Abstract

Understanding what drives risk-taking is fundamental for the study of choice under uncertainty. One widely discussed question is when and why people engage in risk-taking. Prior work finds evidence for an ending effect, where risk-taking increases on the last gamble in a series when outcomes are immediately realized. The authors test whether socially ubiquitous end-of-period temporal landmarks (e.g., last day of the work week, month, year) alter financial risk-taking even when outcomes are not immediate. Using data from a large peer-to-peer investment platform in the United States, they show that investors make riskier financial investment decisions on Fridays relative to those made earlier in the week. Consistent with a broader end-of-period effect, risk-taking also increases on the last day of the month, on the last day of the year, and on weekdays prior to a long weekend. Follow-up lab experiments identify a novel mechanism driving ending effects: As people near the end of a temporal period, they feel more optimistic that their financial risks will pay off, driving greater financial risk-taking. The shift in risk-taking is not without consequence: In this specific peer-to-peer context, the authors show that end-of-period investments perform worse over time, losing money relative to investments made on other days.

Understanding what drives risk-seeking is fundamental for the study of choice under uncertainty. A widely discussed question is when and why people engage in risk-taking. Previous work shows that risk-taking is influenced by how choices are framed (Kahneman 1979; Tversky and Kahneman 1985), whether individuals have experienced a recent loss (Imas 2016), and situational factors, such as whether individuals feel socially supported or excluded (Duclos, Wan, and Jiang 2013; Hsee and Weber 1999). In addition, there is evidence for an ending effect, where individuals are more likely to bet on long shots at the last race of a day of horse racing and choose riskier options on the last gamble in a series of gambles (Ali 1977; McKenzie et al. 2016; Xing et al. 2019). Prior work has attributed ending effects to a desire to break even or to chase an emotionally satisfying ending. Less is known about whether ending effects extend to more ubiquitous endings, such as the last day of the week or last day of the year. Moreover, most financial decisions do not come to fruition over a single day or betting session. Financial decisions may take weeks or even years before outcomes are fully realized.

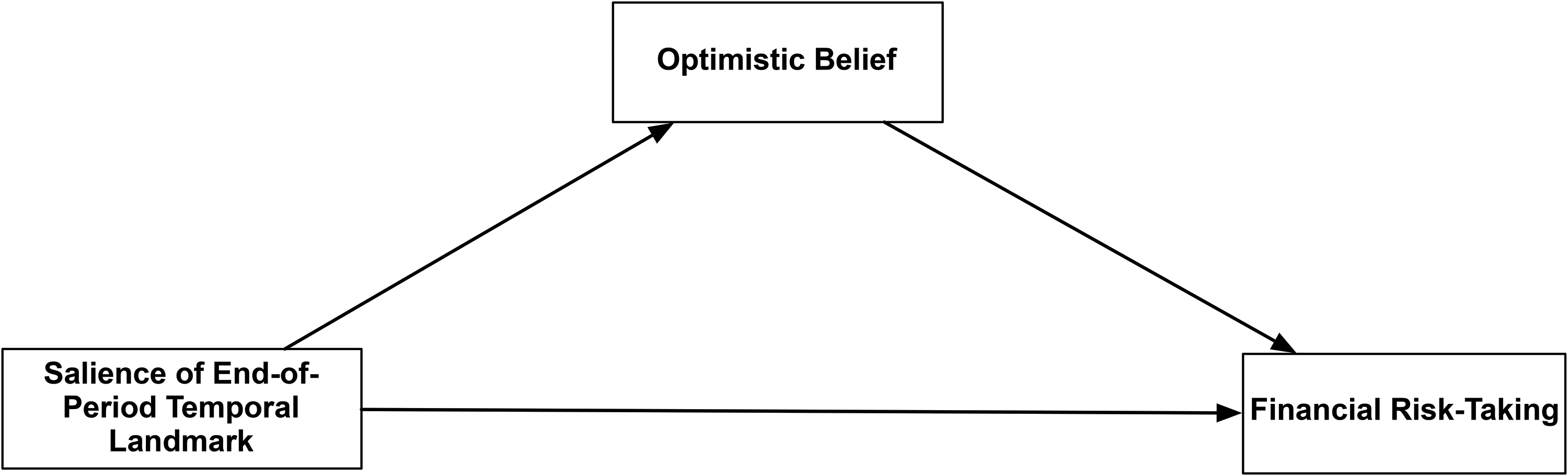

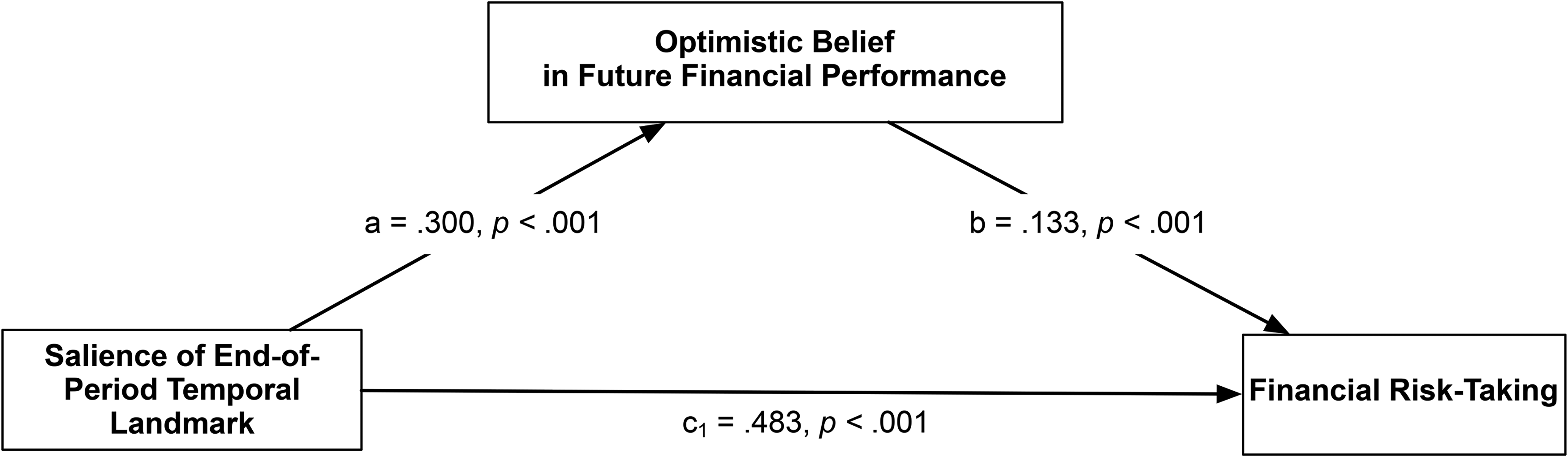

Consumers make choices at different time points of a temporal period (e.g., week, month, year). Previous studies have shown that as one time period ends, individuals often become more optimistic about the future and look forward to a fresh start from a new temporal period (Koo et al. 2020; Peetz and Wilson 2013, 2014; Ungemach, Stewart, and Reimers 2011). This raises a few questions: Are people more inclined to choose riskier investments if they make decisions at the end of the work week, month, or year? Do ending effects influence financial risk decisions when outcomes are longer term? We propose that the timing of when consumers make risk decisions may impact how likely they are to take risks. Building on research on mental accounting, we posit that as the end of a temporal period becomes salient, people are more optimistic and believe that their financial risks will pay off, which leads to greater financial risk-taking propensity (see Figure 1 for our theoretical model).

Theoretical Model.

We test our theoretical model using a mixed-method approach. First, we leverage data from one of the largest peer-to-peer (P2P) investment platforms in the United States, Prosper Marketplace, Inc. (hereafter Prosper). We observe more than five million investment decisions by lenders on the platform during a three-year period. The breadth of our dataset affords the ability to control for individual differences across investors, time- and geographic-based fixed effects, and supply-side and demand-side influences, for example, the availability of loans and overall bidding activity. We find that individuals engage in greater financial risk-taking at the end of a work week, end of a month, and end of a year. We use follow-up laboratory experiments to investigate the mechanism underlying these effects. Through both measurement and manipulation, we find that salient end-of-period temporal landmarks increase optimistic beliefs, leading people to believe that their investments will have a higher probability of success, subsequently leading to a greater likelihood of investing in options that have higher potential returns, but are also financially riskier.

This article makes four main contributions. First, we demonstrate that ending effects increase risk-taking even when outcomes are not immediately realized. Prior work attributes the ending effects to attempts to break even and recoup losses from earlier in the betting period (Ali 1977; McGlothlin 1956) and to chasing a satisfying ending (McKenzie et al. 2016; Xing et al. 2019). These psychological accounts imply that ending effects will only occur when the outcomes of risk decisions are immediately realized. However, there are many contexts where the outcome of a decision may not come to fruition for days, weeks, or even months down the line. For example, in our setting, lenders must wait at least several months following their investment decision. Positive returns from a loan (principal plus interest) will typically occur two years after the initial investment was placed. Losses from defaulted loans occur following three consecutive months of missed borrower payments. In contrast to prior work, the ending effects we observe are less likely to be driven by investors attempting to break even or have a financially rewarding ending. Our findings open the door for novel mechanisms underlying ending effects and, at a broader level, advance the understanding of what factors drive risk-taking.

Second, we demonstrate that the ending effect can apply to end-of-period temporal landmarks. As mentioned previously, previous work finds that individuals are more likely to take risks at the end of a series of gambles, or bet on long shots for the last race of the day. Our work is able to show that even frequent and common socially constructed endpoints, such as the last day of the work week or last day of the month, can affect risk-taking and decision-making as well. Considering that 17.5% of days can be classified as end-of-period temporal landmarks, identifying temporal variations in risk-seeking behavior is important, both theoretically and substantively.

Third, we shed light on a potential mechanism underlying the ending effects. We use survey data and laboratory evidence to document the underlying role that optimism plays in end-of-period financial risk-taking. Specifically, we show that the increased financial risk-taking at end-of-period temporal landmarks is at least partially driven by increased optimistic beliefs that one's financial risks will pay off. Consistent with Loewenstein (1987) and Sharot (2011), as well as research on fresh starts (Dai, Milkman, and Riis 2014, 2015; Koo et al. 2020), we find that as people near the end of a temporal period, they feel more optimistic. Specifically, we find that people are more optimistic that their financial risks will pay off, driving them to increase financial risk-taking.

Fourth, we contribute to the growing research on the role of temporal landmarks on behavior. Temporal landmarks have a meaningful effect on perceptions and behavior (Rajagopal and Rha 2009; Soman 2001). Prior work, however, has focused primarily on beginning-of-period temporal landmarks (e.g., the start of a new year or new academic semester). This line of literature has also focused on how temporal landmarks can increase outcomes related to motivation, self-improvement, and aspirational goal pursuit (Dai, Milkman, and Riis 2014, 2015). Instead, we focus on how end-of-period temporal landmarks affect financial risk-taking. In our P2P setting, we find that end-of-period investments result in significantly worse returns relative to investments made on other days.

Our findings have important implications for consumer welfare and marketing practice. We observe that an increase in risk-taking on end-of-period days can negatively impact investors, lowering their rate of returns. However, greater risk-taking may urge overly cautious investors to invest in financial options that may be profitable over time (e.g., a bull stock market). In other contexts, end-of-period landmarks may increase the likelihood of trying a new product or signing up for a new hobby.

Conceptual Framework

Temporal Landmarks Create Distinct Mental Account Brackets

Contrary to classic economic theories of choice, extant evidence shows that time is not treated as a continuous and fungible resource (Rajagopal and Rha 2009; Soman 2001). Instead, people use specific time points, like the start of a new week, month, and year, as temporal landmarks to help structure cognitive processes and perceptions (LeBoeuf, Williams, and Brenner 2014; Shum 1998; Soster, Monga, and Bearden 2010). Just as physical landmarks or prominent objects help individuals organize and orient themselves spatially, temporal landmarks and prominent calendar dates serve as reference points for how time is organized.

Temporal landmarks operate by creating distinct segments or “chunks” (Tu and Soman 2014) that demarcate the end of one time bracket and start of a new time bracket (Dai, Milkman, and Riis 2014). Temporal bracketing has important implications for understanding and predicting consumer perception and behavior. Previous work in mental accounting has shown that the attractiveness of a choice can vary as a function of choices made earlier (Read, Loewenstein, and Rabin 1999). Choices made within the same temporal bracket tend to have more of an influence on subsequent choices relative to those that were made in a different temporal bracket. Take snack choices, for example. People are more likely to seek variety between choices within the same work week (e.g., Monday's snack choice vs. Thursday's choice) relative to choices made across two weeks (e.g., Friday's snack choice vs. Monday's choice). The temporal brackets are perceived differently in this example, despite the temporal distance being equivalent.

The end of a mental accounting period and temporal bracket can also affect risk-taking. Using betting data from horse races, McGlothlin (1956), Kahneman (1979), and Ali (1977) observe that bettors who experience losses earlier in the day are more likely to try to break even by betting on long shots for the last race of the day. These findings are consistent with prospect theory: Risk-taking is reference dependent (Kahneman 1979; Schmidt 2003; Thaler and Ziemba 1988). Risk propensity is a function of the outcomes of decisions made earlier in the temporal period (Ali 1977; Moher and Koehler 2010).

More recently, studies show that individuals are prone to ending effects, increasing risk-taking propensity at the end of a series of gambles (McKenzie et al. 2016; Xing et al. 2019). These effects have been shown to be reference independent, occurring regardless of how much was either won or lost in previous rounds. Some work has documented that people engage in increased risk-taking at the end of a risky decision task due to the motivation for an emotionally rewarding ending (Xing et al. 2019). Specifically, it is more emotionally rewarding to choose an option that could earn more money, even if the option is riskier.

While prior work suggests that endings can alter decision-making and risk-taking behavior, past evidence has focused predominantly on a single betting day or laboratory session. In these cases, outcomes of the risk-taking decision are immediately realized. This raises two natural questions: Might other landmarks or points in time—for example, the end of a work week or the last day of the month—also trigger people to take more risks? Is risk-taking still affected when the outcomes will not be immediately realized? Determining whether ending effects persist even when the outcomes are not immediately realized is particularly relevant in financial contexts as many investment choices take several days, or even months, to come to fruition. Identifying significant end-of-period effects in contexts that have longer-term outcomes opens up the possibility that other mechanisms may also drive ending effects.

Temporal Landmarks, Optimism, and Financial Risk-Taking

Optimism is defined as having an expectation that future events will be favorable (Carver, Scheier, and Segerstrom 2010). Those who are optimistic tend to have a positive outlook for the future, expecting that good things will happen, while those who are pessimistic have a negative outlook, expecting bad outcomes to occur (Carver, Scheier, and Segerstrom 2010; Scheier, Carver, and Bridges 2001). Trait-level optimism has been shown to affect mood, motivation, career success, and personal relationships (for a review, see Carver and Scheier [2014]). Optimists tend to anticipate that positive events will occur sooner and more frequently for them in comparison to others (Sharot 2011). Optimists also are more likely to discount negative events and overcome minor setbacks more quickly. In the context of financial decision-making, optimists are more likely to invest their money, and allocate a higher percentage of their money to riskier financial options, such as stocks (Angelini and Cavapozzi 2017; Malmendier and Tate 2005; Puri and Robinson 2007). Optimists are also more likely to expect and maintain positive expectations when gambling and tend to be overconfident about their potential returns (Gibson and Sanbonmatsu 2004; Malmendier and Tate 2005).

Prior work on optimism has focused largely on the role of dispositional and trait-level optimism (e.g., Carver and Scheier 2014). Yet, there is evidence that optimism also has a state-level component where positive expectations can fluctuate depending on the specific context or situation (Burke et al. 2000). Individuals who feel greater state-level optimism are more likely to have positive expectations regarding their future and believe that positive events are more likely to occur for themselves relative to others. While trait optimism is considered a more stable component relating to more general outcomes, state-level optimism is more dynamic, and can change the extent to which positive expectations are formed for more contextual and issue-relevant outcomes (Kluemper, Little, and DeGroot 2009).

Recent evidence shows that temporal landmarks can affect state-level optimism. Temporal landmarks can create distinct psychological separations from past, present, and future selves (Dai, Milkman, and Riis 2014, 2015). New temporal periods offer a perceptual “fresh start” or clean slate, separating a person from their past imperfections or failures. Even anticipating a future landmark, such as the start of a new week or month, can increase feelings of optimism in the present (Koo et al. 2020; Loewenstein and Elster 1992; Ungemach, Stewart, and Reimers 2011). Consistent with these findings, Koo et al. (2020) find that anticipating a new period can lead people to optimistically believe that their future self will be successful at pursuing and achieving goals.

Though previous work has focused on how the anticipation of temporal landmarks can trigger individuals to feel more optimistic, less is known about whether socially constructed end-of-period temporal landmarks affect optimism. To explore whether state-level optimism could vary across the week, we first ran a preliminary survey. We asked people (N = 591) to rate the day of the week on which they felt most optimistic (Monday to Sunday; for full details, see Web Appendix A). Out of the 588 respondents, 43.0% listed that they felt most optimistic on Fridays. No other day received more than 16% of responses: Monday, 15.8%; Tuesday, 5.3%; Wednesday, 4.4%; Thursday, 9.7%; Saturday, 13.4%; and Sunday, 8.3%. Using a different sample of respondents (N = 396), we ran a follow-up survey in which respondents could select a no-choice or “all days are about the same” option. Once again, Friday (36.7%) was selected as the day when people felt most optimistic (see Web Appendix A). The results provide preliminary evidence that situational contexts even as frequent as the last day in a work week may increase state-level optimism.

Beyond motivation and aspirational goal pursuit, it is possible that the relationship between temporal landmarks and optimism may also affect other consequential behaviors. In this article, we focus specifically on the role of salient end-of-period temporal landmarks in financial risk-taking. We posit that when ends of periods are salient, people are more optimistic that their financial risks will pay off, subsequently affecting risk perceptions and financial risk-taking propensity. In the next section, we provide empirical support for our theoretical framework using secondary data evidence from the largest P2P lending platform in the United States. We combine our secondary data analysis with two laboratory experiments to establish a more causal relationship between our constructs of interest.

Study 1: Field Study of P2P Lending

Data

Our primary dataset comes from Prosper, the first P2P lending marketplace in the United States. Prosper provides a platform for borrowers to obtain small, unsecured personal loans from individual lenders. 1 Relative to other lending alternatives, Prosper loans are funded faster and required less paperwork than typical small personalized bank loans (Van Doorn 2016). Prosper also offers more competitive rates on average than credit cards, making it an appealing option for borrowers (Van Doorn 2016).

All Prosper loans are fixed rate, unsecured, and fully amortized with simple interest. During our sample period, borrowers could request anywhere from $2,000 to $25,000 per loan. Before a borrower is able to list a loan on the platform, they must go through a verification process. The platform verifies the borrower's social security number and driver's license number, and pulls a credit history report from Experian, which includes historical credit information such as the borrower's income, total number of delinquencies, mortgage, monthly debt, and so forth. Borrowers who pass the verification and credit qualification process are permitted to post a loan listing. We use the terms “listing” and “loan application” interchangeably in this study.

Our dataset contains all listing and bidding data from November 9, 2005, to October 14, 2008. The data include information regarding the listing and borrower, as well as the specific time when bids are made. During this time period, Prosper operated in an eBay-style auction system in which lenders and borrowers together determined the effective loan rate. Specifically, a borrower sets the maximum interest rate they can accept (i.e., reserve interest rate). The reserve interest rate can also signal the borrower's creditworthiness (Kawai, Onishi, and Uetake 2022). Intuitively, borrowers who set a very high reserve interest rate tend to have more difficulty borrowing from other sources. Lenders will be concerned about the borrower's repayment ability, and will subsequently ask for a higher interest rate to compensate for the risk. We will verify this point in the next section. As in many other financial markets, high reward is related to high risk in the P2P lending market. During our sample period, roughly 37% of all loans were in some form of delinquency.

In addition to the reserve interest rate, borrowers have the option to include other information, such as a description of themselves, the purpose of their loan, and how they intend to repay the loan. They can also provide a photograph of themselves. Prosper posts the information provided by the borrower along with the borrower's financial history information (e.g., income, delinquencies in the past) with the listing. Lenders can observe all this information and then decide which listings they want to make a bid on. When submitting a bid, lenders specify both the lowest interest rate that they would accept (i.e., the lender interest rate, which is typically below the reserve interest rate) and the bid amount (in U.S. dollars) that they are willing to contribute above the minimum investment of $50.

This P2P platform provides a compelling setting to investigate our research question for a number of reasons. First, and perhaps most importantly, the dataset has information on how each individual invests on the platform, affording the ability to control for each lender's prior risk decisions as well as their past performance on the platform. Second, the dataset provides information on the precise day and time when investors make decisions, which can help us determine whether end-of-period temporal landmarks are particularly associated with an increase in financial risk-taking relative to non-end-of-period time points. Third, the breadth of the dataset enables us to control for supply-side and demand-side influences, such as the availability of loans and number of competing bids. We are also able to ensure that our results are robust to variations across lenders, differences due to month or year, and differences across geographical locations. Finally, we are able to observe the realized outcome of all loan applications in our dataset (i.e., whether funded loans are fully paid back or whether they default). We can, thus, compare the return rates of investments at end-of-period time points relative to non-end-of-period time points. In the following sections we summarize our final sample and describe our model and analytic strategy.

Variables, Sample Construction, and Summary Statistics

To create our final dataset, we clean the raw data in several steps. First, we drop observations that are missing key information, such as the interest rate of the bids. Next, we drop lenders who have made fewer than 50 bids, 2 allowing for multiple observations for each investor. Doing so enables us to construct measures of the lender's investment experience and past risk preference, providing us with additional within-individual variations in addition to cross-sectional variations. This enables us to better identify the effect of interest. Finally, we combine our dataset with market activity outside of the platform using standard market-level variables of interest, including the average interest rate for a 30-year fixed mortgage, the TED spread (which is an indicator for perceived risk and volatility in the general economy), and the S&P 500 market closing quote from the previous day. The final sample contains 5,278,367 bids submitted by 21,873 lenders. The variables we use in our study are described in detail in Web Appendix Table B1. On average, lenders made 195.2 bids during our sample period, chose loans with an average reserve interest rate of 20.50%, and bid $90.08 per loan.

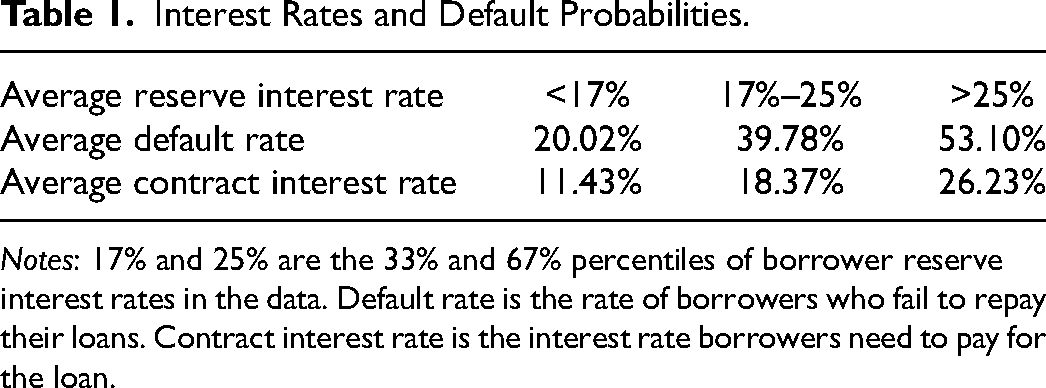

To measure a lender's risk preference, we use the reserve interest rate of the listings the lender selects to bid on. Key to our analysis is the assumption that a listing with a higher reserve interest rate is, in fact, associated with greater risk (i.e., higher default probability). To ensure that this is, indeed, a valid assumption, we examine the default probability as a function of the listing's reserve interest rate during our sample period. Table 1 shows the relationship between the listing reserve interest rate and default probability. On average, borrowers who set their reserve interest rate below 17% default 20.02% of the time. In comparison, borrowers who set the reserve interest between 17% and 25% default 39.78% of the time, while the default rate is 53.10% for those borrowers who set the rate above 25%. These patterns are consistent with other work using Prosper data (e.g., Kawai, Onishi, and Uetake 2022).

Interest Rates and Default Probabilities.

Notes: 17% and 25% are the 33% and 67% percentiles of borrower reserve interest rates in the data. Default rate is the rate of borrowers who fail to repay their loans. Contract interest rate is the interest rate borrowers need to pay for the loan.

Row 3 of Table 1 shows that, consistent with these patterns, the average contract rate (the interest rate a borrower pays on a loan) is higher for borrowers who set their reserve rate higher. The average contract interest rate ranges from 11.43% for loans with a reserve interest rate lower than 17% to 26.23% for loans with a reserve interest rate higher than 25%. Therefore, similar to other financial markets, choosing a higher interest rate option is associated with greater potential returns if loans are paid back in full but also poses a greater risk for default, validating our key measure of interest.

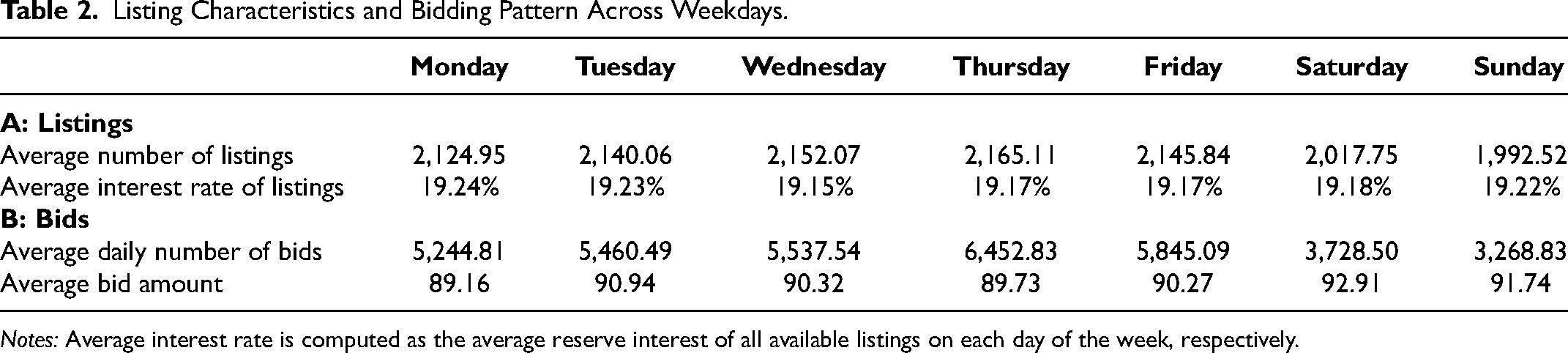

We describe platform activity and bidding activity as a function of the day of week in Table 2. We look at platform activity in terms of the number of available listings across each day of the week. Row 1 of Panel A of Table 2 presents the average number of listings on each weekday. We do not observe any statistically significant differences in the average number of listings from Monday to Friday. However, the number of available listings is significantly lower on weekends. This finding means that the supply side is stable from Monday to Friday (i.e., lenders have almost the same number of listings to bid on). However, lenders’ choice set is limited on weekends.

Listing Characteristics and Bidding Pattern Across Weekdays.

Notes: Average interest rate is computed as the average reserve interest of all available listings on each day of the week, respectively.

Next, we examine whether the volume or frequency of bidding varies across weekdays. Row 1 of Panel B of Table 2 presents the average number of bids submitted as a function of the day of the week. Again, we find that the number of bids submitted from Monday to Friday is relatively stable. However, the number of bids submitted on weekends is significantly fewer. In other words, the demand from lenders is stable from Monday to Friday, but significantly lower on weekends.

The results in Table 2 reveal two key patterns. First, we observe that borrower and lender behavior on weekends is quite different from the behavior on weekdays. Borrowers are significantly less likely to post loan listings on weekends relative to weekdays (MWeekend = 2,005.14 listings, MWeekdays = 2,139.61 listings, t = −1.97, p = .048). Lenders are also less likely to submit bids on weekends relative to weekdays (MWeekend = 3,499.46 bids, MWeekdays = 5,707.36 bids, t = −12.20, p < 001). Both investment activity trends suggest that weekend investment decisions may be systematically different from working weekday investment decisions. As a result, we present our main results both inclusive and exclusive of weekends, but focus most of our attention on days during the work week.

Second, looking at weekdays alone, we observe no differences in the average number of listings or bids on Fridays relative to other weekdays (number of listings: MFridays = 2,145.84 listings, MMon–Thurs = 2,146.63 listings, p = .98; number of bids: MFridays = 5,845.09 bids, MMon–Thurs = 5,673.10, p = .61). Thus, there is initial evidence that differences in bidding behavior across weekdays is not solely attributable to differences in the number of listings available (i.e., supply-side variation) or to bidding activity (i.e., demand-side variation) on Fridays compared with other weekdays. Nevertheless, we include various controls in our analyses to account for supply-side and demand-side variation across days.

Model and Analytic Strategy

Next, we detail our analytic strategy and then present evidence consistent with our main hypothesis that lenders bid on listings with higher reserve interest rate at the end of a week or on the last day in a period. We use a linear regression model to identify the end-of-period effects on lenders’ risk-taking behavior. Our baseline specification is as follows:

Our parameter of interest, β, estimates the end-of-period effect on lenders’ risk-taking decisions. End of Periodt takes the value 1 if the bid is placed on a day that is considered an end-of-period temporal landmark (i.e., Friday, Wednesdays, and Thursdays prior to public holidays, and the last day of the month or year) and 0 otherwise. In addition, we include Xit, which is a vector of variables that capture lender-specific, time-variant controls. In particular, Xit includes the average reserve interest rate of all listings that lender i has placed a bid on prior to period t, which controls for a lender's baseline time-variant risk-taking preference. We use the number of previous bids made by lender i before period t as a proxy for the lender's experience. We also construct variables to capture the dollar value of recent monetary losses (Recent Week Lossit) or recent monetary gains (Recent Week Gainit) that lender i has experienced in the previous weekdays of the same week before period t, respectively. For instance, if the current period is a Friday, then we calculate the lender i's monetary gains and losses from Monday to Thursday earlier in the week. Doing so reduces the likelihood that same period gains or losses underlie potential effects. These variables are included as separate controls in our Xit vector parameter. We make sure to cluster errors at the lender level to account for serial correlation in our dependent variable (Bertrand, Duflo, and Mullainathan 2004).

Borrower-side controls

Another factor that could affect financial risk-taking is properties of the loan listing itself. It is possible that lenders are influenced by certain listing attributes such as the amount of the loan, a borrower's income, occupation, race, reason for the loan request, whether a photo is included, or geographic proximity relative to the lender (Iyer et al. 2016; Lin and Viswanathan 2016). Thus, we include k

l

, which is a vector of listing-specific attributes to absorb any borrower-specific listing effects. Specifically, k

l

includes the listing amount, whether the listing contains a photo, and specific borrower characteristics including borrower monthly income, borrower monthly debt, borrower occupation, whether the borrower is a homeowner, an indicator variable for whether the borrower and lender are from the same state (i.e., home bias), and whether the borrower belongs to a borrower group.

3

Our enhanced regression specification is as follows:

Platform and economic controls

A lender's investment decision may also be affected by the other listings available on the platform, how many people are bidding, and the economic environment. Thus, we include ϕt to control for variation in listing supply, lender competition, and market performance outside of the platform at particular time points. The term ϕt includes the average reserve interest rate of all available listings, and the number of listings that have a low interest rate (i.e., the lowest tercile of all loans listed during our sample period), moderate interest rate (i.e., the middle tercile), and high interest rate (i.e., highest tercile). This term also includes controls for demand-side variation like the daily number of bids submitted in period t. We control for market activity outside of the platform using standard market-level controls: the average interest rate for a 30-year fixed mortgage in the United States, the TED spread, and the S&P 500 market closing quote from the previous day.

Finally, ϕt also includes month and year fixed effects to account for any economic factors that are driven by particular economic time periods. These controls are particularly relevant as our sample period includes the boom and bust period in the years preceding and including the 2008 recession. Our most comprehensive model specification is as follows:

Main Results

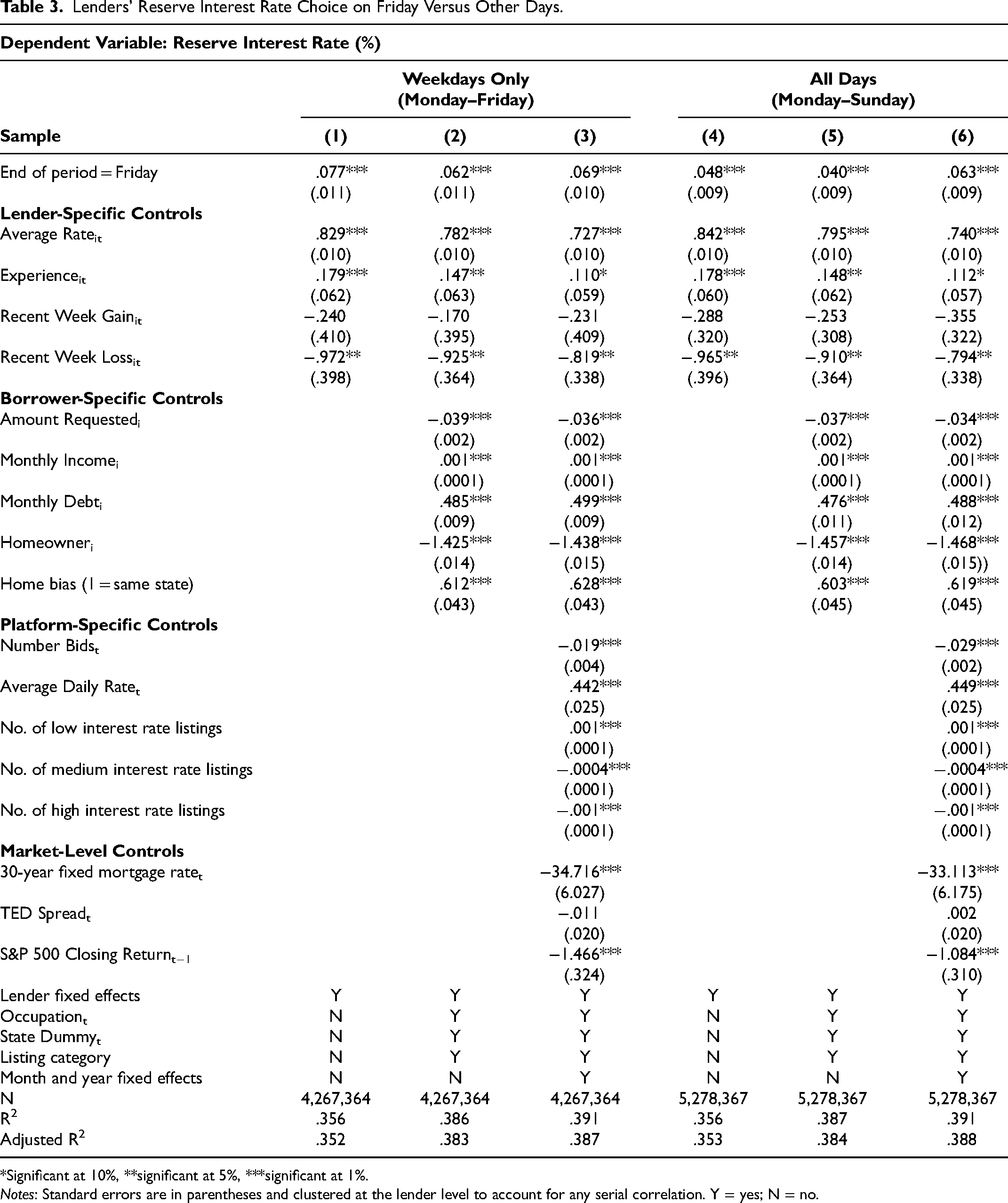

Table 3 presents our main regression results, examining whether lenders’ risk decisions vary on end-of-period Fridays relative to decisions made earlier in the week. Columns 1 through 3 focus on just weekdays and show the results for model specifications 1 through 3, respectively. Columns 4 to 6 present results for model specifications 1 through 3, respectively, where the sample is expanded to weekdays and weekends.

Lenders’ Reserve Interest Rate Choice on Friday Versus Other Days.

*Significant at 10%, **significant at 5%, ***significant at 1%.

Notes: Standard errors are in parentheses and clustered at the lender level to account for any serial correlation. Y = yes; N = no.

In the baseline specification, Column 1, we test our effect inclusive of lender-specific controls and lender fixed effects. We find that bids made on Friday are associated with a .077% (SE = .011, p < .001) higher reserve interest rate in comparison to bids made earlier in the week. In Column 2, we include borrower-side controls as specified in model specification 2. Once again, we find that bids made on Friday are associated with a significantly higher reserve interest rate relative to those made on non-end-of-period weekdays (β = .062, SE = .011, p < .001). Finally, Column 3 reports the results of model specification 3, adding platform, economic controls, and time fixed effects to control for any supply-side, demand-side, and economic condition variations. We observe that bids made on Friday are, again, associated with higher reserve rates relative to bids made on non-end-of-period weekdays (β = .069, SE = .010, p < .001).

In Columns 4 through 6 we repeat our tests including Saturday and Sunday in our analysis. We investigate whether Fridays are associated with higher reserve interest rates relative to all other days of the week. Expanding our sample to all days in the week increases the number of total bids made by roughly 24% (1,011,003 additional bids). We find evidence of a significant end-of-period Friday effect across all three specifications (full estimates inclusive of all control variable coefficients are provided in Web Appendix C).

Robustness of Main Result

We conduct several checks to ensure that our main question of interest is robust to (1) alternative model specifications and (2) alternative end-of-period temporal landmarks.

Using Friday as the baseline

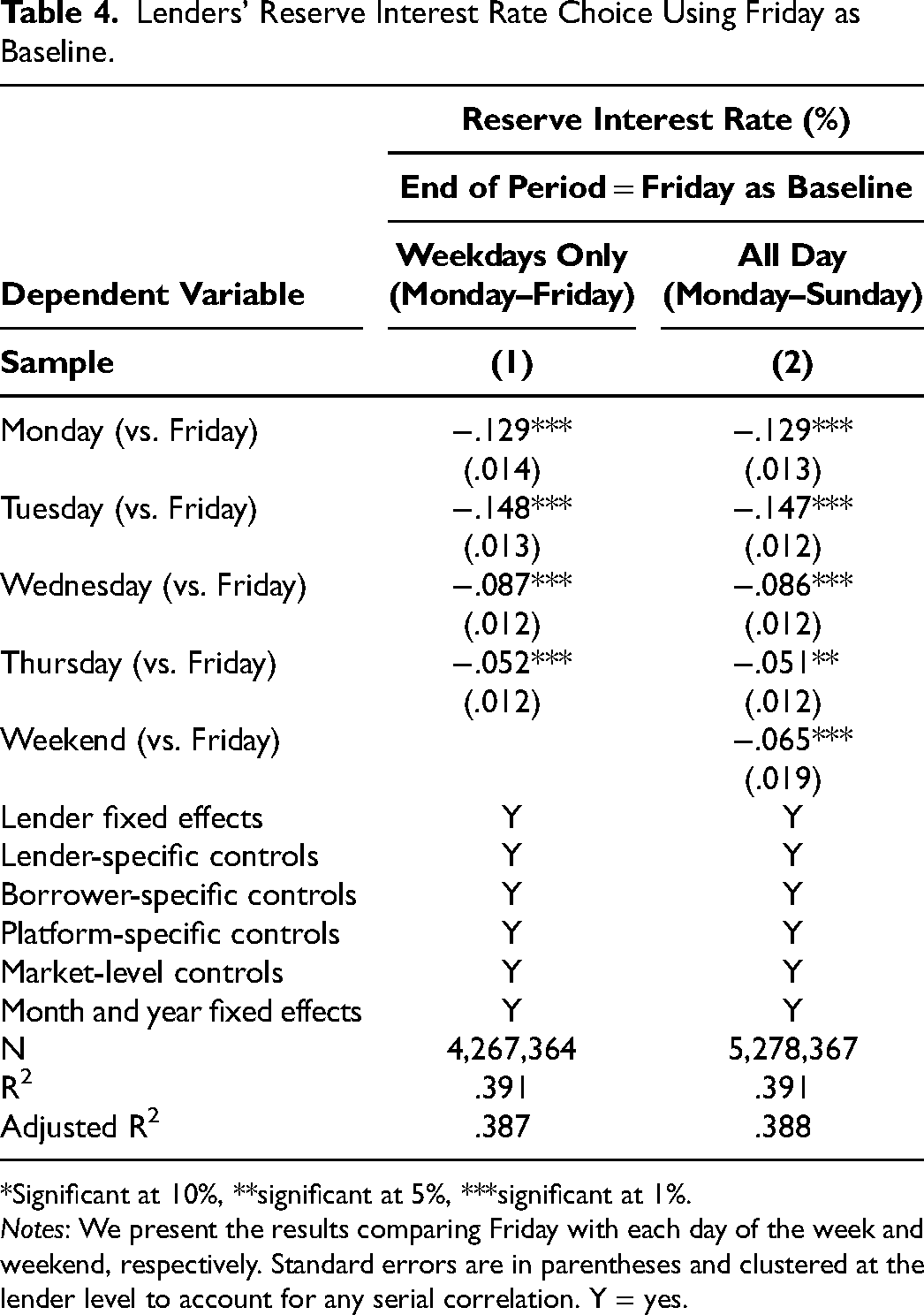

Our main results compare Friday with all other weekdays, using a combined weekday measure. However, it is possible that our effects are driven by large differences in reserve interest rate bidding on just one or two weekdays relative to Friday. Lumping all other weekdays into one comparison group may incorrectly produce a difference between Friday and all other weekdays when only one or two days are actually driving the difference. To test this possibility, we vary our preferred specification by using bids on Friday as the baseline comparison group and investigate whether investors bid on loans with significantly higher reserve interest rates on Fridays as compared with each weekday and weekend, respectively.

Table 4 presents the results of our analyses. In Column 1, we test each weekday using Monday, Tuesday, Wednesday, and Thursday dummies, where each variable takes a value of 1 if the bid was submitted on that particular day. Column 2 presents the results inclusive of both weekday and weekend dummy variables. We test whether Friday is associated with greater financial risk-taking relative to bids submitted on Saturday or Sunday. Across both tests, we find that lenders bid on loans with significantly higher reserve interest rates on Fridays, relative to other non-end-of-period weekdays, regardless of whether we exclude weekend data or not. As discussed previously and to reduce redundancy, we conduct our regression analyses using only weekday data in the following sections.

Lenders’ Reserve Interest Rate Choice Using Friday as Baseline.

*Significant at 10%, **significant at 5%, ***significant at 1%.

Notes: We present the results comparing Friday with each day of the week and weekend, respectively. Standard errors are in parentheses and clustered at the lender level to account for any serial correlation. Y = yes.

Alternative end-of-period landmarks

Next, we test whether our effects are limited only to a Friday effect, or whether this effect also applies to other end-of-period temporal landmarks. We investigate whether alternative end-of-period temporal landmarks are associated with greater financial risk-taking using three different analyses.

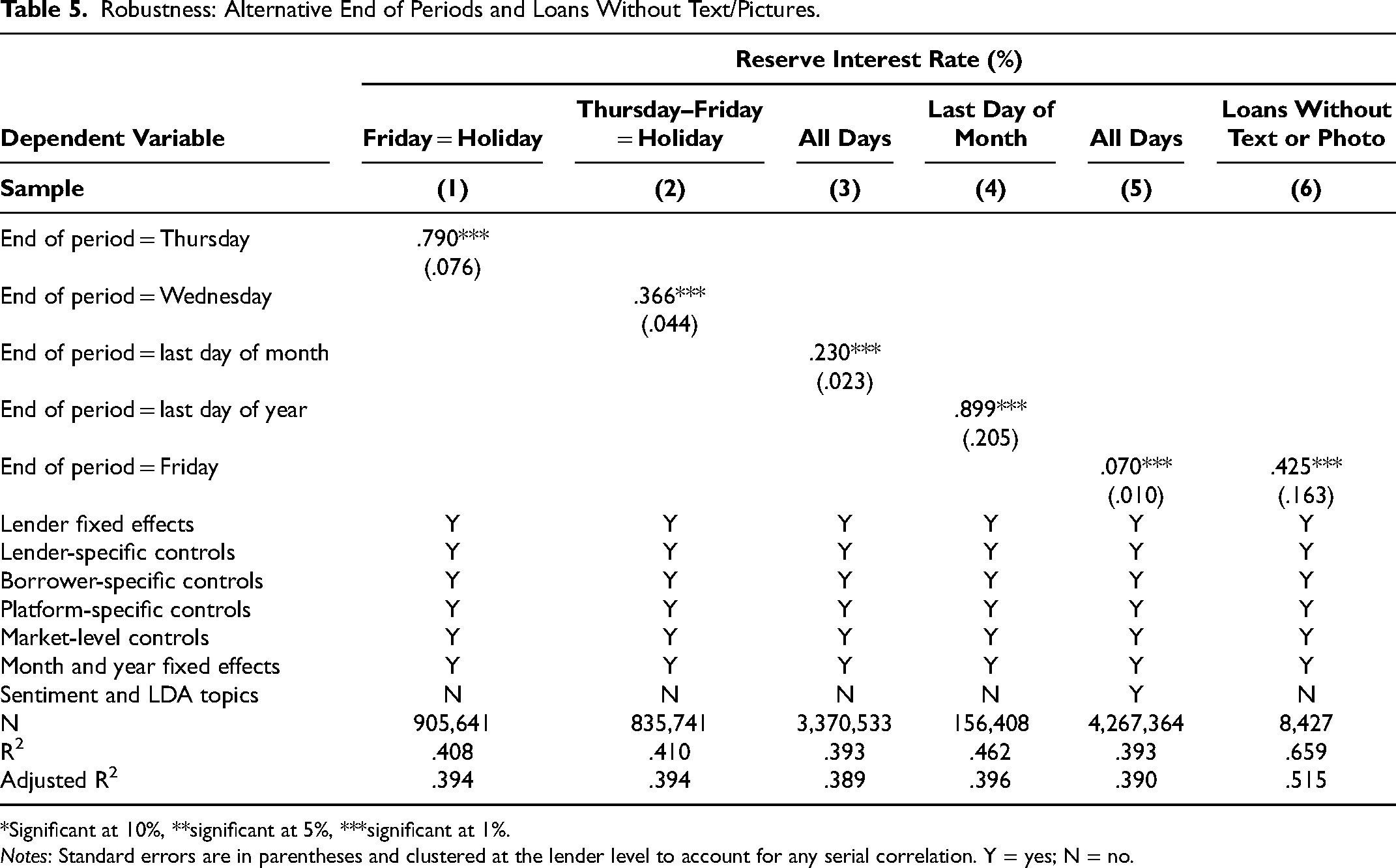

First, we investigate instances where the last day of the work week falls on either a Thursday or a Wednesday. During our sample time period, there were three instances when Friday was a public holiday, making the Thursday prior to the holiday the last day of the work week. 4 In addition, during Thanksgiving week, both Thursday and Friday are typically considered holidays. The Wednesday prior to Thanksgiving is now typically thought of as the last day of the work week. 5 If our effect is limited to just a Friday effect, then we should see no evidence that financial risk-taking is affected on these alternative, end-of-period Thursdays or Wednesdays relative to typical Thursdays and Wednesdays, respectively. However, if our effects are consistent with a broader end-of-period effect, then we should observe greater financial risk-taking by lenders during these salient end-of-period Thursdays and Wednesdays prior to a holiday. We present our results comparing end-of-period Thursdays and Wednesdays to typical Thursdays and Wednesdays in Columns 1 and 2 of Table 5. We show that lenders bid on loans with .79% higher reserve interest rates on end-of-period Thursdays (SE = .076, p < .001) and .366% higher reserve interest rates on end-of-period Wednesdays (SE = .044, p < .001) relative to typical Thursdays or Wednesdays.

Robustness: Alternative End of Periods and Loans Without Text/Pictures.

*Significant at 10%, **significant at 5%, ***significant at 1%.

Notes: Standard errors are in parentheses and clustered at the lender level to account for any serial correlation. Y = yes; N = no.

In our second test we investigate the relationship between end-of-month landmarks and financial risk-taking relative to other days in the month. Mental accounts are based on weekly, monthly, and yearly brackets (e.g., Soster, Monga, and Bearden 2010; Thaler 1985). Accordingly, end-of-periods temporal landmarks, such as the last day of the month or last day of the year, should also be associated with greater financial risk-taking. We test whether end-of-month and end-of-year temporal landmarks are associated with greater risk-taking, making sure to exclude all Fridays and end-of-week Wednesdays and Thursdays to reduce any variance explained from our previous results. Column 3 of Table 5 presents our results. Consistent with an effect that is driven by end-of-period temporal landmarks more broadly, we find that lenders are significantly more likely to bid on listings with higher reserve interest rates on the last day of the month relative to earlier in the month (β = .230, SE = .023, p < .001).

It is possible that our end-of-week and end-of-month results are driven by payday effects. Weekly or biweekly paychecks are commonly issued on the last day of the work week or on the last day of the month. 6 Unfortunately, we do not have access to lenders’ paycheck information or banking information that might allow us to observe when lenders receive a positive income shock. However, it is possible to test whether stronger, more salient end-of-period time points, such as the last day of the year, are associated with greater financial risk-taking even relative to other end-of-month landmarks (Dai, Milkman, and Riis 2014; Koo et al. 2020).

In our third test, we test whether a more salient end-of-period landmark, such as the end of the year, is associated with greater financial risk-taking propensity in comparison to other end-of-month temporal landmarks (e.g., January 31, November 30). If our effects are driven by payday effects alone, then we should be less likely to find differences between December 31 and all other end-of-month landmarks. Column 4 of Table 5 presents the results of our analysis. Lenders choose to invest in listings with significantly higher interest rates on the last day of the year relative to other end-of-month temporal landmarks (

Effect of loan descriptions or pictures

Previous studies have shown that the way borrowers appeal to lenders in the loan description and the pictures or photographs they attach with their loan information affect lender decision-making (Herzenstein, Sonenshein, and Dholakia 2011; Pope and Sydnor 2011). To address the possibility that the content of the loan description could impact risk decisions, we first analyze loan descriptions using a sentiment-based machine-learning analysis (Tirunillai and Tellis 2012) to quantify the overall positive and negative sentiments in each loan description (detailed information regarding this method is provided in Web Appendix D). In addition to sentiment analysis, we also implemented latent Dirichlet allocation (LDA) for each loan description to identify a set of latent topics associated with the description (Blei, Ng, and Jordan 2003; full details of the LDA estimation are provided in Web Appendix D). We include the loan description's sentiment and latent topics as control variables in the regression. Column 5 of Table 5 presents the results, and our end-of-period effect persists (β = .070, SE = .010, p < .001). To reduce the influence of loan descriptions and pictures further, we test whether our end-of-period effects are robust to restricting our analysis to a subsample of loan applications without text descriptions or borrower photos. Still, we find that our Friday effect persists (see Column 6 of Table 5).

Reference dependence

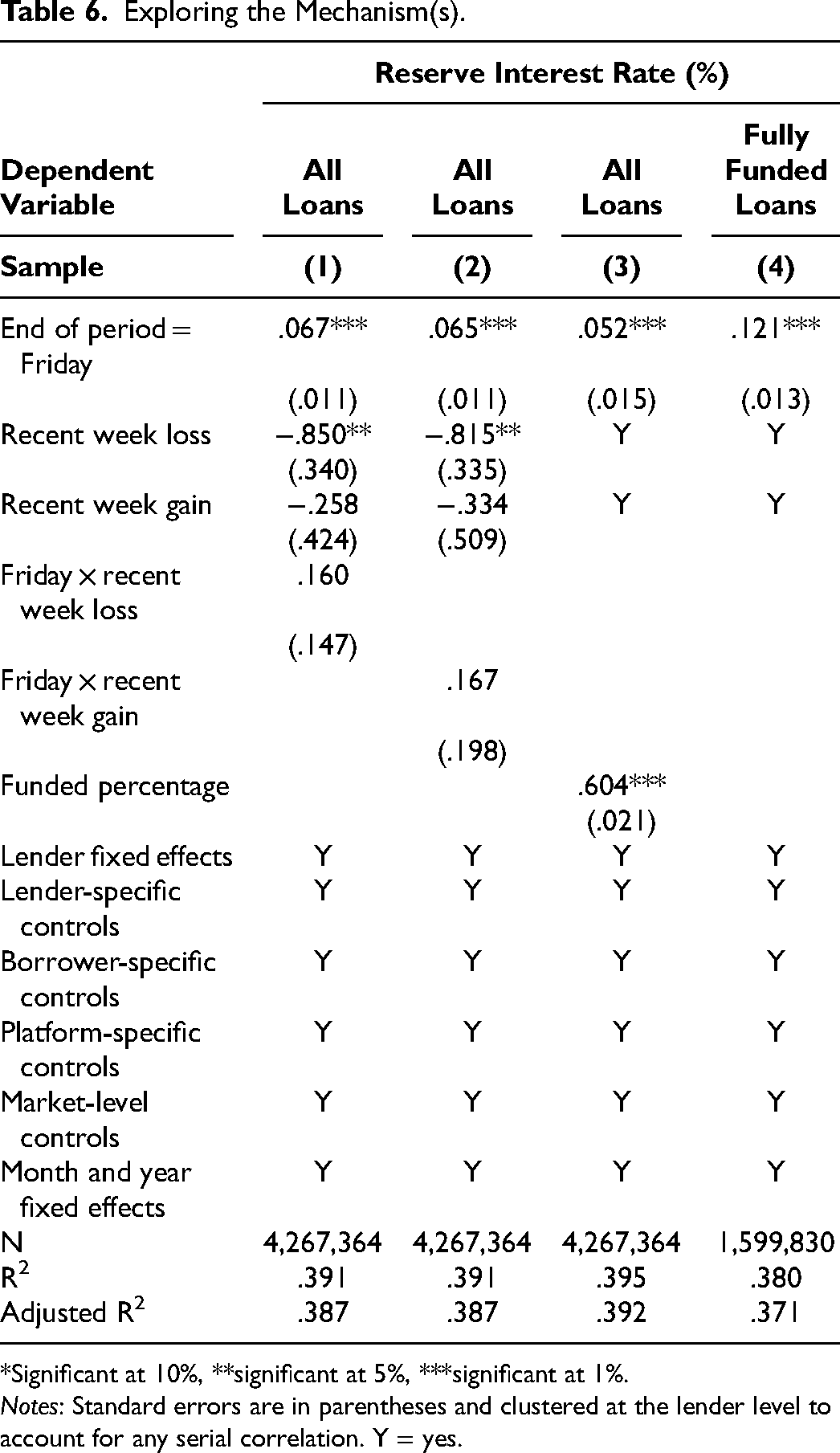

Research examining the role of mental accounting on risk-taking behavior shows evidence of an ending effect that is driven by either reference dependence (Ali 1977; Kahneman 1979; McKenzie et al. 2016) or the desire for an emotionally satisfying ending (McKenzie et al. 2016; Xing et al. 2019). Emotionally satisfying endings are less likely to be the driver in this context given that loans do not come to fruition for months or potentially years at a time. Thus, we focus on determining whether a reference-dependent account is potentially underlying our effects. If reference dependence is driving our ending effects, then lenders who experience financial losses (gains) earlier in the week should be relatively more (less) likely to show end-of-period effects. Although we include controls for gains and losses incurred earlier in the week as part of our lender-specific controls, it is still possible that financial losses or gains occurring within the same week might moderate the strength of end-of-period effects.

Column 1 and 2 of Table 6 present the results. Importantly, we do not find significant interaction effects in either regression analysis. It is less likely that reference dependence alone is driving our end-of-period effects.

Exploring the Mechanism(s).

*Significant at 10%, **significant at 5%, ***significant at 1%.

Notes: Standard errors are in parentheses and clustered at the lender level to account for any serial correlation. Y = yes.

Controlling for conformity or rational herding

We also explore whether conformity or rational herding may underlie our effect (Zhang and Liu 2012). Lenders may bid on loans that are closer to being fully funded as a way to ensure that their bid is successful. If lenders tend to conform or engage in rational herding behavior on Fridays, and the loans that are close to being fully funded are riskier options, then it is possible to observe an end-of-period effect that is driven by conformity or herding.

To address this alternative, we first add a control variable, Funded Percentage, as a way to control for the percentage of the loan application that was already funded. We once again find evidence of greater risk-taking at ends of periods (see Column 3 of Table 6; β = .052, SE = .015, p < .001).

Next, we examine whether our effect persists even using a subsample of listings that are already fully funded. During our time period, Prosper allowed lenders to continue investing even after listings were fully funded, as long as the new lender offered a lower interest rate relative to the initial lenders. Column 4 of Table 6 shows that ends of periods are still associated with greater risk-taking, even for fully funded loans (β = .121, SE = .013, p < .001).

Testing a depletion account

Previous literature has shown that cognitive resource depletion may drive individuals toward impulsive decision-making (Baumeister, Vohs, and Tice 2007; Beal et al. 2005). People may feel physically and mentally exhausted, leading to riskier decision-making. To test whether depletion could be driving our results, we take the time period at the end of the day (10:00 p.m. to 2:00 a.m., time zone adjusted) and end of the workday (4:00 p.m. to 6:00 p.m., time zone adjusted) and investigate whether financial risk-taking varies during these end-of-day time periods, relative to earlier in the day. We present our results in Columns 1 and 2 of Web Appendix Table F1. We do not find significant differences in financial risk-taking during these time periods.

Testing a payday effect account

We further investigate whether our results are driven by a wealth effect or positive income shocks from paydays occurring on end-of-period temporal landmarks. In Web Appendix F, we test whether two common non-end-of-period paydays (i.e., the first of the month and the 15th of the month) are also associated with increased financial risk-taking. In Column 3 of Web Appendix Table F1, we show that there is no evidence of significantly positive effects for either the beginning of the month or the 15th of the month. In fact, we actually observe a significantly negative effect on the 15th of the month (β = −.083, SE = .023, p < .001).

Testing a licensing or distraction account

There is also a possibility that these effects may be a result of licensing or distraction. Evidence shows that licensing may occur in instances where individuals reward themselves with an indulgent behavior after doing something good first. Licensing can subsequently change the preference among a set of alternatives as a function of choices made earlier in the time period (Khan and Dhar 2006; Merritt, Effron, and Monin 2010). Thus, lenders may be risk-averse earlier in the week, treating themselves to a riskier choice on Fridays. We account for this possibility by comparing the bids of investors who bid only on a Friday in a week relative to when these same investors bid on Fridays in weeks when they made bids on multiple days in the week. Column 4 of Web Appendix Table F1 shows that we still find a significant end-of-period effect. In Column 5 of Web Appendix Table F1, we test whether distraction may be driving results by investigating whether risk-taking increases during the lunch hour (DellaVigna and Pollet 2009). We find no evidence that end-of-period risk-taking is consistent with a distraction mechanism.

Testing a lender prosociality account

Finally, it is plausible that lenders are in a better mood on Fridays (or other end-of-period temporal landmarks), making them potentially more likely to invest in riskier loans. We use three tests to rule out this potential account. First, we look at listings where borrowers have not included a picture or any text describing the purpose of the loan (see Column 6 of Table 5). We still find a significant, and even stronger, end-of-period effect (β = .425, SE = .163, p < .001). Second, we look at the interest rates that lenders set on Fridays relative to other days in the week. Setting a lower interest rate is a prosocial action as lenders will charge lower interest from fulfilled loans relative to other lenders. Third, we investigated whether individual lenders set lower interest rates on Fridays relative to the interest rates they set on bids made earlier in the week. We do not find evidence to support a potential prosocial end-of-period effect in either analysis (see Columns 6 and 7 of Web Appendix Table F1).

Discussion of Study 1

Our secondary dataset offers preliminary evidence that end-of-period temporal landmarks (e.g., the last day of the work week or last day of the month) are associated with greater financial risk-taking. End-of-period landmarks that signal a new beginning, such as the last day of the year (e.g., Dai, Milkman, and Riis 2014), have an even higher incidence of risk-taking relative to other end-of-period landmarks. Our dataset also enables us to rule out several potential mechanisms such as reference dependence, conformity or rational herding effects, or biases that may emerge from how borrowers appeal to lenders via photos or descriptions.

It is possible that our end-of-period effects may be driven by an optimism mechanism. Anticipating an upcoming temporal landmark can increase feelings of optimism in the present. Though we are unable to directly observe investor optimism in our P2P setting, we are able to test whether investment behaviors associated with investor optimism are more likely during end-of-period temporal landmarks.

Investors who are more optimistic have a higher propensity for investing in their local equity market (e.g., Shiller, Kon-Ya, and Tsutsui 1996; Solnik and Zuo 2017). Investors tend to believe that they have better information on their local context, leading to less portfolio diversification and less variety seeking. This is consistent with research finding that optimism can increase preferences for what is psychologically more familiar (Yang and Urminsky 2015). If ends of periods increase optimism, then ends of periods should also increase investing in loans originating from the same state. Indeed, we find that lenders exhibit a stronger home bias at the end of a temporal period (see Web Appendix G for full details).

These initial results provide evidence consistent with an optimism mechanism. However, do end-of-period temporal landmarks, specifically, increase optimistic belief that financial risks will pay off? At a conceptual level, would individuals who feel more optimistic during a given time period, that is, those who have a higher level of of state-level optimism, also feel greater optimistic belief for one's financial performance? If so, is financial risk-taking affected? These questions are relevant particularly given that most of the prior work on the role of optimism in financial risk-taking has largely focused on dispositional and trait-level optimism (e.g., Baker and Wurgler 2006; Graham, Harvey, and Puri 2013; Puri and Robinson 2007). Less is known about whether shifts in state-level optimism via salient end-of-period landmarks affect optimistic belief in financial performance and subsequent financial risk-taking behavior.

In Study 2, we use a controlled experiment to test the relationship between end-of-period landmarks and optimistic belief, our proposed mediator. We test whether merely priming individuals to think of frequent end-of-period temporal landmarks, such as Friday—the last day of the work week—shifts their beliefs to be more optimistic that their financial risks will pay off. Our laboratory experiment enables us to test whether mood or happiness are also affected by Fridays relative to other days in the week. Finally, we test whether any boost in state-level optimism increases optimistic belief in one's financial performance, even above and beyond dispositional optimism.

Study 2: Do End-of-Periods Increase State Optimism?

In Study 2, we use an experiment to test whether (1) manipulating the day of the week of an investment decision affects optimistic belief that one's financial risks will pay off, and (2) whether directly increasing state-level optimism will also affect optimistic belief in financial performance. To manipulate the day of the week, we told participants to imagine that it was either a Tuesday, a typical workday, or a Friday (an end-of-period temporal landmark). However, all participants participated in the study on a Thursday. To experimentally manipulate state-level optimism, we adapted King's (2001) best possible self (BPS) intervention, one of the most effective and widely used interventions for increasing state-level optimism (Malouff and Schutte 2017).

Participants

We recruited 351 paid participants using Amazon's Mechanical Turk online-survey sampling site (MAge = 36.42 years, SD = 10.15; 66.4% male, 33.0% female, .3% nonbinary/third gender, 9.9% prefer not to say/missing). All participants were over age 18 and were citizens of the United States.

Experimental Procedure

The study was conducted on a Thursday. Participants were invited to take part in a financial decision-making task. After signing the consent form, participants were told that they would be making future investment decisions where successful investments could earn them up to 100% more in bonus money. Participants were then randomized into one of four experimental conditions: Tuesday, typical workday, Friday, or the BPS.

Participants in a day-of-the-week condition received one of three introductory prompts: “In this survey, you will be asked to rate how you feel about a potential upcoming task. Please think about a typical Friday [Tuesday/weekday] in your life. Thinking about a typical Friday [Tuesday/weekday] means that you imagine yourself on an average Friday [Tuesday/weekday], taking notice of ordinary details of the day that you don’t usually think about. Think of this as moving through your typical Friday [Tuesday/weekday] which is the last day of the work week [in the middle of the work week]. How do you feel on Fridays [Tuesdays/a typical weekday]? What do you typically do on a Friday [Tuesday/weekday]?” Given that the study was conducted on a Thursday, the prompts were also were accompanied with a visual image to increase the salience of the day-of-the-week manipulation (see Web Appendix H for full stimuli).

Participants who received the adapted BPS intervention were given the following instructions: “In this survey, please think about your best possible self. Thinking about your best possible self means that you imagine yourself during a day in the future, after everything has gone as well as it possibly could. You have worked hard and succeeded at accomplishing all the goals of your life. Think of this as the realization of your dreams, and that you have reached your full potential. Thus, you identify the best possible way that things might turn out in your life. Please, start thinking about a day in the future as your best possible self. How do you feel when you are at your best? What do you typically do?” Similar to the other conditions, a corresponding image was included to increase the salience of the BPS intervention see Web Appendix H. Participants were then told to take ten seconds to think about a day when they were their best possible self and then answered the same questions as the other participants.

After prompting participants to either imagine their best possible self or to think about a typical Friday, Tuesday, or typical weekday, participants were given the following instructions: “In this survey, you will make investment decisions that can earn you bonus money based on which options you choose and the potential earnings associated with those options. Depending on the investment that you make, you may have the potential to earn an additional $1.00. It is expected that the average participant will earn a bonus of $.25. However, regardless of how you choose to invest, you will earn $1.00 for your participation in the study.” Participants were not given details of what the investment task would involve.

Next, we measured investor optimism by asking two questions: “Consider that it is a Friday [Tuesday/typical weekday/you are your best possible self], how much do you think you will win over the $1.00 payment?” Participants were given a $.00–$1.00 slider bar, with $.00 indicating no bonus expected and $1.00 indicating full bonus amount expected. Participants were also asked to rate how optimistic they felt about their chances in the investment task by answering a comparative state-level optimism question: “How optimistic do you feel that your investment decisions will earn more than what the average participant will make for a bonus?” Participants were given a 0%–100% slider bar, with 0% indicating that they were not at all optimistic that they would earn more than the average and 100% indicating that they were extremely optimistic of making more than the average.

In addition to their initial payment, all participants were awarded the full bonus for their time. Participants were instructed to complete a trait-level optimism scale using the Revised Life Orientation Test (LOTR; five-point Likert scale: 1 = “Not at all,” and 5 = “Very”; Scheier, Carver, and Bridges 1994) and to rate their current mood via the short-form Positive and Negative Affect Schedule (PANAS, five-point Likert scale: 1 = “Not at all,” and 5 = “Very”; Watson, Clark, and Tellegen 1988). Finally, participants answered basic demographic questions.

Results

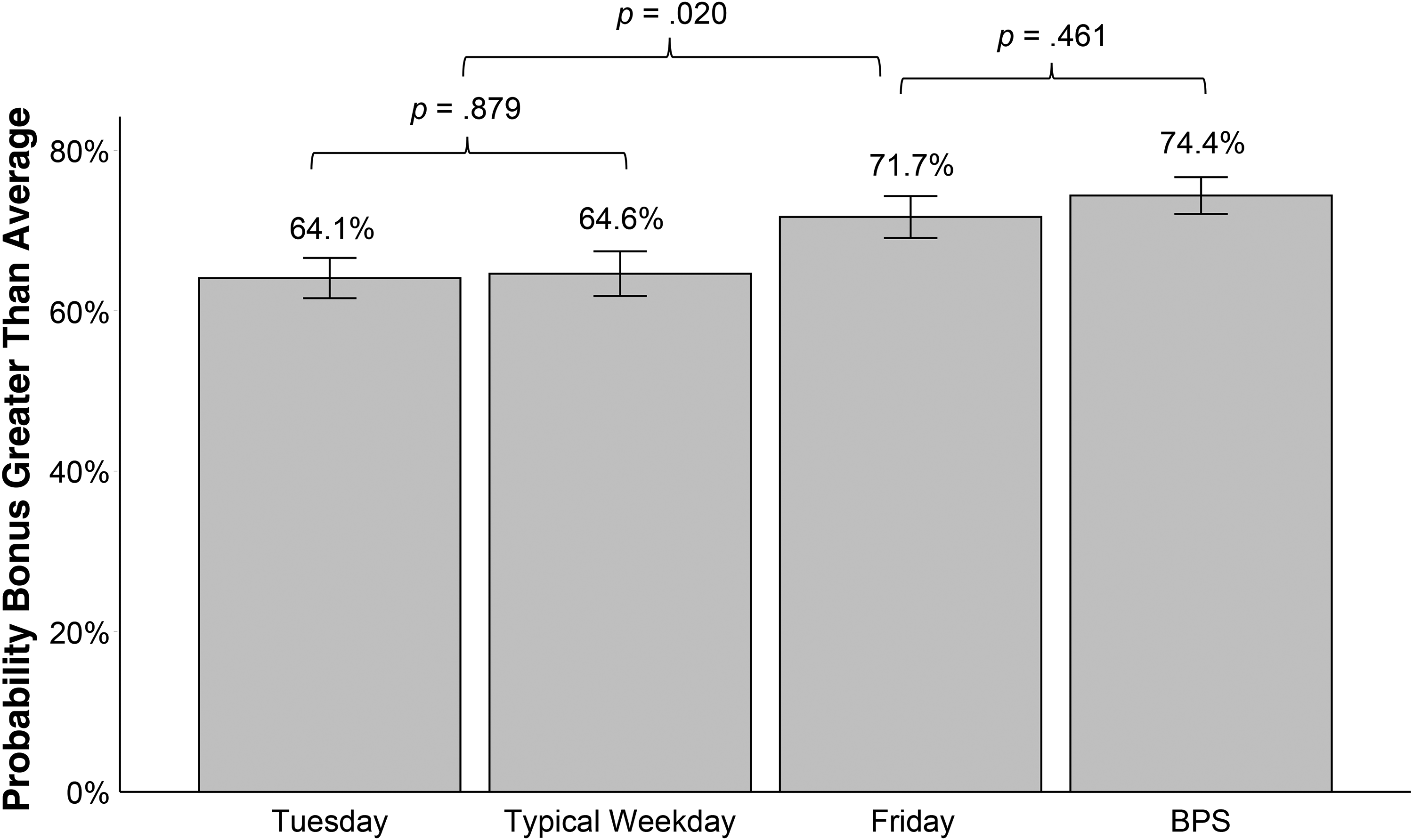

First, we compared our two non-end-of-period temporal landmarks, the Tuesday and typical weekday conditions. There were no significant differences between the two non-end-of-period landmarks for either optimism measure (predicted bonus earnings: MTuesday = $.62, SD = .28; MTypicalWeekday = $.59, SD = .26; t(347) = −.713, p = .477; state-level comparative optimism: MTuesday = 64.1%, SD = 23.7%, MTypicalWeekday = 64.6%, SD = 26.1%; t(347) = .152, p = .879).

Next, we compared whether Fridays increased optimistic beliefs about future financial performance relative to both non-end-of-period days. Using a one-way ANOVA with planned contrasts, we find a significant main effect of end-of-period Fridays relative to non-end-of-period days, with participants more likely to predict that they would earn a higher bonus amount when they were told it was a Friday relative to non-end-of-period weekdays (predicted bonus earnings: MFriday = $.67, SD = .26; t(347) = 2.07, p = .039). Fridays also significantly increased state-level comparative optimism, with Fridays increasing the likelihood that people believed they would earn more than the average participant versus non-end-of-period weekdays (probability of earning more than the average bonus amount: MFriday = 71.7%, SD = 24.2%; t(347) = 2.34, p = .020, see Figure 2).

State-Level Comparative Optimism: Probability of Earning More Than Average Participants.

Next, we tested whether directly increasing state-level optimism via the BPS affected optimistic belief. Those who were told to imagine a day when they were their best possible self were more optimistic regarding their future financial performance and had significantly higher state-level comparative optimism, relative to our typical weekday control variable (predicted bonus earnings: MBPS = $.78, SD = $.24; t(347) = 4.90, p < .001; probability of earning more than average participants: MBPS = 74.4%, SD = 21.5%; t(347) = 2.70, p = .007). The direct manipulation of state-level optimism via the BPS intervention increased predicted bonus earnings in comparison to Friday (t(347) = 2.73, p = .007). However, we do not observe differences between the BPS intervention and Fridays for the predicted probability of winning more than the average bonus amount (t(347) = .738, p = .461).

We investigate whether trait optimism (as measured by the LOTR) could also account for results and affect financial optimism. Consistent with previous findings, we find a significant and positive relationship between trait optimism and both of our outcome variables. Higher trait-level optimism is significantly associated with higher predicted bonus amounts (β = .016, SE = .003, p < .001), and increases state-level comparative optimism perceptions that participants would earn more than other participants (β = 1.49, SE = .284, p < .001). Consequently, we test whether we still find differences in our outcome variables, even after controlling for trait optimism.

We use an ANCOVA specification in which LOTR scores are used as a covariate measure for trait optimism. After controlling for trait-level optimism, we still find evidence that Fridays significantly increase state-level comparative optimism in comparison to non-end-of-period weekdays (contrast estimate = 6.58, p = .037) and marginally increase financial optimism via predicted bonus amount in comparison to non-end-of-period weekdays (contrast estimate = .062, p = .066). Directly manipulating state-level optimism via the BPS condition significantly increases state-level comparative optimism, even after controlling for trait-level optimism (BPS vs. non-end-of-period landmarks: contrast estimate = 9.32, p = .003).

Finally, we investigate whether individuals were in a better mood or reported being happier on Fridays in comparison to Tuesdays, typical days, or any non-end-of-period weekdays overall. To test for general positive affect, we combined positive affect items from a short version of the PANAS, as per Watson and Clark (1994). We find no difference in positive mood when comparing Fridays to each of the non-end-of-period weekday conditions or when both are combined (MTuesday = 23.36, SD = 6.49; MTypicalWeekday = 23.89, SD = 7.97; MFriday = 24.22, SD = 6.64; contrast estimate ps > .543). Fridays also did not increase feelings of happiness, measured using the PANAS item for happiness, relative to non-end-of-period weekdays or when they were combined (MTuesday = 3.69, SD = 1.10; MTypicalWeekday = 3.41, SD = 1.37; MFriday = 3.71, SD = 1.18; contrast estimate ps > .124).

Discussion of Study 2

The results of Study 2 provide two key findings. First, while we find evidence for the relationship between salient end-of-period temporal landmarks, our independent variable, and financial risk-taking, which was our main outcome of interest in Study 1, Study 2 provides more direct and causal support for the pathway between our independent variable and optimistic belief, our proposed mediator. Here, we find that end-of-period temporal landmarks lead people to feel more optimistic that their financial risks will pay off. Second, Study 2 shows that increasing state-level optimism, not just through an end-of-period landmark but through a more direct intervention, also significantly increases optimistic belief that one's financial risks will pay off. Both results provide support that changes in state-level optimism affect optimistic belief that one's financial risks will pay off, even above and beyond trait-level optimism measures (e.g., Malmendier and Tate 2005; Puri and Robinson 2007).

It is important to acknowledge that Study 2 focuses just on the relationship between our independent variable and mediator of interest. Testing the full pathway is essential for providing support for our theoretical account. In Study 3, we use a controlled experiment to test our full theoretical model. Specifically, Study 3 investigates whether salient end-of-period temporal landmarks increase financial risk-taking via increasing optimistic belief that one's financial risks will pay off.

Study 3: Testing an Optimism Mechanism

In Study 3, we investigate whether a cue that increases the salience of an end-of-period temporal landmark alters financial risk-taking beyond the P2P setting via a laboratory experiment. Specifically, we conducted our study on Tuesday, October 31. Doing so afforded the ability to manipulate the salience of an end-of-period temporal landmark, while holding the day itself constant. We test whether framing the day as a Tuesday or as the last day of the month, a salient end-of-period landmark, affects how money is allocated across two financial options that have the same expected value but vary in financial risk (a measure adapted from Han et al. [2019] and He, Inman, and Mittal [2008]). We also test our main mechanism of interest: state-level optimistic belief. The study design, analytic plan, and hypotheses were preregistered and are available at https://aspredicted.org/gb3nk.pdf.

Participants

We recruited 456 paid participants using Prolific's online sampling site (MAge = 36.42 years, SD = 11.62; 39.0% female, 59.5% male, 1.5% nonbinary/prefer not to say). All participants were over age 18 and were from the United States.

Experimental Procedure and Dependent Measures

The experiment was conducted on Tuesday, October 31, 2023, affording the ability of framing the day as either a Tuesday in the middle of the week or as October 31, the last day of the month. Participants were told that they would be participating in an experiment involving financial decision-making. Participants were given one of two prompts. Those in the Tuesday, non-end-of-period condition were told: “Please think about a typical Tuesday (like today). Thinking about your typical Tuesday means that you imagine yourself on an average Tuesday taking notice of ordinary details of your day that you usually don’t think about. Think of this as moving through your typical Tuesday at the beginning of your work week. How do you feel on this Tuesday, with the whole week ahead of you. Please start thinking about how you feel today.” Those in the last-day-of-the-month, end-of-period temporal landmark condition were told the following: “Today is October 31st, the last day of the month. Please think about what it feels like today, the last day of the month, right before a new month is about to begin. Thinking about the last day of the month means that you imagine yourself at the end of this period, taking notice of ordinary details of your day that you usually don’t think about. Think of how you feel moving through this final day of the month right before a new month is about to begin. How do you feel on this last day of the month? Please start thinking about how you feel today.” Each condition included a calendar visual image to increase the salience of the respective manipulation (see Web Appendix I for full stimuli).

We measured optimism by using a general financial optimism question and a comparative state optimism question. First, participants were asked a general financial optimism question: “Considering that you will be making a financial choice today, how optimistic are you that your financial choice will work out for you, on a scale of 0–100?” (0 = “Not at all optimistic,” and 100 = “Extremely optimistic”). Second, we measured state optimism using a more comparative measure: “Relative to the other people's performance, how optimistic do you feel that the financial choice you make today will work out better than the average person in the future?” (0 = “Not at all optimistic,” and 100 = “Extremely optimistic”).

Next, we measured financial risk-taking propensity. Participants were told that they had an extra $5,000 that they should allocate across two financial options, with both choices having the same expected value but varying in financial risk: “It's your typical Tuesday [the last day of the month]. You look into your bank account and see that you have an extra $5,000. You are now deciding what to do with your money. You have been given two options: A. Put your money (or some of your money) into your bank's saving account which offers a guaranteed return of 4% or, B. Invest in a mutual fund that is composed equally of three stock options: Stock 1 has a 45% chance of generating a return of 16%, Stock 2 has a 10% chance of generating a return of 4%, and Stock 3 has a 45% chance of incurring a loss of 8%.” Participants were then asked how they would like to allocate the $5,000 across the two options. They were reminded that the amount allocated to the savings and the stock fund must add up to $5,000. A higher amount of money allocated to the stock fund indicates a higher level of financial risk-taking. They were also asked to rate how likely they were to invest money in the stock fund option (0 = “not at all likely,” and 10 = “extremely likely”).

We then tested the perceived temporal separation between one's present and future self. We adapted the measure from Dai, Milkman, and Riis (2015) to a financial context as follows: “Most people agree that they have not made the most optimal and perfect financial choices in the past (or that their past self has made imperfect choices). There are always some aspects of ourselves and our lives that we think could improve. Sometimes our imperfect, past self feels very far away from who we are, while at other times our past imperfections feel very close. On a scale of 0–100, how much does tomorrow (Wednesday/November 1st) feel like a fresh start/new beginning, where you feel different relative to your past self?” (0 = “Not at all,” and 100 = “Extremely”). Higher ratings indicated feeling greater temporal separation between their current and future selves. Finally, participants answered which day of the week they felt most optimistic and then were asked about their age, gender, and trait optimism via the LOTR scale (see Scheier, Carver, and Bridges [1994] for measures and coding).

Results

We first investigate whether the experimental manipulation had the predicted effect on financial risk-taking and then test whether either psychological separation between the present and future selves or state optimism mediates the relationship between end-of-period temporal landmarks and financial risk-taking. We also test whether these two constructs mediate the end-of-period effect via parallel or serial mediation.

Effects of end-of-period temporal landmarks

Increasing the salience of the end-of-period landmark significantly influenced financial risk-taking. Individuals who were prompted to think of October 31 as the last day of the month allocated more money to the stock fund, the riskier financial option, in comparison to those who were told to think of October 31 as a Tuesday in the middle of the week (MLastDayofMonth = $2,070.79, SD = 1,386.77; MTuesday = $1,406.36, SD = 1,272.60; t(454) = 5.33, p < .001).

Consistent with initial evidence from Study 2, increasing the salience of the end-of-period temporal landmark significantly increased financial optimism. End-of-period framing significantly increased optimism regarding financial performance relative to non-end-of-period framing (MLastDayofMonth = 64.64, SD = 22.92; MTuesday = 60.26, SD = 20.57; t(454) = 2.14, p = .033). Those in the last-day-of-the-month condition also reported higher comparative state-level optimism, and were significantly more likely to say that they would perform better financially than the average participant (MLastDayofMonth = 62.31, SD = 24.39, MTuesday = 55.69, SD = 22.07; t(454) = 3.04, p = .002). Both financial optimism and comparative state optimism were significantly correlated (r = .725, p < .001). In addition, end-of-period framing significantly increased the perceived psychological separation between participants’ current and future selves (MLastDayofMonth = 54.16, SD = 30.56; MTuesday = 45.71, SD = 28.84; t(454) = 3.04, p = .003).

Importantly, we do not find evidence of any dispositional/trait optimism differences as a function of an end-of-period temporal landmark framing manipulation (p = .836). However, consistent with prior work, we find that both optimism measures were significantly correlated with dispositional/trait optimism (optimism for financial performance: β = .535, p < .001; state-level optimism relative to others: β = .439, p < .001). Taken together, our results suggest that increasing the salience of end-of-period temporal landmarks affects state-level optimism measures rather than trait optimism.

Mediation analysis

We assess whether state optimism mediates the relationship between end-of-period temporal landmarks and financial risk-taking. We test for simple mediation using Hayes’s (2017) PROCESS Model 4 and 1,000-draw bootstrapping. Given the significant and established relationship between trait optimism and financial risk-taking, we use trait optimism as a covariate in all mediation analyses, consistent with our preregistered analytic plan. First, we test state-level optimism. We find evidence consistent with partial mediation, with the standardized estimates of our model presented in Figure 3. End-of-period temporal landmark framing has an indirect effect on financial risk-taking in the presence of a state-level optimistic belief mediator (β = .040; 95% CI: [.008, .085]) with a 95% confidence interval that does not include 0. There is also a significant direct effect of end-of-period framing on financial risk-taking (t(454) = 4.84, p < .001).

Mediating Role of Optimism in the Relationship Between Salient End-of-Period Temporal Landmarks and Financial Risk-Taking.

Given the significant correlation between psychological separation between one's current and future self and optimistic belief, we also test two additional mediation pathways: (1) a basic mediation pathway testing whether end-of-period temporal landmarks are driven by the psychological separation between one's current and future selves, and (2) a serial mediation pathway, testing whether the psychological separation between the current and future self influences state optimism, and subsequent financial risk-taking propensity. The results of both mediation analyses are presented in detail in Web Appendix J. We find that the psychological separation between one's current and future self also significantly mediates the relationship between salient end-of-period landmarks and financial risk-taking. However, we do not find evidence consistent with a serial mediation pathway.

Discussion of Study 3

Study 3 shows causal evidence that increasing the salience of end-of-period temporal landmarks increases financial risk-taking, beyond just P2P settings. We are also able to reduce the concern that alternative mechanisms, such as payday effect or other selection effects, are responsible for end-of-period effects alone. Instead, we find evidence consistent with our effects being driven, at least in part, by an optimism mechanism. The results of Study 3 are suggestive of a broader effect of end-of-period landmarks on financial risk-taking. Increasing the salience of end-of-period landmarks increases state-level optimism and, in turn, leads to greater financial risk-taking.

General Discussion

Using over four million investment decisions from one of the largest P2P lending platforms in the United States, along with two controlled laboratory evidence, we find evidence that end-of-period temporal landmarks (e.g., last workday in the week, last day of the month, last day of the year) are associated with greater financial risk-taking propensity. The richness of our dataset, combined with our laboratory evidence, enables us to rule out a number of key alternative explanations, such as payday effects, reference dependence, conformity/rational herding, or potential demand/supply-side variation across days. We use our laboratory experiments to identify potential underlying drivers behind end-of-period effects. Building on research on mental accounting and the role of optimism in risk-taking, we focus on the role of optimistic belief in future financial performance. In Study 3, we find that when end-of-period temporal landmarks are salient, people feel more optimistic and, in turn, engage in greater financial risk-taking.

From a theoretical perspective, our findings show that temporal landmarks not only affect motivation and aspirational goal pursuit, but also serve as salient cues altering financial risk-taking propensity. Previous work has documented the importance of new periods on motivation levels, finding that new periods serve to disconnect individuals from their past selves and offer a “fresh start” (Dai, Milkman, and Riis 2014, 2015). Building on this work, our results suggest that end-of-period landmarks may be important as well, affecting even consequential risk decisions.

Managerial and Substantive Implications

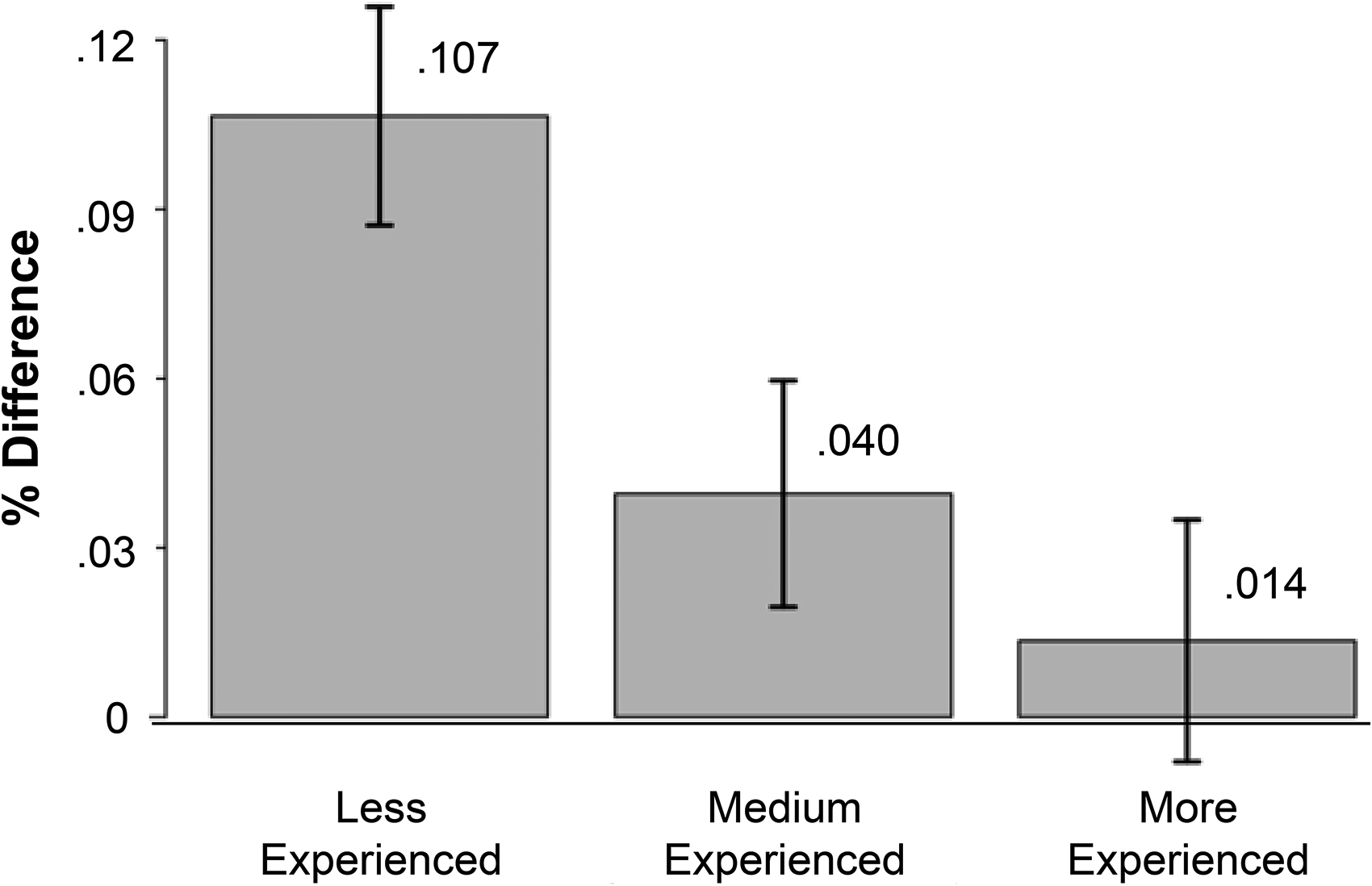

From a welfare and policy standpoint, an important question still remains: Does this end-of-period effect have any impact, positive or negative, on the return rates of investments? Our P2P panel dataset is particularly compelling as we are able to compare the rate of return of investments made at the end of a period with those made at other points in time. All of the loans that originated during our sample period (November 9, 2005, to October 14, 2008) came to fruition in 36 months. For each funded loan, the corresponding return rate is computed as the amount of return (principal repayment + interest paid) divided by the amount requested. Each bid invested in the same funded loan will have the same return rate. We then run a regression to compare the average return rate per bid between those not at ends of periods and those at ends of periods (see Web Appendix K). Across all specifications, we find that the average return rate is significantly lower on bids placed at end-of-period landmarks (i.e., Fridays, Wednesdays and Thursdays before public holidays, and the last day of a month).

In our P2P setting, end-of-period risk-taking has clear downsides for lenders’ financial well-being. End-of-period investments have significantly lower rates of return compared with investments made during non-end-of-period landmarks. But the downsides are not limited to lenders alone. If lenders take a risk by investing in loans that are significantly riskier at ends of periods, then risky borrowers are more likely to get funded at ends of periods, and potentially default over time. Defaulting on a loan is usually associated with a hit to the borrower's credit rating as well as heavy interest penalties. Hence, end-of-period effects are associated with downsides for both borrowers and lenders. Given the potential downsides of end-of-period financial risk-taking, a natural question is whether these effects can be moderated or at least attenuated. We propose three factors and explore them further using experimental and secondary data analysis.