Abstract

How do we theorize and analyze the structural power of finance when global capitalism itself undergoes constant and profound structural transformation? The literature continues to assume that the source of financial structural power is its unique ability to provide credit to the real economy, playing a crucial role in meeting the investment imperative. But recent research documents that most financial market activities no longer facilitate productive investment and can even be a drag on economic development. If the financial sector's primary role is not to support productive investments, then on what basis does it continue to hold structural power? The contributions to this special issue engage with how decades of financialization have transformed the basis of structural power toward alternative functions that have gone unnoticed in the existing literature. These include household and real estate lending that fuels consumption-led growth, concentration and expansion of financial institutions as tools of geo-economic strategy, financing current account deficits that facilitate global imbalances, and wealth preservation that bolsters inequality.

Plenty has been made of the structural power of finance, and a large body of research has now been amassed demonstrating how it affects outcomes in the global economy. But how do we theorize and analyze this power when global capitalism itself undergoes constant and profound structural transformation? This question provides the foundation for the diverse range of contributions to this special issue.

The literature continues to assume that the source of financial structural power is its unique ability to provide credit to the real economy, playing a crucial role in meeting the investment imperative. But recent research has documented that much of the financial sector does not facilitate productive investment and can even be a drag on economic development. If the financial sector is no longer playing a productive role, then on what basis does it continue to hold structural power? What do the changes in the form and function of the financial sector since the 1980s mean for its structural power?

Approaches to Structural Power: Old and New

In the late 1960s and 1970s, a debate surfaced over the source of capitalist power. 1 On the one side was the instrumental view, which held that capitalists exert power by drawing on inordinate resources to directly and purposefully pressure governments into adopting policies in their favor, primarily through campaign financing, lobbying, and elite social relations. On the other side was the structuralist view, which claimed there is an inherent bias in capitalist economies, one that favors private businesses as the main controllers of investment in the productive economy. According to proponents of the concept of structural power, business need not exert direct influence over government to secure favorable outcomes. In capitalist democracies, governments are dependent on votes to stay in power and tax revenues to finance the state apparatus, both of which, they argue, hinge on maintaining high levels of productive investment, employment, and growth. Both electoral success and a healthy tax base depend on a thriving economy, and a thriving economy, in turn, depends on the state of business confidence. If a government implements policies that undermine business confidence, then business may respond with a recession-inducing “investment strike” that damages the incumbent's prospects for reelection. From the perspective of structural power, the looming threat of an investment strike disciplines governments, regardless of their ideological leanings, into adopting policies that work in the interests of capital.

The early literature on structural power conceived of investment strikes as the power to withhold investment from the domestic economy. But in a world of heightened capital mobility in the 1980s and 1990s, researchers began to emphasize how business has the ability not only to withhold investment at home but also to move their investments across jurisdictional lines. 2 Capital mobility enhances the structural power of business by intensifying competitive pressures on governments to design policies that will attract investment. It was in this context that increasing attention was also paid to the distinctiveness of the financial sector's structural power. In this early literature, finance was considered particularly powerful compared to other forms of capital precisely because it is the most mobile across borders. Mobility, combined with the fact that finance is intimately linked to other sectors, means that it has great potential to reduce investment and inflict economic damage. 3

In the aftermath of the global financial crisis of 2008, a new wave of research on the structural power of finance emerged with the bank rescue schemes in various jurisdictions serving as a catalyst for new inquiries. Decisions to bail out some financial institutions in the United States and the European Union that were deemed “too big to fail” without dragging the real economy down with them underscored the important structural position occupied by these institutions in their respective economies and provided apparent support for arguments about the structural power of finance. 4 In addition, scholarship highlighted the variation in bank bailouts and financial reforms across jurisdictions, and this variation was explained with reference to the national diversity in the structural power of finance and perceptions of such power. 5

In exploring how the structural power of finance varied across space and time, and even between individual financial institutions, scholars also engaged with the criticism that structural power arguments were too deterministic and thus unable to explain why business wins some political conflicts but loses others. 6 In fact, the first wave of research on structural power had neglected the role of agency and the importance of perceptions in explaining the variance of capital's structural power even though government fears about potential disinvestment “depend on how credible policymakers believe the threat to be.” 7 Addressing this weakness, Culpepper and Reinke, for instance, show in their comparative analysis of UK and US bank bailouts in the aftermath of the global financial crisis that although structural power can work automatically, financial institutions can also deploy it deliberately, with strategic intent. 8 Bell argues from a constructivist perspective that “power is not just an objective condition but is shaped subjectively and inter-subjectively; it is a relational artifact, produced and mediated through social and ideational realms.” 9 The problem was not that theorists of structural power had failed to acknowledge the fact that capital did not win every conflict. Block, for instance, emphasized that under certain conditions such as war and depression, the structural power of capital wanes. 10 But what was missing is a systematic understanding of such conditions and the factors shaping variation in structural power.

Eschewing the perceived determinism of earlier accounts of structural power, studies in the postcrash years prompted not only investigations of the conditions under which finance wins but also of the conditions under which it loses. 11 And rather than treat the structural and instrumental power of finance as a strict binary, postcrash analyses have brought considerable nuance to the debate by exploring the ways in which these forms of power interrelate and the conditions under which one form prevails over another. 12

Financial Power Meets Financialization

As this brief discussion of the literature shows, the study of the structural power of finance has witnessed plenty of changes over the past three decades. But crucial issues remain unresolved, some of which strike at the very heart of the notion of structural power. In particular, the existing literature continues to assume that the source of financial structural power is its unique ability to provide credit to the real economy, thus playing a crucial role in meeting the investment imperative. 13 We, however, have serious doubts that emphasizing this functional role of finance in the macroeconomy alone can underpin structural power arguments today.

This is because several key developments in core capitalist economies, often lumped together under the term “financialization,” contradict the assumed importance of finance in enabling capital investments as a crucial channel for generating employment and growth. On a macroeconomic level, scholars have shown that, at a certain threshold, deep and sophisticated financial systems can actually become a burden on growth. 14 As financial systems expand beyond a tipping point, economic volatility and the probability of economic crashes increase. 15 However, this is not the only reason why there can be “too much” finance. 16 Additionally, economists have suggested that in larger financial systems, the misallocation of credit increases and rent-seeking activities proliferate, as indicated by constant unit costs of financial intermediation amid rapid technological change. 17 Most importantly, as larger financial systems reinforce inequality, they suppress growth by reducing the purchasing power of those with the highest propensity to consume. 18

The “too much finance” argument closely relates to another perspective on the contemporary role of finance in core capitalist economies, which comes from the “secular stagnation” literature. 19 As this literature argues, demographic trends and rising inequalities increase the supply of, and lower the demand for, capital. We thus confront a situation of capital abundance and a scarcity of investment opportunities, with the result that overall interest rates decline. As just one indication of this trend, firms not only reduce their investments but also increasingly finance these activities with retained earnings. 20 On the face of it, this seems to suggest that firms’ dependencies on actors controlling the means of financing decline rather than increase, raising the question of how finance exercises power over firms (see Braun's contribution in this special issue). To some extent, lending to other sectors, particularly governments and households, 21 compensates for this weakened finance-investment nexus. Along these lines, Baccaro and Pontusson argue that, in some countries, credit to households has become a (fragile) growth driver in its own right. 22 But how financiers exercise structural power via their control over household credit, and to what extent policymakers (particularly central banks) cater to actors feeding household debt bubbles, is still poorly understood.

Significant changes within financial sectors also raise new questions about structural power. Classic bank-lending has lost out proportionally to market-based financial intermediation. This has gone hand in hand with the continued ascendency of shadow banks and asset management firms, 23 which earn their profits through fees. We know that aggressive investment firms such as private equity can extract considerable surplus from nonpublic investments, but how exactly they achieve such returns remains underresearched. Indeed, much of the existing literature suggests that financiers do not use threats of exit to gain profits but exploit their organizational power over companies to restructure assets and liabilities in their own favor. 24 Moreover, “investment chains” or “global wealth chains” have been extended to render increasingly opaque how ultimate beneficiaries, actual owners, their fiduciaries, and various other intermediaries relate. 25 Those impacting actual corporate decisions or government policy are often those managing “other people's money” rather than those providing their own funds. Complexity is further increased through the use of sophisticated financial instruments, like interest rate, exchange rate, or credit default derivatives. 26

While these arguments relate to strongly financialized core capitalist economies, the challenges for reformulating structural power for developing countries are just as large. In this group, financial repression during the postwar era was widespread. Governments used interventionist tools to channel credit to priority sectors considered important for fostering industrialization. Under this system, the financial sector functioned largely as a utility servicing the needs of real economy firms and was rarely a highly profitable sector in and of itself.

Under the neoliberal Washington consensus, developing country governments began to move away from statist developmental policies to embrace economic liberalization in response to external and domestic pressures. Formerly interventionist governments began to liberalize and deregulate their financial systems by abandoning capital controls, privatizing domestic financial institutions, and eliminating interest rate and credit controls. 27 It was expected that capital account liberalization would permit financial resources to flow from capital-abundant developed countries where returns were low, to capital-poor developing countries where returns were higher. This was supposed to increase the pool of investible resources, lower the cost of capital, and increase investment and growth in recipient countries. 28 Similarly, domestic financial deregulation was expected to increase savings and encourage rational, market-based lending decisions, improving the availability and allocation of domestic financial resources and ultimately boosting investment to support economic development. 29

This has played out somewhat differently in reality. In the 1980s, the abandonment of capital controls, combined with rising interest rates in the United States, resulted in a drought of capital. 30 Since the 2000s, although low US interest rates combined with no (or minimal) capital controls have dramatically increased short-term capital inflows into developing and emerging countries, this has not been channeled into productive real sector investments. Instead, these inflows have gone mainly into financial investments, which although profitable in the short term, do not necessarily increase long-run productive capacity. 31 Domestic deregulation has exacerbated this situation by allowing domestic financial institutions to misallocate resources in a similar manner. 32 The result has been declining real investment and increased volatility in domestic asset prices, interest rates, and exchange rates. 33 This volatility in turn weighs further on productive investment decisions, undermining the broad-based growth that developing countries need to overcome their subordinated position in the global economic hierarchy. The rise of international financial centers has exacerbated this situation by facilitating outflows of investible funds by the transnational companies and domestic elites in developing countries. Not only did easier access to international financial markets fail to strengthen developing countries’ productive economies; it has increasingly exposed them to global financial cycles. 34 This in turn has dramatically increased the likelihood of runs toward the main international currencies and ensuing financial crisis. 35

Should we then predict that, since finance does not seem to play its role in facilitating productive investments, its structural power has waned? In fact, whether you look at financial policies (weak regulatory responses to the global financial crisis, extended backstops for markets, quantitative easing) or other policy areas (low taxation, privatized social security, etc.), we see no signs that governments have become less responsive to financial firms’ interests. The same is true in the corporate world, where third-party funding has come to dominate in international investment arbitration and share buy-backs and other strategies are used to maximize shareholder returns. 36 Moreover, in the developing world, governments have increasingly embraced financialization as a growth strategy. This raises a crucial question. If finance no longer relies primarily on its role in facilitating real economic investment, what then is the basis for its continuing or even growing structural power?

To address this puzzle, the contributions to this special issue contend that the study of the structural power of finance must do much more to engage with major transformations in the global economy and in the financial sector itself. In particular, the structural power of finance must be examined against the backdrop of processes of financialization within and across national economies. This perspective allows the contributors to consider how finance derives its structural power from functions that have gone unnoticed in the existing literature, such as household and real estate lending that fuels consumption-led growth, concentration and expansion of financial institutions as tools of geo-economic strategy, financing current account deficits that facilitate global imbalances, and wealth preservation that bolsters inequality.

Summary of Contributions

The first contribution to our special issue, from Ayca Zayim, goes beyond the advanced country focus of the existing literature on the structural power of finance to examine how it operates in developing and emerging economies (DEEs). Zayim's article analyzes financial power in the context of Turkey's financialized (debt-led) growth model, which emerged after the country's banking crisis in 2001, but which gained even further momentum after the global financial crisis. One of the features of Turkey's financialized growth model is increasing dependence on foreign capital. Rather than propelling productive investment in the “real” economy, these capital inflows instead helped to fuel a construction boom and household consumption.

The Turkish case offers an intriguing puzzle. According to conventional wisdom, increasing dependence on foreign capital should make the threat of exit more viable, thereby heightening the structural power of finance. Yet from 2010 to 2014 the Central Bank of the Republic of Turkey (CBRT) managed to engage in an unconventional form of monetary policy, one that, as evidenced in interviews conducted by Zayim, went against the interests of powerful financial actors. Aimed at discouraging hot money flows, this policy of “managed uncertainty” entailed a purposeful generation of ambivalence regarding the movement of short-term interest rates.

Why, then, was Turkey able to exercise this policy autonomy, despite its heavy reliance on foreign capital and despite its subordinate position in the international currency hierarchy? As Zayim makes clear, the CBRT's ability to engage in unconventional monetary policy hinged in important respects on global liquidity conditions. In the aftermath of the global financial crisis, Turkey, like many other emerging market economies, saw an influx of foreign capital, as private investors responded to the easing of monetary policy in advanced economies by chasing higher-yield assets elsewhere. In short, abundant global liquidity opened up policy space allowing the CBRT to experiment with managed uncertainty without spooking investors. And when global liquidity started to gradually dry up in 2013 with the US Federal Reserve's tapering talk, the CBRT's policy space to engage in managed uncertainty began to narrow significantly.

There are two main lessons to draw from Zayim's research on the Turkish case. First, while the existing literature emphasizes how the structural power of finance is contingent on a country's degree of external financing, Zayim reveals how it is also contingent on the source and cost of that external financing. In other words, structural power can be attenuated with abundant and cheap capital. Second, Zayim's research illustrates the necessity of anchoring the analysis of finance's structural power in a global context. Especially for emerging markets like Turkey, sustained policy autonomy is often elusive and shaped externally by the gyrations of the “global financial cycle.” 37 Though the postcrisis ideational shift in central banking may have aided the CBRT in legitimizing its quest for managed uncertainty, Zayim shows that it was Turkey's subordinate position in the international currency hierarchy that proved decisive in the adoption, and subsequent abandonment, of an unconventional policy stance.

In their contribution to the special issue, Florence Dafe and Lena Rethel provide further insights into finance's structural power in DEEs. Through a comparative analysis of Malaysia and Nigeria from the early 2000s to the present, Dafe and Rethel, like Zayim, begin with a puzzle. In both Malaysia and Nigeria, the major banks do not play a significant role in the financing of productive investment and yet they wield considerable power. How do we make sense of this given that much of the existing literature assumes the structural power of finance rests on its ability to withhold investable funds from the real economy?

Dafe and Rethel point to the centrality of financialized development strategies in DEEs, which they argue enhance the structural power of major banks despite their limited role in financing productive investment. Here once again the global context is crucial. Dafe and Rethel point to myriad factors that currently undermine the feasibility of industrialization as achieved by the East Asian development states: prohibitive international rules regarding trade, finance and investment, secular stagnation, and limited and volatile capital flows, as well as competitive pressures from other emerging markets, especially China, and giant industrial MNCs headquartered in the advanced economies. With the path to industrialization fraught with so many challenges, DEEs often turn to other development strategies, including financialization as a substitute for, or complement to, industrial policy. In recent years, governments in DEEs have embraced financial development plans that make the financial sector itself a key target for development. As Dafe and Rethel explain, these financial development plans include measures to enhance the international competitiveness of domestic banks and to establish international or regional financial centers, as well as efforts to expand household access to financial markets. It is within this setting of financialized development that the structural power of major banks is able to thrive.

Drawing on Kevin Young's distinction between structural prominence and structural power, 38 Dafe and Rethel are careful to differentiate the expected causes of the power of large banks from its hypothesized effects. As a key indicator of structural prominence, Dafe and Rethel chart the rise in bank consolidation in both Malaysia and Nigeria from roughly the late 1990s to the global financial crisis. The promotion of banking sector consolidation was part and parcel of state-led financialized development planning; its aim was to create large, internationally competitive financial institutions that would spur economic growth and enhance the reputation of the Malaysian and Nigerian governments. Though consolidation eventually abated in the decade after the crisis, it had lasting implications, fundamentally transforming the business models of large banks in both countries.

In Malaysia, consolidation was accompanied by low interest rate spreads (i.e., between deposit and lending rates), low profit margins, but also lower default risk for domestic lending. The large Malaysian banks responded to these conditions by increasing their lending to middle-class households and the government and by embarking on regional expansion. In Nigeria, consolidation went hand in hand with relatively high interest rate spreads, which prompted large banks to shift their core business activity from foreign exchange trading to lending. Though the largest share of this lending went to the oil and gas sector—deemed a development priority by the Central Bank of Nigeria (CBN)—much of it also flowed to so-called nonpreferred sectors: finance, insurance, real estate, construction, and import finance. Large banks also play a key role in lending to the Nigerian government, helping it to reduce its reliance on external debt.

How did enhanced structural prominence, coupled with the transformed business models of large Malaysian and Nigerian banks, translate into structural power? In both countries, Dafe and Rethel point to several factors that limit the exercise of structural power, including few opportunities to engage in investment strikes and heavy state involvement in the financial system. Yet the structural power of large banks is nonetheless considerable and is augmented by the financialized development strategies pursued in both countries. Crucially, Dafe and Rethel claim that the structural power of large banks may not be based on the actual centrality of finance to the Malaysian and Nigerian economies. Instead, the structural power of large banks may in large part be attributed to “wishful thinking” on the part of regulators, who aspire to foster a central role for finance in their economies. In normal times, governments thus champion their banks, supporting their lending activities both domestically and abroad, as evidenced, for example, in the Malaysian government's efforts to promote the country as an international Islamic financial center. In times of crisis, governments support the large banks by engaging in regulatory forbearance and coordinating moratoria on debt repayments that prevent market-destabilizing defaults. During the early onset of the COVID pandemic, both Bank Negara (the Malaysian central bank) and the CBN implemented moratoria and other targeted interventions reflecting the preferences (and in some instances the lobbying efforts) of large banks.

The comparative analysis of Malaysia and Nigeria brings new insights to our understanding of the structural power of finance. As Dafe and Rethel explain, the existing literature has demonstrated how the perceptions of policymakers can influence the actual structural power wielded by business. But what has been often overlooked in the existing literature, and what is crucial to the study of Dafe and Rethel, is not only perceptions of actual structural power but perceptions of the envisaged role of that structural power within the development process. Thus policymakers’ aspirations for their own financial sectors reinforce the power of large banks. Taking into account the global context, the contribution of Dafe and Rethel also highlights the subordinated agency of policymakers in DEEs. Though policymakers in Malaysia and Nigeria had agency in implementing financialized development strategies that, at least in part, reflected some national priorities, they were nonetheless severely constrained in their abilities to pursue traditional industrialization. As with the Turkish case during the period of managed uncertainty, the Malaysian and Nigerian experiences over the past two decades illustrate how the structural power of finance stands in the way of sustained policy autonomy in DEEs.

The setting for Elsa Massoc's contribution to the special issue is Western Europe in the decade following the global financial crisis. In the early aftermath of the crisis, the dominant position of European banks was under threat, as politicians and policymakers vowed to break up “too big to fail” financial institutions. Yet in the postcrisis period most of the major banks have continued to grow in terms of their global systemic importance; their balance sheets, as well as their off–balance sheet activities, have expanded, and their business models remain largely intact. Why has this been the case? And what does it have to do with structural power?

Massoc argues that the major European banks remain dominant not because they supply credit to the real economy but because they play an indispensable role in their home state's geo-economic strategy. Similar to Dafe and Rethel, Massoc finds that policymaker expectations are key. Interviews with state officials reveal convictions in political circles that strong domestic banks are a vital component of state power insofar as they serve as key nodal points in the provisioning of liquidity in global financial markets. For Massoc, structural power thus hinges on providing an essential dimension to the political economy and also on the power of state officials to define what is essential.

To develop this argument, Massoc adopts a two-part methodological framework. First, she undertakes a discourse analysis of parliamentary debates in France, Germany, and Spain from 2010 to 2019. Despite some variation, this discourse analysis shows that ministers, regardless of their party affiliation, are more concerned with the geo-economic power of the major banks, while members of parliament were more attuned to the role of banks in providing credit to the real economy. Second, Massoc uses a comparative case study of the special tax introduced on banks in France and Germany in the early 2010s to illustrate the role of political arbitrage in determining what structurally matters most. The purpose of this special tax was to force the banking sector to incur some of the fiscal burden of paying for the crisis, and the major banks wielded all facets of their power, both structural and instrumental, to try to defeat it. In both France and Germany, the Ministry of Finance initially put forward a blueprint for the special tax that would be more detrimental to the traditional lending activities of small and medium-sized enterprises (SMEs) than the global market-based activities of major banks. In France, the initial design of the special tax was passed, but in Germany it was altered to make it favorable to the traditional lending activities of SMEs. According to Massoc, these divergent outcomes are the result of contrasting institutional configurations in the two countries. The special tax was able to pass unaltered in France because its Ministry of Finance is more autonomous than in Germany, where the parliament has more influence over the policy-making process.

Massoc's comparative analysis reinforces the importance of the global (“geo-economic”) context, as well as the ideational realm, in shaping finance's structural power. Her study also underscores how complex institutional dynamics shape policy outcomes. Though much has been done in the existing literature on the structural power of finance to open up the “black box” of the state, it is still common to assume that it is a unitary actor that either succumbs to, or resists, the power of finance. As Massoc shows, different institutional organs of the state often have divergent interests in relation to the power of finance, which in some instances cannot be reduced to partisanship. Furthermore, Massoc develops a nuanced understanding of structural power in the context of market-based systems of banking. As her analysis makes clear, global banks derive their structural power not just from credit but from debt and their abilities to borrow vast amounts at low interest rates. In this way, Massoc's empirically rich work has much to offer to the burgeoning literature on the use of “leverage as power.” 39

Focusing on the realm of corporate governance, Benjamin Braun's contribution traces the transformations of financial power through different phases of capitalist development. For Braun, the experience of the United States since the 1970s is puzzling. Over the past few decades, nonfinancial corporations have become less dependent on external financing from the stock market and banks, bringing into question the relevance of the exit-based theory of finance's structural power. Yet at the same time, the long-term historical evidence, namely, data on the gap between the return on capital (r) and economic growth (g), points to the enduring power of finance.

For Braun this puzzle can be explained by shifts in corporate governance away from exit-based to control-based forms of power. He identifies four regimes that have characterized US corporate governance since 1900. The first regime, from the late nineteenth and early twentieth century, was finance capitalism, theorized by Hilferding. Its central features included concentration of share ownership in large banks and control-based power exercised over a small number of giant industrial corporations. The second regime, managerialism, typified US capitalism in the mid-twentieth century and was characterized by household ownership of shares. These households could exit, but this was a weak form of power because of their dispersed nature. The third regime, late twentieth-century shareholder primacy, featured, at least relative to managerialism, rising share concentration through pension funds, heightened exit and voice, and increasing portfolio diversification. The latest regime, what Braun refers to as “asset manager capitalism,” started to take root at the turn of the millennium. In some ways this new regime harkens back to finance capitalism, marking a “Great Re-Concentration” of ownership and a reassertion of the power of control over exit. But the crucial difference is the agents involved. Instead of large banks, asset manager capitalism is dominated by institutional capital pools, especially the “Big Three” asset management companies, BlackRock, Vanguard, and State Street. 40 Because of their enormous size, these capital pools combine de facto control with full diversification, the hallmark of this latest regime.

As “universal” owners exposed to the entire economy, giant asset managers are expected, in principle, to internalize negative externalities and use their power of control to become “forceful stewards” of environmental, social, and governance (ESG) criteria. Though the Big Three sometimes embrace ESG rhetoric, the reality, as demonstrated in their proxy voting record at annual general meetings, shows that they tend to shy away from any stewardship role. Moving beyond principles and developing a theory of actually existing asset manager capitalism, Braun highlights a key dilemma in the business model of asset managers that explains why rhetoric does not match reality. The Big Three strive to maximize revenues, and to maximize revenues under their fee-based model, they must maximize their assets under management (AUM). Yet as their AUM swell, the Big Three are thrust into the spotlight. The more they try to assert control-based power, the more controversy they court from clients, regulators, politicians, and voters. As the risk of regulatory and political backlash grows, Braun argues that asset managers become less concerned with corporate governance outcomes. Recent backtracking on environmental issues can be seen as evidence of the Big Three bowing to political pressures from right-wing forces in Congress.

The corporate governance regime of asset manager capitalism has only been in existence for a short period of time. One of the strengths of Braun's contribution is that it situates this new regime within the long-term dynamics of capital accumulation, providing historically rich insights into the conditions under which financial power changes over time. Braun's theory of actually existing asset manager capitalism is another key contribution. Academics and think tanks alike have amassed plenty of evidence of the failures of the Big Three on ESG, and Braun offers conceptual tools to these failures by anchoring them within the wider political context in which shareholders and managers operate. Taking politics seriously also allows Braun to illuminate crucial differences between exit-based and control-based power; one advantage of the former is its depoliticized nature. When it comes to financialization, Braun's article prompts some important questions for further exploration. Shareholder primacy is often associated with corporate financialization: What does its decline as a corporate governance regime mean for our understanding of financialized capitalism? Has the emergence of asset manager capitalism fundamentally altered financialization or does it simply perpetuate it? Addressing these questions head-on might help deepen our understanding of contemporary capitalism's trajectory. Braun's intervention also invites us to think about the vital, but thus far neglected, connections between financial power and inequality. The persistent gap between the rate of return on capital and the rate of economic growth, a key determinate of income inequality in Piketty's framework, is associated with the reemergence of control-based forms of financial power. Braun's findings show the need for further research into the institutions and practices through which financial intermediaries exercise power in order to prevent the “euthanasia” of wealthy rentiers predicted by Keynes.

Finally, in his contribution to the special issue, Manolis Kalaitzake offers a systematic account of two approaches, comparing and contrasting what he terms traditional structural power (TSP), which emerged in the 1970s and 1980s, with new structural power (NSP), which took hold after the global financial crisis. Though the move from TSP to NSP is often portrayed as a progressive evolution toward sophistication, nuance, and complexity, Kalaitzake adopts a more skeptical view. In short, he claims that the two approaches serve different purposes, and choosing between them involves a number of intellectual trade-offs.

TSP analyses are anchored in the macrostructures of class and capitalism. They aim at “explanation through commonalities” in order to uncover systems-oriented limitation mechanisms (i.e., taking into account the entire range of possibilities to uncover the filtering mechanism that results in a limited list of policy options considered feasible in a capitalist society). Politically, TSP lends itself to the radical Marxist tradition; its class-based focus stresses the fundamental incompatibility between capitalism and democracy, and as a result, it makes a point of considering, and often advocating for, alternatives to capitalism. NSP, in contrast, is focused on fine-grained analyses of microlevel processes. Proponents of NSP favor “explanation through variation” in order to identify agent-oriented selection mechanisms (i.e., taking into account a limited range of possibilities to examine the causal role of various agents in determining the final policy outcome). With an emphasis on variation over time and space, NSP accords a much greater role to state power and autonomy and, in turn, is more optimistic about the possibilities for democratic governance in a capitalist society.

Kalaitzake is careful to pinpoint the relative strengths of both approaches in examining different aspects of the policy process. But the main purpose of his article is to highlight what he refers to as the “analytical and explanatory advantages” of TSP. First, while NSP displays a strong constructivist bent in emphasizing the importance of ideas, Kalaitzake claims that TSP is better equipped to assess precisely when ideas are (and are not) relevant. In a “point of no return” scenario like the Greek debt crisis from 2009 to 2012 (i.e., when policymakers believe in the threat of capital flight and significant capital flight occurs), objective market conditions took precedence over the ideas of policymakers. Second, Kalaitzake maintains that TSP has an analytical advantage over NSP in “understanding how the parameters and boundaries of policy debates are established and regulated.” Though such limit determinations or exclusion mechanisms are difficult to trace empirically, they are important. Kalaitzake gives the example of the absence of substantive regulatory reform after the global financial crisis. Across different national and regional contexts, and across many different policy domains, financial power led to the postponement, watering down, and abandonment of various policies and regulations. While NSP is equipped to understand variation in postcrisis reforms across different national and regional contexts, it is unable to account for the systemic failure of substantive reform efforts across them. For Kalaitzake, a preference for TSP's limit determinations boils down to a key difference in normative stance. The political radicalism of TSP means that it favors an analysis of system-wide vulnerabilities rather than the minor variations in financial reforms that are the analytical focus of NSP.

To leverage the insights from TSP in empirical research, Kalaitzake advocates embedding the approach within what he terms a “contradictory functional” model of explanation. He argues this model can account for why the occasional defeats of finance in the policymaking process are nonetheless compatible with systemic imperatives of capital accumulation, which generate an inherent class bias in policy outcomes. There are three main aspects of the contradictory functional model. The first identifies a “functional fit” between the macrostructure of capitalism and the structural power of finance. In the current historical junction, this involves an attentiveness to how the financialization of accumulation is “functionally enmeshed” with the growing profitability and power of the financial sector at large. The second aspect of the model is an attentiveness to the feedback loop that exists between profinance policies and the threat of capital flight, with the latter having causal primacy. Financialization enhances the risk of capital flight. This forces policy makers to be ever more vigilant about the threat of capital flight and to favor various pro-finance policies including balanced budgets, inflation targeting, and wage controls. The third aspect of the model is to draw attention to system-level dilemmas. In the era of financialized (and globalized) capitalism, TSP must be perceptive to the contradictory binds that policymakers experience in meeting the demands of investors while simultaneously trying to foster social prosperity and public legitimacy.

Kalaitzake's contribution provides a novel assessment of the different approaches to the study of finance's structural power. This provocative analysis should spark plenty of debate, and proponents of NSP will no doubt take issue with many of Kalaitzake's core claims. But serious critics of his approach will find it difficult to uphold the commonly held view of a simple, progressive evolution from TSP to NSP. With clinical precision, Kalaitzake shows what is lost in this shift of perspectives. At minimum, his analysis should encourage us to be more transparent about the relative strengths and weaknesses of the different approaches. And perhaps most importantly, his refreshingly candid normative stance should compel us to be more reflexive about our own assumptions and the political projects that underpin them.

Conclusion

At its core, the concept of structural power implies that actors who control resources that are essential to desired economic outcomes (incomes from labor, fiscal revenues, etc.) have capacities to sanction the behaviors of others (governments, workers, other companies, etc.) who materially depend on those outcomes. This means that certain groups must be responsive to the interests of those who control significant resources, even when the interests of the controllers of resources go against their own. When Winters, Maxfield, Culpepper, and others formulated their arguments about structural power, they focused on finance's role in facilitating investment as the basis for its structural power, and investment strikes and exit threats as the mechanisms by which this power was exercised.

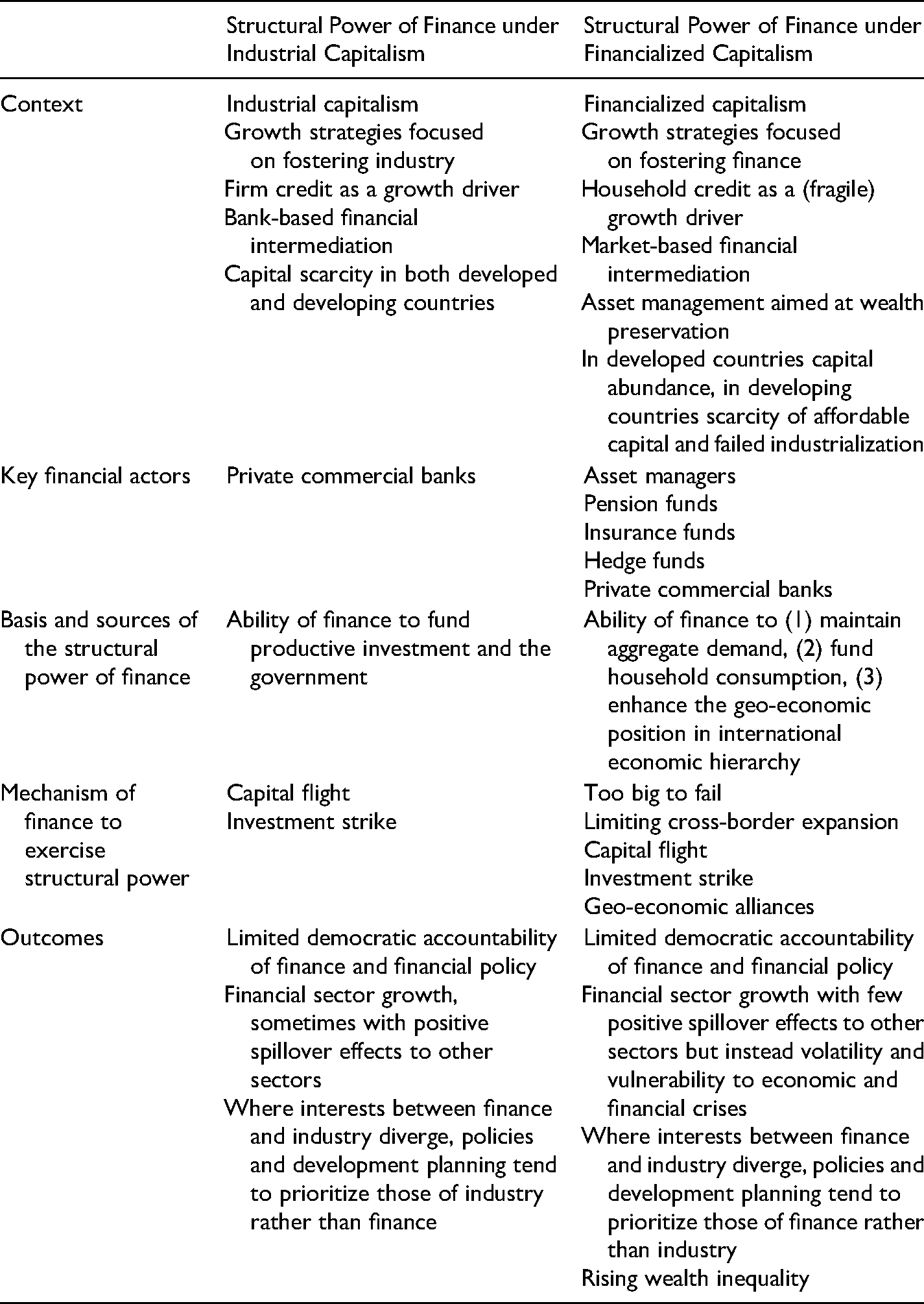

In the age of financialization, core and peripheral economies alike have moved away from traditional growth strategies focused on fostering industry and have moved toward strategies that rely on expanding financial sectors and/or self-reinforcing cycles of debt growth and appreciating asset values. The contributions to this special issue engage with how decades of financialization have transformed the basis of structural power away from facilitating productive investment toward alternative functions that have gone unnoticed in the existing literature, summarized in Table 1.

The Structural Power of Finance under Industrial and Financialized Capitalism.

For instance, in core capitalist economies like the United States, financiers play an ever-smaller role in funding (feeble) corporate investments, and they often cannot credibly threaten exit. Yet, the financial sector, which in financialized capitalism comprises a myriad of players such as asset managers, pension funds, insurance funds, and hedge funds in addition to commercial banks, continues to enjoy strong structural power. This derives not from finance's traditional role in facilitating productive investment but from the post-Fordist growth strategies. Afflicted by secular stagnation, these economies rely on expanding household debt and financial/real estate wealth as significant sources of macroeconomic demand. Moreover, highly concentrated equity ownership, as well as forms of investment outside public markets (like private equity), provides a distinct version of structural power that is reminiscent of Hilferding's notion of finance capital, as Braun's contribution shows. Just as important is how the financial sector gains structural power through geopolitics and geo-economics. In Elsa Massoc's contribution, we learn how state elites see large financial firms (together with tech companies) as strategic tools in international politics. For this geo-economic role, it is not relevant how much a financial firm contributes to financing domestic industry. The crucial mechanism of structural power rather lies in the enormous volumes of financial flows that pass through a firm's balance sheet, as either liabilities or assets.

For developing countries, the special role of finance derives from the perceived failure of (very) late industrialization as a viable growth strategy because of multiple factors, including a host of restrictive trade and investment agreements, increased protections for intellectual property, the rise of global value chains, and increased competition from China. Developing countries have therefore turned to growth strategies that target the financial sector itself. Such strategies rely on supporting concentration in banking to prevent foreign takeovers, encouraging regional expansion of financial institutions, and, increasingly, becoming international financial centers. Instead of using the financial sector to provide subsidized credit to national champion firms, under such development strategies the banks themselves are considered national champions. This means that even though the financial sector might not contribute much to the domestic productive economy, as long as governments rely on it for this growth strategy, it remains structurally powerful.

These transformations have prevented the structural power of finance from waning despite its diminished role as the conventional source of financing productive investment. If anything, the power of finance has increased as financial institutions and profits take on an ever more central role in growth, development, and geopolitical strategies. These strategies tend to go hand in hand with rising concentration and economies of scale among financial institutions, which not only reduce collective action problems but also make these firms more internationally competitive and “too big to fail,” further enhancing financial power. Threats of capital flight and investment strikes remain key mechanisms in the operation of structural power. Yet “too big to fail” and threats to limit the cross-border financial expansion that is central to geopolitical strategies have augmented the ways in which financiers exercise structural power.

Although the contributions to this special issue underscore the enhanced structural power of finance under financialization, they do not imply that finance will always retain its prominence and privileges. Instead, the analyses here should encourage scholars to be attentive to developments in politics and the economy in the face of significant disruptions—like the COVID-19 pandemic—and enormous transformational challenges, particularly those associated with climate change. These developments will likely change the strength and nature of the structural power of finance going forward and might create avenues of resistance. Much remains to be done for social scientists to work in, and advance this, theoretical tradition.

Footnotes

Acknowledgments

The authors would like to thank the Department of International Relations, the London School of Economics, and the Max Planck Institute for the Study of Societies for generously hosting two workshops at which the articles in this special issue were discussed.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.