emerging adults might differ from those of the past. The transition from adulthood is now taking longer than previous generations, with increasingly diverse pathways available (Arnett, 2014; Buchmann, 1989; Côté, 2000; M. J. Shanahan, 2000). Consequentially, emerging adults may now be faced with novel challenges for their psychological wellbeing. Moving forward, it is imperative that we gain a deeper understanding of how to best support emerging adults in modern times.

Career-Optimism Mediates the Relationship Between Financial Stress and Psychological Distress Longitudinally

Empirical literature consistently demonstrates that financial circumstances impact mental health (Conger et al., 2010; Jorgensen et al., 2010; Norvilitis et al., 2003). In this study, increasing financial stress was associated with increasing levels of psychological distress both cross-sectionally and over time. While this relationship is well established, we found evidence of a significant longitudinal mediation in support of our second hypothesis. From 19 to 25-years-of-age, decreasing financial stress predicted divergent trajectories in career-related optimism, which in turn predicted rates of change in psychological distress. Theoretically, financial stress is argued to limit one’s ability to access education, move out of the family home, and take risks in the workforce (Anlezark & Lim 2011; Furstenberg, 2008), all of which could contribute to a steady decline in career-related optimism across emerging adulthood. In turn, decreasing career-related optimism was associated with increasing psychological distress. These findings suggest reductions in optimism relating to one’s career can increase feelings such as hopelessness, worthlessness, and nervousness. Reduced confidence in one’s ability to accomplish desired life goals (Kerpelman & Mosher, 2004) can result in reduced self-efficacy that impacts mental health (Connolly, 1989). Our work emphasizes the important role financial stability plays during emerging adulthood as a formative period that can set the stage for future success (Ammerman & Stueve, 2019).

Although we observed a significant indirect effect when exploring trajectories of change, a significant mediation was not found among the intercepts. Financial stress was still significantly correlated with psychological distress, suggesting young people who report additional financial stressors also report greater depressive symptomology. However, financial stress was not significantly correlated with career-related optimism, even at the level of bivariate correlations. The insights provided by longitudinal latent growth curve modeling are clearly useful here, to capture the interplay of time and development (Jose, 2016; Selig & Preacher, 2009). Indeed, we only observed changes in both optimism and psychological distress when financial stress changes. As these factors are known to change across emerging adulthood development, our methodology allowed us to observe a pattern of results consistent with the lived experiences of emerging adults who exhibit developmental shifts among a backdrop of challenges in our contemporary society.

Implications

Overall, these findings suggest financial wellbeing is important for mental health. Emerging adults’ access to services could be crucial to reduce the cascade of difficulties faced by this age group. On a clinical level, understanding the co-development of financial strain and distress provides opportunities for targeted intervention. Findings from the data suggest optimism may be an important avenue for therapeutic intervention. A meta-analysis by Malouff and Schutte (2017) found that optimism can be increased through a range of clinical interventions; some of these consisted of “the best possible self-exercise,” self-compassion training, cognitive behavioral therapy, and mindfulness. Specifically, the “best possible self-exercise” was found to be the most effective for university aged students. This research may also assist in reducing stigma around the issues faced by emerging adults, by building a developmental understanding of the difficulties faced by young people and how this influences their future outcomes.

While clinicians can provide interventions to promote psychological wellbeing, the government also plays a critical role in mitigating the financial concerns of emerging adults in Australia. We observed that psychological distress was a precursor to subsequent changes in financial stress (as evidenced by the intercept of psychological distress predicting the slope of financial stress). Financial independence for young people lays the foundation for a healthier and happier generation of new adults. Accordingly, it is important to both provide financial support for emerging adults through targeted policy interventions (e.g., study support payments etc; Daniels, 2017), and look after their health and welfare in a world that increasingly presents challenges for mental health. Investments during this developmental period are known to have lasting influences throughout the lifespan (Guan et al., 2022). Despite this, emerging adults are often overlooked in public policies compared to other age groups who are more readily provided with financial support (including in the Australian context, Baxter & Carroll, 2022). Based upon our findings, it is possible that financial support for emerging adults will likely have positive outcomes during this transition. Potential long-term consequences of providing support could include lower economic tolls and stress on the health care system, increased work productivity and a greater quality of life for Australians (Chen et al., 2006; Knapp & Wong, 2020).

Methodological Strengths and Limitations

The longitudinal design of the current study is a substantial strength. By tracking change over time, we have identified valuable insights for policymakers in Australia and other Western democracies. Additionally, the large and diverse sample of Australian residents used in this study ensured the results are representative of young Australians, and generalizable. However, our findings cannot be extrapolated to all contexts. For instance, the presence of welfare services for young people in Australia, such as youth allowance and job seeker, may influence the degree of financial stress experienced by this group among students and home leavers who are most at risk. Future research should explore the role of welfare systems in how financial stressors may shape career-related optimism and psychological distress.

A second limitation relates to the measured time-period; this study captured time points across 6 years. Yet, financial stress can impact people’s day to day lives, creating stress and uncertainty when completing daily tasks (Sturgeon et al., 2014). Due to this, the measurements taken over 6 years in the current study are not sensitive to the lived experiences associated with financial distress. Future research may benefit from doing shorter term studies with more time points and increased sensitivity.

Moreover, Arnett et al. (2014) has contested that in high-income countries, the developmental period of emerging adulthood can last until 29 years of age. Although incomes are likely to continue rising, parenthood, mortgages, and marriages become more common and may introduce new financial stressors and potentially reshape career-related goals. Therefore, future studies could explore the trajectories of financial stress, career optimism and mental health across the entire age range of emerging adulthood to capture the impact of these developmental milestones.

Finally, although this research captures a key developmental period, it’s important to consider whether these general patterns of change withstand the socioeconomic upheaval following COVID-19. Since the conclusion of data collection, there has been a notable rise in the cost of living and more widespread financial instability (ABS, 2021a; Borland & Charlton, 2020). Periods of economic uncertainty and recessions throughout history disproportionately effect young people (Bell & Blanchflower, 2011; Schoon & Mortimer, 2017). A new question has emerged, regarding whether the long-term impact of COVID-19 may alter the strength or significance of the relationships found in this study. Indeed, COVID-19 altered career-related optimism (Chang & Saw, 2021), while experiences of distress seemingly spiked in society (M. J. Shanahan et al., 2022). Emerging data is demonstrating psychological distress is returning to baseline levels (Rifai et al., 2023), but new data is needed to understand how career-related optimism may have shifted in the years following social upheaval and economic recession.

Conclusion

It is understood that financial stress, career-related optimism, and psychological distress change across time. This study highlights how these constructs change concurrently during emerging adulthood. By recognizing the co-occurring changes in financial stress, career-related optimism and psychological distress, interventions and support services can be developed to holistically address the shifting needs and constraints experienced during emerging adulthood. This highlights the need for policymakers and mental health professionals to prioritize the needs of this group, and develop policies, interventions and services that address the specific challenges they are facing. Ultimately, efforts to improve the lives of emerging adults will foster a safer and more prosperous society.

Footnotes

Acknowledgements

The data utilized in the current paper came from the Longitudinal Surveys of Australian Youth (LSAY) conducted by the Department of Education. The findings and views reported in this paper, however, are those of the authors and should not be attributed to the Australian Government or any of the partners. We extend our thanks to everyone involved in developing this study, and to those who participated.

Data Availability Statement

The data supporting the findings of this study are sourced from the Longitudinal Surveys of Australian Youth (LSAY), which is publicly available. The data files are archived with the Australian Data Archive (ADA) at the Australian National University. Access to the data is free but requires a formal request and registration process. Interested readers may access information about data access, guidelines, and measures at ![]() .

.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.