Abstract

New ventures are essential for developing innovations and generating economic and societal value, but they depend on external resources, especially from venture capitalists, who provide seed funding to make necessary advances in the development and commercialization of their innovative products. From the marketing discipline's perspective, the question is whether marketing actions play a role in this early acquisition of critical resources. Building on organizational legitimacy theory, the authors argue that trademark applications are important from day one, as they send important information cues to venture capitalists (e.g., on marketing-related professionalism) that foster the acquisition of venture capital (VC) seed funding. The authors build a dataset using Crunchbase and U.S. Patent and Trademark Office data that follows 5,370 ventures founded between 2007 and 2010 over several years up to 2018. They find that new ventures that file trademark applications have an increased likelihood of acquiring VC seed funding compared with firms that do not file trademark applications. This association is strongest during the first 100 days and diminishes about 1,000 days after foundation. The effect is particularly pronounced in industries characterized by low technological uncertainty and when new ventures do not operate from a location with a cluster of startups, such as Silicon Valley.

Keywords

New ventures are essential for developing innovations and generating economic and societal value, but they need external resources to do so (Zott and Huy 2007). Venture capitalists offer these much-needed external resources in new ventures’ early stages by providing seed funding. Since venture capitalists are highly selective (Sahlman 1990), it is critical to understand what drives their decisions regarding seed funding. While extant entrepreneurship research finds such drivers in founders and management teams, the businesses’ innovativeness, their geographic locations, and their industry settings (e.g., Bertoni, Colombo, and Grilli 2011; Haeussler, Harhoff, and Mueller 2014), marketing's potential role has been examined only by Homburg et al. (2014), who find that, depending on industry conditions, a chief marketing officer's (CMO) human capital (e.g., marketing experience) is positively related to the acquisition of venture capital (VC) seed funding.

While Homburg et al.’s (2014) study sheds first important light on marketing's role in new ventures’ ability to acquire VC seed funding, whether these ventures should engage in marketing actions after their foundation to boost their chances of obtaining VC seed funding is an open question. New ventures can typically offer only an innovation idea when they apply for seed funding (Tyebjee and Bruno 1984), so they are still far from being able to pursue the full repertoire of marketing actions. Yet, some early marketing actions, such as applying for trademarks to start the venture's branding activities, are possible (Lodish, Morgan, and Kallianpur 2001).

However, trademark applications could unnecessarily absorb the ventures’ scarce resources, and some authors claim that technological innovations should be the cornerstone activity of new ventures’ first months (Kazanjian and Drazin 1989). Further, trademark applications could unveil to competition future market entries of ventures that may prefer to remain in “stealth mode” for a surprising market entry. For example, Instagram and Pinterest built their products before they applied for trademarks (U.S. Patent and Trademark Office [USPTO] 2018). Another view suggests that taking a customer perspective (e.g., branding, increasing awareness among potential customers), as reflected in a trademark application, is critical even before finalizing a product (Andreessen Horowitz 2017). WhatsApp did this by filing a trademark application shortly after its foundation (USPTO 2018). Given the importance of the decision to allocate scarce resources to trademark applications, and given the divergent views about ventures’ filing for trademarks, we ask, “Do new ventures with trademark applications have an increased likelihood of acquiring VC seed funding?”

To address this research question, we use legitimacy theory (Zimmerman and Zeitz 2002) and the literature on venture capitalists’ decision-making (Petty and Gruber 2011) to argue that trademark applications are legitimizing actions that improve access to VC seed funding, especially shortly after a venture's foundation. Accommodating the notions that legitimacy considerations are context-dependent (Fisher 2020) and that venture capitalists evaluate ventures holistically (Muzyka, Birley, and Leleux 1996), we expect that venture capitalists do not evaluate the information cue from trademark applications in isolation. Therefore, we develop arguments that trademark applications’ legitimizing force in the eye of the venture capitalist depends on the technological uncertainty and competitive intensity levels of the new venture's industry and its location, in terms of whether it is situated in a cluster of startups.

We employ extended Cox models (Kleinbaum and Klein 2012) and Aalen additive hazards models (Martinussen and Scheike 2006) to test our model, including temporal effects. We combine data from Crunchbase, the USPTO, and Compustat; our final data follow 5,370 U.S.-based ventures founded between 2007 and 2010 over the years up to 2018. Since our model relies on observational data, several observed and unobserved variables may influence whether new ventures apply for trademarks and acquire VC seed funding, so we use a rich set of controls and two-stage residual inclusion (2SRI) models. To complement our arguments, we offer semistructured interviews with ten venture capitalists who engage in seed funding and ten founders who went through the trademark application process. 1

Our study makes three main contributions: First, we extend the marketing–finance research from its stock market focus (Edeling, Srinivasan, and Hanssens 2021) to incorporate venture capitalists as early seed funding investors (Homburg et al. 2014). Specifically, we complement research on (mostly) positive stock market reactions to marketing expenditures and actions of more established firms (e.g., Saboo and Grewal 2013) by finding that venture capitalists who provide seed funding value a new venture's dedication of its scarce time and resources to trademark applications as one important marketing action.

Second, by identifying the temporal boundaries of the drivers of seed funding, we contribute to the emerging literature on venture capitalists’ decision-making in the marketing literature (Homburg et al. 2014) and the broader legitimacy theory and entrepreneurship literatures. To the best of our knowledge, the present study is, even in the entrepreneurship and entrepreneurial finance literatures, the first to show that the effectiveness of funding drivers varies within the stage that leads to seed funding, emphasizing the strong temporal sensitivity of legitimacy-creating forces like trademark applications. (See calls from Lévesque and Stephan [2020] and Ko and McKelvie [2018] to examine such temporal contingencies.)

Third, we contribute to legitimacy theory (e.g., Fisher 2020) and to its application in the marketing literature (e.g., Rao, Chandy, and Prabhu 2008) by unveiling marketing-related legitimizing forces’ dependence on external and internal contingencies. We argue and show that the legitimacy-enhancing effect of trademark applications is moderated by the industry's level of technological uncertainty and whether the venture is located in a startup cluster.

Conceptual Background

New Ventures’ Development and the Nature of the Seed Funding Stage

Organizational life cycle theory describes new ventures’ development as a sequence of stages, where the transitions are typically marked by specific milestones (Kazanjian and Drazin 1989). The stage immediately after foundation comes with unique challenges. It begins with the founding team's starting its entrepreneurial endeavor by setting up the new venture, typically based on a rough product idea. The new venture with minimal resources faces a plethora of challenges, ranging from developing an innovative idea to hiring the first managers and employees, expanding the venture's reputation, and reaching out to external stakeholders to access resources (Timmons, Spinelli, and Zacharakis 2004).

Success Factors in Acquiring Seed Funding and Legitimacy Theory

Acquiring financial resources is among the most critical challenges in the first stage. Without such resources, new ventures cannot invest sufficient time and money in the development of innovations and products that enable future growth (Nuscheler, Engelen, and Zahra 2019). New ventures often receive their first funding in the form of informal and limited amounts from grants, family and friends, or angels, but the significant early resources are provided by venture capitalists’ seed funding (De Clercq et al. 2006).

As opposed to later funding rounds (e.g., Series A investments, initial public offerings), new ventures at the seed funding stage have neither full-fledged products nor market responses (Kazanjian 1988), let alone profitability outlooks. Therefore, the venture's prospects are highly uncertain. Legitimacy theory argues that investors who are operating under such uncertainty look for signals of a new venture's legitimacy (Fisher 2020; Zimmerman and Zeitz 2002), that is, “a generalized perception or assumption that the actions of an entity are desirable, proper, or appropriate within some socially constructed system of norms, values, beliefs, and definitions” (Suchman 1995, p. 574). The underlying assumption is that new ventures that conform to these expectations are more likely to be successful than those that do not (Busenitz, Fiet, and Moesel 2005; De Clercq and Sapienza 2005). Legitimacy theory argues that legitimacy is rooted in the founders and top management (legitimizing attributes) but can also be enhanced by means of specific actions (legitimizing actions) (Plummer, Allison, and Connelly 2016). Importantly, the eyes of the beholder determine a new venture's legitimacy, and different types of stakeholders can come to different conclusions regarding its legitimacy (Fisher et al. 2017).

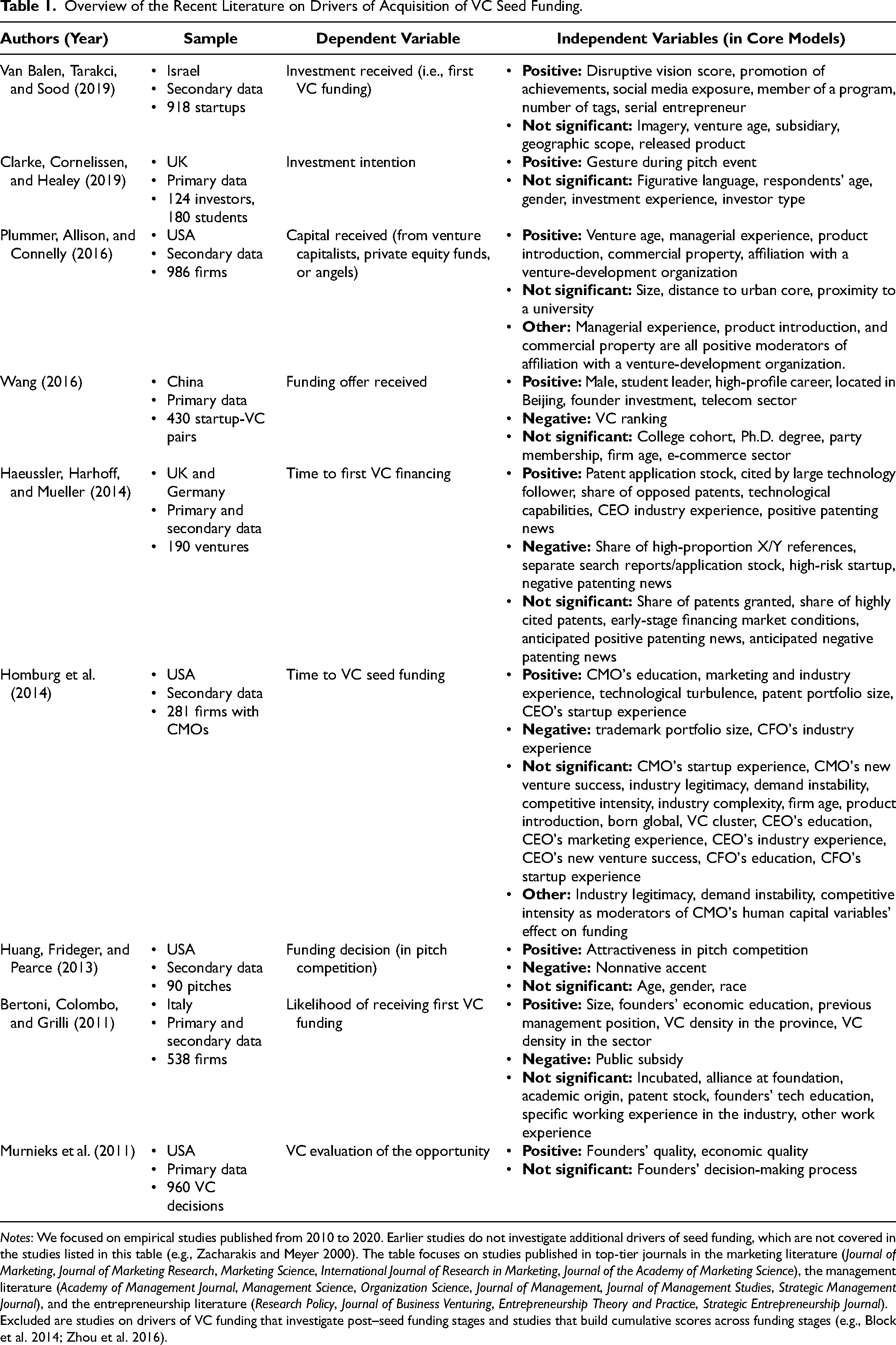

Plummer, Allison, and Connelly (2016, p. 1586) observe for the broader management and entrepreneurship literature that VC seed funding is a “relatively unexplored but critical milestone in the life of a new firm,” in contrast to the significant research on the success factors of later VC funding stages and initial public offerings (Block et al. 2014; Zhou et al. 2016). This observation also applies to the marketing literature, which focuses on stock market reactions to established firms’ marketing actions (see the review by Edeling, Srinivasan, and Hanssens [2021]). Accordingly, our systematic literature review, shown in Table 1, yields only nine studies since 2010 from leading marketing, management, and entrepreneurship journals that explain what drives the acquisition of VC seed funding, among which one study investigates the CMO's human capital (e.g., marketing experience) as a marketing-related driver of seed funding (Homburg et al. 2014). Apart from some success factors in specific phases of the funding-acquisition process, such as gestures during pitch events (e.g., Clarke, Cornelissen, and Healey 2019), the major categories of the drivers of seed funding are founders’ and early managers’ characteristics (e.g., Plummer, Allison, and Connelly 2016), the industry environment (e.g., Homburg et al. 2014), the new venture's location (e.g., Bertoni, Colombo, and Grilli 2011), and the innovativeness of the business and its products (e.g., Haeussler, Harhoff, and Mueller 2014; Van Balen, Tarakci, and Sood 2019).

Overview of the Recent Literature on Drivers of Acquisition of VC Seed Funding.

Notes: We focused on empirical studies published from 2010 to 2020. Earlier studies do not investigate additional drivers of seed funding, which are not covered in the studies listed in this table (e.g., Zacharakis and Meyer 2000). The table focuses on studies published in top-tier journals in the marketing literature (Journal of Marketing, Journal of Marketing Research, Marketing Science, International Journal of Research in Marketing, Journal of the Academy of Marketing Science), the management literature (Academy of Management Journal, Management Science, Organization Science, Journal of Management, Journal of Management Studies, Strategic Management Journal), and the entrepreneurship literature (Research Policy, Journal of Business Venturing, Entrepreneurship Theory and Practice, Strategic Entrepreneurship Journal). Excluded are studies on drivers of VC funding that investigate post–seed funding stages and studies that build cumulative scores across funding stages (e.g., Block et al. 2014; Zhou et al. 2016).

Trademark Applications

Our literature analysis indicates that the CMO's human capital is related to the venture's acquisition of VC seed funding (Homburg et al. 2014), which is in line with legitimacy theory's expectation that legitimacy is created by legitimizing attributes—that is, what a new venture has. However, this theory also suggests that legitimacy is also created by legitimizing actions—that is, what a new venture does (Plummer, Allison, and Connelly 2016). As Table 1 indicates, the literature does not investigate marketing actions as drivers of VC seed funding. Such an investigation would acknowledge that new ventures have no fully developed products for commercialization at this early stage (Tyebjee and Bruno 1984), which limits their repertoire of possible marketing actions to a few options, including trademark applications to prepare for branding activities (Castaldi, Block, and Flikkema 2020). Applications for trademarks can be made as early as at foundation, but they can be made at any time. 2 A trademark application is separate from a final registration. Only if the application meets the filing requirements does an attorney determine whether federal law permits the registration of the trademark (World Intellectual Property Organization [WIPO] 2008). Then the public can file objections. 3

A trademark is a “distinctive sign, which identifies certain goods or services as those produced or provided by a specific person or enterprise” (Manzini and Lazzarotti 2016, p. 581). While a trademark application may also come with downsides, such as revealing the future target markets of ventures that may prefer to remain in “stealth mode” (Fink et al. 2022), it offers a legal basis from which the applicant can develop brand security and protect its marketing investments. The trademark application must document meeting three conditions (Krasnikov, Mishra, and Orozco 2009): distinctiveness, no misleading or immoral character, and the use of (or intent to use) the trademark in the market(s) identified (WIPO 2008). To specify the markets, applicants list one or more of 45 Nice product or service classes. Broader trademarks cover more markets and, in addition to paying higher fees, applicants must demonstrate commercial use in all chosen classes. Most new ventures tend to apply for one or only very few Nice classes (Block et al. 2014). When trademarks are not used, they are canceled.

Trademark applications require marketing and legal expertise and consume new ventures’ extremely scarce resources. All of the founders we interviewed paid for their trademark applications, including the costs of legal support, with money they put into the venture from their private funds. The founders reported that the research, especially research on competitors, was the most time-consuming part of the application process—far more than completing the application itself. Two founders noted that they abstained from applying for trademarks because of the resources that would have to be diverted from other critical activities. As one founder reported: We, the founders, checked all brands and sub-brands of competitors and possible competitors to make sure that our intended trademark was different enough to go through. Since we knew that one competitor had started several lawsuits against other brands, we needed to be super-careful, which made the research and comparison with our intended brand very time consuming. It kept the founder team busy for days, if not weeks, a substantial part of our time while we were setting up the business. (Founder A)

The founders noted that selecting appropriate Nice classes requires a clear understanding of which customers to target and a detailed differentiation from existing brands. For example: We wanted to launch the first products and to start producing labels and marketing, but we were still busy with the trademark application and did not want to use a brand that could be rejected afterwards. One major issue was to understand the classes, which are described in confusing ways, but you need understand very carefully where your relevant classes are and where our customers are likely to be. (Founder F)

Founders also reported that they all required a lawyer to be sure that the trademark would be registered successfully. Two founders provided exemplary statements: While it is theoretically possible to apply for a trademark without a lawyer, we needed a lawyer not only for the application itself, but especially for the consulting. Forms were complex, and we needed expertise on whether our planned trademark is sufficiently unique and would withstand a lawsuit. When you go out with a trademark, you make yourself vulnerable to such things. (Founder A) The process is really complex, and you need legal support. In our case, there was a potential competitor with a corporate identity in yellow. … Together with our lawyers, we understood that it would be better to apply for a trademark with our logo in orange, rather than yellow. These are the nuances we needed to understand. (Founder I)

Hypothesis Development

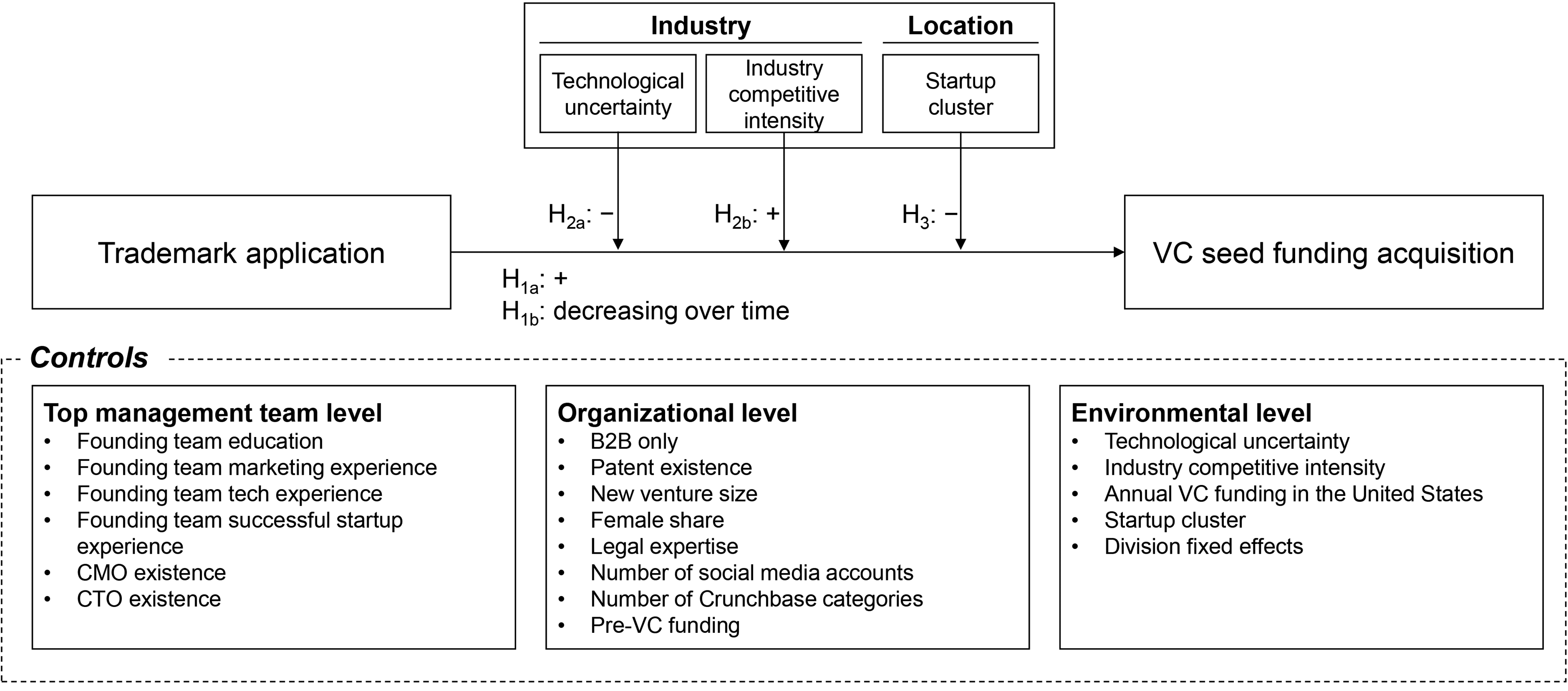

Building on legitimacy theory (e.g., Zimmerman and Zeitz 2002) and the literature on venture capitalists’ decision-making related to seed funding (e.g., Petty and Gruber 2011), we analyze whether trademark applications are a legitimizing action that leads to the acquisition of VC seed funding. To add precision to our investigation, we investigate temporal differences within the stage that leads to seed funding. Further, we elaborate on how the industry environment and the location of a new venture influence trademark applications’ effect on the acquisition of such funding. Figure 1 illustrates our research model.

Research Model.

The Direct Association Between Trademark Applications and Acquisition of VC Seed Funding

For three main reasons, we expect that trademark applications carry a critical information cue that creates legitimacy in the eye of the venture capitalist, thus positively influencing a new venture's chance of acquiring VC seed funding. First, by applying for trademarks, new ventures convey their professionalism and planning ability in building and protecting market-related assets (Block et al. 2015; Castaldi, Block, and Flikkema 2020). Venture capitalists avoid new ventures that they expect will not handle their limited resources well (Gompers 1995), such as when new ventures spend marketing resources without a systematic, planned approach to understanding the customer-acquisition costs. While trademark applications in the seed phase are no guarantee of future market success, venture capitalists may conclude that ventures that make such applications are taking a professional approach to market-related asset protection and plan with foresight when allocating their scarce resources (Srinivasan, Lilien, and Rangaswamy 2008). Some of the venture capitalists we interviewed argued accordingly: However, if a founder tells me he has applied for a trademark, I would take that as a sign that the business is established, more professional, more committed, more secure. (Investor F) Trademarks are a good signal to the investor [that] the team has professional knowledge about brand building and brand protection. The brand is the most important asset in many settings. I also believe that early trademarks signal very ambitious ventures. (Investor C) [A trademark application is] a good sign that I, as an investor, won’t get into any brand-related trouble after making my investment; it is a sign that the company is protected and my investment is safe. (Investor D)

Second, a trademark application requires the applicant to select Nice classes of targeted markets and argue that there are no competitors in the chosen classes that use a similar trademark (Graham et al. 2013). Thus, a trademark application obliges founders to deal with at least a basic market and competitor analysis (Castaldi 2020). Venture capitalists appreciate market analyses, as many new ventures tend to overestimate customer demand for their products, misjudging their products’ distinctiveness (Hills 1985). Research on formal business planning shows that formally writing down and reflecting on ideas helps the new venture to find flaws in its thinking (Brinckmann, Grichnik, and Kapsa 2010; Hills 1985). Trademark applications can function as a mechanism to challenge assumptions about the venture's positioning and competition. One venture capitalist we interviewed related trademark applications to positioning in the market: [A trademark application] is an important proof point because the startup has checked up front whether there is a sweet spot for it in the market where it can position itself. (Investor I)

Third, since trademarks must be used in the market, they signal a serious commitment to commercializing the venture's product ideas (Gao and Hitt 2012). Further, they illustrate professionalism from which venture capitalists can conclude that the new venture will be able to create sellable products. Two venture capitalists noted: The entire branding, including trademarks that we also formally check at the end of the evaluation process, tells us whether the founders are “product persons” or not. Will they able to develop commercially viable products using their technology? The early branding helps us understand the founders’ capabilities in this respect. (Investor A) Trademarks reflect the seriousness of the endeavor. I may conclude that there is the critical competence in the team that is needed to build a successful startup. Particularly when there are trademarks at early stages, I understand that the team has the skills and capabilities that are needed to bring the product to the market successfully. (Investor J)

Overall, we state:

We base on the notion that new ventures are dynamic entities (McMullen and Dimov 2013) our expectation that trademark applications’ relevance to acquiring VC funding varies over time. We expect that trademark applications’ effects are particularly strong at the beginning, that is, the early days after the foundation. We contend that, when ventures apply for trademarks later in this stage, after addressing the first product development challenges, trademark applications may be considered a necessity, not as a way to use foresight to build marketing assets. Consequently, venture capitalists may see some professionalism at that time but not the same planning foresight that they would had the applications been made earlier.

When a venture applies for trademarks early in the seed phase, venture capitalists know that the venture dedicated resources to analyzing and selecting its target groups before it made substantial time investments in the product development. This knowledge addresses venture capitalists’ typical worry that new ventures waste time resources in double work (Loch, Solt, and Bailey 2008). By observing trademark applications, venture capitalists can conclude that the venture pursued product development by taking a customer perspective, which is a success factor in entrepreneurial settings (Lodish, Morgan, and Kallianpur 2001). One of the venture capitalists we interviewed stated the necessity of an early customer lens: [Trademarks] are super-important. In the beginning, there should be patents but also trademarks because the brand should be protected from day one. Logo, claim, and brand need to be protected [as] these things create the recognition value. Therefore, startups should protect their brands right from the start, and they should build strategies around how to build a great brand, including trust. (Investor I)

In the earliest days, progress in terms of product development is naturally lowest (Kazanjian 1988), suggesting that the information cue from trademark applications on this progress is particularly important. When product development advances, prototypes are more developed and first (test) customer feedback is available (Hsu and Ziedonis 2013), reducing trademark applications’ informational character. Therefore:

Legitimacy theory argues that legitimacy considerations are context-dependent (Fisher 2020; Zimmermann and Zeitz 2002), an argument that is particularly applicable to venture capitalists as professional investors who understand the situational dependence of information cues (Colombo 2021). Specifically, we expect both the industry environment and the venture's location to provide frames in which venture capitalists evaluate trademark applications as a legitimizing force. Both industry and location have been identified as legitimizing forces in the broader legitimacy theory literature (e.g., Fisher 2020; Zimmerman and Zeitz 2002) and, as Table 1 indicates, are major determinants of venture capitalists’ decisions related to seed funding.

Moderating Influence of the Industry Environment

Industries differ in their degrees of technological uncertainty and competitive intensity (Li and Calantone 1998). In industries that have high levels of technological uncertainty, products change quickly, and these changes are often difficult to anticipate (Zhou, Yim, and Tse 2005). In these industries, the planning that trademark applications require (which typically is done for only one or few Nice classes) might be too rigid (Brinckmann, Grichnik, and Kapsa 2010) since a high degree of uncertainty requires flexibility and all but ensures unexpected technological opportunities with (possibly) surprising market positioning. Therefore, the unpredictability of products and their positioning (Sarasvathy 2001) reduces the potential for narrow-brand protection in the form of trademarks and impairs trademark applications’ legitimizing force.

Unlike industries that have low levels of technological uncertainty, product ideas are likely to change in highly uncertain industries, so a typically narrow trademark application with one or only a few Nice classes and narrow underlying research required for the application can become outdated quickly. While venture capitalists might still appreciate a new venture's dealing with trademarks and conclude that it has a market-oriented posture, they might not consider the dedication of scarce time to knowledge that may soon become outdated to be appropriate, reducing a trademark application's positive effect (Golis, Mooney, and Richardson 2009).

Trademark applications signal commercialization in the near future (Castaldi 2020). However, when technological uncertainty is high, early trademark applications might be considered premature, as product features might still be subject to changes (Kirtley and O’Mahony 2020), requiring the trademark application to be modified (e.g., regarding Nice classes) or even withdrawn and replaced with a new trademark. A trademark with fixed content might not be a strong predictor of upcoming positions that require adaptations to accommodate technological advances. However, in industries with low levels of technological uncertainty, an early trademark can signal subsequent product development efforts. Therefore:

Industries also differ in their competitive intensity. Competitive intensity is associated with a higher number and diversity of competitors and with stronger rivalry among them (Xue, Ray, and Sambamurthy 2012). Transparency about the competition is reduced, and the likely outcomes of marketing actions are less clear. When competitive intensity is low, only a few large competitors dominate the market (Schilling and Steensma 2001), and certainty about competitors’ actions increases. Competitive industries come with higher pressure on costs (Reimann, Schilke, and Thomas 2010), so wise expenditures that lead to protected market-related assets are particularly important. Brands must also be strong to stand out among competitors (Ward, Light, and Goldstine 1999). Since venture capitalists tend to be critical of ventures that target competitive markets (Fried and Hisrich 1994), information that points to a new venture's professionalism in positioning its products in these industries is particularly well received.

When competitors are both numerous and opaque, a trademark application, as a reflection of at least a basic market analysis, is an important legitimizing force—more than it is in less competitive markets, where competitors are limited and more transparent (Xue, Ray, and Sambamurthy 2012). While not directly referring to trademarks, venture capitalists emphasized in our interviews the need to understand the competition but lamented that some ventures that seek seed funding are not well prepared, a concern that is particularly urgent in competitive markets.

We expect that entering an industry with a first product early, which a trademark application can signal, is particularly important when competitive intensity is strong and uncertainty is high regarding the product's development and how the competition and the market will react. Early feedback is necessary to protect the ability to pivot, an approach that venture capitalists value, as it may preclude spending resources on dead ends for too long (Gompers and Lerner 2001). When the industry is less competitive, the players and their offerings are known, which reduces uncertainty about market reactions (Li and Calantone 1998). Therefore:

Moderating Influence of the Startup Location

New ventures differ in whether they locate in a startup cluster with a social structure that offers rich technical and market knowledge (Rao, Chandy, and Prabhu 2008). Startup clusters also attract skilled employees (Casper 2007). We expect that location in a startup cluster, in proximity to other startups that can provide input on marketing and planning, reduces the value of a new venture's trademark applications as an information cue. When a new venture is not part of a startup cluster, access to experts on various startup-related topics is less likely, requiring venture capitalists to turn to trademark applications to gauge the new venture's professionalism regarding marketing assets.

Startup clusters are excellent locations in which to recruit skilled managers and employees (Gittelman 2007), so when the absence of trademark applications suggests that a new venture may be missing the skills for market and competitor analyses, venture capitalists can expect that, if the venture is located in such a cluster, it has superior access to employees with human capital that can compensate, at least in part, for missing knowledge.

Further, when a new venture can see commercialization successes in proximal peer ventures (Van Rijnsoever 2020) and is well embedded in a knowledge network and surrounded by successfully commercialized role models, venture capitalists are likely to put less emphasis on trademarks. When a new venture is not part of a startup cluster, venture capitalists are likely to need trademark applications as cues for upcoming product commercialization. Therefore:

Methodology

Data Collection and Sample

We started our sample generation with Crunchbase, a database that tracks new venture developments with details on funding events, founders, main decision-makers, and key employees, including hierarchical and functional positions. The information stems from news articles on blogs and online newspapers, and individuals can update and enhance the information. Crunchbase editors and machine learning algorithms check the accuracy of the information (Crunchbase 2021). Crunchbase offers the advantage of providing a relatively complete coverage for startups—both funded and nonfunded—in their early stages.

Crunchbase offers particularly high data quality for U.S.-based ventures (e.g., Winkler, Rieger, and Engelen 2020), so we constructed our sample of ventures founded in 2007–2010 from U.S. ventures and collected data on the years after their foundation up to 2018. After excluding public companies and ventures with missing data, we had 5,370 new U.S. ventures with complete records. (See Web Appendix W5 for a stepwise description of our sample construction.) We matched these new ventures with the USPTO case files dataset (USPTO 2018), which contains all trademark applications and registrations in the United States since 1870 (Graham et al. 2013). Using a fuzzy matching approach based on two distance algorithms (Jaro and Levenshtein distance), we compared the company names in the USPTO case files dataset with our new ventures from Crunchbase. (See Web Appendix W6 for details.) We chose sensitive settings for our algorithms to prevent overlooked matches but then manually confirmed or rejected all matches. We also validated the confirmed matches for 50 companies through a manual name search in the USPTO's web search, which resulted in 100% consistency with our web search results. Finally, we added Compustat data and four-digit Standard Industrial Classification (SIC) codes. (See Web Appendix W7 for details.)

The dataset is arranged as a counting process data structure on a firm-month basis up to the month when VC seed funding was acquired or the end of the observation period if the firm never received VC seed funding, resulting in a dataset of 414,252 firm-month observations.

Empirical Analyses

To accommodate our theory's notion that legitimacy is gained by the occurrence of trademarks and not their numbers, we structure trademark applications as a binary variable. Further, because trademark applications can be made at any time, we code this variable 1 for all months in which at least one trademark application was or had been filed and all the months thereafter, with all other months coded 0 (Zhou et al. 2016). As such, the new venture Infamous Robotics, founded in August 2007, applied for its first trademark in August 2012, so its trademark application scores are 0 until the application in August 2012 and 1 thereafter. The coding for ventures like BlenderHouse, which never applied for a trademark until the end of our observation period or until they received seed funding, remains 0 for the entire observation period. (See also Web Appendix W8.)

In an ideal setting, we would compare the acquisition of VC seed funding that occurred after the venture made a trademark application with the acquisition of VC seed funding for the same firm had it not applied for a trademark. Since we cannot observe the latter, we compare firms that made trademark applications with firms that had not yet done so. In line with previous literature (e.g., Germann, Ebbes, and Grewal 2015), we undertake several corrections to increase the comparability of the treatment group (ventures with trademark applications) and the control group. We model the acquisition of VC seed funding as a function of trademark applications and a large number of controls and use a 2SRI approach. In the following, our analyses move from a correlational inference to a more causal inference.

Model Specification

We use a continuous-time single-failure survival model (Todri, Adamopoulos, and Andrews 2022) and model the hazard of acquiring VC seed funding. We employ an extended Cox model that allows for both time-varying and time-invariant variables and that corrects for censored observations in terms of firms that may have received seed funding after our observation period (Kleinbaum and Klein 2012). The Cox model's key advantage is reasonably good hazard estimates without selecting an underlying type of distribution. Our main estimation equation for VC seed funding acquisition is:

H2 and H3 propose that trademarks’ effect on the acquisition of VC seed funding is moderated by the firm's industry and location. We measure an industry's technological uncertainty as the ratio of research and development expenses to total sales (for all companies in the same four-digit SIC group) (Homburg et al. 2014; Winkler, Rieger, and Engelen 2020). We measure an industry's competitive intensity by subtracting the four-firm concentration ratio (i.e., the market share of the top four firms in the industry) (McAlister, Srinivasan, and Kim 2007; Srinivasan, Lilien, and Sridhar 2011) from 1 since competitiveness is assumed to be higher in less concentrated industries (Eroglu and Hofer 2014). We operationalize location in a startup cluster as a binary variable, coded 1 if a venture's headquarters is in California, New York, or Massachusetts (Sorenson and Stuart 2001),

4

and 0 otherwise, leading to the following equation:

Identification Strategy

Since our model relies on observational data, several observed and unobserved variables may influence whether new ventures apply for trademarks and whether they acquire VC seed funding, so we use a rich set of controls and 2SRI models.

Controls

We use a rich set of controls to reduce endogeneity concerns with regard to omitted variable bias. We include several time-invariant controls that are determined at a venture's founding. In particular, the characteristics of the founding team, including the founders and the first managers, exert an enduring and stable influence on a new venture (Zacharakis and Meyer 2000). We control for the founding team's education since highly educated founders are unlikely to engage in low-quality ventures given high opportunity costs (Ko and McKelvie 2018). Further, their marketing experience is likely to direct the venture's attention to trademarks and to have a positive impact on seed funding because of their inclination toward customer-oriented product developments (Germann, Ebbes, and Grewal 2015). Technical experience might reduce the tendency to deal with trademark applications but can facilitate the acquisition of VC seed funding because of the strong technological products in which investors are interested (Zacharakis and Meyer 2000). In addition, when the founding team has prior startup experience, the team is likely to be informed about the need to protect intellectual property and to be familiar with seed funding requirements (Ko and McKelvie 2018).

Further, we control for whether the new venture operates in a business-to-business (B2B) or business-to-customer (B2C) setting. Brand protection tends to be particularly important in B2C settings (De Vries et al. 2017), and some types of investors focus on one or the other. Ventures also differ in terms of the extent to which they value creating awareness among stakeholders; a high level of importance attributed to building awareness might lead to trademark applications and put the venture on venture capitalists’ radar, opening doors to seed funding. To control for this confounding effect, we use the number of a venture's tags on Crunchbase, since being tagged with more category labels increases the probability of said venture being found by investors. For similar reasons related to building awareness, we control for the number of the venture's social media accounts (taking Twitter, Facebook, and LinkedIn into account) (Van Balen, Tarakci, and Sood 2019). 6 Finally, we control for a venture's location since a location in a startup cluster may influence its ability to acquire seed funding given its proximity to VC investors and the ability to learn about trademark applications from closely located peers (Gittelman 2007).

Unobserved variables may be present that can change over a new venture's first months. During the first months, functional positions emerge. We control for the presence of a CMO since a dedicated marketing manager is likely to deal with trademarks and signal professionalism to investors (Homburg et al. 2014). We also control for the presence of a chief technology officer (CTO) since a CTO, while possibly not inclined to allocate the venture's resources to trademarks, can be a positive signal (e.g., of technological expertise) to investors. Legal expertise in the venture can drive trademark applications and be appreciated by investors as a signal of a professional venture, so we control for legal expertise among the venture's members. Further, we control for the venture's size (founders, managers, and key employees, as reported on Crunchbase), as larger ventures have more resources to deal with intellectual property protection, and venture capitalists might conclude that the venture has strong growth aspirations. The venture's share of women can play a role since female leaders might turn to trademark applications (e.g., because of more careful managerial approaches often found in female leaders). Research also indicates that venture capitalists tend to have a bias toward male entrepreneurs (Guzman and Kacperczyk 2019).

Further, trademark applications might be enabled by the venture's financial resources in a given month, which can originate from angels and public grants before VC seed funding. At the same time, such angel investments and public grants can send a positive reputation signal and the likelihood of progress enabled by these early investments (Hottenrott and Richstein 2020). Therefore, we control for such pre-VC-funding investments. Personal savings from founders might also play a role in this respect, although founders are typically more willing to invest their time and energy than they are their own money. Still, the founders’ work experience, during which money could be saved, can capture a part of these available financial resources.

Time-varying confounders might also affect a venture's innovativeness. As a strong driver of VC funding (e.g., Haeussler, Harhoff, and Mueller 2014), patent activity might indicate a tendency to protect intellectual property, so we control for patent ownership. Patents can also result in products that require trademark applications. Finally, we control for potential time-varying variables in the industry environment. Some industries, such as industries with strong competition, are likely to require trademarks. Extant research also indicates that VCs prefer volatile industries where opportunities emerge regularly, so we control for the industry's competitive intensity and technological uncertainty. We also include industry-fixed effects on the division level in the relevant models. (See Web Appendix W7 for a translation of division levels to two-digit SIC levels.) Finally, since more money in the market increases new ventures’ chances of receiving VC investment, we control for annual VC funding in the United States at the level of the venture's state to capture the seed funding that was available for young ventures. Because this control is correlated with our instrument, we prevent multicollinearity following Keller, Geyskens and Dekimpe (2020) and Ter Braak, Dekimpe, and Geyskens (2013) by removing the time trend from annual VC funding in the United States at the level of the venture's state. Specifically, we regress this variable on time-fixed effects. Then we include in the first stage and the second stage of the 2SRI model the residuals as a control that captures the VC funding amount that was available to each venture. In the uncorrected model without an instrument, we use annual VC funding on the U.S. level as a control without removing the time trend and, as an alternative approach, replace the level of annual VC funding in the United States with year fixed effects. Web Appendix W9 describes all measures.

2SRI model

Despite careful selection of control variables, the possibility remains that unobserved factors influence whether a firm decides to apply for a trademark or succeeds in acquiring VC seed funding. Therefore, we use an endogeneity correction that involves an instrumental variable to account for unobservable differences between ventures that applied for trademarks and those that did not. Specifically, because of the binary nature of our independent variable and our nonlinear core model, we use a 2SRI model with a probit model 7 in the first stage and a Cox model in the second stage (Arora, Ter Hofstede, and Mahajan 2017; Tan, Chandukala, and Reddy 2021; Terza, Basu, and Rathouz 2008). We use a weighted average of trademark presence among peer ventures as an instrument using the categories from Crunchbase (e.g., e-commerce, software) to identify peer ventures. (See Germann, Ebbes, and Grewal [2015] for a similar instrument for CMO prevalence.) Since most ventures are assigned to multiple categories, we create a weighted average of trademark prevalence among a venture's partially overlapping peers per year, defined as the weighted percentage of peers in the various categories with trademark applications in a particular year, excluding perfectly overlapping peers.8,9 We also include a squared term of our instrument to arrive at an effect with diminishing returns. (See also Nath and Bharadwaj [2020] and Dieterle and Snell [2016].) 10

We argue that the instrument is exogenous since both the academic literature on VCs and that on VCs’ practice suggest that VCs have three primary reasons for not comparing peers as investment targets but vet each venture in isolation. The first reason is that ventures that apply for seed funding do so at an early stage, when they have no product that is ready for commercialization, so the evaluation of each venture's potential is highly uncertain. Comparing two highly uncertain “potentials” is difficult and unlikely to produce useful insights (Ramsinghani 2014). The second reason that VCs do not compare peers as investment targets is that, while ventures typically remain generally in the markets and industries in which they started, their offerings often change (Blank 2014). Comparing ventures that are still likely to pivot in this way is not meaningful since it is unclear whether they will end up as competitors. Third, instead of comparing early-stage ventures that are applying for seed funding, VCs tend to use blueprints for successful venture-building to compare ventures that have some history of successful and/or unsuccessful investments (Fried and Hisrich 1994). Since our instrument relies on partially overlapping peer groups, a direct comparison is even less likely. To reduce the influence of industry effects on the firm and its peer groups, we also exclude perfectly overlapping peers from our calculation of the weighted average among industry peers and include division-level fixed effects in the first-stage regression (Germann, Ebbes, and Grewal 2015). The correlation between the instrument and the acquisition of seed funding is low (r = .01).

We argue that our instrument is relevant because founders are known to network extensively with their founder peers and imitate their peers’ best practices to reduce their uncertainty (Elfring and Hulsink 2007; Lieberman and Asaba 2006). The entrepreneurship literature also argues that founders and new ventures typically turn to role models that are at least partly like themselves, as industry peers tend to be (Bosma et al. 2012). Therefore, we expect peers’ trademark-related decisions to have a positive effect on the new venture's decisions but expect the effect to diminish as peers’ trademark applications increase in number. In line with Bikhchandani, Hirshleifer, and Welch (1992), we expect that a low-level increase in peers’ trademark applications signals that these peers are role models that have superior information about the trademark application decision, which encourages the new venture to pursue such applications as well. As founders network with and observe their peers to learn from their behavior and address their own uncertainties, founders are also likely to spot peers that have applied for trademarks. We base on Bikhchandani, Hirshleifer, and Welch our expectation that, as the prevalence of peers’ trademark applications increases, a venture perceives additional peers with trademarks as imitators of the initial adopters, so their trademark applications are less informative and have less effect on the venture. As a result, low to medium numbers of peers that adopt trademarks have a strong effect on a venture, while medium to high numbers have a weaker or even no additional effect.

Empirically, the regression that includes the instrument (including the squared term 11 ) has a significantly better fit than the regression that does not (χ2 = 10,576, p < .001), indicating sufficient instrument strength. The graphic representation in Web Appendix W10 displays the instrument's effect on the treatment, which shows a positive effect with diminishing returns (within the range of the instrument).

We first use a probit model to estimate the effect of our instrument and all control variables on the trademark applications of venture i in period t using the cumulative standard normal distribution function (Φ). This approach allows us to model trademark application as a time-varying variable, as indicated in the following equation:

Results

Descriptive Statistics and Model-Free Evidence

Web Appendix W11 provides descriptive statistics for our variables. (See Web Appendix W12 for more visualizations, including distributions of core variables.) Most correlations between variables are low. The only correlations above |.30| are those between founding team experience-related variables (.33–.48). Out of our full sample of 5,370 firms, about 43% (2,312 ventures) obtained VC seed funding throughout our observation period. Of these funded ventures, almost 37% received seed funding within the first year of the foundation. The average time to seed funding is 819 days, with a median of 591 days. About 26% (1,388 firms) of the ventures in our sample applied for at least one trademark either before acquiring VC seed funding or before the end of the observation period. The mean firm age at trademark application is 822 days. Of the firms that filed for a trademark, 26% did so no later than six months after foundation, and an additional 14% did so during the first year after foundation. About 46% of the ventures that file for a trademark filed only one trademark application prior to their seed funding events or the end of the observation period. The average number of trademark applications before seed funding is .72, and the highest number of applications is 37. When ventures apply for their first trademark, they target, on average, only 1.5 Nice classes (median = 1), so they apply for their first trademark in a limited number of markets.

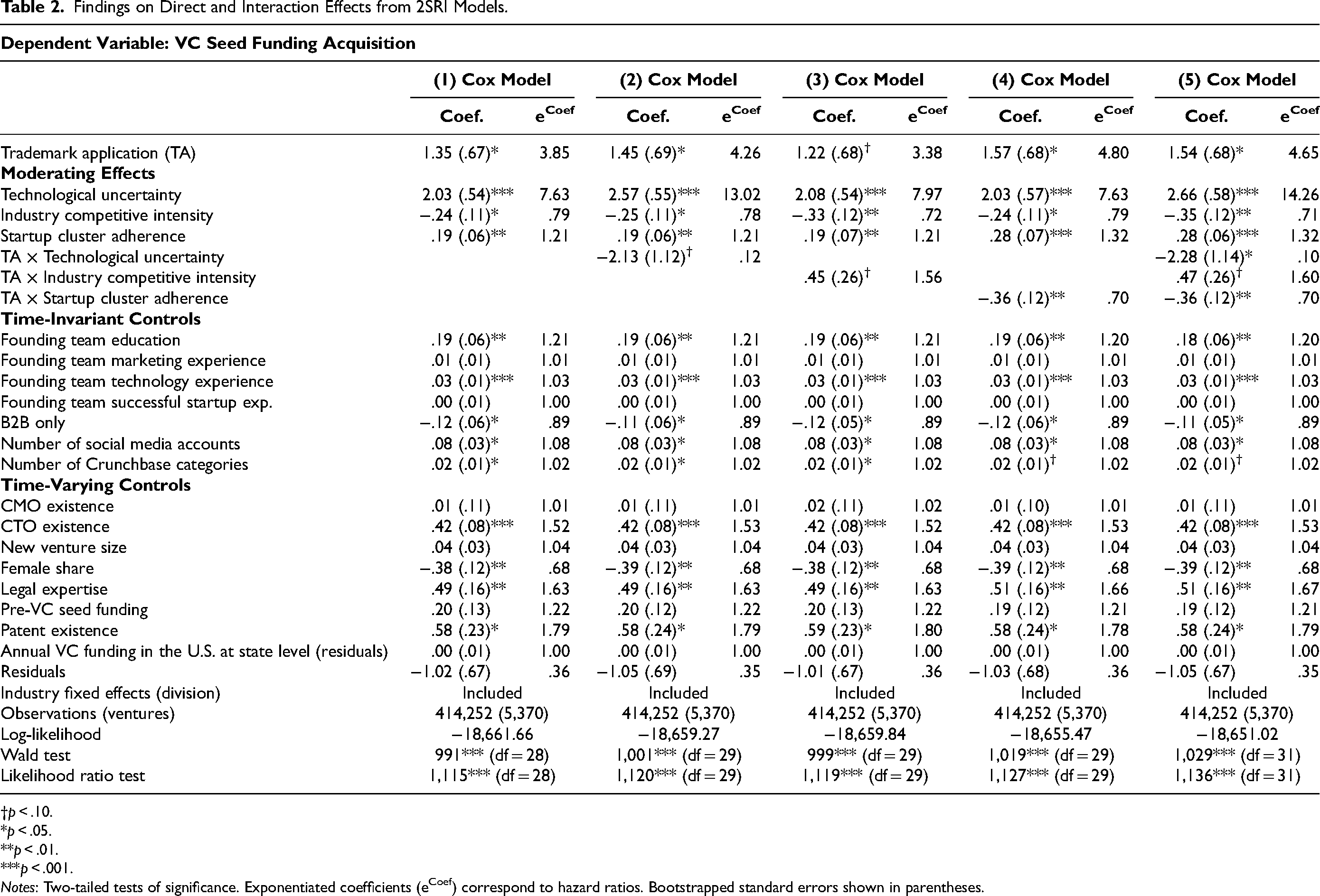

Main Findings on Direct Effect

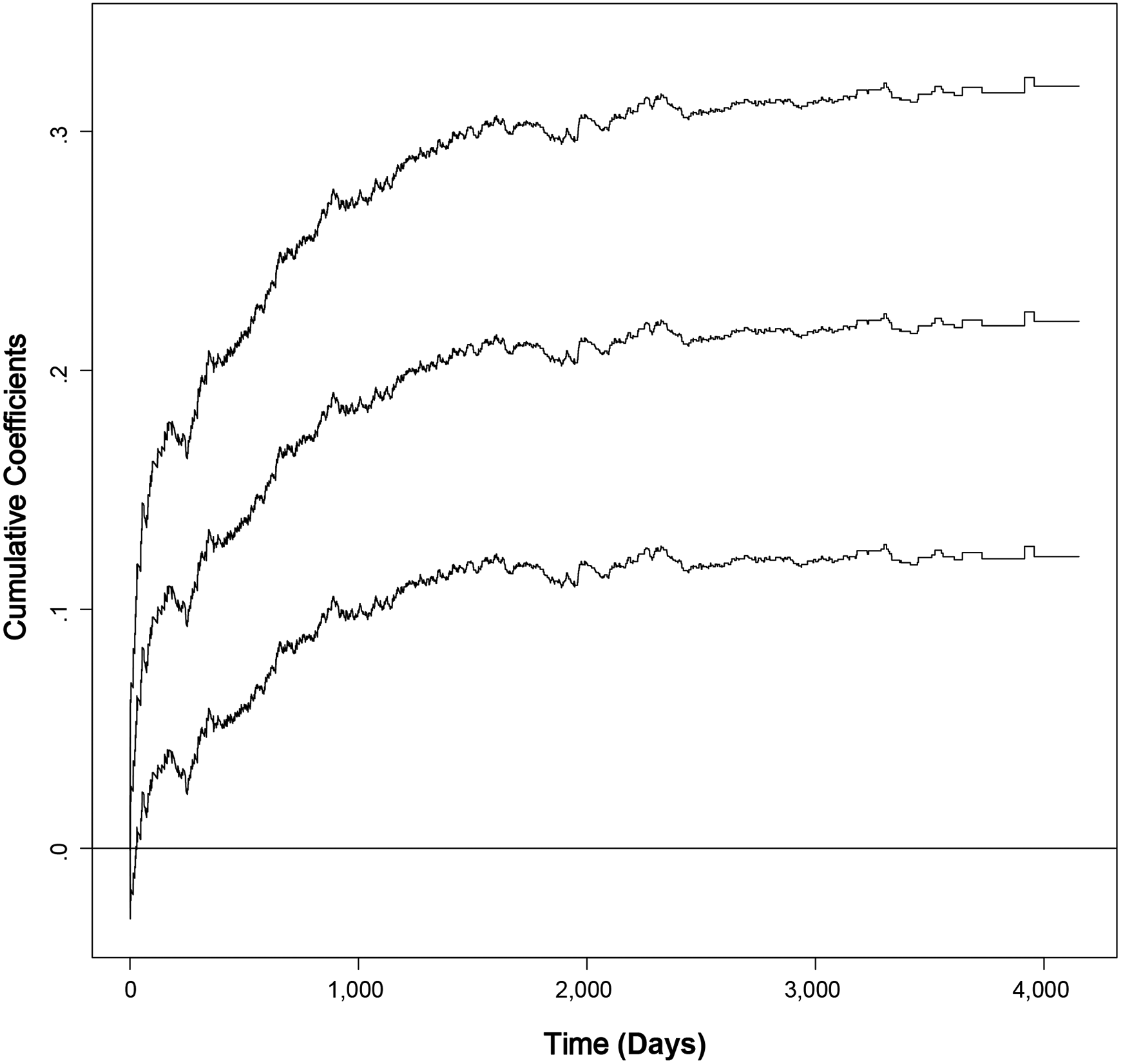

Table 2 shows the results of the 2SRI models. Web Appendix W13 shows the uncorrected results of our basic models. 12 Table 2 shows a significant and positive association between having trademark applications and acquiring VC seed funding (eCoef = 3.85, p < .05; Model 1). 13 The fitted Aalen model (Model 7 in Web Appendix W13, and Figure 2 based on Web Appendix W13) also exhibits a significant and positive effect, supporting H1a.

Cumulative Coefficient Plots for Trademark Applications’ Effect on VC Seed Funding Acquisition (Direct Temporal Effect in Aalen Model).

Findings on Direct and Interaction Effects from 2SRI Models.

p < .10. *p < .05. **p < .01. ***p < .001.

Notes: Two-tailed tests of significance. Exponentiated coefficients (eCoef) correspond to hazard ratios. Bootstrapped standard errors shown in parentheses.

The p-values of both the Kolmogorov–Smirnov test (at least p < .01) and the Cramér–von Mises test (p < .001) are smaller than .05, suggesting that trademark applications be modeled as a time-varying effect in the fitted Aalen model (Martinussen and Scheike 2006). Graphic evidence for the positive and time-varying character of trademark applications is provided in Figure 2. The cumulative coefficients graph for trademark applications in the fitted Aalen model shows a strong positive slope until t = ∼1,000 days, which is particularly positive during the first ∼100 days. After ∼1,000 days, the slope stagnates, suggesting that the positive effect disappears over time, in line with H1b.

Main Findings on Moderating Effects 14

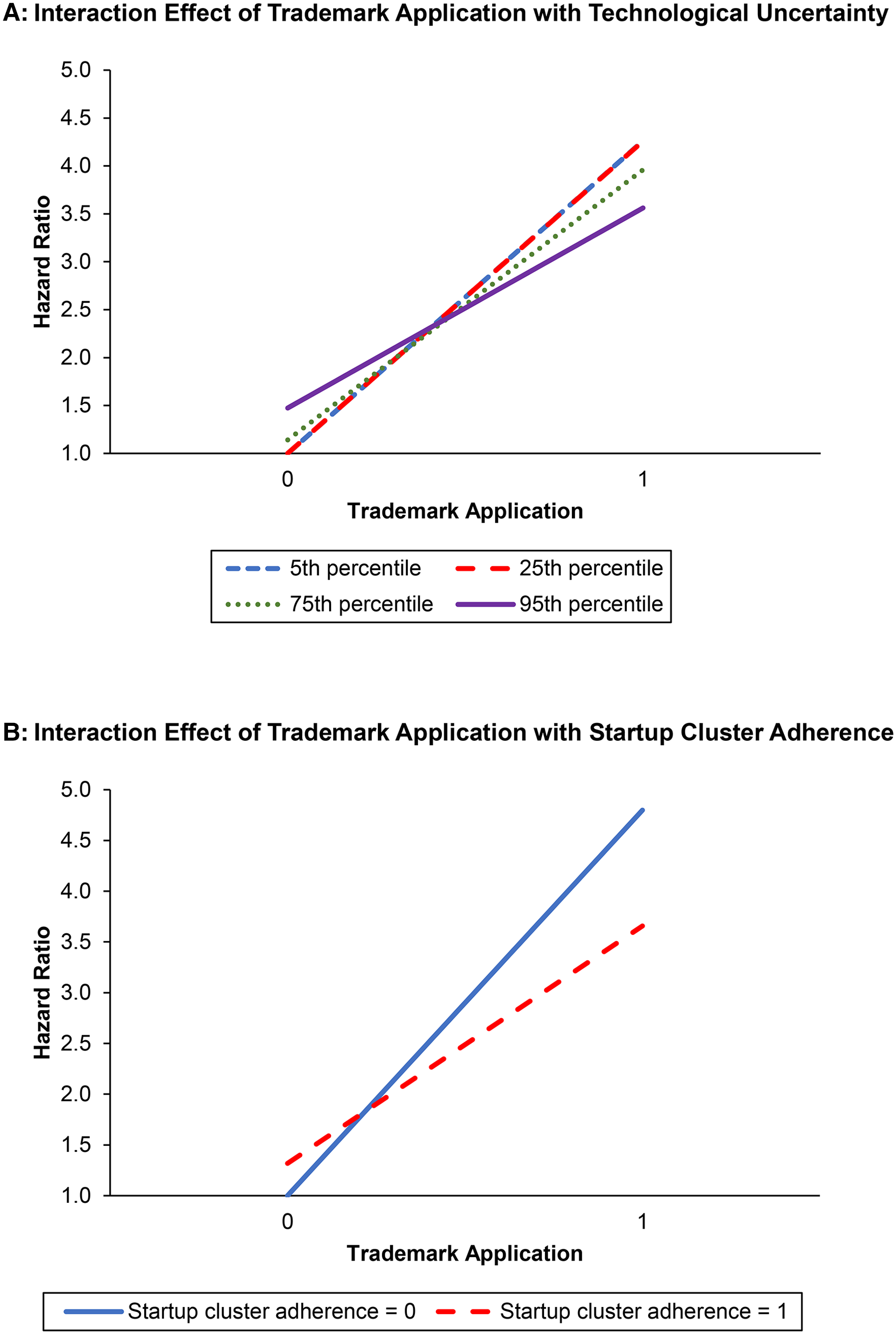

Next, we model interaction effects using an extended Cox model. As Table 2 shows, the effect of a trademark application × technological uncertainty is negative and significant (eCoef = .10–.12, p < .05–.10; Models 2 and 5). We plot hazard ratios for various values of the moderator based on Model 2 in Table 2. As Figure 3 (Panel A) indicates, trademark applications’ positive effect is stronger when technological uncertainty is low than when it is high, supporting H2a. Simple slope tests based on Model 2 in Table 2 indicate that the effect of trademark application is not significant (eCoef = 3.09, p > .10) when technological uncertainty is high (95th percentile) whereas the effect is positive and significant (eCoef = 4.26, p < .05) when technological uncertainty is low (5th percentile). 15

Interaction Plots Based on Cox Models (Dependent Variable: VC Seed Funding Acquisition, Based on Models 2 and 4 in Table 2).

The effect of a trademark application × industry competitive intensity is positive and weakly significant, as shown in Table 2 (eCoef = 1.56–1.60, p < .10; Models 3 and 5), so we find only weak support for H2b. The effect of a trademark application × operating in a startup cluster is negative and significant (eCoef = .70, p < .01; Models 4 and 5). As indicated in Figure 3 (Panel B), which is based on Model 4 (Table 2), the positive effect is stronger when the venture is not located in a startup cluster than when it is. Simple slope tests based on Model 4 (Table 2) also indicate that a trademark application has a stronger effect when the venture is not located in a startup cluster (eCoef = 4.80, p < .05), as the effect weakens when the venture is located in a startup cluster (eCoef = 3.34, p < .10), supporting H3.

Robustness Checks

Propensity score matching

Since ventures self-select into applying for a trademark, control and treatment groups may differ systematically. While we used an instrumental variable approach to account for potential differences between ventures that applied for trademarks and those that did not, all endogeneity corrections come with limitations (Papies, Ebbes, and Van Heerde 2017), so we also use a propensity score matching approach to account for a selection bias (Atefi et al. 2020; Haan et al. 2018; Kumar et al. 2016). Using this approach leads to findings that are similar to those of our main models. (See Web Appendix W15 for details.)

Alternative measures of the independent variable

In an additional analyses, we also test whether the number of trademark applications plays a role. The number of trademark applications is positively related to the likelihood of acquiring seed funding (eCoef = 1.04, p < .05). Further analyses indicate a positive effect with diminishing magnitude. (See Web Appendix W16.)

Alternative measures of technological uncertainty and industry competitive intensity

In robustness checks, we replace technological uncertainty with industry uncertainty, measured as the ratio of selling, general and administrative expenses to total sales in the industry. This analysis renders highly consistent results. (See Web Appendix W17.) We also replace our measure of competitive intensity, the four-firm concentration ratio, with the Herfindahl–Hirschman index. We find no support for H2b.

Alternative models

We validate our findings with two alternative models, an accelerated failure time Weibull model and an accelerated failure time log-logistic model (Kleinbaum and Klein 2012). Both models indicate a significant and positive effect of trademark application on seed funding.

Discussion

Based on legitimacy theory and the literature on venture capitalists’ decision-making, our findings indicate that new ventures’ applying for trademarks right at the beginning increase their chances of obtaining VC seed funding. The effects of trademark applications as drivers of VC seed funding are greater when technological uncertainty in the industry is low and when the new venture is not located in a startup cluster.

Research-Related and Managerial Implications

Among this study's research-related implications is, first, its contribution to extending marketing-finance research past its stock market focus (e.g., Edeling, Srinivasan, and Hanssens 2021) by incorporating earlier investors and how they perceive marketing-related variables. Specifically, complementing Homburg et al.’s (2014) insight that a CMO's human capital is related to the acquisition of VC seed funding, we show that these early investors appreciate a new venture's using its scarce time resources to pursue trademark applications as an early marketing action. This effect materializes at a stage in which the new venture typically has no fully developed product and no paying customers. Therefore, the benefit of trademark applications that venture capitalists see at this stage can hardly originate from immediate customer reactions. Rather, our findings inform founders that trademark applications appear to convey an early marketing-related message to venture capitalists about the new venture's professionalism in, for example, protecting its market-related assets and upcoming product introductions that positions it as a legitimate player meriting seed funding. Thus, our findings suggest that these positive effects outweigh the potential downsides of trademark applications (e.g., providing information on targeted markets to competition) (Fink et al. 2022). The effect of a trademark application is relevant economically, as our results suggest that applying for a trademark increases the likelihood that a new venture will receive seed funding in a particular month by a factor of 1.38–3.85 from its baseline, depending on the model. This notion is realistic given venture capitalists’ expectation that their ventures will pursue a professional market-oriented approach, increasing the chances for ventures’ market success which is so essential for venture capitalists’ return. Very early trademark applications foreshadow such success, at least to some degree. 16

The second research-related implication of this study is that, even within the temporally limited stage that may lead to VC seed funding, the effect of trademark applications is time-contingent. Thus, what qualifies as a marketing-related legitimizing force must be evaluated against the new venture's current situation since venture capitalists’ legitimacy considerations can change quickly, a notion that certainly reflects the highly dynamic nature of a young, evolving venture. We find that trademark applications are a particularly important information cue during ventures’ first months, which challenges, at least for this specific marketing action, the often shared wisdom (e.g., in organizational life cycle models) (Kazanjian 1988) that marketing action is useful only when a fully developed product is ready for commercialization. In this way, founders learn about the importance of timing in marketing-related decisions.

Third, in line with legitimacy theory's notion that legitimacy considerations are context-dependent (Zimmerman and Zeitz 2002), this study contributes the finding that legitimacy considerations related to trademark applications are embedded in external and internal contingencies. Our findings suggest that trademark applications are not per se appreciated by venture capitalists but are a legitimizing force only when they benefit the new ventures. This result is in line with the understanding that venture capitalists value a new venture's resource commitments only when these commitments are necessary in light of the venture's extremely scarce resources (Gompers 1995). When trademark applications might become outdated quickly after causing unnecessary (time) resource investments (e.g., because of high technological uncertainty) or when marketing-related knowledge is accessible elsewhere (such as when the venture is part of a startup cluster), trademark applications’ legitimizing force in the eyes of venture capitalists declines. When technological uncertainty is high, we do not even find a significant effect of trademark applications on seed funding. Taking into consideration founders’ extreme resource constraints after the foundation and before the first VC funding, our findings suggest that founders should not dedicate their scarce resources to trademark applications when technological uncertainty is high, but to other important challenges a venture faces at this stage.

This observation resonates with Homburg et al. (2014), who find in particular that the CMO's human capital matters for the acquisition of VC seed funding and that this relationship is also highly industry dependent. The strong situational dependency, and especially industry dependency, is also a potential explanation for why we do not find a direct effect of CMO presence in our sample when we include the variable as a control as opposed to Homburg et al. (2014) who find such a positive direct effect. The combination of their findings and ours suggests the absence of marketing-related “silver bullets” for increasing the chances of acquiring VC seed funding but that fine-tuned marketing-related levers that are tailored to the venture's situation are necessary.

Finally, our findings suggest that, from the venture capitalist's perspective, startup clusters reduce the legitimizing force that trademark applications can have for ventures. Startup clusters appear to offer access to resources that provide marketing-related legitimization, suggesting that the entrepreneurial marketing literature should differentiate between new ventures that are located in such clusters and those that are not.

Limitations and Avenues for Future Research

Our study has several limitations that pave the way for future research. First, the question concerning which marketing actions are related to subsequent funding rounds after seed funding remains. We tested whether trademark applications play a role in funding success after VC seed funding. For this analysis, we extended the original dataset to include more funding rounds but found no significant association between trademark applications and second-round VC funding. Since subsequent funding rounds are granted only when the venture has a product and a customer base, the set of marketing actions increases, so research could determine which other marketing-related actions facilitate success in acquiring post–seed funding.

Second, our sample is limited to U.S.-based ventures. Since prior research suggests significant differences between investor behavior across nations and differences in economic situations across nations (e.g., Gordon, Goldfarb, and Li 2013), future research could validate our findings in other nations. As such, negative developments or outlooks at the national level may increase trademark applications’ effect, since venture capitalists are generally skeptical that new products will meet market demands, a concern that trademark applications might mitigate.

Third, while we focus on industry- and location-related moderators of the association between trademark applications and the likelihood of obtaining VC seed funding, future research could extend the set of moderators. In an additional analysis, we estimated trademark application's interaction effects with the venture's number of social media accounts and found a positive and significant interaction effect between the number of social media accounts and trademark applications (eCoef = 1.21, p < .01). These findings could indicate that the effectiveness of trademark applications increases when ventures also communicate their activities. Apparently, investors appreciate when the signals trademarks send are complemented by “hands-on” marketing communication to stakeholders, including potential customers, a notion on which future research could elaborate.

Fourth, we focus on whether a firm receives funding as a binary outcome. Our additional analyses show that the amount of VC funding is higher for firms that have applied for trademarks, which could mean not only that trademark applications help ventures get seed funding, but also that ventures that make these applications raise more money. As Fried and Hisrich (1994) point out, the deal-making process is divided into stages, and funding volumes are typically discussed once there is an initial commitment to invest. Trademark applications and their effects on investors may help improve the venture's negotiating power related to funding volumes or, because trademarks signal commercialization in the near future, indicate that the venture's understanding of market sizes is well established, resulting in increased valuation of the venture and similarly increased funding volumes. Motivated by this preliminary finding, future research could delve more deeply into how trademark applications affect such negotiations.

Finally, our findings and additional analyses indicate that the effects of both patent applications and trademark applications on seed funding wane as investors evaluate the venture's progress in terms of customer feedback and development of prototypes (Hoenen et al. 2014; Hsu and Ziedonis 2013). While the effects of patent applications and trademark applications both wane, patent applications’ effects hold longer. One explanation for this result might be that patents have more potential value for future product developments than a typically narrow trademark application does. Future research could look more closely into when and why these effects wane.

Supplemental Material

sj-pdf-1-mrj-10.1177_00222437241272192 - Supplemental material for Zooming In on the Very Early Days: The Role of Trademark Applications in the Acquisition of Venture Capital Seed Funding

Supplemental material, sj-pdf-1-mrj-10.1177_00222437241272192 for Zooming In on the Very Early Days: The Role of Trademark Applications in the Acquisition of Venture Capital Seed Funding by Verena Rieger, Anne Dreller and Andreas Engelen in Journal of Marketing Research

Footnotes

Acknowledgments

The authors thank the JMR review team for their constructive comments during the review process.

Authors Contributions

This article is based on the second author's doctoral dissertation.

Coeditor

Kapil Tuli

Associate Editor

P.K. Kannan

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.