Abstract

This article examines the structural power of domestic finance in developing and emerging economies (DEEs) in the context of a shift toward increasingly activist financial development planning and financial sector reform. Focusing on efforts to create large, internationally competitive banks in Malaysia and Nigeria dating to the late 1990s and early 2000s, it highlights that banks have not played their envisaged role in financing structural transformation via industrial growth and economic development. Nonetheless, (large) banks in DEEs have attained considerable structural power over financial policy, supporting their ability to shape growth and investment strategies. Therefore, the article proposes a revised model of the structural power of finance, recognizing its contingent nature. States pursue various forms of financialization both as a substitute to, or in conjunction with, industrial policy. Financialized development strategies enhance the structural power of large banks in DEEs, notwithstanding their limited role in meeting the investment/development imperative.

This article examines the structural power of domestic banks in developing and emerging economies (DEEs). 1 There is broad agreement, both in policy circles and among scholars, that in DEEs financial institutions have not played their envisaged role in financing economic development and industrial transformation. 2 Instead, financial institutions have often facilitated capital outflows or channeled their funds into unproductive activities such as foreign exchange speculation and consumer lending. At the same time, there is considerable evidence that domestic financial institutions in DEEs, in particular large commercial banks, have considerable structural power. This is commonly understood as power over policy that is derived from the ability to withhold resources for productive investments. 3 How can we explain the structural power of banks in DEEs, given their limited contribution to financing productive investment?

We argue that in order to unravel this puzzle we need to consider financialization, which we define, following Epstein, as “the increasing role of financial motives, financial markets, financial actors and financial institutions in the operation of the domestic and international economies.” 4 Financialization, in our interpretation, is both a response to structural change and implies an ideological shift that gives greater prominence to financial actors and their preferences. DEEs face considerable challenges in advancing economic development for several reasons detailed in the next section. In this context, the feasibility of industrialization as promoted by the East Asian developmental states in the post–World War II period to become a middle- or high-income country has been questioned. At the same time, pressures to develop have remained or even intensified because of factors such as population growth and greater political competition. As a result, in many countries, rather than being perceived merely as a prop to economic development, financial sectors have increasingly become key targets on their own of development-oriented policymaking. 5 This is illustrated, as we discuss in more detail below, by the growing number of countries in both Southeast Asia and sub-Saharan Africa that publish financial development plans. States pursue various forms of financialization, according to their positions within the global economic structure and their socioeconomic histories, as a substitute for or in conjunction with industrial policy. In turn, increasingly financialized development ambitions support finance's ability to shape growth and investment strategies and thus its structural power.

We demonstrate this argument with case studies of banking sector transformations in Malaysia and Nigeria, two large emerging markets, from the early 2000s until today. The two countries differ in regard to their socioeconomic contexts and potential alternative explanatory variables such as the depth of their banking sectors. However, in both countries the banking sectors have come to occupy a “privileged position” in what amounts to increasingly financialized development models. 6 In particular, both countries have pursued similar reform paths, guided by financial development planning. Banking sector consolidations to create large, internationally competitive banks were an important part of this. Financialized developmental planning in turn has increased the systemic importance of large banks in the operation of their domestic political economies and thus the potential of those banks to exercise structural power.

Malaysia and Nigeria share, as an outcome of financialized developmental planning, some alignment between the interests of large banks and their central bank regulators, which have formulated a series of financial sector policies that are responsive to the interests of large banks. In both countries, financial internationalization has taken the path described by Pepinsky; 7 there remain significant restrictions in place on foreign bank entry while the capital account has become more liberalized. Restrictions on new bank entry reflect both the interests of governments to create strong, indigenous banks and the banks’ interest to limit competition.

In this article, we point to a number of further examples of where regulators have formulated policies that are responsive to, rather than just coincide with, the interests of large domestic banks. 8 This includes support for banks’ ambitions to expand regionally (Malaysia); bailouts and regulatory forbearance (Nigeria); and moving away from direct interventions in the banking sector (credit guidelines, etc.) that are associated with developmental states in favor of more market-oriented forms of banking. In illustrating how banks’ structural power operates in increasingly financialized contexts, we consider normal times and crisis times, specifically responses to the onset of the COVID-19 pandemic, focusing on the example of government and bank preferences regarding loan moratoria. As we will show in this article, states’ and banks’ interests align in promoting finance-led growth. However, the policies employed by the Malaysian and Nigerian authorities to achieve this goal and the associated distribution of costs and benefits tend to reflect the interests of the banks rather than of the states.

Our analysis contributes to the literature on the structural power of finance by shedding light on structural power in underresearched DEE settings. 9 Moreover, our article highlights the need to reconceptualize structural power by reassessing its basis, in a context of intensifying external (i.e., global) and internal (i.e., domestic) financialization. Furthermore, our article highlights the agency, albeit subordinated, of DEE policymakers in responding to material pressures for economic development. Although DEE policymakers exercised some agency in employing financialized developmental strategies that reflected national priorities, they nonetheless felt strong pressures to move away from traditional developmental models focusing on industrialization.

The argument of the article is developed as follows. We first review existing work on structural power and its applicability to DEE settings and highlight the value of reconceptualizing some of its elements in a context of financialization. We also situate financial development planning in its historical and conceptual context. We then examine the political economy of banking sector transformations. We first look at the structural transformation of banking sectors in Malaysia and Nigeria, focusing on state-led bank consolidations and implications for banks’ business models. We then consider the implications of these transformations for banks’ potential to exercise structural power. Next, we examine the wider role of the banking sector in the development strategy of the case countries to consider how financialized developmental contexts shape banks’ structural power in both normal and crisis times. From this discussion, we will develop an enhanced model of the structural power of finance in DEEs in the context of financialization. Our analysis draws on interviews with policymakers and market practitioners, descriptive statistics from national and international sources, and the content analysis of financial development plans.

The Politics of Financial Development and the Structural Transformation of Emerging Market Banking Sectors

The starting point of theories of structural power is that states face an “investment imperative” because they need to maintain sufficient investment to achieve the level of growth that is necessary to maintain political support and finance the state apparatus. 10 Investors, broadly defined as business or financial actors, have the ability to withhold much needed resources, either through investment strike or exit in the form of capital flight. This ability forms the basis of their structural power. 11 The structural power of finance, according to these theories, developed in the context of Fordist capitalism, is rooted in the central structural position that finance occupies through the provision of investment resources in the process of financial intermediation for “indebted industrialization” and funding of state activities. 12 Through its central role in the operation of capitalist societies, finance is able to assume a privileged position vis-à-vis other societal groups, which may influence policy outcomes. The structural power of finance is indicated when policymakers employ policies that are responsive to the anticipated or stated interests of finance, such as barriers for new bank entry, micro and macro regulation protecting banks’ profitability, or bank bailouts in times of crisis. 13 Responsiveness in turn serves to avoid a situation where finance punishes unfavorable policies through capital flight or “investment strikes,” that is, the declining willingness to purchase government bonds or invest for “productive purposes.” 14 For a summary, see Figure 1.

The traditional view of the structural power of finance. (Authors’ model of existing literature.)

As Young explains, it is important to distinguish the expected causes of the structural power of finance capital from its hypothesized effects. 15 Accordingly, a central structural position in the economy is thus the cause of the structural power of finance. Young suggests a couple of indicators to capture the extent to which segments or individual firms in the financial sector occupy a central role in the operation of capitalist societies, something he refers to as the degree of “structural prominence.” 16 In particular, he suggests measuring structural prominence through information about the financial industry's importance relative to other industries, as captured by the percentage contribution of the financial sector to value added relative to the value added of other sectors. Other measures he proposes refer to total financial sector assets or employment.

In the context of DEEs, however, data availability and quality are often limited; hence it is difficult to get data on the gross value added share for different industries, including for banking. Data on finance, for instance, are often only available as part of a composite measure of finance, insurance, and real estate, the so-called FIRE sectors. In addition, in resource-rich DEEs, the extractive sector tends to occupy a central position in the economy because of its role in mobilizing foreign exchange and because many resource-rich DEEs are undiversified. In this set of countries, it is important to consider (comparatively) the centrality of the extractive sector when assessing the degree to which finance occupies a central structural position. More generally, in countries with large informal sectors, a core characteristic of many DEEs, the contribution of the financial sector, being among the most formalized ones, tends to be overweighed. 17 Similarly, when it comes to employment, much of the emphasis in DEEs rests on the prospective role of the financial sector in creating new professional jobs and high-skilled employment, rather than the actual employment the financial sector provides. In other words, it is financial sector aspirations rather than achievements that shape financial development thinking and policies, often couched in ambitious language of establishing oneself as an international financial center.

In addition to comparing the banking sector's role in the economy to that of other sectors, we may also try to capture the centrality of banks’ structural position by considering banking sector characteristics, including the potential to provide financing for productive purposes and government. In recent years, with the promotion of financial development by international financial institutions (IFIs) as part of the financialization of development discourse and practice, the availability of data on banking sector characteristics in DEEs has improved. 18 Data on the competitiveness of the banking sector, as captured by indicators of bank concentration, are suggestive of the structural position major banks occupy as potential providers of financing and the degree of their market power. Data on the level and composition of banks’ lending are suggestive of the degree to which they are suppliers of finance to sectors that are, at least from the perspective of the government, essential for the operation and growth of the economy.

Before considering the context in which DEEs are situated and the impact of financialization, it is worth discussing some of the limits to structural power as outlined in the literature. In particular, the centrality of finance in the operation of the economy (or its structural prominence) is limited in a context where banks largely channel credit to sectors considered by government not to be a priority for development. In such a situation, the damage banks may inflict on a political economy by realizing a threat to withhold investible funds from the real economy is limited. Low-conditionality sources of foreign exchange such as oil or, in some countries that are geopolitically important, foreign aid may help to address the external financing needs of import-dependent DEEs, reducing the structural prominence and thus banks’ potential capacity to exert structural power. To assess banks’ structural prominence and structural power, it may thus be useful to consider the extent to which the government has access to and control over resource rents that may replace finance provided by banks. 19

Moreover, a central position, or structural prominence, of finance does not automatically translate into structural power. This is the case, in particular, when governments perceive banks’ threats to punish unresponsive behavior as not credible. 20 This potentially results in a situation where the government will be less responsive, limiting the banks’ structural power. Whether threats of punishment are credible may depend on the exit options that banks have available, 21 as well as the profitability of the banking sector in a given jurisdiction. In both Malaysia and Nigeria, for instance, the banking sector is dominated by domestic banks, making full exit an unlikely option. Structural power is thus a relational type of power and highly contingent. In order to gauge banks’ ability to exercise structural power, it may therefore be useful to examine banks’ sources and level of profit.

How may we have to adapt our conceptualization of structural power if we consider DEEs in the context of financialized capitalism? Today, DEEs face considerable challenges in advancing economic development, including competition from other emerging economies and secular stagnation, shrinking development space due to global rules, externalities of US financialization, and difficulties to attract international capital that is affordable and not subject to (excessive) volatility. These challenges are quite different from the challenges faced by the late industrializers in East Asia such as South Korea or Taiwan in the post–World War II period.

Today's DEEs have to contend with competition from industrial sectors in other emerging economies, notably China, and from monopolistic firms emerging from economic concentration around the globe and contributing to secular stagnation. 22 Pressure to converge with global rules in trade, finance, and investment has been shrinking the development space for diversification and upgrading policies through state intervention, making it harder for developing countries to pursue the kinds of industrial policies adopted by high-income countries when they were developing themselves. 23 Until the global financial crisis (GFC) of 2008, many DEEs also faced major difficulties to attract international capital and borrow internationally at favorable terms. 24 In the postcrisis, low-interest-rate environment, capital flows to DEEs increased. However, this often came at a high price in the form of considerable risk premia on international bonds, 25 or it came with significant volatility due to exogenous factors, such as the global externalities of US financialization as epitomized by US monetary and fiscal policymaking or the COVID-19 pandemic. 26

Under these circumstances, the feasibility of industrialization as promoted by the East Asian developmental states to become a middle- or high-income country is increasingly questioned by developing country policymakers, scholars, and development agencies. 27 At the same time, pressures to develop and raise economic growth have remained or even intensified due to population growth, high rates of youth unemployment, and, in some countries, greater political competition, which increases pressure on politicians to deliver on economic performance. 28

It is in this context that policymakers have turned to finance and especially the banking sector, since many DEEs have bank-based financial systems, as a source and driver of economic growth. Rather than being perceived as subordinated to the needs of the real economy, financial sectors themselves have increasingly become key targets of development-oriented policymaking in many countries. 29 States have pursued financial development as a substitute for or in conjunction with industrial policy, and finance and financialization are increasingly seen as sources of growth and wealth. This is illustrated by the rise of financial development planning, which has gained significant traction among DEE policymakers since the 1990s. A growing number of sub-Saharan African and Southeast Asian countries regularly conduct financial development planning exercises and publish financial development plans and blueprints. We take these plans—typically produced by financial regulators, which in many DEEs are central banks—to reflect the role governments assign banks in their development strategy.

In financialized contexts, these financial development plans cover issues such as banking sector competitiveness, including strategic consolidations aimed at creating larger, internationally competitive banks; the establishment of international or regional financial centers; plans to support citizens’ investing in capital markets; and access to credit for individuals rather than businesses. They are quite different from national development plans of previous eras, which aimed at nudging financial institutions toward the intermediation of savings into productive investments, often targeting specific industries or sectors. While financial development plans often refer to overall planning frameworks espoused in national plans, they focus on only one sector: finance. In both Malaysia and Nigeria, the financial authorities began to undertake regular, multiyear financial development planning exercises from the early 2000s onward. 30

Financial development plans can also provide insights into how policymakers understand the circumstances in which they operate, including conditions of heightened financialization. This is perhaps nowhere clearer than in this excerpt, taken from the Capital Market Masterplan 2 of the Securities Commission Malaysia (our emphases): While financial innovation has channeled greater flows of capital into financing innovation and enterprise, it has also increased the financialization of economic activities relative to the generation of productive wealth. The rising proportion of financial assets relative to physical assets is a phenomenon arising from the globalisation of financial markets as well as the expanding role of intangible assets in creating wealth.

31

On this reading, financialization privileges financial assets over productive purpose and wealth accumulation over industrial transformation. The passage continues to highlight the “inherent instability” associated not just with increases in financial activities but also their increasing complexities in a “multi-venue, multi-product and multi-asset environment.” 32 Importantly, despite moves toward disintermediation, banks have continued to play a central role in DEEs, including as prominent originators and underwriters of capital market products.

Such financialized development strategies, formulated in response to structural challenges and reflective of an ideological shift that gives greater prominence to financial actors and their preferences, play a crucial role in enhancing the structural power of large banks in DEEs, notwithstanding their limited role in meeting the investment imperative. Where governments realize that the financial sector is unwilling to play its envisaged role in the country's development strategy, prima facie the structural power of finance declines given the limited impact that investment strikes would have on the operation of the economy and its growth trajectory. Instead, policymakers envisage a role for the financial sector that is so central to its development strategy that they nonetheless feel strong pressures to be responsive to the preferences of finance. Structural power may thus be based on “wishful thinking”: the aspired rather than the actual centrality of finance in the economy. Such situations have received little attention in the literature but are, as Massoc suggests for France and Spain, and as we will discuss with reference to the experiences of Malaysia and Nigeria, not uncommon. 33 They also point to the importance of considering not only structural factors but also the role of financialized ideologies as reflected in and reinforced by financial development plans and strategies formulated by domestic regulators. 34 These financialized ideologies are a consequence of internalizing pressures for reform deriving from the fundamentally changed environment that contemporary late industrializers face.

In the sections that follow, we illustrate our argument that financialized development strategies enhance the structural power of large banks in DEEs, notwithstanding their limited role in meeting the investment imperative. Our analysis begins by analyzing the major state-led banking sector reforms in both Malaysia and Nigeria, namely, promotion of banking sector consolidations, aimed at creating large, internationally competitive banks, in order to enhance both domestic growth and government standing. As we will show, this had significant implications for banks’ business models.

The Shift toward Financialized Development Planning and the Transformation of Banking Sectors

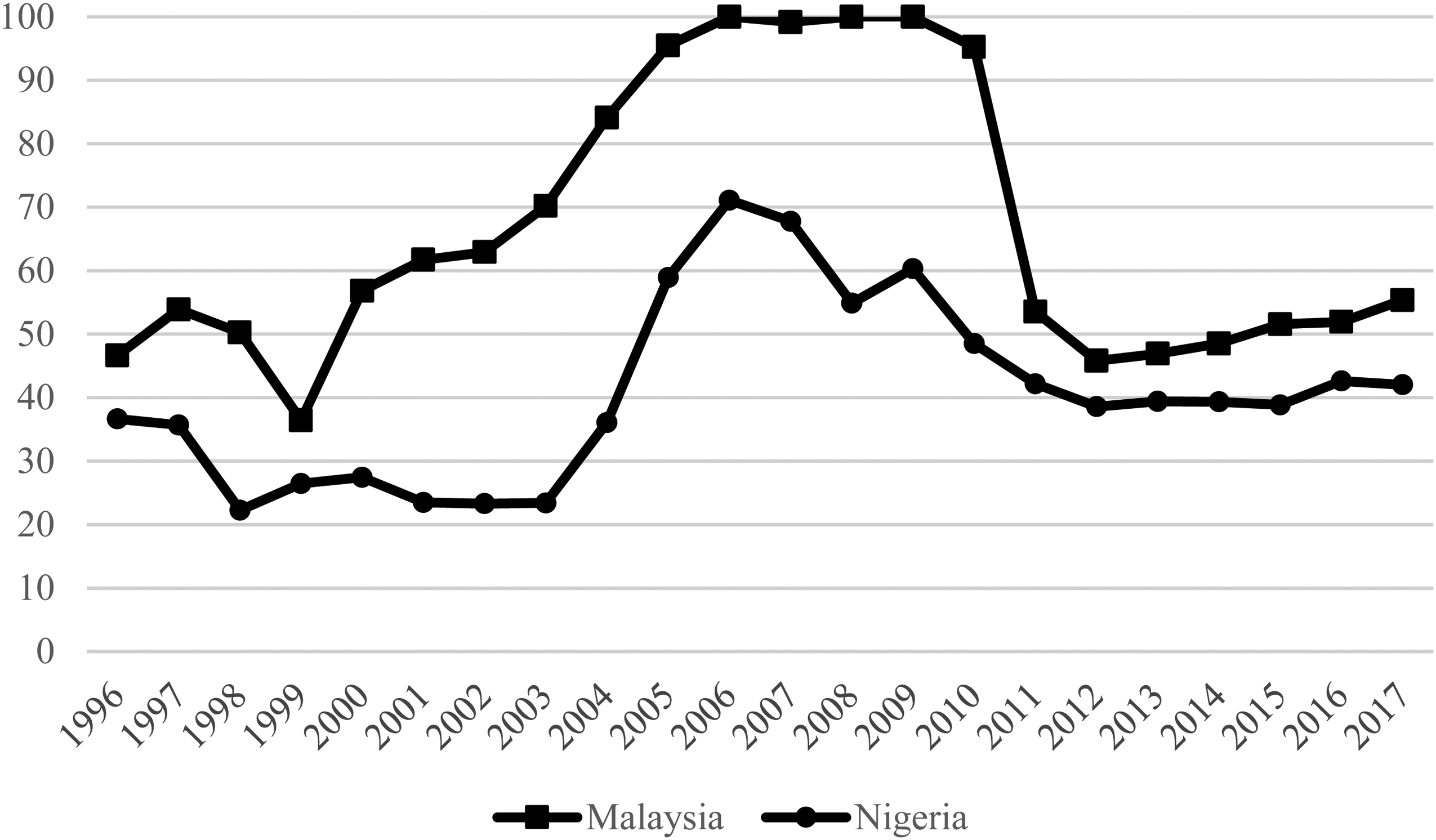

In the first part of this section, we will discuss the political and economic factors shaping bank consolidations and then turn to the implications for the centrality of banks in the economic structure. In both Malaysia and Nigeria, bank consolidation in the late 1990s and early 2000s significantly increased that centrality, in particular the prominence of the largest banks, as indicated in Figure 2. However, this was largely a temporary phenomenon, with increases in the level of bank concentration petering off in the subsequent decade, although stabilizing at a somewhat higher level in Nigeria. Nevertheless, the impact on banks’ business models was more lasting and had important implications for banks’ potential to exercise structural power, as we discuss in the second part of this section.

Bank concentration (percentage of assets of the three largest banks). (World Bank, “Global Financial Development Database.”)

Financial Development Planning and the Government-Led Consolidation of Banking Sectors in Malaysia and Nigeria

The distribution of ownership and control has been a central issue in Malaysia's ethnically stratified political economy. The financial sector has played an important role in the country's developmental model as set out in consecutive Malaysia Plans, the country's five-year planning framework. Indeed, it has been ascribed a crucial role in “the attainment of a high value-added, high-income economy.” 35 In reality, however, financial sector intermediation, focused very much on the provision of household credit, has only played a limited role in this endeavor.

A policy shift in favor of bank consolidation can be traced back to the early 1990s when the central bank—Bank Negara Malaysia (BNM)—introduced a two-tiered regulatory framework to encourage smaller banks to merge with bigger, multipurpose banks. However, in the overheating financial system prior to the Asian crisis of 1997–98, banks felt little market pressure for consolidation. In the aftermath of the Asian crisis, Malaysia pursued a more top-down approach. In January 1998, it announced its consolidation plans for finance companies. This was followed by the announcement in July 1999 that the country's remaining twenty-one banks were to be merged into six anchor groups; following political backlash, this number was raised to eight. 36

In 2001, Bank Negara issued its first Financial Sector Masterplan, covering a ten-year period. 37 The Masterplan identified consolidation as one of the major factors driving competition in Asian and global banking sectors, emphasizing Malaysia's need for greater progress toward it. 38 Among other things, it set out a phased approach to the development and liberalization of the banking sector. During the first phase, domestic banks were to be bolstered. In the second phase, domestic competition was to be strengthened. And in the third phase, new foreign competition was to be introduced. In 2011, Bank Negara released its Financial Sector Blueprint, setting out the planning framework for the subsequent decade. In 2022, delayed by the pandemic and with a shorter planning window of five years given the greater uncertainty faced by policymakers, Financial Sector Blueprint 2022–2026 was published.

Malaysia's banking sector exhibits a greater concentration than that of Nigeria, with the asset share of the top three banks—Maybank, Public Bank, and CIMB—reaching over 90 percent in the aftermath of consolidation before dropping back to below 60 percent in the wake of the GFC (see Figure 1). However, at the same time, bank ownership has become increasingly concentrated in the portfolio of a small number of so-called government-linked investment corporations, or GLICs, a dynamic already envisaged by the Financial Sector Masterplan's call for greater institutional ownership. 39 Significant bank shareholders include schemes managed by the national unit trust company, Permodalan Nasional Berhad (PNB), the Employees Provident Fund (EPF), and Kumpulan Wang Persaraan (Diperbadankan) (KWAP), respectively the mandatory pension schemes for private sector and public sector employees. Their shareholdings in the three biggest banks are significant. EPF holds double-digit shares in all three of them, KWAP holds around 5 percent in each, and the investments by PNB and the schemes it manages ranges from close to 50 percent in Maybank, to a double-digit share in CIMB, to a still significant share of just over 3 percent in Public Bank. 40 In sum, following banking sector consolidation, Malaysia's largest banks have obtained a position of structural prominence albeit significantly restrained by the extent of state shareholdership (via government-linked investment companies), which significantly affected their business models, as we will discuss below.

Nigeria's banking sector has gone through a similar phase of consolidation and concentration, as Figure 1 shows. It emerged from the period of privatization and financial liberalization fragmented and fragile. During that period, the government granted bank licenses to politically connected individuals, many of whom lacked professional experience in banking and were drawn to the sector because of the ability to garner high returns from speculation in foreign exchange transactions. 41 As a result, the number of banks operating in Nigeria tripled between 1986 and 1989, 42 and fragility increased owing to mismanagement and fraud in the new banks and the limited capacities of the Central Bank of Nigeria (CBN) to supervise them.

Nigeria's financial sector has, like Malaysia's, historically played a central role in national development planning. This is epitomized by the developmental mandate of the CBN, which survived the era of financial liberalization; the mandate assigns the CBN a role in enhancing the contribution of the financial sector to the development of the real economy. Over time, however, the financial sector itself, especially the banking sector, has increasingly become a key target of the CBN. For instance, in the late 2000s the Nigerian authorities developed the Financial System Strategy (FSS) 2020, which had as its vision “to be the safest and fastest growing financial system amongst emerging markets.” 43 More specifically, the three-part strategy to achieve this goal consisted of strengthening the domestic financial sector, enhancing integration with external financial markets, and building an international financial center, all of which would lead finance to become a catalyst for growth. These reforms to strengthen the financial system, the CBN claimed, would enable Nigeria to “become one of the world's 20 largest economies.” 44

Building toward this, and partly inspired by the Malaysian experience, 45 in 2004 the CBN promoted the consolidation of the banking sector through an increase of the minimum capital requirement for banks from about US$15 million to US$190 million, which was envisaged to be achieved through mergers and acquisitions. The CBN justified the reforms, which it presented as part of its agenda for repositioning the financial system for the twenty-first century, by explaining that many banks in Nigeria's domestically and privately owned commercial banking sector were fragile, preferred lending to the government rather than to the private sector, and had become reliant on state-owned oil deposits rather than making efforts to mobilize savings from the public. 46 The consolidation through mergers and acquisitions was seen as an instrument for enhancing the banking sector's efficiency, size, and contribution to economic growth. Specifically, the central bank governor, Charles Soludo, explained to bankers that the “goal of the reforms is to help you become stronger players, and in a manner that will ensure longevity and hence higher returns to your shareholders over time and greater impacts on the Nigerian economy.” The Nigerian economy, according to the CBN, would “benefit from internationally connected and competitive banks that would also mobilize international capital for Nigerian development.” 47

At first, the banking consolidation seemed to have achieved positive outcomes: the number of banks declined, so that out of eighty-nine banks, only twenty-five larger banks remained. The banking sector deepened and credit to the private sector increased in response to pressure to use the funds raised from the increased capitalization (see Figure 4). High oil revenues fueled the growth of deposits and thus credit in Nigeria's oil-centered economy. However, the CBN failed to ensure the adequacy of both the capital of merged institutions and their regulation and supervision for the expansion of finance and oil sector lending, producing a systemic banking crisis. 48 In 2009, ten out of the twenty-five remaining banks, accounting for about a third of banking system assets, were either insolvent or undercapitalized, underscoring the risks of major and rapid financial deepening. Under the incoming central bank governor, Sanusi Lamido Sanusi, the CBN not only rescued the failing banks but the government also acquired some ownership stakes in some of the failing banks. The medium-term goal of Sanusi's crisis response was to position the banking sector to support private sector development by strengthening regulation and supervision due to frustration with the banks’ limited contribution to real economic investment. 49 While refraining from introducing credit allocation guidelines, the CBN and the government used government oil revenues to introduce a series of subsidized credit lines that private commercial and state-owned development banks could on-lend to development priority sectors like oil and agriculture.

Overall, Nigeria's banking sector emerged from the crisis with a lower level of concentration, but the three largest banks still have a combined market share of about 40 percent (see Figure 2). While especially the larger banks in Nigeria's privately owned commercial banking sector occupy a central position in the economy, their structural importance is to some extent weakened by the state's control over oil resources, which it uses to substitute for private bank credit. That said, the full impacts of the consolidation on the centrality of banks in the economic structure and thus on their potential to exercise structural power become visible if we also consider how the consolidation shaped banks’ business models.

Implications for Banks’ Business Models

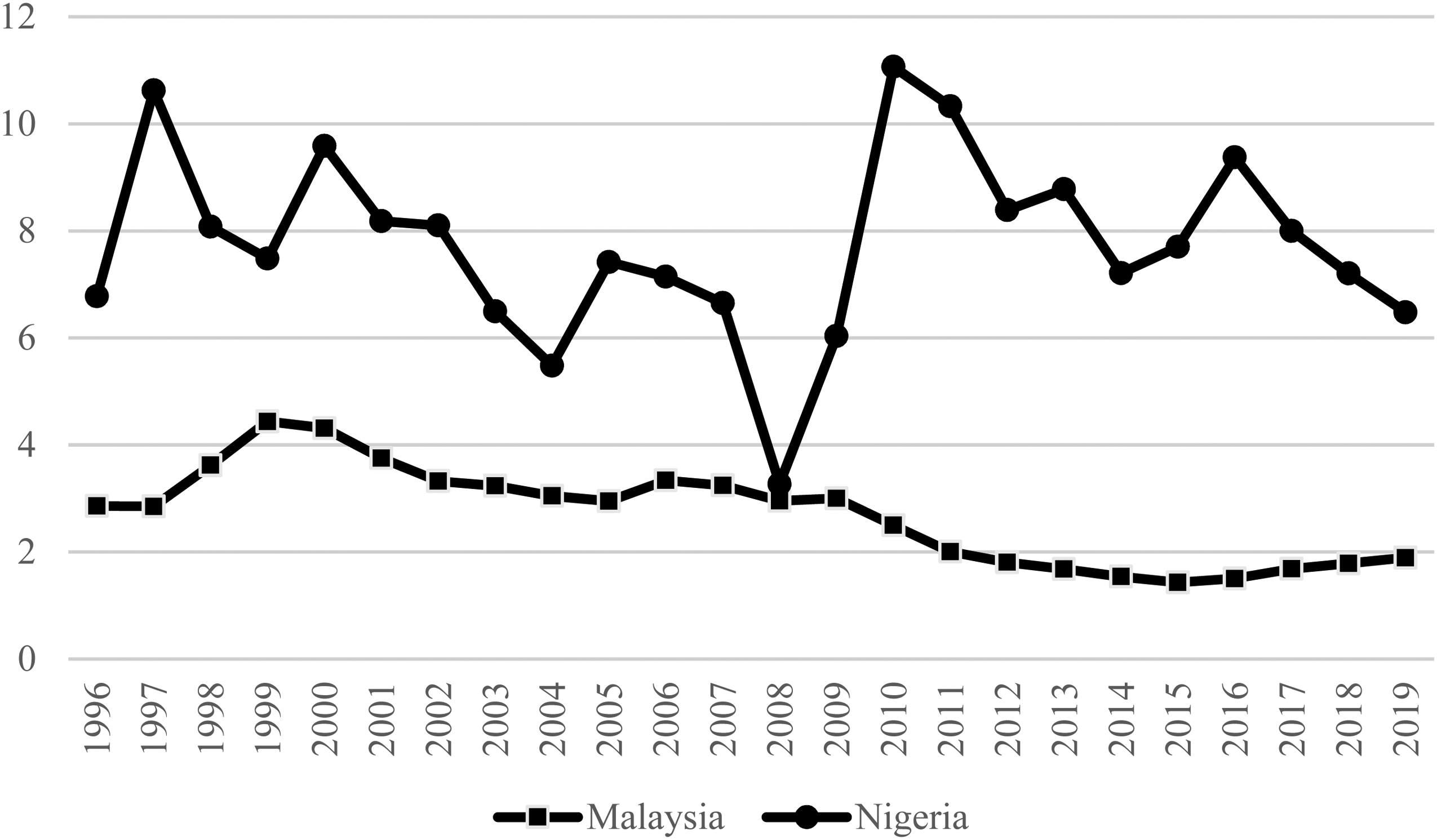

In both countries, bank consolidation had implications that reached far beyond shaping the level of bank concentration and enhancing their structural prominence. It also transformed banks’ business models, affecting not only the levels of profitability but also banks’ strategies to generate profits, albeit in different ways given different political economic constellations, as indicated for example by interest spreads (see Figure 3). What both Malaysia and Nigeria have in common is that banks changed their business models in ways that in turn impacted banks’ structural prominence, and, as we will see in the next section, power.

Comparative interest rate spread (percentage). (World Bank, “Global Financial Development Database.”)

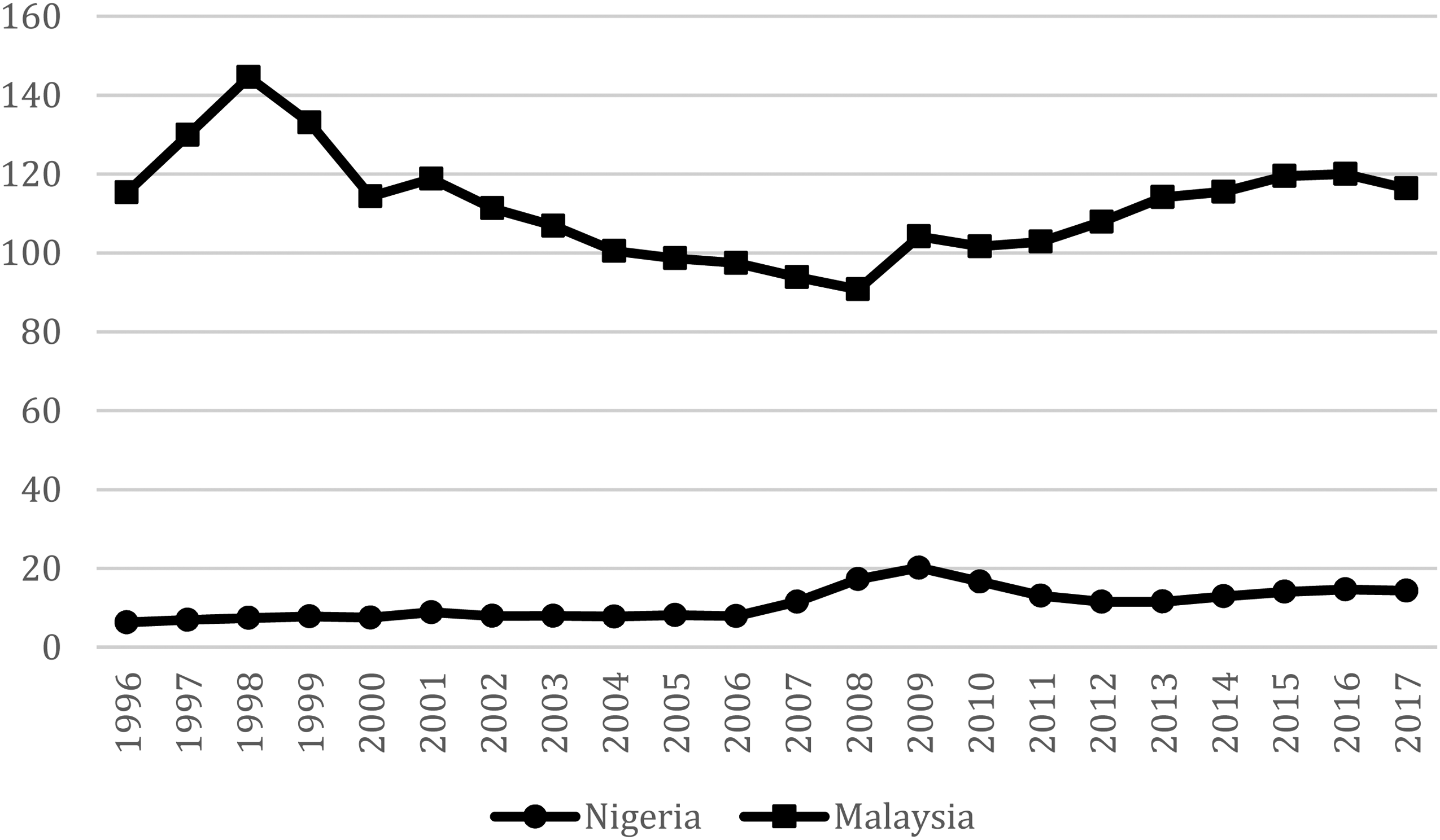

In Malaysia, state shareholdership in the banking sector is a significant source of pressure for dividends; indeed, bank dividends have been an important lifeline in Malaysia's system of shareholder-state capitalism. 50 At the same time, the interest rate differential is low, squeezing banks’ profits. To some extent, this has been mitigated by the overall size of the banking sector in Malaysia's significantly financialized political economy (see also Figure 4). But it further disincentivizes banks from lending to industry, and the majority of lending is concentrated in the household sector.

Private credit by deposit money banks to GDP (percentage). (World Bank, “Global Financial Development Database.”)

This trend was already discernible prior to the Asian crisis and accelerated in its aftermath. To restart bank lending after the crisis, the central bank mandated a lending target of 8 percent in 1998 and 1999. Chin suggests that this “encouraged the recurrence of a build-up of loans for unproductive activities.” 51 In the subsequent decade, household debt ballooned, reaching a high of over 88 percent of GDP in 2015, then declining slightly in subsequent years, before reaching an all-time high of 93 percent in 2020 because of the COVID-19 pandemic. In middle-class Malaysia, this creates what Chwieroth and Walter have dubbed the “wealth effect,” 52 wherein the significant debt exposure of households raises expectations with regard to government support for the banks and so further enhances their prominence.

In addition to low-margin but also low-default domestic lending, the two large Malaysian banks Maybank and CIMB also increasingly pursued regional ambitions, especially in the aftermath of the GFC. Through acquisitions, such as the acquisition of BII by Maybank and of Bank Niaga by CIMB, they have also become important players in the Indonesian banking sector where lending profitability is still relatively high.

In the period from 2008 to 2020, banks were the second-largest holders of domestic government debt after the pension funds, with a share ranging from 21 percent to 34 percent; and they were even the largest holders during the crisis years of 2009 (GFC) and 2020 (pandemic). 53 Moreover, disaggregating domestic debt holdings further, banks are the single largest holder of Shariah-compliant Government Investment Issues, followed by the pension funds. This is potentially significant, as the foreign holdership of GIIs has been hovering between 6 and 8 percent as compared to around 40 percent for conventional domestic government bonds.

While in the period between banking sector liberalization and consolidation Nigerian banks largely made profits through foreign exchange trading, 54 their business models changed following the consolidation. Today, banks largely make money through lending. As a former managing director of a major Nigerian bank explains, banks today make money “on the spread between deposit and lending rate; you might make a guaranteed 7%. And then you lend to the government which is associated with 0% NPLs [non-performing loans]. You do not even need to trade in forex.” 55 The interest rate spread, which averaged 8.5 percent between 2010 and 2019, is significantly higher than in Malaysia and also high in comparison with other DEEs, rendering lending a considerable source of profits. A high bank return on equity, averaging 15 percent between 2012 and 2017, confirms that banking is a profitable activity in Nigeria, at least for the major banks.

Pressure on the banks to use the funds raised from the increased capitalization had two distinct consequences. First, it fueled the expansion of Nigerian banks through subsidiaries on the continent. Second, it increased lending to the private sector. While such lending remains limited, even by African standards, it averaged 13 percent of GDP between 2005 and 2017. Reflecting domestic financialization, the majority of private credit does not go to the sectors the CBN defines as development priority sectors, consisting of agriculture, manufacturing and oil and gas, but to “non-preferred sectors,” which includes sectors such as finance, insurance, real estate, construction, and import finance. 56 The largest share of lending, however, both to the private sector and in general, goes to the oil and gas sector, which is central in Nigeria's growth and development model. Between 2010 and 2017 the share of private lending to this sector was 19 percent.

Another core feature of banks’ business model is lending to the government. As major holders of domestic government debt, Nigerian commercial banks are thus central to the functioning of the state apparatus and its debt management strategy, which prioritizes domestic over external debt to limit vulnerabilities to the volatility of foreign capital flows. Between 2005 and 2008, and again between 2010 and 2014, banks were the largest holders of domestic government debt. In 2009 and between 2015 and 2018, banks were the second-largest holders after the nonbank public, holding between 30 and 43 percent of the domestic government debt.

Structural Power in Financialized Developmental Contexts

This section explores to what extent and in what ways banks’ structural prominence gets translated into structural power, focusing on the wider role of the banking sector in the development strategies of Malaysia and Nigeria. As we will demonstrate, in a financialized context, factors potentially reducing the centrality of banks in the economic structure may actually enhance their role in the envisaged economic model as financial motives become more prominent. This clearly highlights the changing and contingent nature of structural power in increasingly financialized DEE settings, both in normal times and at times of crisis.

We have shown in the previous section that the structural transformation of banking sectors has had significant implications, but in this section we illustrate that its importance for banks’ structural power varies. Importantly, we show how the rise of financialized development strategies tends to augment greatly structural power, even in the face of limiting factors.

The Exercise of Structural Power in Normal Times

Market access is probably the area where Malaysian banks’ preferences and those of their regulators are most closely aligned. In Malaysia, significant state shareholdership in the banking system puts a de facto limit on foreign ownership. Similarly, the process of issuing new banking licenses is strictly controlled as set out in the Financial Sector Masterplan, although a slightly more permissive regime has been put in place for the Islamic finance sector. 57 Overall, and despite tentative steps toward liberalization, barriers to market access remain high.

With regard to the direction of lending and the ability of banks to pursue investment strikes, once more the importance for their ability to exercise structural power is weak. The Malaysian government relies first and foremost on government-linked investment companies and other state capitalist institutions when it comes to lending to and investment in industry. However, given the growing emphasis on positioning Malaysia as a global Islamic finance hub, and the importance that Islamic finance ascribes to financing the real or productive economy, financial regulators have sought to persuade the country's Islamic banks to adopt a model of value-based intermediation. More specifically, Islamic banks are asked to consider their social impact and to align their practice with initiatives such as the Global Alliance for Banking on Values or the UN PRI. Nevertheless, one of the most popular products that resulted from these initiatives are rent-to-own housing finance schemes that have contributed little to achieving the country's developmental goals, especially in the context of an already highly speculative and significantly unaffordable housing market.

The role of banks in financing the government and more generally contributing to revenues—and by extension the ability of credibly threatening to withhold funds—is also limited. For most of its history, Malaysia's pension funds, primarily the EPF, the mandatory private sector pension scheme, have been the largest investors in and holders of government bonds. This means that the Malaysian government has had to rely comparatively less on the banking sector for its financing than other DEE governments. Government revenue consists of tax and nontax revenue, with a ratio of roughly 3:1 before COVID-19. The latter largely consists of a dividend paid to the government by Petronas, the national oil company. The banking sector is thus just one of many sources of government funding. Having said that, the government also draws a dividend from its sovereign wealth fund, Khazanah, with a historical range of RM1–3 billion. 58 Khazanah derives a significant share of its investment income from bank dividends, including through its investments in CIMB.

Thus, at first glance, in its internal relations the potential of banks to exercise structural power has been limited not just by state shareholdership but also by the government's ability to access alternative sources of funding. Additionally, and somewhat paradoxically, their structural power seems weakened by the limited contribution to national development that banks have made historically, which led the government to develop an alternative framework for industrial funding that also served its ambitions to cultivate a bumiputera commercial and industrial class. 59 However, at the same time regulators champion their banks at the regional and international level.

Moreover, in Malaysia's distinctive model of shareholder-state capitalism, the state and its GLICs rely significantly on bank dividends for performance legitimacy, and also on income. This means the government is hesitant to undertake steps that would threaten banks’ profits. Similarly, banks’ “unproductive” lending to households means that they have come to play a significant role in households' wealth accumulation, once more strengthening their structural power. This is in addition to wider developmental aspirations, such as the role of Malaysia as an international Islamic financial center, or the contribution envisaged for the financial sector in moving Malaysia up the value chain, including through the creation of high-skilled jobs.

Nigerian banks’ ability to exercise structural power is, as in Malaysia, highly contingent. On the one hand, there are a couple of factors arising from banks’ business models that limit the ability of banks to exercise structural power. As already outlined above, banking sector credit to the private sector is low, and only a minority of that lending goes to development priority sectors. 60 Low private sector lending, not only by comparison with Malaysia but also by African standards, has been the subject of consistent criticism of the CBN and other government officials lamenting that Nigerian banks do not fulfill their developmental role. 61

The damage that banks may inflict upon Nigeria's economy by realizing a threat to withhold investible funds from the real economy is limited, because banks not only channel credit to sectors that the government does not consider a priority for development, but the government, very much aware of the limited contribution of banks to financing development, has also used its oil revenues to set up its own funding mechanisms. These range from credit lines set up by the central bank to government-owned development banks that substitute for bank lending and inject liquidity in times of crisis. Similarly, the state relies to a major extent on its oil revenues as a source of finance rather than tax revenues from major private corporations like banks. Indeed, about 50 percent of government revenue originates in the oil and gas sector, and these revenues also substitute for banks’ investment in government bonds. 62 As a result, the government has a considerable amount of resources under its control that can substitute for those of banks in financing the state, limiting banks’ structural prominence. Finally, exit does not even seem credible, given how profitably banks operate in Nigeria owing to the high interest rate differential. As outlined in the last section, banks’ margins are high, risk-free lending to the government is profitable, and the major banks occupy a position of market power with limited competition. Banks with high exposure to the oil sector (constituting about 30 percent of all loans) can also expect their profits to increase whenever oil prices rise. 63 Moreover, the state's control over oil revenues also increases banks’ space to pursue risky but profitable strategies, since banks know that the government has the ability to bail them out if it is willing to do so in the event of failure. 64

That being said, in Nigeria's financialized economy some of these factors, which could potentially reduce banks’ ability to exercise structural power, may actually enhance their role in the envisaged economic model as financial motives become more prominent. In particular, Nigerian commercial banks are major holders of domestic government debt and thus central to the government's ambition to develop sovereign bond markets and, more generally, the achievement of its development strategies. Moreover, most of banks’ lending goes to oil and gas, which is central for the growth trajectory of Nigeria's resource-dependent economy. In the aftermath of the consolidation, there has also been an increase of bank lending to finance and insurance. The FIRE sector, in turn, has also come to play an increasingly important role in shaping Nigeria's growth trajectory since the 2000s, with the value added of the finance and insurance sector to GDP averaging 15 percent between 2010 and 2020. This figure is considerably higher than in Malaysia, where the value added averaged 7 percent between 2010 and 2019, although we should keep in mind that these numbers might well be affected by the vastly larger size of the informal economy in Nigeria. Given the government of Nigeria's goal to enhance economic growth quickly, the government is not taking major actions to reduce lending to the financial sector.

In fact, the Nigerian government has in a series of planning exercises outlined strategies to foster the financial sector. As already mentioned, the FSS 2020 not only envisaged Nigeria to have “the safest and fastest growing financial system amongst emerging markets” to drive “rapid and sustainable growth” but also devised a set of reforms aiming, among other things, to make Nigeria “Africa's financial center of choice.” 65 While Nigeria's systemic banking crisis of 2009–10 put several elements of the FSS 2020 on hold, the central bank used its stability and developmental mandate to implement a financial inclusion strategy that aimed at developing an “enabling environment” for the banking sector to not only support the small, medium, and microenterprises sector but also to provide financial services, including credit, to households. 66 From the perspective of the CBN, the enabling role of regulators in driving financial inclusion helped to achieve the government's commitment to make Nigeria one of the top twenty economies by the year 2020, while financial institutions were seen to benefit by expanding “business into the untapped, potential market of the unbanked and underserved people.” 67

A recent development plan, the Economic Growth and Recovery Growth Plan, also set for 2017–20 the following three objectives for the financial sector: to increase the volume of assets and the diversity of financial instruments; to review the capitalization of financial institutions; and to encourage lending at affordable costs to agriculture and manufacturing sectors through syndication with development banks. 68 What emerges from these planning exercises is that finance is conceived as both a driver of real economic development and a growth sector of its own. Importantly, the financialized development model embedded in the government's planning envisages a role for banks that goes far beyond the role they currently play in driving development.

Thus, in a context where the government seeks to promote growth through developing a strong, privately owned financial system, it is not surprising that the government tries to avoid antagonizing major banks, fearing implications on growth and investment, and that we see an alignment of interests in some areas. In particular, the authorities have, while capital inflows are largely liberalized, avoided giving bank licenses and allowing ownership stakes exceeding 10 percent to foreign banks in an effort to create strong, nationally owned banks. 69 This also served to protect domestic banks from increased competition. Another example of the financialized developmental model leading to responsiveness to the interests of banks is that the CBN often exercises regulatory forbearance with Basel II regulation out of fears that bank interventions limit banks’ ability to support development. 70 It is also telling that despite frustration with limited private lending to the real economy, the CBN refrained from reintroducing directed credit allocation guidelines but has provided subsidized credit lines for on-lending that banks are requested to promote and credit guarantee schemes. In doing so, it is the CBN, rather than the banks, that shoulders the actual and potential costs of the expansion of lending.

Nevertheless, banks, especially small ones, do not always get what they want. For instance, while banks were against the CBN's forced banking sector consolidation of 2004, the economic costs fell disproportionally on smaller banks. As a senior IFI official noted, “For some banks the mergers did not do much damage; for some it meant a major damage.” 71 Similarly, when the CBN introduced Basel II in 2013–14, some banks, especially the smaller ones, found their objections to these standards ignored. 72 Nigeria's case thus underlines the finding of extant research that structural power refers to a set of advantages that some, not all, firms enjoy. 73 Overall, however, the picture that emerges is similar to the one in Malaysia: large banks have structural power because of the aspired for rather than actual role of finance in supporting growth and development.

The Exercise of Structural Power at Times of Crisis: Responses to the COVID-19 Pandemic

In normal times, the extent to which structural prominence translates into structural power is highly contingent and has changed over time. How do these dynamics unfold at times of crisis? In the following discussion, we will highlight some of the issues that arose in the context of the COVID-19 pandemic that started in early 2020. The Malaysian approach was perhaps the most stringent for the banks. In late March 2020, Bank Negara imposed a blanket moratorium on loan repayments and suspended enforcement action. 74 It affected 80 percent of loans outstanding and was taken up by 93 percent of individual borrowers (households could voluntarily continue to repay their loans) and 95 percent of SME borrowers. The costs, estimated to have amounted to close to RM100 billion, were primarily borne by the banks; however, Bank Negara implemented a number of interest rate cuts, extended reporting time frames, and also allowed banks to draw down capital buffers. This is in the context of significant debate during the Asian crisis about NPL classifications (IMF mandated three months vs. the Malaysian preference for six months)—with the tighter reporting requirements at the time seen as a key factor in the depth of the crisis. In September 2020, responding to bank lobbying and a relatively successful management of the pandemic, Bank Negara shifted to a system of more targeted assistance.

Thus, while the severity of policy measures at first glance indicates a shift in the power balance between government and banks in favor of the former, their preferences were actually closely aligned given the lasting impact of the Asian crisis, and debates about loan classifications, in the memories of financial elites. In the context of high levels of household debt, preventing defaults was a core concern of both policymakers and the banks, given their exposure. As it became clearer that the impact of the crisis on the banking system was manageable, banks increasingly assertively realized their preferences.

Nigeria was hit hard by the pandemic, experiencing a significant decline in economic growth due to a combination of a pandemic-related lockdown in 2020, plunging oil revenues due to a fall in the demand for oil, and sharp capital outflows in the first quarter of 2020, with the latter two significantly increasing balance-of-payments pressures. 75 Despite limited fiscal space due to the decline in oil revenues in 2014 and a government revenue-to-GDP ratio at only 8 percent in 2019, which is among the lowest in the world, the government responded strongly to the crisis. In finance, notable measures included a one-year moratorium on principal repayments for CBN intervention facilities, new government and CBN facilities for providing subsidized credit for companies and households, interest rate reductions and later a moratorium on loans from the government's subsidized credit lines, a reduction of the monetary policy rate, an increase in the loan-deposit ratio to encourage bank lending, and regulatory forbearance to banks to restructure terms of facilities in affected sectors.

What is clear is that the response of the Nigerian government to the COVID-19 pandemic in relation to the banking sector is in line with its general approach to bear much of the costs of financing development on its own rather than shifting those costs to the banks. The COVID response thus epitomizes the shift in the CBN's approach from direct interventions in the banking sector to encourage lending through policies such as credit allocation guidelines toward “de-risking.” 76 While the increase in the loan-deposit ratio forces banks to lend to the private sector, the measures limit the costs borne by the banks. This is because the banking sector has been resilient, as banks entered the crisis with adequate capital buffers and high profitability, which they are now tapping into. Instead, the Nigerian government negotiated significant loans from the IMF, the World Bank, and the African Development Bank to finance its response.

Structural Prominence and Power in the Context of Financialization

In both case countries, the greater structural prominence of the banking sector has not straightforwardly resulted in greater structural power. Indeed, the impact of what the literature identifies as a key feedback mechanism—investment strikes—has been mixed, given the limited role that banks have traditionally played in providing financing for productive purposes, a trend that has been sharpened by emergent consumer debt regimes. Moreover, policymakers are well aware of the limited contribution banks make to meeting investment and development imperatives. They have proactively sought to establish alternative funding mechanisms: development banks, nonbank development financiers, and bond markets, often increasingly acting in tandem, for example, when development banks and nonbank development financiers finance themselves via debt capital markets. Banks, and the financial sector more generally, have nevertheless come to play an increasingly important role in putative development strategies.

Indeed, the structural transformation of the banking sector, discussed in an earlier section, in itself has been part of this trend. It is reflective of governments’ ambitions to establish domestic banks that are competitive not just vis-à-vis foreign market entrants but also in regional and international markets. In this context, then, the adoption of international standards supports the ambitions of the largest banks as well as their demands for market access, while at the same time proving costly for their smaller domestic competitors. The result is increasingly stratified domestic banking sectors with significant structural power residing with the largest—but not smaller—banks.

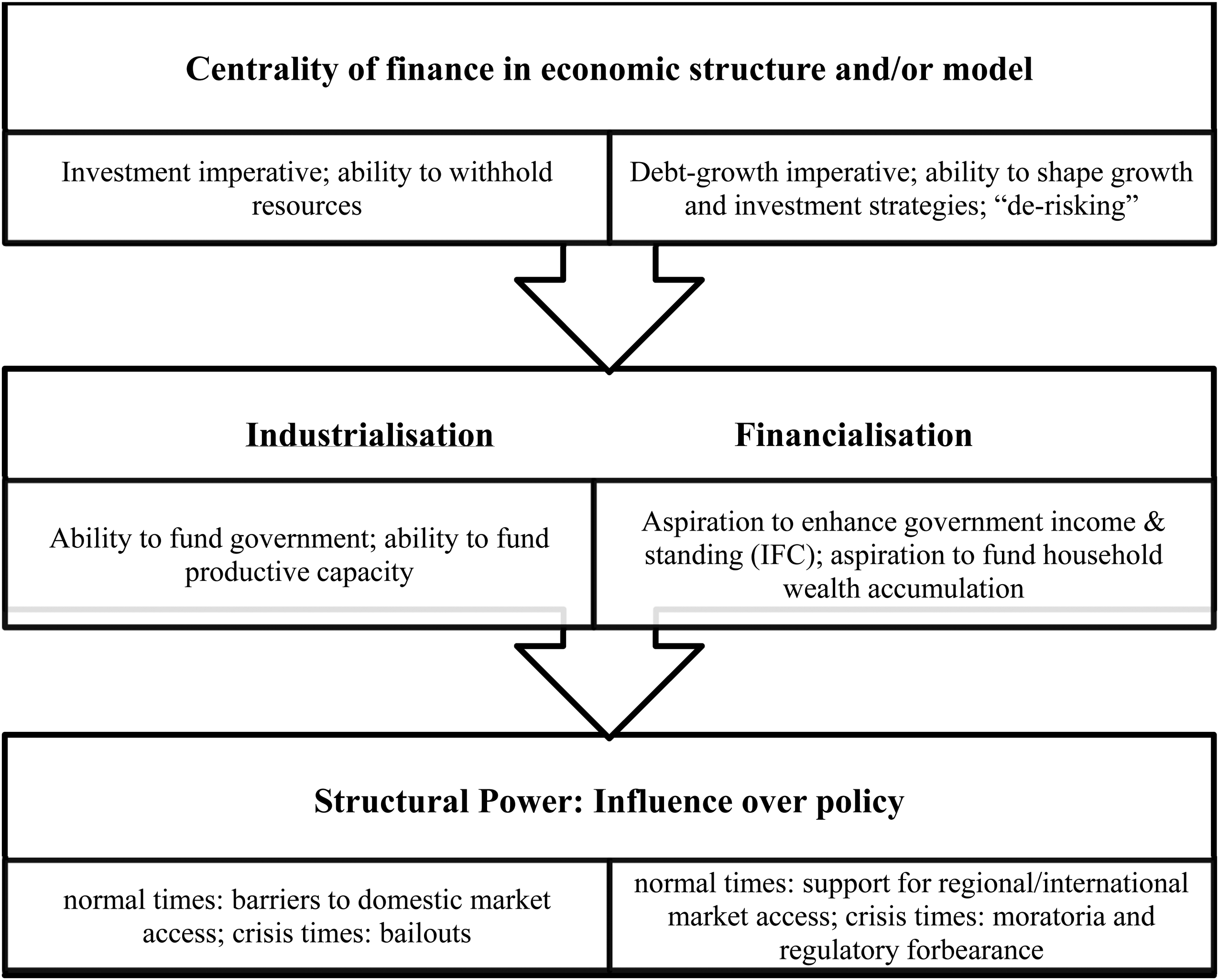

These trends necessitate a reconceptualization of how the structural power of finance operates in an era of heightened financialization and how it affects its sources, contexts, and implications. Figure 5 provides an overview of our enhanced model of structural power in financialized developmental contexts.

Structural power in financialized developmental contexts.

If in the traditional model emphasis rested on states seeking to meet the investment (or development) imperative, then in a financialized developmental context, debt-financed growth and household wealth accumulation are becoming proportionally more important. This generates new interdependencies between the financial sector and politics. 77 This is directly linked to the shift in the proportion between financial and physical (or productive) assets identified in the quotation from the Malaysian Securities Commission in an earlier section. In so doing, finance comes to play an increasingly important role not just in supporting (or boycotting) industrial policy via the (non)provision of funding but also in shaping investment and growth policies. Where previously governments introduced investment-friendly policies, adhering to the “embedded financial orthodoxy” of the “competition state,” 78 in financialized developmental contexts the aim to create a finance-friendly macroeconomic environment becomes increasingly focused on helping finance to achieve high returns, for example via “de-risking” investments. 79

This is closely linked to shifts in the context, if not even raison d’être, of policymaking away from supporting industrialization and structural transformation to enhancing the (global) standing of financial sectors (and by extension the reputation of governments) and the wealth accumulation of a growing middle class. This also reflects the relative decline in income from labor versus income from (financial) assets. In Malaysia, this has been part of an increasingly overheated housing market, fueled by household debt. In Nigeria, it is an aspiration that also underlies much of the government's financial inclusion drive. Nevertheless, in both countries it has contributed to ascribing to the banking sector an importance that would not be warranted if we looked at bank funding for industrial growth alone. Moreover, support for banks is not only reflected in their privileged domestic position, protected for example by barriers to market access, but also in the support that financial authorities in both countries lend to the regional, if not even international, ambitions of their domestic banks.

Conclusion

Banking systems in sub-Saharan Africa and Southeast Asia have witnessed significant structural change. As the experiences of Malaysia and Nigeria illustrate, policymakers in DEEs shaped the structural transformations of their banking sectors in a context of international financialization and strong material pressures to support economic development. Owing to government-led initiatives seeking to create strong, internationally competitive banks, banking sectors became more consolidated, in turn affecting banks’ business models. 80 These structural transformations, which have to be seen in a wider context of the growing prominence of financial developmental planning in DEEs, reflective of and reinforcing the adoption of increasingly financialized ideologies, took different forms in Malaysia and Nigeria. Yet, the pursuit of financialized developmental models, while reflecting variegated forms of financialization, in both countries nonetheless enhanced banks’ structural power, for instance by raising banks’ contribution to the financing of public debt or increasing credit to the private sector. In turn, this supports finance's ability to shape growth and investment strategies. Nevertheless, it is important to reiterate that states can pursue financialization both as a substitute for, or in conjunction with, industrial policy and consequently seek to combine or substitute the pathways identified in this enhanced model.

Prima facie, domestic banks were confronted with a number of limiting factors when it came to exercising structural power. First and foremost, in both countries policymakers had reasserted their agency through the use of state resources to finance developmental projects to substitute for banks’ resources. Similarly, the perception among the authorities that banks fail to play their envisaged role in development reduced their concerns that policies that violate banks’ interests might inflict major damage to the economy. This was temporarily evident at the beginning of the pandemic when Malaysia imposed a blanket moratorium on loan repayments in the context of high levels of household debt.

That said, our analysis suggests that one factor, namely, financialized development strategies, critically augments the structural power of banks, even in a context where a number of factors limit banks’ actual contribution to financing productive investments. Such strategies, often captured in financial development plans, envisage a central role of the financial sector in national development. As a result, governments seek to nurture, as our analysis suggests, their banks by aligning their interests with banks they consider as national champions and being responsive to their policy preferences.

Our analysis yields three broader insights for debates about the structural power of finance in financialized capitalism. First, the debate about the roots of structural power of finance in financialized capitalism is far from settled. Much of the extant literature considers only the actual contribution of finance to productive investment to assess its power. Yet, as the discussion of our DEE case studies suggests, even in contexts where the actual or perceived contribution of finance to support productive investments may be restrained, banks’ structural power may be considerable because of the envisaged role of finance in supporting growth of the real economy or financial sector in financialized development models. In other words, financialization, as a result of structural changes, may give rise to financialized ideologies and give greater prominence to financial actors and their preferences. Thus, considering solely the actual centrality of finance in an economic model may not be sufficient to assess the potential of finance to exercise structural power; its aspired-for role also warrants closer scrutiny.

Second, and relatedly, structural power is highly contingent. As our analysis shows, perceptions of the centrality of finance in the operation of the economy matter for structural power. This centrality can, to some extent, be manipulated by governments, for instance through government shareholdership in major banks or the strengthening of development banks. Where governments have control of low-conditionality resources, such “manipulation” may be easier, but as Naqvi notably shows, alliances between the state and popular movements may also facilitate efforts to counter banks’ structural power. 81

Third, our analysis highlights the agency developing country governments have in financialized capitalism, even though this agency is exercised from a position of subordination to international currency and regulatory hierarchies. Banks’ centrality in the operation of the economy is, to some extent, the result of government policies to create large, domestically owned internationally competitive banks; hence, banks’ structural power results partly from national and sectoral development planning. Similar to what happened at the macro level, DEE states have played a crucial role in the emergence of powerful domestic financial actors. 82 In the short term, this may serve to shore up their own legitimacy, but in the long term it carries the risk of contributing significantly to financial sector moral hazard, creating institutions that are just too big to fail. That being said, it is clear that it is precisely those structural limits to DEE policymakers’ agency, imposed by developing countries’ position in global economic hierarchies, that push them toward financialized developmental models, often limiting further resources that could be channeled toward industrialization.

The analysis presented in this article provides an important step toward conceptualizing the structural power of domestic finance in DEEs, but more work needs to be done to test the robustness and generalizability of our model and add further nuance. There are two potential avenues of future research that we consider as especially important, the first conceptual, the second empirical.

Conceptually, work on structural power has tended to be anchored in the experience of a rather small number of rich countries. As a consequence, this work has tended to conflate economic structure with industrial economic structure. However, in many DEEs industrialization has always at best been rather incomplete; industrial sectors tend to be small and coexist with large informal economies. Moreover, and increasingly so, countries in the Global South confront the phenomenon of what Malaysian political economists have dubbed “premature deindustrialization”: 83 the decline of manufacturing capacity before full industrialization has been achieved. Thus, there is a need to reflect on the centrality of an industrial economic structure for notions of structural power, both historically and contemporarily.

Empirically, and as our case studies have also highlighted, countries pursue various forms of financialization with various degrees of success. In this context, more work is required to distinguish between financialized developmental models, for example, between nascent financialized developmental models (Nigeria) and consolidated financialized models (Malaysia).

Footnotes

Acknowledgments

We thank Louis O'Sullivan for research assistance. We are grateful for feedback on earlier versions of this article provided by the Politics & Society editorial board, Ayca Zayim, Sandy Hager, Natalya Naqvi, and Leon Wansleben, participants at the “Structural Power in Financialised Capitalism” workshop, and seminar audiences at the Universities of Cambridge and Passau.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

Lena Rethel acknowledges support from the Leverhulme Trust (RF-2018-452).