Abstract

This article investigates the spatial patterns of interurban trade in capital market services by analysing 16,324 trade links involving advisers and clients in the Visegrád Four plus Austria and their counter-parties worldwide between 2000 and 2014. We aim to address a gap in the research on financial centres and interurban trade by providing empirical evidence on the relationship between the complexity of services and the size of market areas across which they are traded. We utilise recent contributions to Central Place Theory (CPT), which provide us with suitably general models of interurban trade applicable to financial services. The key proposition of CPT in this respect is that more complex services are traded across larger market areas, thus translating into a further spatial reach of service centres. Given that these propositions are derived at a very general level, we rely on global city theory for explaining the underlying causal mechanisms in the context of capital market services. Our analysis examines the geography of adviser–client trade links to investigate how spatial patterns of interurban trade in capital market services are shaped by the characteristics of the services traded. We uncover evidence that more complex and larger transactions are associated with higher distance between clients and financial services providers. This in turn means that more complex services are traded across larger market areas. While clients in Central and Eastern Europe can generally find suitable providers for less complex capital market services locally, they often rely on financial services providers globally for the most complex transactions.

Introduction

In the last few decades, we have witnessed a meteoric rise in the size and complexity of financial markets (Krippner, 2005). As a consequence, the financial logic has permeated all sectors of the economy, including business, state and households, through a process of financialisation (Epstein, 2005; Erturk et al., 2008; Krippner, 2011). The rise of financial centres has further deepened the financialisation of cities and urban development (Aalbers, 2020; Bassens and van Meeteren, 2015). Capital market services have assumed centre stage due to their high-value, low-volume character and the associated elite culture of investment banks as providers of these services (Wójcik, 2012). The drive for shareholder value maximisation, a central tenet of financialisation, has enhanced demand for capital market services by publicly listed companies striving to cater to the needs of investors (Muellerleile, 2009).

While most literature on the geography of capital market services is focused on leading financial centres and the global north (e.g. Sassen, 2001; Taylor et al., 2003; Wójcik, 2012), this article focuses on medium-sized economies in Central and Eastern Europe (CEE), namely Austria, Poland, the Czech Republic (Czechia), Hungary and Slovakia. The trade patterns in capital market services exhibit a mixture of hierarchical interurban relations as well as uneven and overlapping market areas for services of varying complexity. The Austrian capital, however omnipresent throughout CEE, does not monopolise the region, as the Brussels-headquartered KBC and Parisian Société Générale, for example, facilitate additional linkages to the ‘parent’ financial centres through their subsidiaries. The strong presence of PKO Bank Polski in Warsaw and OTP Bank in Budapest illustrates the growing local capacities to handle financial transactions. The Vienna Stock Exchange failed to consolidate the securities exchanges in CEE, and London still accounts for almost a half of over-the-counter foreign exchange daily turnover for the Polish złoty and Hungarian forint in recent years. 1 The complex structure of external urban relations in capital market services trade stimulates a discussion beyond the horizontal network of international financial centres and their regional ‘hinterlands’.

This article investigates the interurban trade in capital market services by analysing adviser–client trade links. More specifically, we examine how external urban relations are shaped by the characteristics of the capital market services traded. ‘Capital market services’ in this study are defined as intermediary services rendered to firms in the form of bond and equity securities underwriting, loan syndication and mergers and acquisitions (M&A) advisory. While these services are fundamental to international financial centres, many post-socialist economies in CEE seek financial services providers globally to meet increasingly complex local demands. For example, a firm in Katowice, Poland, may import capital market services from London, instead of seeking them in Warsaw (domestic financial centre) or Vienna (regional financial centre). As we show, firms in CEE tend to look beyond their domestic or regional financial centres, particularly if they require services to support very large and complex capital market transactions. Meanwhile, smaller and less complex transactions are typically catered to by domestic or regional financial services providers.

We operationalise our model of interurban trade derived from Central Place Theory (CPT) (Parr and Budd, 2000) by analysing the adviser–client pairwise distance. In doing so, we are able to examine the relationship between the size and complexity of services traded and the size of their market areas. We hypothesise that larger and more complex capital market services have larger market areas. To test this proposition, we examine the relationship between the size of capital market transactions and additional measures of their complexity on one hand, and the pairwise distance between clients and financial services providers on the other. We also investigate potential overlaps between market areas which indicate heterogeneity among capital market services providers and financial centres. We utilise data on capital market transactions sourced from the Dealogic database. Our dataset contains 16,324 trade links, which involve advisers and clients in CEE and their counter-parties worldwide between 2000 and 2014. This database is widely used for market and performance evaluations of investment banks and has become an industrial standard for their ranking tables. We use quantile regression techniques for panel data analysis to estimate our models, and bootstrapped standard errors to evaluate the statistical significance of our coefficient estimates (Greene, 2018; Koenker, 2004).

Our results indicate that the spatial structure of interurban trade in capital market services broadly corresponds to the key proposition of CPT, namely that more complex services are traded across larger market areas (Berry, 1967; Christaller, 1966 [1933]; Lösch, 1954 [1940]; Parr and Budd, 2000; Parr, 2017). This striking resemblance may be surprising at the outset, given that the early CPT research focused on retail services, rather than those provided to corporations. Nevertheless, key concepts from CPT have been adapted to suit the needs of research on financial services and have been shown to be equally relevant in this context (Parr and Budd, 2000). That being said, CPT is applicable to interurban trade in financial services only at a high level of abstraction and does not necessarily pin down the specific processes that generate the observed distribution of trade links related to the provision of financial services. This study therefore complements CPT with insights from global city theory (Sassen, 2001), which theorises the workings of advanced producer services complexes, which form the beating heart of financial centres.

The remainder of this article is divided into five sections. The second section reviews the literature on financial centres, interurban trade in services, CPT and global and world cities. The third section develops three hypotheses. The fourth section explains how we build our dataset and details our econometric modelling methodology. The fifth section first offers a descriptive analysis of interurban trade within the urban systems in Austria, Poland, the Czech Republic, Hungary and Slovakia and then presents our econometric results. The final section concludes and discusses our findings in relation to existing research on the topic.

Financial centres as central places

‘Until very recently, research on external relations of towns and cities was severely neglected in urban geography’ (Taylor et al., 2010: 2815). While Taylor et al. (2010) admit that the CPT models introduced by Christaller (1950, 1966 [1933]) ‘became unfashionable in Geography’ due to their formal (or strictly geometrical) spatial modelling (Taylor et al., 2010: 2803), their survey also notes the Central Place ‘thinking’ in the recent world and global city scholarship (e.g. Sassen, 2001; Taylor, 2004) and the new economic geography (e.g. Krugman, 1998; cf. Mulligan et al., 2012). Bennett and Graham (1998) linked CPT with interregional trade theory to investigate the hierarchy of business services centres. Focusing on the dispersed nature of demand for intermediary financial services, Parr and Budd (2000) extract the principles of CPT to explain the spatial structure of financial centres. Encouraged by these predecessors, this section elaborates on some of the key CPT concepts concerning interurban trade patterns and hierarchical interurban structure. Following the propositions developed by Lösch (1954 [1940]) and Berry (1967), the section highlights the connection between the order and range of goods/services.

In analysing interurban socio-economic activities, Christaller (1950, 1966 [1933]) assumes strict geometrical distribution of settlements, or ‘central places’, arranged in a grid of hexagons. This equidistant arrangement makes central places the best access points of goods/services for the surrounding market area, a concept similar to ‘hinterland’. In fact, Porteous (1999: 105) defines hinterland in relation to a financial centre which ‘provides the best access point for profitable exploitation of valuable information flows’. What differentiates the CPT framework from the models based purely on hinterlands is the source of hierarchical interurban structure. In the latter models, the spatial size of market areas (hinterlands) dictates the capacity of cities to draw resources and information. Therefore, cities compete against each other over the market areas on a level playing field, which can be easily translated into a zero-sum game among cities. In the CPT framework, the production of more complex services is concentrated in fewer places, forming a more spacious matrix of higher order central places over the matrix of lower order central places. The interurban relations are thus hierarchical, based on the capacity to deliver higher order services (Berry, 1967; Berry and Garrison, 1958a, 1958b, 1958c). The higher the order of services (i.e. larger and/or more complex), the wider the range of services (the maximum distance that consumers/clients are willing to travel), making the varying spatial size of market areas primarily a result, rather than a source, of interurban hierarchy.

In generalising Christaller’s models, Lösch (1954 [1940]) relaxes the assumption of perfectly even spatial distribution of demand. Eaton and Lipsey (1982) further elaborate Lösch’s modifications and bring producers’ profit-maximising behaviours into the model, thus building the microeconomic foundations of the CPT framework. By relaxing the assumptions, producers in the modified models are aware of the economies of agglomeration achieved by locating near each other (Fujita and Thisse, 2002; Parr and Budd, 2000), which include the ease of access to a skilled labour force and the development of shared infrastructures. As such, Lösch (1954 [1940]) begins to explain a virtuous cycle of higher order central places, where the agglomeration of producers enables the production of higher order services. As higher order services have larger market areas, the enlarged market area (hence, increased demand) enables the producers to sustain their production at the higher order central places. The sustainable production then strengthens the hierarchical interurban structure.

The lowest sustainable level of production is known as the threshold of production, below which the low level of demand makes the production of (higher order) services uneconomical. In capital market services, different types of services are demanded at different scales and frequencies (e.g. managing loans versus M&A advising, underwriting of new equity issues in Warsaw versus Bratislava). This notion is a significant departure from the even distribution of demand and homogeneous tastes, assumed in the earlier CPT models (Parr and Budd, 2000). Infrequent demands for higher order capital market services in smaller financial centres make the localised production of such services by subsidiaries less economical, even when the benefits of face-to-face interactions (e.g. Jones, 2007) or the economies of co-location (e.g. Krugman, 1991) are considered. As a result, Taylor et al. (2003) observe the clustering – that is, agglomeration of not only advisers but also clients– to be a norm rather than an exception in the financial sector.

The transportation cost, or the ‘distance decay’, has been a major factor for the threshold of production as well as the firms’ localisation strategies, and this proximity–concentration trade-off (Markusen, 1984) is the basis for more elaborated CPT models such as ‘optimal integration strategies’ (Grossman et al., 2006), ‘competing [market] destinations’ (Fotheringham, 1983) and ‘competing central places’ (Fik and Mulligan, 1990). Shearmur and Doloreux (2015) claim that knowledge-intensive business services firms consider proximity to clients to be less significant, thus making their CPT model more hierarchical, based on the capacity to be innovative. Producers of capital market services (hereafter ‘advisers’) shift their focus from spatial proximity to their clients to differentiation/specialisation of their services, and they ‘select an approximately central location within [their] market area’ (Parr and Budd, 2000: 602).

Such heterogeneous strategies and capabilities of multinational enterprises (Goerzen et al., 2013; Yeaple, 2003) lead to the heterogeneity of central places, as opposed to the absolute specialisation among central places, due to synergistic development in clusters (Gordon and McCann, 2000). Sassen (2001) points out in relation to Castells (1996) that firms entertain a spatial division of labour within their global assembly line, in order to maintain the cost-effectiveness of their global production networks and information flows. In other words, each subsidiary office within a global firm may specialise in a certain product, depending on the synergistic characteristics of local clusters. Thus, higher order financial centres and clusters of multinational enterprises are more likely to be exposed to each firm’s heterogeneous strategy, and the exposure culminates in the heterogeneity of financial centres (Bennett and Graham, 1998). As the heterogeneity of financial centres in this framework is partly endogenous to firms’ strategies, the complementarity between subsidiary offices within a firm can easily be translated into the complementarity of financial centres (Beaverstock et al., 2005; Faulconbridge, 2004; Meijers, 2007).

Whether in Parr and Budd (2000), Parr (2017) or Taylor et al. (2010), CPT largely remains a tool to illustrate spatial patterns/structures of relational geographies. On one hand, by departing from Christaller’s (1966 [1933]) highly restrictive models, modified CPT models can be applied to financial services trade with an uneven distribution of demand. The structural association between the order and range of services is interpreted as an association between the size/complexity of services traded and the spatial reach of financial centres. The causal mechanisms underlying the spatial reach of financial centres must, however, be sought outside of CPT, as financial services providers utilise economies of scale, service differentiation and network connectivity, and rely on the institutional environment of the countries they operate from (Pažitka and Wójcik, 2019; Wójcik et al., 2018).

Global city theory informs our understanding of the varying spatial reach of financial centres through its emphasis on the co-production of complex financial services, and recognises the importance of advanced producer services (APS) complexes. These complexes form the heart of financial centres and feature accounting, auditing, law and management consultancy firms as important actors supporting capital market transactions (Sassen, 2001). More complex capital market services require more advanced expertise of financial services providers as well as accounting, auditing, legal and management consulting professionals involved in these transactions. It therefore follows that the more complex the service, the fewer financial centres will have all the necessary skillsets and expertise to support its delivery. Sassen (2001) highlights the roles of New York, London and Tokyo as global cities with the most developed APS complexes. Naturally other cities also display global city characteristics and are plugged into a global network through office networks of multinational companies (Taylor et al., 2010). That being said, both the numbers and quality of offices of APS providers vary widely across cities (Taylor, 2004), and smaller financial centres are therefore unlikely to share the same capabilities and expertise as those of the world’s leading financial centres. Consequently, while the expertise to support smaller, less complex and routine capital market transactions is likely to be available across a higher number of cities, only a very limited number of financial centres will have all the necessary expertise available to support the most complex transactions (Sassen, 2001). This in turn means that companies wishing to access capital market services may find it necessary to look for suitable service providers globally, to support the most complex transactions. The next section lists hypotheses based on these theoretical discussions and model modifications.

Hypotheses development

Drawing on the insights from CPT and global city theory, we therefore propose that more complex capital market services will be traded across larger market areas. In order to develop testable hypotheses for this proposition, we utilise the concept of range from CPT, which is the limit to the size of the market area for a service of a particular order of complexity (Berry, 1967). We use two measures of service complexity – size of transaction and service category. We assume that larger transactions are more complex and require higher levels of expertise, implying that they can be provided from fewer financial centres and consequently are traded across larger market areas. Similarly, we assume that certain types of capital market services, such as M&A advisory, are more complex and are traded across larger market areas than less complex services such as bond underwriting.

Hypothesis 1: Capital market services involving larger transactions are traded across larger market areas.

Hypothesis 2: More complex capital market services, such as M&A advisory, are traded across larger market areas.

The heterogeneity and complementarity of services provided by different financial centres are likely to lead to overlapping market areas. In fact, Berry (1967: 11–12, 17–21, 92) empirically illustrates how customers from the same market area are served by more than one central place. In the context of capital market services, there are several underlying factors that drive the heterogeneity of services provided by different financial centres. First, financial centres in different countries are subject to different institutional environments and different legal frameworks, thus subjecting clients to different regulation (Wójcik, 2013). Second, different financial centres host different capital market services providers, who are able to facilitate access to alternative groups of investors, thus allowing publicly listed companies to diversify their shareholder base beyond what would be likely to be achieved through a single financial centre. Third, the organisational networks of financial services providers located in different financial centres vary widely (Pažitka et al., 2019). Consequently, it may be advantageous to access capital market services through a financial centre, which is best positioned to leverage its network ties of investors, potential targets of acquisitions or lending syndicate partners to meet the client’s needs. Given that such needs may vary with every transaction, the above points are likely to lead to overlapping market areas for capital market services. This means that clients in the same geographical area would be served by multiple financial centres.

Hypothesis 3: Market areas of financial centres overlap with each other, and consequently clients located in the same area are served by advisers from multiple financial centres, even if their demands do not differ in terms of transaction size and service category.

Based on Guérin-Pace (1995) and Krakover (1998), Poon et al. (2004) illustrate increasing competition from regional financial centres (such as Vienna) vis-a-vis larger international financial centres (such as London), partly due to the increasing capacity of the former to produce higher order services in terms of both size and product category. Nevertheless, Esparza and Krmenec (1996) note that smaller (non-capital) cities do not extend their spatial market areas beyond the respective regional (sub-national) urban systems. In other words, larger financial centres are expected to have larger market areas, and their advisers are competing with advisers from smaller financial centres near their clients, rather than advisers from smaller financial centres competing for clients proximate to larger financial centres (Wójcik et al., 2019). The next section describes the data and methods utilised in this study in order to test the above hypotheses.

Data and methodology

In order to identify trade links between clients and providers of capital market services, we track bookrunners (lead advisers in bond and equity issues), mandated lead arrangers of syndicated loans and acquirer and target advisers in M&As. We refer to them as advisers for short. The rationale is that they constitute the primary link to the clients as either the sole adviser on a deal or one of the lead advisers in a syndicate, receiving the vast majority of fees. Our dataset covers clients headquartered in Austria, Poland, the Czech Republic, Hungary and Slovakia (referred to as CEE for short), and we trace their trade links to advisers worldwide. Our data on provision of capital market services are sourced from the Dealogic database. With more than 1 million capital market transactions recorded since 1993, the database has become an industrial standard for market and performance evaluations of investment banks. Our dataset contains 16,324 trade links, which involve advisers and clients in CEE and their counter-parties worldwide between 2000 and 2014. For our econometric analysis we use a subset of 12,473 trade links, involving 2971 clients in CEE and 1045 advisers worldwide. 2 We use the remaining 3851 trade links representing exports from CEE to the rest of the world for a descriptive analysis of regional financial centres in CEE (Vienna, Warsaw, Prague, Budapest and Bratislava). We complement this with data from the Bureau van Dijk-Amadeus database, which provides location data for advisers and clients. This allows us to construct our dependent variable, which is a pairwise distance between the headquarters of the advisor and the client for each transaction.

We analyse our dataset by first offering a descriptive analysis of the spatiality of trade in capital market services. We then proceed to a quantile regression analysis, which we use to test our hypotheses. Given that our hypotheses focus on the size of market areas, modelling the conditional mean of pairwise distance between advisers and clients, as would be the case in standard multivariate regression analysis, would not be appropriate for testing them. We therefore model the conditional percentiles of pairwise distance ranging from 50th to 90th. The 90th conditional percentile is most relevant for the purposes of our analysis, meaning that we effectively use the right tail of the distribution of observed pairwise distances between advisers and clients as a statistical proxy for the size of market areas. We estimate our models using the penalised quantile regression with fixed effects (Koenker, 2004, 2005). We use client fixed effects and time period fixed effects. Standard errors are obtained by bootstrapping (Greene, 2018) based on 100 simulations. 3 We estimate a series of quantile regression equations in the following form:

where disti,j,t is a pairwise distance between client i and adviser j in time period t, measured in kilometres; transaction_sizei,j,t is the deal value of equity/bond securities issue, syndicated loan or M&A, measured in constant 2012 US dollars; city_sizei,j,t is the aggregate value of fees earned from equity/bond securities underwriting, syndicated loans and M&A advisory by advisers located in a financial centre, measured in constant 2012 US dollars; equity_securitiesi,j,t is a binary (0,1) indicator variable for equity securities issues; syndicated_loansi,j,t is a binary (0,1) indicator variable for syndicated loans; M&A_acq_advisoryi,j,t and M&A_tar_advisoryi,j,t are binary (0,1) indicator variables for M&A acquiror and target advisory; Bratislavai, Budapesti, Praguei, Viennai and Warsawi are binary (0,1) indicator variables for clients i being headquartered in the respective cities; ηi is a client fixed effect; γt is a time period fixed effect; εi,j,t is an idiosyncratic error term. Finally, we transform all continuous variables by taking a natural logarithm to allow for non-linear relationships.

We test hypothesis 1 by examining the statistical significance of the coefficient estimate on transaction size, a measure of complexity of service transactions. Similarly, hypothesis 2 is tested by examining the statistical significance on four product category indicator variables. Finally, to test hypothesis 3, we examine the statistical significance of the coefficient on the city size (total fees) of financial centres. Positive and statistically significant partial correlation between financial centre size and pairwise distance indicates overlaps in the associated market areas, when the transaction size and product category are already controlled for.

Results

Dataset description

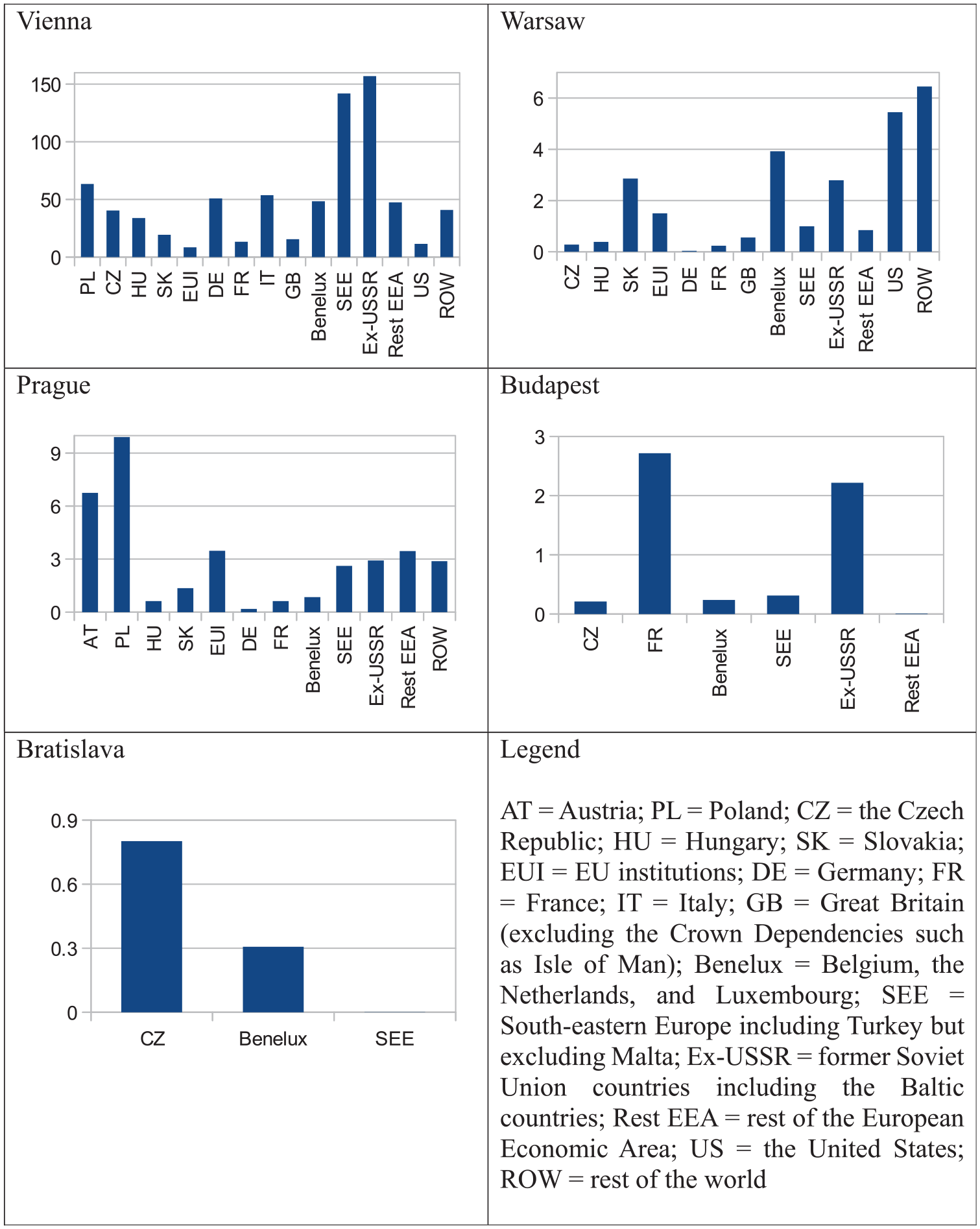

The capital cities dominate the provision of capital market services in CEE and serve as the domestic financial centres. Vienna earned US$1.7 billion in total fees (84.1% of fees collected in Austria), and Warsaw earned US$500 million (86.3% of fees collected in Poland) from 2000 to 2014. The two largest economies in the region, Austria and Poland, exhibited an element of decentralisation by having multiple financial centres (Hashimoto and Wójcik, 2020), while Prague (US$146.5 million total fees), Budapest (US$41.8 million) and Bratislava (US$13.0 million) dominate the capital market services provision in each country. Looking at destinations, Vienna earned 21% of fees from other CEE countries, 21% from the former Soviet Union countries (mainly Russia, US$117 million) and 19% from South-eastern European countries including Turkey (Figure 1). Prague exported as widely as Warsaw in terms of the number of destinations. Yet, beyond Europe and the former Soviet Union, Warsaw’s exports reached as far as the United States, Canada, China, Israel and South Africa, while Prague exported only to South Korea. Prague earned more than half of the cross-border fees from other CEE countries and Bratislava earned 72% from the Czech Republic. Budapest and Bratislava exported to only a limited number of destinations outside of Visegrád.

Destinations of capital market services exports from CEE in US$ million (2012 constant).

Further observations on trade links highlight how a small number of transactions can characterise the export landscape of medium-sized financial centres. Taking Warsaw as an example, Lasanoz Finance in association with CDM Pekao advised South African Naspers in 2007, collecting US$3.3 million. Icentis earned US$5.4 million in fees from Eton Park Capital Management, an American hedge fund. Dom Maklerski Bank Handlowego in association with Excellion Capital collected US$2.7 million in 2010 from Israel. Excellion specialises in cross-border transactions in the UK, Germany, Austria and Israel. Bank Handlowy has been the major adviser for the European Investment Bank, earning US$1.5 million in the studied period. Finally, state-owned PKO Bank Polski advised KGHM (a Polish metal producer) in Canada and Peixin International Group in China in 2013. These transactions explain more than half of the total fees collected from the cross-border trade links in Warsaw. Similar patterns can be observed for Prague, Budapest and Bratislava, although their cross-border trade links are largely shaped by the intra-European subsidiary relations, such as Brussels-based KBC with ČSOB and Patria Group, Deutsche Bank with its direct subsidiaries and Viennese Erste with Česká spořitelna.

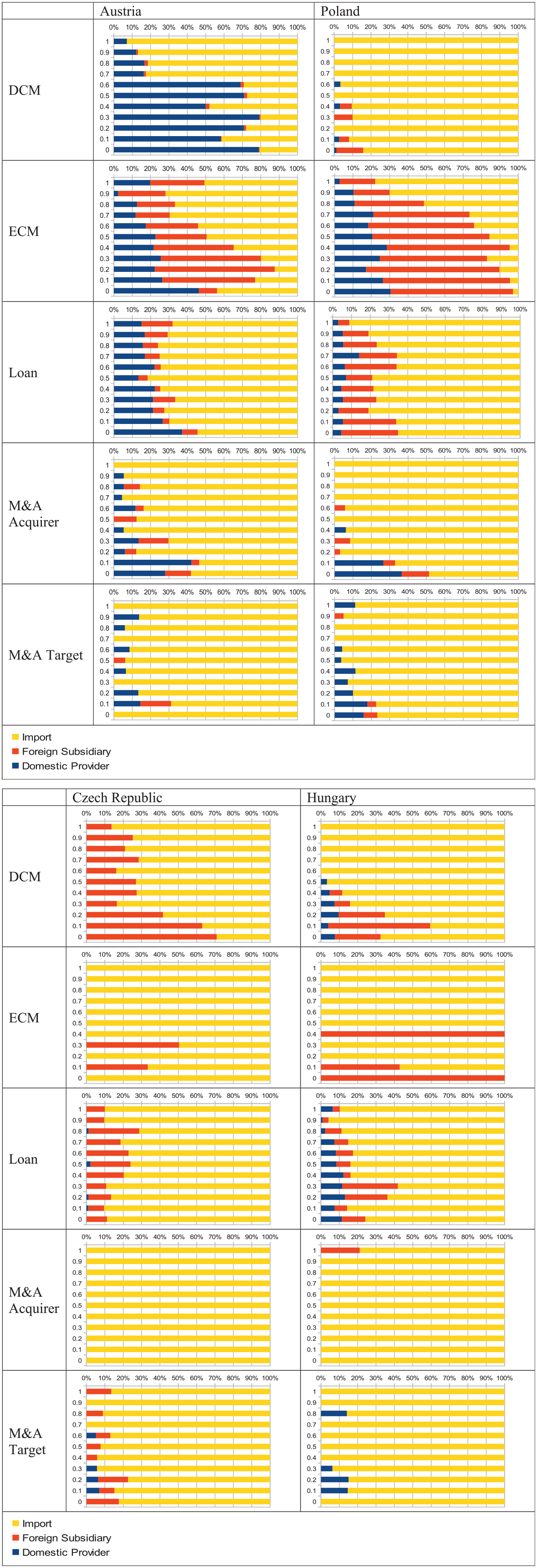

Focusing on the trade links between advisers worldwide and clients in CEE, Figure 2 illustrates how more complex capital market services are more likely to be imported and how the propensity to import varies across the types of services as well as across the countries where clients are located. In particular, debt and equity securities underwriting was less reliant on imports compared with M&A advisory, suggesting different levels of service complexity within this category. Nevertheless, an element of specialisation among the financial centres can be observed. Loans in Hungary showed signs of strong local production, as OTP Bank, MKB Bank and state-owned special purpose financial entities (i.e. Hungarian Development Bank and Hungarian Export-Import Bank) were active in lending. Warsaw hosts the largest stock exchange in the region, 4 and consequently equity securities underwriting is highly concentrated in the capital city. The broker houses of PKO Bank Polski and BOŚ, as well as the online broker house IDM, dominate equity securities underwriting in Poland alongside foreign subsidiaries.

Breakdown of capital market services provision by adviser type.

Figure 2 highlights that particularly smaller financial centres may not be able to provide services for which the domestic demand falls below the minimum threshold necessary to sustain domestic provision of services. In Slovakia, equity underwriting (7 transactions), M&A acquirer advisory (3 transactions) and M&A target advisory (27 transactions) were all imported. M&A advisory has been provided by large foreign investment banks including Lehman Brothers, JP Morgan, Credit Suisse, Citi, Deutsche Bank and HSBC, as well as by management consulting arms of Deloitte and PwC. As these M&A transactions usually involve multiple parties across the region, services were often imported from the advisers’ headquarters in New York (956 trade links, US$2.1 billion) and London (1922 trade links, US$2.2 billion) to acquirers and targets in CEE countries. The need for compliance with EU regulations adds to the demand for more complex and sophisticated services, partly explaining the import behaviours of major international financial centres. The M&A markets in the Czech Republic and Hungary followed similar patterns, with regional firms such as Navigator Capital Group in Warsaw and Wood & Company in Prague being active in the intra-regional transactions alongside foreign subsidiaries such as BRE Bank (Commerzbank) in Warsaw and Patria (KBC) in Prague.

Econometric analysis

Hypothesis 1: Capital market services involving larger transactions are traded across larger market areas.

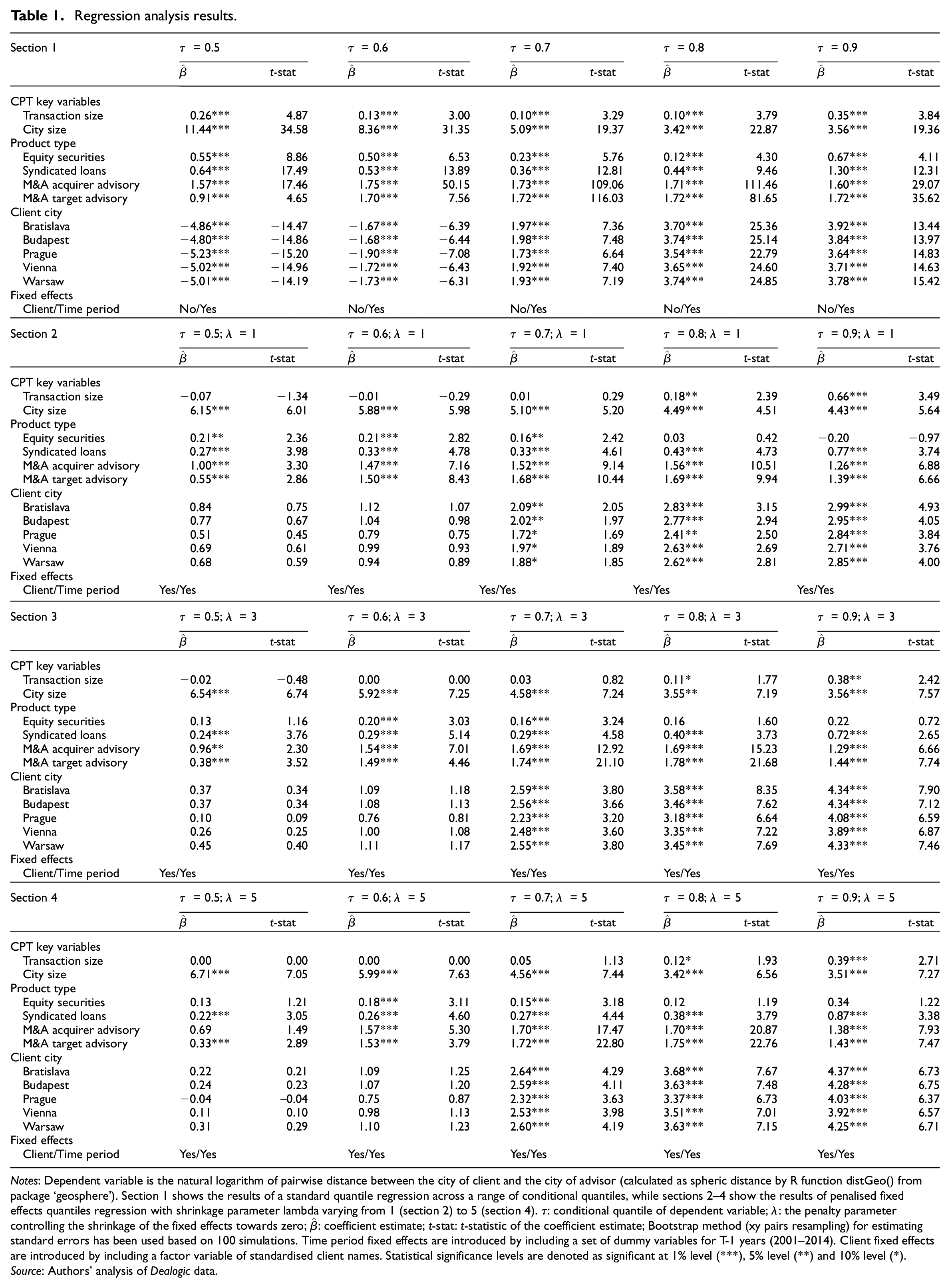

The conditional quantile of the dependent variable (the adviser–client pairwise distance) is represented by τ (tau), and the fixed client effects were penalised by including a factor variable of standardised client names with the shrinkage parameter represented by λ (lambda). 5 Without the shrinking parameter λ (Table 1, section 1), we estimate a 0.26% increase in the median (τ = 0.5) of pairwise distance for every 1 percentile increase in transaction size. The partial correlation is positive and statistically significant throughout the higher conditional quantiles (e.g. a 0.35% increase at τ = 0.9) of pairwise distance. With the client fixed effects introduced (Table 1, sections 2–4), the coefficient estimates at lower conditional quantiles have become smaller in absolute terms and often statistically insignificant. Our coefficient estimates at higher conditional quantiles of geographical distance are, however, consistently statistically significant and positive. For example, we estimate a 0.39% increase in the 90th percentile (τ = 0.9) of pairwise distance for every 1 percentile increase in transaction size using a shrinkage parameter λ = 5. 6 Therefore, even when the unobserved heterogeneity across clients is controlled for using fixed effects, we find a statistically significant and positive relationship between the adviser–client pairwise distance and transaction size. This means that larger transactions are in fact traded over larger market areas, an evidence consistent with hypothesis 1.

Hypothesis 2: More complex capital market services, such as M&A advisory, are traded across larger market areas.

Regression analysis results.

Notes: Dependent variable is the natural logarithm of pairwise distance between the city of client and the city of advisor (calculated as spheric distance by R function distGeo() from package ‘geosphere’). Section 1 shows the results of a standard quantile regression across a range of conditional quantiles, while sections 2–4 show the results of penalised fixed effects quantiles regression with shrinkage parameter lambda varying from 1 (section 2) to 5 (section 4). τ: conditional quantile of dependent variable; λ: the penalty parameter controlling the shrinkage of the fixed effects towards zero;

Source: Authors’ analysis of Dealogic data.

The coefficients for product types are best interpreted in comparison with the base group – bond underwriting in this case. Differences in pairwise distance between different product categories are measured by calculating the difference between their coefficients. The difference between coefficient estimates for bond and equity securities underwriting indicates that the median distance (τ = 0.5) for equity securities was 54.9% higher than bonds ceteris paribus (Table 1, section 1). The differences are 63.8% for syndicated loans, 156.8% for M&A acquirer advisory and 91.2% for M&A target advisory. While the estimates varied, when the shrinkage parameter λ was introduced, the ordering of coefficient estimate was consistent across the service categories. This evidence indicates that the most complex service – M&A advisory – is traded across larger market areas than syndicated loans and equity securities underwriting, which are in turn traded across larger market areas than bond underwriting, which is most localised.

Hypothesis 3: Market areas of financial centres overlap with each other, and consequently clients located in the same area are served by advisers from multiple financial centres, even if their demands do not differ in terms of transaction size and service category.

Christaller’s (1966 [1933]) ‘marketing principle’ model predicts that the city size becomes statistically insignificant when the order of services is controlled for. 7 This is due to the assumed product homogeneity within the respective orders and categories of services. Our results, however, indicate that the coefficient estimates on city size remain positive and statistically significant throughout the conditional quantiles, despite controlling for the order of complexity of services by including transaction size and service category indicator variables. This result implies that market areas of capital market services in fact overlap due to service heterogeneity across different providers and financial centres, evidence consistent with hypothesis 3.

Conclusion

We have analysed the spatial patterns of interurban trade in capital market services by analysing 16,324 trade links involving advisers and clients in Austria, Poland, the Czech Republic, Hungary and Slovakia and their counter-parties worldwide over the period 2000–2014. Our analysis confirms that capital market services of a higher level of complexity are traded across larger market areas. The degree of local production varied from city to city, with Warsaw specialising in equity securities underwriting and Budapest in syndicated loans. With the rise of local enterprises such as PKO Bank Polski in Warsaw, Wood & Company in Prague/Warsaw and OTP Bank in Budapest, the heterogeneity of their business models and specialisations shaped the heterogeneity of financial centres. This heterogeneity in services provided by financial services companies located in different financial centres resulted in overlapping market areas.

These findings are consistent with the key propositions developed by Lösch (1954 [1940]) and Berry (1967) regarding overlaps in market areas as a result of service heterogeneity. The heterogeneity is linked to producers’ profit-maximising behaviours (Eaton and Lipsey, 1982), and the interurban trade patterns in capital market services deepen our understanding of global cities and their external urban relational processes (Sassen, 2001; Taylor et al., 2010). Advisers located in larger financial centres compete with those from smaller centres located nearer to the clients, while advisers from smaller financial centres do not generally export beyond their regional urban system (Esparza and Krmenec, 1996). While Taylor et al. (2010) observe central place ‘thinking’ in global city theory, this study provides empirical evidence on the spatial structure of external urban relations formed through interurban trade in capital market services. In doing so, it confirms the usefulness of CPT models for understanding the spatiality of finance, and demonstrates how such general models of interurban trade can be married with relevant theory that specifically deals with the provision of financial services (Parr and Budd, 2000; Sassen, 2001).

There are several areas for future research. First, the CPT framework could be tested in other types of financial services, including asset management and mortgage markets (cf. Aalbers, 2019). Second, given the limited geographical coverage of this study, it would be interesting to replicate this analysis for other geographical regions or even at a global scale. Third, there is certainly a great deal of scope to develop more refined models of interurban trade as well as to further develop theories that aim to explain patterns of interurban trade. As it stands, we had to combine two theoretical frameworks to support our analysis. In particular, incorporating institutional factors would be helpful in addressing the limitations of CPT in the context of financial services. Firm-specific factors, such as repeated transactions by the same adviser–client pair and corporate ownership links, can be analysed further. It is assumed that foreign subsidiaries (e.g. Société Générale in Prague) facilitated linkages to their parent financial centres. Analyses based on microeconomic data would indicate the influence of such intra-firm and quasi-intra-firm linkages on the spatial reach of financial centres. We hope that future research will build on this contribution.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This work was supported by the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation programme (grant agreement number 681337). The article reflects only the authors’ views and the ERC is not responsible for any use that may be made of the information it contains.