Abstract

Credit card minimum payments are designed to ensure that individuals pay down their debt over time, and scheduling minimum automatic repayments helps people avoid forgetting to repay. Yet minimum payments have additional, unintended psychological default effects by drawing attention away from the card balance due. First, once individuals set the minimum automatic repayment as the default, they then neglect to make the occasional larger repayments they made previously. As a result, individuals incur considerably more credit card interest than late payment fees avoided. Using detailed transaction data, the authors show that approximately 8% of all of the interest ever paid is due to this effect. Second, manual credit card payments are lower when individuals are prompted with minimum payment information. In an experiment, the authors test two new interventions to mitigate this effect—a prompt for full repayment and a prompt asking those repaying little to pay more—yielding large counter effects. Thus, shrouding the minimum payment option for automatic and manual payments and directing attention to the full balance may remedy the unintended effects of default minimum payments.

Default options are frequently presented to individuals across a broad set of contexts and varying financial stakes, including in the domains of organ donation, retirement saving, charitable donations, and energy efficiency. Typically, defaults are applied either automatically or as a prompt to action. How do defaults affect individual actions in practice, and do they work as intended? We examine this question using a ubiquitous example of a default payment option: the credit card minimum payment. Designed to protect consumers from spiraling debts and ensure that credit card companies receive a flow of payments, credit card minimum payments suppress levels of debt and, in the case of automatic minimum payments, provide a form of insurance against forgetting to pay. Further examples of default automatic payments include standard repayments for mortgages and cell phone bills; further examples of default prompted payments include suggested tip amounts for cabs and restaurants (Haggag and Paci 2014).

Analyzing the default effects of minimum payments is important both for understanding the effects of defaults and for protecting consumers in the credit card market. Credit cardholders can choose from a range of levels of repayment, such as the full balance on their credit card, a fixed sum of money, or the minimum payment due. They can choose to make payments manually each month or set up an automatic payment (with the option to manually pay more on top each month). The minimum payment is typically a small fraction of the balance, plus fees and interest. If choosing automatic minimum payments, the card provider automatically debits the cardholder's checking account with the minimum due each month.

Understanding the consequences of minimum payment choices for repayment behavior is an important policy issue. Financial media outlets regularly warn their readership against persistently paying only the minimum payment due (e.g., NerdWallet's online calculator of the excess interest arising due to making only the minimum payment; Elkins 2018). Moreover, credit card borrowing is the main form of unsecured borrowing by consumers in the United States. Credit card debt in the United States exceeds $900 billion (Federal Reserve Bank of New York 2020), having grown steadily over the past decade following a decline during the 2007–2009 Great Recession. Most households are affected, with average household credit card debt of approximately $6,300 (Bhutta et al. 2020).

In this article, we use credit card–level transaction data and an online experiment to study the default effects of minimum payments. In particular, we investigate the unintended consequences of minimum payments. Although, in theory, minimum payments reduce the level of debt, and automatic minimum payments minimize forgetting, in practice there may be unintended outcomes. For example, while minimum automatic repayments reduce missed payments, as consumers do not need to remember to repay, an unintended affect may be lower average payments due to consumers not paying attention to the balance (which might prompt them to make larger payments). In this way, understanding effects across multiple outcomes (in this case, missed and average payments) is critical for evaluating how and whether defaults work and for making policy recommendations. In the presence of unintended consequences, the positive effects of this default in theory may not be seen in practice.

Our first main contribution is to show that the default effect of credit card minimum automatic payments has an unintended consequence of higher interest payments. We use a field study of credit card transaction data to investigate what happens when consumers switch to automatic repayments. We estimate causal effects using two identification methods: (1) a difference-in-differences design utilizing a matched control group (e.g., Fisher, Gallino, and Xu 2019; Gill, Sridhar, and Grewal 2017) and (2) an instrumental variables analysis exploiting peer effects in the adoption of minimum automatic repayment (e.g., Rutz, Bucklin, and Sonnier 2012; Shi, Grewal, and Sridhar 2021). Our results show that although default minimum automatic payments reduce the probability of missed payments to near-zero, they also reduce overall payments (by approximately 40%). This thereby causes higher revolving balances and higher interest costs. We simulate the magnitude of this effect and show that it is large. The simulations show that people using minimum automatic credit card repayments at least once in the data period could save about 19.8% of interest and fees if they did not switch to minimum automatic repayment. This constitutes approximately 8.4% of all interest and fees paid in the credit card market.

Our second main contribution is to test new remedies to overcome the default effect of presenting the credit card minimum payment. Using an experimental study, we replicate the existing finding that merely presenting minimum payment information to cardholders while they choose a level of manual repayment is also detrimental, reducing average repayments by 16% and causing the distribution of payments to be bunched at or just above the minimum. Presenting the minimum payment as a default, implicit repayment amount appears to anchor the manual repayment decision on the minimum payment. We test two new remedies that both have large effects. First, we find that prompting people to pay in full increases average repayments by 24%, without crowding out the effect of removing the minimum payment anchor (a result we replicated from prior studies). Second, we find that when low payment prompts are provided only to people who would have initially chosen to pay the minimum or an amount close to it, these people are then more than twice as likely to revise their repayment choice to a higher amount. Thus, our results show that interventions can work to override the default effect. This finding may be applicable in other contexts in which a default option delivers benefits, but unintended consequences require mitigations to ensure that adverse outcomes are avoided.

Effects of Defaults

Psychological theories suggest that a default option has a large probability of being chosen because of people's cognitive laziness or status quo bias (Johnson and Goldstein 2003). A large body of literature assumes that default options can be used to benefit consumers. This literature has achieved significant policy impact in a wide variety of domains including organ donation, retirement saving, energy efficiency, and web marketing. Jachimowicz et al. (2019) provide a meta-analysis of 58 published studies. However, while more than 45 of these studies identify positive effects from defaults in the outcomes observed (with only 4 estimating negative effects), the authors find a wide range of effect sizes.

In addition, studies that focus on target outcomes (in our example, whether an individual missed a credit card repayment) might omit important other outcomes, especially those that exhibit unintended consequences (in our example, reduced average repayment). Thus, although a particular default might, in theory, achieve a proximate outcome indicating success, the distal effects of the default include unintended consequences that could render the net effect of the default harmful (Guttman-Kenney et al. 2021).

We summarize the findings from previous studies, including evidence of potential downsides of default options, in Table 1 (for more details, see Jachimowicz et al. [2019]). For example, studies of automatic enrollment into retirement saving using pension contribution data from U.S. employers show that the introduction of automatic enrollment increases pension coverage among employees. However, automatic enrollment to a default level of saving can reduce savings rates for employees who would otherwise have saved at a higher rate when making an active choice (Choi et al. 2001), reduce saving by other means, and increase consumers’ level of indebtedness (Beshears et al. 2019). It is not clear whether auto-enrollment increases the overall level of saving (which is the key objective of the policy). Thus, in a variety of settings, there is a need to understand the full effects of defaults and how to mitigate against potential downsides of default options.

Summary of Studies on Effects of Defaults.

Defaults in the Credit Card Market

Many studies have focused on default effects in the credit card market. This issue has received a lot of attention due to (1) the magnitude of credit card debt, and therefore importance of regulatory policy regarding minimum payments, and (2) the availability of objective, high-frequency credit card records providing data on a variety of outcomes. This makes the credit card market a promising test bed for evaluating defaults and informing policy design, especially as policy changes result in fast feedback compared with other settings (e.g., organ donation, retirement saving).

We summarize the findings from these studies in Table 2. A first set of studies focused on whether default information disclosures help stimulate higher payments. For example, using mass transaction data, Agarwal et al. (2015) find that including the minimum level of repayment required to clear debt in three years—as mandated by the U.S. Credit CARD Act (2009)—had no overall effect on repayments. Studies from Mexico (Seira, Elizondo, and Laguna-Müggenburg 2017) and the United Kingdom (Adams et al. 2021) show similar ineffectiveness of informational nudges. A second set of studies focused on whether shrouding the minimum payment on credit card statements and/or online payment journeys (e.g., by either removing the minimum payment completing or showing only the minimum payment when the cardholder attempts to pay below the minimum payment due) might help increase payments. Showing the level of minimum payment may reduce attention to the balance, which might also interact with present-biased preferences (O’Donoghue and Rabin 1999). The minimum payment may also act as an anchor. It is well known that an anchor value selected by an experimenter causes the participant's subsequent estimation to biased toward the anchor (Tversky and Kahneman 1974). Theoretical explanations vary from insufficient adjustment from the anchor (Epley and Gilovich 2001, 2006; Tversky and Kahneman 1974), numerical priming (Jacowitz and Kahneman 1995; Wong and Kwong 2000), selective availability and semantic priming of information during hypothesis testing (Chapman and Johnson 1994; Mussweiler and Strack 1999, 2001), elaboration (Wegener et al. 2010), and scale distortion (Frederick and Mochon 2012)—an overlapping and nonexhaustive list. Even arbitrary numbers affect choices, such as using the last few digits of a phone number (Russo and Shoemaker 1989) or social security number (Ariely, Loewenstein, and Prelec 2003).

Summary of Studies on Effects of Defaults in the Credit Card Market.

Our study complements the existing literature by examining the unintended consequences of minimum payments, exploring whether the forms of unintended consequence seen in the domains described in Table 1 might also exist in the credit card market. If such unintended consequences exist, there is a rationale for taking actions to preserve the positive impact of the default while mitigating the unintended negative consequences. We explore examples of this in the following experimental study.

Field Data Study: Automatic Minimum Payments

In this first study, we explore the effects on repayments of switching to a default minimum automatic repayment.

Empirical Approach

Our empirical approach uses card-level data for a large sample of U.K. cardholders. Assignment to a default minimum automatic repayment is nonrandom, so we therefore use quasiexperimental methods. We first use a difference-in-differences approach based on a matched sample of nontreated cards. We also use an instrumental variable approach, exploiting peer effects in the adoption of default minimum automatic repayment. These methods yield consistent results.

Data and Sampling

Data source

The data were provided by U.K. credit card issuers, which together account for 40% of the U.K. credit card market by number of cards. Credit card products in the United Kingdom resemble those in the United States, with many U.S. credit card issuers active in the U.K. market. The distributions of credit card spending, balances, and payments in U.K. (Financial Conduct Authority 2016) and U.S. (Keys and Wang 2019) data are similar to one another. In addition, repayment patterns found in U.K. data (Gathergood et al. 2019b) have replicated in U.S. data (Gathergood et al. 2019a). The data were extracted and provided by Argus Information & Advisory Services in collaboration with the UK Cards Association, without constraint on the research agenda. Cardholders and issuers are not identified in the data we received. The data are a 10% random sample of all U.K. consumers who held a credit card during January 2013 to December 2014 within Argus's database, which covers nearly 100% of U.K. cardholders.

Complete R source code is available for all steps from importing the data exported from Argus to the statistics, tables, and figures in this article. We are retaining the data for ten years. Data are proprietary but are available for replication on a local computer.

Data cleaning

The cleaned data include card identifiers, balances, required minimum amounts, purchase amounts, purchase types, repayment amounts, and various types of fees and finance charges. The unit of observation in the sample is a card-month. Repayments appear on the statement date for the month after the statement containing the balance. For example, repayments reported in December 2014 statements were made against the bill showing the balance and the required minimum in November 2014. Because no repayment data are available for January 2015, repayments for balances in December 2014 are unknown. Thus, the data provide at maximum 23 balance-repayment observations per card from January 2013 to November 2014. Automatic payment was available as a repayment option for all cards throughout the data period.

The data include records of minimum payment amounts due, together with a record of whether the payment was made manually or automatically. In the United Kingdom, the minimum amount cardholders must pay each month is typically interest and fees accrued within the month plus 1% of the card balance, or a fixed sum (typically £5 or £25), whichever is greater. As long as the cardholder pays at least the minimum payment, they will be in good standing with the card issuer and avoid a late payment fee or other costs such as additional interest costs on balances in arrears and missed payments being recorded on their credit file. Making a repayment of at least the monthly accrued interest ensures that the value of the debt does not grow. In addition, repaying 1% of the balance implies that, over time, the debt will be repaid, though the pay-down horizon is typically many years. Automatic repayments are made by a mechanism known as “Direct Debit.” Direct Debit is an extremely common method for paying bills in the United Kingdom and has growing coverage in the United States, where it has been introduced more recently and is variously known as “AutoPay” or “automatic repayment.”

Sample restrictions

We applied several sample restrictions to create a baseline sample for analysis. First, we excluded cards that were closed or charged off during the data period. Second, we excluded cards that had a balance transfer and those with a zero merchant annual percentage rate (APR) for part of the data period, as balances on these cards do not accrue interest. (Cards were treated as having a balance transfer when an aggregation of the beginning balance and all transaction amounts within a month including purchases, cash advances, fees, finance charges, and repayments differ from the end-of-month balance by £10 or more.) Third, we excluded a small number of cards with unidentified transactions. Fourth, we restricted the sample to extracted card-months with a positive balance due.

Illustrative Results

Finding 1: Switching to automatic payment is common, especially automatic minimum payment

Over one-third of cards in the sample paid by automatic payment, with this share increasing over time. In the sample, 5% of cards switched to automatic repayment during the sample period. Switching back to manual payment is a rare event. If manual payment is made ahead of the automatic payment date, the automatic payment is not taken. Given that cardholders can prepay in this way, the benefits to canceling an autopay instruction are small. Twenty-nine percent were already paying by automatic payment from the start of the sample period; the remaining 66% used manual payment throughout the period.

We classify cards switching to automatic payment into three types by the level of payment: (1) the minimum payment, (2) a fixed monetary value between the minimum and full payment, and (3) the full payment. Table 3 presents a breakdown of switches to different automatic repayment types. Among all cards switching during the data period, we observe 46.7% switching to a minimum automatic repayment. For approximately 15% of cards, we cannot identify the repayment type. For example, we cannot identify the automatic repayment policy for cards whose balance is small enough in all months that the minimum payment required is sufficient to clear the balance. Such cards could be set to repay the full balance, for example, but because the full balance is equal to the minimum payment, we cannot determine the repayment policy from observed payment behavior.

Counts of Switching from No Automatic Repayment to Different Automatic Repayment Types in the Field Data.

Notes: “Min.” = minimum automatic repayment; “Fixed” = fixed automatic repayment covering more than the minimum but less than the full balance; “Full” = full automatic repayment of the balance; “Mixed/Unknown” = automatic repayments that changed between types across months or automatic repayments that we cannot identify the type mostly due to sufficiently small balances and payments throughout the data period.

Table 4 shows card-month-level descriptive statistics for account terms and card usage before and after switching for the sample of switchers. These indicate that, on average, switching does not seem to be associated with large changes in account terms (e.g., APR, credit limit). In additional analysis using linked geodata, we find that there are socioeconomic differences between those who switched to full automatic repayments and those who switched to minimum automatic repayments (full results in Web Appendix Table W1).

Summary Statistics for the Field Data.

Notes: “Min. Auto” = minimum automatic repayment; “Fixed Auto” = fixed automatic repayments covering more than the minimum and less than the full balance; “Full Auto” = full automatic repayment. Median values are calculated using all card-month observations with a positive balance.

Finding 2: Missed payments drop after switching to automatic minimum payment

Figure 1 illustrates the proportion of payments before and after switching to automatic minimum payment. The categories shown are missed (i.e., payment below the minimum payment due), minimum, large (a payment between minimum and full), and full. Note that the figure shows their total actual payments made rather than their automatic payment amount. For example, an individual might have an automatic minimum payment but choose to pay a larger amount, or the full amount. The leftmost bars show that after switching, the proportion of missed payments falls from approximately 12% per month to 1% per month. Missed payments are not completely eliminated, because the account holder may have insufficient funds in the checking account from which the automatic payment is being drawn. This large reduction in missed payments shows the benefit of automatic payment.

Bar chart of proportion of repayments in months before and after switching in four mutually exclusive and exhaustive categories: missed (below minimum), minimum, large, and full.

Finding 3: Switching to automatic minimum payment reduces large and full payments

The bars on the right-hand side of Figure 1 illustrate that after switching, the proportion of large and full payments drops (from approximately 40% to 10% and 29% to 25%, respectively). This is due to a large increase (approximately 19% to 52%) in the proportion of minimum payments. This reduction in large and full payments shows the effect of individuals choosing automatic minimum payments as the default no-action outcome and not making manual payments to the same value as they made before switching. This is the potential downside of automatic minimum payments, as it implies higher revolving balances and, therefore, excess interest charges.

Difference-in-Differences Estimates

Identification strategy

The illustrative results presented suggest that switching to minimum automatic repayments leads to reduced payments due to cardholders being much less likely to make additional payments over the minimum. This result is descriptive. Ideally, to test the causal effect of the treatment (switching to minimum automatic repayment) on the outcome variable (level of repayment), we might like to exploit a randomized-control trial or naturally occurring experiment. However, in reality, switching is likely to be nonrandom and might be correlated with an intention to pay less in future, an omitted variable that could generate endogeneity bias. In such a scenario, payments would have decreased even without the switch to the automatic minimum payment as default. We therefore need an empirical approach to determine the causal effect of automatic minimum repayment on repayment behavior.

To address this, we utilize a difference-in-differences model and, separately, an instrumental variable model. Both of these methodologies are well-established in the marketing literature (e.g., Chevalier and Mayzlin 2006; Fisher, Gallino, and Xu 2019; Gill, Sridhar, and Grewal 2017; Rutz, Bucklin, and Sonnier 2012; Shi, Grewal, and Sridhar 2021). The difference-in-differences approach is to estimate the effect of minimum automatic repayments on payment behavior by introducing a control group whose payment behavior is used as a counterfactual for the switching group (i.e., what would have happened in the absence of the switch). This approach compares the change in repayments of the treatment group (those switching) with the change in repayment of a control group of nonswitchers. The general form of the econometric equation to be estimated is given by

In our setting, estimation of the difference-in-difference model is complicated by two factors. First, we observe repayments only for individuals in months when cardholders make a repayment (i.e., nonmissed payments). As Figure 1 shows, some cardholders miss payments in months both before and after adoption of automatic minimum payment. Second, we do not have a naturally occurring control group. We address the first issue using a first-stage equation to model repayment (using a single-hurdle model exploiting card tenure as an exclusion restriction) and address the second issue through construction of a control group using matching methods.

Single-hurdle difference-in-differences model specification

Given that switching to minimum automatic repayments greatly affects the likelihood of a missed payment, our econometric model needs to account for whether a payment is made. One option could be to omit observations of missed payments from the analysis altogether (see the “Robustness Tests” subsection); however, this approach reduces the sample size and fails to account for the existence of missed payments.

We therefore use a single-hurdle selection model (Cragg 1971) (implemented in R using the code provided by Carlevaro, Croissant, and Hoareau [2009]) to model missed payments. The model includes a single hurdle of a repayment being made (i.e., not missed) before cardholders making a “choice” of a positive repayment value. As an exclusion restriction we draw on card tenure, exploiting the tendency of missed payments to decrease with card tenure due to cardholders’ tendency to forget to repay their cards when that are first issued, a feature of credit card repayments we document and explore in a recent paper (Gathergood et al. 2021). This provides an arguably exogenous source of variation in missed payments.

In the model, Ii,t is an indicator having a value of 0 if the cardholder i misses the repayment in month t, and 1 otherwise. Using the probit model, the first component of our model estimates the probability of not missing a repayment through a latent dependent variable,

The first equation, for missed or not-missed payment, is given by

The second stage of the model estimates the differences-in-differences model (the general form of which is shown previously) where the outcome is the repayment amount

The first and second components of the model are jointly estimated on observed monthly repayment amounts, Repaymenti,t.

Control group design

We construct the control group by using matching methods to select a set of nonswitching cards that have very similar characteristics to the switching cards in the preswitch time period. The implicit assumption in this design is that the constructed control group represents the counterfactual repayment behavior of switchers had they not switched to automatic repayments. Thus, any observed difference in postswitch repayments between the groups is attributable to the effects of switching to automatic repayment. This approach relies on the availability of a good match between treatment and control observations such that the two groups show common trends and characteristics in the outcome of interest. By constructing a control group to resemble the treated group, this matched differences-in-differences approach estimates the average treatment effect on the treated group of switchers.

Control group designs based on matching methods have become widely applied in empirical research in economics and other disciplines (see Abadie 2021), with Athey and Imbens (2017) stating that they are “arguably the most important innovation in the policy evaluation literature in the last 15 years.” Such control group designs offer “systematically more attractive comparisons” by creating improved control groups compared with standard difference-in-differences designs. Fisher, Gallino, and Xu (2019) and Gill, Sridhar, and Grewal (2017) provide recent examples of such methods in marketing.

The data we use provide repeated observations of the same individuals (i.e., time-series cross-sectional sample); thus, the standard matching methods, which have been developed mostly for cross-sectional samples, may not be appropriate for our case. To overcome this issue, we follow a control group designed by Simmons and Hopkins (2005) and use the matching method formalized by Ho et al. (2011).

We first extracted card-months of switchers for the six-month periods pre- and postswitch (12 months total; we label these as the treatment observations). For each card, we then take the average of the covariate values over card-months for the six months before the switch. The covariates used are card balance, utilization rate, spending amount, merchant APR, cash APR, charge-off rate, and card tenure. Second, to create a candidate sample for matches, we extract all consecutive six card-months of nonswitchers and all consecutive six preswitch card-months of switchers that do not overlap to the treatment observations. 1

Then, the covariate values within those six card-months are averaged. This procedure reduces the treatment and control observations to a single data point per covariate. We then apply matching to these observations.

After this transformation of the data, we conducted one-to-one nearest-neighbor matching between switchers and candidate cards based on the Mahalanobis distance in the averaged covariates. The result is that each switching card has one matched control card that is very similar in its six-month average of covariate values. Finally, we combined postswitch card-months of switchers and the subsequent six months following the candidate observations of the matched control group with the matched preswitch observations. Consequently, the matched data for analysis include 12 consecutive card-months of each card, which consist of six months preswitch and six months postswitch observations. As a result, the treatment group includes 3,311 cards and the control group includes 3,239 cards. (Note that some cards in the control group match to multiple cards in treatment group.) Both groups have 39,732 card-month observations, equally split between pre- and postswitch periods.

Results

Table 5 compares preswitch average card profiles between two groups, indicating that the matching created a well-matched control group with similar preswitch card profiles to those of switchers. (We took p-values from the bootstrap Kolmogorov–Smirnov test.) Web Appendix D also shows that the matching exercise produces switching and control groups that are closely matched by socioeconomic characteristics (Table W4) and by preswitch monthly balances (Figure W5).

Comparison of Preswitch Average Card Profile.

Notes: p-values are taken from bootstrap Kolmogorov–Smirnov test (1,000 resamples).

Figure 2 illustrates the main estimates from the single-hurdle difference-in-differences, plotting the coefficient estimates and 95% confidence intervals (CIs) for Switcher × Months from Switch interactions for the dummies from five months before switching to the minimum automatic repayment through to five months after the switch, shown on the x-axis.

Coefficient estimates and CIs for the effect on payments of switchers switching to a minimum automatic repayment.

Results indicate that the coefficient on the interaction term is at or close to zero for the months preceding the month of switch, indicating no difference in repayment levels prior to the switch. At the switch month (month zero), the coefficient becomes negative and statistically significantly different from zero. The coefficients also show no trend upward or downward in the preswitch period. This indicates a reduction in payments due to switching. The coefficient on the interaction terms for the subsequent months remains negative and statistically significantly different from zero in each month. Thus, there is a precisely defined downward effect of switching to minimum automatic repayments on the level of payment.

Table 6 presents the coefficient estimates. The top panel of shows results from the first-stage regression. The coefficient on the tenure variable is positive, indicating that the probability of not missing a payment rises with tenure, as suggested found in previous studies. The coefficients for the interaction terms of switcher dummy and months from switch dummies are positive and precisely estimated for postswitch months, confirming the beneficial effect of automatic repayments eliminating a chance of forgetting a repayment.

Coefficient Estimates from Single-Hurdle Selection Model.

*p < .05.

**p < .01.

***p < .001.

Notes: The prefix of h1 indicates the estimation of the probability of not forgetting a repayment (the first component of the model). The prefix of h2 indicates the estimation of latent repayment given not forgetting a repayment (the second component of the model).

The bottom panel of Table 6 presents results from the second-stage regression. The coefficients on the covariates indicate that the level of repayment increases with card balance and card spend in the preceding month, and decreases with utilization, merchant and cash APRs, and the charge-off rate.

The coefficients for the interaction terms are negative and precisely estimated for all postswitch months, confirming the adverse effect of the minimum automatic repayment reducing ongoing repayments as observed in Figure 2. The coefficient values range from −.65 in the first month after the switch, rising to −.36 after four months. A coefficient value of approximately −.4 for the postswitch interaction in the second element of the model implies that switchers reduce their payments by approximately 40%, which equates to on average £148 (evaluated against the baseline predicted level of repayment from the model).

Instrumental Variable Model

The instrumental variable approach uses an exogenous source of variation in the likelihood of treatment, which serves as an instrument to the treatment selection. This approach has the advantage that it introduces as-good-as-random variation in the likelihood of treatment, but it has the challenge of needing to find an instrument that predicts treatment (here, switching) but is exogenous to the individual's repayment choice.

Here, we exploit geographic peer group switching rates as the instrument in a two-stage design. The rationale for this instrument is that the switching rate to automatic payments within an individual's peer group is likely to spill over to affect the individual's behavior through shared knowledge and social norms. Prior literature has found peer effects to be important determinants of financial decisions (e.g., Bailey et al. 2018; Bursztyn et al. 2014). In marketing, peers have been used as instruments to identify the effects of chief marketing officers on firm performance (Germann, Ebbes, and Grewal 2015) and herding in spending disclosure decisions (Shi, Grewal, and Sridhar 2021) (for an examination of instrumental variable approaches in marketing, see Rossi [2014]). We estimate the local average treatment effect of peer effects induced switching on repayments using a two-stage least squares approach:

We report the results in Table 7. In the first-stage regression, the coefficients on the covariates indicate that the likelihood of switching increases with the merchant APR and decreases with the cash APR, charge-off rate, and level of spending. The coefficient on the instrument is positive (.950) and precisely defined with a standard error of .004, indicating a strong correlation between the switching rate in the locality and the likelihood of the cardholder switching.

Coefficient Estimates from Instrumental Variable Estimate.

*p < .05.

**p < .01.

***p < .001.

Notes: OLS = ordinary least squares; 2SLS = two-stage least squares.

In the second-stage regression, the coefficients on the covariates show that repayments increase with the balance and spend and decrease with the merchant and cash APR, the charge-off rate, and account utilization. The coefficient on the instrumented postswitch variable is negative, taking a value of −.553. This is within the range of the postswitch coefficients from the difference-in-differences model, implying a 55% reduction in repayment arising from the switch to automatic minimum payment.

Robustness Tests

Conditional difference-in-differences model

An alternative approach to modeling repayments in the difference-in-differences framework is to model only nonmissed payments. While the single-hurdle selection model including missed payments is the preferred model, for comparison here we also present ordinary least squares (OLS) estimates of the repayment equation. This is estimated on the subset of observations with a nonmissed payment (67,475 observations, 92.1% of observations from the sample used in the single-hurdle selection model).

Results, shown in Web Appendix F, reveal the same pattern in the difference-in-differences coefficient estimates on the interaction term (Figure W7), with the estimated coefficient for the preswitch months indicating no difference in repayment levels prior to the switch. At the switch month (month zero), the coefficient becomes negative and statistically significantly different from zero. This again indicates a reduction in payments due to switching. Coefficient estimates are reported in Table W5. The estimates from the OLS model are similar in magnitude to those from the single-hurdle selection model (the coefficient on the interaction term for month zero is −.67 in the OLS estimates compared with −.65 in the single-hurdle selection model estimates).

Type II Tobit model

The single-hurdle selection model assumes independence in the error terms across the first-stage and second-stage equations, ε1,i,t and ε2,i,t. However, in practice the error terms may be correlated. To test the robustness of our results to this assumption of independence, we also present estimates from an exponential Type II Tobit model, which assumes dependence of errors across equations. This model is estimated on the same sample of observations as the single-hurdle selection model.

Results, shown in Web Appendix G, again reveal the same pattern in the difference-in-differences coefficient estimates on the interaction term (Figure W8), with the estimated coefficient for the preswitch months once again indicating no difference in repayment levels prior to the switch. At the switch month (month zero) the coefficient becomes negative and statistically significantly different from zero. This again indicates a reduction in payments due to switching. Coefficient estimates are reported in Web Appendix Table W6. The coefficient on the interaction term for month zero is again of similar magnitude in the Type II Tobit model estimates (−.78) to that in the single-hurdle selection model estimates (−.65).

Lender-induced switching sample

As an additional robustness test, we exploit a feature of lenders’ account management practices that arguably introduces a degree of exogeneity in switching for a subset of accounts. Specifically, we focus on a subsample of accounts where lenders are more likely to have played a role in setting up minimum automatic repayments via offering refunds to customers to induce them to switch to automatic payment. Results from this analysis, which are included in Web Appendix E, are consistent with our main results for the effects on levels of repayment of switching to automatic minimum payment.

Excess Interest Cost Simulations

We have used Monte Carlo simulation to estimate the financial cost arising from lower repayments among cardholders switching to a minimum automatic repayment (for details, see Web Appendix I). We also conducted a simulation estimating what proportion of total interest and fees incurred by all cards across the entire credit card market is due to minimum automatic repayments (detailed in Web Appendix J).

The simulation is implemented as follows. We assume two types of agents. The first type of agents never switch to automatic repayment (“Remaining as Nonauto Cards”), while the second type of agents switch to a minimum automatic repayment (“Switching to Min. Auto Cards”). To resemble real-life use of credit cards, the simulation assumes a steady continuation of purchases and repayments.

For both types of agents, we simulate their monthly card usages and repayments, using card-month observations of cards switching to minimum automatic repayments during the data period. At each time-step (i.e., month) in the simulation, a repayment category is drawn from the actual distributions in card-months with similar card profiles. The categories include “missed,” “minimum” (with £10 buffer for rounding up), and “full.” Repayments in the actual distribution that are not included in the missed, minimum, or full categories were categorized as their own absolute value (e.g., £50.00, £100.00, £200.00). Repayments are capped at a corresponding full balance at the time step. For Remaining as Nonauto Cards, we use the preswitch distribution, whereas for Switching to Min. Auto Cards, we use the postswitch distribution. Thus, in the simulations, Remaining as Nonauto Cards are repaid as if cardholders had not switched to a minimum automatic repayment. If an agent missed a repayment, a late payment fee was incurred. In addition, spending and cash advance amounts are also drawn from these distributions. If an agent made a cash advance or the utilization rate exceeded 1, a cash advance fee or an over-limit fee was incurred (regulated fee levels in the United Kingdom were used). The simulation continued for 24 months. We ran the simulation with the mean balance in the months when cardholders switched to minimum automatic repayments (£1,330.34). Further technical details are presented in Web Appendix I.

Figure 3 shows the results where we see consistently higher balances (Panel A) and higher total costs (Panel B) in the 24-month period. Therefore, even accounting for the higher prevalence of late payment fees among Remaining as Nonauto Cards, the simulations show that Switching to Min. Auto Cards creates higher costs of debt for the consumer.

The results from the excess interest cost simulation.

Simulation responses (Web Appendix J) further show that cards using minimum automatic repayments at least once in the data period could save approximately 19.8% of interest and fees if they did not switch to minimum automatic repayment. This is about 8.4% of all interest and fees paid in the credit card market. Even an effect ten times smaller would be economically significant.

Experimental Study: Anchoring Effects of Minimum Payments on Manual Payments

In our second study, we focus on manual credit card repayments and use an online experiment to explore how minimum payments also affect repayment behavior among manual payers (i.e., those not using automatic payments).

We first replicate the finding from previous studies that people anchor on the minimum payment information presented in the credit card payment journey, showing reduced repayments (Jiang and Dunn 2013; Navarro-Martinez et al. 2011; Salisbury and Zhao 2020; Stewart 2009).

We extend the experimental design to test potential remedies to the effect of presenting minimum payments. Specifically, we test for effects of (1) prompting people to pay in full before offering partial and minimum payments options and (2) prompting those who choose to repay below or near the minimum to repay more. These interventions aim to lower the anchoring effect of minimum payments. In the first case, prompting people to pay in full before offering other options was intended to raise this option in people's minds before they chose an amount to repay. In the second case, prompting people who pay too little to pay more provided them with critical information about the time to repay at the moment of choice, without suggesting low repayments to those who spontaneously chose to repay more. We anticipated that these treatments would be effective because they were easy and timely (Service et al. 2014).

We conducted the experiment in collaboration with the U.K. financial regulator, the Financial Conduct Authority (FCA), as part of its study investigating the U.K. credit card market. We did not externally preregister the experiment because of the nature of this study. The experiment received ethical approval from the University of Warwick research ethics committee. A unique property of this experimental design is that it has increased external validity, as research has demonstrated that hypothetical repayment responses are correlated with real-world repayments on linked credit card transaction data (Guttman-Kenney, Leary, and Stewart 2018).

Method

Participants

We used the crowdsourcing platform Prolific Academic to recruit 1,000 participants who were living and employed in the United Kingdom and spoke English as a first language. We decided in advance to eliminate (in a sequential process) those who did not reach the end of the experiment (7), duplicate submissions (112), submissions from the same IP address (35), participants who did not answer “yes” to a question asking if they answered carefully (54), the top 5% of fastest responses (37), and 56 people for whom the experiment duration was not recorded. This left 699 participants.

Design

Participants were randomly assigned to one of four cells in a 2 × 2 design, crossing omission or inclusion of a minimum payment prompt with initially prompting (or not) for a full repayment. While we did not have a theoretical reason to expect an interaction, an interaction would have implications for policy design. Table 8 describes the treatments. The control condition included the minimum payment prompt but did not prompt for full repayment, just as in real-world credit card statements. The omit-minimum condition differed only in omitting minimum payment information from the bill. The include-prompt condition retained the minimum payment information and also initially asked participants whether they would like to pay the bill in full before offering other payment options. The omit-and-prompt condition combined both of the previous treatments, omitting minimum payment information and initially prompting for full repayment.

Experiment Design.

Procedure

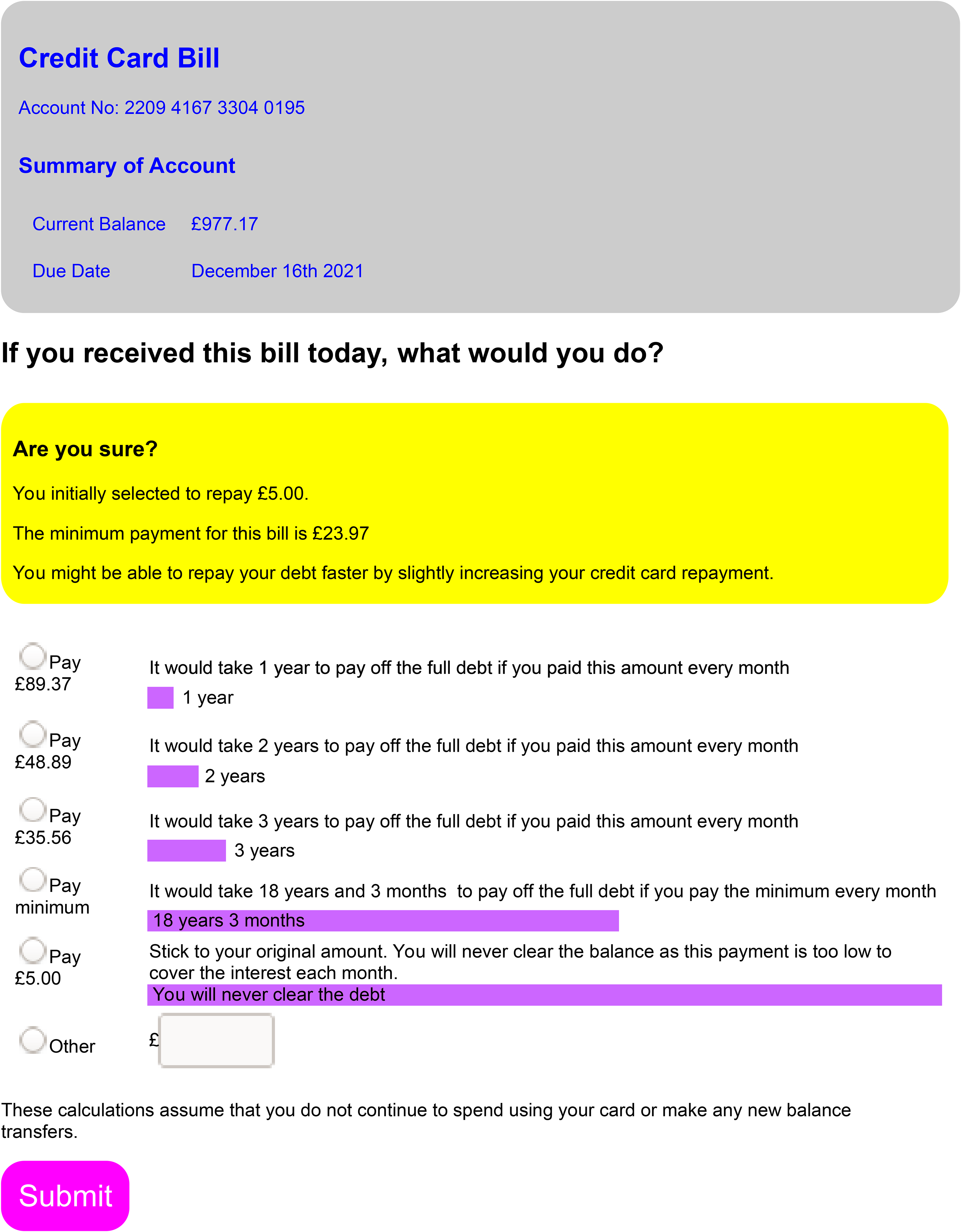

Participants were asked to imagine that they had received a credit card bill, to consider how much money they actually had, and to decide how much of the hypothetical bill they would repay. The bill was for the 2011 U.K. median of £977.17, with the corresponding median minimum payment of £23.97 (Navarro-Martinez et al. 2011).

In the control condition—with the minimum payment amount and without an initial full repayment prompt—participants were given the bill information and entered their hypothetical repayment (see Figure 4, Panel A). In the conditions without the minimum payment amount, the minimum payment information was omitted from the bill (Figure 4, Panel B). In the conditions with an initial full repayment prompt, participants were first asked whether they would like to pay in full or not (Figure 4, Panel C). If they selected “no,” they entered the payment amount.

The presentation of hypothetical statements in the experiment.

Afterward, we asked participants to report whether they have a credit card and whether they paid their bill in full in the previous month. Balance tests in Web Appendix K show that conditions were about equal and did not differ significantly in the fraction of participants who used credit cards or who paid their bill in full in the previous month.

We also collected a secondary measure for some participants, conditional on their initial payment choice. If a participant initially chose a repayment amount at or lower than the minimum payment, they were then shown a “low payment prompt” offering six options: the payments required for one-, two-, and three-year paydown; the minimum; the amount they originally chose; and a blank box for any other amount (Figure 5). If participants chose a repayment above the minimum but below 1.5 times the minimum, they were offered five of the six options. For these participants, we omitted the minimum payment option because they had already chosen to pay more than the minimum, and we did not want to reanchor them to this amount.

Low payment prompts shown to those selecting to pay below 1.5 times the minimum in the experiment.

Measures

Our primary dependent variable was the amount that participants selected as their repayment for the bill. We also had, as secondary dependent variable, a (potentially) revised repayment amount after participants making low payments were prompted to make higher repayments. We describe these in more detail next, along with the independent variables and covariates.

Repayment Amount

The dependent variable was the amount (in £) that participants selected as their repayment for the bill. In conditions with a full repayment prompt, participants could select a radio button to make a full repayment, which was recorded as £977.17. In conditions without a full repayment prompt, or after selecting “no, repay less than the full outstanding statement balance” in conditions with a full repayment prompt, participants typed a repayment amount (in £) in a text box.

Revised Repayment Amount

As described previously, if participants made a low repayment, they were offered a series of prompts to make a higher repayment. The measure was also in British pounds, with radio button responses coded as their amount. This secondary dependent variable was only measured for those who chose an initial repayment less than 1.5 times the minimum (i.e., below £35.96).

Independent Variables

We had two independent variables: (1) whether minimum payment information was included or omitted from the credit card statement and (2) whether participants were asked if they would like to pay in full before being able to give an open response of any repayment amount (if they declined to pay in full).

Measures for Data Quality

We collected three variables to screen for data quality (e.g., Buchanan and Scofield 2018). We asked participants if they chose a repayment option carefully and thoughtfully, with response options of “Yes, I took care” or “No, I just want the payment.” We had decided in advance to exclude anyone answering “No.” We also recorded the duration of the experiment, having decided in advance to exclude the 5% of people who were fastest. We recorded the IP address and Prolific Academic ID to delete participants who made duplicate submissions. 2

Results

Our primary analysis compares repayments with and without minimum payment information and with and without prompts for full repayment. Table 9 reports the mean repayments. As we hypothesized, repayments were higher when minimum payment information was omitted and when participants were first prompted to pay in full.

Experiment Repayment Means and CIs.

Notes: Mean repayments [95% CIs].

To quantify these findings, we analyzed repayments with a linear regression of repayment amount on a minimum-payment-information dummy, a full-repayment-prompt dummy, and their interaction. Because the interaction was not significant, and we had no theoretical reason to expect it to be, we report the regression without an interaction. The coefficient for the minimum-payment-information dummy estimates the increase in repayments when minimum payment information was omitted. The coefficient for the full-repayment-prompt dummy estimates the increase in repayments when full repayment is prompted.

Model 1 in Table 10 shows the coefficients. Averaging over full repayment prompting, omitting minimum payment information raised the mean repayment from £447 (95% CI: [£404, £490]) to £535 (95% CI: [£491, £579]). This was a significant increase of £88 (95% CI: [£26, £149], t(696) = 2.79, p = .005). Averaging over minimum payment inclusion, repayments were also higher when the full repayment prompt was included. Including a full payment prompt raised the mean repayment from £438 (95% CI: [£395, £481]) to £545 (95% CI: [£501, £589]). This is a significant increase of £107 (95% CI: [£45, £169], t(694) = 3.40, p < .001).

Repayment Regression Estimates Including Controls for Card Usage.

*p < .05.

**p < .01.

*** p < .005.

Notes: Intervals are 95% CIs.

Robustness tests

One possibility is that the behavior of participants in our online experiment in part reflects their own financial situation. For example, some participants might select minimum payments because this is their usual repayment behavior on their own credit card—for example, because they face low income or liquidity constraints in their finances. At the suggestion of a reviewer, we draw on the self-reported information provided by participants on their real-world financial position to control for this possible confound (note also that, as we report in Web Appendix K, conditions were balanced on these variables). Models 2 and 3 in Table 10 include a card-user dummy indicating whether the participant has a real credit card. The dummy is included as a covariate in Model 2 and additionally interacted with the experimental manipulations in Model 3. The pattern of results for the experimental manipulations is unchanged. Holding a card is associated with higher repayments. The null interaction shows no evidence that the experimental manipulations are affected by cardholding. Models 4 and 5 repeat the exercise with a full-repayment dummy indicating whether the participant typically repays their bill in full. Again, the pattern of results is unchanged for the experimental manipulations. A history of full repayment is associated with higher repayments but does not interact with the experimental manipulations.

Because the distribution of repayments departs from Gaussian, we have included supplementary analyses. In Web Appendix K we show, consistent with the previous analysis of the means, that the distribution of repayments when the minimum is omitted first-order stochastically dominates the distribution when the minimum is included. Further, the distribution of repayments when full repayment is prompted first-order stochastically dominates the distribution when full repayment is not prompted. We also analyze the probability of making minimum repayments, which is reduced when the minimum is omitted and full repayment is prompted, and the probability of making full repayments, which is increased when the minimum is omitted and full repayment is prompted—again consistent with the analysis of the means.

Low payment prompts

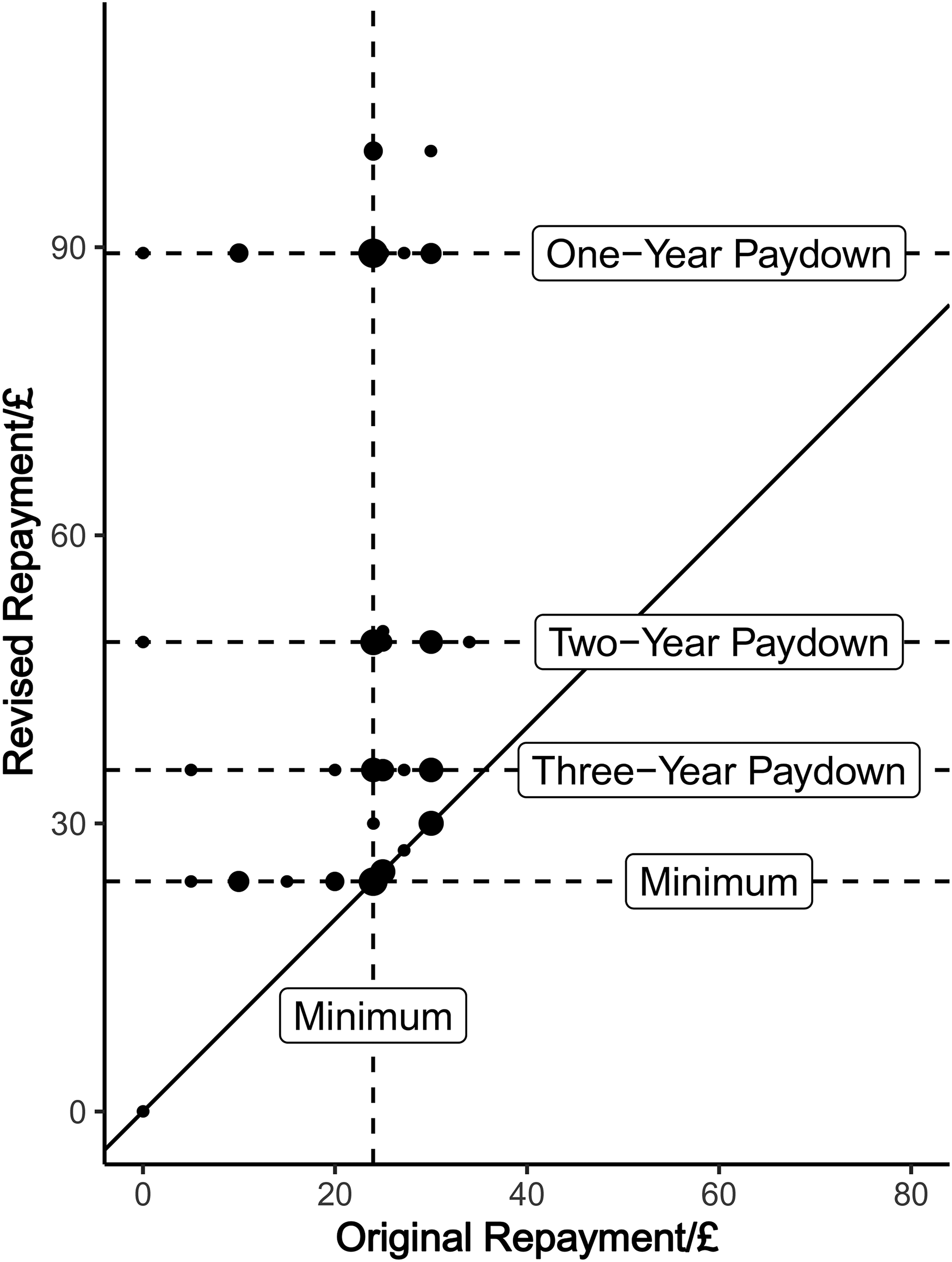

Figure 6 shows how the 106 people paying at or below 1.5 times the minimum (here, £35.95) revised their payments after the low payment prompts. Twenty-eight participants kept their original repayment, no one decreased their repayment, and 78 people revised their repayment upward (typically to one of the prompted payment amounts). For some people, the increase was substantial—for example, moving from initially selecting to pay only the minimum to then selecting to pay an amount that would amortize debt in a year (“One-Year Paydown”) is more than a tripling of payment amounts. Participants were 2.53 (95% CI: [1.68, 3.92]) times more likely to increase their payment than leave it unchanged.

Revised payments for those prompted to pay more in the experiment.

Experiment Discussion

Omitting minimum payment information increased repayments, replicating findings from Jiang and Dunn (2013); Navarro-Martinez et al. (2011), Salisbury and Zhao (2020), and Stewart (2009). We also tested two new interventions. First, an initial prompt to pay in full increased repayments. Second, prompting people who initially selected to pay at or near the minimum to repay more—by providing scenarios about the payments needed to clear the debt in one, two, or three years—also increased repayments for the majority prompted. We think this prompt was successful because (1) it provided scenario information at exactly the right time, unlike previous interventions that found only small effects local to the scenario repayment amount (Agarwal et al. 2015; Hershfield and Roese 2015; Keys and Wang 2019; Navarro-Martinez et al. 2011), and (2) prompting people to make a second choice is a Gricean indication that their first choice was poor (Rose and Blank 1974)—a finding in line with a recent meta-analysis that concluded that defaults are more effective when they are perceived to communicate what a choice architect thinks a decision maker should do (Jachimowicz et al. 2019).

General Discussion

Defaults exist in many areas of individual choice and are commonly used by policy makers as a device to achieve behavioral change. However, there is concern that defaults may have unintended consequences and that the positive effect of introducing a default on one outcome may co-occur with negative effects on other outcomes.

Our analysis of minimum payments indeed shows unintended effects of defaults when multiple outcomes are examined. We find that setting an automatic repayment has the mixed effect of nearly eliminating the likelihood of missed repayments while also decreasing average payments. Why does this occur? One interpretation is that the minimum amount being paid automatically reduces people’s attention to balances. Consumers who choose minimum automatic repayments are selecting a potentially powerful psychological default, one that facilitates inattention. This results in repeated minimum repayments, which greatly increases the debt revolved from month to month and, thus, the interest paid.

This unintended effect of the default raises the need for potential mitigations. Our experimental study explored the efficacy of interventions. We first replicate the now-robust result that merely providing minimum payment information reduces repayment. We also show that providing alternative information—namely, a prompt for full repayment or to reconsider low repayments with explicit higher repayment amounts suggested—mitigates the effect of anchoring on the minimum repayment. While other attempts have failed, we believe ours succeeded because the information was presented just in time, exactly when it was required. Whether consumers are opting in to their own minimum payment default by setting an automatic repayment or are anchoring their manual repayments on the minimum, minimum payments have detrimental effects.

We have focused here on credit card repayments where consumers face an explicit choice about the size of their automatic repayment and can easily make additional manual repayments. However, the power of setting a default repayment is applicable more widely. For example, choosing the term of a mortgage or choosing fixed monthly repayments for a personal loan also sets powerful defaults, and these defaults are administratively harder to change, and changes can even incur additional costs. If people are initially conservative in their choice of repayment level, so they can be sure they can meet their monthly repayments, our findings suggest that they are unlikely to make additional repayments over and above the default even if they can afford to do so to save interest costs.

A limitation of our study is that we cannot provide direct evidence that attention is the mechanism underlying consumer behavior, and therefore the theoretical contribution of our study is limited. Thus, looking to future research, we suggest approaches that could help shed light on the underlying theoretical mechanism, potentially leading to policy solutions. It may be that the unintended effect of minimum automatic repayment could be partially addressed through interventions that bring the repayment decision back to the top of the consumer's mind, drawing attention to the repayment decision and shrouding the minimum payment. More generally, what should policy makers and industry do to avoid introducing defaults with unintended effects? We have two suggestions. The first is to consider the status quo effects resulting from the default itself—is the new status quo unambiguously in the consumer's interest? The second is to assess the effect of the defaults across as broad a range of outcome behaviors as available and to follow up on these assessments over time. This approach will help policy makers fully evaluate the impact of defaults and consider whether mitigations are necessary in the presence of unintended consequences.

Supplemental Material

sj-pdf-1-mrj-10.1177_00222437211070589 - Supplemental material for Default Effects of Credit Card Minimum Payments

Supplemental material, sj-pdf-1-mrj-10.1177_00222437211070589 for Default Effects of Credit Card Minimum Payments by Hiroaki Sakaguchi, Neil Stewart, John Gathergood, Paul Adams, Benedict Guttman-Kenney, Lucy Hayes and Stefan Hunt in Journal of Marketing Research

Footnotes

Acknowledgments

The authors thank David Laibson and Nick Lee for comments and discussion.

Author Contributions

Sakaguchi, Stewart, and Gathergood designed and completed the field data study. Stewart and Gathergood obtained the data. Sakaguchi ran the regressions and created the figures and tables. Stewart, Adams, Guttman-Kenny, Hayes, and Hunt designed and completed the experimental study. Stewart ran the experiment, analyzed the data, and created the figures and tables. Stewart and Gathergood drafted the paper, which was honed by the whole author team. This research was conducted while Adams, Guttman-Kenney, Hayes, and Hunt were employees of the FCA. The views and opinions expressed here are those of the authors and do not necessarily reflect the views of the Financial Conduct Authority, Competition & Markets Authority, their affiliates, or their employees.

Associate Editor

Vikas Mittal

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by Economic and Social Research Council grants ES/N018192/1, ES/K002201/1, ES/P008976/1, and ES/V004867/1, and Leverhulme Trust grant RP2012-V-022. The first author acknowledges PhD studentship 1499648 from the Economic and Social Research Council.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.