Abstract

Economic action is deeply embedded in social contexts. The patterns of accumulation shape the social inequalities, and these patterns must account for contemporary social structures. Through the lens of the Bourdieusian class analysis – an approach that links social structures with socially defined dispositions and practices – the article demonstrates the importance of class differentiation to understand the process and outcomes of accumulation. The article argues that professional domains are a source of collective subjectivities, and distinctions in financial identities shaped and shared within the professional domains are the structuring element of social structures. For conclusive evidence of distinctions in accumulation behaviours, the dispositions to save and amounts regularly saved are examined within the professional-managerial domain using the British Understanding Society survey (2010–2019), and significant between-group contrasts are identified. By exploring the space of positions, this study contributes to sociological literature on wealth dynamics and Bourdieu-inspired studies towards the economic.

Keywords

Introduction

The issues of wealth inequality and accumulation are gaining prominence (Pfeffer and Waitkus, 2021; Piketty, 2014), and recent literature suggests that the dynamics of financial accumulation calls for conceptualisations in class analytical terms (Waitkus et al., 2024). The new perspectives on the contemporary social structures, informed by the approaches that relate the functional activities in the divisions of labour to shared practices and identities have revealed the distinctive patterns in both lifestyles and the distribution of economic capital in the social space of occupation-based groupings (Flemmen et al., 2018; Savage et al., 2015; Weeden and Grusky, 2005, 2012). Prior literature informed by the Bourdieusian (Bourdieu, 1977, 1984; Bourdieu and Wacquant, 1992) class analysis views accumulation as a long-term process by which individuals or groups gather and consolidate advantages, or the various forms of capital – economic, cultural and social – built upon and transferrable into one another, which act to sustain and reinforce social hierarchies over time (Savage, 2000; Savage et al., 2015). Thus, the ability of individuals and groups to gain economic capital, which can result in social and economic inequalities, is contingent upon a variety of individual resources and dispositions (Savage et al., 2005). This approach to class analysis, grounded in the assumption of an inherent linkage between ‘positions and dispositions’ (Atkinson, 2009, 2015; Flemmen, 2012), opens ways to explore class differentiation using the patterns of accumulation-related behaviours, like saving.

Two decades since The Social Structures of Economy (Bourdieu, 2005), research in social structures and ‘the cultural turn’ in class analysis emphasises that expanding inequalities and accumulation can no longer be fully understood with the conventional analytical categories of ‘big classes’ (Atkinson, 2009, 2017; Flemmen, 2013; Weeden and Grusky, 2005). More granular, occupation-based approaches to categorisation within the social structures, especially in the social space of professional domains, bring focus to socio-cultural collectivities with commonality of individuals’ choices and practices (Weeden and Grusky, 2005, 2012). Such collectivities, based on occupational membership, represent the social contexts that shape and update mental schemas and dispositions and have potential to inform and (re-)shape individuals’ distinctions in financial identities, expressed in the regularities of practices such as managing personal finances, saving and other accumulation-related dispositions and behaviours (Aldridge, 1998; Sparkes, 2019). However, there is limited conclusive evidence of distinctions in financial identities informed by the underlying social structures and a lack of discussion around how such distinctions in the patterns of accumulation-related behaviours can illuminate the divisions within the social space.

While the dynamics of capital accumulation involves a comprehensive study of real assets – such as housing – and financial assets – such as savings, insurance and stocks, as well as the various forms of debt (Dwyer, 2018; Killewald et al., 2017; Spilerman, 2000) – the basic propensity for accumulation and the intention to set money aside for a ‘rainy day’, therefore creating liquid assets, are a useful angle to study class differentiation with regard to financial identities. Recent economic turbulence, including the financial crisis of 2008 and COVID-19, affected the landscape of wealth accumulation and distribution with impacts on interest rates, affordability of housing and household savings (Broome et al., 2024). Yet in the presence or absence of such turbulence, some individuals and households tend to navigate accumulation better than others. For example, the Financial Conduct Authority in the UK shared concerns that ‘millions of people are walking a financial tightrope, with one in 10 UK adults saving no money at all’ (Peachey, 2025). This exposes households to cashflow and income shocks, financial vulnerabilities, and the risks of indebtedness. While the lack of saving ‘habit’ by some groups contributes to exacerbating inequalities, the distinction between savers and non-savers and between more or less active saver groups also helps uncover the underlying social structures based on the distinctions in financial identities. Drawing on the Bourdieusian ‘space of positions’ and focusing on the factions of the ‘service class’ (Atkinson, 2017; Flemmen, 2012), this article explores the following question: How can the analysis of dispositions for accumulation behaviours, grounded in Bourdieu’s theory, illuminate the social structures?

This article pursues a dual ambition. First, it elaborates on the idea that the distinctions in financial behaviours and the patterns of accumulation within the professional-managerial domain resonate with the Bourdieusian (Bourdieu, 1977, 1984; Bourdieu and Wacquant, 1992) principle of capital composition. The article focuses on saving as a representative type of accumulation practices and a structuring dimension capable of revealing the distinctions in financial identities and contributing to understanding the underlying social structures within the ‘service class’.

Second, to examine the extent to which saving dispositions and behaviours can be seen as structuring elements in the social structures, capable of capturing the divisions within the social space, this study seeks conclusive evidence of ‘distinctions’. Using data from the British Understanding Society (2010–2019) survey and employing regression models for panel data this article tests the distinctiveness of professional domains in the dispositions to save and the amounts saved. In particular, this study explores the probability of saving and the amounts saved by individuals while accounting for the effects of income and other relevant characteristics. After partialling out these effects, the post-estimation analysis tests the between-group differences in saving behaviours. Alongside a systematic exploration of the professional and managerial groups, the article finds statistically significant contrasts, or distinctions, in line with the Bourdieusian principle of capital composition. This reinforces accumulation behaviours as an important structuring dimension in class analysis and suggests that financial identities can inform the distinctions within the societal structures.

The article highlights the importance of interconnecting class analysis with finance- and accumulation-related behaviours and makes several contributions to the literature. First, it argues that the principles of differentiation within the professional-managerial domain, or the ‘service class’, are important for illuminating how accumulation behaviours vary across the societal fractions. Second, through the empirical investigation of accumulation dispositions and saving behaviours, the article illustrates the variation in financial identities within the ‘service class’ and provides conclusive evidence of distinctive differences within the social space of professions. Finally, the article proposes that distinctions in financial identities have the capacity to reveal the underlying social structures, with implications for understanding inequality and its within-class dynamics.

Literature Background

Bourdieusian Class Analysis: Social Structures and Practices

Recent approaches to social structures developed in the USA and Europe relate the functional activities in the divisions of labour to shared lifestyles, identities and practices (Flemmen et al., 2017, 2018; Savage et al., 2015; Weeden and Grusky, 2005). Defined by the conditions stemming from the divisions of labour, such groupings – occupations and especially professional clusters characterised by social closure and possession of shared abstract knowledge (Abbott, 1988; Weeden and Grusky, 2005) – illuminate the ‘space of positions’ (Atkinson, 2015; Flemmen, 2012). With reference to Bourdieu, the ‘micro-classes’ approach by Weeden and Grusky (2012) explains homogeneity in behaviours and interests, stating that ‘homogeneous conditions of existence impose homogeneous conditionings and produce homogeneous systems of dispositions capable of generating similar practices’ (Bourdieu, 1984: 101; Weeden and Grusky, 2012: 1728). The micro-classes perspective marked a move away from conventional analytically defined ‘big’ classes towards more specific occupation-based approaches and showed some extent of predictability in lifestyles and practices, including the patterns of economic behaviours, especially within the ‘service class’.

Over the last few decades, the Bourdieusian (Bourdieu, 1977, 1984, 2005; Bourdieu and Wacquant, 1992) approach to social structures, grounded in the conceptualisations of field, habitus and the multiple forms of capital, has gained prominence in sociology. The capital composition principle at the core of this approach explains the correspondence between the space of social positions and the space of lifestyles and dispositions. Prior research employs Bourdieu’s theories, for example, to explain how elites signal their superior position via dispositions and preferences for certain modes of cultural consumption (Friedman and Reeves, 2020). It also illuminates the fragmentation within the social space and the conditions for persistent inequalities. For instance, through the Bourdieusian lens Mears (2020) highlights the scope for gender-based inequalities stemming from leisure domains of the global elite, and Lillie and Maxwell (2023) question the cohesion of the global elite as a group, pointing out subtle differences in their consumption across the national fields.

While effectively linking positions with dispositions (Atkinson, 2015), the Bourdieusian analysis maintains occupation as a central indicator of class position and a basis for class differentiation and distinction. Class differentiation underlying the social structure resides in the idea that the social space is constituted of fields defined by the field-specific composition of capital in its different forms. Bourdieusian fields are ‘arenas of production, circulation, and appropriation of goods, services, knowledge, or status, and competitive positions held by actors in their struggles to accumulate, exchange, and monopolise different kinds of power resources (capitals)’ (Swartz, 2019: 178–179). Explaining sharedness of identity among class members and, thus, a certain degree of homogeneity, habitus – a practice-unifying and practice-generating principle – is the mechanism for internalisation of dispositions from within the socio-cultural collectivities. This principle defines the Bourdieusian objective class as a set of agents characterised by homogenous conditions of existence and systems of dispositions capable of generating similar practices and behaviours (Bourdieu, 1984: 95, 166). The between-occupational differences and within-occupational similarities in dispositions, interests, lifestyles and practices of occupational groups stem from the different combinations of the multiple capital forms – economic, social and the different types of cultural capital – that these occupational groupings possess and display (Atkinson, 2015; Flemmen et al., 2017, 2018; Pavlisa, 2024; Savage et al., 2005). The elaborations of the capital composition principle also involve the specific ‘species’ of cultural capital, such as financial capital, commercial acumen and technical capital, that define agents’ identities (Bourdieu, 2011; Friedman and Laurison, 2019).

‘Professional identities are . . . the most salient of any contemporary class-like identifier’, and the Bourdieusian class analysis envisions the middle-class structural divisions, including professional groupings, as holding different motifs that translate into the differences in lifestyles, practices and behaviours (Savage, 2000: 157). Where professional domains are viewed as fields and socio-cultural collectivities (Noordegraaf and Schinkel, 2011; Pavlisa and Scott, 2023), professional identities – adopted, developed and projected by individuals – reflect possession of capitals prioritised and prized in their (professional) field, alongside displaying the related capabilities, forms of knowledge, cultural representations, practices, lifestyles and internalised dispositions. Such dispositions and behaviours include but are not limited to consumption, saving and other accumulation-related practices.

Accumulation, Financial Identity and Professions

With the growing influence of financialised capitalism, wealth disparities and the evolving ‘regime of accumulation’, scholarship in financialisation of everyday life has established the subjectivity of the saving and investing subjects – individuals and households (Van der Zwan, 2014). However, the space for collective subjectivities remains undeservingly neglected (Langley, 2008). Economic arrangements are deeply embedded in social contexts (Granovetter, 2011), and agents’ financial identities expressed in investing and saving behaviours are partly shaped within socio-cultural collectivities. Such collectivities – often defined by demographic, socio-economic and geographical dimensions – differ in their potential, propensity and disposition to accumulate capital, and the inequality gaps between the social groups widen along these dimensions (Froud et al., 2001). For example, Erturk et al. (2007) problematise the variation in households’ calculative competence in the context of financialisation, bringing keen attention to low-income households.

Individual choices cannot be fully understood without considering the objective social structures (Longhurst and Savage, 1997), and it is plausible to suggest that differences in accumulation behaviours bear correspondence to social structures and elaborate the idea that distinction in financial identities is the structuring element of social structures. Accumulation dispositions are not equally distributed in society but rather are embedded in class divisions (Waitkus et al., 2024), and social class is highly relevant in the context of personal finance and wealth accumulation (Van der Zwan, 2014). However, the focus on the hierarchical advantages for capital accumulation alone is analytically insufficient. The analytical categories of traditional stratificational schemes, or ‘big classes’, hide too much pertinent information about dispositions and practices of specific occupational groups (Atkinson, 2009; Wright, 2015), including the distinctive patterns of accumulation. Furthermore, they cannot disentangle more nuanced underlying mechanisms explaining such distinctions.

The linkage between positions and dispositions enacted by the logic of habitus (Atkinson, 2015) suggests that individuals’ finance practices and dispositions, including of investing and saving, are partly ‘internalised’ from their professional fields and become a part of their financial identity. Management of personal finance requires not only economic, but also cultural capital (Aldridge, 1998). In the context of personal finance, cultural capital encompasses financial literacy and knowledge about and access to commitment devices, such as mass-market financial products and services. Such capabilities are partly acquired through financial socialisation, including that which stems from work-related settings.

While formal education (as part of cultural capital) at the early stages of professionalisation plays an important role, career-oriented individuals – over the course of their socialisation into profession (social capital) – accumulate knowledge, skills or ‘resources’ (Savage et al., 2005) that enable them to change and sophisticate their economic behaviour not only in their professional domains, but also their everyday lives. An individual actor internalises the dispositions of the field (Bourdieu and Wacquant, 1992), including more active accumulation-related practices. For example, Van der Zwan (2014) notes that some professions, such as financial managers, political actors and marketing professionals, possess higher levels of financial capability due to the expectations of their professional roles and daily exposure to cultural representations of finance. The specific kinds of capital and resources contribute to individuals’ potential to accumulate, store and retain advantages (Savage et al., 2005), and the kinds of cultural and social capital prevalent in particular professional fields equip individuals to navigate the complexities of financialised capitalism and develop better strategies for accumulating economic capital.

Capturing ‘Distinction’: Methodology for Empirical Investigation

The empirical investigation of distinction in practices and dispositions, capable of illuminating the structural divisions within the social space of the ‘service class’, calls for mixed epistemology. Scholars note the mixed epistemology of Bourdieu’s own work (Christoforou and Laine, 2014): while remaining philosophically aligned with critical realism and constructivism he ‘borrows’ selectively from positivist methods, for example, using categorical variables in multiple correspondence analyses. Bourdieu’s (1984) Distinction (pp. 127, 519–521) explores the large-scale national surveys of household expenditures by the Institut national de la statistique et des études économiques (INSEE). It examines the observable, measurable facts about between-occupational distinctions in how they spend on food, presentation and cultural items and compares the means of expenditure variables, making generalisations. At the same time, while linking the combinations of capital endowments with the patterns of consumption, Bourdieu never detached such variables from their meanings and context.

While Bourdieu’s approach beneficially links practices, lifestyles and dispositions with the social structures, prior research raised concerns about the extent to which between-class differences reflect social structures given the lack of statistical testing for between-class distinctions in Distinction (Glevarec, 2023). Bourdieu’s reluctance to employ positivist methodology is attributed to its association with the ways of thinking that tend to neglect meaning and richer context as well as Bourdieu’s effort to avoid spurious causal reasoning and the difficulty to anticipate ‘the technical developments in regression analysis that would come after his death’ (Atkinson, 2024: 42). However, contemporary research reliant on Bourdieusian class analysis evidences a growing body of quantitative sociological studies using regression analysis as a standard technique of multivariate analysis in quantitative social science, and acknowledges that the language of a non-positivist interpretation of regression – in terms of regularities, associations and probabilities – is not incompatible with Bourdieu’s own (Atkinson, 2024: 41–43; Campbell et al., 2019; Pavlisa, 2024).

Following and extending the Bourdieusian approach, this article draws on the perspectives on social structures informed by critical realism and the rigorous use of methods, capable of capturing the patterns and regularities in the data. To address the scholarly interest in the statistical significance of between-class differences (Brisson and Bianchi, 2017) that would ‘delineate’, or re-confirm the divisions within the social space, this study seeks conclusive evidence of ‘distinctions’ in the dispositions to save and the levels of individuals’ regular savings. While remaining broadly philosophically aligned with Bourdieu’s approach, this article employs several types of regression for panel data – the techniques previously used for exploring individuals’ and households’ saving behaviours (Brown and Taylor, 2016; Guariglia, 2001). Regression models capture the association between saving behaviours and a variety of other factors, including education, income, age, gender, occupation and other characteristics. The post-estimation analyses based on such models also allow for estimating the statistical significance of between-group contrasts, effectively informing the statistical significance of ‘distinctions’ between the groups.

The study sees a professional grouping in the model not as merely an exogenous impact of changing the occupation or a control variable, but rather a sociological theory-informed influence associated with the rich social environment imbued with its members’ dispositions, priorities and strategies of building resources – an interpretation that opens up possibilities for comparative analyses between professional environments and allows for establishing conclusive evidence about between-group differences.

Expectations on ‘Distinctions’: Hypotheses Formulation

Propensities to accumulate economic assets may differ across occupational groups, even controlling for earnings, and sociological literature helps to identify groups with potentially distinctive occupational identities within the professional-managerial category. Professional fields shape individuals’ knowledge, dispositions and everyday practices as the professional ethos guides and informs the development of field-specific knowledge, shared understandings, values and priorities of the field (Friedman and Laurison, 2019).

Professionalisation processes including education, vocational training and on-the-job socialisation create idiosyncratic influences that instil a certain degree of homogeneity among members of specific occupational groups (DiMaggio and Powell, 1983). For example, the systems of dispositions (habitus) of teaching professions are seen as more strongly orientated towards humanitarian goals than materialistic and accumulation goals, in contrast to business and management roles, which are primarily guided by commercial logics (Lamont, 1992), a calculation motive and more pronounced on-the-job financial socialisation. Similarly, the pursuit of creative potential and cultural capital dominates the field of creative professions, in contrast to the financial accumulation orientation that characterises business professions. We hypothesise that professionals whose field prizes financial capability demonstrate more active accumulation behaviour than professions that do not demand substantial financial capability:

H1: Creative professionals save less than business professionals.

H2: Education professionals save less than business professionals.

The choices and dispositions of the relatively heterogeneous groups of managers are also embedded in diverse social environments. For example, while the amount of work and remuneration can be comparable between a manager in a financial institution and a manager in retail or logistics, in the former context the issues of organisational and client finance are regularly discussed, and management of finance is a common topic of conversation. Members of such environments likely have finance-related backgrounds, with potential spillovers of finance-related conversations to the personal level. A manager in a less finance-focused industry is not only less exposed to financial representations but also less likely to engage in discussions on financial issues with colleagues from diverse backgrounds, whether in formal or informal settings.

While managers are a heterogeneous group of occupations, classifications have seen sub-divisions. One analytical division within the managerial group is outlined in the National Statistics Socio-Economic Classification (NS-SEC) as it distinguishes between the higher and lower managerial occupations, accounting for economic and cultural capital, differences in entry requirements of the occupational position, social trajectory and the size of organisation. For example, financial managers are more likely to be allocated to the higher managerial group, while managers in retail, wholesale, restaurant, hospitality, transportation and distribution are allocated to the lower managerial group (Office for National Statistics, 2005). Similarly, Leggatt (1980) divides managers by industry status based on the general social trajectory and prestige the industry entails. Managers in higher-status industries, such as banking and finance, oil and chemical manufacturing, and construction, are distinguished from those in lower-status industries, exemplified by the distribution and transportation sectors. The study of the Cambridge Social Interaction and Stratification (CAMSIS) shows that managers in manufacturing, construction and business services enjoy higher occupational prestige than managers in hospitality or distribution sectors (see Supplement Table S6), which supports the divide within the managerial category. Also, International Standard Classification of Occupations (ISCO88) sub-divides managerial occupations into corporate and general managers. The variation in social trajectories and industry prestige differentiates the socio-cultural influences of working environments where financial socialisation occurs and thus may create more advanced financial identities due to the embeddedness of the managerial roles within these environments.

H3: Corporate managers save more than general managers.

The between-occupational contrasts are expected to remain after the differences in income and other relevant characteristics are accounted for. A granular exploration of occupational categories is expected to identify groups prone to more or less active saving behaviours.

Data and Methodology

Data

The study uses data from waves 2, 4, 6, 8 and 10 of the Understanding Society survey (2010–2019) as these waves include questions about saving behaviour that can be used for generating the dependent variables. Understanding Society is an initiative funded by the UK’s Economic and Social Research Council and various government departments, with scientific leadership by the University of Essex, Institute for Social and Economic Research (2020), and survey delivery by NatCen Social Research and Kantar Public. The survey started in 2009, expanding the British Household Panel Survey (BHPS) in terms of sample size and the range of questions. It collects data from approximately 40,000 households annually.

With the overall low household savings in the UK, household savings tend to sharply rise during recessions (Broome et al., 2024). Using the time period between the financial crisis of 2008 and the start of COVID-19 allows partialling out the disruptions in accumulation behaviours when exploring the between-class distinctions.

Owing to missing values of the key variables used for regression models, the sample was restricted (please see sample restrictions and summary statistics in Supplement Tables S1–S3, S7). Further to sample restrictions, an unbalanced panel of data with 95,635 observations is obtained consisting of 37,675 individuals, observed 2.5 times on average across the fives waves of the survey, with 15% of individuals appearing in all five waves and 35% appearing only once. The benefits of using panel data rather than cross-sectional data include addressing the omitted variable bias caused by unobserved heterogeneity and increasing sample size – due to missing values, using several waves captures a larger number of unique observations. Finally, panel data accounts for change over time, which enhances the efficiency of estimates (Wooldridge, 2013).

The survey uses the following questions to capture saving behaviour: ‘Do you save any amount of your income, for example, by putting something away now and then in a bank, building society or Post Office account, other than to meet regular bills? Please include share purchase schemes and ISAs.’ Where the answer was positive, the second question was asked: ‘About how much on average do you personally manage to save a month?’ Responses to these questions provide values for generating the dependent variables.

Bourdieu’s (1984: 503) principle in exploring class fractions proposes to obtain samples ‘large enough to make it possible to analyse variation in practices . . . in relation to sufficiently homogeneous social units’. Distinction, the text at the core of the Bourdieusian class analysis, examines narrow professional groups – teachers, engineers, commercial employers – largely following the original French INSEE survey design in terms of occupational aggregates. Similarly, this article uses the available occupational variable of the Understanding Society survey – the occupational codes of the ISCO88. Interested in the systematic exploration of between-occupational contrasts in the professional-managerial group of occupations, the two- and three-digit occupational codes are employed (see Supplement Table S5) to create relatively homogeneous professional groups while maintaining sufficiently large sub-samples for modelling purposes.

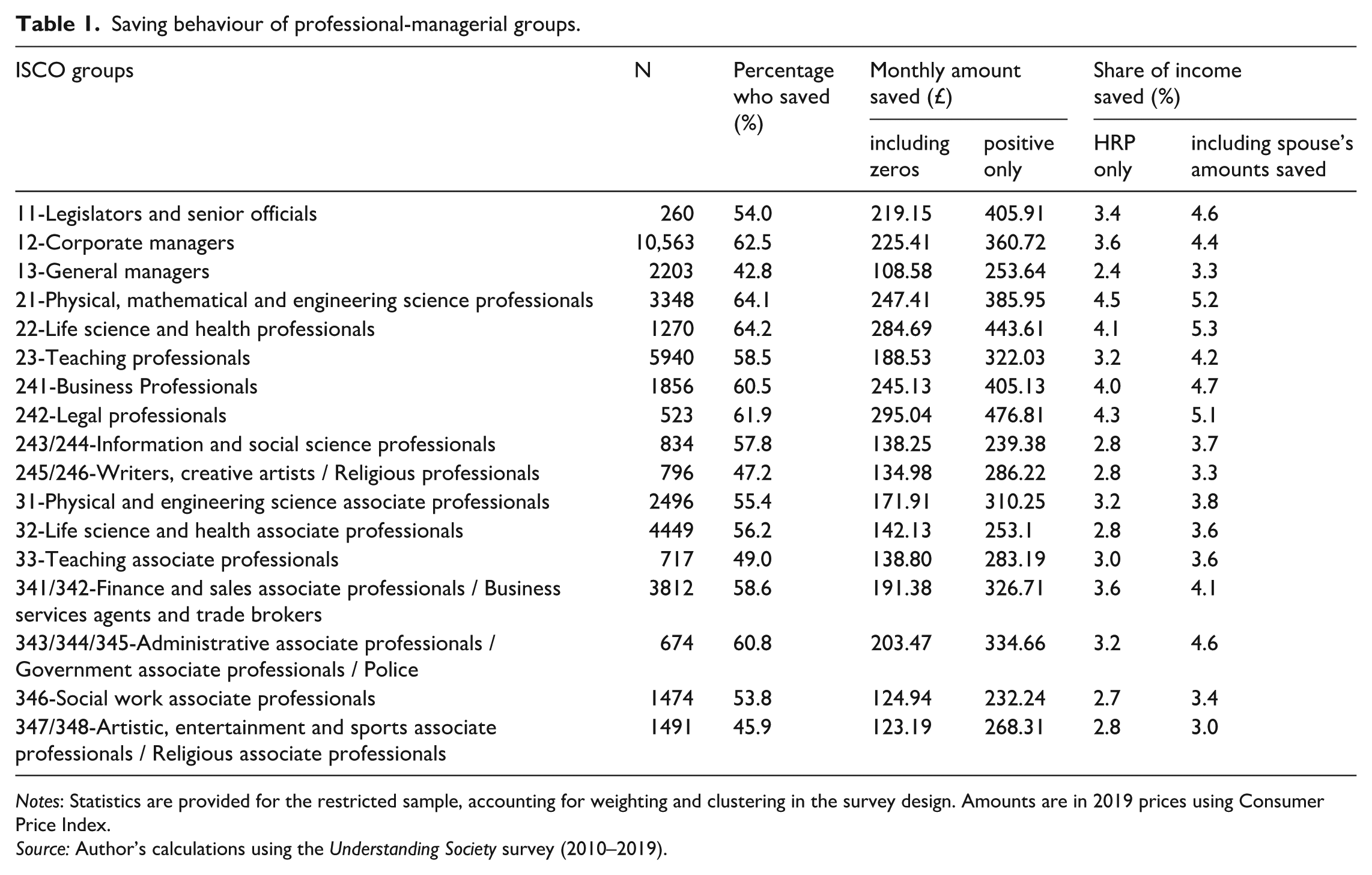

Table 1 shows the occupational codes and summarises the dependent variables for corporate managers and general managers, exact sciences professionals, teaching professionals, business professionals, legal and informational professionals, and those in creative professions. For modelling, professionals and professional associates within the same professional domain are grouped together. The preliminary exploration of managerial, professional and associate professional groups shows substantial differences in their saving behaviours. General managers and representatives of creative professions save significantly lower proportions of income than other professional-managerial categories and have a lower percentage of savers.

Saving behaviour of professional-managerial groups.

Notes: Statistics are provided for the restricted sample, accounting for weighting and clustering in the survey design. Amounts are in 2019 prices using Consumer Price Index.

Source: Author’s calculations using the Understanding Society survey (2010–2019).

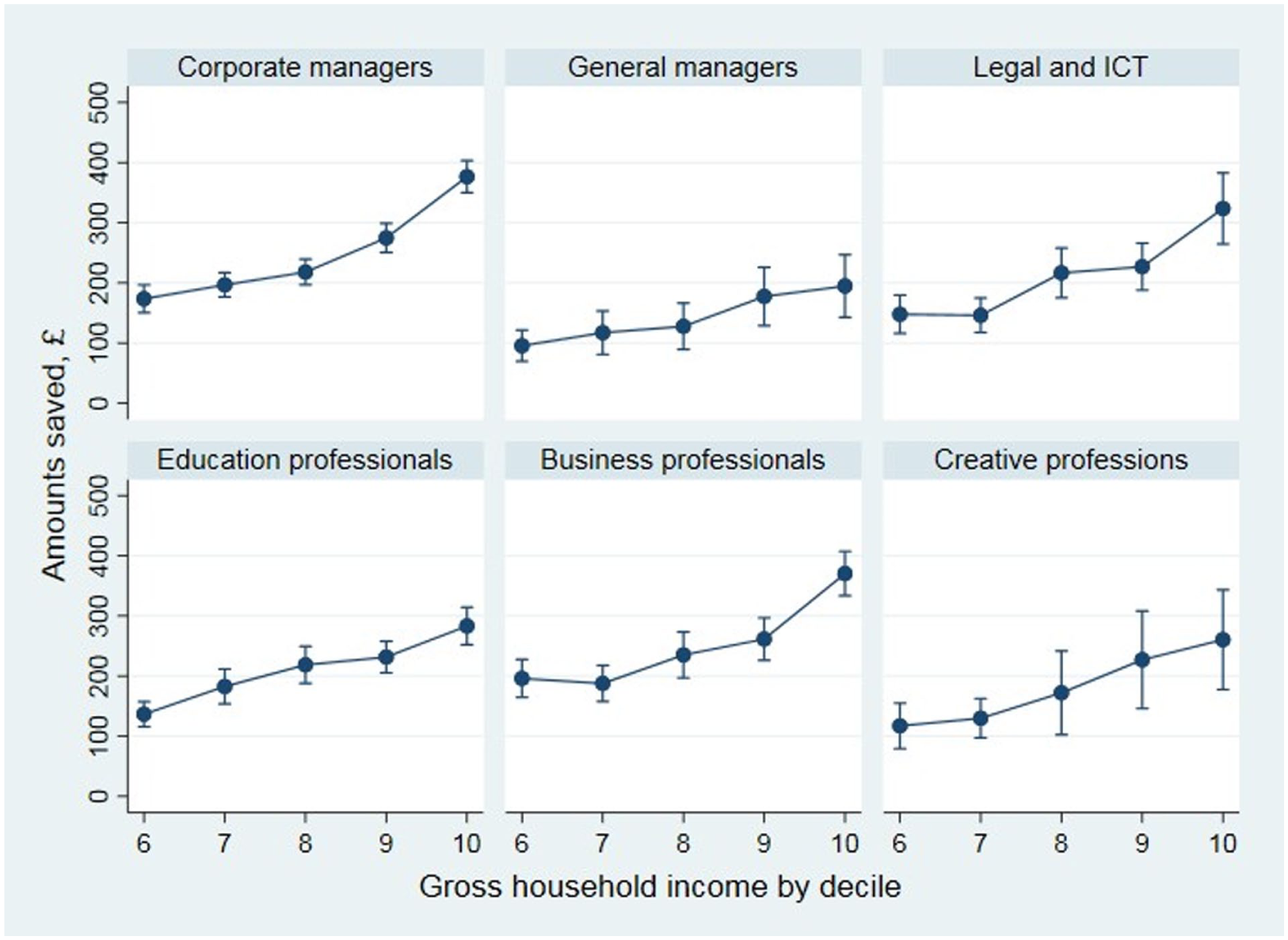

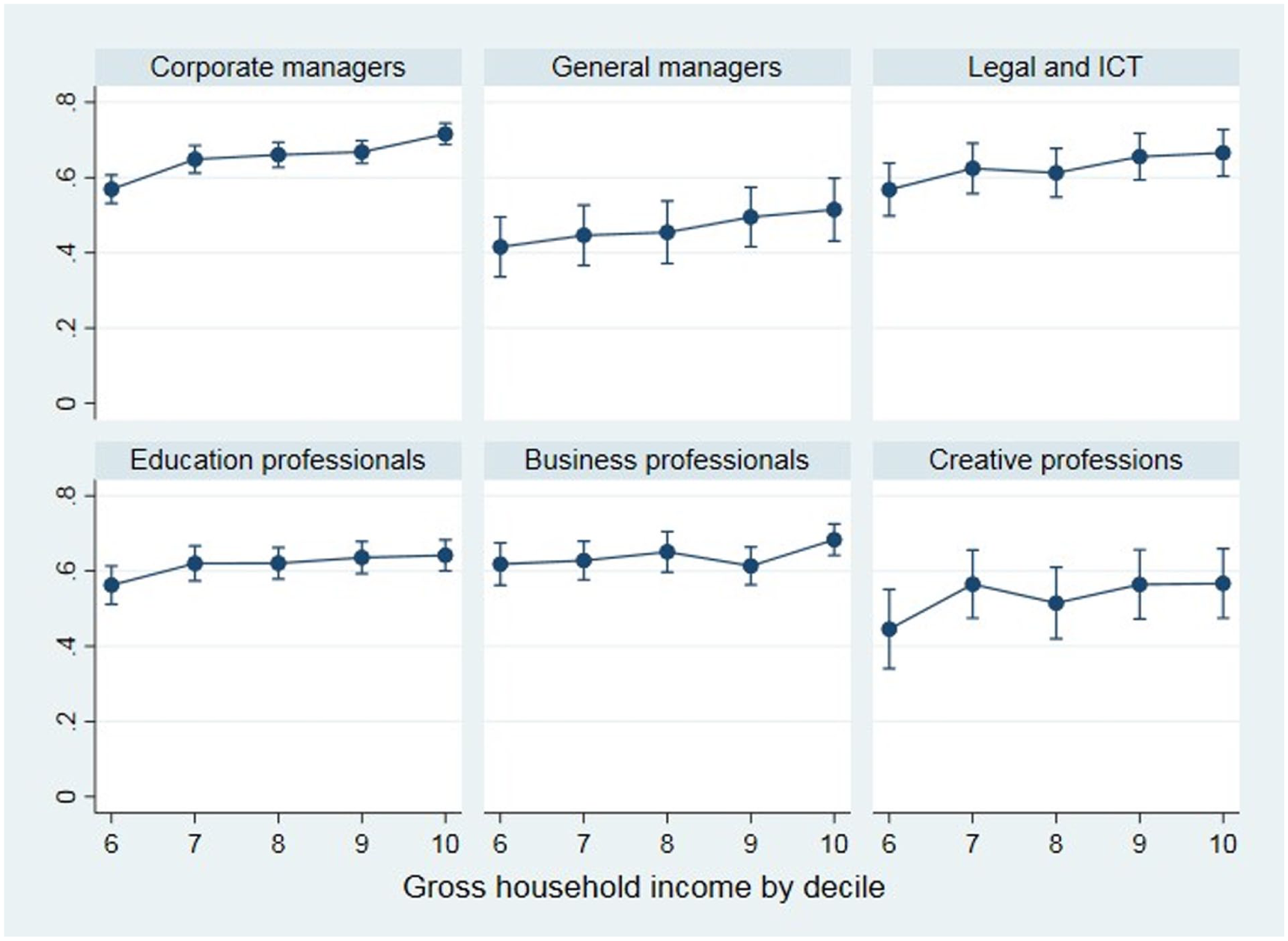

Admittedly, the average incomes may differ among professional-managerial groups and, therefore, the level of individual savings (Figure 1), and the share of income saved by the household reference person (HRP) jointly with their spouse (Figure 2), are explored by occupational group and income decile, focusing on the upper half of the distribution where most of the ‘service class’ belongs (details in Supplement Table S8), to account for the ‘affordability’ of savings.

Amounts saved by individuals, by professional group and income decile (£).

Share of income saved jointly by HRP and spouse, by professional group and income decile (%).

While education professionals fall behind business professionals in the propensity to save, both the least and most wealthy individuals in this occupational group lag in terms of the average amounts and share of income saved. The between-occupational differences in the probability of saving, amounts saved and savings ratios in the summary statistics suggest considerable variation. Yet modelling and the post-estimation analysis of contrasts are expected to provide conclusive evidence.

Analytical Approach

To estimate the between-occupational contrasts, models of saving behaviour are built for the following dependent variables: the propensity to save, the amounts saved by individuals, and the log-transformed values of shares of income saved by HRP and their spouse. The dependent variables are modelled using a correlated random effects (CRE) framework (Wooldridge, 2013), which controls for unobserved heterogeneity and overcomes the limitations of the traditional random- and fixed-effects models for panel data. For example, if we assume that there are unobserved characteristics related to wealth or some occupation-related gains, which potentially impact on how differently people save, these characteristics are typically included in the error term of the regression. The CRE model controls for such unobserved characteristics by explicitly including the averages of time-varying variables in the model (see the Supplement for a detailed model justification). Post-estimation analysis for savings-related outcomes is employed to examine the magnitude and significance of pairwise contrasts between the occupational margins.

The probability of saving is modelled as a function of observable variables and unobserved heterogeneity using the CRE probit panel regression model:

where

As part of post-estimation analysis, the magnitude and significance of pairwise contrasts between occupational margins

Monthly amounts and the share of income saved jointly by an individual (HRP) and their spouse (when applicable) are also modelled with correlated random effects regression models (please see the model specifications in the Supplement).

Results

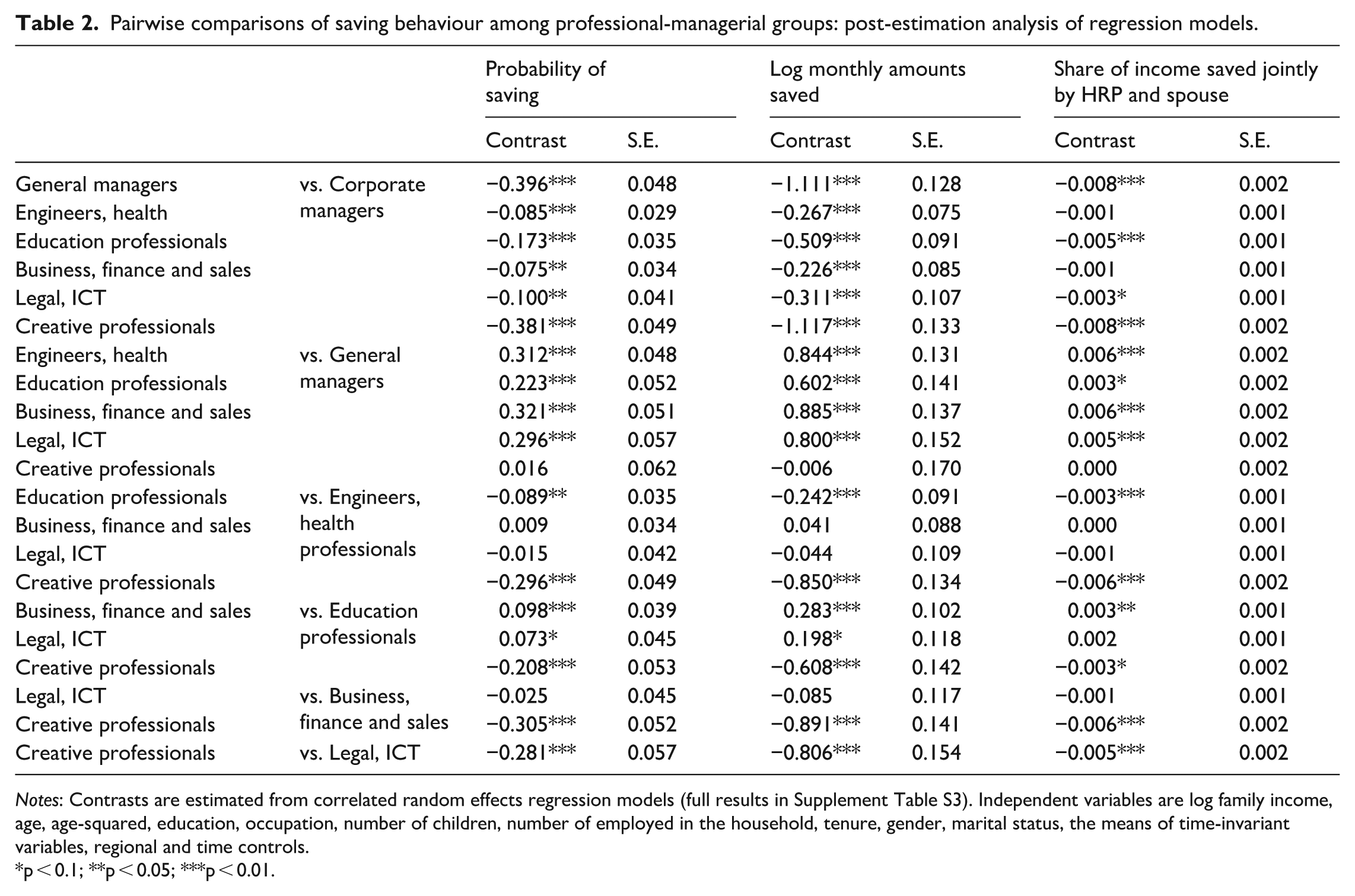

Regression results show the significant effect of income, positive effect of education and the non-linear effect of age, as well as substantial differences in the probability of saving among the professional-managerial group (full regression results are available in the Online Supplement Table S4). Pairwise comparisons show that – accounting for the differences in income and other characteristics – business, finance and sales professions are 10 percentage points (ppt) more likely to save compared with education professionals and 31 ppt more likely to save than creative professionals (Table 2); there is a statistically significant difference of 40 ppt in the probability of saving between corporate and general managers.

Pairwise comparisons of saving behaviour among professional-managerial groups: post-estimation analysis of regression models.

Notes: Contrasts are estimated from correlated random effects regression models (full results in Supplement Table S3). Independent variables are log family income, age, age-squared, education, occupation, number of children, number of employed in the household, tenure, gender, marital status, the means of time-invariant variables, regional and time controls.

p < 0.1; **p < 0.05; ***p < 0.01.

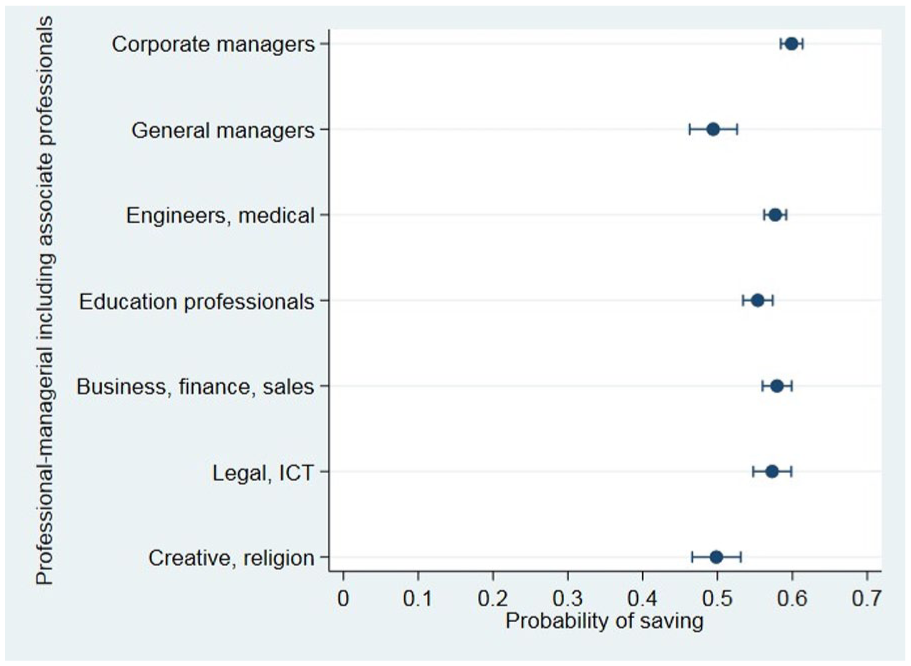

The predictive margins for the professional-managerial groups (Figure 3) illustrate the magnitude and significance of contrasts between professions. The ‘dots’ represent the average predicted values, and the ‘whiskers’ represent the 95% confidence intervals. When there is no overlap in 95% confidence intervals between the groups, the professional groups are statistically significantly different in saving propensities. For example, for creative professions with their predicted average probability of saving of 50%, the 95% confidence interval has no overlap with the 95% confidence interval for business, finance and sales professionals, with their predicted propensity to save of nearly 60%.

Predictive margins of professional-managerial groups in the propensity to save.

In terms of the amounts saved, in support of hypotheses 1–3, business, finance and sales professionals save 89 ppt and 28 ppt more than creative professionals (H1) and educational professionals (H2), respectively (at p < 0.05). The group defined as corporate managers saves more than twice as much as general managers in terms of average monthly amounts saved individually (H3) (Table 2).

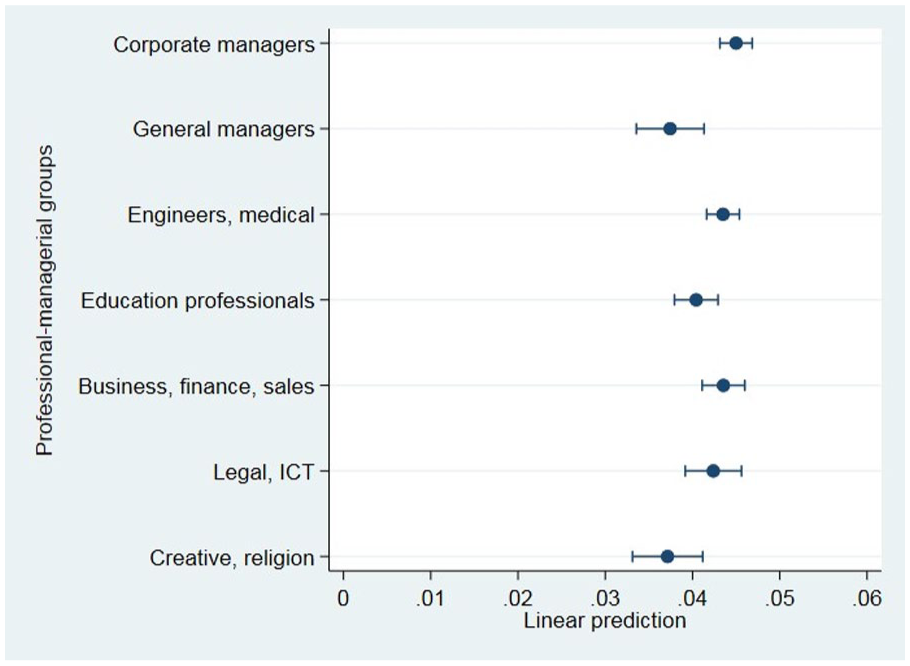

Similarly, the between-occupational contrasts in the shares of income saved jointly by a professional and their spouse (Figure 4 and Table 2) show that, while some groups are more heterogeneous than others, corporate managers and business professionals demonstrate relatively low dispersion and higher levels of savings compared with distinctively under-saving groups like general managers and creative and education professionals. A difference of 0.8% in the share of income saved between corporate and general managers is a difference between the predicted margins of 4.5% and 3.7%, respectively. Business, finance and sales professionals on average exceed creative professionals and education professionals by 0.6% and 0.3%, respectively in the share of income saved, and these three professional groups’ predicted share of income saved is 4.3%, 4.0% and 3.7%, respectively – a substantial difference given that the sample average is 3.4%.

Predictive margins of professional-managerial groups for the share of income saved by the head of household jointly with spouse.

The sensitivity analyses address the issues of the ‘affordability’ of savings. Some professions on average earn more than others; for example, business professionals on average earn more than teachers and, as a group, can afford to save more. On the other hand, alongside early-career banking specialists in the former group the sample also covers late-career university professors and headteachers, thus, offering variability of income within the occupational groups and ensuring between-group comparability. By controlling for income differences the analyses compare like with like and the baseline CRE regression omits observations at the top 1% of household income distribution. The issue of affordability is further investigated as the top 2%, 3%, 4% and 5% of income-earners are removed from the sample. The sensitivity analyses also control for the impact of pension scheme membership. The methodology, results and full interpretation for the sensitivity analyses are provided in the Online Supplement.

Statistically significant differences between the professional groups, captured both through the probability of saving and the amounts saved (individually or jointly with spouse), suggest substantial distinctions in their financial identities in terms of disposition to accumulate economic capital.

Concluding Discussion

In light of the major shifts in the organisation of economy and society, including the turn to cultural economy, the proclaimed ‘end of class’ and wider social transformation (Savage, 2000; Tonkiss, 2006), Bourdieu’s work on social structures remains a key sociological intervention on economic issues. While the conventional concept of class highlights the hierarchical advantages in capital accumulation and remains a valid vantage point to analyse the differentials of power generic to capitalism, modern social structures imply more differentiation (Flemmen, 2012, 2013). Bourdieusian class analysis beneficially brings the focus to meaningful theory-informed differentiation within the ‘service class’, with professional identities remaining the most salient contemporary class-related identifiers (Savage, 2000). It reveals the fragmentation of the social space, where collective subjectivities are shaped and influence individuals’ practices, and it allows for conceptualising professional groups as structural divisions carrying different motifs, which translate into between-group distinctions in dispositions and behaviours, including accumulation behaviours and practices of financialisation.

The article highlights the relevance and value of the capital composition principle for professional clustering, in the context of the financialisation of the everyday. By viewing professional domains as fields signified by the prioritised compositions of the multiple forms of capital, the principle assumes a certain degree of within-domain homogeneity in economic action – consumption and saving (Atkinson, 2017; Savage et al., 2015). Even at comparable income levels, the factions of the ‘service class’ inhabit the social spaces with different sets of competencies, shared dispositions and social influences, including financial socialisation.

The article argues that the acquired dispositions – through internalising the collective subjectivities from professional environments – play a significant role for accumulation-related behaviours. Some groups, such as business, finance and sales professions, by virtue of their positions in the occupational structures and finance-related socialisation and education, are better equipped for accumulation. This advantage is enhanced through representations of finance that permeate their occupational fields, through symbols and discourses (Van der Zwan, 2014).

Accumulation dispositions and behaviours are part of financial identity, and this study offers novel insights about the social structures – the disparities in the collective subjectivities related to accumulation behaviours within the ‘service class’. Prior literature emphasises the high yet under-exploited potential of Bourdieu’s work to provide a foundational rethinking of class and stratification (Flemmen, 2013). This article argues that, alongside lifestyles, practices and consumption patterns (Atkinson, 2015; Weeden and Grusky, 2005, 2012), distinctions in financial identity shaped and shared within professional domains represent a structuring dimension of social structures. While Bourdieu’s (1984) class analysis reveals social structures using the structures of consumption, this article emphasises that these structures can also be understood through the lens of accumulation-related practices.

A systematic exploration of differentiation within the ‘service class’, developed in this article, offers an overview of the existing patterns of distinction in accumulation-related behaviours. Acknowledging the critiques of Bourdieu’s methodology and the interest in formal statistical testing of between-group distinctions (Brisson and Bianchi, 2017; Glevarec, 2023), this study tests the statistical significance of between-group contrasts in saving behaviours within the ‘service class’. The conclusive evidence of the between-group contrasts in the dispositions to save and the rate of accumulation reveals the magnitude of ‘distinction’. The analyses of this article reinforce that, first, Bourdieusian class analysis is a relevant and valuable analytical lens in the context of accumulation and practices of financialisation. Second, the distinctions in financial identities act to ‘delineate’ the social space of professions, and such distinctions can be beneficially operationalised as a structuring dimension in understanding social structures.

Based on the theoretical argument and empirical investigation, the implications of this article are twofold. First, while this study illustrates the differentiation within the ‘service class’ and the magnitude of disparities in accumulation behaviours, the real action of mitigating the gaps and addressing the expanding inequalities resides in the distribution of financial education (Weiss, 2020). Piketty’s (2014) Capital in the Twenty-First Century shows the widening gap in wealth, and his solution for reducing inequalities is to invest in education. Higher educational settings are the context of early professionalisation, and educators bear the transformative potential to ‘re-write’ the habitus by instilling the systems of accumulation-related dispositions, behaviours and attitudes. Expanding financial education initiatives that shape financial identity across disciplines will add economic and social value by enhancing graduates’ long-term financial well-being.

Second, there are implications for further research to enhance the understandings of social structures and the expanding gaps between and within the social strata. There is substantial scope for research into accumulation strategies and explorations of how financial identities are shaped within particularised occupations and professional domains. Professional membership, to some extent, is a ‘catch-all’ concept, and further research around ‘unpacking’ the effect of professional fields is needed. For example, for some – especially those whose parents socialise them into a business profession – professionalisation starts as early as childhood, and their parents can be part of the professional environment as mentors in financial and other behaviours. The mechanism of internalising dispositions, alongside the capital composition principle, are key for the analysis of accumulation behaviours and expanding inequalities, and more nuanced understandings of professional fields would enhance insights into accumulation behaviours.

Further research into wealth inequality and accumulation would benefit from adopting the lens of the Bourdieusian class analysis (Waitkus et al., 2024) alongside empirical explorations of investing behaviours (e.g. stocks, real estate), especially among the wealthier social strata, as well as the patterns of credit and debt. Given the importance of country-specific narratives on inequality (Pfeffer and Waitkus, 2021; Piketty and Saez, 2014), there is scope for further comparative research. While the perspective of different interests and strategies in everyday practices, inspired by Bourdieu, suggests occupation as an important analytical dimension, the forms of saving discipline pertinent to national contexts, the variation in the structural saving propensity for economies with different occupational compositions and the variation in accumulation opportunities across the professional circles in different countries add another layer of complexity.

Named as a key critical sociological intervention on economic issues (Tonkiss, 2006), Bourdieu’s (1977, 1984, 2005) thought-provoking work on the economics of practices emphasised the importance of social structures for the superior analysis of economic action and accumulation. This article echoes the view that the studies of ‘economic’ – including wealth and accumulation – cannot be left to economics alone, and the Bourdieusian class analysis and class-based collective subjectivities are valuable perspectives for the comprehensive analysis of accumulation (Waitkus et al., 2024) that paves the way to new – sociological – narratives about growing wealth disparities and inequality.

Supplemental Material

sj-docx-1-soc-10.1177_00380385251388702 – Supplemental material for The Structures of Accumulation, Financial Identity and Saving: Exploring the Social Space of Professions

Supplemental material, sj-docx-1-soc-10.1177_00380385251388702 for The Structures of Accumulation, Financial Identity and Saving: Exploring the Social Space of Professions by Karina Pavlisa in Sociology

Footnotes

Acknowledgements

I am grateful to the participants of the Annual Conference of the British Sociological Association 2025 for valuable feedback and comments. This work takes inspiration from my PhD thesis, and I am deeply indebted to my former PhD supervisor, Professor Peter M. Scott, for his advice and support. I also would like to thank Chris Brooks, Davide Castellani, Peder Greve, William S Harvey and Peter Miskell for valuable comments. I am also grateful to Mark Casson and Leslie Sklair for inspiring discussions. A special thank you to mentors of the Mentoring Events at the Royal Economic Society and particularly Alessandra Guariglia for her advice in relation to econometric methodology.

Data Availability Statement

The data that support the findings of this study are available from the UK Data Service. Restrictions apply to the data availability. Data are available at: http://doi.org/10.5255/UKDA-SN-6614-14 with the permission the UK Data Service.

Funding

The author received no financial support for the research, authorship and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.