Abstract

Retailers, service providers, and manufacturers have discovered that complementary optional insurance is an attractive source of profit and frequently charge substantial insurance prices compared with the price of the product to be insured. The implicit assumption behind this pricing strategy is that product purchase decisions are independent of the insurance offer. The authors question this assumption and propose that consumers interpret the price of insurance as a risk signal with respect to the underlying product. Perceived risk, in turn, negatively affects consumers’ decision to purchase the product in a given purchase situation. The results of a survey, three online experiments, and two studies using transactional data provide evidence for the proposed insurance price risk signal. The findings reveal that perceived risk mediates the link between the relative insurance price level and consumers’ decision to purchase the underlying product. Offering other optional add-ons and providing objective risk information weakens the insurance price risk signal.

In an attempt to provide a comprehensive shopping experience and boost profits, companies are increasingly offering insurance policies as an attractive add-on service to their core business (Chen, Kalra, and Sun 2009; Jiang and Zhang 2011). The market for usage-based insurance is estimated to grow with a compound annual growth rate (CAGR) of 29% between 2019–2026 and reach a market value of approximately $190 billion by 2026 (Acumen Research and Consulting 2019). Likewise, the global extended warranty market size is projected to reach $170 billion by 2027, growing at a CAGR of 7.4% from 2020 to 2027 (Allied Market Research 2020).

Consumers can purchase insurance for everyday items such as laptops, USB cables, washing machines, travel insurance for a specific holiday, or insurance that covers adventurous activities such as canyoning on a particular date. What all these insurance policies have in common is that they are (1) optional, (2) tailored to cover a specific product or event, and (3) offered as an additional service by retailers, service providers, and manufacturers.

The (relative) insurance price, when compared with the price of the product to be insured, can be quite substantial 1 (Baker and Siegelman 2013; Chen, Kalra, and Sun 2009) and can lead to companies earning contribution margins of up to 80% (Chu and Chintagunta 2009; Jindal 2015).

The implicit assumption behind this pricing strategy is that consumers’ product purchase decision is independent of the insurance offer (Jindal 2015). Thus, in practice, companies set insurance prices assuming that product sales are not affected by the insurance offer, as consumers first choose a product, which is their primary concern, and then decide whether to add insurance (i.e., take-it-or-leave-it decision). Two expert interviews with top managers at large online retailers confirm this assumption. 2 Both managers state that (1) add-on insurance makes “a significant contribution to sales” and that (2) product and insurance purchase decisions are independent, as “consumers first decide upon a product and then think about insurance.”

In this article, we question the assumption that the decision to purchase a product is independent of the insurance offer, as the insurance offer is complementary to the underlying product and reveals information about the same. In particular, we propose that the relative insurance price serves as a cross-product risk signal affecting consumers’ decision to purchase a product.

To investigate this potential violation of the independence assumption, we propose the following research questions: (1) Do consumers interpret the price of insurance as a cross-product risk signal with respect to an underlying product? (2) If so, how does the insurance price risk signal affect consumers’ purchase decisions? (3) Which factors moderate the influence of the insurance price risk signal on consumers’ purchase decisions?

To answer our research questions, we develop hypotheses based on the literature on add-on insurance and the informational role of price. We then explore consumers’ inferences from add-on insurance prices in an open-ended survey (Pilot Study). Subsequently, we test our hypotheses based on an initial examination of the relationship between add-on insurance prices and product purchases (Study 1) using the publicly available Informs Society of Marketing Science (ISMS) durable goods data set (Ni, Neslin, and Sun 2012), three experimental studies (Studies 2, 3, and 4), and a field study (Study 5) with data from a large European online retailer for consumer electronics.

Our results show the following: (1) Consumers establish a link between the relative insurance price level—when compared with the underlying product price—and the perceived risk associated with the product. (2) A relatively high insurance price negatively affects consumers’ decision to purchase the product in a given purchase situation. Moreover, consumer risk perceptions mediate the link between the relative insurance price level and consumers’ decision to purchase the product. (3) The strength of the insurance price risk signal is weaker when (a) objective information on the actual product risk is available and when (b) other optional add-ons for the product are available (in addition to insurance).

Our research contributes to existing research on insurance and on the informational role of price. First, we investigate the relationship between products and insurance from a new perspective. While industry-pricing strategies assume independent decision-making for add-on insurance and product (Jindal 2015), we show that consumers’ product purchase decision is not independent of the insurance offer. Second, we show that consumers use the relative insurance price as a cross-product risk signal. Complementing existing literature on price perception, we show that price may be perceived not only as an indicator of quality and sacrifice (Bornemann and Homburg 2011; Völckner 2008) but also as an indicator of perceived risk: the higher the price of add-on insurance, the stronger the insurance price risk signal with regard to the underlying product.

Our findings are managerially relevant, as many companies offer insurance as an additional service to their customers without being fully aware of the consequences of relatively high insurance prices on consumers’ product purchase decisions. While insurance is supposed to provide consumers with a sense of security, we show that offering insurance at a high price compared with the product price can backfire, leading consumers to reconsider their purchase decision. Companies can thus gain a better understanding of consumers’ decision-making from our research and use these insights to improve their offers.

Related Literature

Literature on Optional Add-On Insurance

Despite the increasing prevalence of optional add-on insurance in practice, Lee and Venkataraman (2022, p. 644) recently noted that literature on add-on insurance “is relatively sparse in both theory and empirical evidence.” Existing research (also referring to terms such as “extended warranties” or “extended service contracts”) primarily examines drivers of add-on insurance purchase likelihood and willingness to pay for such insurance. For instance, the likelihood to purchase add-on insurance is positively related to the underlying product's hedonic value and price, negatively related to the price of the add-on insurance, and generally influenced by consumers’ comparison of the add-on insurance price and the fixed compensation that the insurer offers in the event of a failure (Abito and Salant 2019; Chark, Mak, and Muthukrishnan 2020; Chen, Kalra, and Sun 2009; Hogarth and Kunreuther 1995; Hsee and Kunreuther 2000).

Taking a broader perspective, Jindal (2015) develops a model to delineate the role of loss aversion in consumers’ choice of add-on insurance in which consumers simultaneously consider both product and add-on insurance. In the examined setting, however, failure probabilities and repair costs for the product (washing machines) are provided ex ante to consumers (p. 46).

Abito and Salant (2019) make the explicit assumption that only the product price, but not the add-on insurance price, is observable for consumers. They then quantify consumers’ willingness to pay for add-on insurance and find that this willingness to pay for insurance is primarily driven by consumers’ (often distorted; see also Huysentruyt and Read 2010) estimation of the insured product's failure probability. The potential repair cost is less influential (and assumed to be a deterministic fraction of the price of the insured product).

Our research systematically extends existing literature on add-on insurance. First, it is striking that existing research typically separates the product and insurance purchase from one another (e.g., Chark, Mak, and Muthukrishnan 2020) or restricts the focus to how characteristics of the core product (such as its hedonic value) influence the insurance purchase decision (e.g., Hsee and Kunreuther 2000). Our focus, however, is on understanding the impact of insurance properties on the purchase decision for the core product (irrespective of whether consumers would also purchase the insurance).

Second, we extend research by Abito and Salant (2019) by acknowledging that consumers typically do observe the prices of add-on insurance (which differentiates it from base warranties; Chu and Chintagunta 2011), and we address the call by Jindal (2015) to examine how consumers form beliefs regarding a core product's failure probability (which is typically not available as objective information when making the purchase). We propose that regardless of whether a consumer would purchase add-on insurance for a given product, the price of the add-on insurance will be used as an input by consumers to form beliefs regarding the core product's risk in terms of failure probability—and hence act as a cross-product risk signal. Before we derive our hypotheses, we therefore briefly review central findings on how consumers form price-related beliefs (i.e., the informational role of price).

Literature on Price Signals

To make an informed purchase decision, consumers take into account the available product information (i.e., cue utilization theory; Olson and Jacoby 1972). If tangible product attributes (intrinsic cues) are not available (e.g., for services, activities) or difficult to evaluate, consumers frequently rely on product-related attributes apart from the tangible attributes—referred to as extrinsic cues. In this regard, research has particularly focused on the role of price as an extrinsic cue in product evaluations (Rao and Monroe 1988).

Research on consumer perception of price information distinguishes between two roles that price can assume—in addition to its role as an indicator of monetary sacrifice, consumers may use price as an extrinsic cue to infer properties about the product itself, typically its level of quality (price–perceived quality relationship; Erickson and Johansson 1985; Völckner 2008).

However, the informational role of price may also extend to product properties other than quality and even to the price-setting rationales underlying the observed price. For instance, Grewal, Gotlieb, and Marmorstein (1994) show that consumers may use price information to evaluate a product's performance risk, such that higher product prices may signal lower levels of performance risk (price–perceived risk relationship). In the context of medication pricing, Samper and Schwartz (2013) show that consumers use the price of lifesaving health goods to infer disease-related risks (with lower medication prices signaling higher levels of risk). The authors also show that consumers infer the rules that govern pricing rationales for these types of products (medication for severe diseases needs to be accessible to everyone and should therefore exhibit lower prices).

Importantly, however, research on price perception has thus far focused on stand-alone or complementary products without considering cross-product effects. Therefore, in the case of product and insurance purchases, one would expect both purchase decisions to be independent since the respective prices only signal information about the product they refer to.

In contrast, we expect the insurance price to signal the risk associated with the underlying core product. Specifically, we propose a cross-product risk signal—the insurance price risk signal—which extends the concept of the informational role of price.

Conceptual Framework and Hypotheses

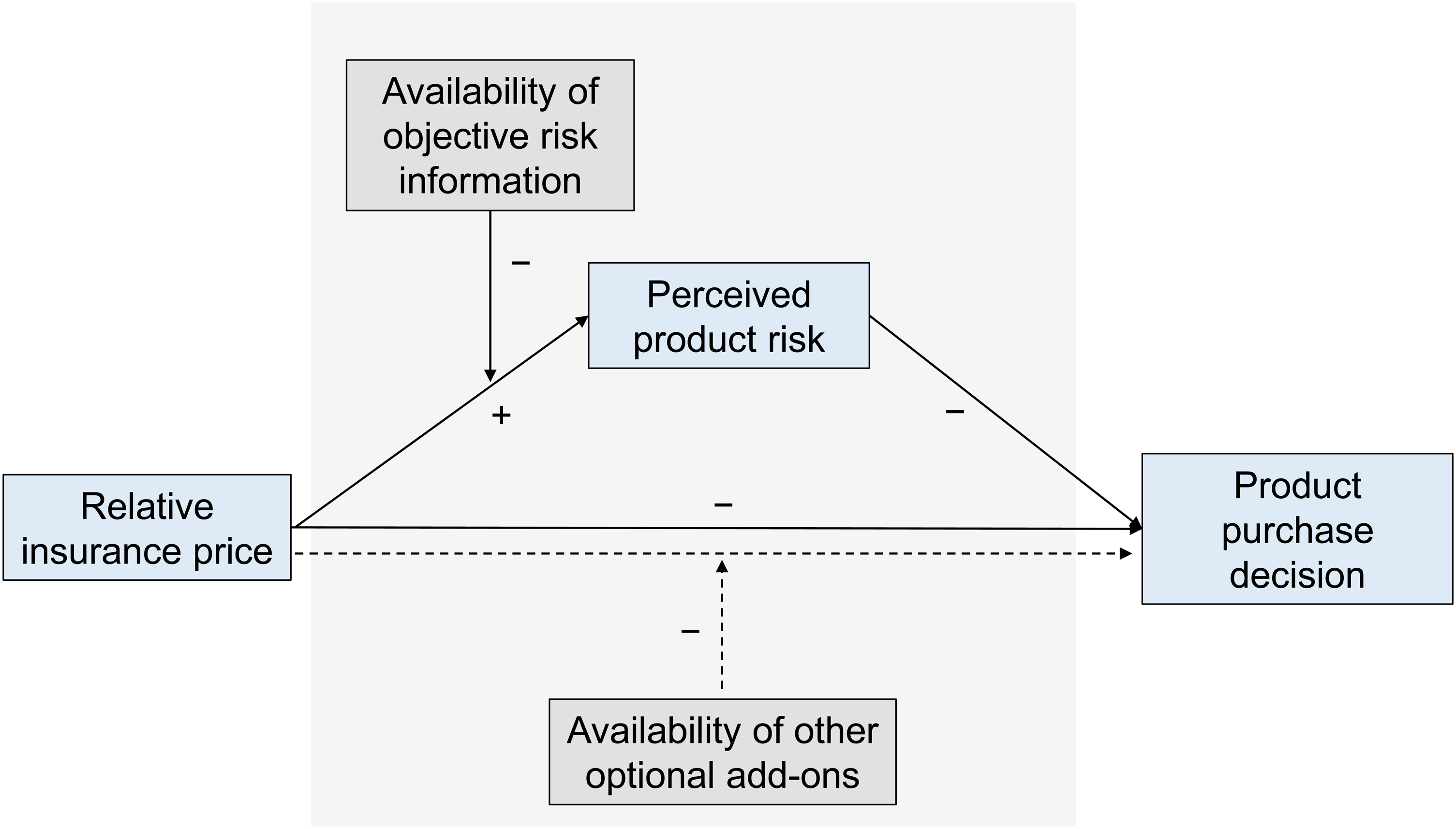

We argue that a higher relative insurance price, compared with the underlying product price, induces a higher level of perceived risk with regard to the core product (H1). Moreover, a higher relative insurance price negatively affects consumers’ decision to purchase the core product (H2a); this effect is mediated by perceived risk (H2b). The strength of the insurance price risk signal is contingent on the availability of more valid (i.e., objective) information on the actual product risk (weakening the indirect effect via perceived risk; H3) and on the availability of other add-ons (H4). Figure 1 depicts our conceptual framework investigating the impact of the relative insurance price on consumers’ decision to purchase the product.

Conceptual Framework.

The Effect of (Relative) Insurance Price on Perceived Risk and Purchase Decisions

While it is reasonable to assume that consumers rely on the insurance price (in terms of informational and sacrifice implications) when deciding whether to purchase insurance, we also propose that they use the insurance price as an informational cue when deciding whether to purchase the underlying product, irrespective of whether they would also purchase the insurance.

The literature typically describes the price of add-on insurance in relative terms with reference to the price of the underlying core product (e.g., extended-warranty-to-product price ratio, Abito and Salant 2019; standardized premium; Estelami, De Maeyer, and Estelami 2016). We assume that consumers also evaluate the insurance price in relation to the product price. Our line of reasoning follows the observation that consumers tend to evaluate numbers relative to a salient reference point (Thaler 1980). Since the add-on insurance price is inextricably linked to the properties of the underlying product, we argue that consumers compare the insurance price with the product price (which also equals the product's replacement cost in case of tangible products) and use the product price as an anchor (Morwitz, Greenleaf, and Johnson 1998) to evaluate the level of the insurance price.

Most consumers know from experience with common types of insurance that insurance premiums depend on risk-related factors (e.g., consumer characteristics and habits such as smoking for health insurance or age for car insurance; Parodi 2014). Specifically, the insurance price (priceinsurance) is a function of the occurrence probability of a negative event (Pr(defect)) times the insurance coverage plus a contribution margin for the insurance (priceinsurance = Pr(defect) × coverage + margin). Abito and Salant (2019) find that consumers’ willingness to pay for add-on insurance (without any knowledge of the price of the insurance) is driven by subjective estimates of product failure probability (Pr(defect)). This observation indicates that consumers indeed have a basic understanding of the risk-based pricing rationale underlying (add-on) insurance.

We hence propose that when consumers can observe the price of add-on insurance relative to the price of the underlying core product (and do not possess objective information on product-related failure or accident probabilities), they will—in line with cue utilization theory (Olson and Jacoby 1972)—rely on the relative insurance price as an informational cue to make risk-related inferences concerning the product. The risk that add-on insurance is supposed to cover refers to the consequences of an adverse event. The type of adverse event depends on the nature of the underlying product and may pertain to aspects such as product failure, accidents, and damage or harm caused by the product or service and its usage.

In line with this rationale and the observation that consumers’ willingness to pay for add-on insurance is driven by their estimates of product failure probability (Abito and Salant 2019), the relative insurance price can be interpreted as a risk signal with respect to the probability that an adverse event related to the core product may occur (e.g., failure probability, accident probability). We hence focus on perceived risk as “consumers’ uncertainty about product performance or ‘functional’ risk” (Folkes 1988, p. 13; Abito and Salant 2019).

We propose that a high relative insurance price triggers perceived risk, which in turn negatively influences consumers’ decision to purchase the underlying product. We hence focus on the common practice where insurance prices are observable by consumers before they make a commitment to purchasing a product (vs. drip pricing; Santana, Dallas, and Morwitz 2020).

Consumers who feel high levels of perceived risk should be more likely to engage in risk-reduction strategies (Dowling and Staelin 1994) and may reconsider or postpone their product purchase decision. We therefore hypothesize:

The Moderating Role of Objective Risk Information

Our rationale for the hypotheses is that consumers use the relative price of add-on insurance as an extrinsic cue to evaluate the risk associated with the underlying product. To further corroborate this reasoning and to introduce a boundary condition to the insurance price risk signal, we propose that the insurance price risk signal should be weakened if more objective information on product risk (i.e., actual failure/accident probabilities) is available to consumers. When different types of information with regard to an important criterion (in this case, product risk) are available, information with a higher relative diagnosticity or predictive value should be more influential in predicting the criterion value (Desai, Kalra, and Murthi 2008). Applied to the add-on insurance context, this implies that objective information on product risk will reduce the extrinsic cue's signaling effect as the latter is less informative about the criterion value (Miyazaki, Grewal, and Goodstein 2005). The availability of objective information on failure or accident probabilities is not only of interest as a theoretical boundary condition, as the provision of such information alongside the add-on insurance offer is even advocated by some researchers and policy makers to improve consumers’ decision-making (Abito and Salant 2019; Lunn, McGowan, and Howard 2018). We hence hypothesize:

The Moderating Role of Other Add-Ons (Attention-Competing Information)

Optional insurance is only one possible add-on that companies offer at the point of sale. For instance, firms may also offer add-ons such as product accessories like laptop cases and smartphone screen protectors or setup and installation.

The availability of more add-ons increases decision complexity (Chernev 2006) and diverts attention from the insurance as consumers try to also attend to the other available add-ons (Zhu and Dukes 2017). The availability of such attention-competing information may thus dilute the informational properties of the relative insurance price (Troutman and Shanteau 1976). It might even be that consumers do not attend to insurance but limit their processing to the add-ons they deem most relevant (i.e., selective attention; Bettman, Luce, and Payne 1998). We hence propose:

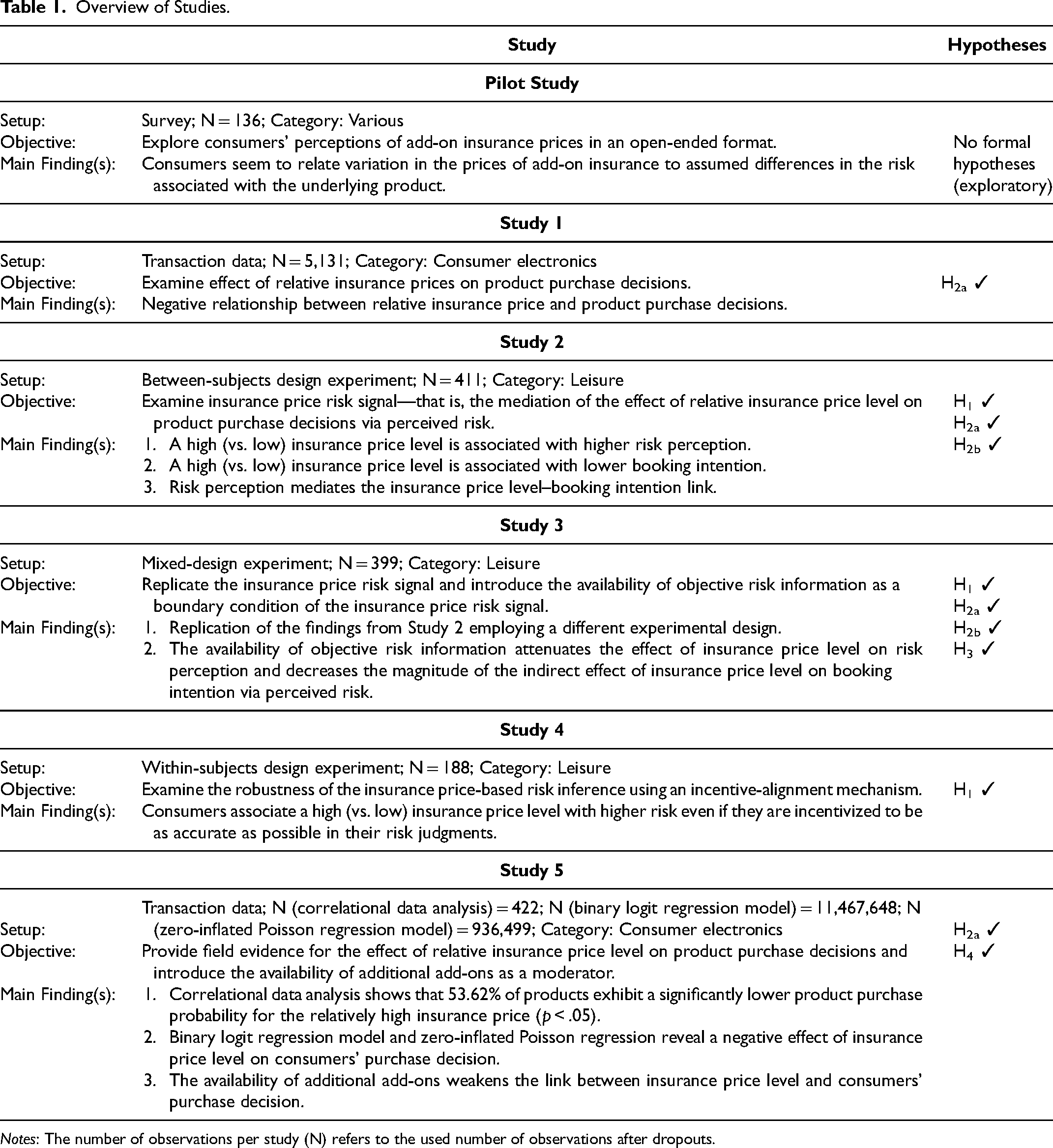

Overview of Studies

Our Pilot Study first explores consumers’ inferences from add-on insurance prices using an open-ended format. Study 1 then provides initial evidence for the link between the relative insurance price level and underlying purchases using a publicly available transactional data set from a consumer electronics retailer. We then present three scenario-based experiments (Studies 2, 3, and 4) and a large field study (Study 5). Study 2 employs a between-subjects design and reveals that consumers associate higher relative insurance prices with higher levels of risk in terms of product failure, leading to lower purchase intentions for the core product. Study 3 replicates these findings in a mixed design where we manipulate the relative insurance price level within-subjects and introduce the availability of objective product failure probabilities as a boundary condition. Study 4 employs a within-subjects design for an incentive-aligned assessment of consumers’ utilization of insurance price information to infer product failure probabilities. Finally, Study 5 uses transaction data from a large European online retailer to provide evidence for the direct link between relative insurance prices and product purchases for consumer electronics products. We also show that offering optional add-ons (in addition to insurance) weakens the negative effect of the relative insurance price on consumers’ purchase decisions. Thus, we show the impact of relative insurance price on different types of dependent variables that reflect consumers’ purchasing decisions with respect to the underlying core product. Our Institutional Review Board approved the research program. We provide an overview and the main findings of all studies in Table 1.

Overview of Studies.

Notes: The number of observations per study (N) refers to the used number of observations after dropouts.

Pilot Study: Consumer Inferences from Relative Insurance Prices

To gain initial insights into consumers’ actual inferences from add-on insurance prices, this pilot study explores consumers’ perceptions of add-on insurance prices in an open-ended format (for a detailed study description, see Web Appendix A).

We exposed 136 participants (recruited via Amazon Mechanical Turk) to a (randomly ordered) set of real add-on insurance offers and asked them to indicate (1) what they perceive as the main reason(s) for the variation of add-on insurance prices in the market and (2) what they regard as the main factor(s) that insurers take into account when determining the price of add-on insurance.

In a multistep process, two coders independently categorized the answers (intercoder reliabilities between .89 and 1.00; Perreault and Leigh 1989). With respect to the perceived reasons for variation of add-on insurance prices, participants most frequently mentioned risk-related reasons (failure likelihood; 60.29%), followed by insurance offer-related reasons (duration, coverage; 36.76%), the price of the core product (29.41%), market-related reasons (competition, demand; 25.74%), consumer-related reasons (age, experience; 23.53%), and profit-related reasons (10.29%). With respect to the factors that insurers take into account when determining the price of add-on insurance, participants most frequently mentioned probability-related factors (probability of failure; 66.91%), followed by cost-related factors (repair/medical treatment; 50.00%), the price of the core product (28.68%), and margin-related factors (21.32%).

This exploratory pilot study suggests that, among other reasons, consumers seem to relate variation in the prices of add-on insurance to assumed differences in the risk associated with the underlying product. Moreover, participants mention the probability of a failure or accident as the most important aspect that insurers take into account when setting the price for add-on insurance. While this pilot study thus provides a first indication that high relative insurance prices may evoke risk associations with regard to an underlying core product, Study 1 aims to provide initial insight into the relationship between the relative price level of add-on insurance and the underlying product purchases using the ISMS durable goods data set (Ni, Neslin, and Sun 2012).

Study 1: Relative Insurance Prices and Product Sales

We analyze the ISMS durable goods data set (Ni, Neslin, and Sun 2012) that contains the transaction history of a major U.S. electronics retail chain over six years (December 1998 to November 2004). The data set comprises 173,262 transactions in 292 product categories, of which 15,033 transactions are insurance purchases. The aim of this study is to examine the effect of relative insurance prices on insurance purchases and to provide initial evidence for the proposed negative effect of higher relative insurance prices on consumers’ purchase decisions (i.e., sales) of the underlying core product. Information about insurance was available to consumers when they were considering product purchase (e.g., through information on the shelf and from salespeople).

Data Preparation

We follow Abito and Salant (2019), who also use the ISMS durable goods data set, when preparing the data for our analyses. Likewise, we include all transactions in which consumers purchase a product with insurance in the respective category where we can unambiguously match the insurance to the product purchases. We then identify the insurance price for the products where we do not observe an insurance purchase. We match the product transactions without insurance with those with insurance for the same product ID and the closest transaction date to determine the insurance prices. Following Abito and Salant, we also omit observations where the product price is lower than the insurance price (i.e., the relative insurance price is larger than 100%). 3

The resulting data contain 5,131 products (48,376 observations) from 112 product categories with corresponding relative insurance prices. We observe an average product price of $311.02 (min. = $7.99, median = $179.99, max. = $6,999.99) and an average insurance price of $64.14 (min. = $2.99, median = $39.99, max. = $1,099.99). The relative insurance price shows an average value of 23.65% (min. = 1.14%, median = 21.67%, max. = 100%). We further observe that for 10.71% (7.14%) of the categories, the entire range of the relative insurance prices is below (above) the average value of 23.65% of the product price. Thus, for the remaining 82.14% of categories, the relative insurance price ranges straddle the overall average. Furthermore, the average purchase rate is 27.01% for insurance across all products. Lastly, we observe an average of 9.45 units sold per product (median = 5.00), with a maximum of 296.

Analyses and Results

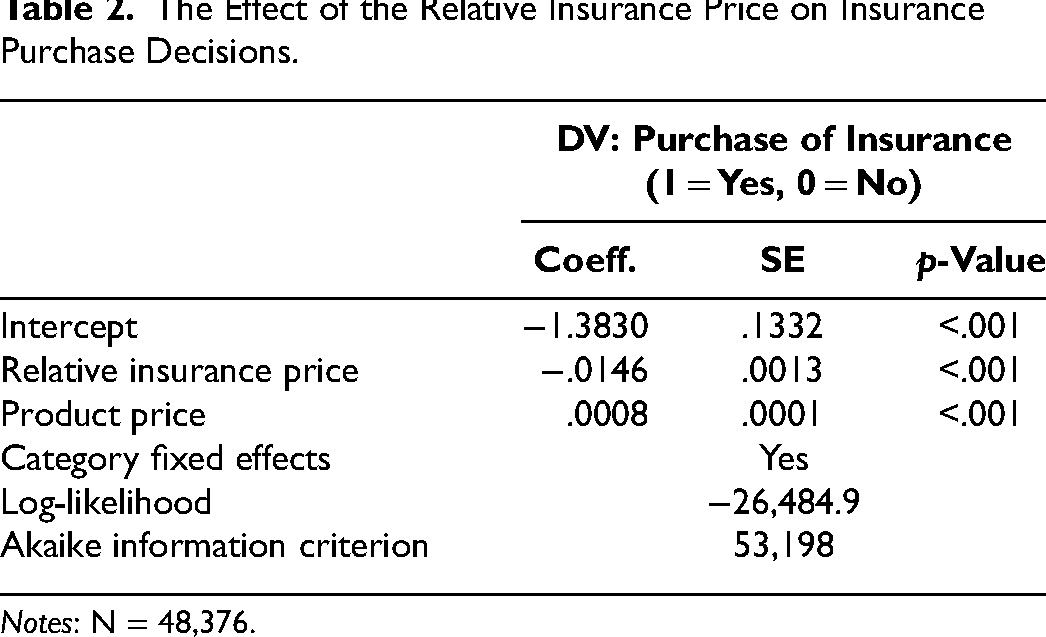

As a first step, we explore the effect of relative insurance prices on the probability that a consumer purchases insurance. Therefore, we estimate a binary logit regression model with insurance purchase (yes = 1, no = 0) as the dependent variable. We use relative insurance and product prices as independent variables and further control for the product categories.

Table 2 shows the estimation results. In line with Chen, Kalra, and Sun (2009), we find a significant negative effect of the relative insurance price (coeff. = −.0146, p < .001). Thus, the probability that a consumer purchases insurance decreases with increasing insurance price. We also find a significant positive effect for the product price (coeff. = .0008, p < .001), indicating that consumers are more likely to buy insurance for higher-priced core products. We conducted several robustness tests (e.g., to test for collinearity) and alternative model specifications (e.g., using the median product and insurance price), and the results do not change.

The Effect of the Relative Insurance Price on Insurance Purchase Decisions.

Notes: N = 48,376.

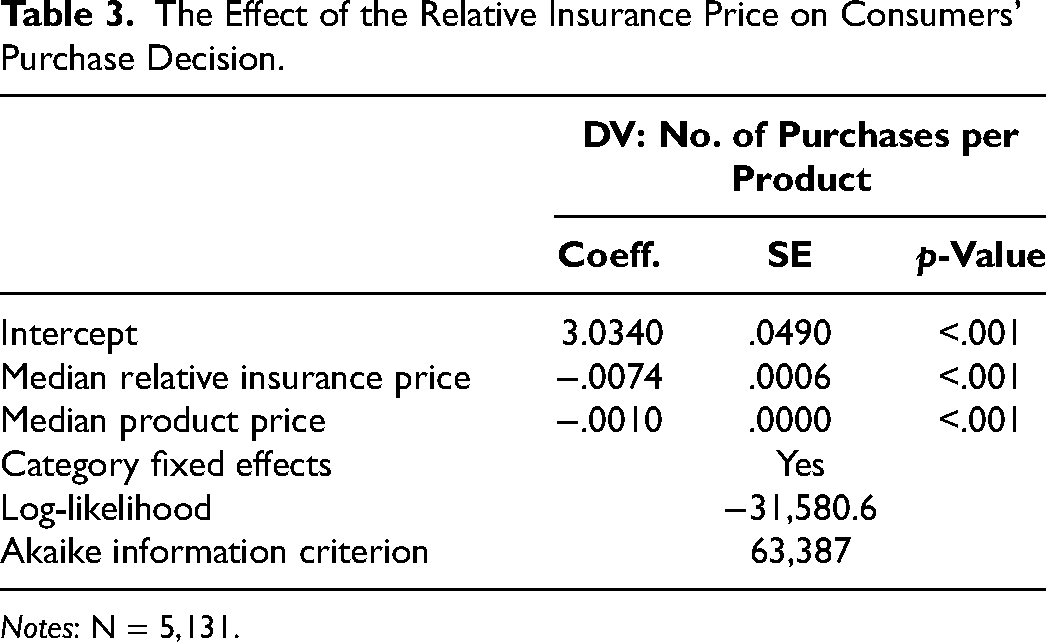

The primary goal of this study is to provide initial evidence that higher relative insurance prices negatively affect consumers’ purchase decision for the respective products. To model this relationship, we have to aggregate the data to the product level. Thus, for each product, we compute the number of units sold (dependent variable), the median relative insurance price, and the median product price (independent variables). We further control for the product categories. We model this purchase quantity model using a Poisson regression model (e.g., Bucklin, Gupta, and Siddarth 1998).

The results (see Table 3) show that higher relative insurance prices have a significant negative effect on product purchases (coeff. = −.0074, p < .001). We further observe that higher product prices have a significant negative impact on product sales (coeff. = −.0010, p < .001). The effect size of the relative insurance price shows that an increase in the relative insurance price by 10% decreases the expected number of units sold by 1.63%. Thus, we find a first indication that the price of add-on insurance affects consumers’ purchase decision and that higher relative insurance prices are associated with lower product sales. Several alternative model specifications (e.g., using the absolute insurance price) confirm the robustness of our results. Moreover, estimating the model using a quasi-Poisson model does not alter the results.

The Effect of the Relative Insurance Price on Consumers’ Purchase Decision.

Notes: N = 5,131.

Summarizing our results, we replicate two findings from prior research, namely that consumers are more likely to insure high-priced products than low-priced products and that they are more likely to purchase insurance when relative insurance prices are low rather than high (Chen, Kalra, and Sun 2009; Hogarth and Kunreuther 1995). Importantly, however, we extend these findings and show that higher relative insurance prices negatively affect consumers’ purchase decision (i.e., core product sales), which is in line with H2a.

Study 2: Experimental Evidence for the Insurance Price Risk Signal

Building on the Pilot Study and Study 1, Study 2 examines the proposed rationale that the perception of a high (vs. low) relative insurance price for a given product increases consumers’ risk perception and subsequently decreases their intention to purchase the respective product in a controlled setting. We use a setting in a leisure context (i.e., canyoning), where optional add-on insurance is common (Elliott 2021).

Method

The study was a single-factorial (relative insurance price: high vs. low) between-subjects design with 421 U.S.-based participants recruited via Prolific (approval rate > 95%, no further prescreening criteria; the sample size was determined based on Brysbaert [2019], accounting for potential dropouts resulting from an instructional manipulation check). Participants who failed the instructional manipulation check (n = 10) were excluded from the analyses, leaving a sample of 411 participants (Mage = 37.22 years; 51.58% male, 46.23% female, 1.46% other, .73% prefer not to answer). The study was preregistered on AsPredicted (https://aspredicted.org/829xr.pdf).

We asked participants to imagine going on a five-day trip to Mexico. Looking for leisure activities, they found a tour provider offering guided canyoning and white-water rafting tours, both at a price of $100. For the relevant period, however, only the guided canyoning tour was available. Participants received the information that the tour provider offers the option to insure against the consequences of accidents that might happen during the tour and that the price of the optional tour insurance would be $79.90 in the high relative insurance price (HRIP) condition and $9.90 in the low relative insurance price (LRIP) condition (the insurance price for the sold out white-water rafting tour was held constant at a price of $14.90; for stimulus details, see the Appendix). We determined the price levels based on an assessment of the actual variation in market prices. 4

We then asked participants to indicate their booking intention irrespective of whether they would also select the optional tour insurance or not (seven-point scale where 1 = “definitely would not book,” and 7 = “definitely would book”; Brough et al. 2022), their interest in purchasing the optional tour insurance (in conjunction with the respective tour), and their risk perception. In line with the findings of our study on consumer inferences and related research, we operationalized risk perception using two items that captured the expectation of the occurrence of an adverse event related to the product (likelihood of accident/experience of physical harm, seven-point scales where 1 = “very low,” and 7 = “very high”; Abito and Salant 2019; Boulding and Kirmani 1993; Folkes 1988). Since the two items were highly correlated (r = .86), we combined them to form a risk index.

Finally, participants answered an attention check and a manipulation check (i.e., to what extent they perceived the add-on insurance price as high compared with the price of the canyoning tour itself), and we collected personal information (age, gender, canyoning experience, swimming skills, climbing skills; experience/skills measured on seven-point scales where 1 = “no experience/skills at all,” and 7 = “very extensive experience/good skills”). Moreover, we assessed whether participants have ever participated in a canyoning tour, their interest in canyoning, their subjective sport-related risk perception, and whether they have ever bought optional add-on insurance.

Results and Discussion

As intended, participants in the HRIP condition indicated a higher agreement with the statement that the insurance price was high than did participants in the LRIP condition (MHRIP = 5.60, SD = 1.42; MLRIP = 2.46, SD = 1.57; t(409) = 21.22, p < .001).

An ANOVA revealed a significant effect of relative insurance price level on perceptions of risk (MHRIP = 4.33, SD = 1.39; MLRIP = 4.00, SD = 1.50; F(1, 409) = 5.47, p < .05, η2 = .013), indicating that participants associated a higher level of risk with the described tour in the HRIP-condition. This result supports our rationale that consumers use the price level of add-on insurance to infer an underlying product's risk in terms of failure/accident probability (H1).

An ANOVA on booking intention likewise revealed a significant effect of relative insurance price level (MHRIP = 3.52, SD = 1.93; MLRIP = 4.50, SD = 1.99; F(1, 409) = 25.65, p < .001, η2 = .059), providing support for H2a. To test whether perceived risk mediates the effect of the relative insurance price on consumers’ decision to purchase the underlying product (H2b), we conducted a mediation analysis (Hayes 2018; Model 4, 10,000 bootstrap resamples). We included relative insurance price level (0 = low, 1 = high) as the independent variable, booking intention as the dependent variable, and perceived risk as a mediator. In line with H2b, the results revealed a significant indirect effect via perceived risk (bindirect = −.10, SE = .05, CI95: [−.2092, −.0151]). Study 2 thus reveals that consumers indeed seem to infer the risk associated with a product from the prices of optional add-on insurance. 5

Study 3: Providing Alternative Information on Product Risk

Study 3 serves two primary purposes. First, we extend our examination of the insurance price risk signal to a within-subjects experimental design. Such a setting enables us to assess the robustness of the effect since in typical consumption situations, consumers are frequently exposed successively to various alternatives. Second, we examine how the provision of objective information on the underlying product's failure/accident probability—and hence the actual risk—influences consumers’ use of relative insurance price information to infer product risk.

Method

The study employed a 2 (relative insurance price: high vs. low) × 2 (provision of objective risk information: yes vs. no) mixed design, where relative insurance price served as the within-subjects factor. We recruited 403 U.S.-based participants via Prolific (approval rate > 95%, no further prescreening criteria; the sample size was determined based on Brysbaert [2019]). Participants who failed an instructional manipulation check (n = 4) were excluded from the analyses, leaving a sample of 399 participants (Mage = 33.45 years; 38.60% male, 58.40% female, 2.26% other, .75% prefer not to answer). The study was preregistered on AsPredicted (https://aspredicted.org/5ah7u.pdf).

The scenario and stimulus material were similar to Study 2. Participants were asked to imagine that they were looking for leisure activities for several days and found a tour provider that offers guided canyoning tours and guided white-water rafting tours, both available at a price of $100. Subsequently, participants received the information that the tour provider offers the option to insure against the consequences of accidents that might happen during the respective tours. Afterward, they were exposed to both tour offers, where one of the tours was shown with a price of $79.90 for the optional tour insurance (HRIP), and the other tour was shown with a price of $9.90 for the optional tour insurance (LRIP) (for the stimulus material, see the Appendix). For each tour, we asked participants to indicate their respective booking intention irrespective of whether they would also select the optional tour insurance, their interest in purchasing the optional tour insurance (in conjunction with the respective tour), and their risk perception using the same two items as in Study 2 (r = .92). Importantly, we counterbalanced the order of relative insurance price (high/low) and which tour was associated with which price.

We chose white-water rafting as the second type of tour in addition to canyoning to manipulate insurance price within-subjects because both types of sport have a similar appeal and target group and exhibit similar levels of objective risk (various sources report accident probabilities for both types of sport that are approximately .5% for supervised tours; e.g., Soulé et al. 2015). This allowed us to design the respective tour descriptions to maximize consistency across descriptions. We conducted a pretest with 60 participants prior to this study based on the employed stimulus material (without mentioning insurance prices), which also indicated similar levels of risk and appeal for both tour offers.

We manipulated the provision of objective risk information between subjects by including the respective information when mentioning the option to insure against the consequences of accidents. Specifically, in the condition where this information was present, we stated that official international accident statistics reveal that the actual accident probabilities for canyoning and white-water rafting are roughly the same. For both types of sports, the accident probability is approximately .5%.

Finally, participants answered an attention check and manipulation checks (i.e., whether insurance prices varied a lot between both tours and whether an actual accident probability was indicated), and we collected personal information (swimming skills, climbing skills, age, gender). Moreover, we assessed whether participants have ever participated in a canyoning or a rafting tour, their experience with, preference for, and interest in both canyoning and rafting, their subjective sport-related risk perception, and whether they have ever bought optional add-on insurance.

Results and Discussion

As intended, participants agreed that the insurance prices varied a lot between both conditions (M = 6.26, SD = 1.56 on a seven-point scale; significantly above the scale midpoint; t(398) = 28.947, p < .001). Moreover, participants in the condition in which objective risk information was provided indicated a higher agreement with the respective manipulation check (Myes = 5.20, SD = 2.20) than did participants in the condition where no objective accident probability was provided (Mno = 2.01, SD = 1.44; t(345.95) = 17.181, p < .001). In addition, the between-subjects provision of objective risk information did not influence participants’ perception of the within-subject insurance price variation (F(1, 397) = 2.169, p > .10).

A mixed-model ANOVA on perceived risk with relative insurance price level as within-subjects factor and the provision of objective risk information as between-subjects factor revealed a significant within-subjects main effect of relative insurance price level (F(1, 397) = 88.73, p < .001, η2 = .183), which is in line with H1 and the predicted interaction (F(1, 397) = 17.40, p < .001, η2 = .042). Participants in the condition without objective risk information associated significantly higher levels of accident likelihood with the high (compared with low) relative insurance price condition (MHRIP = 4.61, SD = 1.36; MLRIP = 3.59, SD = 1.53; F(1, 197) = 64.771, p < .001, η2 = .247). This difference in risk perception, while still significant, was much less pronounced for participants who were provided with objective risk information (MHRIP = 2.56, SD = 1.67; MLRIP = 2.17, SD = 1.31; F(1, 200) = 23.482, p = < .001, η2 = .105).

A second mixed-model ANOVA on booking intention revealed a significant within-subjects main effect of relative insurance price level (F(1, 397) = 28.86, p < .001, η2 = .068), which is in line with H2a, and a significant main effect of the provision of objective risk information (F(1, 397) = 4.83, p < .05, η2 = .012), while the interaction between relative insurance price level and the provision of objective risk information was not significant (F(1, 397) = .24, p = .63, η2 = .001). The patterns of means for booking intention in the respective between-subjects conditions are similar, revealing higher booking intentions for low as compared with high relative insurance price levels (without objective risk information: MHRIP = 3.93, SD = 2.02; MLRIP = 4.49, SD = 1.98; F(1, 197) = 10.55, p < .001, η2 = .051; with objective risk information: MHRIP = 4.24, SD = 2.03, MLRIP = 4.91, SD = 1.93; F(1, 200) = 19.66, p < .001, η2 = .090).

Thus, while we observed that the perception of price as a risk signal was more pronounced if no objective risk information was available (vs. when such information was provided), lower insurance prices were generally associated with higher booking intentions for the core product.

As a next step, we examined for both between-subjects conditions to what extent perceived risk mediates the relationship between the relative insurance price level and booking intention. To do so, we conducted a mediation analysis using the MEMORE macro for within-subjects designs (Montoya and Hayes 2017; Model 1, 10,000 bootstrap resamples). For the condition where no objective risk information was provided, this analysis revealed a significant indirect effect via perceived risk (bindirect = −.43, SE = .11, CI95: [−.6578, −.2154]), while the direct effect of relative insurance price level on booking intention was not significant (bdirect = −.12, SE = .19, CI95: [−.4925, .2457]), providing evidence for full mediation.

For the condition in which objective risk information was provided, we also observed a significant indirect effect via perceived risk (bindirect = −.17, SE = .06, CI95: [−.2970, −.0603]), while the direct effect of relative insurance price level on booking intention was also significant (bdirect = −.50, SE = .16, CI95: [−.8041, −.1859]).

These findings suggest that differences in relative insurance price levels induced differences in consumers’ risk perceptions and that these perceptions fully mediated the association between the insurance price level and booking intention if no objective risk information was available, providing further support for H2b. When additional information on product risk was available, however, the risk-signaling role of insurance price level was reduced as proposed in H3, and risk perceptions only partially mediated the association between insurance price level and booking intention (while there remains a strong direct effect of insurance price level). One potential explanation for this latter finding might be “peace of mind” considerations: objective information indicated that there is a certain (albeit modest) risk associated with the product. In such a situation, the possibility to buy insurance (particularly if available at a rather low price) may ensure “peace of mind” by alleviating this remaining risk and hence act as a purchase incentive for the core product (Huysentruyt and Read 2010).

Study 4: Incentive-Aligned Risk Inference

Our key reasoning is that consumers utilize insurance-related price information to infer the risk related to a core product. Study 4 is designed to test whether the price risk signal still holds when consumers’ motivation to be as accurate as possible in their estimates of accident probability is enhanced by employing an established incentive-alignment mechanism (Abito and Salant 2019).

Method

The study employed a within-subjects design where relative insurance price (high vs. low) served as the within-subjects factor. We recruited 199 U.S.-based participants via Prolific (approval rate > 95%, no further prescreening criteria). Participants who failed an instructional manipulation check (n = 11) were excluded from the analyses, leaving a sample of 188 participants (Mage = 36.59 years; 41.49% male, 57.45% female, .53% other, .53% prefer not to answer). The study was preregistered on AsPredicted (https://aspredicted.org/mm9zv.pdf).

The study employed the same scenario, stimulus material, and pricing schemes used in Study 3. The only difference was that in this study, participants were just asked to indicate their estimate of the actual accident likelihood for the respective tours on a seven-point scale (“The likelihood that an accident may happen during the described tour is approximately …,” where 1 = .5%, 2 = 1%, 3 = 1.5%, 4 = 2%, 5 = 2.5%, 6 = 3%, and 7 = 3.5%). Following Abito and Salant (2019), we incentivized this question by promising participants an additional US$.50 if their estimate was among those closest to the actual statistical accident probability (which was the case for all participants selecting 1 = .5%).

Finally, participants answered an attention and manipulation check, and we collected the same personal information as in Study 3.

Results and Discussion

Participants agreed that the insurance prices varied a lot between both conditions (M = 6.53 and SD = 1.14 on a seven-point scale, significantly above the scale midpoint; t(187) = 30.59, p < .001).

A repeated-measures ANOVA on participants’ estimated accident likelihood revealed a significant main effect of relative insurance price level (F(1, 187) = 93.20, p < .001, η2 = .333). In line with H1, participants estimated significantly higher values of accident likelihood in the high (compared with low) relative insurance price condition (MHRIP = 4.67, SD = 1.98; MLRIP = 2.92, SD = 1.81). This finding further corroborates our reasoning that consumers utilize the relative insurance price as a cross-product risk signal, even if they are incentivized to be as accurate as possible in their risk judgments.

Study 5: Field Evidence

Study 5 provides empirical evidence for the link between the relative insurance price and consumers’ decision to purchase the underlying product using a unique data set of a major European online retailer. The data cover all products in the consumer electronics category, including the subcategories home appliance and multimedia that the retailer offered together with insurance (i.e., protection plans) and other add-ons (e.g., antivirus software, music streaming, setup and installation) between January 11 and April 5, 2021.

The data provide access to 10.97 million browser sessions accounting for 80.61 million page views of 21,621 products (i.e., unique article numbers). A browser session contains one or typically multiple page views and possibly the purchase of none, one, or more products. For example, consumer X goes to the retailer's website and looks at the product pages of product A, then B, then A, and finally B. She purchases product B and leaves the online shop. The browser session thus contains four page views and the product purchase decision for B. Moreover, the browser session resembles the decision process for two products. We observe 1.16 million purchases originating from 12,040 products (55.69% of all products).

The product prices in our data range from €16.99 to €14,449, while we observe insurance prices ranging from €9.99 to €299.99. Insurance was displayed on the respective product page (i.e., consumers observed insurance prices before they made a commitment to purchasing a product). In addition, they received a reminder in case of not having checked the insurance when moving further to the payment. The data further show that up to four other add-ons were offered in addition to the insurance.

Correlational Data Analysis

In our first analysis, we conduct a correlational data analysis to find empirical evidence for the negative impact of the relative insurance price (high vs. low) on the purchase decision for the underlying product. To do so, we search for products that were offered (1) with a single product price and (2) with two distinct insurance prices (i.e., high vs. low). 6 Using a single product price avoids price effects for the core product, such as price promotions or lower prices due to later life cycle stages. Focusing on two insurance prices allows us to compare a low with a high insurance price. We aggregate the data across browser sessions and products to account for consumers’ decision process (i.e., consumer journey within the retailer).

We identified 442 products from all available products that meet the requirements for entering the correlational data analysis (i.e., having one product price and two insurance prices). These 442 products represent 1,459,158 purchase decisions and 25,959 purchases. We observe insurance prices varying between €50 and €199.99 for the high insurance price and a variation between €35 and €79.99 for the low insurance price. For 91.63% of the products, we observe a difference between the high and low insurance prices of €15. For 7.92% of the products, we observe a difference of €30. For the remaining products, we observe a difference larger than €45. Concerning the price of the products, we observe an average product price of €678.70 (median = €650.00, min. = €149, max. = €3,499).

We use a one-sided Mann–Whitney U-test to examine whether the product purchase probability is lower for the relatively high insurance price than for the relatively low insurance price. We derived the product purchase probability from the observed product purchases (binary: 1 = purchase, 0 = no purchase) for each purchase decision. We find that 53.62% (237 products) of 442 products show a significantly lower product purchase probability for the relatively high insurance price (p < .05).

Our findings from the correlational data analysis indicate that RHIPs are associated with lower product purchase probabilities for the majority of the products, which aligns with our expectations.

Binary Logit Regression Analysis

Although the correlational data analysis indicates our proposed insurance price risk signal, the requirements for the analysis limit our analysis to a subset of the available products. Therefore, we conducted an additional analysis in which we relaxed these strict selection requirements to assess the effect of the insurance price (high vs. low) on purchase decisions.

In this subsequent analysis, we consider products that have (1) one or multiple product prices and (2) two or multiple insurance prices. To be as close as possible to our experiments (Studies 2–4), we aim to keep the comparison of relatively high and low insurance prices. To operationalize the binary indicator, we have to define the high and low insurance prices for products with three or more insurance prices. For these products, we use the purchase decisions with the highest and lowest insurance prices. 7

Relaxing the requirements increases the number of available products to 2,710, which relate to 11,467,648 purchase decisions and 221,062 purchases. We observe insurance prices between €9.99 and €199.99 (mean = €50.97, median = €50). For the relatively high (low) insurance price, we observe a variation between €14.99 and €199.99 (€9.99 and €149.99). Differences between the high versus low condition range from €4 to €120, while most products show a difference of €15 (78.23%). The average product price is €669.10 (median = €529.00, min. = €127.00, max. = €3,519). We further observe that for most products add-ons are offered in addition to insurance (93.53%).

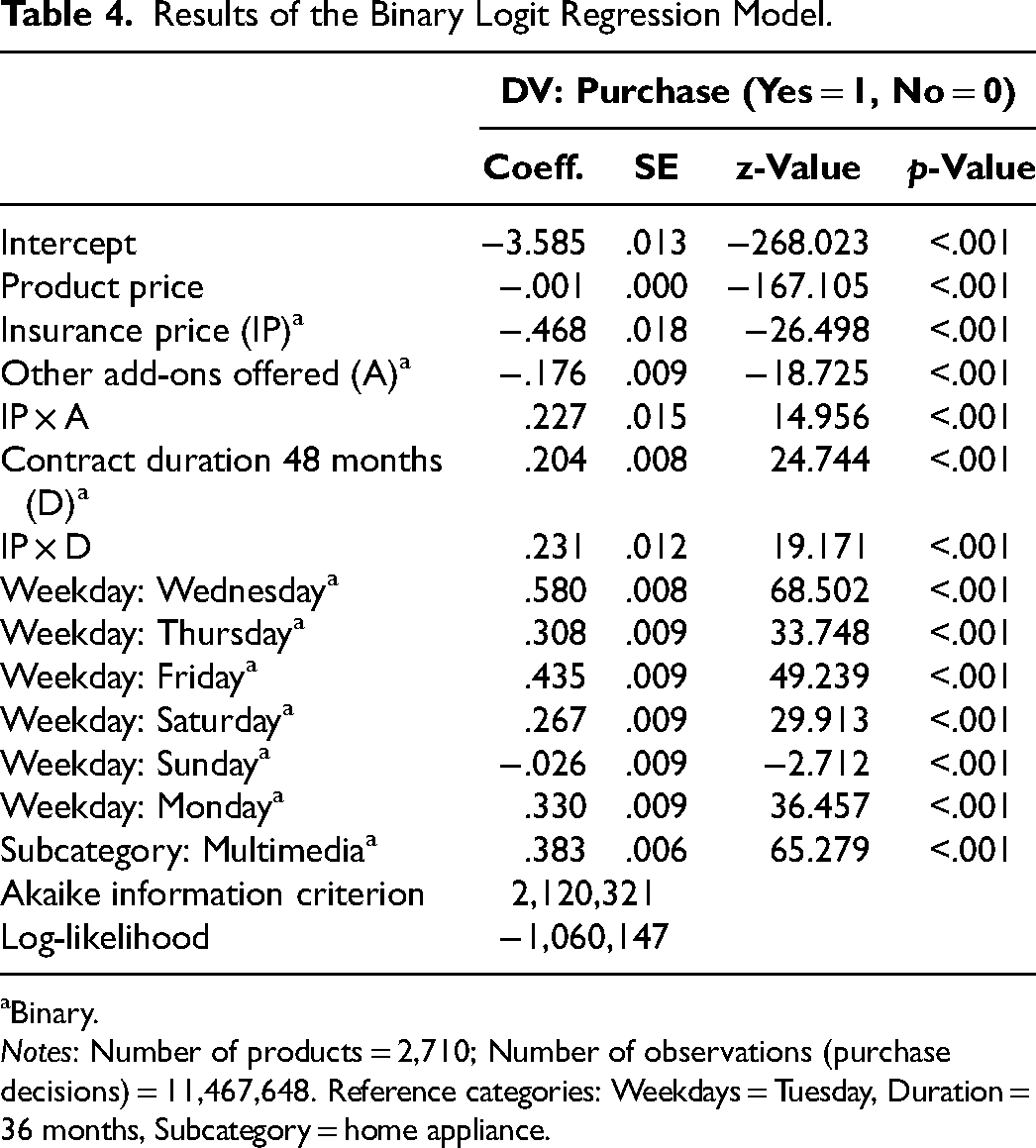

We estimate a binary logit regression model using purchase (1 = purchase vs. 0 = no purchase) as the dependent variable and product price, insurance price (high vs. low), and other add-ons (yes vs. no) in addition to insurance as the independent variables. We further control for the insurance coverage duration (36 vs. 48 months), weekdays, and the multimedia subcategory. Table 4 shows the corresponding estimation results.

Results of the Binary Logit Regression Model.

Binary.

Notes: Number of products = 2,710; Number of observations (purchase decisions) = 11,467,648. Reference categories: Weekdays = Tuesday, Duration = 36 months, Subcategory = home appliance.

For the RHIP, we find the expected negative effect (coeff. = −.468, p < .001). Thus, supporting H2a, we find further evidence for the proposed cross-product risk signal—that relatively high insurance prices have a negative effect on consumers’ product purchase decision. Furthermore, we find that the effect of insurance price changes from −.468 to −.241 (i.e., −.468 + .227) when other add-ons (coeff. = .227, p < .001) are offered in addition to insurance, supporting H4. We conducted several robustness tests (e.g., stepwise inclusion of the interactions), and the results remain robust. We also estimated a binary logit regression model with fixed effects for the brands and products, 8 respectively, and the results do not change substantially.

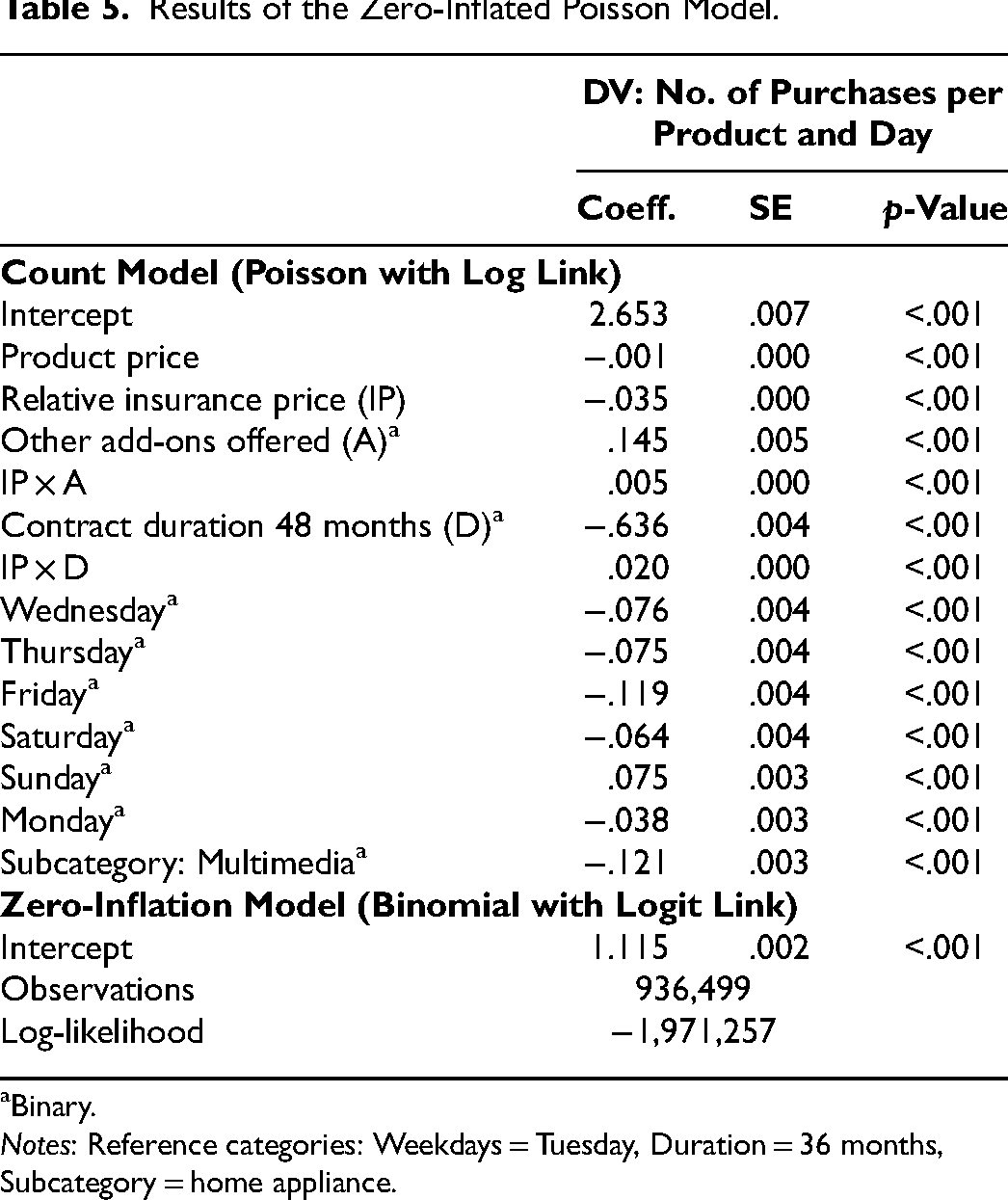

Poisson Regression Analysis

For both preceding analyses, a certain degree of selection is unavoidable. In this third analysis, we relax the assumptions further and use as many products as possible. Similar to Study 1, we implement a purchase model. Since the number of purchases per product and day follow a count distribution, we employ a Poisson regression model (e.g., Bucklin, Gupta, and Siddarth 1998). We extend the model with a zero-inflation component to account for zero purchases 9 (e.g., Bruce, Murthi, and Rao 2017).

The dependent variable of the model is purchases per product and day. Product prices, relative insurance prices, and add-ons offered in addition to insurance (yes vs. no; thus testing H4) serve as independent variables. We control for the duration of the insurance coverage (36 vs. 48 months), weekdays, and the multimedia category. In contrast to the previous two analyses in Study 5 (but in line with Study 1), we use the relative insurance price as a percentage value of the product price.

The analysis is based on 936,499 observations (i.e., purchases per product and day; 21,621 unique products). We observe an average relative insurance price of 10.53% (median = 8.45%, min. = .44%, max. = 147.09%) and an average product price of €618.80 (min. = €16.99, median = €439.99, max. = €14,449.00).

Table 5 shows the expected negative effect of the relative insurance price on product purchases (coeff. = −.035, p < .001) and the expected negative effect of the product price (coeff. = −.001, p < .001). Increasing the relative insurance price by 10% decreases the expected number of purchases per product and day by 1.72% (reflecting the effect size of the relative insurance price).

Results of the Zero-Inflated Poisson Model.

Binary.

Notes: Reference categories: Weekdays = Tuesday, Duration = 36 months, Subcategory = home appliance.

Thus, using a different data structure and modeling approach, we again find support for H2a that HRIPs have a negative effect on consumers’ purchase decision (i.e., number of purchases). Regarding the availability of other optional add-ons (in addition to insurance), we find the expected positive interaction effect (coeff. = .005, p < .001) with relative insurance price. Offering optional add-ons in addition to insurance decreases the negative effect of the relative insurance price on consumers’ purchase decision to −.03 (i.e., −.035 + .005). This finding supports H4. We conducted several robustness tests (e.g., stepwise inclusion of the control variables and interactions, operationalization of the product price using price tiers, and adding brand information), but the result do not vary substantially. Using a quasi-Poisson model for estimation does not alter the results.

Discussion

Summary

Retailers, service providers, and manufacturers have discovered optional insurance policies as an attractive add-on service next to their core business (Chen, Kalra, and Sun 2009; Jiang and Zhang 2011). These optional insurance policies are tailored to cover a specific product or event and are frequently offered at substantial prices (Baker and Siegelman 2013; Chen, Kalra, and Sun 2009). The underlying assumption is that insurance acts as a mere add-on that does not affect consumers’ purchase decision for the product.

In this article, we questioned this assumption, as insurance reveals information about the risk associated with the product to be insured. Using a survey, three online experiments, and two transactional data sets, we addressed the following three research questions: (1) Do consumers interpret the price of insurance as a cross-product risk signal with respect to an underlying product? (2) If so, how does the insurance price risk signal affect consumers’ purchase decisions? (3) Which factors moderate the influence of the insurance price risk signal on consumers’ purchase decisions?

Our analyses provide supporting evidence for the proposed risk-revealing role of the insurance price. The effect of the relative insurance price on product purchase decisions is mediated by perceived risk. Accordingly, consumers associate relatively high insurance prices with higher levels of perceived risk, which in turn decreases their probability of purchasing the product in a given purchase situation. We found evidence for two moderating effects. First, the insurance price risk signal is weaker for insurance offers that reveal objective information on the failure (accident) probability. Second, offering other optional add-ons (besides insurance) weakens the insurance price risk signal.

Theoretical Contributions

Our research contributes to existing research on add-on insurance and price signals. First, we show that consumers’ product and insurance purchases are intertwined. In contrast to the industry assumption that promotes substantial insurance prices, consumers’ purchase decisions are not a simple two-step process in which they first decide on a product and then whether to add insurance (Baker and Siegelman 2013; Jindal 2015). As the insurance offer, particularly the relative insurance price, contains information about the underlying product, consumers use insurance information to reflect on their product purchase decision—which is hence not independent of the insurance offer.

Second, we extend research on price signals (e.g., Erickson and Johansson 1985; Völckner 2008) by proposing the insurance price risk signal as an extension of the informational role of price. We illustrate that consumers use the relative insurance price as a cross-product risk signal to evaluate the risk associated with an underlying product.

Third, our examination of boundary conditions shows that the proposed risk signal is less pronounced when (1) objective information on failure probabilities is provided as part of the offer and when (2) other add-ons for the product (e.g., complementary software) are offered (additional to insurance).

Managerial Implications

In practice, companies push insurance offers and frequently charge substantial insurance prices. Their goal is to elicit insurance sales to generate additional profit. However, our results show that relatively high insurance prices are interpreted as a signal for product-related risk, which, in turn, negatively affects consumers’ decision to purchase the product. Our field data (Study 5) suggest that an increase in the relative insurance price by 10% decreases the expected number of purchases per product and day by 1.72%. These findings provide an economic rationale for firms to refrain from overpricing and to carefully consider at what price insurance should be offered (if it should be offered at all).

One approach to mitigate the negative impact of the insurance price risk signal could be to use our insights about cross-product interdependencies and analyze price–sales effects for products and insurance simultaneously to derive the most profitable outcome.

Insurance represents only one possible kind of add-on that retailers can offer along with the product. Our results suggest that offering add-ons has an impact on consumers’ product purchase decisions. For insurance, we found that add-ons offered additional to insurance dilute the effect of the insurance price risk signal. Thus, when multiple add-ons (insurance being one of them) are available, the risk signal of a relatively high insurance price may be attenuated. At the same time, offering multiple add-ons allows firms to still cater to consumers actively searching for insurance (for whom the salience of the add-on insurance is high anyway).

Our results also show that the insurance price risk signal is attenuated if objective information on the accident/failure probability is provided (Study 3). Researchers and regulators have already advocated the provision of such information alongside the add-on insurance offer to help consumers making better-informed decisions (Abito and Salant 2019; Lunn, McGowan, and Howard 2018). Our results reveal that the provision of such information may also benefit firms since it prevents consumers from developing exaggerated risk perceptions that may ultimately result in them refraining from purchasing the core product.

We expect the insurance price risk signal to become even more relevant as we see a trend toward more insurance personalization. Future applications could leverage consumer characteristics (e.g., product-specific abilities, demographics) to provide personalized insurance offers. For instance, for rental cars (as companies often collect a cross-border fee), leisure activities, or travel, since health risks largely depend on the activity or country traveled.

Limitations and Avenues for Further Research

The current design of our experiments allows us to observe that the purchase intention of a product decreases in a given purchase situation when the relative insurance price is high. Our studies focus on the relative insurance price as the primary information that signals risk to consumers. However, other elements of the insurance offer, such as visual information or message framing of the accompanying text, also merit attention. Moreover, we do not know whether consumers postpone their purchase decision, intensify their search efforts, purchase a different product, purchase the same or a different product at a competing store, or do not make a purchase in the category at all. Thus, consumers’ reactions to relatively high insurance prices merit further attention in future research.

Risk perception also likely varies across product categories and between (tangible) products and services (e.g., Blais and Weber 2006). While we demonstrate the effect of relative insurance price on purchase decisions/intentions for both services and tangible products, 10 we keep the context (leisure) constant in our experimental studies to focus on the underlying process. Although optional add-on insurance is very common in the chosen context (Elliott 2021), generalizations to other domains need to be seen in light of this limitation.

Another element of the insurance offer is its timing (i.e., when firms present insurance to the consumer; Jindal 2015). The information that insurance is available can be presented together with the product (simultaneously), or the insurance can be offered when the consumer buys the product and moves to the payment step (sequentially; e.g., by using a pop-up window showing the insurance offer). This latter approach of a sequential display of product add-ons and their respective prices is generally referred to as drip pricing (Santana, Dallas, and Morwitz 2020). Since exposure to the insurance price information and the possibility of relating product and insurance prices to each other vary between these two offer formats, the induced risk perceptions may also vary, potentially attenuating the cross-product risk signal in case of sequential display. But even if consumers relate higher add-on insurance prices that are revealed sequentially to higher perceptions of product risk, they may be reluctant to start over and revise their initial decision, as research on drip pricing for other types of add-ons suggests (Santana, Dallas, and Morwitz 2020). From a managerial viewpoint, however, one has to consider that some countries, such as the United Kingdom, require a joint (simultaneous) display of product and insurance (Competition & Markets Authority 2021) because it enables consumers to better understand the magnitude of the insurance price.

Our analysis considers the moderating effect of add-ons offered in addition to insurance. It would certainly be interesting to examine in more detail the structure of the add-ons offered in such purchase situations and to investigate whether and how certain combinations of add-ons affect consumers’ purchase decisions. A starting point could be research on cue consistency in the context of quality perceptions (Miyazaki, Grewal, and Goodstein 2005): To what extent may other add-ons (apart from insurance) have implications for consumer risk perceptions (e.g., screen protection for a smartphone), and how does the consistency of the respective risk signals influence consumer risk perceptions?

Finally, the use of price bundling merits further investigation. A bundle could be offered for a product and insurance with a single price tag, which decreases the salience and possibly the risk signal of the insurance price (similar to base warranties; Chu and Chintagunta 2011). Future research could examine the consequences of such a bundling approach for both risk perceptions and consumers’ purchase decision.

Supplemental Material

sj-pdf-1-mrj-10.1177_00222437241270217 - Supplemental material for How Insurance Prices Affect Consumers’ Purchase Decisions: Insurance Price as a Risk Signal

Supplemental material, sj-pdf-1-mrj-10.1177_00222437241270217 for How Insurance Prices Affect Consumers’ Purchase Decisions: Insurance Price as a Risk Signal by Jochen Reiner, Julia Wamsler, Torsten Bornemann and Martin Natter in Journal of Marketing Research

Footnotes

Acknowledgments

A previous version of this article is part of the second author's doctoral dissertation. The second and third author contributed equally to this article.

The authors would like to thank their cooperation partner for sharing the data. They are also grateful for many insights into insurance pricing provided by Joy Müller, former CEO of smile.direct and Lennart Wulff, founder and CEO of situatiVe GmbH. The authors want to thank Stefan Mayer, Reto Hofstetter, Martin Spann, Christian Schlereth, and the faculty of the 2nd EMAC Junior Faculty & Doctoral Student Research Camp, particularly Ajay K. Kohli, for their helpful comments. The authors also want to thank the JMR review team for the helpful comments on earlier versions of this article. Moreover, the authors want to thank the Informs Society of Marketing Science (ISMS; ![]() ) for providing them with the ISMS durable goods dataset.

) for providing them with the ISMS durable goods dataset.

Coeditor

Rebecca Hamilton

Associate Editor

Darren William Dahl

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the University Research Priority Program “Social Networks” at the University of Zurich.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.