Abstract

We study how economic crises relate to the likelihood of experiencing regime changes ‘from within’; that is, transitions brought about, in part or fully, by actors in the incumbent regime. While historically common and influencing the political trajectories of many countries, such processes are far less studied than regime transitions forced by non-incumbent actors, such as coups or revolutions. We synthesize previous arguments and further specify how crises can incentivize leaders to change the regime from within due to two mechanisms. First, crises create windows of opportunity for leaders to pursue transitions they inherently prefer, for instance through self-coup. Second, crises sometimes allow opposition actors to mobilize and threaten the regime, forcing incumbents to liberalize. We leverage new data on timing and mode of regime change for more than 2000 regimes from about 200 countries, during the period 1789–2018. Employing different measurement strategies, estimators, control variables and other specification choices, we find fairly robust evidence that economic crises are related to transitions from within. However, when we distinguish between liberalizing and non-liberalizing guided transitions, we only find that economic crises systematically relate to the latter, suggesting that the window of opportunity mechanism may be especially pertinent in many contexts.

Introduction

Economic crises are associated with different kinds of upheaval. Crises bring increased unemployment, job insecurity and income loss. But they also spur political upheaval, from government change in democracies (Lindvall, 2017) to civil war onset (Hegre & Sambanis, 2006). Cross-national studies have even linked economic crises to increased risk of regime change (Geddes, Wright & Frantz, 2018; Djuve, Knutsen & Wig, 2020). A plausible explanation is that economic crises – for instance through increasing grievances in the population (Gurr, 1970) – mobilize opposition against the regime, which, in turn, leads to forced regime change. Indeed, empirical studies report evidence that economic crises are related to heightened risks of revolutions (Knutsen, 2014) and coups d’état (Gassebner, Gutmann & Voigt, 2016).

Yet, revolutions and coups are far from the only modes through which regimes die, and the aggregated relationship could reflect that crises drive also other modes of regime change. Regime changes often come about through processes where the regime incumbents themselves guide the transition. Globally, over the last two centuries, such ‘transitions from within’ have been about as common as coups, and far more common than revolutions. Transitions from within have thus shaped political development and the current institutional framework in numerous autocracies and democracies. Nonetheless, these processes (and their potential determinants) remain far less studied than coups and revolutions. In this article, we address this gap by asking: do incumbent-guided regime transitions become more likely when a country experiences an economic crisis? If no, this would present an important qualification to the notion that crises generate different kinds of political instability. If yes, this would add to the notion that crises endanger regime survival, but specify that this is not only (or even predominantly) due to crises spurring external actors to directly force regime change.

We argue and show empirically that economic crises do, indeed, spur processes of regime change that originate from ‘within’ the regime. This subset of regime changes includes, first, liberalization processes of previously autocratic regimes that are managed by incumbent regime elites (e.g. Acemoglu & Robinson, 2006). Second, it includes other incumbent-guided transition processes unaccompanied by substantial changes in degree of democracy, such as managed changes from a personalist regime to an institutionalized one-party autocracy (e.g. Geddes, Wright & Frantz, 2018). Finally, it includes self-coups, where a sitting leader concentrates power in his/her own hands under a more autocratic regime (e.g. Svolik, 2015). Despite this heterogeneity, these processes are all managed by representatives of the sitting regime and – we propose – are all more likely to occur immediately after an economic crisis.

We synthesize and further develop insights from existing arguments, elaborating on the conditions under which economic crises likely spur transitions from within. Previous arguments have been restricted to particular types of transitions from within, especially elite-guided democratic transitions (e.g. Acemoglu & Robinson, 2006). Our argument builds on important insights from these contributions, but addresses the more general question: why would incumbents accept changes to their current regimes, and why would they more often do so after economic crises? We propose that economic crises can motivate leaders to change the regime through two main mechanisms. First, crises sometimes weaken opposition actors, increase general distress, and create windows of opportunity for changing the regime in a direction that leaders inherently prefer. Democratically elected leaders who use crises as a pretext for self-coups – the most common source of democratic breakdown in recent decades (Lührmann & Lindberg, 2019; Svolik, 2019) – is one example. Second, crises sometimes mitigate the regime’s power resources and help opposition actors to mobilize. In such circumstances, incumbents might prefer to negotiate regime change with the opposition as a lesser evil, to avoid direct confrontation.

Still, our main contribution is empirical. We are unaware of any similar large-N study that exclusively focuses on processes of regime change from within and how they relate to economic crises (or other potential determinants). This lack of empirical studies is not due to regime changes from within being rare phenomena – we show that they outnumbered regime changes stemming from military coups or revolutions through much of modern history. Instead, the missing empirical studies presumably come from the lack of comprehensive data tracking these changes. This situation has changed with the recent ‘Historical Regime Data’ (HRD; Djuve, Knutsen & Wig, 2020), embedded in the Varieties of Democracy (V-Dem) dataset (Coppedge et al., 2019). We employ these data – recording more than 2000 political regimes and about 700 regime changes from within, from 201 countries and the period 1789–2018 – in our analysis.

We document a fairly robust aggregate relationship, indicating that immediately after an economic crisis the probability of regime change from within increases. When disaggregating our outcome variable, we find a clear link with self-coups and non-liberalizing guided transitions, but not with incumbent-guided liberalization episodes. Given the scope of our analysis and data at hand, we cannot exclude all alternative explanations and precisely identify any causal effect. Nonetheless, our analysis yields evidence in line with the proposed window of opportunity mechanism, but not as clearly in line with the lesser evil mechanism. Hence, we find it plausible that economic crises often drive incumbent-guided transitions by providing sitting elites with an opportunity to change the existing regime to a new one that these elites prefer.

Literature review

Large-N analyses of regime change are plentiful, especially those that consider transitions between autocratic and democratic regimes (e.g. Przeworski et al., 2000; Boix, 2003; Svolik, 2015; Treisman, 2020; Miller, 2021). This holds true even if we consider studies addressing the relevance of economic crises for such transitions. Several cross-country studies find that slow or negative gross domestic product (GDP) per capita growth is conducive to transitions in both directions (Przeworski & Limongi, 1997; Burke & Leigh, 2010; Kennedy, 2010; Brückner & Ciccone, 2011; Ciccone, 2011; Aidt & Leon, 2015), whereas high inflation seems to increase risk of democratic breakdown (Gasiorowski, 1995; Gasiorowski & Power, 1998; Bernhard, Nordstrom & Reenock, 2001). Geddes, Wright & Frantz (2018) report a relationship between slow growth and regime breakdown, overall, but qualify that the relationship depends on the incumbent regime’s institutional structure. Krishnarajan (2019b) finds that this overall relationship is strongly moderated by natural resources income.

Other studies focus on distinct modes of regime change, especially changes being forced by actors external to the regime. Such actors could be large groups of citizens or smaller groups of military officers driving, respectively, popular revolutions (Chenoweth & Stephan, 2011; Celestino & Gleditsch, 2013; Kendall-Taylor & Frantz, 2014) and coups d’état (Powell, 2012; Olar, 2019; De Bruin, 2020). These literatures have generated empirically based insights into how and when regimes die, and one key factor preceding both successful popular revolutions and coups is economic crisis (e.g. Knutsen, 2014; Gassebner, Gutmann & Voigt, 2016). Several scholars (e.g. Davies, 1962; Gurr, 1970) have theorized that economic crises are related to such externally forced regime changes because they enhance grievances. Another (and complementary) argument is that economic crises generate focal points that ease collective action problems among latent regime opponents, allowing them to mobilize simultaneously and ensure that revolutionaries or coup plotters have the collective strength to forcibly remove the regime (e.g. Acemoglu & Robinson, 2006; Knutsen, 2014).

‘Transitions from within’ have not been the subject of many cross-national empirical studies, but thorough cross-national studies consider related phenomena. Aidt & Jensen (2014) find that revolutionary threats spur franchise extensions, but these typically represent one particular type of (liberalizing) transition from within. Work on ‘Gamed Democracy’ by Albertus & Menaldo (2018) is also related to incumbent-guided democratizing transitions. But these authors only indirectly consider the guided nature of transitions, empirically, by considering the continuation of autocratic constitutions after democratization. Djuve, Knutsen & Wig (2020), in their data article, present a brief application with one logit regression assessing the link between GDP growth and incumbent-guided liberalizing transitions (i.e., one of the three transition types that we study); they do not find any significant relationship. Another exception is Svolik (2015), who addresses the consolidation or breakdown of democracies, and estimates the risk of incumbent-guided democratic breakdowns – ‘incumbent takeovers’ – separately. When studying this subset of (autocratizing) incumbent-guided transitions, Svolik finds that slower GDP growth corresponds to increased risk of such transitions. These exceptions notwithstanding, there is little cross-national evidence on what factors drive incumbent-guided regime transitions, more generally, let alone evidence on the role of economic crises.

Several theoretical contributions have addressed dynamics of specific types of regime changes from within (e.g. Boix, 2003; Acemoglu & Robinson, 2006; Svolik, 2012), generating many intriguing hypotheses. While often discussed as an argument predicting that economic crisis spurs popular revolution (see Dorsch & Maarek, 2014), the core formal model of Acemoglu & Robinson (2006) implies that crisis spurs liberalizing transitions from within under certain conditions. Anticipating revolutionary action during crisis, incumbent elites can sometimes pre-empt revolution by initiating a guided liberalization that, in turn, diffuses the popular threat. Also case studies from different regions and historical time periods have elaborated on how economic crises engender liberalizing regime changes from within due to regime elites bowing down and reforming the regime when facing mobilized opposition (see, e.g. Morales & McMahon, 1996; Bratton & van de Walle, 1997; Berger & Spoerer, 2001). Our theoretical argument, presented in the next section, builds on, develops and generalizes these insights, specifying the conditions under which crises are more likely to spur different types of transitions from within.

How economic crises drive transitions from within

We define a political regime as the set of formal and informal rules that are essential for selecting leaders (see also Geddes, Wright & Frantz, 2014). A regime change is defined as a substantial change in these rules, and a ‘regime change from within’ is thus a substantial change in these rules that is, at least in part, guided by incumbent regime elites. Reasonable alternative terms are thus ‘incumbent-guided’ or ‘incumbent-led’ transitions – the primary defining feature is that these transitions are either instigated or negotiated by sitting regime leaders. Notably, this category of transitions is largely orthogonal to the conventional democracy–autocracy dimension. Transitions driven or negotiated by incumbents can lead to more or less democratic regimes or to regimes that are about equally democratic (but different in other vital respects). 1 Our argument consists of two proposed mechanisms, both suggesting that economic crises increase the probability of regime transition from within. We label them the window of opportunity and lesser evil mechanisms. Before detailing each one, let us highlight some commonalities:

Both mechanisms relate to how economic crises impact on the opportunities that incumbent elites have for changing the regime – either through altering the resources or support of the incumbent, or the resources or coordination abilities of opposition groups – or the preferences that incumbents have regarding deliberately altering the regime v. trying to maintain the status quo.

Another commonality is the notion that economic crises affect the behaviour of actors outside the incumbent regime elite. Notably, crises often induce or exacerbate grievances among potential coup-plotters, rebels, or the population at large due to individuals experiencing income loss, unemployment, or high inflation. Such increased grievances – especially if the regime is perceived as responsible for the crisis – might increase (elites’ perceptions of) risks of a forced regime breakdown. This could induce incumbent elites to steer the country through a guided regime transition to mitigate these grievances. However, aggrieved population groups could also direct their anger towards other groups whom they perceive as responsible for their distress. Clever incumbents could then take advantage of this situation to change the regime in a direction they prefer.

Finally, an economic crisis may alter the resources available to incumbents and to opposition actors, thereby altering the power balance between them. We surmise that this change often contributes to increasing the probability of a transition from within, but the more specific nature of this transition depends on, for example, the nature of the crisis and who is perceived as culpable for it.

Path 1: Economic crises as windows of opportunity

Under the first mechanism, which we label the window of opportunity mechanism, crises improve opportunities for incumbent elites to transform the regime into one that they inherently prefer over the status quo. The notion that crises may, for various reasons, momentarily weaken effective constraints on leaders and present them with opportunities to pursue desired changes (of various kinds) is widespread in political science. For instance, crises provide windows of opportunity for wholesale reforms of bureaucracies (Aberbach & Christensen, 2002) and controversial economic reforms (e.g. Keeler, 1993). Crises can strengthen public support for rapid and radical policy-change or other change to mitigate the crisis. This expands incumbents’ ‘mandate’ to govern.

Moreover, crises sometimes weaken institutional bodies that typically check the executive or alter or sever opposition alliances, effectively fragmenting resistance to incumbents. These developments, in turn, mitigate abilities to veto changes pursued by the leader. Furthermore, crises may create a chaotic and opaque environment where leaders can utilize information advantages to push for outcomes that she/he prefers without opposing actors being able to coordinate effective resistance. Leaders sometimes use these opportunities not only to pursue policy reforms, but also desired ‘reforms’ to the way the country is governed. One important example pertains to ‘states of emergency’, where decisionmaking power is concentrated with the executive for rapid and effective crisis responses. Recent cross-country work has documented that democracies more often experience autocratizing regime changes during such situations, partly because leaders take advantage of temporarily extended powers to engineer a regime change that leaves power concentrated in his/her hands more permanently (Lührmann & Rooney, 2020).

Economic crisis may also erode the support for existing institutions in key constituencies, thereby making it less controversial and risky for regime insiders to transform the regime to another system that they prefer. The incumbent not being viewed as culpable, and preferably even being able to divert blame for the crisis to some other (domestic or foreign) group, is seemingly an important scope condition for this mechanism. Sometimes, this perceived culpability of non-regime actors reflects real culpability, but not necessarily. Manipulative incumbents could scapegoat minority groups during crises and fan conspiracies about these groups undermining the economy and the regime, thus justifying institutional changes that enable repression of these minorities and power concentration with the incumbent. Hence, economic crises sometimes spur grievances and alter the preferences and power resources of different constituencies, thereby creating a window of opportunity that clever elites can exploit to change the regime in a direction they prefer.

Path 2: Economic crises triggering liberalization as lesser evil

The second, lesser evil mechanism suggests that crises induce elites to transform the regime to one they find less desirable than the status quo, but more desirable than the regime that could result from their inaction. This mechanism presupposes that economic crises mobilize and empower opposition actors who may threaten the regime through a popular uprising or coup. If so, a crisis creates incentives for sitting leaders to, for example, enter negotiations about regime change with the opposition to avoid forced regime transition. Crises can thus pressure incumbents into accepting regime change, notably guided liberalization, as the lesser of two evils. The incumbent does not inherently prefer the post-transition regime to the pre-transition one, but the transition is nonetheless accepted since the expected costs of resisting a transition are higher than the utility loss of acquiescing (Acemoglu & Robinson, 2000, 2006). Several factors can play into this calculation; notably, being thrown out of office through extra-constitutional means during revolutions or coups substantially increases risks of leaders experiencing death and other forms of punishment (Goemans, 2008). In such instances, leaders who anticipate that the status quo is untenable may want to mitigate the threat by embarking on a guided transition, judging this change to be a lesser evil than risking a forced transition.

In general, an economic crisis may buildup substantial pressure on the regime and the prospects of forced regime change, if nothing is done, increase. Under such conditions, the regime may opt to reform into what incumbents consider a less favourable regime type than the status quo. They do so simply because this outcome, arrived at via a guided regime transition, is preferable to (the perceived high-probability event of) forced regime change by outside actors.

Pressures for change created by an economic crisis can come from increased grievances in different opposition groups, but also from the signalling and coordination functions that crises can play in uniting fragmented opposition actors. Since crises are demarcated in time and of a public nature, they can serve as ‘focal points’ for regime opposition, enabling citizens to take to the streets knowing they will not protest alone (Kuran, 1989). Expectations of such dynamics could induce incumbent elites to reform the regime from within to avoid revolution. One caveat is that incumbent elites may pursue different tactics that stop short of regime change, including targeted co-optation or pre-emptive coups that re-shuffle the leadership (Dorsch & Maarek, 2018) to mitigate threats.

Finally, a crisis may siphon off the regime’s financial resources, and crises that sharply reduce tax revenues may make guided transitions more likely through the lesser evil mechanism. Such crises render regime elites less capable of diffusing threats by eating into funds used for repression or buying support from key groups through social policy spending (Ponticelli & Voth, 2011) or patronage (Bratton & van de Walle, 1997). Under such circumstances, incumbent regime elites may consider a guided transition to be the lesser evil.

Measures and data

Regime transitions from within

We apply the operationalization and data on regime change from Djuve, Knutsen & Wig (2020), which we refer to for detailed descriptions of coding rules and accompanying discussions of reliability and validity. These HRD come with extensive notes detailing all coding decisions and sources. HRD covers 201 polities and are integrated in the V-Dem dataset (v.9; Coppedge et al., 2019). HRD comprises information on more than 2000 regimes from 1789–2018, with specified dates for beginnings and ends of regimes in most cases. Notably, the HRD threshold for coding regime change is generally lower than in related datasets such as Geddes, Wright & Frantz (2014). For instance, HRD captures several short-lived regimes, gradual transition processes between types of autocracies (e.g. dominant party-regimes turning into personalized autocracies) and major expansions of suffrage in otherwise democratic regimes (e.g. from male to universal suffrage). HRD also records type of regime breakdown in a 14-category scheme (Online appendix A), covering, for example, military coups, civil war, foreign intervention, popular uprisings and three categories of regime transition from within.

These three categories are self-coups, other non-liberalizing incumbent-guided transitions and liberalizing incumbent-guided transitions.

2

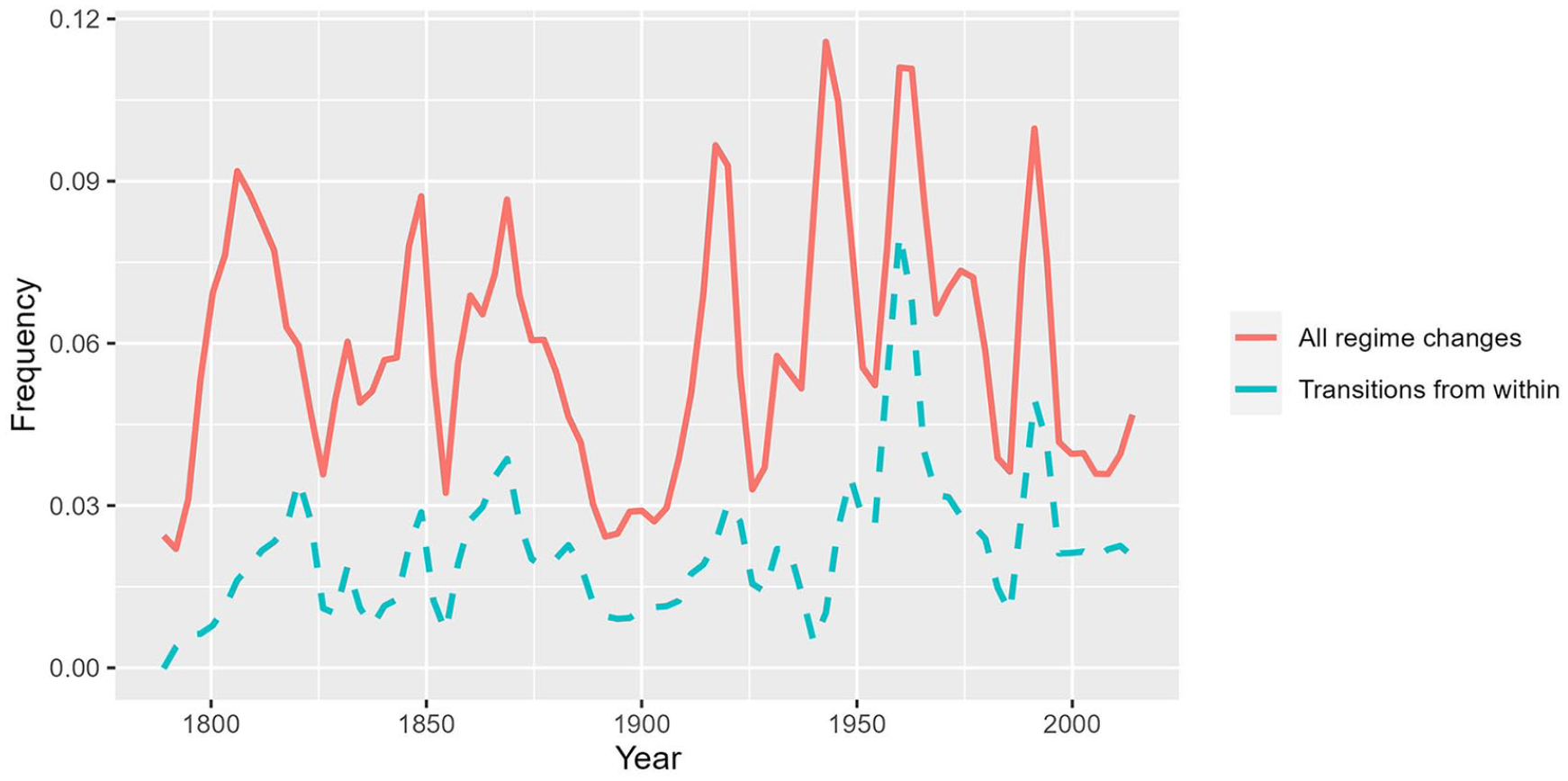

Liberalizing guided transitions are regime changes where the incumbent elite Shares of countries globally that experienced at least one regime breakdown and at least one regime transition from within, by year (Loess smoother, with span of 0.075)

The other two categories – incumbent-guided transitions (unaccompanied by political liberalization) and self-coups by sitting leaders – are sometimes hard to distinguish in practice (Djuve, Knutsen & Wig, 2020). 3 We can think of this distinction as a continuum ranging from very clear self-coups (e.g. Fujimori’s in Peru 1992), via difficult intermediate cases where there may be some additional concentration of power in the leader’s hands, to guided transitions where the new regime is not or only slightly more autocratic/democratic than the previous one (e.g. end of the Fourth Republic in France 1959). Regarding the intermediate cases, these are often characterized by some legislative action to transform the rules of the political game, for example, introducing a new legislative framework for appointing the head of state. Such changes may have (some) effects on the concentration of power with the leadership and induce a somewhat more autocratic outcome, but still stop short of a full-fledged self-coup.

The three transition categories are grouped together when coding our main dummy on ‘transitions from within.’ Guided liberalizations make up 251/2021 regime breakdowns recorded in HRD (12.4%), whereas self-coups account for 104/2021 (5.1%) and ‘other transitions from within’ for 366/2021 (18.1%). Transitions from within thus make up more than a third of all regime changes. 75% of all countries have two or more such transitions recorded (Online appendix Table B.1).

Figure 1 presents time-series lines on the proportions of countries, globally, that experienced at least one regime breakdown (of any kind) and at least one transition from within, per year. The latter have made up a substantial share of all regime changes, globally, through most of modern history, yet Online appendix Figure B.2 details the substantial regional variation. For instance, such transitions accounted for the majority of regime changes in Western Europe and North America during much of the late 19th and early 20th centuries, including episodes where incumbent elites expanded the franchise (Boix, 2003) or introduced parliamentarism and circumscribed the monarch’s powers (Congleton, 2011), but have been far less common in these countries in later decades.

Economic crises

Economic crises can have very different features and underlying causes. There are financial crises, exchange rate-induced crises and property market crashes. Yet, one typical feature is negative rates of GDP per capita growth. In fact, the most common operationalization for a ‘recession’ is negative GDP per capita growth for at least two consecutive quarters. Still, GDP per capita growth is a continuous variable, and setting a threshold for what we should call an economic crisis is inevitably an arbitrary decision. One benefit of using a continuous growth measure is that it increases relevant variation by distinguishing minor crises from major ones. With a continuous measure, we can let the latter crises weigh more heavily in the estimation. Our benchmark measure is therefore continuous GDP per capita growth in a year. 4 Yet, as discussed by Krishnarajan (2019a), this approach also has its shortcomings. We thus test multiple alternative measures, including dummy operationalizations requiring different thresholds for depth and longevity for an economic contraction to be registered as a crisis.

Gross domestic product data are from Fariss et al. (2017), who estimate (logged) income level by using a dynamic latent trait model and drawing on information from different GDP datasets. We use their estimates benchmarked in the Maddison series (Bolt & van Zanden, 2013). Fariss et al.’s latent model estimation mitigates various kinds of measurement error. It also mitigates missing values by imputation, allowing us to extend our time series back to 1789. Yet, we conduct robustness tests by using the original Maddison series, which we then interpolate by assuming constant growth rates across intervals with missing data.

The extensive GDP data allow us to capture numerous economic crises. Other indicators, such as unemployment rates, only have cross-country data extending a few decades back. However, one alternative measure with extensive coverage is inflation from Clio-Infra (de Zwart, 2015). We construct different dummies of crises that capture episodes of high inflation. Yet, since there are information benefits to distinguishing crises by their depth, we once again mainly rely on a continuous measure.

Benchmark specification

Our benchmark is a logit regression with country-year as unit and errors clustered by country to account for panel-specific autocorrelation. We have weak theoretical priors on the exact structure of the autocorrelation process, and clustering allows adjusting standard errors for any within-country pattern of correlation not captured by the additional covariates. Such patterns could, for example, be generated by past histories of regime (in)stability influencing transition likelihood several years later. Clustering might, however, generate biased standard errors, especially when there are few clusters (Esarey & Menger, 2019), and we therefore test different error adjustments in Online appendix Table B.15. We employ the unconditional logit estimator. This estimator has several practical advantages over conditional fixed-effects logit, and concerns about bias are mitigated given our long time series (Katz, 2001). We include a cubic polynomial of regime duration, following Carter & Signorino (2010), to account for differential survival rates throughout regimes’ life-span (Svolik, 2012). We use continuous annual GDP per capita growth as our main independent variable and a dummy capturing (at least one) ‘regime change from within’ as dependent variable.

Our benchmark includes as controls covariates that may influence probability of experiencing economic crisis and regime change from within, including income level (ln GDP per capita from Fariss et al., 2017) and ln population (same source). We log GDP per capita for statistical – the logged version is far less right-skewed – and theoretical reasons. Economic growth theory indicates that (steady-state) GDP per capita growth is a linear function of ln GDP per capita. We also expect a concave relationship between GDP per capita and our outcome. (A 1000 USD difference in GDP per capita presumably induces larger differences in socio-economic structures and conditions for grievances in initially poorer economies). Further, we control for degree of democracy by including Polyarchy (Teorell et al., 2019) from V-Dem, and its squared term, thereby modelling the previously identified inverted U-curve relationship between democracy level and regime breakdown (Gates et al., 2006; Goldstone et al., 2010). All covariates are measured one year before the outcome. This is no surefire way to ensure exogeneity of the covariates; for example, the outcome in t − x could influence covariates in t − 1 and the outcome in t. We still prefer this specification choice, especially since the autocorrelation for both our main independent-variable and outcome variable, are relatively low (r = 0.02 and r = 0.03, respectively, for observations measured in t and t−1). Also, insofar as the covariates affect the outcome, we would, theoretically, anticipate a time lag. It takes time from when a crisis hits to when grievances and subsequent anti-regime mobilization reach their peaks, and additional time before incumbents respond with proposed changes to the regime. However, since we have no clear theoretical justification for the exact lag-length, we assess different specifications in Online appendix Tables B.5 and B.6.

We further include either geographical region dummies (using V-Dem’s six-fold classification of world regions) or country-fixed-effects. These controls should capture stable, unit-specific characteristics that simultaneously affect breakdown and correlate with economic crisis. Since these unobserved factors presumably vary also between countries within the major regions, including country-fixed-effects helps mitigate confounding. Yet, including country-fixed -effects could introduce other issues, notably reduced efficiency, especially for binary outcomes with limited temporal variation (Beck & Katz, 2001). It could also bias results in instances where there are omitted confounders that trend over time, and such biases may even increase with the length of time series (Plümper & Troeger, 2019). Hence, we also assess specifications with region-fixed-effects instead. Furthermore, we include year dummies to account for any (non-linear) time trends and global shocks due to time-varying omitted confounders.

Our benchmark is intentionally sparse since several potentially relevant covariates could not only affect but also be driven by an economic crisis. Indeed, several guided regime transition processes that span multiple years may be inherently linked to change on the Polyarchy scale in year t−1, even if the transition is registered in t. Hence, even our sparse benchmark might over-control for relevant channels through which crises influence our outcome. We therefore also report models only controlling for the duration terms, year-fixed-effects, and region/country dummies. In yet other specifications, we prioritize mitigating omitted variable bias and add extra controls. Still, given possible omitted confounders and reverse causality, the controlled correlation patterns that we present in the next section should not be interpreted as stringent evidence for a causal effect. 5 With these caveats in mind, we present our results.

Empirical analysis

Main analysis

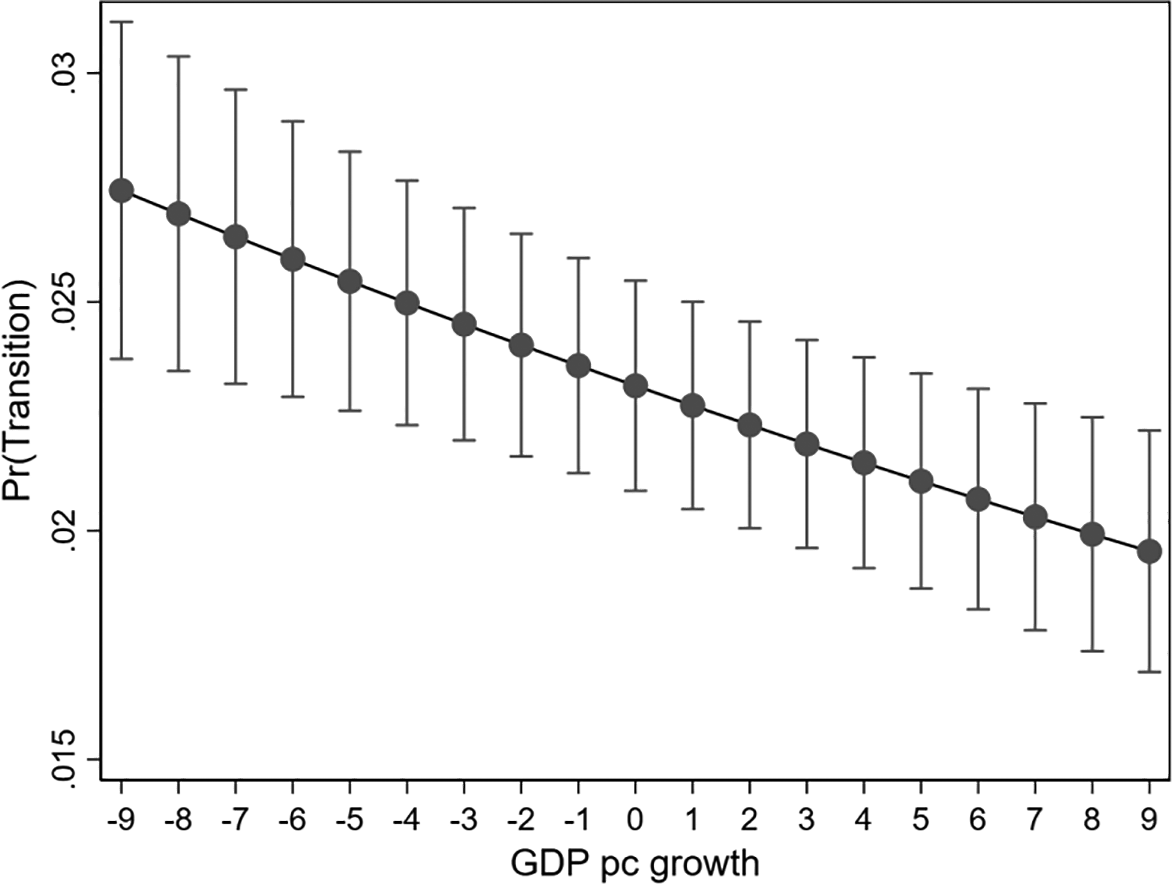

Model 1.1, Table I is the most parsimonious version of our benchmark controlling only for cubic duration terms, year-fixed-effects and world region dummies. This specification draws on 18,243 country-year observations from 164 countries and the longest time-series is 1789–2014. Model 1.2 adds the (one-year lagged) time-variant controls, namely ln GDP per capita, ln population and Polyarchy (linear and squared). Model 1.3 is similar to 1.2, but substitutes the region-fixed-effects with country-fixed-effects. In these models, we use GDP and population data from Fariss et al. (2017).

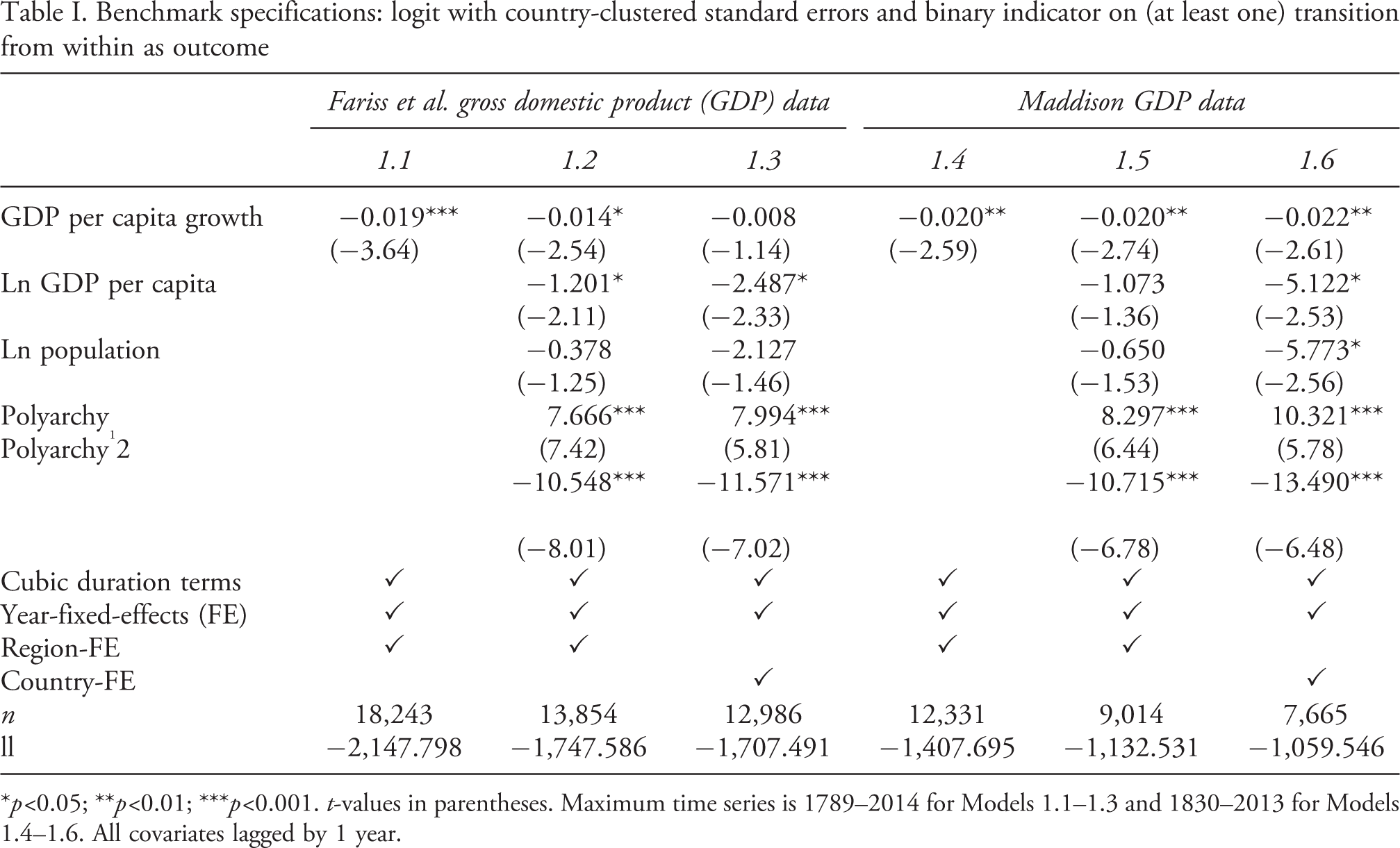

Results from these initial tests follow our expectations; GDP per capita growth is negatively correlated with probability of regime transition from within in t+1. Figure 2 shows the predicted probabilities, with 95% confidence intervals, for growth rates in between −9 and +9%. A change in GDP capita growth from +5 to −5 – with all other covariates at their respective means – corresponds to an increase from 2.1 to 2.5% in the probability of observing a transition from within. A change from +10 to −10, increases the predicted probability from 1.9 to 2.8%. Hence, economic crisis is not a panacea for explaining regime change, as even this substantial drop in growth increases the probability of transition from within by about 45%, and the annualized risk remains low. Metrics of explanatory power of the model is also relatively low. Yet, these features, in part, reflect that regime changes are rare events that are inherently hard to explain with a high degree of temporal accuracy. Moreover, our country-year set-up does not reflect that some crises last for multiple years, and incumbent-guided transitions are sometimes drawn-out processes. Hence, we may underestimate the substantive impact (and explanatory power) of a major crisis.

To further illustrate the substantive relevance of our findings, we compare them with results from similar models that employ regime deaths due to coups or revolutions (also from HRD) as the outcome (see Online appendix Table B.14). The coefficient on crisis is equal to (using Maddison data) or smaller than (Fariss et al. (2017) data) the one for incumbent-led transitions for these externally induced regime changes. This reinforces the point that the modest size of the estimated effect in our benchmark relates to the inherent challenges in predicting rare (but important) events such as regime change.

Benchmark specifications: logit with country-clustered standard errors and binary indicator on (at least one) transition from within as outcome

∗p<0.05; ∗∗p<0.01; ∗∗∗p<0.001. t-values in parentheses. Maximum time series is 1789–2014 for Models 1.1–1.3 and 1830–2013 for Models 1.4–1.6. All covariates lagged by 1 year.

Predicted probabilities of transition for −9% to +9% gross domestic product per capita growth rate

The three rightmost columns in Table I are similar but draw on GDP and population data from Maddison (Bolt & van Zanden, 2013). This change reduces the no. of observations from 18,243 country-years in Model 1.1 to 12,331 in Model 1.4. However, the Fariss et al. time series are imputed, and predictions are presumably poorer for observations without scores on any extant GDP series, the most extensive one being Maddison. Hence, many error-prone observations are likely dropped when using Maddison data. This may be why Coefficients and 95% confidence intervals for gross domestic product per capita growth, from models resembling Model 1.2, Table I, but with growth measured from t−10 to t+1

Robustness tests

We conducted several extra tests to assess robustness. First, we assess the sensitivity of results to different operationalizations of economic crisis. Next, we run linear probability models (LPM) instead of logit. Finally, we try out different sets of controls and standard error adjustments.

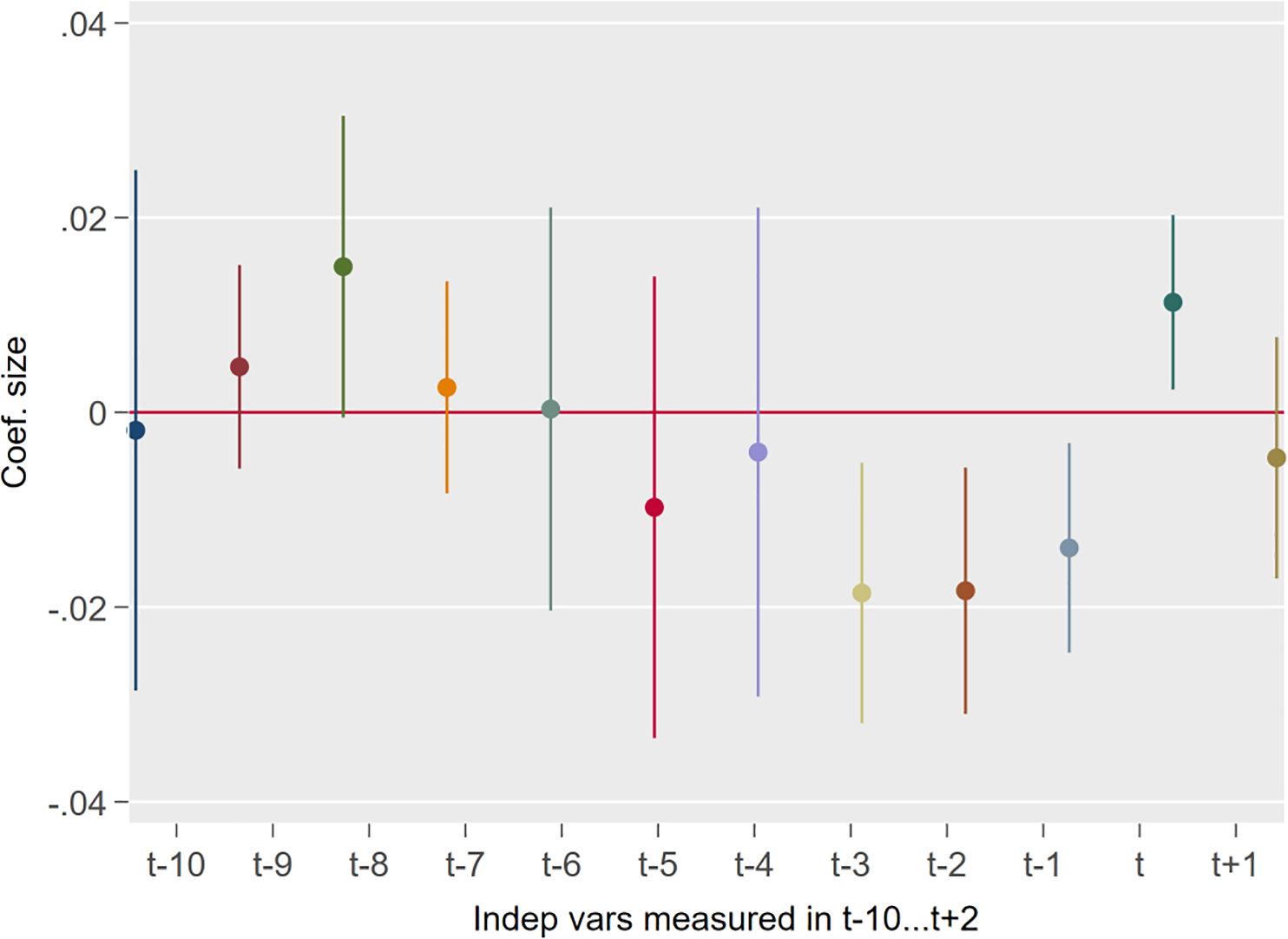

We start by using the continuous GDP per capita growth measure – replicating Model 1.2, Table I – but trying out different lag structures on the independent variables, from t−10 to t+1. Figure 3 maps the resulting growth coefficients and 95% confidence intervals.

We note three patterns: First, GDP per capita growth in t−2 and t−3 are similarly signed and significantly related to the outcome. Second, growth measured concurrently with regime change is positive and significant, which may reflect that crises are likely to produce regime change from within and higher post-crises ‘rebound-growth.’ Third, we did not theoretically expect growth measured relatively far back in history to have any clear relationship with regime outcomes in t. Indeed, growth is insignificant for all lags between t−4 and t−10. Hence, this analysis on different lags and leads arguably provides additional support for our argument. In Online appendix Tables B.5 and B.6, we also show specifications including multiple lags for the covariates; growth in t−1 is not robust to adding contemporaneous covariates, but the direction and size of the coefficient is stable even in this specification.

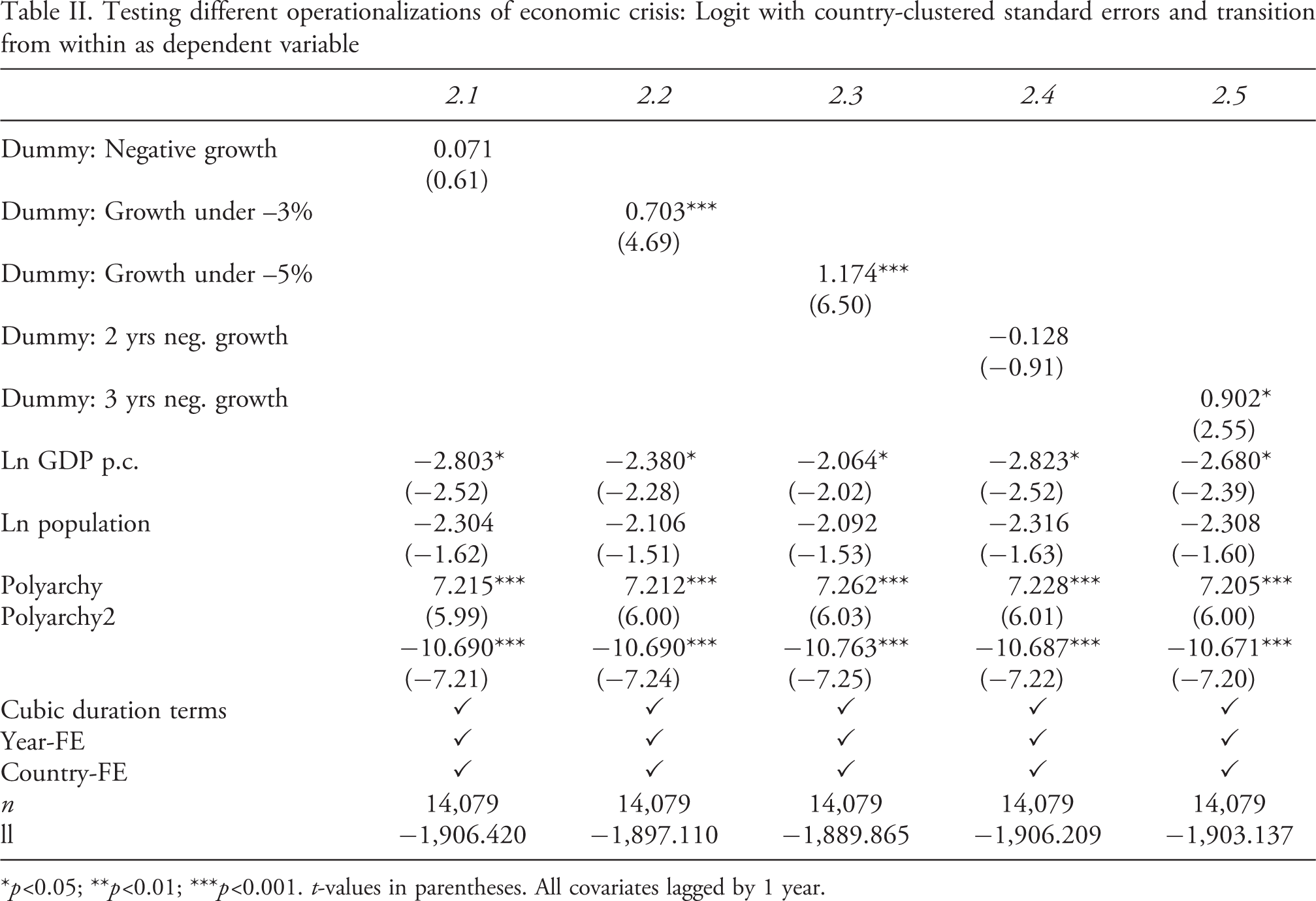

Testing different operationalizations of economic crisis: Logit with country-clustered standard errors and transition from within as dependent variable

∗p<0.05; ∗∗p<0.01; ∗∗∗p<0.001. t-values in parentheses. All covariates lagged by 1 year.

The picture is similar if we consider inflation instead of GDP per capita growth. These tests (Online appendix Table B.3) show that our continuous (log-transformed) measure is systematically correlated with transitions from within in t+1. However, dummy variables coding very-high inflation episodes as crises are sensitive to the particular threshold used. A 100% threshold gives clearer results than a 50% threshold, for example. Moreover, the high-inflation episode dummies are only significant in models including country-fixed-effects.

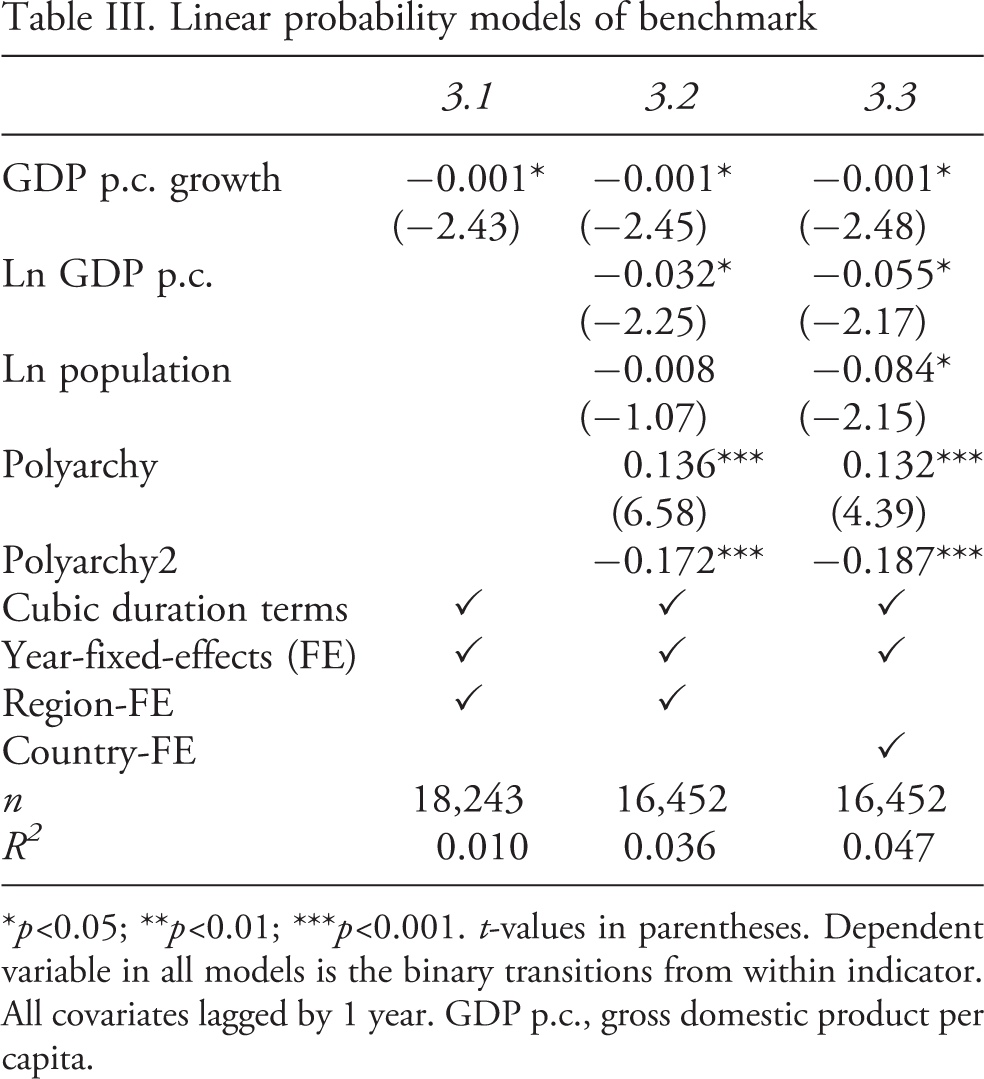

Next, we substituted our logit estimator with ordinary least squares, running ‘LPM’. Table III reports LPM-versions of our benchmark specifications. The growth coefficient is always negative and significant at 5%, and point estimates suggest that a 10-point decrease in GDP per capita growth rate increases the chance of observing regime transition from within in t+1 by about 1 percentage point. This is a non-negligible effect, given that 2.3% of country-years in our sample observed such transitions. LPM specifications also give very similar results to the logit models when testing the various crises dummies discussed above (Online appendix Table B.4).

Linear probability models of benchmark

∗p<0.05; ∗∗p<0.01; ∗∗∗p<0.001. t-values in parentheses. Dependent variable in all models is the binary transitions from within indicator. All covariates lagged by 1 year. GDP p.c., gross domestic product per capita.

Further, civil war or other sources of political instability might simultaneously make crises and regime transitions from within more likely. Yet, results are robust in models using Maddison data and country-fixed-effects when controlling for ongoing civil war or civil war initiation, using data from COW (Dixon & Sarkees, 2015) or political violence from V-Dem (Online appendix Table B.10). In models using Fariss et al. (2017) data and regional dummies, the crisis coefficient turns insignificant. But further analysis shows that this is due to reduced samples (Online appendix Table B.8). We also account for past history of economic crises and regime instability by controlling for no. of crises and regime changes (Online appendix Tables B.8 and B.10). Our benchmark results are also robust to accounting for (the competing risk of) externally driven regime changes more often happening during crises. We ran specifications omitting all observations with regime changes due to coups and revolutions (rather than coding them as zero) or all other regime changes or adding dummy variables for, respectively, regime changes due to coups and revolutions and all regime changes that were not incumbent-guided to the benchmark (Online appendix Table B.12).

Finally, we tried out different permutations of the benchmark where we omit subsets of covariates (see Neumayer & Plümper, 2017), and tested other error correction specifications than clustering by country (Online appendix Table B.15). Results are robust in all specifications except when not including any kind of geographical dummies. This pooled model, however, is likely to give biased results, since it does not account for differences in base-rates across observations (Green, Kim & Yoon, 2001). When employing classical errors or non-clustered sandwich-estimated errors, t-values increase substantially relative to our benchmark, and the crisis coefficient is highly significant even in specifications omitting the geographical dummies.

Disaggregating regime change from within

Up to this point in our analysis, we have employed an aggregated measure that coded different kinds of regime changes driven by incumbent regime elites as ‘transitions from within.’ Yet, this aggregate category captures quite different processes of regime change. Although our theoretical argument suggests that crises should enhance all transitions from within, this is, ultimately, an empirical question. We therefore turn to specifications run on two more finer-grained dependent variables.

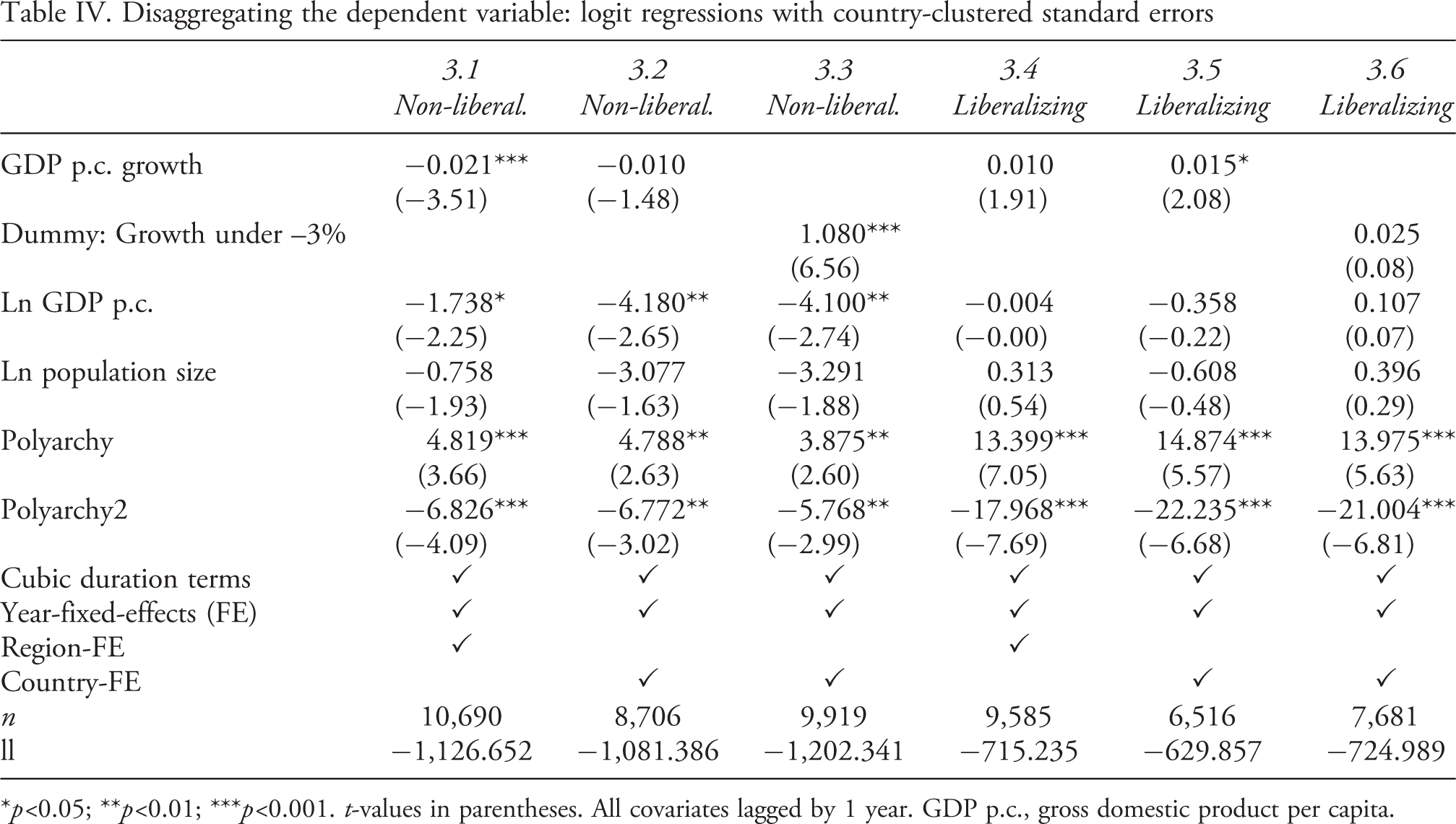

Table IV reports these tests, with a dummy capturing self-coups and other guided transitions as outcome in the three leftmost columns, and guided transitions leading to liberalization in the three rightmost columns. While not entirely robust (see Model 3.2), various regressions show a strong relationship between crisis and non-liberalizing transitions from within. This observation is consistent, for example, with our theoretical mechanism highlighting that opportunistic incumbent elites may use crises as windows of opportunity to conduct self-coups or engage in other types of regime transitions (e.g. from a military regime to a personalist regime) that they consider beneficial.

Disaggregating the dependent variable: logit regressions with country-clustered standard errors

∗p<0.05; ∗∗p<0.01; ∗∗∗p<0.001. t-values in parentheses. All covariates lagged by 1 year. GDP p.c., gross domestic product per capita.

One possible reason for the lack of evidence for the lesser evil mechanism is that incumbents can respond effectively to pressures from crises by using other strategies. If liberalizing the regime is a very undesirable outcome for incumbents, they may be willing to pursue rather expensive policies to co-opt or appease opposition. Examples include investments in various local or national public goods, but targeted social policy programmes are also often introduced or expanded to co-opt specific groups in non-democratic regimes (Knutsen & Rasmussen, 2018). Thus, one potential explanation for the lack of an observed correlation between economic crises and incumbent-guided liberalizing transitions is that incumbent elites might fend off the threats spurred by a crisis by instead pursuing particular redistributive policies.

Conclusion

We have argued that economic crises can provide impetuses for incumbent elites to change the existing regime through two different mechanisms. First, economic crises sometimes create conditions that give elites a window of opportunity to alter the regime towards one that they inherently prefer over the status quo. Second, crises sometimes spur mobilization among dangerous opposition actors, leading strategic incumbent elites to preemptively transform the regime to diffuse opposition threats and avoid even worse outcomes such as a revolution. Still, our main contribution is empirical. We test implications from our argument by using new data on more than 700 regime transitions from within from 201 countries across the period 1789–2018. While results are not entirely robust, we mainly find support for the expected relationship between (various measures of) economic crises and regime transitions from within. When subsequently disaggregating these transitions, we find that economic crises relate to elite-guided regime transitions that do not result in political liberalization, but also, more surprisingly, that crises do not relate to liberalizing, guided regime transitions.

Our study and findings point to different avenues for future research. First, the unexpected lack of a clear relationship between crises and incumbent-guided liberalization episodes means that one key hypothesis from the theoretical democratization literature (notably Acemoglu & Robinson, 2006) lacks empirical support. Granted, Acemoglu & Robinson (2006) predict that the effect of an economic crisis on elite-guided democratization may depend on factors such as income inequality. While recent work finds such more complex interaction patterns for democracy levels and democratization episodes, more generally (Kotschy & Sunde, 2019; Dorsch & Maarek, 2020), future work could thus investigate potential interaction effects between crises and more structural economic factors in inducing this particular type of regime change. Alternatively, we noted how targeted, redistributive policies can sometimes be a sufficient response to an economic crisis, diffusing various pressures against the regime (and thus allow elites to avoid guided liberalization). Choices, and potential trade-offs, between co-optation through redistributive policies vs. institutional change are intriguing topics for future study.

While guided democratic transitions have attracted more attention by scholars historically (e.g. O’Donnell, Schmitter & Whitehead, 1986), democracy researchers have recently started to focus more on ‘self-coups.’ As highlighted by Svolik (2015), self-coups constitute an increasingly common mode of democratic breakdown, and have recently outpaced military coups as a threat to democratic survival. Recent analyses describe how elected leaders, often in an incremental manner, concentrate power in their own hands and dismantle institutional checks on their power until, one day, the regime is no longer democratic (Levitsky & Ziblatt, 2018; Lührmann & Lindberg, 2019; Przeworski, 2019; Svolik, 2019). Despite the recent focus on describing the various steps of self-coups as well as analysis into how autonomous and resourceful parliaments can guard against such regime change (e.g. Fish, 2006), the determinants of successful self-coups remain understudied. Going beyond the role of economic crisis and elaborating on why some democracies experience self-coups and others do not, is thus an important topic for future research.

Footnotes

Replication data

Acknowledgements

We thank Svend-Erik Skaaning, participants at the Danish Political Science Association Annual Meeting in Vejle (2019) and American Political Science Association Annual Meeting in Washington, DC (2019), the editors, and three anonymous reviewers for their valuable comments.

Funding

The authors received the following financial support for the research, authorship, and/or publication of this article: This project has received funding from the European Research Council under the European Union’s Horizon 2020 research and innovation programme (grant agreement No 863486) and a Research Council Norway Grant, pnr 240505.