Abstract

Multichannel sales systems in business-to-business markets vary substantially in their designs and thereby either attenuate or aggravate agency conflicts between manufacturers and sales partners. Drawing on multiple agency theory, the authors introduce direct and indirect channel usage as focal design dimensions of multichannel sales systems and investigate each channel’s performance effects using a matched manufacturer–sales partner data set. Whereas direct channel usage predominantly lowers agency conflicts in terms of information asymmetry and sales partner moral hazard, indirect channel usage amplifies moral hazard concerns. How those sales partner effects translate into manufacturer performance outcomes critically depends on governance mechanisms, confirming predictions from governance value analysis: formalization enhances performance outcomes for manufacturers in the case of indirect channel usage but diminishes performance in the case of direct channel usage. The authors observe converse effects for centralization and information exchange: centralization and information exchange enhance outcomes of direct channel usage but diminish outcomes of indirect channel usage. The focal managerial implication is that managers must align the design of their multichannel sales systems with effective governance mechanisms.

Keywords

Multichannel sales systems have become the norm in business-to-business (B2B) markets (Lawrence et al. 2019; Sa Vinhas and Heide 2015). Of the different sales channels that B2B companies (principal) employ, at least one is an indirect channel (agent) (e.g., dealers, external online shops). This is the case for most—almost 80%—of B2B manufacturers (CMO Survey 2019), likely provoking agency conflicts (e.g., Antia, Mani, and Wathne 2017; Heide 2003; Srinivasan 2006). Thereby, the scale of such agency conflicts likely depends on the design of multichannel sales systems. Manufacturers combine direct and indirect channels to different extents, and these channels typically vary in their economic importance for the manufacturer (i.e., relative revenue contributions) (e.g., Sa Vinhas and Anderson 2005; Van Bruggen et al. 2010).

The design choices within multichannel sales systems can attenuate or aggravate agency conflicts. Increased direct channel usage 1 may provide manufacturers with reference standards for sales partner management, thereby reducing agency conflicts (Dutta et al. 1995; Heide 2003). However, direct channel usage may also induce agency conflict. For example, sales partners may benefit from the manufacturer’s presales activities and reduce their own selling efforts (Sa Vinhas and Heide 2015).

Similarly, increased indirect channel usage may make manufacturers particularly vulnerable to shirking or misdirected efforts by sales partners (Zeng et al. 2015; Zheng et al. 2020). For example, in 2018, when the BMW Group tried to enforce novel contracts with its indirect sales partners, it experienced substantial resistance: 90% of BMW’s indirect sales partners joined forces to combat the novel contract terms, even jointly threatening BMW with terminating their current contracts (Fasse 2018). Relatedly, a manager of a large manufacturer of cutting tools and services that distributes products through direct and indirect channels informed us that 17 to 20 of his sales partners from various sales channels recently formed a purchasing cooperative, which led to a feud. In addition to cooperating on the terms of negotiations, the sales partners began producing the manufacturer’s product on their own.

Prior research (reviewed in Table 1) has investigated differences between multichannel and nonmultichannel settings but has hardly explored design differences within multichannel sales systems. Specifically, very little is known about the effects of direct and indirect channel usage. Consequently, the jury is out as to how companies can counterbalance potential agency conflicts that degrees of direct and indirect channel usage provoke.

Selected Studies on Performance Outcomes of Multichannel Sales System Design.

Notes: ✓ = included in the study; (✓) = partially included in the study; — = not included in the study. a Antia, Mani, and Wathne (2017) refer to dual distribution as “monitoring.” bThe franchising context (company-owned vs. franchisee stores) differs from more “traditional” multichannel contexts (e.g., franchisors have more control). cConcurrent sourcing focus is conceptually related to our context. d Heide, Kumar, and Wathne (2014) conduct a post hoc study with matched manufacturer and sales partner data. e Kabadayi, Eyuboglu, and Thomas (2007) assume a configurational perspective, which does not allow for isolating the individual effects.

Governance mechanisms may represent one effective way to mitigate such agency concerns and increase manufacturer performance (Antia, Mani, and Wathne 2017). Agency theory proposes that formalized “rules of the game” (Fama and Jensen 1983, p. 302) reduce conflict and lower “ex post costs through ex ante alignment” of manufacturer and sales partner interests (Bergen, Dutta, and Walker 1992, p. 8). Thus, we explore the role of formalization, or the degree to which fixed and written rules, polices, and procedures govern sales partner decision making in a channel system (Kabadayi, Eyuboglu, and Thomas 2007). In addition, the delegation of decision making authority to sales partners and information asymmetry between manufacturers and sales partners stimulate agency conflicts in the first place (Eisenhardt 1989; Hoenen and Kostova 2015). Thus, we include centralization (i.e., the degree to which decision making authority in a channel system is concentrated at the manufacturer level; Dwyer and Welsh 1985) to mitigate the former, and we include information exchange (i.e., bilateral expectation that manufacturers and indirect sales partners will provide each other with useful information; Heide and John 1992) to reduce the latter.

In practice, companies likely decide simultaneously on multichannel design and governance mechanisms (Heide, Kumar, and Wathne 2014), which affects their performance results (Ghosh and John 1999, 2005). For example, rigid formal governance might gain importance with increasing indirect channel usage to control sales partner behaviors. However, such rules may restrict manufacturers’ flexibility in reacting to new circumstances and thus undermine their performance outcomes for direct channel usage. Remarkably, such alignment between governance choice and multichannel design remains largely unexplored (Table 1). The importance of this research gap becomes apparent in light of recent findings: Depending on the multichannel design (i.e., single vs. multichannel settings), the performance effects of the same governance mechanism can reverse from positive to negative (Heide, Kumar, and Wathne 2014).

Against this background, our overall research goal is to establish how multichannel design (direct and indirect usage) affects manufacturer performance contingent on governance mechanisms. Essentially, we develop two theoretical ideas. First, drawing on multiple agency theory, we investigate the idea that multichannel system design affects the individual manufacturer–sales partner relationship. Second, we integrate multiple agency theory and governance value analysis and develop alignment effects between multichannel design and governance mechanisms. To aid our empirical investigation, we compiled a unique data set. We collected primary data from a broad range of multichannel manufacturers from different industries that we enriched with objective performance data from archival data sources. In addition, we collected matched sales partner data. Such a design is rare, but it allows us to address calls from prior investigators to demonstrate the effects of multichannel design for both sides of the manufacturer–sales partner dyad (Sa Vinhas and Heide 2011; Sa Vinhas and Johnson 2019).

We offer three contributions through our research. First, we introduce multiple agency theory to the multichannel context. In doing so, we extend the idea that “individual relationships (between manufacturers and sales partners) are embedded in a context of other relationships that could have governance implications” (Heide 1994, p. 81). Moreover, we integrate agency theory with governance value analysis. We find that agency mechanisms not only instill order but also create value (e.g., Heide, Kumar, and Wathne 2014).

Second, we address calls for extending research on the design of multichannel sales systems (e.g., ISBM 2020; MSI 2018; Sa Vinhas and Johnson 2019). Prior research has examined the outcomes of moving from a single channel to multichannel settings (e.g., Dutta et al. 1995), but researchers have only begun investigating design consequences within multiple sales channels (Antia, Mani, and Wathne 2017; Srinivasan 2006). We extend initial research on how design variation within a multichannel context affects both manufacturer performance and matched sales partner behavior. In addition, we contribute to the literature by introducing indirect and direct channel usage as focal design elements. In doing so, we address calls to extend prior measurements of channel usage to the multichannel context (Van Bruggen et al. 2010).

Third, we contribute to the governance literature by addressing calls for exploring the alignment between governance mechanisms and channel design (Frazier 1999; Heide, Kumar, and Wathne 2014), which thus far has remained largely unexplored (Table 1). Extending prior literature, we demonstrate that the same governance mechanism (e.g., formalization) can enhance manufacturer performance in one setting (e.g., aligned with indirect channel usage) but diminish manufacturer performance in the other (e.g., aligned with direct channel usage). In doing so, we also extend literature on formalization, centralization, and information exchange, which has largely investigated their performance effects in a context that differs greatly from the reality of today’s multichannel sales systems (e.g., Boyle and Dwyer 1995). We show that these governance mechanisms are still effective when aligned with multichannel design.

Theoretical Background and Conceptual Model

Multichannel Design and Direct and Indirect Channel Usage

Multichannel sales systems refer to manufacturers simultaneously employing multiple sales channels to sell the same products in the same sales region (e.g., Sa Vinhas and Anderson 2005; Sa Vinhas and Heide 2015). Such systems comprise dual distribution (reliance on both direct and indirect channels) and nondual distribution systems (reliance on either direct or indirect channels) (e.g., Antia, Mani, and Wathne 2017; Heide 2003). Overall, multichannel sales systems can differ in the type of channels (direct vs. indirect dimension) and number of channels installed (variety dimension) as well as in the extent to which each channel is used (intensity dimension) (e.g., Käuferle and Reinartz 2015; we provide an illustrative example in the “Measurement” section). However, companies do not independently decide on these dimensions: After having decided on the type and number of channels, manufacturers need to decide on their intensity of usage (Van Bruggen et al. 2010). Thus, we consider all dimensions jointly. Prior research has followed a similar approach (Sa Vinhas and Anderson 2005) and suggests advantages in jointly considering both dimensions (see the findings Antia, Mani, and Wathne [2017] and Jindal et al. [2007] report in their post hoc tests). 2

We differentiate between direct and indirect channel usage by combining direct versus indirect, variety, and intensity dimensions. We define direct (indirect) channel usage (i.e., direct vs. indirect dimension) as the extent to which companies install (i.e., variety dimension) and use (i.e., intensity dimension) direct (indirect) channels that transact in the same geography and sell the same product. As relationships between manufacturers and their sales partners are embedded in these systems, channel research reveals that evaluating these relationships from an agency perspective is particularly fruitful (e.g., Grewal et al. 2013).

Multiple Agency Perspective on Multichannel Design

In agency relationships, one party (the principal) engages another party (the agent) to undertake an action on its behalf (e.g., Jensen and Meckling 1976). In such a relationship, the problem of moral hazard may arise if an agent refuses to perform the contractually agreed-on behavior. In an indirect channel, such problems of moral hazard derive from the delegation of decision making authority to the sales partner and information asymmetry (i.e., sales partners being better informed about markets or transactions), which likely prevents detection of moral hazard (e.g., Bergen, Dutta, and Walker 1992; Eisenhardt 1989).

Although agency theory has traditionally focused on a dyadic manufacturer–sales partner perspective, individual relationships between manufacturers and sales partners are embedded in a larger context that likely has important governance implications (Heide 1994). Therefore, we draw on multiple agency theory, which also considers interactions between agents (Hoenen and Kostova 2015). Specifically, we develop the idea that manufacturers might use direct channels to reduce information asymmetry and in turn manage indirect channels (in agency terminology, agents [direct channel] are used to manage other agents [indirect channels] [Bohn 1987; Varian 1990]). In addition, multiple agency theory also suggests that interactions between agents (e.g., other indirect channels) can result in opportunism against the principal (e.g., Holmström and Milgrom 1990; Tirole 1986). Thus, multiple agency theory suggests that multichannel design can have an impact on sales partners. Drawing on governance value analysis, we will explore how these effects influence manufacturer performance.

Governing Multichannel Sales Systems for Financial Performance

The core guiding principle of agency theory is to lower potential agency costs. These costs comprise direct costs (e.g., contract costs) but also costs of lost opportunities (i.e., differences in the principal’s welfare due to divergence between the agent’s decisions and decisions that would maximize the principal’s welfare) (e.g., Jensen and Meckling 1976). Governance value analysis emphasizes that minimizing such direct and opportunity costs equates with value creation. According to theory, profit-maximizing manufacturers and sales partners will pursue strategies that maximize their joint value because this will maximize their own profits simultaneously (Ghosh and John 1999), a prediction that Ghosh and John (2005) confirm empirically. However, governance value analysis also suggests that to unfold such a value creation potential, a contingent alignment perspective is necessary. Specifically, governance value analysis emphasizes the alignment between firm resources (e.g., the design of a multichannel sales system) and governance mechanisms. Initial research shows that beneficial effects of channel design on performance unfold in combination with effective governance mechanisms (Antia, Mani, and Wathne 2017; Heide, Kumar, and Wathne 2014).

Drawing on agency theory, we considered formalization, centralization, and information exchange to be important governance mechanisms. Agency theory refers to the “metaphor of a contract” (Eisenhardt 1989, p. 58) as a focal way to resolve agency conflicts. In line with prior research, we interpret contracts in an economic sense as means to create a shared set of rules, procedures, and responsibilities (Hendry 2002). Formalization specifies and codifies the behavior of sales partners in channel relationships by introducing fixed and written rules, policies, and procedures that limit the sales partner’s opportunity to pursue its own goals at the expense of the manufacturer. Thus, we argue that formalization maps onto agency theory’s contract metaphor.

Moreover, a common assumption of agency theory is that manufacturers and sales partners are guided by self-interest and pursue different goals (e.g., regarding assortment decisions). Thus, the delegation of decision making authority to sales partners is likely responsible for creating agency conflicts in the first place (Eisenhardt 1989; Hoenen and Kostova 2015). Consequently, centralization of decision making authority at the manufacturer level might lower the costs of agency conflicts. 3

Finally, information asymmetry likely reduces manufacturers’ ability to detect sales partner shirking or misdirected efforts. Sales partners typically hold an information advantage over manufacturers (e.g., sales partners may possess deeper market and customer knowledge; Frazier et al. 2009). Thus, maintaining information exchange between manufacturers and indirect channels likely lowers agency conflicts.

Hypothesis Development from a Contingent Alignment Perspective

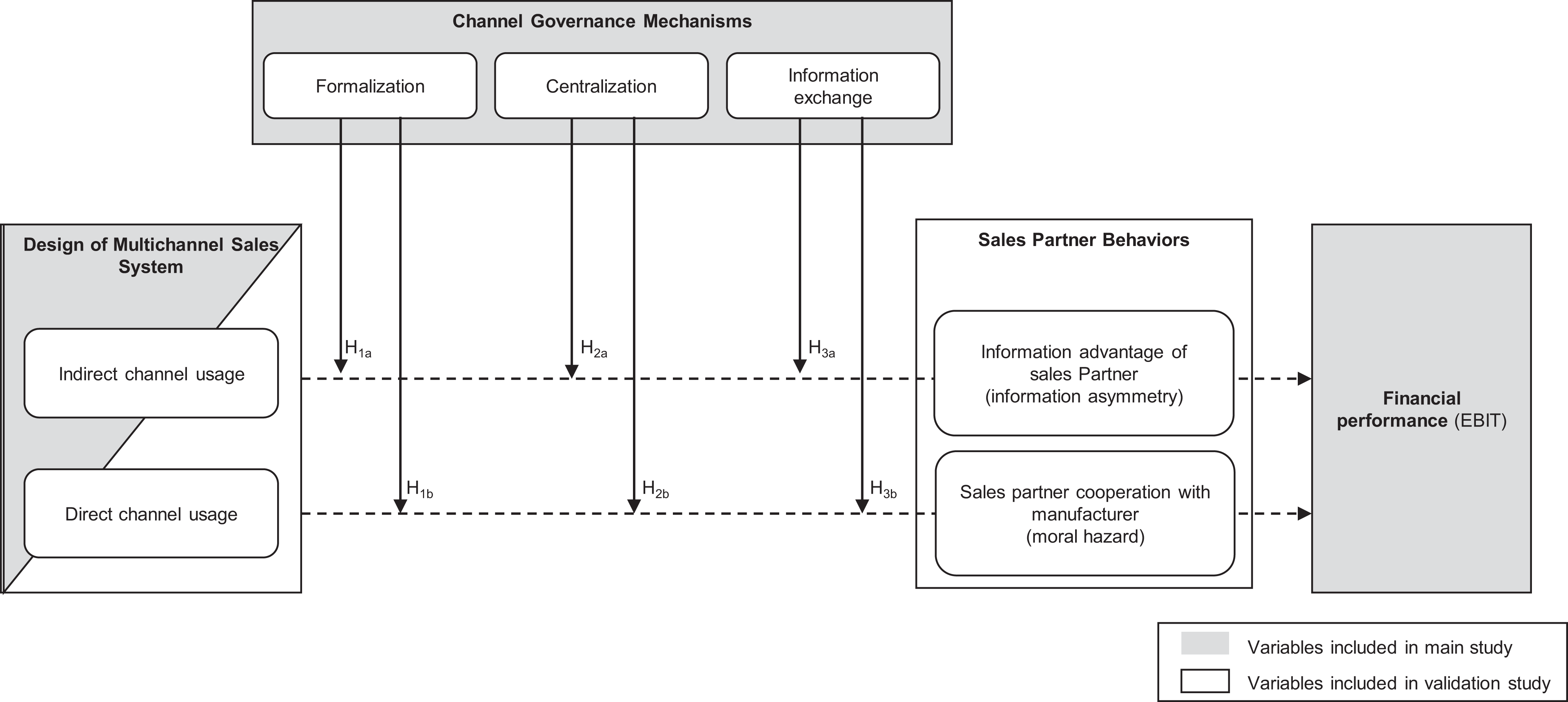

To provide an overview of our logic, we summarize our predictions in Figure 1. Governance value analysis suggests that financial performance effects for the manufacturer result from the alignment between multichannel design (indirect and direct channel usage) and governance mechanisms (formalization, centralization, and information exchange). Thus, we develop our hypotheses from a contingent alignment perspective (main study). However, we will first draw on multiple agency theory to develop baseline effects of multichannel design on sales partners in terms of information asymmetry (sales partners’ information advantage over the manufacturer) and sales partner moral hazard. We investigate those baseline effects in a separate validation study.

Conceptual framework. Notes: In our main study, we assess the financial performance outcomes for the manufacturer. In line with governance value analysis, we develop our hypotheses from a contingency alignment perspective. Thus, we develop hypotheses exclusively for the solid lines. In a validation study, we investigate the impact of multichannel sales system design on sales partner behaviors to test predictions derived from multiple agency theory.

Baseline Effects of Direct Channel Usage on Sales Partner Behavior

Increasing direct channel usage may have downside effects in that, compared to indirect channels, direct channels might be less responsive to market developments and require substantial and binding investments (e.g., Bradach 1997; Srinivasan 2006). However, increased direct channel usage might have beneficial effects such as decreasing sales partners’ information advantage over the manufacturer and reducing moral hazard concerns.

Information asymmetry

Agency theory treats information as a commodity that can be “purchased” (e.g., Eisenhardt 1989). Manufacturers might “purchase” information through in-depth, firsthand experience with direct channel usage. Manufacturers that use various direct channels likely obtain important market know-how (e.g., insights from direct customer contact) and procedural knowledge (e.g., resource requirements for sales processes) (Heide 2003) that sales partners otherwise typically hold, lowering information asymmetry (Frazier al. 2009).

Moral hazard

Such knowledge can favorably spill over to sales partner management and reduce moral hazard. In agency terminology, knowledge accumulated through one agent (direct channel) can be used to manage another agent (indirect channel) (Bohn 1987; Varian 1990). Bradach and Eccles (1989) elaborate that combining franchisee channels with company-owned channels can provide reference standards for evaluating franchisee performance. Research confirms this prediction: Direct sales channels can act as “yardsticks” to evaluate indirect channels (Dutta et al. 1995), or companies can leverage internally generated information to evaluate supplier performance (Heide 2003). Thus, sales partners might anticipate that manufacturers’ internal reference standards (i.e., reduced information asymmetry) help them detect moral hazard (e.g., Antia, Mani, and Wathne 2017).

In addition, manufacturers’ strong engagement in multiple direct channels could serve as a credible threat to replace sales partners, further reducing potential moral hazard and resulting in enforcement benefits (Antia, Mani, and Wathne 2017). In line with our rationale, research reports that concurrent sourcing (i.e., buyers internally producing some proportion of the materials they purchase externally) can indeed lower supplier opportunism (Heide, Kumar, and Wathne 2014). 4

Baseline Effects of Indirect Channel Usage on Sales Partner Behavior

A likely expectation is that indirect channel usage allows manufacturers to benefit from sales partners’ expertise and timely responses to market developments (Srinivasan 2006). However, indirect channel usage likely increases moral hazard concerns and does not lower the manufacturer’s information disadvantage compared with sales partners.

Information asymmetry

Theoretically, similar to direct channel usage, learning from diverse and important indirect channels may lower sales partners’ information advantage over the manufacturer (e.g., reference standards from indirect channels to evaluate other indirect channels) (Butt et al. 2018). However, important tacit knowledge that manufacturers develop from direct channel usage can hardly be obtained from other sources such as indirect channel usage (Kogut and Zander 1992). In addition, explicit knowledge gained from indirect channel usage might also be lower since sales partners may withhold or distort information (e.g., Williamson 1985). For instance, sales partners may withhold information to prevent a common manufacturer from sharing this information with their competitors (Butt et al. 2018). In line with our reasoning, Heide (2003) observes that adding direct channels, but not indirect channels, reduces information asymmetry.

Moral hazard

Multiple agency theory suggests that indirect channel usage increases moral hazard concerns due to competition or cooperation between indirect channels (e.g., Holmstrom 1982; Tirole 1986). Notably, research demonstrates that cooperative and competitive behavior can occur simultaneously; thus, both paths are not mutually exclusive (Luo, Rindfleisch, and Tse 2007; Tsai 2002; Zeng et al. 2015). Sa Vinhas and Heide’s (2015) idea that dual distribution can induce competition between direct and indirect channels can also be transferred to an increase in competition between indirect channels. In B2B settings, indirect channels compete for scarce manufacturer resources (e.g., technical support or product adaptations), likely provoking opportunistic sales partner behavior. For example, sales partners may begin selling products through unauthorized channels, undermining the manufacturer’s sales channel management. Research confirms that competition between indirect channels results in opportunistic behaviors against the manufacturer (Zeng et al. 2015).

Sales partners may, however, also demonstrate cooperative behaviors among each other. Representatives from indirect channels may hold regional meetings and exchange information or run joint promotions or events (El Akremi, Mignonac, and Perrigot 2011; Zeng et al. 2015). Bradach (1997) observes that more senior franchisees train and socialize newer franchisees, which can lead to cooperative behaviors in the future.

Multiple agency theory suggests that such cooperation can lower the manufacturer’s self-interest-seeking behavior (Holmström and Milgrom 1990; Tirole 1986; Waterman and Meier 1998). Sales partners may jointly withhold or manipulate information they share with the manufacturer or directly try to leverage their bargaining power during negotiations. 5 Such behaviors are consistent with the concept of countervailing power in marketing channels (Etgar 1976): Less powerful members join forces to offset the power of a more powerful partner (“common enemy”). Research finds that franchisees work together to offset franchisor power (Zheng et al. 2020) and also reports a significant, positive correlation between sales partner opportunism and cooperation between sales partners (Zeng et al. 2015).

In the following, we examine how those baseline effects translate into manufacturer performance. In line with the governance value analysis, we predict that performance outcomes depend on the alignment between multichannel design (indirect and direct channel usage) and governance mechanisms (formalization, centralization, and information exchange).

Alignment of Multichannel Design and Formalization

Indirect channel usage

We argue that formalization enhances the performance effects of indirect channel usage. A central premise of agency theory is that formalizing rules and procedures likely curtails opportunistic behaviors, which investigators have confirmed in multichannel settings (Sa Vinhas and Heide 2011). On the one hand, formalization may lower competition between indirect channels, reducing opportunistic behavior against the manufacturer. Manufacturers may formalize responsibilities for their sales partners (e.g., provision of technical support or product specifications for sales partners), which may lower perceived competitive pressures (e.g., Sa Vinhas and Heide 2015). In addition, formalization can lower competition for customers when manufacturers clearly allocate customer segments to sales channels. In turn, this may reduce destructive price competition between indirect channels, enhancing manufacturer performance. On the other hand, establishing rules and procedures can guard manufacturers against the capricious mobilization of power (Sa Vinhas and Heide 2011). Thus, formalization might also reduce potential opportunistic sales partner behavior resulting from sales partners exerting countervailing power against the manufacturer.

Curtailing opportunistic tendencies from indirect channel usage through formalization will translate into increased financial performance. Manufacturers can then benefit from sales partners’ expertise and their quick reaction to market developments (Srinivasan 2006). Thus:

Direct channel usage

We expect that the agency cost calculus likely reverses when aligning direct channel usage with formalization. In contrast with indirect channel usage, the opportunism-reducing role of formalization is less important when manufacturers generate revenue from many direct channels. Through the design of the multichannel sales system, manufacturers lower sales partners’ information advantage (Heide 2003) and reduce exchange partner opportunism (Heide, Kumar, and Wathne 2014).

However, when manufacturers use various direct channels, formalization is likely to become a burden, as formalization reduces manufacturers’ scope of action. For example, formalized support for sales partners (e.g., technical support) might restrict manufacturers’ potential to leverage their increased knowledge base (Sa Vinhas and Anderson 2005) and reduce decision-making speed (Baum and Wally 2003). In agency terminology, formalization lowers the principal’s opportunity to engage in self-interest-seeking behavior. Thus, with increasing formalization, opportunity costs “of not shifting to more profitable activities in light of new information” (Ghosh and John 1999, p. 132) arise, in turn lowering financial performance. Thus:

Alignment of Multichannel Design and Centralization

Indirect channel usage

We argue that centralization reduces the performance effects of indirect channel usage. First, centralization will amplify the negative effects of countervailing power that indirect channel usage provokes. Bosse and Phillips (2016) establish that the actions of agents follow the norm of bounded self-interest. This implies that sales partners reciprocate unfair treatments, which can exacerbate agency problems. Sales partners likely perceive centralization as an intrusive governance mechanism that reduces their self-control (Sa Vinhas and Heide 2011), thus creating perceptions of a tilted playing field (Sa Vinhas and Anderson 2005) and reducing perceived fairness. As a likely consequence, sales partners are incentivized to reciprocate by exerting countervailing power against the manufacturer (e.g., withholding information).

Second, aligning centralization and indirect channel usage will not only increase such moral hazard concerns but also amplify their negative performance effects. For centralization to improve the outcomes of indirect channel usage, the focal premise is that manufacturers can adequately specify which sales partner actions best serve their interests. However, when orchestrating multiple and important indirect channels, manufacturers’ “honest incompetence” (Hendry 2002, p. 100) resulting from bounded rationality likely prevents accurate specifications. Bounded rationality arises from limited information-processing capacities, reliance on shortcuts and heuristics, and cognitive biases (Foss and Weber 2016). Manufacturers who use multiple indirect channels, must access many different information sources that might exceed their information-processing capacities. At the same time, amplified moral hazard concerns likely lead sales partners to withhold information or even distort the information they share with the manufacturer (Tsai 2002; Williamson 1985). Thus, manufacturers are likely to rely more strongly on information that is readily available to them (Tversky and Kahneman 1973). If so, they may unconsciously rely too much on firsthand knowledge accumulated from direct channels or even “gut feeling,” which can be problematic because sales partners tend to possess more valuable market knowledge (Frazier et al. 2009).

Consequently, manufacturers might not be able to adequately specify which sales partner actions best serve their interests and rather provide sales partners with biased specifications (Hendry 2002). In the extreme, with increasing centralization, a paradox situation might arise in which manufacturers discourage indirect channels from serving their more general interests but force them to follow biased specifications. Because centralization and indirect channel usage mutually reinforce each other’s negative effects, we predict:

Direct channel usage

In contrast, we expect that centralization likely strengthens performance effects of direct channel usage. The extended knowledge base that manufacturers accumulate from various direct channels that contribute important revenue reduces bounded rationality concerns (i.e., availability bias) to a large extent. Manufacturers will likely more accurately formulate desired sales partner behavior in this context. Thus, when aligned with direct channel usage, manufacturers are likely able to benefit from centralization’s increased decision-making speed (Baum and Wally 2003), enhancing positive returns from direct channel usage.

In addition, centralization is less likely to stimulate moral hazard among sales partners when aligned with direct channel usage. Firsthand experience can provide legitimacy in sales partner management, which can reduce (Heide, Kumar, and Wathne 2014) or even reverse sales partner opportunism (Bosse and Philipps 2016; Heide, Wathne, and Rokkan 2007). For example, in an ethnographic study, Bradach (1997) observes that franchisees are more likely to accept a franchisor’s authority if the franchisor also operates its own outlets. In this case, franchisees respond more favorably to franchisor control, lowering “persuasion costs.” Thus:

Alignment of Multichannel Design and Information Exchange

Indirect channel usage

Aligning indirect channel usage with information exchange reduces the manufacturer’s financial performance. On the positive side, high levels of information exchange with indirect channels may help the manufacturer reduce its information disadvantage compared with sales partners. However, aligned with indirect channel usage, information exchange likely provokes agency costs that exceed such positive outcomes (Tirole 1986). Research on cooperation between competitors shows that high levels of exchanged information between competitors can result in “opportunistic exploitation” (Luo, Rindfleisch, and Tse 2007; Williamson 1985). Sales partners may jointly use the acquired information from manufacturers (e.g., process knowledge, cost structures) to negotiate favorable terms and conditions (Zeng et al. 2015; Zheng et al. 2020). Thus, manufacturers either face high direct costs (e.g., price concessions) or they must invest substantially in safeguarding mechanisms (Ghosh and John 1999), lowering financial performance.

In addition, competition between indirect channels lowers individual sales partners’ incentive to exchange information with the manufacturer in the first place. Sales partners might anticipate “misappropriation of their information” (Baiman and Rajan 2002); that is, the same manufacturer may share sales partner information with competing indirect channels (Butt et al. 2018). Therefore, to maintain ongoing information exchange, manufacturers need to invest continuously in the relationship (e.g., granting access to valuable resources to maintain relationships) (e.g., Heide 1994), which lowers financial performance. Thus:

Direct channel usage

Information exchange with indirect sales partners likely enhances performance effects of direct channel usage. The costs of maintaining information exchange are relatively low and have reduced potential of opportunistic exploitation. Manufacturers that dominantly use direct channels likely have a broader information base than their sales partners (Bradach 1997). Thus, sales partners acting boundedly self-interested are likely to reciprocate by sharing information (e.g., Bosse and Philipps 2016). Individual sales partners may even anticipate competitive disadvantages if they did not obtain the same valuable market information as their competitors. Those benefits likely outweigh the fears of “information misappropriation” and incentivize sales partners to share information. In addition, direct channel usage represents a credible threat for sales partner replacement, and thus, risks that sales partners will opportunistically exploit the shared information against the manufacturer are low.

Notably, although manufacturers largely rely on direct channels, information obtained from sales partners will still enhance their performance (Tsai 2002). According to Bradach (1997), sales partner information complements manufacturer information. Whereas company-internal sources might have a tendency to please, sales partners might be willing to even offer negative information or novel aspects that are viable for manufacturer performance. Relatedly, information exchange can help coordinate sales partners, further enhancing performance. Thus:

Methodology

Research Context and Data Collection

Data on our focal constructs (e.g., multichannel characteristics) are not available from secondary data sources, so we used a primary field study to test our hypotheses. Because we evaluate the management of sales partners, our population of interest comprises B2B firms with at least one indirect sales channel. We conducted interviews with these companies to gain a deeper understanding of multichannel sales management and to guide our research design. Interviewees encouraged us to also collect sales partner data to glean further insights. We followed this advice and collected sales partner data, which we analyzed in a validation study.

We sent a mail questionnaire to 1,454 manufacturers and provided an additional 1,500 manufacturers with an online questionnaire using a business social network. We made several efforts to encourage participation and increase response rates. We assured respondent anonymity and offered manufacturers incentives for participating and for providing sales partner contacts. We made personal telephone calls to manufacturers that had not returned the questionnaire within four weeks. In exchange for participation, each respondent received a summary of the results and a benchmarking report. In addition, we offered respondents a choice of a free sales management textbook, an Amazon.com gift coupon of €30, or a donation of €30 to UNICEF. We received usable responses from 519 manufacturers (a response rate of 18%). We eliminated 20 questionnaires with incomplete answers, most of which related to our focal constructs. For 201 of the 499 remaining respondents, we obtained objective financial performance data.

We also asked our key informants to provide us with contact information for purchasing managers or managing directors from major sales partners. We acquired matched sales partner data for 103 manufacturers (one to nine different sales partners per manufacturer participated).

Table 2 shows the composition of our study. To ensure that our effective sample is representative, we compared it with the relevant B2B industry distribution for Germany, which we obtained from the Nexis Uni database (previously LexisNexis), a widely used database in marketing research (Yang and Goldfarb 2015). A nonsignificant goodness-of-fit test between our effective sample (n = 499) and the overall industry distribution indicated no threats to representativeness (χ2 = 12.85, p = .46; H0: equal distribution in both samples). Another goodness-of-fit test between the matched sample (n = 103) and the overall industry distribution also indicated no threats to representativeness (χ2 = 7.87, p = .85).

Sample Composition.

Measurement

Measurement development

We followed standard psychometric scale development procedures, generating our measurements from a review of extant literature (see the Appendix). We used established scales to measure formalization (e.g., Kabadayi, Eyuboglu, and Thomas 2007), centralization (e.g., Dwyer and Welsh 1985), and information exchange (Heide and John 1992). We used earnings before interest and taxes (EBIT) scaled by total assets to ensure comparability between industries from the AMADEUS database to assess financial performance.

We extended prior measures to capture indirect and direct channel usage (e.g., Jindal et al. 2007; Käuferle and Reinartz 2015; Sa Vinhas and Anderson 2005). In line with prior research and discussions with advising managers, we focused on a set of 11 distinct sales channels for B2B manufacturers to capture the variety dimension (see Table 3). We distinguish direct and indirect channels according to customer contact medium (e.g., personal sales, Internet) (e.g., Jindal et al. 2007). To capture the intensity dimension, key informants assessed the share of revenue obtained for each channel (pij) (e.g., Sa Vinhas and Anderson 2005).

Illustration of the Newly Developed Measures: Direct and Indirect Channel Usage.

Notes: All manufacturers in our sample have at least one indirect channel and, on average, employ two direct and two indirect channels. We illustrate our calculations for Manufacturer A. Our study respondents reported the proportion of sales volume they generate in each channel. With the reported values, we calculated each channel’s (i) proportion of sales volume (pij) relative to the overall channel category (

We rely on an entropy measure (e.g., Groening, Mittal, and Zhang 2016) to convert the obtained responses into a measure of channel usage. However, as we demonstrate in the “Robustness Checks” section, our results are not sensitive to this choice. The entropy measure captures the number of channels after accounting for their relative importance (i.e., relative revenue contribution). An entropy score of 0 refers to a firm that derives all its revenues from one channel. The entropy score increases as the number of channels grows and is attenuated by each channel’s relative revenue (e.g., larger revenue concentration lowers the entropy measure). A firm that uses all channels and obtains equal revenue from them obtains the highest value.

To illustrate our calculations, we introduce five fictitious manufacturers in Table 3. Although the manufacturers are fictitious, the general pattern of their sales channels is realistic. The average manufacturer in our sample employs two indirect and two direct channels, and all manufacturers rely on at least one indirect channel. To calculate separate measures for direct and indirect channels, we rescale the reported relative revenues to the respective channel category (direct: j = 1; indirect: j = 2). We divide the observed measures by the proportion of sales volume generated in each channel category

As a final step, we adjust our measure by the overall importance of direct and indirect channels (Käuferle and Reinartz 2015). This need becomes apparent when comparing Manufacturers B and C: without adjustments, the resulting entropy measures would be identical. Thus, we calculate direct (DCU) and indirect channel usage (ICU) as follows:

where pij refers to the amount of sales volume the manufacturer reports for sales channel i (i ∈ 1 [direct sales force],…, 11 [external online shops]) in channel category j (j ∈ 1 [direct channel] or 2 [indirect channel]).

Table 3 shows that our measures have favorable properties over alternative measures. Merely counting the number of channels would disguise managerial differences between Manufacturers B and C. Manufacturer C employs predominantly direct channels that account for 97% of revenue and uses two additional indirect channels as “test” channels (3% of revenue contribution). By contrast, Manufacturer B generates 30% of its sales volume from the same indirect channels and thus is more dependent on these channels (Sa Vinhas and Johnson 2019). Our measures validly distinguish between the two manufacturers.

Similarly, focusing on the proportion of indirect sales volume alone cannot sufficiently discriminate manufacturers, such as Manufacturers D and E. Although both manufacturers employ only indirect channels (proportion indirect = 100%), Manufacturer E relies on a different number of indirect channels, which likely implies more complexity due to potential channel interactions. Thus, in contrast with measures such as the proportion of indirect sales volume, our measures better capture the unique characteristics of multichannel settings.

Controls

In addition to the focal theoretical variables, we include an extensive set of control variables. In doing so, we preclude potential confounds and account for key dimensions by which multichannel design and governance decisions are affected. Specifically, following agency theory, we control for information asymmetry (i.e., manufacturer’s information disadvantage) (Frazier et al. 2009; Heide 2003). In addition, we include channel management controls. In this way, we account for distribution selectivity, contractual binding, governance expenses, and governance enforcement (Sa Vinhas and Heide 2015). Moreover, because companies’ strategic orientations can guide them in selecting their multichannel design and exchange partners, we account for companies’ customer and cost orientation (Jindal et al. 2007; Käuferle and Reinartz 2015). Finally, we account for industry concentration, which can affect the design of multichannel systems and governance choices (e.g., Kabadayi, Eyuboglu, and Thomas 2007). Table 4 shows the correlations of all measures.

Descriptive Statistics and Correlations.

Notes: Absolute values larger than |.20| are significant at p < .05 (two-tailed tests). The square roots of the AVE are on the diagonal. aObtained from an independent financial database.

Measure Validity

Measurement assessment

We conducted a confirmatory factor analysis that contained all reflectively measured constructs to assess their reliability and validity. We found acceptable model fit (comparative fit index = .93, root mean square error of approximation = .05, standardized root mean square residual = .05). Overall, the analysis had satisfactory results: Composite reliability, average variance extracted (AVE), Cronbach’s alpha, and all indicator reliabilities exceed the recommended threshold values for all constructs (see the Appendix) (e.g., Bagozzi and Baumgartner 1994). Only the cost orientation construct falls slightly below the suggested threshold value of .50 for AVE. However, slight deviations are acceptable, particularly because all other threshold values are met. Moreover, we find no evidence against discriminant validity because the square roots of the AVE from each pair of variables exceed their correlation (Table 4) (Fornell and Larcker 1981).

Key informant bias

We checked whether key informants were sufficiently competent to answer our questions by asking for their job experience (Kumar, Stern, and Anderson 1993). Key informants’ average job experience of 19.8 years (SD = 8.6) indicated that they were able to provide accurate answers. Moreover, most of our constructs pertained to the current situation, were internal to the firm, and were objectively verifiable. Key informants tend to evaluate these constructs accurately (Homburg et al. 2012). Finally, we verified key informants’ responses by comparing subjective and objective measures of sales volume for manufacturers available on the AMADEUS database. The high correlation coefficient (r = .78, p < .01) indicates that key informant bias is not a problem.

Common method bias

Our study’s design largely dispels the risk of potential common method bias because we rely on different data sources to capture the independent and dependent variables. Moreover, analytical and simulation studies suggest that common method bias does not create but only deflates interaction effects (e.g., Siemsen, Roth, and Oliveira 2010).

Model Specification

Our research objectives and our survey methodology imposed several constraints that we accounted for when we specified our model. First, we needed to account for sampling-induced endogeneity from two sources: (1) Owing to less-than-comprehensive public disclosure requirements, we could not obtain financial performance data for many family-, foundation-, or state-owned companies, and (2) we did not receive sales partner contacts from all manufacturers. Second, the design of multichannel sales systems and the choice of governance mechanisms do not follow from a random assignment but a strategic choice (e.g., anticipated future performance), so we had to account for this second type of endogeneity. Third, we checked for multicollinearity, which does not seem to threaten the results of our analyses (largest variance inflation factor is lower than 5 and condition indices are lower than 10).

Sampling-Induced Endogeneity

We first specified the theorized effects of multichannel design and governance mechanisms on manufacturer performance as follows:

where EBIT is at t + 1; DCU (ICU) is direct (indirect) channel usage; FORM is formalization; CENT is centralization; INFO is information exchange; Controls refers to a vector of control variables (EBIT at t, distribution selectivity, information asymmetry, contractual binding, enforcement, governance expenses, customer orientation, cost orientation, and industry concentration); and ε is the residual error term for company i.

However, we needed to account for two potential selection biases. First, we acquired only objective financial performance data from a subset of our surveyed manufacturers. Therefore, we ran a Heckman selection model with the availability of secondary data as the dependent variable (1 = secondary data available) and included the legal form (1 = public company) of the company for identification (Vomberg, Homburg, and Gwinner 2020). In addition, we included all control (except EBIT at t) and focal variables (including their interactive effects) from our main model (Equation 2). Second, for another subset of manufacturers, we obtained sales partner data. Here, we ran a selection model with the availability of sales partner data as the dependent variable (1 = sales partner data available) and included the overall number of sales partners for identification. Thus, we estimated (ignoring subscripts):

where Avail_FinData (Avail_Partner) is the availability of financial performance (sales partner) data; Focal is a vector of the focal variables from Equation 2 and their interactive effects; Controls is a vector of control variables (Equation 2); LEGAL is the legal form of the company; #SALES is the number of sales partners; and ζ and μ are the residual error terms.

Endogeneity of Multichannel Design and Governance Mechanisms

Indirect and direct channel usage as well as governance choices might be endogenous. Prior conflict with sales partners (Sa Vinhas and Anderson 2005), anticipated levels of competition between channels (Sa Vinhas and Heide 2015), or anticipated performance outcomes (Grewal et al. 2013) may determine firms’ emphases on them, introducing correlation with the error term in our model. We rely on the two-step control function approach (Petrin and Train 2010) to address these endogeneity concerns: we include the residuals from the first stage (Equation 5) in the second stage (Equation 6) to correct for potential endogeneity. To obtain the residuals, we regress the potentially endogenous variables—direct channel usage, indirect channel usage, formalization, centralization, and information exchange—on the variables from our main model (Equation 2). For identification, we additionally regress them on a set of instrumental variables. We specify the first-stage regression (ignoring subscripts) as follows:

where END (END’) is a vector of the potentially endogenous variables (excluding the focal one); Controls is a vector of the observed control variables (Equation 2); Instruments is a vector of instrumental variables (specified next); IMR is a vector of inverse Mill’s ratios (Equations 3 and 4); and θ is a vector of the error terms.

Note that the control function approach does not require estimating additional first-stage models for interaction terms (Papies, Ebbes, and Van Heerde 2017). The difficulty lies in identifying appropriate instruments that satisfy the criteria for both relevance (instruments need to correlate with the potentially endogenous variables) and exclusion (instruments must not correlate with the dependent variable).

Drawing on the theory of institutional isomorphism and literature on dominant logic, we argue that industry characteristics and market conditions are key determinants of a firm’s channel management choices (relevance criterion) (Grewal and Dharwadkar 2002). The theory of institutional isomorphism proposes that companies often mimic other companies in their industry to gain legitimacy (DiMaggio and Powell 1983). The literature on dominant logic suggests that in the course of time, industries develop certain mindsets or “world views” that represent certain ways of doing business (Prahalad and Bettis 1986). Thus, we argue that the industry-aggregate measures of channel usage and governance mechanisms influence a company’s engagement in them (Antia, Mani, and Wathne 2017). Similarly, industry aggregated measures of customer orientation and cost orientation are relevant instruments (our results are not sensitive to including them). Firms competing in customer-oriented markets might increase channel usage to cater to customer preferences, and cost-oriented markets may require an efficiency focus, expanding indirect channel usage (Jindal et al. 2007; Srinivasan 2006).

The identifying assumption is that peer firms are unlikely to strategically respond to individual levels of conflict or competition and performance expectations (exclusion criterion). This criterion is met. We used a large number of firms to calculate the focal firm’s instruments. It seems unlikely that peer firms will take collective actions against a single competitor (i.e., stimulate conflict) and then also form other alliances similar in spirit to act against further competitors (Germann, Ebbes, and Grewal 2015). Moreover, from the outside, peers cannot observe competition or performance expectations, which might even represent tacit knowledge inside the firm (Kogut and Zander 1992). Thus, they cannot act on them.

Our unique data set allows us to calculate these industry aggregates. Our matched manufacturer–sales partner data contain 103 cases; however, we collected questionnaires from 499 manufacturers. Significant Sanderson-Windmeijer multivariate F-tests empirically confirm the strength of our instrumental variables (p < .01). In line with common practice (e.g., Lawrence et al. 2019), small and nonsignificant correlations (r < .10) between our instrumental variables with firm performance deliver support for the exclusion criterion.

To correct for the two types of endogeneity in Equation 2, we include the two inverse Mills ratios from Equations 3 and 4 and the effects of the five residual error terms from Equation 5. Thus, we estimate the following model:

where IMR is a vector of two inverse Mills ratios (availability of financial performance data and availability of sales partner data) and θ refers to a vector of endogeneity corrections (Equation 5).

Results

Hypothesis Testing

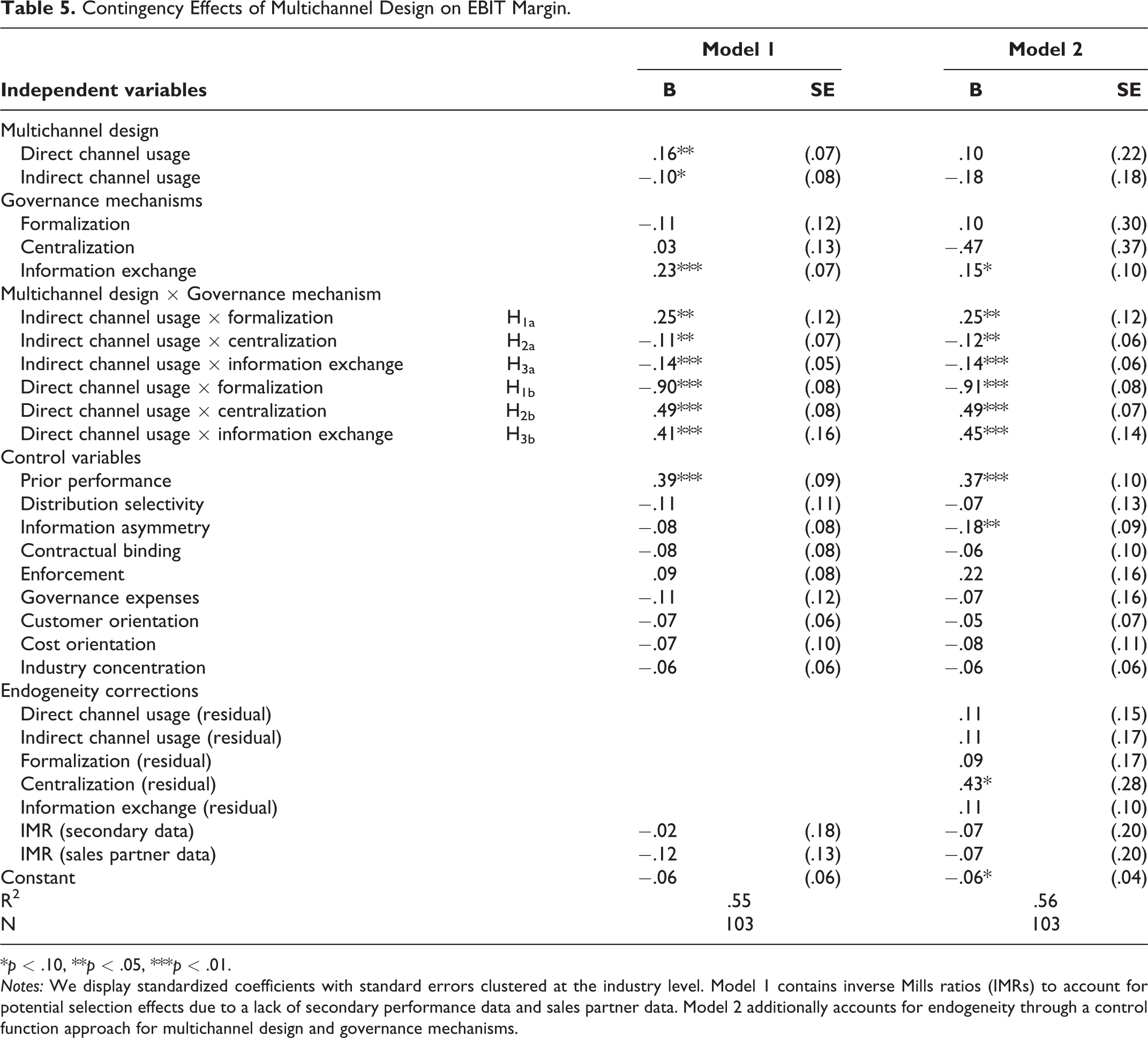

We relied on ordinary least squares regression with standard errors clustered at the industry level to estimate our models. We standardized our variables to account for differences in scaling. Table 5 displays the regression results. Model 1 shows how governance mechanisms moderate the effects of multichannel structure without endogeneity corrections. Model 2 additionally accounts for endogeneity by adding residual terms for multichannel design and governance mechanisms. We refer to Model 2 to test our hypotheses. We find that formalization enhances the performance outcomes of indirect channel usage (βICU × form = .25, p < .05) while diminishing the outcomes of direct channel usage (βDCU × form = −.91, p < .01). Thus, we find support for H1a and H1b, respectively. In addition, we observe that centralization diminishes the performance outcomes of indirect channel usage (βICU × cent = −.12, p < .05) but enhances the outcomes of direct channel usage (βDCU × cent = .49, p < .01), in support of H2a and H2b. Finally, our results indicate that information exchange diminishes the performance outcomes of indirect channel usage (βICU × info = −.14, p < .01) but enhances the outcomes of direct channel usage (βDCU × info = .45, p < .01), in support of H3a and H3b.

Contingency Effects of Multichannel Design on EBIT Margin.

*p < .10, **p < .05, ***p < .01.

Notes: We display standardized coefficients with standard errors clustered at the industry level. Model 1 contains inverse Mills ratios (IMRs) to account for potential selection effects due to a lack of secondary performance data and sales partner data. Model 2 additionally accounts for endogeneity through a control function approach for multichannel design and governance mechanisms.

Floodlight Analysis

To analyze the moderating effects in greater detail, we conducted floodlight analyses at grid values to examine the simple effects of direct and indirect channel usage contingent on our moderators (Spiller et al. 2013). Web Appendix W1 displays the results. We find that moderate to high levels of formalization can offset the negative outcomes of indirect channel usage. However, high levels of centralization and information exchange lead to negative outcomes.

Moreover, we observe important disordinal interaction effects for direct channel usage. Moderate to high levels of formalization provoke negative performance effects of direct channel usage. Notably, when aligned with low levels of centralization or information exchange, direct channel usage entails negative performance outcomes. However, the effect on these governance mechanisms reverses when such levels are moderate to high. This finding is important because prior interfirm research reports predominantly negative effects of centralization (Frazier 1999). Overall, we find that alignments between indirect channel usage and formalization enhance performance, whereas alignments between direct channel usage and centralization and information exchange are beneficial.

Validation Study: Sales Partner Behaviors

Before developing our focal hypotheses on the alignment effects between multichannel design and governance mechanisms, we established the baseline effects of indirect and direct channel usage on sales partner behavior (i.e., information asymmetry and moral hazard). We predicted that direct channel usage would lower manufacturers’ information disadvantage compared with sales partners and reduce sales partner moral hazard. In addition, we predicted that indirect channel usage would increase moral hazard but would not affect information asymmetry. We additionally measured sales partners’ information advantage over the manufacturer and sales partner cooperation with the manufacturer (a manifestation of moral hazard) in the sales partner survey (see the Appendix). Table 6 reports the validation study results (see Web Appendix W2 for further details).

Validation Study: Effects of Multichannel Design on Sales Partner Behavior.

*p < .10, **p < .05, *** p < .01.

Notes: We performed hierarchical linear modeling and display standardized coffiecients with standard errors clustered at the industry level.

Overall, we find support for our predictions. We observe a negative relationship between direct channel usage and the sales partner’s information advantage over the manufacturer (Model 1: βDCU = −.07, p < .05) but no relationship for indirect channel usage (Model 1: βICU = −.10, n.s.). Interestingly, we do not observe linear effects but inverted U-shaped effects between sales partner cooperation with the manufacturer for direct (Model 2: βDCU2 = −.04, p < .01) and indirect (Model 2: βICU2 = −.19, p < .01) channel usage. (In Web Appendix W2, we formally establish these inverted U-shape effects in line with prior literature, e.g., Haans, Pieters, and He 2016; Vomberg, Homburg, and Gwinner 2020.) Low to moderate levels of direct channel usage increase cooperation (reduce moral hazard) potentially because of a manufacturer’s increased ability to detect moral hazard. However, high levels of direct channel usage likely provoke competition, reducing cooperation. In contrast, for indirect channel usage, we observe that the turning point lies close to the lower end of our observed data range. Thus, in line with our prediction that indirect channel usage increases moral hazard, we observe predominantly negative effects of indirect channel usage on sales partner cooperation with the manufacturer.

Robustness Checks

Endogeneity Assessment: Gaussian Copulas

As an additional endogeneity check, we rely on Gaussian copulas (e.g., Ebbes, Papies, and Van Heerde 2016), which represent an instrument-free method of accounting for endogeneity (see Web Appendix W3). The Gaussian copula approach replicates all our findings. Because the control function and the Gaussian copula approach rely on different model-identifying assumptions but provide consistent results, they strongly support the validity of our findings.

Multichannel Characteristics: Alternative Specifications

Herfindahl–Hirschman index

We also tested alternative specifications (for details, see Web Appendix W4). Instead of an entropy measure (Table 3), we could rely on the Herfindahl–Hirschman index (HHI) as an alternative method to operationalize direct and indirect channel usage. Marketing literature largely relies on the HHI to capture diversity (e.g., Fang, Palmatier, and Grewal 2011). We estimated our model (Equation 4) with the alternative HHI specification and replicated all our findings.

Number of channels weighted by revenues

We tested a measure that considered relative revenues not by channel but by channel category (direct vs. indirect; e.g., for Manufacturer A in Table 3: 2 direct channels × 70% revenue from direct channels = .14) (Sa Vinhas and Anderson 2005). Overall, all results but one interactive effect remained stable (βICU × form = .19, n.s.).

Number of channels

We tested a measure that counted the number of direct and indirect channels but did not consider the intensity dimension. Again, all results but one interactive effect remained stable (βDCU × info = −.01, n.s.). Overall, our operationalization choice did not affect our results. In addition, we find best model fit in terms of R-square values for the entropy and HHI specifications, further supporting a joint focus on the variety and intensity dimensions.

Discussion

We introduce direct and indirect channel usage as focal design dimensions of multichannel sales systems. In line with multiple agency theory, we find that direct channel usage can lower manufacturers’ information disadvantage compared with sales partners. Low to moderate levels of direct channel usage also reduce moral hazard concerns, whereas high levels increase moral hazard. Indirect channel usage largely provokes moral hazard concerns. How those sales partner outcomes translate into manufacturer outcomes critically depends on governance mechanisms, which confirms predictions from governance value analysis. Formalization enhances the performance outcomes of indirect channel usage but diminishes outcomes of direct channel usage. Conversely, centralization and information exchange with sales partners enhance the performance outcomes of direct channel usage but diminish outcomes of indirect channel usage. These results have important implications for research and practice.

Research Implications

First, our investigation extends prior research that compares differences between multichannel and nonmultichannel settings (Table 1) by exploring variation within multichannel settings (Antia, Mani, and Wathne 2017; Srinivasan 2006). Prior research demonstrates that the mere presence of direct channels within a sales system can increase agency conflicts (e.g., Heide 2003). We build on this information and show that the degree of channel usage can differently affect agency conflicts. Future research could further explore intradesign differences from an internal perspective. We focused on agency conflicts with external sales partners; however, agency conflicts might also arise within direct channels: the direct sales force may perceive substitution threats from direct online channels (Lawrence et al. 2019), or employees may question management’s ability to cater to the specific interests of their own sales channels while supporting indirect sales channels (Sa Vinhas and Anderson 2005), provoking agency conflicts.

Second, our results emphasize the importance of aligning governance mechanisms with multichannel design, an issue that has received limited attention (cf. Ghosh and John 2005; Heide, Kumar, and Wathne 2014). Extending prior research that demonstrates that the effects of governance mechanisms can vary between multichannel and nonmultichannel settings (Table 1), we show that the same governance mechanism can have divergent performance effects within multichannel settings. For example, centralization enhances direct channel usage by leveraging firsthand knowledge. However, centralization reduces the performance effect of indirect channels usage. Of note, these interactive effects differ within categories of governance mechanisms: Both formalization and centralization represent manifestations of formal governance; however, they result in opposing effects. In addition, although prior research indicates that informal governance (i.e., solidarity norms) can be less effective for multichannel settings (Heide, Kumar, and Wathne 2014), our findings imply that informal governance (i.e., information exchange) can still be effective depending on multichannel design characteristics.

Overall, these observations underscore the need for further research on the effectiveness of governance mechanisms in multichannel settings. For example, research could explore whether manufacturers’ engagement in direct channels similarly strengthens the performance effects of other intrusive governance mechanisms, such as behavioral monitoring (Heide, Wathne, and Rokkan 2007). Moreover, we separately investigate the effects of the fundamentally different approaches of formal and informal governance. Extant research demonstrates counterbalancing (Jap and Ganesan 2000) and reinforcing effects (Poppo and Zenger 2002; Vomberg, Homburg, and Gwinner 2020). Therefore, we call for further research on their joint effects in multichannel settings.

Third, we address calls to link governance mechanisms to financial performance (Heide 2003) and thus extend initial research in this area (e.g., Heide, Kumar, and Wathne 2014). Importantly, we contribute to the theoretical discussion by integrating governance value analysis and multiple agency theory. Such an integration is possible because the underlying assumptions of both theories are compatible or at least are not inconsistent. Both share the behavioral assumptions of bounded rationality and (boundedly) self-interest-seeking actors and focus on minimizing direct and opportunity costs (e.g., Eisenhardt 1989; Rindfleisch and Heide 1997).

Integration expands the theories’ individual partial views of the world (e.g., Bergen, Dutta, and Walker 1992). Governance value analysis complements agency theory by emphasizing that exchange partners strive to achieve joint value because doing so also maximizes their own profits (Ghosh and John 1999). Thus, resolving agency conflicts does not only induce order but can also create value. A focus on joint value also puts the focus on both sides of the principal–agent dyad and thereby complements agency theory’s dominant principal focus. Finally, multiple agency theory complements governance value analysis by helping us understand how interactions outside the dyadic relationship affect performance.

We suggest taking this integration as a starting point and call for further research on financial performance effects of governance mechanisms. Prior research provides rich evidence for the potential of governance mechanisms to create order (e.g., suppressing opportunism). However, governance mechanisms can yield complex effects on preeconomic outcomes (e.g., formalization reduces opportunism but also customer outcomes; Sa Vinhas and Heide 2011). Thus, studies on financial performance effects are important, as they may complement prior research by demonstrating net effects, which are highly relevant to managers.

Relatedly, we call for research that integrates recent agency extensions, such as behavioral agency theory (Hoenen and Kostova 2015), which may offer additional theoretical insights (e.g., inclusion of trust). Behavioral agency, for example, could be relevant for investigating whether (and when) cooperation between sales partners not only hurts (as multiple agency theory predicts) but also benefits the manufacturer (El Akremi, Mignonac, and Perrigot 2011).

Managerial Implications

Our study’s focal managerial implication is that managers need to align multichannel design with governance choices, as multichannel designs can provoke sales partner moral hazard. For example, high levels of direct channel usage can induce sales partners to cooperate against the manufacturer. However, the results of our study imply that governance choices significantly affect whether such sales partner behavior also affects manufacturer performance.

Manufacturers benefit from aligning direct channel usage with centralized decision making. Similarly, also maintaining information exchange with indirect channels strengthens the performance effects of such a multichannel design. However, governing indirect channel usage requires a different governance approach: Manufacturers should adopt formalized rules and procedures in this context. This finding calls to mind the experience of the manager we mentioned at the outset of the study. To end the feud with sales partners that began producing the manufacturer’s product on their own, the manufacturer and sales partners developed agreed-on rules and procedures. One formalized rule stipulated that sales partners could distribute the product only in countries where the manufacturer did not have a presence. As multichannel sales systems tend to develop over time, this also implies that managers need to regularly reevaluate the appropriateness of their governance approaches. Otherwise, they may fall prey to inertia traps, in which managers stick with established but inefficient governance mechanisms (Grewal and Dharwadkar 2002).

To illustrate our point, we demonstrate the performance effects of centralization for different combinations of multichannel designs. We focus on centralization because anecdotal evidence suggests that manufacturers tend to prefer centralized decision making. We reestimated our main model and included the three-way interaction between centralization, direct channel usage, and indirect channel usage (p > .10). We calculated the marginal effects of centralization at low (μ − 2σ) and high (μ − 2σ) levels of both indirect and direct channel usage. At low levels of direct channel usage, centralization hampers manufacturer performance for low (

Supplemental Material

Supplemental Material, Appendix_PDF - Design and Governance of Multichannel Sales Systems: Financial Performance Consequences in Business-to-Business Markets

Supplemental Material, Appendix_PDF for Design and Governance of Multichannel Sales Systems: Financial Performance Consequences in Business-to-Business Markets by Christian Homburg, Arnd Vomberg and Stephan Muehlhaeuser in Journal of Marketing Research

Footnotes

Appendix

Study Measures.

|

|

|

|

|---|---|---|

| Financial performance | ||

| EBIT scaled by total assets [%] | ||

| Direct channel usage and indirect channel usage (M)b

|

||

| Please specify the share of turnover (pij) your firm/business unit realizes in the following channels: | NAc | |

|

Direct sales force (p1,1) ___ % Own outlets (p2,1) ___ % Own telephone sales/call center (p3,1) ___ % Own direct marketing (mail, catalog) (p4,1) ___ % Own online shops, portals, marketplaces (p5,1) ___ % Retailers/specialist dealers (p1,2) ___ % Wholesalers (p2,2) ___ % External sales representatives (p3,2) ___ % External telephone sales/call center (p4,2) ___ % External direct marketing (mail, catalog) (p5,2) ___ % External online-shops, portals, marketplaces (p6,2) ___ % |

||

| Formalization (M) (based on Kabadayi, Eyuboglu, and Thomas 2007) [CR = .91; AVE = .72; CA = .91]d | ||

|

We define clear rules and procedures for our sales partners. Our contacts with our sales partners are on a formal, preplanned basis. There are standard procedures and rules to be followed by every sales partner. Our sales partners have to conform to formal guidelines and written rules. |

.79 |

.63 |

| Centralization (M) (adapted from Dwyer and Welsh 1985; Kabadayi, Eyuboglu, and Thomas 2007) [CR = .76; AVE = .52; CA = .76] | ||

|

There can be little action taken in our sales system until we make decisions. Our sales partners cannot go ahead with actions without checking with us. Any decision a channel member makes regarding our product has to have our approval. |

.68 |

.46 |

| Information exchange (M) (based on Heide and John 1992) [CR = .90; AVE = .69; CA = .89] | ||

|

We exchange information about relevant occurrences with our sales partners. We informally exchange information with our sales partners. We exchange more information with our sales partners than originally intended. We expect our sales partners to forward relevant information to us. |

.73 |

.54 |

| Distribution selectivity (M) (based on Fein and Anderson 1997) [CR = .81; AVE = .59; CA = .81] | ||

|

We try to keep the number of sales partners per trade area low. We assign exclusive trade areas to sales partners. We do not assign additional sales partners to the existing trade areas of other partners. |

.67 |

.45 |

| Information asymmetry (M) (inspired by Heide 2003) [CR = .89; AVE = .73; CA = .88] | ||

|

We have more information about our relevant markets than our sales partners. We know more about our end customers than our sales partners. In general, we have more knowledge about end customers and markets than our sales partners. |

.70 |

.49 |

| Contractual binding (M) (own development) [CR = .89; AVE = .68; CA = .89] | ||

|

We have contracts with our sales partners that closely bind us. We have contracts with our sales partners that bind us for a long time. We have contracts with our sales partners that preclude the quick exchange of sales partners. We have contracts with our sales partners that impede the termination of our relationships. |

.83 |

.69 |

| Enforcement (M) (own development) [CR = .84; AVE = .58; CA = .84] | ||

|

We exert pressure on our sales partners so that they comply with our decisions. We exert pressure on our sales partners so that they do not buy from competing manufacturers. We exert pressure on our sales partners so that they invest in marketing activities. We exert pressure on our sales partners so that they adopt our new products. |

.72 |

.52 |

| Governance expenses (M) (own development) [CR = .86; AVE = .68; CA = .86] | ||

|

The governance of our sales partners involves high personnel expenses. The governance of our sales partners involves high IT expenses. The governance of our sales partners is very costly. |

.77 |

.60 |

| Customer orientation (M), (SP) (adapted from Narver and Slater 1990) [CR = .84b (.80)e; AVE = .58 (.50); CA = .84 (.79) | ||

|

A core part of our company strategy is the creation of customer value. We steadily monitor our efforts for satisfying customer needs. Our competitive advantage is based on the understanding of customer needs. Our main target is satisfying our customers. |

.73b (.66)e

|

.53 (.44) |

| Cost orientation (M), (SP) (based on Homburg, Workman, and Krohmer 1999) [CR = .82b (.86)e; AVE = .48 (.55); CA = .82 (.85)] | ||

|

Pursuing operating efficiencies is one of our most important business targets. We put special emphasis on keeping operative costs on a low. We continuously pursue improving our production processes in order to reduce costs. Pursuing economies of scale and economies of scope are central elements of our strategy. We strictly control our business processes. |

.75b (.68)e

|

.56 (.46) |

| Industry concentration | ||

|

HHI: Sum of squared market shares (SIC code) |

||

| Information advantage (SP)e (inspired by Heide 2003) [CR = .82; AVE = .60; CA = .82] | ||

|

We have more information about our relevant markets than the manufacturer. We know more about our end customers than the manufacturer. In general, we have more knowledge about end customers and markets than the manufacturer. |

.76 |

.58 |

| Sales partner cooperation (SP) (own development) [CR = .81; AVE = .58; CA = .80] | ||

|

The manufacturer and we cooperate strongly regarding logistics to keep costs low. The manufacturer and we intend to set end customer prices so that they are optimal for both of us. The manufacturer and we coordinate regarding promotional measures. |

.75 |

.57 |

| Switching costs (SP) (based on Kim and Hsieh 2003) [CR = .92; AVE = .73; CA = .91] | ||

|

Replacing the manufacturer would cause high costs. Replacing the manufacturer would cost much time. Replacing the manufacturer would lead to technical difficulties. Replacing the manufacturer would lead to uncertainty. |

.88 |

.78 |

| Frequency of manufacturer change (SP) (own development) | NA c | |

|

How often do you change your suppliers? (Likert-type scale: 1 = “very rarely,” and 7 = “very often”) |

||

| Importance of manufacturer (SP) (own development) [CR = .85; AVE = .59; CA = .86] | ||

|

The products of the manufacturer cause high financial expenditures for us. The products of the manufacturer account for a high share of our budget. The products of the manufacturer contribute to the accomplishment of our targets. The products of the manufacturer are of high importance for our business activity. |

.81 |

.65 |

| Sales partner performancef (adapted from Kabadayi, Eyuboglu, and Thomas 2007) [CR = .93; AVE = .78; CA = .93] | ||

| Within our channel shared with the supplier, we achieve our…(Likert-type scale: 1 = “to a very low extent,” and 7 = “to a very high extent”) | ||

|

…performance targets |

.86 | .74 |

|

…sales volume targets |

.94 | .89 |

|

…growth targets |

.90 | .81 |

|

…profit targets |

.81 | .66 |

Items based on seven-point Likert scales (1 = “do not agree at all,” and 7 = “totally agree,” unless indicated otherwise).

a Standardized item loadings (ILs) represent the square root of indicator reliabilities (IRs).

b Manufacturer data (M)

c Not applicable, as the construct is measured with a single item or is part of an index

d Cronbach’s alpha (CA), average variance extracted (AVE), and composite reliability (CR)

e Sales partner data (SP); part of validation study (Table 6 and Web Appendix W2).

f Sales partner data (SP); part of Web Appendix W2.

Acknowledgments

The authors owe special thanks to Josef Vollmayr and Dirk Totzek for their extensive feedback and support and also want to thank Sascha Alavi, Martin Artz, Donald Lehmann, Johannes Habel, Alexander Hahn, Sebastian Hohenberg, Martin Klarmann, Jana Prigge, and Marcus Theel for their helpful comments on earlier versions of this article. The article further benefited from presentations at the 2018 AMA Winter Academic Conference (New Orleans, Louisiana) and the 2018 Theory + Practice in Marketing Conference (Los Angeles, California). Parts of this article were written while Arnd Vomberg was Visiting Scholar at Columbia Business School, Columbia University.

Associate Editor

Detelina Marinova

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

References

Supplementary Material

Please find the following supplemental material available below.