Abstract

With the severity of global climate change becoming increasingly evident, the shift to renewable energy has become the key to achieving sustainable development. Using data from the prefecture level in China, we construct a comprehensive FinTech index from the institutional and individual levels using the entropy method, aiming to capture the multi-dimensional value of FinTech comprehensively. This paper quantifies the momentum that FinTech provides to the urban renewable energy transition. Our investigation shows that FinTech can play a crucial role in enhancing urban renewable energy transition, especially in cities with strict environmental policies, relatively developed economies, and eastern and midland cities. This study further reveals the impact path of FinTech-driven urban renewable energy transformation, and we find that the key path is to curb capital misallocation, strengthen public environmental attention, and improve green innovation. These results expand the research perspective of renewable energy transition and provide a path choice for China to realize renewable energy transition under the dual-carbon goal.

Introduction

Global climate change has profound environmental and socio-economic impacts, and it has become the consensus to adjust the energy structure and reduce greenhouse gas emissions. Promoting the transition to renewable energy is an important way to reach this target, and the Chinese government has proposed a “Dual carbon” goal, and it published the White Book “China's Energy Development in the New Era,” which indicates that the productivity of utilizing renewable energy sources should be prioritized. The renewable energy transition (RET) would not only help alleviate environmental pollution 1 but also have a positive impact on economic and technological progress. 2 Meanwhile, as centers of economic activity and population concentration, cities are major sources of energy consumption and carbon emissions and significantly contribute to the implementation of energy transition policies. 3 Therefore, how to build a breakthrough path drawing a strategic picture of RET needs to be addressed urgently.

The RET is imminent and its potential channels have become a hot topic in academic research. Most existing literature has analyzed the impact of RET from the perspective of energy security, 4 market mechanism, 5 and environmental policy. 6 However, it ignores the impact of the emerging dimension of FinTech on renewable energy. FinTech has promoted the construction of a new production function in the financial industry, bringing a new paradigm of information technology to promote financial innovation. 7–10 With the help of big data analytics and artificial intelligence technology, FinTech platforms can more accurately assess the risks and returns of investment projects, which can promote the tilting of capital towards renewable energy projects with high-efficiency potential, 11 thus affecting urban RET. However, few studies have linked FinTech to the urban RET. Therefore, one of the motivations is to expand the impact of urban RET from a FinTech perspective.

Furthermore, determining how FinTech affects the urban RET not only provides solid support for building a low-carbon system but also helps to achieve economic benefits. First, the application of FinTech has significantly improved the liquidity and utilization efficiency of funds through intelligent algorithms and automated processes, thus accelerating the capital cycle of renewable energy projects. 12 Second, advances in FinTech have promoted innovation in green financial products, such as green bonds and green funds, opening up diversified financing pathways for urban renewable energy projects. Finally, FinTech also provides financial support for technological development in renewable energy and accelerates the transformation process of new technologies from the laboratory to the market. 13 Beyond its direct effects, FinTech can also facilitate the urban RET by mitigating capital misallocation, raising public environmental awareness, and improving green innovation, which is also one of the important motivations.

Therefore, this paper firstly constructs the FinTech development index at the prefecture level, using the entropy value method to construct the index from the institutional and individual levels. Secondly, this paper examines the impact of FinTech on urban RET and its mechanism using a static panel model. The results show that FinTech can drive urban RET, and reducing capital mismatching, enhancing public environmental awareness, and promoting green innovation are important impact channels for FinTech to promote urban RET. Finally, this paper also conducts a group regression, such as the intensity of regional environmental regulation and the level of economic development, to capture the heterogeneous effect of FinTech in driving the urban RET, and we find that cities with stringent environmental regulation and a developed economy have a greater promoting effect.

The marginal contributions of this paper are as follows: First, in the index construction, this paper captures the multi-dimensional characteristics of FinTech from institutional and individual ways and constructs a comprehensive index based on the number of regional FinTech companies collected by the “Tianyan Cha” platform and the Peking University Financial Inclusion Index, aiming to overcome the narrow scope and inherent one-dimensional limitations of the existing FinTech measurement. Thus, the multi-dimensional FinTech can be more comprehensively and deeply captured. Second, we integrate FinTech and urban RET into a unified framework, analyze the driving role of FinTech, and explore the breakthrough way of urban RET under the dual-carbon goal. Unlike previous literature that explores the impact on RET from the perspectives of climate policies 14 and Digital finance.15–17 Third, we also construct the impact mechanism of FinTech on urban RET and reveal the impact path from three aspects: capital misallocation, public environmental awareness, and green innovation, and attempt to provide a new perspective for FinTech to promote the conduction path of RET in cities.

Literature review

Regarding the measurement of FinTech indicators, the existing literature usually uses three methods to measure it. The first method uses objective proxy variables, such as calculating the share of domestic credit in the GDP of the banking industry 18 to measure FinTech development. However, due to the lack of data on FinTech loans, the scope of this method is relatively narrow, which leads to an inaccurate measurement. The second method is to use the Peking University Digital Financial Inclusion Index as a proxy variable to measure the development of FinTech. 19 However, using this index to evaluate FinTech cannot fully capture the characteristics because the Peking University Digital Financial Inclusion Index only focuses on individual users and cannot reflect the dimensions of financial institutions and enterprises. The third type of method is the sentiment index, which is constructed by the popularity of Internet searches. For example, the text mining method is adopted to conduct data mining and structured data transformation on the word frequency of keywords in Baidu News, and the FinTech index is finally synthesized.20,21 The measurement of FinTech development level by keyword table may limit the inaccuracy due to subjectivity. 22

The high degree of global technology and industry integration has greatly accelerated the financial industry's digital transformation and disrupted how traditional finance is delivered, thus significantly enhancing the supporting role of financial services for economic development. The existing literature has made a lot of discussion on the economic effects of FinTech, but no consensus has been reached. Some scholars find that FinTech can bring positive economic effects, while others believe that the risks and challenges that FinTech may bring should not be ignored. From a positive perspective, FinTech has great potential to reduce capital mismatch, 23 improve the availability of corporate financing,24,25 and empower enterprises to innovate green,15–17 to coordinate and promote sustainable social and economic development. However, given that the technology and regulatory regulations are not yet fully mature, FinTech may present problems such as triggering turbulence in financial markets, 26 exacerbating digital divide issues, 27 and affecting their liquidity and credit supply. This in turn may adversely affect economic growth. 28

As for the research on urban RET measurement and influencing factors, the existing research is limited by the availability of data, most of the research focuses on the national and provincial levels of RET, and the data on the urban level of RET are few and rarely studied. For example, Zhou et al. 29 studied the progress of energy transition in 30 provinces in China by constructing a provincial energy transition index. In terms of influencing factors of RET, existing studies mainly focus on macro influencing factors. Scholars have found that Climate policies, 14 technology developments, 30 geopolitical conflicts and militarization, 31 and green industrial policies 32 have an impact on the transition to renewable energy. For example, Omri and Jabeur 14 revealed that Climate policies alone are ineffective in driving the RET. In addition, some scholars also studied the impact of digital finance on the transformation of renewable energy from a digital perspective.15–17,33 Li et al.15–17 found that digital finance is the driving force of low-carbon energy transition. Although digital finance and FinTech are closely linked, there are significant differences in their connotation and emphasis. Compared with digital finance, FinTech has more prominent technical characteristics. Therefore, it is of great significance to explore how FinTech can enable the transformation of renewable energy for urban green development.

To sum up, although existing studies have explored the relationship between FinTech and RET from various aspects, there are still limitations and gaps. First, the existing measurement methods of the FinTech development level have limitations in different dimensions and cannot fully and deeply capture the multidimensional value of financial technology. Second, due to limited data availability, most existing studies focus on the national and provincial levels of RET, and city-level RET data need to be deepened and complemented. Quantifying the city-level RET can help to better analyze and study the problems in implementing and promoting the energy transition. Third, existing studies mostly examine the elements affecting RET from policy and public dimensions, but ignore the emerging dimension of FinTech. Few literatures have linked FinTech with the urban RET.

Theoretical analysis and research hypothesis

Renewable energy, as a form of energy that can be endlessly recycled in nature, has attracted attention for its low carbon effects, it produces almost no greenhouse gas emissions during extraction and has a positive effect on mitigating global climate change.

34

Meanwhile, with the rapid development of information technologies such as big data and cloud computing, FinTech has shown great potential in improving the efficiency of financial services and promoting sustainable development.

35

First, FinTech can help build a docking platform between financial institutions and green projects, achieve information sharing and real-time monitoring among different channels, and accelerate the flow of capital into the renewable energy sector. In addition, FinTech can use big data to capture environmental performance data such as environmental administrative punishment records and negative public opinions of target users. At the same time, blockchain technology can track green bond investments, thereby reducing the risk of greenwashing faced by relevant entities. This forces relevant entities to invest in substantial green projects, such as the transition to renewable energy.

36

Based on this, we propose:

The phenomenon of capital misallocation arises from the structural imbalance and insufficient efficiency in the allocation of financial resources to the real economy, resulting in the overuse of capital resources by low-productivity industries, while high-productivity industries face the dilemma of insufficient capital input, which ultimately leads to a loss of overall economic efficiency. 2 Capital misallocation may lead to a lack of sufficient financial support for technological innovation in the renewable energy sector. Technological innovation is a key factor in promoting the development of renewable energy, and the rational allocation of capital can reduce the capital cost of renewable energy and improve its market competitiveness.

In this paper, we argue that FinTech has the potential to mitigate capital misallocation and drive the RET. Specifically, FinTech can use advanced data analytics techniques to dig deep and analyze large amounts of economic data to more accurately identify the financial needs of the renewable energy sector.8–10 In addition, with the help of internet technology, FinTech enhances the ability to allocate financial resources across time and space,

37

allowing capital to flow more efficiently to the renewable energy industry. Thus, FinTech not only improves the accuracy of capital allocation, but also facilitates the flow of capital to the renewable energy industry, helping to optimize resource allocation, reduce resource waste, and promote the transformation of urban renewable energy. On this basis, we propose the hypothesis:

FinTech can drive the transition to renewable energy by raising public awareness of environmental issues. Raising environmental protection awareness is critical to increasing acceptance and support for renewable energy projects, which can effectively reduce social resistance to their implementation.

38

First, FinTech provides a transparent platform for the transmission of environmental information,

39

which leads to a deeper public awareness of the damaging impact of fossil fuels, increasing the demand for clean energy products. Second, the improvement in environmental awareness also makes the market more sensitive to environmental risks.

40

According to the theory of organizational strategy, the public, as an important external stakeholder of the enterprise, can guide, restrict, and supervise the market behavior.

41

Therefore, with the increase in environmental protection awareness, the market could be more motivated to comply with environmental regulations to meet the public's demand for clean energy products and promote the transition of high-polluting industries to renewable energy to replace traditional fossil energy. In addition, by developing and promoting green financial products, FinTech companies can raise public awareness of environmental issues and encourage the public to invest in renewable energy projects. This investment behavior not only solves the financial problem but also is an important driving force to promote the transition to renewable energy.

42

Green innovation is key to improving the efficiency of natural resource use and promoting the development of clean energy technologies, which may help reduce dependence on fossil fuels and promote the realization of a circular economy.

43

However, due to the dual externalities of green innovation, it is a key factor in improving the efficiency of natural resources. This results in insufficient willingness of urban green innovation subjects (enterprises, universities, research institutes, etc.).

44

This paper believes that FinTech can provide sufficient financial support to urban green innovation subjects, thus promoting urban RET. Specifically, FinTech, as an emerging dimension, breaks the shackles of the traditional financial system.

22

From a certain angle, it can also support green innovation by optimizing the allocation of financial resources from the supply side. By using new technologies, FinTech can enhance the pre-loan examination efficiency of green credit and reduce the post-loan supervision cost, alleviate the expensive financing problem of urban innovation enterprises, and have an incentive effect on green innovation.

45

Furthermore, FinTech can expand the financing channels of urban innovation units. With the help of new technologies, it can break through the spatial limitations of traditional financial fields and establish cross-regional financing platforms, which will help ease the financing difficulties in the process of green innovation,15–17 thus providing solid support for the transition to renewable energy.

Research design

Econometric model

Baseline regression model

To explore the driving effect of FinTech on urban RET, we construct a static panel model referring to Zhang et al.20,21 this paper controls city and year-fixed effects, and adopts robust standard errors clustered by city, the specific settings are as follows:

Mechanism analysis model

To further reveal the mechanism of FinTech on urban RET, this study analyses the impact channels of how FinTech plays a role in urban RET. Drawing on Xiang et al.,

46

we establish the mechanism analysis model as follows.

Variable description

Independent variable

Following Liu et al., 22 we manually collect detailed information and data sets related to FinTech enterprises through the “Tianyan Cha” platform. These data are used to quantify the total number of FinTech enterprises in various cities as a secondary indicator. The entropy method is used to integrate this index with the Peking University Digital Financial Inclusion Index of China (PKU-DFIC) to form a more comprehensive FinTech evaluation system. The FinTech comprehensive indicator is shown in Figure 1. To be more specific, firstly, the Global Financial Stability Board (FSB) defines FinTech as a form of technology that can improve the efficiency of traditional financial services and reduce the cost of use through modern information technology means such as big data, blockchain, and artificial intelligence. Therefore, this paper searches the company name and business scope through the “Tianyan Cha” platform and retains the enterprises with keywords such as “cloud computing,” “big data” and “Internet of things” in the company name or business scope. Secondly, considering that shell companies may have an impact on the measurement results, this study excludes enterprises established less than one year ago or in abnormal operating conditions. Thirdly, regular expressions are used to conduct a fuzzy search for keywords in the financial field (such as “finance,” “insurance,” etc.), and restrictive expressions (such as “prohibited to engage in … Activity” etc.) records. Fourthly, the number of FinTech enterprises obtained according to statistics is used as the development index at the institutional level. Finally, referring to Liu et al., 22 we use the entropy method to merge the number of FinTech companies in the above prefecture-level cities with the PKU-DFIC sub-index, namely the Coverage Span Index, Depth Used Index, and Digitization Index, to obtain a comprehensive FinTech development index.

The construction of the FinTech index.

Dependent variable

RET is the dependent variable. The existing indicator system focuses on the national and provincial levels, while the RET index at the city level still needs to be further constructed. Therefore, drawing on Yang et al., 47 this paper constructs a city-level RET index. Specifically, in the traditional provincial energy balance sheet, we divide energy into four main groups: coal, oil, natural gas, and electricity. The electricity is divided into non-renewable energy, hydropower, wind power, and solar power generation, and an extended provincial energy balance sheet is obtained, as shown in Figure 2. Then, regarding Shan et al., 48 through economic factors, P equals to Indexcity/Indexprovince × 100%, where Indexcity, Indexprovince represent key indicators at the city and provincial levels. Such as GDP, population size, etc. We narrow down the seven energy types in the expanded provincial EBT by industry to the city level, i.e. Ecity = Eprovince × P. Specifically, for “agriculture, forestry, animal husbandry, fishery,” “industry,” “construction,” “transportation, storage, and post,” “wholesale and retail trade, accommodation and catering” and “other services,” the corresponding GDP is used to construct the socio-economic index P. For “resident life,” the energy consumption of urban and rural residents is distinguished, and the corresponding urban and rural population is used to construct the socio-economic index P. Finally, we use city-level hydropower, wind, and solar power as a share of total energy consumption to measure urban RET.

The construction of the urban RET index.

Mechanism variables

Capital mismatch index (Cm). Referring to Gao et al.,8–10 the capital mismatch index is adopted to measure. The specific form calculates the capital price distortion coefficient γKi, which is expressed as the level of the resource corresponding to no distortion. Specifically:

Then, calculating the capital mismatch index as follows: Public environmental concern (Pc). Regarding Wang et al.,

49

the Baidu index of public search for specific environmental keywords is used to construct an indicator of public environmental concern. To be specific, a keyword search is carried out in the Baidu search engine, and the daily search volume of the terms “environmental pollution” and “smog” of the public in various prefecture-level cities is crawled by Python, and the natural logarithm is added to the total plus 1, which is used as a proxy variable for the degree of public concern about the environment in each city. Green innovation (Gi). The green patent data can reflect the output of green innovation more objectively, and considering the long application cycle of green patents, the patent application data can reflect the level of green innovation in cities in a more timely manner than the data on patent grants. Meanwhile, the number of green patent applications includes green invention patent applications and green utility model patent applications, and the innovation and technology level of invention patents is higher than that of utility model patents. Therefore, referring to the practice of Dian et al.,

50

the number of green invention patent applications is measured by adding 1 to the natural logarithm.

Control variables

To obtain efficient estimation results, we select economic development level (El), financial development level (Fl), urbanization level (Ul), fiscal decentralization level (Dl), and infrastructure level (Il) as control variables regarding Liu et al.. 51 Specifically, the relationship between economic development and energy transition has been widely discussed in existing studies, and it has become a consensus that the level of economic development can promote the RET. 52 Secondly, with the continuous promotion of urbanization and the continuous upgrading of industrial structure, the structure of urban energy consumption has changed significantly, which has a significant impact on energy transformation.53,54 Specifically, the variable definitions are shown in Table 1.

Variable definition.

Data source

China's city-level data from 2010 to 2020 is used as the research sample in this study. The data sources include the China Energy Statistical Yearbook, China Urban Statistical Yearbook, and CSMAR database, the authority of these data sources ensures the reliability and timeliness of the research results. In this study, we refer to Tan et al., 40 and the data are strictly screened to exclude samples with serious missing data. Furthermore, we applied a 1% tailing treatment to all variables. After these screening and processing steps, we ended up with 2230 resample data. In Table 2, the descriptive statistics are displayed.

Descriptive statistics.

Empirical results

Baseline regression test

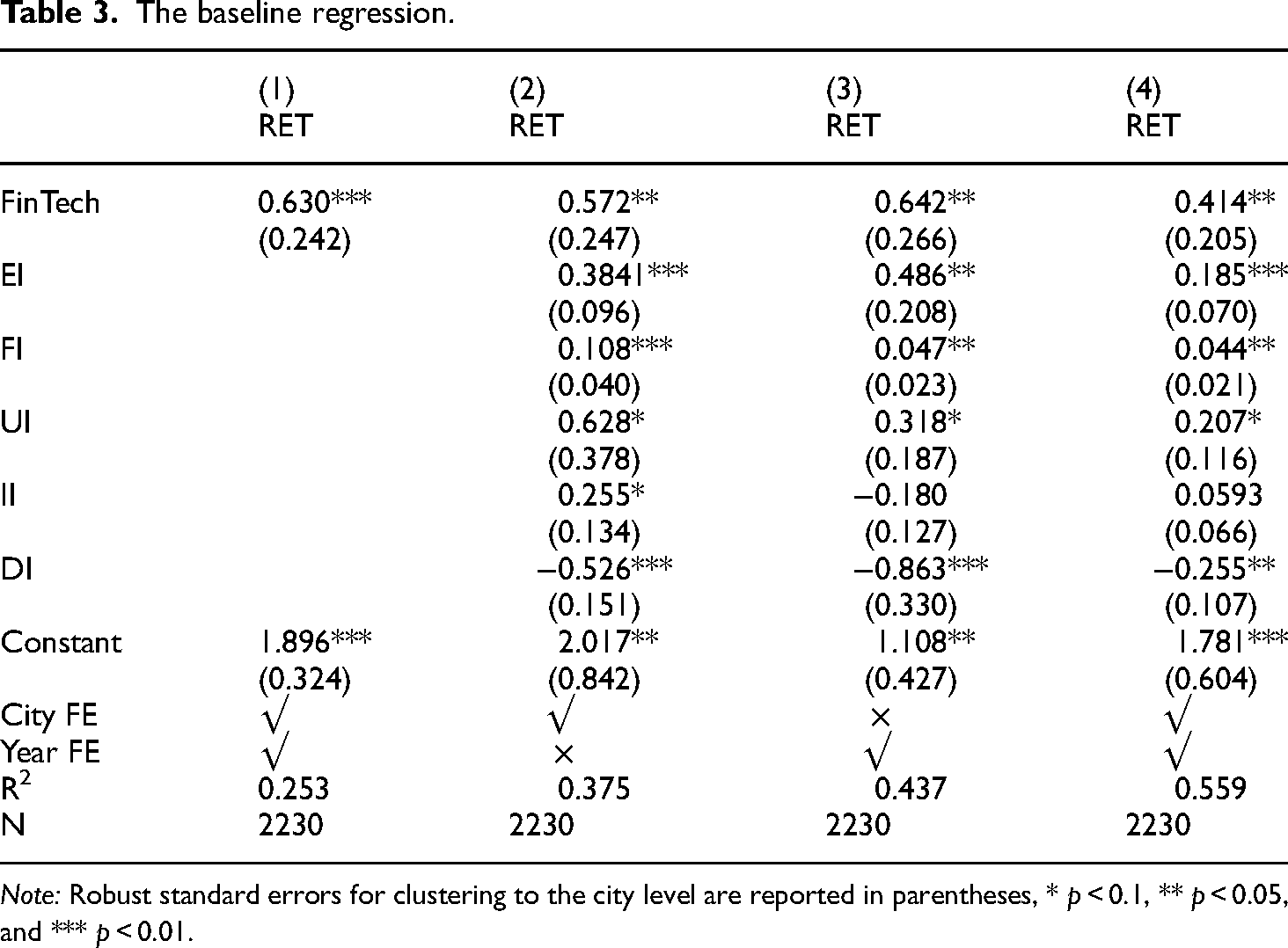

Table 3 shows the results of baseline regression, where column (1) presents the regression result without adding control variables, and columns (2) and (3) are the regression results of adding control variables but only controlling for city-fixed or time-fixed effects respectively. Column (4) contains all the control variables, and city-fixed and time-fixed effects are added. The results demonstrate that the regression coefficients of FinTech are all positive and significant, indicating that FinTech can significantly improve urban RET, which means that the higher the degree of FinTech development, the more conducive to promoting urban renewable energy transformation. Hypothesis 1 is confirmed. As mentioned above, FinTech can improve the coverage and availability of green credit products and accelerate the flow of capital into the renewable energy sector, thus promoting urban RET. 36

The baseline regression.

Note: Robust standard errors for clustering to the city level are reported in parentheses, * p < 0.1, ** p < 0.05, and *** p < 0.01.

Endogenous test

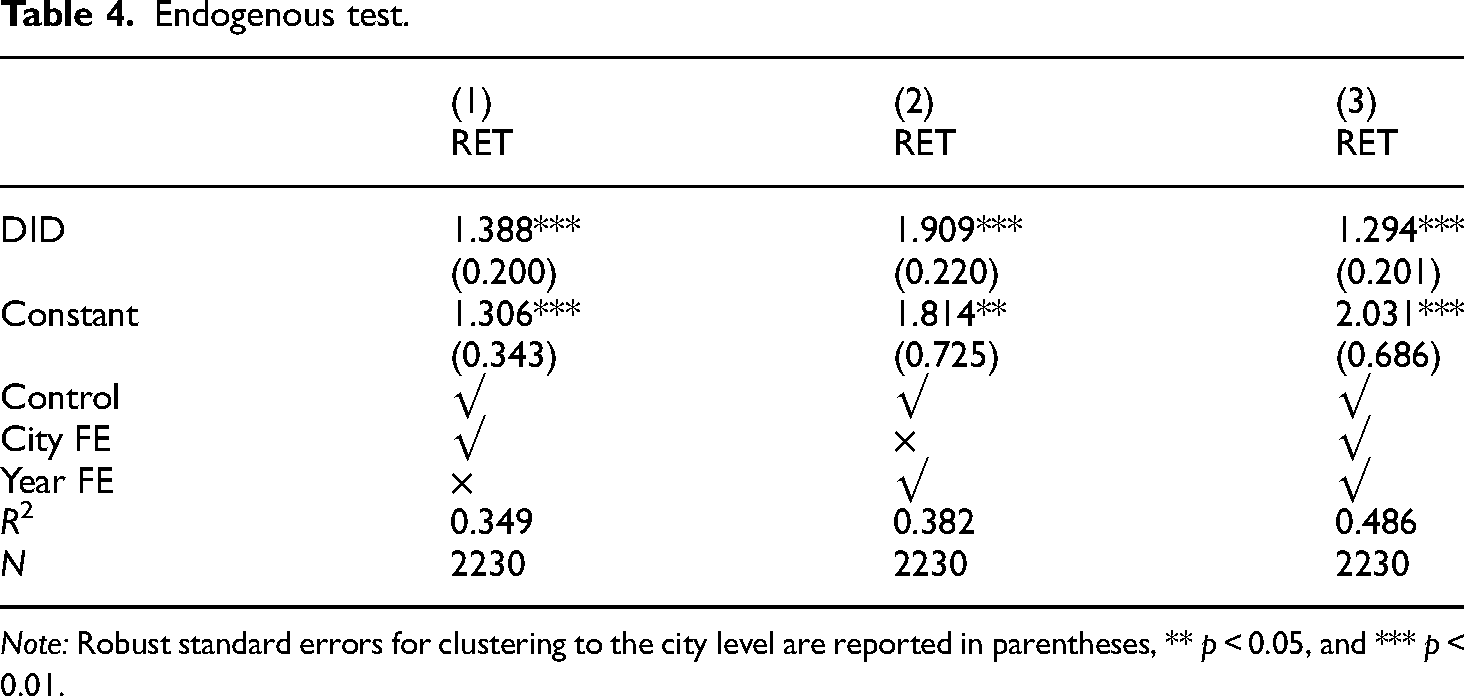

Following Ding et al.55,56 and Gao et al.,8–10 this paper utilizes the differential-in-difference (DID) method to mitigate potential endogenous problems. We take the “Broadband China” pilot policy as a quasi-natural experiment to reassess the potential impact of FinTech development on the RET. The core goal of the pilot policy is to improve the speed and coverage of broadband networks by accelerating the construction and popularization of broadband networks to support the transformation of economic structure and the growth of information consumption. The development of FinTech cannot be separated from the support of network infrastructure, the pilot of “Broadband China” promotes the deep integration of frontier information technology and the financial sector, accelerates the development of FinTech, and provides a good test environment for this paper to carry out the analysis of exogenous policy impact. Therefore, this paper takes the exogenous shock of the implementation of the “Broadband China” strategy as a proxy variable to measure the development of FinTech and uses the DID model to re-estimate the impact effect of FinTech on urban RET.

The premise of the analysis using the DID model is that the sample cities meet the parallel trend assumption. To verify whether this premise is satisfied, a parallel trend test is carried out in this paper, and the test results are shown in Figure 3. Before the impact of the “Broadband China” policy, there is no significant difference in the RET between the treatment group and the control group. However, in the years after the implementation of the policy, the policy effect on the urban RET shows a significant positive promotion effect, satisfying the parallel trend hypothesis.

Parallel trend test.

Table 4 displays the endogeneity test results in columns (1)–(3), where the first two columns only control for city-fixed effect or time-fixed effect respectively, while the last column controls for both city-fixed and time-fixed effects. We can find that the regression coefficients of the DID are all positive, which means that the “Broadband China” policy can positively promote the urban RET, which further supports the regression results of this paper.

Endogenous test.

Note: Robust standard errors for clustering to the city level are reported in parentheses, ** p < 0.05, and *** p < 0.01.

Robustness test

Adding province fixed effect

To further test the robustness of the regression results, we further include the province fixed effect in the regression, and the regression results are shown in column (1) in Table 5. The regression results show that after further including the province fixed effects, the regression coefficient of FinTech is significantly positive at the 1% significance level, and this result is consistent with the benchmark regression part, proving the robustness of the baseline results.

Robustness tests.

Note: Robust standard errors for clustering to the city level are reported in parentheses, ** p < 0.05, and *** p < 0.01.

Excluding the impact of COVID-19

Considering that the COVID-19 epidemic may have an impact on the urban RET, to exclude the impact of the COVID-19 epidemic, this paper removes the 2020 sample data, and the regression results are shown in column (2) of Table 5. The results show that after excluding the sample data of 2020, the regression coefficient of FinTech on RET is still significantly positive at the significance level of 1%, that is, FinTech still has a positive role in promoting urban RET, proving the validity of the benchmark results

Excluding special samples

Considering that municipalities directly under the central government usually have more resources and policy advantages, there are big differences between them and other cities in terms of financial support and innovation strength. Therefore, this study excludes the data of four municipalities directly under the central government of China to conduct a regression test again, and the regression results are shown in column (3) of Table 5. The test results show that even if the sample data of municipalities are excluded, the regression coefficient between FinTech and urban RET is still significantly positive, which further tests the robustness of this study.

Replacing estimation model

To further test the robustness of the regression results, the first-order lag term of the FinTech index is added to the model (1), and the generalized moment method (GMM) is adopted to conduct the regression again. The results are presented in column (4) of Table 5, indicating that after the GMM is regressed, the regression coefficient of FinTech on RET is still significantly positive at the level of 5%, that is, the driving effect of FinTech on RET still exists, and further proves the robustness.

Replacing explanatory variable

Given that the number of financial technology companies in each city is still widely used to measure FinTech development, we use this method to measure the FinTech index at the prefectural level. The regression results are shown in Table 5 in Columns (5). Column (5) shows the regression results after all control variables have been included in the regression model, both of which control for city-fixed and time-fixed effects. The regression results show that the FinTech coefficient is significantly positive at the 5% significance level, meaning that replacing the FinTech measurement has a positive promotional effect on RET, which proves the robustness of the benchmark results.

Mechanism test

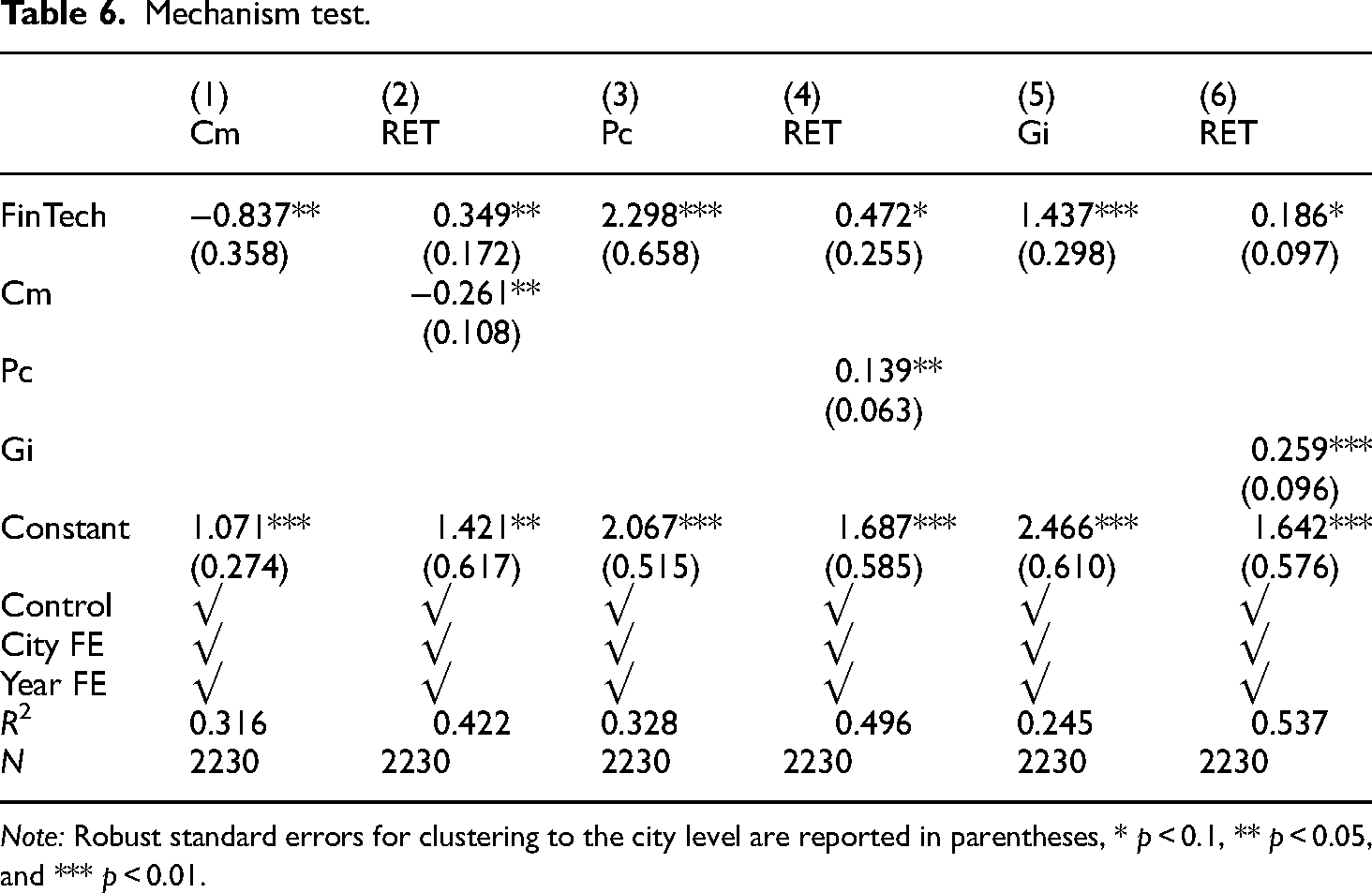

This study also discusses the impact mechanism of FinTech on RET in cities from three channels: capital misallocation, public environmental awareness, and green innovation. The regression results are shown in Table 6. Columns (1)–(2) show the regression results of the capital misallocation effect. The result indicates that the regression coefficient of FinTech is negative at the 5% significance level. At the same time, after including both capital mismatch and FinTech in the regression model, as shown in column (2), the regression coefficient of FinTech is significantly positive, while the regression coefficient of capital mismatch is also significantly negative, meaning that it can facilitate the urban RET by alleviating the capital misallocation, and Hypothesis 2 is verified. A possible reason lies in that FinTech utilizes technologies such as the internet to enhance the cross-temporal and spatial allocation capacity of financial resources. It not only improves the accuracy of capital allocation but also promotes the flow of capital to the renewable energy industry with higher production efficiency, thereby accelerating the urban transition process to renewable energy.8–10 Columns (3)–(4) present the regression results of the public environmental awareness effect. The result shows that the regression coefficients of FinTech on public environmental awareness are significantly positive. Meanwhile, the regression coefficients of FinTech and public environmental awareness on urban renewable energy transformation are both significantly positive, suggesting that it can promote the urban RET by enhancing public environmental concern, and Hypothesis 3 holds. Through its innovative solutions and platforms, FinTech can provide a more transparent and efficient way to disseminate environmental information. This mechanism can increase public awareness about environmental issues and help consumers make more environmentally friendly decisions by providing real-time data and analytics. For example, FinTech can develop applications and tools that allow consumers to easily track and compare the environmental impact of different energy options, thereby incentivizing them to choose renewable energy. These measures can reduce the cost of renewable energy and make it more attractive to consumers, which in turn drives the development of RET.

Mechanism test.

Note: Robust standard errors for clustering to the city level are reported in parentheses, * p < 0.1, ** p < 0.05, and *** p < 0.01.

Columns (5)–(6) present the regression results of the green innovation effect. The result shows that the regression coefficient of FinTech on green innovation is significantly positive. At the same time, the regression coefficient of FinTech and green innovation on urban RET is significantly positive, indicating that financial technology can drive the urban RET by promoting green innovation, and Hypothesis 4 holds. The possible reason may be that the development of FinTech can provide sufficient financial support for urban green innovation entities and promote the improvement of green innovation levels.15–17 FinTech uses emerging technologies to improve the efficiency of pre-loan review of green credit and reduce post-loan supervision costs, accelerate the speed of green innovation entities to obtain research and development funds, and fully meet their financial needs for green innovation activities, providing a powerful guarantee for RET.

Heterogeneity test

The intensity of environmental regulation

Enterprises tend to ignore the protection of the ecology while pursuing the maximization of benefits, and environmental regulation is a key force in curbing the deterioration of the ecological environment. Therefore, this paper calculates the proportion of heavy industry in the GDP of the province based on the database of China industrial enterprises, and then multiplies it with the frequency of occurrence of words related to “environmental protection” in the provincial government work report, to construct the supervision intensity of prefecture-level, and divided them into two groups of high and low government supervision intensity based on the standard of the median. Specifically, if the intensity of government supervision in city i is higher than the median level, the city is in the group of high government supervision intensity; otherwise, it is in the group of low government supervision intensity.

In Table 7, (1) and (2) are listed as the results of the heterogeneity test of regional environmental regulation intensity. It shows that FinTech only significantly promotes the RET in cities with high environmental regulation, while the regression coefficient of cities with low environmental regulation does not have significant statistical significance. A possible explanation for this phenomenon is that strict environmental regulations put pressure and incentives on cities to invest in the environment and stimulate them to explore ways to transition to renewable energy. 57 At the same time, advances in FinTech provide these cities with the necessary financial support for technological innovation, further promoting the RET.

Heterogeneity analysis.

Note: Robust standard errors for clustering to the city level are reported in parentheses, *** p < 0.01.

Economic development

Following Gao et al.,8–10 we divide the sample cities into developing and developed cities according to their level of economic development. Specifically, we classify first-tier cities and new first-tier cities as developed cities and define second-tier, third-tier, fourth-tier, and fifth-tier cities as developing cities based on the city classification published by China Finance News in 2018. First-tier cities include Beijing, Shanghai, Guangzhou, and Shenzhen, which are among the top cities in terms of total GDP. New first-tier cities include Chengdu, Hangzhou, Chongqing, Wuhan, and other 15 cities, these cities have rich economic resources, urban people, lifestyle diversity future plasticity, and other aspects of outstanding performance. The results are listed in (3) and (4) in Table 7. The research results show that the driving effect of FinTech on developed cities is significantly positive at the 1% level, while the regression coefficient for developing cities is not statistically significant. This result might be explained by the fact that cities with higher economic development levels have more abundant technological innovation resources and stronger capital investment,24,25 so developed cities can better enjoy the driving dividends brought by financial technology and promote urban renewable energy transformation.

Geographical location

Considering that there may be large differences in resource endowments and development degrees in different regions, which leads to heterogeneity in the level of FinTech, the impact of FinTech on RET is also heterogeneous. Based on this, we divided the sample into eastern, midland, and western regions according to geographical location for regression analysis, and the regression results are shown in Table 8. The regression results show that FinTech can only have a significant positive impact on the RET in the eastern and midland cities, but has no significant impact on the RET in the western cities. The reason for this result may be that the eastern and midland cities usually have a higher level of economic development and a more complete financial market system. Therefore, FinTech can play a more effective role in these cities by optimizing the allocation of financial resources and improving the efficiency of financial services.

Heterogeneity analysis.

Note: Robust standard errors for clustering to the city level are reported in parentheses, ** p < 0.05, and *** p < 0.01.

Conclusion and policy implications

This study firstly measures the FinTech development at the Chinese prefecture level from 2010 to 2020 from both the institutional and individual perspectives using the entropy approach. Then, this study puts FinTech and urban renewable energy transformation into the same framework and analyzes its driving effect on urban RET. We find that FinTech can significantly promote urban renewable energy transformation, and these results remain valid after robustness tests. We also deconstruct the mechanism of FinTech-driven RET from capital mismatch, public environmental concern, and green innovation. Finally, this paper further examines the heterogeneous effect, and it shows that the role of FinTech is more obvious in cities with high environmental regulation, high economic development levels, and eastern and midland cities.

Although this study has discussed the impact and effect of FinTech on urban RET and its potential mechanism, we have not considered spatial geographical factors and failed to further test the spatial spillover effect of FinTech. Therefore, based on the theoretical basis of this paper, future studies can further investigate whether the influence of FinTech on urban RET has a spatial spillover effect. In addition, future research could further explore whether boundary conditions such as climate risk and environmental concerns of governments have an impact on the driving effects of FinTech.

Based on the above results, we propose the following policy implications: First, the government needs to provide strong policy support for the development of FinTech. To promote the urban RET, the government should formulate policies conducive to the development of FinTech. Policies should support and incentivize the flow of financial resources to scientific and technological innovation, especially in basic research and the development of key technologies. By strengthening the deep integration of the innovation chain, industrial chain, capital chain, and talent chain, FinTech can provide financial support for the promotion of low-carbon technologies and accelerate their popularization, thereby promoting the rapid development of renewable energy and reducing dependence on traditional energy sources.

Second, differentiated policies should be formulated for regions with different economic levels. For developing cities, policy financial support should be increased to fill the shortage of funds in the construction and promotion of FinTech platforms and achieve the rapid development of FinTech. At the same time, the integration of resources between developed and developing cities forms complementary advantages and jointly promotes the implementation and growth of renewable energy projects. In addition, local policy design can also help streamline the funding of renewable energy projects in different geographical areas. Through online platforms, connecting investors and project parties in different regions can reduce financing costs and improve financing efficiency. This model provides solid financial support for interregional renewable energy projects and promotes regional collaborative development of urban RET.

Third, the government should raise public awareness and concern about the environment. According to the findings of this study, FinTech plays an important role in raising public awareness of environmental issues, thereby driving the transition to renewable energy in cities. To this end, the development of green financial products can be encouraged to enable the public to support the development of renewable energy while managing their finances. In addition, the establishment of an online policy feedback mechanism and the use of FinTech platforms to collect public feedback and suggestions on renewable energy policies can improve the adaptability of policies and enhance the sense of public participation. In this way, policymakers can harness the advantages of FinTech more effectively, inspire environmental awareness among the public, and encourage them to actively participate in the process of urban RET.

Footnotes

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported in part by Grants [24SSHZ168YB] Zhejiang Federation of Social Sciences Research Project.