Abstract

This study examines the reasons why between 1979 and 2020 the number of abattoirs licenced to slaughter red blood livestock species in Great Britain fell from 1146 to 200, average throughput per abattoir increased, larger abattoirs specialised in the species slaughtered, and family owned abattoirs have been replaced by international companies owning multiple slaughterhouses and food processing factories. The study combines abattoir sector survey data with findings from a national survey of small abattoirs. Larger abattoirs have exploited economies of size and location to achieve the throughput necessary to supply multiple retailers and/or wholesale markets. Smaller abattoirs have exploited economies of scope to develop the bespoke butchering services needed to supply private kill customers. The high rate of closure of smaller abattoirs suggests the future of small-scale, locally based supply chains in which private kill services supply is threatened. The recently introduced Small Abattoir Fund offers grants towards the purchase of new equipment which will offer some relief. But smaller abattoirs must support their private kill customers by organising collection points for onward transport of livestock to the abattoir and local redistribution centres for meat and carcases.

Keywords

Introduction

In 2018, abattoirs slaughtered red blood livestock species with a combined farmgate value of £6.5 billion – comprising 2.8m cattle (farmgate value of £3 billion) (AHDB, 2020a), 14.4m sheep (£1.9 billion) (AHDB, 2020c) and 10.9m pigs (£1.6 billion) (AHDB, 2020b). The regulations that require all cattle, sheep, pigs and goat meat that enter the human food chain to be slaughtered at a Food Standard Agency (FSA) regulated abattoir making abattoirs an essential part of the livestock farming's infrastructure.

However, ongoing structural changes in the industry threaten the abattoir network. Between 1979 and 2020, the number of abattoirs licenced to slaughter red blood livestock species in Great Britain decreased from 1146 to 200. The trend of a higher proportion of smaller than larger abattoirs closing continued between 2001 and 2017; when the number of large abattoirs (defined as having a throughput above 30,000 Livestock Standard Unit (LSU)/year) 1 in Great Britain increased, whereas the number of smaller abattoirs (defined as having a throughput below 30,000 LSU/year) declined by some 35% (APGAW, 2020: 11 and Figure 1). Between 2019 and 2021, 14 small, family-run abattoirs closed (Farminguk, 2023). A recent FSA report concluded that small abattoirs were closing at a rate of 10%/year (NCB, 2022), but a concurrent survey of small abattoir owners (throughput <1000 LSU/year) across Great Britain reported that 59% of 62 respondents expected to close within five years (Addy, 2021); 26 abattoirs have closed since 2021 (LARK, 2023). 2

The high rate of attrition and expected future closures suggests that small abattoirs are unviable. However, their closure is important. It threatens the livelihoods of some of the 124,000 red meat livestock farmers in the UK (Daera, 2023; DEFRA, 2023b; Scottish Government, 2021; Welsh Government, 2019) who depend on their services, 3 and the delivery of key UK agricultural policy objectives as summarised by the principle of using public money to support public goods (Franks and Peden, 2022). It also raises concerns regarding food chain resilience (UK Parliament, 2020) and animal welfare (EFRA, 2021). This study examines these concerns by analysing the causes of the decline of small abattoirs and asking how they can become commercially viable and sustainable businesses. The next section reviews the literature to outline the commercial and marketing challenges faced by small abattoirs in Great Britain. Section ‘Structural change and consolidation in the UK abattoir industry’ uses abattoir industry data to show how production and marketing economies of size, location and scope have driven structural changes in the abattoir industry in Great Britain resulting in the emergence of two distinctive business models. 4 Section ‘Survey methodology and sample characteristics’ presents the survey into the problems of small abattoir businesses. Section ‘Survey findings’ summarises its findings. Section ‘Discussion’ discusses policies for supporting small abattoirs. Section ‘Conclusions’ concludes.

Literature review of the commercial and marketing challenges faced by abattoirs

The principal difficulties and reasons for the closure of abattoirs identified in the literature are regulatory challenges, administrative-related responsibilities, high overhead costs, lack of capital, shortage of skilled labour and retaining staff, and managing the seasonal demand for slaughter (Charlebois and Summan, 2014; Kennard, 2018; Kennard and Young, 2018; Lewis and Peters, 2012).

In Great Britain, abattoir operations have been subject to increasing regulatory costs since the UK joined the Common Market in 1973 (Kennard and Young, 2018). European Union (EU) Directive 91/497/EC (EEC, 1991) in particular imposed expensive structural and procedural changes which many smaller- and medium-sized abattoirs were unable to meet (Countryside Alliance, 2021). In a survey of 25 small abattoirs (throughput below 10,000 LSU/year) in Great Britain, Kennard (2018) reported that 58% of respondents found administrative-related responsibilities challenging. In the UK regulations currently require inter alia that all livestock ‘passports’ are checked, statutory Food Chain Information paperwork completed, FSA-employed Official Veterinarians (OVs) must be present at the abattoir to oversee the arrival and slaughter of all livestock, and Food Hygiene Inspectors need to inspect each carcase. The costs of these regulations are borne by the abattoir (FSA, 2023a).

Charlebois and Summan (2014) and Kennard (2018) found small abattoirs experience high overhead costs and lack of capital. In the UK, all abattoirs are required to pay a slaughter levy on each animal slaughtered to the Agriculture and Horticulture Development Board (AHDB). It has been estimated to cost small abattoirs between £6000 and £7000 per annum (UK Abattoir Network, 2021). Regulations have also absorbed capital that could have been used for other purposes. For example, in 2018, CCTV recording of all livestock-related operations became mandatory (DEFRA, 2018) imposing an estimated capital cost of between £5000 and £10,000 on small abattoirs (APGAW, 2020: 31).

Studies by Lewis and Peters (2012), Kennard (2018) and Charlebois and Summan (2014) reported that small abattoirs suffered from shortages of skilled labour and experienced difficulties retaining staff. Small abattoirs do not slaughter every day of the week. Therefore slaughtermen need to be able to butcher and pack carcasses. These additional skills make them targets of larger abattoirs which can afford to pay higher salaries.

Abattoirs experience difficulties managing the seasonality of the supply of livestock, with a high demand for slaughter in the autumn and low demand in the spring and early summer (Lewis and Peters, 2012). Farmers select livestock species, breeds and grazing strategies which best suit the farm's resources, climate, and their management and husbandry skills. As a result, abattoirs have to manage a pronounced seasonality of supply for grazing livestock and a wide variation in animal size and conformation. This requires abattoirs to use capital to purchase and service the specialist equipment needed to safely handle large and/or long-horned species and to employ staff with the specialist skills required to remove specified risk materials from over 30-month animals. Other challenges small abattoirs face include,

the fall in the value of cattle hides and sheep skins. By tradition, these are owned by the abattoir. In June 2019, the value of cattle hides had fallen to £5, which is below the economic cost of treating, storing and selling, and sheep skins had become worthless. Disposing of these materials added to the average 7% to 9% of total costs for inspection and waste disposal (Kennard, 2018). The average age of 56 years of owners of small abattoirs, with only half having made any arrangements for a succession of the business (Kennard, 2018). The land and building development value of abattoirs which are located on prime sites in towns can be worth far more for development than for continuing use as an abattoir (Kennard and Young, 2018).

Not all can justify the investment this requires. These challenges, as Lewis and Peters (2012) note, are problems that would not be overcome simply by building larger abattoirs.

Structural change and consolidation in the UK abattoir industry

Economies of size, location and scope may have broad implications for industry structure, performance, growth and change (Hallam, 1991), which was shown to be the case in such different sectors as UK higher education (Johnes and Johnes, 2016), publicly owned US electric utilities (Triebs et al., 2016), Portuguese water sector (Carvalho and Marques, 2016) and biomedical research (Hernandez-Villafuerte et al., 2017). However, this is the first study to use industry sector data to assess the relative importance of these three powerful underlying economic forces on the structure of the abattoir industry in Great Britain.

Economies of size

Economies of size 5 occur when the average cost per unit of production decreases as the size of the business increases until all surplus capacity is used (i.e., over the same level of fixed expenses). This is typically observed in businesses with high fixed-to-total cost ratios. It is because fixed costs (which include full-time labour, rent, business rates, power, interest and bank charges, and building and equipment depreciation) 6 do not vary with throughput that their costs can be spread over an increase in output.

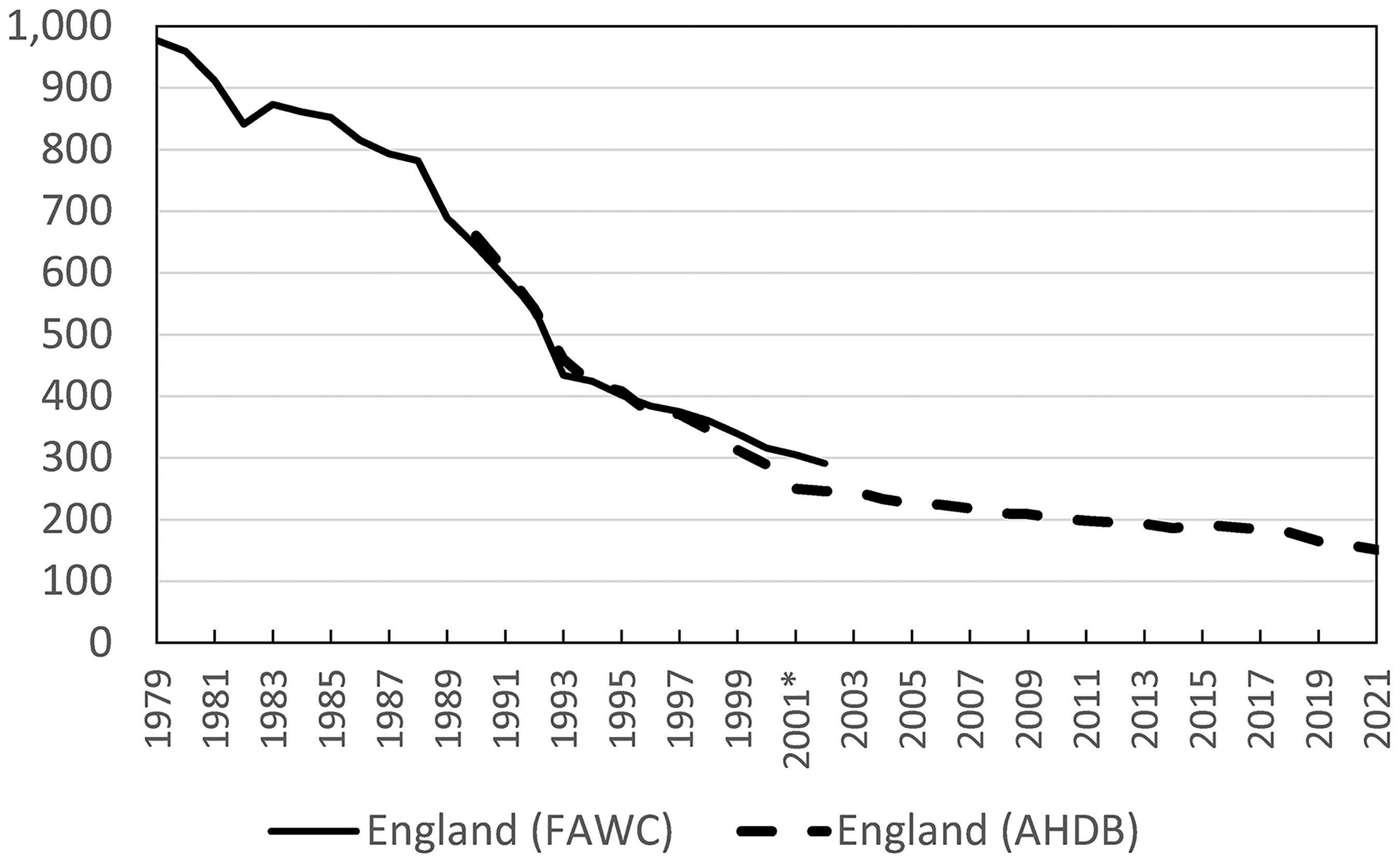

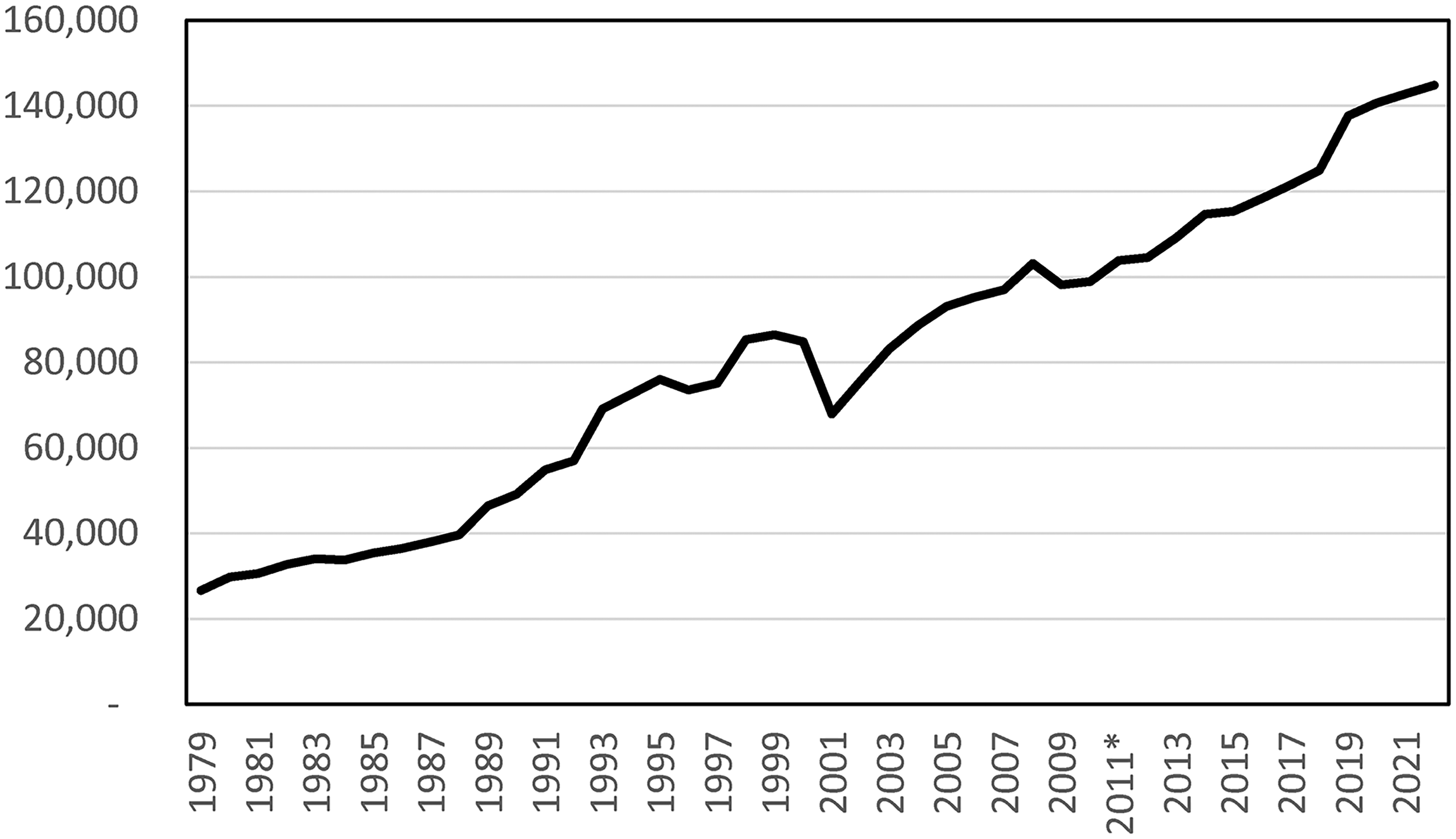

Multiple studies have shown that abattoir businesses are characterised by high fixed to total costs (Franks and Peden, 2022; Houghton, 2011; Kennard, 2018; Kennard and Young, 2018; Owen et al., 2008; SAC Consulting, 2013). The impact of economies of size on the structure of abattoirs is evident from the data on the number of abattoirs and the average number of livestock slaughtered per abattoir. The number of abattoirs in Great Britain fell from 1140 in 1970 to 200 in 2020. Figure 1 shows the reduction in England from 977 to 159 over the same time period and to 151 in 2021 (Farm Animal Welfare Committee (AHDB, 2023a; Farm Animal Welfare Committee (FAWC), 2003). However, Figure 2 shows the average number of livestock slaughtered per abattoir during this period steadily increased – the temporary reduction in slaughtering/abattoir in the years after 1998 was caused by a 35% reduction in the UK pig herd (Sheppard, 2003).

The number of abattoirs in England (various sources). *There were some changes to the classification of slaughterhouses during the outbreak of Foot and Mouth Disease in 2001. Source: AHDB (2019b, 2023a), FAWC (2003: 5 and Table 1).

Average total head of red meat species of livestock slaughtered per abattoir (based on AHDB, 2023a; Farm Animal Welfare Committee, 2003; and authors' own estimates).

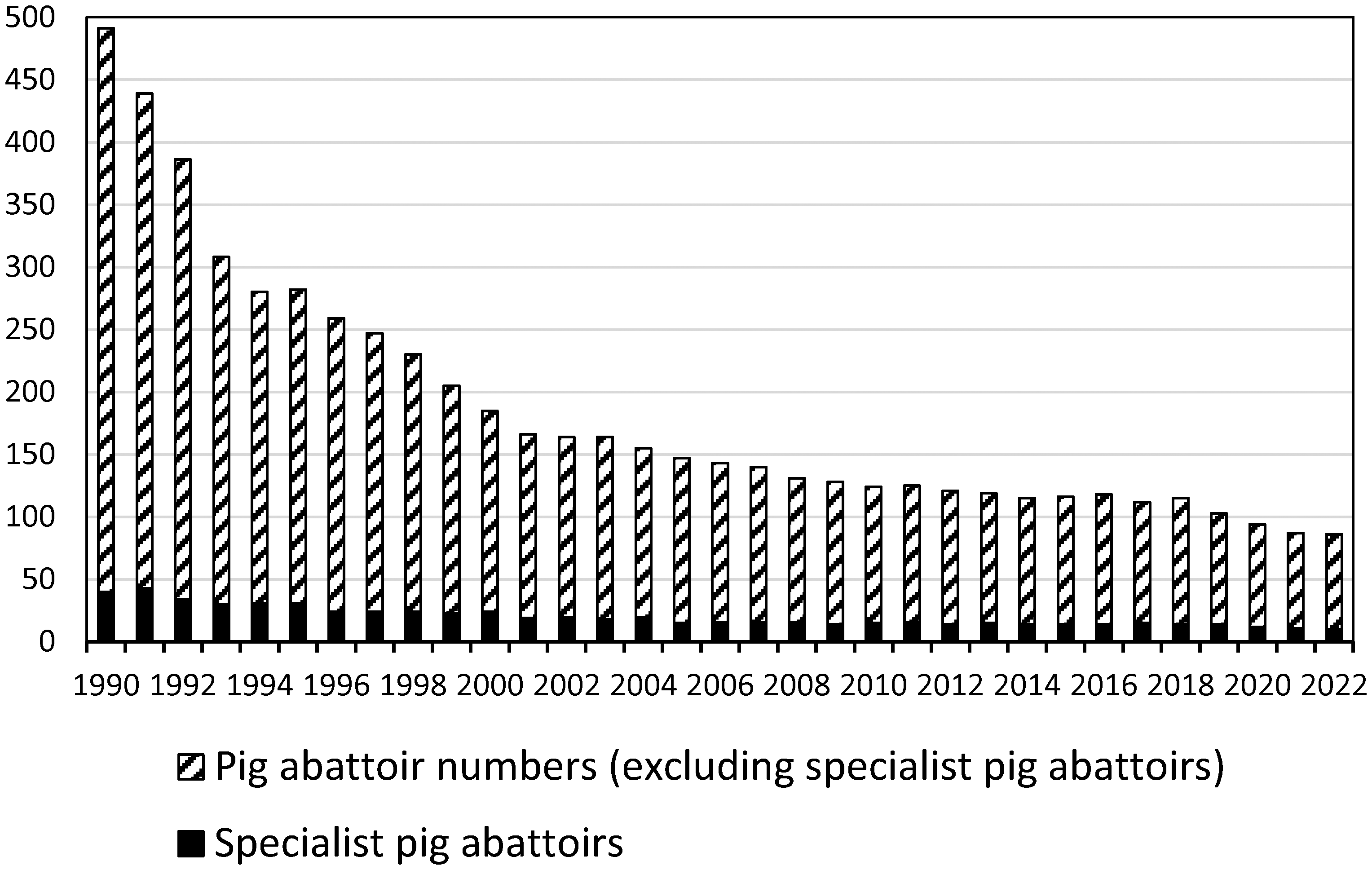

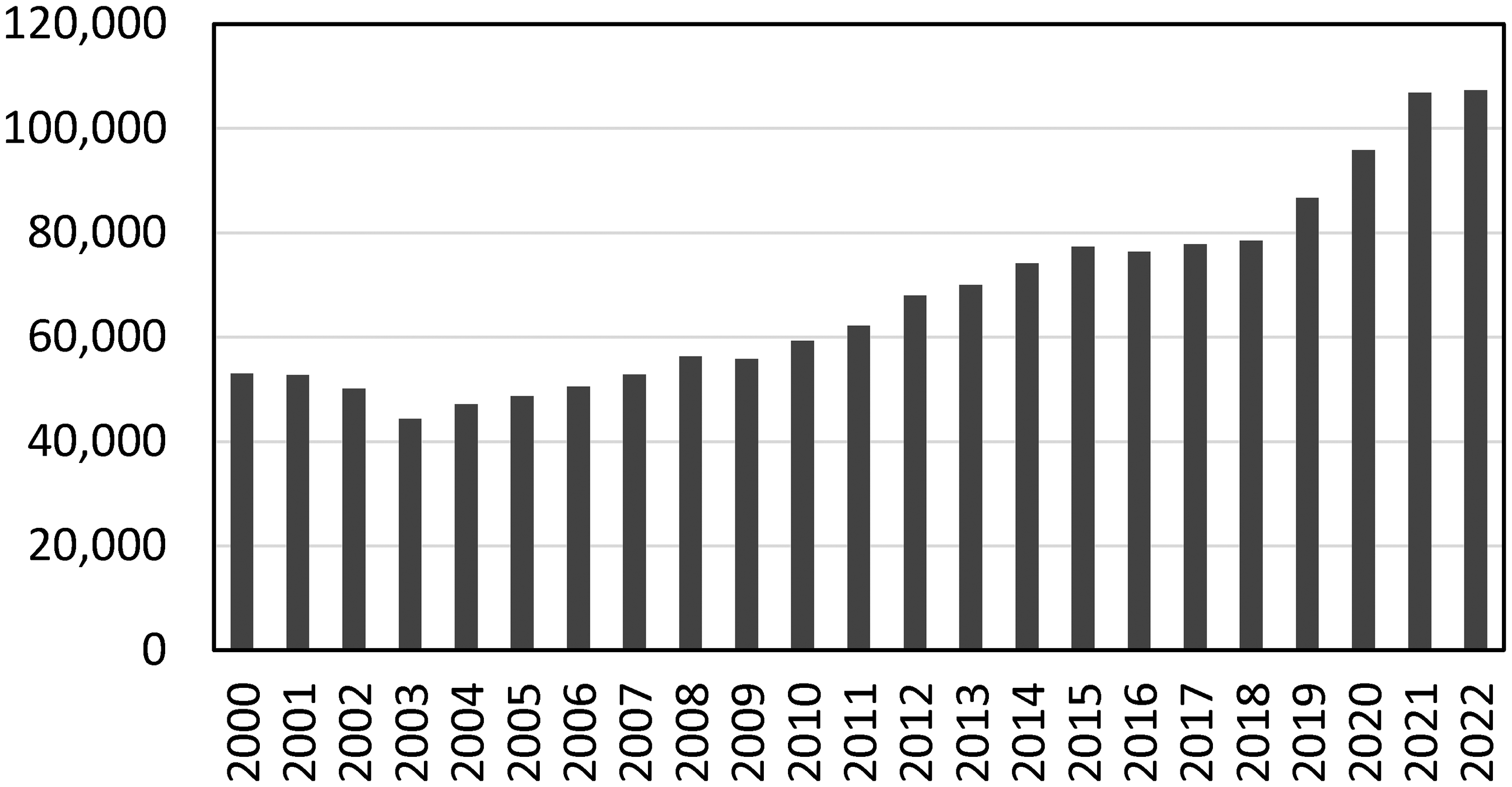

The importance of economies of size in driving the increase of abattoir throughput is most clearly shown by the data for pig slaughtering. Between 1990 and 2021, the number of abattoirs licenced to slaughter pigs in England fell from 491 to 87 (Figure 3). The average number of pigs slaughtered in these 87 abattoirs was some 107,000. However, the 10 specialist pig slaughtering abattoirs in England (defined as over 95% of slaughtering are pigs) slaughtered an average of some 710,000 pigs annually, or 77% of all pigs slaughtered (Figure 4). There has been a less pronounced concentration of slaughtering of cattle and sheep. Nevertheless, in 2018, 13 of the 148 abattoirs licenced to slaughter cattle slaughtered 56% of all cattle. Their average annual throughput was 76,000, compared with 5800 for the remaining 135 abattoirs. A similar concentration of slaughtering is seen in sheep, when, in 2018, 22 abattoirs slaughtered 84% of all sheep. The average annual throughput of the 22 abattoirs was 381,000, compared to 12,500 for the remaining 127 abattoirs.

The number of abattoirs licenced to slaughter pigs operating in England in the calendar year (specialist abattoirs defined where over 95% of slaughtering are pigs). Source: AHDB (2023b).

Average annual throughput of pigs (head) per abattoir licenced to slaughter pigs operating in England the calendar year. Source: AHDB (2023b).

Between 1998 and 2018, red meat consumption per capita has remained stable (AHDB, 2020a). However, there has been a considerable change in the point of sale of meat. In 2018, the five largest multiple retailers sold 63% of beef and sheep meat in Great Britain (AHDB, 2019c) with retailers’ own-label accounting for some 80.7% of total grocery fresh red meat sales (AHDB, 2018: 4). Multiple retailers require large volumes of pre-packed, standard jointed and weighed portions, which requires larger slaughterhouses and food processing plants. Together with their preference to do business with a small number of suppliers (to reduce their costs and help ensure a consistent product) has favoured larger over smaller abattoirs.

By exploiting available economies of size abattoirs have been able to raise their efficiency and productivity. This has allowed them to reduce their slaughter fees, which, in turn, has put pressure on competitors to lower their fees and charges (Kennard and Young, 2018). However, the extent to which fees and charges can be lowered is restricted by the short-term need to cover all direct cash costs (salaries, fuel and power, rents and rates, animal by-produce waste removal charges, AHDB slaughter levy 7 and FSA charges). If fees and charges are reduced to this level investment in training, buildings and equipment must be financed from savings and borrowings. When savings and credit are exhausted, the business is forced to sell up or close.

Economies of location

Economies of location occur where businesses benefit from geographically matching capacity to some important spatial characteristic of the business (Beckmann, 1987). In 1826, Von Thünen identified spatial economies as an important explanation of the relationship between the commodities farmers produce and the distance from the farm to the market. The trade-off between production costs and transportation costs is central to the spatial organisation of an economy because a decline in transportation costs allows for a decline in the number of economic centres and an increase in the size and specialisation of those that remain (Kilkenny and Thisse, 1999).

The UK's warmer southern climate encourages earlier grass growth, which results in grazed livestock becoming ready for slaughter earlier in the year. This geographical characteristic incentivises companies to invest in multiple, spatially distributed abattoirs to allow them to match processing capacity to regional supply. However, larger livestock transporters and improved transport infrastructure have reduced transport costs/animal, which has somewhat diminished these benefits. At the same time, the increased supply of livestock from the enlarged catchment area has allowed larger abattoirs to specialise in the species they slaughter.

These factors have combined to drive the consolidation of abattoir ownership. Dunbia, for example, was established as a family business in Northern Ireland in 1976. After merging with Dawn Meat in 2017 it now manages nine abattoirs (seven in England, one in Scotland and one in Wales) and additional processing facilities. Its abattoirs slaughter more than 3.5m lambs and over 1m cattle each year (Dunbia, 2023). In another example, ABP Food Group, which was established in 1981 through its history goes back to 1954, manages 10 abattoirs (seven in England, two in Northern Ireland and one in Scotland, and is involved in a joint venture with Linden Foods) and has a UK turnover of €1.3 billion. It works with 45,000 farmers operating in nine countries and manages 51 locations across Ireland, the UK and Europe.

Economies of scope

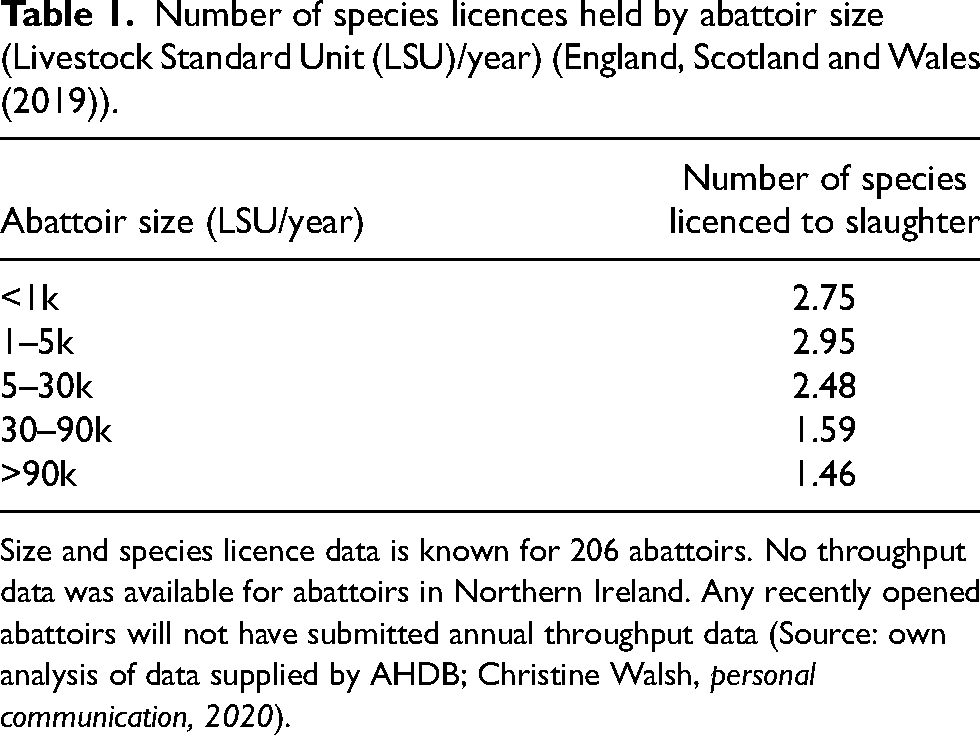

Economies of scope occur when the production of one good reduces the cost of producing another good. This happens when the same inputs and processes are shared by different products. Economies of scope occur in slaughtering cattle and sheep because these species can share the same lairage, use the same slaughter area, the processing and jointing of their carcases uses similar equipment, and their meat can be stored in the same fridges and freezers. Although pig slaughtering shares some of these facilities, the need for specialist pre-slaughter processing and slaughter equipment, and the different skills required for these specialist activities, reduces the economies of scope they share with the slaughter of cattle and sheep. All abattoirs are required to hold an FSA licence for each species they slaughter. Table 1 shows that, on average, smaller abattoirs have a higher number of licences than larger abattoirs, evidence that they continue to exploit economies of scope by offering multi-species slaughter and that large abattoirs have reduced the number of species they slaughter, exchanging economies of scope for economies of size.

Number of species licences held by abattoir size (Livestock Standard Unit (LSU)/year) (England, Scotland and Wales (2019)).

Size and species licence data is known for 206 abattoirs. No throughput data was available for abattoirs in Northern Ireland. Any recently opened abattoirs will not have submitted annual throughput data (Source: own analysis of data supplied by AHDB; Christine Walsh, personal communication, 2020).

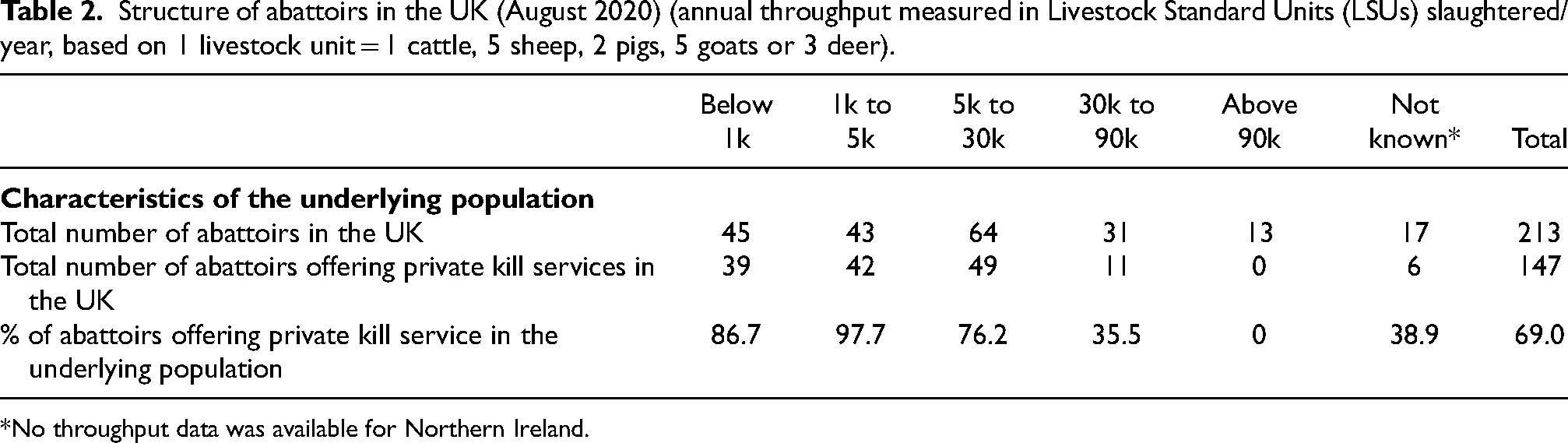

Table 2 shows that smaller abattoirs specialise in providing private kill services. This is one of three abattoir business models commonly found in the UK. Abattoirs can purchase livestock directly from farmers for an agreed price on a delivered, deadweight basis, adjusted for confirmation and any defects, after the deduction of fees and levies. They can also procure livestock from livestock markets, paying the hammer price, and arranging and paying for transport. Or, rather than purchase livestock, abattoirs can charge a fee for slaughter and butchering services, the so-called private kill service. Typically farmers transport small consignments of livestock which they have finished on their own farm to the abattoir, pay a slaughter charge and, if required, butchering fees, and return to collect the offal and carcase/butchered joints to use for private consumption, or to retail themselves, or to sell to local retailers. Another version of private kill service is used by butchers who purchase livestock on farms, arrange and pay for transport to the abattoir, pay the slaughter fee, and collect the carcasses (APGAW, 2020: 19). A survey of independent butchers found that 45% used this service (NCB, 2023). 8 Butchers can also purchase carcases/cuts and offals directly from abattoirs and wholesale markets.

Structure of abattoirs in the UK (August 2020) (annual throughput measured in Livestock Standard Units (LSUs) slaughtered/year, based on 1 livestock unit = 1 cattle, 5 sheep, 2 pigs, 5 goats or 3 deer).

*No throughput data was available for Northern Ireland.

Although this business is essential to the commercial viability of small abattoirs (APGAW, 2020), it is an expensive service to provide because,

private kill customers typically deliver small consignments of livestock to the abattoir several times a year, which increases regulation-related and record-keeping costs, the bespoke butchering services require skilled staff which adds to staff costs, and private kill requires all carcases, meat and offal to be individually labelled and stored, which increases processing time and reduces daily abattoir throughput.

It is because of these higher unit costs that private kill business is not attractive to larger, high throughput abattoirs. However, this niche market is threatened. The growth and dominance of multiple retailers has led to a corresponding decrease in the role of independent butchers, who, in 2018, supplied only 3% of the red meat sales (AHDB, 2019c). An AHDB survey estimated the 6000 independent butchers trading in England in 2016 represented a 60% reduction since 1991 (AHDB, 2019a), a reduction that has reduced demand for private kill services from butchers. Kennard and Young (2018) argue that the growth in red meat sales through multiple retailers has caused small abattoirs to close.

Summary

The fall in the number of abattoirs, increased average throughput per abattoir, increased specialisation and extended geographical coverage of companies which own multiple abattoirs and food processing factories show that, over the last 50 years, economies of size and location have dominated economies of scope. Moreover, the growing importance of supermarkets in the retailing of red meat and improved transport infrastructure have created new economies of scope. The high throughput of larger abattoir companies creates sufficient animal waste to make anaerobic digestors commercially viable, allowing them to convert a waste disposal cost into a saving on power and heat expenditure (APB, 2023). However, the same transport and infrastructure changes also allow butchers to source supplies from wholesale markets at competitive prices. This has removed some economies of scope accruing from the traditional joint ownership of the abattoir and butcher shop. This, in turn, means there are fewer abattoir owners who can use any profits from their retail business to support their abattoir in difficult trading years.

Two distinctive business models have emerged each servicing a different market. Some abattoirs increased throughput to specialise in supplying the high volume multiple retailer market. Other abattoirs have remained small, family owned, diversified businesses, providing the multi-species slaughtering and bespoke butchering service which underpins the locally produced, slaughtered, processed and retailed market. The role small abattoirs play in the rural economy was recognised by EFRA (2021) which declared that ‘small abattoirs are vital to an adequate local [abattoir] network’ and recommended these businesses be recognised as a strategic national asset. The question is, can this strategic national asset be saved?

Survey methodology and sample characteristics

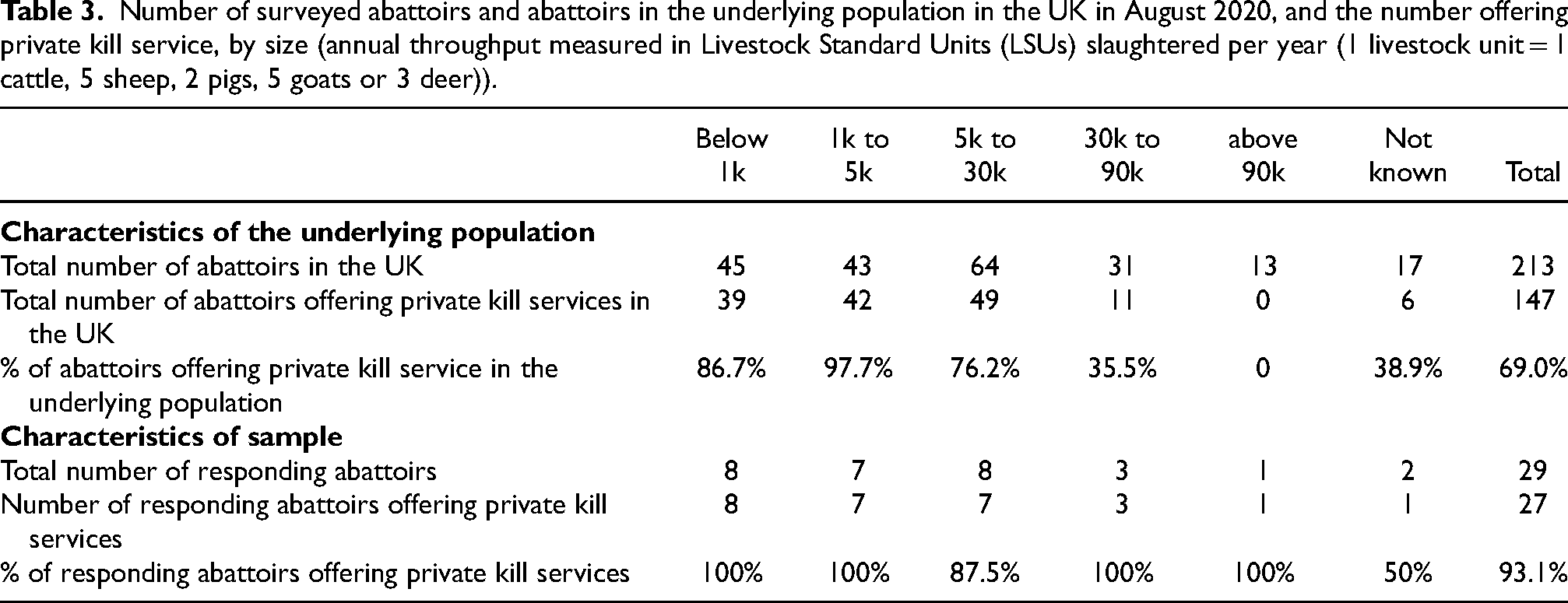

This section presents details of a survey designed to investigate how small abattoirs can become viable and sustainable commercial businesses. Opinions were canvased using an online survey between 15 July and 31 August 2020, which was posted widely via social media streams and by using the mailing lists of four supporting organisations (The Prince's Countryside Fund, Sustainable Food Trust and National Craft Butchers and Soil Association). Twenty-nine useable responses were received from abattoirs, 27 of which offered private kill services (compared to 147 in the underlying UK population in August 2020; Table 3). Twenty-two respondents managed abattoirs in England, three in Wales and four in the Scottish Isles. No responses were received from abattoirs in Northern Ireland or mainland Scotland. Not all respondents answered every question.

Number of surveyed abattoirs and abattoirs in the underlying population in the UK in August 2020, and the number offering private kill service, by size (annual throughput measured in Livestock Standard Units (LSUs) slaughtered per year (1 livestock unit = 1 cattle, 5 sheep, 2 pigs, 5 goats or 3 deer)).

These abattoirs slaughtered some 1.56m cattle, sheep and pigs in a typical (i.e. pre-COVID-19) year, roughly 5.6% of the 28 million cattle, sheep and pigs slaughtered in the UK each year (DEFRA, 2019). Fifteen (51.7%) abattoirs slaughtered fewer than 5000 LSUs/year, compared to 48 (41.3%) in the underlying population.

The abattoirs that offered private kill services held 85 licences between them, an average of three each, compared to an average of 2.3 held by abattoirs in the underlying population. Cattle (26) and sheep (25) were the most commonly held licenses, 18 abattoirs were licensed to slaughter pigs, 13 to slaughter goats and three to slaughter deer. The sample slightly over-represents abattoirs which hold cattle licences in the underlying population (90% to 83%) and sheep licences (86% to 79%), but under-represents abattoirs with pig slaughter licences (50% to 60%).

Survey findings

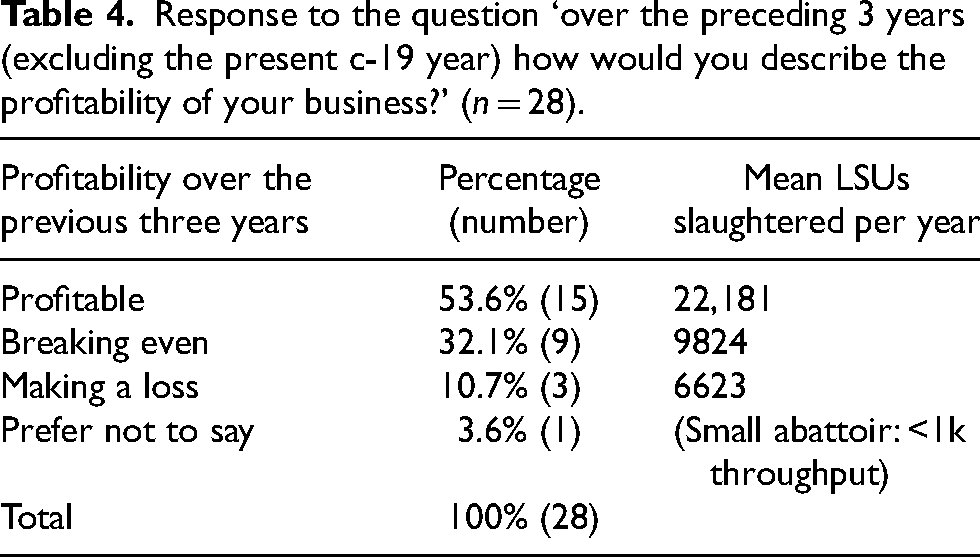

Fifteen respondents (54%), all offering private kill services, reported consistent profitability in each of the three years prior to COVID-19, nine had broken even and three had consistently lost money. Table 4 provides tentative evidence that the break-even throughput of an abattoir is about 10,000 LSU/year, and profitable throughput is in excess of 22,000 LSU/year, the large variability around these values was also noted in Kennard's (2018) survey of 25 small abattoirs. 9

Response to the question ‘over the preceding 3 years (excluding the present c-19 year) how would you describe the profitability of your business?’ (n = 28).

The respondents represent a sample of the survivors working in a sector experiencing a sustained high rate of attrition. Nevertheless, Table 4 shows a proportion of these successful managers continue to report low profitability. This section considers the respondent's views of the options typically available to managers for securing the commercial viability and sustainability of their businesses, these include reducing costs, expanding throughput, increasing fees and charges and diversifying the services they offer.

Reducing costs

Managers are unable to reduce several of their direct costs. For example,

the fixed per head levy paid on each animal slaughtered (at a cost estimated to be between £6000 and £7000 per annum; UK Abattoir Network, 2021). the FSA charge for regulatory and supervisory services (FSA, 2023a)

10

and the need to pay competitive wages to attract and retain skilled staff.

Moreover, fixed costs, such as rent, interest payments, depreciation and business rates vary with the form of ownership, the investments made in previous years, and the abattoir's location.

However, collaboration is one approach to reducing some direct costs. Although respondents believed that consolidation in the rendering industry had resulted in raised animal waste disposal costs (a view reinforced in the evidence presented to APGAW, 2020: 2), and also recognised the potential benefits of jointly tendering for animal by-product waste removal contracts, there was little enthusiasm to do so. Ten respondents were, however, willing to collaborate to develop a national brand which advertised their product as ‘locally produced, slaughtered, butchered and retailed’, perhaps along the lines suggested by Kennard and Young (2018: 9). Managers whose preference is to work individually or in small groups might follow the example of Airey's abattoir which has developed the Lakeland Herdwick Protected Designation of Origin (DEFRA, 2021) to help safeguard the Herdwick breed while also supporting its throughput.

Seven of the 20 respondents who completed ‘free’ comments wanted less onerous regulations and/or more sympathetic regulation by the FSA and its staff. Specific issues raised included the high cost of OV inspections, the inexperience of some OVs and their inconsistent interpretation of regulations, as well as onerous bookwork requirements and an excess of ‘red tape’. The common view was that much paperwork was unnecessary is summarised by one comment, We can work within the regulatory framework with some simplification of bureaucracy if allowed and we can still maintain the current welfare standards.

Increasing throughput

Twenty-six (92.9%) respondents reported having surplus slaughtering capacity, 24 of which could slaughter at least 10% additional livestock each year. Only four respondents thought expansion would be limited by the supply of livestock and only four that expansion would be constrained by the demand for their products. In principle, therefore, even these small abattoirs could reduce unit costs by utilising this spare capacity. The bottlenecks that prevent this include staffing shortages (reported by seven), and lack of fridge/freezer capacity (again reported by seven). Other respondents referred to insufficient cutting-room space, the need to enlarge current buildings and purchase and install solar panels, and planning restrictions. Lack of capital was the principal constraint preventing the removal of these bottlenecks, with 23 businesses needing to prioritise immediate investment to remain viable in the long term.

Increasing fees and charges

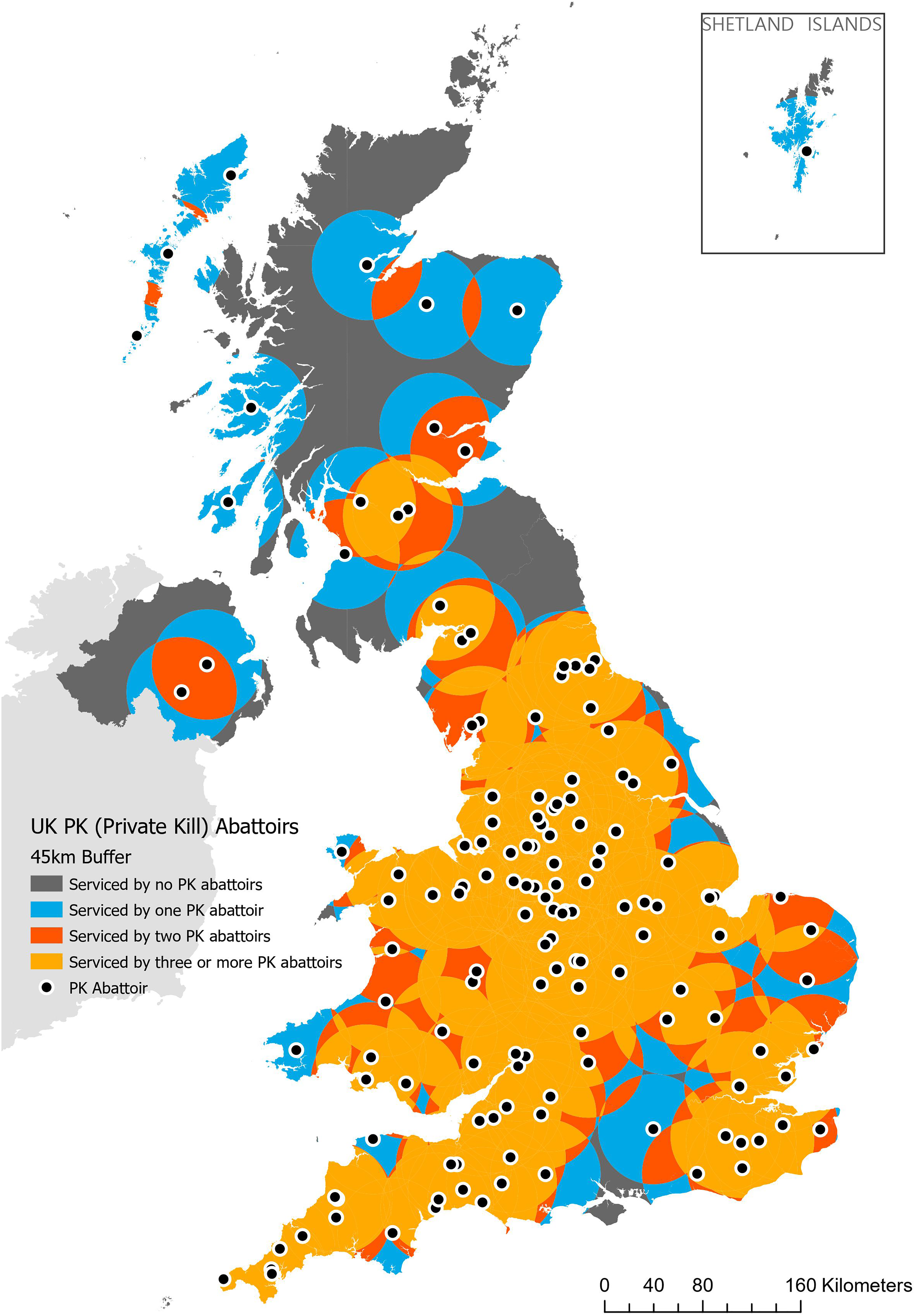

Few small abattoirs publish their slaughter charges and butchering fees, arguing that the bespoke services offered made like-for-like comparisons meaningless. However, their proximity to one other can be used as a proxy for the price competition they face for their private kill services. Figure 5 shows the location of abattoirs which offer private kill services with a 45 km radius drawn around each abattoir. This is the average distance farmers transport livestock from farms to abattoirs for private kill services (Franks et al., 2023) so it represents each abattoir's principal catchment area.

Location of the 147 abattoirs which offer a private kill service in the UK (August 2020) (graphics provided by Jess Hepburn).

Some 18.5% of the UK land area is further than 45 km from an abattoir which provides private kill services, 20.9% of the land area is closer than 45 km to a single private kill abattoir, 13.8% is within 45 km of two such abattoirs, and 47.1% within 45 km of three or more such abattoirs (Franks et al., 2023). The abattoirs closest to one another are likely to have less scope to raise their fees and charges unless they offer some unique and valued service. However, those located near Northumberland, Hampshire, in some regions along the east and west coast, and servicing the Scottish highlands have fewer close competitors and so may be better placed to increase their fees without loss of business to neighbouring slaughterhouses.

As Charlebois and Summan (2014) observed, the closure of neighbouring abattoirs provides opportunities for the surviving abattoirs to increase their throughput by taking trade from closed neighbouring businesses. However, current low profitability and lack of capital to address existing bottlenecks to expansion reduces their ability to absorb this additional business. Also, abattoirs can only increase fees if it remains economically viable for private kill farmers and butchers to use their services.

Diversifying income streams

Small abattoirs could further exploit economies of scope by increasing the range of services they offer. For example, a proportion of farmers do not use their nearest abattoir because it does not hold the necessary slaughter licences, or slaughter certificates (e.g. organic), or offer the farmer's preferred butchering services (Franks and Peden, 2022; SFT & NCB, 2023: 17 and Figure 10). Only 11 abattoirs (39%) offered emergency slaughter of injured animals – meat from which can enter the human food chain is subject to the correct procedures (FSA, 2017). 11 More abattoirs could help reduce farmer's costs by following the example of those that already organised farmers to deliver livestock to a local collecting point (generally a livestock market) for onward transport to the abattoir and to return carcasses/meat to local redistribution points (generally independent butcher shops). Such services would be particularly valuable where distances are great and road networks poor.

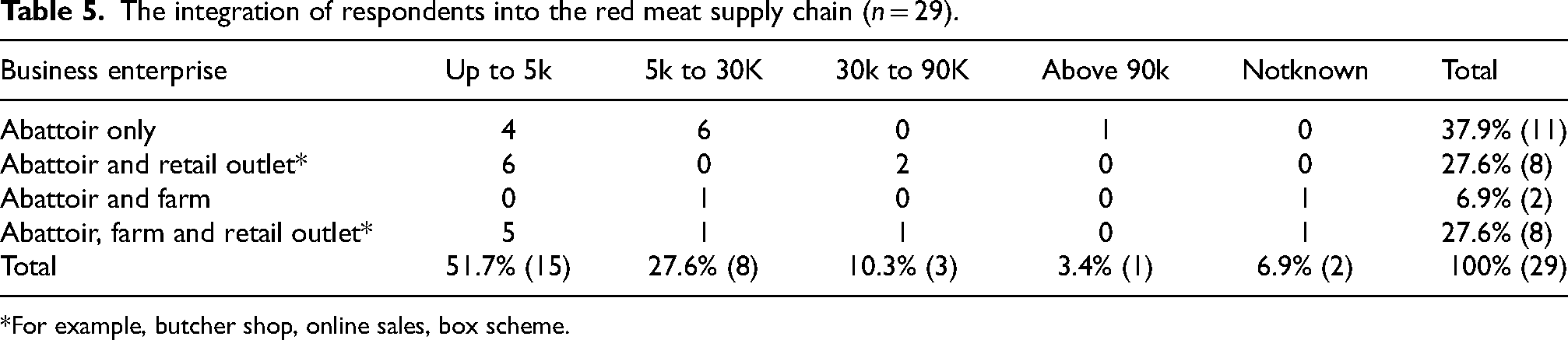

Table 5 shows that 18 (64%) respondents remained vertically integrated into the red meat supply chain. Eight abattoir managers also managed at least one retail outlet and 10 owned farms (eight owned both retail outlet and farm). The relatively high percentage suggests there remains some advantage of the joint ownership of slaughterhouses and retail outlets, both as a source of capital against which loans can be raised, and to allow for the possible cross-subsidisation of businesses. However, eight respondents said their retail business could stand alone from the abattoir, which suggests the long-term trend towards separating ownership of the abattoir and retailer, with the closure of the abattoir, is likely to continue.

The integration of respondents into the red meat supply chain (n = 29).

*For example, butcher shop, online sales, box scheme.

The fall in the value of cattle hides and sheep skin has converted a valuable source of revenue into an additional waste disposal cost (Sustainable Food Trust, 2021). As most hides and skins are exported, their value is determined by global supply and demand (Condon, 2018). Therefore, small abattoirs are price takers. However, they may be able to add value by supporting local and national initiatives, such as, for example, supplying traceable, sustainably produced leather to use to make sustainably produced leather products (Sustainable Food Trust, undated).

Discussion

In the first year of the COVID-19 pandemic, smaller abattoirs reported a 10% increase in throughput (ASG, 2021: 1). This shows the important role they play in maintaining the resilience of the food network. The Government's Health and Harmony paper (HM Government, 2018) accepts there are benefits to having a distributed network of abattoir services (APGAW, 2020). Nevertheless, small abattoirs remain financially vulnerable. This section discusses possible options for helping small abattoirs to become commercially viable businesses.

Complying with new regulatory requirements

Any new technology that is not scale-neutral will, by definition, disadvantage small abattoirs. The compulsory requirement for installing CCTV in 2018 (DEFRA, 2018) is an example of this. An FSA survey undertaken in 2016 reported that 102 out of 207 red meat slaughterhouses (49.3%) in England and Wales had already, voluntarily installed CCTV. These abattoirs covered 92% of cattle, 96% of pigs and 88% of sheep total throughput (FSA, 2016) suggesting the technology is more affordable for larger abattoirs and therefore not scale neutral. In another example, the use of electrical stunning recording equipment was required under European Commission (EC) regulations (EC, 2009). This imposed an estimated cost of between £3000 and £5000 (APGAW, 2020: 32), absorbing capital that could otherwise have been used to improve efficiency by upgrading production lines, expanding fridge capacity and investing in infrastructure maintenance and improvements.

Disproportionate regulations

Responses to this survey, supported by evidence submitted to parliamentary inquiries by the UK Abattoir Network (2021) and presented in APGAW (2020), show widespread support from private kill farmers and abattoir owners for reducing the regulatory burden on small abattoirs. One approach would be to apply the ‘de minimis’ derogation which allows a proportionate approach to regulations on abattoirs with a throughput of <1000 LSUs/year (i.e. applying the 5% rule to “low capacity” abattoirs; FSA, 2007) and which only sell produce within a restrictive geographical area (EU Directive 853/2004/EC (European Commission, 2004: 4, para 13). It is this regulation that allows remote oversight of slaughtering at abattoirs on the islands of Guernsey, Jersey, Alderney and Sark on condition that the meat does not leave the Bailiwick of Guernsey (SA&FC, 2019).

However, although the FSA believes that, Regulatory changes could be made that would deliver official controls that would be less resource intensive, more proportional and that would maintain our current high safety standards in food production. (FSA, 2022: Section 8 Conclusion to Part B)

The FSA has acknowledged several of the problems raised in the survey and in evidence given to the APGAW (2020) inquiry relating to inexperienced OVs and the inconsistency of the interpretation of regulations (FSA, 2023b: Section 3.2, Part A). It intends to address these issues by making better use of technology. For example, using digital tools to inform decision-making and ease the administrative burden on industry and the FSA. It is also considering how the use of DNA identification, live videos, still photography, audio evidence and high-tech thermo-imaging camera technology, enhanced by spectroscopic analysis enhanced by machine learning might allow remote oversight of slaughter. If successful, these technologies could relieve abattoir managers of some of the more burdensome legislative frameworks (AIMS, 2023).

Government support policies

In view of the critical role the APGAW (2020) believes small abattoirs play in ensuring a resilient and sustainable food chain its report supported the introduction of tried and tested remote oversight technologies and a regulatory framework more appropriate to the size of the business. Its additional recommendations include,

establishing emergency funding to ‘rescue businesses without a structured development and business strategy’ (p. 4), evaluation of the waste collection market by the Competition and Markets Authority, reduced business rates for abattoirs processing under 1000 LSU/year, and support for

apprenticeships and training, local food labelling, and mobile abattoirs.

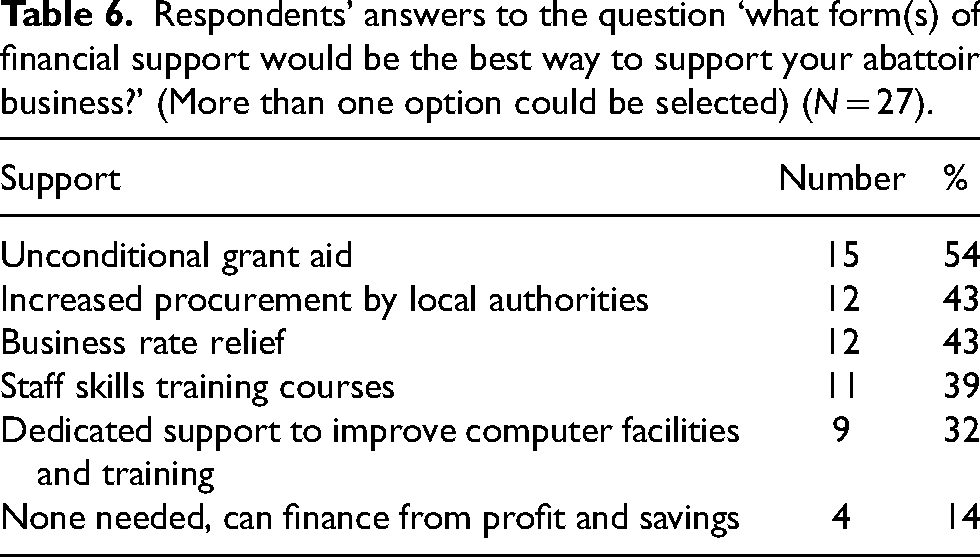

EFRA (2021) suggested that the Future Farming Resilience Fund could be used to pay for business advice to small slaughterhouse businesses. As the fund is designed to offer support to help agriculture businesses adapt to the changes in Agricultural Transition it appears to be an appropriate mechanism. However, there was no evidence from the survey that respondents were anything other than well-informed business people. The survey reported on the forms of financial support respondents favoured (summarised in Table 6). Perhaps unsurprising, the most popular support was unconditional grant aid, but respondents also supported increased procurement by local authorities, business rate relief and funding for staff training.

Respondents' answers to the question ‘what form(s) of financial support would be the best way to support your abattoir business?’ (More than one option could be selected) (N = 27).

The case for supporting small abattoirs has been advocated by the Campaign for Local Abattoirs (CLA) (established in 2018 by The Sustainable Food Trust, National Federation of Meat and Food and National Craft Butchers and others) and more recently by LARK. Through the advocacy of CLA and other organisations, small abattoirs were added to the list of ‘Ancillary Activity’ under the Agriculture Act (Royal Asset, 11 November 2021) which made them eligible for financial support. The £4m Small Abattoir Fund (SAF) was introduced in December 2023 open to abattoirs in England with an annual throughput of <10,000 LSU (DEFRA, 2023a). Applicants are able to apply for up to three grants from a list of items of equipment of between £2000 and £60,000, which either improve productivity, enhance animal health and welfare, add value to primary products or encourage innovation in the use of new technologies. The £60,000 maximum application applies to individual businesses regardless of how many abattoirs they own.

Like the Farm Investment Fund, the SAF offers 40% of the capital cost, but it is more flexible. DEFRA recognises that as ‘each abattoir has different specialisms, requirements and challenges’ applications may be made for equipment which is not on the list. The Scheme has followed recommendations arising from Halliday's (2019) evaluation of the Scottish £66m Food Processing, Marketing and Co-operation (FPMC) scheme in allowing up to three applications from an individual abattoir (to a maximum of £60,000) and flexibility over which items can be purchased. However, DEFRA has ignored other recommendations by requiring abattoirs to pay the entire cost upfront and then claiming the 40% grant back, and it does not offer grants for non-capital items, such as feasibility studies, co-operative ventures and consultancy fees. For example, the FPMC scheme provided £45,000 to undertake a feasibility study into establishing a Scottish Island and Abattoir Association (involving the abattoirs in Barra, Islay, Lockmaddy, Mull, Orkney, Shetland and Stornoway). The SAF cannot provide support for, for example, a feasibility study into the demand for local, or a single national, ‘local meat’ brand.

Conclusions

The slaughtering of red meat livestock in Great Britain is increasingly dominated by international companies which own multiple, geographically distributed, high throughput abattoirs and food processing factories. These businesses have grown by exploiting economies of size and location, and in growing have created new economies of scope by destroying animal waste by-products in anaerobic digesters which saves costs and provides power. Small abattoirs have exploited economies of scope by retaining multi-slaughtering capacity and by developing the bespoke services required by their private kill customers. However, the dominance of economies of size and location over economies of scale has resulted in a high rate of closure of smaller abattoirs which now threatens the provision of private kill networks and therefore of the locally produced, processed and retailed red meat supply chains this service supplies.

These structural changes have been driven by fundamental economic forces that optimise business efficiency. Accepting the contribution of smaller abattoirs to the rural economy and their role in offering a higher value route to market for native and rare breeds, and animal health benefits, the Government has introduced a SAF to offer grants for equipment. It could do more, by, for example, by providing upfront payments to help abattoir's cash flow. It could also lift some of the overbearing regulatory burden by supporting the swift adoption of new technologies designed to allow remote oversight of slaughter. However, small abattoirs also need to work more closely with their private kill customers by, for example, organising local livestock collection for onward transport to the abattoir, and establishing local meat and carcass collection points to help reduce their private kill customers' costs. There is also a need for a feasibility study into the demand for a local value-added brand, and to work together to change the FSA attitude towards facilitating a national ‘local meat’ brand.

Footnotes

Acknowledgements

I would like to thank the abattoir managers who took part in the survey. Particular thanks to Rachel Peden for help with the survey and data analysis, to Jess Hepburn for providing the GIS maps presented in the paper, and to Christine Walsh and Rebecca Wright of the AHDB for providing statistical data. I gratefully acknowledge The Prince's Countryside Fund (now The Royal Countryside Fund since the founder's accession to the throne) for its financial support for this project.

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was funded by The Prince’s Countryside Fund (now The Royal Countryside Fund since the founder’s accession to the throne).