Abstract

The authors study the consequences of rebranding multiple category-specific private-label (PL) brands by “opening the umbrella” and unifying them under a common brand name. Retailers expect positive consequences that may manifest themselves in two ways: (1) an increased intrinsic brand strength and (2) an improved marketing-mix effectiveness. The authors analyze three substantially different retailers that rebranded one of their PL tiers. Consistent with the national-brand literature on umbrella rebranding, all three retailers realized an increase in the rebranded PL tier’s intrinsic brand strength, along with a reduced price elasticity. However, and in contrast to the national-brand literature, the effectiveness of both price-promoting and assortment size dropped for all three retailers after they unified their category-specific PLs under a common umbrella name.

Private labels (PLs) already account for over 22% of the grocery sales in the United States (Stern 2019), and in several European countries (e.g., Spain, the United Kingdom), market shares are approaching the 50% mark. With PLs no longer having to justify their quality, some are making the transition to consumer packaged goods brands in their own right (Seenivasan, Sudhir, and Talukdar 2016). Many retailers, however, still offer PLs with brand names that are restricted to a narrow set of closely related product categories that individually may lack the muscle to become strong brands of their own. To overcome this impediment, retailers are ever more consolidating their category-specific PL brands by “opening the umbrella,” and unifying them under a common brand name. U.S.-based Save-A-Lot, for example, has announced that it will rebrand its standard PLs under a single brand name to replace its multiple individual brand names (Store Brands Decisions 2016). European examples include the Belgian market leader Colruyt, which replaced its more than 50 category-specific standard PL brands, such as “Cribbits,” “Davinia,” and “Galaxi,” with one umbrella brand name (“Boni Selection”). Similarly, the retail chain SPAR unified its 50+ economy PL brands in the Netherlands (among which “Casa Italiana,” “Landhof,” and “Koningssuper”) under the umbrella brand name “OK€.”

Are such rebranding strategies successful? Industry experts believe they are (Pierce 2011; Planet Retail 2014), and also retailers are optimistic about their PL rebranding efforts (Store Brands Decisions 2012a). SuperValu, for example, expected its PL sales to grow by about $70 million per year because of the rebranding (York 2011). These hopes can be attributed to two factors: practitioners feel that “it is easier to build equity in a single brand” (Kolm 2016), and that umbrella branding will “help create efficiencies in…marketing” (Store Brands Decisions 2012b). However, do changes in intrinsic brand strength and marketing-mix effectiveness actually materialize? And are they necessarily positive? Indeed, the rebranding could also backfire if consumers had developed favorable associations with the abandoned category-specific brand names, making them reluctant to embrace the new umbrella positioning. Relatedly, it is unclear whether the presence of the same PL name across all categories throughout the store will affect the sensitivity to additional PL stockkeeping units (SKUs) under that name or to promotional activities for the umbrella-branded PL.

Even though numerous studies have considered conditions under which brand extensions may be more or less appropriate (see, e.g., Völckner and Sattler 2006), few studies have empirically analyzed the reputational effects of umbrella branding (Bronnenberg, Dubé, and Moorthy 2019, p. 338). Moreover, the few studies that did so focused on national brands (NBs; e.g., Aaker and Joachimsthaler 2000; Erdem and Sun 2002). While these studies indeed found that umbrella branding across a few closely related categories increases both the NB’s intrinsic strength and the effectiveness of several marketing-mix instruments, it is not clear that this will also be the case when umbrella branding a retailer’s PL offering. Unlike NB manufacturers, retailers moving to umbrella branding do not have a flagship category with a well-established parent brand to capitalize on. They need to do so for a much larger and broader set of categories that involve not only complementary but also substitute and unrelated categories (Sayman and Raju 2004). Moreover, NBs typically have a greater stake in individual categories. They can invest considerably more resources in developing category-specific associations for their brands than retailers can for each of their many categories (Lamey et al. 2012).

The higher prevalence of umbrella branding in the PL domain (Richards, Yonezawa, and Winter 2015) and the aforementioned intricacies in evaluating its impact (Sayman and Raju 2004) stand in sharp contrast with the scant literature on the issue. We intend to fill this void and thereby address repeated calls for more research on the applicability of NB-based branding principles to the PL domain in general (Grewal, Levy, and Lehmann 2004), and umbrella-branded PLs more specifically (Dekimpe et al. 2011, p. S22; Keller, Dekimpe, and Geyskens 2016, p. 16; Lourenço and Gijsbrechts 2013, p. 381). We aim to address the following research questions:

We empirically study these questions in the context of the Dutch retail banners SPAR and Attent, which rebranded 50+ category-specific economy PL brands to a unified umbrella brand. 1 To better isolate the rebranding effects, we identified seven retail banners that carried the same category-specific PL brands as SPAR and Attent (because they belonged to the same buying group) but that did not change to umbrella branding. For each retail banner, we obtained weekly sales data for a large number of product categories both before and after the rebranding. This data set will enable us to perform before-and-after-with-control-group analyses. Moreover, to rule out that our findings are idiosyncratic to the specific retailers under investigation, we subsequently extend our analysis to a retailer from another country (Colruyt in Belgium), which differs substantially in terms of size, format, positioning, and PL success before the rebranding, and which rebranded its standard rather than its economy PL tier.

Our results provide retailers that still offer category-specific PL brands with insight into the various implications of a shift to umbrella branding. Although PL umbrella branding has become a frequently observed practice in the current retailscape, looking at the market leader (if reported by Euromonitor) in the largest five countries in each of six continents, close to 30% of the banners still use category-specific branding. Importantly, our results speak to both the retailers’ top-level management and the category managers who have to implement the strategy. Specifically, our findings allow category managers to make better-informed decisions, given the potentially changed effectiveness of the various marketing-mix instruments. Moreover, we provide a nuanced way for top-level management to evaluate the overall effectiveness of this strategic initiative.

Theoretical Background

Umbrella or family branding is often motivated on the assumption that the common brand name leads to a “connection in consumers’ minds,” which generalizes consumers’ preferences to the different product categories using the name (Fry 1967, p. 237). The underlying idea for such a halo or spillover effect is that one can not only take advantage of increased brand recognition and recall because of the added exposure potential but also leverage the reputation of the brand across categories (Sebri and Zaccour 2017).

Proponents argue that the use of an umbrella brand name facilitates consumers’ mental categorization and evaluation of these products, as only one recurring brand name is used (Aaker 2012). Categorization theory suggests that consumers organize objects into different cognitive clusters to increase processing efficiency (Cohen and Basu 1987). When consumers can categorize a new object as a member of an earlier defined cluster, they can retrieve their evaluations associated with that cluster and apply them to the new object, resulting in a better understanding and reduced uncertainty (Liu et al. 2017). In a retail setting, consumers frequently rely on external cues, such as brand names or logos (Keller, Dekimpe, and Geyskens 2016), to categorize products.

Using a common brand name (as opposed to multiple different brand names) can also be a way to credibly signal positive quality correlations (Miklós-Thal 2012; Wernerfelt 1988). The ensuing reduction in uncertainty may affect product utility positively and, ultimately, increase the brand’s intrinsic strength (Erdem 1998). Both Erdem (1998) and Erdem and Winer (1998) document that consumers’ preferences for a brand name can indeed be correlated across categories (see also Singh, Hansen, and Gupta [2005]). However, other studies point out that cross-category signaling and learning effects for umbrella-branded products are by no means automatic (Erdem and Chang 2012), nor always positive. When the same name is used across too many or too different categories, the approach may backfire, and result in a reduced identity and intrinsic brand strength (Völckner and Sattler 2006).

In spite of the high incidence of umbrella branding, and even though many game-theoretic studies have studied the potential underlying economics (e.g., Cabral 2009; Miklós-Thal 2012; Wernerfelt 1988), Bronnenberg, Dubé, and Moorthy (2019) concluded that the empirical evidence of spillovers in consumer quality beliefs remains limited and inconclusive. Moreover, most of that limited empirical evidence pertains to brand extensions for NBs. Even though PL branding can, to some degree, be considered an extreme case of a brand extension (Sayman and Raju 2004), there are several key differences. First, umbrella-branded NBs typically evolve gradually from a flagship category (often referred to as the parent category). At the same time, the extensions (where the same name is subsequently applied) usually involve a limited number of closely related complementary categories. Umbrella-branded PLs, in contrast, appear throughout the store and include a much larger number of complementary, substitute, and unrelated categories. Because of that, the danger of brand dilution may, at first sight, be more imminent, as consumers may doubt that the retailer can provide consistent quality across so many different categories (Ailawadi and Keller 2004).

Furthermore, the disappearance of all category-specific brands (within a short period) with a familiar and possibly unique positioning may create confusion among consumers. Category-specific brands typically use a positioning that is congruent with the category (Inman, Shankar, and Ferraro 2004) and/or that adheres to the prevalent trade dress (Van Horen and Pieters 2012), as they do not need to compromise their positioning relative to brands in other product categories (Aaker and Joachimsthaler 2000; Rao, Agarwal, and Dahlhoff 2004). As umbrella PL brands must adapt to a common design grid across categories (De Jong 2019), positive category-specific associations and trade dress advantages can get lost with the rebranding. This could lower consumers’ appreciation of a product, and result in a reduced intrinsic brand strength.

Morrin (1999) and Sayman and Raju (2004), in contrast, argue that because it is difficult to link the PL’s umbrella name to a specific category, consumers may become primed through more abstract (or higher-order) associations (Dacin and Smith 1994), such as value for money or acceptable quality. This would make the large number of rebranded categories a benefit rather than a liability. Using scanner data for up to 13 product categories, Sayman and Raju (2004) found in a cross-sectional (across-retailer) design that a higher number of PLs in other categories indeed corresponds to a higher PL share in a retailer’s target category. Still, this number (while larger than the five categories used in Erdem and Chang [2012] or the three categories studied in Richards, Yonezawa, and Winter [2015]) remains far below the typical number of categories in a retailer’s PL portfolio.

More importantly, none of these prior studies has considered the implications for the PL’s marketing-mix effectiveness. As NBs become stronger, their price elasticity has been found (see, e.g., Datta, Ailawadi, and Van Heerde 2017; Sivakumar and Raj 1997) to become smaller (less negative), while they receive a stronger response to promotional discounts (e.g., Datta, Ailawadi, and Van Heerde 2017). The latter finding has been attributed to the larger pool of customers that stronger brands can attract through their price discounts (Sethuraman 1996, 2009). However, given that PL brands (and especially the economy tier) are already sold at the lowest prices in the market, it is unclear to what extent this will also be the case when the intrinsic strength of the PL brand increases with the rebranding. Similarly, given that the same name is used throughout the store, an unchanged promotional frequency in a given category may still be perceived as higher and thereby result in a lower promotional elasticity (Foekens, Leeflang, and Wittink 1998), even when the PL has become stronger after the rebranding. In terms of assortment size, even though product-line length has been found to be one of the strongest drivers of NB success (Ataman, Van Heerde, and Mela 2010), shoppers may become overwhelmed by the many PL SKUs that now carry the same name, and perceive less variety in the store (Briesch, Chintagunta, and Fox 2009; Rooderkerk, Van Heerde, and Bijmolt 2013), resulting in a much smaller, or even negative, assortment elasticity after the PL rebranding.

In summary, it is not clear to what extent the limited empirical evidence on the positive intrinsic brand strength and marketing-mix effects observed with NBs will automatically extend to a PL setting when retailers decide to change their established category-specific PL names to one common umbrella brand name. Given the widespread and increasing prevalence of such rebrandings, we empirically assess the performance implications of a number of recent PL rebrandings.

Data and Research Setting

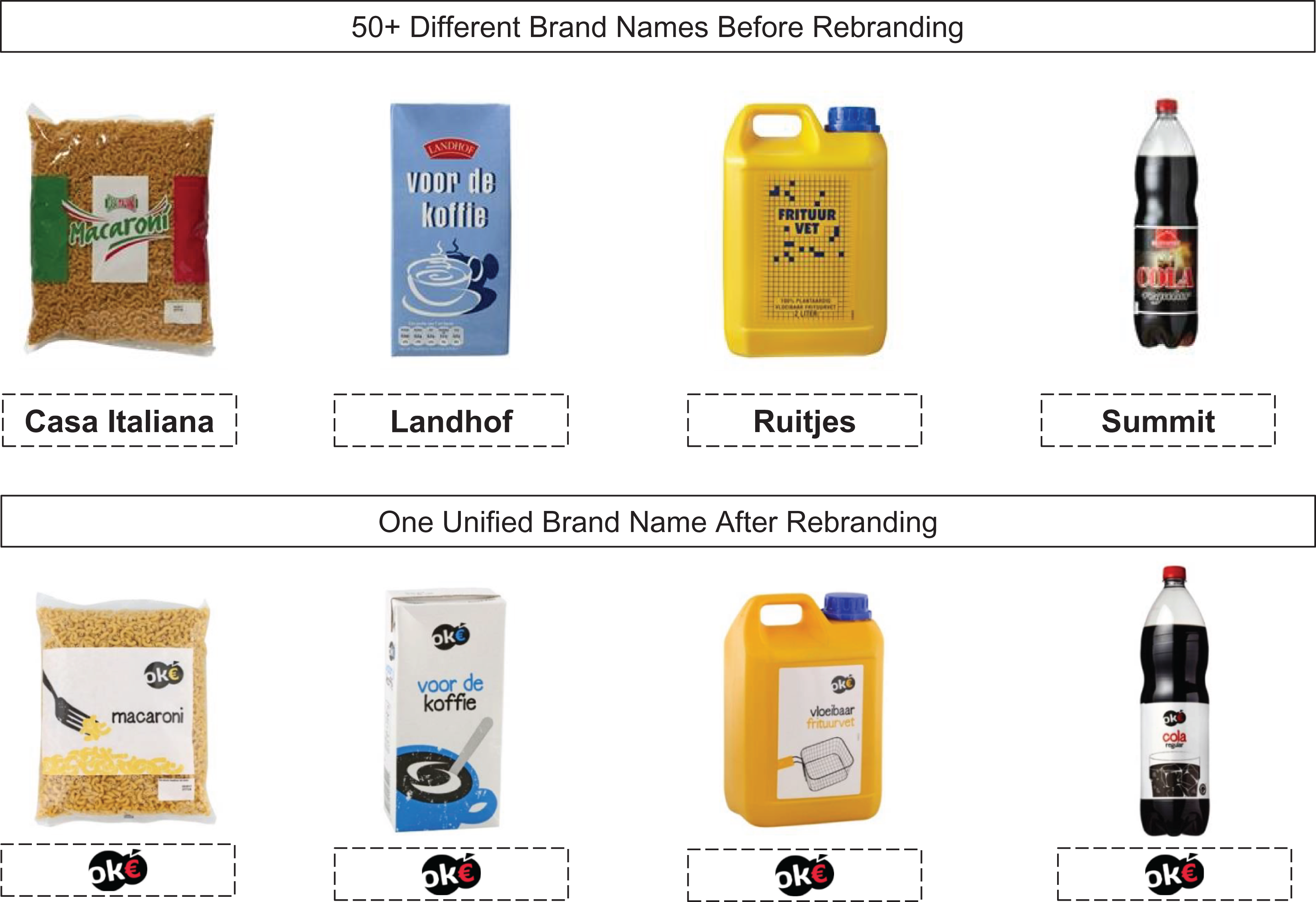

We study a PL umbrella rebranding at two banners, SPAR and Attent, of the leading Dutch convenience-store retailer SPAR Holding. The Netherlands has a highly developed retailing landscape, which has been used repeatedly to study retailing in general and PLs in particular (e.g., Ailawadi, Pauwels, and Steenkamp 2008; Sotgiu and Gielens 2015). SPAR uses a hi–lo price positioning and a high service level. It operated 227 outlets at the end of 2015. In the Netherlands, grocery retailers set prices centrally, implying that no price-zoning practices are used (Sotgiu and Gielens 2015). SPAR carries an economy and a standard PL tier. From March 2013 to November 2014, SPAR rebranded all its category-specific economy PL brands to one umbrella brand, “OK€.” Figure 1 shows four example SKUs before and after the rebranding.

PL-tier rebranding in four example categories to the umbrella brand “OK€.”

Attent is active in the same market as SPAR, also carries an economy and standard PL tier, and rebranded the same (economy) PL tier. However, compared with SPAR, Attent operates smaller neighborhood stores and provides somewhat less service. It sets its own marketing-mix strategy: it offers fewer price promotions than SPAR and uses no advertising. Attent operated 72 outlets at the end of 2015.

SPAR and Attent’s PL rebranding provides a clean setting that allows us to study the effect of the rebranding in isolation. During the rebranding, SPAR and Attent changed neither the physical specifications (e.g., ingredients, package type) of their PL products nor their PL suppliers. Moreover, the rebranding took place on a category-by-category basis such that they rebranded all SKUs within a category within the same week. For the rebranded PL tier, they used only one supplier per category. The order in which they rebranded the categories was determined by the ending date of the current contract with the PL supplier of that category. Typically, PL suppliers procure very short (12 to 24 months long) contracts (De Jong 2019; Ter Braak, Dekimpe, and Geyskens 2013). Whenever a contract was to be renewed, the category was rebranded.

The retailers communicated the name change clearly as a rebranding to their consumers to ensure that consumers would learn in a timely way about the rebranding and not be taken by surprise. For every (to be) rebranded SKU, SPAR and Attent provided a shelf label that announced the old SKU would get a new design and brand name. In the weeks of the rebranding, the new, rebranded SKUs were placed at the back of the shelves and would appear as the old SKUs (with the category-specific brand names) were sold out. In addition, SPAR and Attent created flyers that they prominently displayed at the cash registers. The flyer announced the upcoming/ongoing rebranding of the category-specific brands to the new umbrella brand. The flyer also served to inform those consumers that may not have bought the focal PL yet and may have missed the shelf labels.

Critical to our investigation is that no major changes occurred for SPAR and Attent during our observation period. We used LexisNexis and SDC Platinum to check the business press for potential concurrent events (e.g., store remodelings, startups of online operations, mergers and acquisitions) to rule out that the rebranding coincides with potentially confounding changes at either banner. We also searched SPAR and Attent’s news portals for any press releases or news reports that might suggest changes in the retailer’s strategies around the time of the rebranding. Neither SPAR nor Attent made announcements about events that could have interfered with the rebranding.

We obtained weekly store-scanner data from SPAR and Attent from 2011 to 2015 on all product categories in their rebranded PL tier, ranging from dairy and nondairy food to beverages, household care, and personal care. We analyze 53 (47) categories for SPAR (Attent), all of which (1) have at least 52 weeks of nonzero sales data for the rebranded PL tier both before and after the rebranding, (2) also feature NBs and another PL tier (to control for potential interdependencies between the tiers), and (3) are not fresh goods categories (where products are mostly unbranded). Across these categories, we observe, on average, 129 (130) weeks before and 111 (112) weeks after the rebranding for SPAR (Attent).

In addition to the data described previously, we created a control group to allow us to perform a before-and-after-with-control-group analysis. We identified seven retail banners (e.g., Deen, Deka-Markt, Hoogvliet) that carried the same category-specific PL brands (with the same brand names) as SPAR and Attent (as they were members of the same buying group, a situation described in more detail in Geyskens, Gielens, and Wuyts 2015), but that did not change to an umbrella brand name. For each of these retail banners, we have weekly data for the same categories and time as for SPAR and Attent.

Using data from Spotzi (www.spotzi.com) covering the geolocation of all grocery retail outlets in the Netherlands in the years of our study, we calculated the share of outlets of the treatment retailers that overlapped with any of the control retailers’ outlets within their trading zone. Because the control retailers were mostly active in different regions of the country than the treatment retailers, only 9% (7%) of SPAR (Attent) outlets were within a two-kilometer driving radius, which is the average distance consumers drive to their primary supermarket in the Netherlands (Deloitte 2018). We dropped these outlets before aggregating the outlet level data to the retailer level to rule out direct competition between treatment and control retailers and satisfy the stable unit treatment value assumption (SUTVA) (to which we return subsequently).

The data come at the category-SKU-week level. To reduce the impact of extreme values, we winsorize SKU sales and prices at the 1% and 99% levels (see, e.g., Rego, Morgan, and Fornell 2013). We aggregate the data across SKUs to the PL-tier level, using the procedure outlined in Pauwels and Srinivasan (2004). 2 Similar to Sotgiu and Gielens (2015), we use volume sales as our performance metric. Volume sales is an important performance indicator for managers that is particularly well suited “if [we] want to…assess the impact of changes in the marketing mix” (Hanssens, Parsons, and Schultz 2003, p. 52). We study three of the most prominent category-level marketing-mix tools—price, price promotions, 3 and assortment size—while controlling for the retailer’s marketing-mix instruments that are chain-wide (including advertising and the retailer’s number of outlets), the level of consumer confidence, and national holidays. We deflated the pricing and advertising variables with the consumer price index. Table 1 shows the operationalizations.

Variable Operationalizations.

Notes: For price and price promotions, we aggregate from the SKU level to the PL-tier level using (time-invariant) full-period market shares as weights (for a similar practice, see, e.g., Pauwels and Srinivasan [2004]).

Estimation Strategy

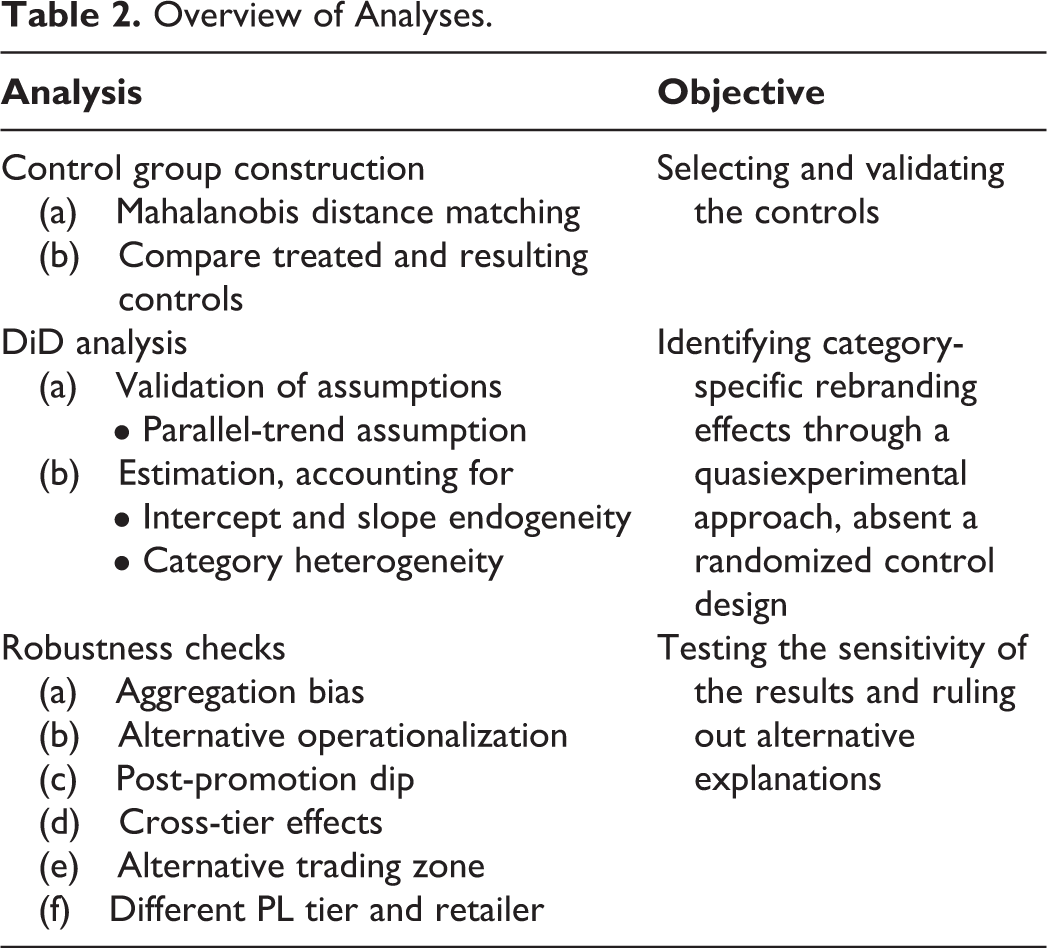

Our objective is to identify the effect of a PL umbrella rebranding on the rebranded PL tier’s sales. In doing so, we face two challenges. First, our data generation process lacks a random assignment of rebranded categories into treatment and control conditions. Therefore, we estimate a difference-in-differences (DiD) model and use a quasiexperimental procedure in which we match categories for the two retailers that rebranded with the same category from one of the retailers that carried the same PL brands but opted not to engage in a PL rebranding exercise. Second, we need to ensure that our findings are not driven by self-selection and endogeneity. We now explain in detail each step of our identification strategy (for an overview, see Table 2).

Overview of Analyses.

Creating a Matched Control Group

We conduct a distance-matching analysis (Guo and Fraser 2015, p. 177) in which we pair each rebranded category of SPAR and Attent with the same category of one of the seven control retailers that did not engage in the rebranding. 4 Using a 52-week pretreatment observation window, we compute for each category the Mahalanobis distance between the treated category and the potential control candidates using the variables in Table 3. We then select the match with the smallest distance. After matching, the rebranded categories and the control categories have become indistinguishable in terms of the pretreatment characteristics, except for the focal PL-NB price differential (ps < .01). This difference is not unexpected, however, given the more service-oriented positioning of SPAR and Attent (we elaborate on this when motivating the constant-bias assumption of the conditioning variable). Table 3, Panel A, reports pretreatment summary statistics for the matched control group.

Summary Statistics by Group before the Rebranding.

*p < .10.

**p < .05.

***p < .01.

Notes: Two-sided tests of significance. As described in footnote 5, we do not include the immediate four weeks before and after each category’s rebranding in the calculation. Variables are operationalized as follows: Category (focal PL) sales growth is measured as the average of the first difference of log-transformed category (focal PL) sales. NB (focal PL) share is the average market share of NBs (focal PLs) in a category. The marketing-mix related variables are operationalized as the average of the ratio of focal PL price (price promotions or assortment size) to NB price (price promotions or assortment size). All averages are taken over the 52 weeks leading up to (Panel A) or following (Panel B) the rebranding and all variables without negative values are log-transformed. The considered variables were selected based on data availability and support for their potential relevance in the extant PL literature (e.g., Dhar and Hoch 1997; Sethuraman and Gielens 2014).

Difference-in-Differences

We use a DiD approach to estimate the effect of the PL rebranding on focal PL sales and compare the PL sales before and after the rebranding with those of the matched category. We estimate a log-log model (that relates the log of volume sales to the log of the continuous covariates) because it offers direct estimates of the marketing-mix elasticities. Formally,

where

Control variables

As control variables (

Accounting for NBs and the other PL tier

We use Equation 1 to estimate the effects of the rebranding on the PL tier’s sales and to calculate changes in the rebranded PL tier’s intrinsic brand strength and marketing effectiveness. However, retailers also offer NBs and often have more than one PL tier, and these may be interdependent. To control for this, we state similar equations for the retailer’s NBs and its other PL tier. Moreover, by also considering these other brand types, we will be able to assess the total revenue implications of the rebranding. To increase efficiency, we estimate these equations jointly with the corresponding equation for the rebranded PL tier using SUR. Thus, the error terms

Identifying assumptions

The DiD approach relies on the assumption of parallel post-treatment counterfactual trends. Because these are unobservable, this assumption is intrinsically untestable. As a proxy, we assess whether the pretreatment trends are parallel, under the assumption that the pretreatment trends would have continued after the treatment in its absence. We follow Angrist and Krueger (1999) (for a recent application in marketing, see, e.g., Gallino and Moreno 2014) by estimating Equation 2 on the prerebranding data:

where

The focal PL tier’s sales evolution before and after the rebranding.

Second, while both the treatment and control retailers belonged to the same buying group (and therefore carried the same category-specific PL brands before SPAR’s and Attent’s rebranding), it is important to note that the choice to rebrand (or not) was not made based on considerations that are themselves influenced by the treatment. Instead, this was determined by the retailers’ time-invariant strategic positioning, in that the more service-oriented banners, SPAR and Attent, opted to rebrand, while the more value-oriented control banners opted not to do so. As discussed in Lechner (2010, p. 178), variables that cannot change over time are exogenous by construction when one considers a time-varying treatment. As such, also the constant-bias or exogeneity assumption of the conditioning variable is satisfied. Finally, as we explained previously, because we dropped the 9% of SPAR outlets and 7% of Attent outlets that were geographically close to one of the control retailers’ outlets, and thus likely to compete directly, violation of the SUTVA assumption is unlikely.

Endogenous Sample Selection

We are confronted with several potential endogeneity problems due to sample selection. In particular, (1) the decision of which tier to rebrand (the economy PL tier or the standard PL tier), (2) the decision of when to start rebranding that tier, (3) the decision of which product categories and SKUs to rebrand within the selected tier, and (4) the decision of in which order to rebrand those categories might all be chosen strategically and thus be endogenous.

One could argue that retailers can choose which PL tier to rebrand. However, SPAR and Attent umbrella-branded their standard PL tier since the brands’ inception (which was more than two decades ago) and no longer had that choice at the time of our study. Moreover, retailers typically make umbrella-rebranding decisions at the PL-tier level. That is, if they decide to rebrand a PL tier, often all product categories of that PL tier are rebranded, as well as all SKUs within those product categories. This was also the case for SPAR and Attent. Thus, we do not face endogeneity issues (1) and (3) in our setting. As for the decision of when to start the rebranding exercise, the decision to make the OK€ umbrella brand available to interested retail members was made at the buying-group level. Therefore, this decision is not likely to be directly related to the outcomes of one specific retailer in the buying group (Sande and Ghosh 2018, p. 198), making issue (2) less of a concern. Moreover, both SPAR and Attent decided right away to make use of the rebranding possibility, rather than strategically postpone to a later point of time.

The sequence in which SPAR and Attent rebranded the various categories within the PL tier was (as indicated previously) exogenously determined by the time existing supplier contracts ended. As such, the order of the rebranding was not strategically chosen to maximize performance. To validate this managerial assertion, we estimated a Cox hazard model with the week of the rebranding as the dependent variable, and the same set of independent variables that we used for the matching (see also Table 3), plus the focal PL’s profitability. We report the results in Web Appendix A. None of the covariates are significant, indicating that they did not drive the order in which the categories were rebranded. 7 This finding increases our confidence in SPAR and Attent’s information that the order in which they rebranded the categories was solely driven by contract expiry dates and not by strategic considerations (e.g., the PL tier’s low/high profitability in the category). Thus, we also do not face an endogeneity issue as to the order in which the categories were rebranded (issue 4).

Endogeneity of Levels of the Marketing-Mix Variables

The marketing-mix variables

In line with Luan and Sudhir (2010) and Chakravarty, Kumar, and Grewal (2014), we account for both intercept and slope endogeneity. Intercept endogeneity has a long tradition in the marketing literature and refers to managers being strategic about setting the marketing mix in response to unobserved (to the researcher) demand shifters (e.g., employee and top-management commitment) (Luan and Sudhir 2010). Slope endogeneity, in contrast, deals with the fact that (marketing-mix) choices are often affected by managers’ private information about the likely differential effectiveness of the marketing mix (e.g., after the rebranding, a retailer may alter its prices to account for a higher expected price effectiveness).

We derive our IVs from two conceptually different sources. As advocated by Nevo (2001), we include the retailer’s wholesale price as a first IV. The underlying idea is that retailers are likely to adjust their marketing mix in response to shocks in the wholesale price (i.e., cost shocks), but given that the wholesale price is unobserved by consumers, these may be unrelated to the unobserved demand shocks (see, e.g., Chintagunta 2002). The second group of IVs consists of the marketing variables (price, assortment size, and banner advertising) from a retailer from a neighboring country (Papies, Ebbes, and Van Heerde 2017, p. 601). The logic is that both countries are driven by common supply shocks (e.g., ingredient costs drive price variation in the two countries in the same way). In addition, no common demand shocks should occur across the two markets, nor should marketing-mix actions be coordinated (Sotgiu and Gielens 2015, p. 791). This is more likely to be the case when a different set of retailers is active in the two markets. In our setting, this overlap was limited, given that the leading Dutch retailers (Albert Heijn, Jumbo, and C1000) were not active in Belgium during our observation window, while the leading Belgian retailers (Colruyt, Delhaize, and Carrefour) were not active in the Netherlands.

8,9 Finally, because of the anticipated potential changes in the endogenous variables by the rebranding, we also include as IVs the interactions of the instruments with

Changes in Intrinsic Brand Strength and Marketing Effectiveness

We can directly derive the changes in intrinsic brand strength and marketing effectiveness from the DiD model in Equation 1. Following Leeflang et al. (2009) and Sriram, Balachander, and Kalwani (2007), we use a brand’s baseline sales (i.e., net of marketing-mix and other effects) as our measure of intrinsic brand strength, which we define (consistent with prior literature) as the sales corresponding to the bare minimum of marketing support. Hanssens, Wang, and Zhang (2016) and Slotegraaf, Moorman, and Inman (2003), for example, have set this minimum at zero, which makes sense for price promotions and banner advertising, but less so for price and assortment size. For the latter, a nonzero base support is required, as an assortment size of zero implies no sales by definition (Ataman, Van Heerde, and Mela 2010). We set assortment size to the minimum level observed in our time span for, respectively, the focal PL tier, the NBs, and the other PL tier, in a given category. To evaluate intrinsic brand strength at these levels, we “minimum-center” (similar to the use of mean-centering) assortment size in our estimation by subtracting the category-specific minimum value from the variable’s values for a given retailer (the minimum support level for the price-promotions variable is zero).

For the price variable, we use the logical counterpart; that is, we “maximum center” by subtracting the maximum level observed per category. Our model accounts for the fact that the intrinsic strength of a brand is not necessarily constant, but can (even in the absence of a rebranding) vary over time (Ho-Dac, Carson, and Moore 2013), by allowing for a flexible, yet parsimonious, evolution through a trend variable and its square. Thus, at any point in time Ti, the change in intrinsic brand strength in category i attributable to the rebranding is

The extent to which the effectiveness of the various marketing-mix instruments j (j = 4, 5, 6) in category i changes after the rebranding is captured directly as

Results

Model-Free Evidence

Table 3, Panel B, compares the sales of the rebranded PL tiers of SPAR and Attent with those of the control group 52 weeks after the rebranding, and the corresponding values for price, price promotions, and assortment size. As Table 3 shows, on average, SPAR’s negative PL growth in the year before the rebranding was turned around after the rebranding, while Attent’s PL growth increased. No such patterns were observed for the control groups. As a result, for both retailers, the nonsignificant difference in PL growth between treatment and control groups before the rebranding became highly significant afterward. This supports the generally positive sentiment about PL umbrella branding. It is, however, unclear whether these effects are due to an increase in the PL’s intrinsic brand strength and/or marketing effectiveness after the rebranding, or to other developments in the Dutch consumer packaged goods market.

Results

Table 4 presents the parameter estimates of the DiD specification in Equation 1, averaged across 53 categories for SPAR and 47 categories for Attent, respectively. Multicollinearity does not seem to be an issue, with all correlations well under the .8 cutoff value suggested by Judge et al. (1998), as shown in Web Appendix B (maximum correlation = .226 for SPAR and .346 for Attent). We account for first-order autocorrelation by applying the Prais–Winsten correction (Datta, Ailawadi, and Van Heerde 2017). Our instruments are strong, as evidenced by an average correlation between first-stage predictions and endogenous variables of, respectively, .83 (SPAR) and .86 (Attent) and significant Sanderson and Windmeijer (2016) multivariate F-tests (ps < .01). The Hansen-J test supports that our instruments are uncorrelated with the error term (p > .10), which attests to their validity (Wooldridge 2002, p. 123). Because the endogeneity correction terms are estimated quantities, we follow Papies et al. (2017) and report bootstrapped standard errors.

Parameter Estimates of the Difference-in-Differences Model.

*p < .10.

**p < .05.

***p < .01.

Notes: Two-sided tests of significance. We only report parameter estimates for the focal PL tier. The reported values refer to the weighted average across product categories. The weight for

Change in intrinsic brand strength following the PL rebranding

One year after the rebranding, SPAR and Attent’s rebranded PL tiers had increased with 36.5% and 20.2% in intrinsic brand strength, respectively (SPAR:

Change in marketing-mix effectiveness following the PL rebranding

For the marketing mix, all rebranding effects are significant, indicating a statistically significant impact of the rebranding. The price sensitivity dropped for both SPAR (

Heterogeneity across categories

One may wonder to what extent the changes in intrinsic brand strength and marketing-mix effectiveness are consistent across categories. As a first probe into this issue, we regressed category-specific changes in intrinsic brand strength and marketing-mix effectiveness on the prior NB concentration in the category (low vs. high; defined using a median split) and the prior PL share in the category (low vs. high; again based on a median split), while controlling for the focal PL revenues in the category before the rebranding. For both SPAR and Attent, we find neither the change in intrinsic brand strength nor any of the changes in marketing-mix effectiveness to differ systematically between high versus low levels of either prior NB concentration or PL share (all ps > .10). All in all, it seems reasonable to conclude that our key insights generalize across categories that differ widely in competitive structure.

Robustness checks

We assess the robustness of our findings to (1) a potential aggregation bias (by comparing our logarithmic model with a linear model; Christen et al. 1997), (2) alternative operationalizations of the base marketing-support level (viz., the 5th and 10th percentiles for assortment size, rather than the minimum observed value, and the 95th and 90th percentiles for price, rather than the maximum observed value), (3) an additional postpromotion dip variable, (4) the inclusion of the other tiers’ marketing-mix variables as additional control variables (e.g., to account for the cross-price effects from NBs and the other PL tier on the rebranded PL tier), and (5) selecting a wider trading-zone radius to drop treated stores and satisfy the SUTVA assumption. In all instances, our focal insights are not affected. The Appendix contains a detailed description of these robustness checks.

In addition, we assess the replicability for a different PL tier at a substantially different retailer, Colruyt. Colruyt is the market leader in Belgium, operates a low-price supermarket format with an average service level (GfK 2016), and is substantially larger in terms of total revenue than either SPAR or Attent. Most importantly, Colruyt differs from SPAR and Attent in that it rebranded its standard PL—which, with a 22.6% share, was already very successful before the rebranding—to the umbrella brand “Boni Selection.” It offers a second PL tier that is positioned as an economy PL. Colruyt operated 233 outlets at the end of 2015. For Colruyt, we have access to GfK household panel data, including a variety of marketing-mix tools, but no wholesale prices. Moreover, we did not find press releases or news reports that might suggest important changes in Colruyt’s strategy during our observation period. Although this is somewhat less clean, we use the same potential control group and matching procedure for Colruyt as for SPAR and Attent. A comparison of Colruyt to SPAR and Attent appears in Table 5.

Summary Comparison of the Three Retailers Studied.

Notes: Based on GfK (2016), the Euromonitor Global Market Information Database, retailer store-scanner data (SPAR and Attent), and GfK household-panel data (Colruyt). Except for total PL share and the rebranded PL tier’s share, where across-category averages are provided based on the data span before the rebranding, data are for 2015.

We present the parameter estimates of the DiD model for Colruyt in Web Appendix C. The results are very consistent across the three cases, despite the retailers’ very different prior success of the rebranded PL tier. As for SPAR and Attent, Colruyt’s rebranded PL tier’s intrinsic brand strength increases after the rebranding (

Discussion

Retailers have been growing their PL portfolios for decades by introducing PLs into new product categories, often with new brand names. At the same time, PLs have become stronger and by now are a “widely accepted brand class of their own” (Seenivasan, Sudhir, and Talukdar 2016, p. 802) that “should be treated as a true consumer brand to succeed in today’s retail environment” (Daymon 2020, p. 6). In light of these developments, retailers often consider rebranding multiple category-specific PL brands within a tier to one umbrella brand. The reasons for this are manifold and range from providing an easier PL categorization for consumers through a unified appearance to expected marketing-effectiveness gains. So far, little research has examined the performance implications of such a PL rebranding strategy, nor whether NB insights automatically generalize to this setting (Ailawadi and Keller 2004). This is surprising, given the high (and increasing) prevalence of umbrella branding among PLs (Richards, Yonezawa, and Winter 2015) and some fundamental differences between both settings (Grewal, Levy, and Lehmann 2004; Sayman and Raju 2004), making the issue both managerially and theoretically relevant.

To address this gap, we identified three substantially different retailers who rebranded one of their PL tiers and derived empirically to what extent the rebranding indeed resulted in the hoped-for intrinsic-brand strength and marketing effectiveness improvements. Importantly, the evidence consistently shows that the rebranded PL tier’s intrinsic brand strength increases considerably after the rebranding. Using the same brand name across an entire PL tier seems to reduce consumers’ uncertainty and increase the sales of the PL brand. The common design grid that umbrella-branded PLs use across categories apparently does not lead to a comparatively larger sales loss due to missed category-specific associations and/or trade dress advantages, resulting in a positive net effect. Thus, even though the common brand name is not restricted (as repeatedly advised in the NB-focused brand extension literature) to a limited set of closely related complementary categories, positive higher-order associations seem to be facilitated through the common PL name across many unrelated and substitute categories. This higher intrinsic brand strength translates (consistent with previous NB findings) into a reduced price elasticity, making the PL less dependent on rock-bottom prices to appeal to potential customers.

However, a very different picture emerges in terms of price promotions and assortment-size effectiveness. While Erdem and Sun (2002) found a higher effectiveness of price promotions for umbrella-branded than for category-specific NBs, this no longer holds when rebranding an entire PL tier, while the effectiveness of SKU additions is found to decrease. The cumulative exposure to the common brand name across a large and diverse set of categories throughout the store seems to lead to a reduced variety perception. Similarly, the negative relationship between promotional frequency and discount effectiveness—that was already documented at the brand (Krishna 1994) and category (Krishna 1994; Raju 1992) level—also appears to hold when the higher perceived intensity of discounts emerges from same-name promotional exposures in other categories. The very different number of categories involved in PL and NB umbrella branding may well explain these diverging findings.

Our study has not only addressed repeated academic calls for more research on key retail-branding decisions (Dekimpe et al. 2011; Grewal, Levy, and Lehmann 2004; Lourenço and Gijsbrechts 2013) but also has clear managerial implications, which we summarize in Table 6. While umbrella branding has become a frequently observed practice in the retailscape, numerous leading retailers across both developed and emerging economies still use category-branded PLs. For example, in the United States (Albertson’s), Australia (Aldi), Canada (Safeway), Colombia (Almacenes Éxito), India (Big Bazaar), Italy (Eurospin), and Mexico (OXXO), one out of the top five retailers—defined in terms of market share—used category-specific branding by the end of 2019. In Croatia (Lidl, Tommy), Germany (Aldi, Lidl), Poland (Biedronka, Lidl), Russia (Magnit, Auchan), and Saudi Arabia (Al Othaim, Al Raya), two out of five, and in Turkey (Bim, A101, Sok), even three out of the top five retailers still use category-specific branding (all information obtained through Planet Retail). Interestingly, Amazon is also currently handling multiple category-specific PL brands, such as “Happy Belly” coffee, “Presto” laundry detergent, and “Wickedly Prime” snack items, with industry observers indicating that they will likely consolidate these various brands under an umbrella brand at a later point in time (Planet Retail 2017). Our findings may help these retailers in understanding the implications of a potential shift to umbrella branding.

Overview of Findings and Implications.

Interestingly, the retailers in our study did not adjust their marketing mix in line with the altered effectiveness of the marketing-mix instruments after the PL rebranding. To compare the retailers’ marketing mix before and after the rebranding, we calculate for each category the average value of each marketing-mix tool 52 weeks after the rebranding and divide it by the average value of that tool 52 weeks before the rebranding. We then compare, using a t-test, this ratio for each of the three retailers with a similar ratio calculated for the respective control groups. We find that none of the retailers changed their price levels relative to the control retailers (ps > .10). However, despite the decreased effectiveness, both SPAR and Attent increased their price promotions (SPAR: t = 2.77, p < .01; Attent: t = 2.10, p < .05), while Attent and Colruyt increased their assortment size (Attent: t = 2.81, p < .01; Colruyt: t = 3.40, p < .01). These findings are in line with research on embedded exchange theory, which has shown that managers are prone to facilitate the outcome of their expectations through their behavior to make sure they are right (Sorenson and Waguespack 2006). In case of a rebranding, this “self-confirming conduct”—which may not always be optimal from a profit-maximizing point of view—may manifest itself through increased marketing support for the rebranded PL line (e.g., by offering more price promotions or introducing additional SKUs), even if the effectiveness of these instruments decreases.

Finally, to provide top-level managers with information about the rebranding’s overall success, we assess the effect on the retailers’ total sales in each category (i.e., their PL [rebranded and other PL tier] as well as NB [value] sales). We do so by first calculating for each retailer the change in category-specific volume sales following the rebranding, based on our DiD analyses. To get to overall chain-wide effects, we consider the revenue implications (given the different units in which the various categories are measured) and multiply the absolute change in a category’s volume sales by the average price in the prerebranding period (this price was not increased relative to the control retailers following the rebranding). In a similar vein, we calculate for every retailer its change in revenues for its other PL tier and the NBs sold in their stores. Subsequently, we sum within categories. For all three retailers, we find that their total revenues across product categories increased after the rebranding, and significantly so for SPAR and Attent (ps < .01).

Limitations and Future Research

First, an advantage of our study is that we had in-depth institutional knowledge, which enabled us to rule out a variety of endogeneity concerns. Still, our study design did not involve a random assignment of retailers and/or categories into the treatment or control conditions, making any causal inference conditional on the validity of our selected control retailers as counterfactual (Goldfarb and Tucker 2014). In addition, it would have been desirable to analyze equally deep data for a broader cross-section of retailers to increase the generalizability of our findings further. Still, even though the three retailers we investigated are very different from each other along multiple dimensions, our empirical results are very similar. Relatedly, while our results generalized across the rebranding of the economy and standard PL tier, it would be interesting to see whether this also holds for the later added premium PL tier (Ter Braak, Geyskens, and Dekimpe 2014). Furthermore, it would be interesting to explore whether our results also hold, and maybe even become stronger, when retailers rebrand their category-specific PLs with an umbrella brand that explicitly includes the banner’s name (Keller, Dekimpe, and Geyskens 2016).

Second, we were unable to investigate whether the effectiveness of PL advertising changes after an umbrella rebranding, because “advertising data providers are still limited to collecting advertising data at the retailer level” (Dekimpe and Geyskens 2019, p. 7). Instead, we controlled for advertising at the retail banner level. We found that the retailer’s focal PL tier becomes less dependent on the retailer’s banner advertising. Future research could investigate whether these results still hold once more granular advertising data, at the PL-tier and product-category level, become available.

Third, one reason for retailers to move to umbrella branding may be cost savings. Because retailers can invest considerably fewer resources in their PLs than brand manufacturers can for their NBs (Lamey et al. 2012), the affordability of umbrella branding may be particularly important for retailers. Future research could investigate the effects of umbrella branding on retailer profitability.

Finally, we are not aware of any empirical studies on the addition of category-specific brands to an existing umbrella brand, either for NBs or for PLs. Future research could explore the flipside of our setting (i.e., instances in which retailers first feature an umbrella brand and then add category-specific brands). Would such a shift entail a positive change in marketing effectiveness (as a symmetric effect would predict), or will the new category-specific brands “get lost in the NB crowd” and experience even lower marketing effectiveness?

Supplemental Material

Supplemental Material, jmr.17.0291-File002 - Opening the Umbrella: The Effects of Rebranding Multiple Category-Specific Private-Label Brands to One Umbrella Brand

Supplemental Material, jmr.17.0291-File002 for Opening the Umbrella: The Effects of Rebranding Multiple Category-Specific Private-Label Brands to One Umbrella Brand by Kristopher O. Keller, Inge Geyskens and Marnik G. Dekimpe in Journal of Marketing Research

Footnotes

Appendix

Acknowledgments

The authors thank Bart Bronnenberg, Els Gijsbrechts, Alina Sorescu, Jan-Benedict Steenkamp, and Harald van Heerde as well as seminar participants at BI Norwegian Business School, Singapore Management University, Tilburg University, University of North Carolina at Chapel Hill, University of South Carolina, University of Texas at Austin, and the 2016 Marketing Science and Theory & Practice in Marketing conferences, for their useful comments. The authors also thank Evi van Uffel and Davy van Raemdonck (GfK Belgium), Erwin Jansen and Jan-Hein van Spaandonk (SPAR Netherlands), and AiMark for their generous data support.

Associate Editor

Venkatesh Shankar

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors are indebted to the Netherlands Organization for Scientific Research (NWO) for financial support under grant number 406-12-07.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.