Abstract

Air transport has historically been subject to significant regulation for safety and initially military reasons. As a result of the Second World War, West Germany was subject to two further restrictions: the Allied flight ban until 1955 and the specific regulations governing air transport to West Berlin until 1990. The successful deregulation of civil air transport in the USA from 1978 put Europe under pressure to reform. Beginning in the late 1980s, deregulation began throughout the European Community, resulting in a substantial increase in flight routes to and within Germany. Air travel became more affordable without compromising flight safety. Although Lufthansa ultimately outcompeted the national competitors that emerged, its profitability was severely constrained by intense competition from international low-cost carriers.

Keywords

Introduction

This article examines the regulation of the air transport market in the Federal Republic of Germany, focusing primarily on measures driven by economic considerations rather than technical factors. Compared to other European countries, Germany was an unusual case due to the imposition of specific regulations from 1945 until 1955, as well as from 1955 until 1990, respectively, because of the Second World War and the subsequent Allied occupation. Beginning in the late 1980s, the European Community (EC) assumed increasing responsibility for regulating the air transport market, including within Germany. Beyond outlining the key regulatory and deregulatory measures from a German perspective, the article focuses on the impact of deregulation on air transport in and to Germany.

Limited literature exists on air transport regulation in Germany and its effects prior to European liberalisation. Lutz Budraß's study on the early Lufthansa is informative for the first post-war decade, while Klaus-Dieter Seifert's comprehensive two-volume work on German air transport from 1955 to 2000 covers the subsequent period extensively. These publications address regulatory issues only peripherally. The same holds from an international perspective for the overviews by Anthony Sampson, Alan Dobson and the recent dissertation of Adrian Cozmuta on Europe's main flagship carriers. While ample literature exists covering transport economics since the 1980s, limited attention is given to the long-run perspective or the specific context of Germany. For this strand of literature, the accounts by economists Guillaume Burghouwt and Jaap de Wit as well as Barry Humphreys represent the current state of the art. 1

We aim to analyse the regulation of air transport before and after European Union (EU) liberalisation, focusing on its impact on airlines, routes and airfares, with a specific emphasis on (West) Germany, the largest EU member state. In contrast to the strongly industry-oriented literature, we attempt to interweave our narrative with literature on contemporary history, e.g. the history of consumption, especially tourism, on the one hand, and empirical studies in transport economics on the other hand. Following a concise overview of the most important international conventions on the regulation of civil air transport (section “The regulation of international air transport since 1944”), we delineate the West German regulatory system, which was subject to constraints imposed by the Allied powers until 1990 (section “The regulation of civil air transport in West Germany from 1945 until deregulation in the late 1980s”). We then trace the individual deregulation steps taken by the EC/EU (section “The deregulation of civil aviation in the EC/EU since 1987”) and go on to discuss their consequences for air transport within Germany and from Germany to other EU countries (section “The consequences of deregulation for air transport in Germany”). Section “Summary and outlook” concludes.

The regulation of international air transport since 1944

Until liberalisation in the late 1970s and 1980s, the international legal framework for international air transport was based on the Chicago Convention, bilateral and multi-lateral air service agreements (ASAs) and rule-setting by two international organisations, ICAO (International Civil Aviation Organisation) and IATA (International Air Transport Association). 2

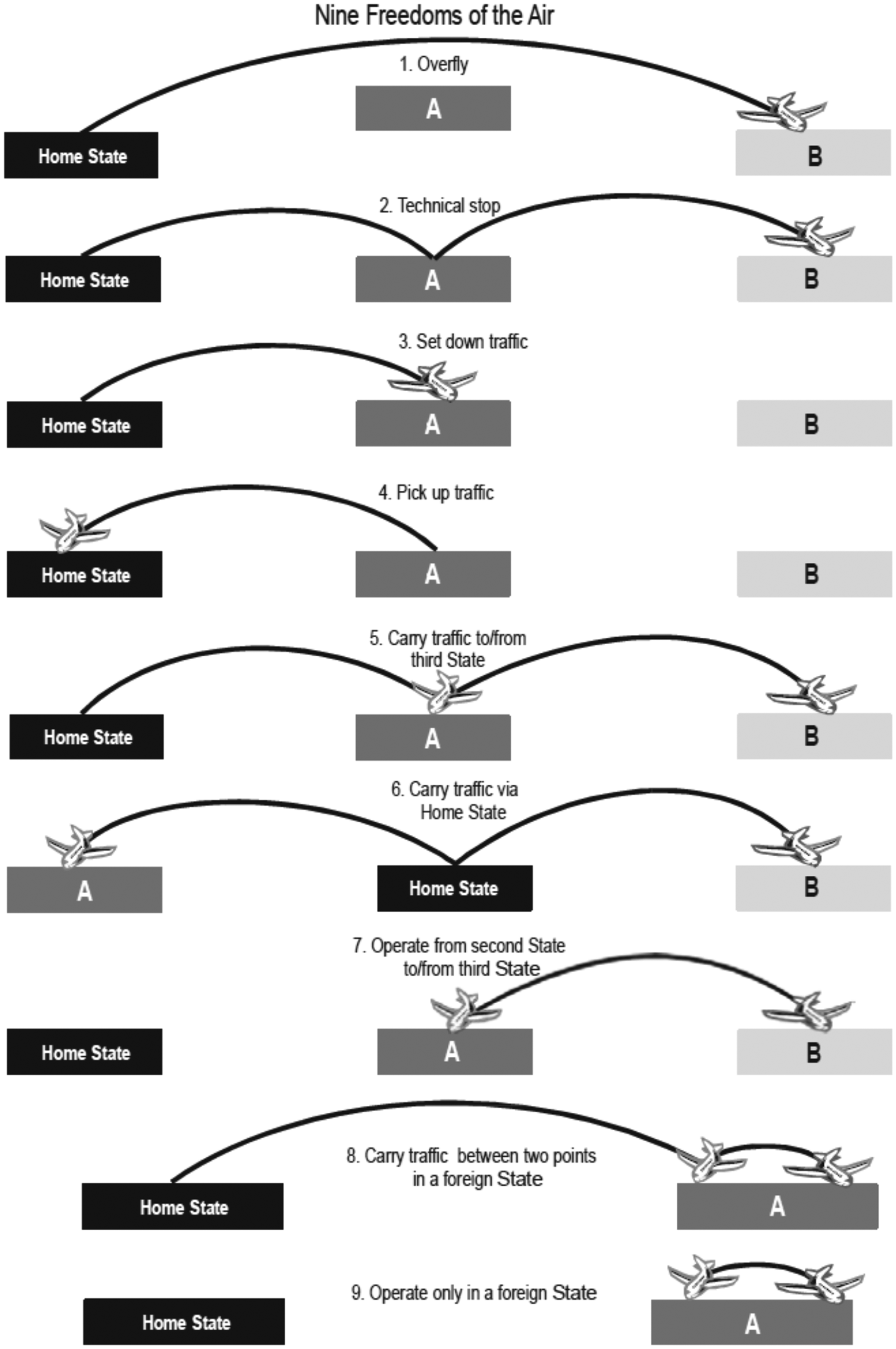

The Convention on International Civil Aviation of December 1944 (Chicago Convention) stipulates that each state maintains responsibility for controlling its national airspace. According to Article 6, each state is free to decide to whom and to what extent it grants traffic rights in scheduled air transport. Consequently, any air transport activity between two states that is not explicitly authorised is prohibited. 3 Subsequently, states signed bilateral or multi-lateral ASAs to define the extent to which contracting parties granted each other the freedoms of the air (Figure 1). In practice, the third and fourth freedoms were initially most significant. It was uncommon for a home state to authorise an airline from a contracting party in country A to transport passengers from its home state to a third country B (fifth freedom). This type of traffic was typically reserved for the home state's flag carrier. In most cases, airlines were required to be substantially owned by a contracting state or its nationals to fully exercise the agreement's rights. 4 Beyond these freedoms, ASAs usually also stipulate very specific capacities and ticket prices, as well as working conditions and safety regulations. These provisions created a highly regulated market environment. 5

Nine freedoms of the air.

The first two freedoms are the subject of a transit agreement concluded at the Chicago Conference (International Air Services Transit Agreement). This agreement represents the largest multi-lateral agreement in aviation, with 135 member states currently participating. A transport agreement was also drawn up for freedoms three to five, but it never came into force. Instead, these are regulated through bilateral ASAs. 6 The lack of codification of freedoms six through nine in international treaties has led the ICAO to term them “so-called freedoms of the air”. 7

Founded in Havana in April 1945 and currently based in Montreal, IATA's original primary function was establishing airfares for international flights. The most important regulatory body was the tariff conferences where IATA members (i.e. the airlines) negotiated international air transport fares. National governments were then required to approve these fares. 8

For instance, scheduled flights between Germany and France were exclusively operated by the national carriers, Air France and Lufthansa, with routes and capacity sharing agreements in place. Ticket prices were standardised, with competition limited to factors such as on-board service and handling quality. Timetables, including fare information, were published in the monthly ABC World Airways Guide (published between 1946 and 1995) which every travel agency subscribed to. The international connections of the Eastern Bloc airlines were also embedded in this tightly regulated system.

In effect IATA was a carefully orchestrated cartel that prevented free price competition. Following deregulation in the late 1970s and 1980s, its significance diminished, and it has since taken on more typical association and lobbying roles for its member airlines. As of July 2025, IATA's membership includes some 350 airlines from 120 countries. 9

The regulation of civil air transport in West Germany from 1945 until deregulation in the late 1980s

During the Second World War, the distinction between civil and military aviation disappeared. Germany's flagship carrier Luft Hansa primarily worked for the Luftwaffe (German air force). Consequently, in 1945, the Allies placed all air transport under their control to prevent Germany from initiating a covert civilian air force, as it had done after the First World War by shifting production to foreign factories or using camouflage organisations. 10 Luft Hansa was banned in 1946 for having been part of the Luftwaffe. 11

As a result, in the first post-war decade, foreign airlines, generously granted traffic rights by the Allied Military Government, took over the West German air transport market. During this period, aircraft from Allied airlines (American Overseas Airlines (AOA) until 1950, Pan American Airways, Trans World Airlines, British European Airways (BEA), Air France) and those from neighbouring European countries (SAS, KLM, Sabena, Swissair) dominated the aprons of West German airports. 12

On 23 May 1949, the West German Basic Law (a quasi-constitution) stipulated that the federal government had exclusive legislative authority over air transport within the Federal Republic of Germany (Article 73, §6). However, it was not until the Paris Treaties were signed in 1954 that the Federal Republic of Germany regained full air sovereignty on 5 May 1955. 13

The Federal Ministry of Transport set up a division for air transport as early as 1949, which was transformed into a department in 1951. A preparatory committee on air traffic, established on 9 November 1951, was tasked with drafting a report on the “tasks, principles, and economic conditions of the future German air transport company". 14 At this time, the concept of a national flag carrier was taken for granted in the Federal Republic of Germany as well as worldwide. 15 Only the USA had several large private airlines at this time, although they were heavily regulated. The committee's final report submitted the following year stipulated that the German airline yet to be founded should have no foreign shareholders, receive start-up funding and join the international air transport cartel IATA. 16

In 1953, AG für Luftverkehrsbedarf (LUFTAG) was founded, which was renamed Deutsche Lufthansa in August 1954 and commenced flight operations in May 1955. Officially, it was independent of the pre-war Luft Hansa. In March 1953, the Federal Institute for Air Traffic Control was also established and in October 1954 the Federal Aviation Office. 17 The institutional infrastructure for the resumption of flight operations by German airlines was thus largely in place. The Federal Republic joined the ICAO in May 1955 and Deutsche Lufthansa joined the IATA in June 1956. 18

Scheduled air transport

With the restoration of sovereignty over its airspace, the Federal Republic claimed the same rights for Lufthansa as other states did for their flag carriers. The regulation of international and even national scheduled air transport in the Federal Republic was effectively governed by the rules of ICAO and IATA.

Scheduled flights to other countries were regulated by IATA. As a latecomer, Lufthansa had a difficult time in the early years when the Federal Republic negotiated ASAs with potential destination countries – the airlines of most partner countries already had landing rights in Germany from the time of Allied air sovereignty. The most important exception was Air France, which Lufthansa regarded as an equal from the outset. 19

Domestic flights were predominantly loss-making until the 1980s and were of little importance to Lufthansa, especially as the Federal Ministry of Transport wanted to avoid competition between the two state-owned companies Bundesbahn, the national railway company, and Lufthansa. The Federal Republic had a majority on Lufthansa's supervisory board through representatives of the federal government, the federal states and the Bundesbahn. 20 Therefore, most domestic flights served as feeder flights for Lufthansa's sole hub at the time, Frankfurt on Main. 21

The pricing of domestic flights was negotiated between the Federal Ministry of Transport and Lufthansa, with a requirement to approve and publish fares until the 1980s. 22 Overall, flying was extremely expensive in the 1950s and 1960s. For a long time, air travel maintained an image of exclusivity. 23

While Lufthansa took over almost all domestic (West) German air transport, the routes to and from West Berlin remained a special case. On 30 November 1945, the Allied Control Council had established three flight corridors to West Berlin as part of an agreement between the four allied forces. From West Berlin, the flight routes went via the Hamburg Air Corridor towards Hamburg and Bremen, via the Bückeburg Air Corridor towards Hanover and on to Cologne/Bonn and via the Frankfurt Air Corridor towards Frankfurt on Main, Stuttgart, Nuremberg and Munich. 24

Prior to German reunification in 1990, only airlines from the three Western Allies were permitted to fly to West Berlin airports. BEA began flying to Gatow in September 1946 and to Tempelhof in 1950, while AOA (acquired by Pan Am in 1950) and later Air France had been operating from Tempelhof since May 1946. All scheduled flights to Berlin were transferred from Tempelhof to the newly built airport in Berlin-Tegel in 1975. 25 That year, Pan Am and BEA successfully applied to the Allied aviation authorities to split the routes to West Germany, which significantly reduced competition. From 1963, western travellers could also fly with Interflug, the East German flagship carrier, from Berlin-Schönefeld to other countries, such as the Soviet Union, Bulgaria and Greece, after having crossed the West–East border in Berlin. 26 From the early 1980s, other airlines from the Western Allies were also granted licences for scheduled flights from Berlin-Tegel to Saarbrücken and to other European countries, including the French regional airline Touraine Air Transport, the British Dan-Air and, in 1987, Trans World Airlines (TWA), Pan Am's major American competitor. 27

In September 1988, Lufthansa and Air France – both companies were still state-owned – founded Euroberlin France. As Air France had a majority shareholding of 51 per cent, it was regarded as a French and therefore Western allied company and was authorised to fly to Berlin-Tegel. This allowed Lufthansa to secure valuable slots, which it was then able to utilise unexpectedly quickly after reunification. In 1990, the airline was renamed Euroberlin and continued to fly as a low-cost carrier (LCC) on behalf of Lufthansa until October 1994, primarily to Düsseldorf, Frankfurt on Main, Cologne/Bonn, Munich and Stuttgart. 28 In October 1990, Lufthansa also took over the slots in the Berlin network of the ailing Pan Am, which urgently needed cash. 29

Charter air transport

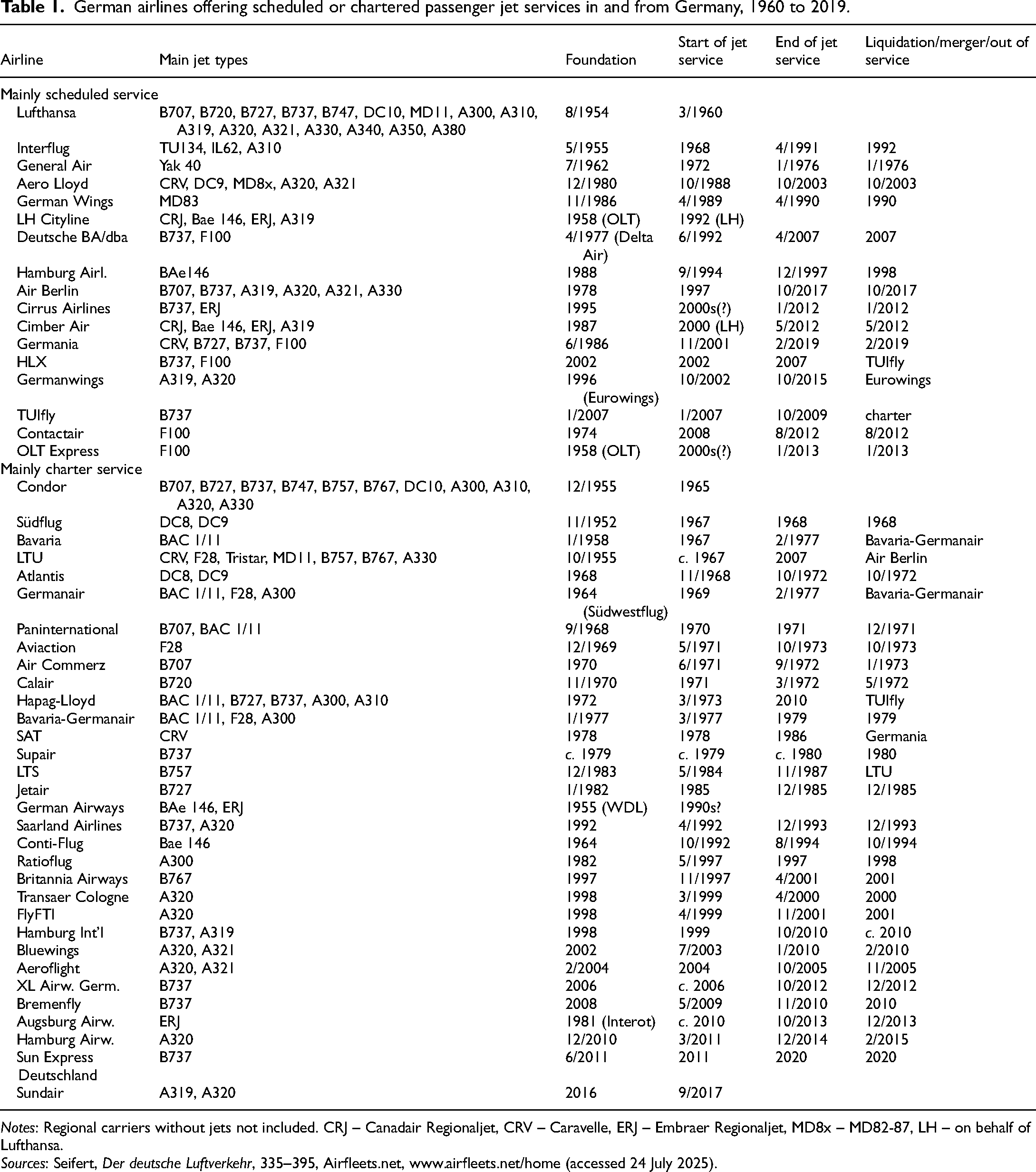

In the 1960s, household incomes in West Germany rose steadily. More people could afford to spend their annual holiday abroad and even take a flight to do so. 30 West German tour operators – Touropa, Scharnow-Reisen, Hummel-Reise and Dr Tigges-Fahrten – joined forces at the end of 1968 to form TUI (Touristik Union International). TUI continued to book overnight stays in hotels, as the hotel industry in Mediterranean countries was inexpensive, as well as ticket contingents with the airlines (charter and scheduled) and offered this in a package as an inclusive tour or package holiday. As a result, charter airlines were able to utilise their aircraft very well. 31 These were increasingly jets (Table 1), including wide-body aircraft such as the Boeing 747 (Jumbo Jet) used by Lufthansa's charter subsidiary Condor from 1971 and the Lockheed Tristar operated by Düsseldorf-based charter airline LTU from 1973. In the 1980s, Spain became the most important main destination for package holidays by German tourists. 32

German airlines offering scheduled or chartered passenger jet services in and from Germany, 1960 to 2019.

Notes: Regional carriers without jets not included. CRJ – Canadair Regionaljet, CRV – Caravelle, ERJ – Embraer Regionaljet, MD8x – MD82-87, LH – on behalf of Lufthansa.

Sources: Seifert, Der deutsche Luftverkehr, 335–395, Airfleets.net, www.airfleets.net/home (accessed 24 July 2025).

As charter flights were not subject to IATA price regulation and typically provided a lower quality of service than flag carriers, package holidays could be offered considerably cheaper than booking scheduled flights plus accommodation separately. However, they had a poorer image than scheduled airlines (the Spanish carrier Spantax alone, which flew many German–Spanish routes, lost several aircraft in accidents 33 ), so Airtours International (a subsidiary of TUI since 1970 34 ), which was founded in 1967, developed a similar concept with scheduled airlines. By combining the scheduled flight ticket with a fictitious hotel voucher, the scheduled flight ticket became de jure a charter flight ticket, so that IATA price restrictions could be circumvented. IATA responded with special fares such as the APEX ticket in 1975, and after deregulation in the 1990s, the status difference between scheduled airlines and charter airlines vanished. 35

The deregulation of civil aviation in the EC/EU since 1987

The liberalisation of civil aviation in the EC would hardly have been possible, or at least not as quickly, without the previous reforms in the USA. As in many areas of aviation, Europe followed its lead.

Deregulation in the USA in 1978

In October 1978, under President Jimmy Carter, the US administration passed the Airline Regulation Act, which revolutionised civil aviation in the USA. Since 1938, the Civil Aeronautics Board (CAB) had set the fares, routes and flight schedules for all domestic air transport routes between different US states (air transport within a state was regulated by the respective administration). While this was a profitable business for the existing airlines, customers and local authorities, who had to subsidise flight routes, suffered from the often very strict regulation of the CAB. During the deregulation the CAB was dissolved in 1984. The remaining regulatory tasks were taken over by the US Department of Transportation. 36

Most of the existing major airlines fell victim to the sudden increase in competition, including Pan Am and TWA, which had specialised in international routes and lacked a connection to the domestic American network. Of the major airlines, only American Airlines, Delta and United have survived to this day (2025); the others either went bankrupt or merged. While they relied on the hub-and-spoke system with central hubs, the new LCCs such as the low-cost pioneer Southwest Airlines mostly flew from point to point and served under-utilised smaller airports. Even though competition increased, an oligopoly of the latter four airlines re-established itself. 37

As hoped, ticket prices fell considerably as competition prevailed on many routes despite oligopolistic structures. The US air transport market was a paradigmatic application of the concept of contestable markets developed in the early 1980s: as long as market entry is not impeded by specific entry barriers, even a monopolist cannot (fully) utilise its market power. 38 Adjusted for inflation, ticket prices in the USA fell by around 20 per cent between 1976 and 1990, which was not only due to increased competition but also due to more efficient aircrafts. 39 Fears that heightened competition would compromise safety were unfounded. Fatalities per 100 million aircraft miles flown in the USA dropped from approximately five in the early 1970s to fewer than two in the 1990s and about 0.1 after the attacks of 11 September 2001. 40

Deregulation in the EC, 1987 to 1997

In Europe, where international air transport was dominated by national flag carriers, the prevailing opinion for a long time was that passenger air transport had to be protected from competition, as it would lead to “ruinous competition” at the expense of quality and safety. 41 Even within the EC, for which the free internal market was virtually constitutive, bilateral ASAs between member states regulated air transport. 42

The obvious success of deregulation on the American market put the EC under pressure to act. The European Commission had already early advocated for liberalisation, and emphasised the interests of consumers in an air transport memorandum in 1979. 43 Several rulings by the European Court of Justice (ECJ), according to which the principles of the Treaty of Rome for the European market should also be applied to air transport, 44 also set in motion efforts to liberalise air transport in the EC–EU since 2009. Britain's Laker Airways proved that low-cost flights could be profitable and safe when it launched scheduled services between London Gatwick and New York-JFK with its Skytrain in September 1977. 45

European policymakers subsequently agreed on three liberalisation packages, which were adopted in 1987, 1990 and 1992 and came into force the following year, respectively. In the first liberalisation package of 1987, the structure of the bilateral agreements (ASAs) was initially retained. However, the strict fare and capacity limits were relaxed, so that a larger number of airlines could now serve the most important international routes within the EC, thus eliminating the monopoly of the flag carriers. In principle, the contracting states granted each other the third to fifth freedom of the air, albeit with restrictions. In addition, cross-border regional air transport was facilitated, which led to a boom in this sector. 46

In the second liberalisation package of 1990, airlines were allowed to agree on prices only with the authorities in their own country. Competing airlines were given easier access to certain routes, resulting in numerous additional direct connections in the EC.

On 1 January 1993, at the same time as the introduction of the EC internal market, the third liberalisation package came into force, which created the conditions for the EC-wide standardisation of operating licences for airlines. This gave all airlines based in the EC access to all cross-border routes within the EC (fifth freedom), if they had previously applied for and obtained an operating licence from the EC. The third liberalisation package, which was converted into a single regulation in 2008, provided exceptions for public service obligations, e.g. on routes to peripheral regions and in the case of code-sharing with airlines from third countries. 47

The abolition of the obligation to obtain authorisation for ticket prices was also very important. These could now be freely determined by the airlines. The third package thus abolished all national controls on the air transport market and invalidated all bilateral air transport agreements between EC countries in favour of one common air transport market.

The fourth and final liberalisation step was added in April 1997 with the freedoms of air eight and nine (cabotage) in the Common Aviation Area for companies of the EC member states, i.e. an airline from an EC country could offer domestic flights in EC country A or international flights from there to any EC country B. This completed the liberalisation of the EC air transport market. 48

The deregulation of the internal market was followed by liberalisation with countries outside the EC/EU. The most important contractual partner of these open skies agreements was the USA. However, due to differing national interests, there was no liberalisation of transatlantic air transport between the EU as a whole and the USA in the 1990s and early 2000s. Instead, bilateral open skies agreements between the EU member states of the Netherlands, Belgium, Finland, Denmark, Sweden, Luxembourg, Austria and Germany (2005) on the one hand and the USA on the other hand have been active from 1992 until 2007.

The European Commission brought an action against the open skies agreements before the ECJ in 1998. In 2002, the Court ruled that bilateral agreements were incompatible with EC law. Specifically, the ECJ declared that the clauses on ownership and control of airlines in the ASAs conflicted with EC legislation on the right of establishment. Additionally, the ECJ established the EC's external competence in air transport, ruling that individual EC states may not conclude bilateral aviation agreements if these agreements violate common EC legal standards, as outlined in the three liberalisation packages. Consequently, a Community clause must be included in bilateral ASAs to ensure that all EC airlines can benefit from the existing bilateral ASAs of all member states. 49 From then on, any new open skies agreements with non-EC countries had to be negotiated exclusively at the EC level, so that the same conditions applied to all EC airlines in international air transport with non-EC countries. Consequently, member states had to cede much of their negotiating power to the EC. As a result, a new open skies agreement concluded between the EC and the USA in 2007 was particularly important. 50 Further agreements were concluded with Switzerland in 2002, Morocco in 2006, Canada in 2009 and Israel in 2013, among others. These agreements reduced the level of regulation but did not grant the contracting parties all the freedoms of the air. 51

The creation of the European Common Aviation Area (ECAA) in 2006 was particularly significant regarding air transport with Northern and Eastern Europe. This extended the liberal provisions that had been created within the EC to non-EC countries, integrating them into the EC air transport market. The decisive point was that the member states of the ECAA fully transposed EC law into national law. The members of the ECAA are all EU states, the EU itself, Albania, Bosnia and Herzegovina, Iceland, Montenegro, North Macedonia, Norway, Serbia and Kosovo. 52

While the regulations above address the liberalisation of competition, the re-regulation of aviation security has also been taking place under the Single European Sky initiative since the 1990s. That is because air traffic control was initially a purely national measure. The six founding states of the EC created Eurocontrol as early as 1963 to better coordinate national air traffic control. Nevertheless, EU air transport is still sub-optimally regulated, so airlines incur unnecessary fuel costs, and the administrative burden remains comparatively high. 53

The consequences of deregulation for air transport in Germany

The consequences of the liberalisation of the EC air transport market were like those in the USA in many, but not all aspects. In general, the effects of liberalisation are difficult to separate from others, particularly the increased economic and technical efficiency of aircraft and computer reservation systems. Other factors include productivity increases in ground logistics. 54

The most significant outcome was the massive increase in competition among airlines within the EU, primarily due to the entry of new LCCs into the market. Since the 1990s, EU airlines have been able to organise their routes and tariffs autonomously within the EU, irrespective of their national origin, including on domestic routes in other EU countries, 55 although the (non-)allocation of attractive slots (take-off and landing rights) at busy airports still allows for some national discretion.

In the EU, too, liberalisation has been accompanied by a further reduction in the risk of accidents. Until today (July 2025), classic LCCs such as Ryanair, easyJet and Wizz have not had any fatal accidents. Germanwings/Eurowings had one fatal accident in 2015 due to the suicide of a co-pilot (150 fatalities). 56

The effects of deregulation on German airlines

The difference with the USA is more apparent on the supply side. Loss-making national flag carriers – except for Swissair and Belgium's Sabena, which both went bankrupt in late 2001 – were kept alive by their governments for a long time (Alitalia until 2021) or even to this day. Some lost their independence (Iberia, Austrian Airlines), but most European flag carriers are still operating today. 57 Almost all of them have been partially or fully privatised since the 1980s. Particularly in the larger countries, the national flag carriers, e.g. Lufthansa, British Airways (BA) have remained or merged, as in the case of Air France and KLM. 58 They continue to focus on quality and comprehensive services and operate a dense intercontinental route network from one base (London-Heathrow, Paris-Charles de Gaulle, Amsterdam-Schiphol) or two hubs (Frankfurt on Main and Munich).

On short- and medium-haul routes in particular, they compete with newly founded LCCs such as Ryan Air, easyJet, Wizz and Norwegian, which have imitated Southwest's business concept and fly point-to-point with low service and low prices (“no frills”). 59 Only a few of the major European LCCs tried to operate on long-haul routes (Norwegian did so from 2013 to 2021) 60 and currently the only one is Lufthansa subsidiary Discover Airlines which in 2021 took over the long-haul routes of Eurowings (long-haul from 2015 to 2020). 61 The main problem for LCCs on long-haul routes is that they are less able to exploit their specific cost advantages (e.g. short turnaround times).

In Germany, liberalisation spurred the emergence of new competitors in scheduled air travel. Between 1995 and 2011 alone, 12 German LCCs operated. 62 Many existing charter airlines entered the market for scheduled services. Moreover, many new charter airlines emerged, part of which also offered scheduled services. Air Berlin, which had been founded by Americans in West Berlin as early as 1978, initially had to restrict itself to charter flights. In German hands since 1991, Air Berlin began operating scheduled flights to popular holiday destinations such as Mallorca in 1997, where the airline later even established a hub for onward flights to the Spanish mainland. Air Berlin subsequently expanded its route network and developed into the second-largest German carrier after Lufthansa. The takeover of Deutsche BA in 2006 (see below), of the Düsseldorf-based charter company LTU in 2007 and of the domestic routes of competitor TUIfly in 2009 also contributed to this. An unclear strategy, high levels of debt and management problems led to the airline's visible decline from 2013, which ended in bankruptcy in 2017. 63

Aero Lloyd began charter flights in 1980 and entered the German domestic scheduled flight market in 1988 but was fiercely opposed by Lufthansa and retained its focus on charter flights. The airline went bankrupt in 2003. 64

A much-noticed newcomer to the German market, i.e. without any previous activity as a charter airline, was German Wings, which offered domestic German routes and routes to Paris in 1989 in open competition with Lufthansa. In contrast to Aero Lloyd, German Wings’ business concept was to offer higher quality, in particular more legroom for the seats, at similar prices to Lufthansa. As German Wings concentrated on the larger German airports (Düsseldorf, Frankfurt on Main, Hamburg, Cologne/Bonn and Munich), it was labelled a cherry picker by Lufthansa, and was specifically targeted, just like Aero Lloyd. Lufthansa's airfares were significantly lower on routes where German Wings competed compared to routes where it maintained a monopoly. Moreover, German Wings had to fight in court for the recognition of its flight tickets under an interlining agreement. In the end, German Wings had to cease flight operations as early as 1990. The Lufthansa Group later acquired the trademark rights in 2008. 65

Pressured by the LCCs easyJet (since 1999, based in Berlin-Schönefeld since 2004) and Ryanair (operating from Hahn in Hunsrück since 2002), Lufthansa penetrated the low-cost segment under the Germanwings brand in 2002. In the following years, it delegated more of its European point-to-point connections from German airports to Germanwings, with the exception of Frankfurt on Main and Munich, which served as hubs. Lufthansa's low-cost offshoot Germanwings has been operating as Eurowings since 2015 and is Germany's second-largest airline in 2025. 66

Under this company name, Eurowings, two small regional airlines, NFD and RFG, had offered scheduled and charter flights from 1993 to the early 2000s, the former partly as a feeder for the hubs of KLM and Air France in Amsterdam-Schiphol and Paris-Charles de Gaulle. It later flew regional services for Lufthansa, which took over the majority shareholding in 2005 and operated the aircraft under the Lufthansa Regional brand. 67

In the early 1990s, BA’s entry into the German domestic market posed a greater threat to Lufthansa than Aero Lloyd and German Wings. BA had initially held unsuccessful talks with (the first) German Wings, the former East German flag carrier Interflug and Aero Lloyd about an investment. Instead, BA took a stake in Delta Air, a small regional airline founded in 1977 which, unlike the aforementioned airlines, was financially sound. Delta Air was renamed as Deutsche BA and in 1992 began operating German domestic flights, mainly to Berlin, and shortly afterwards also scheduled and charter flights to other European countries. 68 The EU’s last liberalisation step in 1997 was used by Deutsche BA (BA as sole owner since 1998) as an opportunity to expand the fight against Lufthansa. This led to even greater pressure on ticket prices, which Deutsche BA was ultimately unable to cope with. As Deutsche BA always remained loss-making, BA lost interest and sold its shares in 2003. After several changes of ownership, Deutsche BA, now dba, was sold to Air Berlin in 2006 as mentioned above. 69

The shipping company Hapag-Lloyd set up a charter airline of the same name in 1972, which integrated its competitor Bavaria-Germanair in 1977. In 2002, TUI, which had been majority-owned by the Hapag-Lloyd Group since 1998, founded the LCC Hapag-Lloyd Express (HLX), which offered scheduled low-cost flights in competition with Air Berlin and Germanwings. As part of a standardisation of its brand image, the TUI Group created the umbrella brand TUIfly, under which Hapag-Lloyd Flug (since renamed Hapagfly) and HLX operated from 2007. During a cross-shareholding with Air Berlin, TUIfly sold its scheduled services, which mainly served Germany and Italy, to Air Berlin in 2009. Since then, TUIfly, now (2025) Germany's fourth-largest airline, has mostly operated charter flights. 70

Like TUIfly, Condor is a holiday airline that is part of larger tourism groups for whose package deals it provides flight services. 71 Condor has been operating since 1956 (until 1961 as Deutscher Flugdienst) and from 1971 was the first holiday airline in the world to use the Boeing 747 (Jumbo Jet). Lufthansa held a blocking minority stake from the outset and was the majority shareholder since 1959. Condor repeatedly bought up other German charter airlines because Lufthansa was keen to keep competition low. 72 It was therefore Germany's largest charter airline from the 1960s to the 1980s. Lufthansa reduced its shareholding in 1997 and has no longer held a stake in Condor, since 2009 Germany's third-largest airline. 73

For a long time, Condor's biggest competitor was LTU, which was founded in 1955 and initially flew for large travel agencies, but from 1986 onwards bought them up itself or took a stake in them. 74 However, unlike Air Berlin and Hapag-Lloyd/TUIfly, LTU and its southern German subsidiary LTS (1984–98) did not participate in scheduled air transport when liberalisation permitted this. LTU was unable to keep up with the fierce price competition and was sold to Air Berlin in 2007. 75

Table 1 gives an overview on the established and the new German airlines until 2019. To avoid inflating the table, only those airlines which operated jets for passenger services and with a minimum of 32 seats (Yakovlev 40) are listed. The fourth and fifth columns give the dates when the airline began to offer scheduled or charter services with passenger jets.

Overall, it can be seen that because of liberalisation, existing charter airlines now also offered scheduled services and new ones were founded, especially after full liberalisation in 1997. Most of them disappeared from the market after a few years. This fate also affected relatively large airlines that had been in existence for some time, such as LTU or Air Berlin. Although the Lufthansa Group (including Eurowings) now owns about 85 per cent of German airlines’ aircraft, the cut-throat competition has led to a different outcome compared to the USA, as many non-German airlines have had significant market shares since 1997, above all (as of July 2024) Ryanair, easyJet, Wizz, Norwegian, Vueling and Air Baltic. 76 Because of this, the Lufthansa group performed poorly in terms of profitability. 77 This supports the idea that the German air traffic market was (and still is) contestable in the sense of the theory.

The impact of deregulation on routes

While the literature on the history of specific deregulation measures in European civil air transport is almost unmanageable, the same cannot be said for the analysis of their economic effects. This is mainly due to the difficulty of obtaining empirical data or, if available, of calculating the effect of liberalisation, especially as the aircraft used have become increasingly efficient over the same period.

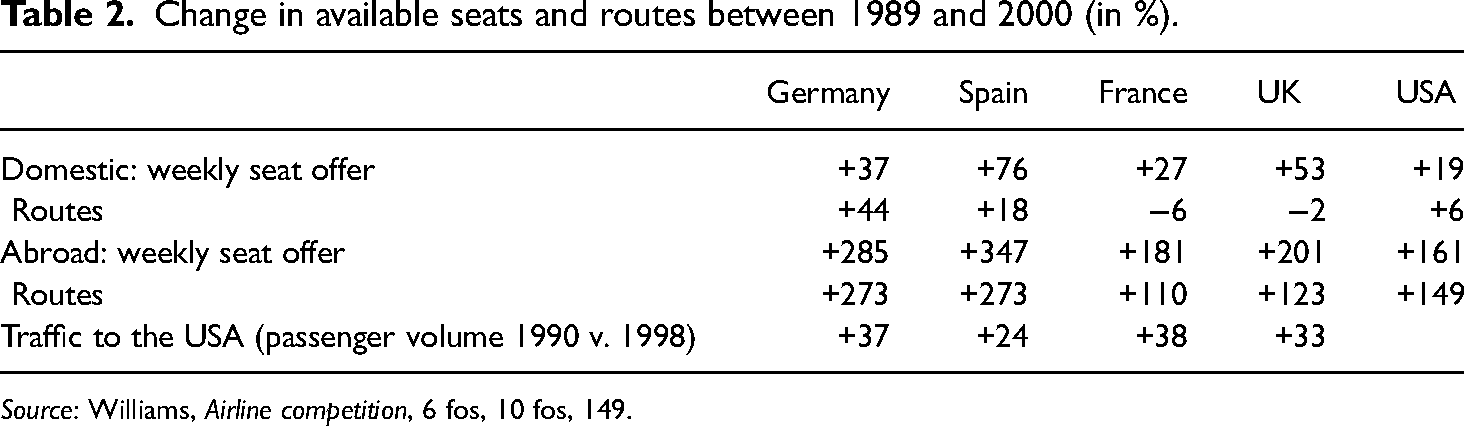

There is relatively easily available data on the number of flight connections and the capacity on offer. This was analysed by George Williams in the early 2000s. Table 2 shows this for some European countries and the USA. Here, deregulation was already a decade ago in 1989, so that the changes in routes (+6 per cent) and capacity (+19 per cent) in the domestic market up to the reference year 2000 were small. In comparison, both figures rose rapidly for Spain, which has a significant domestic flight market, and Germany. The many new routes offered in Germany were partially a consequence of German reunification in 1990. In France, on the other hand, the accelerated expansion of the high-speed train network is likely to have had a dampening effect. Much more impressive is the expansion of international flights. Although it was still common in the 1990s to book return flights and ticket prices in Germany (probably) had fallen less than in other European countries 78 , the number of routes and seats on offer almost quadrupled. This also applies for flights to the USA, which concluded several open-skies agreements in the 1990s, including EC member states and among them Germany.

Change in available seats and routes between 1989 and 2000 (in %).

Source: Williams, Airline competition, 6 fos, 10 fos, 149.

There is a consensus that liberalisation has led to a significant and sustained expansion and increased flexibility of supply within Europe. Transport economists Burghout and de Wit proposed a periodisation. For the years 1990 and 1993, i.e. the period between the second and third liberalisation packages, which was also characterised by macroeconomic weakness, they find little evidence of an effect of liberalisation: the number of routes increased slightly in the study area: EU15 plus Switzerland and Norway (EU15+2). However, the frequency remained essentially constant and the number of airlines per route even fell.

According to them, the second phase from 1994 to 2000 is characterised by the “growth of flag carriers and hub systems”. A number of European flag carriers entered into alliances with major US airlines and began or intensified hub-and-spoke networks. The cooperation started with code-sharing agreements which often led to airline alliances, the first of which was Star Alliance bringing together Air Canada, Lufthansa, SAS, Thai Airways and United Airlines. Star Alliance made its debut in 1997 and was soon followed by Oneworld and SkyTeam. 79 In Germany, Lufthansa even established a second hub for Star Alliance flights in Munich in 2003. 80 In this second phase, the number and frequency of routes within the EC rose sharply, as did the number of airlines per route, i.e. competition intensified.

The expansion of routes is also due to the emergence of LCCs, which have been added since the third liberalisation package and shaped the third phase from 2001 to 2013. With their new point-to-point services, they drew traffic away from the hubs of the flagship carriers, so that although the number of routes and the number of airlines per route continued to rise, the route frequency fell 81 – instead of Frankfurt-Marseille with Air France or Lufthansa, it was now possible to fly Hahn-Montpellier thanks to Ryanair. 82

This increasing competition has been described by Williams in the Frankfurt–London route. Although the number of providers fell from nine to five between 1989 and 2000, this was due to the discontinuation of occasional stopover connections by non-European airlines, which did not play a role in terms of volume. In contrast, the number of seats on offer increased by 59 per cent during this period, with additional airports such as Hahn on the German side and Stansted on the English side now being offered. In 2001, Lufthansa and BA shared the market on the traditional Frankfurt–Heathrow route, but the latter now also flew to Gatwick, while Lufthansa offered City Airport and Stansted. Ryanair flew Stansted–Hahn and Buzz Stansted–Frankfurt. While Lufthansa continued to charge comparatively high prices on the Heathrow route, it tried to undercut Buzz and Ryanair on the Stansted route. In 2001, Lufthansa still had a market share of 52 per cent, BA 31 per cent and the two LCCs together 17 per cent. 83

The market share of LCCs in the EU15+2 region rose from 3 to 27 per cent between 2001 and 2013. However, as in France, the share of LCCs in Germany was not as high as in the UK, Spain or Italy. The many new flight connections led to a process of de-hubbing during this phase. From the perspective of German passengers, this primarily affected the airports in Brussels, Basel and Milan, which lost their hub function. The increasing competition was also reflected in the revenue per passenger kilometre, which fell sharply in US dollar terms, especially after 2011.

In 2014, there were signs of a further trend reversal as not only easyJet, but also the market leader Ryanair, increasingly offered routes to the major airports whose intra-European traffic had previously been largely reserved for the flagship carriers. In addition, new competitors entered the market from Turkey, the Arabian Gulf and South-East Asia, some of which were subsidised by the state, and developed their home airports into hubs for air transport to South and East Asia as well as Australia and New Zealand. 84

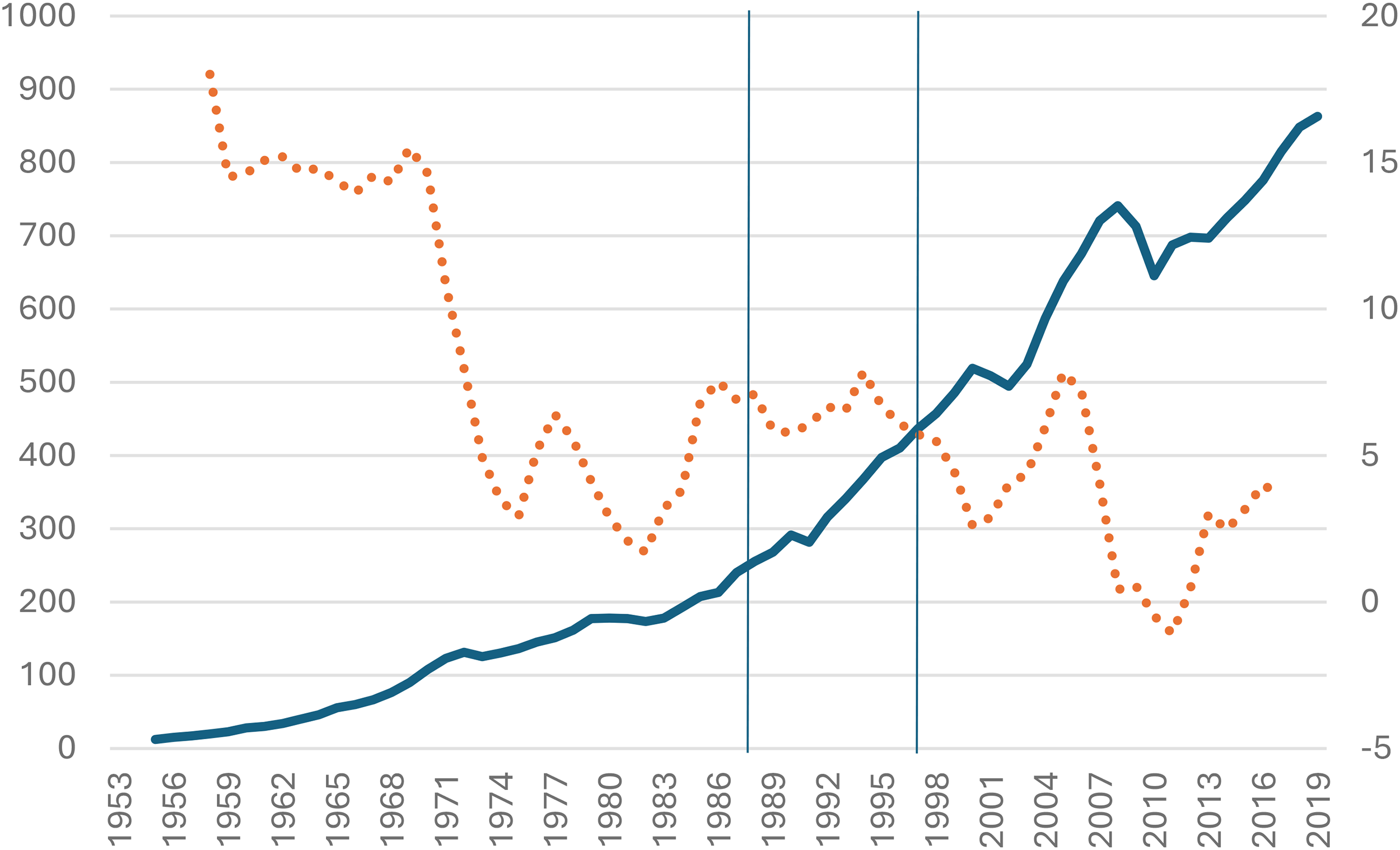

It is difficult to quantify the extent to which deregulation has contributed to the significant increase in passenger kilometres flown to and from Germany. In Figure 2, the passenger kilometres flown to and from (West) Germany are divided by population (solid line). The dotted line shows the (smoothed) rates of change. After years of rapid growth in the 1950s and 1960s, growth levelled off from 1973 and into the early 1980s. Beginning already shortly before the time of the liberalisation of air transport in the EU internal market, there was a renewed surge in growth, with the years 1992 to 1995 being particularly dynamic. There were declines in 2001 because of the attack of 11 September and in 2009/2010 due to the global financial crisis.

Passenger-kilometres (pkm) flown per capita of the population in (West) Germany 1953–2019. Note: Solid line indicates kilometres flown per capita; dotted line the rate of change in 5-year moving averages (in percentage). Unified Germany since 1991. Vertical lines stand for the deregulation period, 1987 to 1997.

Germany experienced a strong resurgence in air-transport growth starting in 1984. However, the impact of liberalisation, at least from 1987 onwards, cannot be clearly determined, as more precise data is lacking. It is very likely, though, that the boom phase from 2003 to 2007 is linked to the strengthening of LCCs.

The impact of deregulation on airfares

Flying has become cheaper because of deregulation, but this is much more difficult to prove empirically than one might think. Firstly, several factors generally have an impact on ticket prices in the medium and longer-term: quality, flexibility, the price of kerosene 85 , the increasing efficiency of aircraft and the logistics behind them, such as computerised reservation systems. Although the effect of liberalisation has been quantified using appropriate econometric methods by comparing prices on structurally similar but differently liberalised routes and controlling for the other influencing factors (difference-in-difference approach), the authors of these studies are interested in using current price data, not data from further back in time. 86

For the period of interest here, shortly before and after liberalisation, i.e. from around the beginning of the 1980s to the mid-2000s, there is simply a lack of publicly accessible, reliable data for Germany (or Europe). 87 The little information available on airfares is of poor quality or lacks comparability. Up to and including 1998, the German Federal Statistical Office did publish airfares on individual routes, such as from Frankfurt on Main to Berlin, Paris or New York. However, it only took into account price data from Lufthansa. In 1999, the Statistical Office started using a broader data basis and explicitly referred to the effects of deregulation. Nevertheless, this (seemingly) considerably more representative data was only calculated back to 1995. 88

Apart from that, the airfare data provided by the German Statistical Office for 1995 to 2010 is implausible. It suggests an increase of economy class airfares for German domestic flights between 1995 and 2010 of 111 per cent(!) and for flights from Germany to European destinations of 58 per cent (German consumer price index: +24.1 per cent). Worse, it is inconsistent. For example, the change of economy class airfares for domestic flights from 2005 to 2006 is −6 per cent in the volume for 2007 and +4 per cent in the volume for 2012. 89 Moreover, there is absolutely no anecdotal evidence that could support an increase for domestic flight airfares between 2004 and 2005 of 31 per cent (2007, p. 5), or between Germany and Austria of 127 per cent from 2010 to 2011 (2018, p. 9). 90

Data providers such as IATA or OAG do not dispose of price information for the period of interest here. The reservation systems Amadeus, which is of great importance for European air transport, Galileo, and Sabre did not respond to corresponding enquiries. 91

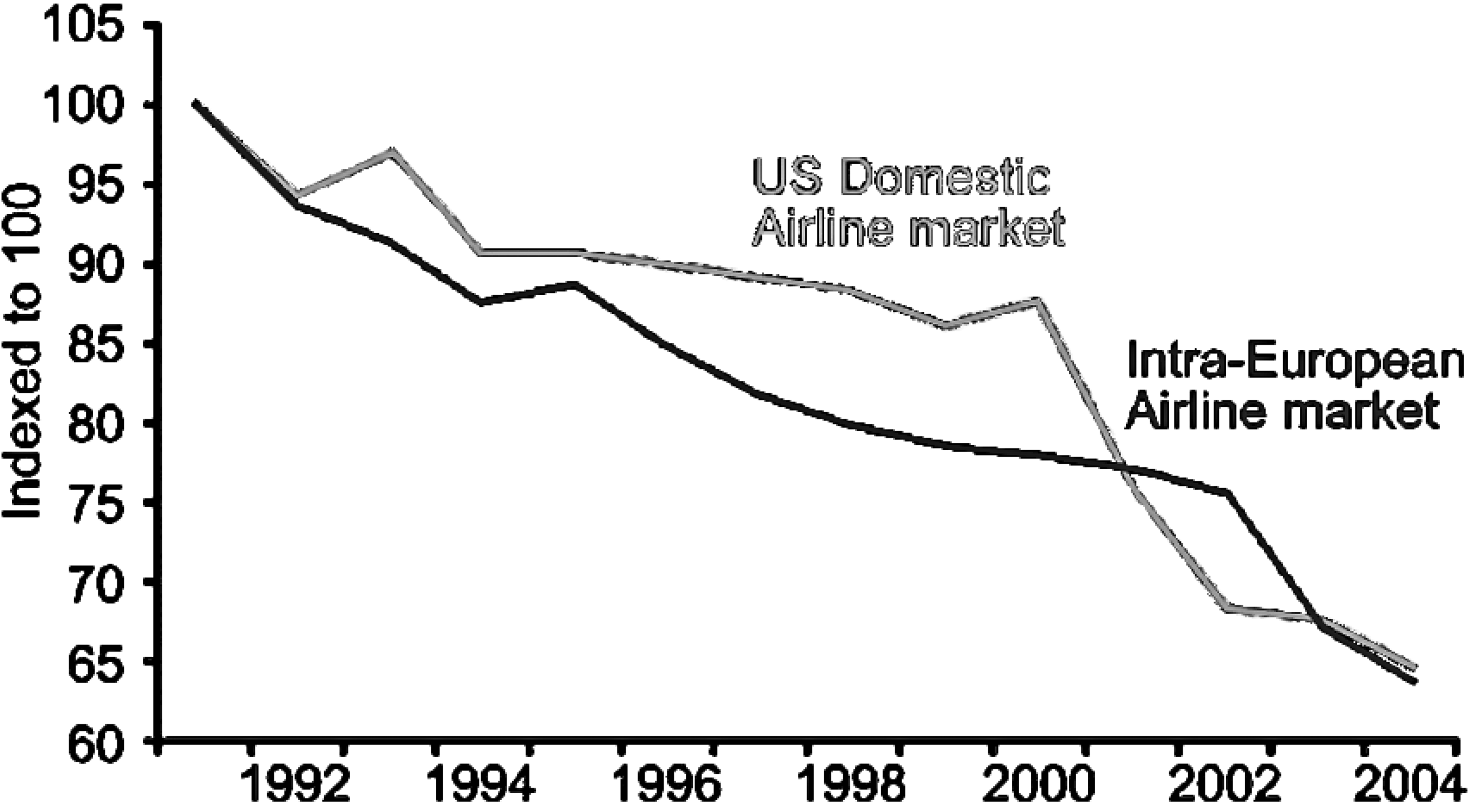

What is clear is that prices fell on the EC level. In its annual report for 2005, IATA published highly aggregated data for the intra-European flight market. According to this, ticket prices in the EU fell by just over 35 per cent in real terms between 1991 and 2004 as a result of liberalisation (Figure 3).

Real ticket prices in liberalised aviation markets (Europe and USA).

For the period from 2002 to 2015, Abate and Christidis analysed ticket prices for flights from the EU to third countries with and without an open skies agreement. Using price data from the Sabre reservation system, they were able to show that liberalisation had a price-reducing effect above all when the partner country adopted the same standards in air transport with the EU. 92 However, this study does not allow any analysis on a differentiated level for the air transport market in Germany or from there to other EU countries.

In the absence of valid longitudinal data, we have to rely on contemporary analyses of ticket prices, i.e. cross-sectional analyses. For routes from the UK, the Netherlands and Germany to Italy, a team of authors used data from the Galileo reservation system for the years 2001 to 2003 to show that ticket prices fell significantly after the fourth stage of liberalisation when competition increased as a result of market entry. This applies both to increased competition from traditional flagship carriers and in particular when LCCs entered the market. 93 The price-reducing function of competition from LCCs hardly changed in Europe, at least until the last few years before the COVID-19 pandemic (2016–19). 94

In an analysis for the year 2001, it was empirically shown for domestic German air transport that Lufthansa remained the clear market leader, but that the ticket price on domestic German flights was lower on those routes where the degree of concentration was lower, i.e. where there tended to be more competition. 95

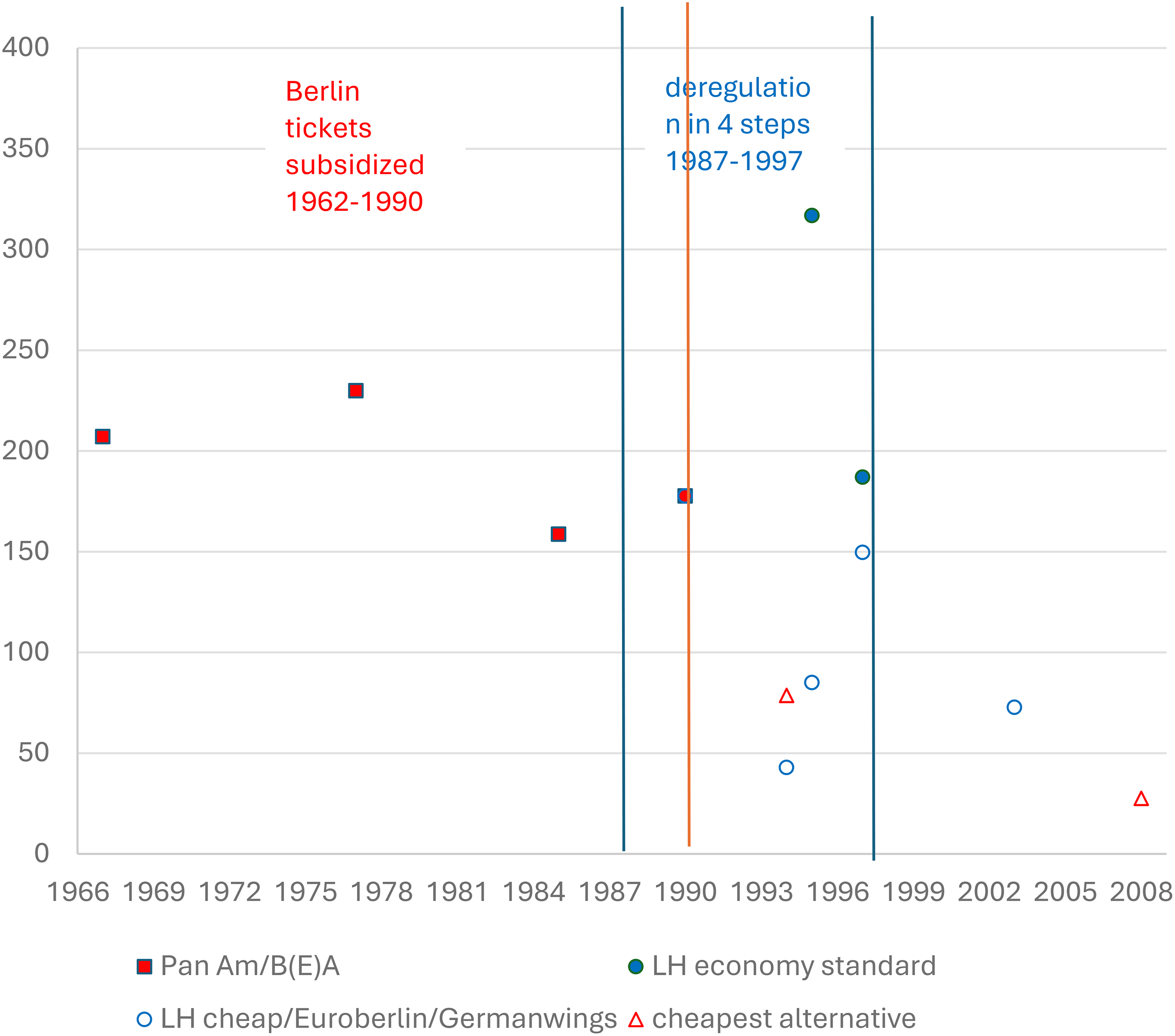

Since we were unable to identify systematic historical airfare data, we compiled prices for an exemplary route – Stuttgart to Berlin – from various sources. During the period of allied air traffic restrictions, this route was operated exclusively by Pan Am and British (European) Airways at least until October 1988 and was heavily subsidised by the West German government (since 1962). In November 1988 Euroberlin (France) commenced operations, followed by Lufthansa, which had taken over the routes from Pan Am in 1990, and Deutsche BA in 1992. 96 In 1994, when Deutsche BA was competing strongly with Lufthansa on this route, the price for Lufthansa's cheapest economy return ticket was, converted from Deutsche Mark, 153€ (thus cheaper than comparable domestic routes without competition), whereas Deutsche BA charged 92€. Special tickets at a Lufthansa fare of 50€ were considered sensationally cheap and sold out very quickly. 97 Lufthansa's ordinary economy return ticket fare for the route was 377€ in 1995 and 230€ in 1997. 98 The same route was served by four airlines in 2008. TUIfly and Air Berlin, which regularly offered tickets to and from Berlin-Tegel for 19.99€ and 29€ respectively, were the cheapest providers when booked early. The LH subsidiary Germanwings flew this route to Berlin-Schönefeld and charged a minimum airfare of 40€ (one-way in each case). Lufthansa, which still served the route at this time, was considerably more expensive. 99

Figure 4 illustrates the decline in air fares on the Stuttgart–Berlin route. It presents the prices for a return ticket, inflation-adjusted to the price level of 1990. Our focus here is on the cheapest price at which one could fly from Stuttgart to Berlin (note that tickets were subsidised by around 20 per cent until 1990).

Fares for a return ticket (economy class) on the route Stuttgart–Berlin (in prices of 1990).

Summary and outlook

The history of EU-wide deregulation of air transport has been frequently described. What makes the German case particularly unique are the special rights of the Allies until 1990. Until 1955, when the Federal Republic regained air sovereignty, foreign airlines completely dominated the market. With the resumption of flight operations by Lufthansa in 1955, the West German air transport market developed similarly to that of other European countries – except for the fact that the largest city, West Berlin, could only be served by Allied airlines until 1990. The increasing competitive pressure resulting from EU-wide deregulation in the late 1980s manifested itself in a sudden rise in the number of airlines that challenged or even displaced the market leaders of the 1970s and 1980s – Lufthansa (scheduled flights), Condor, and LTU (both charter flights). Particularly since the 1990s, the number of flight routes to and from Germany has increased significantly. Traffic grew to such an extent that Lufthansa was able to establish a second hub as the only European airline. Although Lufthansa was ultimately able to drive the national competitors that had emerged in the meantime out of the market, the competitive pressure from foreign LCCs was so great that the company was hardly able to make any profits.

The decline in relative prices for flights to and from Germany during this period can be substantiated through econometric cross-sectional studies for the EU and anecdotal evidence for Germany. However, the specific roles played by deregulation on the one hand and increasing technical efficiency on the other have not been conclusively determined in this paper. Future research will need to conduct a more precise quantitative analysis of these factors. A database containing historical airfares would be essential for such an endeavour. The contribution of liberalisation to the reduction in ticket prices could then be estimated relatively simply using difference-in-difference analyses.

Overall, the evidence suggests that deregulation was highly successful: more Germans were able to travel to more destinations more safely and for less money. However, three decades after deregulation, the disadvantages, such as overtourism and, in particular climate impacts, become apparent. 100 Because the negative impact on the climate is a classic external effect (i.e. one that is not priced in without regulation), air transport will continue to require regulation.

Footnotes

Declaration of conflicting interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.