Abstract

This article examines the evolving dynamics of state entrepreneurialism amid the ongoing restructuring of urban governance in China, focusing on the Shenzhen Qianhai Pilot Zone—a flagship area exemplifying China’s latest advances in financial innovation and territorial development. Drawing on on-site observations and interviews with 13 senior officials from the local authority and key enterprises involved in the zone’s development, this study reveals how the local state strategically initiates innovation in land development. Specifically, it has pioneered a unique “build-operate-transfer”-based land lease model, subsequently transforming it into a real estate investment trust (REIT) product. By bypassing traditional land-use-right transfer and introducing a flexible lease, the authority enables private developers to construct, operate, and profit from lease income during the initial development phase. The innovative practices point to the emergence of new state capacities to formulate development trajectories. However, the use of regulation flexibility and a pragmatic approach in policymaking does not signal the dominance of a hands-off development mode; rather, it reflects a strong commitment to realizing the central government’s political objectives. The state can foster entrepreneurial growth while maintaining decisive control over critical factors, balancing policy experimentation with oversight to ensure that innovations align with higher-level political directives and remain fully manageable.

Introduction

The change of urban governance toward entrepreneurialism has transformed how the state mobilizes capital, manages assets, and drives development in cities. In China, this process has been characterized as state entrepreneurialism (SE)—a governance mode by which the state not only facilitates market activities but also actively participates in rule setting in financial operations and growth (Li et al., 2025; Wu et al., 2022). The state could not only act through the market to achieve a number of regulatory tasks (i.e. leveraging market and societal forces); it could also act as a market participant that becomes a part of other stakeholders to establish frameworks and uphold market functionality, achieving goals beyond pure economic interests.

The role of SE in the urban governance of Chinese cities is apparent. The recent trend in land financialization reveals a more advanced role of the state, which uses financial instruments or engages in financial operations to promote more aggressive modes of development. Land-based finance was the earliest form of financialization, where local governments sell land-use rights to individuals and corporations for a fixed tenure (Wu et al., 2025). As urbanization continues, with more development projects demanding greater financing, generating revenue through increased market liquidity has become the main motivation for the state’s active shift into a financial operator (Aalbers, 2016; Birch and Ward, 2024). Consequently, securitization has become an instrumental means of SE. Real estate and land are liquidized into securities, which are then transformed into various financial products and traded in capital markets.

One gap that remains in the existing literature is a continuous investigation of land financialization against different political-economic contexts. Each mode of financialization is rooted in and can only be explained by certain state–economy relations, underpinned by a unique regulatory philosophy and state capacity. The second gap is that securitization in land development is still new and rapidly changing, from bonds and initial public offerings to more recent real estate investment trusts (REITs). While bonds and initial public offerings have been studied by the existing literature (see Birch and Ward, 2024; Chen and Wu, 2022; Li et al., 2024; Wu et al., 2020), using REITs to finance urban development and their connection with SE has not been sufficiently explored.

To fill these gaps, this article examines land financialization and exemplifies Chinese SE in this new governance era. Shenzhen Qianhai, China’s high-profile development zone, is selected as a case. Qianhai is designated by the central government as a pilot for in-depth cooperation between Guangdong Province and the Hong Kong Special Administrative Region (SAR) in the fields of innovation in modern services (including financial services), technological development, and market opening up. Qianhai also functions as a testing ground for China’s emerging land financialization, with the Shenzhen Stock Exchange hosting its first public REIT based on a real estate development project. The issuance of REIT in Qianhai marks the inception of a new land financialization mode steered by the local authority; the process also involves adapting regulations, fostering fairer relationships with the market, and increasing flexibility within the current institutional design. A study of Qianhai and its latest land development will provide advanced insights into China’s newest land financialization, which will add value to conceptualizing SE beyond the current understanding.

Three research questions guide this study. First, how is SE embodied in the development process of Qianhai, particularly in its land development innovation? Second, what regulatory capacities are deployed to facilitate land financialization, particularly in offering REITs? Third, behind the evolving SE, how could the Chinese state be reconceptualized in urban studies research?

The remainder of the article is structured as follows. The next section reviews theoretical debates on SE and land financialization. This is followed by an examination of the evolution of land financialization in China. The empirical section presents the case of Qianhai, introducing Qianhai Authority as a regulatory entity that bears flexibility and pragmatic entrepreneurialism in driving land development and facilitating the offering of the first REIT. The article concludes by discussing the role of the Chinese state in urban governance restructuring in China and beyond.

State entrepreneurialism and the evolution of land financialization

State entrepreneurialism

According to Max Weber, the state is a static human community with “the monopoly of the legitimate use of physical force within a given territory” (Brenner et al., 2003: 1). The regulation school elaborates the nature of the state from the functional perspective in relation to the economy. Capital accumulation is not self-fulfilling. The norms and modes of capital accumulation should stay in line with specific extra-economic settings, such as political environment, social norms, and means of collective consumption; the latter form the preconditions required for capital circulation (Jessop, 1994, 1997). The state has the capacity to enable those preconditions through its regulatory practices, including state actions and legislation, the establishment of social institutions, changes of behavioral norms and habits, and mobilization of political practices, to cope with non-state actors (Tickell and Peck, 1992). In sum, the state is a coherent institutional structure consisting of state apparatuses at different levels of hierarchy. Functionally, it is also a strategic agent with the capacity to make regulations for the profitable operation of capital and the reproduction of labor (Brenner et al., 2003; Jessop, 1997; O’Neill, 2004; Tickell and Peck, 1992).

The extension of state theory to non-Western contexts, particularly China, provides useful insights into the functions and rationales of state regulation (Sun and Chan, 2017). This is because, although ideologies and practices vary between capitalist and socialist regimes, state intervention exists to address the problems of capital accumulation, such as inflation and unemployment. The difference is that capitalist society has developed a mixed economy, whereas a socialist economy is state directed (Andrusz, 1996).

Conceptually, SE depicts a unique role of the state whose intention and actions are to leverage market instruments or engage in financial logics to further economic, social, and political goals. It is integral to the state’s capacity building in achieving designated regulatory goals. SE’s early manifestation was the state bureau leveraging market opportunities to set up trading and real estate development companies (Duckett, 2001). The profits were used to maintain expenditures (including salaries) and retain their positions under the new administration structure. Accordingly, SE reflects profit-seeking statehood with “risk-taking activities” to cope with challenges arising from market reform and its associated administrative restructuring (Duckett, 1996: 190). SE marks a distinct characteristic that has rarely been observed with the authoritarian statehood: state officials were, in fact, bold and quite flexible in adopting practices beyond their bureaucratic routine. While the majority of the scholarly discussions of SE focus on China, studies in other contexts suggest a similar change in the role of the state from a market facilitator to a business operator (Yılmaz and Aktas, 2021). In this way, the state “not only ‘crowds in’ business investment but also ‘dynamizes it in’, creating the vision, the mission and the plan” (Mazzucato, 2015: 135).

The seminal work by Wu (2023) suggests that SE could be understood as a unique way of governance, with two pillars of “planning centrality” and “market instrument” (Li et al., 2025; Wu, 2018). On one hand, market philosophies and financial approaches are instrumentalized by the state to promote territorial growth, sectoral competitiveness, and high management efficiency. Market approaches in urban development are state induced in the name of reform. Consequently, the state embodies de-regulation, decentralization, and increased devolution to non-state actors. On the other hand, the state reveals its steering and proactive role in market development, particularly by shaping market mechanisms in line with its own interests (Li et al., 2025; Wu, 2018, 2020).

Wu et al.’s (2024, 2025) recent work highlights the notion of “statecraft,” which is understood as the logic, arts, and tactics of governing land and development and managing state–economy relations. SE combines both interventionist and entrepreneurial features of governance—embodied in managerial and entrepreneurial statecraft—to fulfill different regulatory tasks that go far beyond growth and profit seeking (Sun et al., 2024; Wu, 2018). It is an extension of neoliberalism but features strong characteristics of intervention and steering. However, the intervention itself bends the interests of the economy and society, as the overall regulatory goals are multifaceted, encompassing more than just wealth accumulation but societal stability and citizens’ well-being.

Land financialization as a key expression of SE

Financialization means the “increasing dominance of financial actors, markets, practices, measurements, and narratives, at various scales, resulting in a structural transformation of economies, firms (including financial institutions), states, and households” (Aalbers, 2016: 3). The forms and practices of land financialization are constantly evolving. The initial stage of financialization is driven by the devolution of regulatory power from national to local states and institutional reforms. For instance, following China’s economic reform and opening up in the late 1970s, local states gained sufficient autonomy in driving territorial growth and development. This newfound autonomy coincided with the transformation of land and housing into tradable commodities rather than state resources, thanks to the commodification of housing and the marketization of land-use rights. The administrative and fiscal decentralization—particularly after the 1994 tax reform (in which the central government took a significant portion of revenue)—further incentivized the adoption of land-based finance for local economic development.

The 2008 global financial crisis was a turning point. To cope with the financial crisis, the Chinese state introduced a CNY 4 trillion stimulus package, which guaranteed significant spending on urbanization and infrastructure development. Assetization was introduced, which means turning land, infrastructure, and utilities into collateral for borrowing from state-owned banks. Assetization suggests a distinct norm of financialization: instead of commodity production, assetization monetizes future land sales and revenues (Birch and Ward, 2024). The state facilitated assetization by establishing local government financing vehicles (LGFVs, also known as Chengtou). These state-backed corporations were given the mandate of managing and monetizing state-owned lands and resources, most of the time, through mortgages. Assetization serves as a revenue-generating tool that underpins financialization, with clear signals from the Chinese state regarding increased spending on urban development.

Using land as collateral is not without risks, as local economies become heavily dependent on volatile land markets (Wu, 2022). Local debt increases when the market declines. As such, assetization is vulnerable to market volatility and has limited borrowing capacity. It is unable to generate consistent and reliable capital flows at a larger scale or with increased leverage. A new land financialization tool was introduced in 2014, which is a means of bond market capitalization (Li et al., 2024). It is a centralized and formalized means of borrowing, revealing increased regulation from the central government. Provincial governments were authorized to issue local government bonds, including general bonds for public welfare projects and special bonds for revenue-generating purposes (Li et al., 2023). LGFVs’ financial function was then detached from the local state to reduce the risks (Feng et al., 2022). This shift formalizes borrowing practices and ensures sustained financing capability for designated projects in the long run.

As marketization deepens and financial systems expand, the means of financialization become advanced and diversified. Particularly since 2016, the state has implemented stricter regulations to curb the risks associated with shadow banking, off-balance-sheet financing, and speculative market behaviors (Wu, 2022). These efforts aim to further release the potential of the financial market in supporting the national development agenda while safeguarding the financial system against crises. As a mature means of financialization, securitization is invented by the state that enables entities like LGFVs and real estate firms to bundle assets and future revenue streams into profitable and tradable securities, thereby creating upfront capital (Jiang and Waley, 2022). It has emerged as a key mechanism to unlock liquidity, diversify funding sources, and bridge public investment with private capital market (Wu et al., 2022).

Land financialization changed from the bank-based system to a capital-market oriented one (Jiang and Waley, 2022). Through diverse financial instruments and products, such as corporate loans, asset-backed securities, and wealth management products (which are investment products offered by banks and other financial institutions that pool funds from investors to invest in assets, such as municipal bonds, equities, loans, and trust products), household savings and institutional funds are channeled into urban development and infrastructure projects, yielding higher returns. Consequently, Chinese financial markets are linked with public investment (Theurillat, 2022).

Land financialization in China is closely tied to the distinctive regulatory norms and practices that emerged across different stages of SE. At the beginning, the state was an initiator. The state initiated institutional reforms that acknowledged the legitimacy of profit seeking through the alienation of land-use rights, associated with reforms oriented to marketization, privatization, and commodification (Wu et al., 2020). Land markets played a crucial role in the entire economic system.

Assetization highlights the dual characteristics of lands as both resources and profit-bearing properties (Birch and Ward, 2024). The state was a facilitator of assetization by setting up LGFVs, which could leverage land sales and future revenues to secure loans from banks. Consequently, SE is not about creating commodities but about monetizing lands into “financial assets” for borrowing (Wu et al., 2020).

The proliferation of securitization since 2016 marked changes in SE. The shift towards securitization indicates that the Chinese financial system has gradually matured, providing more diverse and transparent fundraising options. This transformation also highlights that to drive growth and achieve multifaceted goals, the state is increasingly adopting financialized logics and operating within liberalized markets—domains traditionally dominated by the private sector (Sun et al., 2024; Wu et al., 2024).

While encouraging securitization to diversify funding sources, the state imposes restrictions on other financial practices with high risks, such as excessive loans. With risks controlled, different financial institutions (such as LGFVs and real estate firms) are involved in securitization, giving rise to various financial instruments and products. While the evolution of land financialization indicates a more open market, mainstream scholarship suggests that the state plays a dominant role in this process. The state exerts control of financialization; it immerses itself in the market by transforming state agencies into financial operators (Wu et al., 2022).

Securitization introduces a more diversified and institutionalized approach that transforms fixed assets and anticipated revenue streams into immediate capital (Wu, 2022). One significant change is the involvement of multiple financial institutions. Conventionally, state-owned banks played a crucial role in either providing lending quota (assetization) or facilitating bond capitalization (by acting as underwriters and investors), connecting state interests in land financialization (Li et al., 2023). In securitization, the role of primary financial institutions extends beyond banks to include fund management corporations. For example, real estate firms are allowed to participate in fundraising practices.

Feng et al. (2023) argued that land financialization is not so much a market instrument but a governance tool by which the state maintains its power in urbanization and financial operation. Although financialization seeks to mobilize financial actors and products in driving development agendas, the local state retains its power through maintaining dominance in shareholding (rather than by external financial institutions) and prioritizing government projects to realize its own interests. Consequently, the goal of financialization is not about creating a market-friendly environment but a means of goal realization through a more strategic yet determined approach. In this way, land financialization bears a strong characteristic of planning centrality. Beyond this discourse, a closer examination of the evolution of Chinese land financialization reveals the state’s growing acceptance of expanding and diversifying financial operations, driven by its need for significant capital and high-level investments (Sun et al., 2024).

Regulation flexibility and pragmatism in the practice of SE

Since financialization means the “growing influence of capital markets, their intermediaries, and processes in contemporary economic and political life” (Pike and Pollard, 2010: 29), more actors involved in value maximization and marketization. Cons-equently, state intervention no longer relies primarily on law and hierarchical forms as the only means of control (Scott, 2004). The top-down models of control and development give way to diverse governance forms, including legitimacy sharing, public–private partnerships, and reciprocity (Besley, 2021). Regulation flexibility means to promote “flexible oversight” (McQuinn, 2019: 2), particularly through alternative means of supervision, coordination, engagement with broader stakeholders, and alignment with broader societal goals, while retaining decisive control over strategic assets and development directions. In fact, the rationale of flexibility has deep roots in the literature on regulatory capitalism, which highlights that contemporary states govern not by withdrawing from markets but by expanding, reconfiguring, and diversifying regulatory instruments and arenas to manage states’ interfaces with other domains (Braithwaite, 2008; Levi-Faur, 2005). Rather than a simple move from “more” to “less” state, regulatory capitalism involves a shift from rigid command-and-control to a negotiated, risk-based, and performance-oriented governance framework (Levi-Faur, 2005).

However, financialization itself is a contradictory process (Vercelli, 2013). Central to financialization is the freedom of decision makers in financial practices. Enhanced freedom may become a privilege for a small group of financiers, rentiers, and politicians. This leads to wealth and power being unevenly distributed across society, paving the way for recurrent crises. Consequently, regulation flexibility is not so much laissez-faire flexibility (letting markets self-regulate) but the reformation of a set of regulatory norms and rationality. In this way, the state balances and mediates various interests, ensuring the efficacy of co-governance (Zhao et al., 2024). By deploying strategic flexibility (adaptable but firm regulations), the financial system itself becomes an essential infrastructure of modern societies to support the functioning of the state and community (De Bruin et al., 2020). Consequently, financialization is internalized as a state capacity to achieve a broader regulatory agenda, with stable growth being one of them.

Pragmatism is a context-sensitive approach to regulation that prioritizes problem solving and feasible solutions. Pragmatism has a long-standing tradition in collaborative planning, emphasizing practical judgment under conditions of uncertainty and the iterative adjustment of strategies as new information and conflicts arise (Healey, 2009). It allows the state to adapt its regulatory tools in response to real-world challenges. Pragmatism is aimed at controlling risks and balancing power relations. The ultimate goal of state regulation is not only to leverage financialization for growth but also to foster positive societal changes (Wu et al., 2024). There are multifaceted goals behind capital accumulation, concerning social reproduction, societal development, and legitimacy building (Wu, 2015). The state’s role in the financialization process extends beyond being a market player; it seeks to mediate and repair the extra-economic conditions essential for the functionality and mutuality of the financial market and society as a whole. Accordingly, innovation and institutional reforms in financial practices become important problem-solving tools (Taylor, 2023).

Research methods and the significance of the Greater Bay Area

The coupling of regulation flexibility and pragmatism is a salient feature of SE in driving land financialization. However, it lacks empirical evidence. This study uses a qualitative approach to explore SE and land financialization in Qianhai. Qianhai, officially the Qianhai Shenzhen-Hong Kong Modern Service Industry Cooperation Zone of Shenzhen Municipality, was established in 2010. It was part of China’s ambitious plan to promote modernization and high-level regional cooperation between the Hong Kong SAR and Guangdong Province, two jurisdictions of China under the unique “one country, two systems” framework (Qianhai Authority, 2023). The pilot zone initially spanned 14.92 km2, with three designated areas focused on financial development, technology services and innovation, and modern logistics. By 2021, the second version of the Qianhai Master Plan expanded the area of Qianhai to 120.56 km2 (Qianhai Authority, 2024). The Qianhai pilot zone is overseen by the Qianhai Authority, a statutory body reporting directly to the Shenzhen Municipal Government.

The research draws on semi-structured interviews conducted from May 2023 to November 2024. Interviewees included 10 section chiefs or senior officials from the Qianhai Authority in the areas of technology and innovation, development and reform, institutional innovation, Hong Kong and Macao services, construction management, and planning management, two managers from a subsidiary owned by the Qianhai Authority for investment and land development, as well as a senior manager from Vanke, a real estate development company that is involved in Qianhai’s property development and the issue of the first REIT. Interviewees were chosen through purposive and snowball sampling, focusing on those directly involved in Qianhai planning, project negotiation, and financial product development. Interviews lasted between 120 and 150 minutes, were conducted in Mandarin, and were transcribed and thematically coded around governance mechanisms, financialization design, risk allocation, and legitimacy concerns.

Although the sample size is relatively small, access to such high-level respondents is rare, and the interviews provided first-hand information seldom available publicly. To enhance reliability, responses were cross-checked across interviews with senior officials in other departments to verify consistency and authenticity. Interview data were also triangulated with official documents, public reports, media sources, policy circulars, and financial records (including annual reports and REIT prospectuses). While these measures strengthen the credibility of the analysis, the limited number of participants remains a limitation to bear in mind when interpreting the findings.

The case is located in the Pearl River Delta region, currently known as the Greater Bay Area (GBA), one of China’s most dynamic city-regions. Covering nine cities and two SARs, the region exemplifies China’s city-regionalism under the “one country, two systems” framework (Qianhai Authority, 2023). Institutional innovations in land development and cross-boundary cooperation between mainland China and the SARs have been quite spontaneous due to their geographic proximity, even before the GBA concept emerged (e.g. “front shop, back factories” in the late 1970s; Sit and Yang, 1997: 656). In 1988, the new land administration law mandated the separation of land ownership and land-use rights, with the first piece of land transacted at Shenzhen. In 2008, the Pearl River Delta was China’s first city-region whose development plan outline was issued and promoted by the highest level of the state, that is, the National Development and Reform Commission, incorporating comments and initiatives from the two SARs.

Following the introduction of the development plan outline, the GBA has been tasked with furthering China’s comprehensive reform and policy experimentation. Within the GBA, three pilot zones with different institutional designs were established, namely Qianhai in Shenzhen, Hengqin in Zhuhai, and Nansha in Guangzhou. The variegated institutional settings governing the three pilot zones reveal the state’s intention to move beyond the one-size-fits-all governance mode.

Qianhai is more of an economic concept than a full jurisdictional entity, with a strong focus on innovation and reforms. Qianhai is located in two districts, namely Bao’an and Nanshan. The two administrative districts manage social and public affairs, such as education, healthcare, and social security. In this way, Qianhai could fully focus on economic development and financial innovation—the strategic positioning set by the central government. This approach liberates the Qianhai Authority from social development obligations, fostering a more neoliberal governance framework focused on efficiency, economic growth, and accountability.

Qianhai Authority is given the mandate to independently approve urban planning, construction projects (e.g. issuing permits and completion inspection), and land development (such as land-use rights transfer), which are conventionally under the municipal government. The authority operates in a marketized and enterprise-like manner. For example, half of the employees in the authority are seconded from the municipal government, while the authority has the ability to conduct independent hiring and bypass the traditional civil service system—exempt from endorsement by the party’s organization department. It could also carry out large-scale campus recruitment, and Hong Kong residents are eligible to apply.

The Qianhai Authority has four subsidiaries, with Shenzhen Qianhai Construction Investment Holdings Group Co., Ltd. (QCIH) being one of them. QCIH was established on December 28, 2011, with a registered capital of CNY 150 million. Usually, state-owned enterprises are overseen by an ad hoc commission set up by the State Council. However, QCIH is wholly owned by the Qianhai Authority as an operational arm in the areas of primary land development (pre-sale land preparation), infrastructure construction, and project investments. QCIH is a developer cum gatekeeper to ensure developments align closely with Qianhai’s strategic positioning.

In a large land parcel where more than one developer is involved, QCIH develops one plot and coordinates the construction process with other developers. For example, for a land parcel in Mawan that includes seven development projects, integrated underground space development is required to create a shared parking space to maximize land-use efficiency. QCIH plays a leading role in developing the detailed plan for the entire underground space and overseeing the construction process. Other developers, when signing contracts for land conveyance, have agreed that the construction of underground space will be coordinated by QCIH with the same contractor and engineering proposal.

The first office complexes through a 1.5-level land development mode

Once the first Master Plan for Qianhai had outlined its high-end strategic positioning, it quickly drew numerous enterprises and corporations—primarily from finance, logistics, and professional services—to establish their regional offices. By 2013, over 1000 enterprises had registered in Qianhai. However, lands for Qianhai were created through reclamation, so there were no pre-existing buildings that could provide adequate office spaces. Most enterprises were registered under the Authority’s office address.

Conventional land conveyance could be an option; however, since no infrastructure or facilities have been built, the developer would likely be very conservative in purchasing the land parcel due to many uncertainties from planning to implementation. Additionally, the entire construction process could take 10–20 years, which would not solve the office shortage problem. The lengthy timeline also conflicts with Qianhai’s reputation as Shenzhen’s most privileged zone. Against this background, the Authority proposed a flexible 1.5-level land development (hereafter 1.5-level mode) as a transition stage between levels 1 and 2. 1

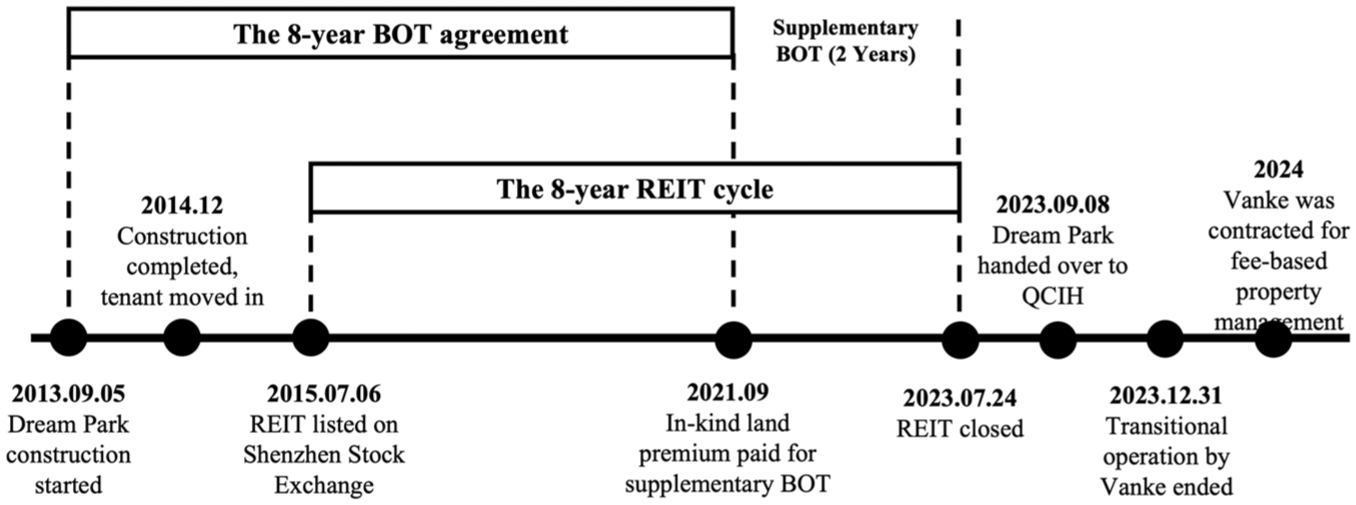

The 1.5-level mode is driven by “build-operate-transfer” (BOT), which has been largely used in infrastructure projects. It is, by nature, a short-term lease agreement: Qianhai Authority first allocated the land-use right to its investment arm QCIH for eight years. Vanke, a real estate developer based in Shenzhen, got the land at zero land premium for an eight-year period through an open bidding and tendering process. Under the BOT agreement, Vanke built and operated the Vanke Qianhai Enterprise Dream Park.

Vanke bore its own construction and operational expenses, earning profits from lease income. All properties were prohibited from sale and would be transferred to QCIH after eight years. The project adopts the neighborhood concept to create low-density office spaces and shared public open spaces, integrated with natural landscapes. Each building is typically two or three stories tall, connected by covered walkways to ensure all-weather accessibility while maintaining ample private spaces (Figure 1).

Vanke Qianhai Enterprise Dream Park. The Dream Park is Qianhai’s first office development project, covering approximately 93,192.96 m2 with a total floor area of 65,000 m2. It includes 33 office buildings and seven public facilities.

Vanke commenced construction on September 5, 2013, and completed it in 475 days, significantly faster than the conventional construction process. The project’s total investment of CNY 773.29 million quickly yielded strong financial returns. By the second quarter of 2015, the Dream Park had reached a 95% occupancy rate, with rental prices ranging from CNY 400 to 600 per m2. Tenants included 32 Fortune 500-listed companies, with more than 80% from the financial sector. Notable occupants included Standard Chartered Bank, HSBC, and the Agricultural Bank of China.

Linking 1.5-level mode with land financialization: Qianhai’s first REIT

A core mandate of Qianhai since its inception has been to serve as a testing ground for financial reform and innovation. This role was formally institutionalized in the 2010–2020 Master Plan, in which Qianhai was named as a strategic platform for piloting China’s financial opening up. In response to this strategic positioning, in 2015 QCIH (authorized by Qianhai Authority), aligned with Penghua Fund Management Company (PFMC) and Vanke’s three corporations (Shenzhen Vanke Qianhai Enterprise Dream Park Construction Management Co., Ltd., China Vanke Co., Ltd., and Shenzhen Vanke Real Estate Co., Ltd.), launched Qianhai’s first REIT. 2

Under the agreement, the REIT was issued by PFMC, was listed on the Shenzhen Stock Exchange on July 6, 2015, and was scheduled to close on July 24, 2023. The product is based on eight years of rental income of the Dream Park from 2015 to July 24, 2023, aiming to pool CNY 3 billion. According to an estimate by consultancy firm Cushman and Wakefield, the rental income from Dream Park between 2015 and 2023 totaled CNY 1.82 billion, considered a highly potential underlying asset for pooling capital. The short investment cycle was due to the property’s temporary land-use status under the BOT agreement. Half of the raised funds were allocated to secondary market investments, such as fixed-income assets. The other half were channeled to Vanke in four phases from 2013 to 2025. The funds are used to purchase a 50% stake in Vanke’s consortium for Dream Park. Although Vanke will buy back 50% of its outstanding shares after eight years, the quick cash enabled Vanke to recover its investment costs, with a surplus of around CNY 0.22 billion (after deducting construction costs) available for new investment opportunities. 3

The REIT agreement required the annual operational income to grow by 9%. To guarantee this, Vanke deposited CNY 20 million into an ad hoc account. If annual income fell short of projections, Vanke was obligated to cover the gap using the deposit and maintain an annual balance of CNY 20 million.

Since the initial BOT contract for the Dream Park lasted from 2013 to 2021, while the REIT’s issuing period spanned from 2015 to 2023, there would be a two-year gap after Vanke’s lease had expired but the REIT still continued. To align the timelines, the Qianhai Authority extended Vanke’s operational rights through a supplementary BOT agreement (Figure 2). To achieve this, Vanke first transferred the Dream Park to the Qianhai Authority. The Authority then leased the property to Vanke for another two years (from September 8, 2021 to July 24, 2023). Different from the first BOT agreement where Vanke leased the empty land, the second lease involved established office complexes. Therefore, Vanke paid an in-kind land premium by lending CNY 248 million to QCIH. QCIH could pay back in phases without interest. For QCIH, the money would provide additional cash flow for its daily operations.

Timeline of the REIT and its alignment with BOT and Dream Park’s operation.

On September 8, 2023, the Dream Park was officially handed over to QCIH. Considering the transaction costs (including the commission paid to PFMC) incurred by Vanke for issuing REIT, QCIH agreed that Vanke would continue to operate the office complexes and retain the proceeds until December 31, 2023, with a cap of CNY 65 million. Any additional proceeds would be transferred to QCIH. Starting in 2024, Vanke was contracted by QCIH as a property management company and shifted to a fee-based service model.

Certainly, REIT has difficulties. Between 2015 and 2023, China’s real estate sector experienced significant volatility as the central government introduced more stringent measures to rein in uncoordinated expansion. Additionally, the COVID-19 pandemic contributed to the decline in demand for office spaces. Rental prices fell from CNY 400 at their peak to CNY 200 per m2. Therefore, REIT might not fully maximize profits due to an eight-year investment cycle and significant fluctuations. A longer period could lead to more promising returns, which was not possible in this case due to the specific lease condition of the Dream Park. However, as China’s first REIT, Qianhai achieved a breakthrough not only due to its early adoption of REITs but also by expanding REITs’ application beyond traditional infrastructure to include real estate properties. 4 The Dream Park project also brings significant extra market value as it represents the company’s first venture beyond the residential sector into the office market. Its successful operation establishes a good track record for Vanke in this segment, enhancing its competitiveness for future similar projects in the GBA.

Discussion: Regulation flexibility and pragmatism in an urban governance experiment

The 1.5-level mode functions as a tool for reshaping state–market relations, which articulates how risks, responsibilities, and benefits would be shared between the local authority and the market. The BOT model in infrastructure development was adapted into the land development process. This arrangement incentivizes market actors to shoulder construction costs and navigate early-stage uncertainties. With developers granted a share of future rental income, private actors assume greater responsibility for placemaking and day-to-day management in order to respond more quickly to tenant requirements.

The 1.5-level mode also acts as a risk-sharing tool in land governance: investment decisions always take future land value into account. Delays in infrastructure development, as outlined in the Master Plan, can lower returns, creating uncertainties. Waivers of land premiums and shorter tenures help mitigate this uncertainty, minimizing investment risks. For the Qianhai Authority, the quick construction addresses the shortages in office spaces.

In order to achieve this, the Qianhai Authority strategically crafts a regulatory framework for short-term land use. Besides this, it employs flexibility to prompt the development agenda and attract private capital. The Authority bypasses conventional land-use right transfers. Instead, land is allocated to its investment subsidiary (QCIH) and leased to a private developer (Vanke) under shorter tenures. This reduces the upfront costs for developers while ensuring quicker project delivery. The mode highlights the authority’s entrepreneurial role in utilizing land resources to create business opportunities and achieve the strategic growth targets set by the central government. Flexibility is also revealed in financial innovations. For example, to ensure the smooth operation of Dream Park and the REIT, the Authority granted a two-year lease extension (from 2021 to 2023) when the first BOT agreement expired.

Pragmatism is evident in Qianhai’s adherence to market rules, with policymaking being outcome based and solution oriented. Despite QCIH’s ownership of the land, the Qianhai Authority did not request preferential treatment—leasing office space in Dream Park at market rates. Upon the concession’s expiration, QCIH ensures a smooth transition by granting Vanke a five-month operational grace period under a contractual profit-sharing mechanism. This arrangement highlights the Authority’s market-oriented adaptability, balancing government and market interests. The phased ownership transition minimizes disruption, reinforcing the Authority’s credibility and consistency in investment and policymaking. This approach underscores the local state’s capacity to adjust regulatory arrangements in response to market needs, acting as a rational and fair regulator. This also demonstrates the Authority’s efforts to build credibility for long-term partnerships with private actors.

The presence of regulation flexibility and pragmatism features Qianhai’s experimental land governance that allows shorter land tenures, faster project delivery, and the subsequent bundling of the project into securitized financial vehicles. This reflects that SE blends both deregulation (market autonomy) and managerialism. On one hand, the private developer independently constructs, finances, and operates the project. The Dream Park was completed in 475 days, whereas most projects in Qianhai typically require three years before they are delivered for use. The returns from the Dream Park not only covered the initial costs but also generated profits that could be used for future investment projects. On the other hand, the exercise of regulation flexibility reflects the Qianhai Authority’s strong commitment to fulfill the KPIs assigned by the central government. One of the Authority’s key priorities is to accelerate land development and deliver tangible results in a timely manner. The project is successful in “building image, attracting popularity, and delivering tangible benefits” (chu xing xiang, ju ren qi, jian xiao yi). This concurs with Wu et al.’s (2024) observation that managerial statecraft remains a salient feature in SE.

Interestingly, much of the literature shows that the financialization of real estate, housing, and urban development often redistributes risk downward to tenants and households, producing new forms of inequality and uneven development (Aalbers, 2020; Christophers, 2022; Wainwright and Manville, 2017). The case of Qianhai, however, appears distinct in that it has not generated significant tensions between the state and the market or between the market and society. First, financial risks are tightly controlled by the state, including the use of a profit-guarantee mechanism to secure minimum returns for investors. Moreover, the Authority actively manages the underlying assets to ensure REIT’s profitability, by offering tax incentives and fee reductions, and by encouraging large corporations to establish offices in Qianhai. In this sense, the REIT in Qianhai is not a straightforward case of “less state and more market” financialization (Aalbers, 2016: 17) but rather is a state-managed financial innovation that contributes to Qianhai’s strategic positioning and its image as a testbed for financial innovation.

Conclusion: A new direction for managerial statecraft?

This article revisits SE and explores its new trends through a case study of Qianhai—a prominent pilot zone in China that exemplifies the nation’s latest advances in territorial development. By analyzing two innovative practices related to land development and financialization, we aim to develop a more nuanced understanding of the role of the state in urban governance transformation, particularly beyond the typical Anglo-American frameworks.

It is important to note that Qianhai represents a distinctive case due to its high-profile positioning as a pilot area with strong political endorsement and support from the central government (State Council, 2023). The Qianhai Authority, a statutory body with elevated decision-making and implementation powers, functions as an ad hoc jurisdiction responsible for approving planning and development projects within the area. Responsibilities related to social welfare provision, education, and routine maintenance of utilities and sanitation remain with the two district governments (Bao’an and Nanshan) in which Qianhai is geographically located. This governance arrangement allows the Authority to focus primarily on economic development and innovation, in line with its central mandate.

Qianhai’s jurisdictional configuration differs markedly from the other pilot new areas in the GBA. Hengqin is co-governed by the Guangdong Provincial Government and the Macao SAR Government, with officials from both sides jointly assigned to the management committee overseeing the New Area. Nansha, by contrast, is administered by an ad hoc commission under the Guangzhou Municipal Government, with its development largely initiated by state-owned enterprises. Together, these contrasts underscore the uniqueness of Qianhai, which sets a specific context for regulation flexibility and pragmatism.

The innovative practices in land development and financialization point to the emergence of new state capacities to formulate development trajectories. However, the use of regulation flexibility and a pragmatic approach in policymaking does not signal a less-harnessed, hands-off development mode; rather, it is driven by a strong commitment to realizing the central government’s political objectives for “high-quality development,” particularly its expectation of Qianhai to “start from zero and achieve visible progress year by year” (State Council, 2023: 5). In this sense, although the Qianhai Authority exercises considerable flexibility, its practices remain firmly embedded within a broader framework of planning centrality.

Taken together, these findings suggest that SE is not a departure from but rather an accentuation of evolving managerial rationalities in urban governance. This feature aligns with recent scholarship that describes managerial statecraft as key to building regulatory capacity (Wu et al., 2025). Interestingly, being “managerial” does not necessarily entail rigidity, rule-bound practices, or a return to old-style command-and-control regulation. Instead, market-friendly instruments and land governance tools can function as alternative managerial instruments to drive local development and more effectively achieve regulatory and developmental objectives. In this way, the state can foster entrepreneurial growth while maintaining decisive control over critical factors, balancing policy experimentation with oversight to ensure that innovations align with higher-level political directives and remain fully manageable.

Footnotes

Acknowledgements

We would like to express our heartfelt gratitude to the officials of the Authority of Qianhai Shenzhen-Hong Kong Modern Service Industry Cooperation Zone of Shenzhen Municipality and to the interviewees from Vanke for their invaluable support during our fieldwork. Their insights into the latest developments in Qianhai greatly enriched our understanding and contributed substantially to this research. We are also grateful to the two anonymous referees for their constructive comments.

Ethical considerations

Ethical review was approved by the Institutional Review Board of the Hong Kong Polytechnic University (HSEARS20191027001-01).

Consent to participate

All participants gave their consent prior to the interviews.

Author contributions

The two authors contributed equally to this work. Their names appear in alphabetical order.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The work described in this article was fully supported by a grant from the Research Grants Council of the Hong Kong Special Administrative Region, China (Project No. PolyU 25609920).

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data availability statement

The interview data collected and analyzed during the current study are not publicly available due to privacy and ethical restrictions.