Abstract

Consumers often take on debt at different points in time. As a result, debts may be months, if not years, apart in age. In this research, the authors ask whether and how debt age affects installment debt prepayment decisions. While the ideal strategy for prepaying older versus newer debt depends on specific account parameters (e.g., interest rate, monthly payment), in many circumstances it is financially advantageous to prioritize paying down newer debt. This is because debt amortization (i.e., repayment) schedules often result in reduced interest payments when newer installment debts are paid first. However, across eight studies, including a secondary dataset of consumer loans, the authors find that consumers prefer to prepay older debt first—even when it is financially disadvantageous to do so. The authors refer to this as a FIFO (first-in, first-out) preference and demonstrate that consumers prioritize older versus newer debt prepayment because they feel they have invested greater effort (i.e., mental or physical work and energy) to repay it. Accordingly, reducing the effort required to repay an older debt (e.g., through automated payments) or shifting consumers’ focus from invested effort to remaining effort attenuates the FIFO preference. These findings offer implications for theory, managerial practice, and consumer welfare.

Total household debt in the United States rose to a record high of $18.20 trillion in the first quarter of 2025 (Federal Reserve Bank of New York 2025). This record-breaking figure includes mortgage balances exceeding $12 trillion, auto loan and student loan balances totaling $1.6 trillion each, and credit card balances exceeding $1 trillion. Given such mounting debts, it comes as little surprise that paying down debt is a common goal held by consumers, with many consumers striving not only to reduce their debt but also to become debt-free. Considering such ambitions, how should consumers strategize debt prepayment, or the early repayment of debt, across multiple debt accounts?

To understand possible debt prepayment strategies, it is important to recognize that while individual debts may have different repayment parameters (i.e., repayment periods, interest rates, and/or origination amounts), consumer debt can be characterized into two groups: installment debt and revolving debt. With installment debts, such as auto loans, student loans, and personal loans, a fixed amount is borrowed and then repaid in equal installments across a predefined period according to an amortization (repayment) schedule. The amortization schedule accounts for both principal reduction and the compounded effect of interest over time. As the debt is repaid, the principal balance decreases until the debt is repaid in full and the account is closed.

One notable difference between installment and revolving debt is that installment debts have clear repayment schedules accompanied by an origination date and a maturity date. In contrast, revolving debts, such as credit cards, have no predefined maturity date as consumers may hold the accounts in perpetuity, even without maintaining an account balance. Thus, consumers may be more likely to think about installment debts in terms of debt age, or the time that has passed since the origination date. 1

In this research, we consider the effect of debt age on installment debt prepayment, or the early repayment of debt. Understanding how debt age affects installment debt prepayment is critical because consumers rarely take out multiple installment debts at the same time. Instead, many consumers take out different installment debts at varying points in time throughout their lives. For instance, consider a consumer who takes out a mortgage to purchase a home one year, and a personal loan to complete a home renovation several years later.

It follows, then, that consumers may hold multiple debts that vary in age at the same time. This is further evidenced by the 66% homeownership rate in the United States (fixed-rate mortgages accompany most home loans), combined with the $3.89 trillion in other installment debt (i.e., student loans, auto loans, personal loans) held by U.S. consumers (Federal Reserve Bank of New York 2025). Additionally, according to the 2022 Federal Reserve Survey of Consumer Finances (Board of Governors of the Federal Reserve System 2023), 28.7% of respondents had two or more outstanding installment loans (compared with 27.3% of respondents who had two or more credit cards with outstanding balances). Importantly, these data points capture only part of consumers’ debts, as neither captures medical debt, “buy now, pay later” (BNPL) loans, or other repayment arrangements consumers may have (e.g., loans from family and/or friends). Thus, the percentage of U.S. consumers with multiple installment loans is likely even greater.

To facilitate paying off their debt accounts, consumers may accelerate their payments by making principal-only prepayments, which is recommended by financial experts (Fidelity 2024) and embraced by many consumers. For instance, in 2023, approximately 30% of borrowers made prepayments on their student loans (Federal Reserve Bank of Philadelphia 2024). In this research, we focus on how consumers strategize to prepay their multiple debts, which is important to understand given the millions of consumers who have more than one installment account that they desire to repay as quickly as possible.

While in many cases it is financially advantageous to prepay newer loans sooner, because interest is determined based on each account's principal balance and the principal balance is greatest earlier in the life of installment debt accounts, we demonstrate that consumers prioritize prepaying older loans. We refer to this prioritization as a first-in, first-out, or FIFO, preference. This terminology captures consumers’ preference to pay loans that they secured earlier relative to those that were added later to their portfolio. We also delineate the process underlying this preference. We propose that the FIFO preference emerges because consumers feel that they have invested greater effort, through their own mental or physical work and energy, in repaying an older versus newer debt. Finally, we examine theoretically relevant as well as practical interventions that can be used to help consumers make more optimal prepayment decisions.

This research makes three main contributions to theory and/or practice that offer important implications for financial managers and consumer welfare. First, we add to existing knowledge about the factors that influence debt repayment. Whereas past research has provided many useful insights into how consumers strategize to repay multiple revolving debts, less academic work has examined the factors that influence how consumers decide to repay multiple installment debts. The present research helps to fill this gap and introduces a factor (debt age) that influences how consumers decide to prepay their installment debt accounts. Second, we contribute to literature on the sunk cost effect, which has repeatedly shown that individuals prioritize options for which they have already invested resources. In the context of debt repayment, we find that invested effort, which we define as the cumulative mental or physical work and energy expended in repaying a debt, is an especially important driver of the FIFO preference for prepayments. We provide evidence through both mediation and moderation that heightened invested effort associated with older debt underlies consumers’ preference to prepay older debt first. Our investigation further highlights the importance of invested effort versus invested money, as we show that even when the monetary amount repaid on the newer debt is greater than that for the older debt, consumers still prefer to prepay the older debt. Third, we contribute to literature on just-in-time interventions that consumers and financial professionals (e.g., advisors) can implement to aid consumers as they make financial decisions.

Theoretical Background

Prior research highlights the impact of lender communications (such as credit card statements) on consumers’ debt repayments. Much of this research considers repayment decisions for a single debt account (e.g., Agarwal et al. 2015; Hershfield and Roese 2015; Stewart 2009), while other studies explore how consumers prioritize repayments among multiple debt accounts (see Table 1). Collectively, these research streams primarily focus on revolving debt accounts (e.g., credit cards), which do not have a predefined repayment term or amount, and document how various factors influence revolving debt repayment decisions. Revolving debts typically have two important components: interest rate and account balance. Researchers have broadly identified two strategies that consumers use to repay revolving debt—one that focuses on interest rates, and one that focuses on account balances. With an interest rate strategy, also known as the debt avalanche method (e.g., Hirshman and Sussman 2022), consumers focus on repaying accounts with the highest interest rates first. Repaying accounts with the highest interest rates first is arguably the financially optimal approach to pursue because it reduces the total interest that consumers pay.

Previous Debt Repayment Research.

Despite the financial advantage of paying down revolving accounts with the highest interest rates first, many consumers instead adopt a lowest account balance strategy, known as the debt snowball method (Amar et al. 2011; Besharat, Carrillat, and Ladik 2014; Gal and McShane 2012; Kettle et al. 2016). With this method, consumers prioritize accounts with the smallest balances first, which helps them feel that they are making greater progress on their debt repayment and sustains their motivation to tackle higher balance accounts thereafter. Consumers may also use other account balance–based repayment strategies, such as allocating more money to accounts with higher outstanding balances (Gathergood et al. 2019; Ponce, Seira, and Zamarripa 2017), allocating evenly across accounts (Hirshman and Sussman 2022), or prioritizing debts with round-number balances (Isaac, Wang, and Schindler 2021). Lastly, consumers may be sensitive to factors unrelated to the interest rate or the account balance, such as whether they can “repay by purchase” (Donnelly et al. 2023) or identify debts that were incurred for hedonic (vs. utilitarian) expenses (Besharat, Varki, and Craig 2015).

Much less is known, however, about repayment decisions across multiple installment debt accounts. A key defining feature of installment debt is that in addition to having fixed lump-sum borrowed amounts, interest rates, and repayment installments, it has predefined repayment term lengths with an origination date and a maturity date, which adds a new factor to the decision mix: the age of the account. Our focus is on multiple installment debts, and we posit that consumers use the age of each debt account as a factor in their installment debt prepayment decisions. 2 Next, we discuss key facets of installment debt accounts and explicate our theory.

Installment Debt Accounts, Age, and Prepayment

Installment debt accounts are traditionally associated with loans procured primarily from banks (e.g., auto loans). However, installment debt is becoming more common in other sectors. For example, in the consumer marketplace, retailers frequently use BNPL programs, where consumers purchase a product now but pay a fixed installment over a prearranged period of time (Consumer Financial Protection Bureau 2021). Retailers are increasingly offering these programs for expensive products, such as appliances and furniture, as well as everyday lower-priced products, such as apparel and groceries; even credit card companies now allow consumers to convert credit card debt into fixed repayment loans (Chase 2023). In other contexts, such as with hospital bills or life insurance plans, consumers can choose to pay a fixed amount in installments over a predetermined time period.

Installment debt is typically amortized, meaning the total interest cost associated with the debt is calculated based on the loan amount, interest rate, and term length of the debt. The required installment (payment) is structured so that each payment is the same amount throughout the life of the loan. As payments are made, a portion of each payment is applied to accumulated interest (based on the outstanding balance of the account), and the remaining portion is applied to the outstanding principal balance, reducing the outstanding principal over time until it is eliminated with the last payment in the amortization schedule. For monthly payments earlier in the life of the loan, a larger proportion of each payment is applied to the required interest charges while a smaller proportion is applied to principal. As the principal balance decreases with each successive payment, a lower proportion of each payment is applied to interest, and a higher proportion is applied to the remaining principal balance.

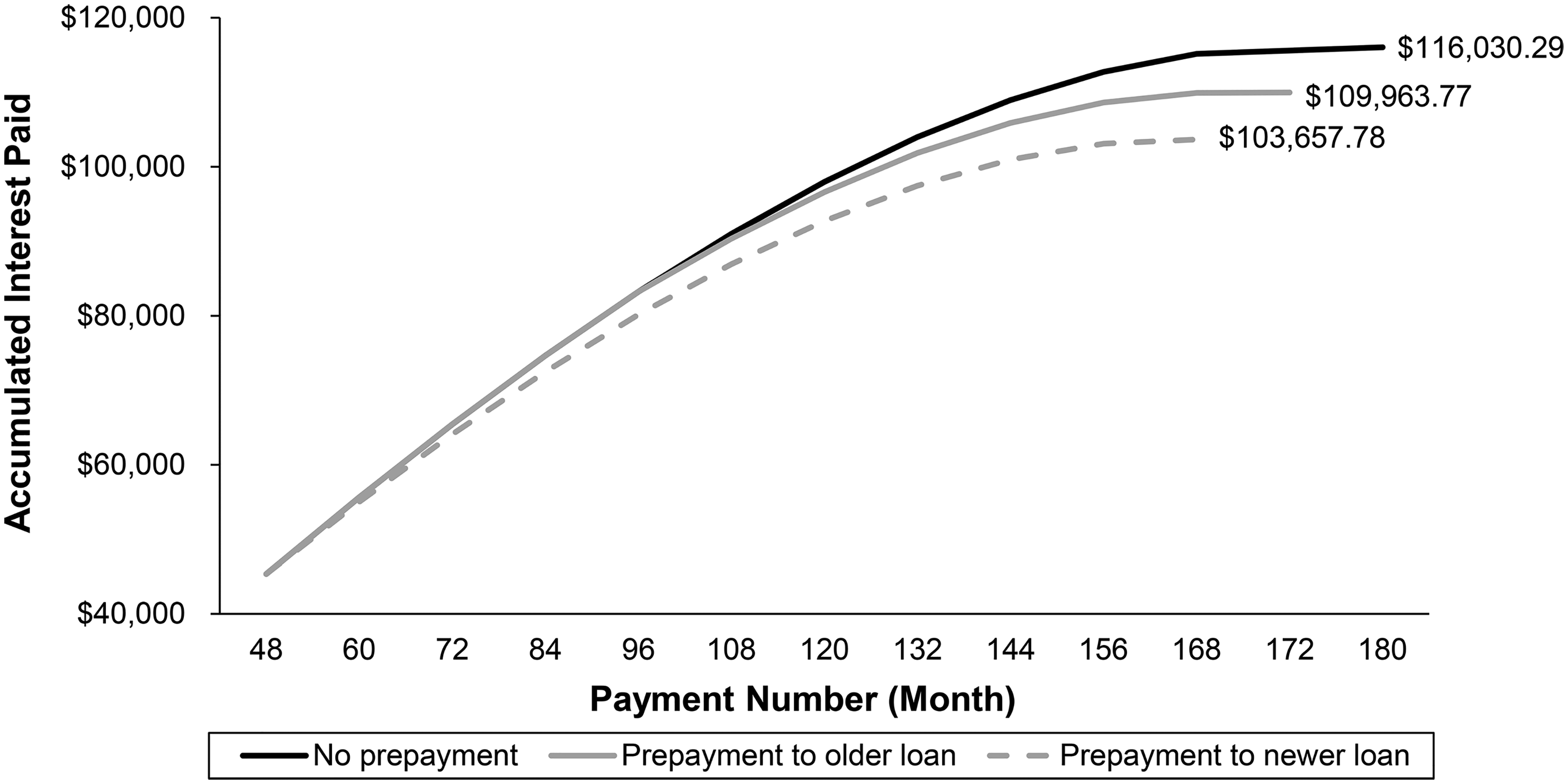

Amortization has an interesting effect on what happens when a consumer with multiple installment debt accounts makes a prepayment (i.e., an “extra” payment that is incremental to the planned payment schedule) to one of their accounts. To demonstrate the impact of a prepayment (also known as principal curtailment), consider a consumer who has two identical loans for $100,000 each, with 15-year terms and a 12% interest rate. One loan was taken four years ago, and the other loan was taken eight years ago. How would applying a $5,000 prepayment to the newer loan affect the amount of interest as well as the time saved in the repayment term?

Because of amortization, a loan prepayment that is made earlier in the term of a loan will have a greater effect on the amount of interest paid, as well as the lifetime of the loan (assuming no prepayment penalties). The sooner a prepayment is made on an account, the lower the proportion of each successive monthly payment applied to interest, resulting in greater cumulative interest savings over the life of a loan than if the principal balance is reduced later in the life of a loan. Thus, prepaying the newer loan first may be more financially advantageous because it reduces the principal balance earlier in the life of that loan. By applying the $5,000 prepayment to the newer loan, the consumer would save $12,373.51 in interest costs and about 12 months on the repayment term. If the consumer instead applied the $5,000 prepayment to the older loan, the consumer would save only $6,066.52 in interest costs and about eight months on the repayment term. In other words, applying the entire prepayment to the newer loan would save the consumer $6,305.99 more in interest and four additional months of repayments relative to prepaying the older loan instead (see Figure 1). Given this specific scenario, when consumers can make a prepayment, it is financially beneficial to make the payment toward the newer debt.

Impact of a $5,000 Prepayment Across Alternative Prepayment Scenarios.

The benefit of paying down newer installment debt is clearest when loans vary only in age, as in the aforementioned hypothetical scenario. However, this situation is not always the one that consumers face, as they may have multiple installment debts that differ on several loan parameters, including but not limited to age. In such situations, it is more difficult to ascertain which debt to prioritize because, although the financially optimal answer can be found using amortization schedules or calculus, 3 it depends on the interest rates, remaining balances, and remaining loan terms. Once consumers have gathered all the information, they would then have to calculate the interest savings between multiple options. Given this multistep process, consumers are unlikely to engage in such calculations, even with the aid of accessible amortization tools and schedules. Instead, consumers are more likely to rely on simplifying heuristics such as affective inputs to guide their decision-making (e.g., Slovic et al. 2007). In the current research, we suggest that a relevant factor that influences installment debt prepayment is that consumers feel they have invested more effort to repay older versus newer debt.

Installment Debt Accounts and Invested Effort

Prior research has shown that consumers often allocate resources in a way that disproportionately favors previous investments of time, money, or effort, a phenomenon widely known as the sunk cost effect or sunk cost fallacy (Arkes and Blumer 1985; Garland 1990; Garland and Newport 1991; Soman 2001). Specifically, consumers consider resource investments that they have made in the past and make decisions that align with prior investments even when it is suboptimal to do so. In other words, they double down based on sunk costs (Staw 1981; Whyte 1986). The privileged position given to prior resource investments is irrational when these investments cannot be recovered and are therefore irrelevant for making decisions.

Prior research suggests that the sunk cost effect may arise because individuals feel the need to defend themselves and justify their previous investments so as not to appear incompetent or wasteful. To abandon previous resource investments without further investment may seem like an acknowledgment of prior incompetence or an admission that earlier investments were wasteful (Arkes and Blumer 1985; Staw 1981). Indeed, the sunk cost effect may be characterized as “throwing good money after bad” (i.e., investing additional resources in a failed project).

However, it is worth reiterating that the sunk cost effect applies not only to monetary investments but also to effort investments (Shou et al. 2026)—that is, mental and physical work or energy that has already been expended in pursuit of a specific goal. For instance, Zeelenberg and Van Dijk (1997) demonstrate that consumers are more motivated to attain outcomes that align with their previously invested effort. Similarly, in the domain of goal pursuit, Zhang et al. (2011) show that previously invested mental or physical effort (e.g., transcribing a passage or climbing more stairs) can increase consumers’ future effort to attain their goal. Collectively, these findings provide evidence of the importance consumers place on previously invested effort.

In the context of debt repayment, we contend that the prior investment of mental and physical effort or energy to repay a particular loan plays a crucial role in increasing one's desire to fulfill that goal (i.e., to pay off the debt). To manage their debts effectively, consumers must regularly attend to and ensure their accounts remain in good standing and that each monthly installment is made on time. In other words, consumers must invest regular effort to maintain their debt accounts. This effort may entail work and energy that is mental (e.g., thinking about and planning payments) and/or physical (e.g., writing a check, logging onto a website) in nature. The longer consumers maintain their debt accounts, the greater the cumulative effort they invest in managing and maintaining them. We anticipate that this level of invested effort will affect how consumers prioritize their installment debt prepayments. Specifically, if individuals have expended more effort toward older versus newer debts, we predict that they will have a stronger desire to pay down an older debt.

Although there is often a correlation between consumers’ cumulative monetary investment and their effort investment toward a particular loan, this may not always be case. While we acknowledge that the collective monetary amount that has been put toward repaying a loan may also affect how much consumers prioritize it when making prepayment decisions, we suggest that invested effort will be a particularly influential factor in their decision-making. This is because installment debts are often large enough that consumers are responsible for managing their debt accounts each month for many years until the debt is paid in full. For instance, repaying a 30-year fixed mortgage may involve undertaking 360 unique repayment actions (i.e., one per month) over a span of three decades. Thus, we predict that the cumulative effect of sustained mental and physical work and energy that has already been expended in repaying an older debt causes consumers to prioritize older debt when making prepayment decisions.

There are likely to be multiple second-order intermediating routes—both cognitive and affective in nature—that link perceptions of invested effort with the FIFO preference. From a cognitive standpoint, Zhang et al. (2011) reason that invested effort serves as a signal of the value one places on a goal (e.g., the repayment of a particular debt). In terms of affect, being indebted constitutes a source of anxiety for consumers (Dackehag et al. 2019; Dunn and Mirzaie 2023) that may become more intense when a goal remains incomplete for longer (i.e., when an debt is older). Given that the route from invested effort to the FIFO preference is likely to be multiply determined and involve several intervening factors, we focus in this research on documenting that invested effort affects debt prepayment decisions and offer additional thoughts on second-order intermediaries in the “General Discussion” section.

Interventions to Reduce FIFO Preference

If consumers prioritize prepaying their older debts because they feel they have invested more effort toward them, then reducing the effort invested toward the older debt should reduce their FIFO preference. When making debt repayments, consumers often have the option to make their debt payments manually or enroll in automatic payments. While payment processes vary across institutions, manual payments often require consumers to log in online, enter their account information, verify account balances, and submit payments each month. In lieu of paying online, some consumers may even handwrite and mail checks to their financial institution and monitor their accounts thereafter to ensure funds are applied to their loans. Such processes are indeed more effortful than the alternative, which is to set up automatic transfers where consumers provide financial institutions permission to pull funds from a specified account each month and automatically apply said funds to their loan accounts. Automatic repayments are less effortful than manual ones. Thus, we suggest that managing a loan using manual or automatic payments will affect the relative effort invested between two loans and moderate the effect of debt age on debt prepayment prioritization.

Additionally, if debt age underlies perceptions of invested effort, then shifting focus away from the age of the loan should also attenuate consumers’ FIFO preference while providing further support for our age-based process explanation. Previous research on goal pursuit has shown that such shifts in focus can alter judgments and decisions (Koo and Fishbach 2012; Toyama 2022). For instance, conceptualizing one's progress toward a goal in terms of what has been accomplished thus far, as opposed to what remains to be accomplished, has been shown to affect goal progress perceptions, motivation, and consequential downstream behaviors (Koo and Fishbach 2012). To influence whether consumers focus on the past or on the future, marketers have respectively adopted “to-date” and “to-go” frames in their communications. For instance, some nonprofit organizations and fundraisers communicate the amount of funds raised so far (to-date frame) and others focus on the amount needed to reach their end goal (to-go frame).

We propose that these temporal frames can be leveraged in installment debt management to influence the FIFO preference. Communicating the term of the installment debt and the age of the debt can be considered a to-date frame. Communicating the term of the installment debt and the remaining duration of the debt would provide equivalent information (age is simply the difference between those two pieces of information) but can be characterized as a to-go frame. In line with our theorizing, while a to-date framing may cause older debt to generate heightened perceptions of invested effort, a to-go frame would be expected to mitigate this perception since it focuses consumers on the effort that is still required to fulfill the goal of repaying each debt.

Lastly, an assumption underlying our investigation is that consumers would like to maximize the total interest savings of their prospective prepayment allocation decisions, but they do not fully understand the consequences of their actions. However, an alternative argument could be that consumers are not overly concerned about decreasing their interest charges and other considerations overwhelm this goal. One way to document that this effect emerges because they do not fully understand the consequences of their decisions is to provide consumers with a decision aid. One such decision aid could be just-in-time interest savings information. Indeed, such an intervention would be easily implementable by financial advisors or online calculators. Providing information about the total interest savings implications of a prospective allocation in a straightforward manner will make the cost of the FIFO preference clear and encourage allocations that result in higher interest savings. Taking these points together, we predict:

We test these hypotheses in eight studies. In Study 1, using behavioral peer-to-peer loan data, we find that consumers with multiple loans are more likely to prioritize older debt accounts. In Study 2a and preregistered Study 2b, we demonstrate in both choice and preference tasks that consumers prioritize older versus newer installment debt when there is no financial advantage to prepaying one debt sooner than the other (H1). In preregistered Study 3, we replicate the effect on allocation where consumers can allocate any amount of their prepayment to either loan (H1).

In preregistered Study 4, we show that FIFO preference emerges because consumers believe they have invested more effort into an older (vs. newer) debt (H2). In preregistered Study 5a, we use a causal chain design to provide support for the proposed invested effort process (H2 and H3a). In preregistered Study 5b, we document a managerially useful temporal framing intervention by showing that FIFO preference is attenuated when consumers focus on the time remaining to pay off their debts rather than on debt age (H3b). In preregistered Study 6, we offer another managerially relevant intervention by demonstrating that providing just-in-time information about the total interest savings of prospective payment allocations helps consumers make more optimal choices (H4).

Across our experiments, we also rule out various alternative explanations for consumers’ prioritization of older debt. While we carefully design our experiments to account for those that can be controlled in each scenario (e.g., older loans could have shorter remaining terms, so we hold the remaining term constant), two possible explanations warrant further discussion. First, consumers could perceive that prepaying an older (vs. newer) loan would most help reduce the total number of outstanding accounts (i.e., debt account acceleration). While older debt may not necessarily have a smaller balance, and while funds are insufficient to repay accounts in full in each of our studies, this explanation fits with prior findings that consumers desire to close out accounts with smaller balances (see Table 1). Second, consumers could perceive that prepaying an older vs. newer loan would be more beneficial for their credit score (i.e., credit score impact). Whether that is true depends on many factors in consumers’ credit histories, but they may not have an accurate understanding of how debt repayment affects their credit scores (Lyons, Rachlis, and Scherpf 2007). These two explanations are rooted in consumers’ subjective beliefs, and they could influence consumer decision-making regardless of whether the intuitions are correct. Accordingly, we measure and account for both in Study 4.

For all experiments, we report all measures, conditions, and data exclusions. There were no exclusions in Studies 1 and 2a. In Studies 2b, 4, 5a, and 6, responses from participants who failed an attention check at the end of the study were removed prior to analyses (in accordance with the studies’ respective preregistrations); including these responses does not affect the results. In Studies 3 and 5b, participants who failed an instructional manipulation check (Oppenheimer, Meyvis, and Davidenko 2009) at the beginning of each study were directed to an alternative task and did not participate in the main study. Data and preregistrations for all studies can be found on OSF (https://osf.io/sy4cz/?view_only=7a09e15f8af74ab59c2925f999d351ab).

Study 1: Prioritization of Older Debt in Peer-to-Peer Loan Repayment Data

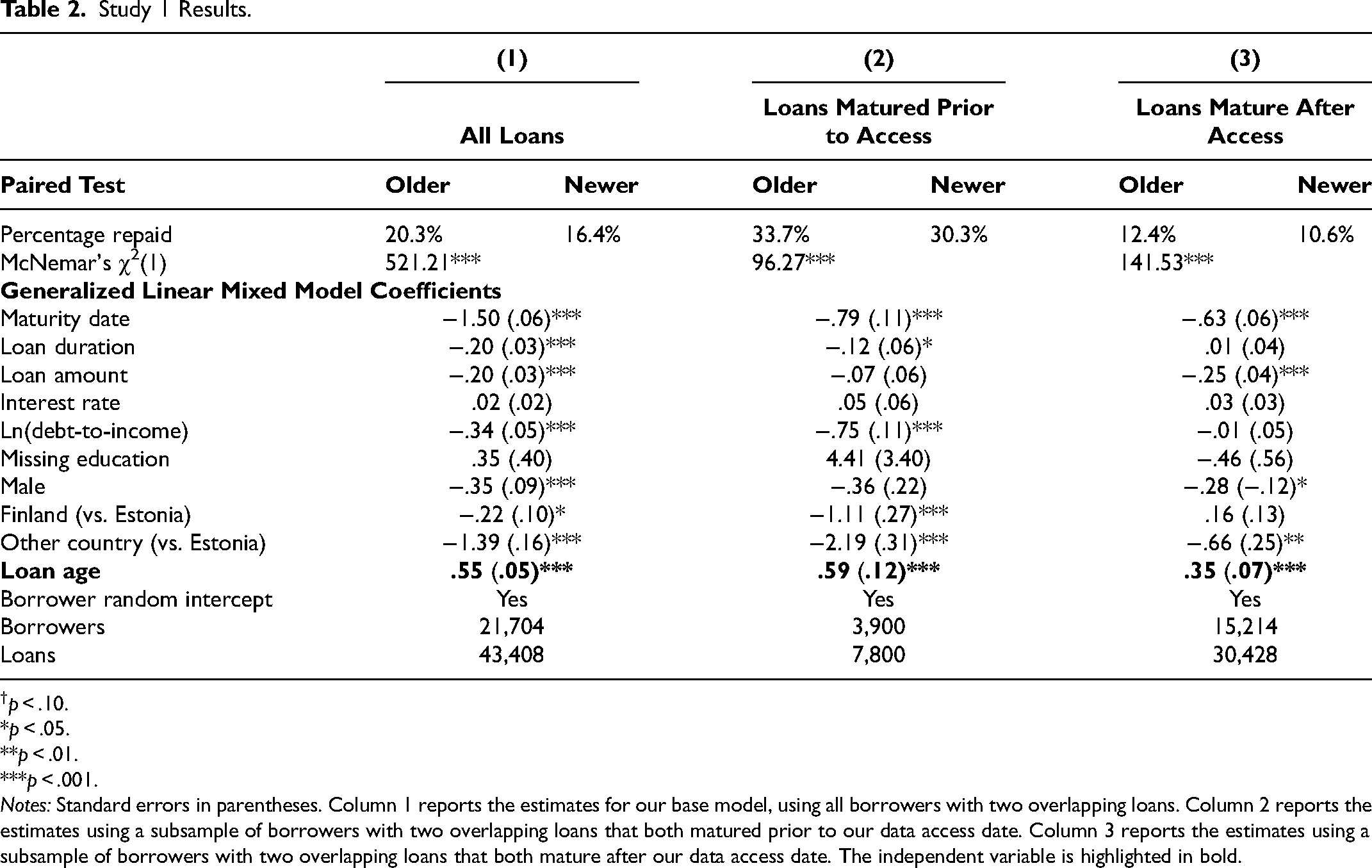

We studied the relationship between relative debt age and debt repayment in peer-to-peer installment loan data from Bondora (2023). Bondora is an Estonian peer-to-peer lending platform that enables investors to browse loans that have been prescreened by Bondora. Bondora made its loan data openly available, subject to data protection laws. The dataset consists of 314,787 loans among 142,318 borrowers originated from February 2009 through July 2023. This dataset is structured as a cross-sectional inventory of loans, rather than as a longitudinal stream of payments. We observe information about each loan and its status as of the date of access, so we are cautious not to label all these repayments as prepayments.

Because we were interested in how the relative ages of loans affect borrowers’ repayment choices, we needed to observe loans among borrowers who had more than one loan. To simplify the analysis, we filtered this dataset down to only the borrowers who had exactly two loans (54,166 loans among 27,083 borrowers). Given that our research focuses on repayment choices when borrowers have two loans at the same time, we needed to further filter out borrowers whose loans did not overlap. First, we required that the loan periods overlapped (i.e., the maturity date of the older loan was after the origination date of the newer loan). Since borrowers could have already defaulted on the older loan before originating the newer loan, our second requirement was that the last payment on the older loan also overlapped with the loan period of the newer loan (i.e., the last payment date of the older loan was after the origination date of the newer loan). Both criteria were met by approximately 80% of the borrowers, resulting in our final sample of 43,456 loans among 21,728 borrowers.

Method

Bondora provided variables indicating whether the loan had been fully repaid, the account was current, the account was late, or the account was defaulted on. Our focal dependent variable was whether each loan had been repaid (1 = repaid, 0 = else). Our focal independent variable was the within-borrower factor of loan age (1 = newer loan, 2 = older loan). Borrowers were more likely to have repaid their older loans (20.3%) than their newer loans (16.4%, McNemar's χ2(1) = 521.21, p < .001, g = .31), but we ran a more complex model to provide a more rigorous test. Because we observe repayment status at a snapshot in time (July 2023), older loans may have been repaid more often simply because they also had earlier maturity dates. Although loan age and maturity date were weakly correlated (r = .04), we controlled for maturity date (years from January 1, 1970, the default in R) in our model. We also controlled for loan amount (M = $3,173, SD = $2,091), loan duration or term (M = 50.53 months, SD = 16.81 months), and interest rate (M = 29.85%, SD = 16.77%). Even though each borrower serves as their own control given our data structure, we also controlled for some borrower characteristics: debt-to-income ratio (Muntransformed = 2.99, SD = 10.78, log-transformed for the analysis), whether the borrower reported their education (repayment tendencies did not differ by education level, but did differ between those with an observed education level and those without in some models; no education reported: 1%), gender (54% male, 46% female), and country (36.3% Estonia, 51.7% Finland, 12.1% the Netherlands, Slovakia, or Spain; these latter three countries were combined for analysis because there were few borrowers from the Netherlands and Slovakia, and repayment tendencies were similar across them in most models). To facilitate model convergence, all continuous predictors were standardized. Since we were modeling a dichotomous response with within-borrower predictors, we tested our hypothesis using a generalized linear mixed model with logit link in R (R Core Team 2022). To address heterogeneity in repayment patterns across borrowers, we modeled a random intercept for borrowers. We modeled all other effects as fixed.

Results and Discussion

Main results

The effects of maturity date (b = −1.50, z = −25.96, p < .001), loan duration (b = −.20, z = −7.38, p < .001), loan amount (b = −.20, z = −7.37, p < .001), debt-to-income ratio (b = −.34, z = −7.41, p < .001), male gender (b = −.35, z = −3.37, p < .001), borrowing from Finland (b = −.22, z = −2.11, p = .035), and borrowing from other countries (b = −1.39, z = −8.52, p < .001) were negative and significant, indicating that loans with later maturity dates, longer durations, or greater initial amounts and loans made to borrowers who had a greater debt burden, were male, or were non-Estonian were less likely to have been repaid. Interest rate (b = .02, z = .70, p = .484) and failing to report education (b = .35, z = .90, p = .371) did not have significant effects on likelihood of repayment. Importantly, the effect of loan age was positive and significant (b = .55, z = 10.33, p < .001): Older loans were more likely to have been repaid.

Robustness tests

We also conducted two additional robustness tests using subsamples of the data. Although we controlled for maturity date in our model, the inclusion of these robustness tests was motivated by the fact that simply repaying the prearranged installment amount each month would likely (depending on the loan durations) lead to the same pattern of repaying older loans before newer loans. First, we reran the analysis using only borrowers whose loans had maturity dates prior to our accessing the data—this tests our hypothesis using only retrospective data where the newer loan was known not to be outstanding. Our second subsample provided an even more stringent test. We reran the analysis using only borrowers whose loans had maturity dates after our accessing the data—this tests our hypothesis using only outstanding loans where a repayment can readily be interpreted as a prepayment. These robustness tests yielded the same conclusions and are presented in Table 2. Finally, we also conducted all tests in all three subsamples using two additional alternative dependent variables: whether the loan was in default or had a late status. These additional robustness tests yielded the same conclusions (only with a reversed sign—being more likely to repay corresponds with being less likely to default or pay late) and are presented in the Web Appendix.

Study 1 Results.

p < .10.

*p < .05.

**p < .01.

***p < .001.

Notes: Standard errors in parentheses. Column 1 reports the estimates for our base model, using all borrowers with two overlapping loans. Column 2 reports the estimates using a subsample of borrowers with two overlapping loans that both matured prior to our data access date. Column 3 reports the estimates using a subsample of borrowers with two overlapping loans that both mature after our data access date. The independent variable is highlighted in bold.

This study provides initial support for H1 in real installment debt repayment data. Consumers with multiple loans were more likely to prioritize repaying older versus newer debt accounts. While this study provides initial support for this effect, and although our control variables help address observable heterogeneity among the loans and our random intercept helps address heterogeneity among the borrowers, ultimately the results from this study are correlational in nature. To draw more solid causal conclusions, the remainder of our empirical work examines the effect of relative debt age using experiments, enabling us to control the loan characteristics and to directly observe prepayment choices.

Studies 2a and 2b: Prioritization of Older Debt When There Is No Financial Advantage to Prepaying Either Loan Sooner

We hypothesized that consumers prefer to prepay older versus newer installment debt. In Studies 2a and 2b, we sought to demonstrate this preference using two different installment loan types (secured and unsecured), two different prepayment sources (windfall and budget slack), and two different measures of our dependent variable (choice and preference). We also sought to demonstrate FIFO preference when there is no financial advantage to prepaying either loan sooner than the other. To do so, in both studies, we held the interest rates, monthly payments, and outstanding balances constant between the two loans. Additionally, prior research demonstrates that consumers commonly adopt a payment-benefit matching heuristic and repay loans for purchases that have shorter remaining useful lives (Hirst, Joyce, and Schadewald 1994). Further, it is possible that consumers seek to prepay whichever lender they first took out a loan from. We designed these studies to test our proposition and rule out these two alternative explanations. In Study 2a, we held the repayment terms (useful lives) constant between two automobile loans, and in Study 2b, we held the lenders constant between two loans.

Method

Two hundred CloudResearch-approved (Litman, Robinson, and Abberbock 2017) participants from Amazon's Mechanical Turk platform (123 men, 77 women; Mage = 39.7 years) participated in Study 2a, and 150 Prolific participants participated in preregistered (https://aspredicted.org/fx7b-zgny.pdf) Study 2b for monetary compensation. Study 2a did not have an attention check. In Study 2b, four participants failed an attention check near the end of the study that asked participants to indicate the windfall/slack amount provided in the study ($0, $20, $50, $75). Those who did not accurately recall this amount were screened out, as preregistered, leaving 146 participants (56 men, 88 women, 1 nonbinary/other, 1 prefer not to answer; Mage = 39.4 years; modal education = bachelor's degree; modal household income = $20,000–$39,999 and $60,000–$79,999).

In both studies, we used a one-cell design. In Study 2a, all participants imagined they recently received $1,000 as a Christmas gift and could use the money to prepay some of their debt, which consisted of two automobile loans. We informed participants that both loans had the same interest rate (4.5%), monthly payment ($626), current balance ($14,331), and remaining term (two years). Additionally, participants read that one loan had an original balance of $45,000 and was taken out five years ago, while the second loan had an original balance of $33,552 and was taken out three years ago. Participants then read that they had been making monthly payments for both loans on time and planned to keep each vehicle for the next two years.

In Study 2b, all participants imagined they had two BNPL loans. We informed participants that the two BNPL loans were amortized and provided an overview of how amortized loans work (Pomroy 2022). Next, participants viewed monthly statements of their two BNPL loans, which were from the same lender (Klarna) but had different account numbers. To ensure participants processed the information that was given to them, we reminded them that the two loans had the same monthly payment ($33.40), interest rate (19.9%), and current balance ($516.21), as was conveyed in the statements. Additionally, the loan with account number 5EJN83K was taken out about a year and a half ago (originated in April 2023), and the loan with account number E583THN was taken out about six months ago (originated in April 2024). Then, participants imagined they had $20 left over each month after all their other expenses were paid, which they would like to use to get ahead on their debt. We told participants that they had made each payment for both loans on time, there was no prepayment penalty on either loan, and any amount paid would be applied to principal only.

In Study 2a, participants chose which loan to pay their $1,000 toward and responded to an open-ended question asking them to briefly explain how they made their decision. In Study 2b, participants indicated the loan to which they would prefer allocating the additional $20 per month (1 = “Definitely the loan with account number 5EJN83K,” 5 = “Either loan,” 9 = “Definitely the loan with account number E583THN”), which we reverse-coded so that higher values would indicate a preference for the older loan (with account number 5EJN83K).

Results and Discussion

In Study 2a, participants strongly preferred to prepay the older automobile loan (older: 72.5%, z = 6.36 [vs. 50%], p < .001, OR = 2.64). In Study 2b, participants strongly preferred to allocate their $20 a month budget slack to the older BNPL loan (M = 6.18, SD = 2.73; t(145) = 5.25 [vs. scale midpoint of 5], p < .001, d = .43). Combined, these two studies provide initial support for H1. Consumers were more likely to choose to prepay, and more strongly preferred to allocate their monthly budget slack to, the older loan when there was no financial advantage to prepaying one loan earlier than the other (i.e., the interest rate, monthly payment, and term remaining were the same at the time the decision was made). In Study 2a, by keeping the repayment term and useful life constant, we rule out that consumers prefer to prepay older installment debt due to the payment-benefit matching heuristic (Hirst, Joyce, and Schadewald 1994). In Study 2b, by keeping the lender constant, we rule out that consumers prefer to prepay the older debt due to wanting to prepay whichever lender they first took out a loan from. Though these studies provide initial evidence of our hypothesized preference (H1) while keeping most parameters constant at the time of decision-making, in the real world consumers are likely to have loans with parameters that differ. In the next study, we demonstrate the effect in these instances as well.

Study 3: Prioritization of Older Debt When There Is a Financial Advantage or Disadvantage to Prepaying One Loan Sooner

In this study, we sought to evaluate whether consumers prefer to prepay older debt when there is a financial advantage or disadvantage to prepaying either loan based on a different parameter (i.e., other than age). Additionally, we sought to replicate consumers’ preference to prepay older debt when they can allocate a monetary bonus however they wish between the two loans. To test the effect of age on consumers’ allocations toward older debt when it is financially disadvantageous to do so, we varied the interest rates such that the older loan had a lower interest rate than the newer loan, and we held the current balance and monthly payment constant between the two loans. With this design, any preference to prepay the older loan was to participants’ financial disadvantage as it would save them less in interest costs than if they were to allocate all their funds to the newer loan. To test the effect of age on consumers’ preference to prepay older debt when it is financially advantageous to do so, we varied the current balances between two loans such that the older loan had a higher current balance than the newer loan, and this time we held the interest rate and monthly payment constant between the two loans. Any preference to prepay the older loan was to participants’ financial advantage as, due to the higher outstanding balance, consumers would save more in interest if they allocated more to the older loan. Lastly, to test the effect of age while holding the parameter differential constant, we also vary whether we withhold versus provide age information to participants. This design allows us to test whether participants’ allocation decisions differ when the age of each debt is known (vs. unknown), and when it is financially advantageous or disadvantageous to do so.

Method

Six hundred four Prolific participants participated in this preregistered (https://aspredicted.org/myjk-5w6k.pdf) study for monetary compensation. We included an instructional manipulation check (Oppenheimer, Meyvis, and Davidenko 2009) at the beginning of the study. The instructional manipulation check question asked participants to demonstrate that they were reading instructions by selecting “2” for a specified item. Fifty-five participants who failed this check were directed to an alternative task and did not participate in the main study. These participants were thus screened out, as preregistered, leaving 549 participants (284 men, 256 women, 7 nonbinary/other, 2 prefer not to answer; Mage = 38.78 years; modal household income = $40,000–$59,999). We used a 2 (age information: absent vs. present) × 2 (parameter differential: interest rate vs. current balance) between-subjects design. First, all participants imagined they had two loans, both of which are amortized, and read the same overview of how amortized loans work as in Study 2b. Next, participants imagined they had received a $2,500 bonus from work that they would like to use to get ahead on their debt. Then, in the age information absent conditions, we informed participants that one loan was taken out from Orion Bank and one from Novo Bank. In the age information present conditions, participants learned that the loan from Orion Bank was taken out eight years ago, and the loan from Novo Bank was taken out four years ago. We informed participants in the interest rate differential conditions that the loan from Orion Bank had an interest rate of 4.5%, the loan from Novo Bank had an interest rate of 4.9%, and both loans had a monthly payment of $626 and a current balance of $14,331. In the current balance differential conditions, we told participants that the loan from Orion Bank had a current balance of $14,331, the loan from Novo Bank had a current balance of $13,221, and both loans had an interest rate of 4.5% and a monthly payment of $626. Then, similar to Study 2a, participants read that they had made every monthly payment on time, and there was no prepayment penalty on either loan. Lastly, participants indicated how they would allocate the funds between the two loans before responding to demographics.

Results and Discussion

For ease of comparison across studies, in all studies we transformed the dollar allocation to allocation share by dividing the dollar allocation by the total available funds (in this study, $2,500). We control for demographics in all analyses in this and future studies.

4

The effect of interest was the main effect of age information. A priori, we did not hypothesize an interaction between the age information and parameter differential conditions, or a main effect of parameter differential, because neither were central to our theorizing. For transparency, however, we report all findings for this study. The parameter differential main effect was significant (F(1, 541) = 30.11, p < .001,

As expected, the main effect of age information on allocation share was also significant (F(1, 541) = 16.73, p < .001,

This study demonstrates that when the age of each installment debt is present, participants have a stronger preference to prepay their older versus newer debt irrespective of whether it is to their financial advantage or disadvantage to do so (H1). In previous studies, we held interest rate, monthly payment, and current balances constant between two loans so there was no financial advantage to prepaying either loan early. In this study, we relax this constraint and vary loan parameters between two loans. In the interest differential condition, we vary the interest rates so that the loan from Orion Bank (i.e., the older loan when age information is present) has a lower interest rate than the loan from Novo Bank (i.e., the newer loan when age information is present). With this design, participants would save the most on interest costs by allocating all of their funds to the loan with a higher interest rate (i.e., Novo). Despite this financial advantage (i.e., greater interest savings), we find that participants exhibited FIFO preference by allocating more of their bonus to the loan from Orion Bank, the loan with a lower interest rate, when the age of each debt was present.

In the current balance differential condition, we vary the current balances so that the loan from Orion Bank (i.e., the older loan when age information is present) has a higher balance than the loan from Novo Bank (i.e., the newer loan when age information is present). With this design, participants save the most on interest costs by allocating all of their funds to the loan with a higher balance (i.e., Orion). To participants’ financial benefit (i.e., greater interest savings), we find that participants in this condition allocated a greater share of their bonus to the higher current balance loan from Orion Bank when the age of each debt was present. Finally, in this study, where participants could allocate as much of their bonus as they wished to either loan, we observe prioritization of older installment debt with a fourth measurement approach (i.e., allocation) that complements the measures in our earlier studies (i.e., actual behavior, choice, and preference).

Study 4: Mediation via Invested Effort

In Study 4, we seek to demonstrate that consumers exhibit FIFO preference because they feel they have invested more effort to repay their older debt. Additionally, as another measure of our dependent variable, we ask consumers which loan they feel more motivated to prepay. Lastly, we measure and rule out two possible alternative explanations for the effect of debt age on consumers’ preference to prepay older installment debt accounts: a perception that partially prepaying the older loan would most help reduce the total number of outstanding accounts (i.e., debt account acceleration) and a perception that partially prepaying the older loan would be more beneficial for one's credit score (i.e., credit score impact).

Method

Three hundred one participants recruited through CloudResearch’s Connect platform participated in this preregistered study (https://aspredicted.org/zdbk-nrbx.pdf) for monetary compensation. Three participants failed an attention check near the end of the study that asked participants to indicate the savings amount provided in the study ($0, $500, $1,200, $1,600). Those who did not accurately recall this amount were screened out, as preregistered, leaving 298 participants (176 men, 120 women, 1 nonbinary/other, 1 prefer not to answer; Mage = 39.2 years; modal education = bachelor's degree; modal household income = $40,000–$59,999). We used a two-cell (age information: absent vs. present) between-subjects design, where participants imagined they had two student loans for which we provided monthly statements. Before viewing the monthly statements, participants were informed both loans are amortized and read the same overview of how amortized loans work as in Study 2b. As shown in the statements, one student loan was from Orion Bank and one was from Novo Bank. Both loans were identical at this point (same interest rate [6.0%], monthly payment [$276.77], current balance [$14,520.47], no prepayment penalty, and so on). In the age information absent condition, the statements indicated both loans were current. In the age information present condition, rather than providing the loan status, the statements indicated the loan from Orion Bank originated on May 13, 2020, and the loan from Novo Bank originated on May 13, 2024. To ensure participants processed the information on the statements, we reiterated the information shown on their statements. Participants then imagined they had $1,200 available in their savings that they would like to use to pay down some of their debt, and we informed them the prepayment would be applied to principal only.

Participants indicated the loan to which they would prefer to allocate their $1,200 in savings (1 = “Definitely the loan from Orion Bank,” 5 = “Either loan,” 9 = “Definitely the loan from Novo Bank”). As another measure of our focal dependent variable, participants also indicated which loan they were more motivated to repay (1 = “Definitely the loan from Orion Bank,” 5 = “I’m equally motivated to repay either loan,” 9 = “Definitely the loan from Novo Bank”). We reverse-scored both of these measures so higher response values indicated participants had a stronger preference to prepay, and were more motivated to prepay, the loan from Orion Bank (the older loan when age information was present). To measure invested effort, participants indicated which loan had required more effort to manage, had required more work to repay, and had required more of their energy to handle up until the present time (1 = “Definitely the loan from Orion Bank,” 9 = “Definitely the loan from Novo Bank”; α = .93), which we transformed and averaged so that higher values reflect relatively greater invested effort into the loan from Orion Bank (the older loan when age information was present). Then, participants responded to our debt account acceleration and credit score impact items as potential alternative explanations for our effect. Specifically, participants indicated which loan they thought repaying early would most help reduce the total number of outstanding loan accounts (1 = “Definitely the loan from Orion Bank,” 5 = “Either loan,” 9 = “Definitely the loan from Novo Bank”) and how prepaying each loan would impact their credit score in the near term (1 = “Significantly hurt my credit score,” 5 = “Have no impact on my credit score,” 9 = “Significantly improve my credit score”). Lastly, participants completed an attention check and provided demographic information.

Results and Discussion

Preference

As expected, when age information was present, participants more strongly preferred to prepay the loan from Orion Bank (the older loan) versus when age information was absent (MPresent = 5.55, SD = 2.75 vs. MAbsent = 4.89, SD = 1.24; t(291) = 2.57, p = .011, d = .31).

Motivation

Consistent with their preferences, participants were more motivated to prepay the loan from Orion Bank in the age information present versus absent condition (MPresent = 5.69, SD = 2.51 vs. MAbsent = 4.88, SD = 1.19; t(291) = 3.67, p < .001, d = .41).

Invested effort

Participants in the age information present (vs. absent) condition indicated they had invested more effort to repay the loan from Orion Bank (MAgeInfoPres = 6.25, SD = 2.04 vs. MAgeInfoAbs = 4.79, SD = .67; t(291) = 8.23, p < .001, d = .96).

Debt account acceleration

There was no difference between the age information conditions for participants’ perceptions about how repaying either loan early would most help reduce their total number of outstanding loan accounts (MAgeInfoPres = 5.18, SD = 2.12 vs. MAgeInfoAbs = 4.87, SD = .97; t(291) = 1.47, p = .143, d = .19).

Credit score impact

There was no difference between the age information conditions for participants’ perceptions about the impact of prepaying the loan from Orion Bank (MAgeInfoPres = 6.53, SD = 1.63 vs. MAgeInfoAbs = 6.72, SD = 1.58; t(291) = −1.11, p = .267, d = −.12) or Novo Bank (MAgeInfoPres = 6.45, SD = 1.54 vs. MAgeInfoAbs = 6.74, SD = 1.64; t(291) = −1.60, p = .110, d = .00). 6

Mediation

Given there were no significant effects of age information on debt account acceleration or credit score impact, we conducted a mediation analysis using 5,000 bootstrapped resamples using PROCESS Model 4 to test if invested effort mediates the effect of age information on prepayment preference, controlling for demographics (Hayes 2013). As expected, the indirect effect through invested effort was significant (abInvEffort = .48, SE = .15, 95% CI: [.17, .78]). The age information present (vs. absent) condition increased the amount of effort participants perceived they had invested in the loan from Orion Bank versus the loan from Novo Bank (b = 1.46, t(292) = 8.26, p < .001). The more effort participants perceived they had invested in the loan from Orion Bank versus Novo Bank, the more strongly they preferred to prepay the loan from Orion Bank (b = .33, t(291) = 4.10, p < .001). The remaining direct effect of age information on prepayment preference was nonsignificant (b = .20, t(291) = .76, p = .45). These results show that perceptions of invested effort underscore consumers’ FIFO preference (H2). Specifically, the same debt (i.e., the loan from Orion Bank) was perceived as having required greater effort to service and maintain when age information was present, which in turn led to this debt being prioritized in prepayment.

Study 5a: Manipulating Invested Effort

In Study 5a, we seek to provide causal chain process evidence by manipulating invested effort (Spencer, Zanna, and Fong 2005). We hypothesized that consumers prioritize older versus newer debt because they feel they have invested more effort into their older debt. Thus, reducing the effort consumers feel they have invested into their older debt should reduce the amount they allocate to it. Because in our other studies a higher dollar amount had been repaid to the older loan, in this study we inform participants that a higher dollar amount had been repaid to the newer loan. This design allows us to differentiate between consumers’ effort investments and their monetary investments (i.e., their financial sunk cost) and show that the FIFO preference persists even when the monetary amount repaid on the newer debt is larger than that for the older debt. 7

Method

Six hundred one participants recruited through CloudResearch Connect participated in this preregistered study (https://aspredicted.org/cv22-dp25.pdf) for monetary compensation. We included an attention check near the end of the study asking participants to select the color of the sky on a clear day. No participants failed this check, so all 601 participant responses remained in our analyses (321 men, 273 women, 4 nonbinary/other, 3 prefer not to answer; Mage = 39.9 years; modal education = bachelor's degree; modal household income = $40,000–$59,999 and $140,000 or more). We used a three-cell (effort: control, older-higher, and older-lower) between-subjects design, where participants first imagined they had two student loans. Participants were informed that both loans are amortized and read the same overview of how amortized loans work as in Study 2b. Next, participants imagined they had received a $2,500 bonus from work, which they would like to use to pay down some of their debt. Participants then read that one student loan was from Orion Bank and one was from Novo Bank. Both loans had the same 4.5% interest rate, and neither had a prepayment penalty. In all conditions, participants were informed that the loan from Orion Bank was taken out five years ago, and the loan from Novo Bank was taken out four years ago. Further, participants were informed they had repaid $4,500 toward the Orion Bank loan balance and $4,730 toward the Novo Bank loan balance. In other words, participants had repaid more to their newer loan.

To manipulate invested effort, we varied whether participants had manually repaid their loans each month or had enrolled in automatic transfers so their bank transferred payments to their loans each month. In the control condition, participants read that since taking out both of their loans, they have logged into their account to personally transfer funds from their account to their loans every month. As a result, much personal effort has been required in terms of logging into and entering their account numbers, checking their account balances, initiating transfers, and making sure each loan payment is made on time each month. In the older-higher effort condition, participants read that since taking out their loan from Orion Bank (the loan taken out five years ago), they have logged in every month to personally transfer funds from their account to their loans. As a result, much personal effort has been required in terms of logging into and entering their account numbers, checking their account balances, initiating transfers, and making sure each loan payment is made on time each month. Further, when they took out their loan from Novo Bank (the loan taken out four years ago), they set up direct deposit and automatic transfers such that Novo Bank has automatically transferred the funds to their loan every month. As a result, no personal effort has been required with this loan in terms of logging in, checking their account balance, or initiating a transfer each month to make their loan payments. In the older-lower effort condition, participants read the same as above; however, they were informed that the loan from Orion Bank (the loan taken out five years ago) had direct deposit and automatic transfers, whereas the loan from Novo Bank (the loan taken out four years ago) had manual payments. We expected that participants would spontaneously believe they had invested more effort into the older loan in the control condition and that our two differential-effort conditions would successfully manipulate perceptions of relative invested effort.

Participants then indicated how they would prefer to allocate the $2,500 to their two loans (constant sum). As a manipulation check, participants indicated which loan has required more of their effort to manage, which loan has required more of their work to repay, and which loan has required more of their energy to handle (1 = “Definitely the loan from Orion Bank,” 5 = “Both loans have required the same amount of effort/work/energy,” 9 = “Definitely the loan from Novo Bank”; α = .89), which we transformed and averaged so that higher values reflect relatively greater invested effort into the loan from Orion Bank (the older loan). Lastly, participants completed an attention check and provided demographic information.

Results and Discussion

Manipulation check

There was a significant effect of condition on invested effort (F(2, 598) = 487.09, p < .001,

Allocation

As expected, condition had a significant effect on allocation share (F(2, 592) = 42.19, p < .001,

This study provides causal chain process evidence that the invested effort of servicing older debt contributes to consumers’ prioritization of older versus newer debt (H2). 9 Specifically, reducing the invested effort toward an older debt by automating payments reduced prioritization of older debt (H3a). Notably, as shown by the significant FIFO preference in the control condition, we found that invested effort played a larger role in determining how participants made allocation decisions relative to their monetary investment (i.e., their financial sunk cost).

Study 5b: Manipulating Temporal Frame

In Study 5b, we seek to provide additional causal evidence that consumers feel they have invested more effort to service their older debt by manipulating the loan repayment frame that consumers focus on when evaluating their loans. In our previous studies, participants who were given age information were informed how long ago their debts were taken out. In this study, some participants are informed how long each loan has left. We expect this manipulation to shift consumers’ focus from invested effort to remaining effort and attenuate the FIFO preference.

Method

Five hundred fifty-one CloudResearch-approved participants from CloudResearch's Connect platform participated in this preregistered study (https://aspredicted.org/B91_71M) for monetary compensation. Seventy-seven participants failed the same instructional manipulation check used in Study 3 (Oppenheimer, Meyvis, and Davidenko 2009) at the beginning of the study and were screened out, as preregistered, leaving 474 participants (251 men, 213 women, 6 nonbinary/other, 4 prefer not to say; Mage = 38.1 years; modal education = bachelor's degree; modal personal income = $20,000–$39,999; modal household income = $60,000–$79,999). We used a three-cell (age information: absent vs. to-date vs. to-go) between-subjects design, where participants imagined recently receiving a $2,500 bonus, which they could use to pay down their debt. Their debt consisted of two loans: one from Goldview Bank and one from Newell Bank (order counterbalanced). Both loans were identical (same interest rate [6.0%], repayment term [15 years], current balance [$21,825], no prepayment penalty, and so on). In the age information absent condition, no additional information was provided. In the to-date condition, participants were told that the loan from Goldview Bank was taken out ten years ago while the loan from Newell Bank was taken out five years ago. In the to-go condition, participants were told that the loan from Goldview Bank had five years remaining while the loan from Newell Bank had ten years remaining. Next, participants allocated the $2,500 bonus between the two loans and responded to an open-ended question asking them to briefly explain how they made their decision. Lastly, participants responded to three items adapted from Schindler et al. (2023) measuring which loan made them more anxious (see the Web Appendix). 10

Results and Discussion

Allocation

As expected, condition had a significant effect on allocation share (F(2, 465) = 9.76, p < .001,

This study demonstrates that shifting consumers’ focus from the time that has passed on their loans to the time that remains on their loans also shifts their focus away from the effort already invested, and in turn reduces their allocations to their older debt (H3b). This also provides indirect support for our proposed invested effort process (H2).

Study 6: Total Interest Savings Intervention

In Study 6, we seek to devise a decision aid that can help consumers make better loan prepayment decisions. Specifically, we examine whether a decision aid intervention informing consumers of the total interest savings of their prospective allocations affects their allocations to their older debt. An assumption underlying our investigation is that consumers would like to maximize the total interest savings of their prospective payment allocation decisions, but they are unable to do so because they do not fully understand the consequences of their actions. In addition to providing a practical tool to mitigate the negative impact of the FIFO preference, this study also allows us to test our assumption. We hypothesized that in a context where prepaying the newer loan provides higher interest savings, consumers will allocate relatively more of their funds to the older loan when the total interest savings intervention is not provided compared with when the total interest savings intervention is provided.

To test the effect of age on consumers’ allocations toward their older debt when it is financially disadvantageous to do so, we varied the current balances such that the older loan had a lower current balance than the newer loan, and we held the interest rate and monthly payment constant between the two loans. Additionally, in this study, we varied the loan types such that the older loan was a student loan and the newer loan was an auto loan. With this design, any preference to prepay the older loan sooner was to participants’ financial disadvantage as it would save them less in interest costs than if they were to allocate their available funds to the newer loan with the higher current balance. We predict that when the age of each debt is known, participants will allocate more to their older versus newer debt, but when the age of each debt is known and we provide participants with the total interest savings of their allocations, we expect participants to allocate much less to their older debt and much more to their newer debt, saving them more money. Thus, we anticipate that merely providing participants with their interest cost savings will lead consumers to make a more financially optimal allocation.

Method

Four hundred fifty-one CloudResearch-approved participants from CloudResearch's Connect platform participated in this preregistered study (https://aspredicted.org/hrmr-d4j9.pdf) for monetary compensation. Three participants failed the attention check near the end of the study that asked participants to indicate the bonus amount received in the study ($500, $2,500, $5,000, other) and were screened out, as preregistered, leaving 448 participants (216 men, 222 women, 8 nonbinary/other, 2 prefer not to say; Mage = 39.0 years; modal education = bachelor's degree; modal household income = $40,000–$59,000).

We used a three-cell (age information: absent vs. present vs. present + intervention) between-subjects design. First, participants imagined they had two loans, both of which are amortized, and read the same overview of how amortized loans work as in Study 2b. Next, participants imagined they had recently received a $2,500 bonus, which they could use to pay down their debt. They had two loans: a student loan from Orion Bank and a car loan from Novo Bank. The loans were structured so that participants would save the most interest by allocating $166.02 to the Orion loan and $2,333.98 to the Novo loan: The Orion loan had a monthly payment of $626 with a 4.5% interest rate and $21,044 current balance, while the Novo loan had the same monthly payment and interest rate but a $23,212 current balance. In the age information absent condition, no additional information was provided. In the age information present and age information present + intervention conditions, participants were directly told that the loan from Orion Bank was taken out 12 years ago and the loan from Novo Bank was taken out 20 months ago. Next, participants allocated their $2,500 between the two loans using a slider. In the intervention condition, before making their allocation, participants were shown a straightforward graph of total interest savings as a function of allocation between the loans, informed of the allocation at which total interest savings was maximized, and also dynamically shown the total interest savings of their prospective allocations as they moved the allocation slider. Such types of adaptive decision aids are common in the marketplace as methods to help consumers calculate and understand the financial consequences of their debt decisions (e.g., Credit Karma 2025; NerdWallet 2025) and can even include graphical displays (e.g., Calculator.net 2025; WalletHub 2025). Lastly, participants completed an attention check and reported demographics.

Results and Discussion

As expected, condition had a significant effect on allocation share (F(2, 440) = 32.69, p < .001,

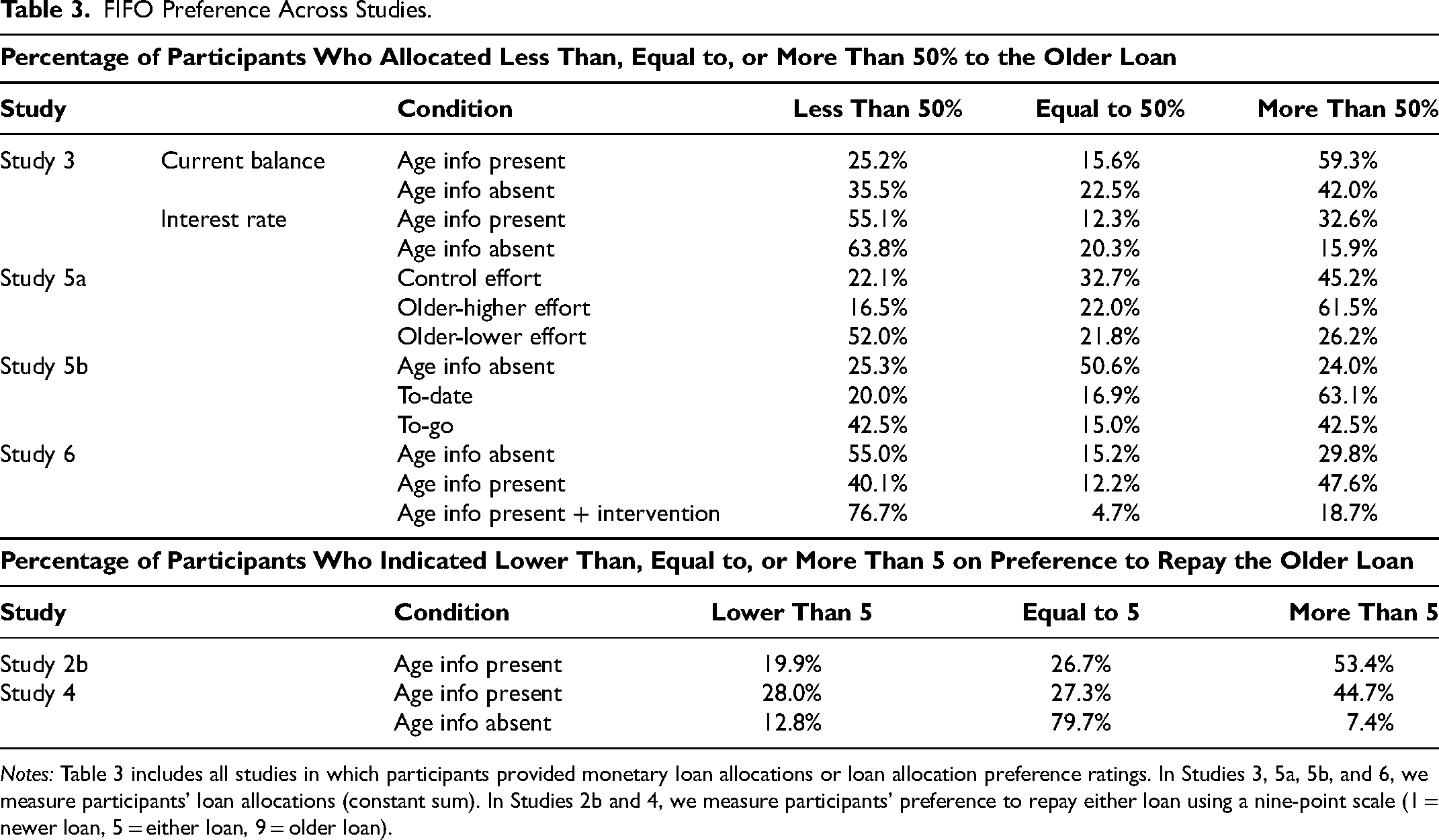

In this and our other studies, we also conducted a series of supplemental analyses by trichotomizing our preference and allocation variables into prioritization variables and by conducting nonparametric tests for allocation (fully discussed in the Web Appendix). In Table 3, we report frequencies of older-loan prioritizers and break out the non-older-loan prioritizers into those who prioritized the newer loan or split their allocation equally between the two loans. These results add nuance to our findings—it is not always the case that a majority of participants prioritize the older loan. However, these tests provide converging support for the notion that consumers account for debt age in installment debt prepayment decisions (see H1).

FIFO Preference Across Studies.

Notes: Table 3 includes all studies in which participants provided monetary loan allocations or loan allocation preference ratings. In Studies 3, 5a, 5b, and 6, we measure participants’ loan allocations (constant sum). In Studies 2b and 4, we measure participants’ preference to repay either loan using a nine-point scale (1 = newer loan, 5 = either loan, 9 = older loan).

General Discussion

Across eight studies, we show that the ages of installment debt accounts affect consumer debt prepayment decisions. Specifically, we demonstrate that consumers prefer to prepay, and allocate more prepayments to, older versus newer installment debt, irrespective of whether it is financially advantageous (Study 3) or disadvantageous to do so (Studies 1, 3, and 6). Further, we find that consumers allocate more money to older versus newer debt because they feel they have invested greater effort into their older versus newer debt (Studies 4 and 5a). While we find consumers prioritize older versus newer debt, this prioritization is tempered when the relative amount of effort consumers feel they have invested into their older debt is reduced (Study 5a), when debt age is reframed from elapsed time (to-date) to time remaining (to-go; Study 5b), and when just-in-time total interest savings information is provided (Study 6).

Our results appear both across multiple experimental lab studies and in secondary data of real consumer installment loan repayment behavior. Our results are also robust; we find a preference to prepay older versus newer amortized debt across loans with different interest rates, repayment terms, current balances, loan amounts, and loan types within and across studies. We find that the results hold regardless of the age format (we used both age and date formats), age differences between the loans (two to nine years apart in age), loan type (auto loan, BNPL loan, student loan, and loans more generally), and loan parameters (interest rate, loan amount, outstanding balance) within and between conditions. Additionally, we differentiate between consumers’ effort investments and their monetary investments and show that the FIFO preference persists even when the monetary amount repaid on the newer debt is larger than that for the older debt. We also account for and rule out possible alternative explanations that may contribute to consumers’ preference to prepay older debt. Taken together, our findings contribute to understanding consumer financial decision-making by identifying debt age as an important factor that affects consumer debt prepayment decisions.

Theoretical Contributions

This research builds on prior debt repayment literature and adds to our existing knowledge about the factors that affect consumer debt repayment decisions. Prior research, which has focused primarily on revolving debt repayment, has identified two account features that appear to drive consumer debt repayment decisions: the interest rate and account balance. We extend this investigation into the realm of installment debt and make three fundamental contributions. First, we identify a preference that influences how consumers prepay loans. We refer to this as the FIFO preference and document that consumers prioritize older versus newer debt accounts when making debt prepayment decisions. Even when differences in other key parameters (e.g., interest rates, outstanding balances) indicate that it is financially advantageous to prepay the newer loan, the FIFO preference can still lead consumers to prioritize older debts and therefore make a financially suboptimal prepayment allocation. We replicate these effects across different debt ages and age formats (e.g., “four years ago” and “originated in April 2024”), and different prepayment sources (windfall, recurring budget slack, and savings).

We also provide an explanation for why this effect emerges. It is well known that consumers often allocate resources in a way that disproportionately favors previous investments of time, money, or effort, a phenomenon widely known as the sunk cost effect or sunk cost fallacy (Arkes and Blumer 1985; Garland 1990; Garland and Newport 1991; Soman 2001). We propose that consumers also invest significant effort (mental or physical work and energy) in repaying debt. For example, consumers must ensure that their accounts are in good standing, and they have to make any necessary adjustments to their budgets to guarantee that they are able to make their regular monthly payments. We contend that the cumulative effect of sustained effort that has already been expended in repaying an older debt causes older debt to be prioritized when consumers make prepayment decisions.

Finally, we describe three different manipulations that attenuate FIFO preference. First, we identify a debt repayment feature that reduces the relative invested effort consumers feel they have expended toward their debt accounts, which in turn attenuates FIFO preference. Specifically, consumers who have opted for automatic versus manual repayments feel they have invested less effort toward their older debt and allocate less toward prepaying their older versus newer debt. Second, we describe how shifting consumers’ focus from time foregone to time remaining shifts their focus from invested effort to remaining effort and lessens their allocations to older debts. Third, we identify a decision aid that can help attenuate FIFO preference. Specifically, tools and communications that inform consumers of their interest savings from different loans as a function of varying prepayment amounts can aid consumers in making debt prepayment decisions that are more advantageous for consumers’ own financial well-being.

Practical Implications

This research also offers practical implications for both consumers and financial professionals. Because of amortization, which allows a debt to be repaid over a set period of time in equal installments, consumers’ debt portfolios often consist of multiple debt accounts that vary in age. When consumers are able to make prepayments on their debt accounts, prepaying older debt accounts first offers the benefit of aligning financial outcomes (debt prepayment) with the effort consumers feel they have already invested in their older debt. However, it often comes at the financial cost of reducing the total interest consumers end up paying on their debt accounts to a lesser extent than prepaying newer debt first; prepaying newer debt first will incur the greatest financial savings, unless there is a significant interest rate, initial balance, or repayment term differential. While individual consumers must make these trade-offs for themselves, the general propensity to prioritize older debt suggests that such trade-offs may not be occurring adequately.